Republic of Kenya Sept 2013, Nairobi, Kenya Ministry of Energy and Petroleum ENERGY DAY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Republic of Kenya

Sept 2013, Nairobi, Kenya

Ministry of Energy and Petroleum

ENERGY DAY

THE THRUST

5000+MW FOR TRANSFORMING KENYA:

ADEQUATE CAPACITY AT A

COMPETITIVE TARIFF

CONTENTS

MoEP Mission and Vision 1

Energy Sector Structure 2

Power Cycle: Generation to Distribution 3

40-Month 5,000+MW Initiative 4

Investment Opportunities in the Sector 5

MISSION & VISION

… to facilitate provision

of clean, sustainable, affordable, reliable and secure energy for national development while protecting the environment …

Mission

… affordable

quality energy for

all Kenyans …

Vision

1

2. Developing Least Cost Power Development Master Plan

3. Undertaking Geological, Geophysical and Geochemical mapping

for geo-energy minerals

4. Promoting Development of Renewable Energy, Energy Efficiency &

Conservation

5. Exploring, Appraising and Developing Petroleum Resources

MINISTRY KEY FUNCTIONS 1

1. Setting the Energy Sector Policy, Vision and Strategic Direction

Source: KenGen;

ENERGY SECTOR STRUCTURE 2.

Ministry of Energy and

Petroleum (MoEP)

(setting policy)

Energy Regulatory

Commission(ERC) (regulating energy sector)

KPC (Transport)

KPRL (Refinery)

NOCK (Marketer)

Private

Marketers

PETROLEUM

KETRACO – Kenya Electricity Transmission Company Ltd REA – Rural Electrification Authoirity KPLC – Kenya Power & Lighting Company Ltd GDC – Geothermal Development Company Ltd IPPs – Independent Power Producers KPC – Kenya Pipeline Company Ltd KPRL – Kenya Petroleum Refinery Ltd NOCK – National Oil Company of Kenya KNEB – Kenya Nuclear Electricity Board

GDC (Geo-

Resource

Assess-

ment)

IPPs (Power

Gene-

ration)

KenGen (Power

Gene-

ration)

KE-

TRACO ( New Trans-

mission)

REA

(Rural

Elec-

trification)

Kenya

Power (Dx &

Existing Tx

Lines

Generation Transmission

& Distribution

Energy Tribunal (ET) (arbitrating energy sector)

ELECTRICITY

KNEB (Nuclear)

Source: KenGen; MoEP

PROJECTED POWER DEMAND 2.

Source: KenGen; MoEP

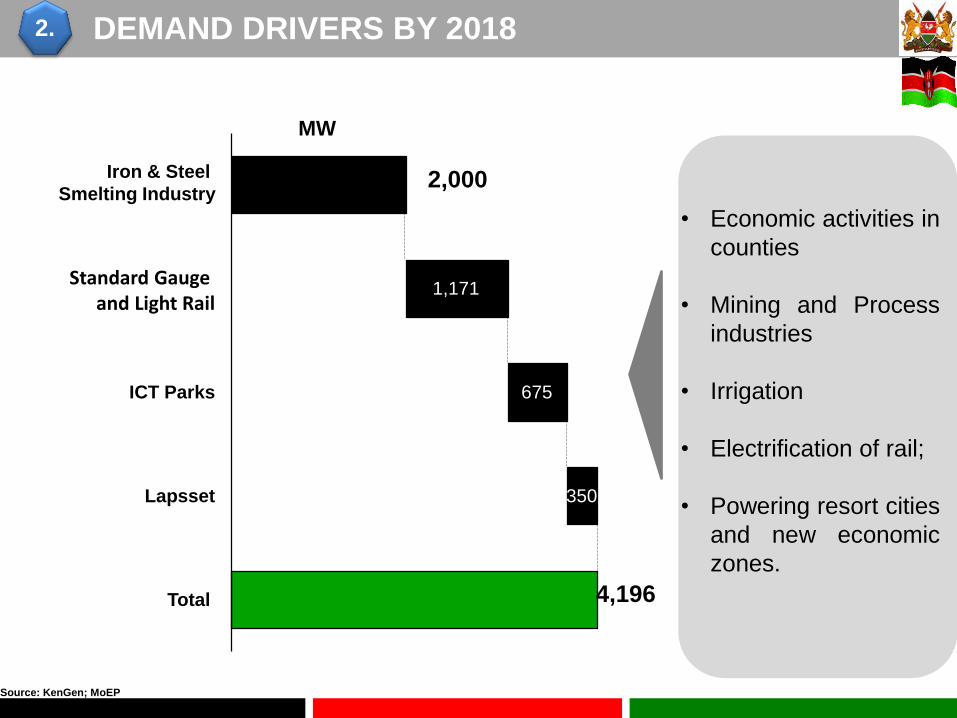

DEMAND DRIVERS BY 2018 2.

2,000

4,196 Total

Iron & Steel

Smelting Industry

Standard Gauge and Light Rail

ICT Parks

1,171

675

MW

Lapsset 350

• Economic activities in

counties

• Mining and Process

industries

• Irrigation

• Electrification of rail;

• Powering resort cities

and new economic

zones.

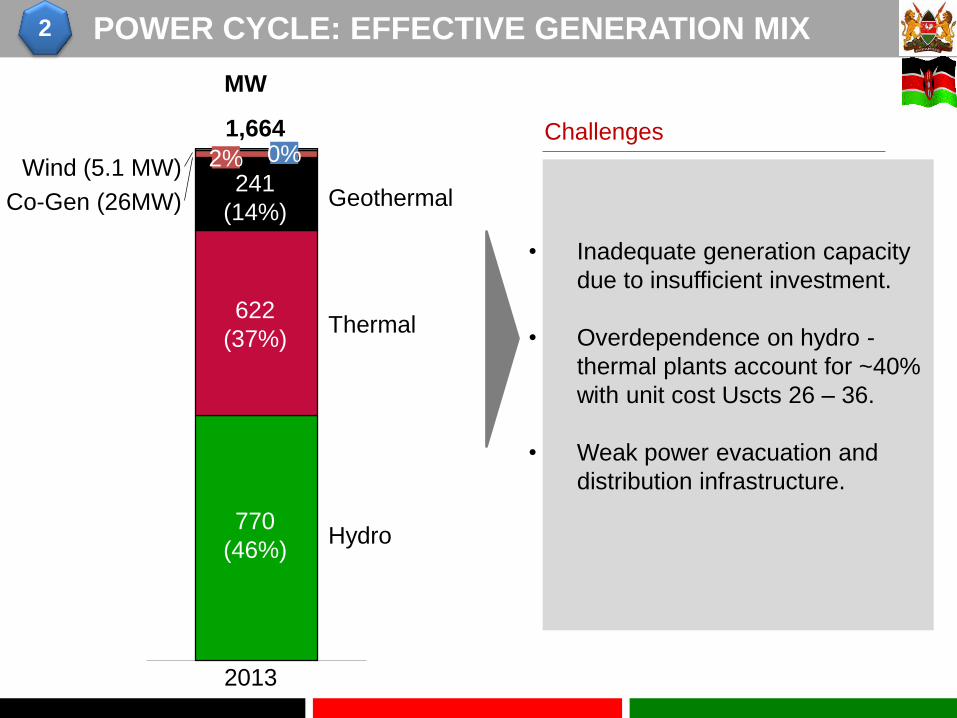

POWER CYCLE: EFFECTIVE GENERATION MIX 2

1,664 0%

622

(37%) Thermal

Wind (5.1 MW)

2013

241

(14%) Geothermal Co-Gen (26MW)

2%

770

(46%) Hydro

MW

• Inadequate generation capacity

due to insufficient investment.

• Overdependence on hydro -

thermal plants account for ~40%

with unit cost Uscts 26 – 36.

• Weak power evacuation and

distribution infrastructure.

Challenges

POWER CYCLE: PEAK DEMAND (MW) 1

2013

30% Reserve Margin

Suppressed

Current Peak 1,357

343

536

2,236

1700 MW

• Current installed capacity

≈ 1,700MW required

2,236MW

• Shortfall; ≈536 MW,

after providing for a 30%

reserve margin

…due to

transmission and

distribution system

weaknesses

… true

peak …

INITIATIVES TO REDUCE SUPPRESSED DEMAND 3.

• 220kV ring around

Nairobi

• 1,114km 132 kV lines by

2014 (~cost US$ 250m)

• 1,760km 220/400kV

lines by 2015 (~cost

Kshs US$738m)

• 2nd National Control

Centre

• Underground Cables in

Urban Areas

• Aerial(insulated)

Bundled Conductors

(ABC) in rural & peri-

urban areas

• Additional substations

across the country

• Scaling up of

connectivity

• Electrification of

informal

settlements with

appropriate

infrastructure

Trans., Dist. &

Substation

Component

Connectivity

Component

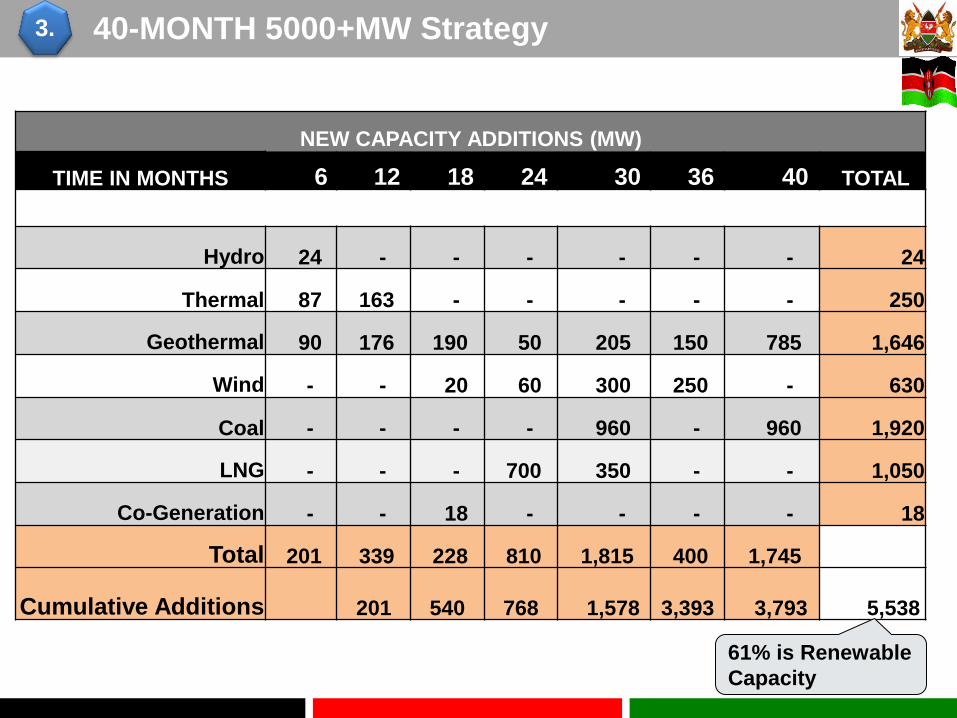

40-MONTH 5000+MW Strategy 3.

NEW CAPACITY ADDITIONS (MW)

TIME IN MONTHS 6 12 18 24 30 36 40 TOTAL

Hydro 24 - - - - - - 24

Thermal 87 163 - - - - - 250

Geothermal 90 176 190 50 205 150 785 1,646

Wind - - 20 60 300 250 - 630

Coal - - - - 960 - 960 1,920

LNG - - - 700 350 - - 1,050

Co-Generation - - 18 - - - - 18

Total 201 339 228 810 1,815 400 1,745

Cumulative Additions 201

540

768 1,578

3,393 3,793 5,538

61% is Renewable

Capacity

TARIFF EVOLUTION WITH THE NEW CAPACITY 3.

1664

2342

5017

6762

14.14

12.49

11.03

9.03

9

19.78

17.73

13.46

11.19 10.43

0

5

10

15

20

25

0

1000

2000

3000

4000

5000

6000

7000

8000

0 6 12 18 24 30 36 40

Tari

ff P

rogr

ess

ion

Cu

mu

lati

ve In

stal

led

Cap

acit

y

Cumulative MW

Industrial/Commercial Tariff (US$cts/kWh)

Domestic Tariff Progression (US$cts/kWh)

37% reduction

47% reduction

PROJECT DESCRIPTION DUE DATE

1.

Olkaria Wellhead

70 MW 2014 December

2.

Olkaria V

140 MW 2015 December

3.

Olkaria VI

140 MW 2016 December

GEOTHERMAL PROJECTS REQUIRING INVESTORS 3.

Total 350 MW Estimated Capex US$ 875m

PROJECT DESCRIPTION DUE DATE

1.

2.

90 MW Menengai

50 MW Menengai

2014 December

GEOTHERMAL PROJECTS REQUIRING INVESTORS

3.

4.

100 MW Menengai

100 MW Menengai

2015 December

5.

6.

100 MW Menengai

50 MW Suswa

2016 December

7.

8.

100 MW Suswa

200 MW Baringo

2016 December

2016 June

2016 June

2016 December

3.

2015 June

Total 790 MW Estimated Capex US$ 1,975m

PROJECT DESCRIPTION DUE DATE

1. 170,000 m3 Floating Storage & Regasification Unit 2015 June

LNG PROJECTS

2. Dredging; approximately 300m at Dongo Kundu 2015 June

3. 4x200MW Power Plant at Dongo Kundu 2015 June

4. Conversion 90 MW Rabai Power Plant to LNG 2015 June

5. Re-engineering 190 MW Kipevu I & III to LNG 2015 June

6. Re-engineering 70 MW Kipevu II to LNG 2015 June

3.

PROJECT DESCRIPTION DUE DATE

1. Construction of Coal Dry Cargo Handling Jetty 2015 December

COAL PROJECTS

2. 3x320 MW Power Plant at Kilifi/Lamu 2015 December

3. 3x320 MW Power Plant at Kitui/Lamu 2016 October

3.

PROJECT DESCRIPTION DUE DATE

50km, 400kV double circuit line for power

evacuation from 700 MW LNG plant 2015 Jul

TRANSMISSION PROJECTS…

2016 Dec 620km, 400kV double circuit line for

power evacuation from 960MW Kitui

Coal plant

2014 Dec 20km, 132kV for power evacuation from

90MW Menengai geothermal plant

80km, 400kV double circuit line for power

evacuation from 960MW Kilifi Coal plant. 2015 Dec

Dongo Kundu - Mariakani

Mariakani -

Kitui- Nairobi

East Line

Menengai T-

off Jinja Line

Kilifi/Lamu-

Mariakani

3.

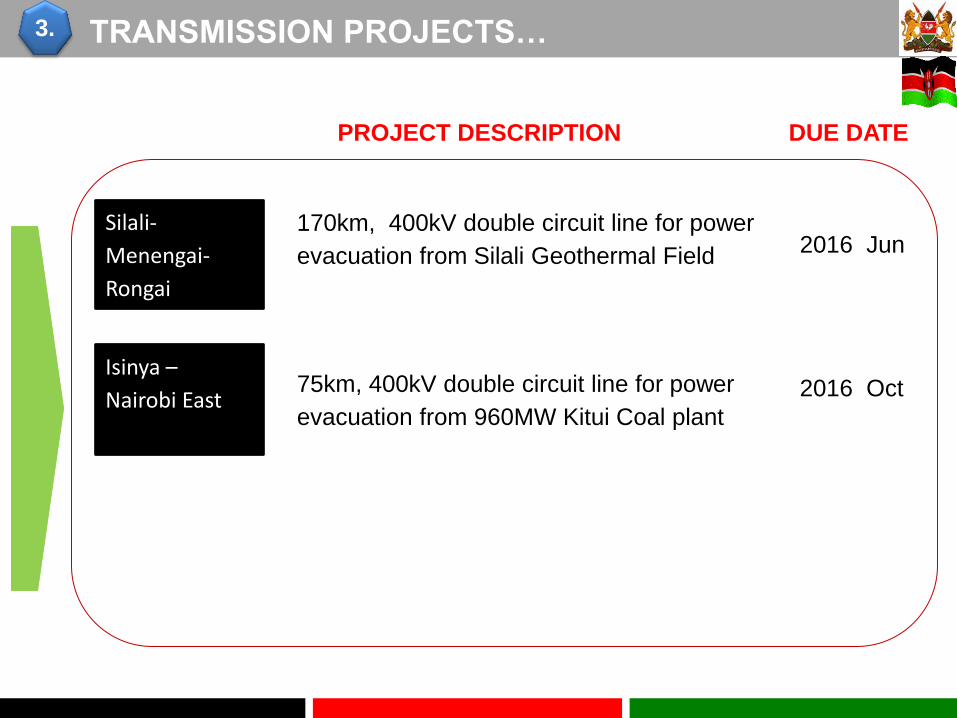

PROJECT DESCRIPTION DUE DATE

170km, 400kV double circuit line for power

evacuation from Silali Geothermal Field 2016 Jun

TRANSMISSION PROJECTS…

2016 Oct 75km, 400kV double circuit line for power

evacuation from 960MW Kitui Coal plant

Silali-

Menengai-

Rongai

Isinya –

Nairobi East

3.

OTHER INVESTMENT OPPORTUNITIES… 3.

1. Strategic Petroleum Reserves

2. Single Buoy Mooring Facility

3. LAPPSET

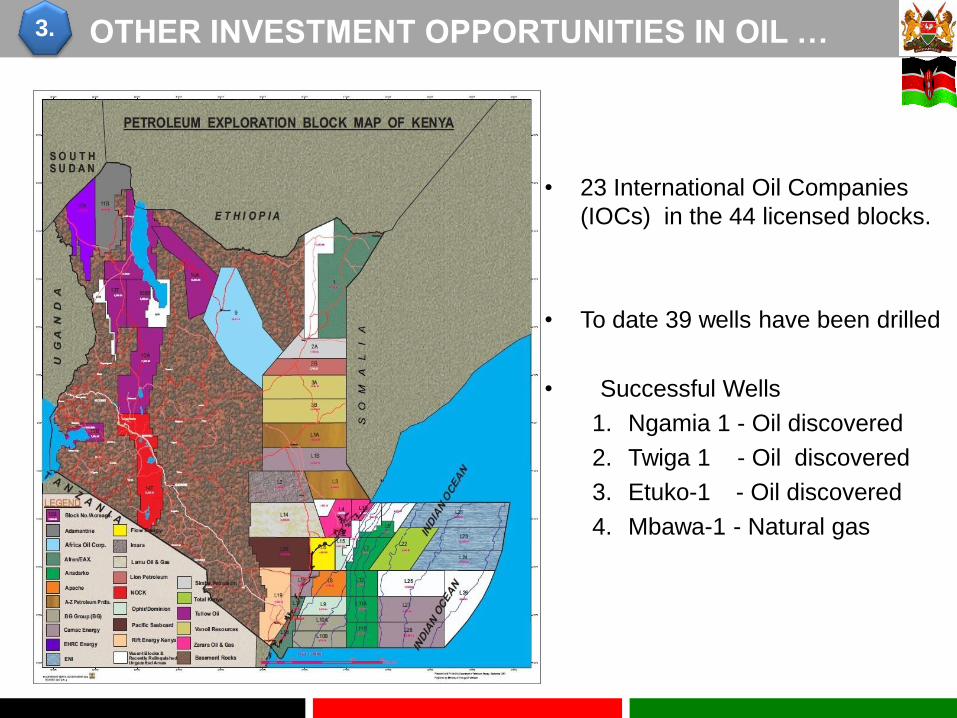

OTHER INVESTMENT OPPORTUNITIES IN OIL … 3.

• 23 International Oil Companies

(IOCs) in the 44 licensed blocks.

• To date 39 wells have been drilled

• Successful Wells

1. Ngamia 1 - Oil discovered

2. Twiga 1 - Oil discovered

3. Etuko-1 - Oil discovered

4. Mbawa-1 - Natural gas

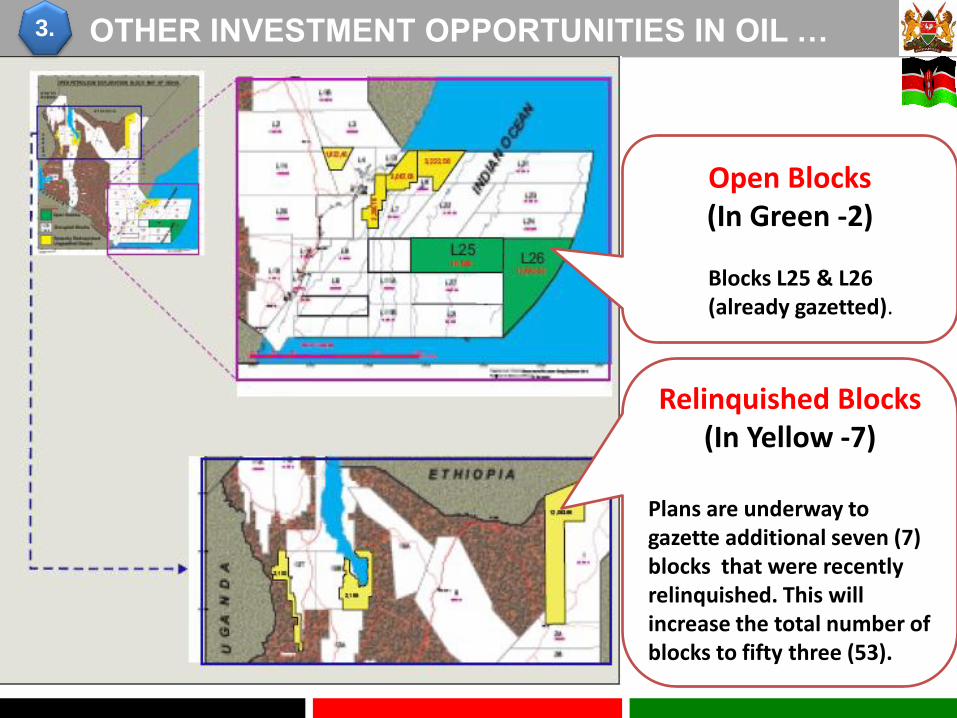

Relinquished Blocks (In Yellow -7)

Plans are underway to gazette additional seven (7) blocks that were recently relinquished. This will increase the total number of blocks to fifty three (53).

Open Blocks (In Green -2)

Blocks L25 & L26

(already gazetted).

3. OTHER INVESTMENT OPPORTUNITIES IN OIL …

Mutomo

Kitui

Mwingi

Mutitu

MUTITU

ZOMBE

VOO

ENDAU

MIA

MB

AN

I

ATHI

YAT

TA

YA

TTA

MUTHA

MUTOMO

IKU

TH

A

NZA

MB

AN

I

MUINUU

TSEIKURU

THARAKA

MIVUKONI

KATSE

NGOMENI

UKASI

MIG

WA

NI

MUTUNGONI

MATINYANI

IKANGA

KISASI

MU

LA

NG

OM

IWA

NI

KANZIKU

Kyuso

KYUSO

ENDUI

Basement rocks (Mozambiquan Belt)

Mui Basin

Wamwathi

Mutwang’ombe

Mutitu

Kabati

Yoonye

Zombe

Mui

Isekele

MathukiKarunga

4 60 2 Km

Basement rocks

Mui Basin Sediments

TAN

A R

IVE

R

GAR

ISSA

KIL

IFI

TAITA TAVETA

KWALE

MA

CH

AK

OS

MERU

EM

BU

ISIO

LO

LAMU

IND

IAN

OC

EA

N

Mombasa

SO

MA

LIA

TANZANIAINDEX 2

North

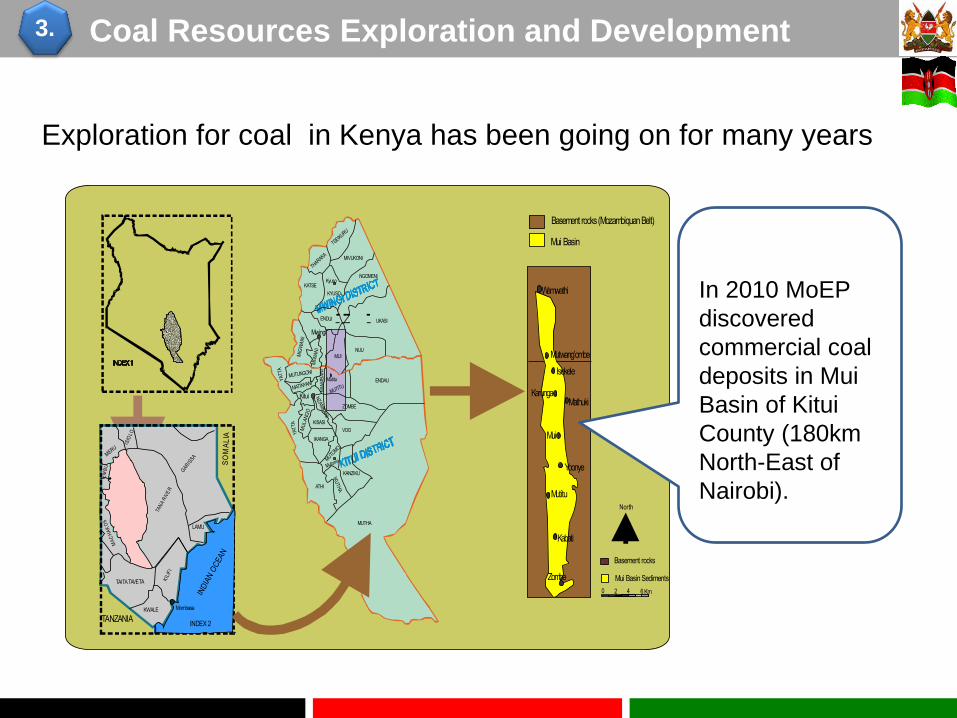

3. Coal Resources Exploration and Development

Exploration for coal in Kenya has been going on for many years

In 2010 MoEP

discovered

commercial coal

deposits in Mui

Basin of Kitui

County (180km

North-East of

Nairobi).

Endau

Mwingi

Waita

Kamuwongo

Kisa si

Katse Kyuso

Tseikuru

Usueni

Ngom eni

EnziuNguni

BLOCK D

BLOCK C

BLOCK B

BLOCK A

Kisa si

Kitui

Mui

Kabati

Migwani

Endau

Mwingi

Waita

Kamuwongo

Kisasi

Katse Kyuso

Tseikuru

Usueni

Ngomeni

EnziuNguni

BLOCK D

BLOCK C

BLOCK B

BLOCK A

Kisasi

Kitui

Mui

Kabati

Migwani

MWINGI

KITUI

LOCATION OF MUI BASIN IN MWINGI & KITUI DISTRICTS

4 4.02 0 8.0 12.0 16.0

KILOMETRES

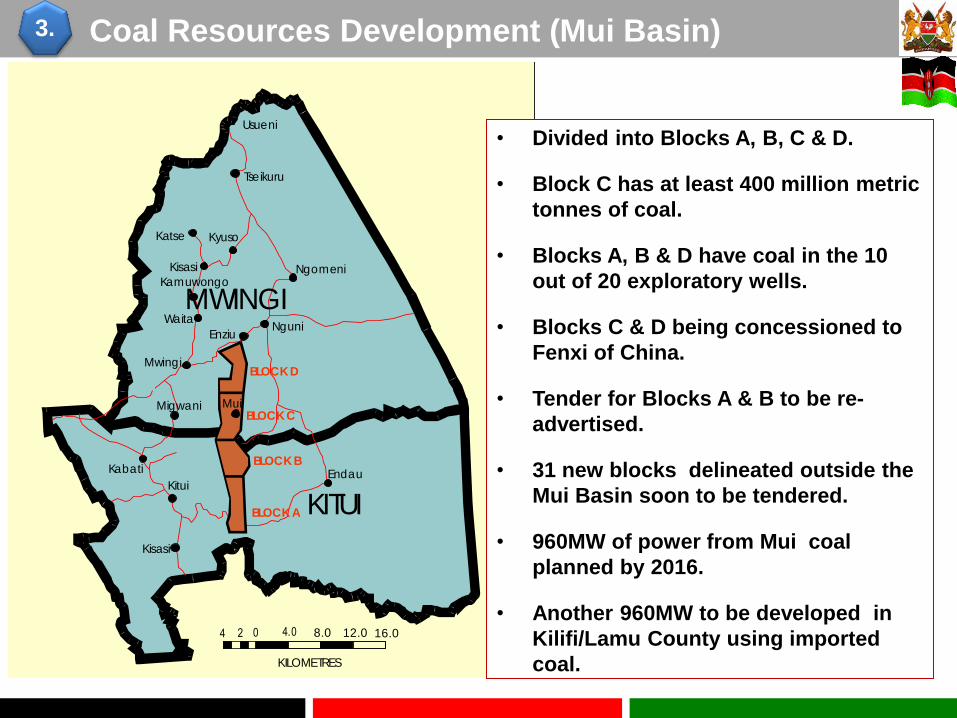

3. Coal Resources Development (Mui Basin)

• Divided into Blocks A, B, C & D.

• Block C has at least 400 million metric

tonnes of coal.

• Blocks A, B & D have coal in the 10

out of 20 exploratory wells.

• Blocks C & D being concessioned to

Fenxi of China.

• Tender for Blocks A & B to be re-

advertised.

• 31 new blocks delineated outside the

Mui Basin soon to be tendered.

• 960MW of power from Mui coal

planned by 2016.

• Another 960MW to be developed in

Kilifi/Lamu County using imported

coal.

THANK YOU

Related Documents