PREPARED FOR THE COMING OF AGE FOR SENIORS HOUSING By: Zach Bowyer, MAI November 14, 2013 This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

SeniorsHousing_Bowyer

Aug 12, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PREPARED FORTHE COMING OF AGE FOR SENIORS HOUSINGBy: Zach Bowyer, MAINovember 14, 2013

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

2 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

What Drives Pricing What Drives Value Case Studies CBRE Insights & Outlook

The Coming of Age for Seniors HousingPRESENTATION OVERVIEW

Objective: As seniors housing marks its place as a core property type within institutional portfolios, a greater understanding of the sector and more sophisticated approach to operating these assets will allow investors to further diversify their portfolios to achieve higher risk adjusted returns in a changing economic environment.

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

3 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

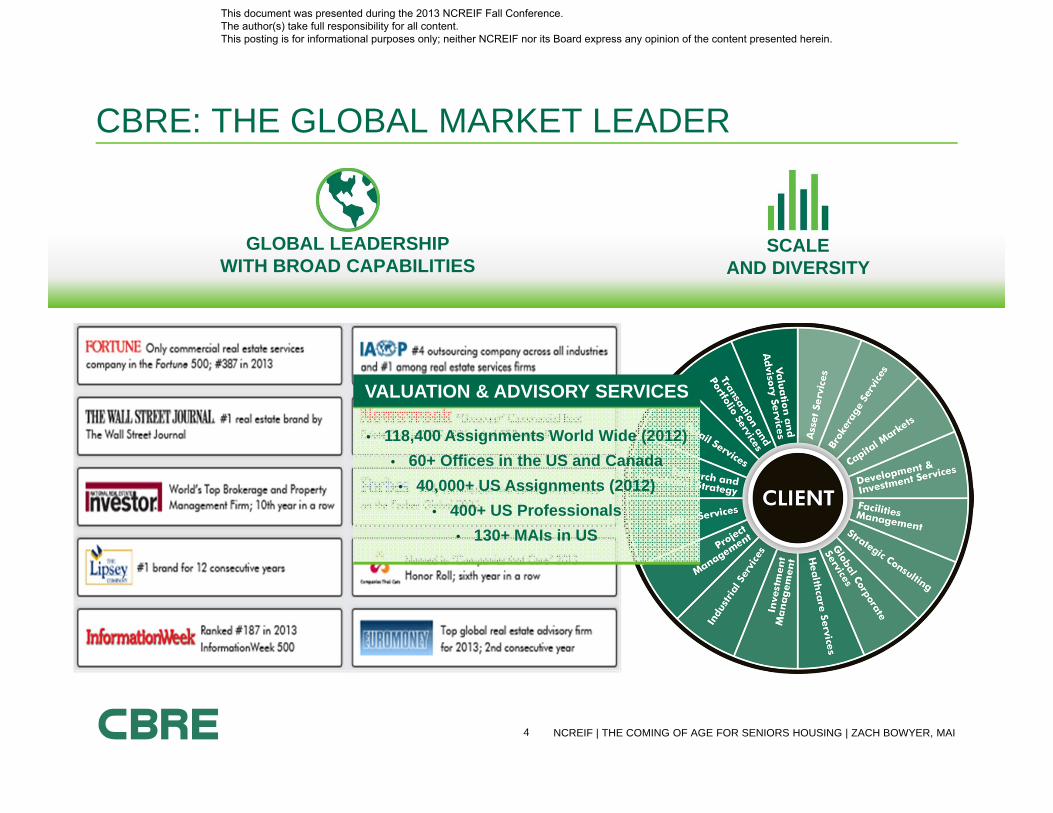

CBRE: THE GLOBAL MARKET LEADER

GLOBAL LEADERSHIP WITH BROAD CAPABILITIES

SCALE AND DIVERSITY

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

4 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

CBRE: THE GLOBAL MARKET LEADER

GLOBAL LEADERSHIP WITH BROAD CAPABILITIES

SCALE AND DIVERSITY

• 118,400 Assignments World Wide (2012)• 60+ Offices in the US and Canada

• 40,000+ US Assignments (2012)• 400+ US Professionals

• 130+ MAIs in US

VALUATION & ADVISORY SERVICES

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

5 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

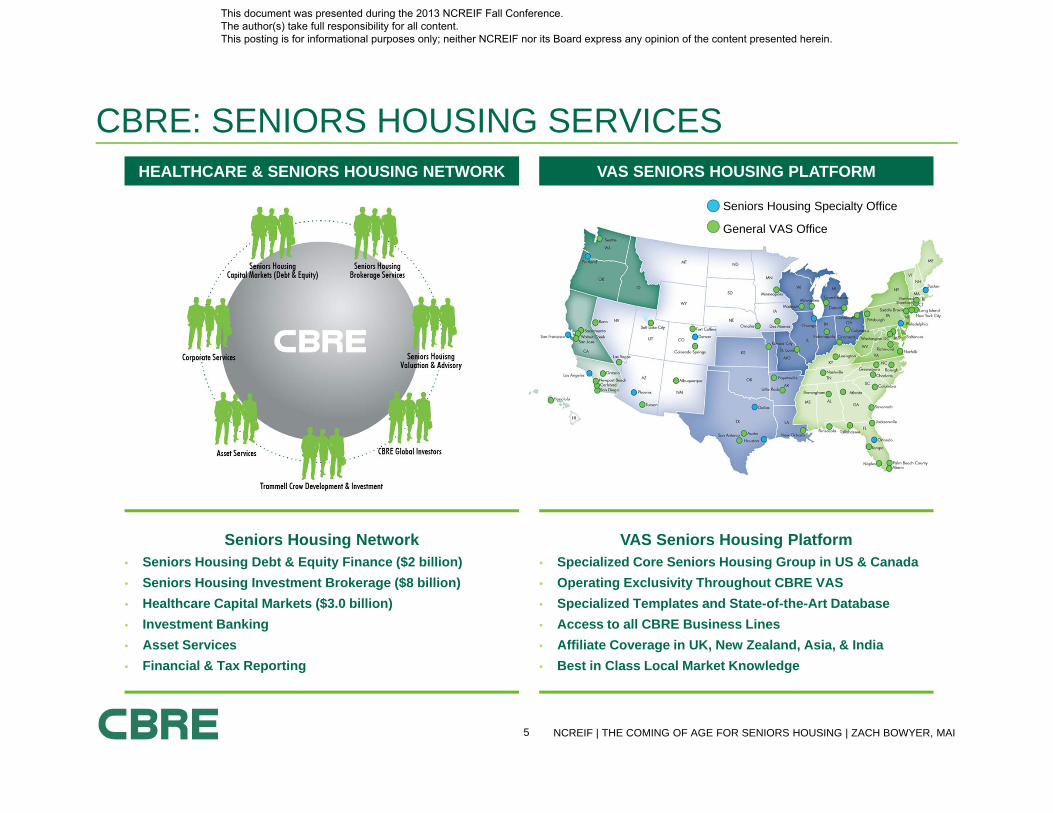

CBRE: SENIORS HOUSING SERVICESHEALTHCARE & SENIORS HOUSING NETWORK VAS SENIORS HOUSING PLATFORM

VAS Seniors Housing Platform• Specialized Core Seniors Housing Group in US & Canada• Operating Exclusivity Throughout CBRE VAS • Specialized Templates and State-of-the-Art Database• Access to all CBRE Business Lines• Affiliate Coverage in UK, New Zealand, Asia, & India • Best in Class Local Market Knowledge

Seniors Housing Specialty Office

Seniors Housing Network• Seniors Housing Debt & Equity Finance ($2 billion) • Seniors Housing Investment Brokerage ($8 billion)• Healthcare Capital Markets ($3.0 billion)• Investment Banking• Asset Services• Financial & Tax Reporting

General VAS Office

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

6 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

Inputs for Real Estate ValuesWHAT DRIVES PRICING

To paraphrase Buzz McCoy, real estate valuations are based on the following components:

InterestRates

CapitalMarkets

PropertyMarkets

Economy

As an appraiser, our world revolves around property markets which include property level operations and local market supply and demand fundamentals.

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

7 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

Cap Rate Trends vs. Apartment Caps & 10-Year TreasuryWHAT DRIVES PRICING

Source: NIC MAP & CBRE Econometric Advisors

0%

2%

4%

6%

8%

10%

12%

14%

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

NC

AL

IL

Apartment

10Y - T

Rational Market DemographicInfluence

IrrationalExuberance

OverCorrection

REITImpact Back to Rational Market

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

8 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

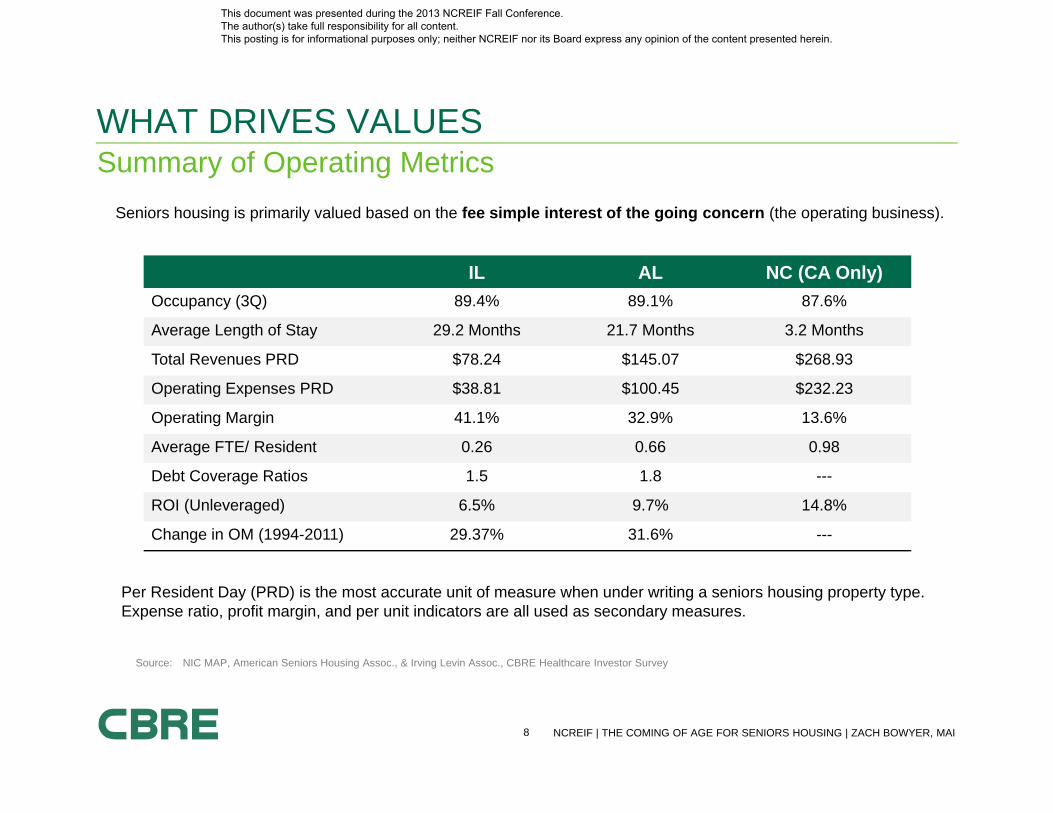

Summary of Operating MetricsWHAT DRIVES VALUES

IL AL NC (CA Only)Occupancy (3Q) 89.4% 89.1% 87.6%

Average Length of Stay 29.2 Months 21.7 Months 3.2 Months

Total Revenues PRD $78.24 $145.07 $268.93

Operating Expenses PRD $38.81 $100.45 $232.23

Operating Margin 41.1% 32.9% 13.6%

Average FTE/ Resident 0.26 0.66 0.98

Debt Coverage Ratios 1.5 1.8 ---

ROI (Unleveraged) 6.5% 9.7% 14.8%

Change in OM (1994-2011) 29.37% 31.6% ---

Source: NIC MAP, American Seniors Housing Assoc., & Irving Levin Assoc., CBRE Healthcare Investor Survey

Seniors housing is primarily valued based on the fee simple interest of the going concern (the operating business).

Per Resident Day (PRD) is the most accurate unit of measure when under writing a seniors housing property type. Expense ratio, profit margin, and per unit indicators are all used as secondary measures.

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

9 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

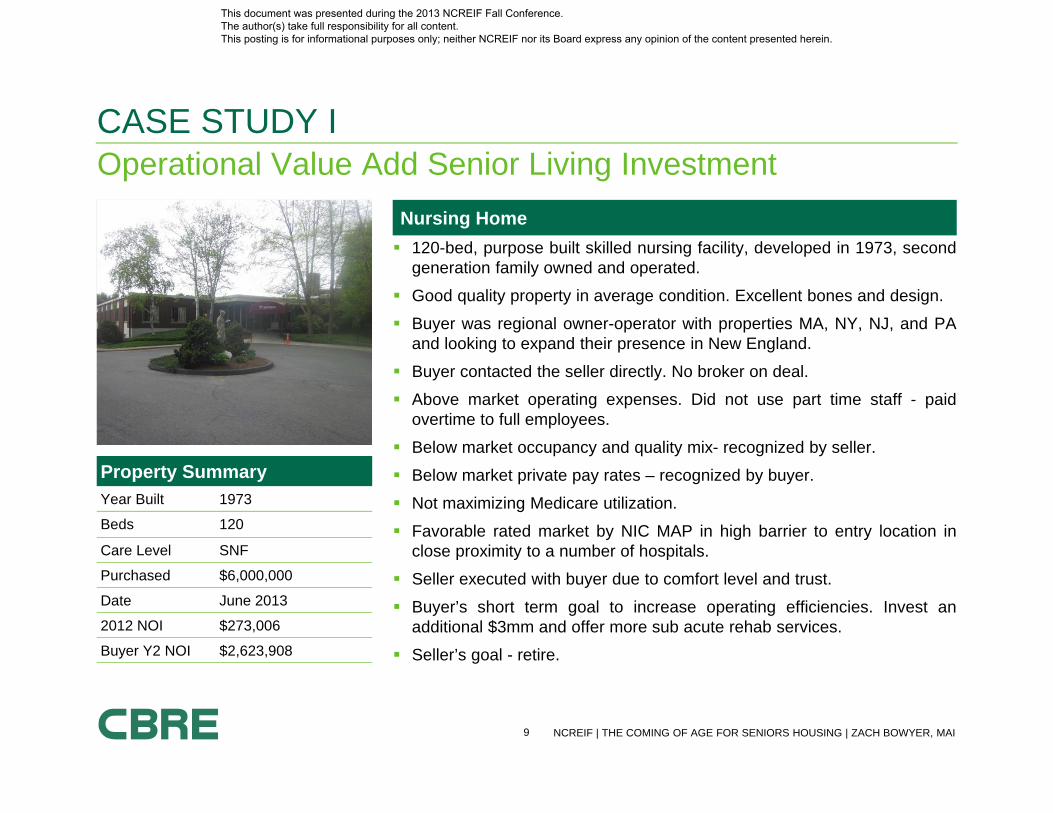

Operational Value Add Senior Living InvestmentCASE STUDY I

Nursing Home 120-bed, purpose built skilled nursing facility, developed in 1973, second

generation family owned and operated.

Good quality property in average condition. Excellent bones and design.

Buyer was regional owner-operator with properties MA, NY, NJ, and PAand looking to expand their presence in New England.

Buyer contacted the seller directly. No broker on deal.

Above market operating expenses. Did not use part time staff - paidovertime to full employees.

Below market occupancy and quality mix- recognized by seller.

Below market private pay rates – recognized by buyer.

Not maximizing Medicare utilization.

Favorable rated market by NIC MAP in high barrier to entry location inclose proximity to a number of hospitals.

Seller executed with buyer due to comfort level and trust.

Buyer’s short term goal to increase operating efficiencies. Invest anadditional $3mm and offer more sub acute rehab services.

Seller’s goal - retire.

Property SummaryYear Built 1973

Beds 120

Care Level SNF

Purchased $6,000,000

Date June 2013

2012 NOI $273,006

Buyer Y2 NOI $2,623,908

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

10 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

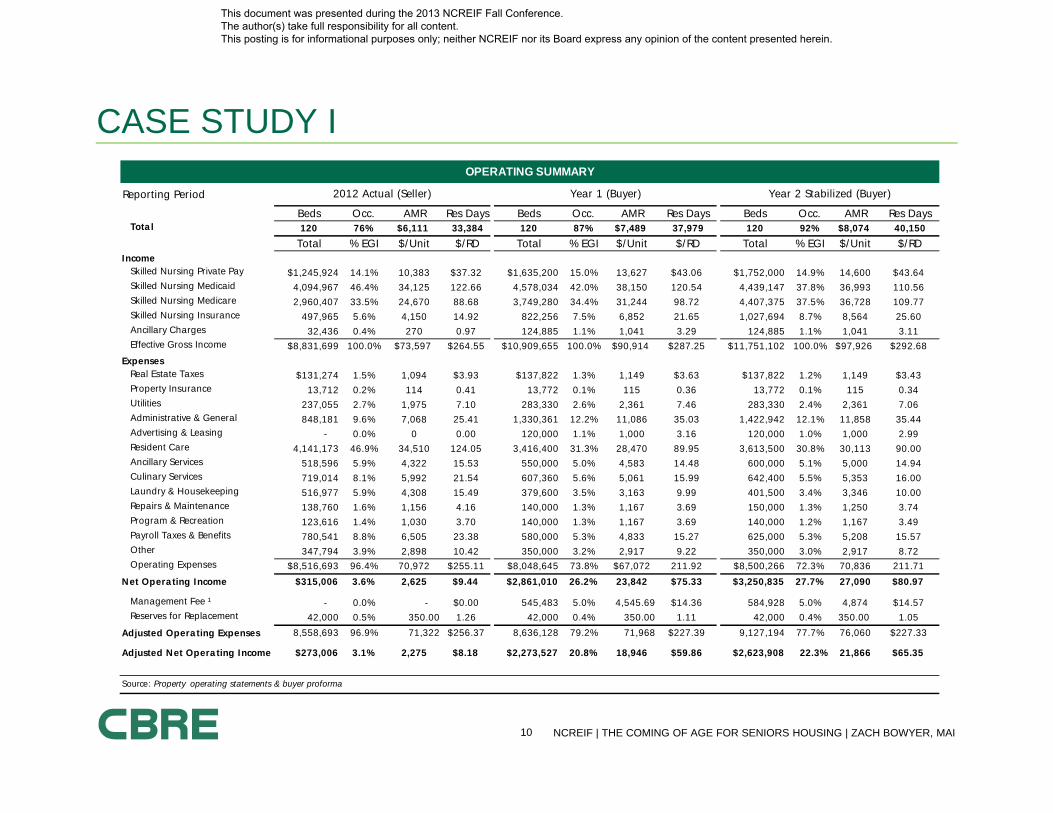

CASE STUDY IOPERATING SUMMARY

Reporting Period

Beds Occ. AMR Res Days Beds Occ. AMR Res Days Beds Occ. AMR Res DaysTota l 120 76% $6,111 33,384 120 87% $7,489 37,979 120 92% $8,074 40,150

Total % EGI $/Unit $/RD Total % EGI $/Unit $/RD Total % EGI $/Unit $/RDIncome

Skilled Nursing Private Pay $1,245,924 14.1% 10,383 $37.32 $1,635,200 15.0% 13,627 $43.06 $1,752,000 14.9% 14,600 $43.64Skilled Nursing Medicaid 4,094,967 46.4% 34,125 122.66 4,578,034 42.0% 38,150 120.54 4,439,147 37.8% 36,993 110.56Skilled Nursing Medicare 2,960,407 33.5% 24,670 88.68 3,749,280 34.4% 31,244 98.72 4,407,375 37.5% 36,728 109.77Skilled Nursing Insurance 497,965 5.6% 4,150 14.92 822,256 7.5% 6,852 21.65 1,027,694 8.7% 8,564 25.60Ancillary Charges 32,436 0.4% 270 0.97 124,885 1.1% 1,041 3.29 124,885 1.1% 1,041 3.11Effective Gross Income $8,831,699 100.0% $73,597 $264.55 $10,909,655 100.0% $90,914 $287.25 $11,751,102 100.0% $97,926 $292.68

ExpensesReal Estate Taxes $131,274 1.5% 1,094 $3.93 $137,822 1.3% 1,149 $3.63 $137,822 1.2% 1,149 $3.43Property Insurance 13,712 0.2% 114 0.41 13,772 0.1% 115 0.36 13,772 0.1% 115 0.34Utilities 237,055 2.7% 1,975 7.10 283,330 2.6% 2,361 7.46 283,330 2.4% 2,361 7.06Administrative & General 848,181 9.6% 7,068 25.41 1,330,361 12.2% 11,086 35.03 1,422,942 12.1% 11,858 35.44Advertising & Leasing - 0.0% 0 0.00 120,000 1.1% 1,000 3.16 120,000 1.0% 1,000 2.99Resident Care 4,141,173 46.9% 34,510 124.05 3,416,400 31.3% 28,470 89.95 3,613,500 30.8% 30,113 90.00Ancillary Services 518,596 5.9% 4,322 15.53 550,000 5.0% 4,583 14.48 600,000 5.1% 5,000 14.94Culinary Services 719,014 8.1% 5,992 21.54 607,360 5.6% 5,061 15.99 642,400 5.5% 5,353 16.00Laundry & Housekeeping 516,977 5.9% 4,308 15.49 379,600 3.5% 3,163 9.99 401,500 3.4% 3,346 10.00Repairs & Maintenance 138,760 1.6% 1,156 4.16 140,000 1.3% 1,167 3.69 150,000 1.3% 1,250 3.74Program & Recreation 123,616 1.4% 1,030 3.70 140,000 1.3% 1,167 3.69 140,000 1.2% 1,167 3.49Payroll Taxes & Benefits 780,541 8.8% 6,505 23.38 580,000 5.3% 4,833 15.27 625,000 5.3% 5,208 15.57Other 347,794 3.9% 2,898 10.42 350,000 3.2% 2,917 9.22 350,000 3.0% 2,917 8.72Operating Expenses $8,516,693 96.4% 70,972 $255.11 $8,048,645 73.8% $67,072 211.92 $8,500,266 72.3% 70,836 211.71

Net Opera ting Income $315,006 3.6% 2,625 $9.44 $2,861,010 26.2% 23,842 $75.33 $3,250,835 27.7% 27,090 $80.97

Management Fee ¹ - 0.0% - $0.00 545,483 5.0% 4,545.69 $14.36 584,928 5.0% 4,874 $14.57Reserves for Replacement 42,000 0.5% 350.00 1.26 42,000 0.4% 350.00 1.11 42,000 0.4% 350.00 1.05

Adjusted Opera ting Expenses 8,558,693 96.9% 71,322 $256.37 8,636,128 79.2% 71,968 $227.39 9,127,194 77.7% 76,060 $227.33

Adjusted Net Opera ting Income $273,006 3.1% 2,275 $8.18 $2,273,527 20.8% 18,946 $59.86 $2,623,908 22.3% 21,866 $65.35

Source: Property operating statements & buyer proforma

2012 Actual (Seller) Year 1 (Buyer) Year 2 Stabilized (Buyer)

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

11 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

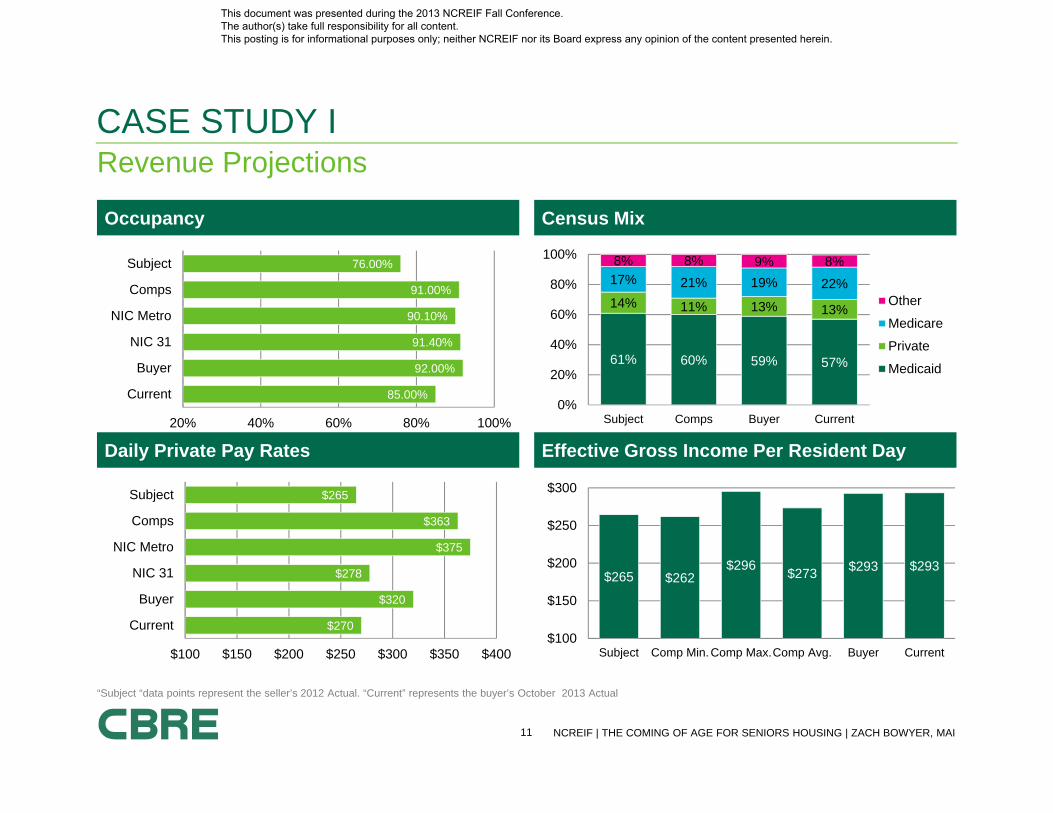

Revenue ProjectionsCASE STUDY I

Occupancy Census Mix

Daily Private Pay Rates Effective Gross Income Per Resident Day

61% 60% 59% 57%

14% 11% 13% 13%

17% 21% 19% 22%

8% 8% 9% 8%

0%

20%

40%

60%

80%

100%

Subject Comps Buyer Current

Other

Medicare

Private

Medicaid

$270

$320

$278

$375

$363

$265

$100 $150 $200 $250 $300 $350 $400

Current

Buyer

NIC 31

NIC Metro

Comps

Subject

$265 $262$296 $273 $293 $293

$100

$150

$200

$250

$300

Subject Comp Min. Comp Max.Comp Avg. Buyer Current

85.00%

92.00%

91.40%

90.10%

91.00%

76.00%

20% 40% 60% 80% 100%

Current

Buyer

NIC 31

NIC Metro

Comps

Subject

“Subject “data points represent the seller’s 2012 Actual. “Current” represents the buyer’s October 2013 Actual

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

12 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

Expense Projections and The Bottom LineCASE STUDY I

Operating Costs Per Resident Day (PRD) Expense Ratio (Before Mgt Fee & Reserves)

Profit Margin (Before Mgt Fee & Reserves) NOI PRD (Before Mgt Fee & Reserves)

16.00%

27.70%

8.60%

22.40%

17.80%

3.60%

0% 5% 10% 15% 20% 25% 30% 35%

Current

Buyer

Comp Min.

Comp Max.

Comp Avg.

Subject

$8

$32

$59

$36

$60$40

$0$10$20$30$40$50$60$70

Subject Comp Min.Comp Max.Comp Avg. Buyer Current

$253.12

$211.92

$228.06

$240.32

$204.39

$255.51

$100 $150 $200 $250 $300 $350

Current

Buyer

Comp Avg.

Comp Max.

Comp Min.

Subject

97%78% 81% 83% 72% 84%

0%

20%

40%

60%

80%

100%

Subject Comp Min.Comp Max.Comp Avg. Buyer Current

“Subject “data points represent the seller’s 2012 Actual. “Current” represents the buyer’s October 2013 Actual

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

13 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

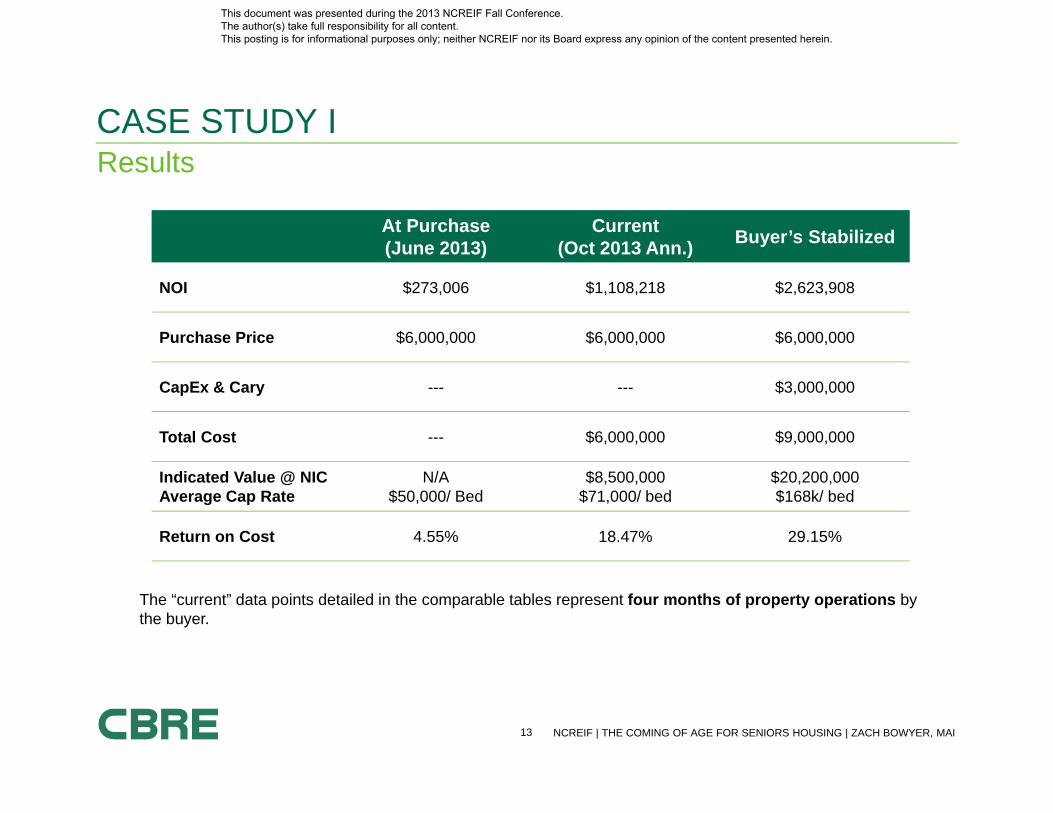

ResultsCASE STUDY I

At Purchase(June 2013)

Current (Oct 2013 Ann.) Buyer’s Stabilized

NOI $273,006 $1,108,218 $2,623,908

Purchase Price $6,000,000 $6,000,000 $6,000,000

CapEx & Cary --- --- $3,000,000

Total Cost --- $6,000,000 $9,000,000

Indicated Value @ NIC Average Cap Rate

N/A$50,000/ Bed

$8,500,000$71,000/ bed

$20,200,000$168k/ bed

Return on Cost 4.55% 18.47% 29.15%

The “current” data points detailed in the comparable tables represent four months of property operations bythe buyer.

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

14 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

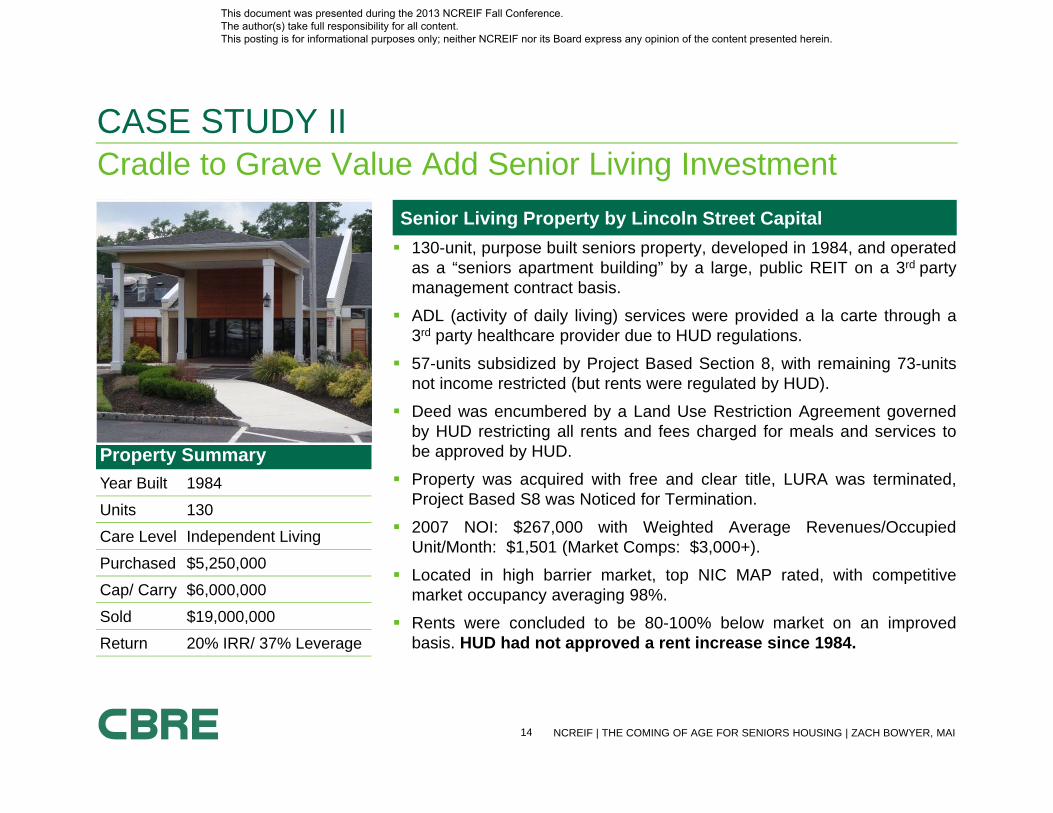

Cradle to Grave Value Add Senior Living InvestmentCASE STUDY II

Senior Living Property by Lincoln Street Capital 130-unit, purpose built seniors property, developed in 1984, and operated

as a “seniors apartment building” by a large, public REIT on a 3rd partymanagement contract basis.

ADL (activity of daily living) services were provided a la carte through a3rd party healthcare provider due to HUD regulations.

57-units subsidized by Project Based Section 8, with remaining 73-unitsnot income restricted (but rents were regulated by HUD).

Deed was encumbered by a Land Use Restriction Agreement governedby HUD restricting all rents and fees charged for meals and services tobe approved by HUD.

Property was acquired with free and clear title, LURA was terminated,Project Based S8 was Noticed for Termination.

2007 NOI: $267,000 with Weighted Average Revenues/OccupiedUnit/Month: $1,501 (Market Comps: $3,000+).

Located in high barrier market, top NIC MAP rated, with competitivemarket occupancy averaging 98%.

Rents were concluded to be 80-100% below market on an improvedbasis. HUD had not approved a rent increase since 1984.

Property SummaryYear Built 1984

Units 130

Care Level Independent Living

Purchased $5,250,000

Cap/ Carry $6,000,000

Sold $19,000,000

Return 20% IRR/ 37% Leverage

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

15 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

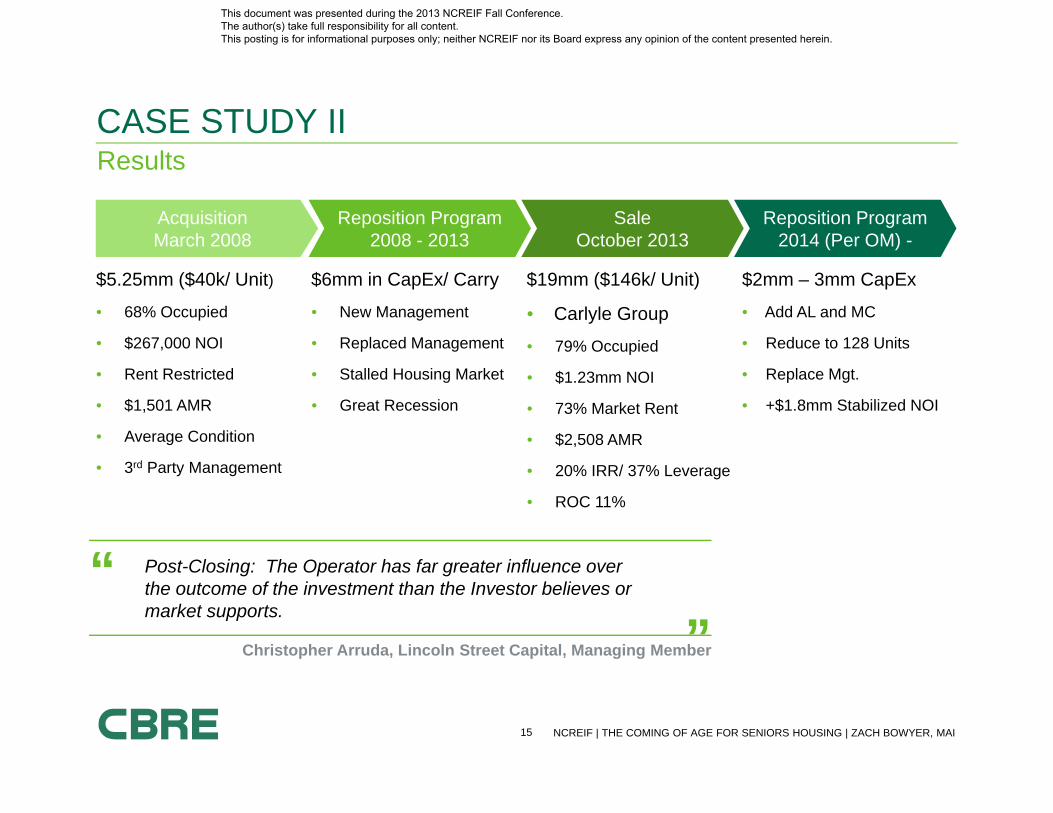

ResultsCASE STUDY II

$5.25mm ($40k/ Unit)

• 68% Occupied

• $267,000 NOI

• Rent Restricted

• $1,501 AMR

• Average Condition

• 3rd Party Management

$6mm in CapEx/ Carry

• New Management

• Replaced Management

• Stalled Housing Market

• Great Recession

$19mm ($146k/ Unit)

• Carlyle Group

• 79% Occupied

• $1.23mm NOI

• 73% Market Rent

• $2,508 AMR

• 20% IRR/ 37% Leverage

• ROC 11%

$2mm – 3mm CapEx

• Add AL and MC

• Reduce to 128 Units

• Replace Mgt.

• +$1.8mm Stabilized NOI

AcquisitionMarch 2008

Reposition Program2008 - 2013

SaleOctober 2013

Reposition Program2014 (Per OM) -

“ Post-Closing: The Operator has far greater influence over the outcome of the investment than the Investor believes or market supports.

”Christopher Arruda, Lincoln Street Capital, Managing Member

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

16 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

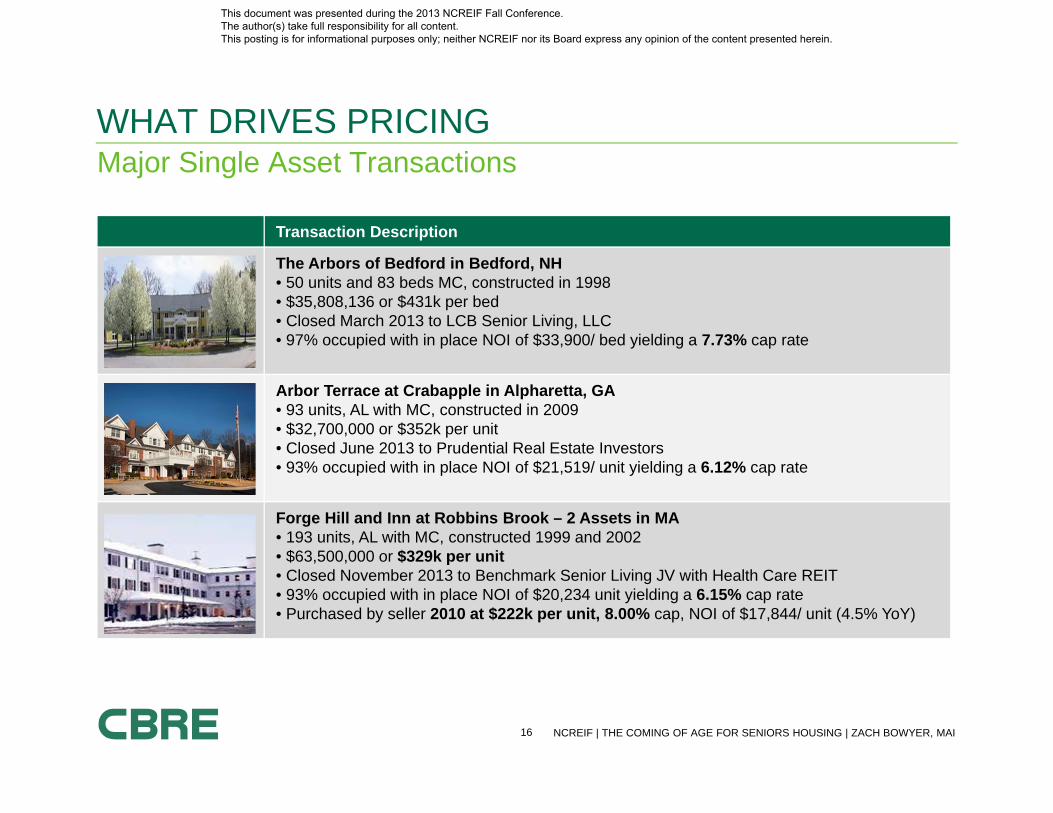

Major Single Asset TransactionsWHAT DRIVES PRICING

Transaction Description

The Arbors of Bedford in Bedford, NH• 50 units and 83 beds MC, constructed in 1998• $35,808,136 or $431k per bed• Closed March 2013 to LCB Senior Living, LLC• 97% occupied with in place NOI of $33,900/ bed yielding a 7.73% cap rate

Arbor Terrace at Crabapple in Alpharetta, GA• 93 units, AL with MC, constructed in 2009• $32,700,000 or $352k per unit• Closed June 2013 to Prudential Real Estate Investors• 93% occupied with in place NOI of $21,519/ unit yielding a 6.12% cap rate

Forge Hill and Inn at Robbins Brook – 2 Assets in MA• 193 units, AL with MC, constructed 1999 and 2002• $63,500,000 or $329k per unit• Closed November 2013 to Benchmark Senior Living JV with Health Care REIT• 93% occupied with in place NOI of $20,234 unit yielding a 6.15% cap rate• Purchased by seller 2010 at $222k per unit, 8.00% cap, NOI of $17,844/ unit (4.5% YoY)

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

17 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

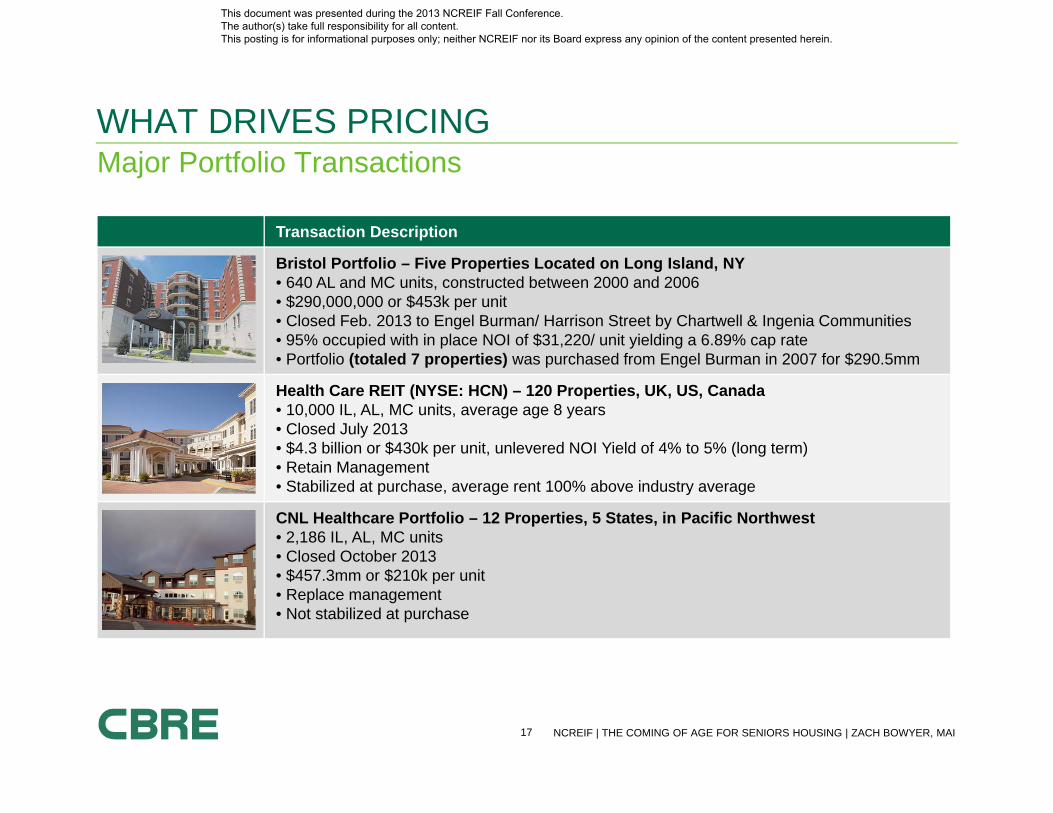

Major Portfolio TransactionsWHAT DRIVES PRICING

Transaction Description

Bristol Portfolio – Five Properties Located on Long Island, NY• 640 AL and MC units, constructed between 2000 and 2006• $290,000,000 or $453k per unit• Closed Feb. 2013 to Engel Burman/ Harrison Street by Chartwell & Ingenia Communities• 95% occupied with in place NOI of $31,220/ unit yielding a 6.89% cap rate• Portfolio (totaled 7 properties) was purchased from Engel Burman in 2007 for $290.5mm

Health Care REIT (NYSE: HCN) – 120 Properties, UK, US, Canada• 10,000 IL, AL, MC units, average age 8 years• Closed July 2013• $4.3 billion or $430k per unit, unlevered NOI Yield of 4% to 5% (long term)• Retain Management• Stabilized at purchase, average rent 100% above industry average

CNL Healthcare Portfolio – 12 Properties, 5 States, in Pacific Northwest• 2,186 IL, AL, MC units• Closed October 2013• $457.3mm or $210k per unit• Replace management• Not stabilized at purchase

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

18 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

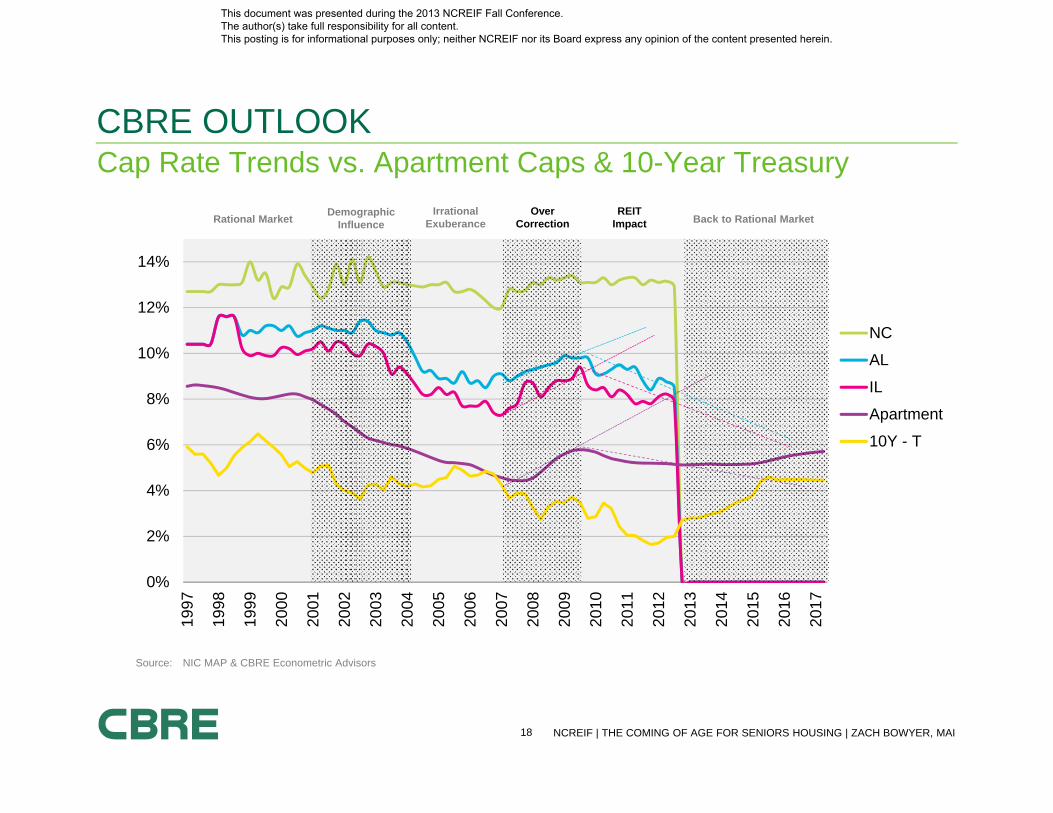

Cap Rate Trends vs. Apartment Caps & 10-Year TreasuryCBRE OUTLOOK

Source: NIC MAP & CBRE Econometric Advisors

0%

2%

4%

6%

8%

10%

12%

14%

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

NC

AL

IL

Apartment

10Y - T

Rational Market DemographicInfluence

IrrationalExuberance

OverCorrection

REITImpact Back to Rational Market

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

19 NCREIF | THE COMING OF AGE FOR SENIORS HOUSING | ZACH BOWYER, MAI

CBRE INSIGHT

• Understand the property specific operations and understand the market; hire a local or regional operator with scale, experience and relationships in the local market and deeply vest them into the property’s underwritten success.

• Understand where your property fits in the market; current property trend lines may not be telling the whole story.

• Even the strongest market opportunities with the best market capitalizations will fall below expectations if the operator isn’t a good fit or fails to understand the asset strategy and market dynamic.

• Capitalize the opportunity to age your resident base in place throughout their acuity progression.

• Replacing senior living operators mid-stream is far more challenging and costly than the other four property types: office, industrial, retail, and multifamily.

• Expect cap rate compression between AL and IL, and AL and Apts to continue. The increase in capital flow, operational and market understanding, and growth in product demand will continue to mitigate investors’ perceived risk when pricing this property type.

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.

For more information regarding this presentation please contact:Zach Bowyer, MAIManaging Director & Seniors Housing Practice LeaderT +1 617 912 [email protected]

www.cbre.com

This document was presented during the 2013 NCREIF Fall Conference. The author(s) take full responsibility for all content. This posting is for informational purposes only; neither NCREIF nor its Board express any opinion of the content presented herein.