Semiperipheral varieties of capitalism: state capacities and energy policies in BRIC Carlos Henrique Santana Assotiate Researcher at INCT and AvH/Capes Fellow at TU Darmstadt International Conference RETHINKING THE STATE IN GLOBALIZED CAPITALISM 21-24 March 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Semiperipheral varieties of capitalism:statecapacities and energy

policiesinBRIC

CarlosHenriqueSantanaAssotiate Researcher at INCTand

AvH/CapesFellow at TUDarmstadt

International ConferenceRETHINKINGTHESTATEINGLOBALIZEDCAPITALISM

21-24March2018

Why energy policiesamong BRICcountries?

• Between 2000and 2006,55percent of the globalgrowth of CO2emissions happened inChina.In2004,Chinabecame the world’s largest extractor of fossil fuels;two years later,iteclipsed the USasthe topemitter;

• Emissions Embodied inTrade(EET)and Fossil Capital:From 1990to 2009Foreign Direct Investimentsquintupled.Chinawas the main destination forFDInearly twice those of Russia and India combined.In2002,industry inChinaabsorved morethan 90percent of all coal consumed and 48percent of the country’stotalemissions between 2002and 2008were generated inthe export sphere (Malm 2016).

• Beside to be stillacountrywith the most renewable energy inthe world– 43,5percent of totaldomesticenergy supply is renewable – Brazil has discovered inpre-salt one of the world’s most important oil reservesinthe past decade.Thepre-salt province comprises large accumulations of excellent quality,highcommercial value lightoil;

• Due to be the largest naturalgas exporter and second biggest inoil,Russia has an economy and fiscalbudgetincreasingly dependent on energy commodities.

• Despite the percapitaelectricity consumption has been continuously increasing overthe years,India stillhasone of the lowest percapitaconsumption inthe world.India power generation mix is quitesimilarwithChinese – coal playing approximately 70percent.Thechallenge is how to rise the percapta eletricityconsumption inIndia without reproducing the same pattern from China

0

100

200

300

400

500

600

700

800

900

1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Mto

e

Coal** Oil Natural gas Nuclear Hydro Biofuels/waste Geothermal/solar/wind

Total primary energy supply*

IEA Energy Statistics

India

* Excluding electricity trade. ** In this graph, peat and oil shale are aggregated with coal, when relevant.

Statistics on the web: http://www.iea.org/statistics/

For more detailed data, please consult our on-line data service at http://data.iea.org.© OECD/IEA 2016

0

500

1 000

1 500

2 000

2 500

3 000

3 500

1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Mto

e

Coal** Oil Natural gas Nuclear Hydro Biofuels/waste Geothermal/solar/wind

Total primary energy supply*

IEA Energy Statistics

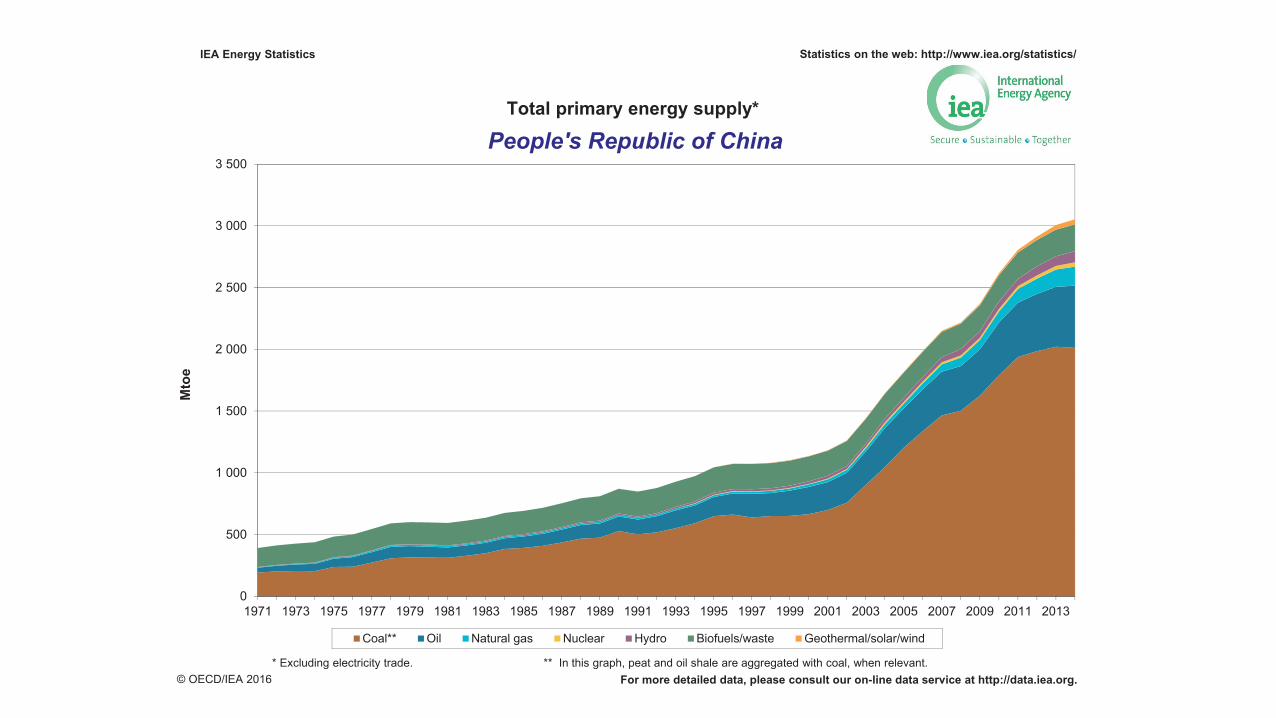

People's Republic of China

* Excluding electricity trade. ** In this graph, peat and oil shale are aggregated with coal, when relevant.

Statistics on the web: http://www.iea.org/statistics/

For more detailed data, please consult our on-line data service at http://data.iea.org.© OECD/IEA 2016

0

50

100

150

200

250

300

350

1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Mto

e

Coal** Oil Natural gas Nuclear Hydro Biofuels/waste Geothermal/solar/wind

Total primary energy supply*

IEA Energy Statistics

Brazil

* Excluding electricity trade. ** In this graph, peat and oil shale are aggregated with coal, when relevant.

Statistics on the web: http://www.iea.org/statistics/

For more detailed data, please consult our on-line data service at http://data.iea.org.© OECD/IEA 2016

0

100

200

300

400

500

600

700

800

900

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mto

e

Coal** Oil Natural gas Nuclear Hydro Biofuels/waste Geothermal/solar/wind

Total primary energy supply*

IEA Energy Statistics

Russian Federation

* Excluding electricity trade. ** In this graph, peat and oil shale are aggregated with coal, when relevant.

Statistics on the web: http://www.iea.org/statistics/

For more detailed data, please consult our on-line data service at http://data.iea.org.© OECD/IEA 2016

0100020003000400050006000700080009000

10000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

TotalCarbon Dioxide Emissions from the Consumption of Energy(Million Metric Tons)

Brazil China India Russia

Source:InternationalEnergyAgency

Source:WorldBank,WorldDevelopment Indicators

0

1000

2000

3000

4000

5000

6000

7000

8000

ElectricPowerConsumption(KWhpercapta)

Brazil China India Russia

Classical State Capacities

• State capacities ascoertion:“Theonly human Gemeinschaft which lays claim tothe monopoly on the legitimated useof physical forceoveracertain geographicalarea”(Weber)

• State capacities asInfrastructural power:“institutional capacities of acentralstate,despotic or not,to penetrate itsterritories and loggistically implementdecisions.This is collective power,“power through”society,coordinating sociallife through state infrastrutures.Itdefinestate asasetof centraland radialinstitutions penetrating itsterritories”(Mann)

• State capacities asbureaucratic performance:“meritocratic recruitment,whichideally is based on somecombination of education and examination;andpredictable career ladder,which provides long-term tangible and intangiblerewards forthose recruited into the bureaucracy”(Rauch and Evans)

What’s missing on state capacities approachto analyse BRICcountries?

• Most of state capacities accounts fail to attend to infranationalvariation instate effects or to analyze coordination (or conflict)between regionaland national ruler;

• Inmultilevel systems,regionalinstitutions impact investments flowsand investitors’decisions inthree distinct ways:

• 1)ensuring complementarity between contradictory organizational(horizontalor vertical)or ownership (public or privat)forms;

• 2)providing (un)reliable information;and• 3)enhancing (or reducing)the uncertainty and credibility of higher-level decisions and policies(Sinha 2005)

Howexploreenergypolicyasaninstrumentthroughwhichstatecapacitiesorganizeandfeedthemselvesasanaxisofinstitutional

complementaritiesonBRICcountries?• 1- recognitionofvariousdomesticinstitutionsasthemostrelevantfactorforunderstandingthemaintrendsinenergypolicy;

• 2- panoramaoffederalismdilemmasthataffectedenergypoliciesinthe1990sthatareimportantforthecomprehensionofmarketreformsaswellfortheevaluationofthecentralizationmovementwhichoccurredinthefollowingdecade;

• 3- roleofadministrativereforms,ortheabsencethereof,inordertounderstandthebureaucraticcapacitiesasacoordinatingelementofenergypolicies;

• 4- theroleofpublicbanksandstate-ownedenergycompaniesasaninstrumentofpolicysupportaswellascircumventingthecentrifugalmechanismsofstatecapacities

Whydomesticinstitutionsasthemostrelevantfactorforunderstandingthemaintrendsinenergypolicy?

• 1)provideenergyatpricesthatpermitthesupplychainofotherindustriestoexportgoodsatacompetitiveprice;

• 2)instrumentoffiscal,monetaryanddistributiveaccommodation,asitservesasanimportantsourceofrevenuecollectionforthegovernmentandmoderatesinflationarypressures,whichpreventsthelossofwages’purchasingpower;

• 3)instrumentforpoliticalbargainingandaccommodatedomesticpoliticalstrugglesamonginterestgroupsandinstitutionaldecision-makerslayers.Energybillsareacentralinstrumentforguaranteeingmacroeconomicmaneuveringspacefornationalgovernment,aswellaslong-termgrowth.

Developmental Triad

CentralState

BusinessActorsSubnational StateActors

Multi-level Model

CentralPolicyElites

Institutions at FederalLevel:State-Owned Enterprises(Banksand EnergyCompanies)Regulatory agencies

RegionalPolicyElites

Institutions at RegionalLevels

PrivateBusinessGroups

InvestmentLevels

Source:Sinha (2003)

Thefederalism dilemmas

• Though trends,rhythms and pressures between strategic actors mayhave gone indiverging directions,the necessity to stabilizeendogenous pressures inthe political systemand incorporatestrategic domestic powers innational policy solutions have beeninescapable themes forenergy policy guidelines.

• Inorderforthistobedone,itisnecessarytoemphasizethesizeandshapeofthestate,observingtheimplementationofeconomicpoliciesastheproductofanintergovernmentalinteraction.Inotherwords:atypeof“theoryofpolycentrichierarchy.”(Sinha2005)

China• ThemainpolicystrategyoftheChineseCommunistParty’sleadersforimplementingtheeconomicreformwasfinancialdecentralization,orasitwaspopularlyknown:“eatinginseparatekitchens”(fenzao chifou).Basedonfinancialautonomyforprovincialgovernments,thisstrategyguaranteedtangibleinstrumentsoffinancialincentivestosub-nationalbureaucraticleadershiptosupportthereform’sagenda.(Oi1992).

• EventhoughtheChinesestateisunitary,differentfromRussia,BrazilandIndia(thatarefederal),thereformsthattookplaceunderDengXiaopingincorporatedtheprovincesatthecenterofthedecision-makingprocess,significantlyexpandingtheirbargainingpower;

• Fiscaldecentralizationwasnotonlytheresultofthebeliefthatthemarketwasthebestinstrumentforstimulatinginvestmentandproductivitybutalsothemainpoliticalmechanismforguaranteeinginstrumentsforthemobilizationofstrategicactorsinfavorofreforms(vestedinterests);

• Fromthatpointon,theevolutionoffiscalschemeshaverevealedthecapacitiesofprovincialpubliccadrestoobtainconcessionsfromcentralleaders,necessaryforguaranteeingsupportforreformsaswellastheirownpoliticalcareers.Aconstellationofregionalandlocalgovernmentalactorsthatresultedfromthereformshavethoroughlyconsolidatedthemselvesintheenergysector,includingprovincialgovernments(investmentfunds),state-ownedenterprisesandsubsidiarytransmissiongroups(Cunningham2015).

India

• thecentralgovernment,seekingtoguaranteethefinancialsustainabilityofenergyenterprisesasameansofprotectingitsownfinances,andontheother,stategovernmentsseekingtoguaranteethemeansofsustainingitsconstituencies;

• thecentralgovernmentneedstobargainwithsub-nationalleadershiptoguaranteepoliticalsupportandsub-nationalleadersneedpublicstatebanks,controlledbythecentralgovernment,asameansofrefinancingDiscoms’debts;

• GuaranteeingabalancethatdoesnotharmpowerfulgroupsofinterestinaneconomicallyrelevantwayhasbeenamainchallengeinthearrangementofIndia’spolycentrichierarchy

Russia• Shocktherapyadoptedin1990’smeantanextensiveprivatizationprogramwhichputtogetherdifferentinterestgroupsagainstthecentralizedbureaucracywhohadnaturalresistancetomarket-orientedreforms.“Every enterpriserippedoutofthestateandtransferredtothehandsofaprivateownerwasawayofdestroyingcommunisminRussia”(AnatolyChubais – architectofRussia’sprivatizationprogram).

• Thebackbonefordismantlingofcentralstatesovereigntywasenergysector.Notonlytheprivatizationofstate-ownedenterprisesbutalsobroadadministrativeconcessionsforstategovernors;

• Theunbundling,restructuring,andsaleofelectricityassetsorchestratedbyliberalreformersundercutregionalutilities.Theregionalmonopolies– Energos – weredissolvedandthemostvaluablepowerplantswerebundledinto“de-territorialized”holdingcompanies,theso-calledOGKs.(Wengle 2015)

• Incentivesforacquiringpropertywentbeyondthepursuitofprofit: theassetswerekeytoestablishing,defending,orexpandingone’spositioninthenewsystem.Asasourceofpoliticalpower,ownershipcouldmeansignificantinfluenceoverpoliticians(Barnes)

• Thefinancialcrisesofthe1990scausedtheRussiangovernmenttoalienatevaluablepetroleumandminingassets,usingcontractualmechanisms(loansforshares)wheretheKremlinofferedthecontrolofstate-ownedenterprisesasawayofguaranteeingtheriskofnonpaymentofloanstakenfromprivateagents,popularlyknownasoligarchs(Hoffman2002).

Brazil

• centrifugalpatternofBrazilianfederalism:between1982and1994,abroadprocessofdecentralizationinbothfinancialandpoliticalterms,andapredatoryandnon-cooperativemodelofintergovernmentalrelations;

• Asfarascentralgovernmentlostitsfiscalcapacitiestomakedirectinvestment,thenewConstitutionfrom1988transferredaseriesofrevenueinstrumentstosubnationalspheres.Withthisinmind,theabilitytoimplementinfrastructurepolicies,suchasenergy,hasbeenchallengedwithlackofcoordinationandbureaucraticspecializationwhichthesubnationalgovernmentsdon'thaveinisolation(Afonso;Araújo;andBiasoto 2005).

• between1995-2010,centraladministrationrecoveredfiscalcapacitiesandestablishedcapstofiscalexpendituresofsubnationalspheres- nottoimprovedirectinvestmentcapacitiesofcentralstatebuttofeedapredatorymonetarypolicybasedonhighbenchmarkinterestrates onwhichthestabilizationplanwasbased.

• Thecentralgovernment’surgentnecessitytoregainsovereigntyovermonetaryemissioninmiddleof1990scoincidedwiththecollapseofstategovernments’publicfinancesthatbecamedeprivedofthefinancingmechanisms.Regionalstate-ownedbanksandenterprises(electricityretailers)wereprivatizedinexchangeofnationalizationofregionaldebts;

Tax revenue (centralgovernment)aspercentage of GDP

0

2

4

6

8

10

12

14

16

18

India RussianFederation Brazil

%

Source:WorldDevelopment Indicators (WorldBank)

Bureaucratic cohesion asacoordinating element ofenergy policies

China

• LocalStatecorporatism:Fiscalreformhasassignedlocalgovernmentspropertyrightsoverincreasedincomeandhascreatedstrongincentivesforlocalofficialstopursuelocaleconomicdevelopment.Localgovernmentshavetakenonmanycharacteristicsofabusinesscorporation,withofficialsactingastheequivalentofboardofdirectors

• Corporatizationofenergyministriesintointernationalstate-ownedenterprisesmeantthedismantlingofironricebowlsystemwhichprovidedwelfareservices.

• Civilservice systemwas officially established in1993,however the CCPkept control overthe cadre systemassolid asitwas.Promulgation of the full CivilServants Lawin2005toreplace the Temporary Regulations.Since then the regulations were extended toemployees infunctional organizations;judiciary;mass organizations

• Chineseleadershipcentralizedtheirmanagementin2003usinganeworganizationcalledState-OwnedAssetsSupervisionandAdministrationCommission (SASAC).State-ownedenergycompaniesareamongthemostimportantactorsinthisgroupofstrategiccompaniesundertheSASACumbrella;

India• Market-orientedreformsinIndiahadapragmaticscope,avoidinglargeprivatizationsprocedures:between1991and2008privatizationsraised$12.9billionat2011exchangerates,comparedwithacumulativeinvestmentinthe242survivingCPSEsof$91billionoverthesameperiod(Pratap,2011)Thereare849operatingstatelevelpublicenterprises(SLPEs)inIndiawithabout18.0lakhemployees(GoI,2012).MajorsectorsofoperationofSLPEsaremanufacturing,finance,power,infrastructure,agricultureandalliedservices.

• InthepowersectorinIndia,therehavebeenimpressivedevelopmentsincapacitygeneration,privatesectorparticipation,expansionofelectricitymarketsandrestructuringofstateelectricityboards(SEBs).Distributionandretailsupply,however,remaintheweakestlinkintheentirevaluechain.Theenactment of the Electricity Act,2003mandated unbundling of the SEBs into separateand independent generation,transmission and distribution companies (Discoms).Reforminitiatives were extended through the Accelerated PowerDevelopment and Reforms Programme(APDRP)in2002-03and Restructured-APDRPin2008

• ShortaveragedurationsofemploymentofIndiaAdministrativeService (IAS)workersandagrowingnumberofpositionswithvaryingsalaries,levelsofimportanceandrequirementsallowpoliticalleadershiptopromotelateraltransferstopunishbureaucratics thatgoagainsttheirinterests(Iyer andMani2012);

Russia

• VladimirPutin’sgovernmentpromotedinstitutionalcentralizationinaprivatizationprogramthatrestructuredtheenergyproductionchain,reducingthenumberofstrategicactorsbymeansofconsolidatingthecorporatestructure;

• Whilein1990therewereseventy-oneEnergos,eachtoaregionalgovernment,by2008ahandfulconglomeratesownedmostelectricitygenerationassets.OGK’sassetswerebothmorephysicallydispersedaswellascentrallymanagedthantheenergos hadeverbeen.

• TheadjustmentproposedbyPutinreestablishedtheKremlin’ssovereignruleoverotheractorswithoutnecessaryremovingthemfromeconomicinstitutionalassets.

• WhenemployingthebureaucraticstructureoftheFSB,Putinconstructedaverticalchainofcommand(vertikal’vlasti)that,whenaddedtoaparallelexecutivebranch,creatednewfederaldistrictsandanetworkofregionalinspectors;

• Thesiloviki (namegiventoFSBemployees)fulfilledarole,occupyingimportantpositionsincrucialareasofRussianinfrastructure,followingtheexampleoftheenergy,military,transportandcommunicationscomplex(Kryshtanovskaya andWhite2011)

Brazil

• Deverticalization oftheenergychaininthe1990scausedthecentralgovernmenttolosepartofitsinstrumentsofpolicycoordination.CentralStatebureaucraticmachinewasalsosignificantlydilapidatedwithmassretirementinpublicserviceandsuspensionofhirings foralmostonedecade.State-ownedenterprisesinenergysector,suchasEletrobras andPetrobras,wereforcedtocollaboratewithfiscalsurplustofeedpredatorymonetarypolicy;

• Withthisbackdrop,anoutsourcingfeverbeganinthegreaterpartofpublicservices,reducingthequality,raisingcostsandmultiplyingthenumberofaccidents,suchasblackoutsoroilspillsnearoffshoreplatforms.Investmentsduringtheperiodwereinsufficienttoaccompanytherateofgrowthandtoalsoguaranteethemaintenanceofinstallations.

• Accordingtodataconcerningprofissionalization thereisahighlevelofqualificationintheenergysector’sbureaucracy,71%withspecializedtraining.Butinrelationtoautonomy52%ofemployeesinenergysectorhavestablejobsand49%mentionnedpoliticalinterferenceasaprimaryproblemaffectingworkroutines(Gomide andPereira2016)

State-ownedbanksandenergyenterprisesreinforcingstatecapacitiesandcircumventingthe

centrifugalmechanisms

-8672-13830 -15389

-37986-44469

-71621-67336

-58275

-80000

-70000

-60000

-50000

-40000

-30000

-20000

-10000

02005-06 2006-07 2007-08 2008-09 2009-10 2012-13 2013-14 2014-15

AggregateLosses- IndiaUtitlitiessellingdirectlytoconsummers(SubsidyReceivedBasis)

RsCrores

Source:PowerFinance CorporationLtd.

0

2000

4000

6000

8000

10000

12000

14000

16000

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15

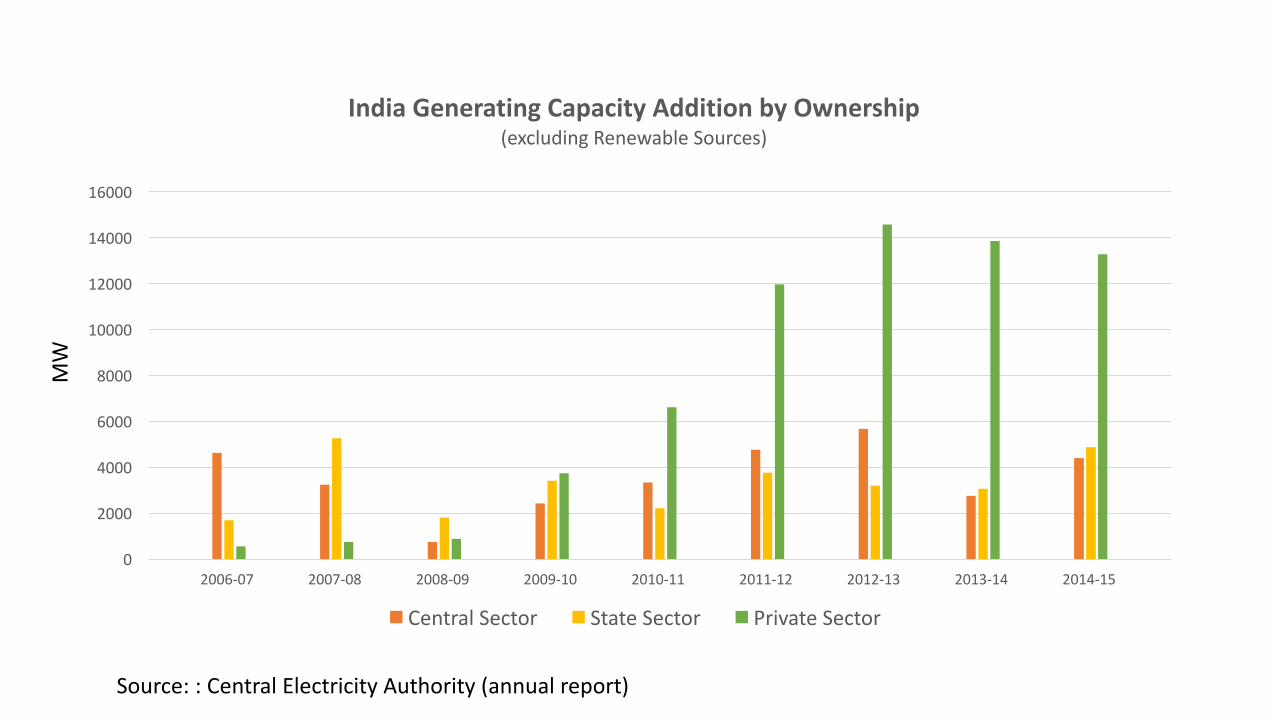

India Generating Capacity Addition by Ownership(excluding Renewable Sources)

CentralSector StateSector PrivateSector

Source::CentralElectricity Authority (annual report)

MW

India Installed Electricity Generation Capacity

27%

38%

35%

By Ownership(2015)

CentralSector PrivateSector StateSector

15%

70%

2%

13%

By Source(2015)

Hydro Thermal Nuclear RenewableEnergySources

India

• One of the key reasons forthe deteriorating finances of distribution entities is delay and non-payment of subsidiesby state governments.These subsidiesaremeant to be paid to theDiscoms to compensate forcheaper power supplies to certain segments promised by thestate governments,specially the farm sector.

• Electricity is aconcurrent subject under the purview of states;asaresult,oversight ofDiscoms is the domain of state governments.Nevertheless,key reforms undertaken overtheyears have largely been at the initiative of the CentralGovernment through policy guidanceaswell asproviding suitable environment forenabling regulations inconsultations with stategovernments.

• Avaiable datareport the existence of 853State Level Public Enterprises that accounted for7,1%of the GDPem2008.60%of the investments of these enterprises arefinanced by long-term loans,oririgating from public state-owned banks (Mishra;Kumari and Srinivas 2004)

• Thetotalcapitalemployed by commercial banks inthe power sectorhas progressivelyincreased overthe years despite the weak financialpositionof Discoms.Outstanding debt ofDiscoms has increased from about Rs.2.4lakh crore in2011-12to about `4.3lakh crore in2014-15,with interest ratesinthe rangeof 14-15percent.Asof September 2015,banks’exposure to Discoms was inthe rangeRs 1.6-1.8trillion,which comprise about 30percent ofbanks’exposure to the power sector(ICRA,2015).

0

50

100

150

200

250

300

350

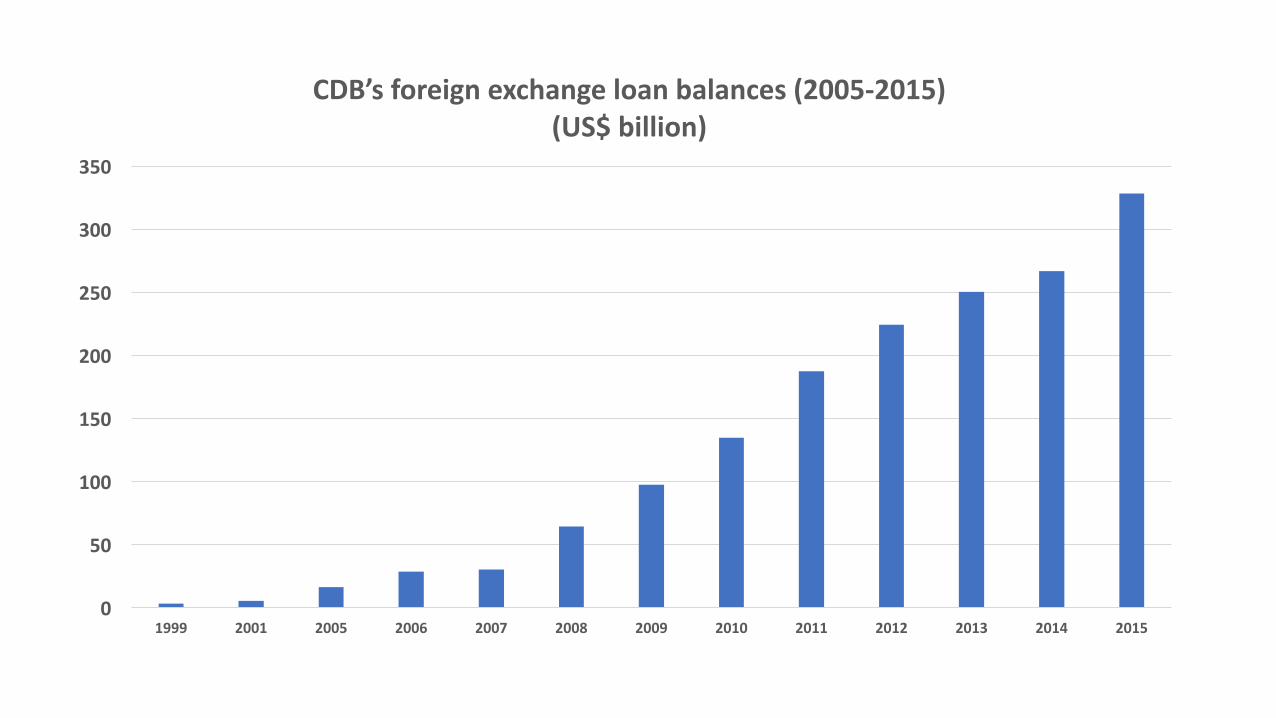

1999 2001 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CDB’s foreign exchange loan balances(2005-2015)(US$billion)

Chinese Enterprises among the 100largest globalCompaniesRANK COMPANY Ownership REVENUES($M)2 State Grid EnergySOE $315,1993 SinopecGroup EnergySOE $267,5184 ChinaNational Petroleum EnergySOE $262,57322 Industrial&Commercial Bankof China State Owned Bank $147,67524 ChinaState Construction Engineering StateOwnedBank $144,50528 ChinaConstructionBank State Owned Bank $135,09338 AgriculturalBankofChina State Owned Bank $117,27541 SAICMotor SOE $113,86142 BankofChina State Owned Bank $113,70847 ChinaMobileCommunications SOE $107,11751 ChinaLifeInsurance SOE $104,81855 ChinaRailwayEngineering SOE $96,97958 ChinaRailwayConstruction SOE $94,87783 HuaweiInvestment&Holding Employee-owned company $78,51186 ChinaResourcesNational SOE $75,77689 PacificConstructionGroup Private $74,629100 ChinaSouthernPowerGrid EnergySOE $71,242

Source:Fortune

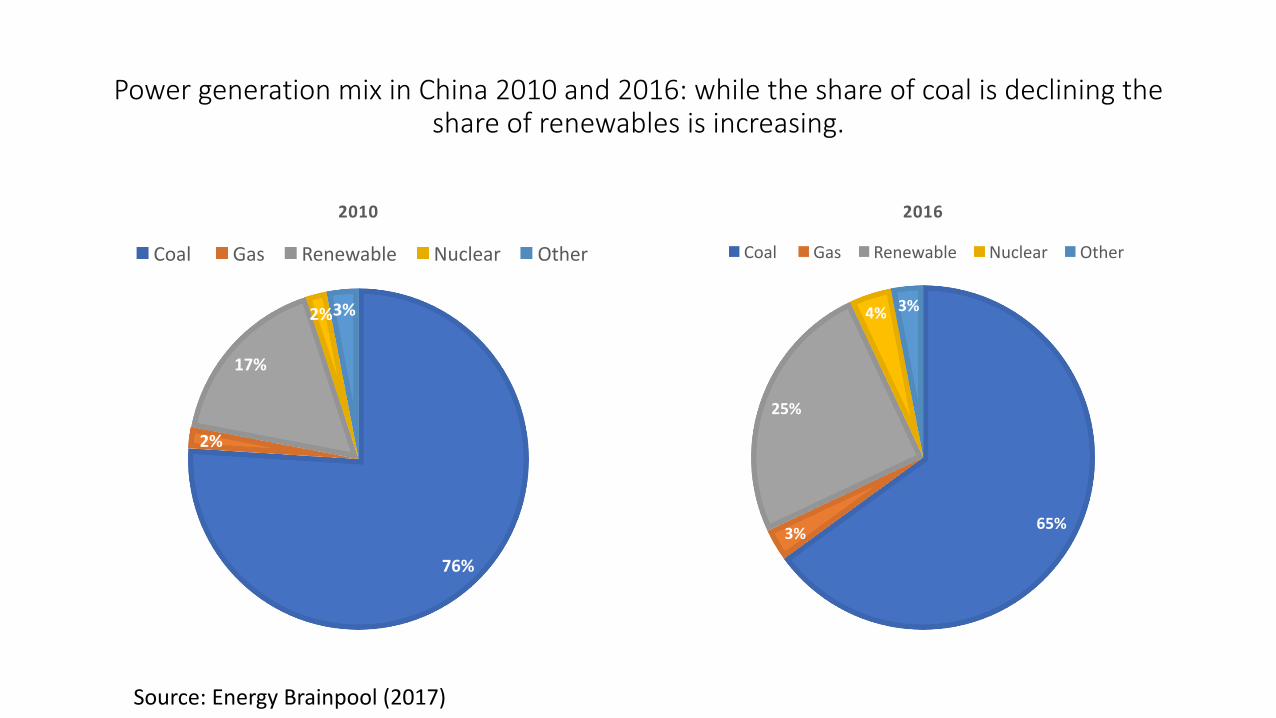

Powergeneration mix inChina2010and 2016:while the share of coal is declining theshare of renewables is increasing.

65%3%

25%

4% 3%

2016

Coal Gas Renewable Nuclear Other

76%

2%

17%

2%3%

2010

Coal Gas Renewable Nuclear Other

Source:EnergyBrainpool (2017)

China

• Between 1978and 2008,the number of SOEs fell by 33%and employees declined by 23,8%while totalassets grew by 59%;revenue and profit increased 35and 40fold,respectively during the same period.Chinese investments inenergy exceeded US$211billion between 2008and 2015,or 4.5timeswhatwas invested between 2000-07;

• Chinadismantled the State PowerCorporationon December 29,2002and setup 11newcompanies inamoveto end the corporation’s monopoly of the power industry.Theformer State PowerCorporationowned 46%of the country’s electricity generation assets and 90%of the electricity supply assets.

• Em2008,Chinaannounced astimulus package equivalent to 12.5%of that year’s GDPdue to financialcrisis.ChinesegovernmentdecidedthatitwouldbecoordinatedbythestatebankingsystembymeansofLocalGovernmentFinancingVehicles(LGFVs)Using funds obtained by the issuance of ling-termliabilities,the ChinaDevelopment bank (CDB)became the centraloperator of this financing.

• Thefinancialcenterof Chinese energy enterprises is policy banks,among which the CDBand Exportand Import Bankof China(Chexim)arethe most relevant.Chinese banks loans to energy companies forexternal investment (OFDI)totalled US$144billion between 2002and 2012,of which 88%camefromCDBand Chexim and the rest from commercial banks;

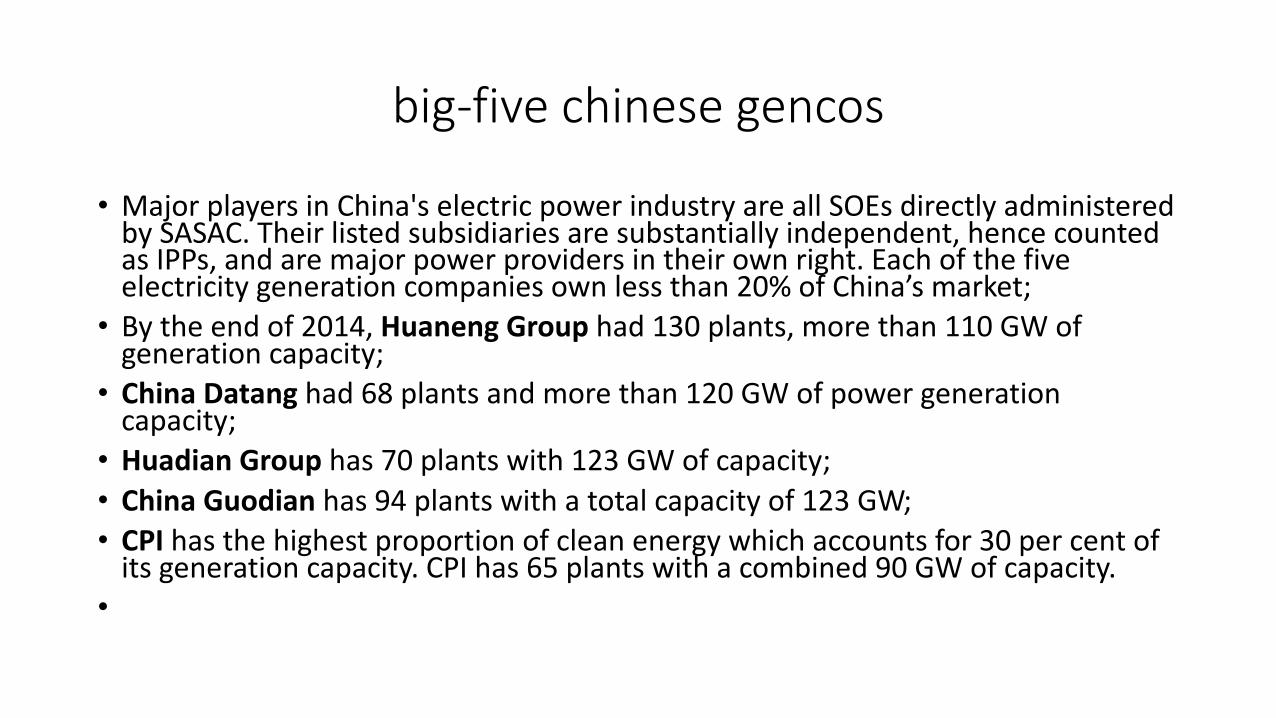

big-five chinese gencos

• MajorplayersinChina's electric power industry areall SOEs directly administeredby SASAC. Their listed subsidiaries aresubstantially independent,hence countedas IPPs,and aremajorpower providers intheir own right.Each of the fiveelectricity generation companies own less than 20%of China’s market;

• By the end of 2014,Huaneng Group had 130plants,morethan 110GWofgeneration capacity;

• ChinaDatang had 68plants and morethan 120GWof power generationcapacity;

• Huadian Group has 70plants with 123GWof capacity;• ChinaGuodian has 94plants with atotalcapacity of 123GW;• CPI has the highest proportion of cleanenergy which accounts for30percent ofitsgeneration capacity.CPIhas 65plants with acombined 90GWof capacity.

•

0

20

40

60

80

100

120

140

160

180

200

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

BNDESBrazilian Development Bank- Disbursement(Billions Reais)

Source:BNDES

Brazilian domestic supply of energy in2016

Oilandderivatives

65%

NaturalGas22%

MineralCoal10%

Nuclear2%

Othernon-renewable

1%

NON-RENEWABLE ENERGY(56,5PERCENT)

Sugarcanebiomass40%

Hydraulic29%

Firewoodandcharcoal18%

Otherrenewables

13%

RENEWABLE ENERGY(43,5PERCENT)

BNDESinvestment inelectricity generation(2007-2014)

Installedcapacity2007*(A)

Increaseininstalledcapacity2007e2014(B)

Variationininstalledcapacity(B/A)

CapacityaddedbyprojectssupportedbytheBNDES(C)

BNDESparticipation(C/B)

Hydroelectric 71.747 12.348 17% 12.348 100%

Thermoelectric 22.487 17.330 77% 6.811 39%

Wind 142 4.746 3339% 3.011 63%

Smallhydro 2.041 3.058 150% 1.892 62%

Totalgeneration 96.417 37.480 39% 24.061 64%

Ownership Structure inBrazilian electricity matrix - 2015

GenerationTransmission Lines

Distribution

Enterprise GW Percentage Enterprise KM(thousands) Percentage Enterprise Consumers

(millions) Percentage

Eletrobras 45,39 32,22 Eletrobras 68,09 52,66 Neoenergia 10,6 13,41Tractebel 7,3 5,18 CTEEP 18,47 14,28 Cemig 8,1 10,26Cemig 7,13 5,06 TAESA 7,5 5,8 AES 8,1 10,23CTG 6 4,26 CEMIG 7,5 5,8 CPFL 7,7 9,69Copel 5,6 3,98 CEEE 6,6 5,1 Energisa 6,4 8,11AES 3,3 2,34 StateGrid 5,7 4,41 ENELBrasil 6 7,58

CPFL(State Grid) 3,1 2,2 Energisa 4 3,09 Equatorial 4,6 5,79EDP 2,7 1,92 Copel 3,7 2,86 Copel 4,4 5,59DUKE 2,3 1,63 Neoenergia 0,6 0,46 Light 4,3 5,45

Neoenergia 1,61 1,14 - - - Eletrobras 4,1 5,13Subtotal 84,43 59,94 Subtotal 122,15 94,47 Subtotal 64,2 81,25Total 140,87 100 Total 129,3 100 Total 78,9 100

Source:MinistériodeMinaseEnergia,AbradeeeDemonstraçõesFinanceirasdasEmpresas

The10Largest Enterprises on Installed Capacity inBrazil(PowerPlants inOperation)2017

Enterprises PowerInstalled (MW)

CHESF(SOE) 10.609FURNAS(SOE) 9.411ELETRONORTE(SOE) 9.199

ChinaThree Gorges Corporation (Foreign Enterprise) 8.270

ENGIEBRASILENERGIAS.A.ENGIE(Foreign Enterprise) 7.251ITAIPU(SOE) 7.000PETROBRAS(SOE) 6.239CEMIG(Subnational SOE) 5.308

CopelGeraçãoeTransmissãoS.A. (Subnational SOE) 4.921NorteEnergiaS.A.(Mixed capital) 3.938

Source:ANEELupdated by newmergers and aquisitons took in2017

Brazil• Anewregulatorymodelwasadoptedin2004whichgavethecentralgovernmentaroleincoordinatingtheenergymarketagain.Lulaadministration(2003-2010)raisedgovernmentspendingbyanaveragerealvalueof3.2percentperyear,whileinvestmentbypublicadministrationandstateenterprisesgrewby14%and16,3%,respectively;

• Inlate2010,thegovernmentdecidedtostopthisgrowthtrend,promotingarigorousfiscaladjustmenttoattainaprimarysurplusof3.1%ofGDPin2011.Thegovernmentconsumptionfellby2.2%andpublicinvestments,inboththecentralgovernmentandstate-ownedenterprisesfellby17,9%and7.8%,respectively.Investmentofpublicadministrationdecreasedbyrealannualaveragevalueof1%between2011and2014whileinvestmentsinstateenterprisesgrewby2.7%duringthesameperiod;

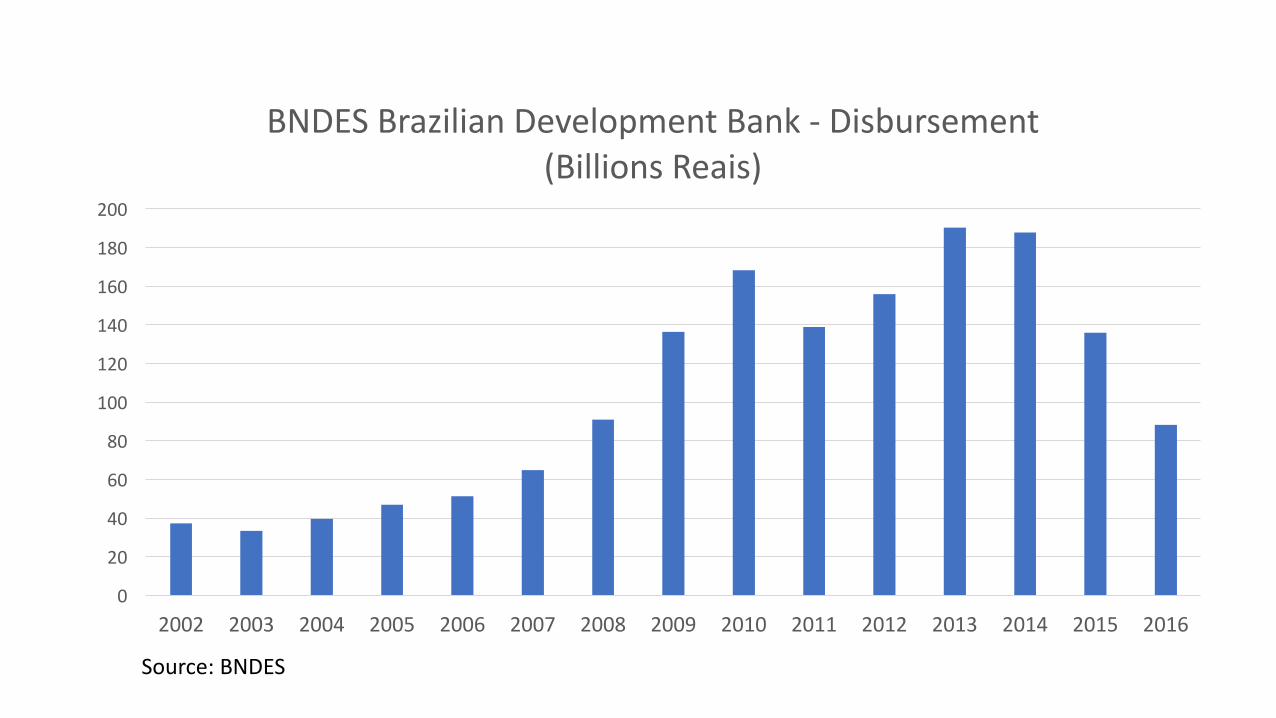

• TheNationalBankofDevelopment(BNDES)isamongthefivelargestbanksofthismodalityintheworldandwasthemaininstrumentofcountercyclicalfiscalpolicyinBrazilduringthecriticalperiodoftheglobalcreditcrisisof2007/08.TotalBNDESdisbursementsbetween2007and2014grewatanaveragerealrateof12%peryear,reachinganequivalentof3.7%oftheGDP.

• TheBNDESfinancedallninenewhydroelectricplantsthatwentonlineinBrazilbetween2007and2014usingamodelofprojectfinanceandcofinance withcommercialbanks,multilateralorgansandinfrastructuredebentures.Inotherrenewableenergyprojects(windandsmallhydro)theparticipationoftheBNDESwascloseto63%.Thebankwasalsoresponsiblefor39%ofnewthermoelectricenergyaddedtothegrid.

05000000

1000000015000000200000002500000030000000350000004000000045000000

Volumeof Loans Granted by 30Largest Russian Banksto Resident LegalEntities and IndividualEntrepreneurs,by Economic Activity and Useof Funds

(millions rubles)

2009 2010 2011 2012 2013 2014 2015 2016

Source:Author's elaboration based on datafrom Russia's CentralBank

Distribution of Russia state ownership byindustry,2006–2014(%)

percent inthe sample of114companies

the average totalsharesowned by the state

Nuclearpower 2,63 99,93Banking 6,14 30,46

Oilandgas 11,4 26,59Pipelinetransportation 0,88 100

Electricpower 21,93 38,21Infrastructure construction 1,75 47,06

Source:Abramova;Radygina;Chernova (2017)

Rosfnet39%

lukoil16%

Surgutneftegaz12%

Gazprom(including

GazpromNeft)10%

Tatneft5%

Slavneft3%

Bashneft3%

Russneft3%

PSAoperators3%

Novatek1%

Others5%

Russia's Oil Production by Company, 2014 Thousand b/d

Gazprom69%

Novatek10%

Rosneft9%

Lukoil3%

Surgutneftegaz1%

PSAoperators5%

Others3%

Russia's Natural Gas Production by Company, 2014Bcf/d

Two majorRussian SOEs

Share of Gazpromand Rosneft inthe GDP,revenues,and totalcapitalization,2006and 2014(%)

2006,shareof: 2014,shareof:

GDP revenues capitalization GDP revenues capitalization

Gazprom 7,1 2,7 28,1 6,9 2,2 13,3Rosneft 4,6 1,5 10,1 6,3 2,9 9Total 11,7 4,2 38,2 13,2 5,1 14,2

Source:Abramova;Radygina;Chernova (2017)

Russia

• Alongside the return of the Kremlin’s bureaucratic coordination and the institutional reformsadopted by Putin’s government,itis also important to highlight the roleof Russian state-owned banks asan instrument of financialleverage and energy policy consolidation;

• Russian bankingsystemis highly concentrated and subject to interventions from the RussianCentralBank.Russian state-owned banks control 60.4%of all family savings deposits(Vernikov 2015)

• While inthe 1990there were seventy-one Energos,each tied to aregionalgovernment,by2008ahandful vertically structured conglomerates owned most electricity generation assets;

• the activation and acquired regulatory functions fornewly created vertically integratedorganizations inanumber of industries,state corporations and other developmentinstitutions;

• the transfer of non-public state-owned company property into capital,“pseudo-privatization”processes;and the expansion of spheres (control areas)of government regulation ratherthan asimple increase inthe shareholdings owned by the state inthe capitalof majorpubliccompanies (Abramova;Radygina;Chernova 2017).

Electricity industry structures and forms of ownership,regulationand competition

China Russia Brazil IndiaIndustry model Corporatised Corporatised Corporatised CorporatisedOwnership ofgeneration State Mixed private and

governmentMixed private and

governmentMixed private and

governmentOwnership oftransmission State State Federaland state Federalgovt

Ownership ofdistribution State State Mixed Mixed

Keylegislation State and federal Federal Federal State and federal

Form of regulation Priceregulation Priceregulation Competitive marketoversight Price regulation

Regulator/s NDRC,State ElectricityRegulatory Commission

Ministry of Energy,FederalTariff Service,

FAS

MME,ANEEL,CNPEand CMSE MoP,CERC

Extent of competitionCompetition to buildnewpower plants,but

not fordispatchNone

Limited:periodicauctions held fornewgeneration capacity

Nocompetitive market.Capacity shortages and

substantial self-generation

Source:Wilson,Yangand Kuang (2015)

Centrifugal tendenciesState-owned BanksandEnterprises

BureaucraticCapacities FederalismDilemmas

Brasil(1982-2000)

Privatizations on electricityretailers and corporativization ofoil SOEand Eletrobras

dismantlement of bureaucraticpersonal due the low ratesof publicinvestments and privatizations

Fiscaldecentralization due torevenue transfers to subnationalspheres by 1988Constitution andnon-cooperative model ofintergovernmental relations

Russia (1990-2000)

Privatization of oil sectoranddecentralization of electricityretailers

Thecollapse of centralbureacraticauthority upon electricity systemandoil sector

Therise of subnational sovereiginityoverenergy policiesand collapsetributary capacity of centralgovernment

China(1978-2002)

Decentralization of electricityretailers (coal producers)andCorporativization oil state-ownedenterprises

Former energy ministries hasbecome corporations and suppressedthe iron ricebowl system.Overlapping of regulatory bodies onenergy policies

Fiscaldescentralization

Índia(1991-2003) State Divestment andCorporativization

Long-term coordination problems byCentralgovernment and electricityretailers under subnational control

Conservation of extensiveprerogatives from regionalpowerupon State Electricity Boards

Centripetal tendenciesState-ownedBanksandEnterprises BureaucraticCapacities FederalismDilemmas

Brasil(2004-2016)

Centralgovernment recoveredcoordinating roleinenergymarket in2004and StateOwned Banksresumed itsanti-cyclical role

Recouvering ofstatebureaucraticpersonel

Fiscalcentralizationduetoinflationstabilizationplanwhichraisedcentralgovernmenttaxextration tothedetrimentofsubnationalspheres

Russia (2001-2016)

Verticalization andcorporateconcentrationofoilandelectricityindustrialchain

Recovering ofcommanding chain bycentralbureaucracy

Thedemiseofsubnationalsovereiginity overenergypoliciesandtaxreformswhichenabledcentraladministrationtocapturethelargeramountofenergyrevenuesurplus

China(2003-2016)

Therise national championpolicy under SASACcoordination

Promulgation of the fullCivilServants Lawin2005to replace the TemporaryRegulations.

Recoveryof centralgovernment tributaryand fiscalcapacities and exponential creditpoliciesby State-Owned Banksasmainstayof energy investment

Índia(2003-2016)

Enactment of Electricity Act2003

Centralgovernment has attempted to usefinancialleverage from Public SectorComercialBanksto share the burden ofsubsidieswith regionalgovernments –without asuccess

Related Documents