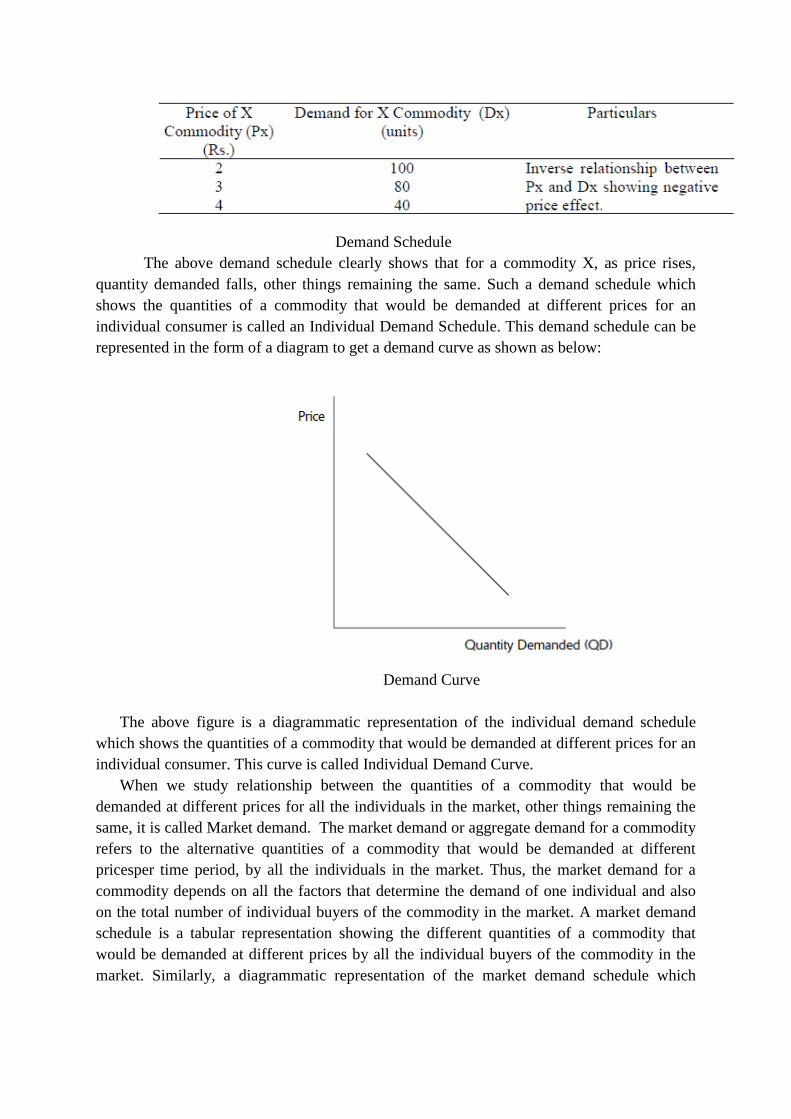

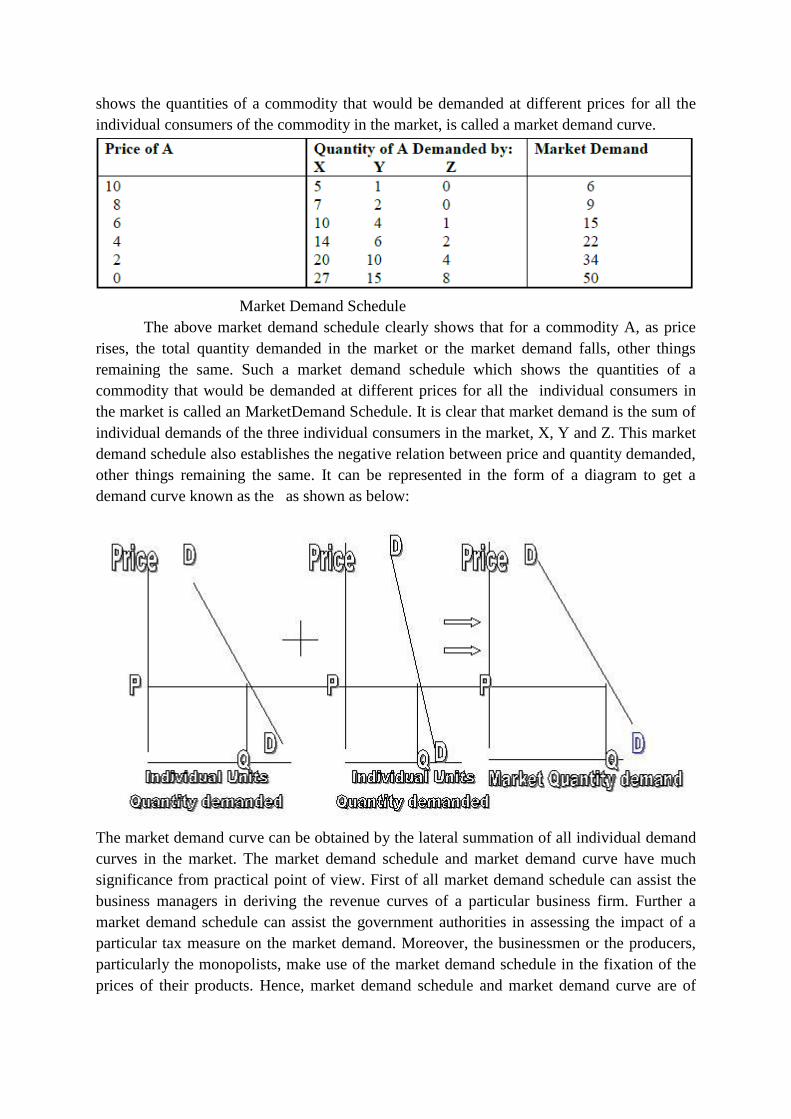

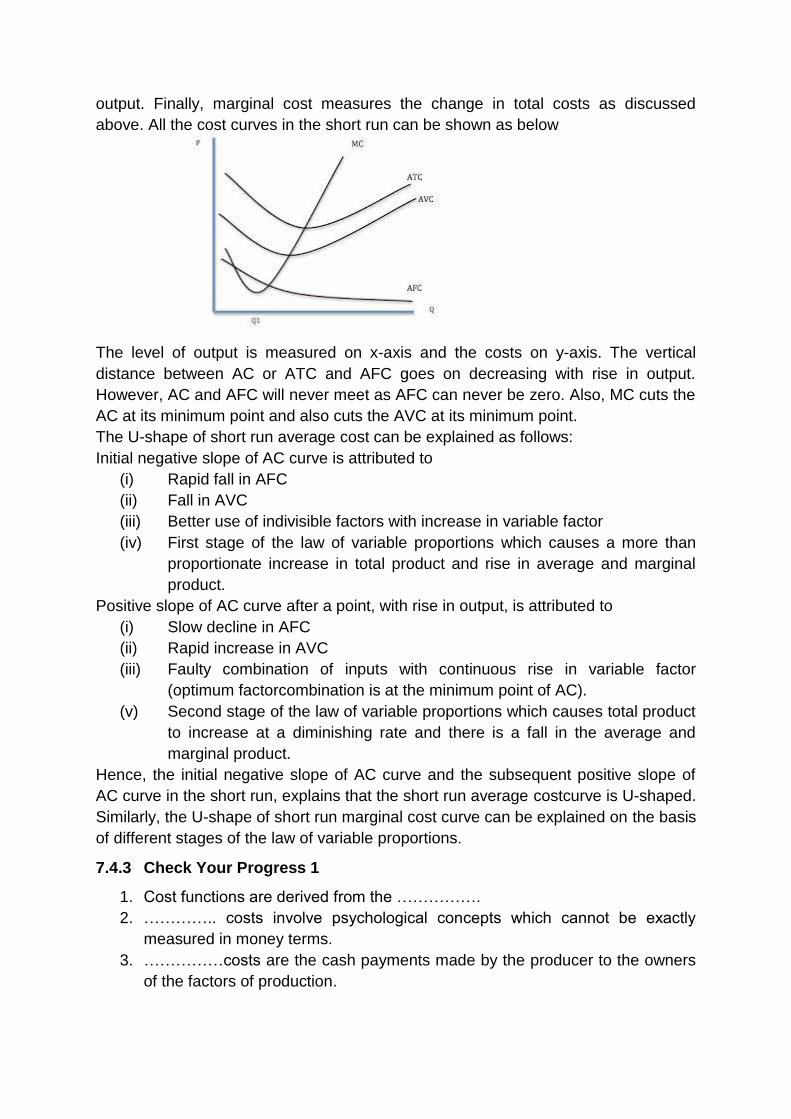

Self Learning Material Managerial Economics (MCOP-201) Course: Masters of Commerce Semester-II Distance Education Programme I.K. Gujral Punjab Technical University Jalandhar

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Self Learning Material

Managerial Economics (MCOP-201)

Course: Masters of Commerce

Semester-II

Distance Education Programme

I.K. Gujral Punjab Technical University

Jalandhar

Syllabus

I.K. Gujral Punjab Technical University

MCOP-201 MANAGERIAL ECONOMICS

OBJECTIVE AND EXPECTED OUTCOME OF THE COURSE:

Aims to provide a broader understanding of Managerial Economics and its managerial

applications.

UNIT-I Introduction: Nature and scope of Managerial Economics, Role and Responsibility of Managerial economics in business. Fundamental business concepts – Incremental concept,

Opportunity cost concept, Time perspective, Discounting principle.

UNIT-II Demand analysis and Forecasting for consumer goods and capital goods - use of business indicators - type of elasticity. Demand Forecasting for new products. Test marketing, Opinion

pooling, Life cycle.

UNIT-III Concept and resources allocation - Cost Analysis - Short run and long run Cost functions - production functions - cost price - Output relations.Economics of size and capacity

Utilization - Input - Output analysis - Market Structure - Pricing and output general

equilibrium.

UNIT-IV Pricing Objectives - pricing methods and approaches - price discrimination, Product line pricing and Cost control. Theories of profit, Tools of profit planning. Business Cycles:

Meaning, Causes, Phases, Theories of Business cycles

SUGGESTED READINGS/ BOOKS:

1. Peterson, managerial economics, 4th edition - Pearson education - New Delhi.

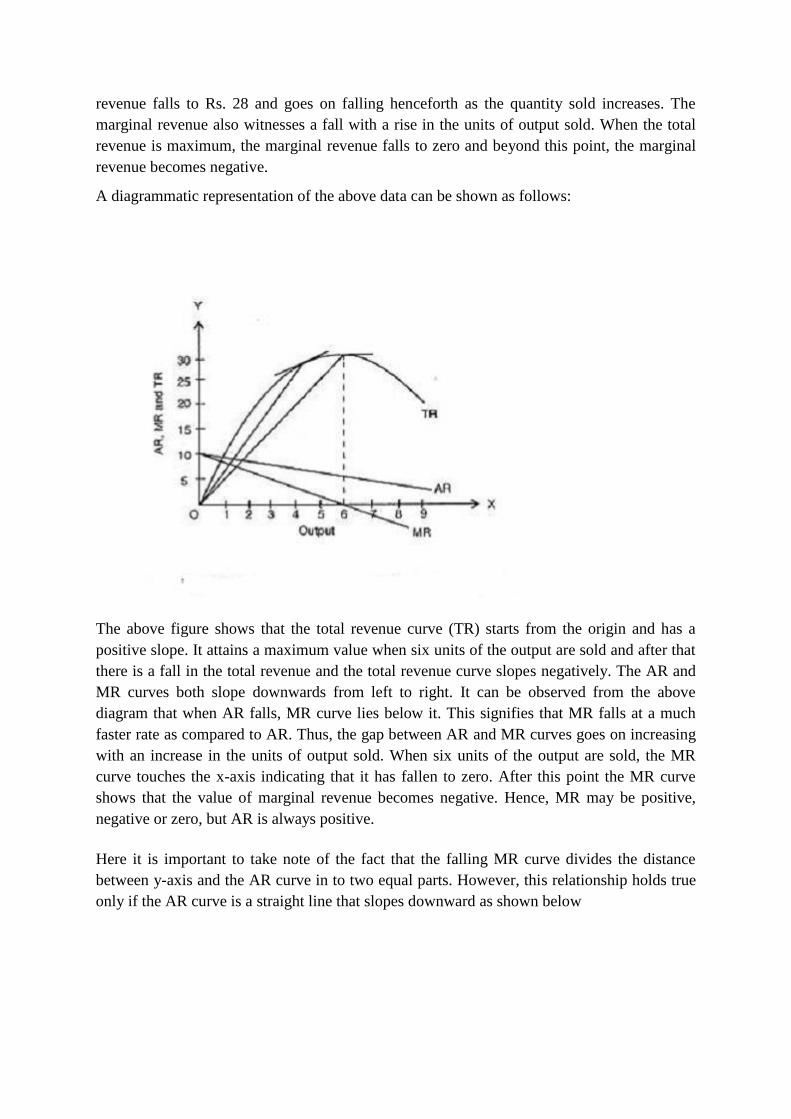

2. Sampat Mokherjie, Business and Managerial Economics, New Central Book Agency,

Calcutta.

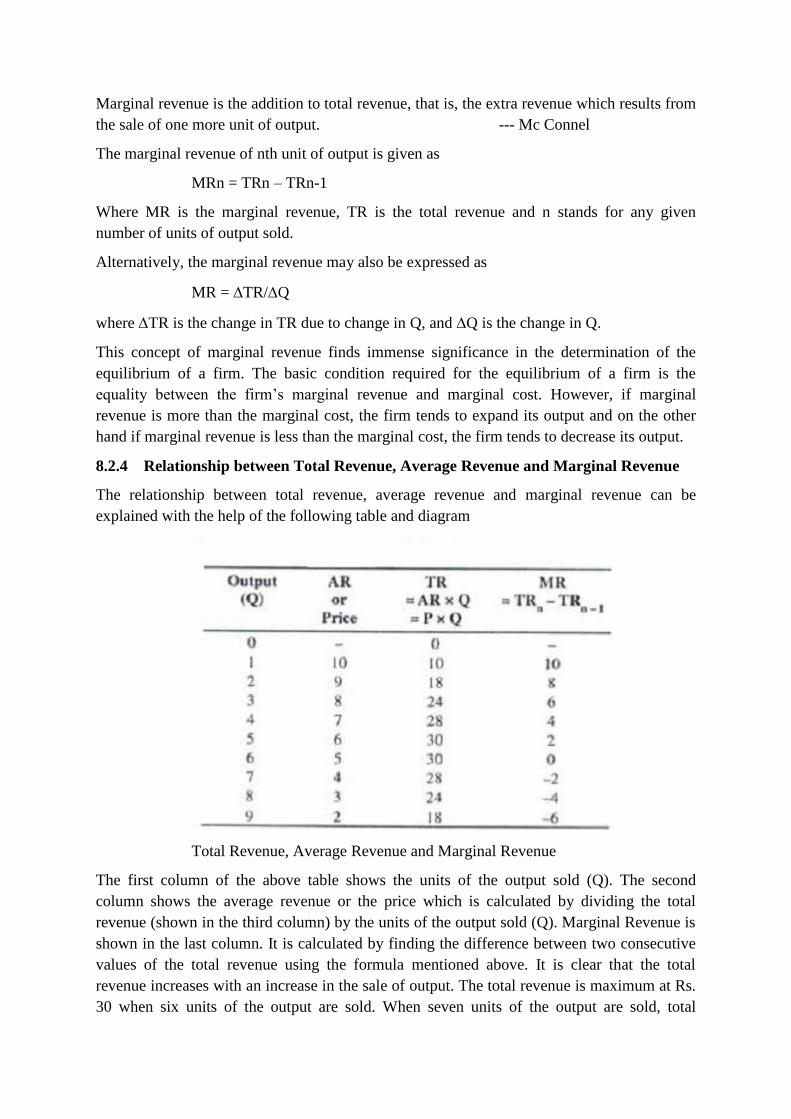

3. Spencer M.H.Managerial Economics Text, Problems and short cases, Richard D.Inwin

INC.

4. Sankaran.S, Managerial Economics Margham Publications, Chennai.

5. Dwivedi D.N , Managerial Economics, Vikas-New Delhi

6. Mankar & Denkar, Business Economics, Himalaya publishing House, Bombay

7. Joel Dean, Managerial Economics, Prentice Hall of India - New Delhi.

8. R.L. Varshney & K.L. Maheshwari, Managerial Economics-Sultan Chand & Sons, New

Delhi.

Table of Contents

Lesson No. Title Page No.

1 Managerial Economics: Meaning, Nature and Scope

1

2 Utility Analysis

17

3 Demand Analysis

39

4 Elasticity of Demand

58

5 Demand Forecasting

80

6 Theory of Production

96

7 Theory of Costs

117

8 Revenue and Revenue Curves

140

9 Market Structure and Pricing

158

10 Pricing Methods and Approaches

177

11 Profit

196

12 Business Cycles

207

Written by:

Ms.Deepali,

KMV College, Jalandhar

Reviwed by:

Dr.Mandeep Kaur,

IKGPTU, Jalandhar

© IK Gujral Punjab Technical University Jalandhar

All rights reserved with IK Gujral Punjab Technical University Jalandhar

LESSON – 1

Managerial Economics: Meaning, Nature and Scope

Structure

1.0 Objectives

1.1 Introduction

1.2 Definitions of Managerial Economics

1.3 Nature of Managerial Economics

1.4 Scope of Managerial Economics

1.5 Relationship of Managerial Economics with Other Disciplines

1.6 Role of Managerial Economics in Business Decision-Making

1.7 Summary

1.8 Glossary

1.9 Answer to Check Your Progress

1.10 References

1.11 Suggested Readings

1.12 Terminal and Model Questions

1.0 OBJECTIVES

After reading this lesson, you should be able:

To understand the basic theme of managerial economics.

To bring out the nature and scope of management.

To explain the role of managerial economics in decision-making.

1.1 INTRODUCTION

Business decision making has witnessed an increasing use of economic

concepts, theories and principles, which in turn has led to the development of

managerial economics or business economics as a separate branch of economics.

Managerial economics is an outcome of the close relationship between economics

and management. Management in business firms involves appropriate decision-

making which requires weighing different available alternatives and making the best

possible choice. This involves co-ordination among a group of individuals to help

them perform in an efficient and effective manner in order to attain common

objectives. On the other hand, economics involves the analysis of and solution to the

basic problem i.e. problem of choice. The universal problem of choice stems from

scarcity of resources available to satisfy unlimited human wants. This necessitates a

rational choice both at the individual level (individual as a producer and as a

consumer) as well as at the level of economy as a whole. Thus, economics helps to

study optimal allocation of scarce available resources to maximize gains both at the

micro level (individual) and the macro level (aggregate economy).

Such economic decision-making by firms and managers constitutes the core

of managerial economics. This appropriate decision making has become an

extremely complex task in the light of market imperfections, risk and uncertainties.

Managerial economics or business economics, thus, comes as a useful tool for the

business managers in the process of decision-making for the firms. Hence,

managerial economics is also sometimes referred to as „Economics for Managers‟.

Managerial economics makes use of both of the two very basic branches of

economics- microeconomics as well as macroeconomics. Managerial economics

may be considered as applied microeconomics to a large extent as it relies on the

tools and techniques provided by microeconomic theory to ease managerial

decision-making. However, it draws heavily from macroeconomic theory also as the

macroeconomic environment cannot be ignored in the rational decision-making

process for a firm. However, economic principles in general, make a significant

contribution in improving the performance of business managers. Managers with

some working knowledge of economics can perform their functions more effectively

and efficiently than those without such knowledge. Managerial economics, thus,

enables the managers to find the most efficient way to allocate scarce organizational

resources in order to achieve the given objectives of the firm.

1.2 Definitions of managerial economics

The meaning of managerial economics can be still better understood with the

help of its definition. A large number of eminent economists have defined managerial

economics in different ways. A few important ones are listed below:

“Managerial economics is concerned with the application of economic principles and

methodology to the decision-making process within the firm or organization. It seeks

to establish rules and principles to facilitate the attainment of the desired economic

goals.” -Douglas

“Managerial economics refers to the application of economic theory and the tools of

analysis of decision science to examine how an organization can achieve its

objectives most effectively.” -Salvatore

“Managerial economics applies economic theory and methods to business and

administrative decision-making.” -Pappas and Hirschey

“Managerial economics is concerned with the application of economic concepts and

economics to the problems of formulating rational decision-making.” -Mansfield

“Managerial economics is the study of allocation of limited resources available to a

firm or other unit of management among the various possible activities of that unit.”

-Henry and Haynes

Different definitions of managerial economics make it clear that managerial

economics is the application of economic theories, logic, concepts and tools of

economic analysis to the process of business decision-making in order to help the

business managers in taking best possible decisions. Although no single definition

can claim to be a perfect one, still a study of these different definitions of managerial

economics throw light on its basic nature and meaning.

1.3 Nature of Managerial Economics

The performance of business managers – their duties and responsibilities

relies heavily on a working knowledge of economics. The primary function of the

managers of a business firm is maximization of the given objective subject to the

constraint of limited availability of resources. It is quite obvious that there would not

have been any problem of decision making had there been an unlimited supply of

resources. As we are confronted with scarcity of resources- both natural and man-

made, so the problem of choice is the central problem of any economy or even of the

firm. The typical problems faced by managers in one way or the other can be

categorized as follows:

What to produce?

How to produce?

For whom to produce?

The first major economic decision to be taken for an economy is what to

produce? A choice has to be made between different alternative combinations of

goods and services that can be produced because the resources are limited. Such a

decision at firm level necessitates a review of market demand and the availability of

raw materials and technology. Hence, it leads to the problem of choice.

After this decision is made, the next question confronting the economy is how

to produce, as to what techniques of production should be used which would

maximize production or social benefit. This, again, leads to the problem of choice.

The next basic problem which any economy will face relates to the problem

of distribution of the total national output among the different economic agents.

There again lies a problem of choice as to which principle should be followed in

distribution.

If it were possible to specify the uses to which resources could be put,

perhaps the decision-making process in a situation with resource constraints could

be relatively easy. For instance if you have Rs. 1000 and you are told that out of Rs.

1000, you should spend Rs. 500 on books, Rs. 200 on moves and the remaining on

food, the decision-making would have not been very complicated. However, in

practical reality, resources have alternative uses, Rs. 1000 could be used in

innumerable different ways. Hence, the decision making process becomes complex.

It is here that economic logic, tools and techniques come to the rescue. Hence,

optimization of use of scarce resources is the primary task of managers. Economics

helps the managers in this task of decision-making by providing models, tools and

techniques to achieve the goals of organizations; to reduce the degree of uncertainty

and risk arising due to uncertain market forces, dynamic business environment,

government policy, competitors, impact of international factors, social and political

factors and many others; and to predict future market conditions and business

prospects. Economic theories have, therefore, gained widespread application in

practical problems of business.

Thus, allocation of scarce resources among alternative uses to achieve the

desired objectives is the primary duty of a manager, which is done with the help of

economic tools, techniques and logic. This link between the responsibility of the

managers and economic logic, tools and techniques justifies the name managerial

economics. Highlighting the importance of managerial economics as a separate

discipline, different and distinct from economics in general, Prof. D .M .Mithani has

stated the following characteristics of managerial economics:

Managerial economics involves the application of the working knowledge

of economic theory, especially microeconomics, to solve practical

business problems.

Managerial economics is both a science as well as an art which facilitates

better and rational business decision making. As a science it is both a

positive science (it is a systematic knowledge and answers the question

„what is?‟) as well as a normative science (it involves value judgement

answers the question „what ought to be?‟)

Managerial economics is primarily concerned with optimum allocation of

scarce resources available to a firm which have alternative uses for any

business activity.

These features of managerial economics clearly throw light on its meaning and

nature and form a basis to study the scope of managerial economics or as it is

synonymously called business economics.

Activity A

Managerial economics is the discipline which deals with the application of ‘economic

theory to business management’. Comment.

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------------------

---

1.4 Scope of Managerial Economics

Managerial economics is the study of allocation of scarce resources available

to a firm (financial, human, machines, etc.) among alternative uses in order to realize

the objective of profit maximization or other specified objectives. Managerial

economics comprises of both microeconomic theories and macroeconomic theories

as both of these are applied to business decision-making and analysis in one way or

the other. The scope of managerial economics comprises all the areas of business

issues to which economic theories could be applied in one way or the other. The

important among these can be enlisted as follows.

Allocation of resources: As it has already been discussed earlier in the

context of problem of choice, a business manager has to decide how to

allocate the scarce available resources to their respective uses within the firm

in order to achieve the desired objectives.

Management of Inventory: Inventory problems relate to the issue of holding

an optimum stock of both finished goods and raw materials. Along with it

queuing problems also arise in which decisions have to be taken about

installing new machines or employing extra labour so as to balance the

business requirements.

Pricing and sales promotion: How to fix the prices for the products, how

to face price competition and how to promote sales are important business

decisions to be undertaken with regard to the pricing policy of the firm.

Investment Issues: Decisions regarding investment problems are

crucial to a firm- how to decide on investing in new plants, how much to

invest, how to manage capital and profits, etc.

The above mentioned problems appear in decision-making and forward

planning in any business firm. Micro economics as a part of managerial economics

deals with such operational or internal issues faced by managers of business firms.

The study of the following important microeconomic theories in this context is crucial

in order to make rational business decisions:

Demand Analysis: The theory of demand helps in making the choice of

products, determining their price and optimum level of production.

Product Analysis and cost analysis: The theory of production and

production decisions is very helpful in determining the size of the firm, its total

output & factors of production to be employed in order to attain the given

objectives of the firm.

Pricing Theory and policies: Analysis of market structure and pricing

theory helps in price determination under different market conditions. It also

aids in evaluating the possibility and feasibility of price discrimination and

advertisement for expansion of sales of a given commodity.

Profit Analysis: The theory of profit helps the firms to measure and

manage their profits keeping in view the uncertainties and the risk involved.

Capital Budgeting: The theory of capital and investment decisions helps in

making investment decisions, choice of projects, capital budgeting for

investment decisions, etc for the business firm.

Besides the above mentioned issues, the scope of managerial economics

also includes the general business environment. This general business environment

of the economy relates to the economic, social and political set-up of the country.

These environmental factors include the type of economic system in the country-

socialist, capitalistic or mixed economy; general trends in national income,

employment, output, prices saving and investment etc.; trends in the working of the

financial institutions of the economy; the trends in foreign trade; the extent of

globalization of the economy; political factors, etc. These types of external issues

strongly influence the business and the functioning of the firms. Therefore, business

managers have to give due consideration to these external environmental factors

also in the process of decision making. These external environmental factors may

be broadly classified as follow:

Major Macroeconomic Parameters: Issues concerning the trends in

macroeconomic variables like national income, output, employment, prices,

investment etc. are extremely helpful in forward planning like setting up a new

plant or expanding the existing plant size for business expansion. The study

of these macro economic variables help the firms to make crucial decisions

regarding business expansion keeping in mind the external conditions

prevalent in the eonomy.

Foreign trade: Trade - internal and/or external is an important outcome

all business activity undertaken by the firms. Trade links with the rest of the

world influence the functioning of business firms directly or indirectly. Study of

monetary mechanism and international trade help the managers understand

international trade, prices, exchange rates, fluctuations in the foreign markets,

capital flows, etc.

Government policies: Regulatory government policies have a huge impact

on the working of business undertakings. Government tries to regulate and

control all types of business activities through its policy measures. Any

business activity which goes against the social well being or disturbs the

welfare of the society have to be and are checked by the government through

regulatory policies directed towards the concerned business activities. For

instance government policies to check environment pollution, traffic

congestion in cities etc. affect the concerned firms. Hence, the business

managers need to have complete information about government policies and

their repercussions on business. Their business decisions should be carefully

framed with an effort to not to violate any such government rules and

regulations. In this context the business managers also need to be aware and

sensitive towards the needs of the society so that no business action of theirs

reduces the welfare of the society as a whole or a section of the society.

Besides the above mentioned economic theories, the scope of managerial

economics may include any other issues influencing the working of managers in

business firms. However, these theories largely constitute the scope of

managerial economics with room for further additions.

Check Your Progress 1

1. State whether the following statements are True or False:

(i) Managerial economics is the application of economic tools to business.

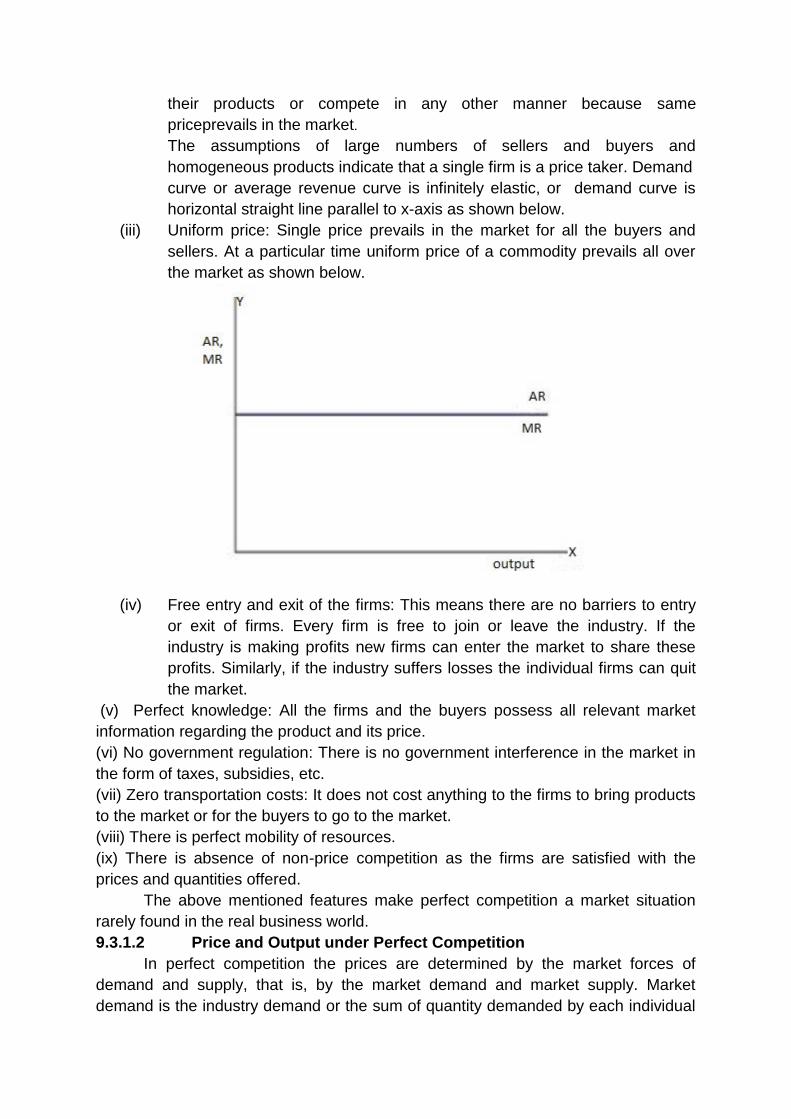

(ii) Managerial economics is the study of micro economics only.

(iii) The basic problem of an economy is the problem of choice.

(iv) Managerial economics helps the managers to make efficient use of

scarceresources.

(v) The scope of managerial economics does not include the pricing policy.

1.5 Relationship of Managerial Economics with other disciplines

Essentially managerial economics involves the study of economic tools, logic

and analysis applied to the decision making process of business firms. However,

besides microeconomics and macroeconomics, managerial economics is also

associated with various other disciplines. These related fields of study include the

following:

Operations research: This field of study is an inter disciplinary solution

finding technique used to find an optimum solution to the managerial

problems subject to the given constraints. These problems are solved using

models built with the help of economics, mathematics and statistics. Linear

programming and goal programming are two important techniques studied

under operations research which are useful in business decision making.

Mathematical and Statistical Tools: Mathematical logic and tools are very

helpful in economic analysis as most of the concepts dealt by the managers of

business firms are quantitative in nature like cost, price, demand, profit,

interest, wages, stock etc. Advanced optimization techniques and

mathematical tools, thus, form an integral part of managerial economics.

Similarly statistical tools prove extremely helpful in collecting,

processing and analyzing data for business firms. Regression analysis

probability theory, forecasting techniques, etc. help in forecasting the future

values of economic variables and the probable outcome of the business

decisions undertaken.

Management Theory and Accounting: These disciplines have a close link

with the study of managerial economics. Various management theories make

an attempt to study the behaviour of the business firms which in turn are

working to attain certain desired and pre stated objectives. Hence, a business

manager needs to have sufficient knowledge of management theory in order

to ascertain changes in the behaviour and objectives of the firms with change

in the conditions- internal and/or external. On the other hand accounting data

and statements help in reflecting the working the firm and evaluating its

performance.

Psychology and Organisation Behaviour: Managerial economics helps the

business managers to make rational business decisions by studying the

behaviour of individual buyers and sellers. This involves the study of the

psychological factors influencing the demand and supply patterns, needs,

expectations and aspirations of the market players- the buyers and sellers. In

fact, psychological economics has emerged as recent field of study for the

psychological analysis of the buying behaviour of the consumer. In addition to

the study of individual buyers, various behavioural models studying

organizational psychology have been developed of late to analyse the

economic behaviour of a firm.

Thus, the scope of managerial economics is immensely wide and beyond the

reach of this entire book. However, the above mentioned issues form the basic core

of managerial economics and its scope cannot be complete without the mention of

these issues.

1.6 Role of Managerial Economics in Business Decision-Making

The role of business managers in business decision making is to select

the best possible alternative out of the opportunities available to the business firm.

The process of business decision making primarily comprises of the following

stages:

Stage I : To determine and define the objective(s) to be achieved.

Stage II : To collect and analyse data and information regarding economic,

social, political, and technological environment.

Stage III : To invent, develop and analyse the possible alternatives to achieve

the desired objectives.

Stage IV : To rationally select the best possible alternative.

It is essential to take a note of the fact that stages II and III are very crucial in

order to make the right business decision and involve a need for in depth knowledge

of economic theories and tools, concepts and logic along with individual skills of the

business managers. For example, say a firm plans to launch a new product in the

market and many close substitutes of that product are already available in the

market. The foremost business decision to be taken would whether to launch the

product or not. In order to do so the business manager will have to carefully study

the market; the product and all issues relating to it; and issues relating to the sales.

Here comes the role of the different economic concepts, including demand, supply,

cost, price, etc., that can be and are used by the business managers in business

analysis. Various economic theories, tools, concepts and logic help in arriving at

appropriate and right conclusions as regards the business problem.

The primary responsibility of the manager of a business firm is the attainment

of the desired objectives. A managerial decision can be evaluated only in the context

of its objective. For this the objectives of the firm should be clearly stated which may

be various and conflicting. The conventional theory of firm takes profit maximization

as the primary objective of a business firm. This is defended on the basis of the

argument that making profit is indispensable for the survival of the firm in the long

run. Further, the achievement of alternative objectives of the firm like maximizing

long run growth, maximizing sales revenue, increasing market share and such like

are themselves dependent more or less on the profit objective, as profit is a relatively

more reliable measure of a firm‟s efficiency. Moreover, profit maximization

hypothesis is a time- tested one and is largely used to explain the price and output

decisions of the business firms.

However, whatever may be the objective of a firm, all the business decisions

taken by the managers aim at the attainment of pre determined objective(s).

Traditionally the process of business decision making relied on the rule of thumb

technique. Such a technique evolved out of traditional business practices, serves the

purpose where simple business decisions are involved. However, complex issues in

business decision-making involve the use of some basic economic concepts. A few

important economic concepts and their role in business decision-making are listed

below.:

1.6.1 Principle of opportunity cost

The business manager or as we may call the managerial economist needs to

sacrifice some alternatives against the selected ones in a rational manner in almost

all aspects of business -- the problem of choice. Since human wants are infinite and

means to satisfy them are scarce, it is impossible to satisfy all the wants. In order to

satisfy some wants, it becomes necessary to give up or postpone some other wants.

Similarly resources – natural and man-made are scarce in relation to their demand

but have alternative uses. This scarcity and possible alternative uses of the

resources leads to the concept of opportunity cost.

The opportunity cost or alternative cost is what has been sacrificed to have a

certain thing. It is the benefit foregone of the alternative that has not been chosen.

For example say a worker works in an ice factory and gets a wage of Rs. 4000 per

month. Alternatively if he gets employment in a shoe factory, he might be getting a

wage of Rs. 3000 per month. So the earning in the next best alternative (Rs. 3000) is

the opportunity cost or alternative cost of his services. Similarly a firm has limited

resources at its disposal which can be put to alternative uses. For example a firm

may have different options available to expand its output using a capital of say Rs.

10 million- setting up a new unit having expected annual return of Rs. 2.5 million or

expanding the existing unit having expected annual return of 1.8 million. A rational

business manager would definitely go in for the first alternative other things

remaining the same. This means that the manager will have to sacrifice Rs. 1.8

million- the annual return of second option which is not selected, in order to get an

annual return of Rs. 2.5 million (the selected alternative). Hence, the opportunity cost

of setting up a new unit in this example is the sacrifice involved is not expanding the

existing unit.

Thus, the opportunity cost is the cost of the next best alternative which is

foregone. This concept of alternative or opportunity cost is applicable to all types of

resources involved in business decision where alternative uses are possible.

1.6.2 Marginal Principle and Incremental concept

Marginal analysis is widely used in economic theory -marginal utility in utility

analysis; marginal cost in theory of production and marginal revenue in the theory of

pricing. As regards business decision making, marginal principle is applicable in the

cases where marginal revenue(MR) and marginal cost (MC) can be exactly

computed. According to marginal analysis, marginal cost is the change in total cost

(TC) due to a unit change in total output.

Or

Marginal cost of nth unit is the total cost of n units minus total of cost of n-1 units.

MCn = TCn –TC n-1

where n is the number of units of output.

MCChange in Total Cost

Change in Total Output

Similarly Marginal Revenue (MR) is the change in total revenue due to a unit change

in total output.

Change in Total RevenueMR=

Change in Total Output

Or

Marginal revenue of nth unit is the total revenue of n units minus total of revenue of

n-1 units.

Mrn = TRn – TRn-1

where n is the number of units of output.

The decision rule under the marginal principle for a profit maximizing firm is given as

MC = MR

In other words for a business firm the profit will be maximum when marginal

cost equals marginal revenue, that is the cost of producing an additional unit

becomes equal to the revenue earned by selling that additional unit.

However, a major drawback of this approach is that it is applicable only when

exact calculation of marginal cost and marginal revenue is possible and variable cost

can be subjected to a unit change. A relatively convenient concept which can instead

be used is the incremental principle. The incremental concept is of great use when

bulk production is involved and total cost and total revenue witness large changes.

The increase in revenue due to a given business decision would be called

incremental revenue. On the other hand similar increase in cost (due to say

expansion in the size of the firm) is called incremental cost. The business decision

rule in this context is that the given business decision taken to correct if it leads to a

higher incremental revenue as compared to incremental cost. If it is otherwise the

given business proposition is not accepted. Although marginal analysis is more

precise yet incremental concept finds more practical applicability.

1.6.3 Time perspective

The time element needs to be given due importance in the process of

business decision making. Every single business decision needs be undertaken with

a given time perspective. This means business managers should make decisions by

taking into account the time angle of business propositions well in advance. Relevant

past and foreseeable future have to be given due consideration while taking a

business decision. The time difference or duration between relevant past and

foreseeable future refers to the time perspective. Relevant past indicates the time

period of past experience and trends which are important for any business decision

in the present. Some of the business decisions involve short run outcome while

others may have long run pay-offs. A certain business decision may be more

profitable in the short-run than in the long-run and vice-versa. For instance say a

business firm decides to increase its expenses on medical facilities along with other

facilities to its workers. Such a decision may escalate costs in the short-run but in the

long run it may lead to increasing revenues by way of enhanced productivity of

workers. Therefore, time perspective is of utmost importance in business decision

making.

1.6.4 Production Possibility Curve

Production Possibility Curve (PPC) is a curve which indicates different

combinations of two commodities that can be produced in an economy at any point

of time with the help of given techniques and resources. Production Possibility Curve

(PPC) is also called Production Possibility Frontier or Transformation Curve. For an

individual consumer, a PPC shows the different combinations of the two

commodities which a consumer can buy given his income and prices of the two

commodities. However, for the economy as a whole, it depicts the opportunity cost or

alternative cost of producing one good in terms of the amount of the other good

sacrificed subject to the limited availability of resources. This concept is also very

important for the business managers for decision making.

Activity B

How does the study of managerial economics help a business manager in decision making?

Illustrate your answer with examples from production and pricing issues.

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-------------------------------------------------------------------------------------------------------------------------

-----------------------------------------------------------------------------------------------------------------------

Check Your Progress 2

Fill up the blanks with correct words

(i) Managerial economics is a ………………to an end for managers in any business.

(ii) Marginal concept is applied when …………….calculation of MC and MR is

possible.

(iii) The opportunity cost is the cost of the benefit …………..

(iv) A rational decision involves ……………… incremental revenue as compared to

incremental cost.

1.7 Summary

Managerial economics has emerged as a separated branch of economics due

to increased applicability of economics in business decision-making process by the

managers. Managerial economics helps the business managers in choosing the

most efficient allocation of scarce resources to achieve the given objects. It is micro

as well as macro in nature. Its scope is immensely vast comprising economic

theories and concepts used to analyse business issues and to find practical solutions

to business problems. Managerial economics can thus be referred to as working

knowledge of economics applied to business decision making. It is also linked to

other fields of study, including mathematical tools, statistics, operation management

theory. The role of managerial economics in business decision making is extremely

important for the overall development of business activity. Important decision making

concepts include the principle of opportunity cost, marginal and incremental

principle, time perspective and production possibility curve.

1.8 Glossary

Managerial Economics: The study of economic theories, logic and tools of

economic analysis used in the process of business decision making.

Microeconomics: It attempts to study the economic behaviour of particular small

units of the entire economic system such as a consumer, a producer, a firm, a

worker, price of a particular commodity, etc.

Microeconomics: It attempts to study the economic problems concerning

aggregates in the economic system such as aggregate demand, aggregate supply,

general price level, gross national expenditure, growth rate of the economy, etc.

Opportunity cost: It is cost of the next best alternative which is not selected or

foregone.

Production Possibility Curve: It is a graph showing different combination of two

commodities which can be produced in an economy, given the scarce availability of

resources.

1.9 ANSWERS TO CHECK YOUR PROGRESS

Check Your Progress 1

1) (i) true

(ii) false

(iii) true

(iv) true

(v) false

Check Your Progress 2

1) (i) means

(ii) precise

(iii) foregone/not selected

(iv) higher

1.10 References

1. Spencer, M.H, and Seigelman, L., Managerial Economics, Irwin Illinois

2. Douglas, Evan J., Managerial Economics: Analysis and Strategy, Prentice-

Hall, N.J

3. Baye, Micheal R., Managerial Economics and Business Strategy, McGraw

Hill, Toronto.

4. Mithani D.M. : Managerial Economics, Himalaya Publishing House, Mumbai

5. Dwivedi, D.N. : Managerial Economics, Vikas Publishing House Pvt. Ltd, New

Delhi

1.11 Suggested Readings

1. Dean, Joel, Managerial Economics, Prentice Hall of India, New Delhi.

2. Solvatore, D., Managerial Economics, Mc Graw Hill, New York.

3. Davis, R and S. Chang, Principles of Managerial Economics, Prentice Hall,NJ

1.12 Terminal Questions

1) What do you understand by managerial economics? Explain its nature and

characteristics.

2) Discuss in detail the scope of managerial economics in modern business

environment.

3) Managerial economics is applied economics Discuss

4) Mention the important features of managerial economics.

5) Discuss the link of managerial economics with other disciplines. How do they

contribute to managerial economics?

6) The study of managerial economics helps a business manager in decision

making. Do you agree?

7) What is opportunity cost principle as applied to decision making?

8) How is time perspective important in business decision making?

LESSON – 2

Utility Analysis

Structure

2.0 Objectives

2.1 Introduction

2.2 Utility: Meaning and Features

2.3 Measurement of Utility

2.3.1 Cardinal Utility Analysis

2.3.1.1Assumptions of Cardinal Utility Analysis

2.3.1.2 Law of Diminishing Marginal Utility

2.3.1.3 Law of Equi Marginal Utility

2.3.1.4 Marginal Utility and Demand Curve

2.3.2 Ordinal Utility Analysis

2.3.2.1 Indifference Schedule and Indifference Curve

2.3.2.2 Properties of Indifference Curves

2.3.2.3Marginal Rate of Substitution

2.3.2.4 Price Line

2.3.2.5Consumer’s Equilibrium

2.4 Summary

2.5 Glossary

2.6 Answers to Check Your Progress

2.7References

2.8Suggested Readings

2.9Terminal and Model Questions

2.0 OBJECTIVES

After reading this lesson, you should be able:

To understand the meaning and features of utility

To bring out the difference between cardinal utility analysis and ordinal utility

analysis

To comprehend the concept of consumer’s equilibrium

2.1 INTRODUCTION

An individual as a consumer forms the basis of all production. The individual

consumer has a role to play in two markets in the economy- the factor market and the product

market. The individuals own the productive resources to be used for production and sell these

inputs to the firms in the factor market. On the other hand, as a consumer the individual lays a

demand on goods and services produced by the firms and makes a decision about the quality

and quantity to be bought and at what price. Hence, the force of demand is determined solely

by the behavior of the consumers in the product market. Any change in this force of

consumer demand can altogether change the market solution involving the forces of demand

and supply. Moreover, it is this consumer demand which forms the basis of all production

taking place in the economy. Hence, it is very important rather essentially required for all the

business managers to study the consumer’s behavior in the market. Given his income, prices

of different commodities and other factors, the consumer tries to find optional solutions for

several issues important to him like how much to buy, from whom to buy, what quality to

buy, and at what price to buy. In turn, these issues influence and frame the force of demand

for that particular product in the market.

The producers or sellers also want to know and need to know the preference and

choice of consumers. This insight into the buying behavior of consumers helps the firms in

taking important decisions regarding product type, its pricing, advertisement, new products

and many others. The consumer’s buying behavior or the consumer demand and choice, thus,

is crucial to the process of business decision making. In economic theory the consumer’s

choice and buying behavior have been explained with the help of the concept of utility.

2.2 Utility: Meaning and Features

The entire process of production is guided by the behavior of consumers. The

consumer behavior is explained on the basis of utility. Man by nature is full of desires, all of

which cannot be satisfied as the resources to satisfy them are limited. So the consumer has to

allocate his limited income among unlimited wants in such a way that he gets maximum

possible satisfaction or utility. The term utility owes its original to British philosopher Jeremy

Bentham. It refers to that quality or power in a commodity or service that satisfies a human

want. Every consumer buys several commodities because these commodities can satisfy his

wants. This want satisfying power of a commodity or a service is called utility.

Utility is a psychological or subjective concept, slightly different from satisfaction.

For instance say a consumer wants to buy a chocolate. This shows that chocolate has utility

for the consumer. When the consumer eats it, the good feeling that he gets is satisfaction. Had

he not liked the chocolate he would not have got satisfaction (although it had utility for him,

that is why he bought the chocolate). Thus, utility implies expected satisfaction whereas

satisfaction stands for realized satisfaction. Another feature of utility is its ethical neutrality.

The commodities like liquor, drugs, tobacco and the like too have utility for the consumer but

may be unethical, immoral and even illegal in some cases. Further, utility is a relative term in

the sense that it varies from person to person, place to place and time to time. Cigarettes have

great utility for a chain smoker while no utility for a non-smoker. A person living in a

metropolitan city may have an intense want for a car while a person living in a remote village

may not need it at all. People have greater utility of woollens during winter months than in

summer season. Hence, utility is a relative concept which may vary from person to person,

place to place and even time to time.

2.3 Measurement of Utility

Two different views are found in economic literature regarding the measurement of

utility. The first view point assumes that the utility can be exactly measured in cardinal

numbers and like cardinal numbers the utility from different units of commodities can be

added or subtracted. This approach is called the cardinal utility analysis. On the other hand,

according to the second viewpoint the utility cannot be exactly measured in cardinal

numbers- it can only be ranked just like the ordinal numbers. Hence, this approach is referred

to as the ordinal utility analysis. Both these approaches to utility analysis are discussed

below.

2.3.1 Cardinal Utility Analysis

The cardinal approach to utility analysis is based on the assumption that the utility

derived from a commodity is quantifiable and can be exactly measured in numbers. Based on

the cardinal measurement of utility there are two main concepts of utility.

(i) Total Utility: Total Utility is the sum of utilities derived from the consumption of all

the units of a commodity or service within a given time period. Thus, if a consumer buys five

mangoes, the sum of utilities from all the five units of mangoes is the total utility. Total

utility is a direct function of the quantity purchased. As the quantity purchased increases it

leads to an increase in the total utility. This can be expressed as

TUx = f (Qx)

Where TUx is the total utility derived from x commodity and Qx refers to the units of x

commodity.

(ii) Marginal Utility: Marginal Utility refers to the utility derived from the last or

marginal unit of a given commodity. It is defined as the addition made to total utility by

consuming an additional unit of the commodity within a given period of time. It can be

measured as follows

MUn = TUn – Tun – 1

where MUn is the marginal utility of nth

unit

TUn = Total utility from n units.

TUn-1 = Total utility from (n-1) units

Alternatively marginal utility can also be defined as the rate of change of total utility

due to a unit change in the quantity of given commodity. On the basis of this definition,

marginal utility can be measured as follows:

where MUx is the marginal utility of x commodity

∆ TUX is the change in total utility of x commodity

∆ Qx is the change in quantity of x commodity consumed by one unit.

An important feature of the concept of marginal utility is that it can be either positive

or zero or negative. When total utility increases with purchase of an additional unit of the

commodity marginal utility is positive and marginal utility is negative if purchase of an

additional unit of the given commodity results in a fall in total utility. However, if there is no

change in total utility by purchasing an additional unit of the said commodity, marginal utility

is zero. When marginal utility becomes zero, total utility is maximum. This point of

maximum total utility and zero marginal utility corresponds to the point of maximum

satisfaction and is referred to as the point of saturation. If the consumer still continues to buy

more units of this commodity beyond the point of saturation, total utility begins to decline

and marginal utility becomes negative.

2.3.1.1 Assumptions of Cardinal Utility Analysis

The cardinal utility analysis maintains that utility can be added and subtracted.

However the explanation of consumer’s behavior- choices, tastes and preferences using

cardinal utility approach rests on the following main assumptions:

(i) Utility can be measured in cardinal numbers which means that it can be added or

subtracted.

(ii) Consumption of one commodity is not affected by its related goods. Utility of one

commodity is assumed to be independent of the utilities of other commodities.

(iii) Each unit of the given commodity being consumed should be homogenous or of

uniform quality.

(iv) The size of each unit of the commodity to be consumed should be standard, neither

very small nor very large.

TUxMU = X Qx

(v) The consumption of successive units should be continuous, that is no gap in

consumption of successive units should be there.

(vi) There should be no change either in the income of the consumer or in the price of the

commodity being consumed during the course of consumption.

(vii) There should be no change tastes and preferences of the consumer during the course

of consumption.

(viii) The commodity being consumed should be normal and non addictive in nature.

(ix) The most fundamental assumption in the cardinal utility analysis is that the consumer

is rational and aims to maximize his satisfaction.

The above stated assumptions of the cardinal utility analysis form the basis for the

two fundamental laws of economics- the law of diminishing marginal utility and the law of

equi marginal utility.

2.3.1.2 Law of Diminishing Marginal Utility

The law of diminishing marginal utility states that other things remaining the same, as

the consumer goes on buying more and more units of a commodity, the utility derived from

each successive unit goes on diminishing. This law is one of the basic laws of Economics and

is also called the first law of consumption. This diminishing marginal utility with each

additional unit of the commodity consumed can be attributed to two reasons:

(a) Each particular want is satiable. Inspite of the fact that there are unlimited wants, every

single want can be completely satisfied. Thus, when a consumer goes on consuming more

and more units of a commodity, his want gets fully satisfied and he does not wish to have any

more increase in the commodity. As such his marginal utility starts falling when consumption

increases.

(b) Goods are imperfect substitutes for one another. Satisfaction derived from any two

commodities is not same. Different goods satisfy different wants. If it were possible to

perfectly substitute a good for another good, it would have satisfied all other wants also.

Hence, its marginal utility would not have fallen rather would have increased.

The law of diminishing marginal utility can be explained with the help of a table and diagram

given below:

The above table shows that as the consumer goes on consuming more and more units of

apples, the total utility (TU) derived from the consumption of apples increases but marginal

utility (MU) declines continuously, so much so that it becomes zero when 6th unit of apple is

consumed. At this point TU is maximum corresponding which MU is zero. This is the point

of saturation or satiety or the point of maximum satisfaction. Beyond this point TU begins to

decrease as MU becomes negative. No rational consumer will continue consumption beyond

the point of satiety. The MU curve can be derived from the above schedule as below.

Marginal Utility

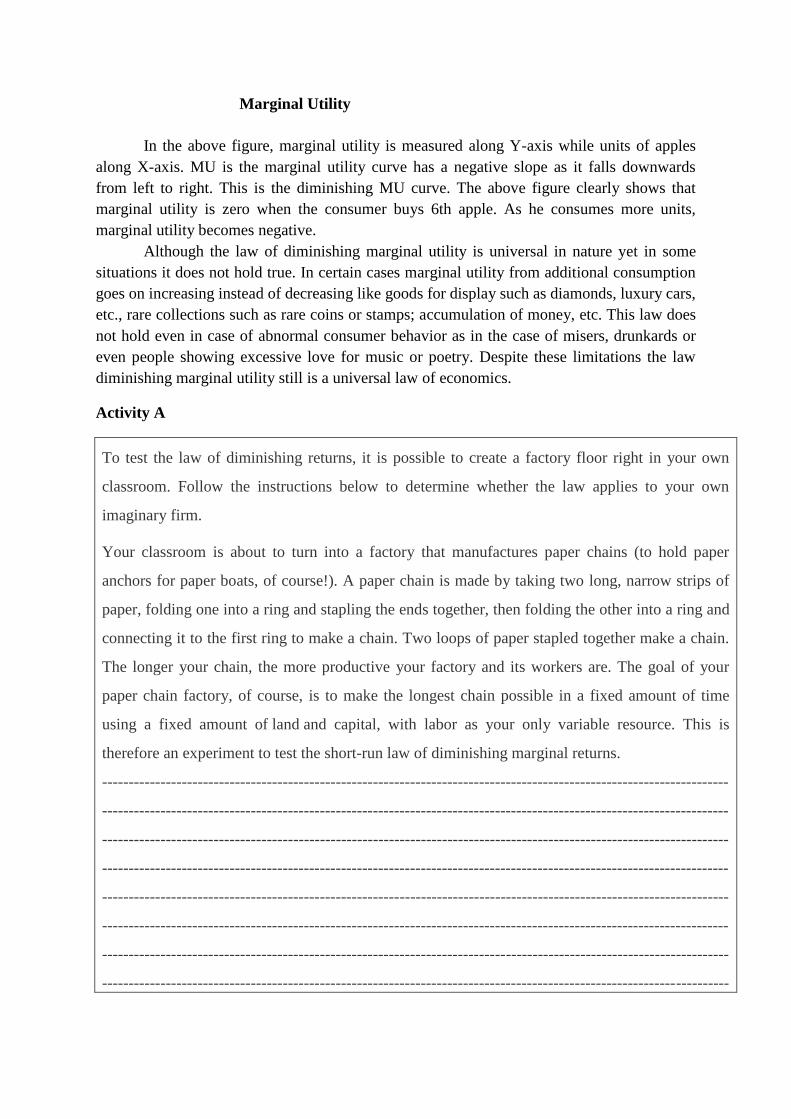

In the above figure, marginal utility is measured along Y-axis while units of apples

along X-axis. MU is the marginal utility curve has a negative slope as it falls downwards

from left to right. This is the diminishing MU curve. The above figure clearly shows that

marginal utility is zero when the consumer buys 6th apple. As he consumes more units,

marginal utility becomes negative.

Although the law of diminishing marginal utility is universal in nature yet in some

situations it does not hold true. In certain cases marginal utility from additional consumption

goes on increasing instead of decreasing like goods for display such as diamonds, luxury cars,

etc., rare collections such as rare coins or stamps; accumulation of money, etc. This law does

not hold even in case of abnormal consumer behavior as in the case of misers, drunkards or

even people showing excessive love for music or poetry. Despite these limitations the law

diminishing marginal utility still is a universal law of economics.

Activity A

To test the law of diminishing returns, it is possible to create a factory floor right in your own

classroom. Follow the instructions below to determine whether the law applies to your own

imaginary firm.

Your classroom is about to turn into a factory that manufactures paper chains (to hold paper

anchors for paper boats, of course!). A paper chain is made by taking two long, narrow strips of

paper, folding one into a ring and stapling the ends together, then folding the other into a ring and

connecting it to the first ring to make a chain. Two loops of paper stapled together make a chain.

The longer your chain, the more productive your factory and its workers are. The goal of your

paper chain factory, of course, is to make the longest chain possible in a fixed amount of time

using a fixed amount of land and capital, with labor as your only variable resource. This is

therefore an experiment to test the short-run law of diminishing marginal returns.

----------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------

----------------------------------------------------------------------------------------------------------------------

2.3.1.3 Law of Equi marginal Utility

The law of diminishing marginal utility is based on the consumption of a single

commodity. However in real life a consumer buys many commodities simultaneously to

maximize his satisfaction. In such a situation, when a consumer spends his limited income on

two or more commodities, the law of equi marginal utility comes into operation. This law of

equi marginal utility is just an extension of the law of diminishing marginal utilityto two or

more than two commodities. This law of equi marginal utility is known by different names :

the Law of Substitution, the Law of Maximum Satisfaction, the Law of Indifference, the

Proportionate Rule and the Gossen’s Second Law. It may be defined as follows:

The household maximizing the utility will so allocate the expenditure between commodities

that the utility of the last penny spent on each item is equal.

--- Lipsey

Every consumer has unlimited wants but limited income. The consumer is, therefore,

faced with a choice among many commodities. The objective of a rational consumer is to

maximize the total utility derived by spending his limited income on two or more

commodities. A rational consumer, in order to get the maximum satisfaction from his limited

income compares (i) the utility of a particular commodity and its price and (ii) the utility of

the other commodities which he can buy with his limited resources. If he finds that a

particular expenditure in a commodity is yielding less utility than another, he will shift the

unit of expenditure from the commodity yielding less marginal utility to a commodity

yielding more marginal utility. The consumer will reach his equilibrium position when it will

not be possible for him to increase the total utility further. The equilibrium will be reached

when the marginal utility of each commodity is in proportion to its price and the ratio of the

prices of all goods is equal to the ratio of their marginal utilities. In other words, the objective

of maximum satisfaction is achieved when the consumer is able to spend his limited income

in such a way that the utility of the last rupee spent on the various commodities is the same.

This can be expressed mathematically as:

MUa / Pa = MUb / Pb = MUc /Pc = …….= MUn / Pn

Where a,b,c,…….,n are different commodities consumed.

In such a situation the consumer becomes indifferent among different commodities

and gets maximum possible satisfaction. Any change in spending pattern against the law of

equi marginal utility results in a loss in satisfaction.

However, in certain cases, the actual behavior of the consumer is found inconsistent

with this law such as change in income, prices, tastes and preferences, ignorance on the part

of the consumer or difficulty in measurement of utility. Still both the law of diminishing

marginal and the law of equi marginal utility are of great practical importance and can also be

used to derive the demand curve for a commodity and hence are crucial importance.

2.3.1.4 Marginal Utility and Demand Curve

Dr. Alfred Marshall derived the demand curve using the law of diminishing marginal

utitlity. The law of diminishing marginal utility states that as the consumer purchases more

and more units of a commodity, he derives lesser utility from each successive unit of the

commodity purchased. Also, as the consumer buys more and more units of one commodity,

he is left with lesser money at his disposal. A rational consumer, therefore, while purchasing

a commodity compares its price with the utility he receives from it. As long as the marginal

utility of a commodity is higher than its price (MUx > Px), the consumer would demand more

units of it till its marginal utility becomes equal to its price (MUx = Px) and the equilibrium

condition is achieved. In other words, as the consumer consumes more and more units of a

commodity, marginal utility derived from the commodity goes on diminishing. Hence, the

consumer would demand more units of a commodity only at a diminishing price.

(a) (b)

Marginal Utility and Demand Curve

The part (a) of the above figure shows that the marginal utility curve of commodity X,say,

being consumed by the consumer is negatively sloped. This shows that as the consumer buys

larger quantities of commodity X, its marginal utility decreases. As a result at diminishing

price, the quantity demanded of the commodity x increases as is shown in part (b) of the

above diagram. When the quantity purchased is X1, the marginal utility of the commodity x

is MU1. By definition, this is equal to P1. The consumer in this case demands OX1 quantity

of the commodity at P1 price. Similarly, X2 quantity of the commodity is equal to price P2 as

at P2 price, the consumer will buy OX2 quantity of commodity. As is clear now, at price P3,

the consumer will buy OX3 quantity and so on. Hence, as the purchase of the units of

commodity X is increased, its marginal utility goes on diminishing. Equivalently, at a

diminishing price, the quantity demanded of good X increases as is clear from the diagram.

The law of demand (to be discussed later) states that, other things remaining the same, when

price of a commodity falls, its quantity demanded increases and vice versa. In other words,

the demand curve, which shows the relation between price of a commodity and its quantity

demanded, has a negative slope. Hence, the marginal utility curve of a commodity depicts its

downward sloping demand curve.(The negative part of marginal utility curve does not form a

part of the demand curve as negative quantities make no sense).

Therefore, the concept of marginal utility enjoys an integral place in utility analysis.

Moreover the utility approach or the cardinal utility analysis is of paramount importance in

explaining the theory consumer behavior, rather the theory consumer behavior remains

incomplete without it.

Check your progress 1

1. _________ is the attribute of a commodity to satisfy a consumer’s wants.

2. The __________________ analysis maintains that utility can be added and subtracted.

3. The utility derived from an additional unit of a commodity is called __________.

4. When marginal utility is zero, the total utility becomes_________.

5. Total utility is the summation of __________________ from all the units of a

commodity.

2.3.2 Ordinal Utility Analysis

The traditional cardinal utility approach suffers from several serious limitations. Out

of these, exact measurement of utility and cardinal measurement of utility were the ones

which received a lot of criticism. In view of the defects in cardinal utility approach, an

alternative theory of consumer behavior known as indifference curve theory or ordinal utility

analysis was developed. This approach of indifference curve analysis was first introduced in

1915 by a Russian economist Slustsky. It was later developed by J.R. Hicks and R.G.D. Allen

in 1928. In contrast to the cardinal utility approach, the indifference curve analysis is based

on the ordinal measurement of utility. It totally ruled out the possibility of cardinal

measurement of utility. This approach emphasized that only ordinal measurements or

comparisons of satisfaction from different combinations of commodities were possible. The

ordinal approach assumes that utilityis purely subjective and cannot be measured. Further, an

individual is interested in a buying a combination of related goods and not in the purchase of

one commodity at a time. So this theory of consumption is based on a scale of preferences or

a list of priorities prepared by the consumer in his mind according to the satisfaction levels

got from different combinations of goods.

In ordinal utility analysis, a consumer’s tastes and equilibrium is shown by

indifference curves. An indifference curve is a curve which shows the various combinations

of two commodities X and Y which yield equal utility or satisfaction to the consumer. An

indifference curve shows an ordinal rather than a cardinal measure of utility. It is also called

an iso-utility curve and all the combinations lying on an indifference curve yield equal

satisfaction.

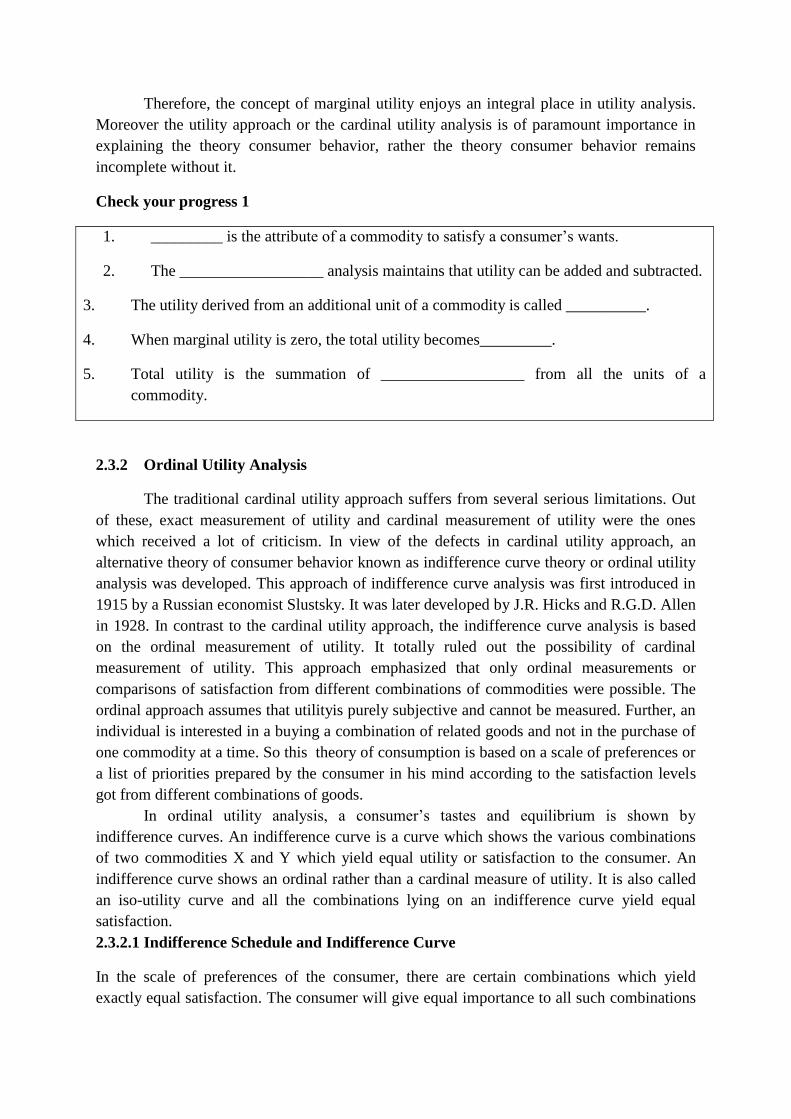

2.3.2.1 Indifference Schedule and Indifference Curve

In the scale of preferences of the consumer, there are certain combinations which yield

exactly equal satisfaction. The consumer will give equal importance to all such combinations

with no preference to any. He will be indifferent or neutral about these combinations. Such an

indifference on the part of the consumer about thecombinations of two commodities may be

explained with the help of an indifference schedule and indifference curve. An indifference

schedule is the tabular statement which shows the different combinations of two commodities

yielding the same level ofsatisfaction as shown below:

Indifference Schedule

Suppose the consumer is indifferent among the five combinations I, II, III, IV and V

of rice and wheat shown in the indifference schedule above. All these combinationsyield the

same level ofsatisfaction and the consumer gives equal preference to all. The consumer is

ready to give up four units of wheat(Y) to get one more unit of rice(X), only then

combination I and II will yield the same level ofsatisfaction. Similarly in combination III, the

consumer is ready to give up three units of wheat(Y) to get one more unit of rice(X) to get

same level ofsatisfaction, and so on. If a curve is drawn such that each point on the curve

shows a combinations of two commodities which yield the same level ofsatisfaction, such a

curve is called an indifference curve.

In the words of Leftwitch, “A single indifference curve shows the different

combinations of X and Y goods that yield equal satisfaction to the consumer.”

According to Hicks, “An indifference curve is the locus of the points representing

pairs of quantities between which the individual is indifferent.”

On the basis of the different combinations of two commodities yielding the same level

ofsatisfaction, an indifference curve can be shown as follows:

Indifference Curve

The indifference curve IC shown above indicates that the consumer gets equal level

ofsatisfaction from the combinations A, B, C, D, so he is indifferent among them, hence it is

called an indifference curve. Based on indifference curves, an indifference map can be drawn.

A set of indifference curves representing the scale of preference at different levels of

satisfaction is known as indifference map as shown below.

Indifference Map

All combinations lying on indifference curve 1 (IC1) provide the same satisfaction but

the level of satisfaction on Indifference curve 2 (IC2) will be greater than the level of

satisfaction on indifference curve 1 (IC1). Similarly, all combinations lying on indifference

curve 2 (IC2) provide the same satisfaction but the level of satisfaction on Indifference curve

3 (IC3) will be greater than the level of satisfaction on indifference curve 2 (IC2).

2.3.2.2 Properties of Indifference Curves

An indifference curve shows different combinations of two goods about which a

consumer is indifferent. The main properties or of indifference curvesare as follows:

An indifference curve slopes downwards from left to right.This means that when

the quantity of one good in the combination is increased, the quantity of the other

good should be reduced so that the total level of satisfaction remains constant.

However, if the indifference curve is a horizontal straight line parallel to x-axis

(figure (a)), it would mean that the consumer would remain indifferent between

various combinations even if the amount of good X increases while the amount of

good Y remains constant. This is not possible because the consumer always prefers

larger quantity of a good to lesser quantity of that good. Similarly an indifference

curve cannot be a vertical or upward sloping as shown below.

(a) (b) (c)

Higher the indifference curve higher is the level of satisfaction.This means thatthe

combination of commodities which lies on a higher indifference curve will be

preferred by a consumer to the combination which lies on a lower indifference curve.

Indifference Map

Indifference Curves are Convex to the Origin.As the consumer substitutes

commodity X for commodity Y, the marginal rate of substitution of X for Y decreases

along an indifference curve. As the consumer moves from combination A to B to C

to D, he is ready to give up lesser and lesser amounts of Y to get an additional unit of

X. Equivalently, the marginal rate of substitution of X for Y, that is, the quantity of Y

good that the consumer is willing to give up to get an additional unit of X, goes on

diminishing. The slope of IC is negative and it is convex to the origin as shown

below.

Two indifference curves can never intersect each other. An indifference curve

represents all those combinations of two goods which give equal level of satisfaction

to the consumer. In the figure given below the combinations represented by points A

and C will give equal satisfaction as they lie on the same indifference curve (IC2) just

as the combinations B and C will give equal satisfaction as they lie on IC1.

If combination A is equal to combination C and combination B is equal to combination C, it

means that the combination A will be equal to B. However, this is not possible as the

consumer will definitely prefer combination A to combination B. Hence, two indifference

curves can never cut each other.

2.3.2.3 Marginal Rate of Substitution

The concept of marginal rate of substitution (MRS)in the ordinal analysis was

introduced by Hicks and Allen. They used this concept to substitute the law of diminishing

marginal utility and to study the behavior of the consumer as to how the consumer prefers

one commodity to another and maintains the same level of satisfaction.The rate at which

commodities X and Y have to be exchanged is known as the marginal rate of substitution

(MRS)of X for Y. It may be defined as follows:

The marginal rate of substitution of X for Y measures the number of units of Y that must be

scarified for unit of X gained so as to maintain a constant level of satisfaction.

--- Hicks

Say there are two commodities X and Y which are imperfect substitutes of each other

and the consumer is willing to exchange good X for Y. The rate at which goods X and Y will

be exchanged is known as the marginal rate of substitution of X for Y (MRS

xy).Mathematically, marginal rate of substitution of X for Y (MRS xy) is expressed as

follows:

MRS xy = ∆Y∕∆X

where ∆Y shows change in quantity of Y commodity and ∆X shows change in quantity of X

commodity.

It is important to note that in case of indifference curve analysis the law of

diminishing marginal rate of substitution holds, which means that as the consumer increases

the purchase of X commodity, marginal rate of substitution of X for Y (MRS xy) goes on

diminishing.

Check your progress 2

1. State whether the following statements are True or False:

(i) The demand curve cannot be drawn using the marginal utility curve.

(ii) The ordinal utility approach is based on exact measurement of utility.

(iii) A single indifference curve shows the different combinations of X and Y goods that yield

equal satisfaction to the consumer.

(iv) Higher the indifference curve higher is the level of satisfaction.

(v) An indifference curve is always concave to the origin.

2.3.2.4Price Line

A price line or a budget line shows all those combinations of two commodities which

the consumer can buy given his money income and the prices of two commodities. The price

line is an important element of the theory of consumer behavior and preferences. The

indifference map reflects people’s preferences for different combinations of two goods under

consideration. Every consumer will try to to reach the highest possible indifference curve.

However, the actual choices made will depend on the income of the consumer and prices of

the two commodities. The price line or the budget line defines those combinations of two

goods under consideration which the consumer can actually buy within his income and prices

of the both commodities. Any combination lying outside the price line is beyond the reach of

the consumer and he cannot afford to buy it out of his limited income. The concept of price

line or the budget line can be explained with the help of the following diagram:

Price Line

Suppose a consumer has Rs.100 which he wants to spend on two commodities X and

Y. Let the prices of commodities X and Y be Rs.10 per unit and Rs. 5 per unit respectively. If

the consumer spends his entire income (Rs.100) on X, he would be able to buy 10 units of X,

and if he spends his total income on Y, he would buy 20 units of Y. If a straight line is drawn

joining 10 units of X and 20 units of Y, we get a line which is called the price line or budget

line.

The price line is drawn as a continuous straight line. Its slope is measured as the ratio

of prices of the two commodities. In the above diagram, slope of the price line is measured as

Slope of Price Line = Price of X Commodity/ Price of Y Commodity

If the prices of the two commodities remain the same but the income of the consumer

rises, the slope of price line will remain the same but it shifts its position to the right; and

vice-versa as shown in the figure below. It shows that if prices remain unchanged and income

rises, price line shifts to the right from L1 M1 to L2 M2.

Shift in Price Line

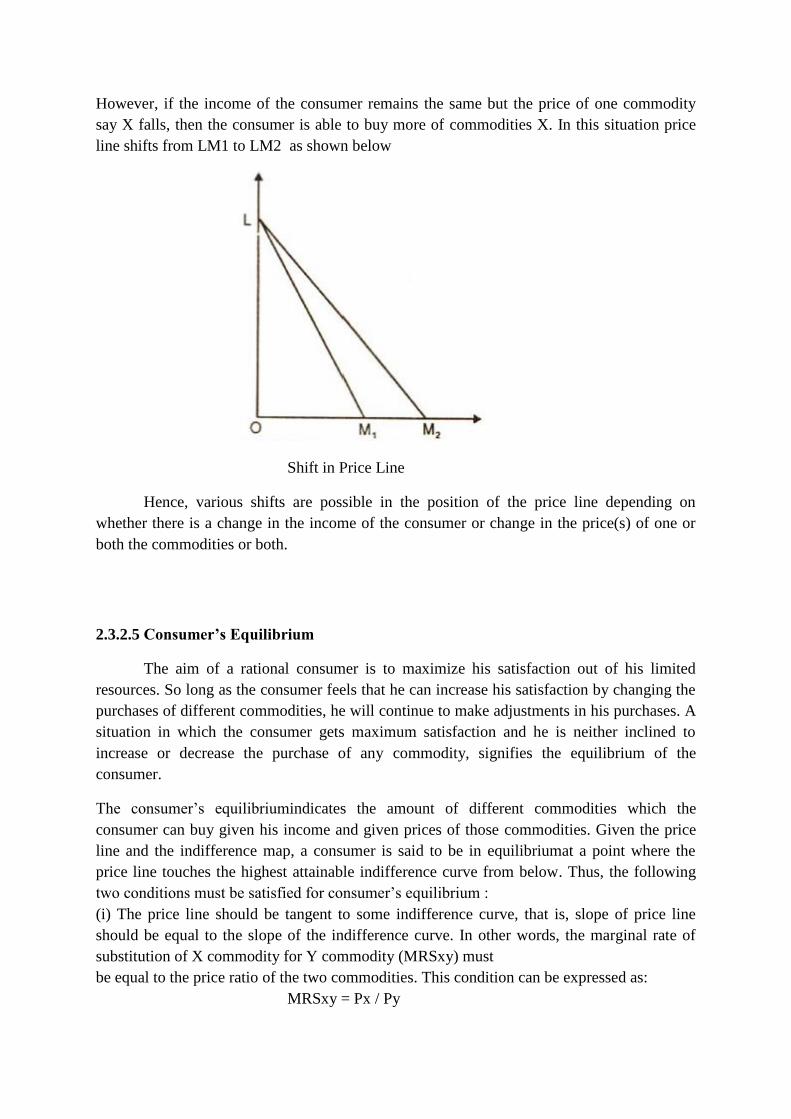

However, if the income of the consumer remains the same but the price of one commodity

say X falls, then the consumer is able to buy more of commodities X. In this situation price

line shifts from LM1 to LM2 as shown below

Shift in Price Line

Hence, various shifts are possible in the position of the price line depending on

whether there is a change in the income of the consumer or change in the price(s) of one or

both the commodities or both.

2.3.2.5 Consumer’s Equilibrium

The aim of a rational consumer is to maximize his satisfaction out of his limited

resources. So long as the consumer feels that he can increase his satisfaction by changing the

purchases of different commodities, he will continue to make adjustments in his purchases. A

situation in which the consumer gets maximum satisfaction and he is neither inclined to

increase or decrease the purchase of any commodity, signifies the equilibrium of the

consumer.

The consumer’s equilibriumindicates the amount of different commodities which the

consumer can buy given his income and given prices of those commodities. Given the price

line and the indifference map, a consumer is said to be in equilibriumat a point where the

price line touches the highest attainable indifference curve from below. Thus, the following

two conditions must be satisfied for consumer’s equilibrium :

(i) The price line should be tangent to some indifference curve, that is, slope of price line

should be equal to the slope of the indifference curve. In other words, the marginal rate of

substitution of X commodity for Y commodity (MRSxy) must

be equal to the price ratio of the two commodities. This condition can be expressed as:

MRSxy = Px / Py

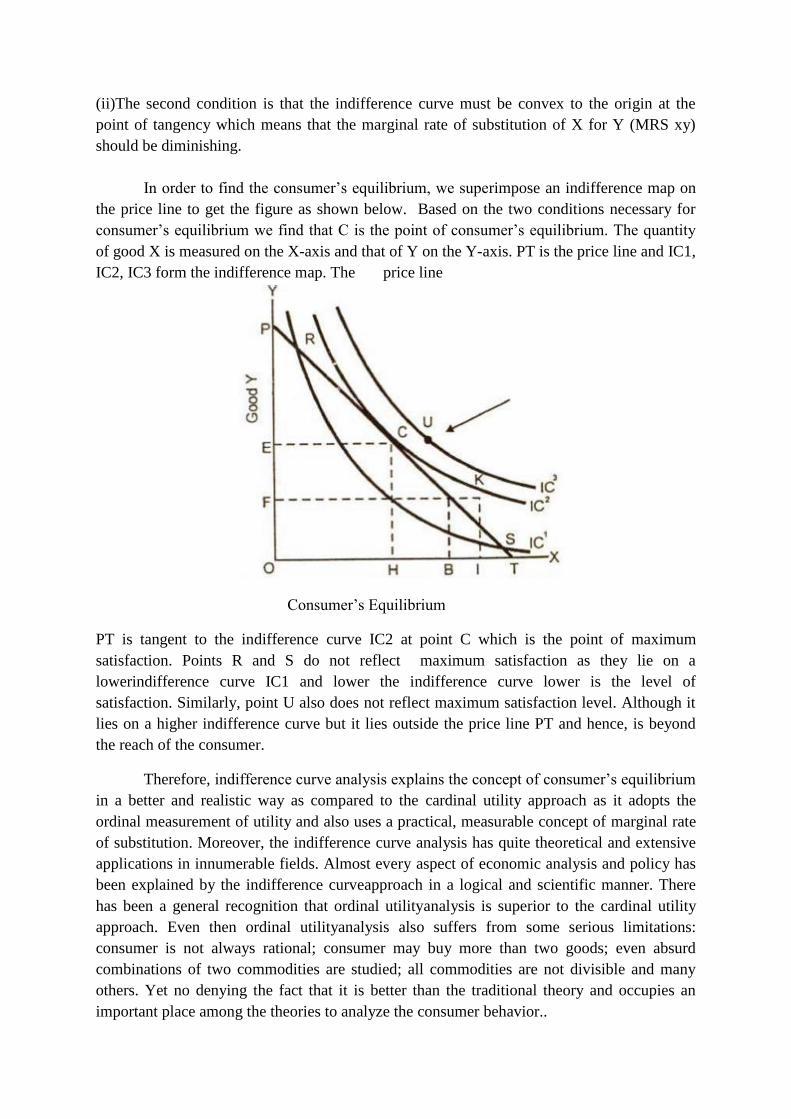

(ii)The second condition is that the indifference curve must be convex to the origin at the

point of tangency which means that the marginal rate of substitution of X for Y (MRS xy)

should be diminishing.

In order to find the consumer’s equilibrium, we superimpose an indifference map on

the price line to get the figure as shown below. Based on the two conditions necessary for

consumer’s equilibrium we find that C is the point of consumer’s equilibrium. The quantity

of good X is measured on the X-axis and that of Y on the Y-axis. PT is the price line and IC1,

IC2, IC3 form the indifference map. The price line

Consumer’s Equilibrium

PT is tangent to the indifference curve IC2 at point C which is the point of maximum

satisfaction. Points R and S do not reflect maximum satisfaction as they lie on a

lowerindifference curve IC1 and lower the indifference curve lower is the level of