Seeding a Steel Industry in Indonesian Established upon Local Raw Materials May 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Seeding a Steel Industry in Indonesian Established upon Local Raw Materials

May 2013

This document has been prepared as a summary only, and does not contain all information about the Company’s assets andliabilities, financial position and performance, profits and losses, prospects and the rights and liabilities attaching to theCompany’s securities. This document should be read in conjunction with any public announcements and reports (includingfinancial reports and disclosure documents) released by Indo Mines Limited. The securities issued by the Company areconsidered speculative and there is no guarantee that they will make a return on the capital invested, that dividends will bepaid on the Shares or that there will be an increase in the value of the Shares in the future.

Further details on risk factors associated with the Company’s operations and its securities are contained in the Company’sprospectuses and other relevant announcements to the Australian Stock Exchange.

Some of the statements contained in this release are forward-looking statements. Forward looking statements include butare not limited to, statements concerning estimates of recoverable pig iron, expected product prices, expected costs,statements relating to the continued advancement of the Company’s projects and other statements which are not historicalfacts. When used in this document, and on other published information of the Company, the words such as “aim”, “could”,“estimate”, “expect”, “intend”, “may”, “potential”, “should” and similar expressions are forward-looking statements.

Although the Company believes that its expectations reflected in the forward-looking statements are reasonable, suchstatements involve risk and uncertainties and no assurance can be given that actual results will be consistent with theseforward-looking statements. Various factors could cause actual results to differ from these forward-looking statementsinclude the potential that the Company’s projects may experience technical, geological, metallurgical and mechanicalproblems, changes in product prices and other risks not anticipated by the Company or disclosed in the Company’spublished material.

The Company does not purport to give financial or investment advice. No account has been taken of the objectives, financialsituation or needs of any recipient of this document. Recipients of this document should carefully consider whether thesecurities issued by the Company are an appropriate investment for them in light of their personal circumstances, includingtheir financial and taxation position.

Disclaimer

2

Indonesia Overview

• Democracy with population of 240 million+

• Reformed financial institutions

• The worlds 3rd fastest growing

economy

• Credit upgrade by Fitch, S&P and Moody

in the last year

• Resource rich (iron*, coal, oil….)

• One of the top performing economies

through the GFC

• Close to the major markets and growing

economies of the world

• Government to invest >US$600 billion in

new infrastructure projects

% GDP Growth

Gross Domestic Product US$ billion

3

0

100

200

300

400

500

600

700

800

900

1000

1990 1995 2000 2005 2010

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

2007 2008 2009 2010 2011 2012

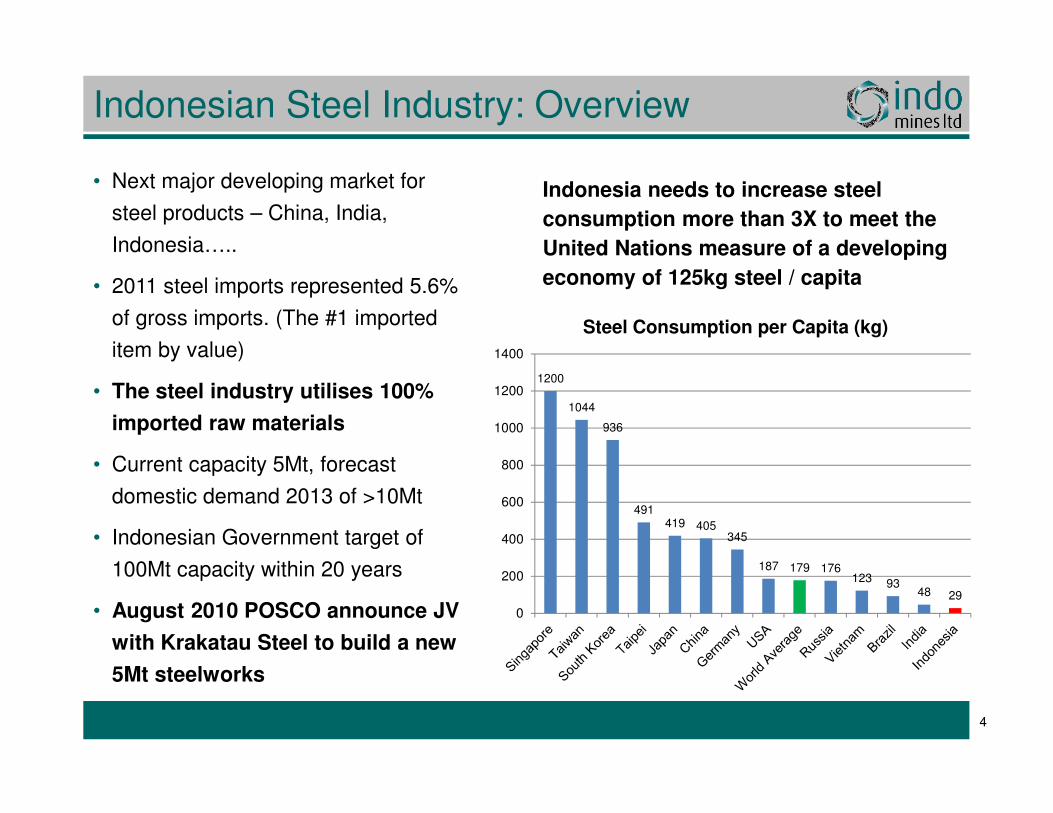

Indonesian Steel Industry: Overview

• Next major developing market for

steel products – China, India,

Indonesia…..

• 2011 steel imports represented 5.6%

of gross imports. (The #1 imported

item by value)

• The steel industry utilises 100%

imported raw materials

• Current capacity 5Mt, forecast

domestic demand 2013 of >10Mt

• Indonesian Government target of

100Mt capacity within 20 years

• August 2010 POSCO announce JV

with Krakatau Steel to build a new

5Mt steelworks

Indonesia needs to increase steel

consumption more than 3X to meet the

United Nations measure of a developing

economy of 125kg steel / capita

1200

1044

936

491419 405

345

187 179 176123 93

48 29

0

200

400

600

800

1000

1200

1400

Steel Consumption per Capita (kg)

4

Steel Industry Overview

• The origins of the world steel industry can be

traced back to the early 1800’s and the

development of the Bessemer and Blast

Furnace processes in Europe

• The processes were established to process

local Haemetite iron ore and coking coal

• Indonesia has a limited Haemetite and coking

coal resources but abundant, low cost local

iron ore in the form of iron sand and thermal

coal

• The development of an iron making

processes to consume iron sand was

commercialised in New Zealand in 1967

• The advancements in Direct Reduced Iron

(DRI) technology has created the opportunity

to develop a steel industry based entirely

upon iron sand and thermal coal

5

Iron Sand: What is it?

• Iron Sand is Titano-magnetite, an abundant ore produced by volcanic activity

• It contains up to 60% Iron combined with up to 9% Titania and 0.5% Vanadium

• The high Titania content reduces the quantity that can be consumed by the Iron making Blast Furnace

• However, it is an ideal feed material for the Direct Reduction Iron technologies

• The ore has the added advantage of containing Vanadium, a potential valuable by-product Also: Titania slag is produced in the iron smelting process, which is used as feedstock for the Titania industry, or as high quality skid resistant road aggregate

An Overview of Titanomagnetite Ore

A composite of Iron and Titania. The grade of Fe is increased by grinding to remove attached Calcium alumino silicates

8

The Iron Project Consists Of Four Process stages

2 - Mineral Processing.1 – Mining.

3 – Reduction / Metallisation. 4 – Smelting

Genuine “Green” Mining

• Mining is simple, low cost and

environmentally friendly

• Simple excavation with no need for blasting or chemicals

• More than 92% of the material mined is returned to the ground after the iron is extracted

• Rehabilitation begins as soon as the waste is re-deposited

• Improved crop productivity after land rehabilitation

Rehabilitation of mined area

Technology Selection

The choice of which Direct Reduction Iron making technology to apply to any given resource is dependent on the selection of the fuel source:

Fuel Source: Jogja Magasa Iron

1. Natural gas availability is limited and cost prohibitive2. The project has therefore focused on coal as the desired local fuel3. DRI plants are designed for a minimum 25 year life4. Small changes in coal chemistry have a significant impact on the operation

of a DRI process5. The process will consume up to 3000t of coal per day. It requires a long-

term commercial contract from a single large consistent reliable seam (>40 million tonnes).

6. 74 coals have been tested to date. The preferred coal, primarily due to commercial considerations is a coal from Sumatra. Further ‘commercial’ testing is planned 2013

Company Overview

A New Generation Minerals Producer

Targeting a Unique Market Niche:

‘Seeding a steel industry

established upon local raw

materials’

Vision :

• To be the domestic raw material supplier of choice to the Growing Indonesian Steel and Metals Industry

• A supplier of choice to the Asian Metals Industry

Seeding a Local Steel Industry in Indonesia Indonesia

Strategy:To build on existing relationships within Indonesia to progress development of the Jogjakarta Pig Iron project and to capitalise on opportunities through effective management of the Company’s cash reserves.

13

Jogjakarta Iron Project

Jakarta

Jogjakarta

Iron Sands

100km

Potential

JAVA

20km

Iron Sand Mining Concession

Additional Resource Potential

Additional Resource Potential

JOGJAKARTA

Krakatau/POSCO

Jogjakarta Iron Project – Basic Infrastructure in Place

J o g j a k a r t a

2km

Mining Lease Boundary

• Java-Bali Power Interconnection close

to site capable of meeting power

requirements of the concentrate plant

• Barging wharf on Western boundary of

project area is under construction

15

(1) As at 16 May 2013(2) 31 March 2013

Jogjakarta Iron Project

Indo Mines Overview

• ASX-listed company

• Major asset: Jogjakarta Iron Sands (JMI) Project

(70% owned) covered by a Contract of Works

(CoW)

• Looking at additional iron sand and heavy mineral

opportunities

Jogjakarta Iron Project / JMI (70% IDO, 30% JMM)

• Development project located ~30 km’s from major

city of Jogjakarta, Indonesia

• Subject to receipt of necessary approvals, two

staged development of the project:

– Initial focus on 2Mtpa production of iron

concentrate

– Introduce Direct Reduction Iron (DRI) making

technology to develop a 1Mtpa pig iron plant

Substantial ShareholdersRajawali Group 57.1% RockCheck Trading Limited 8.3%Anglo Pacific Group 5.6%

16

Project Implementation Strategy

1. Initial 500,000 tonne per annum facility 1

2. Establish 2 million tonne feedstock capability ahead of Pig iron plant commissioning

3. Utilise local raw materials and technical expertise to manufacture Pig Iron with the maximum cash margin

1 Subject to receipt of export permit

The progressive construction of the integrated Pig Iron facility on the defined Pig Iron plant location

17

Simple Iron making Economics

Direct Reduction Iron Plant

Supplied from Local Raw materials:

• 100% Iron sand concentrate <US$25/t (55% Fe)

•Thermal Coal US$90/t.

Total iron cost <$300/t

18

Conventional Blast Furnace

Plant Supplied from imported Raw materials:

• 100% Iron ore US$140/t (62% Fe)

• Metallurgical coke >US$140/t

Total iron cost >$400/t

Project Timeline

19

Iron Concentrate Development

• Capital and associated costs of the

2 million tonne plant US$158m

Pig Iron Project Development• Estimated capital to complete Pig Iron

Definitive Feasibility Study (DFS) US$50m• Estimated capital to complete Pig Iron

project US$500m to US$600M excluding infrastructure

• Build time 30 months from funds approved

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015Pig Iron PlantHand OverQ1 2017

5ooktConc Plant

2.0 MtConc Plant

Pig IronTest WorkComplete

ConceptualEng Study

ProjectTender Award

1 Subject to receipt of export permit

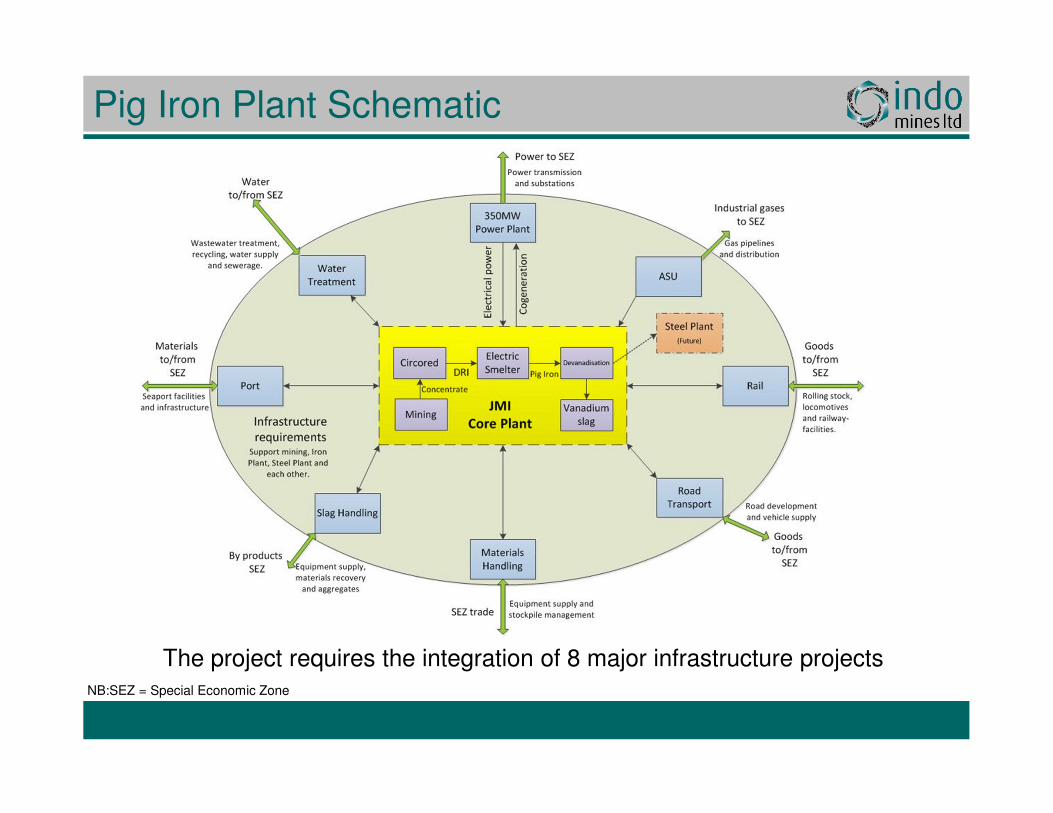

Pig Iron Plant Schematic

The project requires the integration of 8 major infrastructure projects NB:SEZ = Special Economic Zone

Proposed Business Structure

Activity JMI Government Joint Venture Private Business

Mega Project Coordination

Mining

Iron Concentrate

Pig Iron

Steel making

Air Separation Plant

Railway

Road

Materials Handling

Slag Products

Port

Water Treatment

Power Plant / Cogen

Critical / current priority Medium term priority 21

Pig Iron Market and Opportunity

Market Overview• Pig iron is a direct substitute for

scrap metal.• Blast furnace and electric arc

furnace operations require scrap as feed.

• Reduced availability of scrap, as developing countries are in the construction phase.

• Increasing correlation between pig iron and iron ore price.

However the highest margin is achieved through converting liquid iron to steel products

$0

$100

$200

$300

$400

$500

$600

$700

$800

Jan-0

3

Jul-0

3

Jan-0

4

Jul-0

4

Jan-0

5

Jul-0

5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

Jul-0

8

Jan-0

9

Jul-0

9

Jan-1

0

Pig Iron Price

Iron Ore Price

Strong Board

Over 100 years of resources exploration, development and operational experience

Managing Director – Strategy and Governance Rajawali Group since 2005. More than 20 years'experience in the finance and telecommunications industries including head of South East AsiaPractice with Coopers and Lybrand.

Peter J. ChambersChairman

Over 30 years experience in the iron and steel business including 23 years with New Zealand Steelwhere he was responsible for their iron sands operations, iron making, steel making, and by-products businesses

Martin HaconManaging Director

A metallurgist with over 20 years experience in the design and commissioning of mineralprocessing plants. In addition to his role with Indo Mines, Darryl is a Director of Outotec Australiaand ASX listed Consolidated Tin

Darryl HarrisNon-Executive Director

Over 20 years experience in corporate roles, including as company secretary of other ASX and AIMlisted companies

Stacey ApostolouCompany Secretary

Hendra SuryaChief Operating Officer

Highly experienced executive with over 25 years experience in the development and operation ofresources projects. Inaugural CFO of Fortescue Metals Group

Christopher CatlowNon-Executive Director

Joined the Rajawali Group in 2005 and is currently the Deputy Managing Director – Mining andResources. Previously with PricewaterhouseCoopers where he was involved with a number ofgovernment related projects and a wide number of privatisation and major project financings

Managing Director – Mining and Resources Rajawali Group appointed 2005. Mr Setiawan, whojoined the Rajawali group in 1996, also managers the group’s government and external relations.

Darjoto SetiawanNon-Executive Director

23

• Potential to become one of the lowest cost pig iron producers in the world

− Pilot plant has successfully manufactured the first pig iron ingots using Outotec

Ausiron© smelting process

− Conceptual plant design is underway

• Well located to key end users

− Off-take discussions with key Asian steel producers for both iron concentrate and pig

iron production

• Strong Board and management team with proven track record of developing and

operating resource projects including iron sand

• Utilising strong relationships to achieve strategy of becoming a supplier of choice

to the growing Indonesian and Asian steel and metals industry

• Significant cash balance to enable the Company to consider other investment

opportunities

• Excellent local partners, essential for success in Indonesia

Summary

24

Thank you

Head Office

68 South Terrace

South Perth WA 6951

Australia

Telephone: +61 8 9474 7710

Fax: +61 8 9368 1780

Email: [email protected]

Website: www.indomines.com.au

Business Risk: Land ownership & Logistics

Landownership Key Questions:

– Who owns the IUP

– Is the land currently leased or occupied

– What is the current use of the land?

– Is the land forested, does it require permits?

– Is the land owner a potential partner? (New mining law)

Logistics:

– What is currently in place?

– What is the ownership structure?

– What options are possible?

– What back up is required / available

27

Socialisation

• An absolute key to a successful project and essential at three levels:

– National Government

– Provincial Government

– Local villages

• Mining has a very poor image in the minds of many local people

• Perceived threats to way of life and traditional values are very real

28

Factors to Consider:

•Current land use•Current drivers of the local economy•What is currently missing•Employment & training •What legacy will be left after mining

Environment and Sustainability

Environment:• Intimately linked to Socialisation

• Create leverage through imposing Western Standards:

– Adopt a zero waste philosophy

– Rehabilitate immediately employing local businesses

Sustainability:• Demonstrate a whole of business

approach, profit, environment and social responsibility

• Demonstrate the long term benefits to the local people, employment, training etc

• Plan mine closure from day 1

29

Related Documents