SECURITISATION – A TOOL TO MODERN FINANCING. Index EXECUTIVE SUMMARY 3 INTRODUCTION TO SECURITISATION 5 1. INTRODUCTION 5 2. MEANING 7 3. HISTORY 9 4. BASIC PROCESS 11 5. FORMS OF SECURITISATION STRUCTURES 13 6. METHOD OF TRANSFER OF ASSETS 16 7. MOTIVATION AND BENEFITS 18 8. RISK PROFILE 23 9. PARTIES TO SECURITISATION 27 10. TYPES OF ASSETS THAT CAN BE SECURITISED 30 THE INDIAN EXPERIENCE 33 1. SECURITISATION IN INDIA 33 2. NEED FOR SECURITISATION IN INDIA 35 3. MAJOR CONSTRAINTS OF SECURITISATION IN INDIA 36 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SECURITISATION – A TOOL TO MODERN FINANCING.

IndexEXECUTIVE SUMMARY 3

INTRODUCTION TO SECURITISATION 5

1. INTRODUCTION 5

2. MEANING 7

3. HISTORY 9

4. BASIC PROCESS 11

5. FORMS OF SECURITISATION STRUCTURES 13

6. METHOD OF TRANSFER OF ASSETS 16

7. MOTIVATION AND BENEFITS 18

8. RISK PROFILE 23

9. PARTIES TO SECURITISATION 27

10. TYPES OF ASSETS THAT CAN BE SECURITISED 30

THE INDIAN EXPERIENCE 33

1. SECURITISATION IN INDIA 33

2. NEED FOR SECURITISATION IN INDIA 35

3. MAJOR CONSTRAINTS OF SECURITISATION IN INDIA 36

4. FUTURE PROSPECTS OF SECURITASATION IN INDIA 39

BANKING & SECURITISATION 41

1. THE CONCEPT 41

2. THE PROCESS AND PARTICIPANTS 41

3. IMPACT ON BANKS 44

4. IMPACT ON THE INDIAN BANKING SECTOR 46

1

SECURITISATION – A TOOL TO MODERN FINANCING.

INFRASTRUCTURE DEVELOPMENT AND FINANCING 50

1. INTRODUCTION 50

2. WHAT IS INFRASTRUCTURE? 50

3. WHY IS INFRASTRUCTURE IMPORTANT? 51

4. KEY ISSUES 52

5. FISCAL INCENTIVES FOR INVESTING IN

INFRASTRUCTURE PROJECTS 54

6. TECHNIQUE OF SECURITISATION IN INFRASTRUCTURE

FINANCING 55

7. INTRODUCTION TO THE VARIOUS SECTORS UNDER

INFRASTRUCTURE 57

8. RELEVANCE OF SECURITISATION TO DIFFERENT

SECTORS OF INFRASTRUCTURE 59

9. CRITERIA FOR STRUCTURING A SECURITISATION

TRANSACTION 62

10. PRE REQUISITES FOR STRUCTURING 64

11. SECURITISATION IN THE PRE IMPLEMENTATION

STAGE 65

12. SECURITISATION IN THE POST COMMISSIONING STAGE 66

THE NHB – HDFC – RMBS TRANSACTION 67

HDFC COMPLETES ASSET BACKED SECURITISATION 77

CONCLUSION 78

BIBLIOGRAPHY 79

2

SECURITISATION – A TOOL TO MODERN FINANCING.

Securitisation – A Tool to Modern Financing

EXECUTIVE SUMMARY

The objective of this study is to understand the concept of Securitisation, its

history, and its importance in the field of financing in an ever booming global

economy.

Securitisation is the process of conversion of existing assets or future cash flows

into marketable securities. In other words, securitisation deals with the conversion

of assets which are not marketable into marketable ones.

The meaning of "Securitisation" is to create a multiple assets generation at a lower

Cost of Capital while protecting the Beneficial Interest of the Investors. It is a

financial instrument for various investment projects. Securitisation in simple

words can be defined as "Structured Project Finance.” Thus it can be said with

ease that the objective of "True Securitisation" is to create a multiple assets

generation at a lower Cost of Capital while protecting the Beneficial Interest of the

Investors.

The study also gives an overview on the Indian experience of securitisation, its

help in financing infrastructure projects & building credit off stake for banks and

its importance and future in the Indian economy

Provision of quality infrastructure services at a reasonable cost, is a necessary

condition for achieving sustained economic growth. In fact, one of the major

challenges being faced by the Indian economy is to enhance infrastructure

investment and to improve the delivery system and quality of services. There is a

3

SECURITISATION – A TOOL TO MODERN FINANCING.

huge critical importance of the infrastructure sector and high priority for

development of various infrastructure is being given these days. Investments in

these sectors involve high risk, low return, lumpiness of huge investment, high

incremental capital/output ratio, long payback periods, and superior technology.

The Infrastructure Sector, it is the biggest Capital Deficit Sector of Indian

Economy; it requires Financial Engineering and Innovations to Fund the

Infrastructure Projects. One of best the solutions to this problem is

"Securitisation."

The need of securitisation is not only felt by the infrastructure sector but also the

banking sector. Other than freeing up the blocked assets of banks, Securitisation

can transform banking in other ways as well - it helps in the growth of credit off

stake of banks thus funding for release of more loans.

This will benefit investors as they will have a claim over the future cash flows.

The Originator will also benefit as loan obligations will be met from cash flows

generated.

The reasons why Securitisation gains over other forms is its low capital costs for

high asset generation, an alternative source of fund and minimal risks involved.

Therefore Securitisation can be viewed as a major tool for financing the various

projects over different sectors in the present as well as for the years to come

4

SECURITISATION – A TOOL TO MODERN FINANCING.

INTRODUCTION TO SECURITISATION

INTRODUCTION

"Securitisation will be the major financial instrument for the next decade,"

-by ICICI chairman K V Kamat.

Recent years have witnessed the wide spread of Western financial innovations into

developing markets. Globalisation and integration of capital markets, started in the

1990s, have made it possible for such big global players as India to adopt new

financial strategies which allow increasing liquidity and accelerating development

of the capital markets. One of these financial innovations is securitisation, the

process of transformation of illiquid assets into a security which can be traded in

the capital markets.

Securitisation is the buzzword in today's World of Finance. It's not a new subject

to the developed economies. It is certainly a new concept for the emerging markets

like India. The Technique of Securitisation definitely holds great promise for a

Developing Country like India.

Funds of a firm get blocked in various types of assets such as loans, advances,

receivables etc. To meet its growing funds requirements, a firm has to raise

additional funds from the market while the existing assets continue to remain on

its books. This adversely affects the capital adequacy and debt equity ratio of the

firm and may also raise its cost of capital. An alternative available is to use the

existing illiquid assets for raising funds by converting them into negotiable

instruments. E.g. a housing loan finance company, which has a portfolio of loan

advances having periodic cash flows, may convert this portfolio to instant cash.

Though the end result of securitisation is financing, it is not financing as such

5

SECURITISATION – A TOOL TO MODERN FINANCING.

since the firm securitizing its assets is not borrowing money, but selling a stream

of cash flows that are otherwise to accrue to it.

Securitisation is "Structured Project Finance". The financial instrument is

structured or tailored to the risk-return and maturity needs of the investors, rather

than a simple claim against an entity or asset. The popular use of the term

Structured Finance in today's financial world is to refer to such financing

instruments where the financier does not look at the entity as a risk: but tries to

align the financing to specific cash accruals of the borrower.

The actual and a current meaning of securitisation is a blend of two forces that are

critical in today's world of Finance: Structured Project Finance and Capital

Markets.

The process of Securitisation creates a strata of risk-return and different maturity

securities and is marketable into the capital markets as per the needs of the

investors. The basic idea is to take the outcome of this process into the market, the

capital market. Thus, the result of every securitisation process, whatever might be

the area to which it is applied, is to create certain instruments, which can be placed

in the market.

Securitisation is the process of de-construction of an entity: If one envisages an

entity’s assets as being composed of claims to various cash flows, the process of

securitisation would split apart these cash flows into different buckets, classify

them, and sell these classified parts to different investors as per their needs. Thus

securitisation breaks the entity into various sub-sets.

Securitisation is the process of integration and differentiation: The entity that

securitizes its assets first pools them together into a common hotchpot assuming it

is not one asset but several assets. This is the process of integration. Then, the pool

6

SECURITISATION – A TOOL TO MODERN FINANCING.

itself is broken into instruments of fixed denomination. This is the process of

differentiation.

MEANING

Securitization is the process of homogenizing and packaging financial instruments

into a new fungible one. Acquisition, classification, collateralization, composition,

pooling and distribution are functions within this process

As defined by The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002:

“Securitisation” means acquisition of financial assets by any securitisation

company or reconstruction company from any originator, whether by raising of

funds by such securitisation company or reconstruction company from qualified

institutional buyers by issue of security receipts representing undivided interest in

such financial assets or otherwise.

Securitisation is the process by which, financial assets such as household

mortgages, credit card balances, hire-purchase debtors and trade debtors, etc., are

transformed into securities by the owner (the Originator) in return for an

immediate cash payment and/or deferred consideration through a Special Purpose

Vehicle (SPV) created for this purpose.

The pooling standard prescribes that the asset portfolio has to be homogeneous in

terms of underlying financial asset, maturity and risk profile. This ensures an

efficient analysis of the credit risk of the asset portfolio and a common payment

pattern. It means only one type of asset (e.g. car loans) of similar duration (e.g. 20

to 24 months) having uniform risk (whose repayment is continuous during the first

10 to 12 months of the loan) will be bundled for creating one securitized

instrument.

7

SECURITISATION – A TOOL TO MODERN FINANCING.

The Special Purpose Vehicle finances the assets transferred to it by the issue of

debt securities such as loan notes or Pass through Certificates, which are

generally monitored by trustees. Pass through Certificates are certificates

acknowledging a debt where the payment of interest and/or the repayment of

principal are directly or indirectly linked or related to realisations from securitised

assets.

Let us consider some examples:

1) Suppose Mr X wants to open a multiplex and is in need of funds for the

same. To raise funds, Mr X can sell his future cash flows (cash flows arising from

sale of movie tickets and food items in the future) in the form of securities to raise

money.

This will benefit investors as they will have a claim over the future cash flows

generated from the multiplex. Mr X will also benefit as loan obligations will be

met from cash flows generated from the multiplex itself.

2) A finance company with a portfolio of car loans can raise funds by selling

these loans to another entity. But this sale can also be done by “securitizing” its

car loans portfolio into instruments with a fixed return based on the maturity

profile (the period for which the loans are given). If the company has Rs 100 crore

worth of car loans and is due to earn 17 per cent income on them, it can securitize

these loans into instruments with 16 % return with safeguards against defaults.

These could be sold by the finance company to another if it needs funds before

these loan repayments are due. The principal and interest repayment on the

securitised instruments are met from the assets which are securitised, in this case,

the car loans.

8

SECURITISATION – A TOOL TO MODERN FINANCING.

Selling these securities in the market has a double impact. One, it will provide

the company with cash before the loans mature. Two, the assets (car loans) will go

out of the books of the finance company, a good thing as all risk is removed.

HISTORY

Securitization in its present form originated in the mortgage markets in USA. It

was promoted with the active support of the government. The government wanted

to promote secondary markets in mortgages to allow liquidity for mortgage

finance companies. Government National Mortgage Association (GNMA) was the

first one to buy mortgages from mortgage companies and to convert them into

pass through securities - this was 1970. GNMA were passing through securities

backed by Mortgage insured by FHA.

These pass through have the full credit and the backing of the US government,

since GNMA has guaranteed both the repayment of the principal and timely

payment of the interest. The 1970 program (GNMA -I) is still in operation. In

1983, GNMA launched another pass through program called GNMA - II. These

programs are further classified based on the type of mortgages pooled therein,

such as single family (SF) loans, mobile home (MH) loans, project loans (PL) etc.

Other US government agencies, FNMA and Freddie Mac jumped in later. The first

FNMA Mortgage Backed Securities (MBS) was issued in 1981. The agency

played a crucial role in promoting securitisation of Adjustable-Rate Mortgages

(ARMs) and Variable Rate Mortgages (VRMs). FHLMC was created in 1970 to

promote an active national secondary market in residential mortgages and has been

issuing mortgage-backed securities since 1971.

The first securitisation of receivables outside the mortgage markets happened in

1975 when Sperry Corporation securitised its computer lease receivables.

9

SECURITISATION – A TOOL TO MODERN FINANCING.

Another mortgage funding device, slightly different from the US-type Pass

through Certificates, has existed in Europe for almost two centuries in the past. In

Denmark, for example, mortgage bonds are more than 200 years old. Germany

also has a long history of mortgage bonds and it is stated that there have been no

defaults on these instruments for all these years.

Other countries in Europe have been relatively slow starters, though regulatory

and legislative changes in Germany, France, Belgium and Spain have been

fashioned to assist development of securitisation. In Japan, the securitisation

market was not well developed until recently; the Government had restricted

securitisation to the assets of leasing, consumer loans and credit card companies.

The Government has, however, amended laws to allow full-scale securitisation in

May 1997.

India

The first widely reported securitisation deal in India occurred in 1990 when auto

loans were secured by Citibank and sold to the GIC mutual fund. However, the

sound legal framework for securitisation was not drafted until 2002 when the

Securitisation and Reconstruction of Financial Assets and Enforcement of Security

Ordinance (Ordinance) was promulgated by the president of India. According to

this law, securitisation was defined as “acquisition of financial assets by any

securitisation company or reconstruction company from any originator, whether

by raising funds by such securitisation or reconstruction company from qualified

institutional buyers by issue of security receipts representing undivided interest in

such financial assets or otherwise”. The notion of financial assets for the above

definition is stated as any debt or receivables. Non-surprisingly, it follows that the

definition of securitisation in India is very close to that of western countries,

10

SECURITISATION – A TOOL TO MODERN FINANCING.

especially taking into account that the experience of the UK is of special relevance

to India.

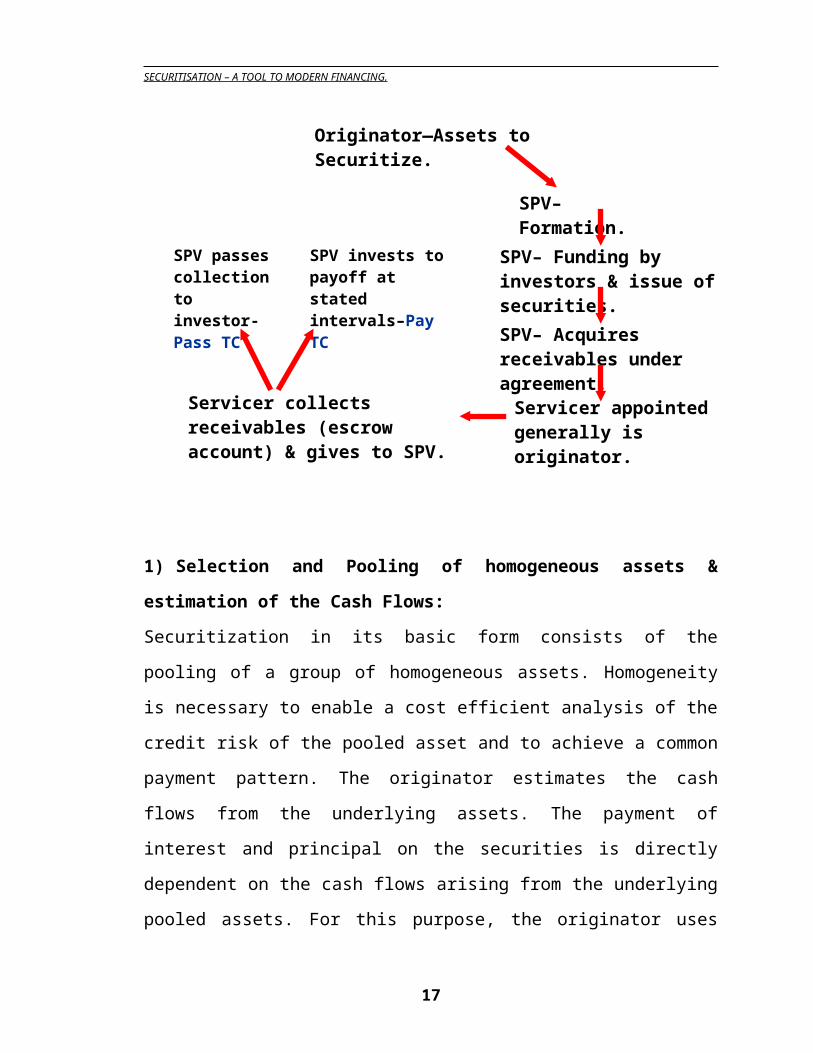

BASIC PROCESS

The basis process of Securitisation is explained in the following steps:

1) Selection and Pooling of homogeneous assets & estimation of the Cash

Flows:

Securitization in its basic form consists of the pooling of a group of homogeneous

assets. Homogeneity is necessary to enable a cost efficient analysis of the credit

risk of the pooled asset and to achieve a common payment pattern. The originator

Servicer appointed generally is originator.

Originator—Assets to Securitize.

SPV– Formation.

SPV– Funding by investors & issue of securities.

SPV– Acquires receivables under agreement.

Servicer collects receivables (escrow account) & gives to SPV.

SPV passes collection to investor- Pass TC

SPV invests to payoff at stated intervals–Pay TC

11

SECURITISATION – A TOOL TO MODERN FINANCING.

estimates the cash flows from the underlying assets. The payment of interest and

principal on the securities is directly dependent on the cash flows arising from the

underlying pooled assets. For this purpose, the originator uses his historical data.

Appropriate and accurate calculations are done keeping in view of the pre payment

rates, amortization, etc for estimation of the cash flows.

2) Creation of SPV:

The next step is to create an SPV.

The basis logic behind the creation of an SPV is

a) To isolate the underlying assets from the originator. This is an important

step in the whole process as the ultimate result of this is "Bankruptcy

Remoteness" from the Originator.

b) Aggregation of the underlying assets into a Pool. Thus the assignment of

the cash flow to the SPV is done in this manner.

3) SPV issues securities/notes to the Investors:

The SPV formed (Trust / MF / Corporate Form) now issues securities/notes to

the investors to invest in the securitised exercise done by the originator.

4) Investors - Proceeds of the issue of securities to SPV

The collection from the investors for their investment in the securitised instrument

is forwarded to the SPV. The SPV, in turn, channelises these proceeds to the

Originator.

5) Collections and Servicing from the Obligors:

The Originator generally performs this function. In some cases, specialized

servicing agents are appointed to collect and service from the loan obligors.

6) Pass Over to the SPV:

12

SECURITISATION – A TOOL TO MODERN FINANCING.

In this step the Servicing agent passes the collected payments from the obligors to

the SPV less his fees.

7) Reinvestment of Cash Flows:

The SPV if permitted reinvests the proceeds from the Servicing agent (Generally

in the Pay through Structures) and in turn receives the reinvestment proceeds also.

If the structure of the instrument is the Pass Through Structure then Step no. 8 is

followed directly after Step no. 6.

8) Payment to the Investors:

The Investor earns on his investments by receiving the proceeds from the SPV.

Depending upon the structure of the Instrument the payment of the investment is

made to the Investors.

9) Originators Residuary Profit:

After the payments are made to the Investors if any residue is left, it is passed on

the Originator as his residuary profit, which is generally maintained, by the

originator for the over-collaterisation and guarantee purpose.

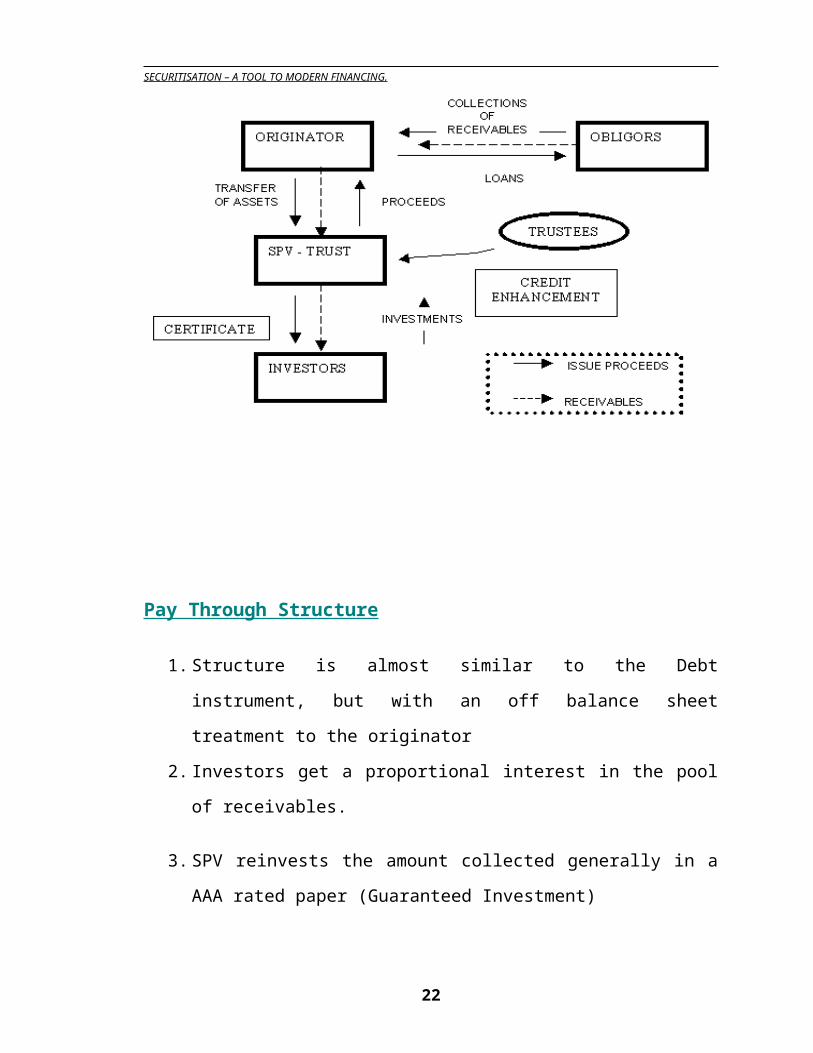

FORMS OF SECURITISATION STRUCTURES

The financial structure of the securitized product is a function of the type of the

instrument to be issued:

1. Pass Through Structure

2. Pay Through Structure.

13

SECURITISATION – A TOOL TO MODERN FINANCING.

Pass Through Structure

1. Investors get a proportional interest in the pool of receivables.

2. Monthly Collections are divided proportionally among the Investors.

3. All the investors receive proportional payments - no slower or faster

payments.

4. Refinement can be done in the form of 'Senior' or 'Junior' investors to

enhance the credit rating of the transaction.

5. Pre-payments are passed on to the Investors.

6. No reinvestment of cash collected.

7. Thus, SPV is a passive conduit.

Figure 1. Pass Through Structure

14

SECURITISATION – A TOOL TO MODERN FINANCING.

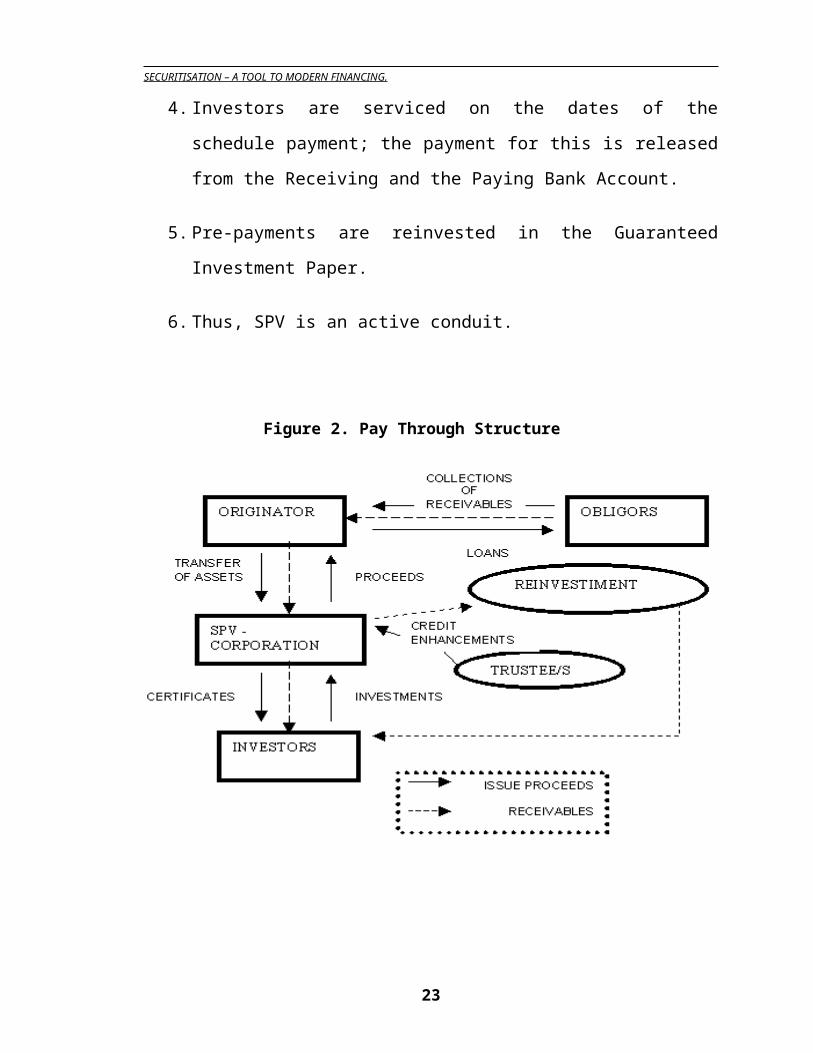

Pay Through Structure

1. Structure is almost similar to the Debt instrument, but with an off balance

sheet treatment to the originator

2. Investors get a proportional interest in the pool of receivables.

3. SPV reinvests the amount collected generally in a AAA rated paper

(Guaranteed Investment)

4. Investors are serviced on the dates of the schedule payment; the payment

for this is released from the Receiving and the Paying Bank Account.

5. Pre-payments are reinvested in the Guaranteed Investment Paper.

15

SECURITISATION – A TOOL TO MODERN FINANCING.

6. Thus, SPV is an active conduit.

Figure 2. Pay Through Structure

METHODS OF TRANSFER OF ASSETS

There could be three basic methods of transfer of assets, viz.,

1. Novation,

2. Assignment and

3. Sub-participation.

16

SECURITISATION – A TOOL TO MODERN FINANCING.

1. Novation is the clearest way of selling a loan and effectively transferring

both the rights and obligations. In novation, the existing loan between the

originator and the borrower is cancelled and a new agreement between the

investor and the borrower is substituted. The buyer steps into the shoes of

the original lender or seller who ceases to have any obligations to the

borrower. The loan, is therefore, excluded from the balance sheet of the

seller.

2. An assignment transfers from the seller to the buyer, all rights to principal

and interest. Assignments for the purpose of disposing off assets may fall

into two basic legal categories. The first is statutory assignment,

transferring both legal and beneficial title. A statutory assignment will pass

and transfer from the seller to the buyer all the legal rights to the principal

and the interest. In most cases, it will also pass on all the legal remedies

available against the borrower to ensure discharge of debt. In other words,

the buyer acquires the full legal and beneficial interest in the loan. The

second is equitable assignment, transferring only beneficial title. It does not

transfer legal rights. Thus, a buyer may not be able to proceed directly

against a borrower. The seller must be joined in action. However, the seller

is not liable for debt.

3. Sub-participation does not transfer any of the seller's rights, remedies or

obligations against the borrower to the buyer. But, it is an entirely separate,

back-to-back, non-recourse funding arrangement, under which the buyer

places funds with the seller. In return, the seller passes on to the buyer,

17

SECURITISATION – A TOOL TO MODERN FINANCING.

payments under the underlying loan, which the borrower makes to him.

But, the loan itself is not transferred.

18

SECURITISATION – A TOOL TO MODERN FINANCING.

MOTIVATION AND BENEFITS

TO THE ISSUER

Any company with a minimum of $400 million in sales and working capital needs

of at least $50 million should consider trade receivable securitisation, according to

the experts. "The securitisation structure is well established and is the logical next

step for companies who are approaching a half billion dollars in sales," says Dan

Hom, Senior Vice President, GE Capital Commercial Finance. "This mechanism

can either entirely support working capital needs, or it can become an integral part

of the total capital structure."

1. Capital requirement:

The issuer can raise funds of longer maturities than he would have been able to

through the conventional routes like bonds or term loans. For instance, in the case

of toll roads, the financing costs can normally be recovered only over a very long

period of time. A loan where repayments can be made over a long period may not

be easily available.

Here, securitisation can provide a solution. For instance, conventional loans are

generally backed by the borrower’s existing assets. In many cases, the borrower

may not be in a position to offer the required collateral. The process of

securitisation allows the borrower to raise funds against future cash flows rather

than existing assets.

Securitisation keeps the other traditional lines of credit undisturbed.

Hence, it increases the total financial resources available to a firm.

2. Off balance sheet financing:

This off balance sheet feature could be looked at either, from accounting

viewpoint, or from regulatory viewpoint. The tendency of financial institutions

19

SECURITISATION – A TOOL TO MODERN FINANCING.

and others to prefer off balance sheet funding over on-balance sheet funding is

because the former allows higher returns on assets, and higher returns on equity,

without affecting the debt-equity ratio. Securitisation allows a firm to create assets,

make income thereon, and yet put the assets off the balance sheet the moment they

are transferred through the securitisation device.

3. Influence on Financial Ratio:

By being able to market an asset outright securitisation avoids the need to raise a

liability, and hence, it improves the capital structure. Alternatively if securitisation

proceeds are used to pay off existing liabilities, the firm achieves a lower debt-

equity ratio. Securitisation also leaves the firm with a healthier balance sheet and

reduced risk.

4. Raising funds at cheaper rates:

Cost reduction is one of the most important motivations in securitisation.

Securitisation seeks to break an originating company’s portfolio into echelons of

risks, trying to align them to different investors’ risk appetite. This alchemy

supposedly works - the weighted overall cost of a company that has securitised its

assets seems lower than a company that depends on generic funding. It is

important to note that one of the most tangible effects of securitisation is to reduce

the extent of risk capital or equity required for a given volume of asset creation.

Assuming that equity is the costliest of all sources of capital, lower equity

requirements do result into lower costs.

5. Providing Market access:

Securitisation enables a financial intermediary to retail-market its assets to a large

section of investors.

20

SECURITISATION – A TOOL TO MODERN FINANCING.

6. Perfect matching of assets and liabilities:

As a liability is created (in the real sense, no liability is created: only an asset is

disposed off) perfectly matching up an asset, it avoids the need to manage maturity

mismatches.

7. Makes the issuer rating irrelevant:

Being an asset based financing, securitisation may make it possible even for a low-

rated borrower to seek cheap finance, purely on the strength of the asset quality.

Hence, the issuer makes himself irrelevant in a properly structured securitisation

exercise.

8. Multiplies asset creation ability:

Securitisation makes it possible for the issuer to create any amount of asset with

given equity. The extent of assets that he can create is solely dependent on the

conversion cycle, that is, the period that elapses between the date an underlying

receivable is created and is marketed.

9. Helps in capital adequacy requirements:

Capital adequacy requirements are the requirements relating to minimum

regulatory capital for financial intermediaries. One of the very strong motivations

for securitisation is that it allows the financial entity to sell off some of its on-

balance sheet assets, and thus, remove them from the balance sheet, and hence

reduce the amount of capital required for regulatory purposes. Alternatively, if the

amount raised by selling on-balance-sheet assets is used for creating new assets,

the entity is able to increase its asset-creation without a haircut for its capital.

10. Risk trenching / Unbundling:

Securitisation has also been used by many entities for reducing credit

concentration. Concentration either sectoral, or geographical, implies risk.

21

SECURITISATION – A TOOL TO MODERN FINANCING.

Securitisation by transferring a non-recourse basis exposure by an entity has the

effect of transferring the risk.

11. Avoids interest rate risks:

One of the primary motives in securitisation of mortgage receivables was to

transfer interest rate risk to the investors. The lenders were subject to the risk since

the mortgages carried a fixed rate of return while the loans taken by the lenders

had a variable rate. When the mortgages were securitised, the lender made an

instant spread on the basis of a fixed rate, and therefore, completely avoided the

price risk.

12. Escapes taxes based on interest:

For technical purposes securitisation would not be treated as “interest on loans’.

Hence, if there are taxes based on interest earnings, the same would not be

applicable to investors earnings in securitised products.

TO THE INVESTOR

1. Yield premiums:Securitised offerings have offered good yields with adequate security. Empirical

data about securitisation offerings reveal that an investor who maintained a good

balance of the emerging market and developed market offerings has been able to

come out with good rates of return.

2. Diversification:

Securities issued by SPEs are typically backed by numerous assets. By investing

in a pool of assets rather than in an individual asset, investors can diversify their

risk. This is similar to the difference between investing in mutual funds as opposed

to individual stocks.

22

SECURITISATION – A TOOL TO MODERN FINANCING.

3. Liquidity:

From the point of view of the financial system as a whole, securitisation increases the

number of debt instruments in the market, and provides additional liquidity in the market.

There is an active secondary market in many types of ABS and MBS, whereas there is

relatively little trading in the underlying assets themselves. It could widen the market by

attracting new players on account of superior quality assets being available.

4. Varying investor needs:

Securitized instruments can be designed, or “structured” to meet different investor

needs. For example, some investors require shorter-term investments, while others

wish to make longer-term investments. Investors looking for a safe high-grade

investment can pick up a senior most a-type product, while those looking for a

mediocre risk but with a higher rate of return can opt for a B-type option.

5. Stability:

The securitisation market has exhibited very stable credit performance overall, and has

experienced relatively few adverse credit events such as downgrading or default of SPE

securities or bankruptcy of SPEs.

23

SECURITISATION – A TOOL TO MODERN FINANCING.

RISK PROFILE

The inherent nature of the securitized instrument makes it less risky. The cash

flow from the securitized instrument is backed by tangible identified financial

assets earmarked exclusively for an instrument and is independent of the

originator. Dependability of these cash flows is further strengthened as signified

by the ageing of the portfolio. This means, an asset having a cash flow for three

years would be monitored for the first 8 to 10 months to determine its historic loss

profile. Earmarking a specific pool of aged assets is the core feature contributing

to lowering the risk associated with securitized product. Further, the pool of

borrowers creates a natural diversification in terms of capacity to pay, geography,

type of the loan etc and thereby lowers the variability of cash flows in comparison

to cash flows from a single loan. So, lower the variability, lower is the risk

associated with the resulting securitized instrument.

Understanding of risk enhancement measures, which at times are used in

combination, is also necessary to analyze the risk profile of securitized product.

Normally, these risk enhancement measures are provided to cover the historic risk

profile (first level risk) of the financial assets and some percentage of losses,

which may be higher than the historic risk profile (second level risk).

Internal risk enhancement measures like over- collateralization, liquidity reserve,

corporate undertaking, senior / sub-ordinate structure, spread account etc. cover

the first level risk. External risk enhancement measures like insurance, guarantee,

and letter of credit are used to cover the second level risk.

Over-collateralisation means for servicing an instrument of Rs. 100/- cash flow

from underlying asset valuing Rs. 110/- are earmarked. Similarly, cash worth Rs.

5/- called Liquidity Reserve may be separately earmarked for servicing an

24

SECURITISATION – A TOOL TO MODERN FINANCING.

instrument of Rs. 100/-. These features cover investors against the likely default in

cash flow from the borrower to the extent of Over-collateralisation / Liquidity

Reserve.

In case of Senior/Sub-ordinate debt, cash flows from two groups of borrowers are

independently used to bundle two sets of securities. These two trenches of

securities are issued with a pre-determined priority in their servicing. This means

the senior trench has prior claim on the cash flows from the underlying assets so

that all losses will accrue first to the junior securities up to a pre-determined level.

Thereby, the losses of the senior debt are borne by the holders of the sub-ordinate

debt, normally the originator.

The difference between yield on the assets and yield to investors is the spread,

which is the gain to the originator. A portion of the amount earned out of this

spread is kept aside in a spread account to service investors. This amount is taken

back by the originator only after the payment of principal and interest to investors.

Other third party credit enhancement measures such as insurance, guarantee and

letter of credit are also used by originator to get a better credit rating for the

instruments.

With such multiple options for risk reduction and natural diversification inherent

in the product, can a securitized instrument be presumed to be risk free? No.

Primary risks associated with securitized product are pre-payment risk and credit

risk. The pre-payment means refinancing at lower rate of interest or early

repayment of the loan amount in part or in full. This risk is associated with

mortgaged backed products using the Pass Through Structure (PTC).

Generally, loan agreements allow the borrower to make an early payment of the

principal amount. The risk originates from the possibility of obligor making such

25

SECURITISATION – A TOOL TO MODERN FINANCING.

early payment of principal amount and thereby disturbing the yield and the

investment horizon of the investors.

For premium securities, accelerated pre-payment reduces the average life and yield

since the principal is received at par which is less than the initial price. Opposite is

the case of securities purchased at a discount. Consequently, investors have to

predict the average life of such securities and may have to look for alternate

investment opportunities in a changed interest rate scenario.

The Act provides for PTC as the securitized instrument and so the pre-payment

risk will exist in Indian market. Factors affecting pre-payment and corresponding

pre-payment models to evaluate this risk will have to be developed in order to

make investment decisions.

Credit risk reflects the risk that the obligor may not be able to make timely

payments on the loans or may even default on the loans. In case of defaults,

internal and external risk enhancement measures will come into play.

Finally, the mortgaged backed securitized products in the foreign markets are

backed by a guarantor who guarantees to the investors the timely payment of

interest and principal. As of now, such guarantees do not exist in Indian market.

However, National Housing Board (NHB) is working in this direction to guarantee

securitisation of housing loan mortgages.

Transaction Legal Risk represents the possibility that some of the fundamental

legal assumptions in the transaction are proved invalid. For example, a court may

disregard the SPV’s title over the receivables recharacterising the whole

transaction as a financial transaction. Or, the SPV may be consolidated with the

originator, and so on.

26

SECURITISATION – A TOOL TO MODERN FINANCING.

Tax uncertainties may sometimes affect the investors. If the SPV is liable to entity

level taxes and payments to investors are treated as payment to equity holders, the

entire cash flows in the transaction may be subjected to unprecedented taxes.

Sometimes, the underlying cash flows may be subjected to a withholding tax

requirement. These are risks that concern the investors, and they need to study

these risks carefully.

27

SECURITISATION – A TOOL TO MODERN FINANCING.

PARTIES TO SECURITISATION

The number of players in the securitisation process is large. They can be grouped

in two categories the ‘main players’ and the ‘facilitators’. The main players and

their role are as follows –

1. The SPV

‘Special Purpose Vehicle’ (SPV) is a legal entity in the form of a trust or company

created for the purpose of securitisation. By its very nature, an SPV must be

distanced from the sponsor both in terms of management and ownership, because

if the SPV were to be owned or controlled by the sponsor, there is no difference

between a subsidiary and an SPV. It buys assets (loans / receivables etc.) from

originator and packages them into security for further sale to investors. In

securitisation, one of the primary concerns of participants is to ensure non-

bankruptcy of the SPV. In order to make SPV bankruptcy proof its registration net

worth, corporate governance requirements are specified.

2. The Originator

The ‘Originator’ is an entity owning the financial assets that are the subject matter

of securitisation. Originator is normally making loans to borrowers or is having

receivables from customers. It is the originator who initiates the process for

securitisation and is the major beneficiary of it. Only banks and financial

institutions can securitize their financial assets thereby restricting the Originators

of securitisation. So, it may not be possible to securitize assets and receivables of

other business entities having such assets and receivables from credit card, export

earnings, sale of tickets, car rentals, electricity and telephone bill etc. within the

parameters of the Act.

28

SECURITISATION – A TOOL TO MODERN FINANCING.

3. The Investor

The ‘Investor’ is the entity buying the securitized instrument. Principally, large

and sophisticated institutional investors, such as Private pension funds, Credit

unions, Government pension funds, Insurance companies, Government agencies,

Money market funds, Banks, Mutual funds, Bank trust departments. This is a new

product only big investors informed and capable of taking risk shall be allowed to

invest in it.

4. The obligor(s)

The ‘Obligor’ (borrower) takes the loan or uses some service of the originator that

he has to return. His debt and collateral constitutes the underlying financial asset

of securitisation.

5. The Rating agency

Credit Rating Agency provides rating to the securitized instrument and thus

provides value addition to security.

6. Receiving and Paying Agent

Receiving and Paying Agent is the entity responsible for collecting periodic payment

from obligors and paying it to investors. Normally, the originator performs this activity.

7. Agent and Trustee

The Trustee acts on behalf of the investors and has priority interest in the financial

asset supporting the securitized product. Trustee oversee the performance of other

parties involved in securitisation transaction, review periodic information on the

status of the pool, superintend the distribution of the cash flow to the investors and

29

SECURITISATION – A TOOL TO MODERN FINANCING.

if necessary declare the issue in default and take legal action necessary to protect

investors interest.

8. Facilitators

Facilitators play a very crucial role in the securitisation chain. Their services are

instrumental in enhancing the credit worthiness of the product which is one of the prime

reasons apart from collateral for the run away success of securitized products.

30

SECURITISATION – A TOOL TO MODERN FINANCING.

TYPES OF ASSETS THAT CAN BE SECURITISED

Any asset having a cash flow profile over a period of time can be securitized.

Some of the assets which may be securitised are housing loans, car loans, term

loans, export credits, and future receivables like credit card payments, toll

collections from roads or bridges, and sales of petroleum-based products from oil

refineries, ticket sales, album sales, car rentals, electricity and telephone bill

receivables etc. In fact, artists have even raised funds by securitizing the royalty

they will get out of future sales of their records. For example, David Bowie

securitized royalties from his music catalogue. Thus, any present or future

receivables in part or in whole can be securitised.

The most readily securitizable assets are those which display the following

characteristics:

Predictable cash flows;

Isolation from the Originator.

Consistently low delinquency and default experience;

Total amortization of principal at maturity;

Many demographically and geographically diverse obligors; and

Underlying collateral with high liquidation value and utility to the obligors.

31

SECURITISATION – A TOOL TO MODERN FINANCING.

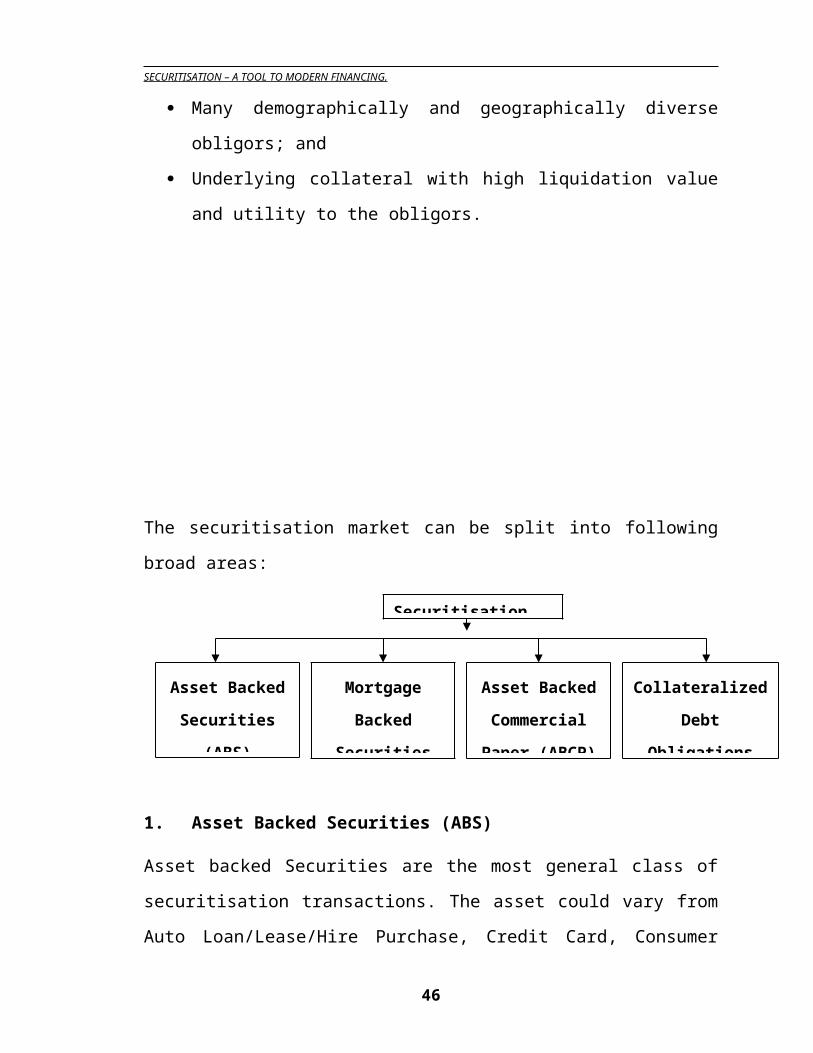

The securitisation market can be split into following broad areas:

1. Asset Backed Securities (ABS)

Asset backed Securities are the most general class of securitisation transactions.

The asset could vary from Auto Loan/Lease/Hire Purchase, Credit Card,

Consumer loan, student loan, healthcare receivables and ticket receivables to even

future asset receivables.

2. Mortgage Backed Securities (MBS, RMBS, CMBS)

MBS constitutes about 76% of the securitized debt market in the US. In contrast,

the MBS market in India is nascent - National Housing Bank (NHB), in

partnership with HDFC and LIC Housing Finance, issued India’s first MBS.

3. Asset Backed Commercial Paper (ABCP)

Asset Backed Commercial Paper (ABCP) is usually issued by Special Purpose Entities

(ABCP Conduits) set up and administered by banks to raise cheaper finances for their

clients. ABCP conduits are usually ongoing concerns with new CP issuances taking out

the previous ones. Apart from legal requirements, an active ABCP market requires a

large number of investors who understand the instrument and have appetite. India’s

securitisation market may not be mature currently for instruments like ABCPs.

32

Securitisation Market

Asset Backed

Securities (ABS)

Mortgage Backed

Securities (MBS,

RMBS, CMBS)

Asset Backed

Commercial

Paper (ABCP)

Collateralized Debt

Obligations (CDO,

CLO, CBO)

SECURITISATION – A TOOL TO MODERN FINANCING.

4. Collateralized Debt Obligations (CDO, CLO, CBO)

In this era of bank consolidations, CDOs can help banks to proactively manage

their portfolio. CDOs can also help banks in restructuring their stressed assets.

ICICI made an aborted attempt to do a CBO issuance in August 2000. The CDO

market in India is, however, likely to grow slowly owing to its complexities. The

taxation and accounting treatment for CDOs needs to be clarified.

33

SECURITISATION – A TOOL TO MODERN FINANCING.

THE INDIAN EXPERIENCE

SECURITISATION IN INDIA

While there has been a lot of discussion about the potential of securitisation in

India, actual deal activity has not kept pace. While some early adopters like ICICI,

TELCO and Citibank have been actively pursuing securitisation, almost all the

transactions in the market so far have been privately placed with a majority of

them being bilateral fully bought out deals.

Lack of appropriate legislation and legal clarity, unclear accounting treatment,

high incidence of stamp duties making transactions unviable, lack of

understanding of the instrument amongst investors, originators and, till recently,

even rating agencies are some of the glaring reasons for the lack of activity in the

area of securitisation in India.

In India By Securitisation bill parties which are allowed to securitise assets

are Banks, FIs & NBFCs

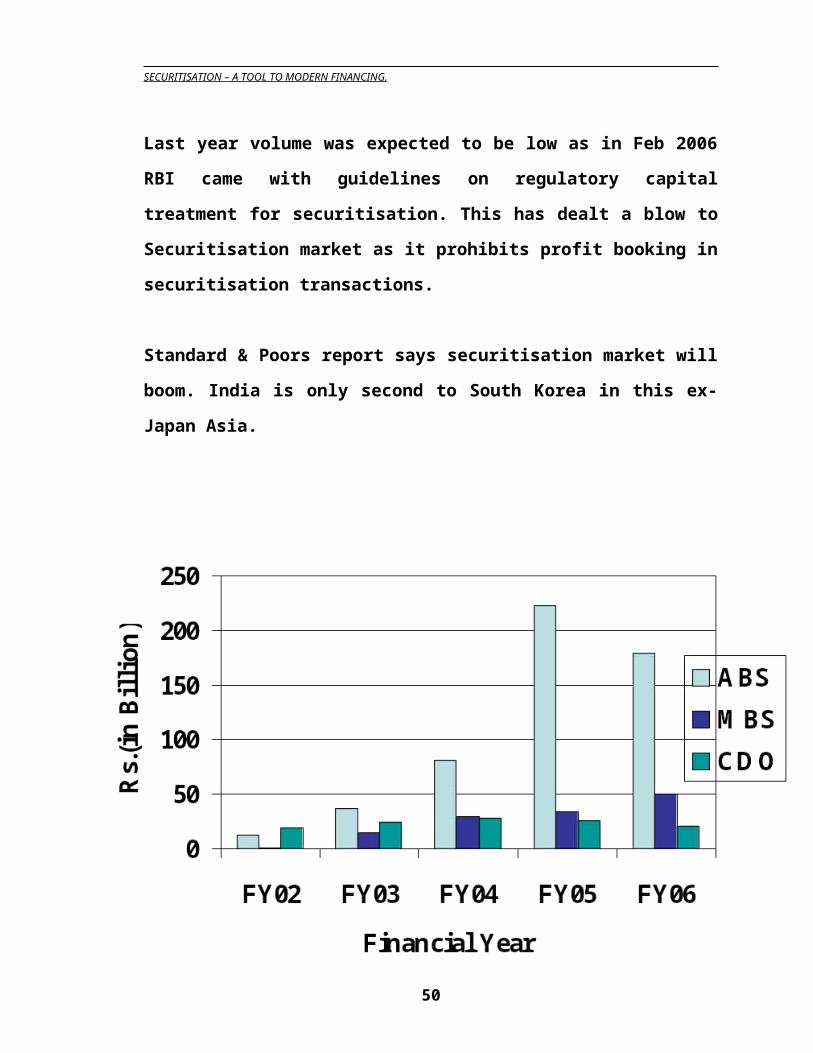

Last year volume was expected to be low as in Feb 2006 RBI came with

guidelines on regulatory capital treatment for securitisation. This has dealt a

blow to Securitisation market as it prohibits profit booking in securitisation

transactions.

Standard & Poors report says securitisation market will boom. India is only

second to South Korea in this ex-Japan Asia.

34

SECURITISATION – A TOOL TO MODERN FINANCING.

35

SECURITISATION – A TOOL TO MODERN FINANCING.

Need for Securitisation in India

The generic benefits of securitisation for Originators and investors have been

discussed above. In the Indian context, securitisation is the only ray of hope for

funding resource starved infrastructure sectors like Power. For power utilities

burdened with delinquent receivables from state electricity boards (SEBs),

securitisation seems to be the only hope of meeting resource requirements. As on

December 31, 1998, overall SEB dues only to the central agencies were over Rs.

184 billion.

Securitisation can help Indian borrowers with international assets in piercing the

sovereign rating and placing an investment grade structure. An example, albeit

failed, is that of Air India’s aborted attempt to securitize its North American ticket

receivables. Such structured transactions can help premier corporates to obtain a

superior pricing than a borrowing based on their non-investment grade corporate

rating.

A market for Mortgage backed Securities (MBS) in India can help large Indian

housing finance companies (HFCs) in churning their portfolios and focus on

what they know best – fresh asset origination. Indian HFCs have traditionally

relied on bond finance and loans from the National Housing Bank (NHB). MBS

can provide a vital source of funds for the HFCs. After the merger of India’s

largest financial institution ICICI with ICICI Bank, ICICI, faced with SLR and

other requirements, is actively seeking to launch a CLO to reduce its overall asset

exposure. It appears to be only a matter of time before other Public Financial

Institutions merge with other banks. Such mergers would result in the need for

more CDOs in the foreseeable future.

36

SECURITISATION – A TOOL TO MODERN FINANCING.

MAJOR CONSTRAINTS OF SECURITISATION IN INDIA

The Obstacles & Policy recommendations

1) Lack of appropriate legislation

Though THE SECURITISATION AND RECONSTRUCTION OF FINANCIAL ASSETS AND ENFORCEMENT OF SECURITY INTEREST ACT, 2002 has given the much needed relief in terms of a law framed for securitisation transactions. The following are the key areas where legislation is required:

a) True Sale (Isolation from bankruptcy of the Originator)

The central idea of a securitisation transaction is to isolate the assets of the

Originator from Originator’s balance sheet and seek a higher credit rating than the

Originator’s own rating. A key requirement for that is to achieve a “true sale” of

the assets to the Special Purpose Entity.

b) Tax neutral bankruptcy remote SPE

The special purpose entity that buys assets from the Originator should be a

bankruptcy remote conduit for distributing the income from the assets to the

investors. While banks have experimented with company revocable trust and

mutual fund structures, no clear vehicle has emerged for performing securitisation.

This should be addressed by the Securitisation act.

c) Stamp Duties

Stamp Duty is a state subject in India. Stamp Duties on transfer of assets in

securitisation can often make a transaction unviable. While five Indian states have

recognized the special nature of securitisation transactions and have reduced the

stamp duties for them, other states still operate at stamp duties as high as 10% for

transfer of secured receivables. The Working Group of RBI has recommended a

uniform rate of 0.1% duty on all transactions. The acceptance of these

37

SECURITISATION – A TOOL TO MODERN FINANCING.

recommendations by other states can boost the securitisation activity in India

especially in the MBS area.

d) Taxation & Accounting

At present there are no special laws governing recognition of income of various

entities in a securitisation transaction. Certain trust SPE structures actually can

result in double taxation and make a transaction unviable. The Securitisation Act,

when it comes to force, should address all taxation matters relating to

securitisation. Securitisation legislation should also specify requirements for off

balance sheet treatment for securitisation and regulatory capital requirements for

Originator and Investors.

e) Eligibility

Only recently Mutual funds have been allowed to invest in PTCs. The government

should lay down norms governing investment eligibility for various securitisation

instruments.

2) Debt market

Lack of a sophisticated debt market is always a drawback for securitisation for

lack of benchmark yield curve for pricing. The appetite for long ended exposures

(above 10 years) is very low in the Indian debt market requiring the Originator to

subscribe to the bulk of the long ended portion of the financial flows. The

development of the Indian debt market would naturally increase the securitisation

activity in India.

3) Lack of Investor Appetite

Investor awareness and understanding of securitisation is very low. RBI, key

drivers of securitisation in India like ICICI and Citibank and rating agencies like

CRISIL and ICRA should actively educate corporate investors about

38

SECURITISATION – A TOOL TO MODERN FINANCING.

securitisation. Mandatory rating of all structured obligations would also give

investors much needed assurance about transactions. Once the private placement

market for securitized paper gathers momentum, public retail securitisation

issuances would become a possibility.

39

SECURITISATION – A TOOL TO MODERN FINANCING.

FUTURE PROSPECTS OF SECURITISATION IN

INDIA

A big boost for securitisation has been the introduction of the `Securitisation and

Reconstruction of Financial Assets And Enforcement of Security Interest

Ordinance 2002’ that was promulgated in May, has given a more acceptability to

this product.

With the Ordinance, securitisation as an activity has got a legal status and now it is

possible to define securitisation under the laws of the land. Its very existence will

change the boisterous and evading attitude of the commercial dealers and

defaulters in our economy

The traditional drivers of securitisation have seen the desire of the issuer to raise

funds without adding to borrowings. This helped companies which had high debt

equity ratio. The motivating factor in some securitisation transaction in the past

was the ability to book profits upfront. While these could continue to be the

drivers demanded for securitisation. Securitisation is likely to be increasingly used

for better asset liability management. As securitisation replaces long to medium

term assets by cash, the weightage average maturity of assets of the company

comes down. This is a big comfort, as typically, NBFCs were funding three-year

assets with one year fixed deposits. Further, the NBFCs, which are required to

bring down the excess deposit level, could use the proceeds of securitisation to

retire the fixed deposits.

Traditionally in the fund based business segment of the financial services sector in

India, a single entity was engaged in the entire gamut of activities viz raising

funds, locating borrowers, credit appraisal of the borrowers, servicing of the loans

and recovery. Owing to the rapidly changing environment, some kind of

40

SECURITISATION – A TOOL TO MODERN FINANCING.

realignment is likely to happen in this sector. One could see some specializations

emerging in the market. In developed economies, particularly in the mortgage

market, there is a lot of specialization. Typically in these markets a single entity

could not perform more than one or two of the activities mentioned earlier. This is

also in line with the increasing emphasis on "core competence". Instead of an

entity engaging in all the activities, it makes sense to focus on a few areas where it

has competitive advantage.

The trend is already visible in the auto loan sector. Owing to many regulatory

changes, many NBFCs are finding it difficult to raise funds at competitive rates.

These NBFCs, however, have a relatively low cost distribution network in place to

originate and service loans.

On the other hand, large companies and Foreign Banks find that it is not

economical to create a large distribution network in terms of extensive branch

network across the country due to their high cost structure. However, these

companies, given their size, parent support, managerial talent and a high credit

rating have a much stronger funding capability.

Securitisation could be effectively used to combine these two complementary pool

of resources. NBFCs could originate loans and securities them and sell to large

companies. And they could use the proceeds of the sale to originate more loans

and the process could go on. The small NBFCs could continue to service the loans

which would ensure a steady flow of fee income.

While many transactions are under way in the auto loan sector, this trend has also

extended to housing sector also. In housing finance the funding required is of a

much longer tenure and thus far more difficult to rise.

41

SECURITISATION – A TOOL TO MODERN FINANCING.

BANKING AND SECURITISATION

'Banks will have to unload bad loans to Asset Reconstruction Companies by

FY2007' read a leading business newspaper headline sometime back.

The concept

In the traditional lending process, a bank makes a loan, maintaining it as an asset

on its balance sheet, collecting principal and interest, and monitoring whether

there is any deterioration in borrower's creditworthiness.

This requires a bank to hold assets (loans given) till maturity. The funds of the

bank are blocked in these loans and to meet its growing fund requirement a bank

has to raise additional funds from the market. Securitisation is a way of unlocking

these blocked funds.

Section 5 of the Securitisation and Reconstruction of Financial Assets and

Enforcement of Security Interest Act, 2002, mandates that only banks and

financial institutions can securitise their financial assets

The process and participants

Consider a bank, ABC Bank. The loans given out by this bank are its assets. Thus,

the bank has a pool of these assets on its balance sheet and so the funds of the

bank are locked up in these loans. The bank gives loans to its customers. The

customers who have taken a loan from the ABC bank are known as obligors.

To free these blocked funds the assets are transferred by the originator (the person

who holds the assets, ABC Bank in this case) to a special purpose vehicle (SPV).

42

SECURITISATION – A TOOL TO MODERN FINANCING.

The SPV is a separate entity formed exclusively for the facilitation of the

securitisation process and providing funds to the originator. The assets being

transferred to the SPV need to be homogenous in terms of the underlying asset,

maturity and risk profile.

What this means is that only one type of asset (eg: auto loans) of similar maturity

(eg: 20 to 24 months) will be bundled together for creating the securitised

instrument. The SPV will act as an intermediary which divides the assets of the

originator into marketable securities.

These securities issued by the SPV to the investors and are known as pass-

through-certificates (PTCs).The cash flows (which will include principal

repayment, interest and prepayments received ) received from the obligors are

passed onto the investors (investors who have invested in the PTCs) on a pro rata

basis once the service fees has been deducted.

The difference between rate of interest payable by the obligor and return promised

to the investor investing in PTCs is the servicing fee for the SPV.

The way the PTCs are structured the cash flows are unpredictable as there will

always be a certain percentage of obligors who won't pay up and this cannot be

known in advance. Though various steps are taken to take care of this, some

amount of risk still remains.

The investors can be banks, mutual funds, other financial institutions, government

etc. In India only qualified institutional buyers (QIBs) who posses the expertise

and the financial muscle to invest in securities market are allowed to invest in

PTCs.

Mutual funds, financial institutions (FIs), scheduled commercial banks, insurance

companies, provident funds, pension funds, state industrial development

43

SECURITISATION – A TOOL TO MODERN FINANCING.

corporations, et cetera fall under the definition of being a QIB. The reason for the

same being that since PTCs are new to the Indian market only informed big

players are capable of taking on the risk that comes with this type of investment.

In order to facilitate a wide distribution of securitised instruments, evaluation of

their quality is of utmost importance. This is carried on by rating the securitised

instrument which will acquaint the investor with the degree of risk involved.

The rating agency rates the securitised instruments on the basis of asset quality,

and not on the basis of rating of the originator. So particular transaction of

securitisation can enjoy a credit rating which is much better than that of the

originator.

High rated securitised instruments can offer low risk and higher yields to

investors. The low risk of securitised instruments is attributable to their backing by

financial assets and some credit enhancement measures like

insurance/underwriting, guarantee, etc used by the originator.

The administrator or the servicer is appointed to collect the payments from the

obligors. The servicer follows up with the defaulters and uses legal remedies

against them. In the case of ABC bank, the SPV can have a servicer to collect the

loan repayment installments from the people who have taken loan from the bank.

Normally the originator carries out this activity.

For an originator (ABC bank in the example), securitisation is an alternative to

corporate debt or equity for meeting its funding requirements. As the securitised

instruments can have a better credit rating than the company, the originator can get

funds from new investors and additional funds from existing investors at a lower

cost than debt.

44

SECURITISATION – A TOOL TO MODERN FINANCING.

Impact on banks

Other than freeing up the blocked assets of banks, securitisation can transform

banking in other ways as well.

The growth in credit off take of banks has been the second highest in the last 55

years. But at the same time the incremental credit deposit ratio for the past one-

year has been greater than one.

What this means in simple terms is that for every Rs 100 worth of deposit coming

into the system more than Rs 100 is being disbursed as credit. The growth of credit

off take though has not been matched with a growth in deposits.

So the question that arises is, with the deposit inflow being less than the credit

outflow, how are the banks funding this increased credit offtake?

Banks essentially have been selling their investments in government securities. By

selling their investments and giving out that money as loans, the banks have been

able to cater to the credit boom.

This form of funding credit growth cannot continue forever, primarily because

banks have to maintain an investment to the tune of 25 per cent of the net bank

deposits in statutory liquidity ratio (SLR) instruments (government and semi

government securities).

The fact that they have been selling government paper to fund credit off take

means that their investment in government paper has been declining. Once the

banks reach this level of 25 per cent, they cannot sell any more government

securities to generate liquidity.

45

SECURITISATION – A TOOL TO MODERN FINANCING.

And given the pace of credit off take, some banks could reach this level very fast.

So banks, in order to keep giving credit, need to ensure that more deposits keep

coming in.

One way is obviously to increase interest rates. Another way is Securitisation.

Banks can securitise the loans they have given out and use the money brought in

by this to give out more credit.

Not only this, securitisation also helps banks to sell off their bad loans (NPAs or

non performing assets) to asset reconstruction companies (ARCs). ARCs, which

are typically publicly/government owned, act as debt aggregators and are engaged

in acquiring bad loans from the banks at a discounted price, thereby helping banks

to focus on core activities.

On acquiring bad loans ARCs restructure them and sell them to other investors as

PTCs, thereby freeing the banking system to focus on normal banking activities.

46

SECURITISATION – A TOOL TO MODERN FINANCING.

Impact on the Indian Banking Sector

The growth in credit off take of banks has been the second highest in the last 55

years. But at the same time the incremental credit deposit ratio for the past one-

year has been greater than one.

Asset Reconstruction Company of India Limited (ARCIL) was the first (till date

remains the only ARC) to commence business in India. ICICI Bank, Karur Vyasya

Bank, Karnataka Bank, Citicorp (I) Finance, SBI, IDBI, PNB, HDFC, HDFC

Bank and some other banks have shareholding in ARCIL.

A lot of banks have been selling off their NPAs to ARCIL. ICICI bank- the second

largest bank in India, has been the largest seller of bad loans to ARCIL last year. It

sold 134 cases worth Rs.8450 Crore. SBI and IDBI hold second and third

positions.

ARCIL is keen to see cash flush foreign funds enter the distressed debt markets to

help deepen it. What is happening right now is that banks and FIs have been

selling their NPAs to ARCIL and the same banks and FIs are picking up the PTCs

being issued by ARCIL and thus helping ARCIL to finance the purchase. A recent

report in a business daily quotes , Rajendra Kakkar, ARCIL's Chief Executive as

saying, "We have got a buyer, we have got a seller, it so happens that the seller is

the loan side of the same institutions and buyer is the treasury side."

So the risk from the balance sheet of banks and FIs is not being completely

removed as their investments into PTCs issued by ARCIL will generate returns if

and only if ARCIL is able to affect recovery from defaulters.

A recent survey by the Economist magazine on International Banking, says that

securitisation is the way to go for Indian banking.

47

SECURITISATION – A TOOL TO MODERN FINANCING.

As per the survey, "What may be more important for the economy is to provide

access for the 92% of Indian businesses that do not use bank finance. That

represents an enormous potential market for both local and foreign banks, but the

present structure of the banking system is not suitable for reaching these

businesses. Securitising micro-loans- bundling many loans together and selling the

resulting cash flow- may be the way of achieving economies of scale. One private

bank, ICICI, securitised $4.3 million of micro-loans last year. But most Indian

banks are more interested in competing for affluent customers".

48

SECURITISATION – A TOOL TO MODERN FINANCING.

Problems faced by the Banking Sector in India

1) Lack of Proper Legal Measures on part of the Govt.

In spite of various legislative measures, there are hardly any securitisation

transactions undertaken pursuant to amended legislations. The SARFAESI Act

was enacted with specific object of facilitating securitisation of healthy/standard

assets, but RBI has taken a stand that the SARFAESI Act is intended only for

dealing with stressed assets and there are no RBI regulations for standard assets.

Amendments to the SCRA Act have been done very recently and the object of the

amendments is to facilitate securitisation of financial assets by raising funds from

investors. While SCRA amendments contemplate issue of securitised debt

instruments to the pubic, the SARFAESI Act restricts issue of security receipts

only to Qualified Institutional Payers. The SARFAESI Act equates a securitisation

company with any bank or financial institution and confers powers of recovery of

defaulted loans without the intervention of the court on the securitisation

companies. The SCRA amendment, on the other hand, makes no provision for

recovery of defaulted loans by special purpose distinct entity (SPDE) and such

SPDEs are required to file suits in civil courts. The SCRA covers any kind of debt

or receivables for securitisation but SARFAESI is restricted to loans and advances.

2) Lack of Proper Legal Awareness regarding Securitisation Norms

In spite of all the legislative measures, till RBI issued directives to banks last year,

securitisation transactions were being undertaken under the general law applicable

to private trusts and the Indian Contracts Act, 1872. The RBI directives to banks

are restrictive and some constraints discouraging securitisation are:

On securitisation of financial assets, banks cannot book profits upfront and

49

SECURITISATION – A TOOL TO MODERN FINANCING.

Investors are not permitted to treat the investment in securitised debt instruments

as exposure to underlying debts.

3) Confusion and Complexities over Stamp Duty

To add to the confusion and complexities, there is a major issue of stamp duties

payable as per State laws on securitisation transaction. While some States have

reduced stamp duties on securitisation, there is no uniformity. Some have reduced

duty on housing loans securitisation while others have done it only for SARFAESI

securitisation. The Reserve Bank, SEBI and the Ministry of Finance need to take a

total view of this matter and facilitate securitisation of any assets by banks and FIs

without any impediments whether legal or regulatory. There is a need for the

Parliament to enact a comprehensive new law for securitisation of debts and

receivables, by treating assignment of debts and receivables as a new kind of

transfer of property.

Since such debt-instruments issued pursuant to securitisation have to be provided

characteristic of transferability by endorsement and delivery, the new Law can

also provide for rates of stamp duties for documents effecting assignment of debts

and receivables for securitisation and issue of debt instruments, overriding any

State Laws on stamp duties.

Conclusion

Securitisation is expected to become more popular in the near future in the

banking sector. Banks are expected to sell off a greater amount of NPAs to ARCIL

by 2007, when they have to shift to Basel-II norms. Blocking too much capital in

NPAs can reduce the capital adequacy of banks and can be a hindrance for banks

to meet the Basel-II norms.

50

SECURITISATION – A TOOL TO MODERN FINANCING.

Thus, banks will have two options- either to raise more capital or to free capital

tied up in NPAs and other loans through securitization.

51

SECURITISATION – A TOOL TO MODERN FINANCING.

Infrastructure Development

And Financing

INTRODUCTION

The availability of adequate infrastructure facilities is imperative for the overall

economic development of the country. Infrastructure adequacy helps determine

success in diversifying production, expanding trade, coping with population

growth, reducing poverty and improving environmental conditions. Today, it is

necessary to broaden one's concern from increasing the quantity of infrastructure

stocks to improving the quality of infrastructure services. In recent years, there has

been a revolution in thinking about who should be responsible for providing

infrastructure stocks and services, and how these services should be delivered to

the users.

One of the bottlenecks in infrastructure development in India is the conflict arising

out of the confusion over the government's role in being licensers for infrastructure

development, an infrastructure developer and operator, and finally a regulator. A

clear separation of these roles would be essential. To further aid this process, the

financial, insurance and legal sectors would have to play a significant role.

WHAT IS INFRASTRUCTURE?

As per India Infrastructure Report:

"Infrastructure is generally defined as the physical framework of facilities through

which goods and services are provided to public. Its linkages to the economy are

multiple and complex, because it affects production and consumption directly,

52

SECURITISATION – A TOOL TO MODERN FINANCING.

creates negative and positive spillover effects (externalities) and involves large

flow of expenditure.

Infrastructure contributes to economic development, both by increasing

productivity and by providing amenities which enhance the quality of life. The

services provided lead to growth in production in several ways:

Infrastructure services are intermediate inputs to production and any reduction in

these input costs raises the profitability of production, thus pertaining higher levels

of output, income and or employment.

These raise the productivity of other factors including labour and other capital.

Infrastructure is thus often described as an "Unpaid Factor of Production", since its

availability leads to higher obtainable from other capital and labour.

WHY IS INFRASTRUCTURE IMPORTANT?

As per India Infrastructure Report:

"The availability of adequate infrastructure facilities is imperative for the overall

economic development of the country. Infrastructure adequacy helps determine

reducing poverty and improving environmental conditions."

"Research indicates that total infrastructure stocks increase by 1% with each 1%

increment in per capita GDP."

53

SECURITISATION – A TOOL TO MODERN FINANCING.

KEY ISSUES IN INFRASTRUCTURE DEVELOPMENT

AND FINANCING

The Key issues in infrastructure development are: -

1. Privatization

The importance of privatization is because it brings along with it

a) Additional resources and

b) Improved managerial efficiency in asset creation, asset utilisation and customer

service leading to better financial health, due to stake holding.

2. Unbundling and Project Structuring

Unbundling is a necessary condition before attracting private participation is

unbundling the infrastructure into logical sub activities which can be privatised

separately to enable private parties not to have to bite more than what they can

chew.

To enable unbundling necessary acts shall have to be overhauled. Regulatory

reform would also be essential to provide increased autonomy, especially for

capital investment, even as a precursor to unbundling. Another reason for

regulatory reform is to exercise controls over implicit monopoly situations.

Project Structuring is also a key issue as since projects have to be structured small

enough to make them investment friendly, and at the same time "Commercial"

viable.

3. Project Appraisal and Financing

The key issue here is one of appraising the project against future cash flows rather

than an asset base or collaterals. Various forms of revenue, control over revenue

54

SECURITISATION – A TOOL TO MODERN FINANCING.

and risk guarantees would also be related concerns. A vital banking infrastructure

to complement all this would be essential.

4. Project Implementation

Speed of project implementation would be imperatives, in the context of

environmental and other regulatory issues.

55

SECURITISATION – A TOOL TO MODERN FINANCING.

FISCAL INCENTIVES FOR INVESTMENT IN

INFRASTRUCTURE PROJECTS

The Government of India has sought to alleviate some of these concerns/issues by

providing certain fiscal incentives, concessions and policy reforms. Some of these

reforms have been:

1. Income Tax exemptions under Section 10 (23)(g) for interest and capital gains

income earned for infrastructure projects

2. Income Tax exemptions under Section 54 (EA/EB) for capital gains which can

be reinvested in infrastructure project companies

3. Deduction under Section 88 for investment in infrastructure projects -

Deduction available for individual investors.

4. Exemption from Minimum Alternative Tax

5. Concessional import duties and port charges for project-related imports.

6. Increased limits for External Commercial Borrowings.

7. Five year tax holiday to be claimed within 12 years of operation. For the

balance years, a 30% exemption is available.

56

SECURITISATION – A TOOL TO MODERN FINANCING.

TECHNIQUE OF SECURITISATION IN

INFRASTRUCTURE FINANCING

Securitisation of wholesale assets refers mainly to the use of securitisation as a

technique for infrastructure financing. Securitisation works on the principle of

unbundling the cash flows, customizing risk and evolving superior credit structure

in Infrastructure Financing.

Securitisation will benefit infrastructure financing because it: -

1. Permits funding agencies whose sector exposures are choked, to continue

funding to those sectors.

2. Permits the participation of a much large number of investors by issue of

marketable securities.

3. Lowers the cost of funding infrastructure projects; long term funding ( a sine

quo non for most infrastructure projects) is more feasible in securitised

structures than conventional lending.