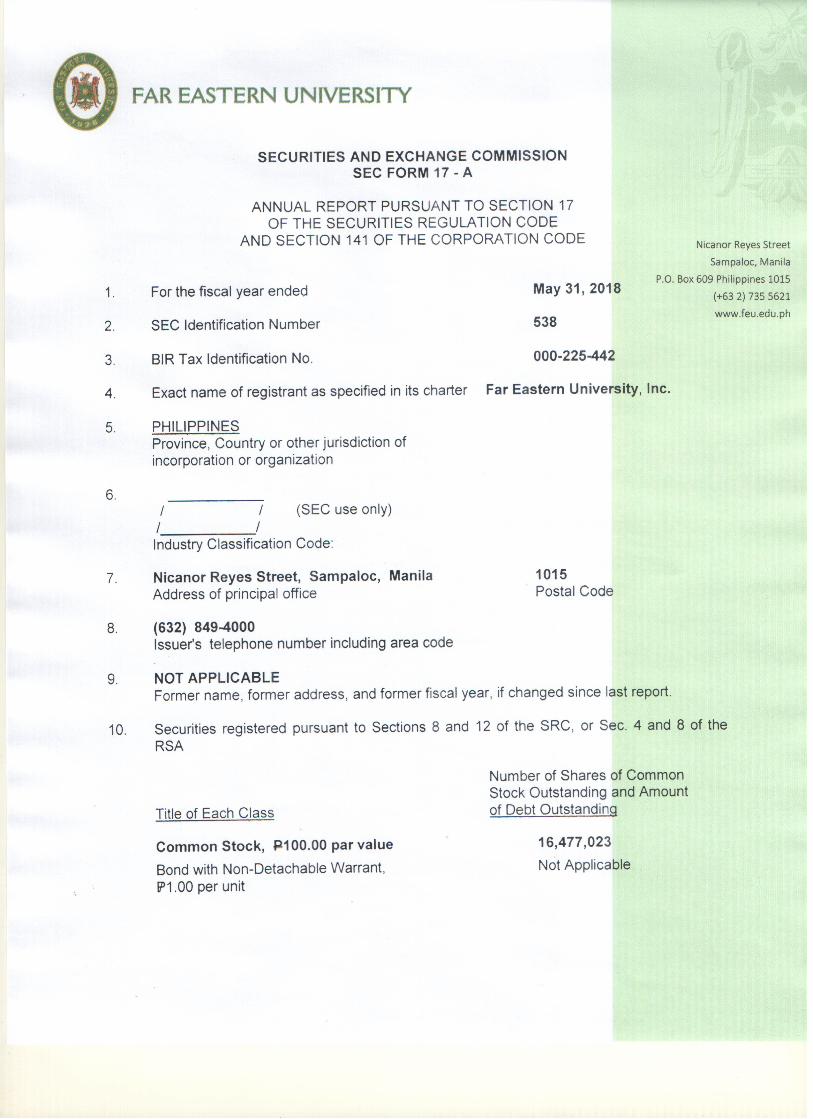

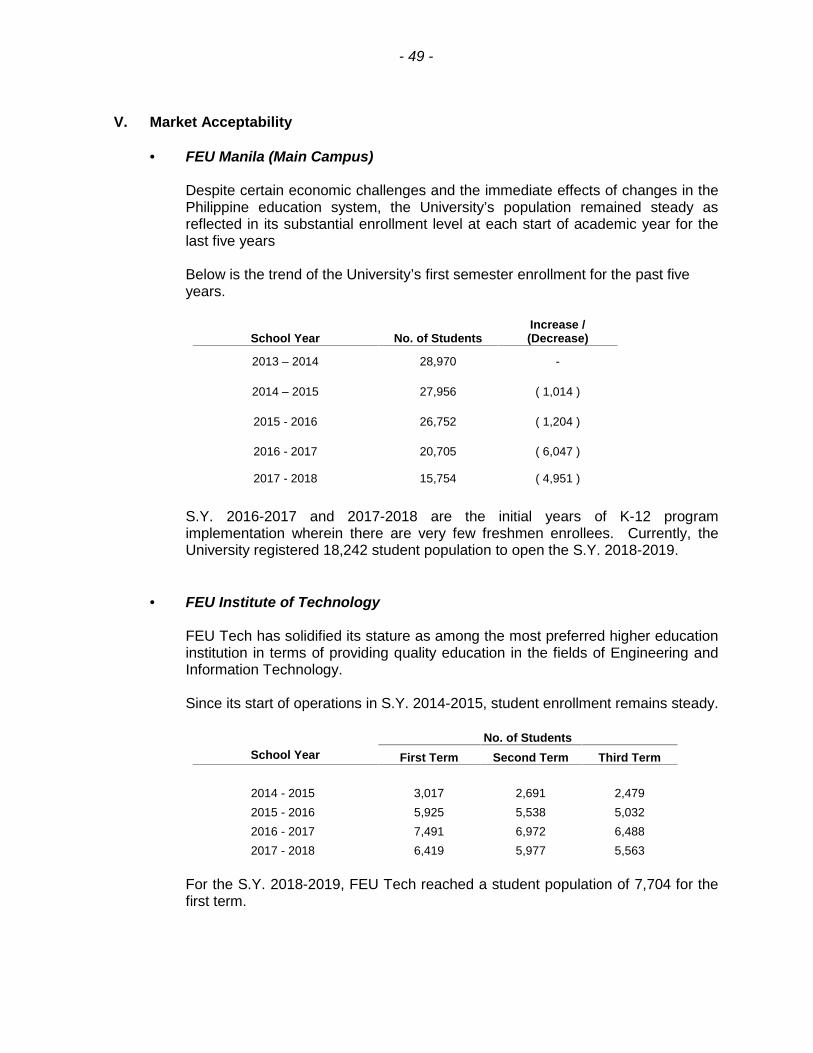

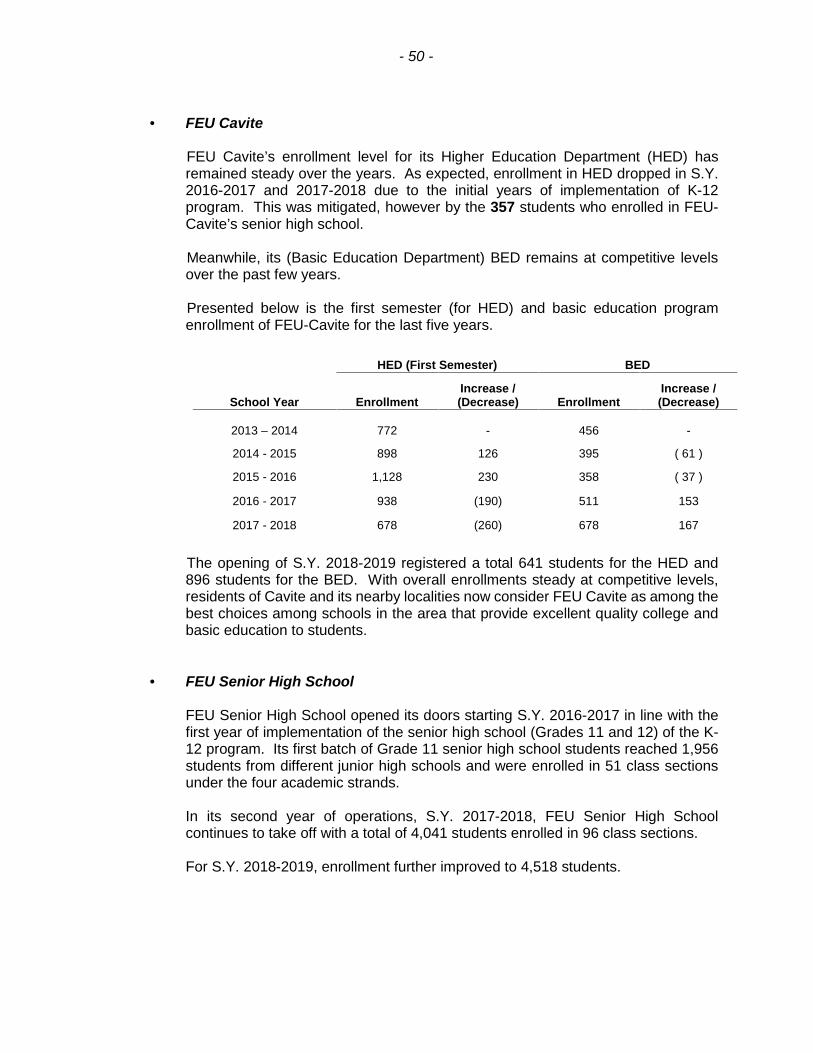

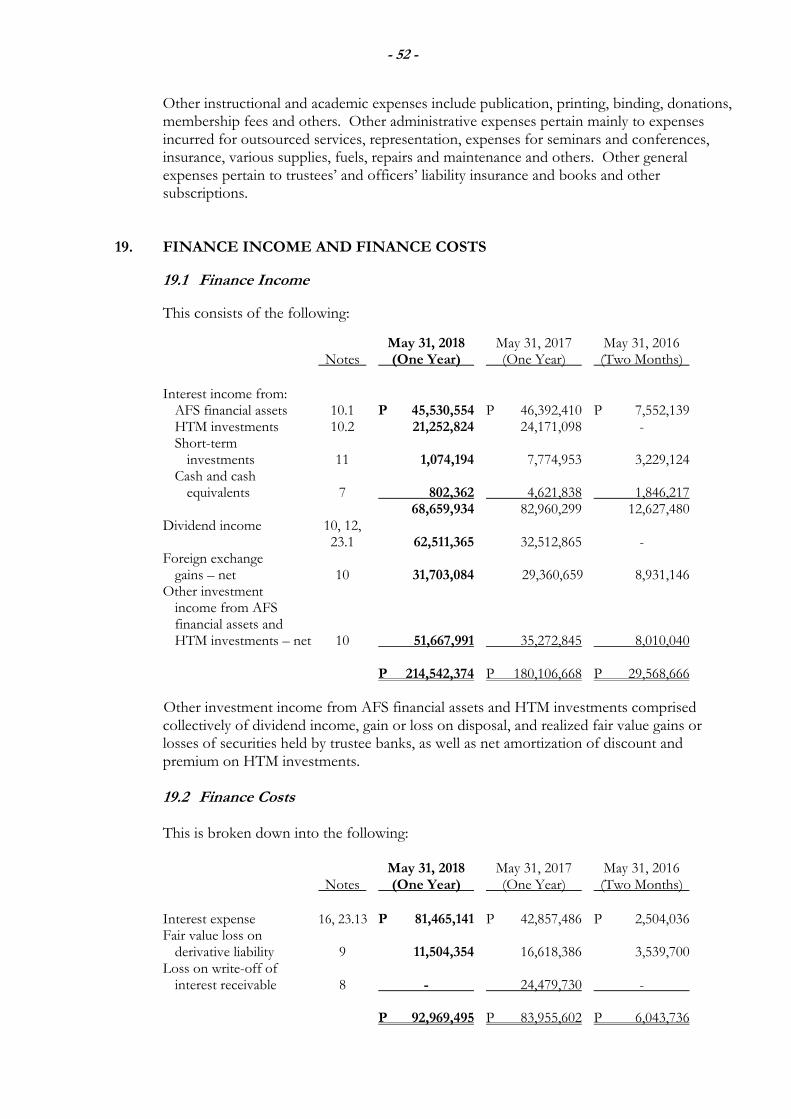

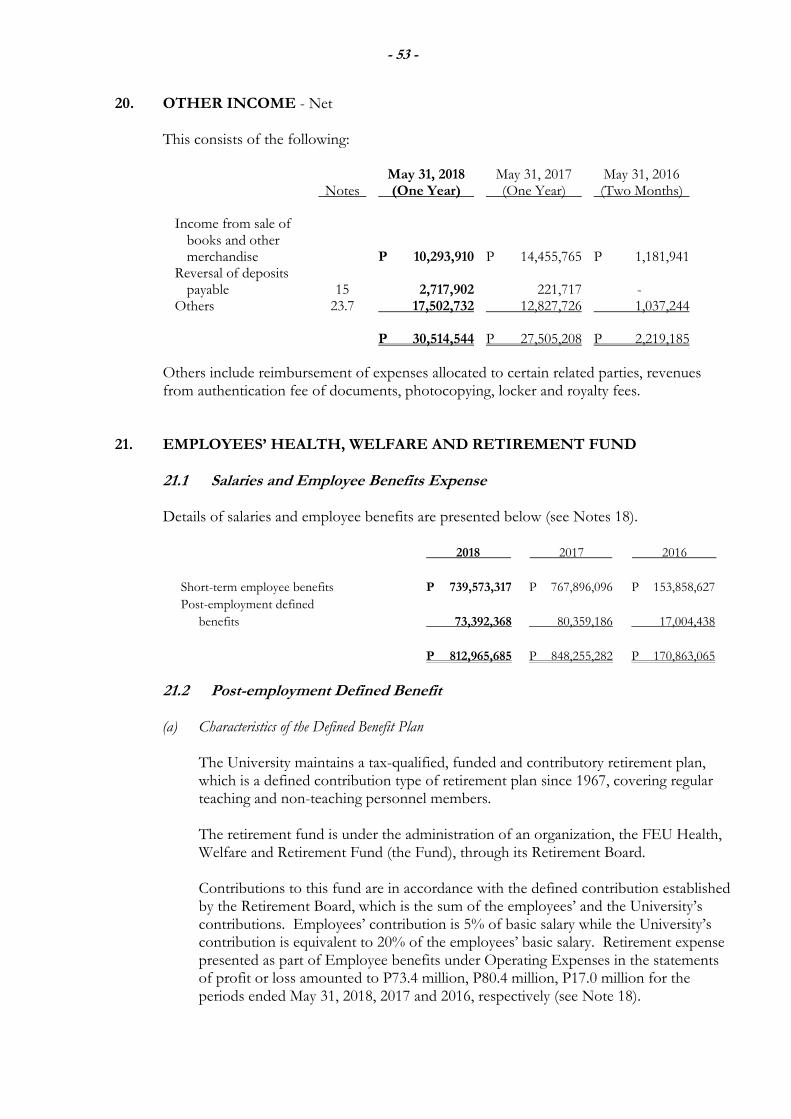

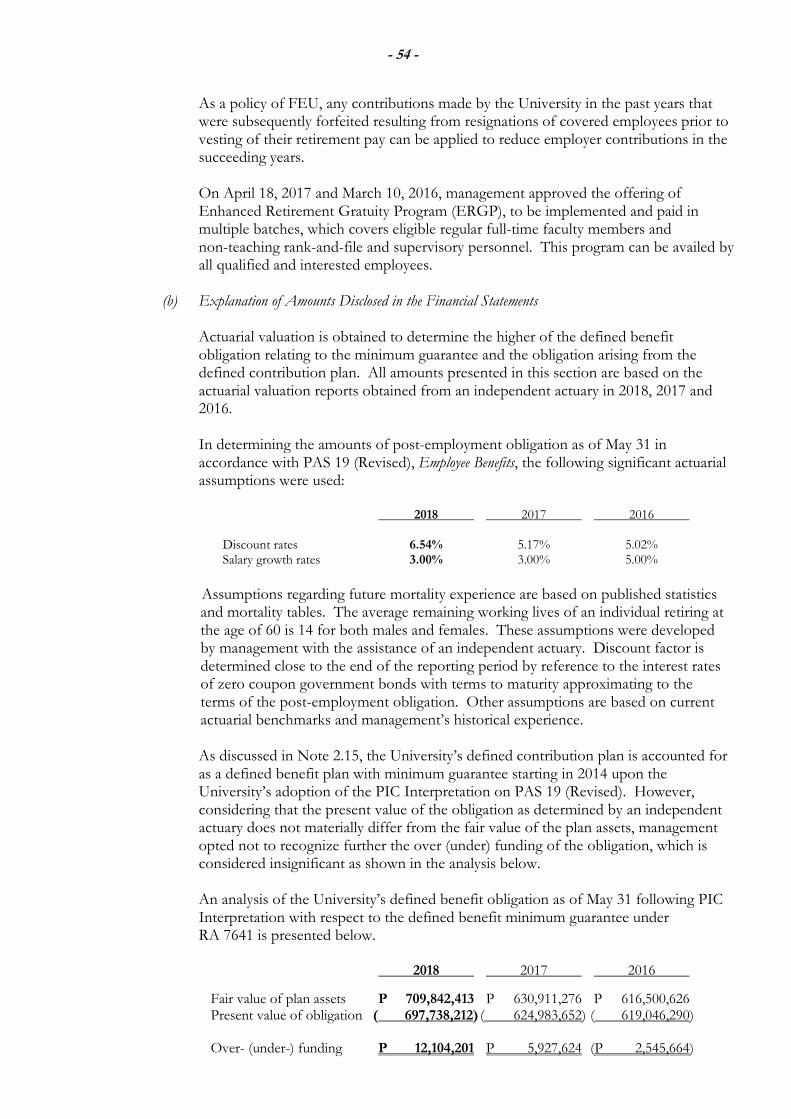

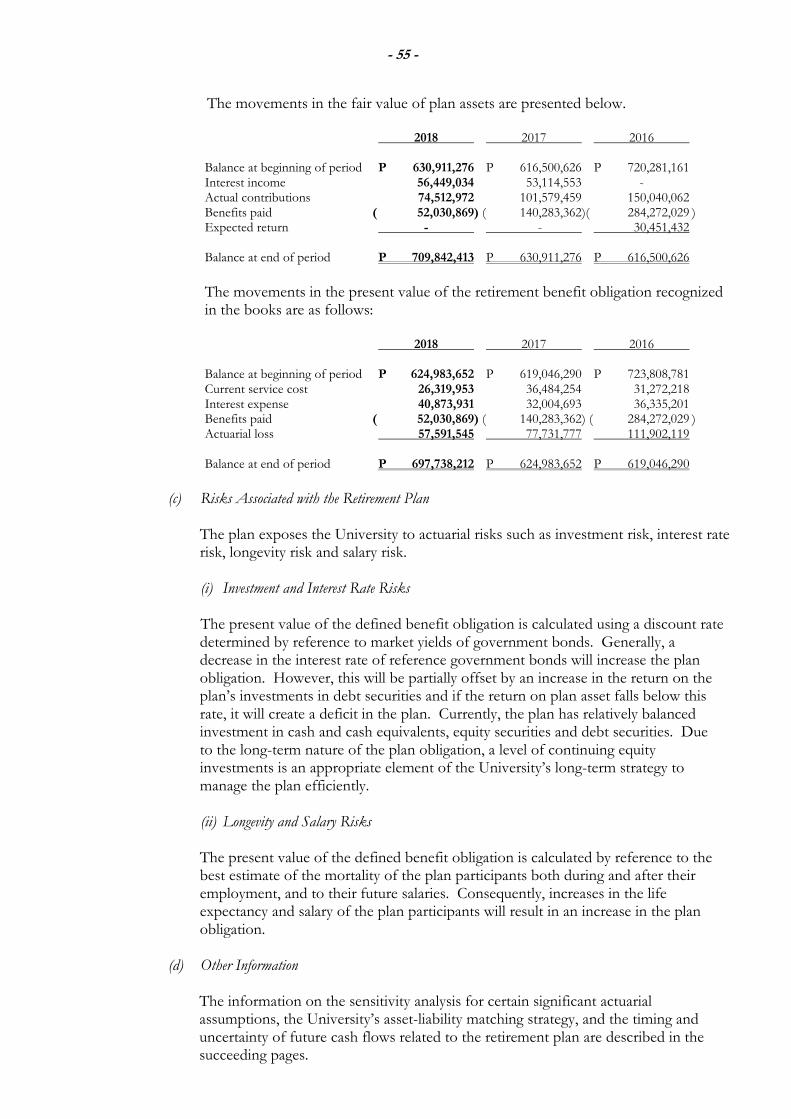

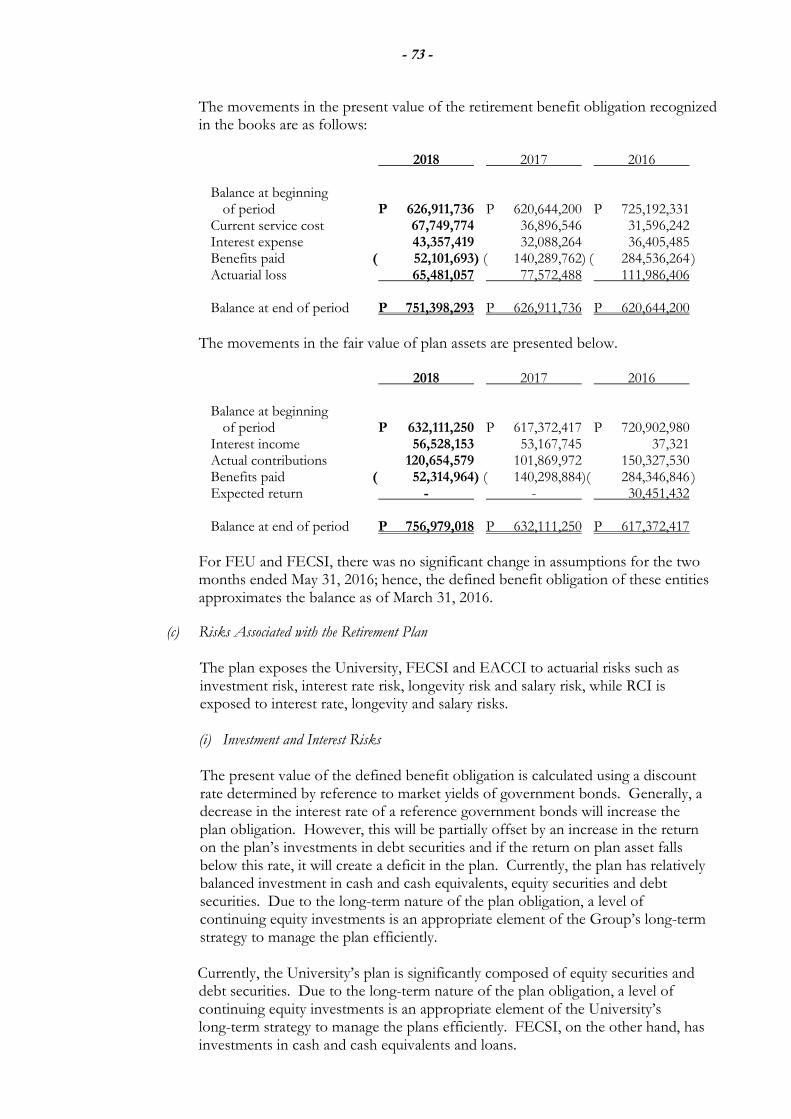

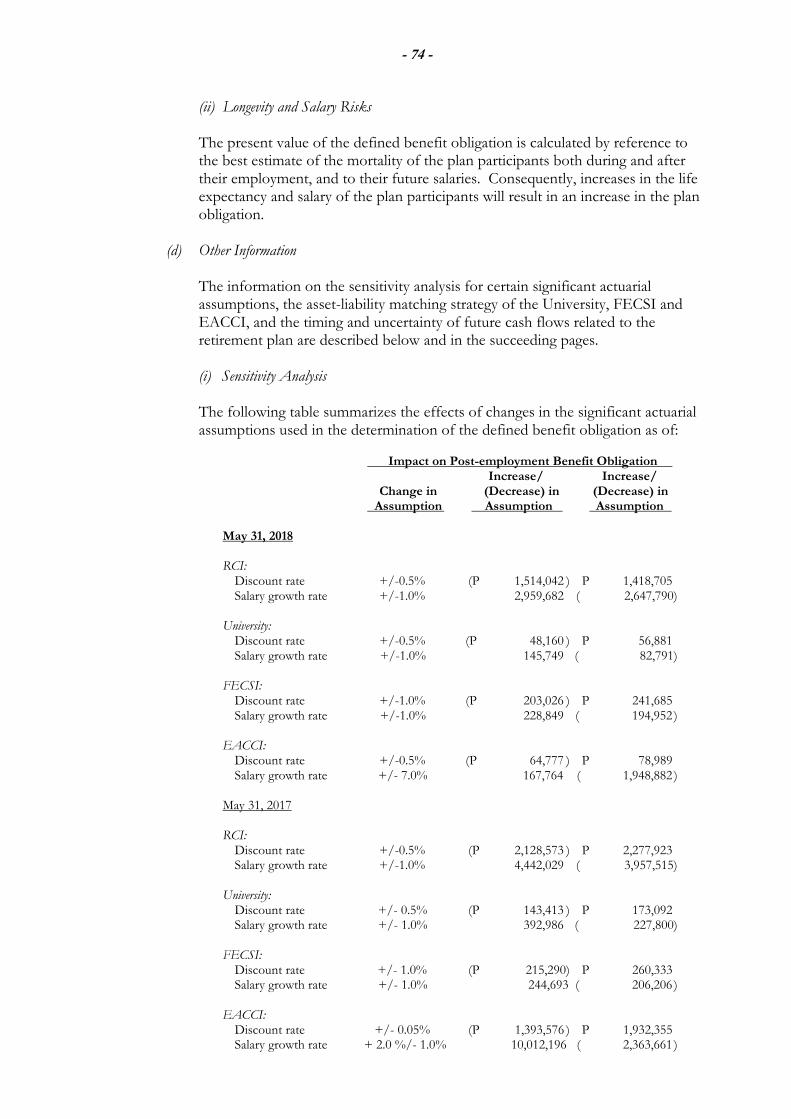

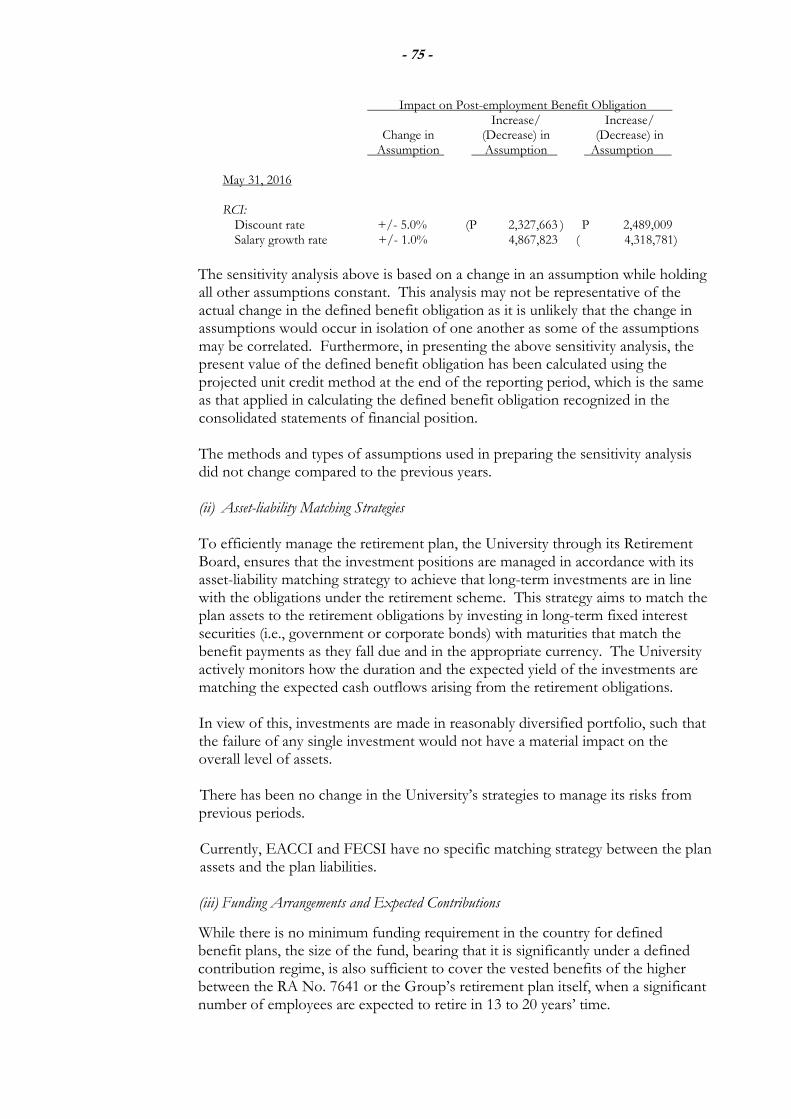

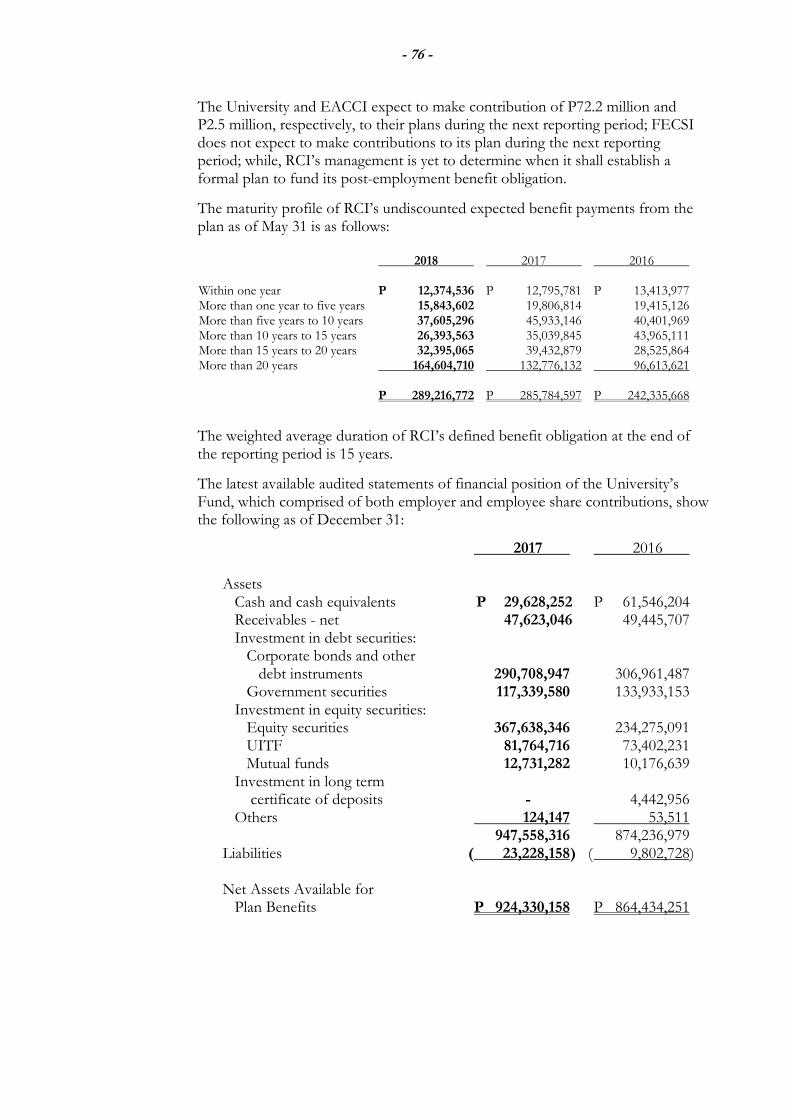

No Yes CR05818-2018 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended May 31, 2018 2. SEC Identification Number PW538 3. BIR Tax Identification No. 000-225-442 4. Exact name of issuer as specified in its charter FAR EASTERN UNIVERSITY, INC. 5. Province, country or other jurisdiction of incorporation or organization Philippines 6. Industry Classification Code(SEC Use Only) 7. Address of principal office Nicanor Reyes Street, Sampaloc, Manila Postal Code 1015 8. Issuer's telephone number, including area code (632) 849-4000 9. Former name or former address, and former fiscal year, if changed since last report - 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding COMMON 16,477,023 11. Are any or all of registrant's securities listed on a Stock Exchange? If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange, Inc. 12. Check whether the issuer:

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

No Yes

CR05818-2018

SECURITIES AND EXCHANGE COMMISSIONSEC FORM 17-A, AS AMENDED

ANNUAL REPORT PURSUANT TO SECTION 17OF THE SECURITIES REGULATION CODE AND SECTION 141

OF THE CORPORATION CODE OF THE PHILIPPINES

1. For the fiscal year ended

May 31, 20182. SEC Identification Number

PW5383. BIR Tax Identification No.

000-225-4424. Exact name of issuer as specified in its charter

FAR EASTERN UNIVERSITY, INC.5. Province, country or other jurisdiction of incorporation or organization

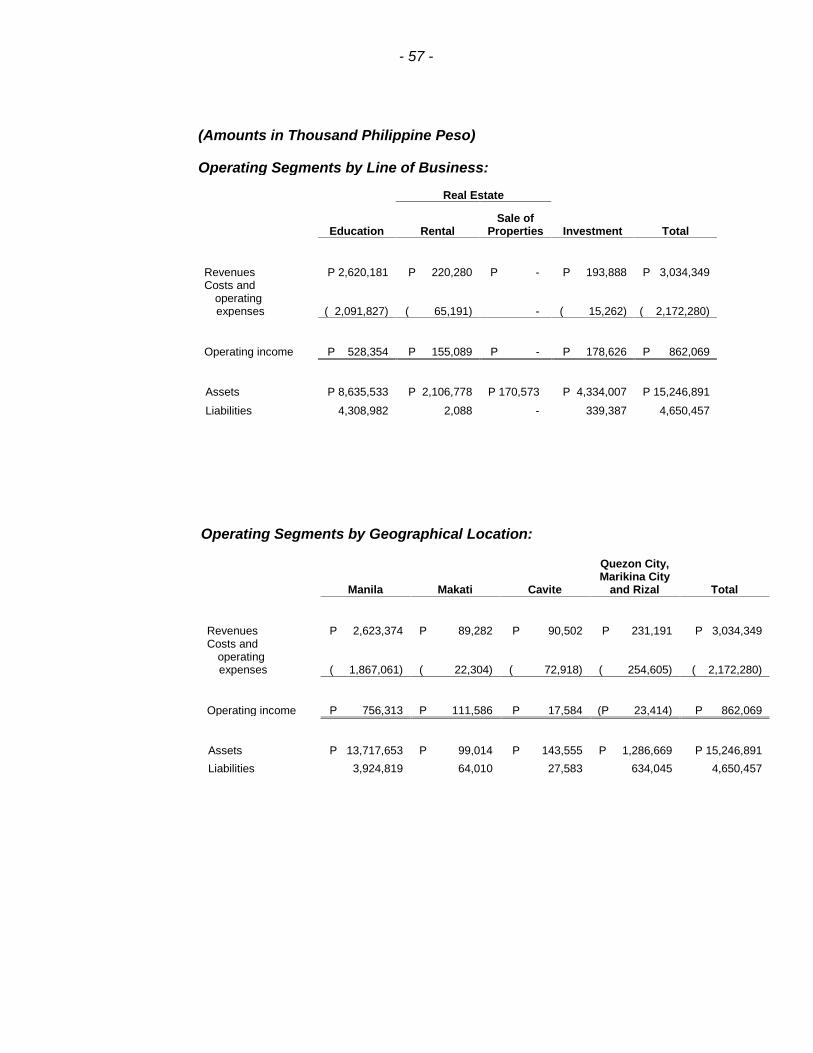

Philippines6. Industry Classification Code(SEC Use Only)

7. Address of principal office

Nicanor Reyes Street, Sampaloc, ManilaPostal Code1015

8. Issuer's telephone number, including area code

(632) 849-40009. Former name or former address, and former fiscal year, if changed since last report

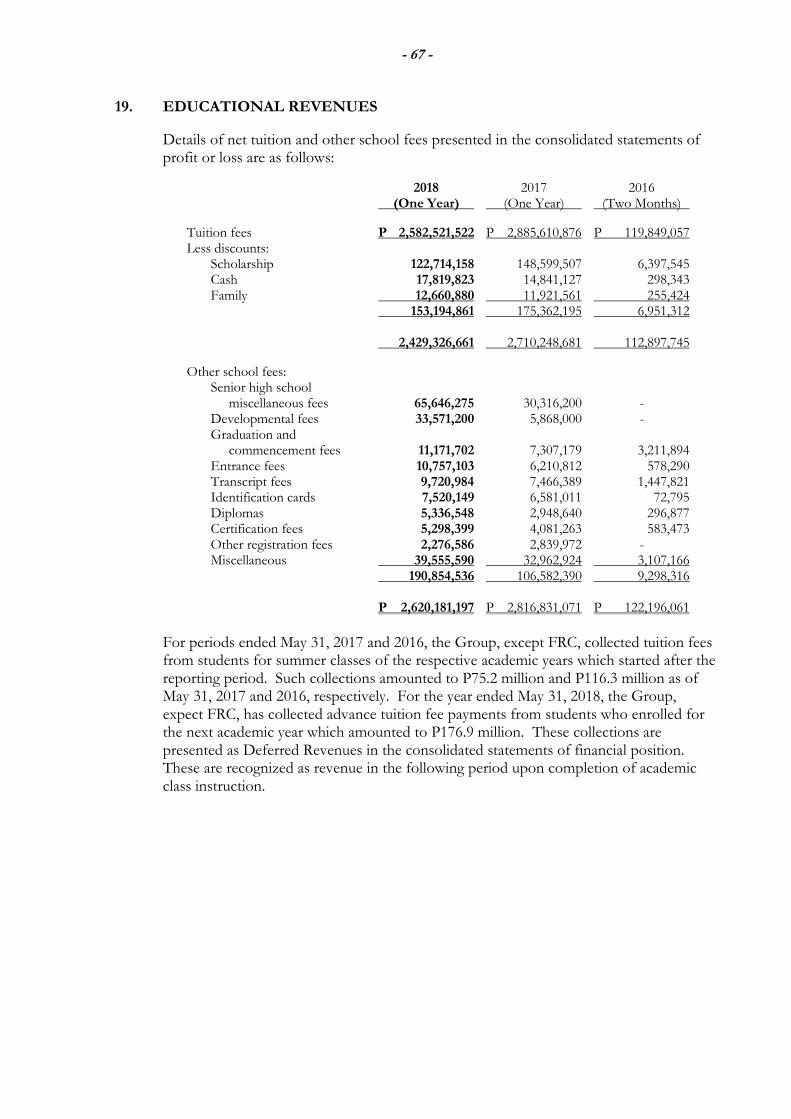

-10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA

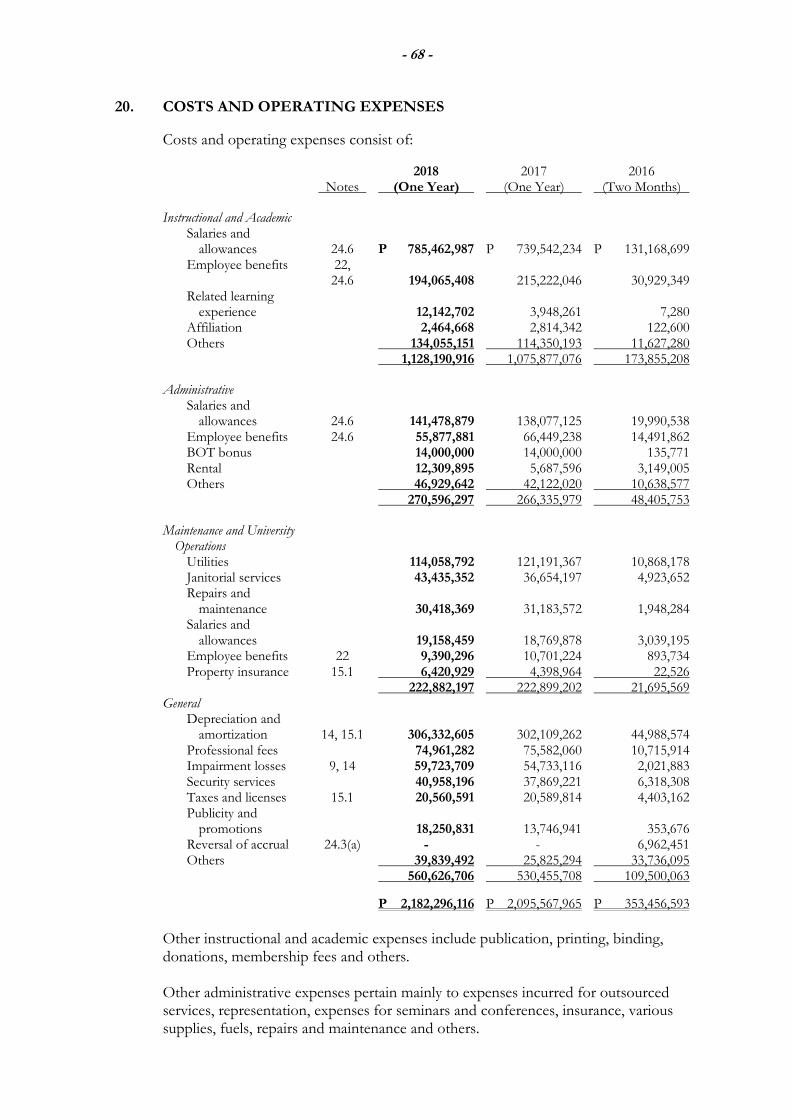

Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding

COMMON 16,477,023

11. Are any or all of registrant's securities listed on a Stock Exchange?

If yes, state the name of such stock exchange and the classes of securities listed therein:

Philippine Stock Exchange, Inc.12. Check whether the issuer:

No Yes

No Yes

No Yes

(a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141of The Corporation Code of the Philippines during the preceding twelve (12) months (or for suchshorter period that the registrant was required to file such reports)

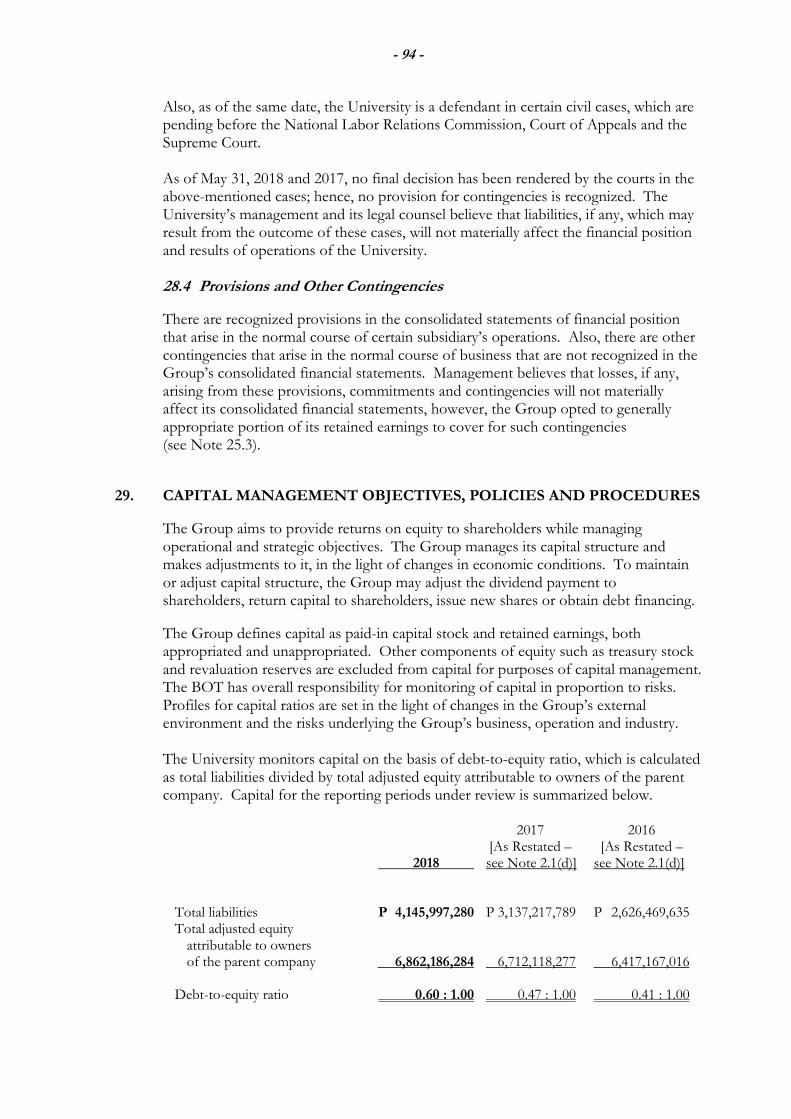

(b) has been subject to such filing requirements for the past ninety (90) days

13. State the aggregate market value of the voting stock held by non-affiliates of the registrant. Theaggregate market value shall be computed by reference to the price at which the stock was sold, orthe average bid and asked prices of such stock, as of a specified date within sixty (60) days prior tothe date of filing. If a determination as to whether a particular person or entity is an affiliate cannot bemade without involving unreasonable effort and expense, the aggregate market value of the commonstock held by non-affiliates may be calculated on the basis of assumptions reasonable under thecircumstances, provided the assumptions are set forth in this Form

None

APPLICABLE ONLY TO ISSUERS INVOLVED ININSOLVENCY SUSPENSION OF PAYMENTS PROCEEDINGS

DURING THE PRECEDING FIVE YEARS

14. Check whether the issuer has filed all documents and reports required to be filed by Section 17 ofthe Code subsequent to the distribution of securities under a plan confirmed by a court or theCommission.

DOCUMENTS INCORPORATED BY REFERENCE

15. If any of the following documents are incorporated by reference, briefly describe them and identifythe part of SEC Form 17-A into which the document is incorporated:

(a) Any annual report to security holders

N/A

(b) Any information statement filed pursuant to SRC Rule 20

N/A

(c) Any prospectus filed pursuant to SRC Rule 8.1

N/A

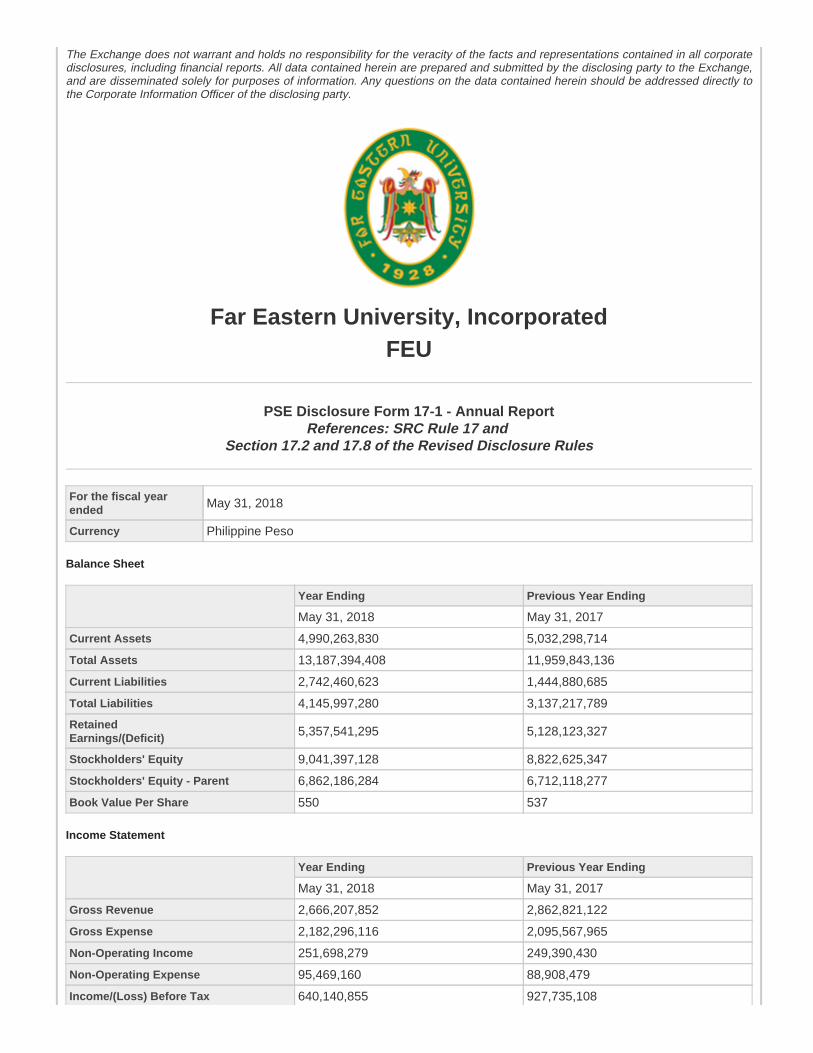

The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporatedisclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange,and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly tothe Corporate Information Officer of the disclosing party.

Far Eastern University, IncorporatedFEU

PSE Disclosure Form 17-1 - Annual ReportReferences: SRC Rule 17 and

Section 17.2 and 17.8 of the Revised Disclosure Rules

For the fiscal yearended May 31, 2018

Currency Philippine Peso

Balance Sheet

Year Ending Previous Year Ending

May 31, 2018 May 31, 2017

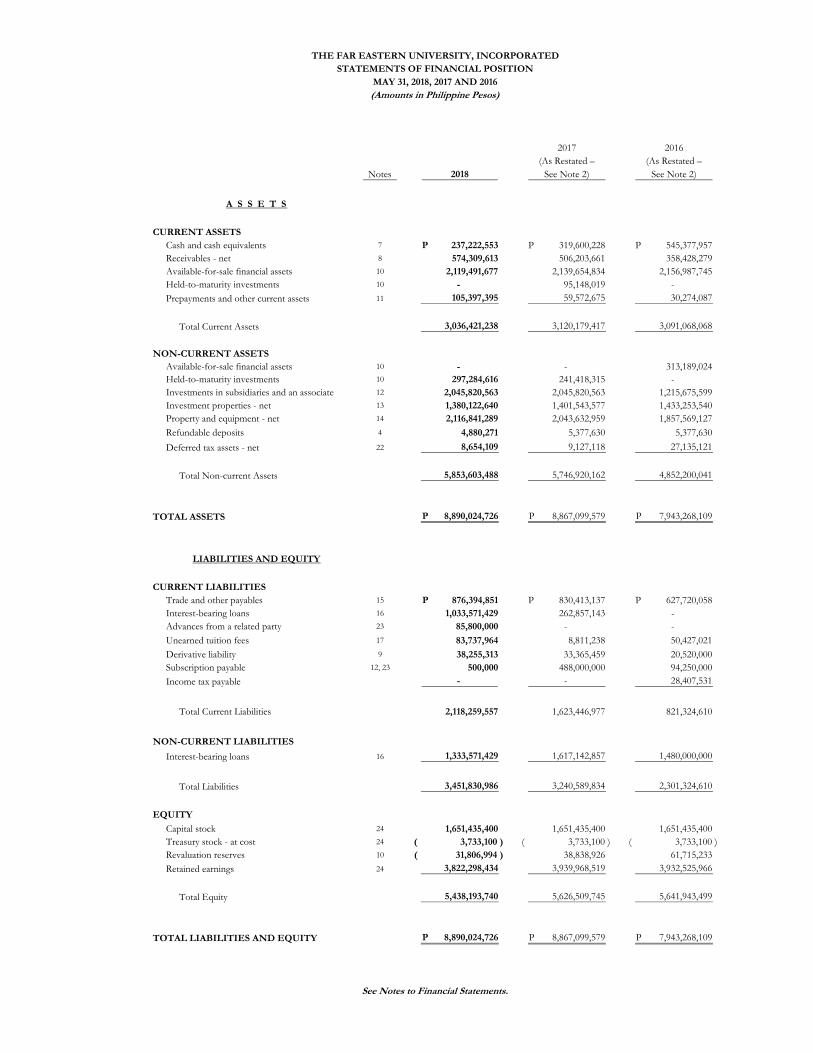

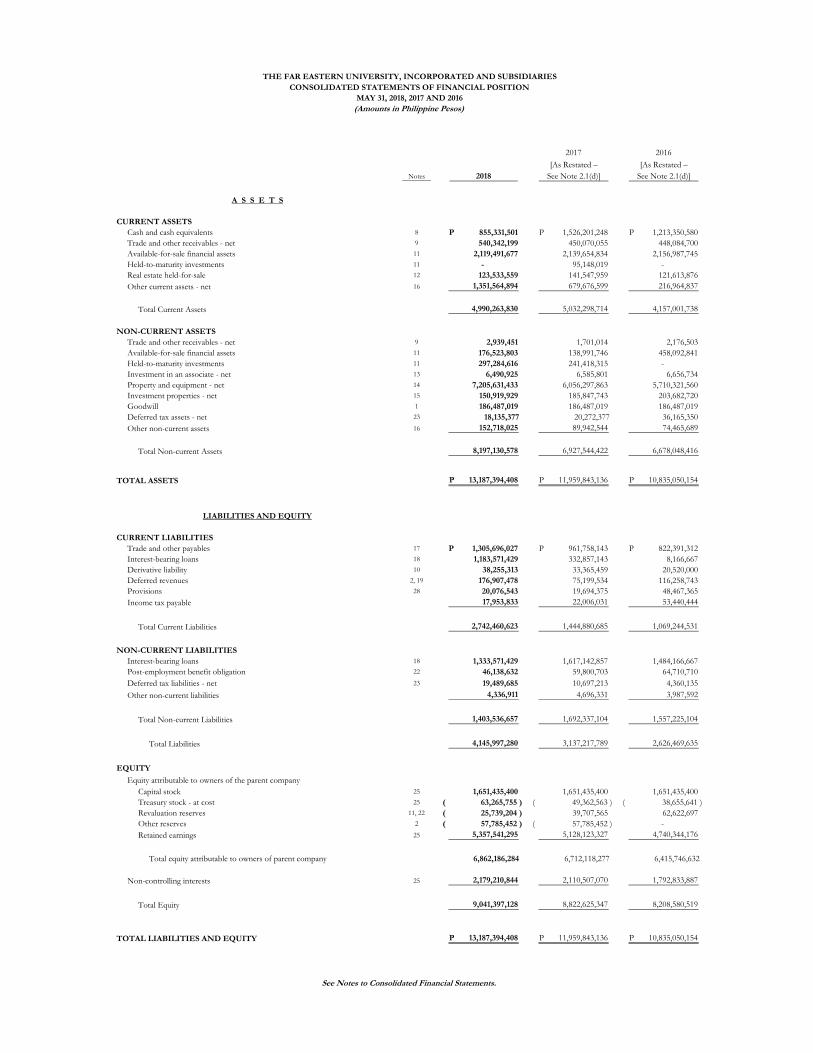

Current Assets 4,990,263,830 5,032,298,714

Total Assets 13,187,394,408 11,959,843,136

Current Liabilities 2,742,460,623 1,444,880,685

Total Liabilities 4,145,997,280 3,137,217,789

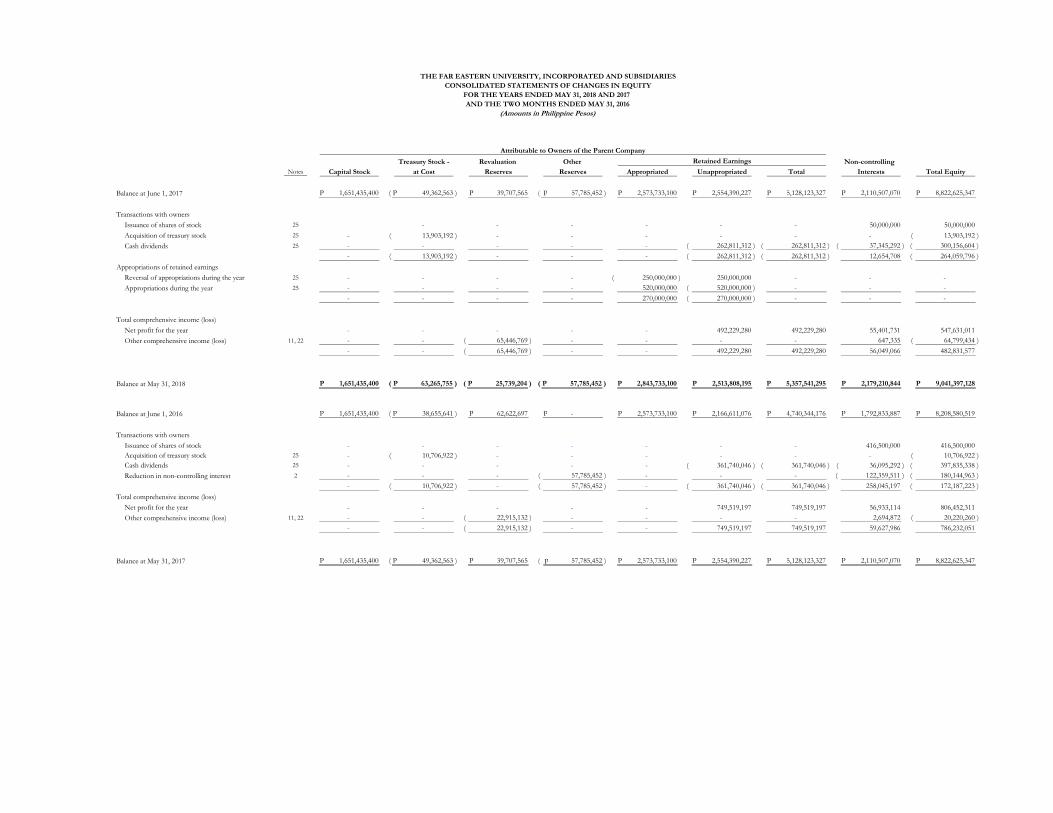

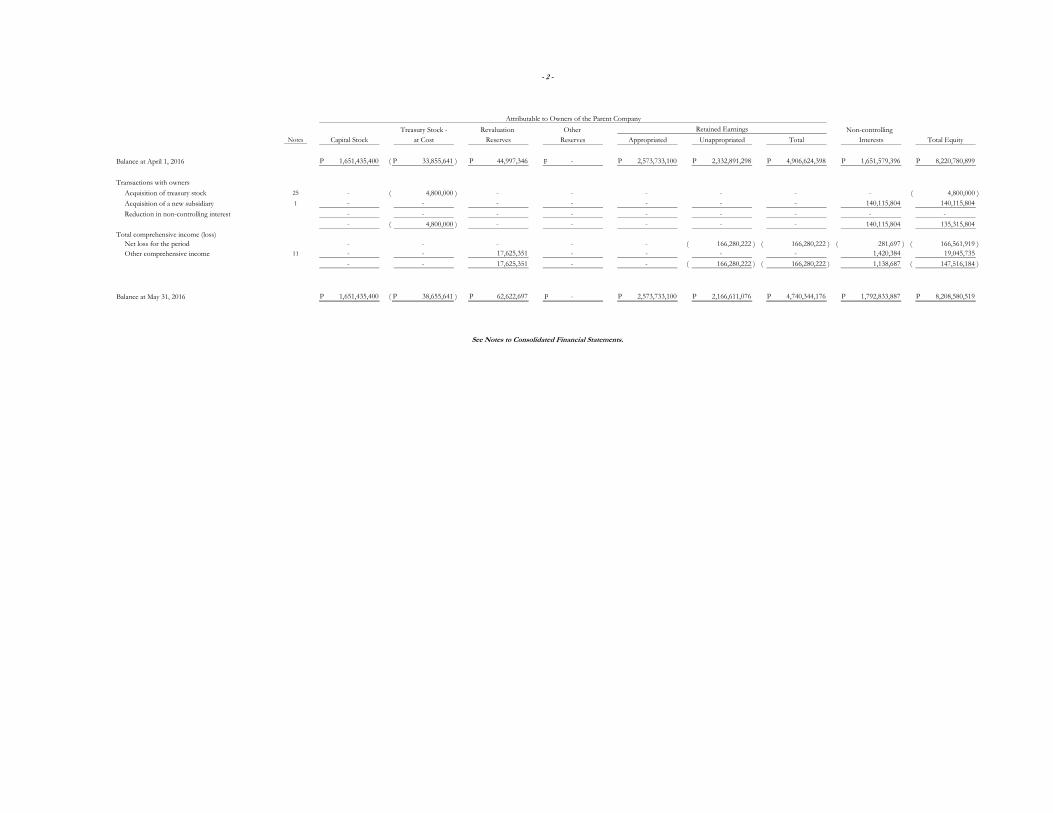

RetainedEarnings/(Deficit) 5,357,541,295 5,128,123,327

Stockholders' Equity 9,041,397,128 8,822,625,347

Stockholders' Equity - Parent 6,862,186,284 6,712,118,277

Book Value Per Share 550 537

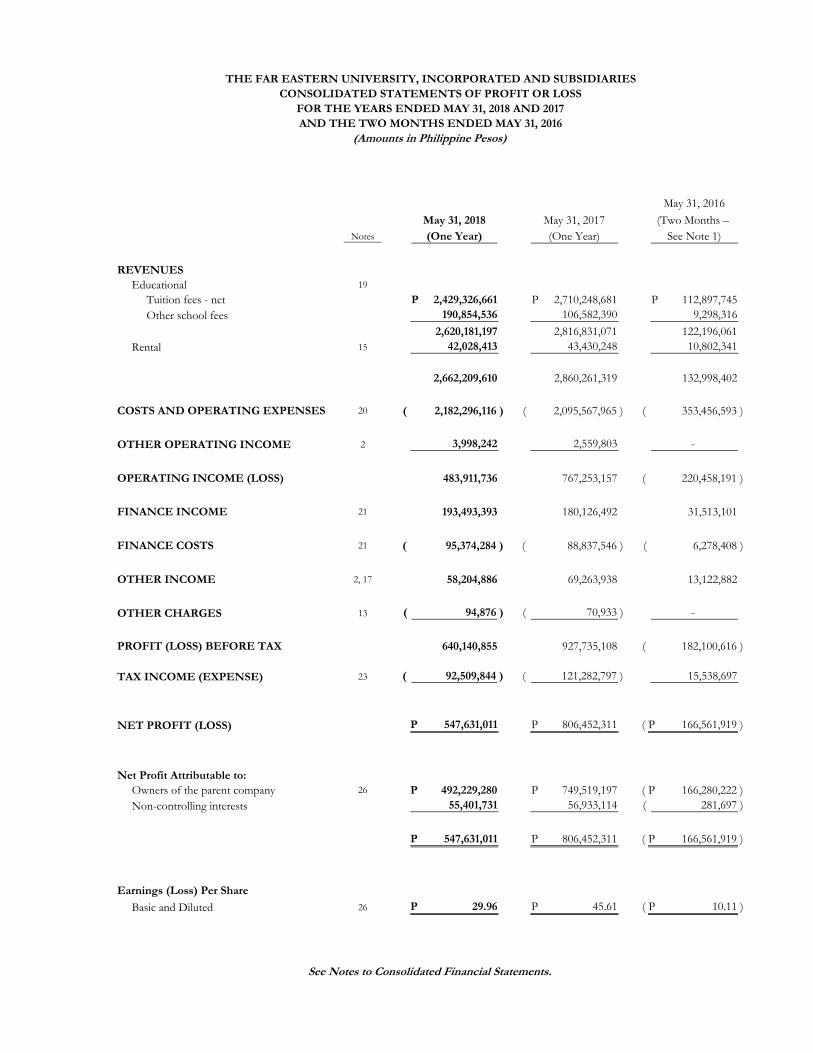

Income Statement

Year Ending Previous Year Ending

May 31, 2018 May 31, 2017

Gross Revenue 2,666,207,852 2,862,821,122

Gross Expense 2,182,296,116 2,095,567,965

Non-Operating Income 251,698,279 249,390,430

Non-Operating Expense 95,469,160 88,908,479

Income/(Loss) Before Tax 640,140,855 927,735,108

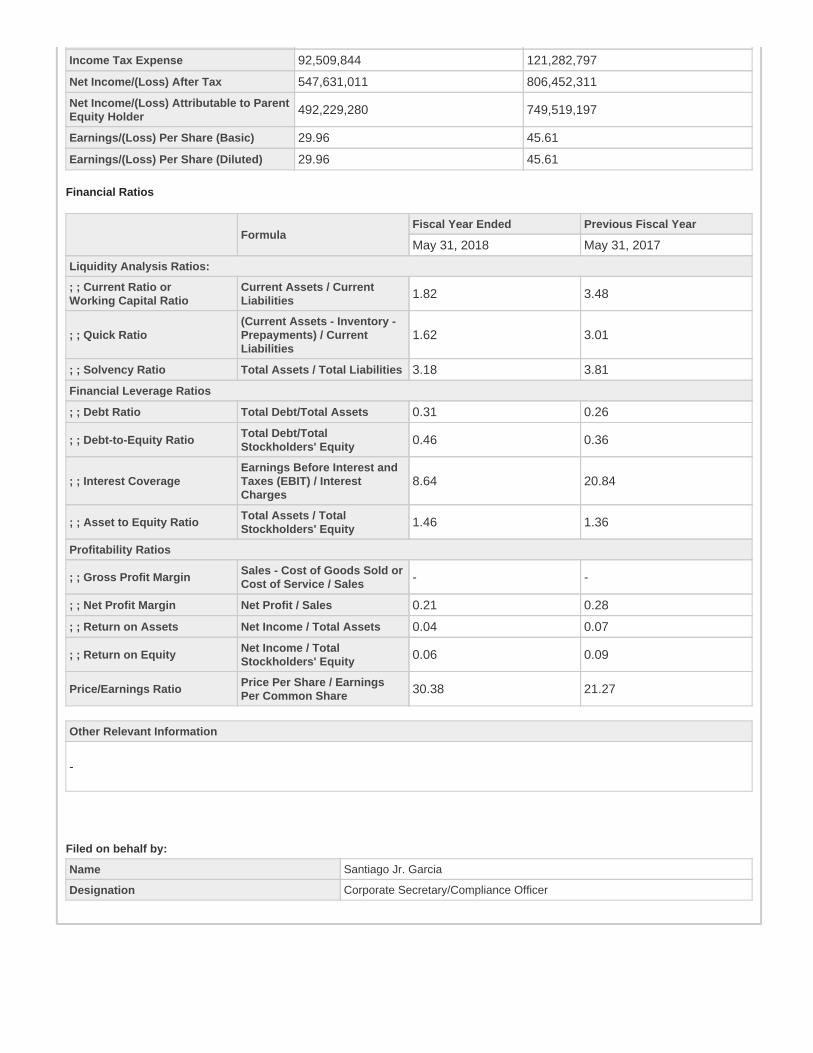

Income Tax Expense 92,509,844 121,282,797

Net Income/(Loss) After Tax 547,631,011 806,452,311

Net Income/(Loss) Attributable to ParentEquity Holder 492,229,280 749,519,197

Earnings/(Loss) Per Share (Basic) 29.96 45.61

Earnings/(Loss) Per Share (Diluted) 29.96 45.61

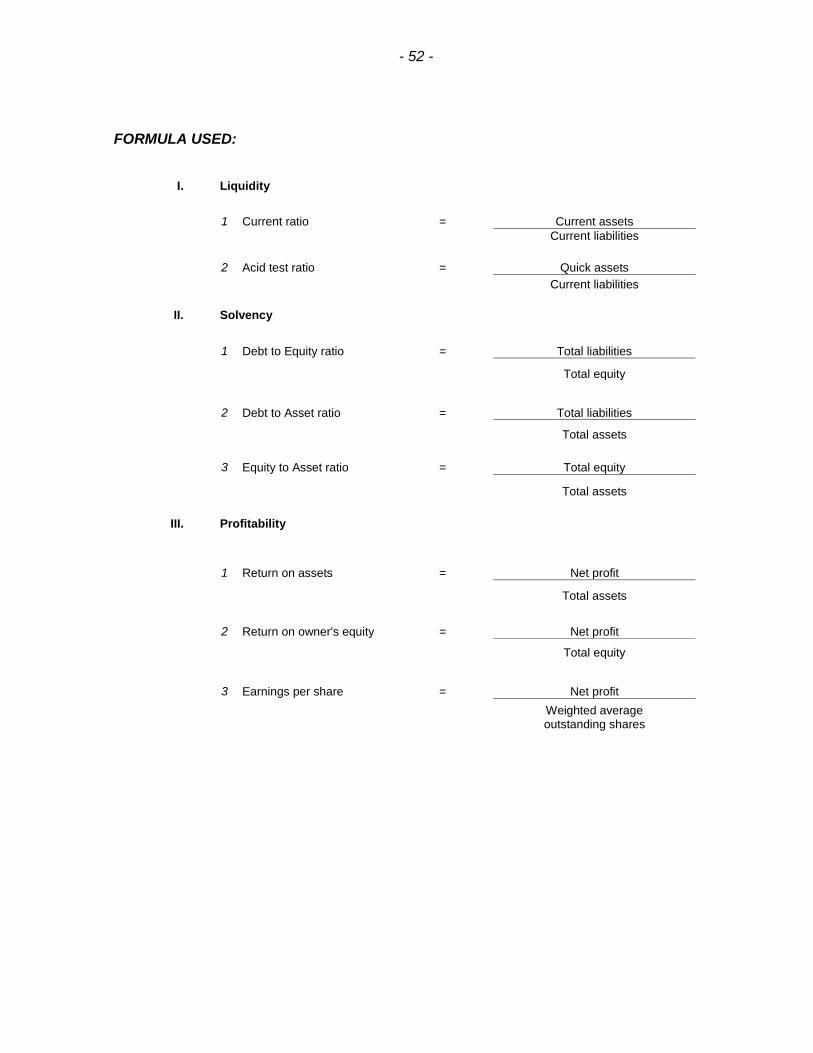

Financial Ratios

FormulaFiscal Year Ended Previous Fiscal Year

May 31, 2018 May 31, 2017

Liquidity Analysis Ratios:

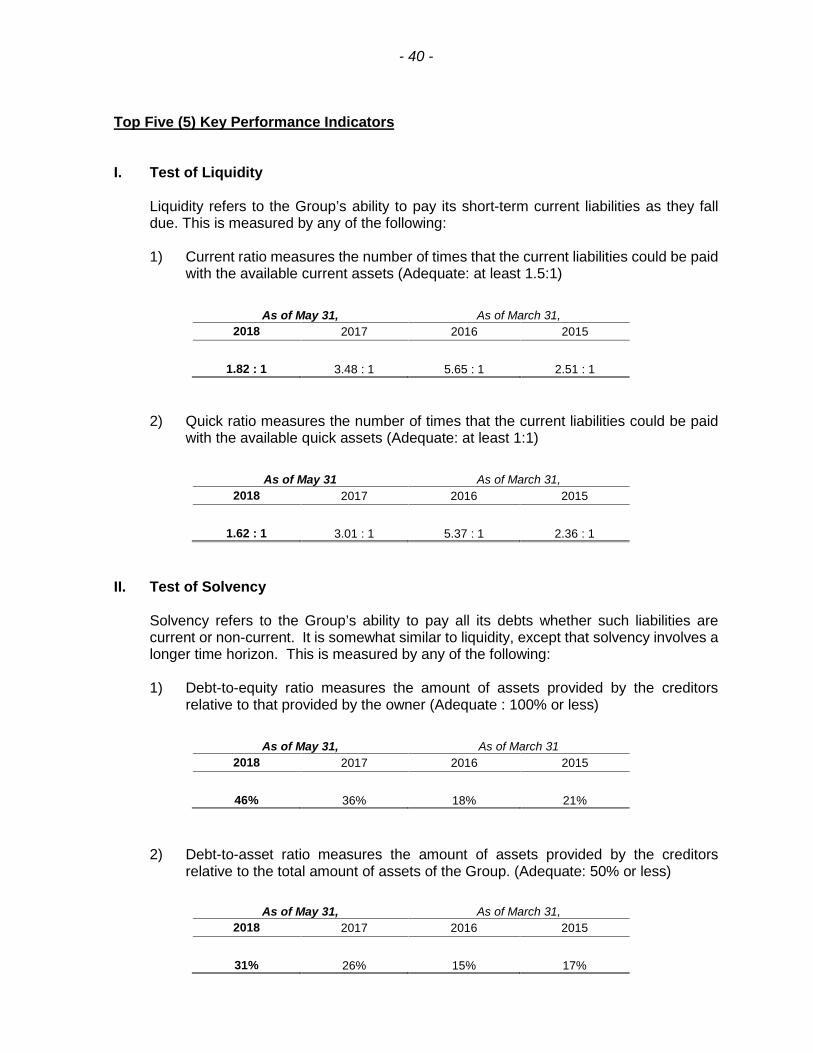

; ; Current Ratio orWorking Capital Ratio

Current Assets / CurrentLiabilities 1.82 3.48

; ; Quick Ratio(Current Assets - Inventory -Prepayments) / CurrentLiabilities

1.62 3.01

; ; Solvency Ratio Total Assets / Total Liabilities 3.18 3.81

Financial Leverage Ratios

; ; Debt Ratio Total Debt/Total Assets 0.31 0.26

; ; Debt-to-Equity RatioTotal Debt/TotalStockholders' Equity 0.46 0.36

; ; Interest CoverageEarnings Before Interest andTaxes (EBIT) / InterestCharges

8.64 20.84

; ; Asset to Equity RatioTotal Assets / TotalStockholders' Equity 1.46 1.36

Profitability Ratios

; ; Gross Profit MarginSales - Cost of Goods Sold orCost of Service / Sales - -

; ; Net Profit Margin Net Profit / Sales 0.21 0.28

; ; Return on Assets Net Income / Total Assets 0.04 0.07

; ; Return on EquityNet Income / TotalStockholders' Equity 0.06 0.09

Price/Earnings RatioPrice Per Share / EarningsPer Common Share 30.38 21.27

Other Relevant Information

-

Filed on behalf by:

Name Santiago Jr. Garcia

Designation Corporate Secretary/Compliance Officer

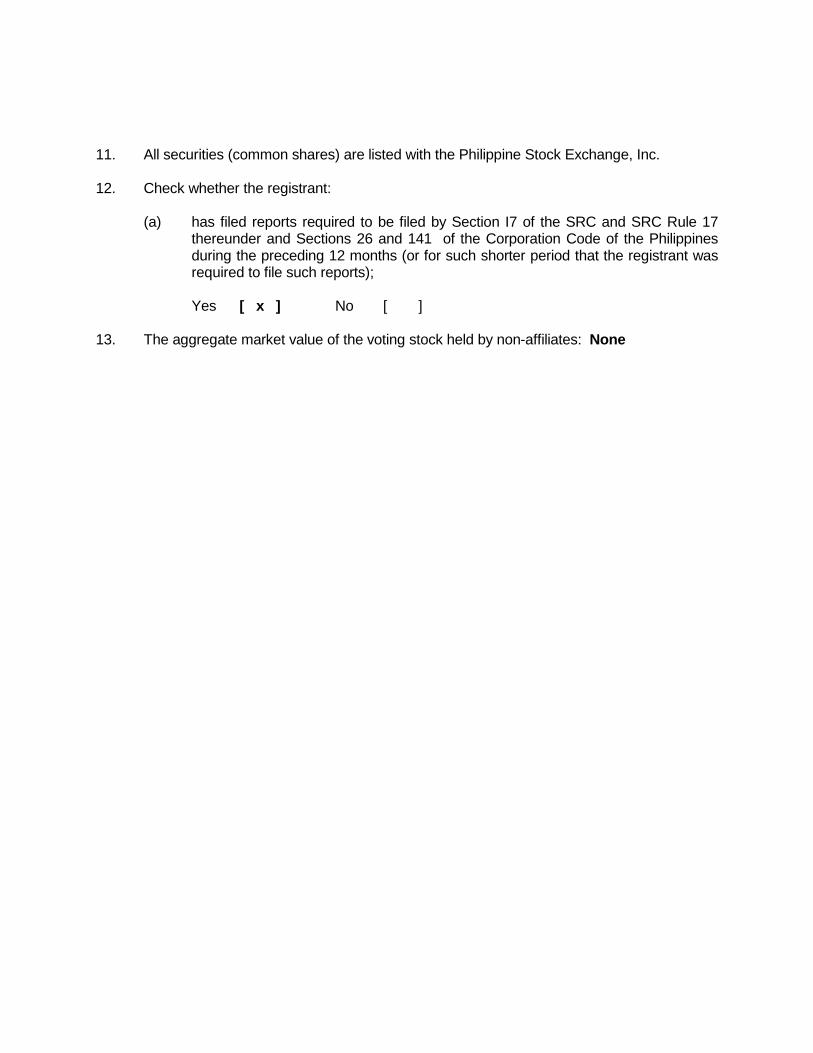

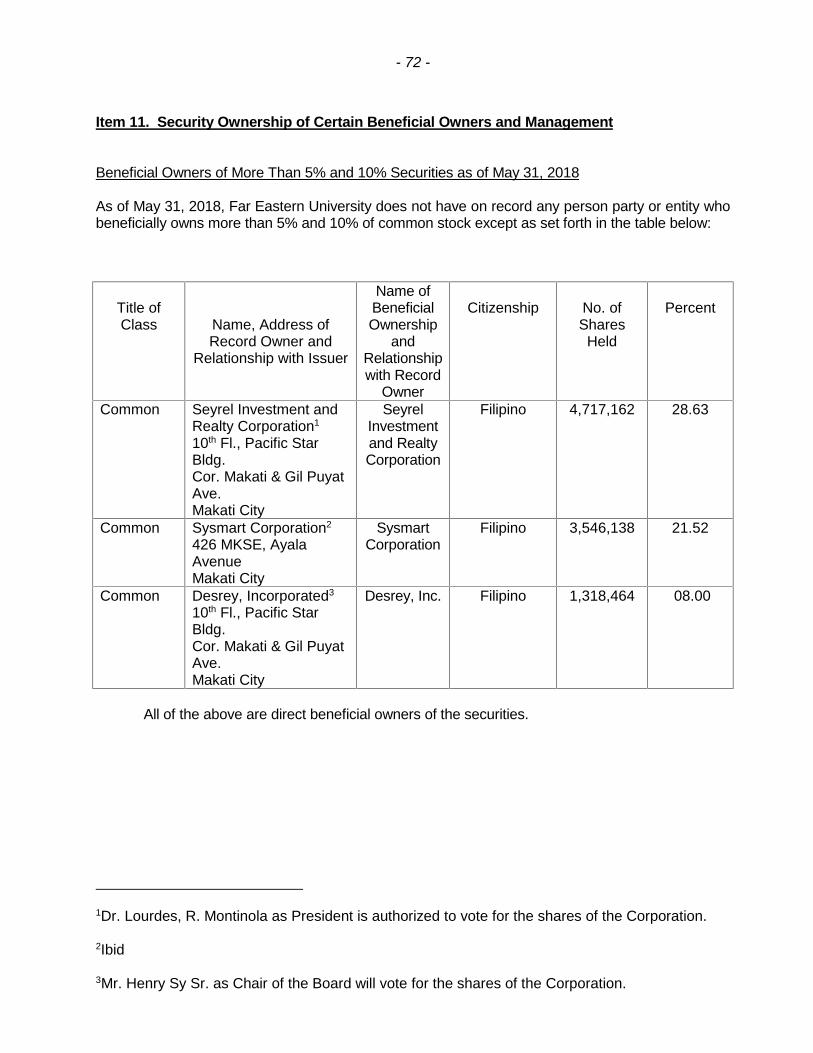

11. All securities (common shares) are listed with the Philippine Stock Exchange, Inc.

12. Check whether the registrant:

(a) has filed reports required to be filed by Section I7 of the SRC and SRC Rule 17thereunder and Sections 26 and 141 of the Corporation Code of the Philippinesduring the preceding 12 months (or for such shorter period that the registrant wasrequired to file such reports);

Yes [ x ] No [ ]

13. The aggregate market value of the voting stock held by non-affiliates: None

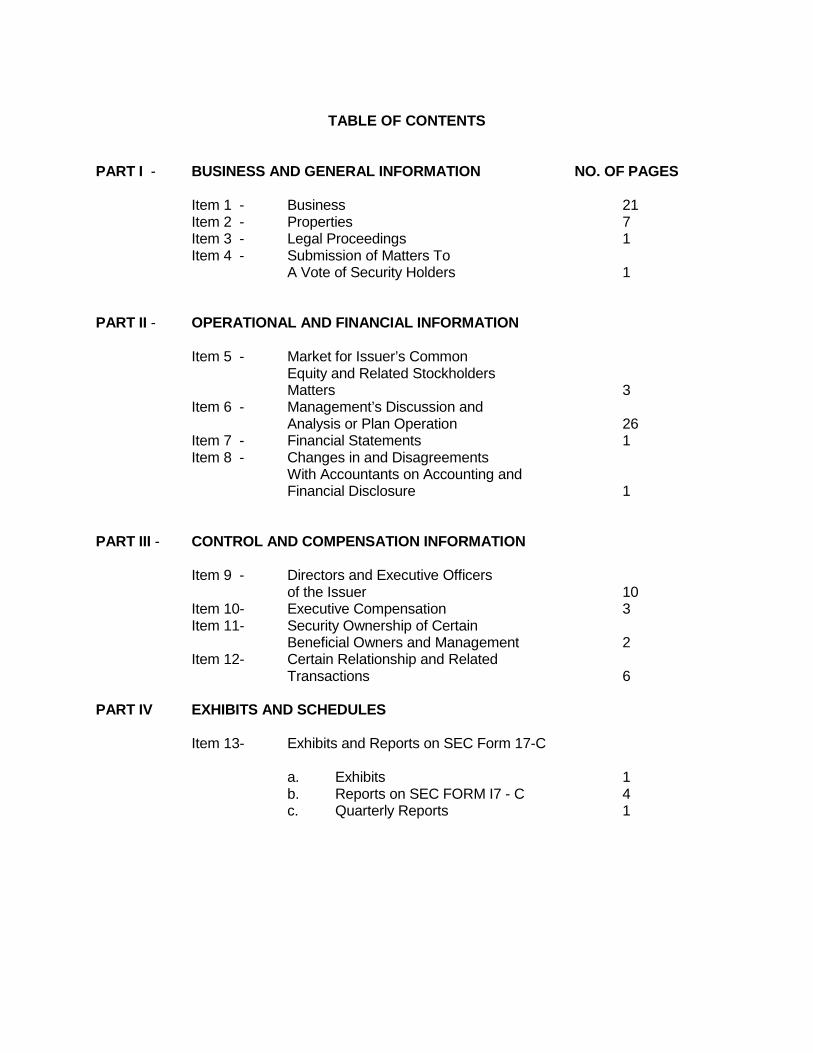

TABLE OF CONTENTS

PART I - BUSINESS AND GENERAL INFORMATION NO. OF PAGES

Item 1 - Business 21Item 2 - Properties 7Item 3 - Legal Proceedings 1Item 4 - Submission of Matters To

A Vote of Security Holders 1

PART II - OPERATIONAL AND FINANCIAL INFORMATION

Item 5 - Market for Issuer’s CommonEquity and Related StockholdersMatters 3

Item 6 - Management’s Discussion andAnalysis or Plan Operation 26

Item 7 - Financial Statements 1Item 8 - Changes in and Disagreements

With Accountants on Accounting andFinancial Disclosure 1

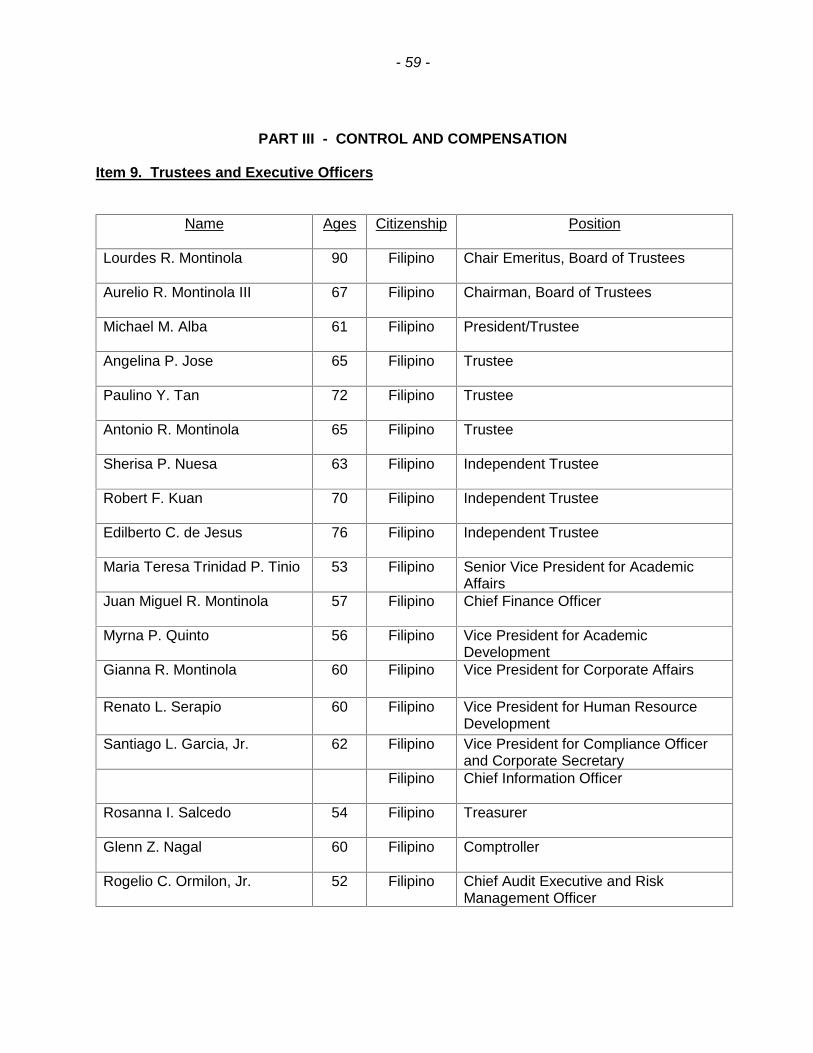

PART III - CONTROL AND COMPENSATION INFORMATION

Item 9 - Directors and Executive Officersof the Issuer 10

Item 10- Executive Compensation 3Item 11- Security Ownership of Certain

Beneficial Owners and Management 2Item 12- Certain Relationship and Related

Transactions 6

PART IV EXHIBITS AND SCHEDULES

Item 13- Exhibits and Reports on SEC Form 17-C

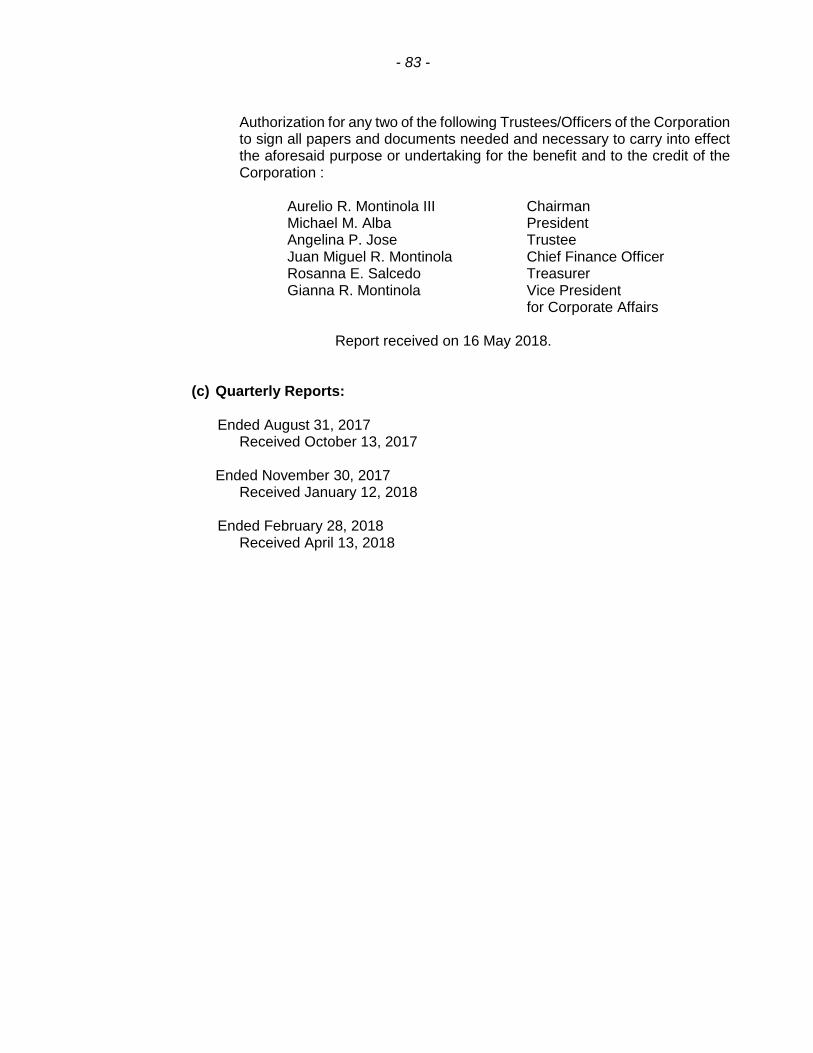

a. Exhibits 1b. Reports on SEC FORM I7 - C 4c. Quarterly Reports 1

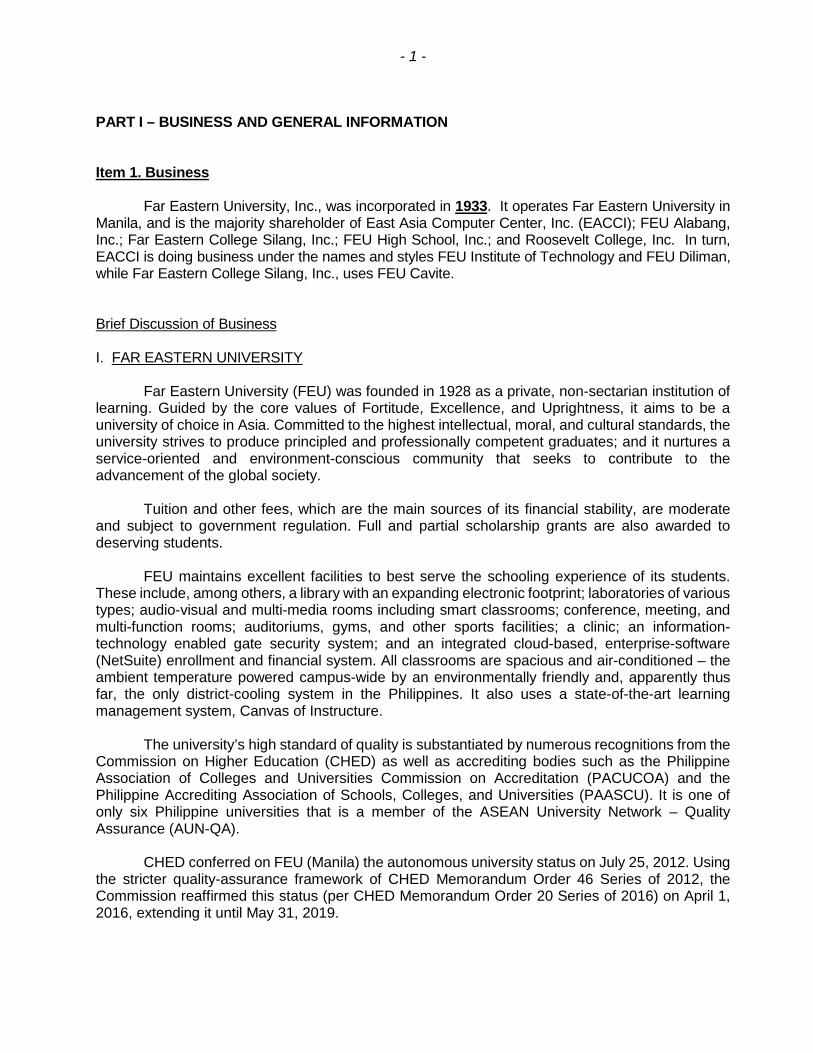

- 1 -

PART I – BUSINESS AND GENERAL INFORMATION

Item 1. Business

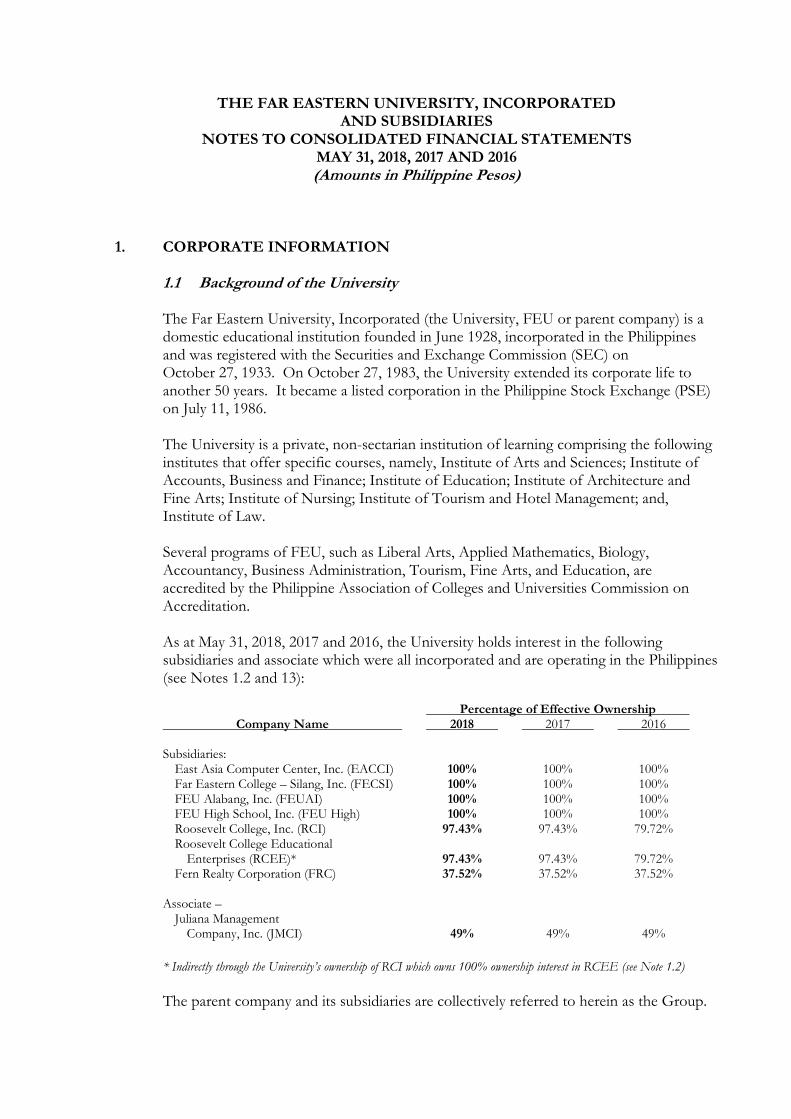

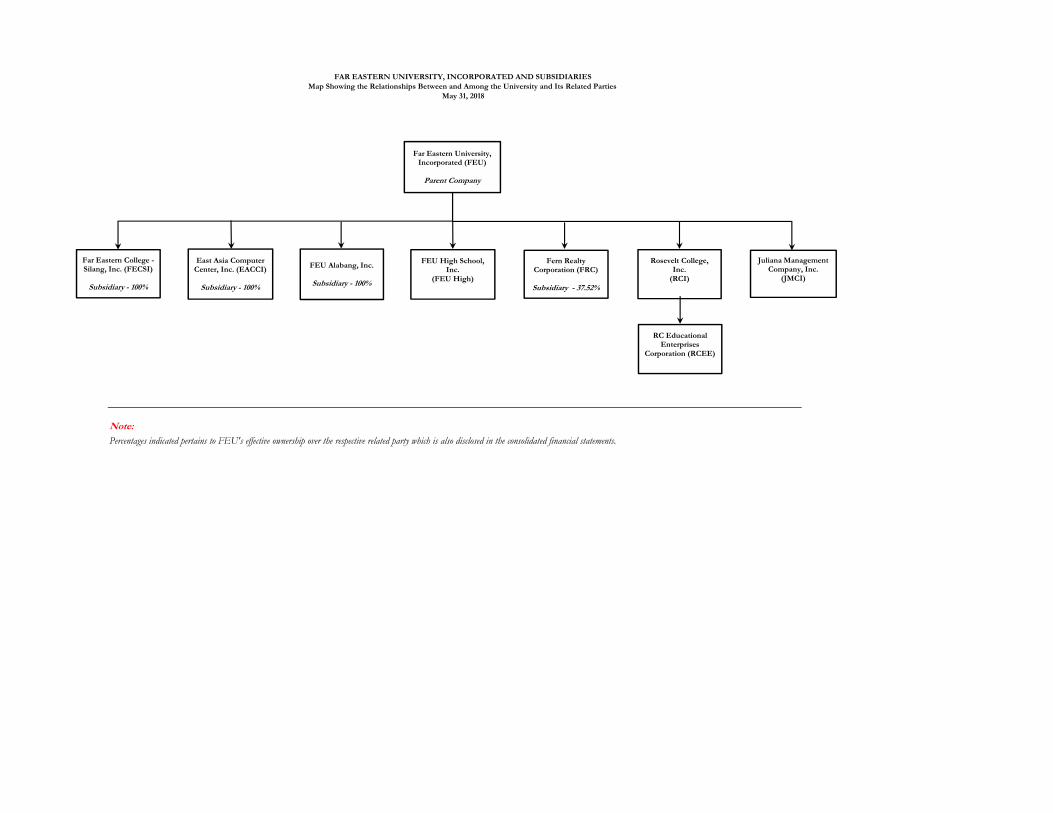

Far Eastern University, Inc., was incorporated in 1933. It operates Far Eastern University inManila, and is the majority shareholder of East Asia Computer Center, Inc. (EACCI); FEU Alabang,Inc.; Far Eastern College Silang, Inc.; FEU High School, Inc.; and Roosevelt College, Inc. In turn,EACCI is doing business under the names and styles FEU Institute of Technology and FEU Diliman,while Far Eastern College Silang, Inc., uses FEU Cavite.

Brief Discussion of Business

I. FAR EASTERN UNIVERSITY

Far Eastern University (FEU) was founded in 1928 as a private, non-sectarian institution oflearning. Guided by the core values of Fortitude, Excellence, and Uprightness, it aims to be auniversity of choice in Asia. Committed to the highest intellectual, moral, and cultural standards, theuniversity strives to produce principled and professionally competent graduates; and it nurtures aservice-oriented and environment-conscious community that seeks to contribute to theadvancement of the global society.

Tuition and other fees, which are the main sources of its financial stability, are moderateand subject to government regulation. Full and partial scholarship grants are also awarded todeserving students.

FEU maintains excellent facilities to best serve the schooling experience of its students.These include, among others, a library with an expanding electronic footprint; laboratories of varioustypes; audio-visual and multi-media rooms including smart classrooms; conference, meeting, andmulti-function rooms; auditoriums, gyms, and other sports facilities; a clinic; an information-technology enabled gate security system; and an integrated cloud-based, enterprise-software(NetSuite) enrollment and financial system. All classrooms are spacious and air-conditioned – theambient temperature powered campus-wide by an environmentally friendly and, apparently thusfar, the only district-cooling system in the Philippines. It also uses a state-of-the-art learningmanagement system, Canvas of Instructure.

The university’s high standard of quality is substantiated by numerous recognitions from theCommission on Higher Education (CHED) as well as accrediting bodies such as the PhilippineAssociation of Colleges and Universities Commission on Accreditation (PACUCOA) and thePhilippine Accrediting Association of Schools, Colleges, and Universities (PAASCU). It is one ofonly six Philippine universities that is a member of the ASEAN University Network – QualityAssurance (AUN-QA).

CHED conferred on FEU (Manila) the autonomous university status on July 25, 2012. Usingthe stricter quality-assurance framework of CHED Memorandum Order 46 Series of 2012, theCommission reaffirmed this status (per CHED Memorandum Order 20 Series of 2016) on April 1,2016, extending it until May 31, 2019.

- 2 -

Product: An educational institution composed of seven institutes and an extension campus (inMakati), the university offers the following baccalaureate and graduate programs:

A. Institute of Accounts, Business, and Finance (IABF)

Baccalaureate Programs:

Bachelor of Science in Accountancy Bachelor of Science in Business Administration major in Business Economics Bachelor of Science in Business Administration major in Business

Management Bachelor of Science in Business Administration major in Financial Management Bachelor of Science in Business Administration major in Human Resource

Development Management Bachelor of Science in Business Administration major in Internal Auditing

(leading to the Bachelor of Science in Accountancy) Bachelor of Science in Business Administration major in Legal Management Bachelor of Science in Business Administration major in Marketing

Management Bachelor of Science in Business Administration major in Operations

Management

Baccalaureate Programs (Makati campus):

Bachelor of Science in Accountancy Bachelor of Science in Accounting Technology Bachelor of Science in Business Administration major in Business Economics Bachelor of Science in Business Administration major in Business

Management Bachelor of Science in Business Administration major in Financial Management Bachelor of Science in Business Administration major in Human Resource

Development Management Bachelor of Science in Business Administration major in Legal Management Bachelor of Science in Business Administration major in Marketing

Management Bachelor of Science in Business Administration major in Operations

Management Bachelor of Science in Information Technology

Graduate Program (Makati campus):

Master in Business Administration

B. Institute of Architecture and Fine Arts (IARFA)

Baccalaureate Programs:

Bachelor of Fine Arts major in Advertising Arts Bachelor of Fine Arts major in Painting Bachelor of Science in Architecture

- 3 -

C. Institute of Arts and Sciences (IAS)

Baccalaureate Programs:

Bachelor of Arts in Communication Bachelor of Arts in English Language Bachelor of Arts in Interdisciplinary Studies Bachelor of Arts in International Studies Bachelor of Arts in Literature Bachelor of Arts in Political Science Bachelor of Science in Applied Mathematics with Information Technology Bachelor of Science in Biology Bachelor of Science in Medical Technology Bachelor of Science in Psychology

Graduate Programs:

Doctor of Philosophy in Psychology major in Clinical Psychology Doctor of Philosophy in Psychology major in Forensic Psychology Doctor of Philosophy in Psychology major in Industrial Psychology Master of Arts in Communication Master of Arts major in Letters Master of Arts in Psychology specialization in Clinical Psychology Master of Arts in Psychology specialization in Industrial Psychology Master of Science in Biology

D. Institute of Education (IE)

Baccalaureate Programs:

Bachelor of Elementary Education major in General Education Bachelor of Elementary Education major in Preschool Education Bachelor of Elementary Education major in Special Education Bachelor of Physical Education major in School Physical Education Bachelor of Secondary Education major in English Bachelor of Secondary Education major in General Science Bachelor of Secondary Education major in Mathematics Bachelor of Bachelor of Secondary Education major in Sports and Recreational

Management

Certificate Program:

Teacher Certificate Program

- 4 -

Graduate Programs:

Doctor of Education major in Curriculum and Instruction Doctor of Education major in Educational Administration Doctor of Education major in Language and Literature Education Master of Arts in Education major in Curriculum and Instruction Master of Arts in Education major in Educational Administration Master of Arts in Education major in English Language Teaching Master of Arts in Education major in Literature and Language Education

(English) Master of Arts in Education major in Special Education Master in Physical Education

E. Institute of Law (IL)

Graduate Programs (Makati campus):

Bachelor of Laws Juris Doctor

F. Institute of Nursing (IN)

Baccalaureate Program:

Bachelor of Science in Nursing

Graduate programs:

Master of Arts in Nursing specialized in Community Health Master of Arts in Nursing specialized in Maternal-Child Health Master of Arts in Nursing specialized in Medical-Surgical Nursing Master of Arts in Nursing specialized in Mental Health and Psychiatric Nursing Master of Arts in Nursing specialized in Nursing Systems Administration

G. Institute of Tourism and Hotel Management (ITHM)

Baccalaureate Programs:

Bachelor of Science in Hotel and Restaurant Management Bachelor of Science in Tourism Management

All of these academic program offerings were approved and/or granted permits by the CHED, theLegal Education Board (in the case of the Bachelor of Laws and Juris Doctor programs), and otherrelevant government agencies.

- 5 -

Program Accreditations

Far Eastern University continuously strives for excellence in teaching, research and development,and extension work. Validations of this institutional effort include CHED’s citations of (a) the teacher-education programs of the IE as a Center of Excellence and (b) the Bachelor of Science in BusinessAdministration program of the IABF as a Center of Development.

Local Accreditations

Almost all of the academic programs in the Manila campus are accredited by PACUCOA. Thefollowing programs have PACUCOA Level IV accreditation status (the highest), for the periodDecember 2015 to December 2020:

Bachelor of Arts in Communication Bachelor of Elementary Education Bachelor of Science in Accountancy Bachelor of Science in Applied Mathematics with Information Technology Bachelor of Science in Biology Bachelor of Science in Business Administration Bachelor of Science in Psychology Bachelor of Secondary Education

The Bachelor of Science in Nursing is the only academic program in the Manila campus that isaccredited by PAASCU. It has Level III Reaccredited status for the period August 2018 to November2021.

Programs with PACUCOA Level II first-reaccreditation status are as follows:

o February 2017 ‒ February 2022:

Doctor of Education Master of Arts in Education Master of Arts in Psychology

o September 2015 ‒ September 2018

Bachelor of Arts in English Language Bachelor of Arts in Literature Bachelor of Arts in Political Science Bachelor of Science in Tourism Management

Programs with PACUCOA Level I formal-accreditation status are as follows:

o November 2016 ‒ September 2019

Bachelor of Arts in Hotel and Restaurant Management Bachelor of Arts in International Studies Bachelor of Fine Arts Bachelor of Science in Medical Technology

o February 2017 ‒ September 2020

Bachelor of Science in Architecture

- 6 -

In addition, two graduate programs were granted Candidate status by PACUCOA from May 2018to May 2020:

MS Biology MA Communication

Three programs of FEU Makati were granted Candidate status by PACUCOA effective March 2017to March 2019:

Bachelor of Science in Accountancy Bachelor of Science in Accounting Technology Bachelor of Science in Business Administration

International Accreditations

Far Eastern University is a member of the ASEAN University Network ‒ Quality Assurance (AUN-QA) and the Association to Advance Collegiate Schools of Business (AACSB).

ITHM’s Bachelor of Science in Tourism Management program is also accredited by the Asia-PacificInstitute for Events Management (APIEM) as a Center of Excellence, effective February 2017 toFebruary 2021.

--------Both PAASCU and PACUCOA recommend the accreditation status they have assessed for anacademic program to the Federation of Accrediting Agencies of the Philippines (FAAP), which isrecognized by CHED to approve and issue the certification of said accreditation status. A detaileddescription of the various program accreditation levels may be found in CMO 1 Series of 2005.

- 7 -

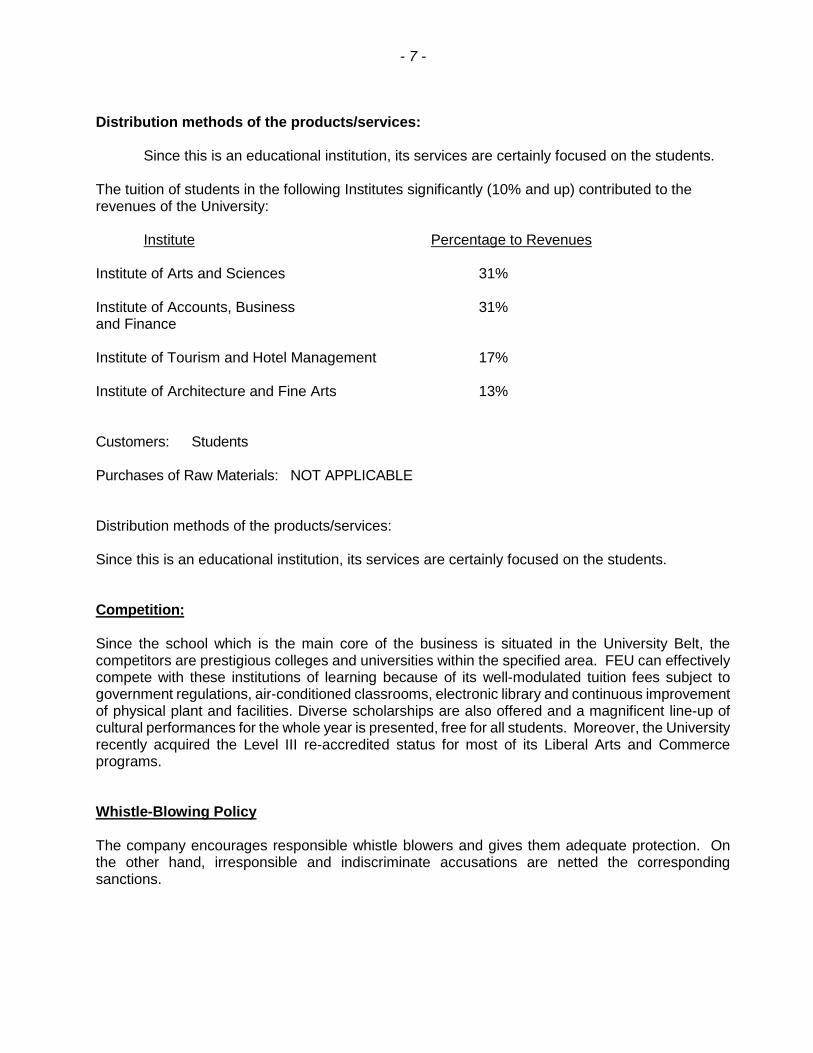

Distribution methods of the products/services:

Since this is an educational institution, its services are certainly focused on the students.

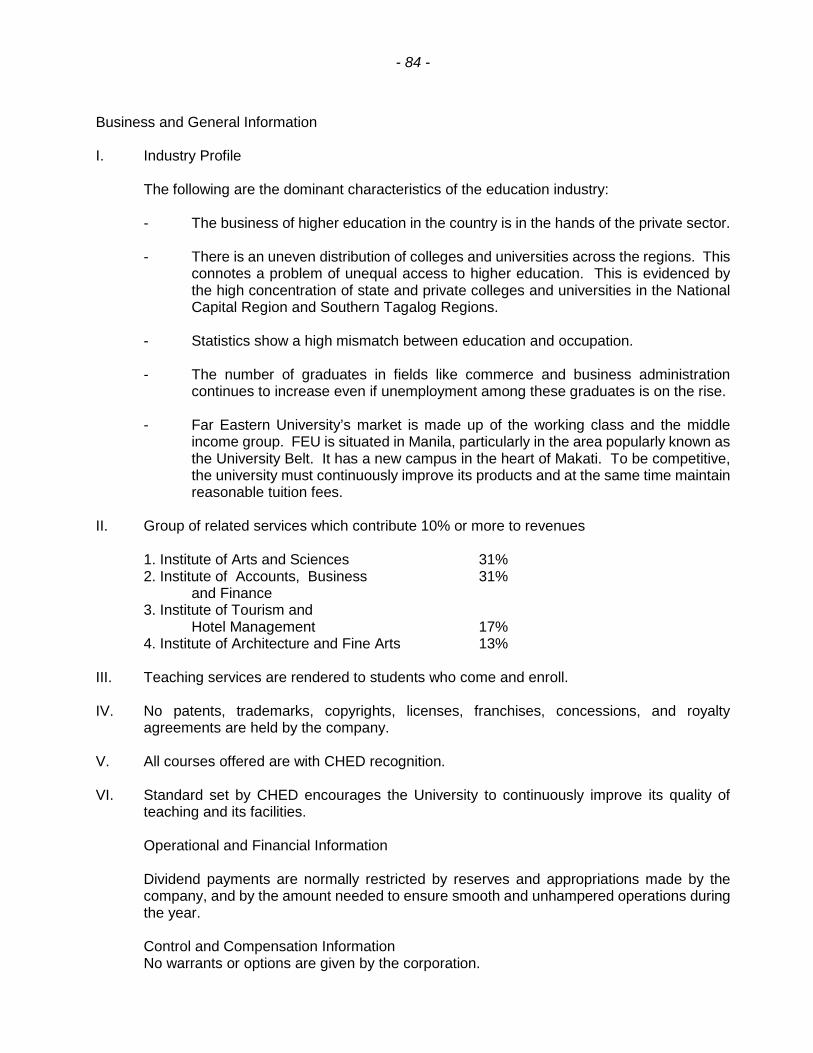

The tuition of students in the following Institutes significantly (10% and up) contributed to therevenues of the University:

Institute Percentage to Revenues

Institute of Arts and Sciences 31%

Institute of Accounts, Business 31%and Finance

Institute of Tourism and Hotel Management 17%

Institute of Architecture and Fine Arts 13%

Customers: Students

Purchases of Raw Materials: NOT APPLICABLE

Distribution methods of the products/services:

Since this is an educational institution, its services are certainly focused on the students.

Competition:

Since the school which is the main core of the business is situated in the University Belt, thecompetitors are prestigious colleges and universities within the specified area. FEU can effectivelycompete with these institutions of learning because of its well-modulated tuition fees subject togovernment regulations, air-conditioned classrooms, electronic library and continuous improvementof physical plant and facilities. Diverse scholarships are also offered and a magnificent line-up ofcultural performances for the whole year is presented, free for all students. Moreover, the Universityrecently acquired the Level III re-accredited status for most of its Liberal Arts and Commerceprograms.

Whistle-Blowing Policy

The company encourages responsible whistle blowers and gives them adequate protection. Onthe other hand, irresponsible and indiscriminate accusations are netted the correspondingsanctions.

- 8 -

Affiliates and Subsidiaries

EAST ASIA COMPUTER CENTER, INC. (EACCI)

Although incorporated in 1992, East Asia Computer Center, Inc. (EACCI), started doing businessunder the name and style FEU Institute of Technology (or “FIT” or “FEU Tech”) only in 2014. InMarch 2018, it began to use the name and style FEU Diliman as well.

I. FEU INSTITUTE OF TECHNOLOGY

FEU Tech is a private, non-sectarian institution that provides quality education in the fields ofengineering and information technology. It is housed in two buildings: the Technology Building ofthe FEU Manila campus along Nicanor Reyes Street and the 17-story FEU Tech Building on P.Paredes Street. The school’s facilities include well-equipped, air-conditioned classrooms,laboratories, and engineering workshops; a library with a large collection of digital media; a coveredgym; a 25-meter four-lane swimming pool; study areas for both individual and collaborative work;exhibit areas; and multi-function rooms. Other notable features include scenic elevators; an e-building high-tech security system; and an observation deck that provides a scenic view of theManila landscape.

FEU Tech offers innovative academic programs that are complemented by strong industry andacademic partnerships, which provide students additional opportunities for immersive learningexperiences. Students receive real-world training and work experience from an intense and well-designed internship program with industry partners – a network of some 800 technology andengineering corporations nationwide. In addition, study abroad and internship abroad programsallow students to learn and be immersed in multicultural environments and cultures with partnerschools in Taiwan and Korea.

FEU Tech offers the following programs and specializations:

College of Engineering:

Bachelor of Science in Civil Engineering Bachelor of Science in Computer Engineering Bachelor of Science in Electronics Engineering Bachelor of Science in Electrical Engineering Bachelor of Science in Mechanical Engineering

College of Computer Studies:

Bachelor of Science in Computer Science, with specialization in:

o Software Engineeringo Business Analytics

Bachelor of Science in Information Technology, with specialization in:

o Animation and Game Developmento Digital Artso Service Management and/or Business Analyticso Web and Mobile Applications

Bachelor of Science in Entertainment and Multimedia Computing, with specialization in:

o Digital Animation Technology

- 9 -

II. FEU DILIMAN

FEU Diliman is a private, non-sectarian educational institution with a 10-hectare campus that islocated in in Mapayapa Village, Quezon City. Its offerings cover the full spectrum of kindergarten,grade school, junior high school, senior high school, and college.

For basic education, FEU Diliman delivers an advanced curriculum in English, Science, andMathematics, which integrates 21st-century skills development. Students are provided with holisticdevelopment through engagement in sports, culture, values formation, and socio-civic activities andprograms. Value-added courses are embedded primarily to prepare the FEU Diliman basiceducation graduates to pursue higher education in the top universities of the country.

For higher education, FEU Diliman is working toward becoming a professional institution that isrecognized for the business and information technology fusion of its academic programs.Professional core courses for technical proficiency and internship for real-world practice form thecore of the curriculum. Technology-driven, non-traditional delivery strategies allow higher levels ofstudent engagement and motivation to achieve the intended learning goals. Graduates areenvisioned to be technology-empowered, highly qualified, and principled professionals and leaderspoised to provide innovative solutions to the future challenges of their work places.

The college offerings of FEU Diliman include:

BS Accountancy BS Business Administration major in Marketing Management BS Business Administration major in Financial Management BS Business Administration major in Operations Management

- 10 -

III. FEU ALABANG, INC.

Founded on July 21, 2016, FEU Alabang, Inc., carries Far Eastern University’s mission to providequality education to the south of Metro Manila. It is located in Filinvest City, Alabang, one of themost progressive areas in Southern Metro Manila. Set to open in August 2018, the 1.8-hectarecampus will welcome students to its 17-story academic building, which will come equipped withmodern classrooms and laboratories, as well as a campus accented by lush green spaces andfeaturing a 200-seat chapel and gymnasium.

FEU Alabang will be offering the following programs:

Senior High School Science, Technology, Engineering, and Mathematics (STEM) Accountancy, Business, and Management (ABM) Humanities and Social Science (HUMSS) General Academic Strand (GAS)

College of Engineering Bachelor of Science in Civil Engineering Bachelor of Science in Computer Engineering Bachelor of Science in Electronics Engineering Bachelor of Science in Electrical Engineering Bachelor of Science in Mechanical Engineering Bachelor of Science in Manufacturing Engineering

College of Computer Studies and Multimedia Arts Bachelor of Arts in Multimedia Arts Bachelor of Science in Computer Science Bachelor of Science in Entertainment and Multimedia Computing

- 11 -

IV. FAR EASTERN COLLEGE SILANG, INC.

Established in 2009, Far Eastern College Silang, Inc., is doing business under the name and styleof FEU Cavite, and is the first subsidiary of Far Eastern University, Inc., outside Metro Manila. It islocated inside MetroGate Silang Estates, a gated community in Silang, Cavite, and hence servesas the “Home of the Tamaraws in the South. It admitted its first batch of pre-school, grade school,and college students in June 2010 and of senior high school students in 2016.

FEU Cavite aspires to be a school of choice in the Southern Tagalog region by pursuing the twingoals of inculcating a love for learning among its students and being an engine for the region’scommunity development. It seeks to develop its students as values-driven, service-oriented, andfuture-ready global citizens through a technology-empowered and individualized learning system.Its social mission is to fuel community growth by heritage preservation and environmentalstewardship.

FEU Cavite offers the following programs:

Basic Education Department (BED)

Pre-kindergarten Kindergarten Grade School Junior High School

Senior High School (SHS) Department

Academic Tracks Science, Technology, Engineering, and Mathematics Accountancy, Business Management Humanities and Social Sciences

Higher Education Department (HED)

Bachelor of Science in AccountancyBachelor of Science in Accounting TechnologyBachelor of Science in Business AdministrationBachelor in Elementary and Secondary EducationBachelor of Science in Hotel and Restaurant ManagementBachelor of Science in Information TechnologyBachelor of Science in Tourism ManagementBachelor of Science in PsychologyTESDA-accredited course on Bread and Pastry Production

- 12 -

V. FEU HIGH SCHOOL, INC.

Far Eastern University High School (FEU HS), Inc., was established as a subsidiary of Far EasternUniversity, Inc., in 2013 in response to Republic Act No. 10533, the “Enhanced Basic EducationAct of 2013,” which extended the Philippine basic education program to 13 years, adding Grades11 and 12 to the secondary education level. Nestled inside the FEU Manila Campus, FEU HSopened its doors to its first batch of senior high school students in June 2016.

Guided by the core values of Fortitude, Excellence, and Uprightness, FEU High School providesquality education that prepares its graduates for college, the world of work, and life. Its curriculumis student-centered, values-oriented, and competency-laden; its delivery methods technology-enabled, and its learning activities project-based.

FEU HS offers the following strands under the academic track of the senior high school program:Science, Technology, Engineering, and Mathematics (STEM); Accountancy, Business, andManagement (ABM); Humanities and Social Sciences (HUMSS); and the General Academic Strand(GAS).

- 13 -

VI. ROOSEVELT COLLEGE, INC.

Roosevelt College, Inc. (RCI), has a long history of establishing good-quality nonsectarian privatehigh schools, first as Marikina Academy in 1933 and as RCI starting 1946. Soon after its founding,the academy ranked among the top 20 of the 70 private high schools in the Philippines.

RCI became a member of the Far Eastern University (FEU) group of schools in May 2016 whenFEU purchased 79.72% of the outstanding capital stock of RCI and gained management control ofall its existing campuses as well as affiliated companies. Significantly contributing to the expansionof the FEU group’s geographic and demographic footprint and to the growth of its basic educationprogram, RCI is expected to carry forward FEU’s mark of offering quality educational programs andfacilities while improving its accessibility to more Filipino families.

RCI envisions the formation of a productive and responsible citizenry empowered througheducation. It offers the following degree programs and short programs:

Basic Education Program: K-12

Developmental Kindergarten for 4-year olds (RCI Cainta and RCI Rodriguez)

Special Science Program for Junior High School students with high aptitude in Science, Math,and English (RCI Cainta)

Senior High Schoolo Academic Track: ABM, HUMSS, and STEM strandso Tech-Vocational: Home Economics strand (RCI Rodriguez)

Tertiary Education (RCI Cainta except if otherwise indicated)

Undergraduate Programs AB Broadcasting

o AB Psychology (RCI Marikina)o Bachelor of Elementary Education with Specialization in Early Childhood Educationo Bachelor of Elementary Education with Specialization in Special Educationo Bachelor of Secondary Education Major in Englisho Bachelor of Secondary Education Major in Mathematicso Bachelor of Secondary Education Major in Music, Arts, Physical Education and

Healtho BS Information Technology (RCI Marikina)o BSBA Human Resources Management (RCI Marikina)o BSBA Operations Management (RCI Marikina)o BS Hotel and Restaurant Management

Graduate Programo MA in Education Major in Educational Managemento MA in Education Major in Educational Technologyo MA in Education Major in Teaching in the Early Gradeso MA in Education Major in Social Studieso MA in Education Major in Filipino Educationo MA in Education Major in Mathematics Educationo MA in Education Major in Science Educationo MA in Education Major in English Studies & Instructiono MA in Education Major in Guidance & Counsellingo MA in Education Major in Special Educationo Teacher Certificate Program

- 14 -

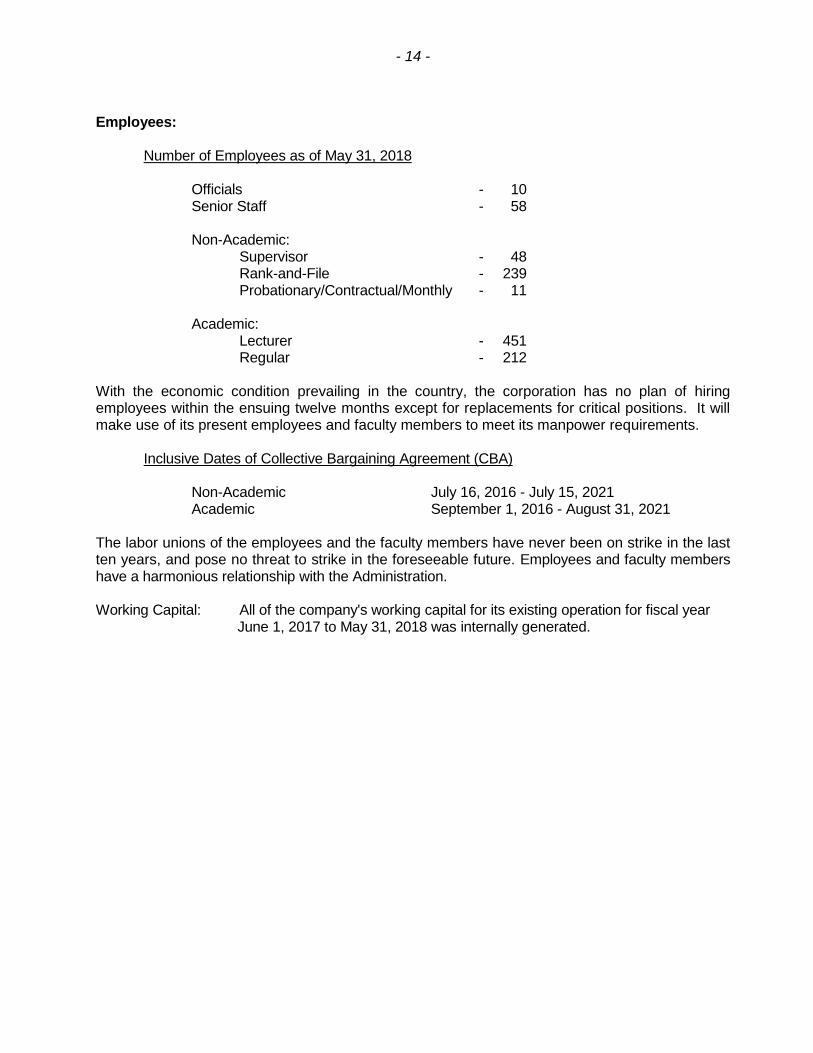

Employees:

Number of Employees as of May 31, 2018

Officials - 10Senior Staff - 58

Non-Academic:Supervisor - 48Rank-and-File - 239Probationary/Contractual/Monthly - 11

Academic:Lecturer - 451Regular - 212

With the economic condition prevailing in the country, the corporation has no plan of hiringemployees within the ensuing twelve months except for replacements for critical positions. It willmake use of its present employees and faculty members to meet its manpower requirements.

Inclusive Dates of Collective Bargaining Agreement (CBA)

Non-Academic July 16, 2016 - July 15, 2021Academic September 1, 2016 - August 31, 2021

The labor unions of the employees and the faculty members have never been on strike in the lastten years, and pose no threat to strike in the foreseeable future. Employees and faculty membershave a harmonious relationship with the Administration.

Working Capital: All of the company's working capital for its existing operation for fiscal yearJune 1, 2017 to May 31, 2018 was internally generated.

- 15 -

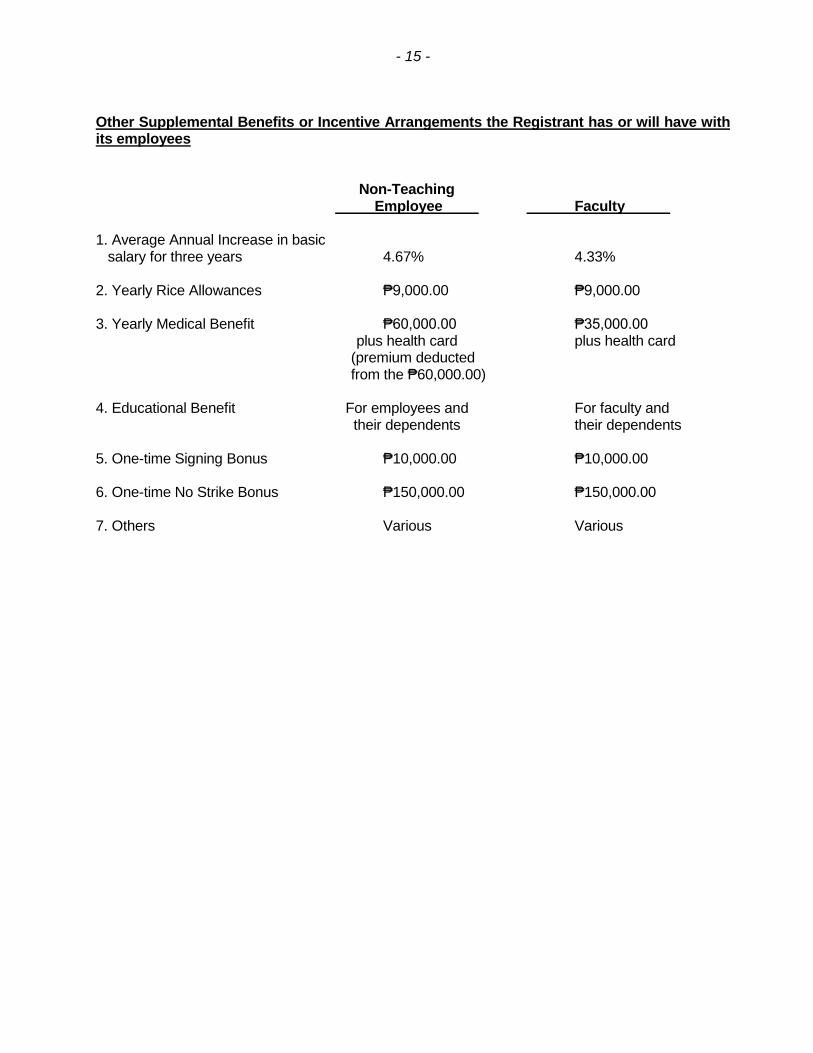

Other Supplemental Benefits or Incentive Arrangements the Registrant has or will have withits employees

Non-TeachingEmployee Faculty

1. Average Annual Increase in basicsalary for three years 4.67% 4.33%

2. Yearly Rice Allowances ₱9,000.00 ₱9,000.00

3. Yearly Medical Benefit ₱60,000.00 ₱35,000.00plus health card plus health card

(premium deductedfrom the ₱60,000.00)

4. Educational Benefit For employees and For faculty andtheir dependents their dependents

5. One-time Signing Bonus ₱10,000.00 ₱10,000.00

6. One-time No Strike Bonus ₱150,000.00 ₱150,000.00

7. Others Various Various

- 16 -

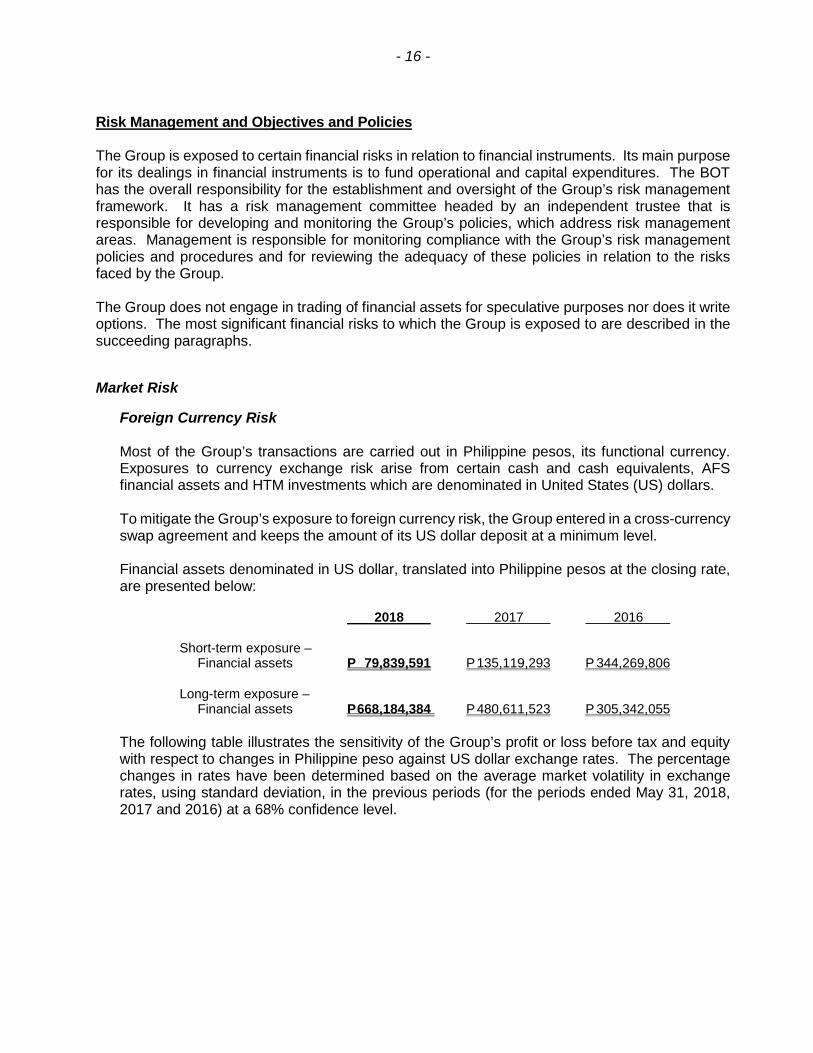

Risk Management and Objectives and Policies

The Group is exposed to certain financial risks in relation to financial instruments. Its main purposefor its dealings in financial instruments is to fund operational and capital expenditures. The BOThas the overall responsibility for the establishment and oversight of the Group’s risk managementframework. It has a risk management committee headed by an independent trustee that isresponsible for developing and monitoring the Group’s policies, which address risk managementareas. Management is responsible for monitoring compliance with the Group’s risk managementpolicies and procedures and for reviewing the adequacy of these policies in relation to the risksfaced by the Group.

The Group does not engage in trading of financial assets for speculative purposes nor does it writeoptions. The most significant financial risks to which the Group is exposed to are described in thesucceeding paragraphs.

Market Risk

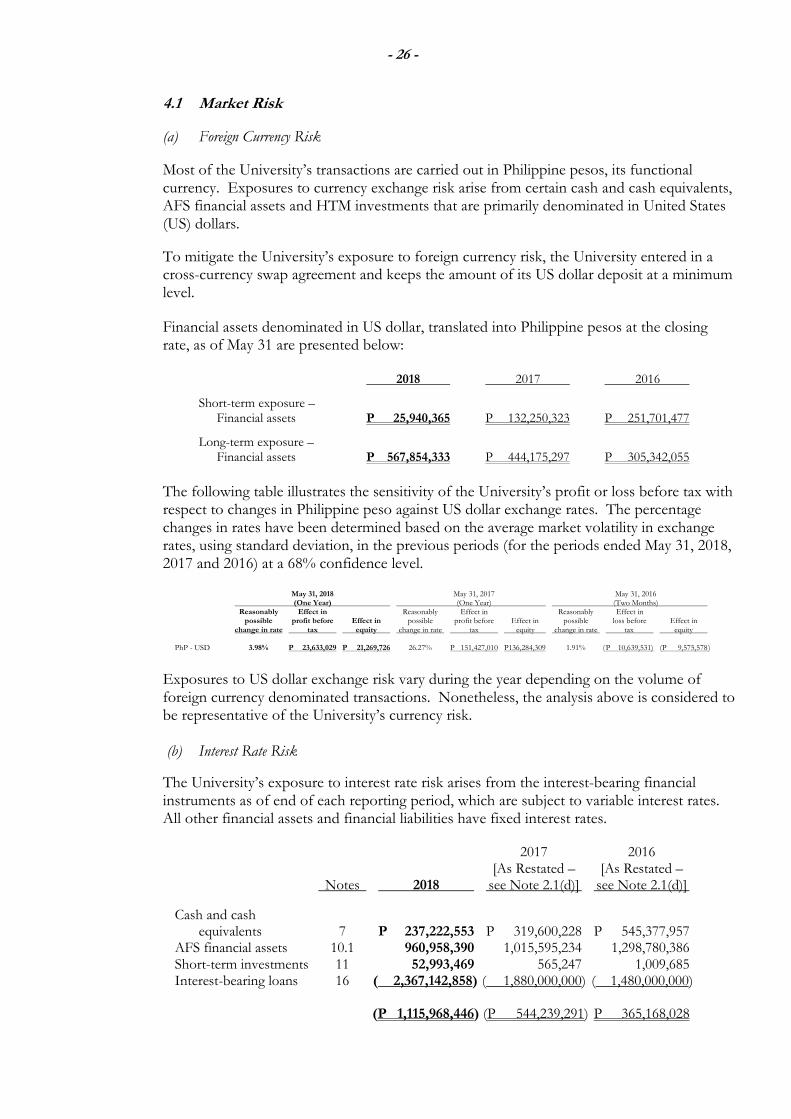

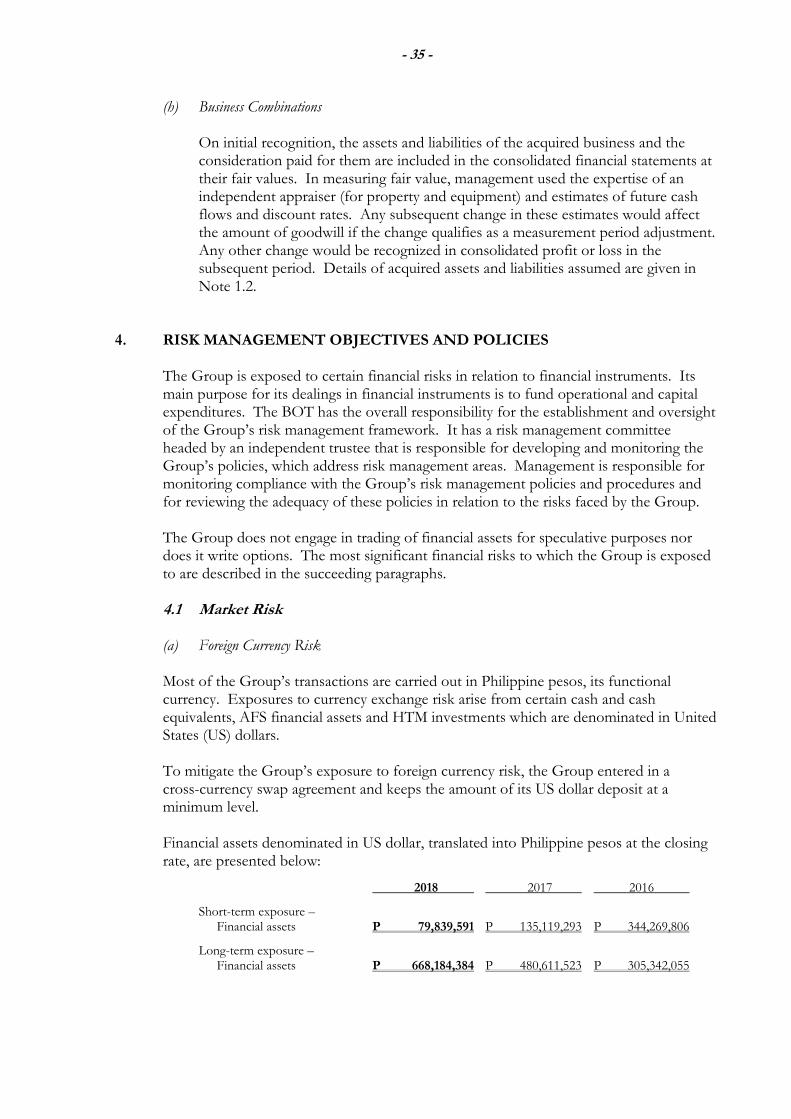

Foreign Currency Risk

Most of the Group’s transactions are carried out in Philippine pesos, its functional currency.Exposures to currency exchange risk arise from certain cash and cash equivalents, AFSfinancial assets and HTM investments which are denominated in United States (US) dollars.

To mitigate the Group’s exposure to foreign currency risk, the Group entered in a cross-currencyswap agreement and keeps the amount of its US dollar deposit at a minimum level.

Financial assets denominated in US dollar, translated into Philippine pesos at the closing rate,are presented below:

2018 2017 2016

Short-term exposure –Financial assets P 79,839,591 P135,119,293 P 344,269,806

Long-term exposure –Financial assets P668,184,384 P480,611,523 P 305,342,055

The following table illustrates the sensitivity of the Group’s profit or loss before tax and equitywith respect to changes in Philippine peso against US dollar exchange rates. The percentagechanges in rates have been determined based on the average market volatility in exchangerates, using standard deviation, in the previous periods (for the periods ended May 31, 2018,2017 and 2016) at a 68% confidence level.

- 17 -

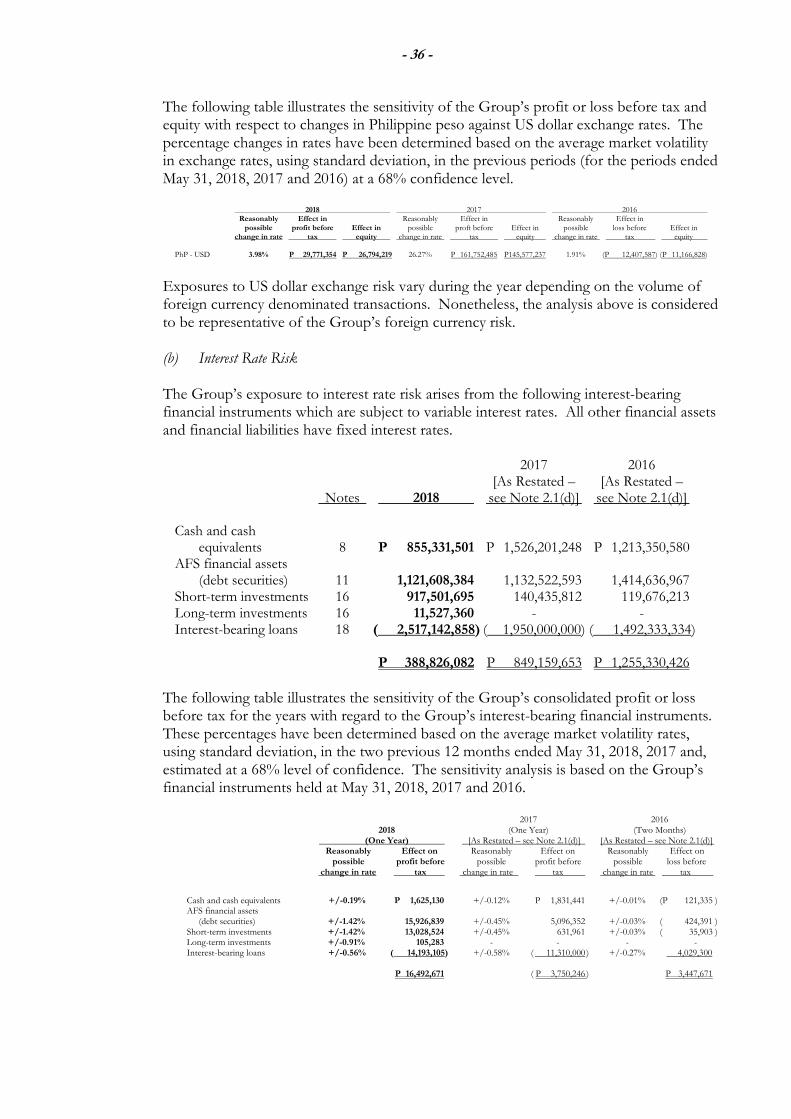

May 31, 2018 May 31, 2017 May 31, 2016Reasonably Effect in Reasonably Effect in Reasonably Effect in

possible profit before Effect in possible proft before Effect in possible loss before Effect inchange in rate tax equity change in rate tax equity change in rate tax equity

PhP - USD 3.98% P 29,771,354 P 26,794,219 26.27% P 161,752,485 P145,577,237 1.91% (P 12,407,587) (P 11,166,828)

Exposures to US dollar exchange risk vary during the year depending on the volume of foreigncurrency denominated transactions. Nonetheless, the analysis above is considered to berepresentative of the Group’s foreign currency risk.

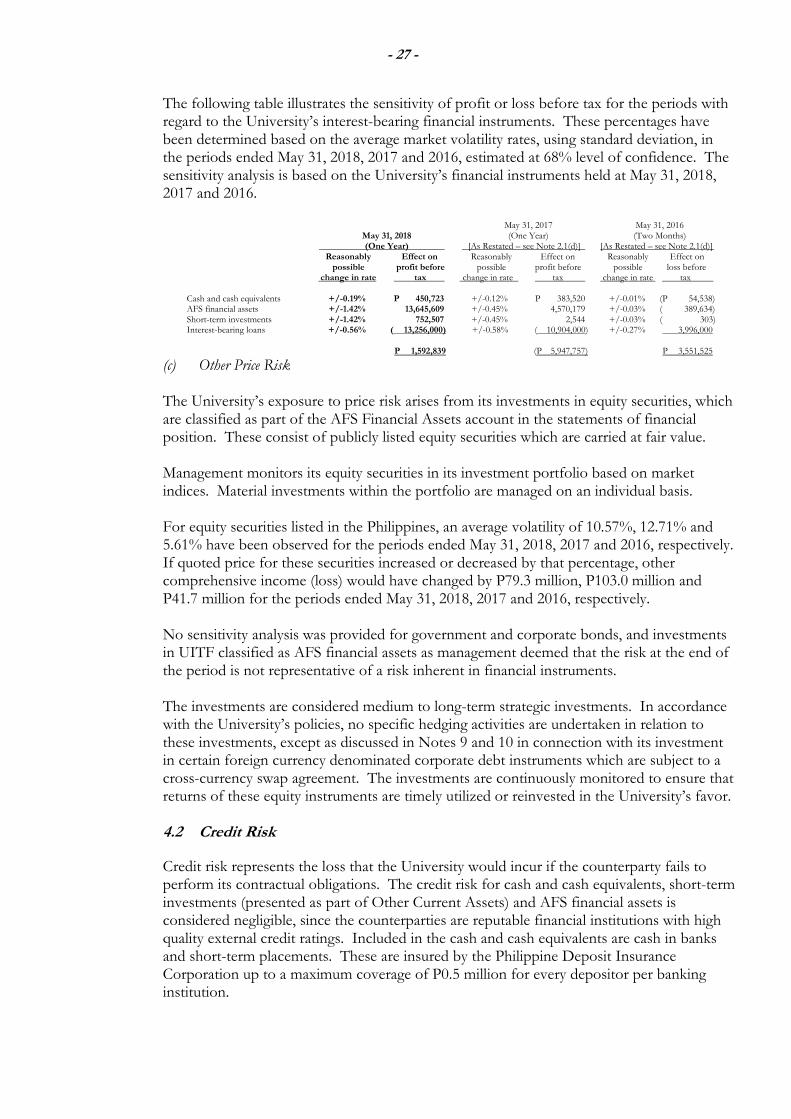

Interest Rate Risk

The Group’s exposure to interest rate risk arises from the following interest-bearing financialinstruments which are subject to variable interest rates. All other financial assets and financialliabilities have fixed interest rates.

2017 20162018 (As Restated) (As Restated)

Cash and cashequivalents P 855,331,501 P 1,526,201,248 P 1,213,350,580

AFS financial assets(debt securities) 1,121,608,384 1,132,522,593 1,414,636,967

Short-term investments 917,501,695 140,435,812 119,676,213Long-term investments 11,527,360 - -Interest-bearing loans ( 2,517,142,858) ( 1,950,000,000) ( 1,492,333,334)

P 388,826,082 P 849,159,653 P 1,255,330,426

The following table illustrates the sensitivity of the Group’s consolidated profit or loss before taxfor the years with regard to the Group’s interest-bearing financial instruments. Thesepercentages have been determined based on the average market volatility rates, using standarddeviation, in the two previous 12 months ended May 31, 2018, 2017 and, estimated at a 68%level of confidence. The sensitivity analysis is based on the Group’s financial instruments heldat May 31, 2018, 2017 and 2016.

May 31, 2018 May 31, 2017 May 31, 2016(One Year) (One Year0 (One Year)

Reasonably Effect on Reasonably Effect on Reasonably Effect onpossible profit before possible profit before possible loss before

change in rate tax change in rate tax change in rate tax

Cash and cash equivalents +/-0.19% P 1,625,130 +/-0.12% P 1,831,441 +/-0.01% (P 121,335 )AFS financial assets

(debt securities) +/-1.42% 15,926,839 +/-0.45% 5,096,352 +/-0.03% ( 424,391 )Short-term investments +/-1.42% 13,028,524 +/-0.45% 631,961 +/-0.03% ( 35,903 )Long-term investments +/-0.91% 105,283 - - - -Interest-bearing loans +/-0.56% ( 14,193,105) +/-0.58% ( 11,310,000) +/-0.27% 4,029,300

P 16,492,671 ( P 3,750,246) P 3,447,671

- 18 -

Other Price Risk

The Group’s exposure to price risk arises from its investments in equity securities, which areclassified as part of the AFS Financial Assets account in the consolidated statements of financialposition. These consist of publicly-listed equity securities which are carried at fair value.

Management monitors its equity securities in its investment portfolio based on market indices.Material investments within the portfolio are managed on an individual basis.

For equity securities listed in the Philippines, an average volatility of 10.57%, 12.71% and 5.61%have been observed for the periods ended May 31, 2018, 2017 and 2016, respectively. If quotedprices for these securities increased or decreased by that percentage, other comprehensiveincome (loss) would have changed by P79.8 million, P105.6 million and P42.3 million for theperiods ended May 31, 2018, 2017 and 2016, respectively.

No sensitivity analysis was provided for government and corporate bonds, and investments inUITF classified as AFS financial assets as management deemed that the risk at the end of theperiod is not representative of a risk inherent in financial instruments.

The investments are considered medium to long-term strategic investments. In accordancewith the Group’s policies, no specific hedging activities are undertaken in relation to theseinvestments, except as discussed in Notes 10 and 11 of the consolidated financial statements,in connection with its investment in certain foreign currency denominated corporate debtinstruments which are also subject to a cross-currency swap agreement. The investments arecontinuously monitored to ensure that returns of these equity instruments are timely utilized orreinvested in the Group’s favor.

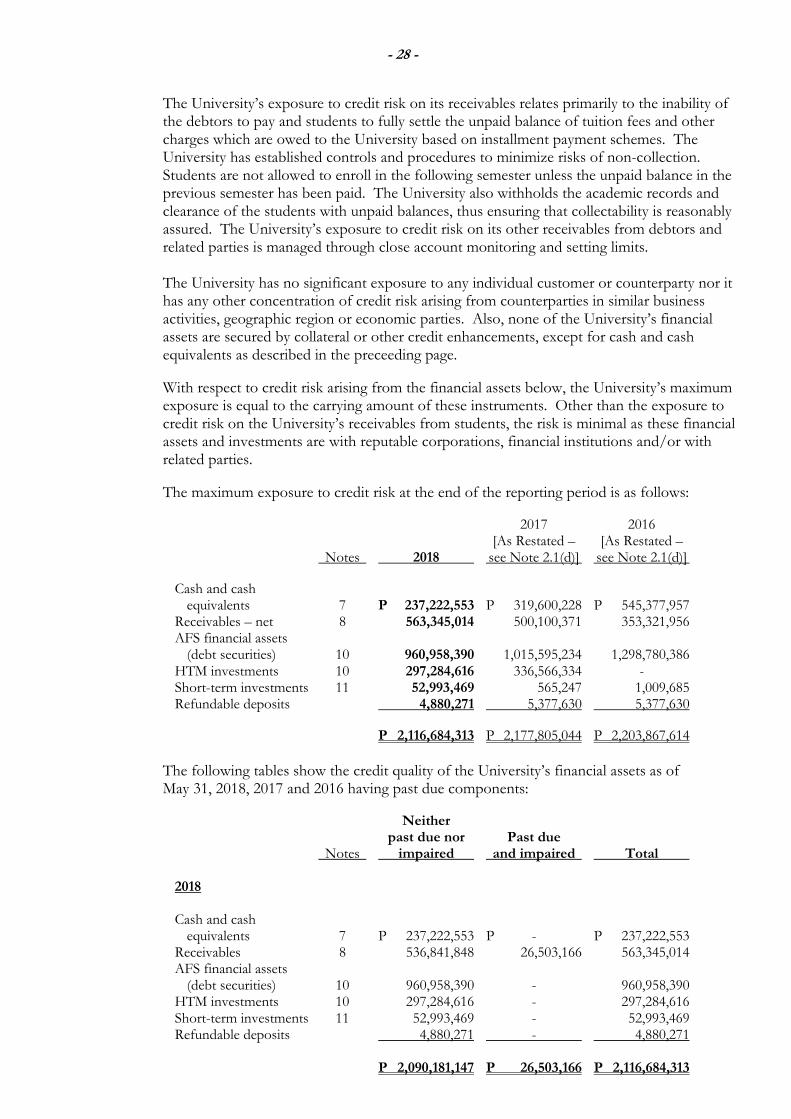

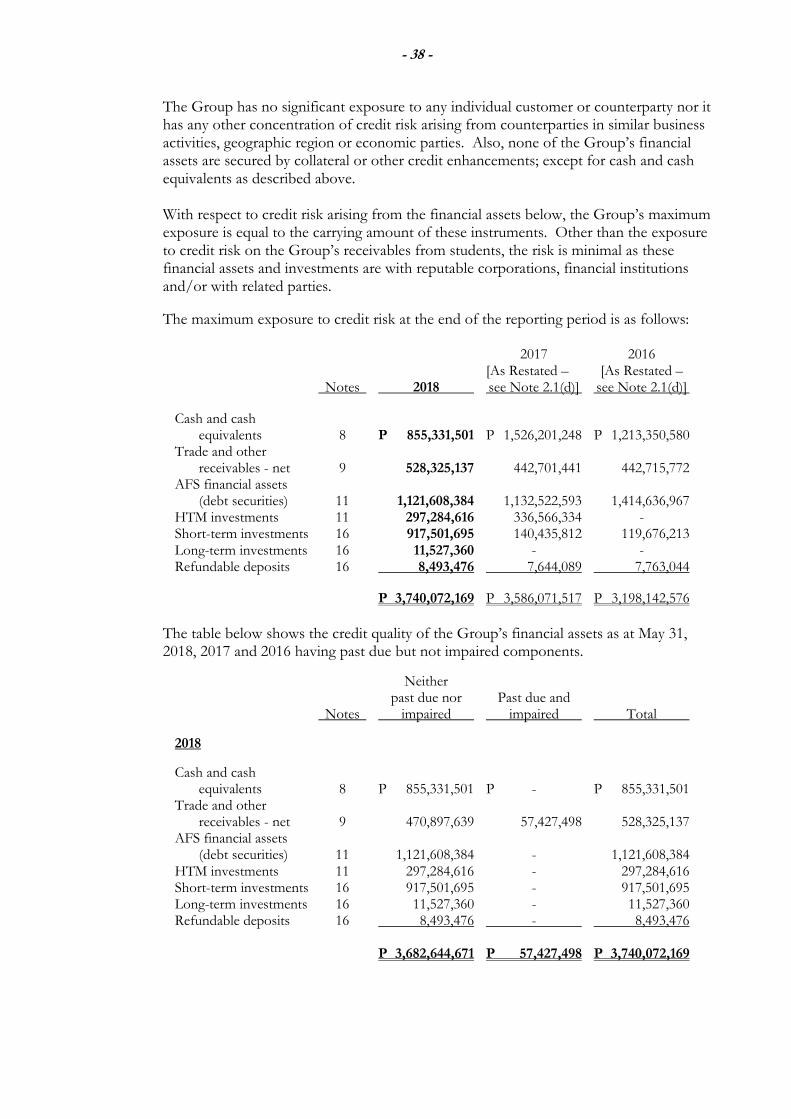

Credit Risk

Credit risk represents the loss that the Group would incur if the counterparty fails to perform itscontractual obligations. The credit risk for cash and cash equivalents, short-term investments(presented as part of Other Current Assets), AFS financial assets and HTM investments isconsidered negligible, since the counterparties are reputable financial institutions and privatecompanies with high quality external credit ratings. Included in the cash and cash equivalents arecash in banks and short-term placements. These are insured by the Philippine Deposit InsuranceCorporation up to a maximum coverage of P0.5 million for every depositor per banking institution.

The Group’s exposure to credit risk on its receivables related primarily to the inability of the debtorsto pay and students to fully settle the unpaid balance of tuition fees and other charges which areowed to the Group based on installment payment schemes. The Group has established controlsand procedures to minimize risks of non-collection. Students are not allowed to enroll in thefollowing semester unless the unpaid balance in the previous semester has been paid. The Groupalso withholds the academic records and clearance of the students with unpaid balances, thusensuring that collectability is reasonably assured. The Group’s exposure to credit risk on its otherreceivables from debtors and related parties is managed through close account monitoring andsetting limits.

- 19 -

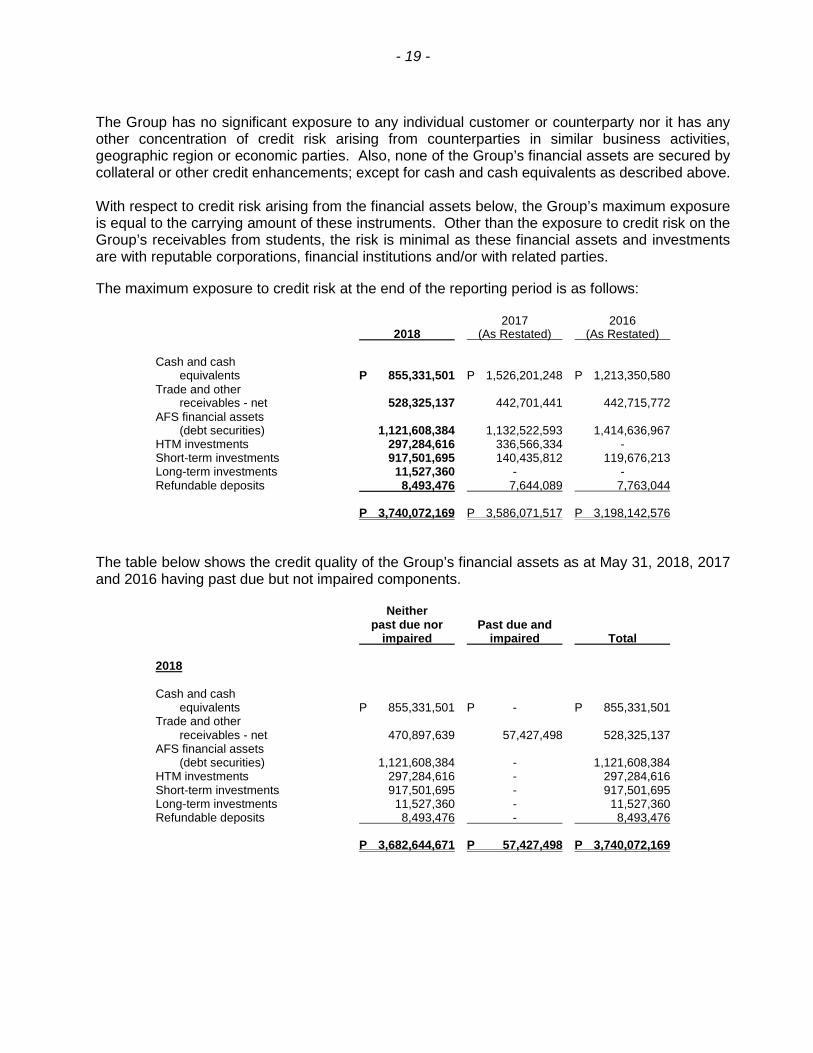

The Group has no significant exposure to any individual customer or counterparty nor it has anyother concentration of credit risk arising from counterparties in similar business activities,geographic region or economic parties. Also, none of the Group’s financial assets are secured bycollateral or other credit enhancements; except for cash and cash equivalents as described above.

With respect to credit risk arising from the financial assets below, the Group’s maximum exposureis equal to the carrying amount of these instruments. Other than the exposure to credit risk on theGroup’s receivables from students, the risk is minimal as these financial assets and investmentsare with reputable corporations, financial institutions and/or with related parties.

The maximum exposure to credit risk at the end of the reporting period is as follows:

2017 20162018 (As Restated) (As Restated)

Cash and cashequivalents P 855,331,501 P 1,526,201,248 P 1,213,350,580

Trade and otherreceivables - net 528,325,137 442,701,441 442,715,772

AFS financial assets(debt securities) 1,121,608,384 1,132,522,593 1,414,636,967

HTM investments 297,284,616 336,566,334 -Short-term investments 917,501,695 140,435,812 119,676,213Long-term investments 11,527,360 - -Refundable deposits 8,493,476 7,644,089 7,763,044

P 3,740,072,169 P 3,586,071,517 P 3,198,142,576

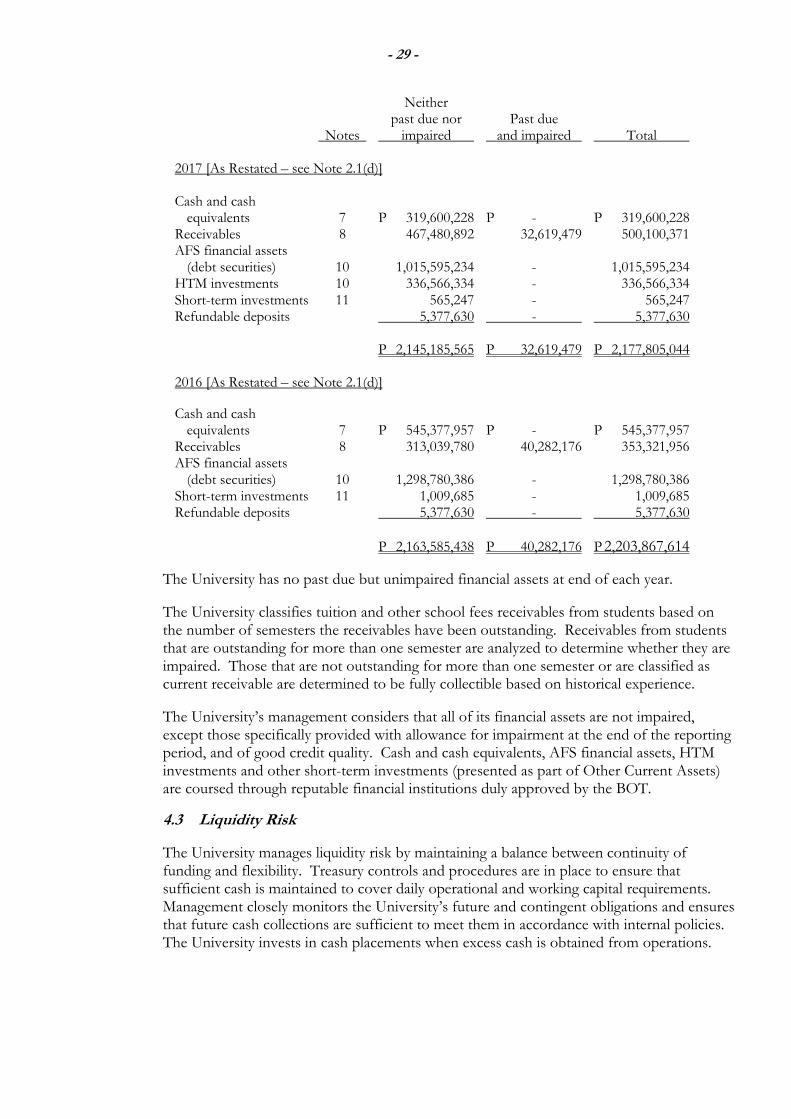

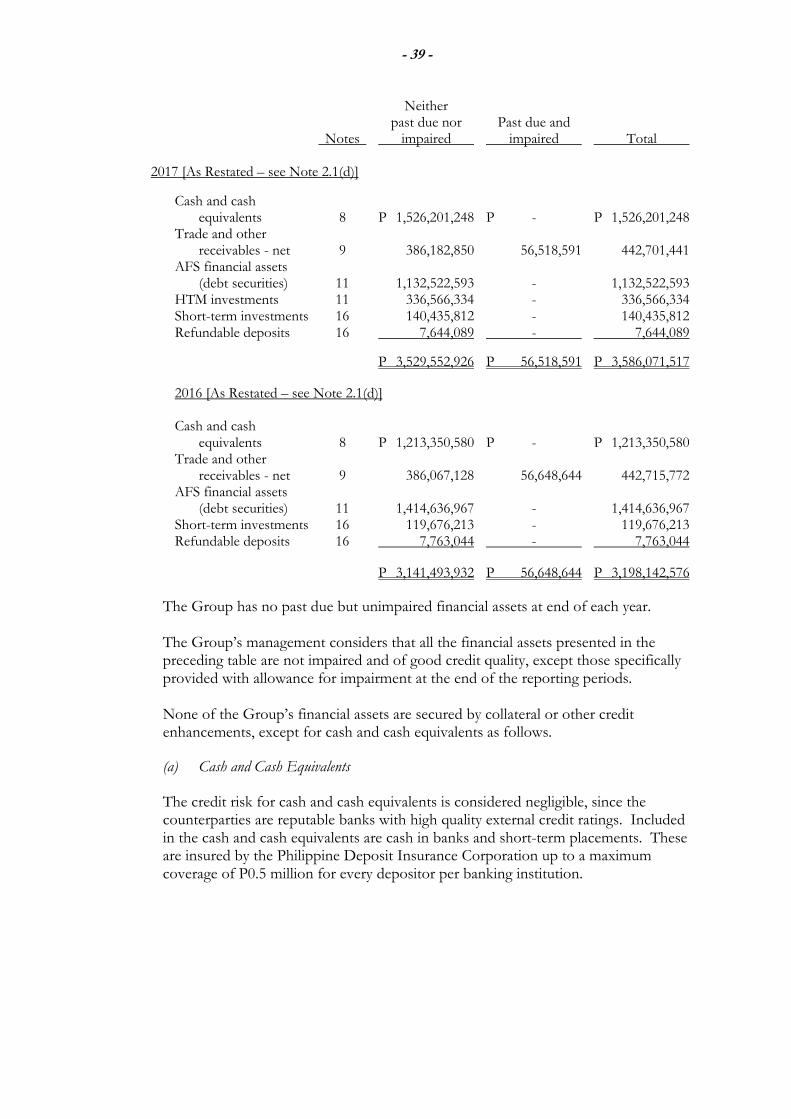

The table below shows the credit quality of the Group’s financial assets as at May 31, 2018, 2017and 2016 having past due but not impaired components.

Neitherpast due nor Past due and

impaired impaired Total

2018

Cash and cashequivalents P 855,331,501 P - P 855,331,501

Trade and otherreceivables - net 470,897,639 57,427,498 528,325,137

AFS financial assets(debt securities) 1,121,608,384 - 1,121,608,384

HTM investments 297,284,616 - 297,284,616Short-term investments 917,501,695 - 917,501,695Long-term investments 11,527,360 - 11,527,360Refundable deposits 8,493,476 - 8,493,476

P 3,682,644,671 P 57,427,498 P 3,740,072,169

- 20 -

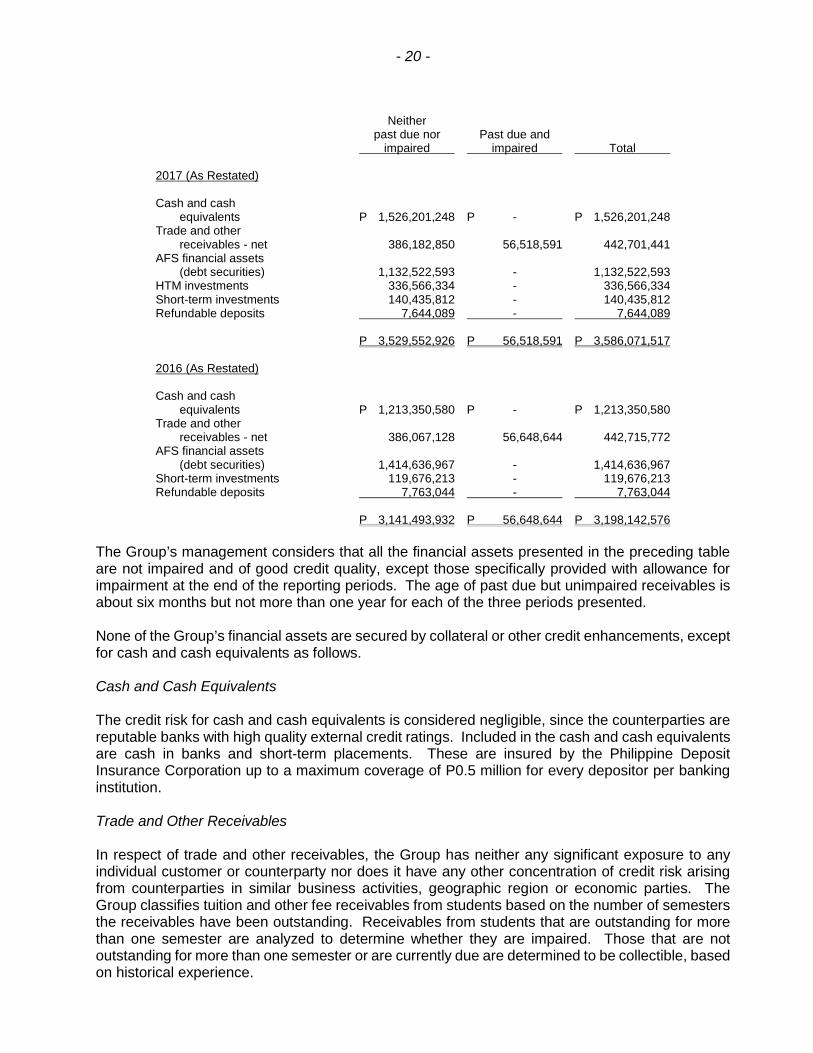

Neitherpast due nor Past due and

impaired impaired Total

2017 (As Restated)

Cash and cashequivalents P 1,526,201,248 P - P 1,526,201,248

Trade and otherreceivables - net 386,182,850 56,518,591 442,701,441

AFS financial assets(debt securities) 1,132,522,593 - 1,132,522,593

HTM investments 336,566,334 - 336,566,334Short-term investments 140,435,812 - 140,435,812Refundable deposits 7,644,089 - 7,644,089

P 3,529,552,926 P 56,518,591 P 3,586,071,517

2016 (As Restated)

Cash and cashequivalents P 1,213,350,580 P - P 1,213,350,580

Trade and otherreceivables - net 386,067,128 56,648,644 442,715,772

AFS financial assets(debt securities) 1,414,636,967 - 1,414,636,967

Short-term investments 119,676,213 - 119,676,213Refundable deposits 7,763,044 - 7,763,044

P 3,141,493,932 P 56,648,644 P 3,198,142,576

The Group’s management considers that all the financial assets presented in the preceding tableare not impaired and of good credit quality, except those specifically provided with allowance forimpairment at the end of the reporting periods. The age of past due but unimpaired receivables isabout six months but not more than one year for each of the three periods presented.

None of the Group’s financial assets are secured by collateral or other credit enhancements, exceptfor cash and cash equivalents as follows.

Cash and Cash Equivalents

The credit risk for cash and cash equivalents is considered negligible, since the counterparties arereputable banks with high quality external credit ratings. Included in the cash and cash equivalentsare cash in banks and short-term placements. These are insured by the Philippine DepositInsurance Corporation up to a maximum coverage of P0.5 million for every depositor per bankinginstitution.

Trade and Other Receivables

In respect of trade and other receivables, the Group has neither any significant exposure to anyindividual customer or counterparty nor does it have any other concentration of credit risk arisingfrom counterparties in similar business activities, geographic region or economic parties. TheGroup classifies tuition and other fee receivables from students based on the number of semestersthe receivables have been outstanding. Receivables from students that are outstanding for morethan one semester are analyzed to determine whether they are impaired. Those that are notoutstanding for more than one semester or are currently due are determined to be collectible, basedon historical experience.

- 21 -

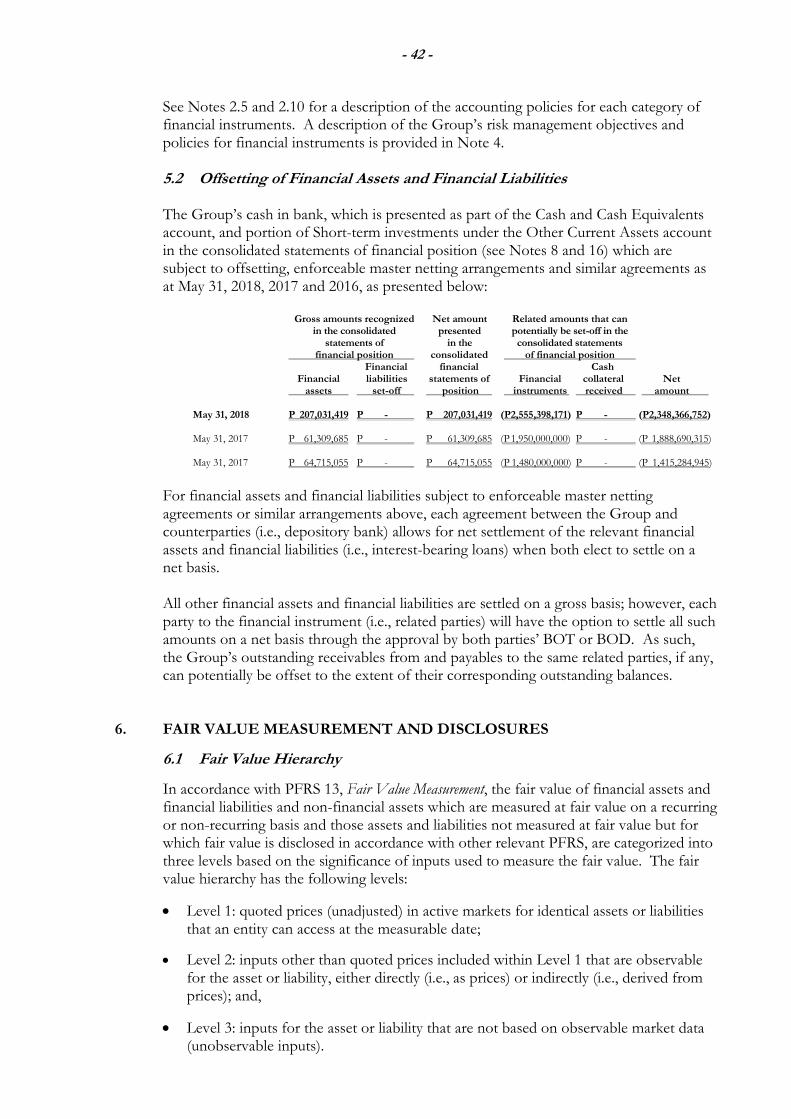

Financial Assets at FVTL and AFS Financial Assets

AFS financial assets and HTM investments are coursed through reputable financial institutions andprivate corporations duly approved by the BOT of the University and BOD of the subsidiaries.

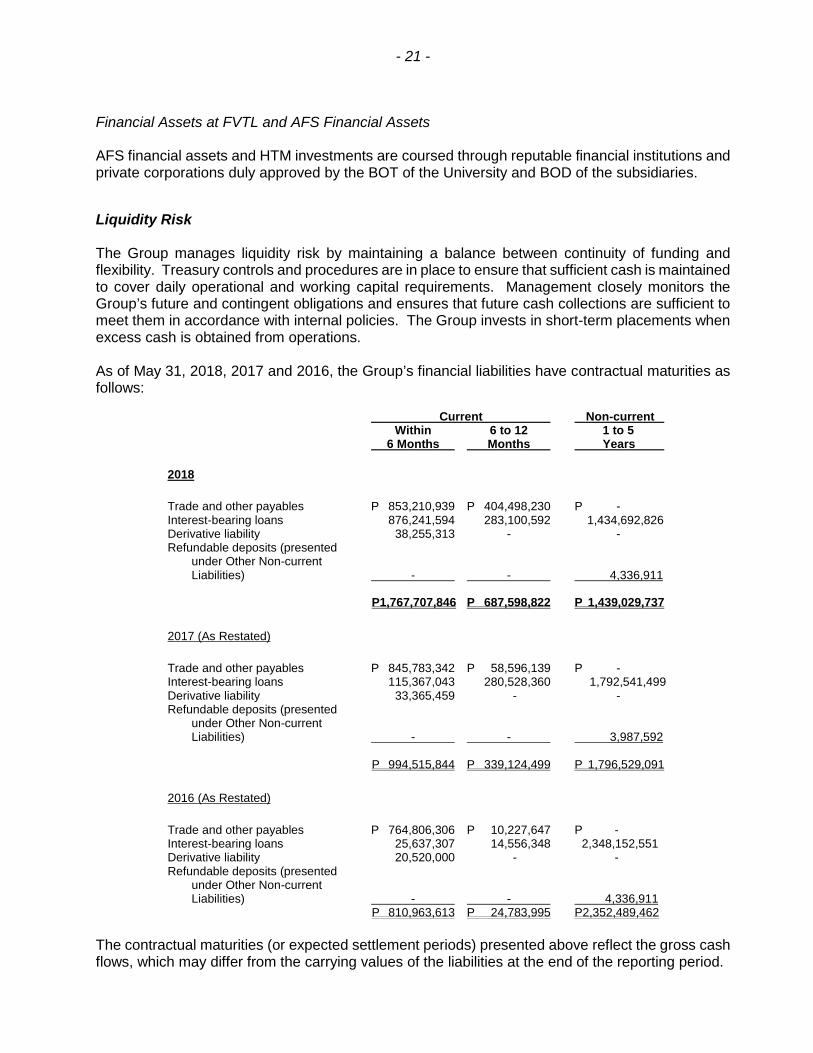

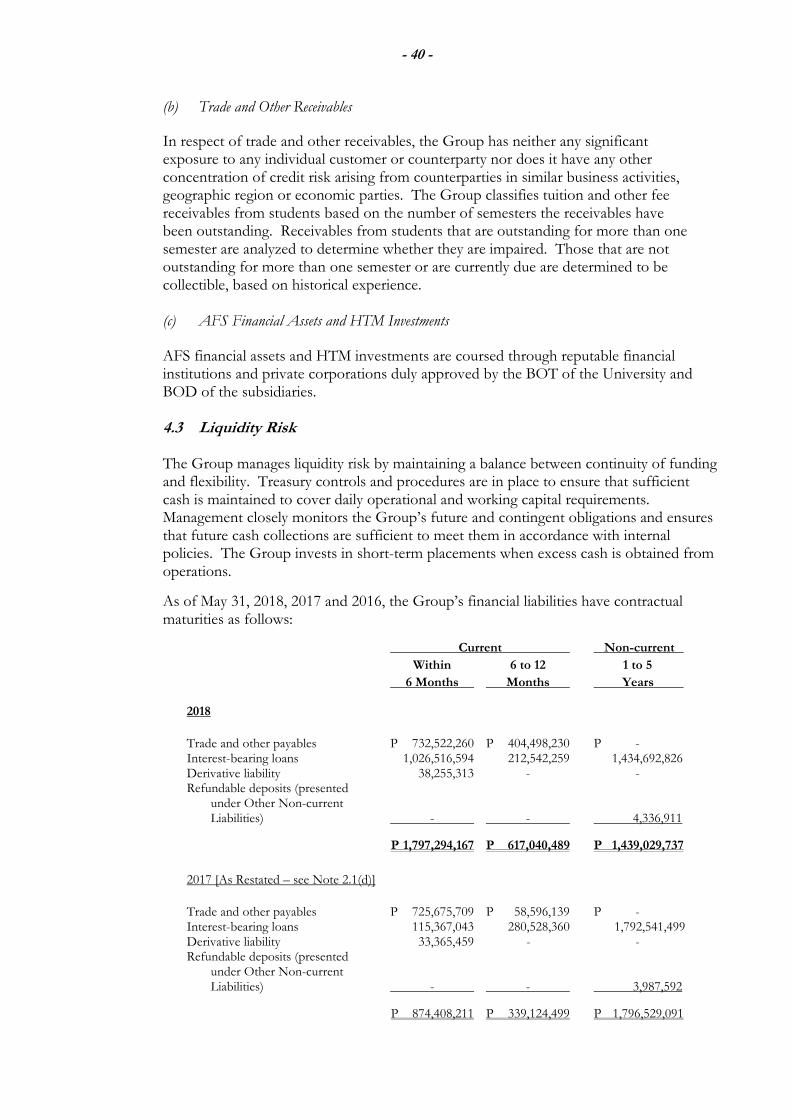

Liquidity Risk

The Group manages liquidity risk by maintaining a balance between continuity of funding andflexibility. Treasury controls and procedures are in place to ensure that sufficient cash is maintainedto cover daily operational and working capital requirements. Management closely monitors theGroup’s future and contingent obligations and ensures that future cash collections are sufficient tomeet them in accordance with internal policies. The Group invests in short-term placements whenexcess cash is obtained from operations.

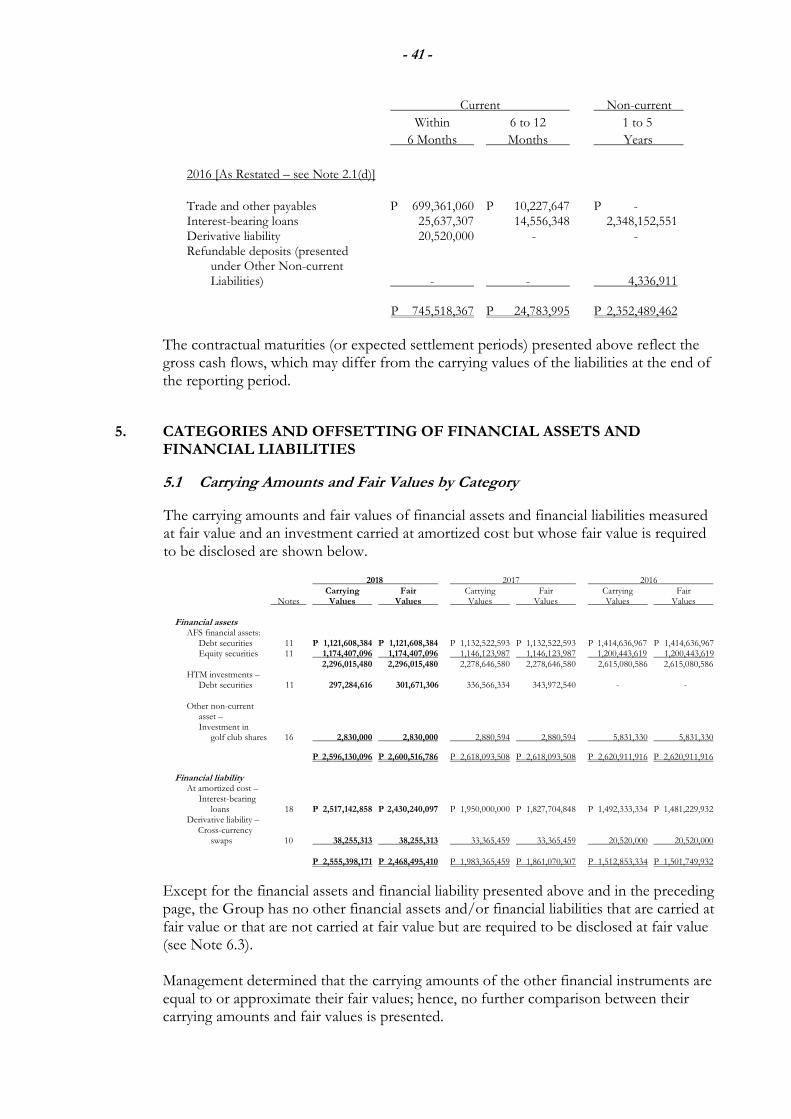

As of May 31, 2018, 2017 and 2016, the Group’s financial liabilities have contractual maturities asfollows:

Current Non-currentWithin 6 to 12 1 to 5

6 Months Months Years

2018

Trade and other payables P 853,210,939 P 404,498,230 P -Interest-bearing loans 876,241,594 283,100,592 1,434,692,826Derivative liability 38,255,313 - -Refundable deposits (presented

under Other Non-currentLiabilities) - - 4,336,911

P1,767,707,846 P 687,598,822 P 1,439,029,737

2017 (As Restated)

Trade and other payables P 845,783,342 P 58,596,139 P -Interest-bearing loans 115,367,043 280,528,360 1,792,541,499Derivative liability 33,365,459 - -Refundable deposits (presented

under Other Non-currentLiabilities) - - 3,987,592

P 994,515,844 P 339,124,499 P 1,796,529,091

2016 (As Restated)

Trade and other payables P 764,806,306 P 10,227,647 P -Interest-bearing loans 25,637,307 14,556,348 2,348,152,551Derivative liability 20,520,000 - -Refundable deposits (presented

under Other Non-currentLiabilities) - - 4,336,911

P 810,963,613 P 24,783,995 P2,352,489,462

The contractual maturities (or expected settlement periods) presented above reflect the gross cashflows, which may differ from the carrying values of the liabilities at the end of the reporting period.

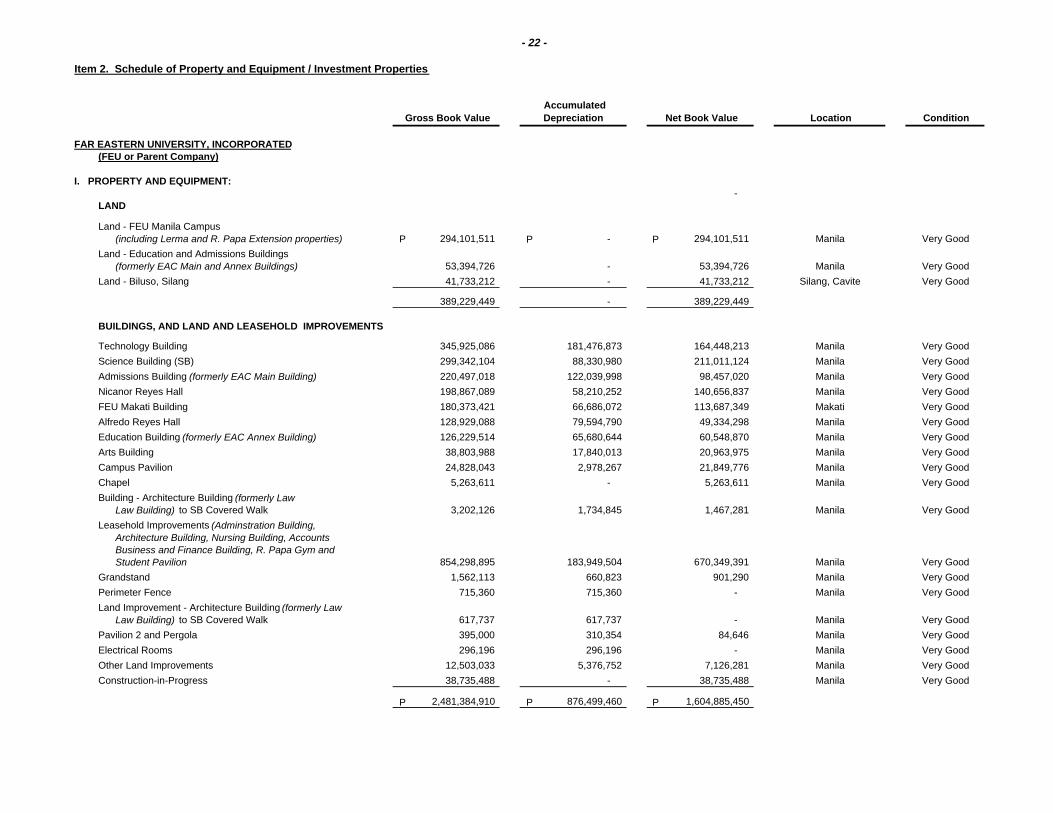

Item 2. Schedule of Property and Equipment / Investment Properties

Gross Book Value AccumulatedDepreciation Net Book Value Location Condition

FAR EASTERN UNIVERSITY, INCORPORATED(FEU or Parent Company)

I. PROPERTY AND EQUIPMENT:-

LAND

Land - FEU Manila Campus(including Lerma and R. Papa Extension properties) 294,101,511 - 294,101,511 Manila Very Good

Land - Education and Admissions Buildings(formerly EAC Main and Annex Buildings) 53,394,726 - 53,394,726 Manila Very Good

Land - Biluso, Silang 41,733,212 - 41,733,212 Silang, Cavite Very Good

389,229,449 - 389,229,449

BUILDINGS, AND LAND AND LEASEHOLD IMPROVEMENTS

Technology Building 345,925,086 181,476,873 164,448,213 Manila Very GoodScience Building (SB) 299,342,104 88,330,980 211,011,124 Manila Very GoodAdmissions Building (formerly EAC Main Building) 220,497,018 122,039,998 98,457,020 Manila Very GoodNicanor Reyes Hall 198,867,089 58,210,252 140,656,837 Manila Very GoodFEU Makati Building 180,373,421 66,686,072 113,687,349 Makati Very GoodAlfredo Reyes Hall 128,929,088 79,594,790 49,334,298 Manila Very GoodEducation Building (formerly EAC Annex Building) 126,229,514 65,680,644 60,548,870 Manila Very GoodArts Building 38,803,988 17,840,013 20,963,975 Manila Very GoodCampus Pavilion 24,828,043 2,978,267 21,849,776 Manila Very GoodChapel 5,263,611 - 5,263,611 Manila Very GoodBuilding - Architecture Building (formerly Law

Law Building) to SB Covered Walk 3,202,126 1,734,845 1,467,281 Manila Very GoodLeasehold Improvements (Adminstration Building,

Architecture Building, Nursing Building, AccountsBusiness and Finance Building, R. Papa Gym andStudent Pavilion 854,298,895 183,949,504 670,349,391 Manila Very Good

Grandstand 1,562,113 660,823 901,290 Manila Very GoodPerimeter Fence 715,360 715,360 - Manila Very GoodLand Improvement - Architecture Building (formerly Law

Law Building) to SB Covered Walk 617,737 617,737 - Manila Very GoodPavilion 2 and Pergola 395,000 310,354 84,646 Manila Very GoodElectrical Rooms 296,196 296,196 - Manila Very GoodOther Land Improvements 12,503,033 5,376,752 7,126,281 Manila Very GoodConstruction-in-Progress 38,735,488 - 38,735,488 Manila Very Good

2,481,384,910 876,499,460 1,604,885,450

- 22 -

P P P

P P P

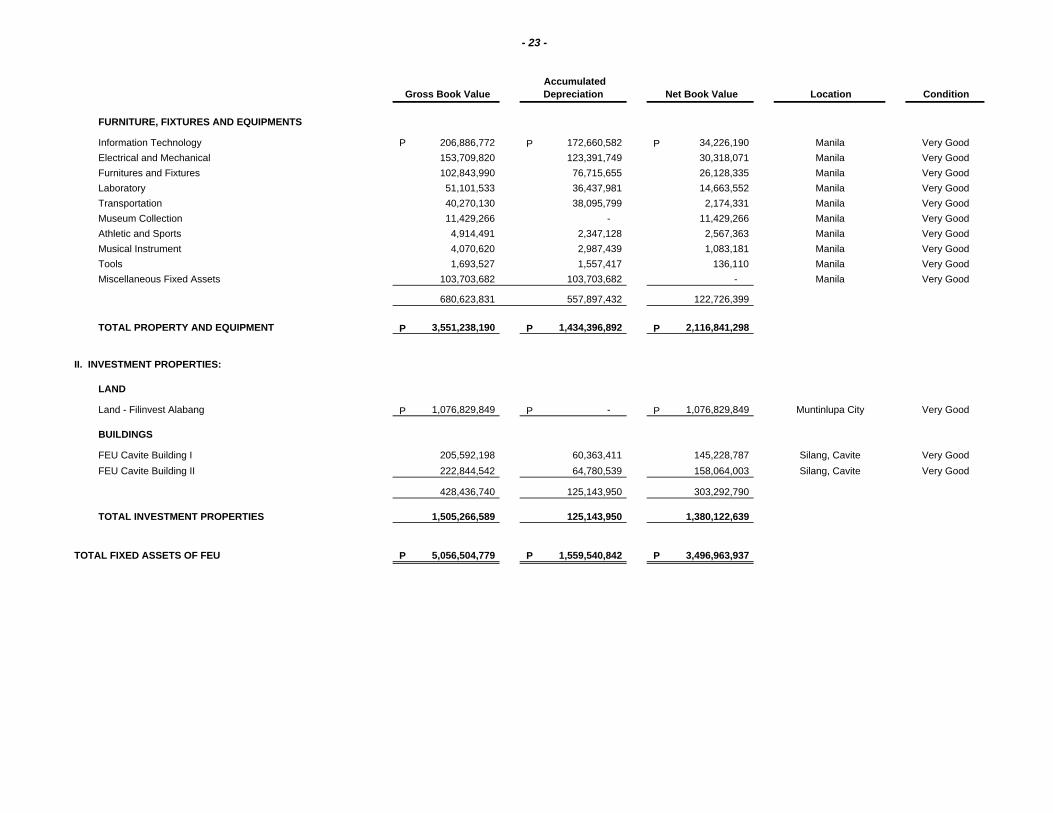

Gross Book Value AccumulatedDepreciation Net Book Value Location Condition

FURNITURE, FIXTURES AND EQUIPMENTS

Information Technology 206,886,772 172,660,582 34,226,190 Manila Very GoodElectrical and Mechanical 153,709,820 123,391,749 30,318,071 Manila Very GoodFurnitures and Fixtures 102,843,990 76,715,655 26,128,335 Manila Very GoodLaboratory 51,101,533 36,437,981 14,663,552 Manila Very GoodTransportation 40,270,130 38,095,799 2,174,331 Manila Very GoodMuseum Collection 11,429,266 - 11,429,266 Manila Very GoodAthletic and Sports 4,914,491 2,347,128 2,567,363 Manila Very GoodMusical Instrument 4,070,620 2,987,439 1,083,181 Manila Very GoodTools 1,693,527 1,557,417 136,110 Manila Very GoodMiscellaneous Fixed Assets 103,703,682 103,703,682 - Manila Very Good

680,623,831 557,897,432 122,726,399

TOTAL PROPERTY AND EQUIPMENT 3,551,238,190 1,434,396,892 2,116,841,298

II. INVESTMENT PROPERTIES:

LAND

Land - Filinvest Alabang 1,076,829,849 - 1,076,829,849 Muntinlupa City Very Good

BUILDINGS

FEU Cavite Building I 205,592,198 60,363,411 145,228,787 Silang, Cavite Very GoodFEU Cavite Building II 222,844,542 64,780,539 158,064,003 Silang, Cavite Very Good

428,436,740 125,143,950 303,292,790

TOTAL INVESTMENT PROPERTIES 1,505,266,589 125,143,950 1,380,122,639

TOTAL FIXED ASSETS OF FEU 5,056,504,779 1,559,540,842 3,496,963,937

- 23 -

P P P

P P P

P P P

P P P

Gross Book Value AccumulatedDepreciation Net Book Value Location Condition

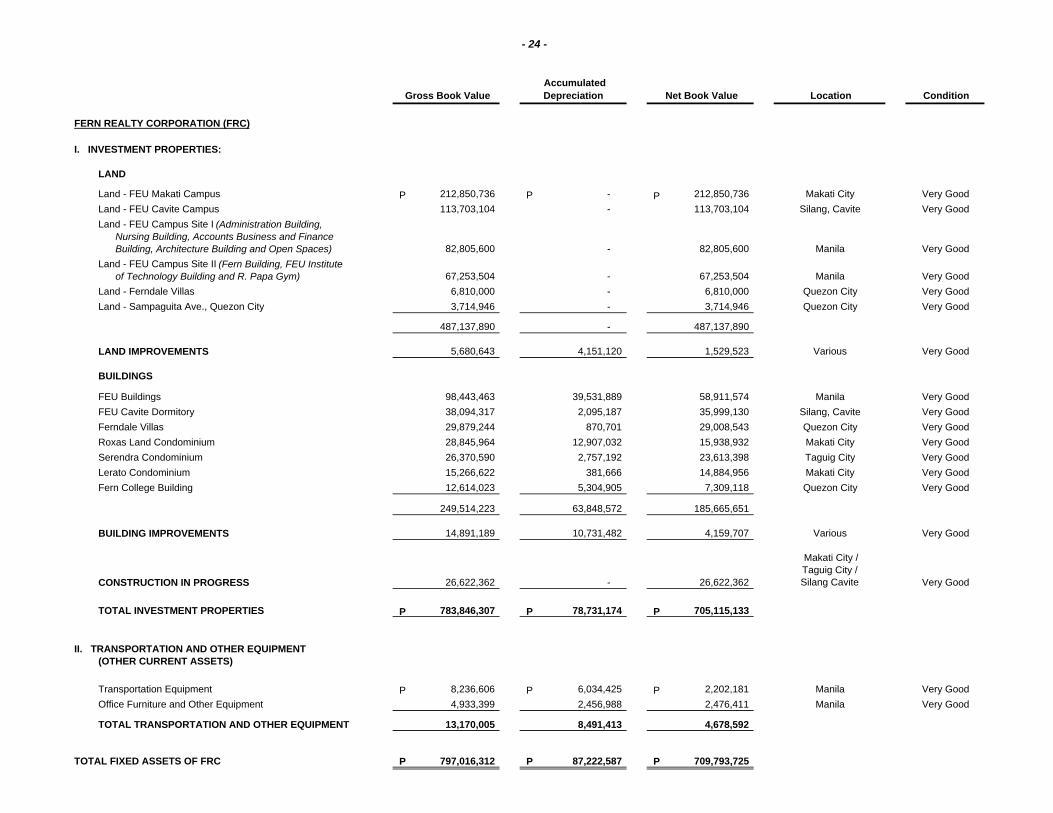

FERN REALTY CORPORATION (FRC)

I. INVESTMENT PROPERTIES:

LAND

Land - FEU Makati Campus 212,850,736 - 212,850,736 Makati City Very GoodLand - FEU Cavite Campus 113,703,104 - 113,703,104 Silang, Cavite Very GoodLand - FEU Campus Site I (Administration Building,

Nursing Building, Accounts Business and FinanceBuilding, Architecture Building and Open Spaces) 82,805,600 - 82,805,600 Manila Very Good

Land - FEU Campus Site II (Fern Building, FEU Instituteof Technology Building and R. Papa Gym) 67,253,504 - 67,253,504 Manila Very Good

Land - Ferndale Villas 6,810,000 - 6,810,000 Quezon City Very GoodLand - Sampaguita Ave., Quezon City 3,714,946 - 3,714,946 Quezon City Very Good

487,137,890 - 487,137,890

LAND IMPROVEMENTS 5,680,643 4,151,120 1,529,523 Various Very Good

BUILDINGS

FEU Buildings 98,443,463 39,531,889 58,911,574 Manila Very GoodFEU Cavite Dormitory 38,094,317 2,095,187 35,999,130 Silang, Cavite Very GoodFerndale Villas 29,879,244 870,701 29,008,543 Quezon City Very GoodRoxas Land Condominium 28,845,964 12,907,032 15,938,932 Makati City Very GoodSerendra Condominium 26,370,590 2,757,192 23,613,398 Taguig City Very GoodLerato Condominium 15,266,622 381,666 14,884,956 Makati City Very GoodFern College Building 12,614,023 5,304,905 7,309,118 Quezon City Very Good

249,514,223 63,848,572 185,665,651

BUILDING IMPROVEMENTS 14,891,189 10,731,482 4,159,707 Various Very Good

CONSTRUCTION IN PROGRESS 26,622,362 - 26,622,362

Makati City /Taguig City /Silang Cavite Very Good

TOTAL INVESTMENT PROPERTIES 783,846,307 78,731,174 705,115,133

II. TRANSPORTATION AND OTHER EQUIPMENT(OTHER CURRENT ASSETS)

Transportation Equipment 8,236,606 6,034,425 2,202,181 Manila Very GoodOffice Furniture and Other Equipment 4,933,399 2,456,988 2,476,411 Manila Very Good

TOTAL TRANSPORTATION AND OTHER EQUIPMENT 13,170,005 8,491,413 4,678,592

TOTAL FIXED ASSETS OF FRC 797,016,312 87,222,587 709,793,725

- 24 -

P P P

P P P

P P P

P P P

Gross Book Value AccumulatedDepreciation Net Book Value Location Condition

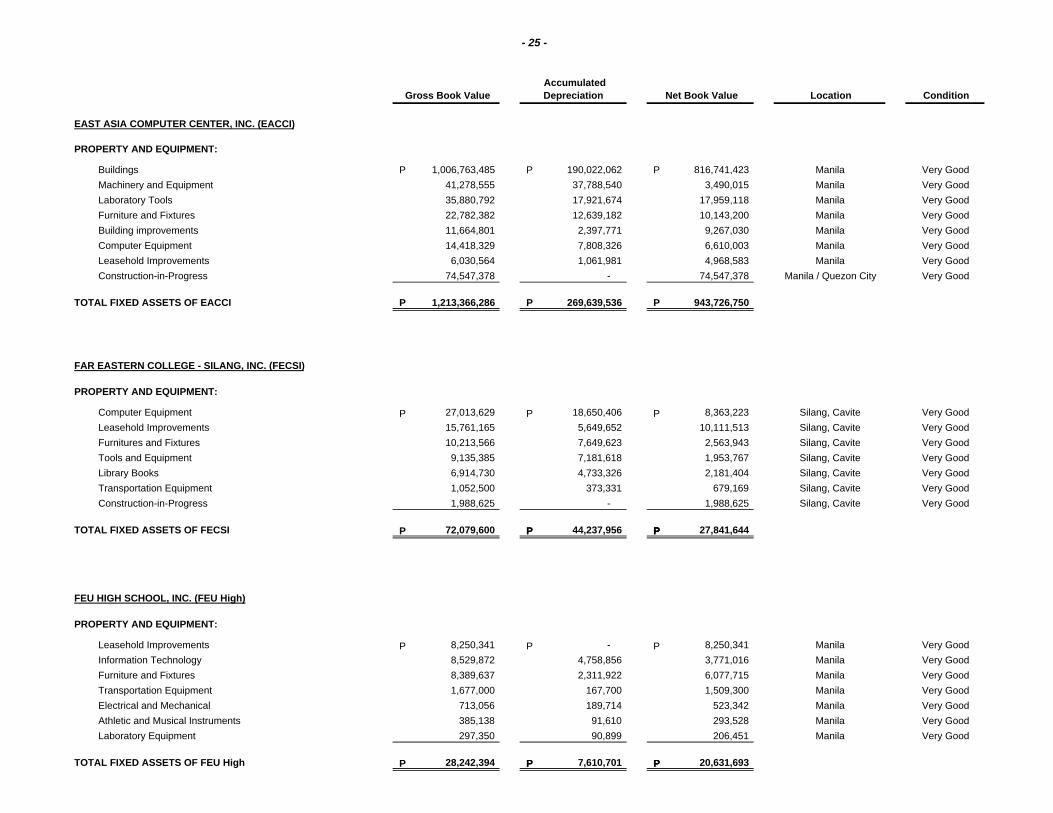

EAST ASIA COMPUTER CENTER, INC. (EACCI)

PROPERTY AND EQUIPMENT:

Buildings 1,006,763,485 190,022,062 816,741,423 Manila Very GoodMachinery and Equipment 41,278,555 37,788,540 3,490,015 Manila Very GoodLaboratory Tools 35,880,792 17,921,674 17,959,118 Manila Very GoodFurniture and Fixtures 22,782,382 12,639,182 10,143,200 Manila Very GoodBuilding improvements 11,664,801 2,397,771 9,267,030 Manila Very GoodComputer Equipment 14,418,329 7,808,326 6,610,003 Manila Very GoodLeasehold Improvements 6,030,564 1,061,981 4,968,583 Manila Very GoodConstruction-in-Progress 74,547,378 - 74,547,378 Manila / Quezon City Very Good

TOTAL FIXED ASSETS OF EACCI 1,213,366,286 269,639,536 943,726,750

FAR EASTERN COLLEGE - SILANG, INC. (FECSI)

PROPERTY AND EQUIPMENT:

Computer Equipment 27,013,629 18,650,406 8,363,223 Silang, Cavite Very GoodLeasehold Improvements 15,761,165 5,649,652 10,111,513 Silang, Cavite Very GoodFurnitures and Fixtures 10,213,566 7,649,623 2,563,943 Silang, Cavite Very GoodTools and Equipment 9,135,385 7,181,618 1,953,767 Silang, Cavite Very GoodLibrary Books 6,914,730 4,733,326 2,181,404 Silang, Cavite Very GoodTransportation Equipment 1,052,500 373,331 679,169 Silang, Cavite Very GoodConstruction-in-Progress 1,988,625 - 1,988,625 Silang, Cavite Very Good

TOTAL FIXED ASSETS OF FECSI 72,079,600 44,237,956 27,841,644

FEU HIGH SCHOOL, INC. (FEU High)

PROPERTY AND EQUIPMENT:

Leasehold Improvements 8,250,341 - 8,250,341 Manila Very GoodInformation Technology 8,529,872 4,758,856 3,771,016 Manila Very GoodFurniture and Fixtures 8,389,637 2,311,922 6,077,715 Manila Very GoodTransportation Equipment 1,677,000 167,700 1,509,300 Manila Very GoodElectrical and Mechanical 713,056 189,714 523,342 Manila Very GoodAthletic and Musical Instruments 385,138 91,610 293,528 Manila Very GoodLaboratory Equipment 297,350 90,899 206,451 Manila Very Good

TOTAL FIXED ASSETS OF FEU High 28,242,394 7,610,701 20,631,693

- 25 -

P P P

P P P

P P P

P P P

P P P

P P P

P PP

P PP

Gross Book Value AccumulatedDepreciation Net Book Value Location Condition

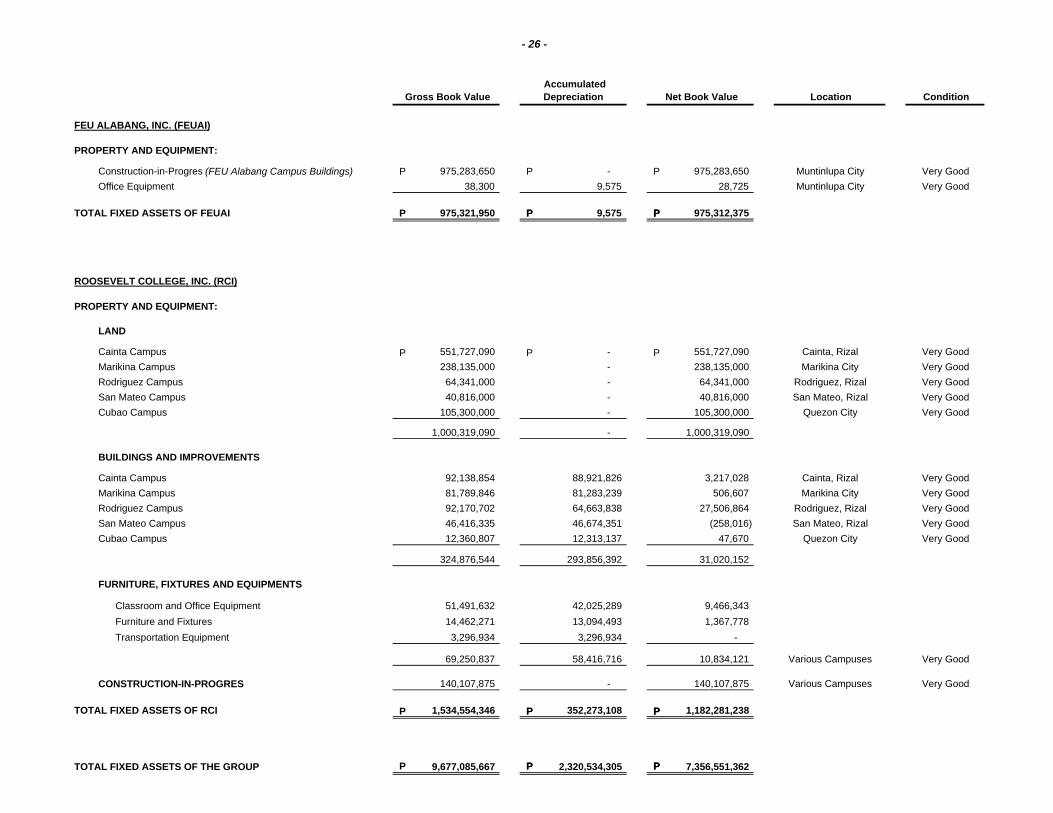

FEU ALABANG, INC. (FEUAI)

PROPERTY AND EQUIPMENT:

Construction-in-Progres (FEU Alabang Campus Buildings) 975,283,650 - 975,283,650 Muntinlupa City Very GoodOffice Equipment 38,300 9,575 28,725 Muntinlupa City Very Good

TOTAL FIXED ASSETS OF FEUAI 975,321,950 9,575 975,312,375

ROOSEVELT COLLEGE, INC. (RCI)

PROPERTY AND EQUIPMENT:

LAND

Cainta Campus 551,727,090 - 551,727,090 Cainta, Rizal Very GoodMarikina Campus 238,135,000 - 238,135,000 Marikina City Very GoodRodriguez Campus 64,341,000 - 64,341,000 Rodriguez, Rizal Very GoodSan Mateo Campus 40,816,000 - 40,816,000 San Mateo, Rizal Very GoodCubao Campus 105,300,000 - 105,300,000 Quezon City Very Good

1,000,319,090 - 1,000,319,090

BUILDINGS AND IMPROVEMENTS

Cainta Campus 92,138,854 88,921,826 3,217,028 Cainta, Rizal Very GoodMarikina Campus 81,789,846 81,283,239 506,607 Marikina City Very GoodRodriguez Campus 92,170,702 64,663,838 27,506,864 Rodriguez, Rizal Very GoodSan Mateo Campus 46,416,335 46,674,351 (258,016) San Mateo, Rizal Very GoodCubao Campus 12,360,807 12,313,137 47,670 Quezon City Very Good

324,876,544 293,856,392 31,020,152

FURNITURE, FIXTURES AND EQUIPMENTS

Classroom and Office Equipment 51,491,632 42,025,289 9,466,343Furniture and Fixtures 14,462,271 13,094,493 1,367,778Transportation Equipment 3,296,934 3,296,934 -

69,250,837 58,416,716 10,834,121 Various Campuses Very Good

CONSTRUCTION-IN-PROGRES 140,107,875 - 140,107,875 Various Campuses Very Good

TOTAL FIXED ASSETS OF RCI 1,534,554,346 352,273,108 1,182,281,238

TOTAL FIXED ASSETS OF THE GROUP 9,677,085,667 2,320,534,305 7,356,551,362

- 26 -

P P P

P P P

P P P

P P P

P P PP PP

P PP

P PP

PROPERTY LEASED BY FEU FROM FRC:

Annual Rental Current

Contract Period

Gymnasium Two (2) storey building made of concrete materials located at 9,927,658.27 April 1, 2018 toR. Papa St., Sampaloc, Manila plus applicable VAT March 31, 2019

Athletes' Quarters Ground floor (234.44 sq. meters) of a five (5) storey building 683,911.92 December 1, 2017 tomade of concrete materials located at P. Paredes corner plus applicable VAT November 30, 2018S.H. Loyola Streets, Sampaloc, Manila

Athletes' Quarters Portion of 2nd floor (790 sq. meters) of a five (5) storey building 2,801,255.52 December 1, 2017 tomade of concrete materials located at P. Paredes corner plus applicable VAT November 30, 2018S.H. Loyola Streets, Sampaloc, Manila

FEU Makati Campus Parcel of land (2,186 sq. meters) located at the Makati Central 8,967,701.35 December 1, 2017 toBusiness District bounded by Sen. Gil Puyat Avenue, plus applicable VAT November 30, 2018Malugay Street and Geronimo Street Makati City.

FEU Fern Bookstore Portion of Ground floor (48 sq. meters) of a five (5) storey building 115,188.29 February 11, 2017 tomade of concrete materials located at Sampaguita Avenue, plus applicable VAT January 10, 2018Barangay Pason Tamo, Quezon City.

FEU-Manila Buildings:

Eight (8) storey building made of concrete materials located at 62,052,477.03 July 1, 2017 toFEU Manila Campus, Nicanor Reyest St., Manila plus applicable VAT June 30, 2018

Nursing Building Eight (8) storey building made of concrete materials located at subject to 5%FEU Manila Campus, Nicanor Reyest St., Manila escalation yearly

Architecture Building (Law Building) Four (4) storey building made of concrete materials located atFEU Manila Campus, Nicanor Reyest St., Manila

Administration Building Four (4) storey building made of concrete materials located atFEU Manila Campus, Nicanor Reyest St., Manila

- 27 -

Accounts, Business and Finance Buidling(formerly Education Building)

PROPERTY LEASED BY FRC FROM FEU:Annual Rental Contract Date

FEU Foodcourt Mezzanine of the Technology Building with an area of 693 sq. meters 1,496,880.00 September 1, 2017 toplus applicable VAT August 31, 2018

PROPERTY LEASED BY FECSI FROM FEU:Annual Rental Contract Date

FEU - Cavite Buildings Two (2) concrete buildings located as Silang, Cavite 600,000.00 August 1, 2012 toplus applicable VAT July 31, 2022

on initial year,yearly rates to be

determined annually- or -

the amount equivalentto 5% of its grossannual revenues,

whichever is higher

PROPERTY LEASED BY EACCI (FEU INSTITUTE OF TECHNOLOGY) FROM FEU:Annual Rental Contract Date

Portions of Technology Building 4th to 7th floors and three (3) rooms of the 9th floor of the 24,480,705.60 July 1, 2017 toTechnology Building inclusive of VAT June 30, 2018

on initial year,yearly rates to be

determined annually

PROPERTY LEASED BY FEU HIGH SCHOOL, INC. FROM FEU:Annual Rental Contract Date

FEU Senior High School Buildings 35,515,764.96 June 1, 2017 to(Nursing Building and portion of the plus applicable VAT May 31, 2018Accounts, Business and Finance Building)

The lease contract shall not be deemed extended by implication beyond the contract period for any cause or reason whatsoever, but only by negotiationand written agreement of the LESSOR and the LESSEE.

Amount

Properties inteded to be acquired in the next 12 months: NONE NOT APPLICABLE

- 28 -

- 29 -

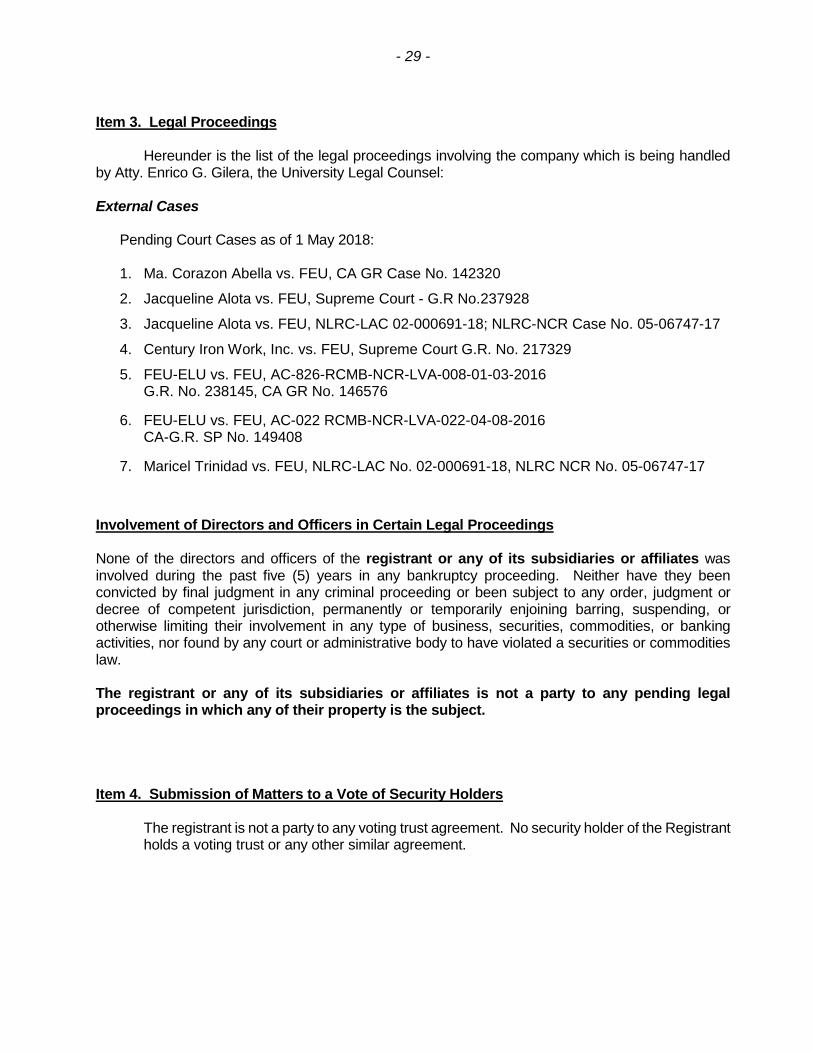

Item 3. Legal Proceedings

Hereunder is the list of the legal proceedings involving the company which is being handledby Atty. Enrico G. Gilera, the University Legal Counsel:

External Cases

Pending Court Cases as of 1 May 2018:

1. Ma. Corazon Abella vs. FEU, CA GR Case No. 142320

2. Jacqueline Alota vs. FEU, Supreme Court - G.R No.237928

3. Jacqueline Alota vs. FEU, NLRC-LAC 02-000691-18; NLRC-NCR Case No. 05-06747-17

4. Century Iron Work, Inc. vs. FEU, Supreme Court G.R. No. 217329

5. FEU-ELU vs. FEU, AC-826-RCMB-NCR-LVA-008-01-03-2016G.R. No. 238145, CA GR No. 146576

6. FEU-ELU vs. FEU, AC-022 RCMB-NCR-LVA-022-04-08-2016CA-G.R. SP No. 149408

7. Maricel Trinidad vs. FEU, NLRC-LAC No. 02-000691-18, NLRC NCR No. 05-06747-17

Involvement of Directors and Officers in Certain Legal Proceedings

None of the directors and officers of the registrant or any of its subsidiaries or affiliates wasinvolved during the past five (5) years in any bankruptcy proceeding. Neither have they beenconvicted by final judgment in any criminal proceeding or been subject to any order, judgment ordecree of competent jurisdiction, permanently or temporarily enjoining barring, suspending, orotherwise limiting their involvement in any type of business, securities, commodities, or bankingactivities, nor found by any court or administrative body to have violated a securities or commoditieslaw.

The registrant or any of its subsidiaries or affiliates is not a party to any pending legalproceedings in which any of their property is the subject.

Item 4. Submission of Matters to a Vote of Security Holders

The registrant is not a party to any voting trust agreement. No security holder of the Registrantholds a voting trust or any other similar agreement.

- 30 -

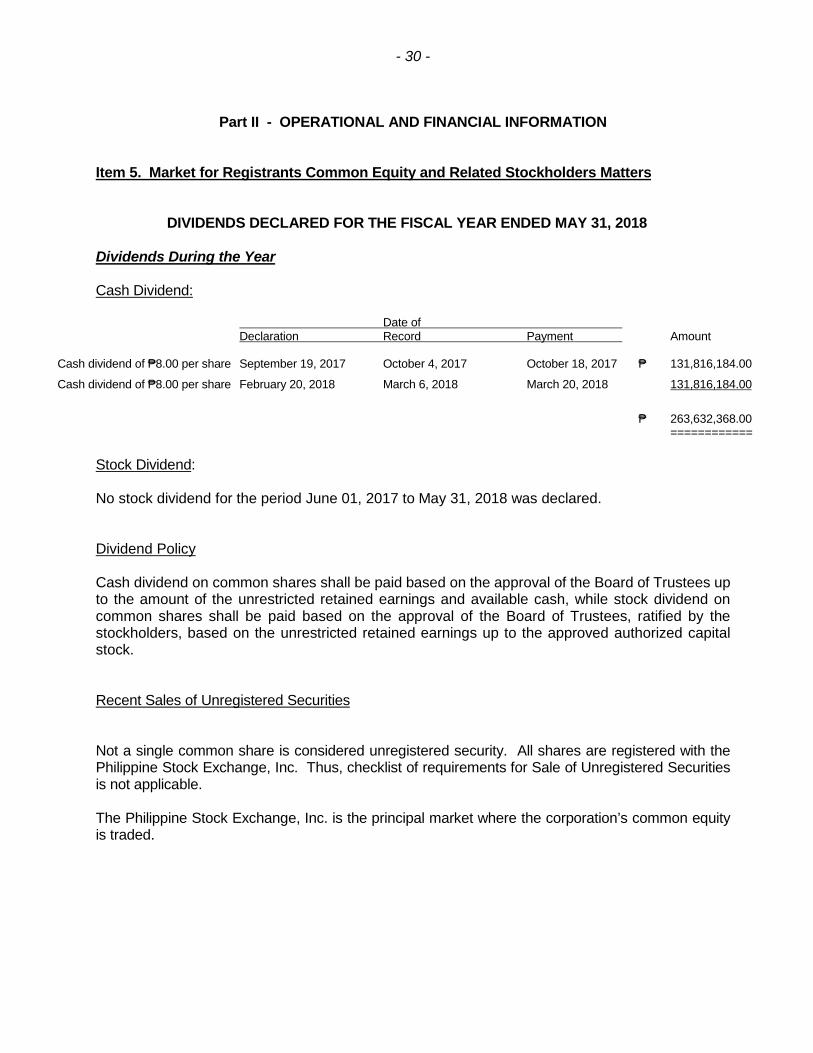

Part II - OPERATIONAL AND FINANCIAL INFORMATION

Item 5. Market for Registrants Common Equity and Related Stockholders Matters

DIVIDENDS DECLARED FOR THE FISCAL YEAR ENDED MAY 31, 2018

Dividends During the Year

Cash Dividend:

Date ofDeclaration Record Payment Amount

Cash dividend of ₱8.00 per share September 19, 2017 October 4, 2017 October 18, 2017 ₱ 131,816,184.00

Cash dividend of ₱8.00 per share February 20, 2018 March 6, 2018 March 20, 2018 131,816,184.00

₱ 263,632,368.00============

Stock Dividend:

No stock dividend for the period June 01, 2017 to May 31, 2018 was declared.

Dividend Policy

Cash dividend on common shares shall be paid based on the approval of the Board of Trustees upto the amount of the unrestricted retained earnings and available cash, while stock dividend oncommon shares shall be paid based on the approval of the Board of Trustees, ratified by thestockholders, based on the unrestricted retained earnings up to the approved authorized capitalstock.

Recent Sales of Unregistered Securities

Not a single common share is considered unregistered security. All shares are registered with thePhilippine Stock Exchange, Inc. Thus, checklist of requirements for Sale of Unregistered Securitiesis not applicable.

The Philippine Stock Exchange, Inc. is the principal market where the corporation’s common equityis traded.

- 31 -

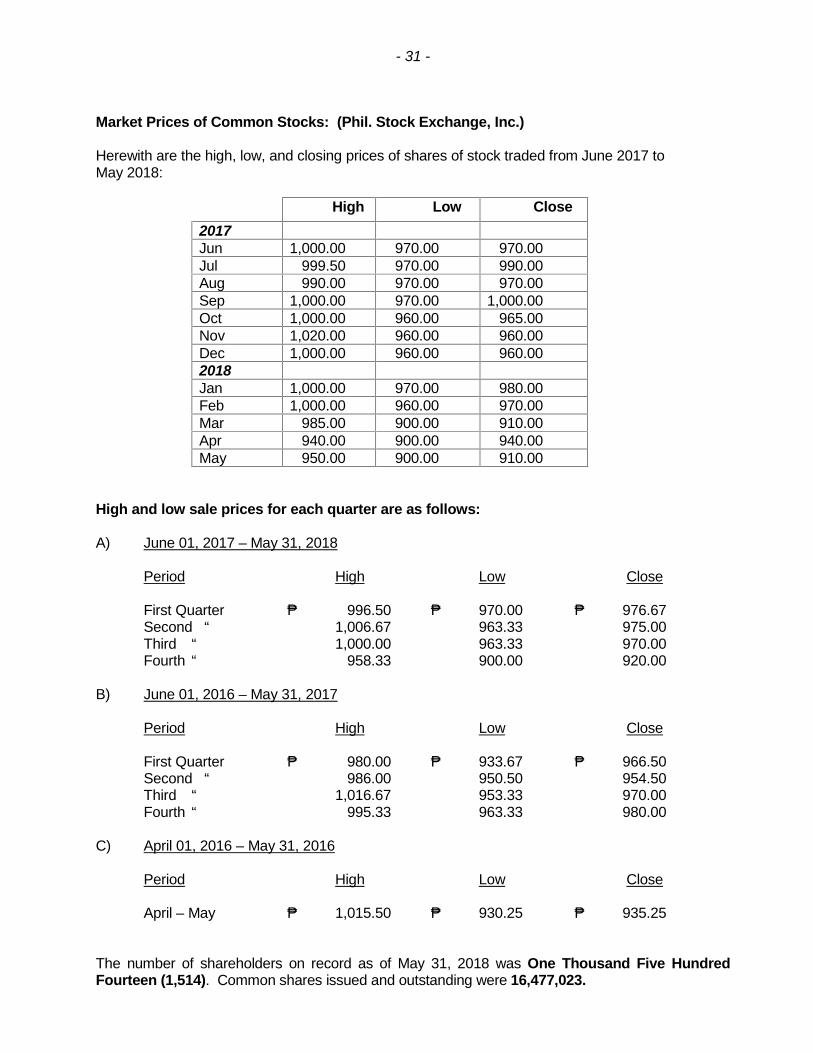

Market Prices of Common Stocks: (Phil. Stock Exchange, Inc.)

Herewith are the high, low, and closing prices of shares of stock traded from June 2017 toMay 2018:

High Low Close2017Jun 1,000.00 970.00 970.00Jul 999.50 970.00 990.00Aug 990.00 970.00 970.00Sep 1,000.00 970.00 1,000.00Oct 1,000.00 960.00 965.00Nov 1,020.00 960.00 960.00Dec 1,000.00 960.00 960.002018Jan 1,000.00 970.00 980.00Feb 1,000.00 960.00 970.00Mar 985.00 900.00 910.00Apr 940.00 900.00 940.00May 950.00 900.00 910.00

High and low sale prices for each quarter are as follows:

A) June 01, 2017 – May 31, 2018

Period High Low Close

First Quarter ₱ 996.50 ₱ 970.00 ₱ 976.67Second “ 1,006.67 963.33 975.00Third “ 1,000.00 963.33 970.00Fourth “ 958.33 900.00 920.00

B) June 01, 2016 – May 31, 2017

Period High Low Close

First Quarter ₱ 980.00 ₱ 933.67 ₱ 966.50Second “ 986.00 950.50 954.50Third “ 1,016.67 953.33 970.00Fourth “ 995.33 963.33 980.00

C) April 01, 2016 – May 31, 2016

Period High Low Close

April – May ₱ 1,015.50 ₱ 930.25 ₱ 935.25

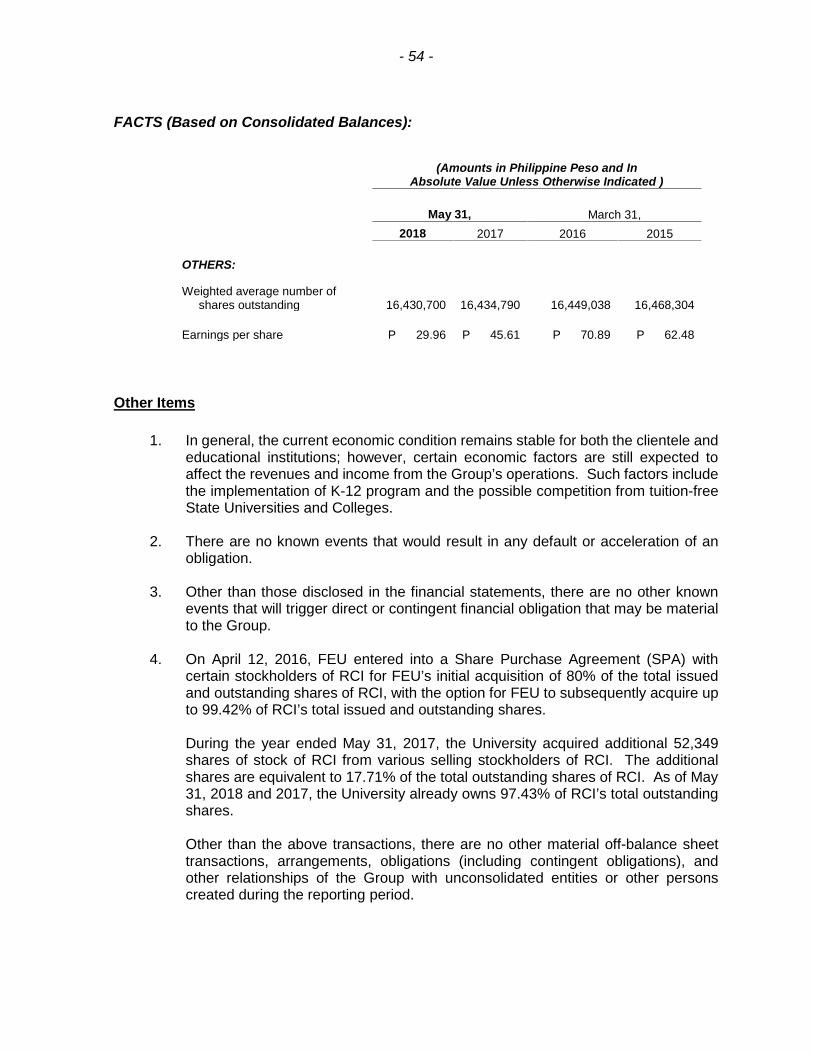

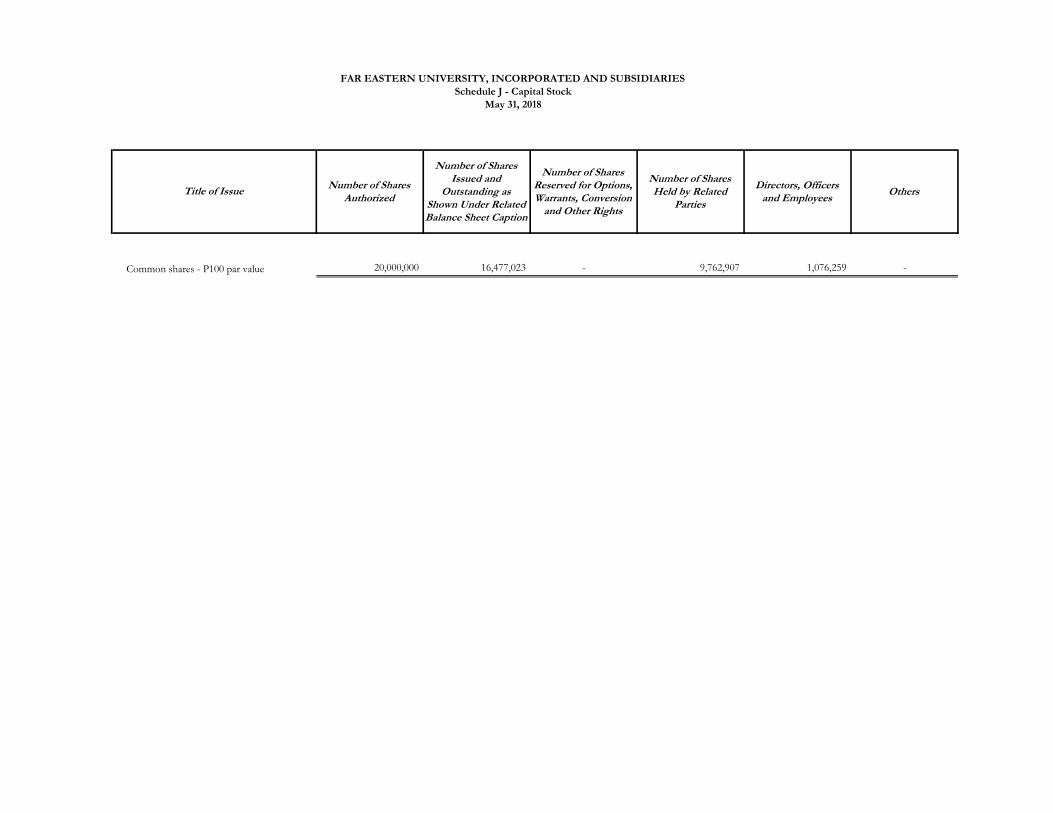

The number of shareholders on record as of May 31, 2018 was One Thousand Five HundredFourteen (1,514). Common shares issued and outstanding were 16,477,023.

- 32 -

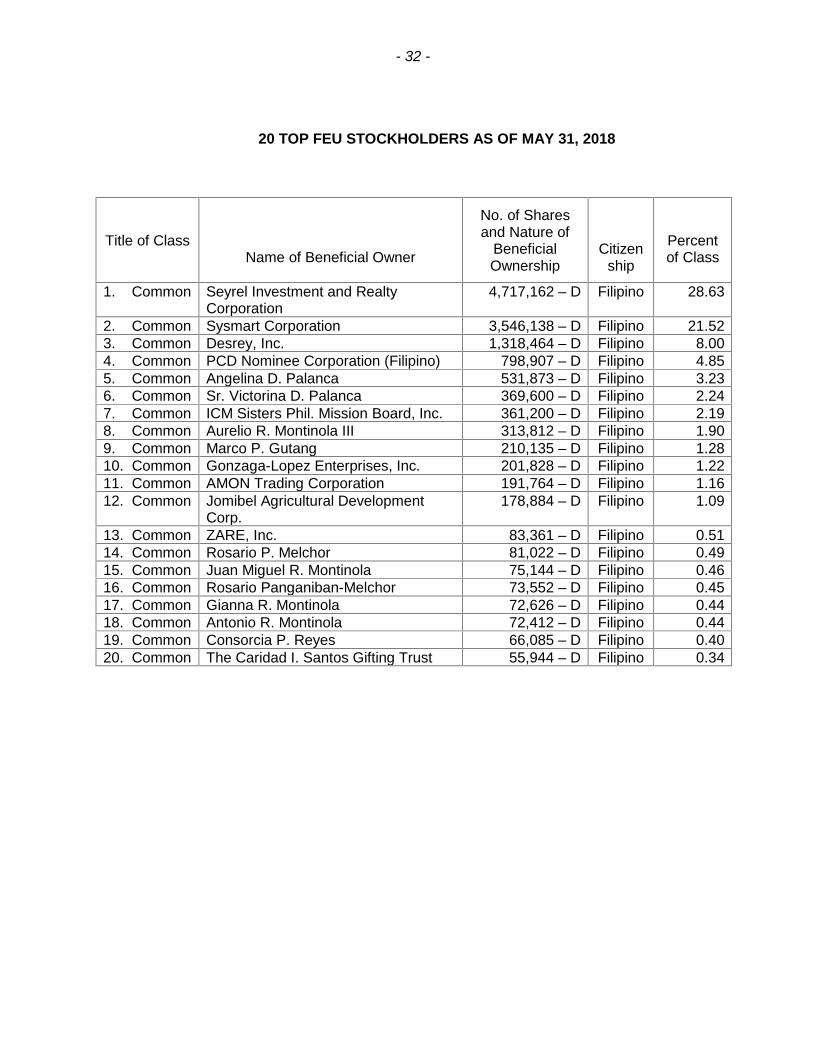

20 TOP FEU STOCKHOLDERS AS OF MAY 31, 2018

Title of ClassName of Beneficial Owner

No. of Sharesand Nature of

BeneficialOwnership

Citizenship

Percentof Class

1. Common Seyrel Investment and RealtyCorporation

4,717,162 – D Filipino 28.63

2. Common Sysmart Corporation 3,546,138 – D Filipino 21.523. Common Desrey, Inc. 1,318,464 – D Filipino 8.004. Common PCD Nominee Corporation (Filipino) 798,907 – D Filipino 4.855. Common Angelina D. Palanca 531,873 – D Filipino 3.236. Common Sr. Victorina D. Palanca 369,600 – D Filipino 2.247. Common ICM Sisters Phil. Mission Board, Inc. 361,200 – D Filipino 2.198. Common Aurelio R. Montinola III 313,812 – D Filipino 1.909. Common Marco P. Gutang 210,135 – D Filipino 1.2810. Common Gonzaga-Lopez Enterprises, Inc. 201,828 – D Filipino 1.2211. Common AMON Trading Corporation 191,764 – D Filipino 1.1612. Common Jomibel Agricultural Development

Corp.178,884 – D Filipino 1.09

13. Common ZARE, Inc. 83,361 – D Filipino 0.5114. Common Rosario P. Melchor 81,022 – D Filipino 0.4915. Common Juan Miguel R. Montinola 75,144 – D Filipino 0.4616. Common Rosario Panganiban-Melchor 73,552 – D Filipino 0.4517. Common Gianna R. Montinola 72,626 – D Filipino 0.4418. Common Antonio R. Montinola 72,412 – D Filipino 0.4419. Common Consorcia P. Reyes 66,085 – D Filipino 0.4020. Common The Caridad I. Santos Gifting Trust 55,944 – D Filipino 0.34

- 33 -

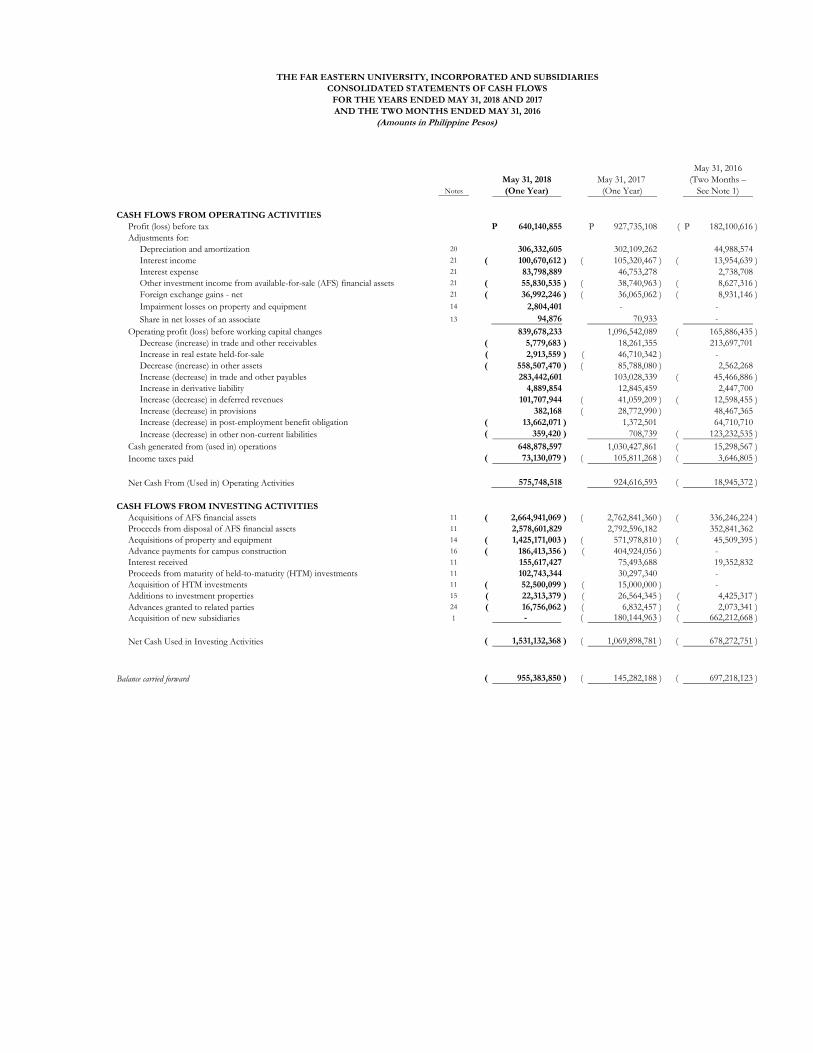

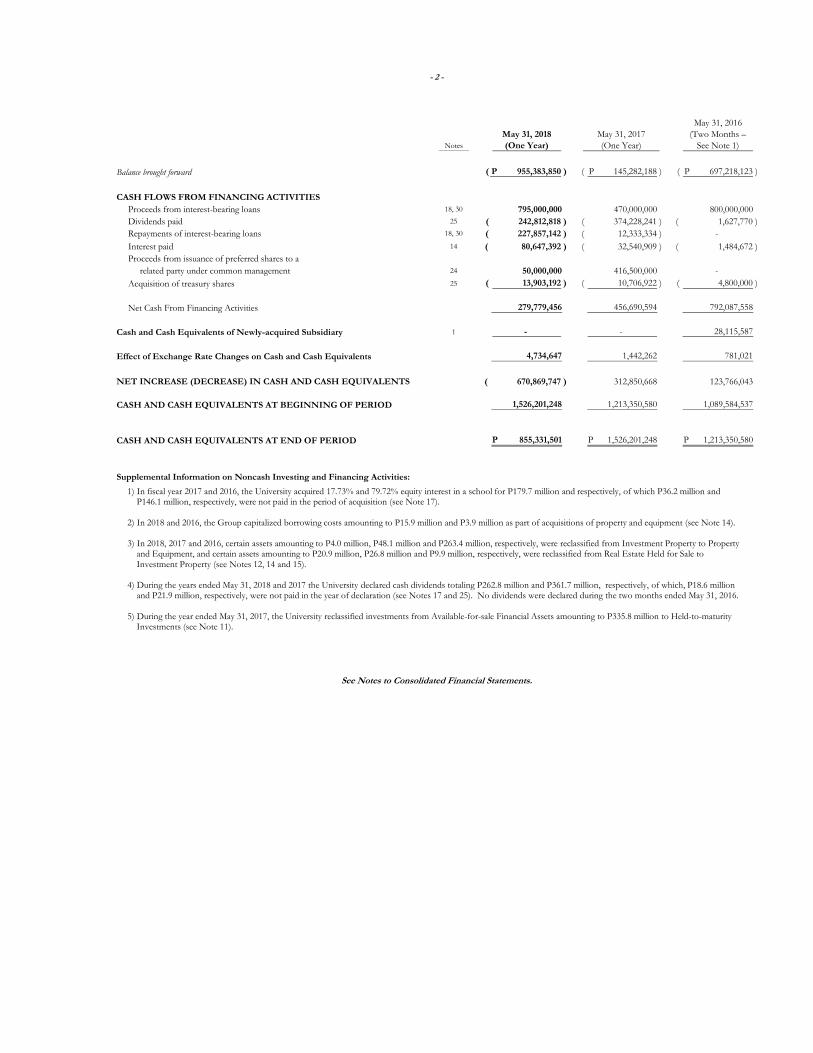

Item 6. Management’s Discussion and Analysis or Plan of Operation

As an academic institution, The Far Eastern University, Incorporated and its subsidiaries (TheGroup or FEU) is fully aware of the importance of education in nation building and to itsstudents who benefit from quality instruction, research and community extension.

The Group is committed to continuously uplift academic standards through updating of itscurricula, developing the faculty, improving the services to its students and providing the besteducational facilities.

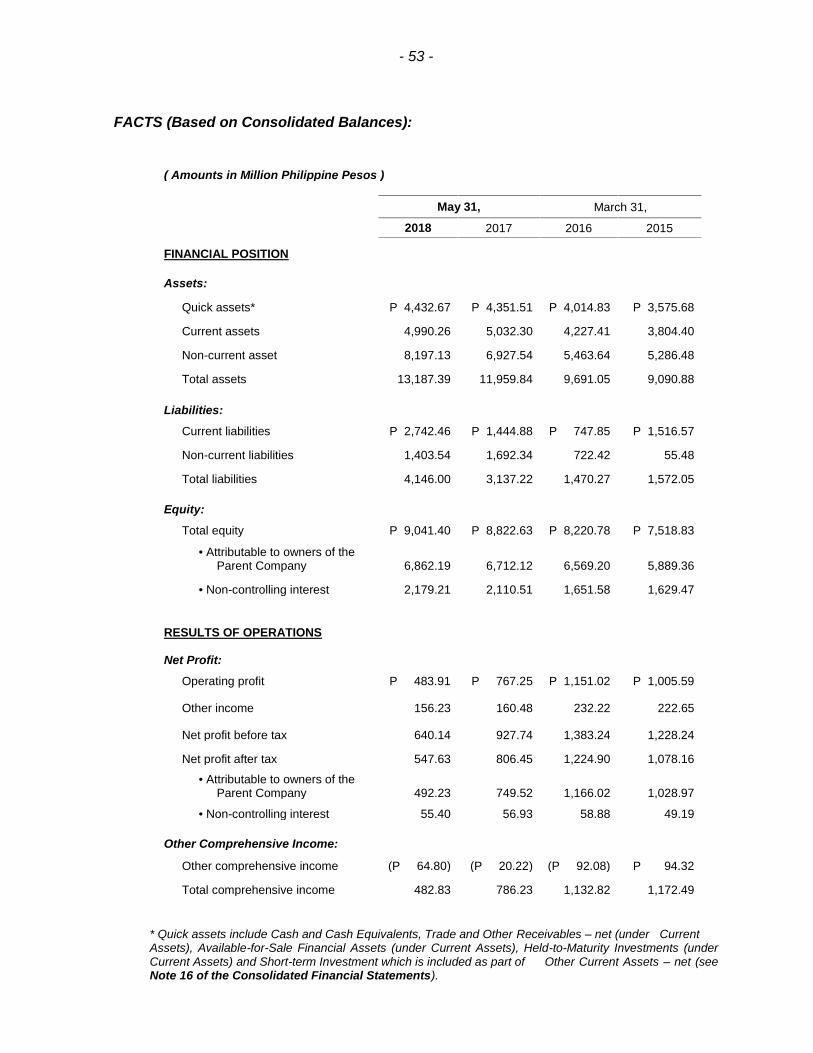

Consolidated Financial Position

The consolidated financial position of the Group remains strong as of May 31, 2018 and 2017,and March 31, 2016.

The Group’s consolidated total assets as of March 31, 2016 reached P9,691.05 million, whichis composed of P4,227.41 million and P5,463.64 million, current and non-current assets,respectively. Total equity remains firm with portions attributable to the owners of the ParentCompany amounting to P6,569.2 and non-controlling interest (NCI) amounting toP1,651.58 million. Current and debt-to-equity ratios were at 5.65:1 and 18%, respectively.

As of May 31, 2017, consolidated total assets further increased to P11,959.84 million, whichwas 23.4% higher than the previous year’s P9,691.05 million. The increase is mainlyattributable to non-current assets which grew by 26.8%, from P5,463.64 million to P6,927.54million; current assets also went up by 19.0%, from P4,227.41 million as of March 31, 2016, toP5,032.3 million as of May 31, 2017. Consolidated total liabilities likewise soared by 113.4%to P3,137.22 million as of May 31, 2017 compared to the March 31, 2016 balance amountingto P1,470.27 million. Balances as of March 31, 2016 have increased in May 31, 2017, fromP747.85 million to P1,444.88 million, and from P722.42 million to P1,692.34 million, for bothcurrent and non-current liabilities, respectively. Total consolidated equity remains stable withportions attributable to the owners of the Parent Company and NCI at P6.712.12 million andP2,110.51 million, respectively.

Current and debt-to-equity ratios as of March 31, 2017, remains favorable at 3.48:1 and 36%,respectively.

As of the end of the current fiscal year, consolidated total assets have reached anothermilestone as it reached P13,187.39 million, which was 10.3% above the previous year’sbalance of P11,959.84 million. Non-current assets grew by 18.3%, from P6,927.54 million asof May 31, 2017 to P8,197.13 million as of May 31, 2018. Meanwhile, current assets slid by1%, from P5,032.3 million as of May 31, 2017 to P4,990.26 million as of May 31, 2018.

- 34 -

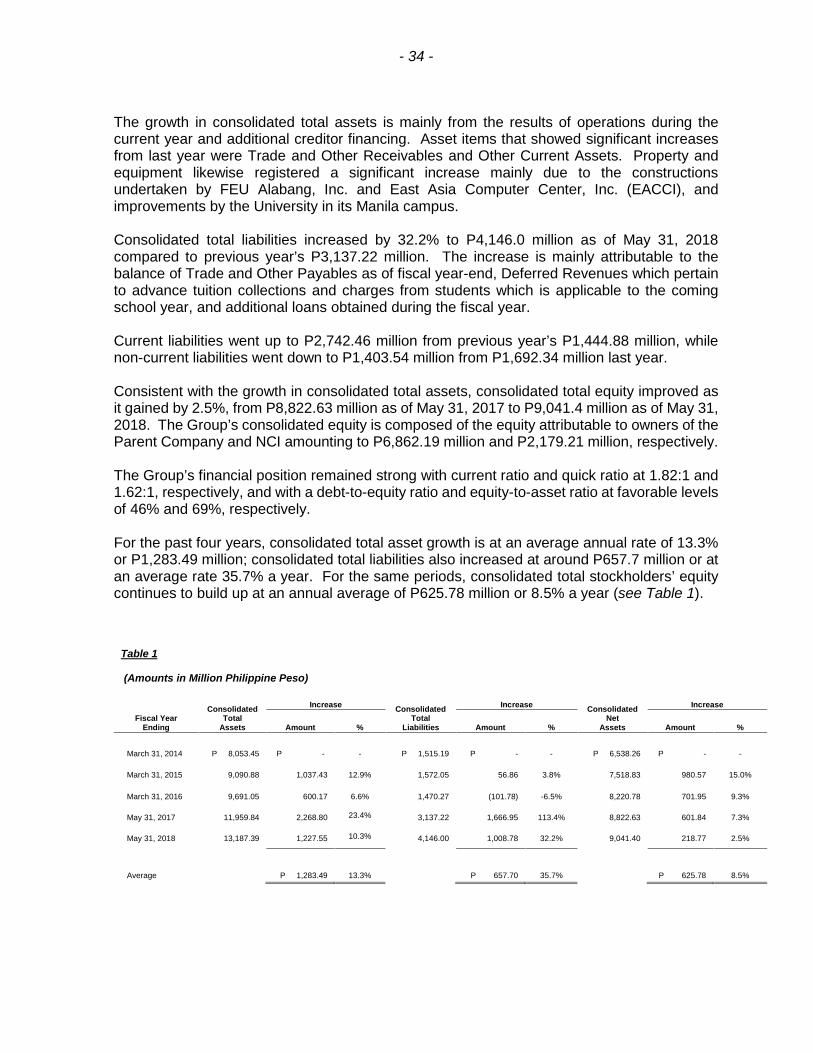

The growth in consolidated total assets is mainly from the results of operations during thecurrent year and additional creditor financing. Asset items that showed significant increasesfrom last year were Trade and Other Receivables and Other Current Assets. Property andequipment likewise registered a significant increase mainly due to the constructionsundertaken by FEU Alabang, Inc. and East Asia Computer Center, Inc. (EACCI), andimprovements by the University in its Manila campus.

Consolidated total liabilities increased by 32.2% to P4,146.0 million as of May 31, 2018compared to previous year’s P3,137.22 million. The increase is mainly attributable to thebalance of Trade and Other Payables as of fiscal year-end, Deferred Revenues which pertainto advance tuition collections and charges from students which is applicable to the comingschool year, and additional loans obtained during the fiscal year.

Current liabilities went up to P2,742.46 million from previous year’s P1,444.88 million, whilenon-current liabilities went down to P1,403.54 million from P1,692.34 million last year.

Consistent with the growth in consolidated total assets, consolidated total equity improved asit gained by 2.5%, from P8,822.63 million as of May 31, 2017 to P9,041.4 million as of May 31,2018. The Group’s consolidated equity is composed of the equity attributable to owners of theParent Company and NCI amounting to P6,862.19 million and P2,179.21 million, respectively.

The Group’s financial position remained strong with current ratio and quick ratio at 1.82:1 and1.62:1, respectively, and with a debt-to-equity ratio and equity-to-asset ratio at favorable levelsof 46% and 69%, respectively.

For the past four years, consolidated total asset growth is at an average annual rate of 13.3%or P1,283.49 million; consolidated total liabilities also increased at around P657.7 million or atan average rate 35.7% a year. For the same periods, consolidated total stockholders’ equitycontinues to build up at an annual average of P625.78 million or 8.5% a year (see Table 1).

Table 1

(Amounts in Million Philippine Peso)

Fiscal YearEnding

ConsolidatedTotal

Assets

Increase ConsolidatedTotal

Liabilities

Increase ConsolidatedNet

Assets

Increase

Amount % Amount % Amount %

March 31, 2014 P 8,053.45 P - - P 1,515.19 P - - P 6,538.26 P - -

March 31, 2015 9,090.88 1,037.43 12.9% 1,572.05 56.86 3.8% 7,518.83 980.57 15.0%

March 31, 2016 9,691.05 600.17 6.6% 1,470.27 (101.78) -6.5% 8,220.78 701.95 9.3%

May 31, 2017 11,959.84 2,268.80 23.4% 3,137.22 1,666.95 113.4% 8,822.63 601.84 7.3%

May 31, 2018 13,187.39 1,227.55 10.3% 4,146.00 1,008.78 32.2% 9,041.40 218.77 2.5%

Average P 1,283.49 13.3% P 657.70 35.7% P 625.78 8.5%

- 35 -

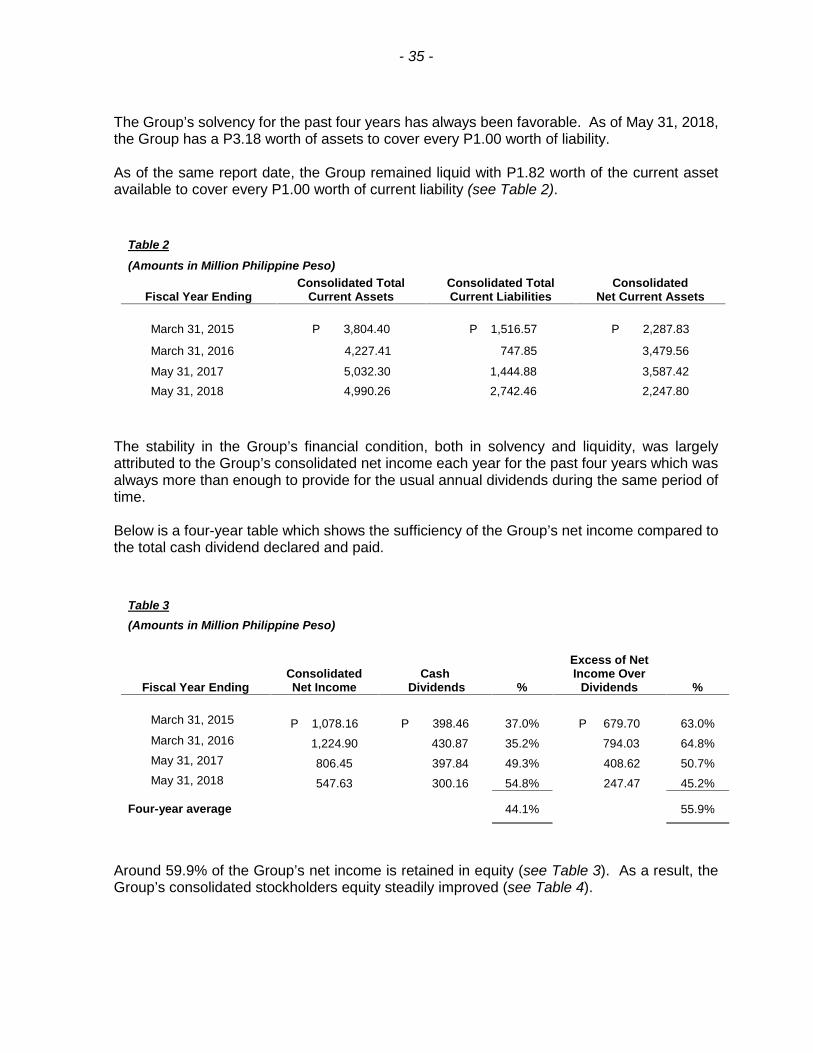

The Group’s solvency for the past four years has always been favorable. As of May 31, 2018,the Group has a P3.18 worth of assets to cover every P1.00 worth of liability.

As of the same report date, the Group remained liquid with P1.82 worth of the current assetavailable to cover every P1.00 worth of current liability (see Table 2).

Table 2

(Amounts in Million Philippine Peso)

Fiscal Year EndingConsolidated Total

Current AssetsConsolidated TotalCurrent Liabilities

ConsolidatedNet Current Assets

March 31, 2015 P 3,804.40 P 1,516.57 P 2,287.83

March 31, 2016 4,227.41 747.85 3,479.56

May 31, 2017 5,032.30 1,444.88 3,587.42May 31, 2018 4,990.26 2,742.46 2,247.80

The stability in the Group’s financial condition, both in solvency and liquidity, was largelyattributed to the Group’s consolidated net income each year for the past four years which wasalways more than enough to provide for the usual annual dividends during the same period oftime.

Below is a four-year table which shows the sufficiency of the Group’s net income compared tothe total cash dividend declared and paid.

Table 3(Amounts in Million Philippine Peso)

Fiscal Year EndingConsolidatedNet Income

CashDividends %

Excess of NetIncome Over

Dividends %

March 31, 2015 P 1,078.16 P 398.46 37.0% P 679.70 63.0%March 31, 2016 1,224.90 430.87 35.2% 794.03 64.8%May 31, 2017 806.45 397.84 49.3% 408.62 50.7%May 31, 2018 547.63 300.16 54.8% 247.47 45.2%

Four-year average 44.1% 55.9%

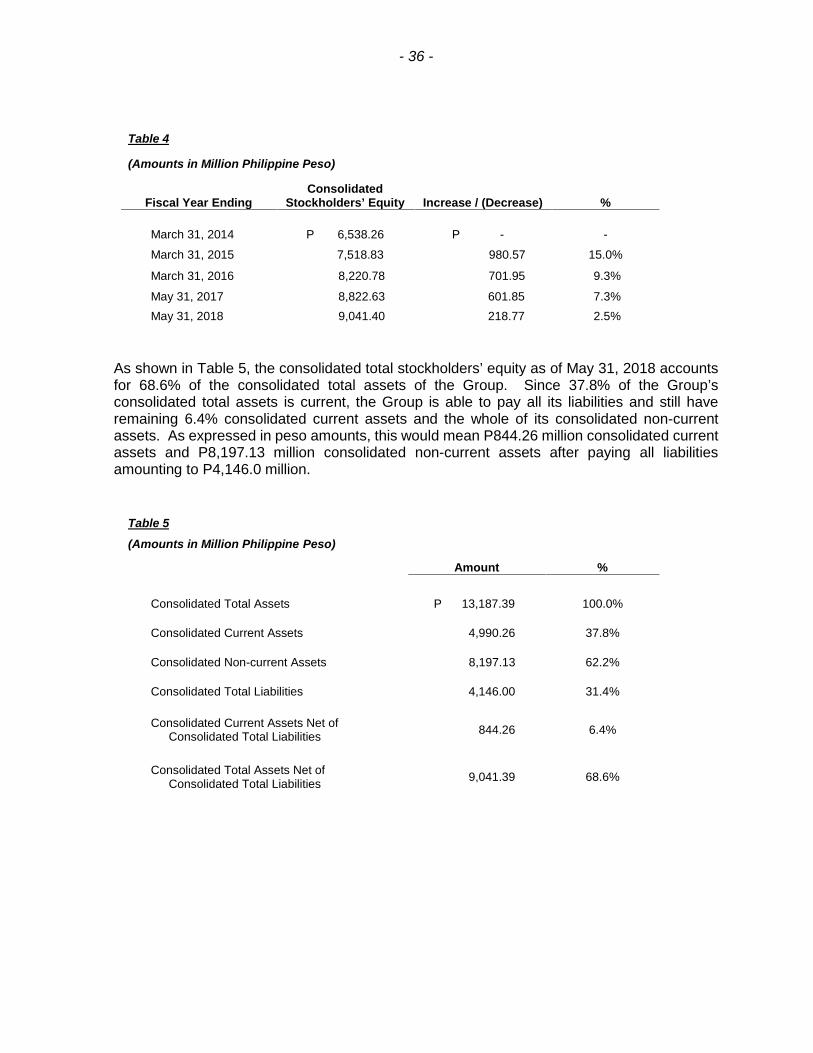

Around 59.9% of the Group’s net income is retained in equity (see Table 3). As a result, theGroup’s consolidated stockholders equity steadily improved (see Table 4).

- 36 -

Table 4

(Amounts in Million Philippine Peso)

Fiscal Year EndingConsolidated

Stockholders’ Equity Increase / (Decrease) %

March 31, 2014 P 6,538.26 P - -

March 31, 2015 7,518.83 980.57 15.0%

March 31, 2016 8,220.78 701.95 9.3%

May 31, 2017 8,822.63 601.85 7.3%May 31, 2018 9,041.40 218.77 2.5%

As shown in Table 5, the consolidated total stockholders’ equity as of May 31, 2018 accountsfor 68.6% of the consolidated total assets of the Group. Since 37.8% of the Group’sconsolidated total assets is current, the Group is able to pay all its liabilities and still haveremaining 6.4% consolidated current assets and the whole of its consolidated non-currentassets. As expressed in peso amounts, this would mean P844.26 million consolidated currentassets and P8,197.13 million consolidated non-current assets after paying all liabilitiesamounting to P4,146.0 million.

Table 5

(Amounts in Million Philippine Peso)

Amount %

Consolidated Total Assets P 13,187.39 100.0%

Consolidated Current Assets 4,990.26 37.8%

Consolidated Non-current Assets 8,197.13 62.2%

Consolidated Total Liabilities 4,146.00 31.4%

Consolidated Current Assets Net ofConsolidated Total Liabilities 844.26 6.4%

Consolidated Total Assets Net ofConsolidated Total Liabilities 9,041.39 68.6%

- 37 -

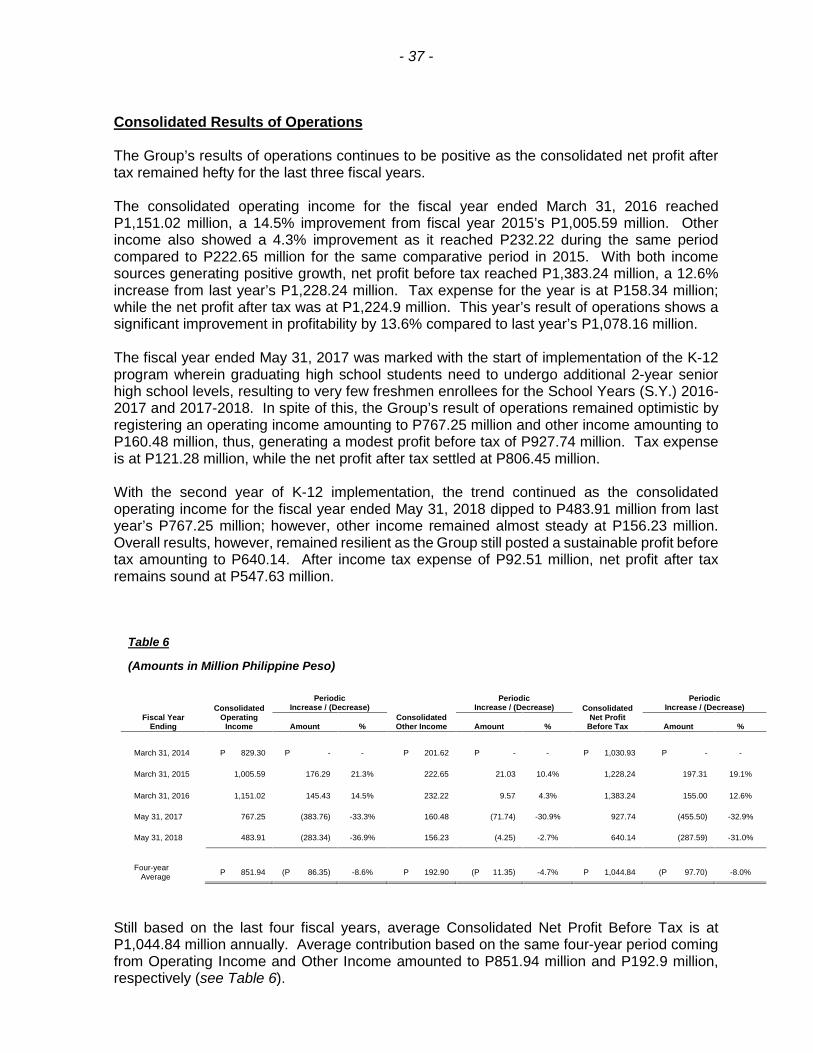

Consolidated Results of Operations

The Group’s results of operations continues to be positive as the consolidated net profit aftertax remained hefty for the last three fiscal years.

The consolidated operating income for the fiscal year ended March 31, 2016 reachedP1,151.02 million, a 14.5% improvement from fiscal year 2015’s P1,005.59 million. Otherincome also showed a 4.3% improvement as it reached P232.22 during the same periodcompared to P222.65 million for the same comparative period in 2015. With both incomesources generating positive growth, net profit before tax reached P1,383.24 million, a 12.6%increase from last year’s P1,228.24 million. Tax expense for the year is at P158.34 million;while the net profit after tax was at P1,224.9 million. This year’s result of operations shows asignificant improvement in profitability by 13.6% compared to last year’s P1,078.16 million.

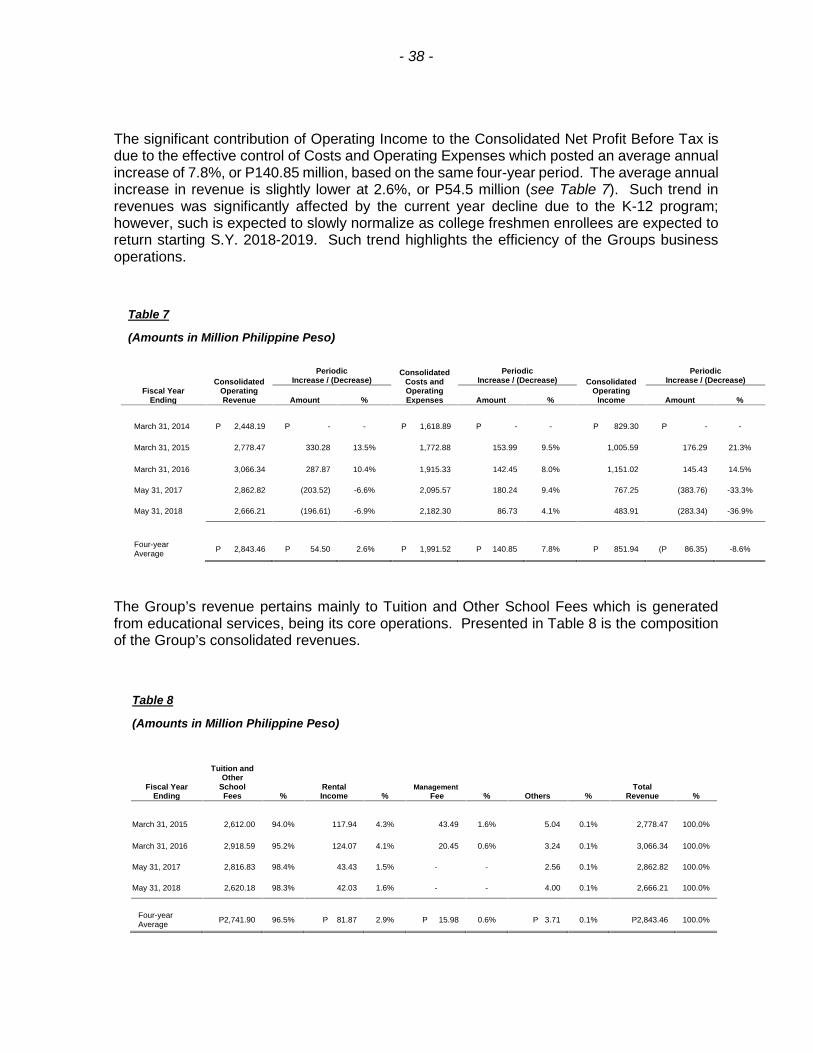

The fiscal year ended May 31, 2017 was marked with the start of implementation of the K-12program wherein graduating high school students need to undergo additional 2-year seniorhigh school levels, resulting to very few freshmen enrollees for the School Years (S.Y.) 2016-2017 and 2017-2018. In spite of this, the Group’s result of operations remained optimistic byregistering an operating income amounting to P767.25 million and other income amounting toP160.48 million, thus, generating a modest profit before tax of P927.74 million. Tax expenseis at P121.28 million, while the net profit after tax settled at P806.45 million.