D2C - changing landscape not fully factored in Sector Thematic FMCG

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

D2C - changing landscape not fully factored in

Sector Thematic

FMCG

SECTOR THEMATIC

FMCG In comparison to other sectors, the FMCG sector has historically been more resilient to external challenges, leading to strong earnings (12.5% CAGR) and valuation rerating (2x) in the last two decades. Earnings traction was steady, driven by (1) share gains from regional/small players, (2) distribution expansion (particularly in rural areas), (3) consistent success with brand extensions, (4) high brand recall to drive premiumisation, and (5) outsourcing to help deploy funds to increase competitiveness. Top-tier mainstream companies have had a smooth ride, boosting investor confidence in earnings visibility. However, in the evolving competitive landscape, we remain sceptical about sustaining these drivers/assumptions. D2C/New age consumer brands are far more disruptive/ agile than traditional/regional competition. Established incumbents are no longer protected by entry barriers (distribution and brand), resulting in a level playing field and category fragmentation - a structural trend. While these new age companies presently account for only 3% of total revenue, given targeted white spaces their share could reach 8-10% in the next few years, which can potentially slice off 100-200bps of growth for incumbents. For new age brands with critical scale in terms of income levels, ease of distribution, and funding, a flywheel effect is in motion. While the majority of these individual brands will likely not scale beyond a certain point, a long tail of brands will emerge.

Varun Lohchab

+91-22-6171-7334

Naveen Trivedi

+91-22-6171-7324

Saras Singh

+91-22-6171-7336

10 March 2022 FMCG Thematic

FMCG

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

D2C – changing landscape not fully factored in

In comparison to other sectors, the FMCG sector has historically been more

resilient to external challenges, leading to strong earnings (12.5% CAGR) and

valuation rerating (2x) in the last two decades. Earnings traction was steady,

driven by (1) share gains from regional/small players, (2) distribution expansion

(particularly in rural areas), (3) consistent success with brand extensions, (4) high

brand recall to drive premiumisation, and (5) outsourcing to help deploy funds to

increase competitiveness. Top-tier mainstream companies have had a smooth ride,

boosting investor confidence in earnings visibility. However, in the evolving

competitive landscape, we remain sceptical about sustaining these

drivers/assumptions. D2C/New age consumer brands are far more disruptive/

agile than traditional/regional competition. Established incumbents are no longer

protected by entry barriers (distribution and brand), resulting in a level playing

field and category fragmentation - a structural trend. While these new age

companies presently account for only 3% of total revenue, given targeted white

spaces their share could reach 8-10% in the next few years, which can potentially

slice off 100-200bps of growth for incumbents. For new age brands with critical

scale in terms of income levels, ease of distribution, and funding, a flywheel

effect is in motion. While the majority of these individual brands will likely not

scale beyond a certain point, a long tail of brands will emerge.

We have seen how the market punishes when long term growth assumptions

change. ITC, Emami, Colgate, Bajaj Consumer, Jyothy Laboratories were

penalised (>30% derating) in last few years. It reflects the fact that valuation

multiples are quite dynamic, and one must stay ahead of the curve to predict these

shifts. We have been underweight on the sector since early 2020; the sector has

underperformed in the last two years, with mild de-rating in progress.

Despite the correction, we do not see room for any valuation upsides; rather, we

expect more valuation risks in the next few years. We cut our multiples for

companies under our coverage (link) and maintain REDUCE for HUL, NESTLE,

BRITANNIA and EMAMI. We rate ITC as a BUY and maintain ADD on DABUR,

MARICO, GCPL, and COLGATE.

D2C – disruption or opportunity? We interacted with various D2C companies,

investors, and listed established players along with pricing/product analysis to

understand the change in the competitive landscape and future trends. Some D2C

players are disrupting categories (particularly BPC), but at an aggregate level, they

are expanding the market (particularly in F&R). We believe D2C companies have the

right-to-win in BPC, and established incumbents need to step up their game to

sustain market shares.

Our long-term thesis (1) We continue to believe that category leaders will be unable

to sustain high market shares, which will be impacted by competition from niche

offline/D2C players. Category leaders in India hold a high market share (in some

cases, >50%), in contrast to developed countries, where competition is more level

playing. (2) Relevant product, pricing, and communication will continue support

D2C/new age brands for customer acquisition. (3) Alternate channels (MT+ ecomm)

will continue to gain share, despite a significant increase in the last two years. India’s

share could be larger than that of developed countries, given the vast differences in

consumer buying experiences between GT and alternate channels. (4) Margin

expansion for most companies will be muted, as many have already hit the wall. A

large part of cost control has already been captured. Companies must prioritise

growth above margins. (5) Over the last five years, many consumer discretionary

companies have expanded/gone public, providing a variety of options to investors in

the consumption space. In comparison to history, changing assumptions will cause

the valuation metric to shift relatively quickly.

Company CMP (INR) Reco.

HUL 1,998 REDUCE

ITC 229 BUY

Nestle 17,146 REDUCE

Britannia 3,124 REDUCE

Dabur 528 ADD

GCPL 702 ADD

Marico 493 ADD

Colgate 1,449 ADD

Emami 471 REDUCE

FMCG Universe: Earnings vs. Valuation

(Ex-ITC)

Sector (Ex-ITC) P/E (12-month rolling

forward)

Varun Lohchab

+91-22-6171-7334

Naveen Trivedi

+91-22-6171-7324

Saras Singh

+91-22-6171-7326

Page | 2

FMCG: D2C Disruption

Focus Charts

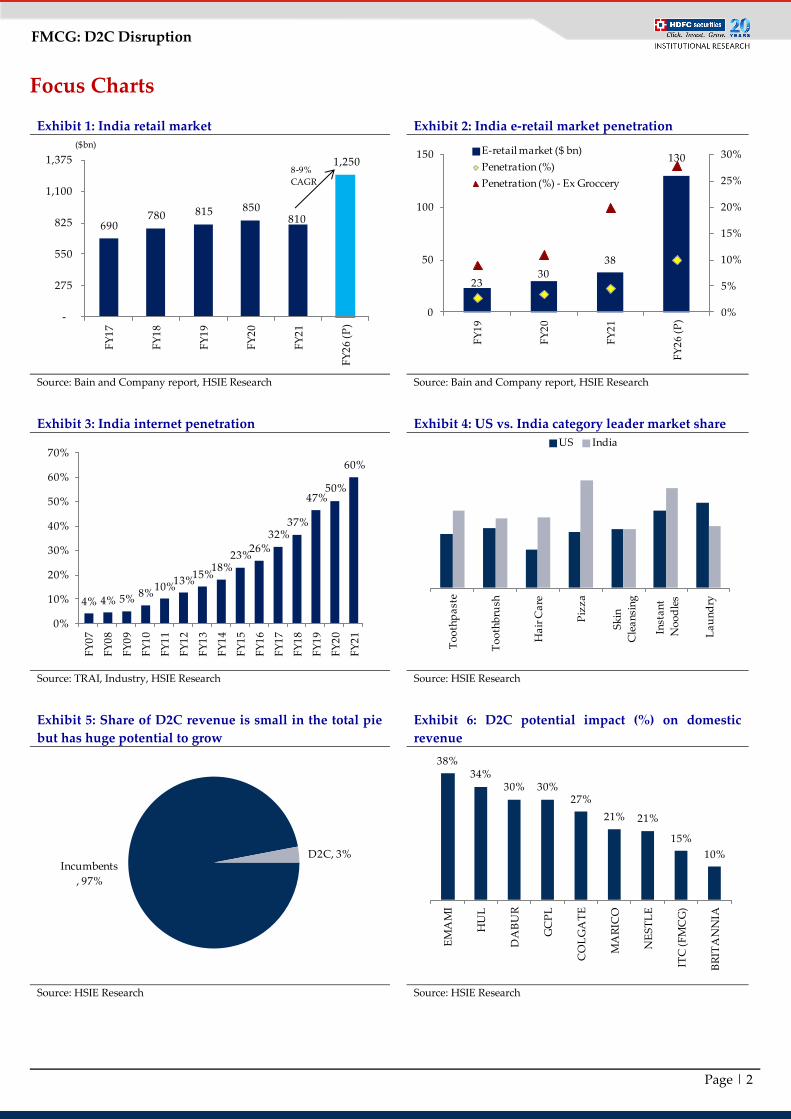

Exhibit 1: India retail market Exhibit 2: India e-retail market penetration

Source: Bain and Company report, HSIE Research Source: Bain and Company report, HSIE Research

Exhibit 3: India internet penetration Exhibit 4: US vs. India category leader market share

Source: TRAI, Industry, HSIE Research Source: HSIE Research

Exhibit 5: Share of D2C revenue is small in the total pie

but has huge potential to grow

Exhibit 6: D2C potential impact (%) on domestic

revenue

Source: HSIE Research Source: HSIE Research

4% 4% 5%8%

10%13%

15%18%

23%26%

32%37%

47%50%

60%

0%

10%

20%

30%

40%

50%

60%

70%

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

690 780 815 850

810

1,250

-

275

550

825

1,100

1,375

FY

17

FY

18

FY

19

FY

20

FY

21

FY

26

(P

)

8-9%

CAGR

($bn)

2330

38

130

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

FY

19

FY

20

FY

21

FY

26

(P

)

E-retail market ($ bn)

Penetration (%)

Penetration (%) - Ex Groccery

To

oth

pa

ste

To

oth

bru

sh

Ha

ir C

are

Piz

za

Sk

in

Cle

an

sin

g

Inst

an

t

No

od

les

La

un

dry

US India

Incumbents

, 97%

D2C, 3%

38%34%

30% 30%27%

21% 21%

15%

10%

EM

AM

I

HU

L

DA

BU

R

GC

PL

CO

LG

AT

E

MA

RIC

O

NE

ST

LE

ITC

(F

MC

G)

BR

ITA

NN

IA

Page | 3

FMCG: D2C Disruption

Content

Is D2C temporary or structural? .........................................................................................4

- E-retail penetration to further improve

- “Jio effect”

- D2C and e-retail are global trends, fired in pandemic

- India was always short of consumer brands, D2C adding options for

consumers

- Success of naturals/ayurvedic products was the first real indicator of change

- Institutional funding aiding wings to fly long

- Inspiring background of D2C companies’ founders

D2C: Key success factors ................................................................................................... 12

- Unique product proposition

- Support from rapid development of the ecosystem

- A new age of customer interactions

D2C: Disruption or opportunity ..................................................................................... 14

- Feedback - mainstream, D2C companies and investors

- Potential impact (%) on domestic revenue of mainstream companies

What is correct valuation premium, as assumptions alter? ......................................... 16

- Will changing business assumption impact valuation premium?

- Valuation Summary

- Change in Estimate, Target Multiple, TP and Rating

Competitive landscape change in BPC and F&R ......................................................... 21

- Cosmetics

- Skin Care

- Hair Oil

- Shampoo

- Personal Wash

- Feminine Hygiene

- Men's Grooming

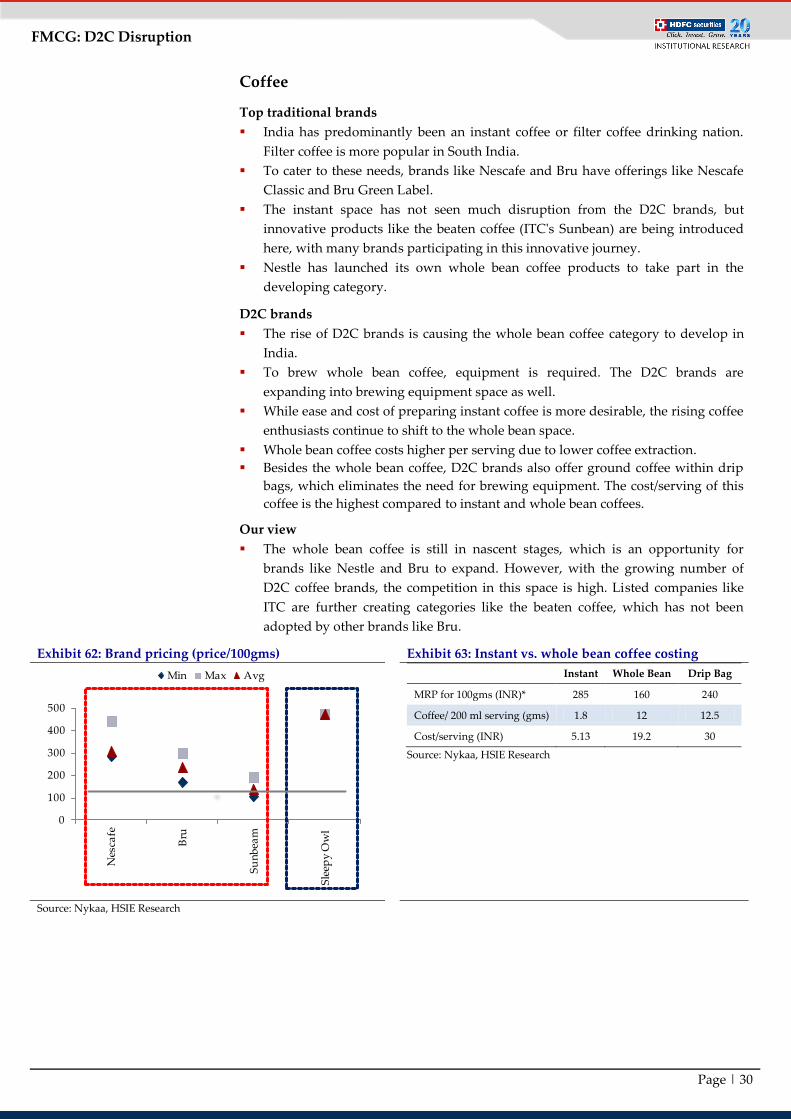

- Coffee

- Milk & Milk Products

- Nutrition – Supplements

- Food/Staple

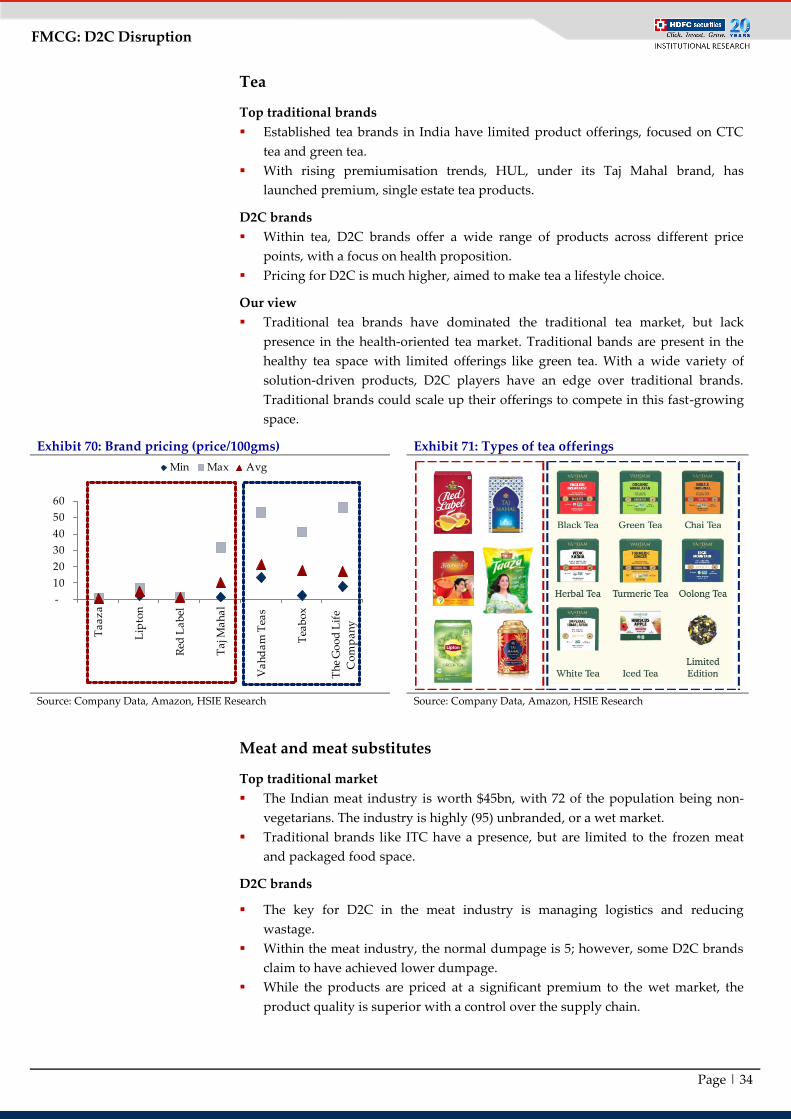

- Tea

- Meat & Meat Substitute

D2C companies profile ...................................................................................................... 36

- Mamaearth

- SUGAR Cosmetics

- The Good Glamm Group

- WOW

- Bombay Shaving Company

- Pee Safe

- Licious

- Country Delight

- Vahdam Teas

- OZiva

- True Elements

- Sleepy Owl

Page | 4

FMCG: D2C Disruption

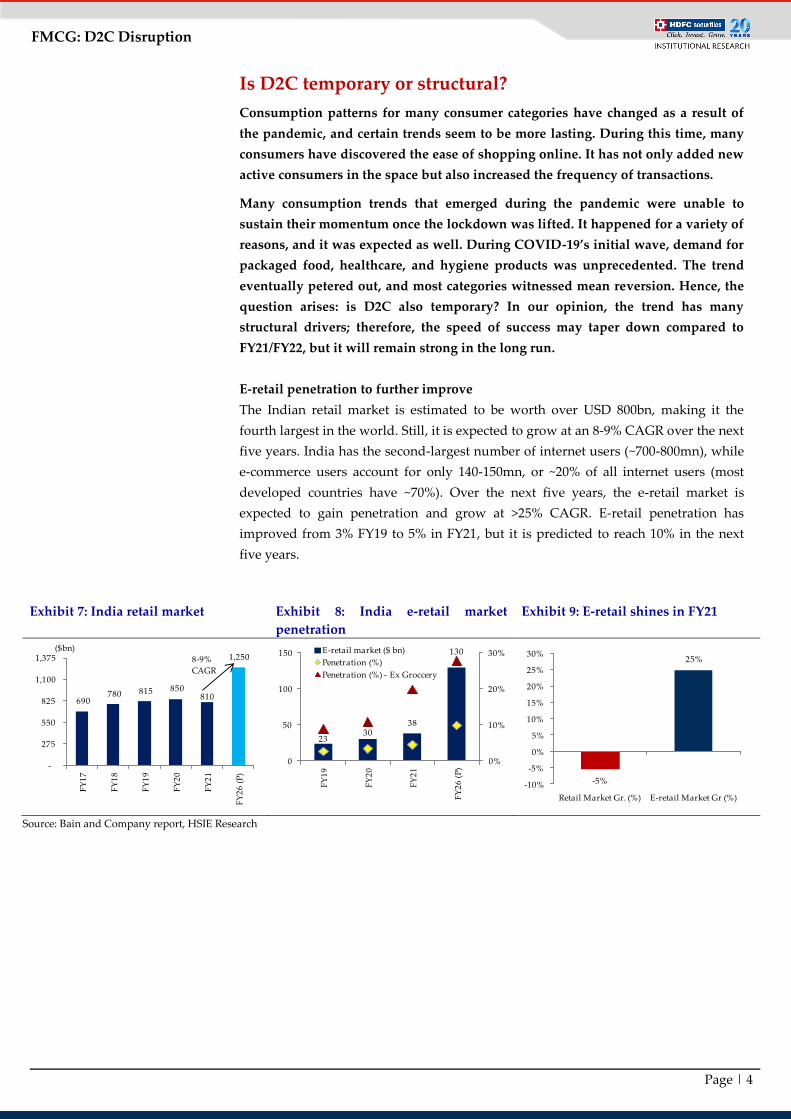

Is D2C temporary or structural?

Consumption patterns for many consumer categories have changed as a result of

the pandemic, and certain trends seem to be more lasting. During this time, many

consumers have discovered the ease of shopping online. It has not only added new

active consumers in the space but also increased the frequency of transactions.

Many consumption trends that emerged during the pandemic were unable to

sustain their momentum once the lockdown was lifted. It happened for a variety of

reasons, and it was expected as well. During COVID-19’s initial wave, demand for

packaged food, healthcare, and hygiene products was unprecedented. The trend

eventually petered out, and most categories witnessed mean reversion. Hence, the

question arises: is D2C also temporary? In our opinion, the trend has many

structural drivers; therefore, the speed of success may taper down compared to

FY21/FY22, but it will remain strong in the long run.

E-retail penetration to further improve

The Indian retail market is estimated to be worth over USD 800bn, making it the

fourth largest in the world. Still, it is expected to grow at an 8-9% CAGR over the next

five years. India has the second-largest number of internet users (~700-800mn), while

e-commerce users account for only 140-150mn, or ~20% of all internet users (most

developed countries have ~70%). Over the next five years, the e-retail market is

expected to gain penetration and grow at >25% CAGR. E-retail penetration has

improved from 3% FY19 to 5% in FY21, but it is predicted to reach 10% in the next

five years.

Exhibit 7: India retail market Exhibit 8: India e-retail market

penetration

Exhibit 9: E-retail shines in FY21

Source: Bain and Company report, HSIE Research

690 780 815 850

810

1,250

-

275

550

825

1,100

1,375

FY

17

FY

18

FY

19

FY

20

FY

21

FY

26

(P

)

8-9%

CAGR

($bn)

2330

38

130

0%

10%

20%

30%

0

50

100

150

FY

19

FY

20

FY

21

FY

26

(P

)

E-retail market ($ bn)

Penetration (%)

Penetration (%) - Ex Groccery

-5%

25%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Retail Market Gr. (%) E-retail Market Gr (%)

Page | 5

FMCG: D2C Disruption

“Jio Effect”

India’s digital ecosystem is becoming favorable for D2C brands. Rising affluence

towards e-retail business was already in favour, as internet users started seeing a

massive jump after 2016, dubbed the “Jio Effect”. Since 2015 (when JIO was

introduced), data tariffs have been lowered dramatically, and India is now the

world's cheapest data country. It was especially beneficial in underpenetrated

countries like India, where penetration has increased dramatically.

Exhibit 10: Internet users in India –

The Jio Effect

Exhibit 11: India internet

penetration

Exhibit 12: India average data tariff

fall

Source: TRAI, Industry

Exhibit 13: Digital ecosystems

India Digital Funnel Growth (%)

FY21

User base (mn)

FY21 FY26

Internet users 5% 625-675 850-900

Chatting and social media 15% 400-450 725-775

Video content 25% 350-400 600-650

Service transactors 18% 200-250 500-550

Product transactors 32% 140 350-400

Source: Bain and Company report

D2C and e-retail are global trends, fired in pandemic

E-retail penetration expansion and the success of D2C are two global trends that

exploded during the pandemic. Despite a robust show in the last two years, the

Indian e-retail market and D2C are still in their infancy. With a large number of

internet users, rising affluence, and the increasing ease of using buying platforms,

India will continue to boost e-retail and D2C brands.

Exhibit 14: E-retail to outgrow MT in

India

Exhibit 15: Number of D2C Brands in

India

Exhibit 16: Global E-retail

penetration - % of retail

Source: Bain and Company report, HSIE Research

0

20

40

60

80

100

120

140

FY

17

FY

20

FY

21

FY

26

P

MT e-Retail($bn)

30-40K

70-80K

200-250K

20

18

20

20

20

25

(P

)

27%

22%

15%

7%

3%

30%28%

20%

12%

5%

0%

5%

10%

15%

20%

25%

30%

35%

Ch

ina

So

uth

-

Ko

rea

US

Au

stra

lia

Ind

ia

2018 2020

0

50

100

150

200

250

300

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

(INR/GB)

4% 4% 5%8%

10%13%

15%18%

23%26%

32%37%

47%50%

60%

0%

10%

20%

30%

40%

50%

60%

70%

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

42 81 100 137 239

286 342

422 494

637 749

845

1,186

-

300

600

900

1,200

FY

07

FY

09

FY

10

FY

12

FY

13

FY

14

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

26

(P

)

(mn)

Page | 6

FMCG: D2C Disruption

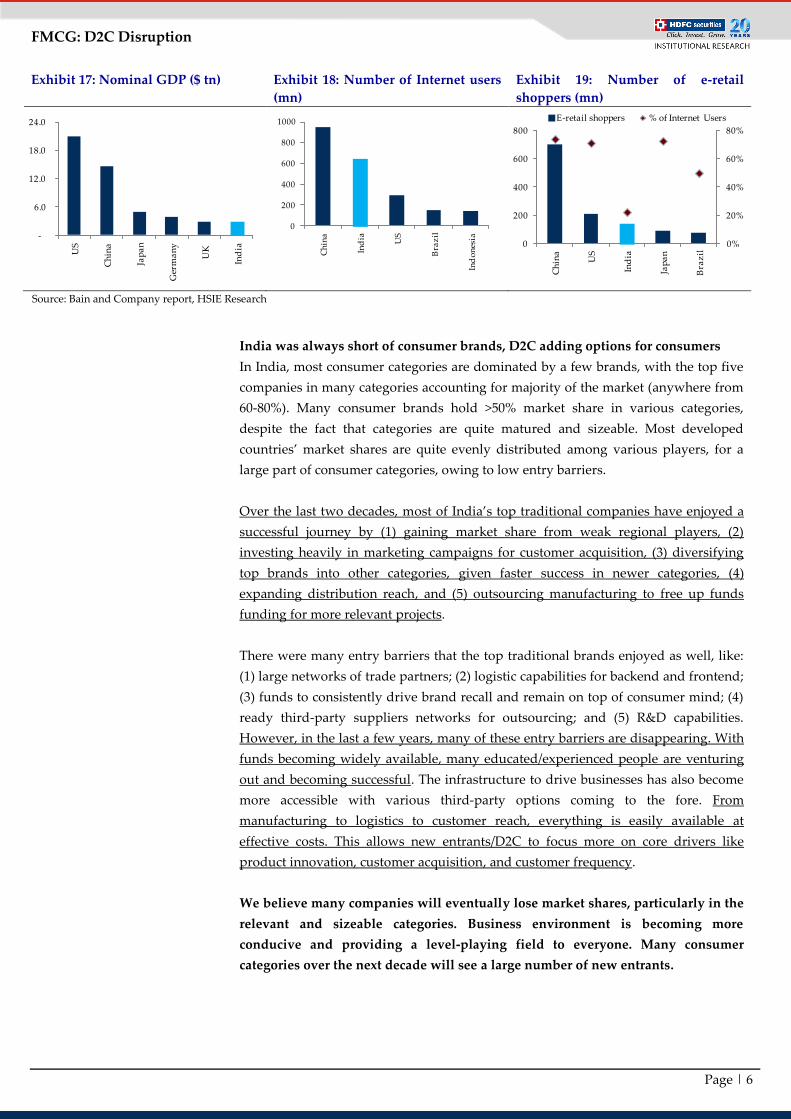

Exhibit 17: Nominal GDP ($ tn) Exhibit 18: Number of Internet users

(mn)

Exhibit 19: Number of e-retail

shoppers (mn)

Source: Bain and Company report, HSIE Research

India was always short of consumer brands, D2C adding options for consumers

In India, most consumer categories are dominated by a few brands, with the top five

companies in many categories accounting for majority of the market (anywhere from

60-80%). Many consumer brands hold >50% market share in various categories,

despite the fact that categories are quite matured and sizeable. Most developed

countries’ market shares are quite evenly distributed among various players, for a

large part of consumer categories, owing to low entry barriers.

Over the last two decades, most of India’s top traditional companies have enjoyed a

successful journey by (1) gaining market share from weak regional players, (2)

investing heavily in marketing campaigns for customer acquisition, (3) diversifying

top brands into other categories, given faster success in newer categories, (4)

expanding distribution reach, and (5) outsourcing manufacturing to free up funds

funding for more relevant projects.

There were many entry barriers that the top traditional brands enjoyed as well, like:

(1) large networks of trade partners; (2) logistic capabilities for backend and frontend;

(3) funds to consistently drive brand recall and remain on top of consumer mind; (4)

ready third-party suppliers networks for outsourcing; and (5) R&D capabilities.

However, in the last a few years, many of these entry barriers are disappearing. With

funds becoming widely available, many educated/experienced people are venturing

out and becoming successful. The infrastructure to drive businesses has also become

more accessible with various third-party options coming to the fore. From

manufacturing to logistics to customer reach, everything is easily available at

effective costs. This allows new entrants/D2C to focus more on core drivers like

product innovation, customer acquisition, and customer frequency.

We believe many companies will eventually lose market shares, particularly in the

relevant and sizeable categories. Business environment is becoming more

conducive and providing a level-playing field to everyone. Many consumer

categories over the next decade will see a large number of new entrants.

-

6.0

12.0

18.0

24.0

US

Ch

ina

Jap

an

Ger

ma

ny

UK

Ind

ia 0%

20%

40%

60%

80%

0

200

400

600

800

Ch

ina

US

Ind

ia

Jap

an

Bra

zil

E-retail shoppers % of Internet Users

0

200

400

600

800

1000

Ch

ina

Ind

ia US

Bra

zil

Ind

on

esia

Page | 7

FMCG: D2C Disruption

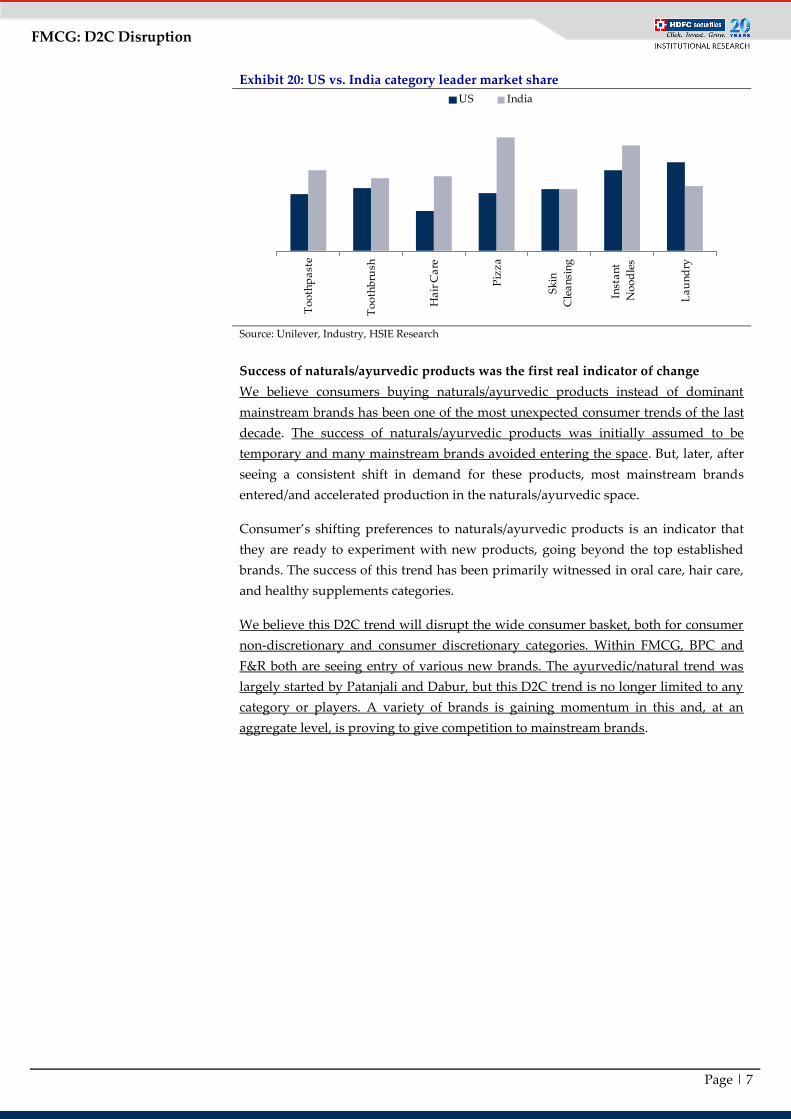

Exhibit 20: US vs. India category leader market share

Source: Unilever, Industry, HSIE Research

Success of naturals/ayurvedic products was the first real indicator of change

We believe consumers buying naturals/ayurvedic products instead of dominant

mainstream brands has been one of the most unexpected consumer trends of the last

decade. The success of naturals/ayurvedic products was initially assumed to be

temporary and many mainstream brands avoided entering the space. But, later, after

seeing a consistent shift in demand for these products, most mainstream brands

entered/and accelerated production in the naturals/ayurvedic space.

Consumer’s shifting preferences to naturals/ayurvedic products is an indicator that

they are ready to experiment with new products, going beyond the top established

brands. The success of this trend has been primarily witnessed in oral care, hair care,

and healthy supplements categories.

We believe this D2C trend will disrupt the wide consumer basket, both for consumer

non-discretionary and consumer discretionary categories. Within FMCG, BPC and

F&R both are seeing entry of various new brands. The ayurvedic/natural trend was

largely started by Patanjali and Dabur, but this D2C trend is no longer limited to any

category or players. A variety of brands is gaining momentum in this and, at an

aggregate level, is proving to give competition to mainstream brands.

To

oth

pa

ste

To

oth

bru

sh

Ha

ir C

are

Piz

za

Sk

in

Cle

an

sin

g

Inst

an

t

No

od

les

La

un

dry

US India

Page | 8

FMCG: D2C Disruption

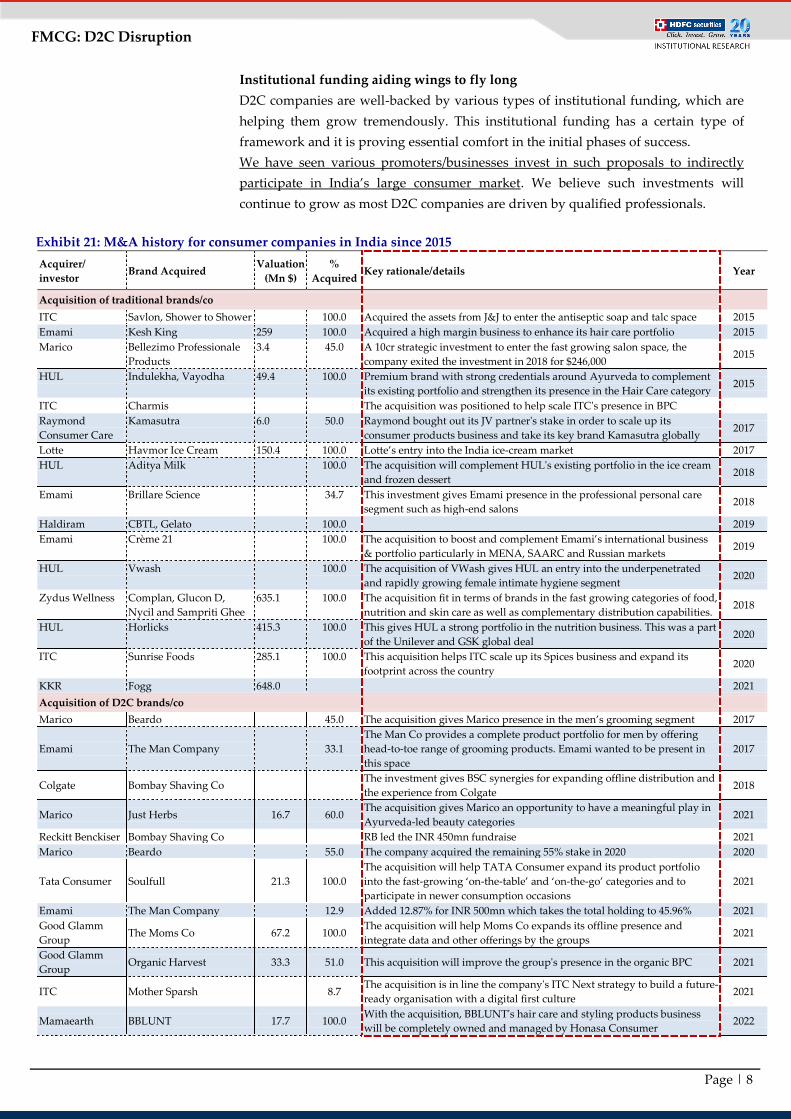

Institutional funding aiding wings to fly long

D2C companies are well-backed by various types of institutional funding, which are

helping them grow tremendously. This institutional funding has a certain type of

framework and it is proving essential comfort in the initial phases of success.

We have seen various promoters/businesses invest in such proposals to indirectly

participate in India’s large consumer market. We believe such investments will

continue to grow as most D2C companies are driven by qualified professionals.

Exhibit 21: M&A history for consumer companies in India since 2015

Acquirer/

investor Brand Acquired

Valuation

(Mn $)

%

Acquired Key rationale/details Year

Acquisition of traditional brands/co

ITC Savlon, Shower to Shower 100.0 Acquired the assets from J&J to enter the antiseptic soap and talc space 2015

Emami Kesh King 259 100.0 Acquired a high margin business to enhance its hair care portfolio 2015

Marico Bellezimo Professionale

Products

3.4 45.0 A 10cr strategic investment to enter the fast growing salon space, the

company exited the investment in 2018 for $246,000 2015

HUL Indulekha, Vayodha 49.4 100.0 Premium brand with strong credentials around Ayurveda to complement

its existing portfolio and strengthen its presence in the Hair Care category 2015

ITC Charmis The acquisition was positioned to help scale ITC's presence in BPC

Raymond

Consumer Care

Kamasutra 6.0 50.0 Raymond bought out its JV partner's stake in order to scale up its

consumer products business and take its key brand Kamasutra globally 2017

Lotte Havmor Ice Cream 150.4 100.0 Lotte’s entry into the India ice-cream market 2017

HUL Aditya Milk 100.0 The acquisition will complement HUL's existing portfolio in the ice cream

and frozen dessert 2018

Emami Brillare Science 34.7 This investment gives Emami presence in the professional personal care

segment such as high-end salons 2018

Haldiram CBTL, Gelato 100.0 2019

Emami Crème 21 100.0 The acquisition to boost and complement Emami’s international business

& portfolio particularly in MENA, SAARC and Russian markets 2019

HUL Vwash 100.0 The acquisition of VWash gives HUL an entry into the underpenetrated

and rapidly growing female intimate hygiene segment 2020

Zydus Wellness Complan, Glucon D,

Nycil and Sampriti Ghee

635.1 100.0 The acquisition fit in terms of brands in the fast growing categories of food,

nutrition and skin care as well as complementary distribution capabilities. 2018

HUL Horlicks 415.3 100.0 This gives HUL a strong portfolio in the nutrition business. This was a part

of the Unilever and GSK global deal 2020

ITC Sunrise Foods 285.1 100.0 This acquisition helps ITC scale up its Spices business and expand its

footprint across the country 2020

KKR Fogg 648.0 2021

Acquisition of D2C brands/co

Marico Beardo

45.0 The acquisition gives Marico presence in the men’s grooming segment 2017

Emami The Man Company

33.1

The Man Co provides a complete product portfolio for men by offering

head-to-toe range of grooming products. Emami wanted to be present in

this space

2017

Colgate Bombay Shaving Co

The investment gives BSC synergies for expanding offline distribution and

the experience from Colgate 2018

Marico Just Herbs 16.7 60.0 The acquisition gives Marico an opportunity to have a meaningful play in

Ayurveda-led beauty categories 2021

Reckitt Benckiser Bombay Shaving Co

RB led the INR 450mn fundraise 2021

Marico Beardo

55.0 The company acquired the remaining 55% stake in 2020 2020

Tata Consumer Soulfull 21.3 100.0

The acquisition will help TATA Consumer expand its product portfolio

into the fast-growing ‘on-the-table’ and ‘on-the-go’ categories and to

participate in newer consumption occasions

2021

Emami The Man Company

12.9 Added 12.87% for INR 500mn which takes the total holding to 45.96% 2021

Good Glamm

Group The Moms Co 67.2 100.0

The acquisition will help Moms Co expands its offline presence and

integrate data and other offerings by the groups 2021

Good Glamm

Group Organic Harvest 33.3 51.0 This acquisition will improve the group's presence in the organic BPC 2021

ITC Mother Sparsh

8.7 The acquisition is in line the company's ITC Next strategy to build a future-

ready organisation with a digital first culture 2021

Mamaearth BBLUNT 17.7 100.0 With the acquisition, BBLUNT's hair care and styling products business

will be completely owned and managed by Honasa Consumer 2022

Page | 9

FMCG: D2C Disruption

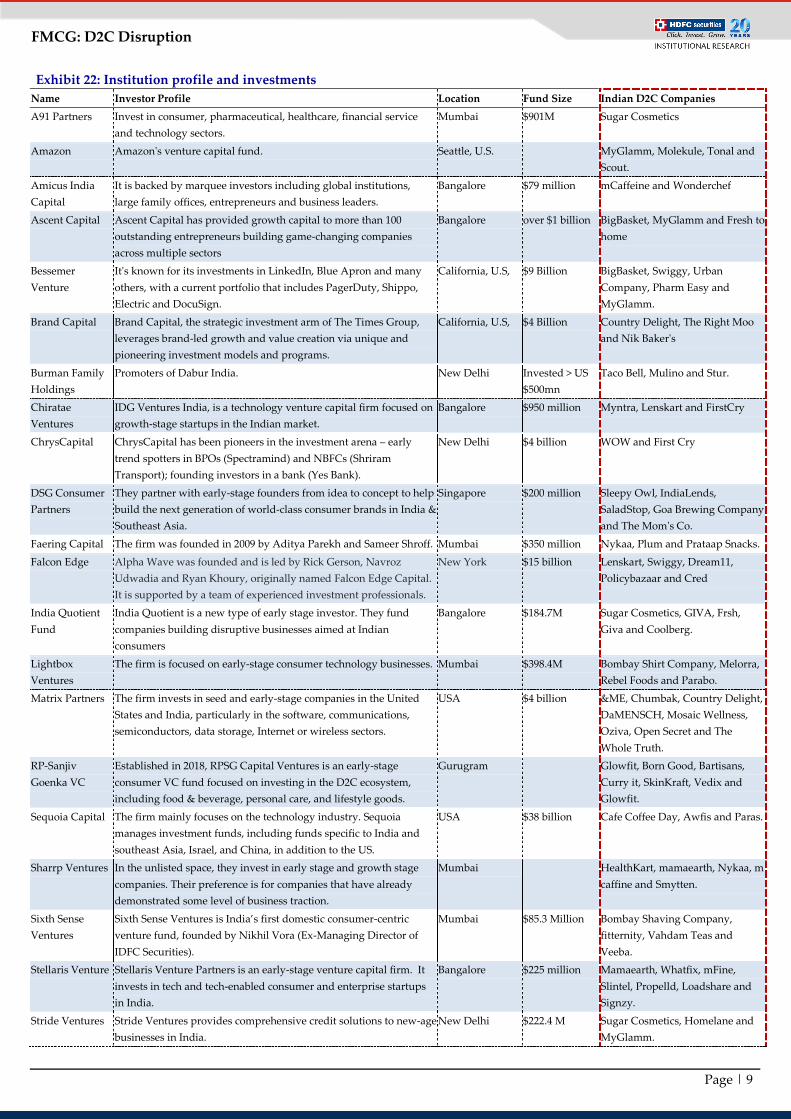

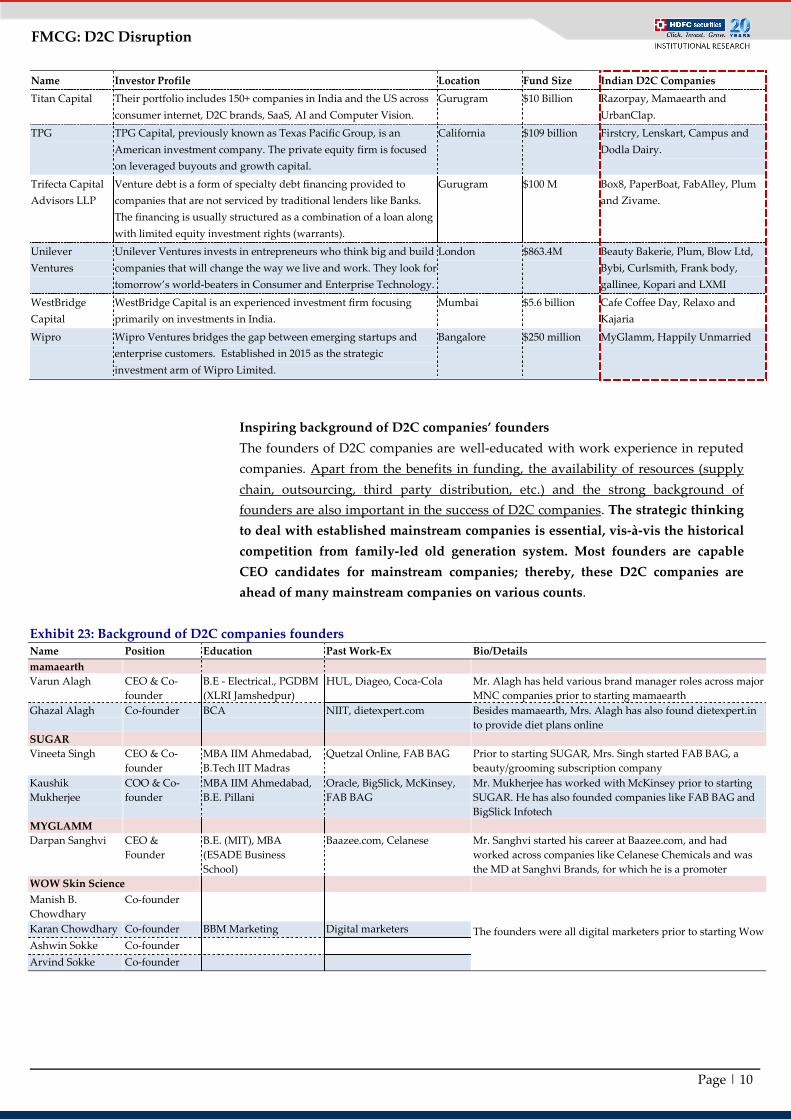

Exhibit 22: Institution profile and investments

Name Investor Profile Location Fund Size Indian D2C Companies

A91 Partners Invest in consumer, pharmaceutical, healthcare, financial service

and technology sectors.

Mumbai $901M Sugar Cosmetics

Amazon Amazon's venture capital fund. Seattle, U.S. MyGlamm, Molekule, Tonal and

Scout.

Amicus India

Capital

It is backed by marquee investors including global institutions,

large family offices, entrepreneurs and business leaders.

Bangalore $79 million mCaffeine and Wonderchef

Ascent Capital Ascent Capital has provided growth capital to more than 100

outstanding entrepreneurs building game-changing companies

across multiple sectors

Bangalore over $1 billion BigBasket, MyGlamm and Fresh to

home

Bessemer

Venture

It's known for its investments in LinkedIn, Blue Apron and many

others, with a current portfolio that includes PagerDuty, Shippo,

Electric and DocuSign.

California, U.S, $9 Billion BigBasket, Swiggy, Urban

Company, Pharm Easy and

MyGlamm.

Brand Capital Brand Capital, the strategic investment arm of The Times Group,

leverages brand-led growth and value creation via unique and

pioneering investment models and programs.

California, U.S, $4 Billion Country Delight, The Right Moo

and Nik Baker's

Burman Family

Holdings

Promoters of Dabur India. New Delhi Invested > US

$500mn

Taco Bell, Mulino and Stur.

Chiratae

Ventures

IDG Ventures India, is a technology venture capital firm focused on

growth-stage startups in the Indian market.

Bangalore $950 million Myntra, Lenskart and FirstCry

ChrysCapital ChrysCapital has been pioneers in the investment arena – early

trend spotters in BPOs (Spectramind) and NBFCs (Shriram

Transport); founding investors in a bank (Yes Bank).

New Delhi $4 billion WOW and First Cry

DSG Consumer

Partners

They partner with early-stage founders from idea to concept to help

build the next generation of world-class consumer brands in India &

Southeast Asia.

Singapore $200 million Sleepy Owl, IndiaLends,

SaladStop, Goa Brewing Company

and The Mom's Co.

Faering Capital The firm was founded in 2009 by Aditya Parekh and Sameer Shroff. Mumbai $350 million Nykaa, Plum and Prataap Snacks.

Falcon Edge Alpha Wave was founded and is led by Rick Gerson, Navroz

Udwadia and Ryan Khoury, originally named Falcon Edge Capital.

It is supported by a team of experienced investment professionals.

New York $15 billion Lenskart, Swiggy, Dream11,

Policybazaar and Cred

India Quotient

Fund

India Quotient is a new type of early stage investor. They fund

companies building disruptive businesses aimed at Indian

consumers

Bangalore $184.7M Sugar Cosmetics, GIVA, Frsh,

Giva and Coolberg.

Lightbox

Ventures

The firm is focused on early-stage consumer technology businesses. Mumbai $398.4M Bombay Shirt Company, Melorra,

Rebel Foods and Parabo.

Matrix Partners The firm invests in seed and early-stage companies in the United

States and India, particularly in the software, communications,

semiconductors, data storage, Internet or wireless sectors.

USA $4 billion &ME, Chumbak, Country Delight,

DaMENSCH, Mosaic Wellness,

Oziva, Open Secret and The

Whole Truth.

RP-Sanjiv

Goenka VC

Established in 2018, RPSG Capital Ventures is an early-stage

consumer VC fund focused on investing in the D2C ecosystem,

including food & beverage, personal care, and lifestyle goods.

Gurugram Glowfit, Born Good, Bartisans,

Curry it, SkinKraft, Vedix and

Glowfit.

Sequoia Capital The firm mainly focuses on the technology industry. Sequoia

manages investment funds, including funds specific to India and

southeast Asia, Israel, and China, in addition to the US.

USA $38 billion Cafe Coffee Day, Awfis and Paras.

Sharrp Ventures In the unlisted space, they invest in early stage and growth stage

companies. Their preference is for companies that have already

demonstrated some level of business traction.

Mumbai HealthKart, mamaearth, Nykaa, m

caffine and Smytten.

Sixth Sense

Ventures

Sixth Sense Ventures is India’s first domestic consumer-centric

venture fund, founded by Nikhil Vora (Ex-Managing Director of

IDFC Securities).

Mumbai $85.3 Million Bombay Shaving Company,

fitternity, Vahdam Teas and

Veeba.

Stellaris Venture Stellaris Venture Partners is an early-stage venture capital firm. It

invests in tech and tech-enabled consumer and enterprise startups

in India.

Bangalore $225 million Mamaearth, Whatfix, mFine,

Slintel, Propelld, Loadshare and

Signzy.

Stride Ventures Stride Ventures provides comprehensive credit solutions to new-age

businesses in India.

New Delhi $222.4 M Sugar Cosmetics, Homelane and

MyGlamm.

Page | 10

FMCG: D2C Disruption

Name Investor Profile Location Fund Size Indian D2C Companies

Titan Capital Their portfolio includes 150+ companies in India and the US across

consumer internet, D2C brands, SaaS, AI and Computer Vision.

Gurugram $10 Billion Razorpay, Mamaearth and

UrbanClap.

TPG TPG Capital, previously known as Texas Pacific Group, is an

American investment company. The private equity firm is focused

on leveraged buyouts and growth capital.

California $109 billion Firstcry, Lenskart, Campus and

Dodla Dairy.

Trifecta Capital

Advisors LLP

Venture debt is a form of specialty debt financing provided to

companies that are not serviced by traditional lenders like Banks.

The financing is usually structured as a combination of a loan along

with limited equity investment rights (warrants).

Gurugram $100 M Box8, PaperBoat, FabAlley, Plum

and Zivame.

Unilever

Ventures

Unilever Ventures invests in entrepreneurs who think big and build

companies that will change the way we live and work. They look for

tomorrow’s world-beaters in Consumer and Enterprise Technology.

London $863.4M Beauty Bakerie, Plum, Blow Ltd,

Bybi, Curlsmith, Frank body,

gallinee, Kopari and LXMI

WestBridge

Capital

WestBridge Capital is an experienced investment firm focusing

primarily on investments in India.

Mumbai $5.6 billion Cafe Coffee Day, Relaxo and

Kajaria

Wipro Wipro Ventures bridges the gap between emerging startups and

enterprise customers. Established in 2015 as the strategic

investment arm of Wipro Limited.

Bangalore $250 million MyGlamm, Happily Unmarried

Inspiring background of D2C companies’ founders

The founders of D2C companies are well-educated with work experience in reputed

companies. Apart from the benefits in funding, the availability of resources (supply

chain, outsourcing, third party distribution, etc.) and the strong background of

founders are also important in the success of D2C companies. The strategic thinking

to deal with established mainstream companies is essential, vis-à-vis the historical

competition from family-led old generation system. Most founders are capable

CEO candidates for mainstream companies; thereby, these D2C companies are

ahead of many mainstream companies on various counts.

Exhibit 23: Background of D2C companies founders Name Position Education Past Work-Ex Bio/Details

mamaearth

Varun Alagh CEO & Co-

founder

B.E - Electrical., PGDBM

(XLRI Jamshedpur)

HUL, Diageo, Coca-Cola Mr. Alagh has held various brand manager roles across major

MNC companies prior to starting mamaearth

Ghazal Alagh Co-founder BCA NIIT, dietexpert.com Besides mamaearth, Mrs. Alagh has also found dietexpert.in

to provide diet plans online

SUGAR

Vineeta Singh CEO & Co-

founder

MBA IIM Ahmedabad,

B.Tech IIT Madras

Quetzal Online, FAB BAG Prior to starting SUGAR, Mrs. Singh started FAB BAG, a

beauty/grooming subscription company

Kaushik

Mukherjee

COO & Co-

founder

MBA IIM Ahmedabad,

B.E. Pillani

Oracle, BigSlick, McKinsey,

FAB BAG

Mr. Mukherjee has worked with McKinsey prior to starting

SUGAR. He has also founded companies like FAB BAG and

BigSlick Infotech

MYGLAMM

Darpan Sanghvi CEO &

Founder

B.E. (MIT), MBA

(ESADE Business

School)

Baazee.com, Celanese Mr. Sanghvi started his career at Baazee.com, and had

worked across companies like Celanese Chemicals and was

the MD at Sanghvi Brands, for which he is a promoter

WOW Skin Science

Manish B.

Chowdhary

Co-founder

The founders were all digital marketers prior to starting Wow Karan Chowdhary Co-founder BBM Marketing Digital marketers

Ashwin Sokke Co-founder

Arvind Sokke Co-founder

Page | 11

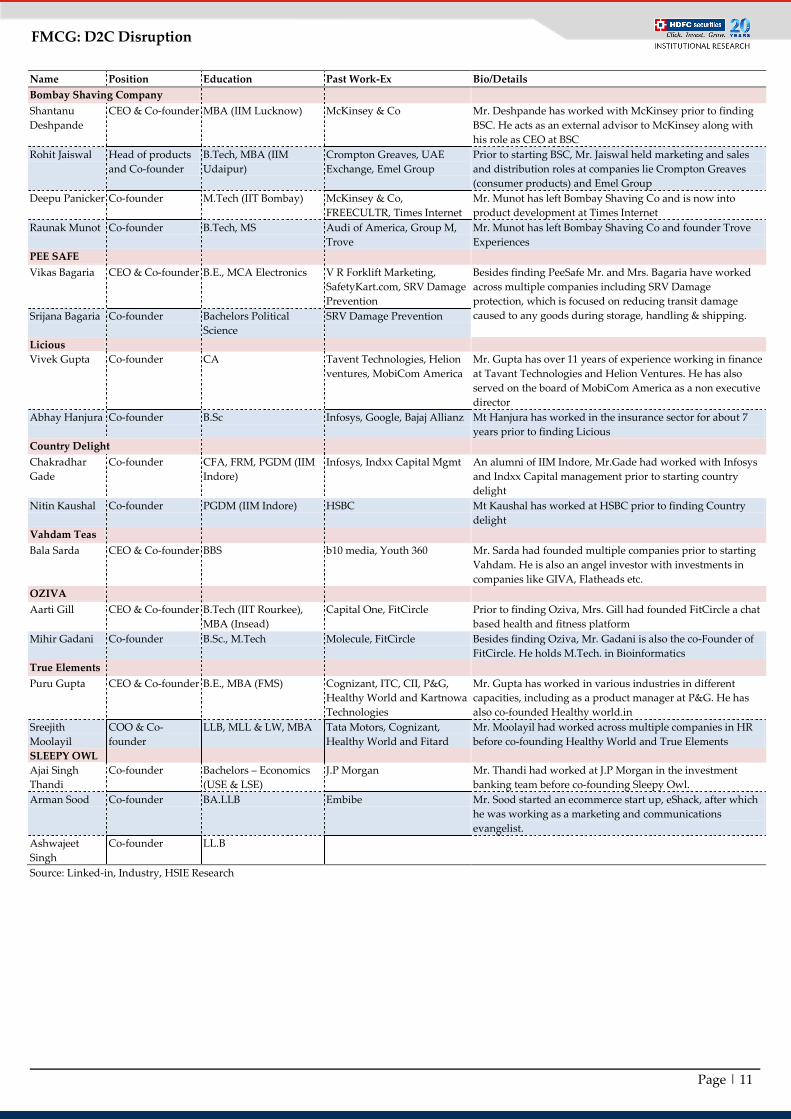

FMCG: D2C Disruption

Name Position Education Past Work-Ex Bio/Details

Bombay Shaving Company

Shantanu

Deshpande

CEO & Co-founder MBA (IIM Lucknow) McKinsey & Co Mr. Deshpande has worked with McKinsey prior to finding

BSC. He acts as an external advisor to McKinsey along with

his role as CEO at BSC

Rohit Jaiswal Head of products

and Co-founder

B.Tech, MBA (IIM

Udaipur)

Crompton Greaves, UAE

Exchange, Emel Group

Prior to starting BSC, Mr. Jaiswal held marketing and sales

and distribution roles at companies lie Crompton Greaves

(consumer products) and Emel Group

Deepu Panicker Co-founder M.Tech (IIT Bombay) McKinsey & Co,

FREECULTR, Times Internet

Mr. Munot has left Bombay Shaving Co and is now into

product development at Times Internet

Raunak Munot Co-founder B.Tech, MS Audi of America, Group M,

Trove

Mr. Munot has left Bombay Shaving Co and founder Trove

Experiences

PEE SAFE

Vikas Bagaria CEO & Co-founder B.E., MCA Electronics V R Forklift Marketing,

SafetyKart.com, SRV Damage

Prevention

Besides finding PeeSafe Mr. and Mrs. Bagaria have worked

across multiple companies including SRV Damage

protection, which is focused on reducing transit damage

caused to any goods during storage, handling & shipping. Srijana Bagaria Co-founder Bachelors Political

Science

SRV Damage Prevention

Licious

Vivek Gupta Co-founder CA Tavent Technologies, Helion

ventures, MobiCom America

Mr. Gupta has over 11 years of experience working in finance

at Tavant Technologies and Helion Ventures. He has also

served on the board of MobiCom America as a non executive

director

Abhay Hanjura Co-founder B.Sc Infosys, Google, Bajaj Allianz Mt Hanjura has worked in the insurance sector for about 7

years prior to finding Licious

Country Delight

Chakradhar

Gade

Co-founder CFA, FRM, PGDM (IIM

Indore)

Infosys, Indxx Capital Mgmt An alumni of IIM Indore, Mr.Gade had worked with Infosys

and Indxx Capital management prior to starting country

delight

Nitin Kaushal Co-founder PGDM (IIM Indore) HSBC Mt Kaushal has worked at HSBC prior to finding Country

delight

Vahdam Teas

Bala Sarda CEO & Co-founder BBS b10 media, Youth 360 Mr. Sarda had founded multiple companies prior to starting

Vahdam. He is also an angel investor with investments in

companies like GIVA, Flatheads etc.

OZIVA

Aarti Gill CEO & Co-founder B.Tech (IIT Rourkee),

MBA (Insead)

Capital One, FitCircle Prior to finding Oziva, Mrs. Gill had founded FitCircle a chat

based health and fitness platform

Mihir Gadani Co-founder B.Sc., M.Tech Molecule, FitCircle Besides finding Oziva, Mr. Gadani is also the co-Founder of

FitCircle. He holds M.Tech. in Bioinformatics

True Elements

Puru Gupta CEO & Co-founder B.E., MBA (FMS) Cognizant, ITC, CII, P&G,

Healthy World and Kartnowa

Technologies

Mr. Gupta has worked in various industries in different

capacities, including as a product manager at P&G. He has

also co-founded Healthy world.in

Sreejith

Moolayil

COO & Co-

founder

LLB, MLL & LW, MBA Tata Motors, Cognizant,

Healthy World and Fitard

Mr. Moolayil had worked across multiple companies in HR

before co-founding Healthy World and True Elements

SLEEPY OWL

Ajai Singh

Thandi

Co-founder Bachelors – Economics

(USE & LSE)

J.P Morgan Mr. Thandi had worked at J.P Morgan in the investment

banking team before co-founding Sleepy Owl.

Arman Sood Co-founder BA.LLB Embibe Mr. Sood started an ecommerce start up, eShack, after which

he was working as a marketing and communications

evangelist.

Ashwajeet

Singh

Co-founder LL.B

Source: Linked-in, Industry, HSIE Research

Page | 12

FMCG: D2C Disruption

D2C: Key success factors

While the above macro drivers and ecosystem were the seeds of D2C channel’s

growth, the channel’s growth was further facilitated and accelerated by various

effective D2C companies’ initiatives. These companies disrupted the traditional

business model, and their out-of-the-box approach gave them the x-factor in

customer acquisition in categories that were heavily backed by well-established

brands. Although there will be a variety of success factors, we believe the

following aspects are the most pertinent (also highlighted by D2C founders).

Unique product proposition

Filling in the white gaps with relevant product innovation

D2C brands provide a sheer variety of products across BPC and F&R space. This

benefits the customers with the increase in choice.

D2C brands in the F&R space are more inclined to the naturals-based health food

space, where established brands have a limited presence, thus giving rise to a

new space.

In categories like coffee, D2C brands have given rise to the more premium coffee

space with drip coffee and whole bean coffee offerings.

While F&R is not limited to the creation of new sub-categories, BPC categories

like feminine hygiene and men’s grooming are being popularized by D2C

brands.

Going the natural way

The brands in the BPC space have introduced innovative products in categories

like cosmetics, hair care, personal wash, and cream space. These products are

more focused on naturals and are plant based, with many having accreditations

from global and Indian standard bodies.

Ingredient-based products by D2C brands (onion hair care) have seen large

consumer adoption.

Some D2C brands are investing heavily in R&D to develop innovative products

with high saliency.

Categories like packaged food products, beverages, tea, etc., are seeing a rise of

health-oriented products. Priced at a premium, the products are made of natural

ingredients and are focused on either promoting healthy living, or solving health

problems.

Individualisation and customisation

D2C brands have been collecting and using customer data to develop new

products for a more targeted audience.

According to industrial participants, given the ease and desirable speed of

launches, D2C brands are able to conduct test launches conveniently with a more

effective consumer feedback loop.

Brands like True Elements offer hyper customisation where individual customers

can curate their snacks/muesli.

Page | 13

FMCG: D2C Disruption

Support from rapid development of the ecosystem

Streamlined logistics supports D2C

The boom of D2C brands was supported by development of logistic partners

enabling the industry to deliver 100mn parcels (across sectors) in FY21. Industry

participants expect this to reach 600mn by FY26.

Logistics partners continue to invest in technology and high quality

infrastructure to meet demand.

Logistic partners not only help D2C brands to deliver products at a speedy rate

pan India, but also aid in better inventory management.

A speedy delivery is a key customer satisfaction metric for D2C brands.

Trust in online payment, a key enabler

Adoption of online payment has been a key enabler for the growth of D2C

brands.

Online ecommerce transactions were historically heavily dependent on cash on

delivery (COD), rather than online payments.

Cash on delivery (COD) transactions have reduced from 60-70% five years back

to less than 30% currently.

The rise in adoption of online payments has been enabled by seamless and secure

transactions by customers through trusted payment gateways.

Changes in shopping habits a key positive

Return to origin (RTO) is 13-14x higher for COD vs. online payments.

RTOs impact D2C brands’ margins and lead to inventory overheads.

With consumers gaining trust in the payment systems, COD transactions are

gradually reducing.

A new age of customer interactions

Using new-age media for reaching customers

D2C brands are adopting social media to enhance their presence.

Regional strategy is old, consumer segmentation is the future.

Brands like SUGAR Cosmetics have leveraged the social media platforms to

educate women on makeup, which has helped it build its community.

Influencer marketing and social media help in generation hype towards a brand.

Nykaa has been one of the first brands in India to leverage this space and grow.

New platforms being developed to support reach

The influx of social media marketing gave rise to an Indian social commerce

platform, Trell. The platform targets the mass audience with consumer content in

vernacular languages.

Trell helps brands excel in tier-2 cities and beyond.

Tech enabled social media presence

D2C brands are using platforms like GupShup that facilitate WhatsApp

commerce.

The platform helps brands acquire new customers and leads, communicate

offers, enter transactions and make payments, improve website/app conversions,

and facilitate customer care and order updates.

Page | 14

FMCG: D2C Disruption

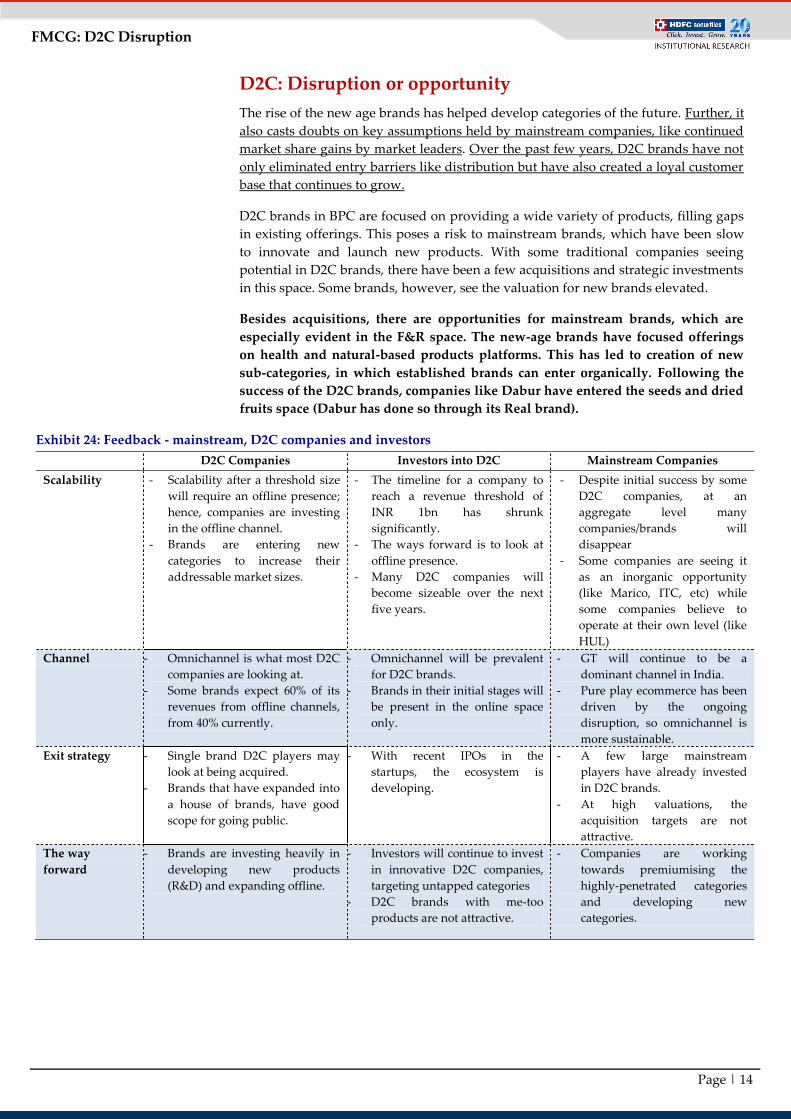

D2C: Disruption or opportunity

The rise of the new age brands has helped develop categories of the future. Further, it

also casts doubts on key assumptions held by mainstream companies, like continued

market share gains by market leaders. Over the past few years, D2C brands have not

only eliminated entry barriers like distribution but have also created a loyal customer

base that continues to grow.

D2C brands in BPC are focused on providing a wide variety of products, filling gaps

in existing offerings. This poses a risk to mainstream brands, which have been slow

to innovate and launch new products. With some traditional companies seeing

potential in D2C brands, there have been a few acquisitions and strategic investments

in this space. Some brands, however, see the valuation for new brands elevated.

Besides acquisitions, there are opportunities for mainstream brands, which are

especially evident in the F&R space. The new-age brands have focused offerings

on health and natural-based products platforms. This has led to creation of new

sub-categories, in which established brands can enter organically. Following the

success of the D2C brands, companies like Dabur have entered the seeds and dried

fruits space (Dabur has done so through its Real brand).

Exhibit 24: Feedback - mainstream, D2C companies and investors

D2C Companies Investors into D2C Mainstream Companies

Scalability - Scalability after a threshold size

will require an offline presence;

hence, companies are investing

in the offline channel.

- Brands are entering new

categories to increase their

addressable market sizes.

- The timeline for a company to

reach a revenue threshold of

INR 1bn has shrunk

significantly.

- The ways forward is to look at

offline presence.

- Many D2C companies will

become sizeable over the next

five years.

- Despite initial success by some

D2C companies, at an

aggregate level many

companies/brands will

disappear

- Some companies are seeing it

as an inorganic opportunity

(like Marico, ITC, etc) while

some companies believe to

operate at their own level (like

HUL)

Channel - Omnichannel is what most D2C

companies are looking at.

- Some brands expect 60% of its

revenues from offline channels,

from 40% currently.

- Omnichannel will be prevalent

for D2C brands.

- Brands in their initial stages will

be present in the online space

only.

- GT will continue to be a

dominant channel in India.

- Pure play ecommerce has been

driven by the ongoing

disruption, so omnichannel is

more sustainable.

Exit strategy - Single brand D2C players may

look at being acquired.

- Brands that have expanded into

a house of brands, have good

scope for going public.

- With recent IPOs in the

startups, the ecosystem is

developing.

- A few large mainstream

players have already invested

in D2C brands.

- At high valuations, the

acquisition targets are not

attractive.

The way

forward

- Brands are investing heavily in

developing new products

(R&D) and expanding offline.

- Investors will continue to invest

in innovative D2C companies,

targeting untapped categories

- D2C brands with me-too

products are not attractive.

- Companies are working

towards premiumising the

highly-penetrated categories

and developing new

categories.

Page | 15

FMCG: D2C Disruption

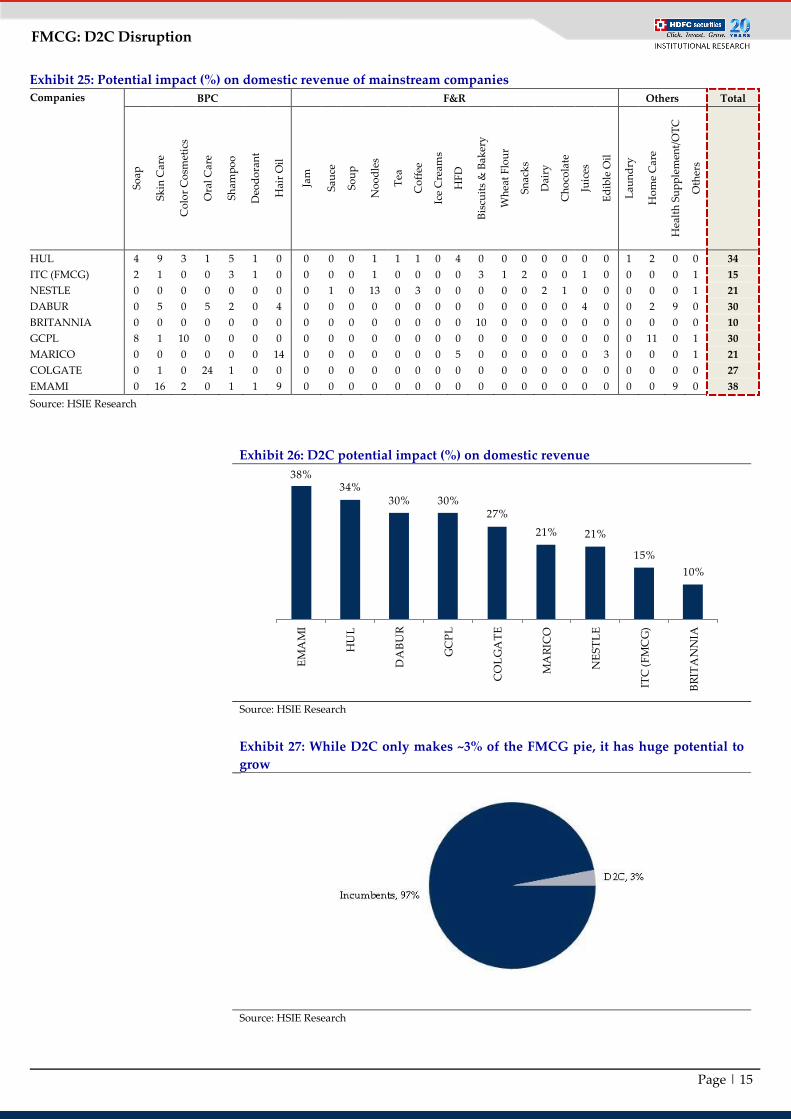

Exhibit 25: Potential impact (%) on domestic revenue of mainstream companies

Companies BPC F&R Others Total

So

ap

Sk

in C

are

Co

lor

Co

smet

ics

Ora

l C

are

Sh

amp

oo

Deo

do

ran

t

Hai

r O

il

Jam

Sau

ce

So

up

No

od

les

Tea

Co

ffee

Ice

Cre

ams

HF

D

Bis

cuit

s &

Bak

ery

Wh

eat

Flo

ur

Sn

ack

s

Dai

ry

Ch

oco

late

Juic

es

Ed

ible

Oil

Lau

nd

ry

Ho

me

Car

e

Hea

lth

Su

pp

lem

ent/

OT

C

Oth

ers

HUL 4 9 3 1 5 1 0 0 0 0 1 1 1 0 4 0 0 0 0 0 0 0 1 2 0 0 34

ITC (FMCG) 2 1 0 0 3 1 0 0 0 0 1 0 0 0 0 3 1 2 0 0 1 0 0 0 0 1 15

NESTLE 0 0 0 0 0 0 0 0 1 0 13 0 3 0 0 0 0 0 2 1 0 0 0 0 0 1 21

DABUR 0 5 0 5 2 0 4 0 0 0 0 0 0 0 0 0 0 0 0 0 4 0 0 2 9 0 30

BRITANNIA 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 10 0 0 0 0 0 0 0 0 0 0 10

GCPL 8 1 10 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 11 0 1 30

MARICO 0 0 0 0 0 0 14 0 0 0 0 0 0 0 5 0 0 0 0 0 0 3 0 0 0 1 21

COLGATE 0 1 0 24 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 27

EMAMI 0 16 2 0 1 1 9 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 9 0 38

Source: HSIE Research

Exhibit 26: D2C potential impact (%) on domestic revenue

Source: HSIE Research

Exhibit 27: While D2C only makes ~3% of the FMCG pie, it has huge potential to

grow

Source: HSIE Research

38%34%

30% 30%27%

21% 21%

15%

10%

EM

AM

I

HU

L

DA

BU

R

GC

PL

CO

LG

AT

E

MA

RIC

O

NE

ST

LE

ITC

(F

MC

G)

BR

ITA

NN

IA

Page | 16

FMCG: D2C Disruption

What is correct valuation premium, as assumptions alter?

FMCG companies have undergone substantial valuation rerating in the last 10-15

years, owing to sustained growth outperformance (compared to GDP/other sectors)

and the belief that outperformance would sustain. These companies have also

established growth visibility by consistently gaining market share and creating entry

barriers for new players. Customer stickiness and consistent upgradation provided

several levers to drive operating margin. Most companies have seen EBITDA margins

expand at around >500bps over the last decade.

However, the question is that, after seeing changes in those assumptions that drove

valuations, how much valuation premium is justified. The following key assumptions

are now undergoing changes.

Assumption 1: Market leaders will continue to gain market share

Top mainstream top brands have gained massive market shares, largely from

regional brands in the last two decades.

Regional players focused on being present in the mass segment only.

Consumers were upgrading, so buying top brands was natural.

D2C competition is up-down, unlike regional brands.

D2C is well-funded and well-managed.

Market share gain assumption will remain in check over the next decade.

Assumption 2: Distribution and supply chain provide a competitive edge

Supply chain capabilities and network of trade partners were the key entry

barriers for new entrants.

Now, supply chain is easily available for a new entrant.

Alternative distribution channels are proving to be level-playing fields.

Distribution, which was once a competitive edge for mainstream brands (and an

entry barrier for others) is gradually becoming less relevant with an increase in

alternative sales channels.

Assumption 3: Consumers will not experiment in BPC

Top brands were positioned like the best-in-class for product quality.

BPC was under-penetrated, with consumers trusting top brands only.

D2C launched out-of-the-box products with global packaging.

Now BPC seems to be the most exposed category from D2C brands.

Assumption 4: Food is a safe haven for top brands

Quality product with consistency was the right-to-win for most mainstream

brands.

Trust was the key driver.

D2C companies are focusing on product differentiation through health benefits.

D2C companies are creating new F&R categories.

Assumption 5: Premiumisation only for market leaders

Mainstream brands have seen huge benefits of premiumisation, as all of

consumer upgradation benefits have been accrued by top available brands.

D2C brands are at a premium to market leaders for most categories.

Now competition for mainstream brands is coming from up-down.

Page | 17

FMCG: D2C Disruption

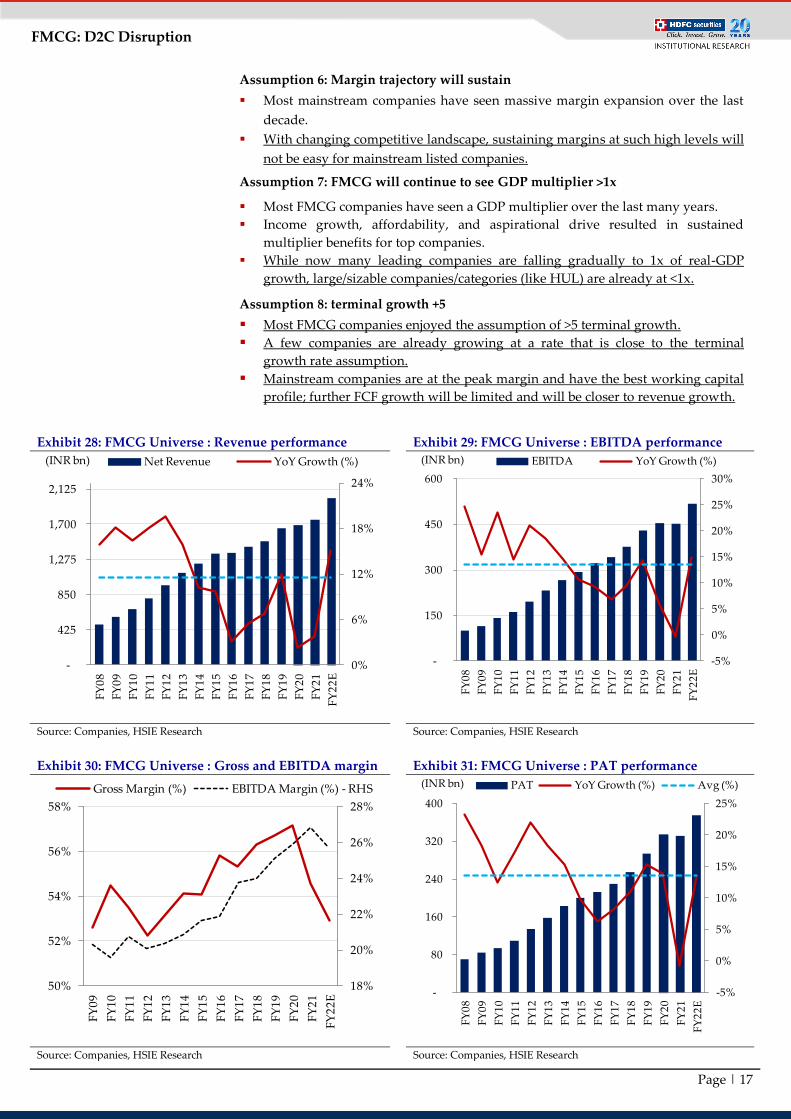

Assumption 6: Margin trajectory will sustain

Most mainstream companies have seen massive margin expansion over the last

decade.

With changing competitive landscape, sustaining margins at such high levels will

not be easy for mainstream listed companies.

Assumption 7: FMCG will continue to see GDP multiplier >1x

Most FMCG companies have seen a GDP multiplier over the last many years.

Income growth, affordability, and aspirational drive resulted in sustained

multiplier benefits for top companies.

While now many leading companies are falling gradually to 1x of real-GDP

growth, large/sizable companies/categories (like HUL) are already at <1x.

Assumption 8: terminal growth +5

Most FMCG companies enjoyed the assumption of >5 terminal growth. A few companies are already growing at a rate that is close to the terminal

growth rate assumption. Mainstream companies are at the peak margin and have the best working capital

profile; further FCF growth will be limited and will be closer to revenue growth.

Exhibit 28: FMCG Universe : Revenue performance Exhibit 29: FMCG Universe : EBITDA performance

Source: Companies, HSIE Research Source: Companies, HSIE Research

Exhibit 30: FMCG Universe : Gross and EBITDA margin Exhibit 31: FMCG Universe : PAT performance

Source: Companies, HSIE Research Source: Companies, HSIE Research

0%

6%

12%

18%

24%

-

425

850

1,275

1,700

2,125

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

Net Revenue YoY Growth (%)(INR bn)

-5%

0%

5%

10%

15%

20%

25%

30%

-

150

300

450

600

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

EBITDA YoY Growth (%)(INR bn)

18%

20%

22%

24%

26%

28%

50%

52%

54%

56%

58%

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

Gross Margin (%) EBITDA Margin (%) - RHS

-5%

0%

5%

10%

15%

20%

25%

-

80

160

240

320

400

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

PAT YoY Growth (%) Avg (%)(INR bn)

Page | 18

FMCG: D2C Disruption

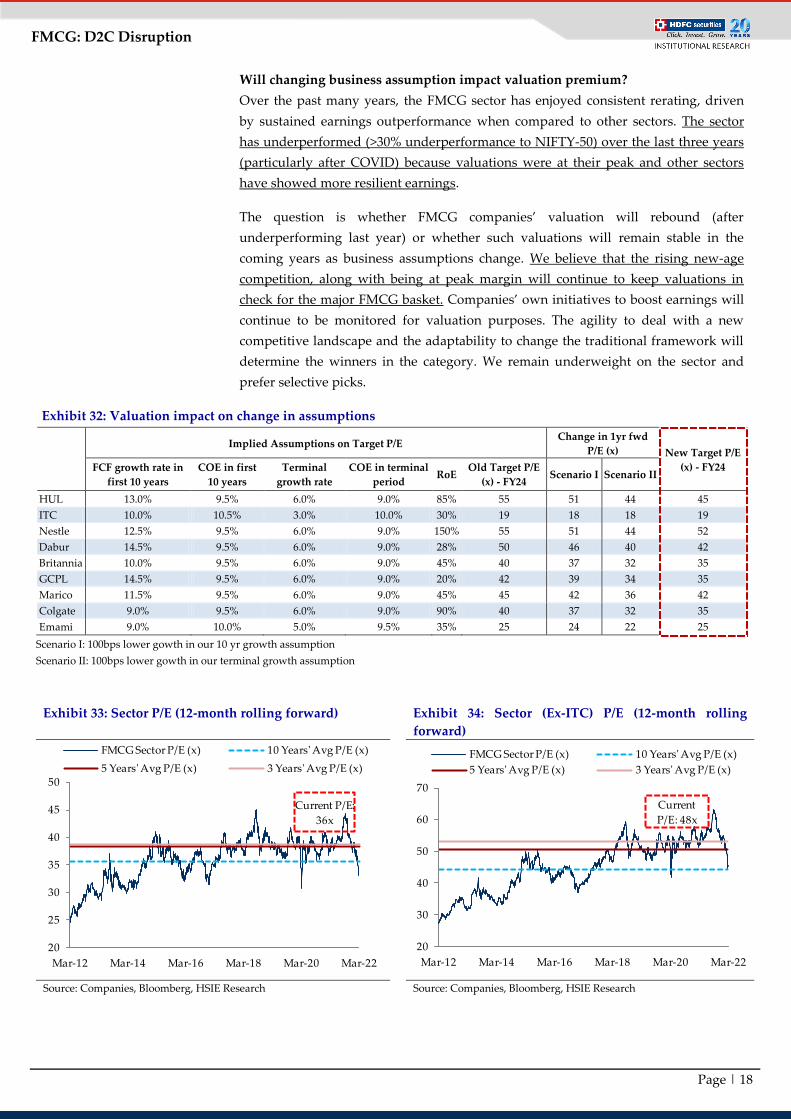

Will changing business assumption impact valuation premium?

Over the past many years, the FMCG sector has enjoyed consistent rerating, driven

by sustained earnings outperformance when compared to other sectors. The sector

has underperformed (>30% underperformance to NIFTY-50) over the last three years

(particularly after COVID) because valuations were at their peak and other sectors

have showed more resilient earnings.

The question is whether FMCG companies’ valuation will rebound (after

underperforming last year) or whether such valuations will remain stable in the

coming years as business assumptions change. We believe that the rising new-age

competition, along with being at peak margin will continue to keep valuations in

check for the major FMCG basket. Companies’ own initiatives to boost earnings will

continue to be monitored for valuation purposes. The agility to deal with a new

competitive landscape and the adaptability to change the traditional framework will

determine the winners in the category. We remain underweight on the sector and

prefer selective picks.

Exhibit 32: Valuation impact on change in assumptions

Implied Assumptions on Target P/E

Change in 1yr fwd

P/E (x) New Target P/E

(x) - FY24

FCF growth rate in

first 10 years

COE in first

10 years

Terminal

growth rate

COE in terminal

period RoE

Old Target P/E

(x) - FY24 Scenario I Scenario II

HUL 13.0% 9.5% 6.0% 9.0% 85% 55 51 44 45

ITC 10.0% 10.5% 3.0% 10.0% 30% 19 18 18 19

Nestle 12.5% 9.5% 6.0% 9.0% 150% 55 51 44 52

Dabur 14.5% 9.5% 6.0% 9.0% 28% 50 46 40 42

Britannia 10.0% 9.5% 6.0% 9.0% 45% 40 37 32 35

GCPL 14.5% 9.5% 6.0% 9.0% 20% 42 39 34 35

Marico 11.5% 9.5% 6.0% 9.0% 45% 45 42 36 42

Colgate 9.0% 9.5% 6.0% 9.0% 90% 40 37 32 35

Emami 9.0% 10.0% 5.0% 9.5% 35% 25 24 22 25

Scenario I: 100bps lower gowth in our 10 yr growth assumption

Scenario II: 100bps lower gowth in our terminal growth assumption

Exhibit 33: Sector P/E (12-month rolling forward) Exhibit 34: Sector (Ex-ITC) P/E (12-month rolling

forward)

Source: Companies, Bloomberg, HSIE Research Source: Companies, Bloomberg, HSIE Research

20

25

30

35

40

45

50

Mar-12 Mar-14 Mar-16 Mar-18 Mar-20 Mar-22

FMCG Sector P/E (x) 10 Years' Avg P/E (x)

5 Years' Avg P/E (x) 3 Years' Avg P/E (x)

Current P/E:

36x

20

30

40

50

60

70

Mar-12 Mar-14 Mar-16 Mar-18 Mar-20 Mar-22

FMCG Sector P/E (x) 10 Years' Avg P/E (x)

5 Years' Avg P/E (x) 3 Years' Avg P/E (x)

Current

P/E: 48x

Page | 19

FMCG: D2C Disruption

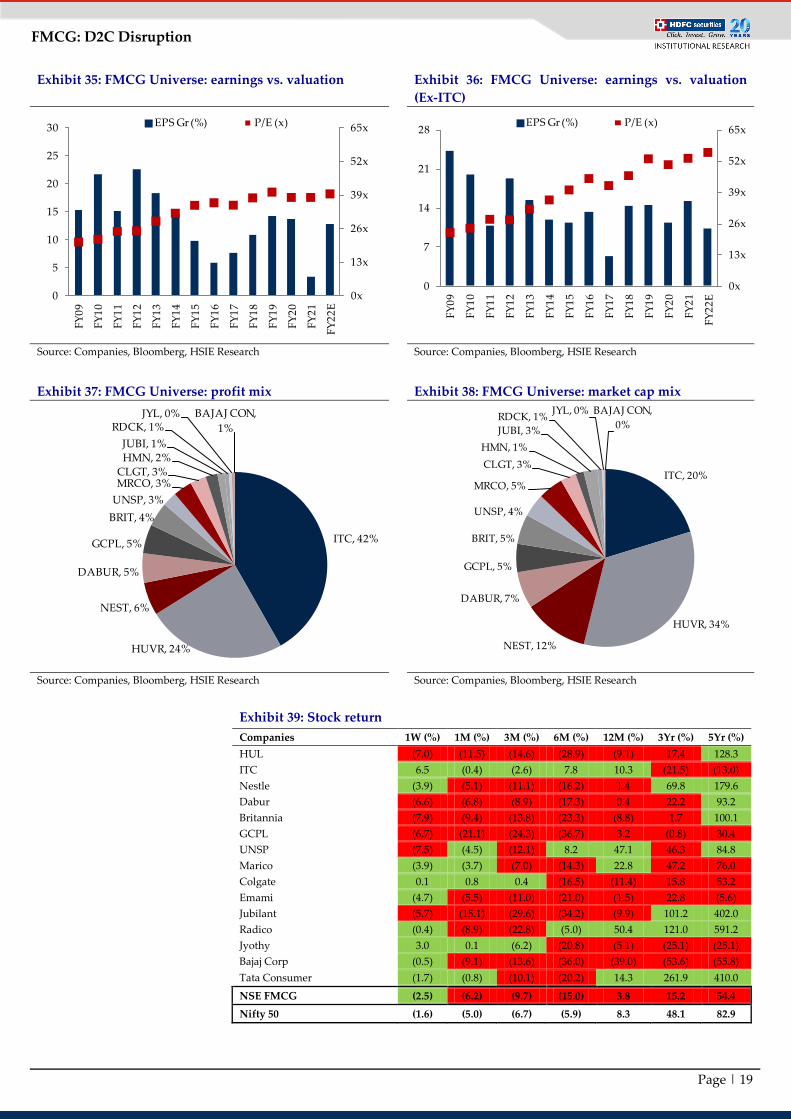

Exhibit 35: FMCG Universe: earnings vs. valuation Exhibit 36: FMCG Universe: earnings vs. valuation

(Ex-ITC)

Source: Companies, Bloomberg, HSIE Research Source: Companies, Bloomberg, HSIE Research

Exhibit 37: FMCG Universe: profit mix Exhibit 38: FMCG Universe: market cap mix

Source: Companies, Bloomberg, HSIE Research Source: Companies, Bloomberg, HSIE Research

Exhibit 39: Stock return

Companies 1W (%) 1M (%) 3M (%) 6M (%) 12M (%) 3Yr (%) 5Yr (%)

HUL (7.0) (11.5) (14.6) (28.9) (9.1) 17.4 128.3

ITC 6.5 (0.4) (2.6) 7.8 10.3 (21.5) (13.0)

Nestle (3.9) (5.1) (11.1) (16.2) 1.4 69.8 179.6

Dabur (6.6) (6.8) (8.9) (17.3) 0.4 22.2 93.2

Britannia (7.9) (9.4) (13.8) (23.3) (8.8) 1.7 100.1

GCPL (6.7) (21.1) (24.3) (36.7) 3.2 (0.8) 30.4

UNSP (7.5) (4.5) (12.1) 8.2 47.1 46.3 84.8

Marico (3.9) (3.7) (7.0) (14.3) 22.8 47.2 76.0

Colgate 0.1 0.8 0.4 (16.5) (11.4) 15.8 53.2

Emami (4.7) (5.5) (11.0) (21.0) (1.5) 22.8 (5.6)

Jubilant (5.7) (15.1) (29.6) (34.2) (9.9) 101.2 402.0

Radico (0.4) (8.9) (22.8) (5.0) 50.4 121.0 591.2

Jyothy 3.0 0.1 (6.2) (20.8) (5.1) (25.1) (25.1)

Bajaj Corp (0.5) (9.1) (13.6) (36.0) (39.0) (53.6) (55.8)

Tata Consumer (1.7) (0.8) (10.1) (20.2) 14.3 261.9 410.0

NSE FMCG (2.5) (6.2) (9.7) (15.0) 3.8 15.2 54.4

Nifty 50 (1.6) (5.0) (6.7) (5.9) 8.3 48.1 82.9

0x

13x

26x

39x

52x

65x

0

5

10

15

20

25

30

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

EPS Gr (%) P/E (x)

0x

13x

26x

39x

52x

65x

0

7

14

21

28

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

E

EPS Gr (%) P/E (x)

ITC, 42%

HUVR, 24%

NEST, 6%

DABUR, 5%

GCPL, 5%

BRIT, 4%

UNSP, 3%

MRCO, 3%CLGT, 3%

HMN, 2%

JUBI, 1%

RDCK, 1%JYL, 0% BAJAJ CON,

1%

ITC, 20%

HUVR, 34%

NEST, 12%

DABUR, 7%

GCPL, 5%

BRIT, 5%

UNSP, 4%

MRCO, 5%

CLGT, 3%

HMN, 1%

JUBI, 3%

RDCK, 1%JYL, 0% BAJAJ CON,

0%

Page | 20

FMCG: D2C Disruption

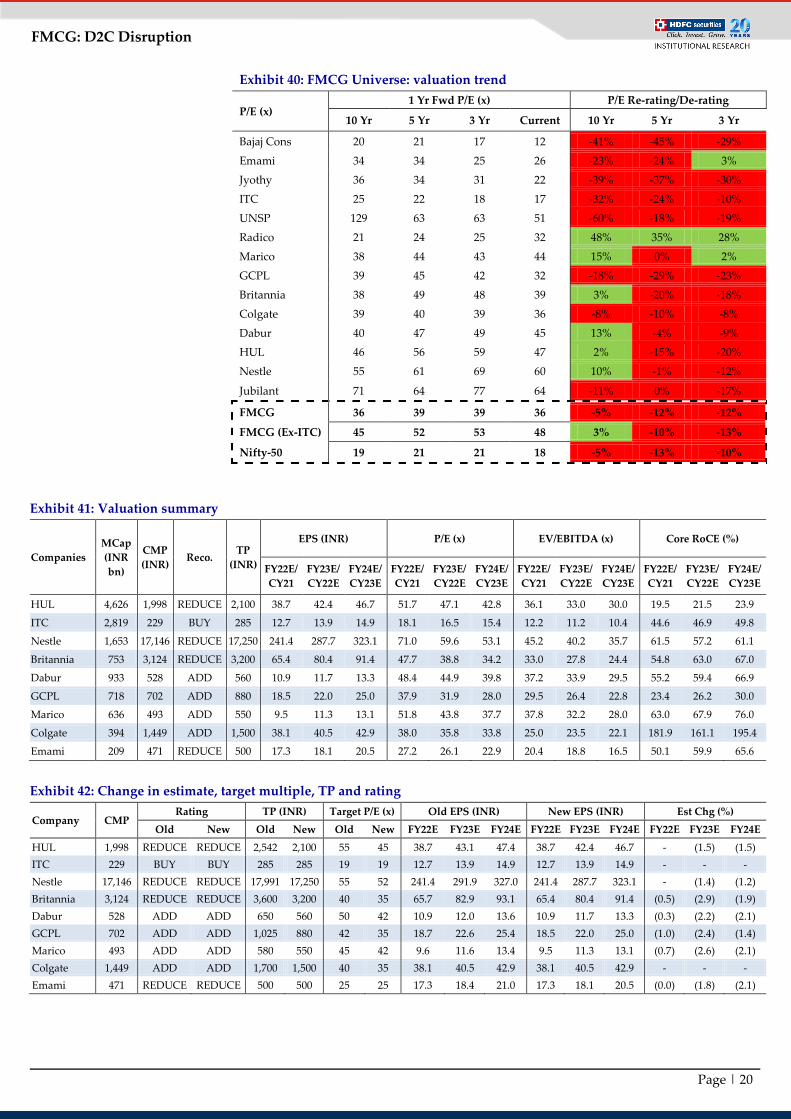

Exhibit 40: FMCG Universe: valuation trend

P/E (x) 1 Yr Fwd P/E (x) P/E Re-rating/De-rating

10 Yr 5 Yr 3 Yr Current 10 Yr 5 Yr 3 Yr

Bajaj Cons 20 21 17 12 -41% -45% -29%

Emami 34 34 25 26 -23% -24% 3%

Jyothy 36 34 31 22 -39% -37% -30%

ITC 25 22 18 17 -32% -24% -10%

UNSP 129 63 63 51 -60% -18% -19%

Radico 21 24 25 32 48% 35% 28%

Marico 38 44 43 44 15% 0% 2%

GCPL 39 45 42 32 -18% -29% -23%

Britannia 38 49 48 39 3% -20% -18%

Colgate 39 40 39 36 -8% -10% -8%

Dabur 40 47 49 45 13% -4% -9%

HUL 46 56 59 47 2% -15% -20%

Nestle 55 61 69 60 10% -1% -12%

Jubilant 71 64 77 64 -11% 0% -17%

FMCG 36 39 39 36 -5% -12% -12%

FMCG (Ex-ITC) 45 52 53 48 3% -10% -13%

Nifty-50 19 21 21 18 -5% -13% -10%

Exhibit 41: Valuation summary

Companies

MCap

(INR

bn)

CMP

(INR) Reco.

TP

(INR)

EPS (INR) P/E (x) EV/EBITDA (x) Core RoCE (%)

FY22E/

CY21

FY23E/

CY22E

FY24E/

CY23E

FY22E/

CY21

FY23E/

CY22E

FY24E/

CY23E

FY22E/

CY21

FY23E/

CY22E

FY24E/

CY23E

FY22E/

CY21

FY23E/

CY22E

FY24E/

CY23E

HUL 4,626 1,998 REDUCE 2,100 38.7 42.4 46.7 51.7 47.1 42.8 36.1 33.0 30.0 19.5 21.5 23.9

ITC 2,819 229 BUY 285 12.7 13.9 14.9 18.1 16.5 15.4 12.2 11.2 10.4 44.6 46.9 49.8

Nestle 1,653 17,146 REDUCE 17,250 241.4 287.7 323.1 71.0 59.6 53.1 45.2 40.2 35.7 61.5 57.2 61.1

Britannia 753 3,124 REDUCE 3,200 65.4 80.4 91.4 47.7 38.8 34.2 33.0 27.8 24.4 54.8 63.0 67.0

Dabur 933 528 ADD 560 10.9 11.7 13.3 48.4 44.9 39.8 37.2 33.9 29.5 55.2 59.4 66.9

GCPL 718 702 ADD 880 18.5 22.0 25.0 37.9 31.9 28.0 29.5 26.4 22.8 23.4 26.2 30.0

Marico 636 493 ADD 550 9.5 11.3 13.1 51.8 43.8 37.7 37.8 32.2 28.0 63.0 67.9 76.0

Colgate 394 1,449 ADD 1,500 38.1 40.5 42.9 38.0 35.8 33.8 25.0 23.5 22.1 181.9 161.1 195.4

Emami 209 471 REDUCE 500 17.3 18.1 20.5 27.2 26.1 22.9 20.4 18.8 16.5 50.1 59.9 65.6

Exhibit 42: Change in estimate, target multiple, TP and rating

Company CMP Rating TP (INR) Target P/E (x) Old EPS (INR) New EPS (INR) Est Chg (%)

Old New Old New Old New FY22E FY23E FY24E FY22E FY23E FY24E FY22E FY23E FY24E

HUL 1,998 REDUCE REDUCE 2,542 2,100 55 45 38.7 43.1 47.4 38.7 42.4 46.7 - (1.5) (1.5)

ITC 229 BUY BUY 285 285 19 19 12.7 13.9 14.9 12.7 13.9 14.9 - - -

Nestle 17,146 REDUCE REDUCE 17,991 17,250 55 52 241.4 291.9 327.0 241.4 287.7 323.1 - (1.4) (1.2)

Britannia 3,124 REDUCE REDUCE 3,600 3,200 40 35 65.7 82.9 93.1 65.4 80.4 91.4 (0.5) (2.9) (1.9)

Dabur 528 ADD ADD 650 560 50 42 10.9 12.0 13.6 10.9 11.7 13.3 (0.3) (2.2) (2.1)

GCPL 702 ADD ADD 1,025 880 42 35 18.7 22.6 25.4 18.5 22.0 25.0 (1.0) (2.4) (1.4)

Marico 493 ADD ADD 580 550 45 42 9.6 11.6 13.4 9.5 11.3 13.1 (0.7) (2.6) (2.1)

Colgate 1,449 ADD ADD 1,700 1,500 40 35 38.1 40.5 42.9 38.1 40.5 42.9 - - -

Emami 471 REDUCE REDUCE 500 500 25 25 17.3 18.4 21.0 17.3 18.1 20.5 (0.0) (1.8) (2.1)

Page | 21

FMCG: D2C Disruption

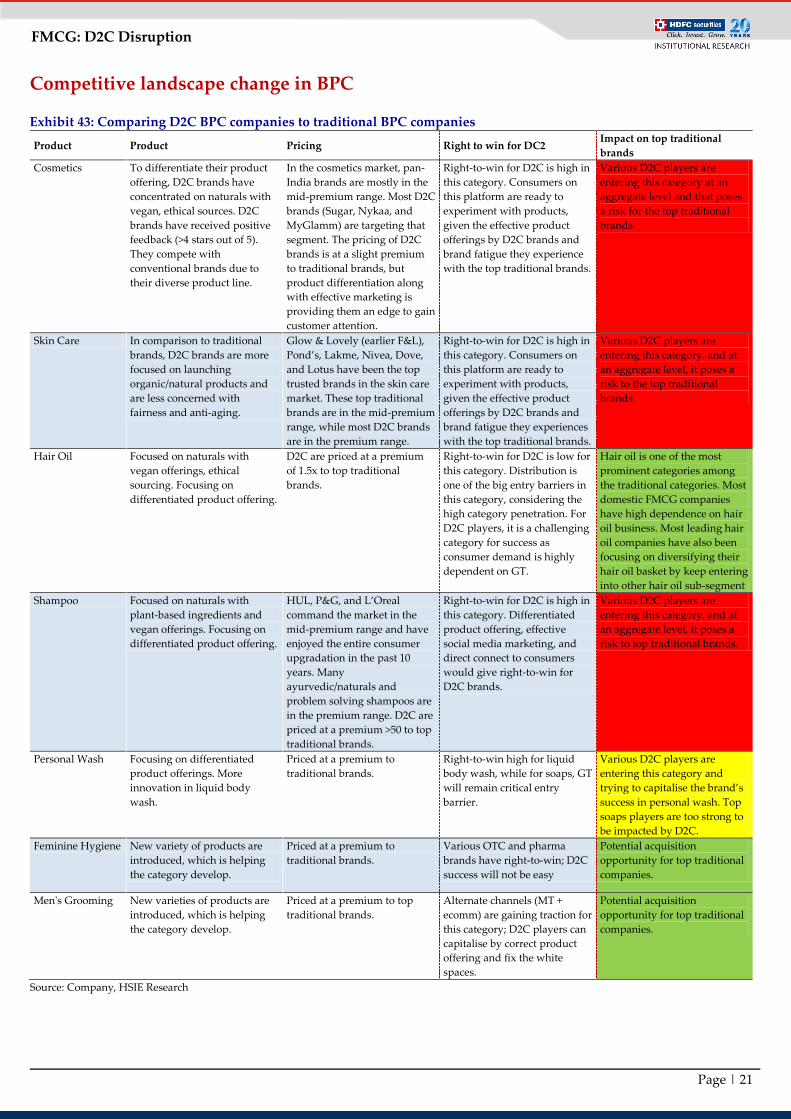

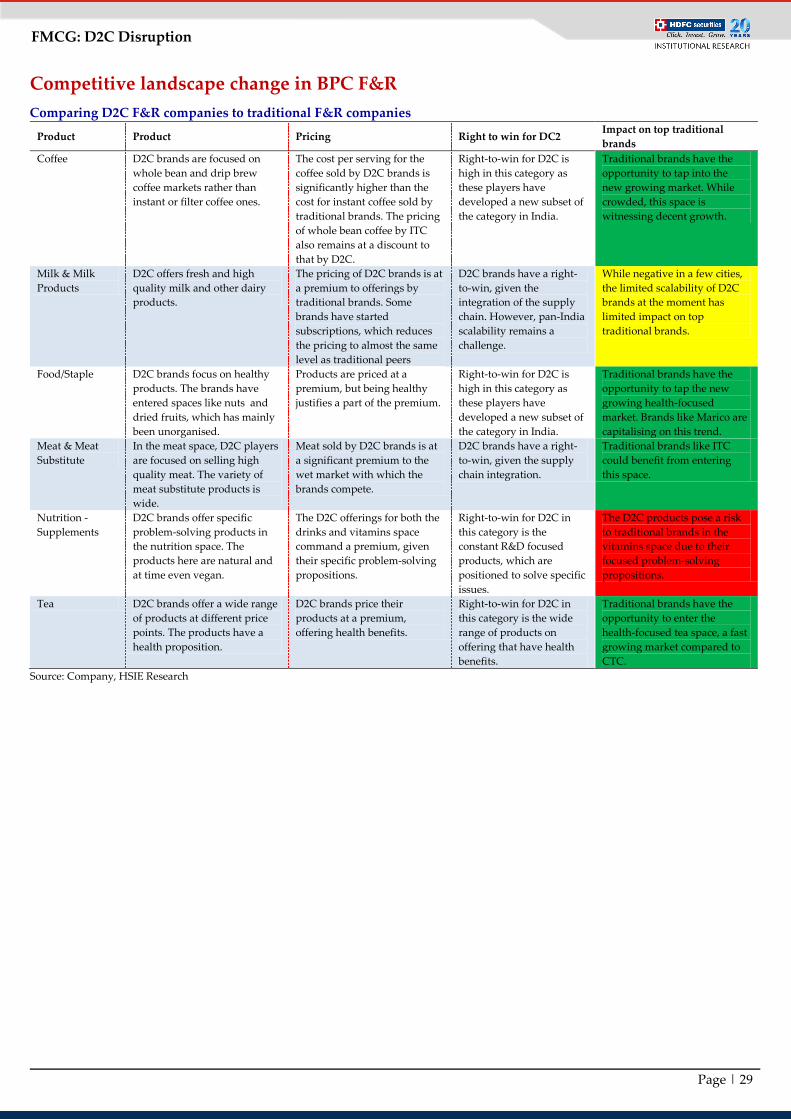

Competitive landscape change in BPC

Exhibit 43: Comparing D2C BPC companies to traditional BPC companies

Product Product Pricing Right to win for DC2 Impact on top traditional

brands

Cosmetics To differentiate their product

offering, D2C brands have

concentrated on naturals with

vegan, ethical sources. D2C

brands have received positive

feedback (>4 stars out of 5).

They compete with

conventional brands due to

their diverse product line.

In the cosmetics market, pan-

India brands are mostly in the

mid-premium range. Most D2C

brands (Sugar, Nykaa, and

MyGlamm) are targeting that

segment. The pricing of D2C

brands is at a slight premium

to traditional brands, but

product differentiation along

with effective marketing is

providing them an edge to gain

customer attention.

Right-to-win for D2C is high in

this category. Consumers on

this platform are ready to

experiment with products,

given the effective product

offerings by D2C brands and

brand fatigue they experience

with the top traditional brands.

Various D2C players are

entering this category at an

aggregate level and that poses

a risk for the top traditional

brands

Skin Care In comparison to traditional

brands, D2C brands are more

focused on launching

organic/natural products and

are less concerned with

fairness and anti-aging.

Glow & Lovely (earlier F&L),

Pond’s, Lakme, Nivea, Dove,

and Lotus have been the top

trusted brands in the skin care

market. These top traditional

brands are in the mid-premium

range, while most D2C brands

are in the premium range.

Right-to-win for D2C is high in

this category. Consumers on

this platform are ready to

experiment with products,

given the effective product

offerings by D2C brands and

brand fatigue they experiences

with the top traditional brands.

Various D2C players are

entering this category, and at

an aggregate level, it poses a

risk to the top traditional

brands

Hair Oil Focused on naturals with

vegan offerings, ethical

sourcing. Focusing on

differentiated product offering.

D2C are priced at a premium

of 1.5x to top traditional

brands.

Right-to-win for D2C is low for

this category. Distribution is

one of the big entry barriers in

this category, considering the

high category penetration. For

D2C players, it is a challenging

category for success as

consumer demand is highly

dependent on GT.

Hair oil is one of the most

prominent categories among

the traditional categories. Most

domestic FMCG companies

have high dependence on hair

oil business. Most leading hair

oil companies have also been

focusing on diversifying their

hair oil basket by keep entering

into other hair oil sub-segment

Shampoo Focused on naturals with

plant-based ingredients and

vegan offerings. Focusing on

differentiated product offering.

HUL, P&G, and L’Oreal

command the market in the

mid-premium range and have

enjoyed the entire consumer

upgradation in the past 10

years. Many

ayurvedic/naturals and

problem solving shampoos are

in the premium range. D2C are

priced at a premium >50 to top

traditional brands.

Right-to-win for D2C is high in

this category. Differentiated

product offering, effective

social media marketing, and

direct connect to consumers

would give right-to-win for

D2C brands.

Various D2C players are

entering this category, and at

an aggregate level, it poses a

risk to top traditional brands.

Personal Wash Focusing on differentiated

product offerings. More

innovation in liquid body

wash.

Priced at a premium to

traditional brands.

Right-to-win high for liquid

body wash, while for soaps, GT

will remain critical entry

barrier.

Various D2C players are

entering this category and

trying to capitalise the brand’s

success in personal wash. Top

soaps players are too strong to

be impacted by D2C.

Feminine Hygiene New variety of products are

introduced, which is helping

the category develop.

Priced at a premium to

traditional brands.

Various OTC and pharma

brands have right-to-win; D2C

success will not be easy

Potential acquisition

opportunity for top traditional

companies.

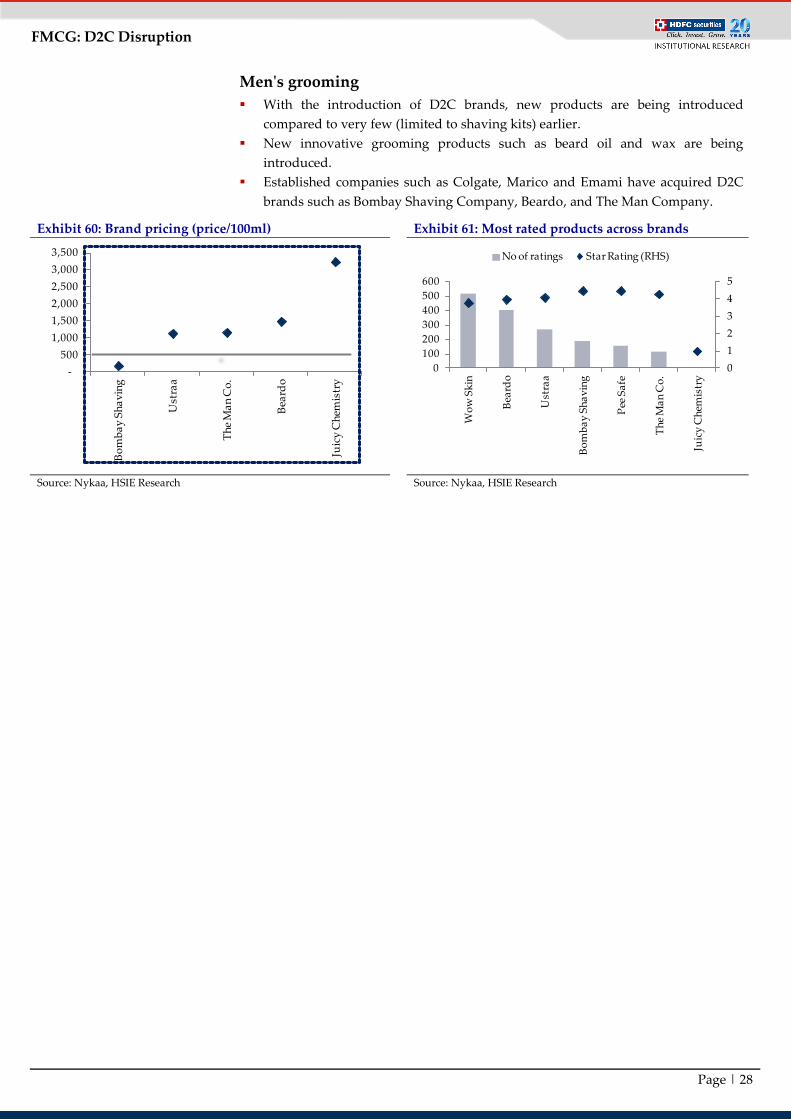

Men's Grooming New varieties of products are

introduced, which is helping

the category develop.

Priced at a premium to top

traditional brands.

Alternate channels (MT +

ecomm) are gaining traction for

this category; D2C players can

capitalise by correct product

offering and fix the white

spaces.

Potential acquisition

opportunity for top traditional

companies.

Source: Company, HSIE Research

Page | 22

FMCG: D2C Disruption

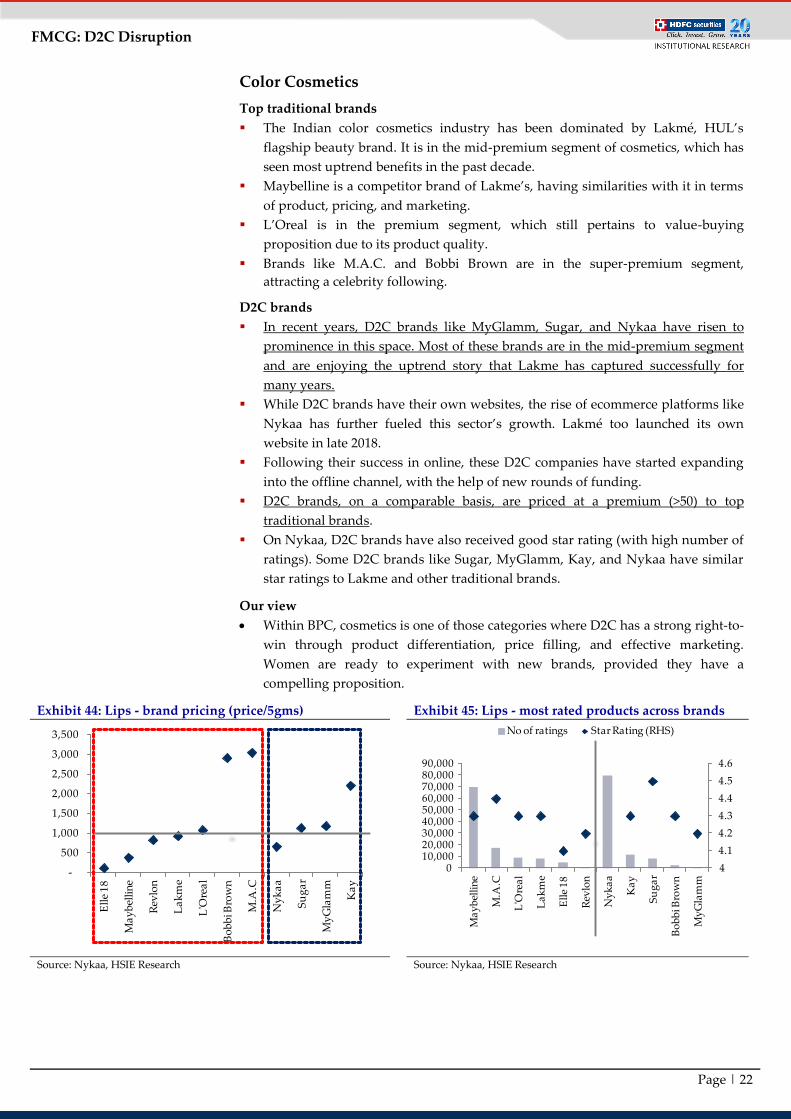

Color Cosmetics

Top traditional brands

The Indian color cosmetics industry has been dominated by Lakmé, HUL’s

flagship beauty brand. It is in the mid-premium segment of cosmetics, which has

seen most uptrend benefits in the past decade.

Maybelline is a competitor brand of Lakme’s, having similarities with it in terms

of product, pricing, and marketing.

L’Oreal is in the premium segment, which still pertains to value-buying

proposition due to its product quality.

Brands like M.A.C. and Bobbi Brown are in the super-premium segment,

attracting a celebrity following.

D2C brands

In recent years, D2C brands like MyGlamm, Sugar, and Nykaa have risen to

prominence in this space. Most of these brands are in the mid-premium segment

and are enjoying the uptrend story that Lakme has captured successfully for

many years.

While D2C brands have their own websites, the rise of ecommerce platforms like

Nykaa has further fueled this sector’s growth. Lakmé too launched its own

website in late 2018.

Following their success in online, these D2C companies have started expanding

into the offline channel, with the help of new rounds of funding.

D2C brands, on a comparable basis, are priced at a premium (>50) to top

traditional brands.

On Nykaa, D2C brands have also received good star rating (with high number of

ratings). Some D2C brands like Sugar, MyGlamm, Kay, and Nykaa have similar

star ratings to Lakme and other traditional brands.

Our view

Within BPC, cosmetics is one of those categories where D2C has a strong right-to-

win through product differentiation, price filling, and effective marketing.

Women are ready to experiment with new brands, provided they have a

compelling proposition.

Exhibit 44: Lips - brand pricing (price/5gms) Exhibit 45: Lips - most rated products across brands

Source: Nykaa, HSIE Research Source: Nykaa, HSIE Research

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Ell

e 1

8

Ma

yb

elli

ne

Rev

lon

La

km

e

L'O

rea

l

Bo

bb

i Bro

wn

M.A

.C

Ny

ka

a

Su

ga

r

My

Gla

mm

Ka

y

4

4.1

4.2

4.3

4.4

4.5

4.6

010,00020,00030,00040,00050,00060,00070,00080,00090,000

Ma

yb

elli

ne

M.A

.C

L'O

rea

l

La

km

e

Ell

e 1

8

Rev

lon

Ny

ka

a

Ka

y

Su

ga

r

Bo

bb

i Bro

wn

My

Gla

mm

No of ratings Star Rating (RHS)

Page | 23

FMCG: D2C Disruption

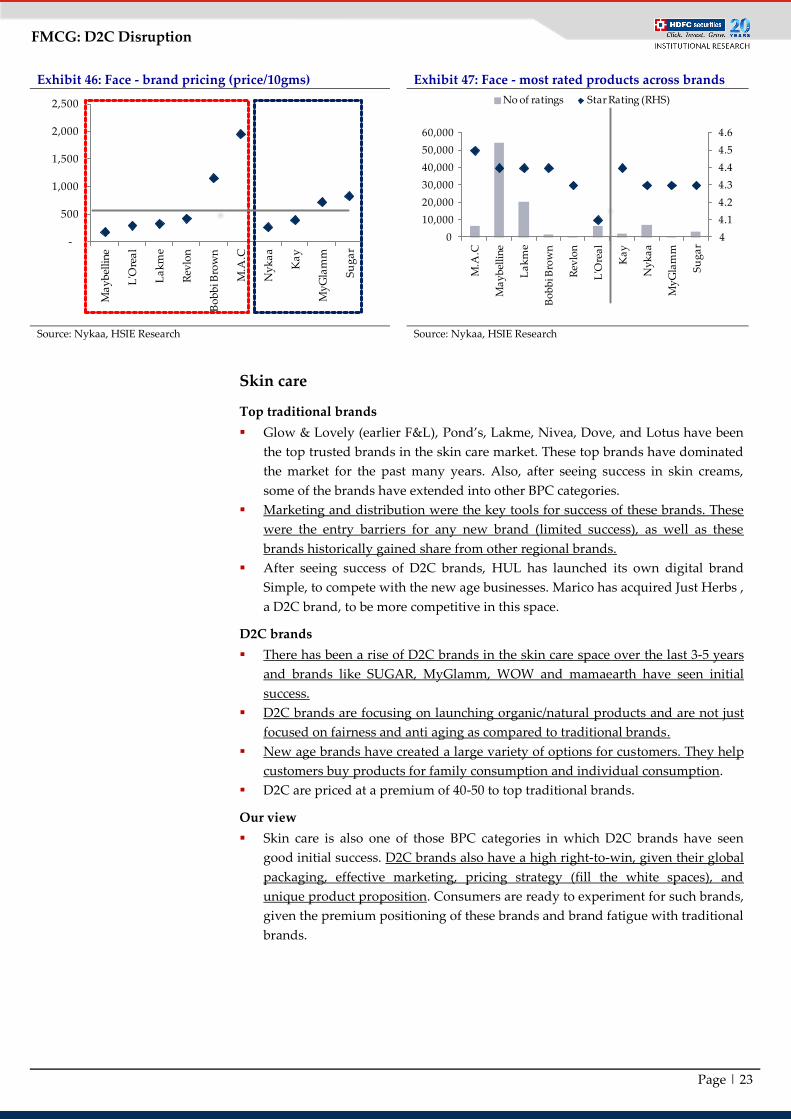

Exhibit 46: Face - brand pricing (price/10gms) Exhibit 47: Face - most rated products across brands

Source: Nykaa, HSIE Research Source: Nykaa, HSIE Research

Skin care

Top traditional brands

Glow & Lovely (earlier F&L), Pond’s, Lakme, Nivea, Dove, and Lotus have been

the top trusted brands in the skin care market. These top brands have dominated

the market for the past many years. Also, after seeing success in skin creams,

some of the brands have extended into other BPC categories.

Marketing and distribution were the key tools for success of these brands. These

were the entry barriers for any new brand (limited success), as well as these

brands historically gained share from other regional brands.

After seeing success of D2C brands, HUL has launched its own digital brand

Simple, to compete with the new age businesses. Marico has acquired Just Herbs ,

a D2C brand, to be more competitive in this space.

D2C brands

There has been a rise of D2C brands in the skin care space over the last 3-5 years

and brands like SUGAR, MyGlamm, WOW and mamaearth have seen initial

success.

D2C brands are focusing on launching organic/natural products and are not just

focused on fairness and anti aging as compared to traditional brands.

New age brands have created a large variety of options for customers. They help

customers buy products for family consumption and individual consumption.

D2C are priced at a premium of 40-50 to top traditional brands.

Our view

Skin care is also one of those BPC categories in which D2C brands have seen

good initial success. D2C brands also have a high right-to-win, given their global

packaging, effective marketing, pricing strategy (fill the white spaces), and

unique product proposition. Consumers are ready to experiment for such brands,

given the premium positioning of these brands and brand fatigue with traditional

brands.

-

500

1,000

1,500

2,000

2,500 M

ay

bel

lin

e

L'O

rea

l

La

km

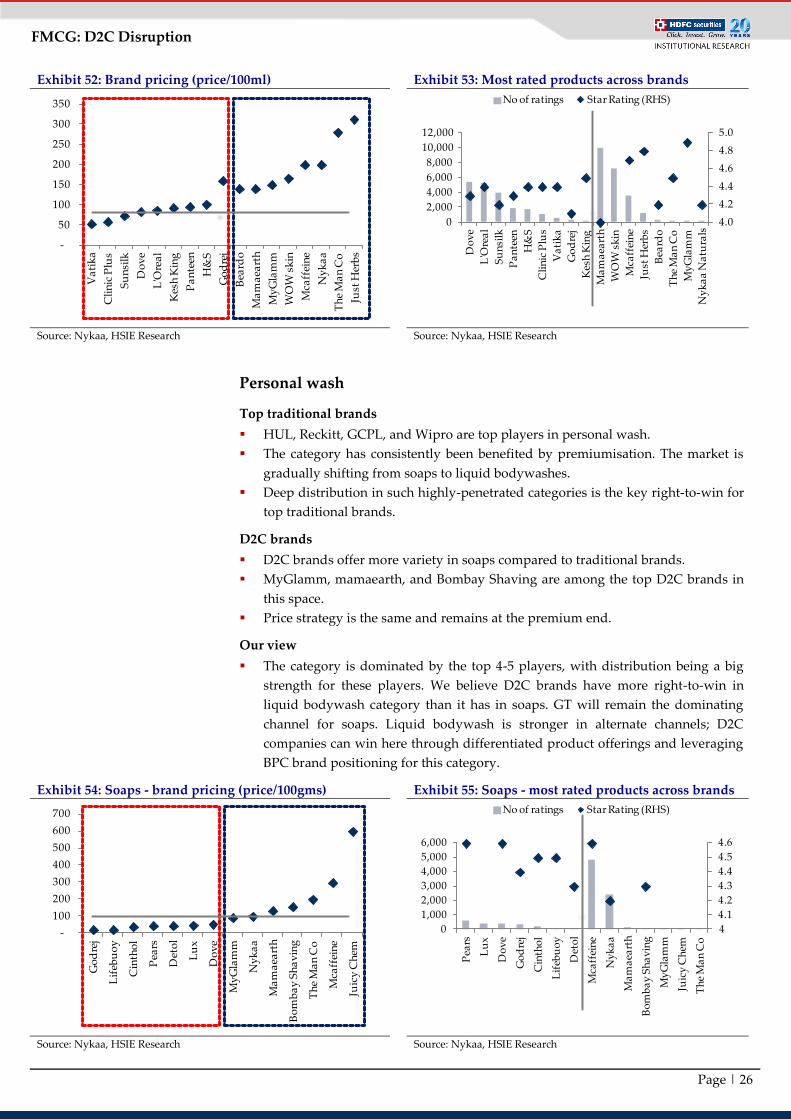

e

Rev

lon

Bo

bb

i Bro

wn

M.A

.C

Ny

ka

a

Ka

y

My

Gla

mm

Su

ga

r

4

4.1

4.2

4.3

4.4

4.5

4.6

0

10,000

20,000

30,000

40,000

50,000

60,000

M.A

.C

Ma

yb

elli

ne

La

km

e

Bo

bb

i Bro

wn

Rev

lon

L'O

rea

l

Ka

y

Ny

ka

a

My

Gla

mm

Su

ga

r

No of ratings Star Rating (RHS)

Page | 24

FMCG: D2C Disruption

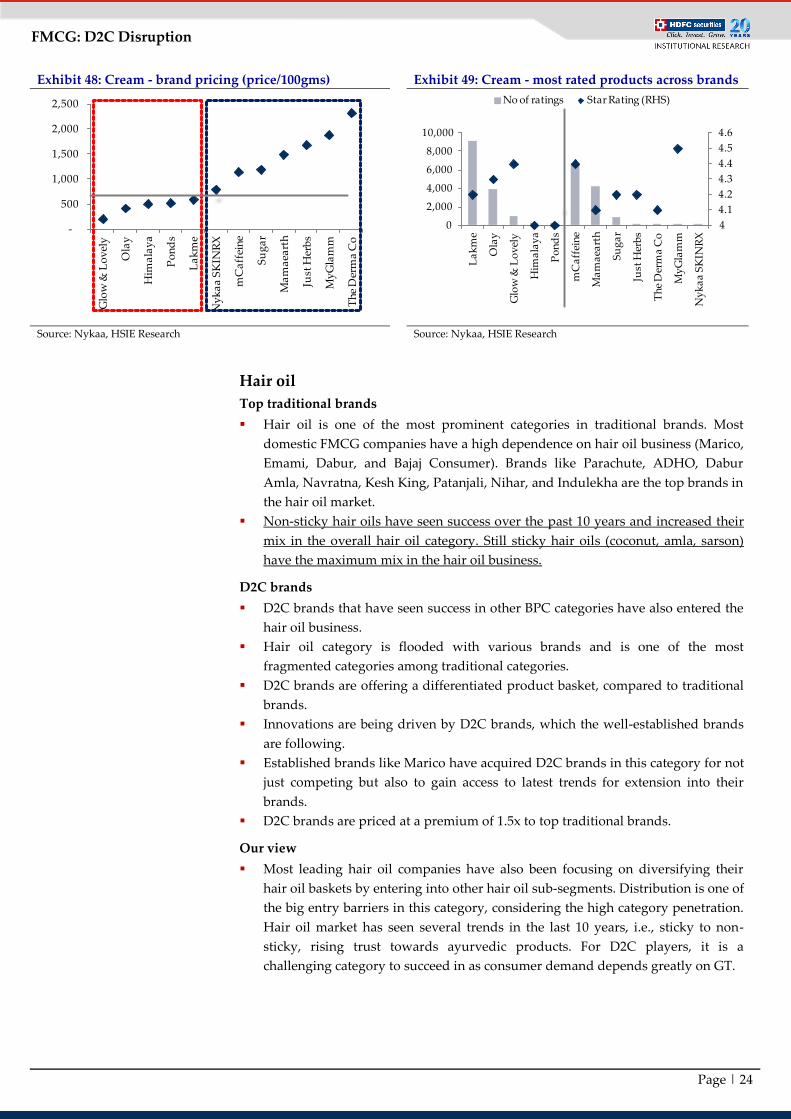

Exhibit 48: Cream - brand pricing (price/100gms) Exhibit 49: Cream - most rated products across brands

Source: Nykaa, HSIE Research Source: Nykaa, HSIE Research

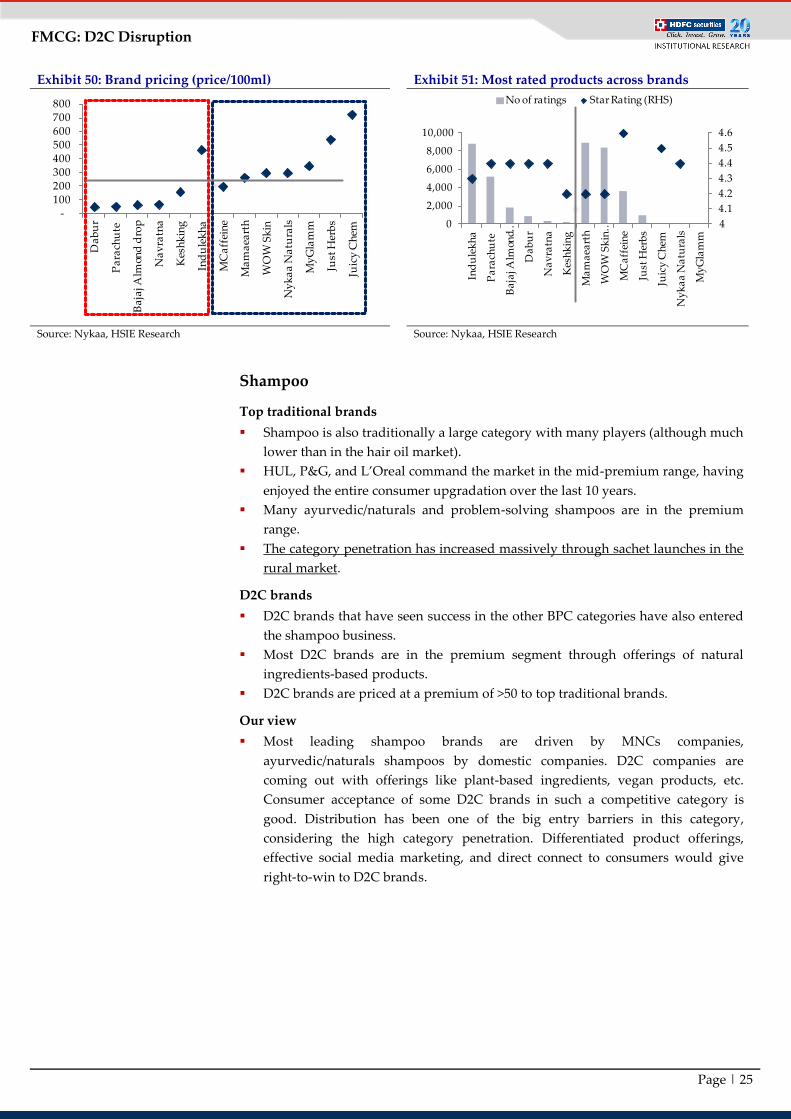

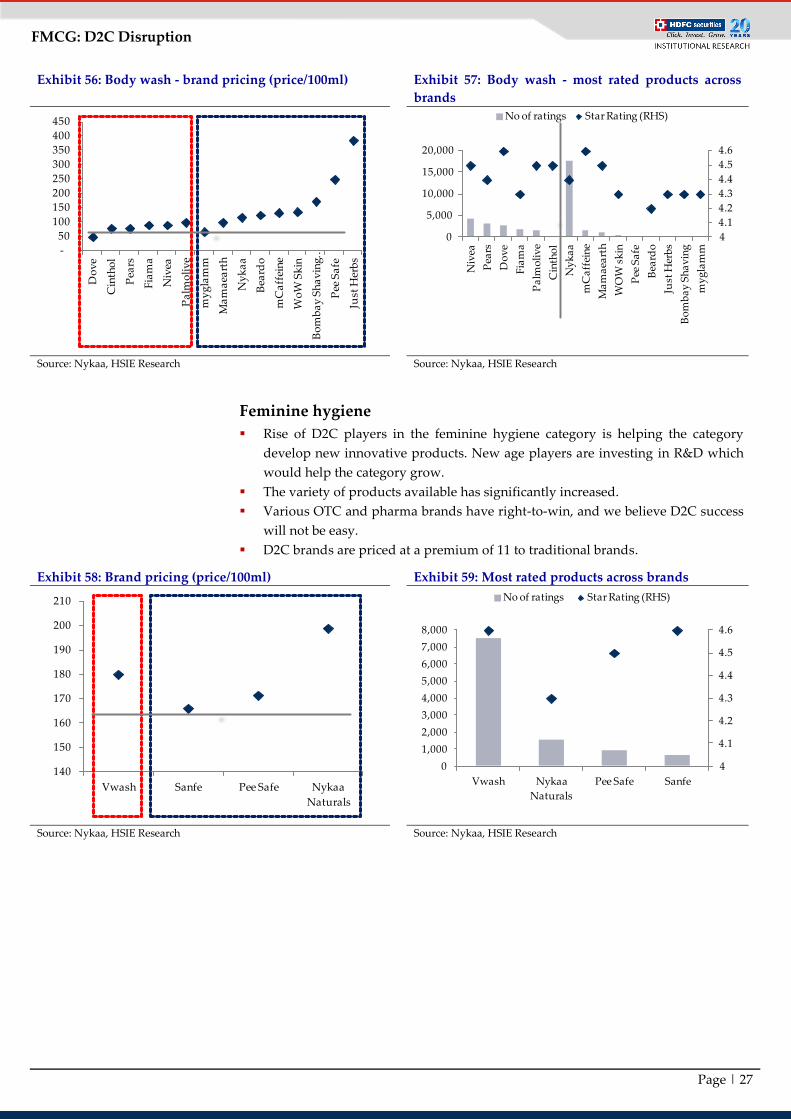

Hair oil

Top traditional brands