October 2021 Edelweiss Securities Limited Sector Report BFSI Fintech Fortunes-BNPL: Credit where it's due f cus Prakhar Agarwal +91 22 6620 3076 Prakhar.Agarwal@edelweissfin.com Santanu Chakrabarti +91 22 4342 8680 Santanu.Chakrabarti@edelweissfin.com Parth Sanghvi Parth.Sanghvi@edelweissfin.com Vinayak Agarwal +91 22 6620 3020 Vinayak.Agarwal@edelweissfin.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

October 2021

Edelweiss Securities Limited

Sector Report

BFSI

Fintech Fortunes-BNPL: Credit where it's due

fcus

Prakhar Agarwal+91 22 6620 [email protected]

Santanu Chakrabarti+91 22 4342 [email protected]

Parth Sanghvi

Vinayak Agarwal+91 22 6620 [email protected]

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset Edelweiss Securities Limited

BFSI

BNPL: Credit where it’s due

Buy Now Pay Later (BNPL) is making a splash as the hottest financial segment in India’s consumer-driven market. To be sure, BNPL adds a new dimension to traditional credit. At the same time, hyperbole is evident. We bring in a reality check.

A consumer’s delight, BNPL has been adopted rather quickly across the ecosystem—marketplaces (Amazon, Flipkart, etc), fintechs (PayTM, Mobikwik among 30-plus firms) and lenders (HDFC, ICICI, etc).

Here’s the deal: our global/domestic analysis reveals: i) BNPL is set to log a 45%-plus CAGR, snowballing into USD15bn by 2024 and forming 9% of e-commerce payments. ii) It targets the largest addressable market (mid-income), but India is fraught with unknowns and idiosyncrasies. Growth trajectory, while probable, is thus not given. iii) International precedents show partnerships and M&A define the

space—Square buying Afterpay, PayPal buying Paidy, and Amazon, Walmart and Apple jumping onto the BNPL bandwagon (global TAM USD22tn). iv) Overhang on credit cards is more rhetoric than reality, particularly for SBI Cards (refer to Calling Card).

We argue BNPL is not a slice but a loaf: there’s enough. Biggest banks are already digging in, and substantial investments in fintechs (20-plus players) testify to the opportunity at hand. Indeed, fintechs are the first movers, but banks have been agile to jump in, and we expect NBFCs to begin to feel the heat sooner rather than later. Far-fetched though, a credit layer atop UPI could be a game changer. That said, regulatory and customer debt management risks are key variables.

Adding new dimension to retail credit—a USD15bn opportunity

BNPL is making promising progress (USD3–3.5bn disbursals in FY21), and is touted

as a secular trend and not just a flash in the pan. Underlying vectors comprising i)

largest addressable market (huge mid-income, demographic dividend etc), ii)

proliferation of e-commerce, with expected consumer internet market of USD00bn

by FY26 (~USD90bn, 27% CAGR), iii) changing financial behaviour–consumption

oriented mindset; and iv) lower retail credit penetration form a perfect cocktail

driving uptake of BNPLs. We see BNPL solutions clocking >45% CAGR, thereby

forming 9% of e-commerce and 1.3% of payments (from sub-40bps in FY21).

Business model: Evolving; profitability build-up still sometime away

There are many evolving variants of BNPL offerings; the two basic ones prevalent in

India are: i) deferred payments; and ii) shopping EMI loans. Revenue levers for BNPL

providers are: i) take rates from merchants (depending on GMV, ranging from 2–6%);

or ii) fee from customers (late fee, monthly fee, interest rates, subscription fee, etc).

In terms of costs, customer acquisition cost is critical. While impairment cost is

uncertain given the lower ticket size, faster churn and higher fee income

dependence, the cross-cyclical impact is relatively low. Our analysis suggests that

high acquisition cost makes it more of a scale game (fee income forms a larger

chunk) and hence building up profitability can be time-consuming.

BFSI

Edelweiss Securities Limited

2 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Globally successful but Indian idiosyncrasies warrant higher scrutiny

Internationally, BNPLs are heating up with Square buying out Afterpay in a USD29bn

deal and PayPal buying Paidy for USD2.7bn, thereby creating a buzz that Affirm,

Klarna, Sezzle, and Zip could be next in line. Moreover, Amazon, Walmart and Apple

are all looking to jump onto the bandwagon and creating a halo around BNPL.

India has seen quick adoption across the ecosystem – marketplaces (Amazon,

Flipkart, etc), fintechs (20-plus players) and lenders (HDFC, ICICI, etc). That said, we

see a key difference in Indian context: i) the basic working model is different – sales

facilitator versus payment options; ii) challenges in acquisition and merchant

monetisation; and iii) a very nascent market positions India differently. And thus

expect BNPL’s touted growth trajectory to be fraught with unknowns.

Bank versus Fintech: Partnership and M&A to define the space

Slow to warm up to the idea, banks have now started embracing BNPL offerings

either via modified product offerings (own-in house product offerings) or through

partnership models (viz., via white-label BNPL players).

A quick comparison of the pioneer BNPL offerings and traditional banking products

shows the difference is likely to narrow as BNPL playesr try to eventually morph into

retail banking (internationally, this has begun with Klarna), whereas banks would try

to leverage their lower capital cost to wade through challengers.

We argue there is enough to partake for each type of player: biggest bank already

foraying into it, substantial investment in fintech plays (20-plus) is an

acknowledgment of the sizeable opportunity, not to mention that payment

platforms are valued even higher than some of the biggest banks.

While we expect fintechs to leverage their first-mover advantage, banks have been

quick to spot and appreciate the opportunity. NBFCs meanwhile are likely to get

challenged much more.

Credit cards cannibalisation is hard to crystalise; overhang rhetorical

We believe that cannibalisation is hard to crystalise given the inherent difference in

customer segment, product offerings, wider usage and stage of evolution. In fact

BNPL products can expand market for credit cards given its potential to widen

addressable market as customers graduate.

Moreover, we have seen credit cards companies evolving into similar product

offerings—trends already apparent in mature markets. Evolving partnership with

while-label fintechs, viz., Pine Labs will ensure – in our view – that market expands.

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 3

Key risks: Not all sunshine and rainbow

Two of the biggest challenges that we believe would play out for BNPL players are

regulation and controlling customer debt.

Potential customer base, product offerings and high growth with widening

unnoticed debt burden form a perfect cocktail for regulatory intervention over

period of time. Internationally, regulators have started taking note.

Looking at the target base of younger population and mass market appeal, the high

growth with lack of aggregated view of all pending BNPL payments at different BNPL

players will essentially pull regulatory attention.

A survey (by RBA) suggests 20% of consumers went without essentials (e.g. meals)

given potential overleveraging (more prevalent among consumers with multiple

BNPL offerings). It is indicative of dire consequences of over-indebtedness arising

out of BNPL offerings.

BFSI

Edelweiss Securities Limited

4 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

The Story in Charts

India consumer GTV is expected to grow >27%…

..propelling BNPL to a USD15bn market by 2024

Frenzy on perceivable benefit across ecosystem…

…but profitability build-up is actually far off

Global experience, local wisdom: the real deal is…

…valuation aspiration (payment > banks seen)

Source: Company, Edelweiss Research, RBI, NPCI

90+

125+

300+

0

70

140

210

280

350

FY21 FY22E FY26E

(USD

bn

)

India consumer Internet GTV - Overall market

3

15

0.0

3.6

7.2

10.8

14.4

18.0

2020 2024(

USD

bn

)

Customer Instant Credit

Cheap Credit

Soft CIBIL score

Merchant Higher AOVHIgher

conversionHigher

retention

Lenders Better reach

Higher cross sell

Higher profitability

2-6%

+/-5%

1-2%

1-5%

2-6%

0

2

4

6

8

10

Merchantfees

Late fees Impairmentcost

other(CAC/Tech

etc)

Net

(%)

0

1

3

4

5

7

Jun-19

Jun-20

Jun-21

CY19 CY20 Jun-19

Jun-20

Jun-21

AfterPay (AUD mn) Klarna (SEK mn) Affirm (USD mn)

Loss

% o

f G

MV

480

380

293

120

475

327

120

46 34 29

0

120

240

360

480

600

Vis

a

MC

Pay

Pal

Am

ex

JP M

org

an

Bo

FA GS

Kla

rna

Aff

irm

Aft

erP

ay

MC

ap U

SD b

n

Critical to contain and thus need investments

Reflects the need for scale & frequency

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 5

Adding new dimension to retail credit

Rapidly evolving payment ecosystem and financing behaviour are adding new

dimensions to traditional credit. Convergence of evolving technology and innovative

businesses has metamorphosed the unsecured consumer credit landscape in India,

with fintechs acting as a fulcrum. Given several catalysts and perceivable benefits

across the value chain, there has been strong proliferation of one such alternative

payment method dubbed as Buy Now- Pay-Later (BNPL).

Underlying drivers intact to drive growth if managed well

BNPL is making promising progress (USD3–3.5bn disbursals in FY21), and is touted

as a secular trend and not just another flash in the pan. Underlying vectors

comprising i) growth of e-commerce, with expected consumer internet market of

USD300bn by FY26 (~USD90bn, 27% CAGR), ii) changing financial behaviour, and

iii) lower retail credit penetration are the ingredients of the cocktail driving BNPLs.

And it essentially reflects the step change in consumers’ mindset—from being

savings-focused to consumption. Consumer lending from banks/NBFCs across use

cases was estimated to be ~USD267bn in FY17; it ballooned to USD437bn by FY20.

Growing consumption behaviour, particularly among millennials and Gen-Z, will

further expand the need for credit.

Accordingly, tech-based credit solutions will be better placed to target this credit

need than traditional credit institutions, especially considering pervasive adoption

of smartphones and mobile payments among such consumers.

Riding digital penetration and…

Source: Company, SEBI

…>27% potential growth in India’s consumer GTV…

Source: Company, SEBI

…imply target categories are poised for rapid growth…

(USD bn) FY21 FY26E CAGR

Online retail 41 140-160 28-31%

Online travel 9-11 35-40 30%

e-Grocery 3.7 22-27 43-49%

Food delivery 2.7-3 13-14 30%

E-Health 1.5 12-16 50-60%

Source: Company, SEBI

650-70049% 500-550

38%

250-30020%

950-100068% 800-850

48% 700-75050% +

0

250

500

750

1000

1250

Access tointernet

Smart phoneusers

Onlinetransactors

(mn

)

2020 2025E

90+

125+

300+

0

70

140

210

280

350

FY21 FY22E FY26E

(USD

bn

)

India consumer Internet GTV - Overall market

BFSI

Edelweiss Securities Limited

6 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

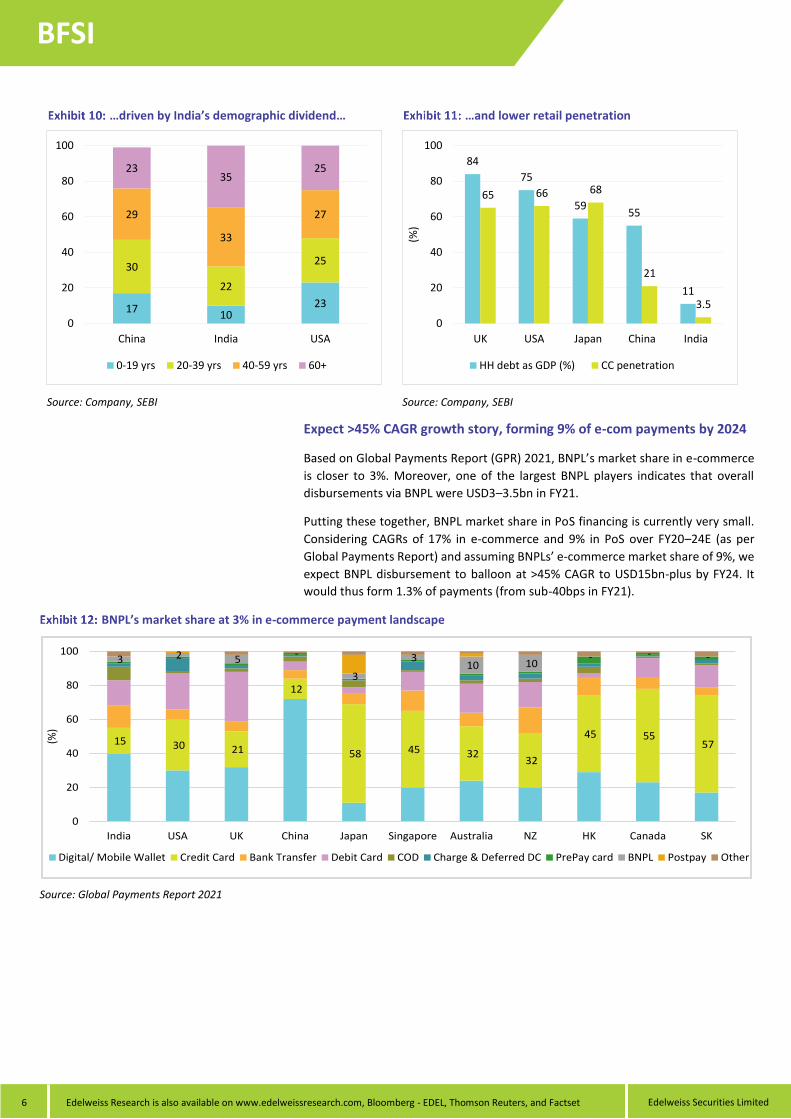

…driven by India’s demographic dividend…

Source: Company, SEBI

…and lower retail penetration

Source: Company, SEBI

Expect >45% CAGR growth story, forming 9% of e-com payments by 2024

Based on Global Payments Report (GPR) 2021, BNPL’s market share in e-commerce

is closer to 3%. Moreover, one of the largest BNPL players indicates that overall

disbursements via BNPL were USD3–3.5bn in FY21.

Putting these together, BNPL market share in PoS financing is currently very small.

Considering CAGRs of 17% in e-commerce and 9% in PoS over FY20–24E (as per

Global Payments Report) and assuming BNPLs’ e-commerce market share of 9%, we

expect BNPL disbursement to balloon at >45% CAGR to USD15bn-plus by FY24. It

would thus form 1.3% of payments (from sub-40bps in FY21).

BNPL’s market share at 3% in e-commerce payment landscape

Source: Global Payments Report 2021

1710

23

30

22

25

29

33

27

2335

25

0

20

40

60

80

100

China India USA

0-19 yrs 20-39 yrs 40-59 yrs 60+

84

75

5955

11

65 66 68

21

3.5

0

20

40

60

80

100

UK USA Japan China India

(%)

HH debt as GDP (%) CC penetration

15 30 21

12

58 45 32 32

45 55 57

3 2 5 -

3

3 10 10

- - -

0

20

40

60

80

100

India USA UK China Japan Singapore Australia NZ HK Canada SK

(%)

Digital/ Mobile Wallet Credit Card Bank Transfer Debit Card COD Charge & Deferred DC PrePay card BNPL Postpay Other

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 7

BNPL to grow at > 45% CAGR into USD15bn disbursements by 2024

USD bn FY20 FY24E CAGR (%)

eCom turnover 60 111 16.6

POS 737 1035 8.9

Total 797 1146 9.5

BNPL – Ecom 1.8 10.0 53.5

BNPL - POS 1.2 4.3 38.6

BNPL - Total 3 14 48.1

BNPL – Ecom. - Mkt shr. (%) 3 9

BNPL - Total - Mkt shr. (%) 0.4 1.3

Source: GPR, Edelweiss Research

Perceivable value across the value chain

Looking at the product characteristics, BNPL variants seems to be a win-win for all

stakeholders with creation across value. This is one of the main reasons for the

product’s speedy uptake.

Benefits for customers

Source: Edelweiss Research

Benefits for merchants

Source: Edelweiss Research

Benefits for lenders

Source: Edelweiss Research

Chaep credit -No fee, No

interest

Soft credit score

Instant Credit

HIgher Average Order Value

Higher Retention

Higher Conversion

Improved profitability

and valuations

Higher cross sell potential

Wider market

BFSI

Edelweiss Securities Limited

8 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

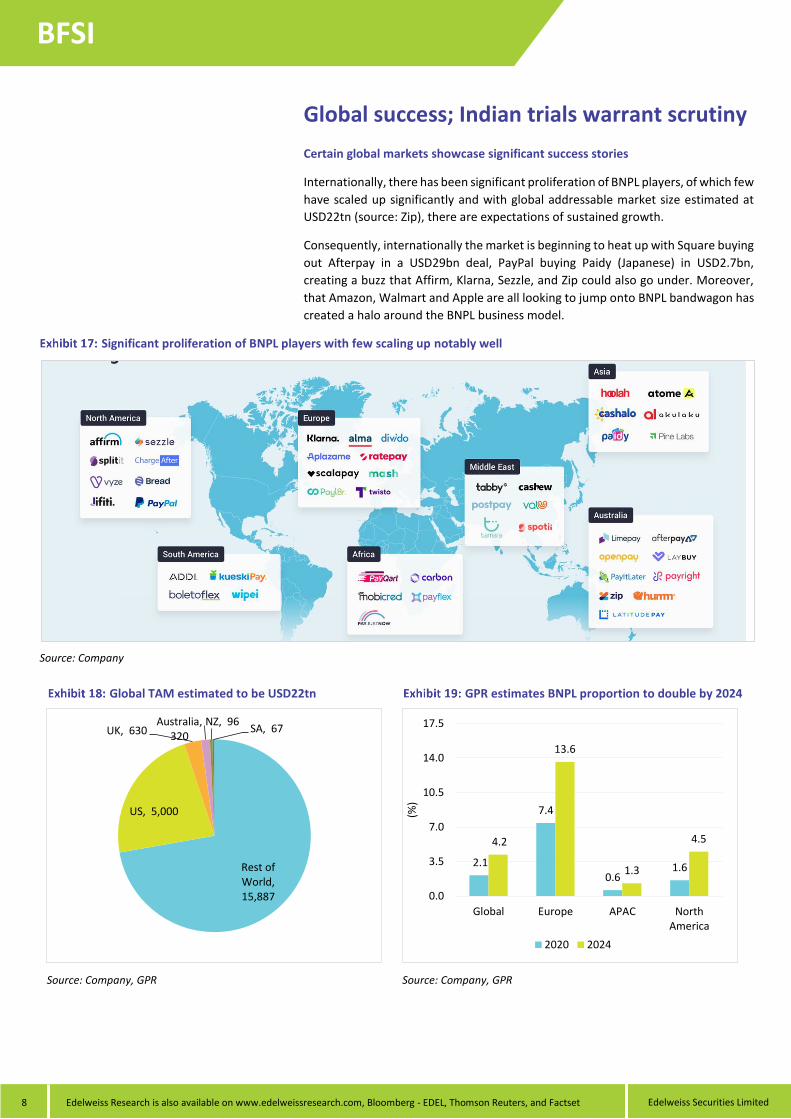

Global success; Indian trials warrant scrutiny

Certain global markets showcase significant success stories

Internationally, there has been significant proliferation of BNPL players, of which few

have scaled up significantly and with global addressable market size estimated at

USD22tn (source: Zip), there are expectations of sustained growth.

Consequently, internationally the market is beginning to heat up with Square buying

out Afterpay in a USD29bn deal, PayPal buying Paidy (Japanese) in USD2.7bn,

creating a buzz that Affirm, Klarna, Sezzle, and Zip could also go under. Moreover,

that Amazon, Walmart and Apple are all looking to jump onto BNPL bandwagon has

created a halo around the BNPL business model.

Significant proliferation of BNPL players with few scaling up notably well

Source: Company

Global TAM estimated to be USD22tn

Source: Company, GPR

GPR estimates BNPL proportion to double by 2024

Source: Company, GPR

Rest of World, 15,887

US, 5,000

UK, 630 Australia,

320 NZ, 96

SA, 67

2.1

7.4

0.61.6

4.2

13.6

1.3

4.5

0.0

3.5

7.0

10.5

14.0

17.5

Global Europe APAC NorthAmerica

(%)

2020 2024

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 9

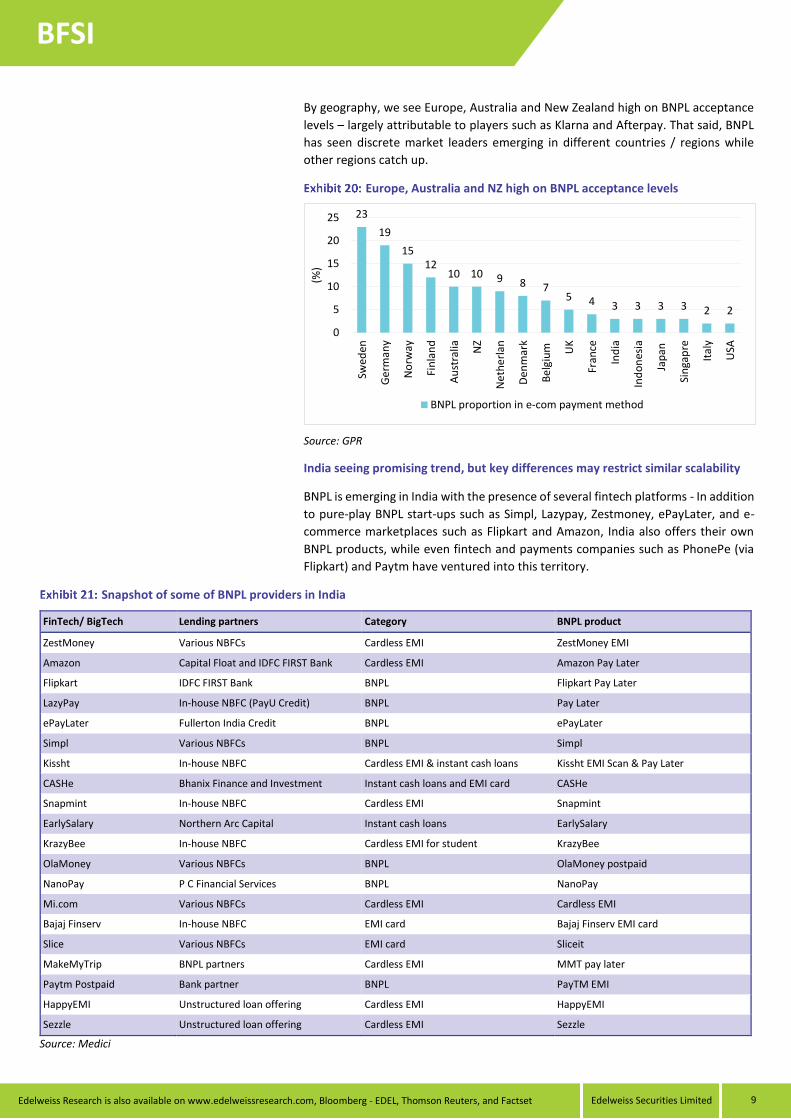

By geography, we see Europe, Australia and New Zealand high on BNPL acceptance

levels – largely attributable to players such as Klarna and Afterpay. That said, BNPL

has seen discrete market leaders emerging in different countries / regions while

other regions catch up.

Europe, Australia and NZ high on BNPL acceptance levels

Source: GPR

India seeing promising trend, but key differences may restrict similar scalability

BNPL is emerging in India with the presence of several fintech platforms - In addition

to pure-play BNPL start-ups such as Simpl, Lazypay, Zestmoney, ePayLater, and e-

commerce marketplaces such as Flipkart and Amazon, India also offers their own

BNPL products, while even fintech and payments companies such as PhonePe (via

Flipkart) and Paytm have ventured into this territory.

Snapshot of some of BNPL providers in India

FinTech/ BigTech Lending partners Category BNPL product

ZestMoney Various NBFCs Cardless EMI ZestMoney EMI

Amazon Capital Float and IDFC FIRST Bank Cardless EMI Amazon Pay Later

Flipkart IDFC FIRST Bank BNPL Flipkart Pay Later

LazyPay In-house NBFC (PayU Credit) BNPL Pay Later

ePayLater Fullerton India Credit BNPL ePayLater

Simpl Various NBFCs BNPL Simpl

Kissht In-house NBFC Cardless EMI & instant cash loans Kissht EMI Scan & Pay Later

CASHe Bhanix Finance and Investment Instant cash loans and EMI card CASHe

Snapmint In-house NBFC Cardless EMI Snapmint

EarlySalary Northern Arc Capital Instant cash loans EarlySalary

KrazyBee In-house NBFC Cardless EMI for student KrazyBee

OlaMoney Various NBFCs BNPL OlaMoney postpaid

NanoPay P C Financial Services BNPL NanoPay

Mi.com Various NBFCs Cardless EMI Cardless EMI

Bajaj Finserv In-house NBFC EMI card Bajaj Finserv EMI card

Slice Various NBFCs EMI card Sliceit

MakeMyTrip BNPL partners Cardless EMI MMT pay later

Paytm Postpaid Bank partner BNPL PayTM EMI

HappyEMI Unstructured loan offering Cardless EMI HappyEMI

Sezzle Unstructured loan offering Cardless EMI Sezzle

Source: Medici

23

19

1512

10 10 9 8 75 4 3 3 3 3 2 2

0

5

10

15

20

25

Swed

en

Ge

rman

y

No

rway

Fin

lan

d

Au

stra

lia NZ

Ne

the

rlan

Den

mar

k

Bel

giu

m UK

Fran

ce

Ind

ia

Ind

on

esia

Jap

an

Sin

gap

re

Ital

y

USA

(%)

BNPL proportion in e-com payment method

BFSI

Edelweiss Securities Limited

10 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

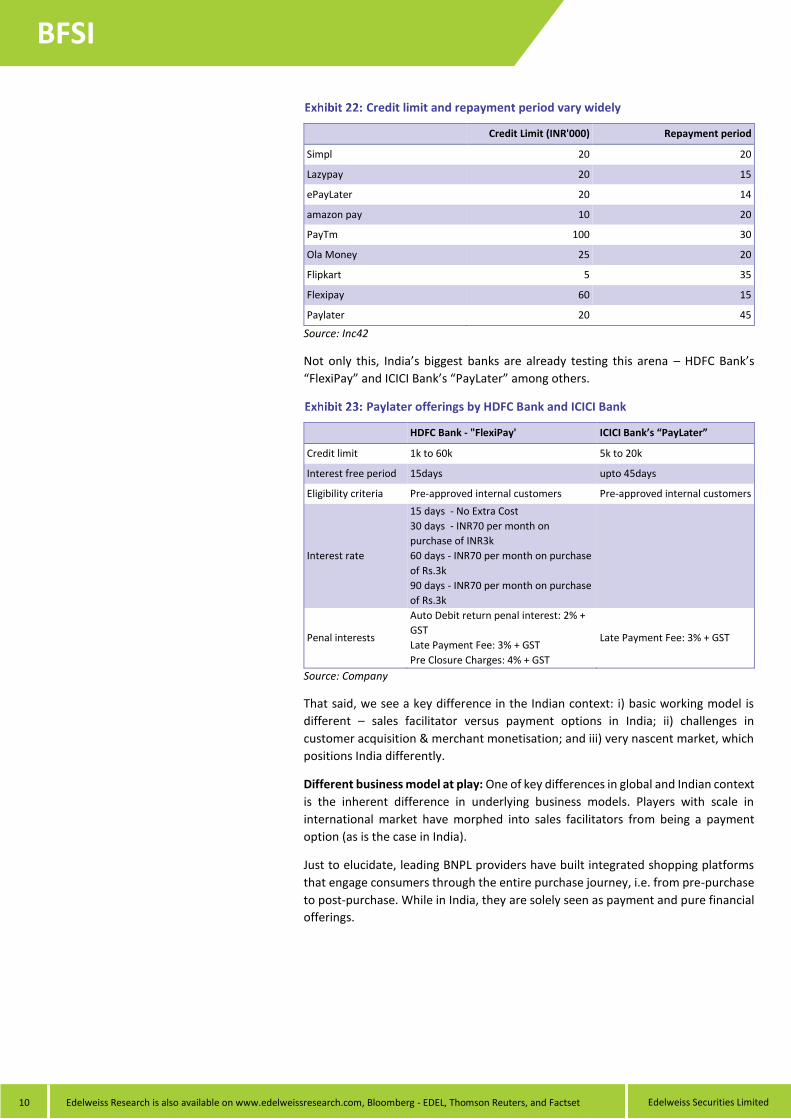

Credit limit and repayment period vary widely

Credit Limit (INR'000) Repayment period

Simpl 20 20

Lazypay 20 15

ePayLater 20 14

amazon pay 10 20

PayTm 100 30

Ola Money 25 20

Flipkart 5 35

Flexipay 60 15

Paylater 20 45

Source: Inc42

Not only this, India’s biggest banks are already testing this arena – HDFC Bank’s

“FlexiPay” and ICICI Bank’s “PayLater” among others.

Paylater offerings by HDFC Bank and ICICI Bank

HDFC Bank - "FlexiPay' ICICI Bank’s “PayLater”

Credit limit 1k to 60k 5k to 20k

Interest free period 15days upto 45days

Eligibility criteria Pre-approved internal customers Pre-approved internal customers

Interest rate

15 days - No Extra Cost

30 days - INR70 per month on

purchase of INR3k

60 days - INR70 per month on purchase

of Rs.3k

90 days - INR70 per month on purchase

of Rs.3k

Penal interests

Auto Debit return penal interest: 2% +

GST

Late Payment Fee: 3% + GST

Pre Closure Charges: 4% + GST

Late Payment Fee: 3% + GST

Source: Company

That said, we see a key difference in the Indian context: i) basic working model is

different – sales facilitator versus payment options in India; ii) challenges in

customer acquisition & merchant monetisation; and iii) very nascent market, which

positions India differently.

Different business model at play: One of key differences in global and Indian context

is the inherent difference in underlying business models. Players with scale in

international market have morphed into sales facilitators from being a payment

option (as is the case in India).

Just to elucidate, leading BNPL providers have built integrated shopping platforms

that engage consumers through the entire purchase journey, i.e. from pre-purchase

to post-purchase. While in India, they are solely seen as payment and pure financial

offerings.

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 11

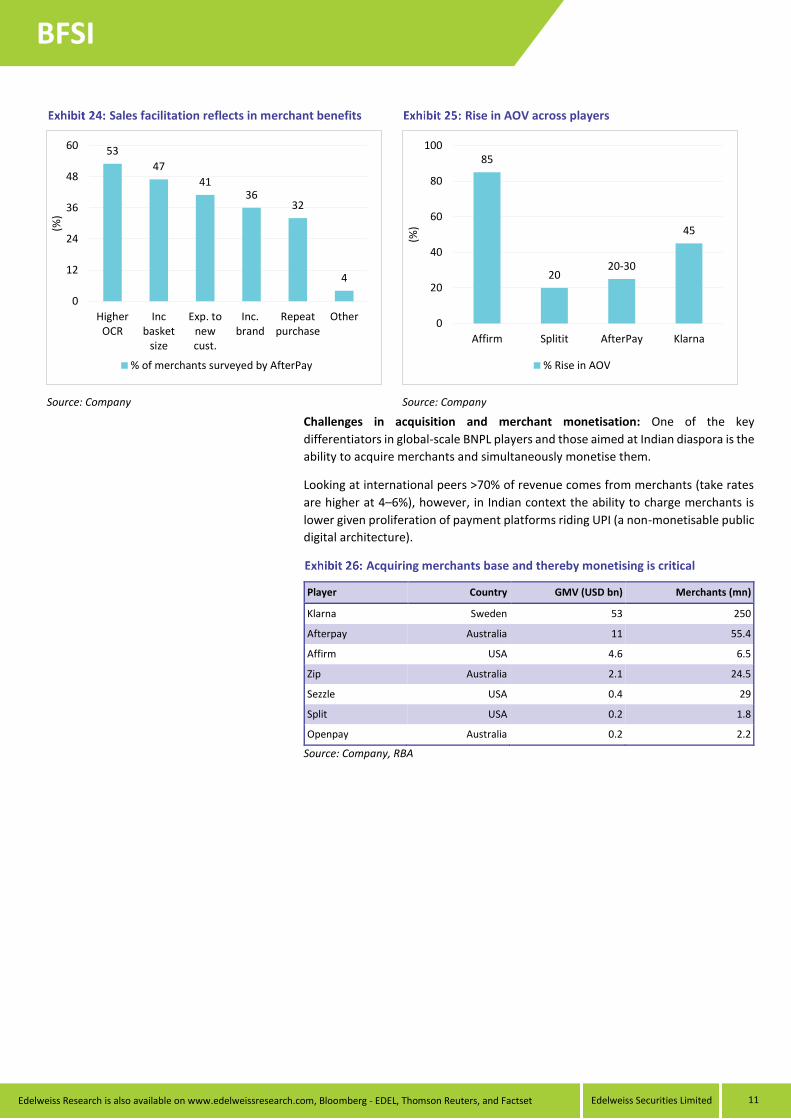

Sales facilitation reflects in merchant benefits

Source: Company

Rise in AOV across players

Source: Company

Challenges in acquisition and merchant monetisation: One of the key

differentiators in global-scale BNPL players and those aimed at Indian diaspora is the

ability to acquire merchants and simultaneously monetise them.

Looking at international peers >70% of revenue comes from merchants (take rates

are higher at 4–6%), however, in Indian context the ability to charge merchants is

lower given proliferation of payment platforms riding UPI (a non-monetisable public

digital architecture).

Acquiring merchants base and thereby monetising is critical

Player Country GMV (USD bn) Merchants (mn)

Klarna Sweden 53 250

Afterpay Australia 11 55.4

Affirm USA 4.6 6.5

Zip Australia 2.1 24.5

Sezzle USA 0.4 29

Split USA 0.2 1.8

Openpay Australia 0.2 2.2

Source: Company, RBA

53

47

4136

32

4

0

12

24

36

48

60

HigherOCR

Incbasket

size

Exp. tonewcust.

Inc.brand

Repeatpurchase

Other

(%)

% of merchants surveyed by AfterPay

85

2020-30

45

0

20

40

60

80

100

Affirm Splitit AfterPay Klarna

(%)

% Rise in AOV

BFSI

Edelweiss Securities Limited

12 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

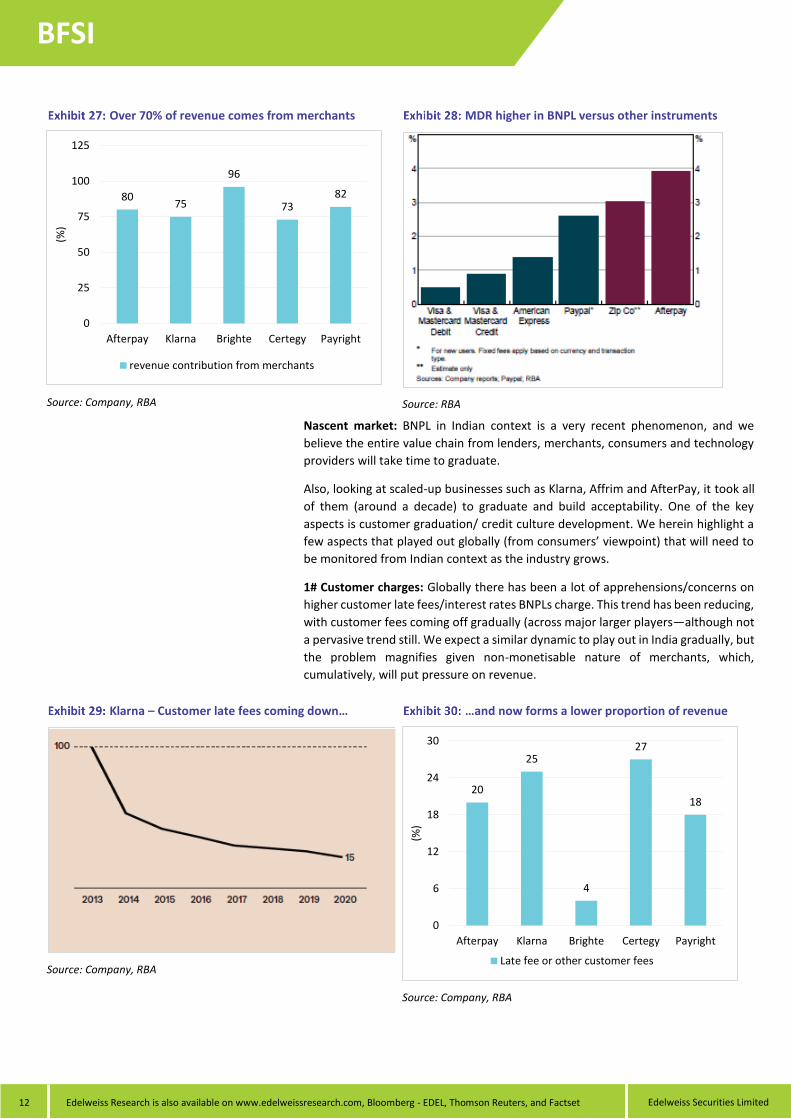

Over 70% of revenue comes from merchants

Source: Company, RBA

MDR higher in BNPL versus other instruments

Source: RBA

Nascent market: BNPL in Indian context is a very recent phenomenon, and we

believe the entire value chain from lenders, merchants, consumers and technology

providers will take time to graduate.

Also, looking at scaled-up businesses such as Klarna, Affrim and AfterPay, it took all

of them (around a decade) to graduate and build acceptability. One of the key

aspects is customer graduation/ credit culture development. We herein highlight a

few aspects that played out globally (from consumers’ viewpoint) that will need to

be monitored from Indian context as the industry grows.

1# Customer charges: Globally there has been a lot of apprehensions/concerns on

higher customer late fees/interest rates BNPLs charge. This trend has been reducing,

with customer fees coming off gradually (across major larger players—although not

a pervasive trend still. We expect a similar dynamic to play out in India gradually, but

the problem magnifies given non-monetisable nature of merchants, which,

cumulatively, will put pressure on revenue.

Klarna – Customer late fees coming down…

Source: Company, RBA

…and now forms a lower proportion of revenue

Source: Company, RBA

8075

96

7382

0

25

50

75

100

125

Afterpay Klarna Brighte Certegy Payright

(%)

revenue contribution from merchants

20

25

4

27

18

0

6

12

18

24

30

Afterpay Klarna Brighte Certegy Payright

(%)

Late fee or other customer fees

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 13

2# Younger age to have higher cost given missed payments: In one of the surveys

by RBA, 21% of BNPL customers missed payments in FY19. In fact, most completed

transactions were made by consumers under the age of 35, and for completed

transactions that had missed payment fees, the same age cohort accounted for 67%

of these transactions.

All of this implies that missed payment is more prevalent in younger population and

thus will have a higher cost attached to them.

Younger population tends to miss payments more often

Source: RBA

3# Over-indebtedness leading to financial difficulties: One of the critical aspects

that needs to be managed well is over-indebtedness caused by BNPLs. A survey

conducted by RBA) suggests: i) 20% of consumers cut back on or went without

essentials (e.g. meals); and ii) 15% said they had taken out an additional loan. These

trends (more prevalent among consumers using multiple BNPL offerings) indicates

dire consequences of over-indebtedness arising out of BNPL offerings.

This over-indebtedness also seemingly pulls along other credit options—a similar

survey finds that a consistently higher proportion of BNPL credit card users incurred

interest charges on their credit cards (between 66% and 73%). While, in the same

period, only 42% to 46% of other credit card users incurred an interest charge on

their credit card.

23 27

3840

2220

12 1041

0%

20%

40%

60%

80%

100%

All completed transactions Completed transactions that incurredat least

one missed payment fee

18-24 25-34 35-44 45-54 55-64 65+

BFSI

Edelweiss Securities Limited

14 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

High charges for people that use credit cards for BNPLs over others

Source: RBA

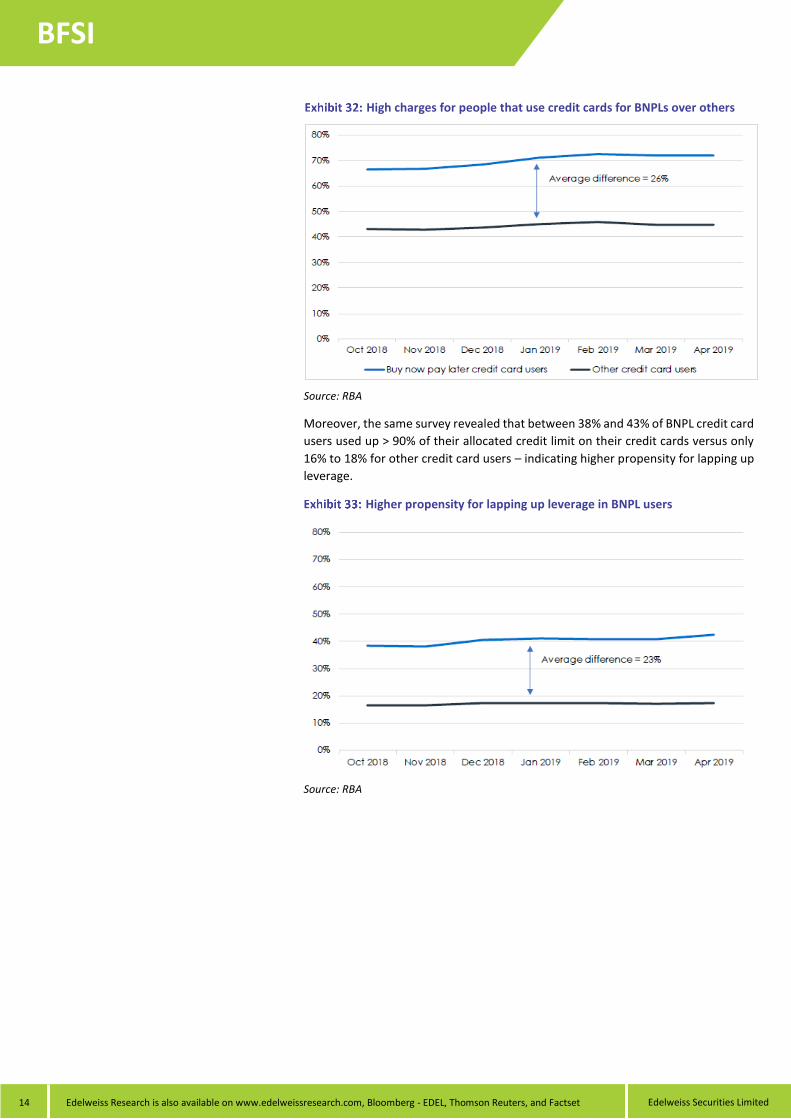

Moreover, the same survey revealed that between 38% and 43% of BNPL credit card

users used up > 90% of their allocated credit limit on their credit cards versus only

16% to 18% for other credit card users – indicating higher propensity for lapping up

leverage.

Higher propensity for lapping up leverage in BNPL users

Source: RBA

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 15

Business model: Still evolving

Buy Now Pay Later (BNPL) offerings are evolving. The two basic variants that are

prevalent in India are: i) deferred payments; and ii) shopping EMI loans.

Deferred payment models are adopted mostly in online transaction services such as e-commerce, food delivery, e-grocery, online ticketing and utility bill payments. Deferred payment models work like credit cards, offering a 15/30 day repayment period without any interest or charges while allowing customers to revolve by paying a fee.

Players in the shopping EMI loans model offer higher loan amounts with a longer repayment periods (3/6/12 months).

Stylised financial flows in a BNPL transaction

Source: Edelweiss research

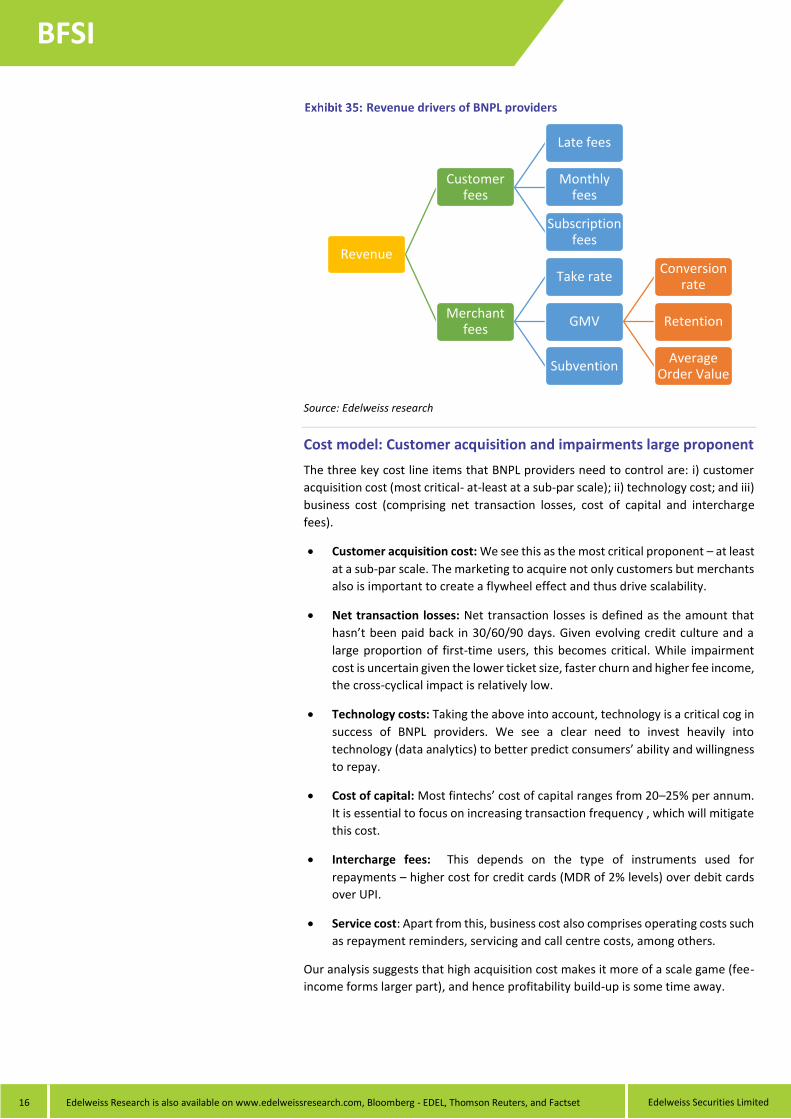

Revenue model – Largely contingent on fee income

The revenue model for BNPL is contingent on the business model, viz., customer-

centric (no charge to customers) or merchant-centric (bundled with other product

offerings). Consequently, revenue levers for BNPL providers are: i) merchant fees

take rates from merchants (depending on GMV, generally ranging from 2–6%) and

subvention income; or ii) fees from customers (late fee, monthly fee, interest rates,

subscription fee). The revenue model only works when the integration between the

customer and merchant exists, i.e flywheel effect does get created.

Card-issuing financial

Institution (“issuer”)

BNPL provider’s financial

Institution (“Acquirer”)

BNPL provider

Consumer Merchant

Interchange fee

Issuer & Acquirer settle

3 Installment payments

Goods/service

1. Upfront payment

2 BNPL merchant fee

Merchant service fee

BFSI

Edelweiss Securities Limited

16 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Revenue drivers of BNPL providers

Source: Edelweiss research

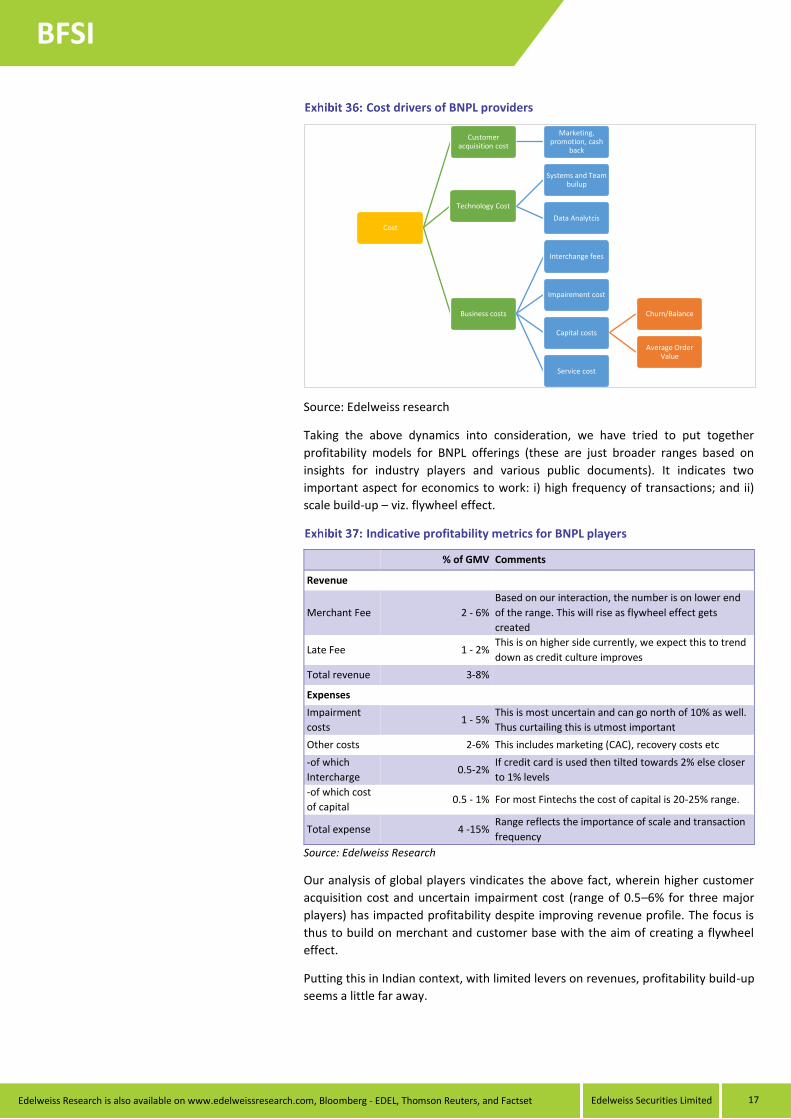

Cost model: Customer acquisition and impairments large proponent

The three key cost line items that BNPL providers need to control are: i) customer

acquisition cost (most critical- at-least at a sub-par scale); ii) technology cost; and iii)

business cost (comprising net transaction losses, cost of capital and intercharge

fees).

Customer acquisition cost: We see this as the most critical proponent – at least

at a sub-par scale. The marketing to acquire not only customers but merchants

also is important to create a flywheel effect and thus drive scalability.

Net transaction losses: Net transaction losses is defined as the amount that

hasn’t been paid back in 30/60/90 days. Given evolving credit culture and a

large proportion of first-time users, this becomes critical. While impairment

cost is uncertain given the lower ticket size, faster churn and higher fee income,

the cross-cyclical impact is relatively low.

Technology costs: Taking the above into account, technology is a critical cog in

success of BNPL providers. We see a clear need to invest heavily into

technology (data analytics) to better predict consumers’ ability and willingness

to repay.

Cost of capital: Most fintechs’ cost of capital ranges from 20–25% per annum.

It is essential to focus on increasing transaction frequency , which will mitigate

this cost.

Intercharge fees: This depends on the type of instruments used for

repayments – higher cost for credit cards (MDR of 2% levels) over debit cards

over UPI.

Service cost: Apart from this, business cost also comprises operating costs such

as repayment reminders, servicing and call centre costs, among others.

Our analysis suggests that high acquisition cost makes it more of a scale game (fee-

income forms larger part), and hence profitability build-up is some time away.

Revenue

Customer fees

Late fees

Monthly fees

Subscription fees

Merchant fees

Take rate

GMV

Conversion rate

Retention

Average Order Value

Subvention

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 17

Cost drivers of BNPL providers

Source: Edelweiss research

Taking the above dynamics into consideration, we have tried to put together

profitability models for BNPL offerings (these are just broader ranges based on

insights for industry players and various public documents). It indicates two

important aspect for economics to work: i) high frequency of transactions; and ii)

scale build-up – viz. flywheel effect.

Indicative profitability metrics for BNPL players

% of GMV Comments

Revenue

Merchant Fee 2 - 6%

Based on our interaction, the number is on lower end

of the range. This will rise as flywheel effect gets

created

Late Fee 1 - 2% This is on higher side currently, we expect this to trend

down as credit culture improves

Total revenue 3-8%

Expenses

Impairment

costs 1 - 5%

This is most uncertain and can go north of 10% as well.

Thus curtailing this is utmost important

Other costs 2-6% This includes marketing (CAC), recovery costs etc

-of which

Intercharge 0.5-2%

If credit card is used then tilted towards 2% else closer

to 1% levels

-of which cost

of capital 0.5 - 1% For most Fintechs the cost of capital is 20-25% range.

Total expense 4 -15% Range reflects the importance of scale and transaction

frequency

Source: Edelweiss Research

Our analysis of global players vindicates the above fact, wherein higher customer

acquisition cost and uncertain impairment cost (range of 0.5–6% for three major

players) has impacted profitability despite improving revenue profile. The focus is

thus to build on merchant and customer base with the aim of creating a flywheel

effect.

Putting this in Indian context, with limited levers on revenues, profitability build-up

seems a little far away.

Cost

Customer acquisition cost

Marketing, promotion, cash

back

Technology Cost

Systems and Team builup

Data Analytcis

Business costs

Interchange fees

Impairement cost

Capital costs

Churn/Balance

Average Order Value

Service cost

BFSI

Edelweiss Securities Limited

18 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

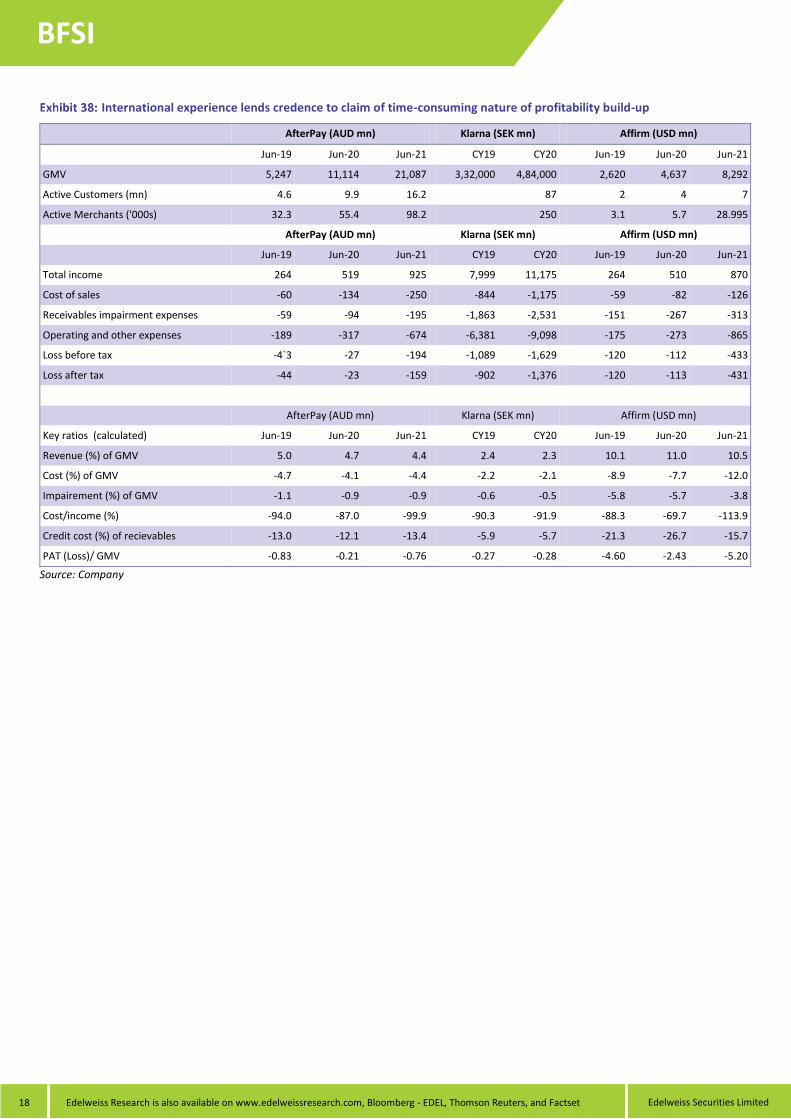

International experience lends credence to claim of time-consuming nature of profitability build-up

AfterPay (AUD mn) Klarna (SEK mn) Affirm (USD mn)

Jun-19 Jun-20 Jun-21 CY19 CY20 Jun-19 Jun-20 Jun-21

GMV 5,247 11,114 21,087 3,32,000 4,84,000 2,620 4,637 8,292

Active Customers (mn) 4.6 9.9 16.2 87 2 4 7

Active Merchants ('000s) 32.3 55.4 98.2 250 3.1 5.7 28.995

AfterPay (AUD mn) Klarna (SEK mn) Affirm (USD mn)

Jun-19 Jun-20 Jun-21 CY19 CY20 Jun-19 Jun-20 Jun-21

Total income 264 519 925 7,999 11,175 264 510 870

Cost of sales -60 -134 -250 -844 -1,175 -59 -82 -126

Receivables impairment expenses -59 -94 -195 -1,863 -2,531 -151 -267 -313

Operating and other expenses -189 -317 -674 -6,381 -9,098 -175 -273 -865

Loss before tax -4`3 -27 -194 -1,089 -1,629 -120 -112 -433

Loss after tax -44 -23 -159 -902 -1,376 -120 -113 -431

AfterPay (AUD mn) Klarna (SEK mn) Affirm (USD mn)

Key ratios (calculated) Jun-19 Jun-20 Jun-21 CY19 CY20 Jun-19 Jun-20 Jun-21

Revenue (%) of GMV 5.0 4.7 4.4 2.4 2.3 10.1 11.0 10.5

Cost (%) of GMV -4.7 -4.1 -4.4 -2.2 -2.1 -8.9 -7.7 -12.0

Impairement (%) of GMV -1.1 -0.9 -0.9 -0.6 -0.5 -5.8 -5.7 -3.8

Cost/income (%) -94.0 -87.0 -99.9 -90.3 -91.9 -88.3 -69.7 -113.9

Credit cost (%) of recievables -13.0 -12.1 -13.4 -5.9 -5.7 -21.3 -26.7 -15.7

PAT (Loss)/ GMV -0.83 -0.21 -0.76 -0.27 -0.28 -4.60 -2.43 -5.20

Source: Company

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 19

BNPLs versus credit cards: Big hot debate

The sizzling growth of BNPL offerings is casting a shadow over credit cards, even their

potential cannibalisation.

We argue: i) total cannibalisation is hard to play by given the inherent difference in

customer segment, product offerings and wider usage; ii) in fact BNPL products can

expand the market for credit card players; iii) credit cards companies are getting into

similar product offerings – trends already seen in mature markets; iv) evolving

partnership with while-label fintech companies, viz., Pine Labs; v) penetration level

in India for credit card market is still lower, offering a steady growth runway despite

losing payments market share; and vi) regulatory challenges might emerge on BNPL

(which is clearly very loosely regulated versus credit cards, which has undergone a

large change in regulatory frameworks).

Nuances of BNPL and credit card offerings

BNPL Credit Cards

Product Offerings Option to split payments - Offers consumers a line of credit

Usage Specific one-time purchases Open line , used for bill pay, etc as well

Credit limit Much lower High, generally goes into multiples of earnings

Interest rate 0%, no processing fees 0%, with processing fees

Late fee Yes Yes

Late payment interest charges No Variable rates based on revolving balances

Fexibility Choose payment terms as per need,

cant digress from payment schedule then

Flexibility in payment schedule within grace period to avoid

late charges

Application Process Instant, generally for untested (new to

credit) customers

Takes time and stricter eligibility, generally with credit tested

customers

Acceptance Improving across merchants Has very high acceptance, even for services

Credit bureaus reporting Rare instances Gets reported

Perks Not much, low on perks Reward points which can be used

Merchant charges Variable, generally high viz. 2-6% Variable generally 1.5-2.5% range

Regulations Loosely bound Stricter regulation

Source: Edelweiss Research

Incumbent players’ new product offerings to capitalise on the trend

Company New product initiatives

American Express Card members can choose to create monthly payment plans with a fixed fee and no interest, carry a monthly balance

with interest or pay their bill in full

Chase My Chase Plan is available for purchases over USD100 and enables customers to select a recent transaction and

choose a repayment timeframe and personal monthly payment amount that can range from 3 to 18 months

Nab

NAB launched the NAB StraightUp Card, Australia’s first no-interest credit card. The StraightUp Card gives customers

access to credit of up to USD3k for a flat monthly charge, and customers don’t pay the monthly fee if the card is not

used and there are no other fees or charges

Royal Bank of Canada Royal Bank of Canada moves into BNPL market through partnership with Alliance Data’s Bread

Visa Kicks off BNPL pilots in the US to help its issuer clients give eligible consumers more flexibility to pay by using their

existing Visa credit cards at checkout

Source: FT partners

BFSI

Edelweiss Securities Limited

20 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

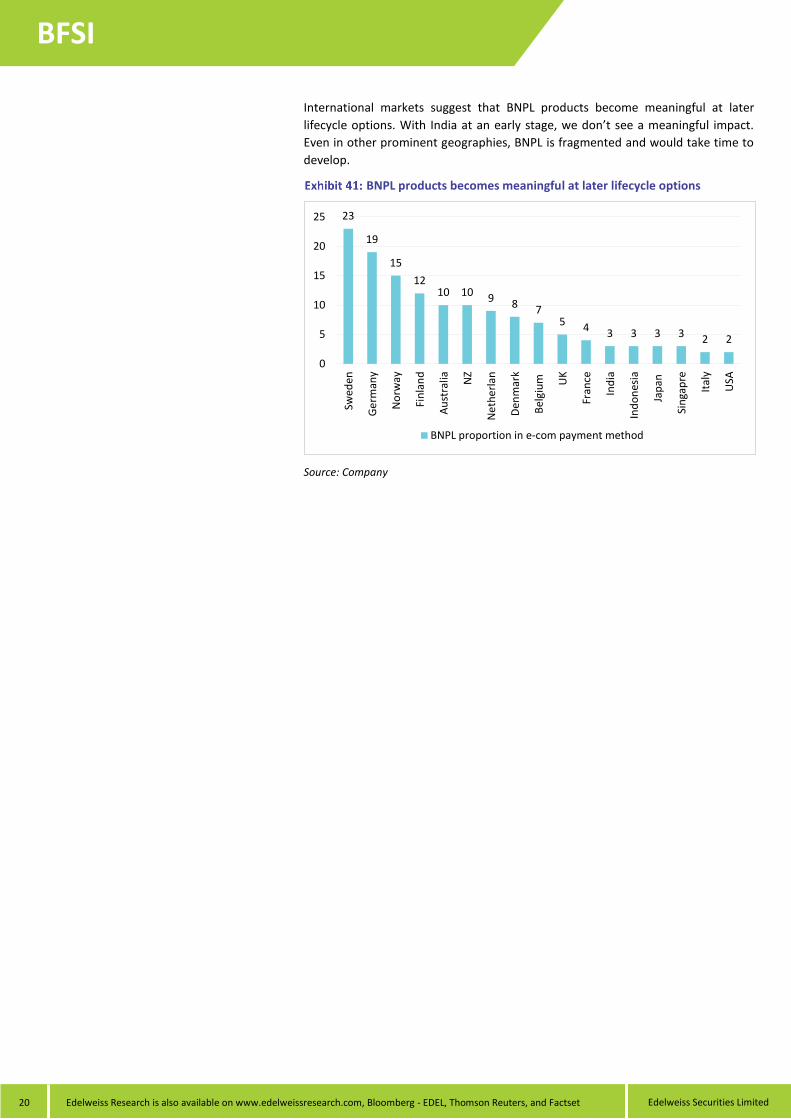

International markets suggest that BNPL products become meaningful at later

lifecycle options. With India at an early stage, we don’t see a meaningful impact.

Even in other prominent geographies, BNPL is fragmented and would take time to

develop.

BNPL products becomes meaningful at later lifecycle options

Source: Company

23

19

15

1210 10 9 8 7

5 4 3 3 3 3 2 2

0

5

10

15

20

25

Swed

en

Ge

rman

y

No

rway

Fin

lan

d

Au

stra

lia NZ

Ne

the

rlan

Den

mar

k

Bel

giu

m UK

Fran

ce

Ind

ia

Ind

on

esia

Jap

an

Sin

gap

re

Ital

y

USA

BNPL proportion in e-com payment method

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 21

Bank or Fintech: Alliance, alliance and more

Slow to warm up to the idea, banks have now started to move towards BNPL

offerings either via modified product offerings (own-in house product offerings) or

through partnership models (via white label BNPL players). The rationale: it not only

captures wide growth opportunity given changing customer behaviour, but also

enables them to capture them young and leverage them through the lifecycle.

Looking at the pioneer BNPL offerings and traditional banking products, the

difference is likely to narrow as BNPL players will try and gradually increase credit

limits (which will be their trial by fire for sustainability) and eventually morph into

retail banking (internationally, this has started with Klarna getting a banking licence)

while banks will leverage their lower capital cost to wade through challengers.

Looking at the evolving dynamics, the market is in hyper-growth mode (albeit at low

base) with competition rising (pioneer BNPL players, payment companies, super

apps, and now banks). Strategies are evolving across players to gain more market

share.

The key differentiator would be ability to build brand and leverage that (banks

already ahead on this) and build a flywheel effect starting from building merchant

relationships (this we believe will require deep pockets).

Partnerships between incumbent players and BNPL providers

Companies Partnership details

Stripe Quadpay

QuadPay customers can select up to USD500 of goods to purchase instantly, which QuadPay pays for using a virtual

card issued through Stripe Issuing and customers then repay QuadPay in four interest-free instalments over six

weeks

Mastercard Splitit Splitit will integrate its instalment solution with Mastercard’s suite of technology as a network partner to enable

merchants to deliver seamless and secure consumer experiences at both online and offline checkout

Amazon Citi

Citi announces launch of Citi Flex Pay on Amazon that gives existing card members who’ve recently

shopped on Amazon with an eligible Citi card the option to pay off large purchases with an equal monthly payment

plan with no formal application, fees or credit check required

Afterpay Stripe Afterpay and Stripe join forces to offer Afterpay’s payment service to Stripe merchants through an easy

and seamless integration without any application, on-boarding, or underwriting process

Source: Company

BFSI

Edelweiss Securities Limited

22 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Risk: Not all sunshine and rainbow

Regulatory supervision likely to mount

One of the biggest challenges for BNPL players is regulation. The potential customer

base, product offerings, and high growth with widening unnoticed debt burden form

a perfect cocktail for regulatory intervention over a period of time—we have seen

regulators around the world sitting up and taking notice.

Looking at the target base of younger population and mass market appeal, the high

growth of BNPLs with lack of an aggregated view of all pending BNPL payments at

different BNPL players will essential pull regulatory attention - as customers start to

face financial difficulties to pay back cumulative instalments.

Competitive pressure to pave way for consolidation

Banks have started to move towards BNPL offerings. Their key advantage is the

ability to offer fully integrated services while leveraging their inherently lower cost

of capital.

We believe while fIntechs have the first-mover advantage and are evolving

innovative and leaner business models, this advantage is unlikely to persist for long.

Given the upcoming number of players, we expect consolidations over time.

Edelweiss Securities Limited

BFSI

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 23

DISCLAIMER Edelweiss Securities Limited (“ESL” or “Research Entity”) is regulated by the Securities and Exchange Board of India (“SEBI”) and is licensed to carry on the business of broking, Investment Adviser, Research Analyst and related activities.

This Report has been prepared by Edelweiss Securities Limited in the capacity of a Research Analyst having SEBI Registration No.INH200000121 and distributed as per SEBI (Research Analysts) Regulations 2014. This report does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Securities as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 includes Financial Instruments and Currency Derivatives. The information contained herein is from publicly available data or other sources believed to be reliable. This report is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this report should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in Securities referred to in this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors.

This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ESL and associates / group companies to any registration or licensing requirements within such jurisdiction. The distribution of this report in certain jurisdictions may be restricted by law, and persons in whose possession this report comes, should observe, any such restrictions. The information given in this report is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. ESL reserves the right to make modifications and alterations to this statement as may be required from time to time. ESL or any of its associates / group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. ESL is committed to providing independent and transparent recommendation to its clients. Neither ESL nor any of its associates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including loss of revenue or lost profits that may arise from or in connection with the use of the information. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein. Past performance is not necessarily a guide to future performance .The disclosures of interest statements incorporated in this report are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The information provided in these reports remains, unless otherwise stated, the copyright of ESL. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of ESL and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.

ESL shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the ESL to present the data. In no event shall ESL be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented by the ESL through this report.

We offer our research services to clients as well as our prospects. Though this report is disseminated to all the customers simultaneously, not all customers may receive this report at the same time. We will not treat recipients as customers by virtue of their receiving this report.

ESL and its associates, officer, directors, and employees, research analyst (including relatives) worldwide may: (a) from time to time, have long or short positions in, and buy or sell the

Securities, mentioned herein or (b) be engaged in any other transaction involving such Securities and earn brokerage or other compensation or act as a market maker in the financial

instruments of the subject company/company(ies) discussed herein or act as advisor or lender/borrower to such company(ies) or have other potential/material conflict of interest with

respect to any recommendation and related information and opinions at the time of publication of research report or at the time of public appearance. ESL may have proprietary long/short

position in the above mentioned scrip(s) and therefore should be considered as interested. The views provided herein are general in nature and do not consider risk appetite or investment

objective of any particular investor; readers are requested to take independent professional advice before investing. This should not be construed as invitation or solicitation to do business

with ESL.

ESL or its associates may have received compensation from the subject company in the past 12 months. ESL or its associates may have managed or co-managed public offering of securities for the subject company in the past 12 months. ESL or its associates may have received compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months. ESL or its associates may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months. ESL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research report. Research analyst or his/her relative or ESL’s associates may have financial interest in the subject company. ESL and/or its Group Companies, their Directors, affiliates and/or employees may have interests/ positions, financial or otherwise in the Securities/Currencies and other investment products mentioned in this report. ESL, its associates, research analyst and his/her relative may have other potential/material conflict of interest with respect to any recommendation and related information and opinions at the time of publication of research report or at the time of public appearance.

Participants in foreign exchange transactions may incur risks arising from several factors, including the following: ( i) exchange rates can be volatile and are subject to large fluctuations; ( ii) the value of currencies may be affected by numerous market factors, including world and national economic, political and regulatory events, events in equity and debt markets and changes in interest rates; and (iii) currencies may be subject to devaluation or government imposed exchange controls which could affect the value of the currency. Investors in securities such as ADRs and Currency Derivatives, whose values are affected by the currency of an underlying security, effectively assume currency risk.

Research analyst has served as an officer, director or employee of subject Company: No

ESL has financial interest in the subject companies: No

ESL’s Associates may have actual / beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report.

Research analyst or his/her relative has actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report: No

ESL has actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report: No

Subject company may have been client during twelve months preceding the date of distribution of the research report.

There were no instances of non-compliance by ESL on any matter related to the capital markets, resulting in significant and material disciplinary action during the last three years except that ESL had submitted an offer of settlement with Securities and Exchange commission, USA (SEC) and the same has been accepted by SEC without admitting or denying the findings in relation to their charges of non registration as a broker dealer.

A graph of daily closing prices of the securities is also available at www.nseindia.com

Analyst Certification:

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

BFSI

Edelweiss Securities Limited

24 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Additional Disclaimers

Disclaimer for U.S. Persons

This research report is a product of Edelweiss Securities Limited, which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Edelweiss Securities Limited only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Edelweiss Securities Limited has entered into an agreement with a U.S. registered broker-dealer, Edelweiss Financial Services Inc. ("EFSI"). Transactions in securities discussed in this research report should be effected through Edelweiss Financial Services Inc.

Disclaimer for U.K. Persons

The contents of this research report have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 ("FSMA"). In the United Kingdom, this research report is being distributed only to and is directed only at (a) persons who have professional experience in matters relating to investments falling within Article 19(5) of the FSMA (Financial Promotion) Order 2005 (the “Order”); (b) persons falling within Article 49(2)(a) to (d) of the Order (including high net worth companies and unincorporated associations); and (c) any other persons to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”). This research report must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this research report relates is available only to relevant persons and will be engaged in only with relevant persons. Any person who is not a relevant person should not act or rely on this research report or any of its contents. This research report must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person. Disclaimer for Canadian Persons

This research report is a product of Edelweiss Securities Limited ("ESL"), which is the employer of the research analysts who have prepared the research report. The research analysts preparing the research report are resident outside the Canada and are not associated persons of any Canadian registered adviser and/or dealer and, therefore, the analysts are not subject to supervision by a Canadian registered adviser and/or dealer, and are not required to satisfy the regulatory licensing requirements of the Ontario Securities Commission, other Canadian provincial securities regulators, the Investment Industry Regulatory Organization of Canada and are not required to otherwise comply with Canadian rules or regulations regarding, among other things, the research analysts' business or relationship with a subject company or trading of securities by a research analyst.

This report is intended for distribution by ESL only to "Permitted Clients" (as defined in National Instrument 31-103 ("NI 31-103")) who are resident in the Province of Ontario, Canada (an "Ontario Permitted Client"). If the recipient of this report is not an Ontario Permitted Client, as specified above, then the recipient should not act upon this report and should return the report to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any Canadian person.

ESL is relying on an exemption from the adviser and/or dealer registration requirements under NI 31-103 available to certain international advisers and/or dealers. Please be advised that (i) ESL is not registered in the Province of Ontario to trade in securities nor is it registered in the Province of Ontario to provide advice with respect to securities; (ii) ESL's head office or principal place of business is located in India; (iii) all or substantially all of ESL's assets may be situated outside of Canada; (iv) there may be difficulty enforcing legal rights against ESL because of the above; and (v) the name and address of the ESL's agent for service of process in the Province of Ontario is: Bamac Services Inc., 181 Bay Street, Suite 2100, Toronto, Ontario M5J 2T3 Canada.

Disclaimer for Singapore Persons

In Singapore, this report is being distributed by Edelweiss Investment Advisors Private Limited ("EIAPL") (Co. Reg. No. 201016306H) which is a holder of a capital markets services license and an exempt financial adviser in Singapore and (ii) solely to persons who qualify as "institutional investors" or "accredited investors" as defined in section 4A(1) of the Securities and Futures Act, Chapter 289 of Singapore ("the SFA"). Pursuant to regulations 33, 34, 35 and 36 of the Financial Advisers Regulations ("FAR"), sections 25, 27 and 36 of the Financial Advisers Act, Chapter 110 of Singapore shall not apply to EIAPL when providing any financial advisory services to an accredited investor (as defined in regulation 36 of the FAR. Persons in Singapore should contact EIAPL in respect of any matter arising from, or in connection with this publication/communication. This report is not suitable for private investors.

Disclaimer for Hong Kong persons

This report is distributed in Hong Kong by Edelweiss Securities (Hong Kong) Private Limited (ESHK), a licensed corporation (BOM -874) licensed and regulated by the Hong Kong Securities and Futures Commission (SFC) pursuant to Section 116(1) of the Securities and Futures Ordinance “SFO”. This report is intended for distribution only to “Professional Investors” as defined in Part I of Schedule 1 to SFO. Any investment or investment activity to which this document relates is only available to professional investor and will be engaged only with professional investors.” Nothing here is an offer or solicitation of these securities, products and services in any jurisdiction where their offer or sale is not qualified or exempt from registration. The report also does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of any individual recipients. The Indian Analyst(s) who compile this report is/are not located in Hong Kong and is/are not licensed to carry on regulated activities in Hong Kong and does not / do not hold themselves out as being able to do so. Copyright 2009 Edelweiss Research (Edelweiss Securities Ltd). All rights reserved.

Aditya Narain

Head of Research

Edelweiss Securities Limited, Edelweiss House, off C.S.T. Road, Kalina, Mumbai 400 098Tel: +91 22 4009 4400. Email: [email protected]

Related Documents