© 2013 Winston & Strawn LLP Section 409A Update November 4, 2013 Michael Falk

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2013 Winston & Strawn LLP

Section 409A Update November 4, 2013

Michael Falk

© 2013 Winston & Strawn LLP 2

Today’s eLunch Presenter

Michael Falk EBEC Practice Group

Chicago [email protected]

(312) 558-7232

© 2013 Winston & Strawn LLP 3

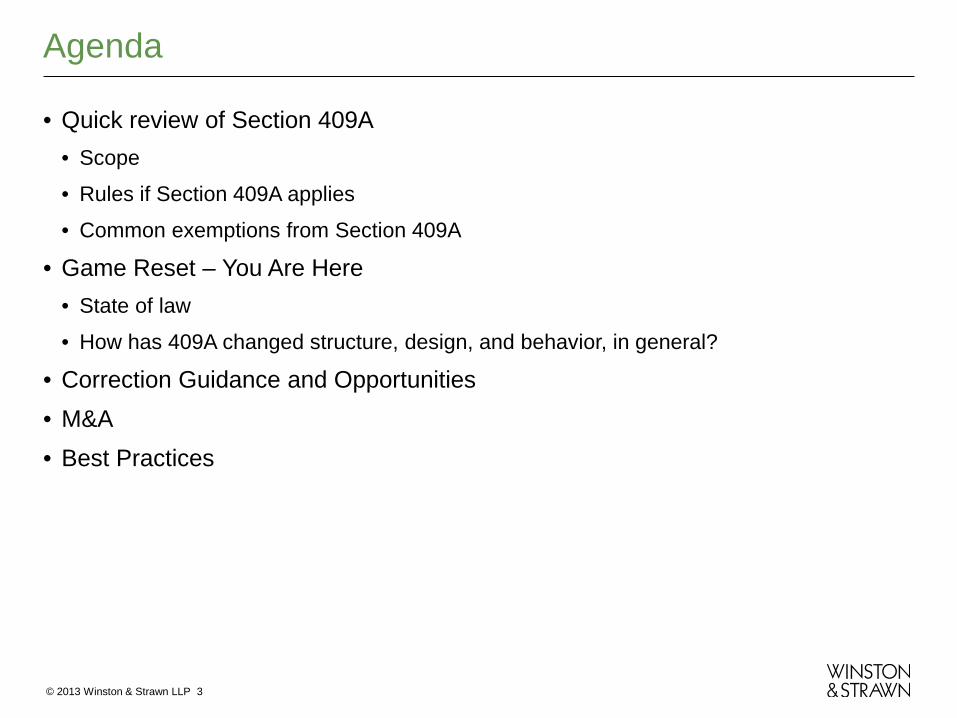

Agenda

• Quick review of Section 409A • Scope

• Rules if Section 409A applies

• Common exemptions from Section 409A

• Game Reset – You Are Here • State of law

• How has 409A changed structure, design, and behavior, in general?

• Correction Guidance and Opportunities • M&A • Best Practices

© 2013 Winston & Strawn LLP 4

Quick Review

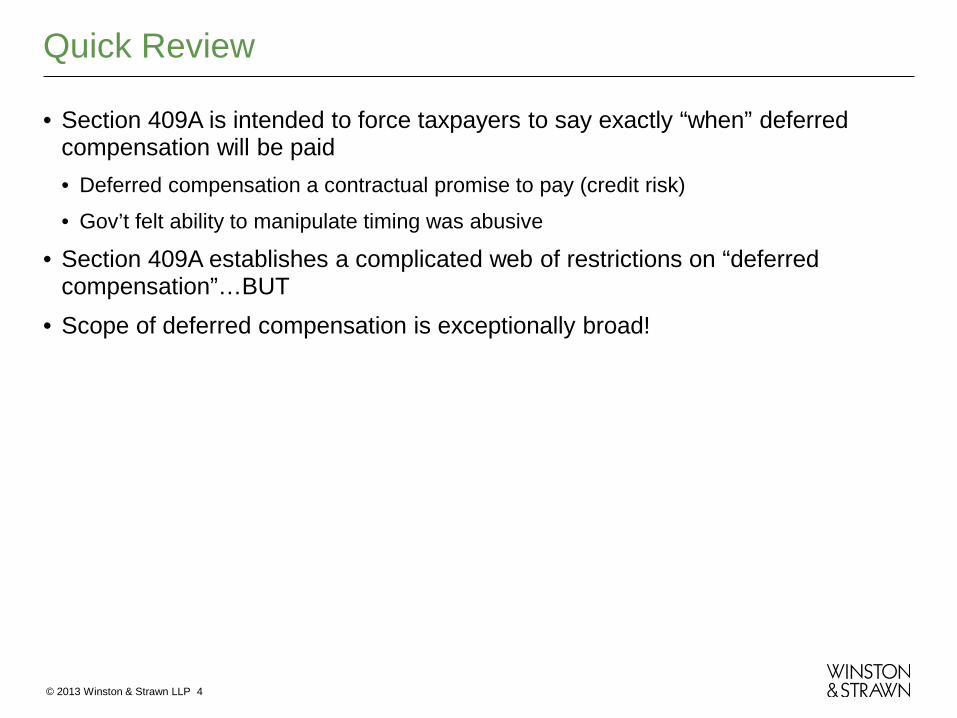

• Section 409A is intended to force taxpayers to say exactly “when” deferred compensation will be paid • Deferred compensation a contractual promise to pay (credit risk)

• Gov’t felt ability to manipulate timing was abusive

• Section 409A establishes a complicated web of restrictions on “deferred compensation”…BUT

• Scope of deferred compensation is exceptionally broad!

© 2013 Winston & Strawn LLP 5

Quick Review (continued)

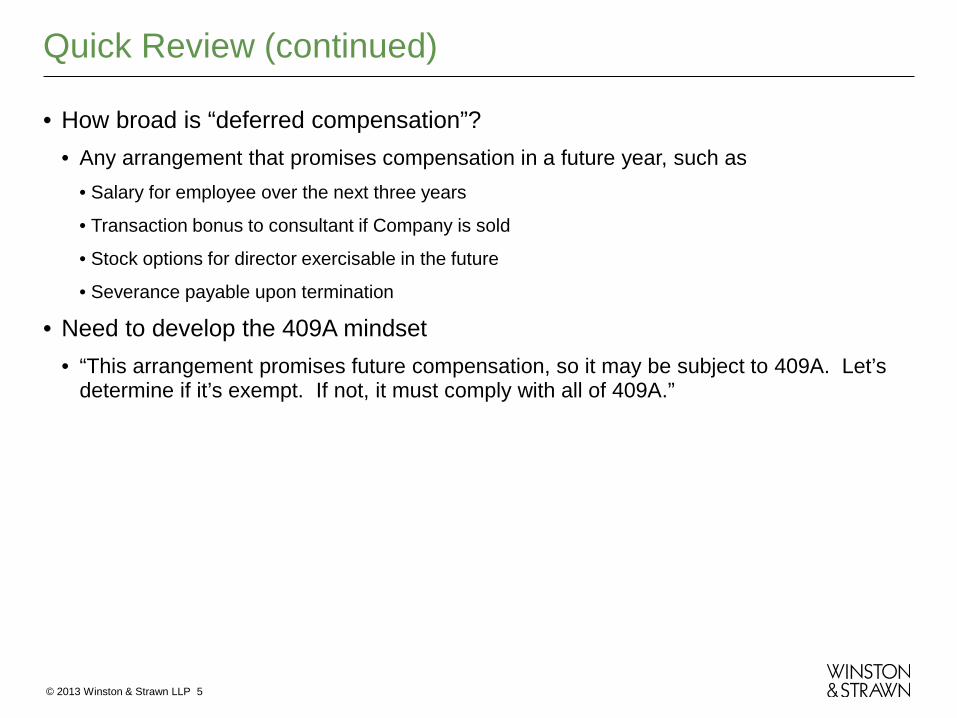

• How broad is “deferred compensation”? • Any arrangement that promises compensation in a future year, such as

• Salary for employee over the next three years

• Transaction bonus to consultant if Company is sold

• Stock options for director exercisable in the future

• Severance payable upon termination

• Need to develop the 409A mindset • “This arrangement promises future compensation, so it may be subject to 409A. Let’s

determine if it’s exempt. If not, it must comply with all of 409A.”

© 2013 Winston & Strawn LLP 6

Quick Review (continued)

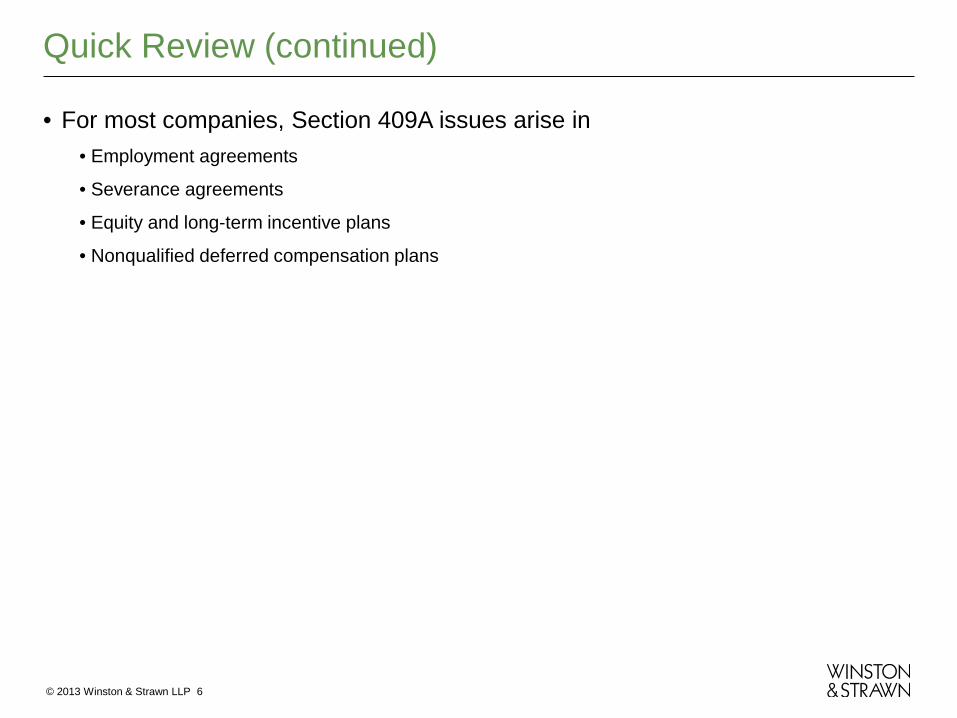

• For most companies, Section 409A issues arise in • Employment agreements

• Severance agreements

• Equity and long-term incentive plans

• Nonqualified deferred compensation plans

© 2013 Winston & Strawn LLP 7

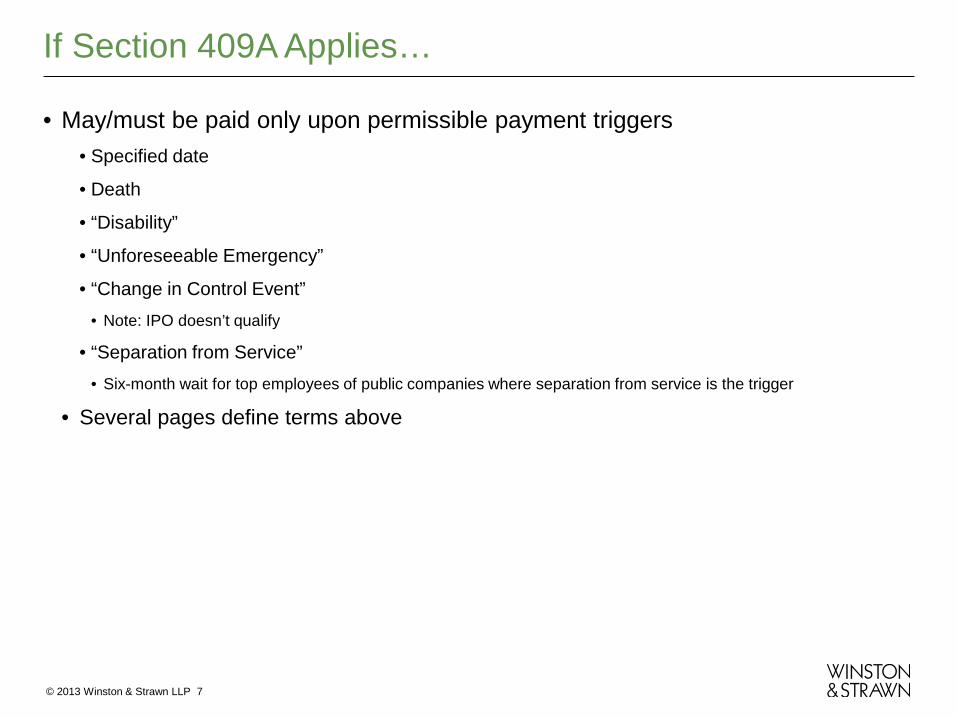

If Section 409A Applies…

• May/must be paid only upon permissible payment triggers • Specified date

• Death

• “Disability”

• “Unforeseeable Emergency”

• “Change in Control Event” • Note: IPO doesn’t qualify

• “Separation from Service” • Six-month wait for top employees of public companies where separation from service is the trigger

• Several pages define terms above

© 2013 Winston & Strawn LLP 8

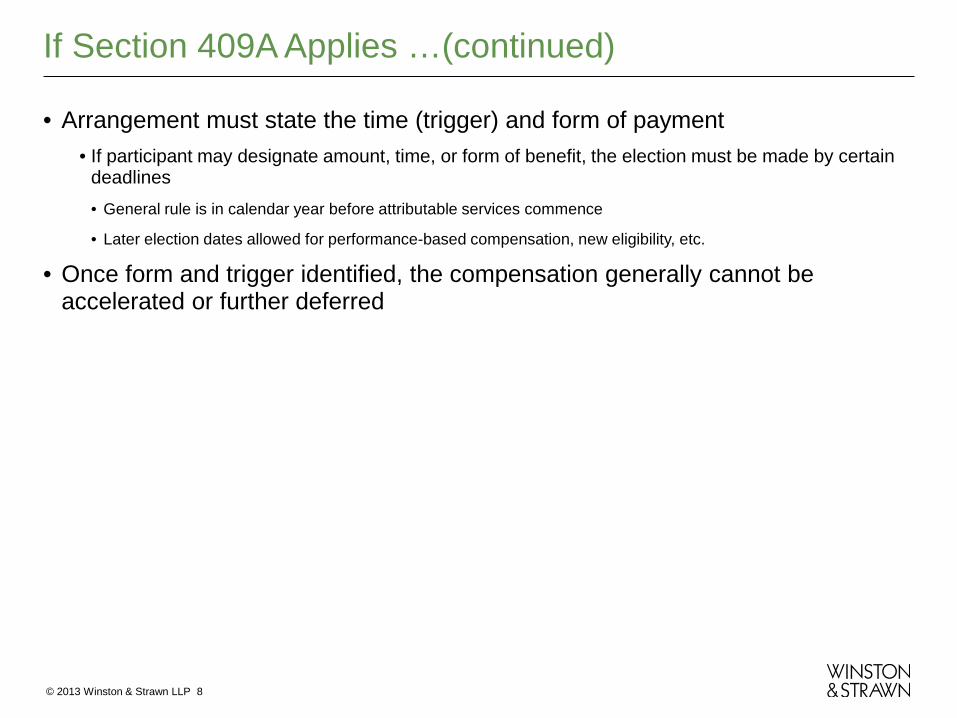

If Section 409A Applies …(continued)

• Arrangement must state the time (trigger) and form of payment • If participant may designate amount, time, or form of benefit, the election must be made by certain

deadlines • General rule is in calendar year before attributable services commence

• Later election dates allowed for performance-based compensation, new eligibility, etc.

• Once form and trigger identified, the compensation generally cannot be accelerated or further deferred

© 2013 Winston & Strawn LLP 9

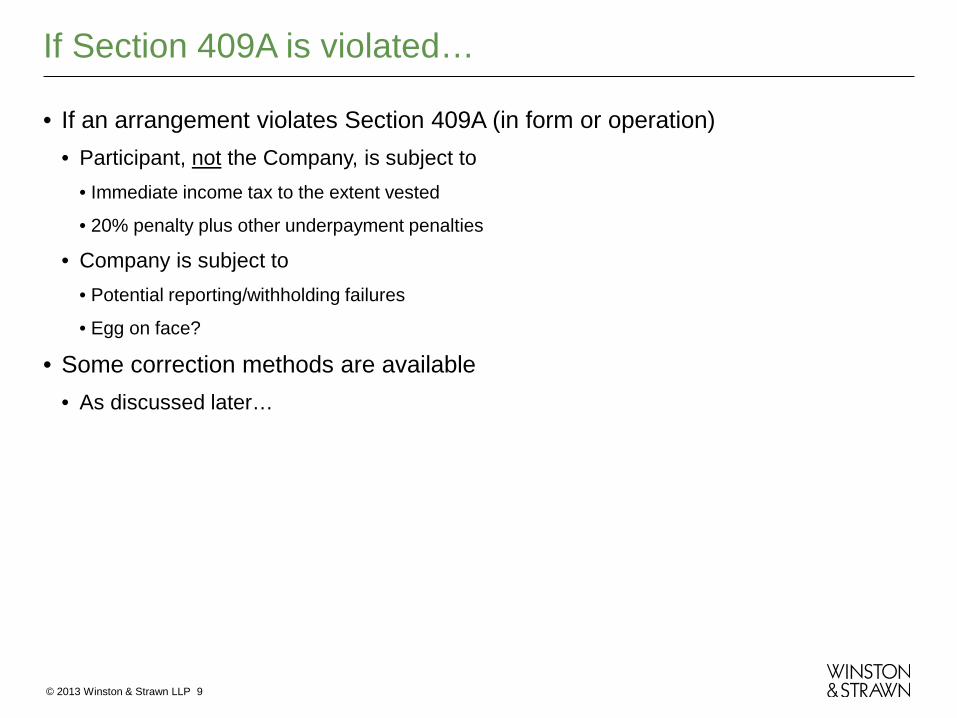

If Section 409A is violated…

• If an arrangement violates Section 409A (in form or operation) • Participant, not the Company, is subject to

• Immediate income tax to the extent vested

• 20% penalty plus other underpayment penalties

• Company is subject to • Potential reporting/withholding failures

• Egg on face?

• Some correction methods are available • As discussed later…

© 2013 Winston & Strawn LLP 10

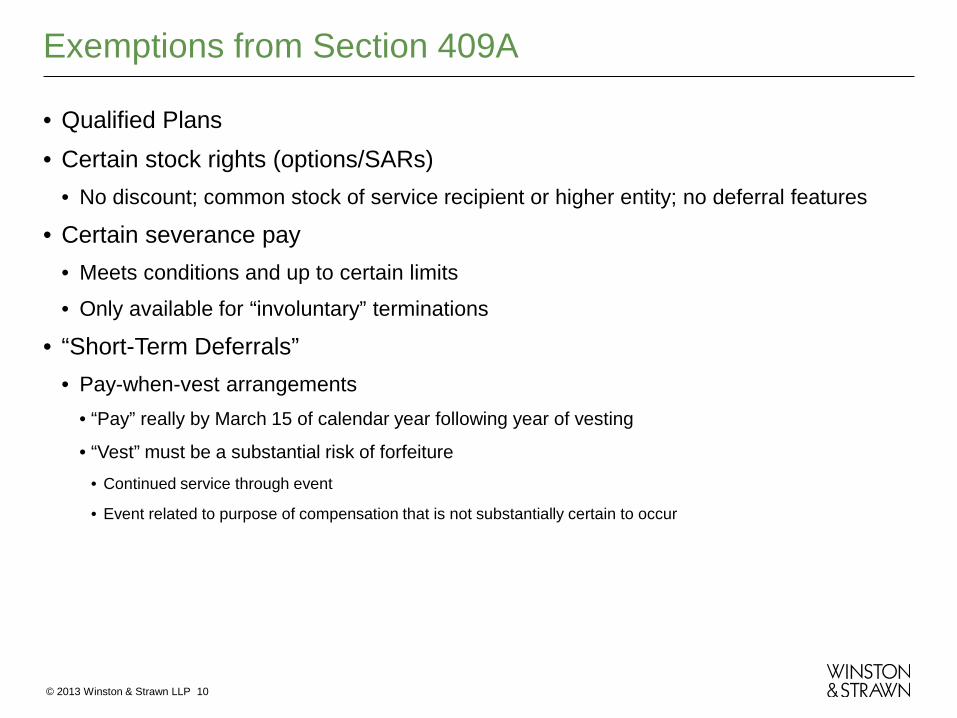

Exemptions from Section 409A

• Qualified Plans • Certain stock rights (options/SARs)

• No discount; common stock of service recipient or higher entity; no deferral features

• Certain severance pay • Meets conditions and up to certain limits

• Only available for “involuntary” terminations

• “Short-Term Deferrals” • Pay-when-vest arrangements

• “Pay” really by March 15 of calendar year following year of vesting

• “Vest” must be a substantial risk of forfeiture • Continued service through event

• Event related to purpose of compensation that is not substantially certain to occur

© 2013 Winston & Strawn LLP 11

Game Reset – You Are Here

• Section 409A is alive and in effect • Violations (form or operation) trigger full wrath of Section 409A penalties unless

corrected under applicable guidance • Section 409A penalties calculated pursuant to proposed regulations

• Still awaiting final regulations

• Chill out, California: • Oct 2013: Reduces its State 20% penalty to 5%

© 2013 Winston & Strawn LLP 12

Game Reset – You Are Here (continued)

• 409A experts still among least popular in the room • Documents are longer, with many technical provisions meaningless to lay

people • Uncertainty regarding gray areas and likelihood of enforcement/discovery • Bogeyman (so far) isn’t the IRS, it’s counterpart in corporate transactions

© 2013 Winston & Strawn LLP 13

Overall Effect of 409A • How has 409A changed structure, design, behavior generally?

• Traditional nonqualified deferred compensation

• Still popular – newly increased tax rates will only cause more demand • Certain plan features now strategize for 409A

• To avoid hassle of determining “specified employee,” some public co. plans impose six-month wait on everyone

• To maximize distribution flexibility, use five buckets to “ladder” distributions

• Redeferral rules usually require five-year broad jump (move Year 7 distribution to at least Year 12)

• Companies more vigilant about plan operation

© 2013 Winston & Strawn LLP 14

Overall Effect of 409A (continued) • How has 409A changed structure, design, behavior generally?

• Employment agreements/severance • Now contain lots of 409A boilerplate

• Specific release timing language

• More conservative definitions of Good Reason/fewer walk-away windows

• Lump-sum severance slightly more common

• Post-employment COBRA or retiree medical less common and approached differently

• 409A indemnity?

© 2013 Winston & Strawn LLP 15

Overall Effect of 409A (continued)

• How has 409A changed structure, design, behavior generally? • Equity compensation

• Stock options still popular, but more sensitive for private companies • “Fair Market Value” methods vary for exercise price (geography, ownership)

• RSUs often designed to pay-when-vest • “Retirement” vesting less common, but still out there

• Phantom design often has pimples • If vest before payment, must use 409A “change in control”

• Often frustrating that IPO doesn’t qualify

© 2013 Winston & Strawn LLP 16

409A Corrections – General

• IRS has provided correction guidance for both: • Operational errors (Notices 2008-113, 2010-6, & 2010-80)

• Document errors (Notices 2010-6 & 2010-80)

• Many corrections require one-page notice to be attached to both employee’s and company’s next tax returns • Increase audit risk?

• Need good communication among internal groups (HR, Tax, etc.)

• Some companies more hesitant than others to use correction guidance • Look to argue correction guidance not necessary

• Even concede violation in some cases

© 2013 Winston & Strawn LLP 17

Good News for Immature and Overripe

• Immature = Not yet vested • Proposed income inclusion regulations give very helpful ability to correct unvested

amounts • Amounts are includible in income and subject to additional 409A taxes in the first year in which

• Amount vests (i.e., no longer subject to “substantial risk of forfeiture”) AND

• Deferred amount is subject to a 409A error (form or operation)

© 2013 Winston & Strawn LLP 18

Unvested Amounts (continued)

• May self-correct while unvested • Operational or document problems

• Helpful for discounted options/linked plans

• No need to use formal correction guidance or to attach notices • Can’t abuse it…

• Only used to correct inadvertent errors

• No pattern of using rule to abuse 409A

© 2013 Winston & Strawn LLP 19

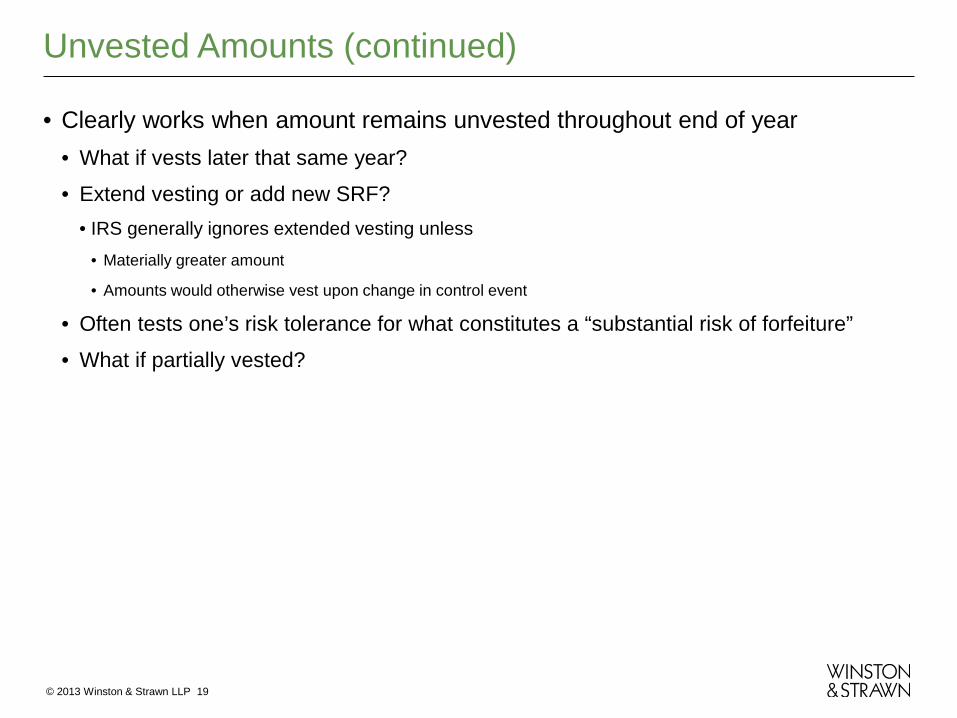

Unvested Amounts (continued)

• Clearly works when amount remains unvested throughout end of year • What if vests later that same year?

• Extend vesting or add new SRF? • IRS generally ignores extended vesting unless

• Materially greater amount

• Amounts would otherwise vest upon change in control event

• Often tests one’s risk tolerance for what constitutes a “substantial risk of forfeiture”

• What if partially vested?

© 2013 Winston & Strawn LLP 20

Good News for Immature and Overripe

• Overripe = Closed tax years • Proposed income inclusion regs concede that 409A violation in closed tax year is non-

event • Example: Distribution due in 2007 was never made. Violation occurred in 2007 and can be paid

now without 409A problem. Normal income tax applies.

© 2013 Winston & Strawn LLP 21

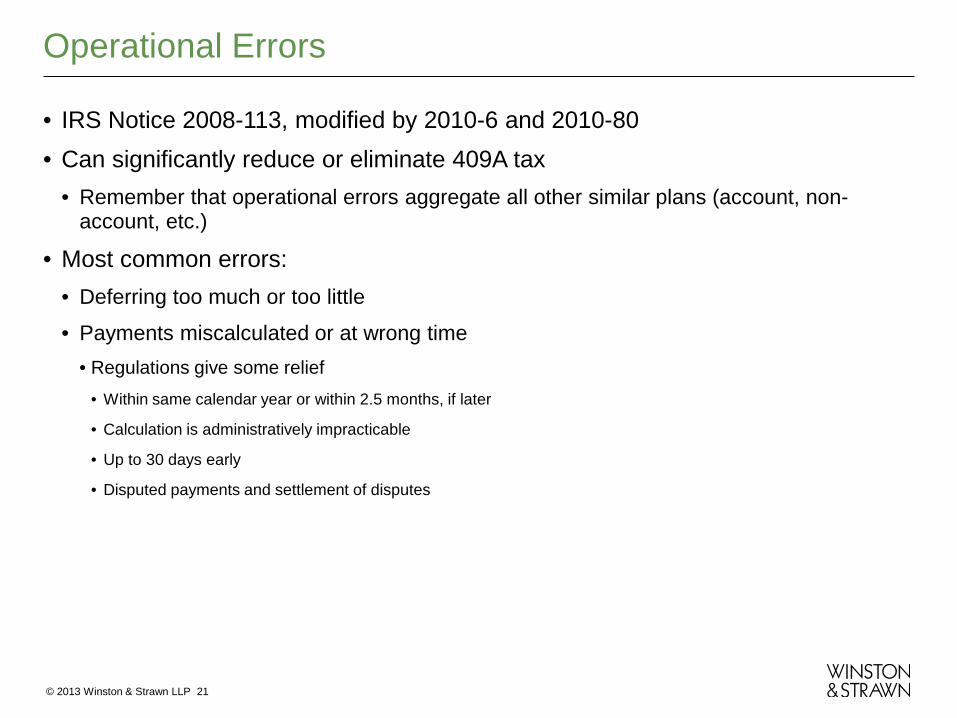

Operational Errors

• IRS Notice 2008-113, modified by 2010-6 and 2010-80 • Can significantly reduce or eliminate 409A tax

• Remember that operational errors aggregate all other similar plans (account, non-account, etc.)

• Most common errors: • Deferring too much or too little

• Payments miscalculated or at wrong time • Regulations give some relief

• Within same calendar year or within 2.5 months, if later

• Calculation is administratively impracticable

• Up to 30 days early

• Disputed payments and settlement of disputes

© 2013 Winston & Strawn LLP 22

Operational Errors (continued)

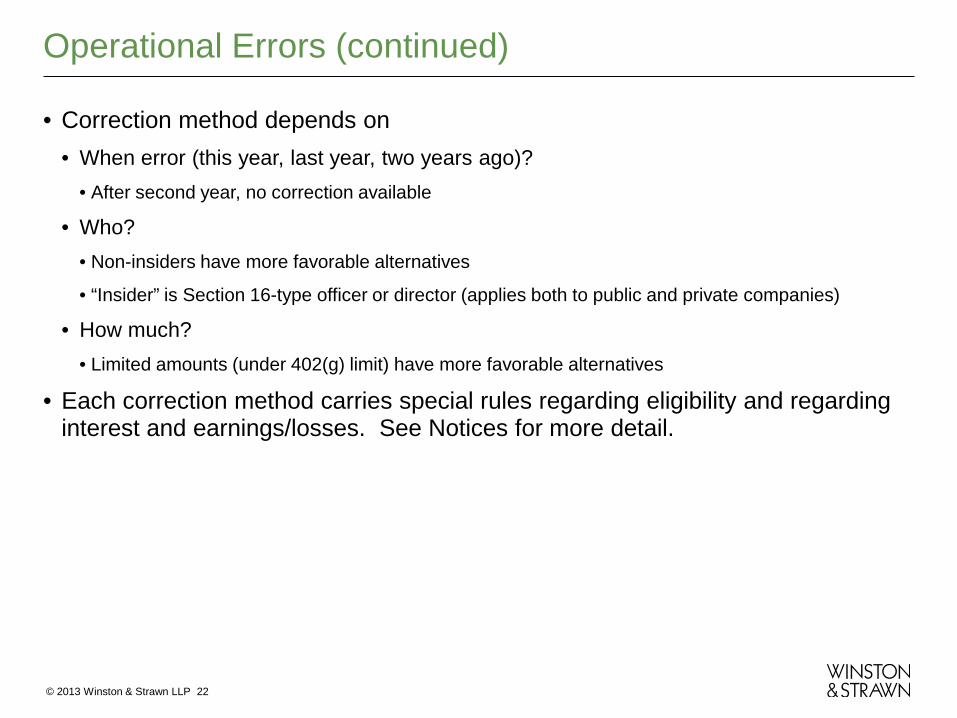

• Correction method depends on • When error (this year, last year, two years ago)?

• After second year, no correction available

• Who? • Non-insiders have more favorable alternatives

• “Insider” is Section 16-type officer or director (applies both to public and private companies)

• How much? • Limited amounts (under 402(g) limit) have more favorable alternatives

• Each correction method carries special rules regarding eligibility and regarding interest and earnings/losses. See Notices for more detail.

© 2013 Winston & Strawn LLP 23

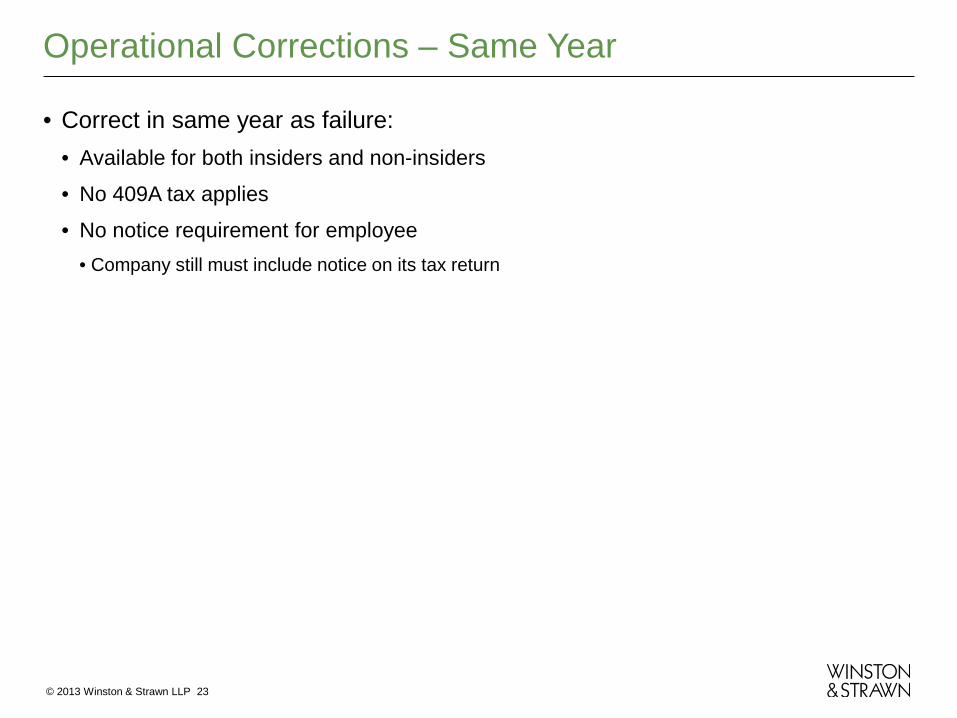

Operational Corrections – Same Year

• Correct in same year as failure: • Available for both insiders and non-insiders

• No 409A tax applies

• No notice requirement for employee • Company still must include notice on its tax return

© 2013 Winston & Strawn LLP 24

Operational Corrections – Same Year (continued)

• Failure to defer or payment at least one tax year too early • Employee must contribute/repay amount to the plan

• Non-insiders have up to 24 months

• Insiders must pay during that year

• Pay too early within year or violate “six-month delay” rule • Employee must repay amount to the plan

• Payment then delayed beyond original date by number of days employee had the money

© 2013 Winston & Strawn LLP 25

Operational Corrections – Same Year (continued)

• Excess Deferral • Plan must distribute

• Stock Rights • If unintentionally discounted, may adjust price up to at least grant-date FMV

• Again, for these same-year corrections… • Available for both insiders and non-insiders

• No 409A tax applies

• No notice requirement for employee, but company must include notice on its tax return

© 2013 Winston & Strawn LLP 26

Operational Corrections – Next Year

• Correct in following taxable year: • Only for non-insiders

• No 409A tax applies

• Notice requirement on tax returns of both employee and company

© 2013 Winston & Strawn LLP 27

Operational Corrections – Next Year (continued)

• Failure to defer or payment at least one tax year too early • Repay back to the plan

• Paid too early within year or violated six-month rule • Repay back to the plan and then wait for period equal to number of days by which

original payment was too early

© 2013 Winston & Strawn LLP 28

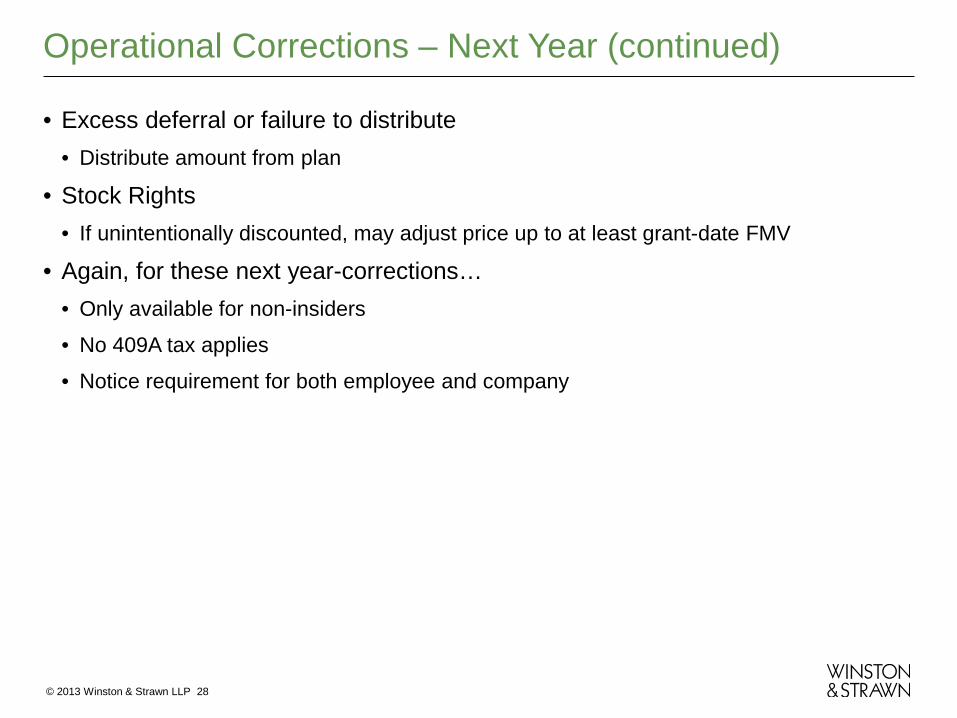

Operational Corrections – Next Year (continued)

• Excess deferral or failure to distribute • Distribute amount from plan

• Stock Rights • If unintentionally discounted, may adjust price up to at least grant-date FMV

• Again, for these next year-corrections… • Only available for non-insiders

• No 409A tax applies

• Notice requirement for both employee and company

© 2013 Winston & Strawn LLP 29

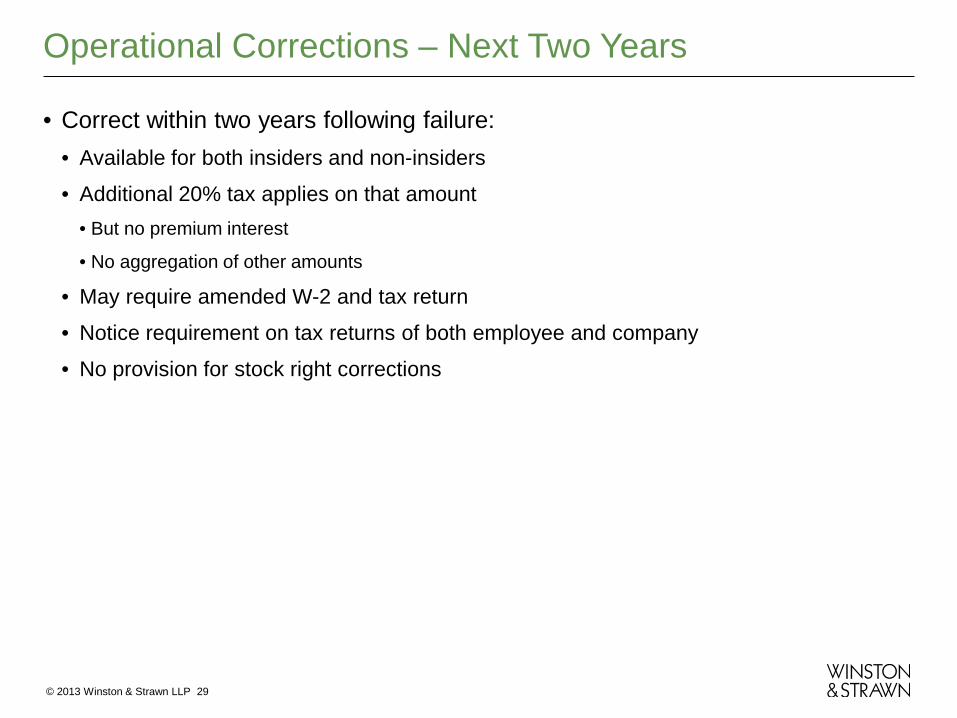

Operational Corrections – Next Two Years

• Correct within two years following failure: • Available for both insiders and non-insiders

• Additional 20% tax applies on that amount • But no premium interest

• No aggregation of other amounts

• May require amended W-2 and tax return

• Notice requirement on tax returns of both employee and company

• No provision for stock right corrections

© 2013 Winston & Strawn LLP 30

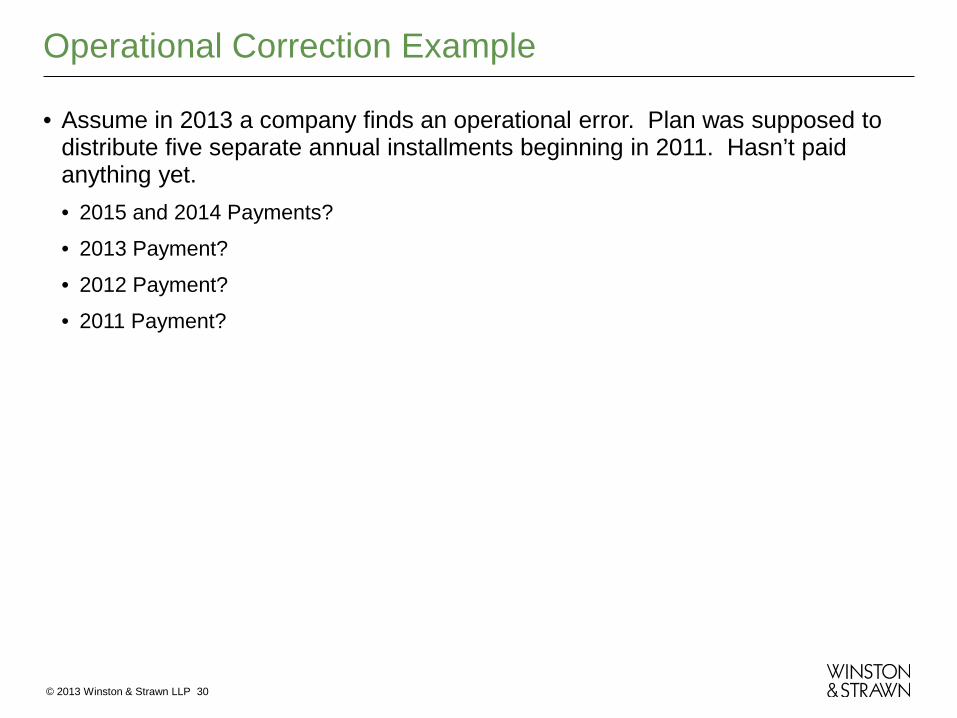

Operational Correction Example

• Assume in 2013 a company finds an operational error. Plan was supposed to distribute five separate annual installments beginning in 2011. Hasn’t paid anything yet. • 2015 and 2014 Payments?

• 2013 Payment?

• 2012 Payment?

• 2011 Payment?

© 2013 Winston & Strawn LLP 31

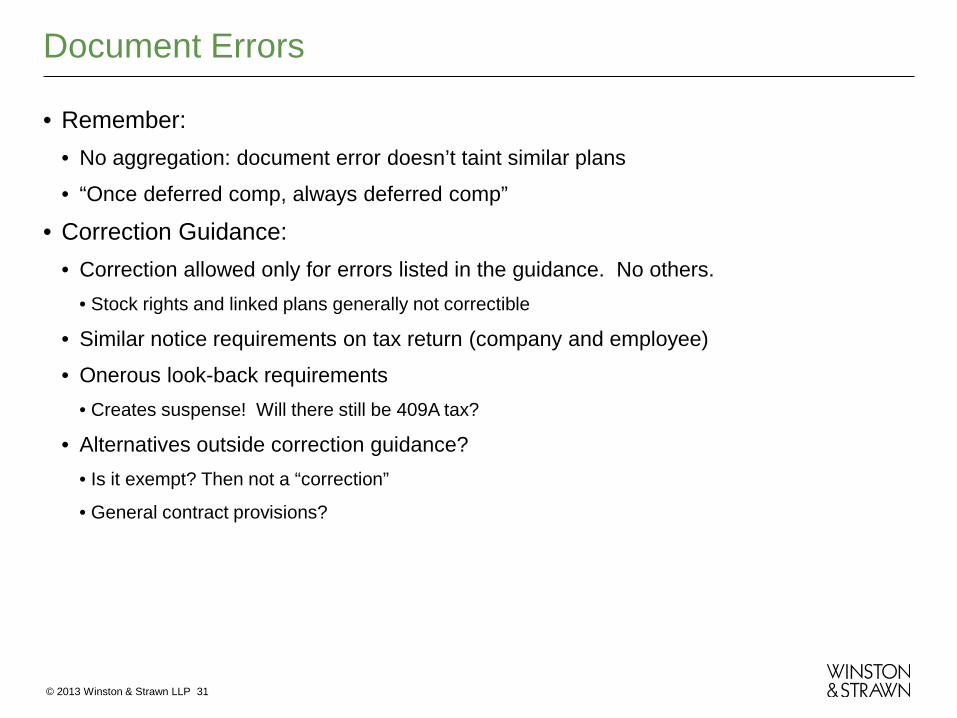

Document Errors

• Remember: • No aggregation: document error doesn’t taint similar plans

• “Once deferred comp, always deferred comp”

• Correction Guidance: • Correction allowed only for errors listed in the guidance. No others.

• Stock rights and linked plans generally not correctible

• Similar notice requirements on tax return (company and employee)

• Onerous look-back requirements • Creates suspense! Will there still be 409A tax?

• Alternatives outside correction guidance? • Is it exempt? Then not a “correction”

• General contract provisions?

© 2013 Winston & Strawn LLP 32

Document Errors (continued)

• 2010-6 allows informal corrections for minor document problems • No need to do filings. No look-back. Not a violation.

• “As soon as practicable” • No problem as long as it follows a permissible payment trigger (“PPT”)

• Ambiguous definition or no definition • Document complies if savings clause

• No document violation as long as interpreted consistently with PPT

© 2013 Winston & Strawn LLP 33

Document Errors (continued)

• Bad definitions of otherwise PPT • Amend to correct the definition

• If bad trigger happens within 12 months, then 409A tax applies to some portion of the plan benefit • Bad definition of “separation from service”: 50% subject

• Bad definition of “change in control” or disability: 25%

• Bad payment periods following PPT (too long a period or impermissible employee discretion, such as an unlimited release period) • If fix before PPT occurs, no portion subject to 409A tax

• If fix after PPT occurs, 50% subject to 409A tax

© 2013 Winston & Strawn LLP 34

Document Errors (continued)

• Multiple triggers: some good PPTs, some bad • Remove bad trigger

• If bad trigger happens within 12 months, 50% subject to 409A tax

• Only bad triggers • Remove all bad triggers and replace with later of separation from service and six-year

anniversary of correction

• 409A tax automatically applies to 50% of the benefit

• Multiple schedules/time form of payment and employee discretion • Amend to eliminate all but the latest

• If triggering event happens within 12 months, 50% subject to 409A tax

• Impermissible Employer discretion to accelerate payment • Amend to eliminate discretion before exercised

© 2013 Winston & Strawn LLP 35

Document Errors (continued)

• Bad language regarding in-kind benefits • Amend language

• If event that would trigger benefit occurs within 12 months, 50% subject to 409A tax

• Document fails to include six-month delay • Amend before applicable separation from service to provide for payment on later of 18

months following correction or six months from separation from service

• If separation from service occurs within 12 months, 50% subject to 409A tax

• Big help? Any document error can be corrected within first year of new plan.

© 2013 Winston & Strawn LLP 36

Audits and Cavity Searches

• IRS audit activity minimal to date • Early Information Document Requests sought information about SRFs and short-term

deferrals • Difficult at times to know whether a plan is subject to Section 409A (that is “we think it’s exempt but

it complies anyway…”)

• Cavity searches occur in corporate transactions • Buyer, lender, etc.

• Valuable to self-audit, categorize and correct or amend documents ahead of transaction rush

• Typical reps/warranties

© 2013 Winston & Strawn LLP 37

M&A Issues

• Exempt animals are your friends (great flexibility) • Short-term deferrals

• Stock rights (options)

• Exempt severance

• If substituting stock options, need to comply with 409A rules (e.g., ratio test) • Is there a “change in control” or “separation from service”? • Earn-outs • Special rule allows plan termination upon 409A change in control

© 2013 Winston & Strawn LLP 38

Best Practices

• Educate everyone: No compensatory document goes out without 409A review • Adopt an overarching “409A Policies and Procedures” document to fill in gaps • Design for exemption!

• Short-term deferrals, severance exemption, stock rights

• Simplifies corrections and gives more flexibility to eliminate, amend, accelerate, etc.

• Watch out for “Retirement” trap!

• Include change in control as payment trigger or rely on termination rule?

© 2013 Winston & Strawn LLP 39

Best Practices (continued)

• If allowing participant elections, dissect election forms to avoid errors • What compensation? (Bonus, annual, plan name)

• New elections affect existing deferrals?

• Complying with deferral timing rules? • Example: really “performance based”/“newly eligible”?

• What if compensation changes during year?

• Preemptively compliant stock options • For private companies

• Does it really change behavior?

© 2013 Winston & Strawn LLP 40

Contact Information

Michael Falk EBEC Practice Group

Chicago (312) 558-7232

Buy my book! ◦ Practical Guide to Code Section 409A (CCH, 2012) ◦ Holidays will be here before you know it!

© 2013 Winston & Strawn LLP 41

Questions?

© 2013 Winston & Strawn LLP 42

Thank You.

© 2013 Winston & Strawn LLP 43

• Required Circular 230 Notice: Any Federal tax advice contained herein is not written to be used for, and the recipient and any subsequent reader cannot use such advice for, the purpose of avoiding any penalties asserted under the Internal Revenue Code. If the foregoing contains Federal tax advice and is distributed to a person other than the addressee, each additional and subsequent reader hereof is notified that such advice should be considered to have been written to support the promotion or marketing of the transaction or matter addressed herein. In that event, each such reader should seek advice from an independent tax advisor with respect to the transaction or matter addressed herein based on the reader’s particular circumstances.

Related Documents