Understanding you and your Mortgage & Protection Needs Date of Fact Find Face to Face Meeting Non Face to Face Meeting Client 1 Name Client 2 Name Contact Details (phone number, email address) Contact Details (phone number, email address) Preferred Contact Method Home Preferred Contact Method Home Work Work Email Email Post Post Buyer Type Home Owner First Time Buyer Buy to Let Framework for our meeting: What do you want to get from the meeting? What do you know about our firm and myself? How to we deliver solutions to you? Understanding more about your needs Which solutions suit you the best? What can we expect from each other? Adviser Name Firm Name 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Understanding you and your Mortgage & Protection Needs

Date of Fact FindFace to Face Meeting

Non Face to Face Meeting

Client 1 Name Client 2 Name

Contact Details (phone number, email address)

Contact Details (phone number, email address)

Preferred Contact Method

Home Preferred Contact Method

Home

Work Work

Email Email

Post Post

Buyer Type Home Owner First Time Buyer Buy to Let

Framework for our meeting: What do you want to get from the meeting? What do you know about our firm and myself? How to we deliver solutions to you? Understanding more about your needs Which solutions suit you the best? What can we expect from each other?

Adviser Name

Firm Name

Version 1.0 – November 2015

1

ContentsSection 1a – Your expectations and perceptions...........................................................................................3

Section 1b – Your requirements...........................................................................................................................4

Mortgage Purpose.................................................................................................................................................4

Mortgage Loan.......................................................................................................................................................4

Mortgage Term......................................................................................................................................................4

Mortgage Repayment..........................................................................................................................................4

Your Budget............................................................................................................................................................5

Mortgage Product..................................................................................................................................................5

Mortgage lenders & features............................................................................................................................5

Protecting you and your home.........................................................................................................................6

Section 2 - Your financial situation.....................................................................................................................6

Initial costs..............................................................................................................................................................6

Deposit and Anti-Money Laundering Requests...........................................................................................6

Mortgage expenditure.........................................................................................................................................7

Existing financial commitments.......................................................................................................................9

Other financial commitments.........................................................................................................................10

Income & Salary..................................................................................................................................................11

Existing protection & lump sum arrangements from policies and work benefits.........................12

Existing Pensions.................................................................................................................................................13

Existing Investments..........................................................................................................................................14

Section 3 - Your future plans...............................................................................................................................15

Potential changes - Lifestyle...........................................................................................................................15

Potential changes – Mortgage........................................................................................................................15

Section 4 – Perceptions versus actual needs................................................................................................16

Mortgage purpose...............................................................................................................................................16

Mortgage loan......................................................................................................................................................16

Mortgage term.....................................................................................................................................................16

Mortgage repayment.........................................................................................................................................17

Your budget...........................................................................................................................................................17

Mortgage Product................................................................................................................................................17

Mortgage lenders & features..........................................................................................................................18

Section 5 – Hard facts............................................................................................................................................19

Section 6 – Protecting you and your mortgage............................................................................................23

Section 7 – Appendices.........................................................................................................................................24

Section 8 – Key Contact Details.........................................................................................................................28

2

Section 1a – Your expectations and perceptions

What has prompted you to come and see me now?

Tell me about your current situation? (family, work, home)

What are your thoughts about what you feel you need? (initial thoughts about your situation and requirements)

What is important to you & why? (e.g. mortgage repayment goals, lifestyle, certainty – peace of mind)

What plans do you have for the future? (thoughts on changing situation, job, family, other finances)

What services do you expect from me?

3

Section 1b – Your requirementsMortgage Purpose

What is the loan for? Purchase Remortgage Debt Consolidation

Buy to Let Let to Buy Further AdvanceSecond Home Secured Other

Notes

Mortgage Loan

Purchase prices for the new loanEstimated value of the propertyAmount of loan required

Amount of deposit

How long do you plan to be in this property?

Client 1 Client 2Have you ever had a mortgage on a property which has been repossessed or voluntarily surrendered?

Yes No Yes No

Mortgage TermDetails

When would you like to have your mortgage paid off by and why?

Specific dateSpecific ageBy retirement dateAs soon as affordableDon’t knowWhen Inheritance receivedOther

This would mean a term of... years

Mortgage Repayment

Do you have a view on how you would like to repay your mortgage?

Repayment Part & PartInterest only No preference

If Part & Part – amount on Interest Only and Repayment

Interest

Only£ Repaymen

t £

4

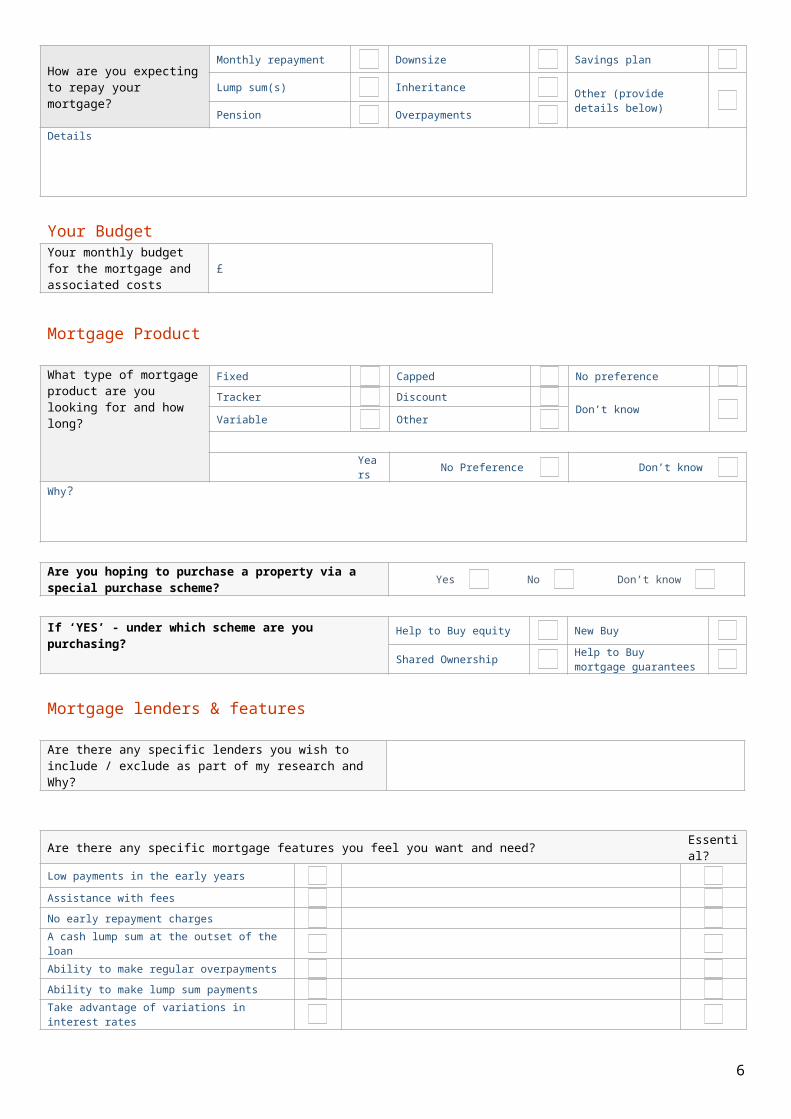

How are you expecting to repay your mortgage?

Monthly repayment Downsize Savings plan

Lump sum(s) Inheritance Other (provide details below)Pension Overpayments

Details

Your BudgetYour monthly budget for the mortgage and associated costs

£

Mortgage Product

What type of mortgage product are you looking for and how long?

Fixed Capped No preferenceTracker Discount

Don’t knowVariable Other

Years No Preference Don’t know

Why?

Are you hoping to purchase a property via a special purchase scheme? Yes No Don’t know

If ‘YES’ - under which scheme are you purchasing?

Help to Buy equity New Buy

Shared Ownership Help to Buy mortgage guarantees

Mortgage lenders & features

Are there any specific lenders you wish to include / exclude as part of my research and Why?

Are there any specific mortgage features you feel you want and need?Essential?

Low payments in the early yearsAssistance with feesNo early repayment chargesA cash lump sum at the outset of the loan Ability to make regular overpayments Ability to make lump sum payments Take advantage of variations in interest ratesStability of payments Linked to Bank of England base rateAbility to budgetFlexible payment arrangements

5

Protecting you and your home

How are you planning to protect your home and your possessions?Buildings (compulsory)ContentsOther

How are you planning to protect your income that funds your mortgage and lifestyle costs?

FullyPartiallyDon’t know

How are you planning to repay your mortgage if you become ill or die?FullyPartiallyDon’t know

Section 2 - Your financial situationInitial costs

Type Estimated?Stamp Duty £Legal fees/Land registry £Estate Agent £Removal costs £Mortgage valuation £Mortgage lenders arrangement fee £Early repayment fee on existing loan(s) £High lending charge £Mortgage advice / implementation fee £

Total £

Where is this being funded from?

Deposit and Anti-Money Laundering Requests

What is the source of your deposit?

Savings (and how accrued) £Family Gift (how much and from whom) £Equity £Other £

Total £

Details (including evidence you can provide)

6

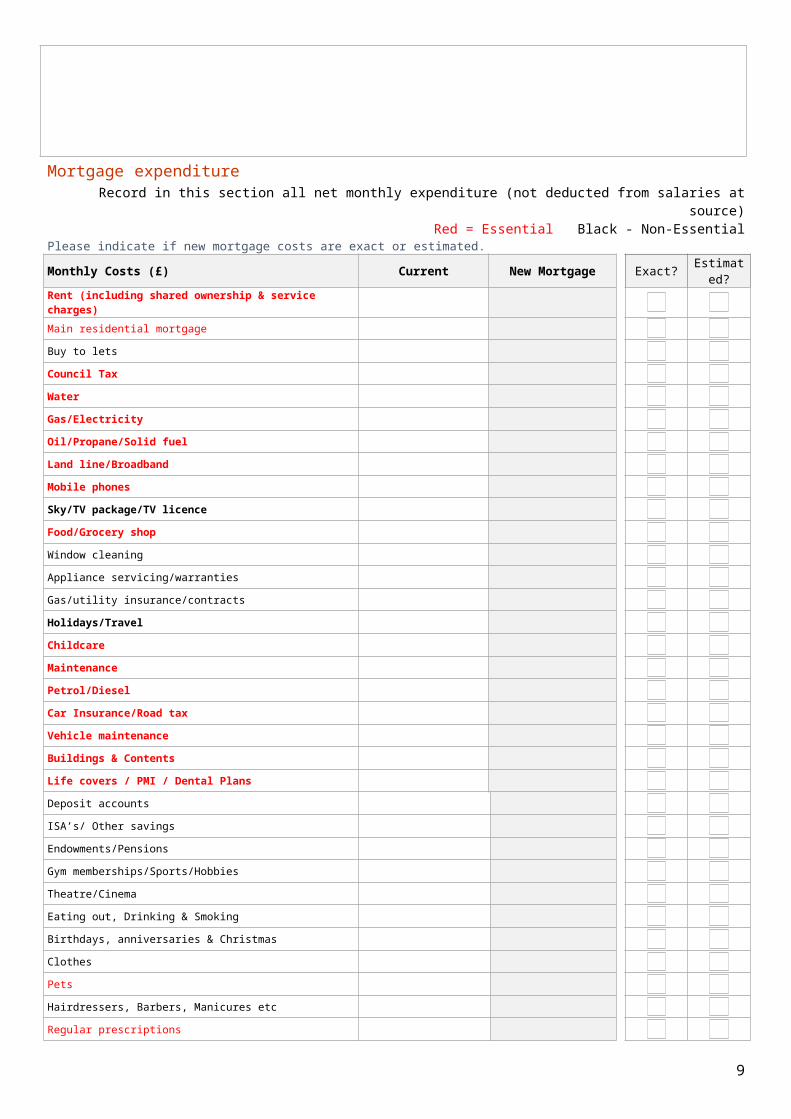

Mortgage expenditure Record in this section all net monthly expenditure (not deducted from salaries at source)

Red = Essential Black - Non-EssentialPlease indicate if new mortgage costs are exact or estimated.Monthly Costs (£) Current New Mortgage Exact? Estimate

d?Rent (including shared ownership & service charges)Main residential mortgage

Buy to lets

Council Tax

Water

Gas/Electricity

Oil/Propane/Solid fuel

Land line/Broadband

Mobile phones

Sky/TV package/TV licence

Food/Grocery shop

Window cleaning

Appliance servicing/warranties

Gas/utility insurance/contracts

Holidays/Travel

Childcare

Maintenance

Petrol/Diesel

Car Insurance/Road tax

Vehicle maintenance

Buildings & Contents

Life covers / PMI / Dental Plans

Deposit accounts

ISA’s/ Other savings

Endowments/Pensions

Gym memberships/Sports/Hobbies

Theatre/Cinema

Eating out, Drinking & Smoking

Birthdays, anniversaries & Christmas

Clothes

Pets

Hairdressers, Barbers, Manicures etc

Regular prescriptions

Catalogue payments

Student loans/tuition cost

7

Ongoing credit commitmentsCharity donationsUnion fees

Pay Day Loans

House maintenance

Other

Monthly emergency fund

Total Essential monthly outgoings

Total Non Essential monthly outgoings

Total Outgoings

Net Income £ Outgoings £

8

Existing financial commitments

Do you have any mortgages? Yes No

Who owns it?

Mortgage 1 Mortgage 2Client 1 Client 1Client 2 Client 2

Other OtherIs this the main mortgage for your current address? Yes No Yes No

Mortgage lender *Mortgage account numberProduct typeInterest rateProduct end dateOutstanding balance

Repayment basisRepayment Repayment

Interest only Interest OnlyPart and part Part and part

Start dateMortgage end dateOutstanding mortgage termCurrent monthly paymentMortgage to be repaid? Yes No Yes NoIf yes, do penalties apply to the mortgage? Yes No Yes No

Penalty amountExpiry date

Who owns it?

Mortgage 3 Mortgage 4Client 1 Client 1Client 2 Client 2

Other OtherMortgage lender *Mortgage account numberProduct typeInterest rateProduct end dateOutstanding balance

Repayment basisRepayment Repayment

Interest only Interest OnlyPart and part Part and part

Start dateMortgage end dateOutstanding mortgage termCurrent monthly payment

Mortgage to be repaid? Yes No Yes NoIf yes, do penalties apply to the mortgage? Yes No Yes No

Penalty amountExpiry date

For Professional Landlords please attach full details. This can be a spreadsheet or other listing. 9

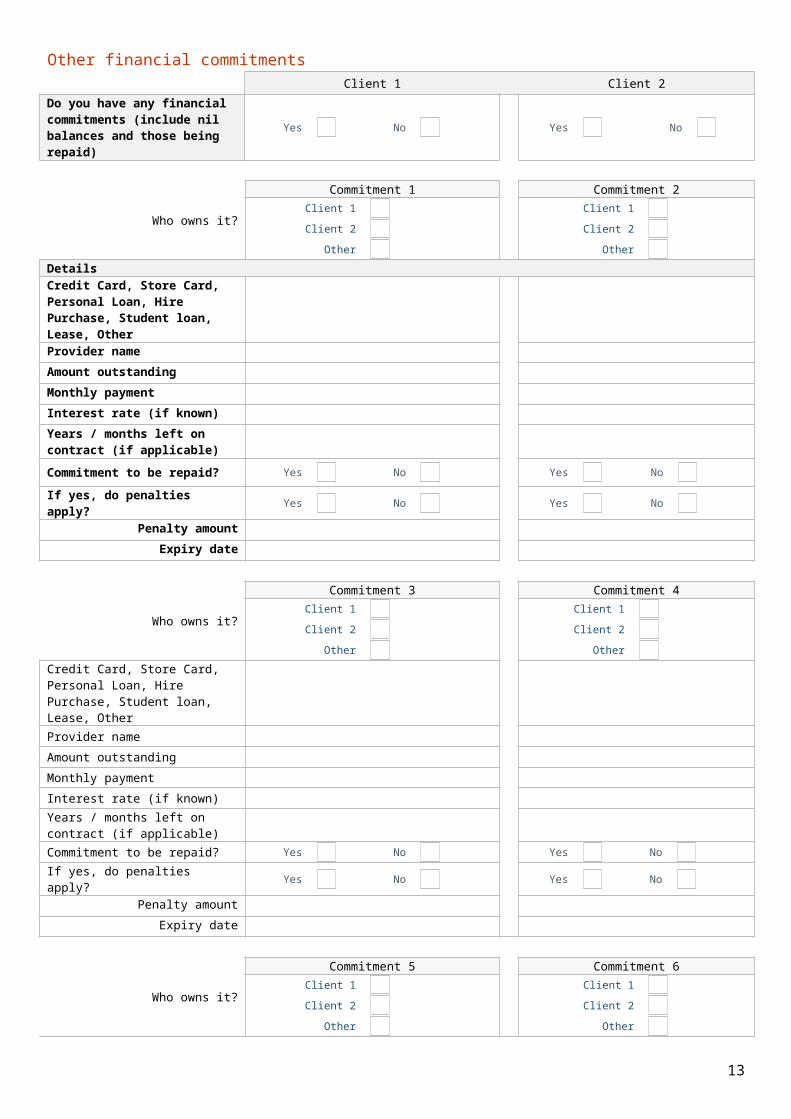

Other financial commitmentsClient 1 Client 2

Do you have any financial commitments (include nil balances and those being repaid)

Yes No Yes No

Who owns it?

Commitment 1 Commitment 2Client 1 Client 1Client 2 Client 2

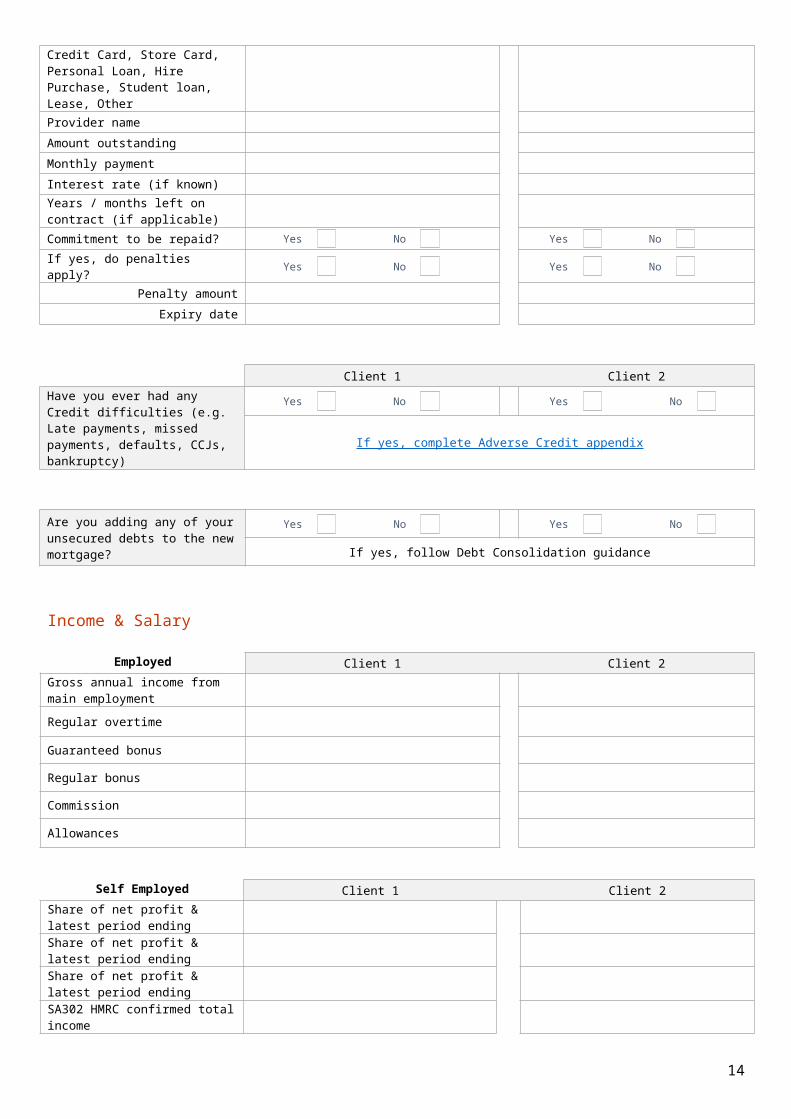

Other OtherDetailsCredit Card, Store Card, Personal Loan, Hire Purchase, Student loan, Lease, OtherProvider nameAmount outstandingMonthly paymentInterest rate (if known)Years / months left on contract (if applicable)Commitment to be repaid? Yes No Yes No

If yes, do penalties apply? Yes No Yes NoPenalty amount

Expiry date

Who owns it?

Commitment 3 Commitment 4Client 1 Client 1Client 2 Client 2

Other OtherCredit Card, Store Card, Personal Loan, Hire Purchase, Student loan, Lease, OtherProvider nameAmount outstandingMonthly paymentInterest rate (if known)Years / months left on contract (if applicable)Commitment to be repaid? Yes No Yes NoIf yes, do penalties apply? Yes No Yes No

Penalty amountExpiry date

Who owns it?

Commitment 5 Commitment 6Client 1 Client 1Client 2 Client 2

Other OtherCredit Card, Store Card, Personal Loan, Hire Purchase, Student loan, Lease, OtherProvider nameAmount outstandingMonthly paymentInterest rate (if known)Years / months left on contract (if applicable)Commitment to be repaid? Yes No Yes NoIf yes, do penalties apply? Yes No Yes No

10

Penalty amountExpiry date

Client 1 Client 2Have you ever had any Credit difficulties (e.g. Late payments, missed payments, defaults, CCJs, bankruptcy)

Yes No Yes No

If yes, complete Adverse Credit appendix

Are you adding any of your unsecured debts to the new mortgage?

Yes No Yes No

If yes, follow Debt Consolidation guidance

Income & Salary

Employed Client 1 Client 2Gross annual income from main employmentRegular overtime

Guaranteed bonus

Regular bonus

Commission

Allowances

Self Employed Client 1 Client 2Share of net profit & latest period endingShare of net profit & latest period endingShare of net profit & latest period endingSA302 HMRC confirmed total income

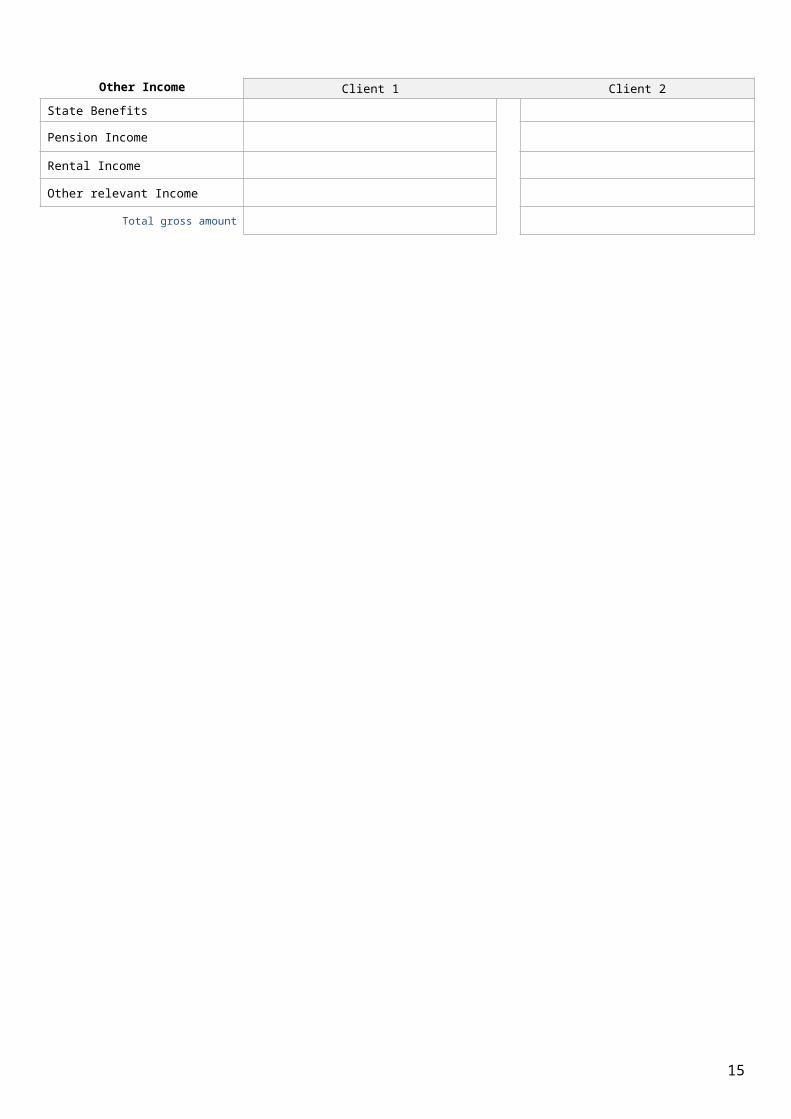

Other Income Client 1 Client 2State Benefits

Pension Income

Rental Income

Other relevant Income

Total gross amount

11

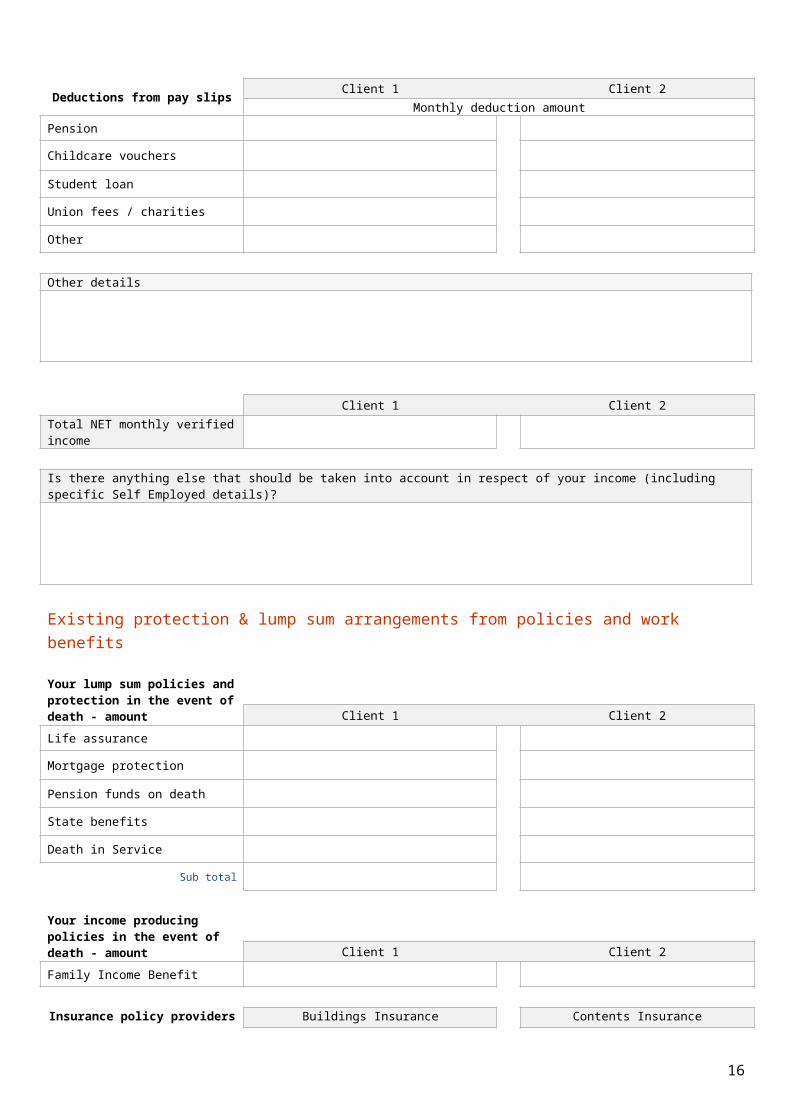

Deductions from pay slips Client 1 Client 2Monthly deduction amount

Pension

Childcare vouchers

Student loan

Union fees / charities

Other

Other details

Client 1 Client 2Total NET monthly verified income

Is there anything else that should be taken into account in respect of your income (including specific Self Employed details)?

Existing protection & lump sum arrangements from policies and work benefits

Your lump sum policies and protection in the event of death - amount Client 1 Client 2Life assurance

Mortgage protection

Pension funds on death

State benefits

Death in Service

Sub total

Your income producing policies in the event of death - amount Client 1 Client 2Family Income Benefit

Insurance policy providers Buildings Insurance Contents Insurance

12

Total available to you from your savings and investments Client 1 Client 2ISAStocks and sharesBank / Building societyOther

Sub total

Total income available to you in the event of being unable to work Client 1 Client 2Monthly sick pay from employerIncome protection policiesAccident, sickness & unemployment policiesState benefits (ESA)Other

Sub total

Total lump sums available in the event of suffering a serious or critical illness Client 1 Client 2Critical illness policiesOther cash

Sub total

Existing Pensions Client 1 Client 2

Pension 1 Pension 1Description ProviderValue Monthly contributionRetirement age

Pension 2 Pension 2Description ProviderValue Monthly contributionRetirement age

Client 1 Client 2Pension 3 Pension 3

13

Description ProviderValue Monthly contributionRetirement age

Purpose of Pensions

Existing Investments Client 1 Client 2

Investment 1 Investment 1Description ProviderValue Regular paymentMaturity End date

Investment 2 Investment 2Description ProviderValue Regular paymentMaturity End date

Investment 3 Investment 3Description ProviderValue Regular paymentMaturity End date

Purpose of Investments

14

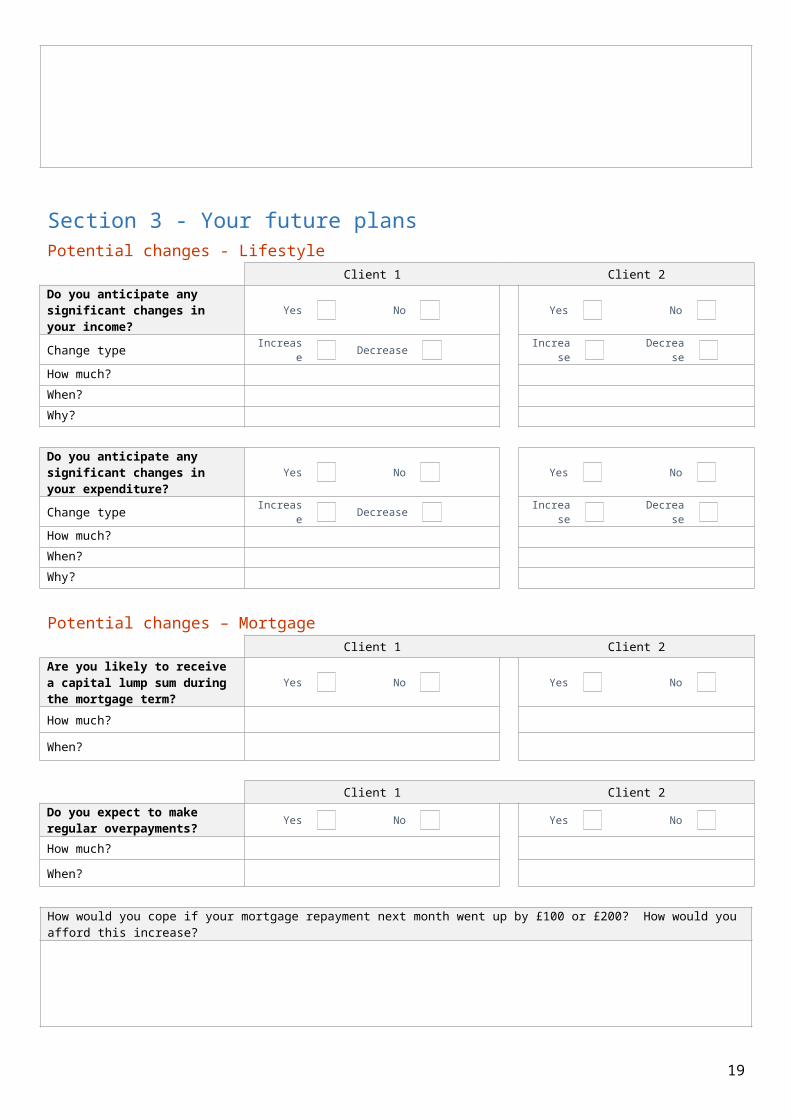

Section 3 - Your future plansPotential changes - Lifestyle

Client 1 Client 2Do you anticipate any significant changes in your income?

Yes No Yes No

Change type Increase Decrease Increase

Decrease

How much?When?Why?

Do you anticipate any significant changes in your expenditure?

Yes No Yes No

Change type Increase Decrease Increase

Decrease

How much?When?Why?

Potential changes – MortgageClient 1 Client 2

Are you likely to receive a capital lump sum during the mortgage term?

Yes No Yes No

How much?

When?

Client 1 Client 2Do you expect to make regular overpayments? Yes No Yes No

How much?When?

How would you cope if your mortgage repayment next month went up by £100 or £200? How would you afford this increase?

How would it affect you if your mortgage repayment changed several times a year? Could you afford this?

Do you want certainty about the amount of mortgage repayment for a period of time? If so, how much and for how long?

15

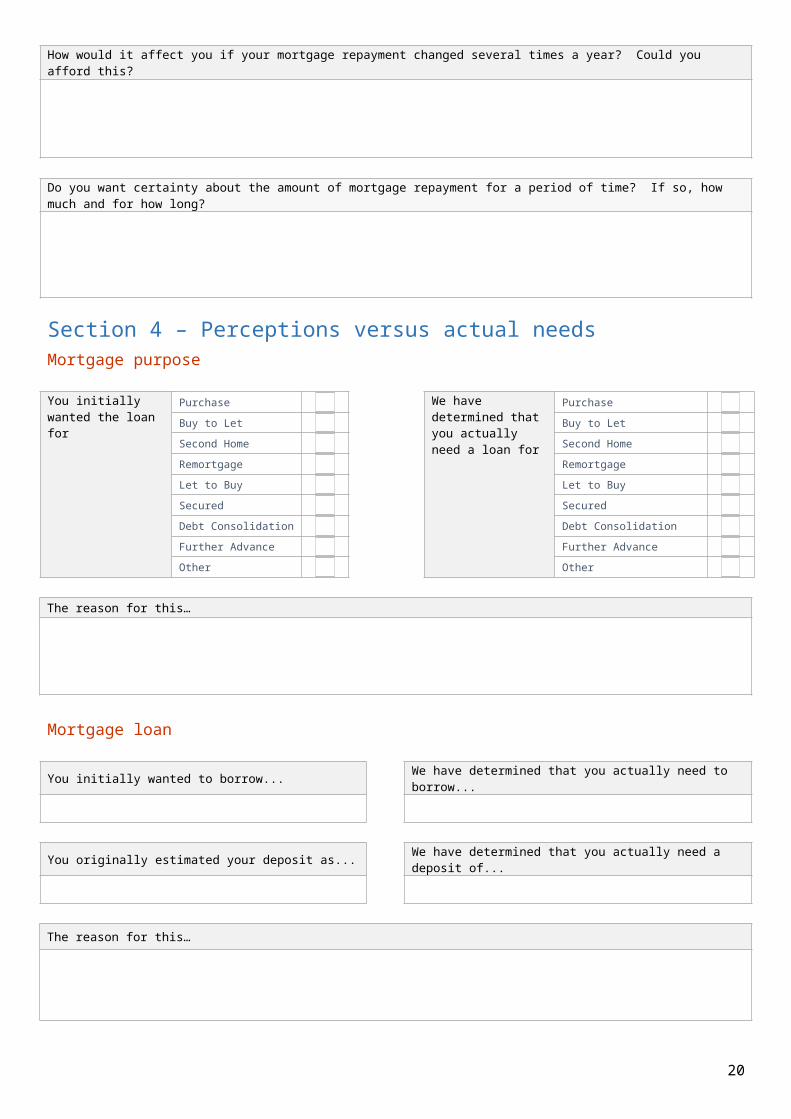

Section 4 – Perceptions versus actual needsMortgage purpose

You initially wanted the loan for

Purchase We have determined that you actually need a loan for

PurchaseBuy to Let Buy to LetSecond Home Second HomeRemortgage RemortgageLet to Buy Let to BuySecured SecuredDebt Consolidation Debt ConsolidationFurther Advance Further AdvanceOther Other

The reason for this…

Mortgage loan

You initially wanted to borrow... We have determined that you actually need to borrow...

You originally estimated your deposit as... We have determined that you actually need a deposit of...

The reason for this…

Mortgage term

Your preferred mortgage term was... We have determined that the most suitable mortgage term for you is...

The reason for this…

16

Mortgage repayment

Your original preferred repayment method was

Repayment We have determined that your most suitable repayment method is

RepaymentInterest Only Interest OnlyPart and Part Part and PartDon’t know

The reason for this…

Your budget

Your initial estimated monthly budget for your mortgage and associated costs was... Your actual monthly budget is...

The reasons for this…

Mortgage Product

Your original preferred mortgage product was

Fixed We have determined that the most suitable mortgage product for you is

Fixed Tracker Tracker Variable Variable Capped Capped Discount Discount Other

OtherNo preference

You initially specified a term for this product as Years

We determined that the most suitable term for this product is

Years

No preference

Don’t know

17

The reason for this…

Mortgage lenders & features

You asked me to include or exclude the following lenders as part of my research...

We agreed to include offers from the following previously excluded lenders…

The reasons for this decision are…

Mortgage features you initially felt were essential to you were (in order priority order, 1 being highest)

We have determined that these are the essential features for your new mortgage (in priority order, 1 being highest)

Low payments in the early years Low payments in the early yearsAssistance with fees Assistance with feesNo extended early repayment charges No extended early repayment chargesA cash lump sum at the outset of the loan

A cash lump sum at the outset of the loan

Ability to make regular overpayments Ability to make regular overpayments Ability to make lump sum payments Ability to make lump sum payments Take advantage of variations in interest rates

Take advantage of variations in interest rates

Stability of payments Stability of payments Linked to Bank of England base rate Linked to Bank of England base rateAbility to budget Ability to budgetFlexible payment arrangements Flexible payment arrangements

The reason for this…

Client 1 Client 2Are you likely to receive a capital lump sum during the mortgage term?

Yes No Yes No

How much?

When?

18

Client 1 Client 2Have you indentified the client as vulnerable?Describe the nature of the vulnerability

Record the additional actions taken to address this vulnerability (e.g. presence of a third party at the meetings)

Explain how the recommendation solution takes this vulnerability into consideration

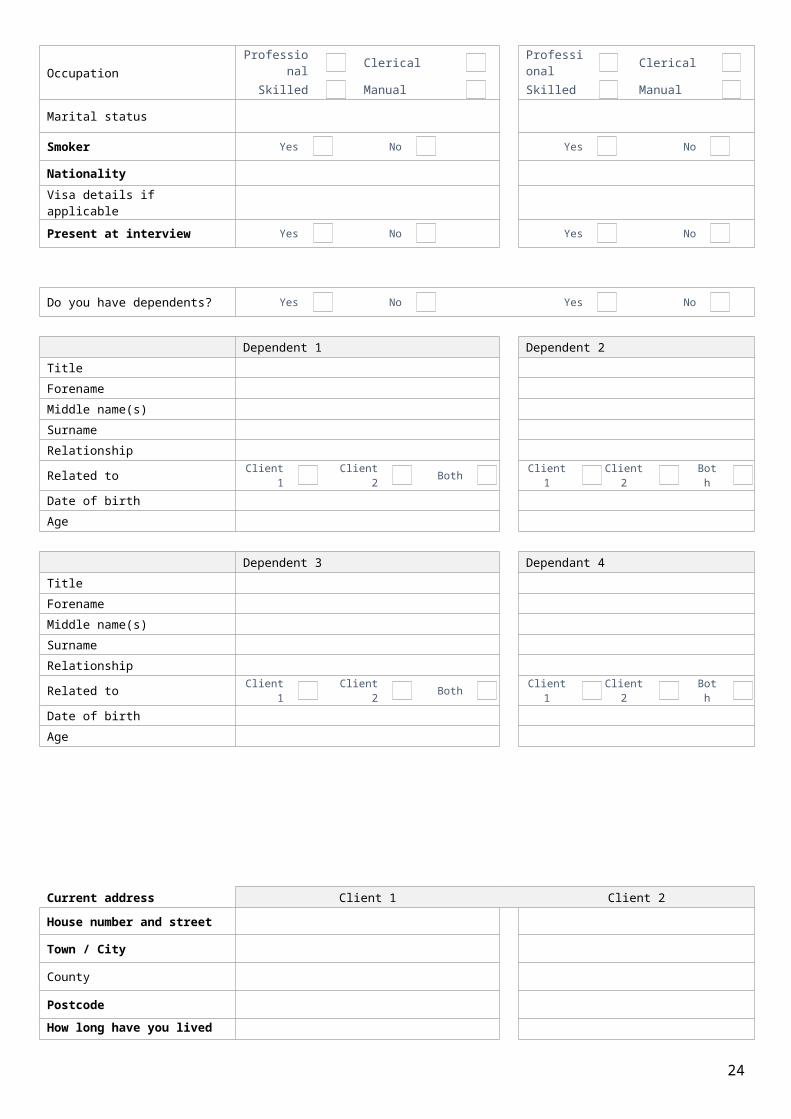

Section 5 – Hard factsPersonal details Client 1 Client 2Title – Mr, Mrs, Miss, Ms, OtherForenameMiddle name(s)SurnamePreferred namePrevious name/Maiden nameDate of name changeDate of birthGender Male Femal

e Male Female

Main employment Status Employed Self Employed

Employed

Self Employed

Contract Other Contract Other

OccupationProfession

al Clerical Professional Clerical

Skilled Manual Skilled Manual

Marital status

Smoker Yes No Yes No

Nationality

Visa details if applicable

Present at interview Yes No Yes No

Do you have dependents? Yes No Yes No

Dependent 1 Dependent 2TitleForenameMiddle name(s)SurnameRelationshipRelated to Client

1 Client 2 Both Client 1 Client 2

Both

Date of birthAge

19

Dependent 3 Dependant 4TitleForenameMiddle name(s)SurnameRelationshipRelated to Client

1 Client 2 Both Client 1 Client 2

Both

Date of birthAge

Current address Client 1 Client 2House number and street

Town / City

County

PostcodeHow long have you lived at this address? (Previous address if less than 3 years)

Residential status

Previous address Client 1 Client 2House number and street

Town / City

County

Postcode

Occupancy typeDate you moved into your previous addressHow long did you live at this address?

Residential status

Homeowner Homeowner Tenant Tenant

Living with family or friends Living with family or friends

New address Client 1 Client 2Present at interview Yes No Yes No

House number and street

Town / City

County

20

Postcode

Residential statusHomeowner Homeowner

Tenant Tenant

Living with family or friends Living with family or friends

21

Employments Client 1 Client 2National insurance numberTax office details

County

Employment status

Employed EmployedSelf employed Self employed

Unemployed UnemployedRetired Retired

Contractor ContractorAgency AgencyStudent Student

House person House personFull time or Part time Full time Part

time Full time Part time

Occupation

Main occupation Yes No Yes No

On probation Yes No Yes No

Probation end date

Preferred retirement date

Employer name

Nature of business

Employer address

Start date

End date

Length of service

Other Employment Client 1 Client 2

Full time or part time Full time Part time Full time Part

timeOccupationMain occupation Yes No Yes No

On probation Yes No Yes No

Probation end datePreferred retirement date

Employer name

Nature of business

Employer address

Start date

End date

Length of service

22

Self Employed Client 1 Client 2

Business nameWhat is the nature of your business / occupationYear established

Partner / Sole Trader PartnerSole

Trader

Partner Sole Trader

What % of the shares in this business do you own?How long have you owned / part owned this business?

Notes

23

Section 6 – Protecting you and your mortgageTell me about your lifestyle? (hobbies, home, holidays, children)

Tell me about plans you have for the future (future house move, jobs, retirement, etc.)

In an IDEAL world, if your income stopped yesterday,

what impact would you want this to have on your

ability to remain in your home?

What things could happen to affect your ability to maintain your mortgage?

What are the CHANCES that any of these things could happen?

(Use Risk Calculator - www.riskreality.co.uk/intrinsic )

What RISKS do you want to resolve, and in what order?

Repay the Mortgage Loan on deathRepay the Mortgage Loan on diagnosis of a Critical Illness

Continue to make mortgage payments on illness, disability or redundancy

Priority Priority Priority(High Medium Low) (High Medium Low) (High Medium Low)

Client 1 Client 1 Client 1

Client 2 Client 2 Client 2

24

Section 7 – Appendices Adverse Credit details

Client 1 Client 2Have you missed more than 2 consecutive credit card or store card payments in the last 3 years?

Yes No Yes No

Details

Are you currently or have you ever been in arrears with your rent, mortgage payments or other loans?

Yes No Yes No

Details

Have you been bankrupt? Yes No Yes No

Details

Have you ever had a County Court Judgement (CCJ) against you?

Yes No Yes No

Details

Have you ever made arrangements with creditors (Individual Voluntary Agreement)?

Yes No Yes No

Details

Have you been declined a mortgage on any property in the last 5 years?

Yes No Yes No

25

Details

Existing Life Protection policiesLife Protection policies Policy 1 Policy 2Owner Client 1 Client 2 Joint Client 1 Client 2 Joint ProviderPolicy type (LTA, DTA, WOL, FIB) Policy Number

Remaining Term

Sum Assured - Life £Lump Sum

£Lump Sum

Per annum Per annum

Sum Assured – Critical Illness Cover (if included)

£Lump Sum

£Lump Sum

Per annum Per annum

Life BasisSingle Life Single Life

Joint Life First Death Joint Life First DeathJoint Life Second Death Joint Life Second Death

Purpose of Policy Lifestyle Protection Lifestyle ProtectionMortgage Protection Mortgage Protection

Written in Trust Yes No Yes No

(If Endowment) – Maturity Value £ £Premium & Frequency £ per £ per

Details of Critical Illness Conditions covered

Existing Standalone Critical Illness policiesStand alone Critical Illness Policies

Policy 1 Policy 2

Owner Client 1 Client 2 Joint Client 1 Client 2 Joint

Policy type

Provider

Policy Number

Remaining Term

Sum Assured - £ £Purpose of Policy Lifestyle Protection Lifestyle Protection

26

Mortgage Protection Mortgage ProtectionPremium & Frequency £ per £ per

Renewal Date

Details of Critical Illness Conditions covered

Existing Mortgage Payment Protection or ASU policies

Mortgage Payment Protection or ASU policies

Policy 1 Policy 2

Owner Client 1 Client 2 Joint Client 1 Client 2 Joint

Policy TypeDisability Disability

Unemployment UnemploymentBoth Both

ProviderPolicy NumberBenefit Amount / FrequencyBenefit PeriodDeferred PeriodBenefit 2 Amount / FrequencyBenefit Period 2

Deferred Period 2Premium & Frequency £ per £ per

Renewal Date

PurposeLifestyle Lifestyle

Mortgage MortgageBoth Both

Existing Private Medical Insurance policiesPrivate Medical Insurance Policy 1 Policy 2

Owner Client 1 Client 2 Joint Client 1 Client 2 Joint

Cover Type

Family FamilySingle Single

Joint JointSingle Parent Single Parent

Employee benefit or Private Cover? Employee Private Yes No

ProviderPremium & Frequency £ per £ per

27

Renewal Date

28

Existing Income Protection policies

Income Protection Policies

Policy 1 Policy 2

Owner Client 1 Client 2 Joint Client 1 Client 2 Joint

Income Protection Income Protection Group Income Protection Group Income Protection

Employers Benefit Employers BenefitMulti Benefit Multi Benefit

ProviderPolicy NumberStart DateBenefit 1 AmountDeferred Period weeks weeksBenefit 2 AmountDeferred Period weeks weeksBenefits Indexed? Yes No Yes NoWaiver of Premium included? Yes No Yes NoFrequency of Benefit PaymentsBenefits payable for

Term in Years Term in YearsUntil Age Until Age

Premium & Frequency £ per £ per

Renewal Date

Purpose Lifestyle LifestyleMortgage Mortgage

Existing Buildings & Contents policiesBuilding & Contents Policy 1 Policy 2

Cover Type Buildings Contents Buildings Content

s

Property Usage

Main Residence Main ResidenceBuy to Let Buy to Let

Overseas Property Overseas PropertyUK holiday home UK holiday home

Unoccupied UnoccupiedAccidental Damage cover included?

Yes No Yes No

Cover Amount £ £

Provider

Policy NumberPremium & Frequency £ per £ per

Renewal Date

29

Section 8 – Key Contact DetailsDetails of Client 1 Details of Client 2Client Name Client Name

Address Address

Email address Email addressHome Telephone

Home Telephone

Mobile MobileWork Telephone

Work Telephone

Details of Accountant Details of Solicitor

Name of Firm Name of FirmContact Name Contact Name

Address Address

Email address Email address

Telephone Telephone

Mobile Mobile

Website Website

Details of Introducer Other

Name of Firm Name of FirmContact Name Contact Name

Address Address

Email address Email address

Telephone Telephone

Mobile Mobile

Website Website

30

Related Documents