Secondary Mortgage Markets The Agencies Institutions G innieM ae: G overnm entN ationalM ortgageA ssociation Fannie M ae: FederalNationalM ortgageA ssociation Freddie M ac: FederalH om e Loan M ortgage Corporation G innie M ae isa governm entow ned m ortgage association w ithin the U S D epartm entofH ousing and U rban D evelopm ent(H U D). Fannie M ae and Freddie M ac are privately owned, Federally chartered institutions. They are collectively know sas G overnm entSponsored Enterprises(G SEs).

Secondary Mortgage Markets The Agencies.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Secondary Mortgage MarketsThe Agencies

Institutions

Ginnie Mae: Government National Mortgage Association Fannie Mae: Federal National Mortgage Association Freddie Mac: Federal Home Loan Mortgage Corporation

Ginnie Mae is a government owned mortgage association within the US Department of Housing and Urban Development (HUD). Fannie Mae and Freddie Mac are privately owned, Federally chartered institutions. They are collectively knows as Government Sponsored Enterprises (GSEs).

Secondary Mortgage Markets The Agencies

Institutions The National Housing Act of 1934 (and subsequent amendments)

Created the Federal Housing Administration (FHA) Title II of the Act provides insurance for home loans Title III of the Act chartered mortgage associations that buy and sell insured

FHA (and later) Veterans Administration (VA) loans The Federal National Mortgage Association (FNMA) was created in 1938 In 1968, FNMA was separated into two entities:

1. The Government National Mortgage Assocation (GNMA),Ginnie Mae

2. The Federal National Mortgage Association (FNMA), Fannie Mae

Secondary Mortgage Markets The Agencies

Ginnie Mae www.ginniemae.gov

Guarantees pools of FHA/VA mortgages issued by private lenders

Unconditionally guarantees GNMA investors timely payment of interest

and principal First GNMA MBS issued in Dallas in 1970, retired in 2000 Reached $2 trillion of cumulative issuance in mortgage backed securities

(MBS) on 11/20/2002 Has provided financing for over 27 million households in the US since

its creation in 1968 GNMA obligations are backed by the full faith and credit of the US

Secondary Mortgage Markets The Agencies

Fannie Mae www.fanniemae.com

Chartered by Congress in 1938 to provide a secondary market for

FHA/VA mortgages Partitioned into a separate, privately owned, federally chartered, mortgage

association in 1968, went public in 1970; recently had problems with financial statements (accounting for interest rate hedges using derivatives).

Authorized to purchase conventional (privately insured) mortgages in

1970 Traded on NYSE as FNM and is part of SNP 500. Has provided housing finance for over 58 million US households since

1968.

Secondary Mortgage Markets The Agencies

Freddie Mac www.freddiemac.com

Chartered by Congress in 1970 by the Federal Home Loan Mortgage

Corporation Act (the "Freddie Mac Act") to develop a conventional secondary market; traded on NYSE as FRE.

Buys conventional, graduated payment, and adjustable rate (privately

insured, conforming) mortgages and sells mortgage backed securities Optional Delivery Program: Freddie agrees in advance to purchase a

specified dollar amount of loans at a specified yield. Introduced SWAP Program in 1981: Freddie buys mortgages and

simultaneously sells securities backed by the same mortgages (MBSs more liquid)

Introduced Collateralized Mortgage Obligations (CMOs) in 1983: CMOs

are structured mortgage backed bonds that create different pay classes, or tranches.

Secondary Mortgage Markets The Agencies

Freddie Mac www.freddiemac.com

Freddie Mac's statutory purposes are:

To provide stability in the secondary market for residential mortgages To respond appropriately to the private capital market To provide ongoing assistance to the secondary market for residential markets

(including mortgages on housing for low- and moderate-income families involving a reasonable economic return that may be less than the return earned on other activities)

To promote access to mortgage credit throughout the United States (including

central cities, rural areas and underserved areas) by increasing the liquidity of mortgage investments and improving the distribution of investment capital available for residential mortgage financing.

Secondary Mortgage Markets Non-Agencies

Ginnie Mae, Fannie Mae, and Freddie Mac (The Agencies) concentrate their mortgage packaging activity on conforming, "A" borrower credit rated, owner-occupied, 1-to-4 family property mortgages.

The private sector issues MBSs for "non-conforming" loans

A mortgage can be non-conforming for a variety of reasons:

1. Jumbo loans: loan amounts above the conforming loan limit (currently $417,000 in most states)

2. Investor loans: 1-to-4 family property mortgages for non-owner-occupied homes; single-family properties held for investment

3. Inadequate documentation (e.g. self-employed)

4. Subprime: "B" and "C" rated borrowers (FICO < 620)

5. Home equity loans

6. Second mortgages

7. Manufactured housing mortgages

Secondary Mortgage Markets Non-Agencies

Major Issuers Jumbo Loans: Countrywide, Norwest, Residential Funding Corporation,

GE Capital, Chase and Citicorp Mfg. Investor Loans (and limited documentation mortgages): Indy Mac,

Norwest and Residential Accredit Loans, Inc. Subprime Loans: Residential Assets Securities Corporation, Option One,

Long Beach Home Equity Loans: EquiCredit, Advanta, United Companies Financial

Corporation, Money Store, ContiMortgage, Green Tree Manufactured Housing: Green Tree, GreenPoint, Associates First,

Vanderbilt, Oakwood Source: Salomon Smith Barney

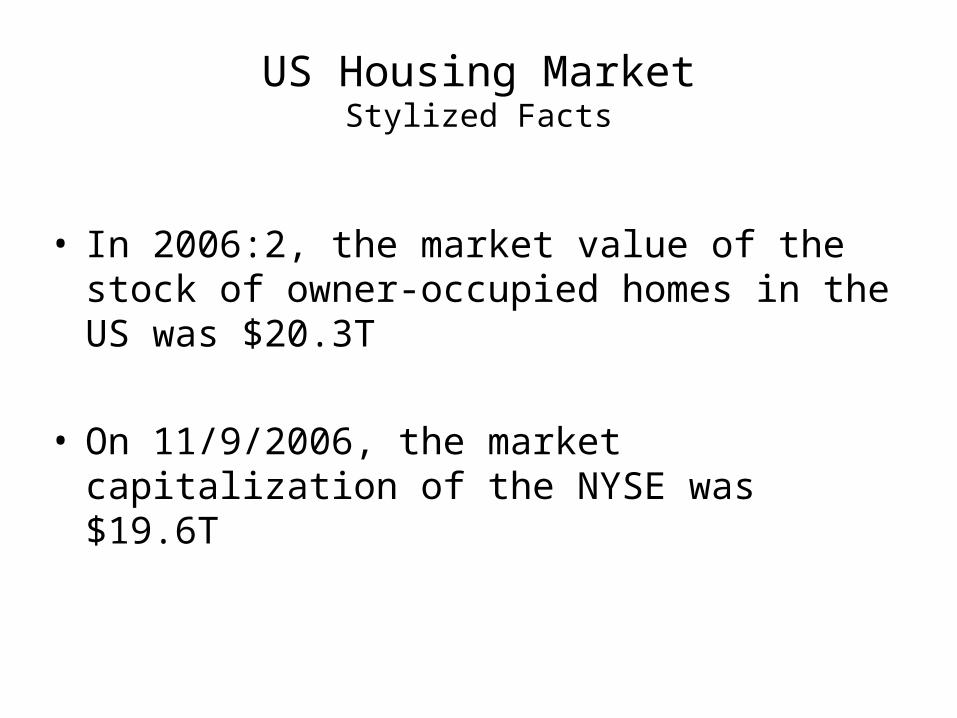

US Housing MarketStylized Facts

• In 2006:2, the market value of the stock of owner-occupied homes in the US was $20.3T

• On 11/9/2006, the market capitalization of the NYSE was $19.6T

Secondary Mortgage Markets Stylized Facts

A Statistical Summary of Housing and Mortgage Finance Activities

By

Fannie Mae

2007

Source: www.fanniemae.com

Secondary Mortgage Markets Stylized Facts

The US National Debt: Marketable and Intragovernmental

Residential Mortgage Debt Outstanding by Property Type

Residential Mortgage Total Credit Risk

Residential Mortgage Credit Risk: Credit Guarantee

Residential Mortgage Credit Risk: Whole Loans

Secondary Market Activity

Agency Activity

US National Debt: 1990-2006

0.0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

Year

Bill

ion

s o

f U

SD

US National Debt

US Intragov't Debt

Total US Govt Debt

Residential Mortgage

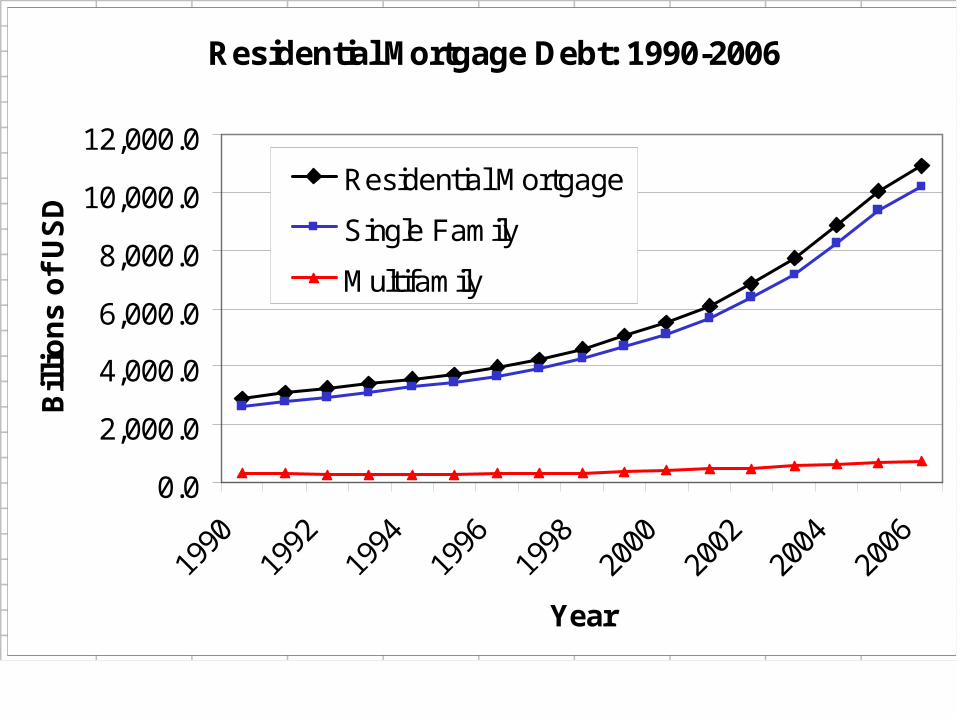

Residential Mortgage Debt: 1990-2006

0.0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

Year

Bil

lio

ns

of

US

D

Residential Mortgage

Single Family

Multifamily

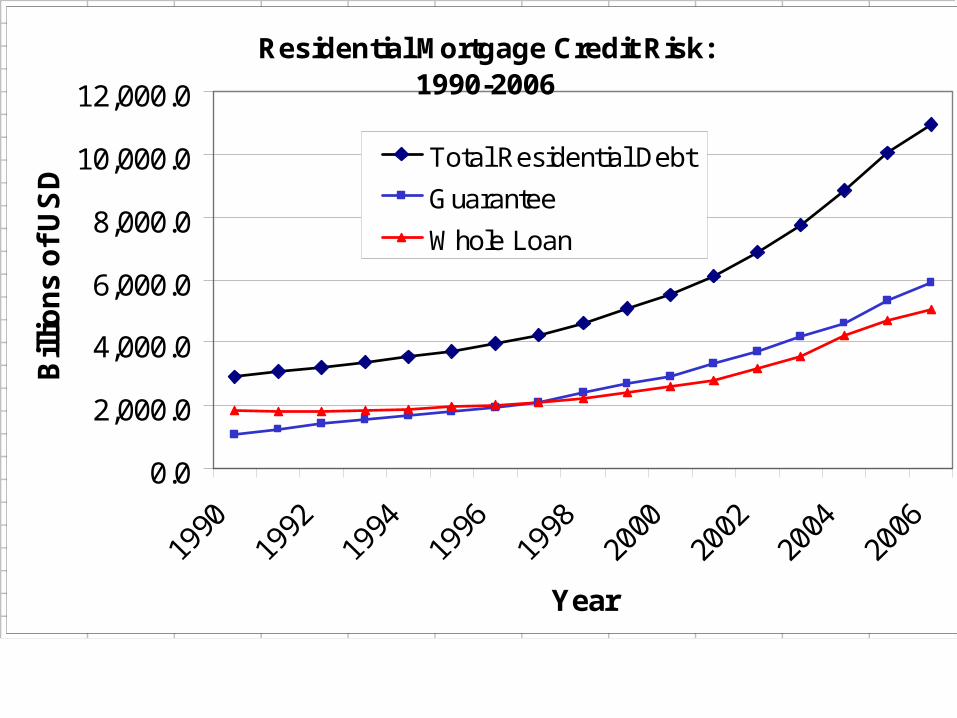

Residential Mortgage Credit Risk: 1990-2006

0.0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

Year

Bill

ion

s o

f U

SD

Total Residential Debt

Guarantee

Whole Loan

Residential Mortgage Credit Risk: Guarantees

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

7,000.0

Year

Bill

ion

s o

f U

SD

Total

Fannie

Freddie

Ginnie

Private

Residential Mortgage Credit Risk: Whole Loans

0.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

Year

Bil

lio

ns

of

US

D Total

Fannie Mae

Freddie Mac

Commercial Banks

Savings Institutions

Others

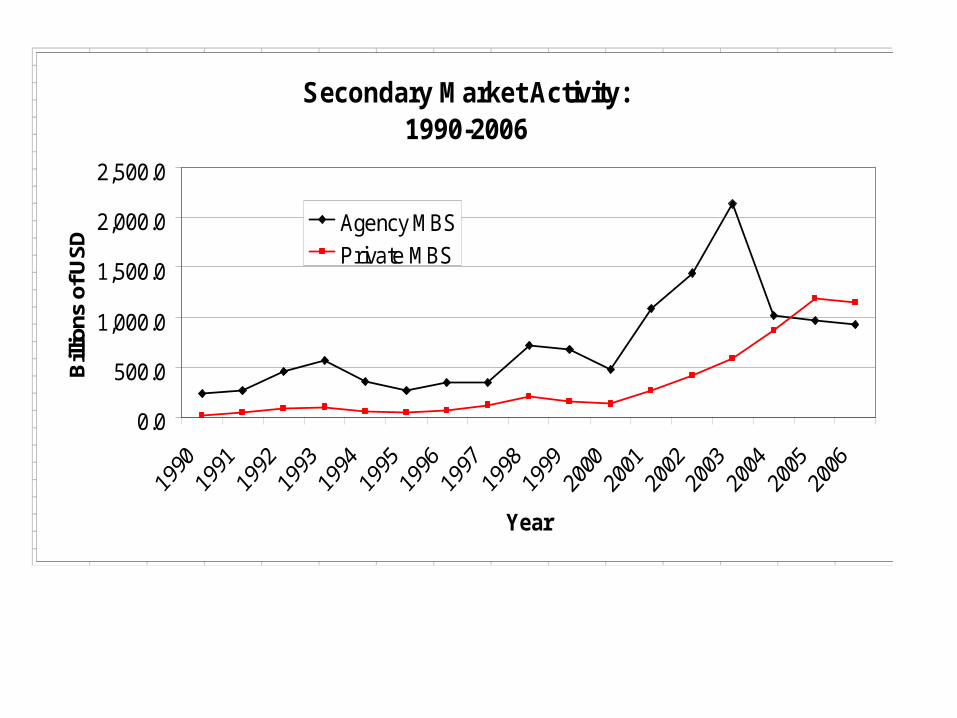

Secondary Market Activity: 1990-2006

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

Year

Bill

ions

of U

SD

Agency MBSPrivate MBS

Agency Secondary Market Activity:1990-2007

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

Year

Bill

ion

s o

f U

SD Total

Fannie

Freddie

GNMA

Secondary Mortgage Markets The Current Debate

Government Bestowed GSE Benefits

GSEs can borrow directly from the US Treasury (though they don't) Capital markets trade GSE debt as if it is guaranteed by the US govt

(it isn’t) GSEs are exempt from state and local taxes (and other regulations)

effectively lowering GSEs operating costs GSE MBS issues exempt from SEC registration and disclosure

requirements (and consequently avoid registration fees) The Uniform Securities Disclosure Act (H.R. 4071), introduced on

March 20, 2002, would repeal Fannie's and Freddie's exemptions from SEC's registration and disclosure requirements.

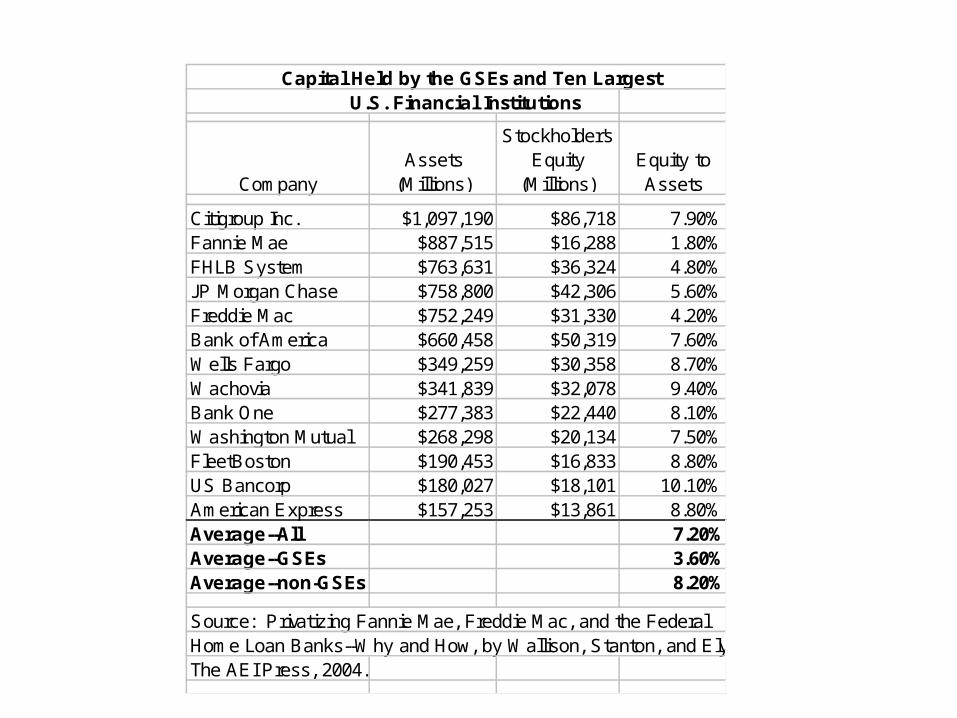

Capital Held by the GSEs and Ten Largest U.S. Financial Institutions

CompanyAssets

(Millions)

Stockholder's Equity

(Millions)Equity to Assets

Citigroup Inc. $1,097,190 $86,718 7.90%Fannie Mae $887,515 $16,288 1.80%FHLB System $763,631 $36,324 4.80%JP Morgan Chase $758,800 $42,306 5.60%Freddie Mac $752,249 $31,330 4.20%Bank of America $660,458 $50,319 7.60%Wells Fargo $349,259 $30,358 8.70%Wachovia $341,839 $32,078 9.40%Bank One $277,383 $22,440 8.10%Washington Mutual $268,298 $20,134 7.50%FleetBoston $190,453 $16,833 8.80%US Bancorp $180,027 $18,101 10.10%American Express $157,253 $13,861 8.80%Average--All 7.20%Average--GSEs 3.60%Average--non-GSEs 8.20%

Source: Privatizing Fannie Mae, Freddie Mac, and the FederalHome Loan Banks--Why and How, by Wallison, Stanton, and ElyThe AEI Press, 2004.

Secondary Mortgage Markets The Current Debate

The GSE Response

GSEs lower the cost of homeownership by reducing interest rates Proof: 25-40bp spread between jumbo and conforming loan

rates Secondary mortgage market economics require a few large

institutions to take advantage of economies of scale, diversify risk, etc.

HUD mandated GSE housing goals have increased low-income

homeownership Low equity loan programs have made homeownership more

accessible

Secondary Mortgage MarketsMortgage Backed Securities

Pass-through securities: investors receive a pro-rata share of the

interest (net of guarantee and servicing fees) and principal on the underlying mortgages

1. Standard: P & I passed through monthly 2. Modified: P & I passed through quarterly, semi-annually,

annually

Mortgage-backed bonds: principal repaid from mortgages deposited in a sinking fund and repaid to investors in predetermined amounts; interest obligations paid without regard to interest repaid on mortgages

Mortgage pay-through bonds: a hybrid security containing elements of

pass-throughs and mortgage-backed bonds. Like a pass-through, these bonds pass-through principal paid on the underlying mortgages. Like a bond, these securities are debt obligations of the issuer, who pays interest based on the bond's coupon and who retains ownership of the mortgage pool.

Secondary Mortgage MarketsMortgage Backed Securities

Single Class: mortgage loans are packaged into a security where each

investor receives a pro-rata share of all principal (scheduled amortization and unscheduled prepayments) and interest (net of guarantee and servicer fees) paid by the underlying mortgages.

Multiple Class: a mortgage-backed security with different pay classes.

Each pay class, or tranche, is separately tradeable.

Real Estate Mortgage Investment Conduits (REMICs) and Collateralized Mortgage Obligations (CMOs) create pay classes with different speeds of principal repayment. The fastest pay class receives coupon interest plus all repaid principal. Most other pay classes receive only coupon interest while the fastest pay class receives all the principal repayment. These MBSs frequently have a zero-coupon tranche.

Stripped Mortgage Backed Security (SMBS): have pay classes that

separate interest cash flows (IO) from principal cash flows (PO).

Secondary Mortgage Markets

GNMA Mortgage Backed Securities

GNMA I

Modified pass throughs

Based on single-issuer pools

Minimum pool $1 million

Minimum certificate $25,000

Underlying mortgages have same (or similar) contract interest rates

GNMA I Coupon 50 basis points less than mortgage interest rate

1. 6 basis points for GNMAs unconditional guarantee of timely payment of interest and principal

2. 44 basis points for servicer

Secondary Mortgage Markets

GNMA Mortgage Backed Securities

GNMA II

Introduced in 1983

MBS coupon rate 50-150 bp below mortgage interest rate

Permits multiple issuers

Permits adjustable rate mortgages

Pays investors on 20th of each month

As of March 20, 2002, all Ginnie Mae Securities settled through the Federal Reserve

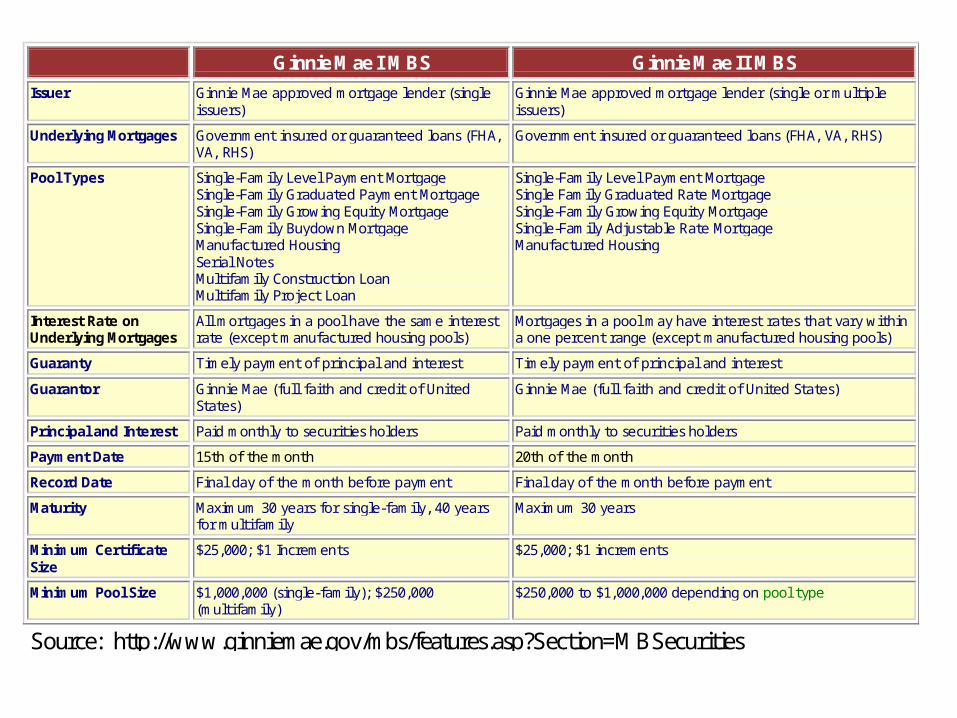

Ginnie Mae I MBS Ginnie Mae II MBS Issuer Ginnie Mae approved mortgage lender (single

issuers) Ginnie Mae approved mortgage lender (single or multiple issuers)

Underlying Mortgages Government insured or guaranteed loans (FHA, VA, RHS)

Government insured or guaranteed loans (FHA, VA, RHS)

Pool Types Single-Family Level Payment Mortgage Single-Family Graduated Payment Mortgage Single-Family Growing Equity Mortgage Single-Family Buydown Mortgage Manufactured Housing Serial Notes Multifamily Construction Loan Multifamily Project Loan

Single-Family Level Payment Mortgage Single Family Graduated Rate Mortgage Single-Family Growing Equity Mortgage Single-Family Adjustable Rate Mortgage Manufactured Housing

Interest Rate on Underlying Mortgages

All mortgages in a pool have the same interest rate (except manufactured housing pools)

Mortgages in a pool may have interest rates that vary within a one percent range (except manufactured housing pools)

Guaranty Timely payment of principal and interest Timely payment of principal and interest Guarantor Ginnie Mae (full faith and credit of United

States) Ginnie Mae (full faith and credit of United States)

Principal and Interest Paid monthly to securities holders Paid monthly to securities holders Payment Date 15th of the month 20th of the month Record Date Final day of the month before payment Final day of the month before payment Maturity Maximum 30 years for single-family, 40 years

for multifamily Maximum 30 years

Minimum Certificate Size

$25,000; $1 Increments $25,000; $1 increments

Minimum Pool Size $1,000,000 (single-family); $250,000 (multifamily)

$250,000 to $1,000,000 depending on pool type

Source: http://www.ginniemae.gov/mbs/features.asp?Section=MBSecurities

Secondary Mortgage Markets

Fannie Mae Mortgage Backed Securities

Mortgage Pass-Through Certificates. The mortgages are held in Trust on behalf of Fannie Mae. Fannie Mae guarantees timely payment of principal and interest; this

guarantee IS NOT BACKED BY THE FULL FAITH AND CREDIT OF THE U.S. GOVERNMENT.

Minimum certificate $1,000. Makes distributions to certificate holders on the 25th of each month.

Secondary Mortgage Markets

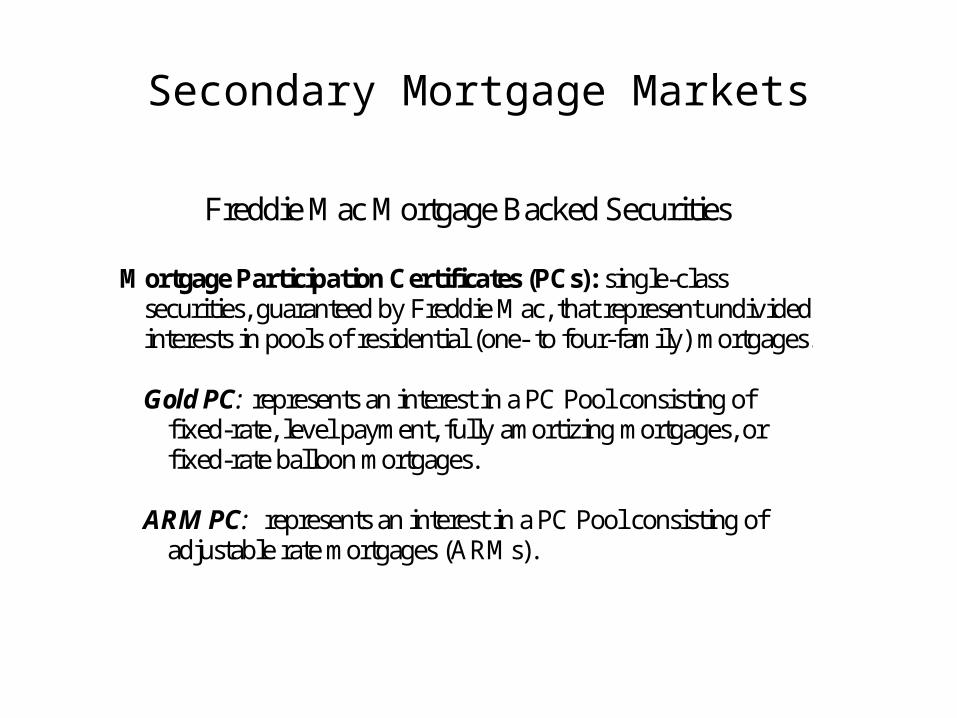

Freddie Mac Mortgage Backed Securities

Mortgage Participation Certificates (PCs): single-class securities, guaranteed by Freddie Mac, that represent undivided interests in pools of residential (one- to four-family) mortgages.

Gold PC: represents an interest in a PC Pool consisting of

fixed-rate, level payment, fully amortizing mortgages, or fixed-rate balloon mortgages.

ARM PC: represents an interest in a PC Pool consisting of

adjustable rate mortgages (ARMs).

Secondary Mortgage Markets

Freddie Mac Mortgage Backed Securities

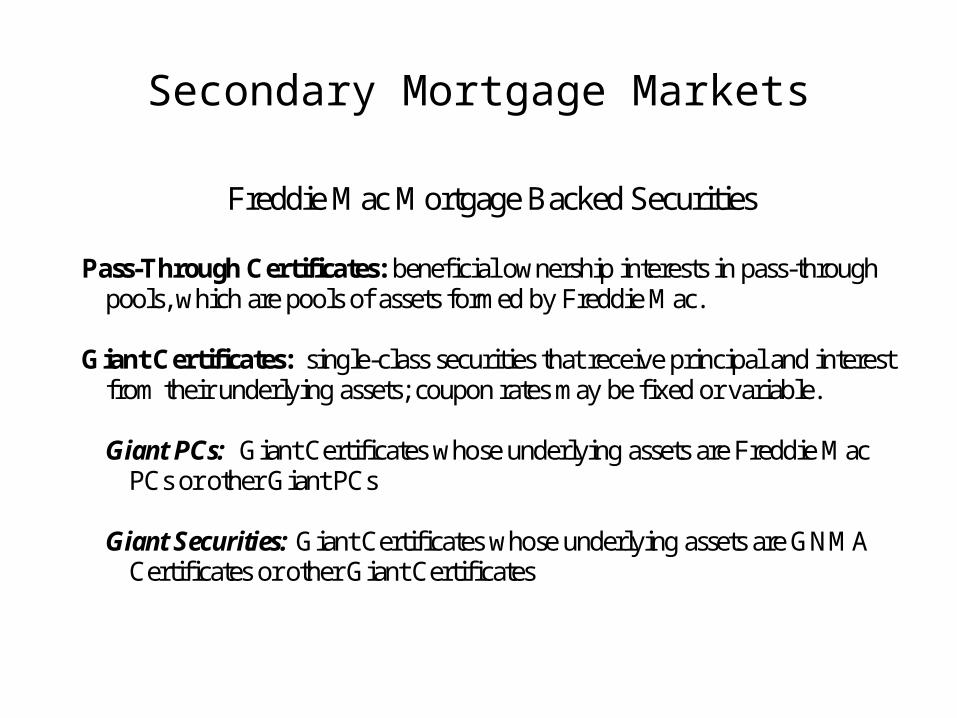

Pass-Through Certificates: beneficial ownership interests in pass-through pools, which are pools of assets formed by Freddie Mac.

Giant Certificates: single-class securities that receive principal and interest

from their underlying assets; coupon rates may be fixed or variable.

Giant PCs: Giant Certificates whose underlying assets are Freddie Mac PCs or other Giant PCs

Giant Securities: Giant Certificates whose underlying assets are GNMA

Certificates or other Giant Certificates

Secondary Mortgage Markets

Freddie Mac Mortgage Backed Securities Striped Giant Certificates: consist of two or more classes that receive

principal only, interest only or both principal and interest from the underlying asset. Each series is backed by a single Giant Certificate

Modifiable and Combinable Securities (MACS): Striped Giant Securities

are issued in series consisting of one interest only class, one principal only class, and multiple classes that receive both principal and interest with different class coupons, ranging from deep discount to high premium coupons.

Structured Pass-Through Certificates (SPCs): are issued in series

consisting of one or more classes. Each class receives payment from one or more assets. The assets are usually REMIC classes issued by Freddie Mac or another party.

Secondary Mortgage MarketsPricing MBS

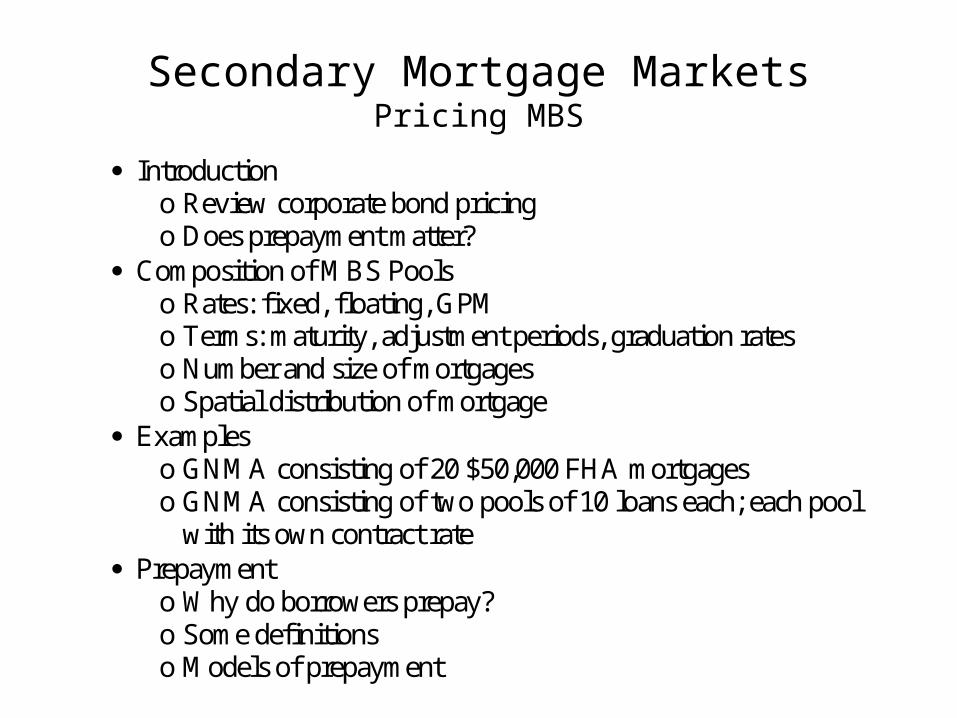

Introduction o Review corporate bond pricing o Does prepayment matter?

Composition of MBS Pools o Rates: fixed, floating, GPM o Terms: maturity, adjustment periods, graduation rates o Number and size of mortgages o Spatial distribution of mortgage

Examples o GNMA consisting of 20 $50,000 FHA mortgages o GNMA consisting of two pools of 10 loans each; each pool

with its own contract rate Prepayment

o Why do borrowers prepay? o Some definitions o Models of prepayment

Secondary Mortgage MarketsPricing MBS

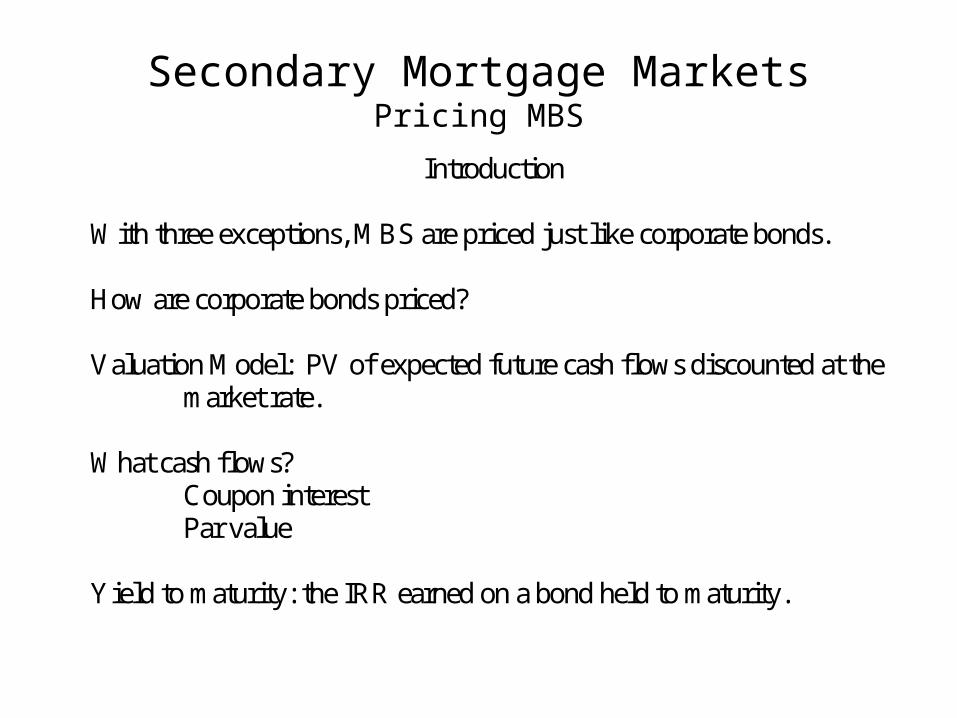

Introduction

With three exceptions, MBS are priced just like corporate bonds. How are corporate bonds priced? Valuation Model: PV of expected future cash flows discounted at the market rate. What cash flows? Coupon interest Par value Yield to maturity: the IRR earned on a bond held to maturity.

Secondary Mortgage MarketsPricing MBS

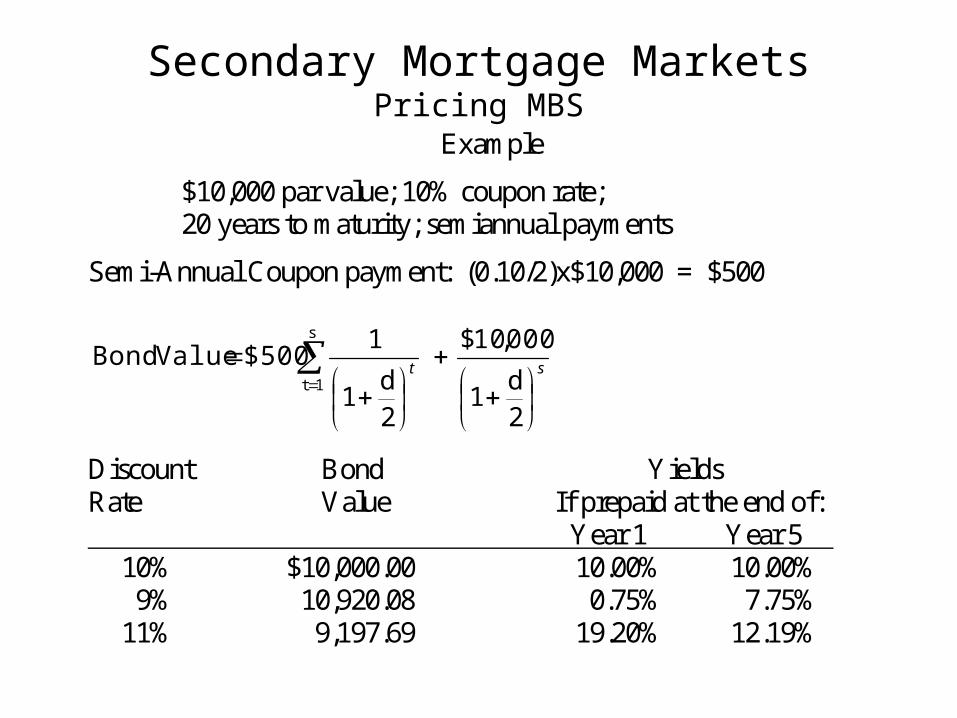

Example

$10,000 par value; 10% coupon rate; 20 years to maturity; semiannual payments

Semi-Annual Coupon payment: (0.10/2)x$10,000 = $500

st

2d

1

000,10$

2d

1

1$500 Value Bond

s

1t

Discount Bond Yields Rate Value If prepaid at the end of: Year 1 Year 5 10% $10,000.00 10.00% 10.00% 9% 10,920.08 0.75% 7.75% 11% 9,197.69 19.20% 12.19%

Secondary Mortgage MarketsPricing MBS

Exceptions

MBS pass through principal (as well as interest) Underlying mortgages in the pool may not have the same rate,

terms, etc…

MBSs offer little (no?) call protection: prepayment of underlying (single-family) mortgages usually permitted at any time, without prepayment penalty

So, how do you price MBS?

o Expected cash flows? o Discount rate?

Secondary Mortgage MarketsPricing MBS

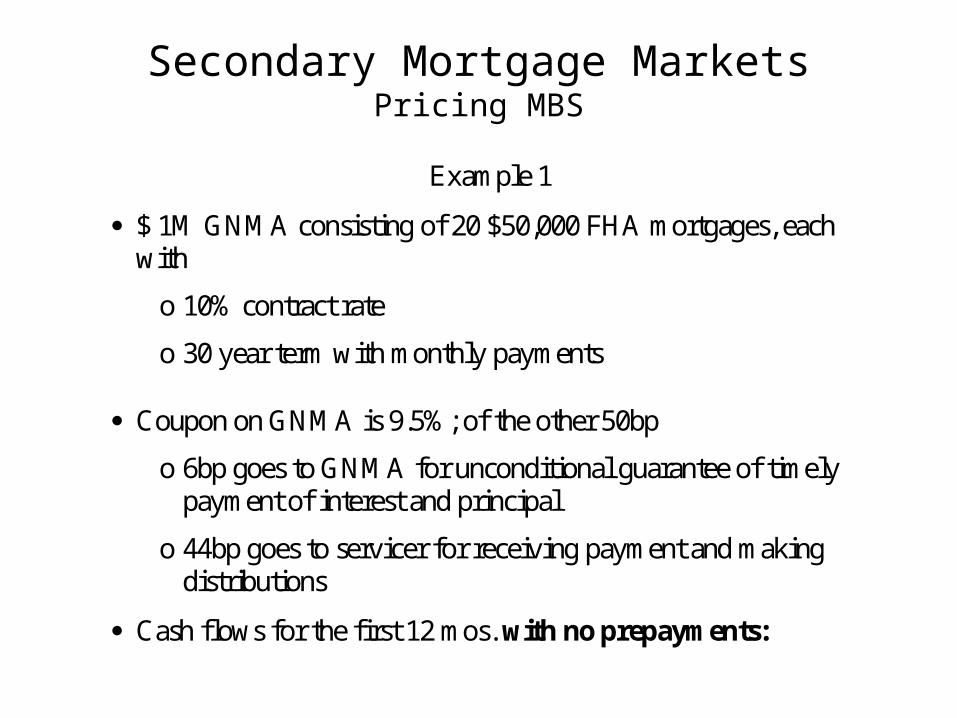

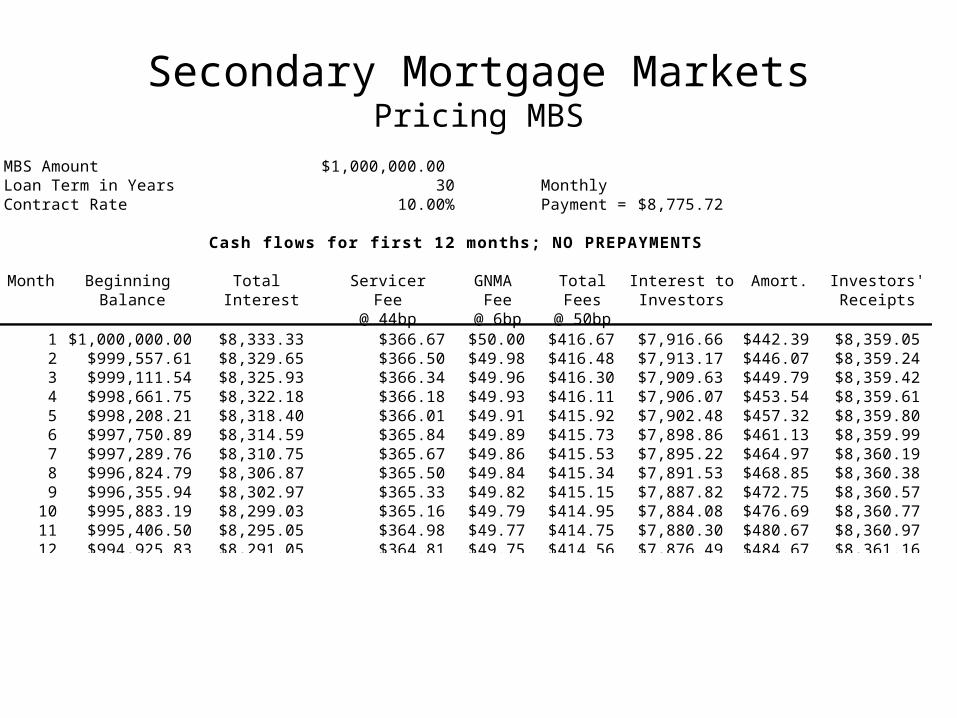

Example 1

$ 1M GNMA consisting of 20 $50,000 FHA mortgages, each with

o 10% contract rate

o 30 year term with monthly payments

Coupon on GNMA is 9.5%; of the other 50bp

o 6bp goes to GNMA for unconditional guarantee of timely payment of interest and principal

o 44bp goes to servicer for receiving payment and making distributions

Cash flows for the first 12 mos. with no prepayments:

Secondary Mortgage MarketsPricing MBS

MBS Amount $1,000,000.00Loan Term in Years 30 MonthlyContract Rate 10.00% Payment = $8,775.72

Cash flows for first 12 months; NO PREPAYMENTS

Month Beginning Total Servicer GNMA Total Interest to Amort. Investors'Balance Interest Fee Fee Fees Investors Receipts

@ 44bp @ 6bp @ 50bp 1 $1,000,000.00 $8,333.33 $366.67 $50.00 $416.67 $7,916.66 $442.39 $8,359.052 $999,557.61 $8,329.65 $366.50 $49.98 $416.48 $7,913.17 $446.07 $8,359.243 $999,111.54 $8,325.93 $366.34 $49.96 $416.30 $7,909.63 $449.79 $8,359.424 $998,661.75 $8,322.18 $366.18 $49.93 $416.11 $7,906.07 $453.54 $8,359.615 $998,208.21 $8,318.40 $366.01 $49.91 $415.92 $7,902.48 $457.32 $8,359.806 $997,750.89 $8,314.59 $365.84 $49.89 $415.73 $7,898.86 $461.13 $8,359.997 $997,289.76 $8,310.75 $365.67 $49.86 $415.53 $7,895.22 $464.97 $8,360.198 $996,824.79 $8,306.87 $365.50 $49.84 $415.34 $7,891.53 $468.85 $8,360.389 $996,355.94 $8,302.97 $365.33 $49.82 $415.15 $7,887.82 $472.75 $8,360.57

10 $995,883.19 $8,299.03 $365.16 $49.79 $414.95 $7,884.08 $476.69 $8,360.7711 $995,406.50 $8,295.05 $364.98 $49.77 $414.75 $7,880.30 $480.67 $8,360.9712 $994,925.83 $8,291.05 $364.81 $49.75 $414.56 $7,876.49 $484.67 $8,361.16

Secondary Mortgage MarketsPricing MBS

Prepayment

Why Do Homeowners Prepay their Mortgages?

1. Financial incentives: market rate < contract rate 2. Relocation: change jobs

3. Change in housing consumption

a. Want larger house b. Want smaller house c. Change location (suburbs to city or vice versa)

4. Disaster losses: property destroyed 5. Mortgage default

Secondary Mortgage MarketsPricing MBS

Some Definitions

Pool Factor: the ratio of the remaining principal balance of a pool to the original principal amount of the entire pool.

Mortgage Balance (of a pass through): the ratio of the remaining

principal balance to the original loan amounts of the outstanding mortgages.

Unconditional Probability of Prepayment (in period t): the ratio of

the number of mortgages that prepay in period t to the number of mortgages originally in the pool.

Conditional Probability of Prepayment (in period t): the ratio of the

number of mortgages that prepay in period t to the number of mortgage in the pool at the beginning of the period.

Secondary Mortgage MarketsPricing MBS

Some Definitions

Weighted Average Rate: the average mortgage interest rate, weighted by the outstanding principal balances of the outstanding mortgages.

Weighted Average Maturity: the average loan maturity, weighted by the outstanding principal balances of the outstanding mortgages.

Weighted Average Life: the average amount of time that a dollar of principal is expected to be outstanding; the weighted average time to repayment of all principal payouts using the principal repayments as weights.

Half Life: the amount of time until one-half of the principal is repaid.

Duration: the average amount of time that a dollar of cash flow is expected to be outstanding; the weighted average of the payment periods using the PV of the total CFs as weights.

Secondary Mortgage MarketsPricing MBS

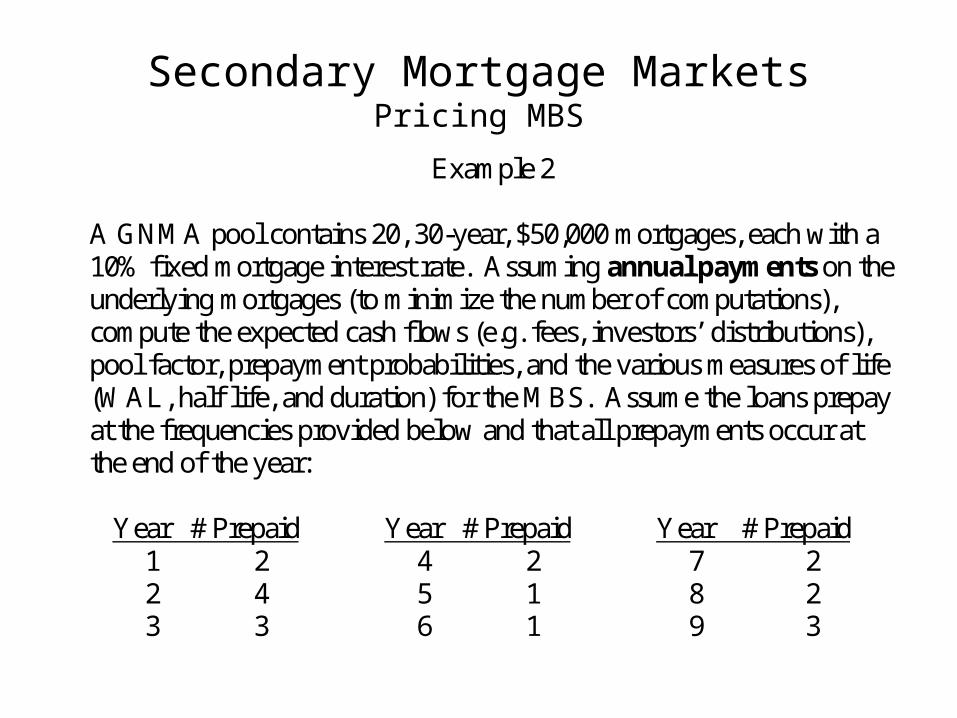

Example 2

A GNMA pool contains 20, 30-year, $50,000 mortgages, each with a 10% fixed mortgage interest rate. Assuming annual payments on the underlying mortgages (to minimize the number of computations), compute the expected cash flows (e.g. fees, investors’ distributions), pool factor, prepayment probabilities, and the various measures of life (WAL, half life, and duration) for the MBS. Assume the loans prepay at the frequencies provided below and that all prepayments occur at the end of the year: Year # Prepaid Year # Prepaid Year # Prepaid 1 2 4 2 7 2 2 4 5 1 8 2 3 3 6 1 9 3

Ginnie Mae Pool: $1,000,000 MBS Discount 9.50% Rate = 20 $50,000 FHA mortgages @ 10.0% for 30 years Year Number of Number of Principal Repayments Total Mortgages Mortgages Principal Prepaid Outstanding Amortization Prepayment

1 2 18 $6,079.25 $99,392.08 $105,471.32 2 4 14 $6,018.46 $197,446.72 $203,465.17 3 3 11 $5,149.12 $146,981.65 $152,130.78 4 2 9 $4,450.31 $97,178.62 $101,628.93 5 1 8 $4,005.28 $48,144.28 $52,149.56 6 1 7 $3,916.28 $47,654.74 $51,571.02 7 2 5 $3,769.42 $94,232.51 $98,001.93 8 2 3 $2,961.68 $93,047.84 $96,009.52 9 3 0 $1,954.71 $137,617.05 $139,571.76

Year Investors' Total Principal Average Year x Interest Distribution Repaid Life Avg. Life To Date Weight Weight

1 $95,000.00 $200,471.32 $105,471.32 0.105471 0.105471 2 $84,980.22 $288,445.40 $308,936.49 0.203465 0.406930 3 $65,651.03 $217,781.81 $461,067.27 0.152131 0.456392 4 $51,198.61 $152,827.54 $562,696.21 0.101629 0.406516 5 $41,543.86 $93,693.42 $614,845.77 0.052150 0.260748 6 $36,589.65 $88,160.67 $666,416.79 0.051571 0.309426 7 $31,690.41 $129,692.33 $764,418.72 0.098002 0.686014 8 $22,380.22 $118,389.75 $860,428.24 0.096010 0.768076 9 $13,259.32 $152,831.08 $1,000,000.00 0.139572 1.256146

1.000000 4.655719

Secondary Mortgage MarketsPricing MBS

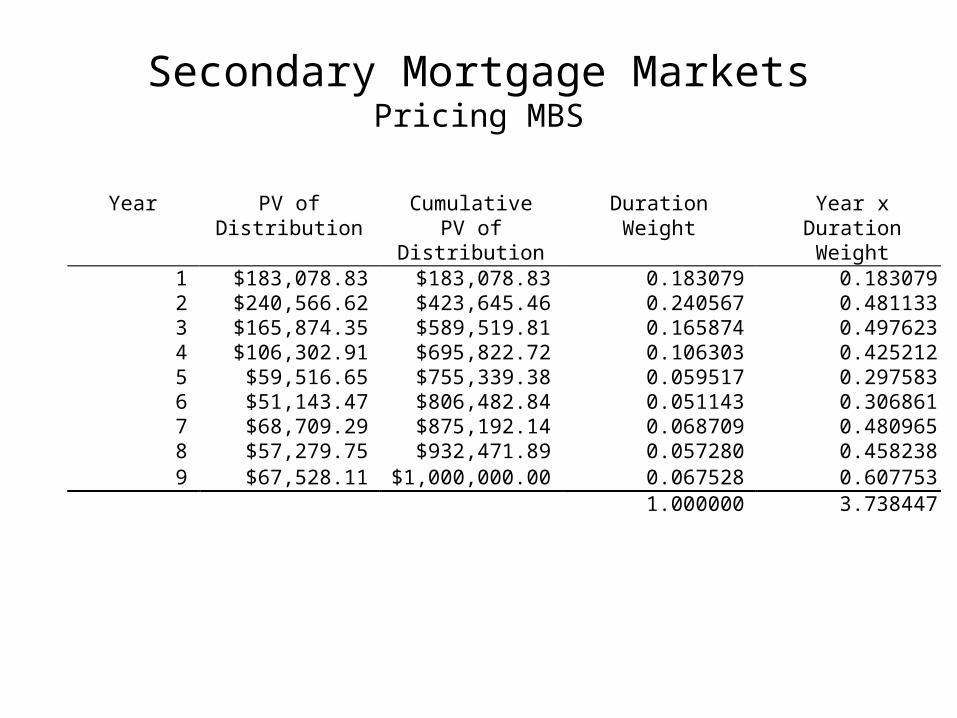

Year PV of Cumulative Duration Year x Distribution PV of Weight Duration Distribution Weight

1 $183,078.83 $183,078.83 0.183079 0.183079 2 $240,566.62 $423,645.46 0.240567 0.481133 3 $165,874.35 $589,519.81 0.165874 0.497623 4 $106,302.91 $695,822.72 0.106303 0.425212 5 $59,516.65 $755,339.38 0.059517 0.297583 6 $51,143.47 $806,482.84 0.051143 0.306861 7 $68,709.29 $875,192.14 0.068709 0.480965 8 $57,279.75 $932,471.89 0.057280 0.458238 9 $67,528.11 $1,000,000.00 0.067528 0.607753

1.000000 3.738447

Secondary Mortgage MarketsPricing MBS

MBS Life Calculations

WAL = 0.105471 x 1 + 0.203465 x 2 + 0.152131 x 3 + ….. = 0.105741 + 0.406930 + 0.456392 = 4.66 years Half life: when is ½ of the beginning principal repaid? = 3 + (500,000 – 461,067)/(562,696 – 461,067) = 3 + 0.3831 = 3.38 years Duration = 0.1831 x 1 + 0.2406 x 2 + 0.1659 x 3 = 0.1831 + 0.4811 + 0.4976 + ….. = 3.74 years

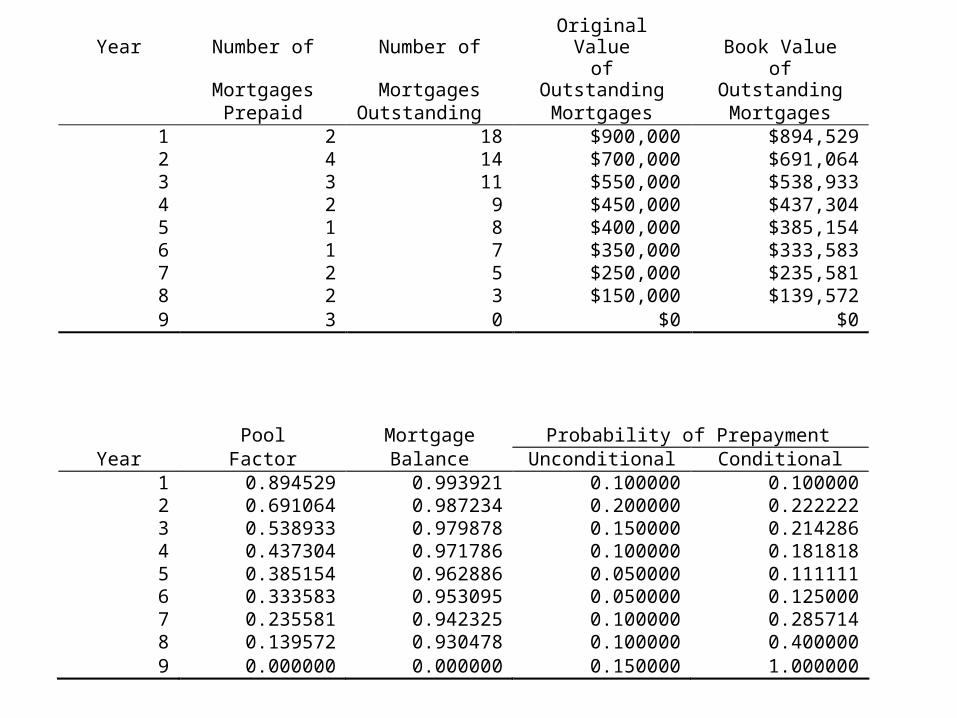

Year Number of Number of Original Value Book Value

Mortgages Mortgages of

Outstanding of

Outstanding Prepaid Outstanding Mortgages Mortgages

1 2 18 $900,000 $894,529 2 4 14 $700,000 $691,064 3 3 11 $550,000 $538,933 4 2 9 $450,000 $437,304 5 1 8 $400,000 $385,154 6 1 7 $350,000 $333,583 7 2 5 $250,000 $235,581 8 2 3 $150,000 $139,572 9 3 0 $0 $0

Pool Mortgage Probability of Prepayment

Year Factor Balance Unconditional Conditional 1 0.894529 0.993921 0.100000 0.100000 2 0.691064 0.987234 0.200000 0.222222 3 0.538933 0.979878 0.150000 0.214286 4 0.437304 0.971786 0.100000 0.181818 5 0.385154 0.962886 0.050000 0.111111 6 0.333583 0.953095 0.050000 0.125000 7 0.235581 0.942325 0.100000 0.285714 8 0.139572 0.930478 0.100000 0.400000 9 0.000000 0.000000 0.150000 1.000000

Secondary Mortgage MarketsPricing MBS

Year Beginning Pool Servicing Ginnie Mae Total Balance Fees Fees Fees

1 $1,000,000 $4,400.00 $600.00 $5,000.00 2 $894,529 $3,935.93 $536.72 $4,472.64 3 $691,064 $3,040.68 $414.64 $3,455.32 4 $538,933 $2,371.30 $323.36 $2,694.66 5 $437,304 $1,924.14 $262.38 $2,186.52 6 $385,154 $1,694.68 $231.09 $1,925.77 7 $333,583 $1,467.77 $200.15 $1,667.92 8 $235,581 $1,036.56 $141.35 $1,177.91 9 $139,572 $614.12 $83.74 $697.86

Secondary Mortgage MarketsPricing MBS

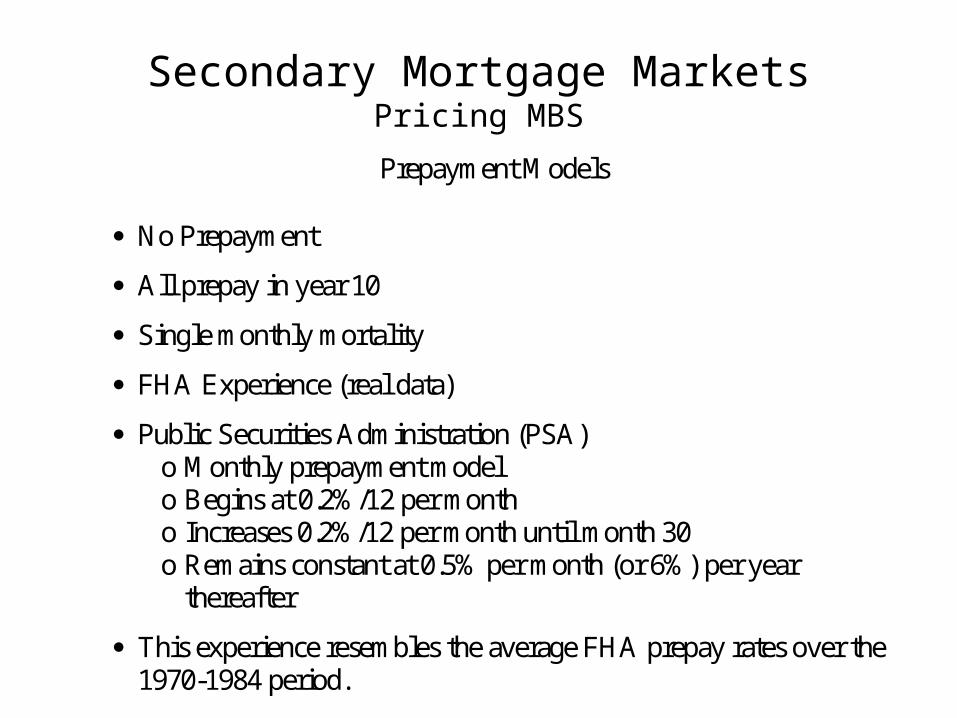

Prepayment Models

No Prepayment

All prepay in year 10

Single monthly mortality

FHA Experience (real data)

Public Securities Administration (PSA) o Monthly prepayment model o Begins at 0.2%/12 per month o Increases 0.2%/12 per month until month 30 o Remains constant at 0.5% per month (or 6%) per year

thereafter

This experience resembles the average FHA prepay rates over the 1970-1984 period.

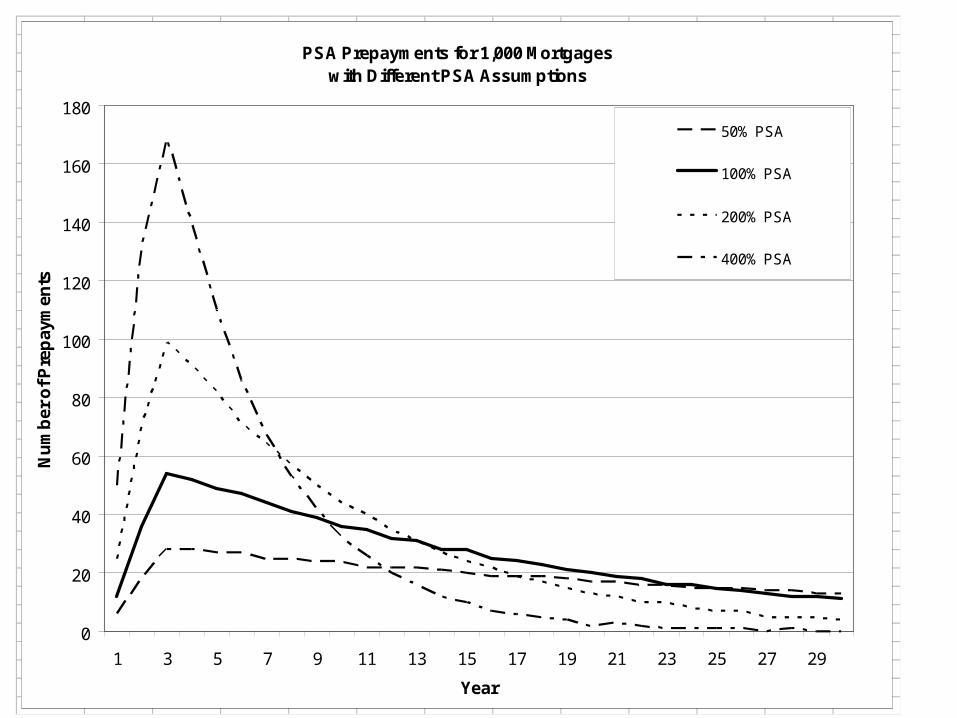

Secondary Mortgage MarketsPricing MBS

Prepayment Models

The 100% PSA Prepayment Model captures the average prepayment performance of FHA mortgages over the 1970-1984 period.

Expected (and actual) prepayment rates may be very different.

To capture differences, investors “adjust” the PSA prepayment

model by taking percentages of the 100% PSA Prepayment Model

o 50% PSA: about ½ of the 100% PSA prepayments o 200% PSA: about twice the 100% PSA prepayments o 400% PSA: about four times the 100% PSA prepayments

6 12 25 5018 36 70 13228 54 99 16928 52 91 14027 49 82 11027 47 71 8625 44 64 6725 41 57 5324 39 50 4224 36 44 3222 35 40 2622 32 35 2022 31 31 1621 28 27 1220 28 24 1019 25 22 719 24 19 619 23 17 518 21 15 417 20 13 217 19 12 316 18 10 216 16 10 115 16 8 115 15 7 115 14 7 114 13 5 014 12 5 113 12 5 013 11 4 0

PSA Prepayments for 1,000 Mortgageswith Different PSA Assumptions

0

20

40

60

80

100

120

140

160

180

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Year

Nu

mb

er o

f Pre

pay

men

ts

50% PSA

100% PSA

200% PSA

400% PSA

Related Documents