SECONDARY LEAD & ZINC INDUSTRY - GLOBAL & INDIAN SCENARIOS L Pugazhenthy Past President The Indian Institute of Metals & Executive Director India Lead Zinc Development Association MRAI International Conference Gurgaon, 22-23 January 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SECONDARY LEAD & ZINC INDUSTRY - GLOBAL & INDIAN SCENARIOS

L Pugazhenthy Past President

The Indian Institute of Metals & Executive Director

India Lead Zinc Development Association

MRAI International Conference Gurgaon, 22-23 January 2016

Global Demand for Lead

Source: ILZSG

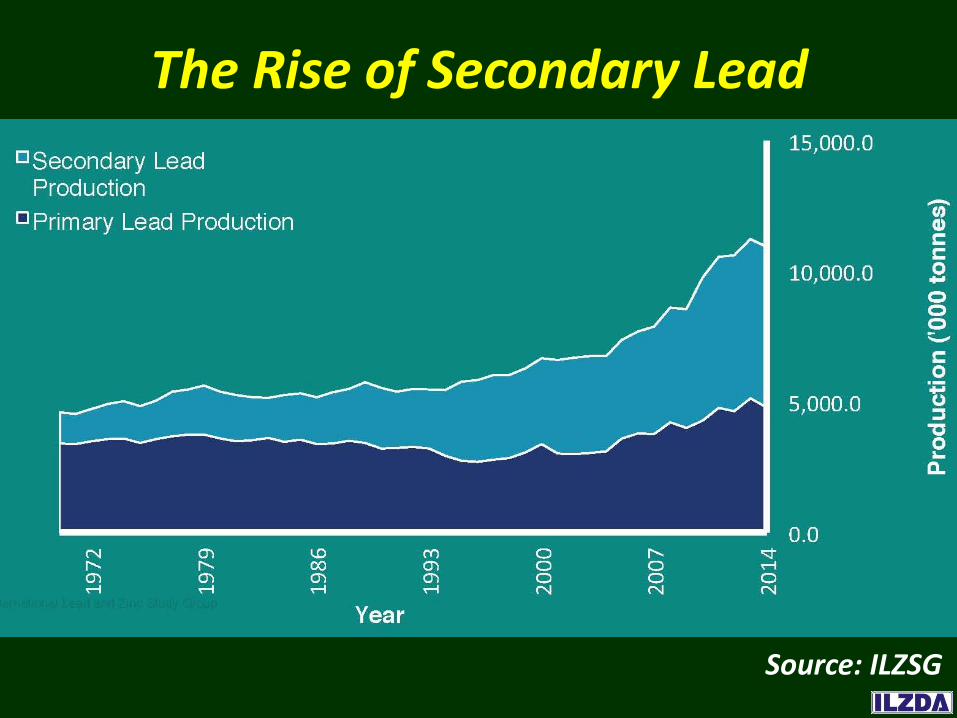

The Rise of Secondary Lead

Source: ILZSG

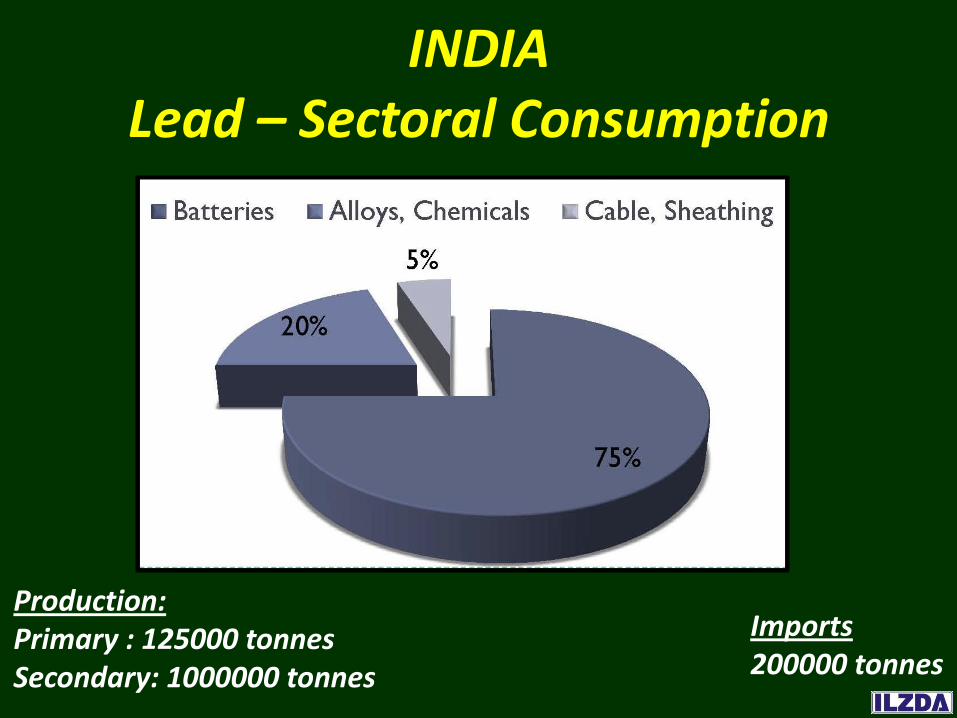

INDIA Lead – Sectoral Consumption

Production: Primary : 125000 tonnes Secondary: 1000000 tonnes

Imports 200000 tonnes

Battery Industry Structure

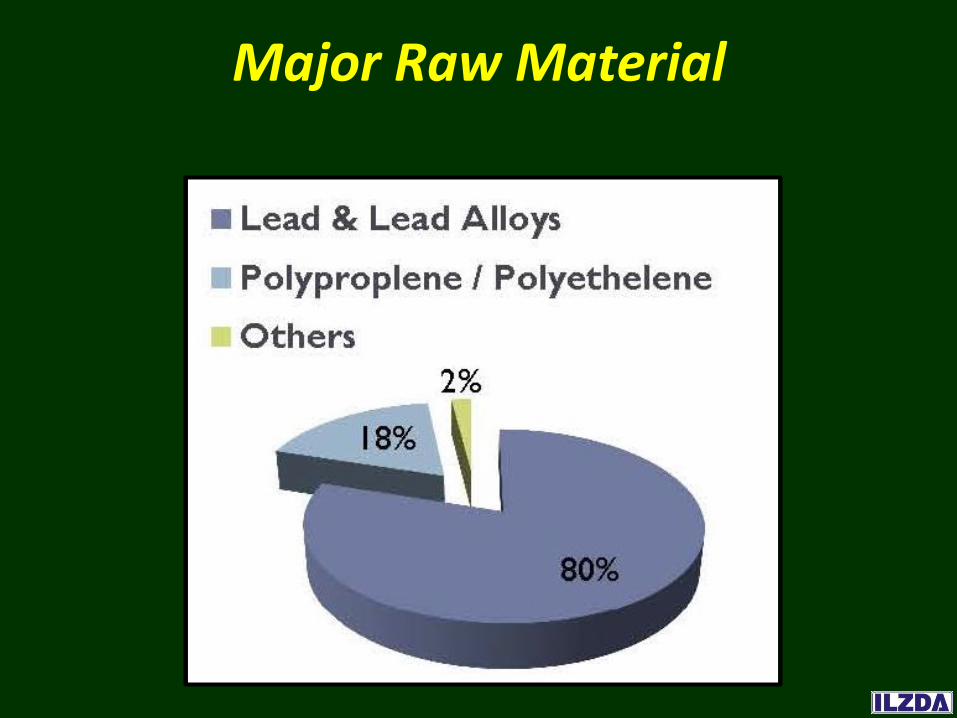

Major Raw Material

(Source: SIAM)

India’s Automobile Production

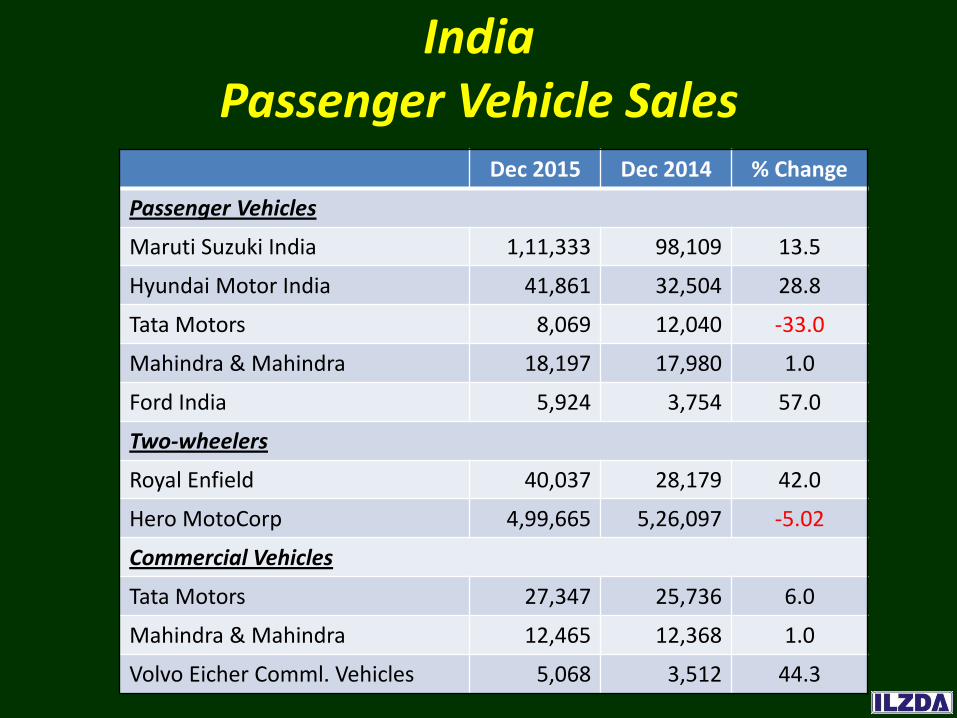

India Passenger Vehicle Sales

Dec 2015 Dec 2014 % Change

Passenger Vehicles

Maruti Suzuki India 1,11,333 98,109 13.5

Hyundai Motor India 41,861 32,504 28.8

Tata Motors 8,069 12,040 -33.0

Mahindra & Mahindra 18,197 17,980 1.0

Ford India 5,924 3,754 57.0

Two-wheelers

Royal Enfield 40,037 28,179 42.0

Hero MotoCorp 4,99,665 5,26,097 -5.02

Commercial Vehicles

Tata Motors 27,347 25,736 6.0

Mahindra & Mahindra 12,465 12,368 1.0

Volvo Eicher Comml. Vehicles 5,068 3,512 44.3

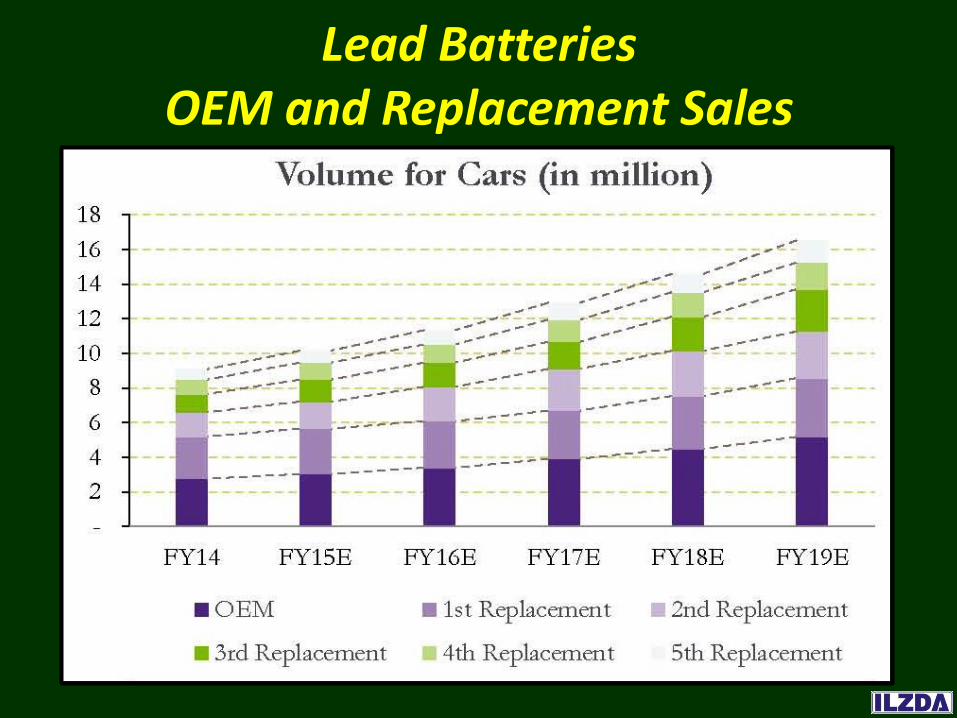

Lead Batteries OEM and Replacement Sales

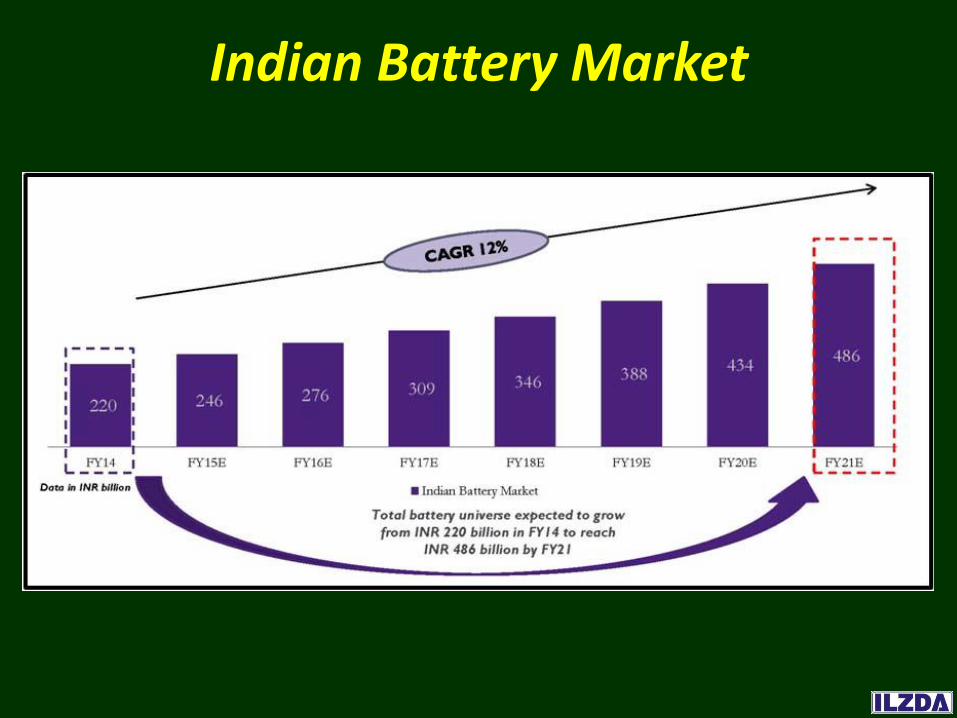

Indian Battery Market

100,000 MW OF SOLAR

60,000 MW OF WIND

5,000 MW OF SMALL HYDRO

10,000 MW OF BIO ENERGY

Renewable Energy Targets by 2022

Electric Vehicles

India Trends in Battery Markets

• Increased Automobile Production

• Continued Power shortage; Inverters ↑

• Telecom Growth Continues (1030 million)

• Incentives for EV Manuf. & Purchase

• More Producers of EVs (4,3 and 2 wheelers)

• Move for Charging Stations

• More Emphasis on Renewable Energy

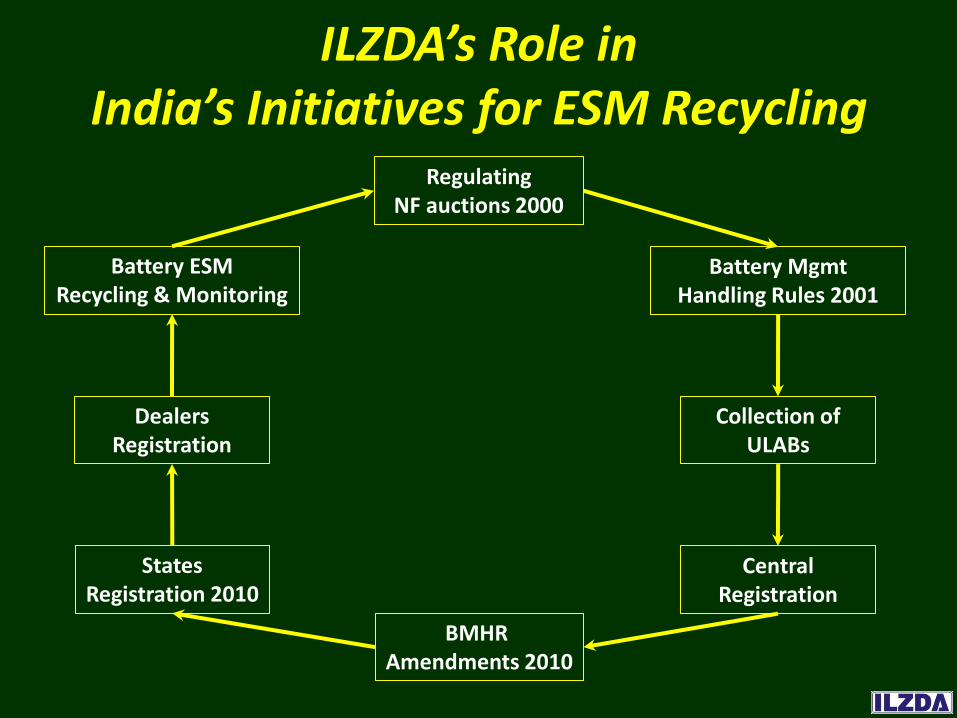

ILZDA’s Role in India’s Initiatives for ESM Recycling

Regulating NF auctions 2000

Central Registration

Battery Mgmt Handling Rules 2001

Collection of ULABs

Battery ESM Recycling & Monitoring

Dealers Registration

States Registration 2010

BMHR Amendments 2010

Battery (Management & Handling) Rules 2001 SALIENT FEATURES

All Stakeholders

(Manufacture, Process, Sale, Purchase, Import, Use)

– Manufacturer

– Importer (new batteries)

– Reconditioner

– Assembler

– Dealer

– Recycler

– Auctioneer

– Consumer (Individual & Bulk)

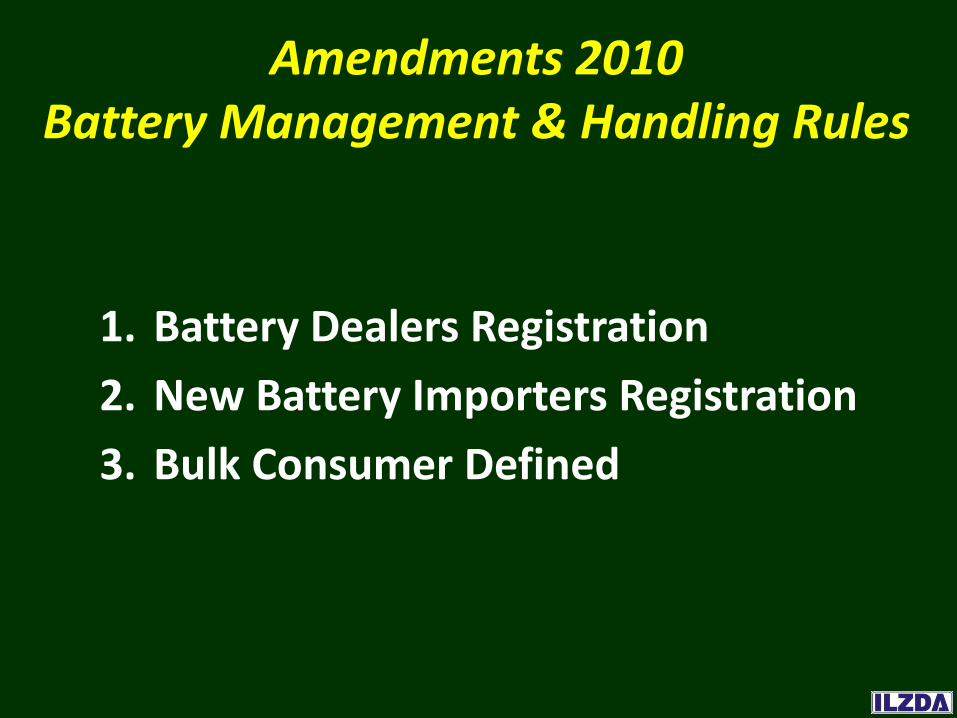

Amendments 2010 Battery Management & Handling Rules

1. Battery Dealers Registration

2. New Battery Importers Registration

3. Bulk Consumer Defined

Trends in ULAB Recycling

• Secondary Lead Production Share: 85%

• ESM Units Allowed to Import ULAB (70%)

• Increasing Rotary Furnaces

• Increasing Mechanized Breaking

• Emphasis on Better Occupational Exposure Practices

• Monitoring of Disposal of Acids, Plastics etc.,

Lead Battery Recycling Shifting to Rotary

Zinc – Global Scenario (Jan-Nov 2015) (million tonnes)

Mine Production 12.32

Metal Production 12.86

Metal Usage 12.68

Secondary Zinc Production 4.00

Zinc – Indian Scenario (tonnes)

Production Capacity 850,000 per annum

Production (2014-15) 737,830

Zinc Usage - Global

Galvanizing, 56%

Die Cast Alloys, 12%

Brass, 11%

Oxides & Chemicals, 9%

Semis, 8% Misc, 4%

(Source: IZA)

19% HDG 37% CG

Zinc Usage - India

Zinc Coating, 77%

Alloys, 10%

Oxides, 5%

Batteries, 3% Zinc Dust, 3% Others, 2%

(Source: HZL)

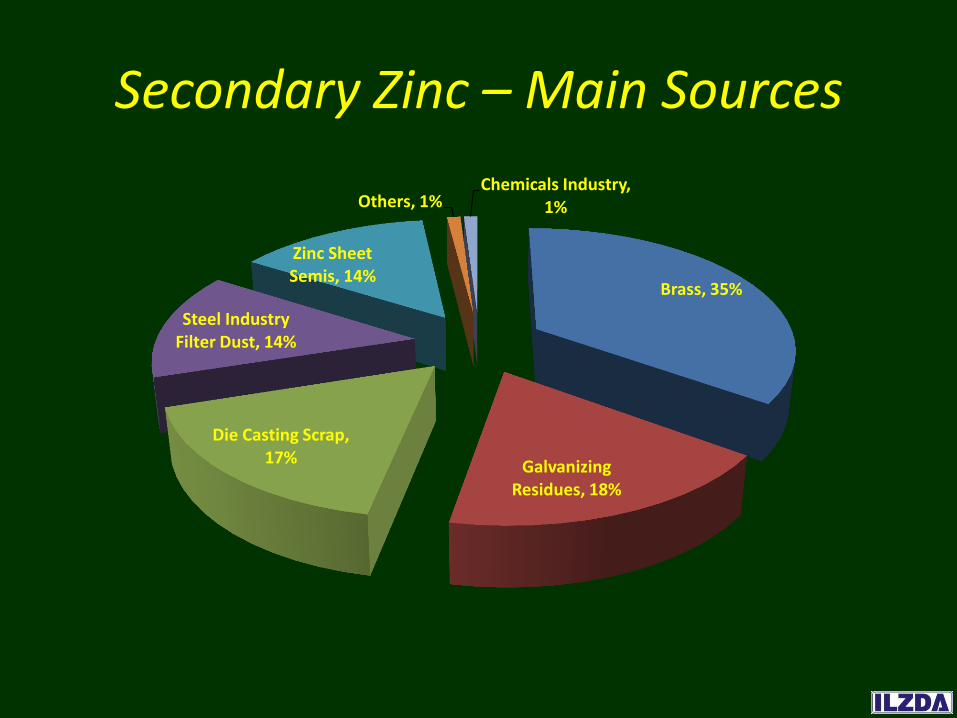

Secondary Zinc – Main Sources

Brass, 35%

Galvanizing Residues, 18%

Die Casting Scrap, 17%

Steel Industry Filter Dust, 14%

Zinc Sheet Semis, 14%

Others, 1% Chemicals Industry,

1%

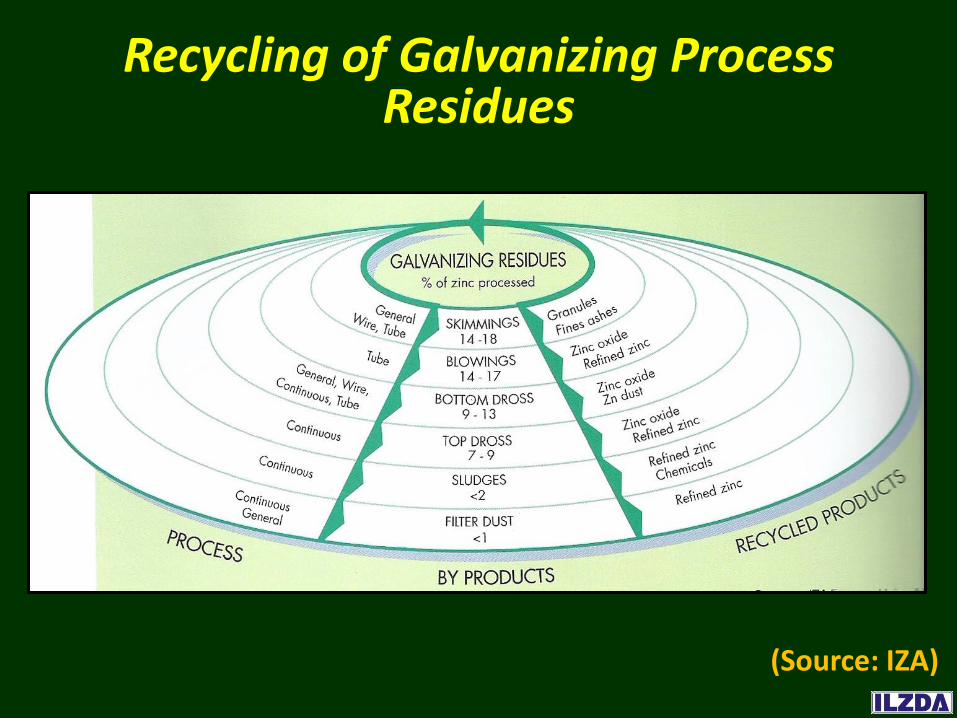

Recycling of Galvanizing Process Residues

(Source: IZA)

The Waelz Process

CONCLUSIONS • Secondary Lead & Zinc

– will continue to grow

• Wastes Minimization

– increasing awareness

• Trends in Several Countries

– recycling within / nearby

• Organized Collection

– imperative need

• Regulatory Bodies

– strict implementation

• Recycling Industry

– voluntary initiative

Related Documents