Debt Overhang, Rollover Risk, and Corporate Investment: Evidence from the European Crisis S . ebnem Kalemli- ¨ Ozcan, University of Maryland, CEPR and NBER Luc Laeven, ECB and CEPR David Moreno, University of Maryland and Central Bank of Chile BIS-OECD-IMF Conference on Weak Productivity, January 2018

Sebnem Kalemli Özcan - Debt Overhang, Rollover Risk, and Corporate Investment: Evidence from the European Crisis

Jan 22, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Debt Overhang, Rollover Risk, and CorporateInvestment: Evidence from the European Crisis

S. ebnem Kalemli-Ozcan, University of Maryland, CEPR and NBER

Luc Laeven, ECB and CEPR

David Moreno, University of Maryland and Central Bank of Chile

BIS-OECD-IMF Conference on Weak Productivity, January 2018

Corporate Investment/GDP

United States

Euro area

Periphery

-0.5

0.0

0.5

1.0

1.5

99 01 03 05 07 09 11 13 15

1 / 22

Corporate Debt/GDP

United States

Euro area

Periphery

0.9

1.2

1.5

1.8

2.1

99 01 03 05 07 09 11 13 15

2 / 22

Is Sluggish Investment Due to Corporate Indebtedness?

We ask whether high levels of corporate debt hold back privatecorporate investment and what is the role of banks in the process?

1 We consider both the level of corporate indebtedness and thematurity structure of the debt, to capture the effects from debtoverhang and rollover risk

2 Novel big data approach:

We use matched firm-bank data based on banking relations in 8European countries obtaining over 2 million observations

We measure both firm and bank balance sheet deterioration

We control for aggregate demand conditions

3 / 22

What is Debt Overhang?

Myers (1977): High levels of debt curtailing investments becausethe benefits from additional investment in firms financed by riskydebt accrue largely to existing debt holders rather than shareholders

More generally in finance literature: A debt burden that is so largethat a firm cannot take on additional debt to finance futureprojects, even if the investment opportunities are profitable enoughto enable it to reduce its indebtedness over time

Debt overhang can lead to sluggish investment via two mainchannels: de-leveraging and low net worth (cannot borrow)

We capture debt overhang using the ratio of corporate debtto assets

Due to de-leveraging, debt service is also important: measure withdebt to income

4 / 22

What is Rollover Risk?

Short-term debt increases rollover risk during crises, when lendersare unwilling to renew expiring credit lines as collateral values dropand financial conditions deteriorate for lenders themselves(Diamond 1991)

We measure rollover risk using ratio of short term debt (lessthan 1 year remaining maturity) in total debt

5 / 22

Corporate Indebtedness as an Overlooked Channel

Existing explanations for low investment in Europe are:

Low demand and aggregate uncertainty

Weak financial conditions from sovereign and bank distress

Banks are weakened by losses from real estate, reducing credit supplySovereign stress further reduces credit supply by imposing losses onbanks with sovereign exposure and deteriorating bank fundingconditions (sovereign-bank linkages)

A high debt-overhang firm may choose not to invest even ifits bank is not weak

6 / 22

Our Contribution

1 Focus on identifying corporate indebtedness for investment slump,conditional on other channels

2 Pan-European setting where we exploit heterogeneity not only ofbanks but also of sovereigns for real outcomes

3 Use a unique hand-matched firm-bank-sovereign data from allEurope that includes small firms

Major difference from the literature that mostly focuses on the listedfirms (1 percent of our sample)Small firms make up a large fraction of economic activity in Europe(70 percent)Cannot switch to alternative sources of fundingDebt overhang effects are presumably larger in small firms givenhigher information asymmetry and riskiness

7 / 22

Share of Debt by Maturity and Size of Firms

64

36

59

41

60

40

0

20

40

60

80

100

Long-Term Short-Term Total

Large firms SME firms

8 / 22

Findings

Investment slump can be linked to higher leverage, increased debtservice, and having a relationship with a weak bank.

Firms with a higher share of long-term debt increase theirinvestment since the rollover risk for those firms is lower.

⇒ This result is driven by firms linked to weak banks. These firmsincrease investment more if they have a higher share of long-termdebt, suggesting these firms are less exposed to rollover risk.

The direct negative effect of weak banks on the average firm’sinvestment disappears once demand shocks are controlled for,although the differential effects remain.

The debt overhang and rollover risk channels explain about 60percent of the actual decline in aggregate corporate investmentduring the crisis.

9 / 22

Findings

Investment slump can be linked to higher leverage, increased debtservice, and having a relationship with a weak bank.

Firms with a higher share of long-term debt increase theirinvestment since the rollover risk for those firms is lower.

⇒ This result is driven by firms linked to weak banks. These firmsincrease investment more if they have a higher share of long-termdebt, suggesting these firms are less exposed to rollover risk.

The direct negative effect of weak banks on the average firm’sinvestment disappears once demand shocks are controlled for,although the differential effects remain.

The debt overhang and rollover risk channels explain about 60percent of the actual decline in aggregate corporate investmentduring the crisis.

9 / 22

Findings

Investment slump can be linked to higher leverage, increased debtservice, and having a relationship with a weak bank.

Firms with a higher share of long-term debt increase theirinvestment since the rollover risk for those firms is lower.

⇒ This result is driven by firms linked to weak banks. These firmsincrease investment more if they have a higher share of long-termdebt, suggesting these firms are less exposed to rollover risk.

The direct negative effect of weak banks on the average firm’sinvestment disappears once demand shocks are controlled for,although the differential effects remain.

The debt overhang and rollover risk channels explain about 60percent of the actual decline in aggregate corporate investmentduring the crisis.

9 / 22

Findings

Investment slump can be linked to higher leverage, increased debtservice, and having a relationship with a weak bank.

Firms with a higher share of long-term debt increase theirinvestment since the rollover risk for those firms is lower.

⇒ This result is driven by firms linked to weak banks. These firmsincrease investment more if they have a higher share of long-termdebt, suggesting these firms are less exposed to rollover risk.

The direct negative effect of weak banks on the average firm’sinvestment disappears once demand shocks are controlled for,although the differential effects remain.

The debt overhang and rollover risk channels explain about 60percent of the actual decline in aggregate corporate investmentduring the crisis.

9 / 22

ORBIS-AMADEUS Data

ORBIS database provided by Bureau van Dijk (BvD), harmonizedworldwide (130million+). Focus on AMADEUS, the Europeansubset of ORBIS starting 1999.

Balance sheets and income statements at 4-digit NACE industryclassification.

Collected from official business registers, annual reports, andnewswires.

Private and public firms (advantage over Compustat/Worldscope).

Mimics official size distribution where less than 250 employee firmsaccount for 70 percent of the economic activity for most Europeancountries

10 / 22

Matching firms to banks and sovereigns

We use KOMPASS database to match bank and firms (firms reporttheir main banker that they borrow from and secondary banker inmost cases).

Then use Bankscope to get the bank balance sheet

We match firms both to their direct relationship bank, and to theparent bank of the relationship bank (to capture internal capitalmarket effect)

For most observations, bank and firm sovereign are identical (withexception of Eastern Europe, which we do not use in mainregressions to keep MP constant)

11 / 22

Identification Methodology

A key challenge is to control for changes in demand (orproductivity shocks)—four-digit sector-country-year fixed effects

Identifying assumption is that firms face demand shocks at theirfour-digit sector level but subject to similar idiosyncratic demandshocks regardless of indebtedness.

An additional challenge is weak firms borrow from weak banks:

We have fixed effects for both to account time-invarying nature ofthis selection issueWe have the balance sheet for both and so can account for thisdirectly in dynamics too

12 / 22

Measurement

Net Investment-to-Capital Ratio: Kt−Kt−1

Kt−1, where Kt are fixed

assets net of depreciation

Leverage: Debt to Capital

Debt Service Interest payments to EBITDA

Maturity: Long term debt (credit institutions and bonds) andshort term debt (bank loans, trade credit, LT payable)

To proxy for firm growth opportunities: Sales growth

To proxy for firm size: log (Capital)

13 / 22

Measuring Weak Banks and Weak Sovereigns

We have several measures for weak banks and weak sovereigns; resultsbelow use:

Weak bank: measured using the ratio of sovereign holdings (total,own, periphery) over total assets

Weak sovereign: measured by the spread of the sovereign bondover the Deutsche Bund of constant 10-year maturity

14 / 22

Benchmark Regression

∆

(Investment

Capital

)i

= β ∆

(Debt

Assets

)i

(1)

+ δ ∆Maturityi + φ ∆

(Interest Paid

ebitda

)i

+ θ ∆Weak Bankib + ∆Xi′ γ + αc,4s + εi

15 / 22

DID Regression

(Investment

Capital

)it

= POSTt ×Weak Bankib,t−1 ×Wi ,t−1′β (2)

+ POSTt ×Wi ,t−1′δ

+ Weak Bankib,t−1 ×Wi ,t−1′θ

+ POSTt ×Weak Bankib,t−1

+ ωWi ,t−1 + αi + αb + δc,4s,t + εi

W: Leverage, Maturity, Debt Service

16 / 22

Parallel Trends in Investment by Leverage

0.00

0.05

0.10

0.15

0.20

0.25

2000 2002 2004 2006 2008 2010 2012

High Low

17 / 22

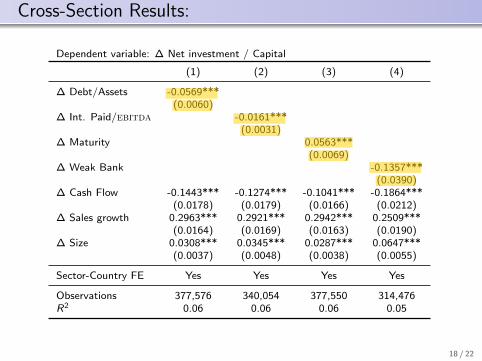

Cross-Section Results:

Dependent variable: ∆ Net investment / Capital

(1) (2) (3) (4)

∆ Debt/Assets -0.0569***(0.0060)

∆ Int. Paid/ebitda -0.0161***(0.0031)

∆ Maturity 0.0563***(0.0069)

∆ Weak Bank -0.1357***(0.0390)

∆ Cash Flow -0.1443*** -0.1274*** -0.1041*** -0.1864***(0.0178) (0.0179) (0.0166) (0.0212)

∆ Sales growth 0.2963*** 0.2921*** 0.2942*** 0.2509***(0.0164) (0.0169) (0.0163) (0.0190)

∆ Size 0.0308*** 0.0345*** 0.0287*** 0.0647***(0.0037) (0.0048) (0.0038) (0.0055)

Sector-Country FE Yes Yes Yes Yes

Observations 377,576 340,054 377,550 314,476R2 0.06 0.06 0.06 0.05

18 / 22

kalemli

Highlight

kalemli

Highlight

kalemli

Highlight

kalemli

Highlight

Cross-Section Results:

Dependent variable: ∆ Net investment / Capital

∆ All Sovereign ∆ OwnSovereign

∆ OwnSovereign

(Periphery)

∆ Debt/Assets -0.0559*** -0.0536*** -0.0535***(0.0086) (0.0095) (0.0095)

∆ Int. Paid/ebitda -0.0131*** -0.0119*** -0.0119***(0.0037) (0.0040) (0.0040)

∆ Maturity 0.0531*** 0.0575*** 0.0575***(0.0081) (0.0083) (0.0083)

∆ Weak Bank -0.0670* -0.2754*** -0.2581**(0.0358) (0.0992) (0.1075)

∆ Cash Flow -0.1793*** -0.1770*** -0.1769***(0.0230) (0.0238) (0.0238)

∆ Sales growth 0.2905*** 0.2957*** 0.2957***(0.0192) (0.0175) (0.0175)

∆ Size 0.0143*** 0.0146*** 0.0146***(0.0044) (0.0047) (0.0047)

Sector-Country FE Yes Yes Yes

Observations 294,255 226,412 226,412R2 0.07 0.07 0.07

19 / 22

kalemli

Highlight

Weak Bank - Weak Sovereign Linkages (Domestic Bonds)

Interaction effects:

Postt× Weak Bankt−1× Debt/Assetst−1 -1.3694*** -0.9501*** -0.9515***(0.2477) (0.2586) (0.2902)

Postt× Weak Bankt−1× Int. Paid/ebitdat−1 0.0244 0.1603 0.159(0.1562) (0.1567) (0.1734)

Postt× Weak Bankt−1× Maturityt−1 1.1579*** 0.5139** 0.5232**(0.2208) (0.2194) (0.2512)

Total effects:

Debt/Assetst−1 -0.069*** -0.092*** -0.092***(0.007) (0.0072) (0.007)

Int. Paid/ebitdat−1 -0.0033** -0.0046*** -0.0046***(0.0016) (0.0016) (0.0015)

Maturityt−1 -0.2301*** -0.2229*** -0.2229***(0.0049) (0.0049) (0.0046)

Weak Bankt−1 -0.1316*** 0.0297 0.0609(0.0259) (0.0256) (0.05)

Firm FE Yes Yes YesSector-Country-Year FE No Yes YesBank FE No No Yes

Observations 1,316,624 1,315,060 1,315,060R2 0.33 0.34 0.34

20 / 22

kalemli

Highlight

kalemli

Highlight

kalemli

Highlight

kalemli

Highlight

The Role of Weak Sovereigns (Periphery Domestic Bonds)

Interaction effects:

Postt× Weak Bankt−1× Debt/Assetst−1 -1.6240*** -1.1084*** -1.1088***(0.2345) (0.246) (0.268)

Postt× Weak Bankt−1× Int. Paid/ebitdat−1 -0.0252 0.1654 0.1654(0.1519) (0.1522) (0.1642)

Postt× Weak Bankt−1× Maturityt−1 1.6169*** 0.9235*** 0.9303***(0.2175) (0.2217) (0.2416)

Total effects:

Debt/Assetst−1 -0.0693*** -0.092*** -0.0921***(0.007) (0.0072) (0.007)

Int. Paid/ebitdat−1 -0.0034** -0.0047*** -0.0047***(0.0016) (0.0016) (0.0015)

Maturityt−1 -0.2309*** -0.2235*** -0.2235***(0.0049) (0.005) (0.0046)

Weak Bankt−1 -0.1317*** 0.0240 0.0603(0.0255) (0.0248) (0.0504)

Firm FE Yes Yes YesSector-Country-Year FE No Yes YesBank FE No No Yes

Observations 1,316,624 1,315,060 1,315,060R2 0.33 0.34 0.34

21 / 22

Conclusions

1 We document significant debt-overhang and roll over risk effects inEurozone which cause sluggish investment.

High leverage, due to accumulated debt before crisis, depressinvestment during crisis times, consistent with debt overhang(increase debt service and low net worth).

Firms who enter the crisis with a shorter maturity of debt reduceinvestment more during the crisis when those firms are linked toweak banks consistent with an increase in rollover risk associatedwith increased sovereign risk that weaken the bank balance sheets.

Firms whose main bank’s balance sheet deteriorated because of largeexposure to sovereign risk during crisis invested less (lendingchannel) and experience more debt overhang and rollover risk

2 Policy implication:The debt overhang and rollover risk channels can explain 60 percentof the investment decline.Bank recapitalization (done) and dealing with legacy debt will helpbut not completely solve the investment problem.

22 / 22

Conclusions

1 We document significant debt-overhang and roll over risk effects inEurozone which cause sluggish investment.

High leverage, due to accumulated debt before crisis, depressinvestment during crisis times, consistent with debt overhang(increase debt service and low net worth).

Firms who enter the crisis with a shorter maturity of debt reduceinvestment more during the crisis when those firms are linked toweak banks consistent with an increase in rollover risk associatedwith increased sovereign risk that weaken the bank balance sheets.

Firms whose main bank’s balance sheet deteriorated because of largeexposure to sovereign risk during crisis invested less (lendingchannel) and experience more debt overhang and rollover risk

2 Policy implication:The debt overhang and rollover risk channels can explain 60 percentof the investment decline.Bank recapitalization (done) and dealing with legacy debt will helpbut not completely solve the investment problem.

22 / 22

Conclusions

1 We document significant debt-overhang and roll over risk effects inEurozone which cause sluggish investment.

High leverage, due to accumulated debt before crisis, depressinvestment during crisis times, consistent with debt overhang(increase debt service and low net worth).

Firms who enter the crisis with a shorter maturity of debt reduceinvestment more during the crisis when those firms are linked toweak banks consistent with an increase in rollover risk associatedwith increased sovereign risk that weaken the bank balance sheets.

Firms whose main bank’s balance sheet deteriorated because of largeexposure to sovereign risk during crisis invested less (lendingchannel) and experience more debt overhang and rollover risk

2 Policy implication:The debt overhang and rollover risk channels can explain 60 percentof the investment decline.Bank recapitalization (done) and dealing with legacy debt will helpbut not completely solve the investment problem.

22 / 22

Conclusions

1 We document significant debt-overhang and roll over risk effects inEurozone which cause sluggish investment.

High leverage, due to accumulated debt before crisis, depressinvestment during crisis times, consistent with debt overhang(increase debt service and low net worth).

Firms who enter the crisis with a shorter maturity of debt reduceinvestment more during the crisis when those firms are linked toweak banks consistent with an increase in rollover risk associatedwith increased sovereign risk that weaken the bank balance sheets.

Firms whose main bank’s balance sheet deteriorated because of largeexposure to sovereign risk during crisis invested less (lendingchannel) and experience more debt overhang and rollover risk

2 Policy implication:The debt overhang and rollover risk channels can explain 60 percentof the investment decline.Bank recapitalization (done) and dealing with legacy debt will helpbut not completely solve the investment problem.

22 / 22

Conclusions

1 We document significant debt-overhang and roll over risk effects inEurozone which cause sluggish investment.

High leverage, due to accumulated debt before crisis, depressinvestment during crisis times, consistent with debt overhang(increase debt service and low net worth).

Firms who enter the crisis with a shorter maturity of debt reduceinvestment more during the crisis when those firms are linked toweak banks consistent with an increase in rollover risk associatedwith increased sovereign risk that weaken the bank balance sheets.

Firms whose main bank’s balance sheet deteriorated because of largeexposure to sovereign risk during crisis invested less (lendingchannel) and experience more debt overhang and rollover risk

2 Policy implication:The debt overhang and rollover risk channels can explain 60 percentof the investment decline.Bank recapitalization (done) and dealing with legacy debt will helpbut not completely solve the investment problem.

22 / 22

EXTRA SLIDES

20 / 22

Size Distribution, Manufacturing, 2006 (from Gopinath,Kalemli-Ozcan, Karabarbounis, Villegas-Sanchez, 2015)

Spain Italy Portugal Germany France Norway

Employment

ORBIS-AMADEUS 1-19 employees 0.24 0.13 0.25 0.05 0.10 0.1820-249 employees 0.50 0.55 0.53 0.32 0.35 0.47250+ employees 0.26 0.32 0.22 0.63 0.56 0.35

Eurostat (SBS) 0-19 employees 0.31 0.41 0.34 0.15 0.20 0.2020-249 employees 0.43 0.37 0.48 0.32 0.34 0.42250+ employees 0.26 0.22 0.18 0.53 0.46 0.38

Gross Output

ORBIS-AMADEUS 1-19 employees 0.14 0.12 0.12 0.06 0.05 0.1120-249 employees 0.42 0.49 0.43 0.27 0.23 0.40250+ employees 0.45 0.40 0.46 0.67 0.72 0.49

Eurostat (SBS) 0-19 employees 0.14 0.21 0.15 0.06 0.10 0.1320-249 employees 0.38 0.41 0.42 0.22 0.27 0.36250+ employees 0.49 0.38 0.43 0.72 0.63 0.51

21 / 22

Related Literature

Macro models with corporate debt overhang: Lamont (1995),Whited (1992), Occhino and Pescatori (2010)

Empirical debt overhang literature: focus on banks, sovereigns andhouseholds: Philippon and Schnabl (2013), Becker and Ivashina(2014), Melzer (2012).

Lack of corporate sector focus is due to data limitations—with listed USfirms: Bond and Meghir (1994), Hennessy (2004), Hennessy, Levy,Whited (2007)

22 / 22

Related Documents