Sustainable Development Policy Institute Budget for Sustainable Development and Job Creation 1 1 Pre-budget Proposals 2015-16 A Green Budget for Sustainable Development and Job Creation Sustainable Development Policy Institute April 10, 2015 Islamabad

SDPI Pre-Budget Proposals

Jul 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

1

1

Pre-budget Proposals 2015-16

A Green Budget for Sustainable Development and Job Creation

Sustainable Development Policy Institute April 10, 2015

Islamabad

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

2

2

1. About SDPI

The Sustainable Development Policy Institute (SDPI) is an independent, non-profit policy research institute and oldest civil society think tank in Pakistan, which produces knowledge on sustainable development to enhance the capacity of government and private sector in making informed policy decisions. Over the past 23 years, SDPI has produced and advocated policy research on all facets of sustainable development, including inclusive economic growth, social justice, societal sustainability, climate change and environmental protection. The institute’s advice is sought for targeted interventions through change in legislation, policy rules, policy practice, budgetary allocations and efficiency with which these allocations are disbursed. An important area of SDPI’s work has been to bridge research policy gaps through continued and sustained involvement of citizens. The citizen’s involvement is particularly important for improving service delivery in social sectors especially education and health.

2. Background

PML-N Government inherited a weak economy, with all macroeconomic indicators at their historic low. During the past five years, Pakistan’s average economic growth remains around 3.4% per annum. This growth rate is hardly enough to absorb: a) existing unemployed labour force, and b) increased young entrants into working age population. The public sector with meagre resource mobilization may not be able to provide adequate jobs whereas for private sector, sustained energy supplies and structural reforms such as removal of distortions from taxation regime is urgently required to create jobs. To let formal economy flourish, the public sector needs to put in place measures that curtail the growth of undocumented and informal economy. An important pillar of inclusive growth is openness of trade and investment. The trade regime in the country is unfortunately not in line with the vision set in the Strategic Trade Policy Framework. The past governments have struggled to fund the well intentioned interventions of the trade policy. The facilitation measures for exporters are sporadic and uncertain. A similar pattern of weak facilitation is seen in Pakistan’s foreign direct investment. The fiscal incentives provided for such investors are rarely possible in practice and in turn lead to costly tax expenditures. The recent difficulties in repatriation of profits by foreign investors signify the gap between approved and in-practice Central Bank policy measures. The confidence of domestic investor remains low despite an improvement in macroeconomic fundamentals during 2014-15. This is reflected from heavy official and non-official outflow of capital from Pakistan into Middle East, EU and other investor-

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

3

3

friendly destinations. Only meaningful reforms in energy sector, public sector enterprises, trade facilitation, currency alignment and debt management can boost the confidence of domestic investors. As Pakistan’s investment to GDP ratio fell below the average of South Asia and even sub-Saharan Africa, job creation process will continue to struggle. This is also a security challenge as youth who remain unemployed for a longer time period are prone to social evils like radicalization and terrorism. The challenges associated with sustainable development inform us that the inter-generational justice is becoming difficult to achieve. While the 18th Amendment and increased fiscal transfers to the provinces have allowed some improvement in the public service delivery of education and health, there are key aspects of social justice and environmental protection that lack ownership both in terms of agenda-setting and budgetary allocations. The issues of climate change and food security will continue to threaten the future of our coming generations. While current government is appreciative of participatory decision making and always willing to include the suggestions from concerned stakeholders in policy formulation and implementation, many of the stakeholders including consumers, labourers, marginalized groups and right based groups are not organized enough to meaningfully engage the policy makers through solid evidences. SDPI considers linking stakeholders to the policy making circles a public duty and thus not only bridges research policy gaps but also the gap between people and decision makers.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

4

4

3. Objectives

The key objectives of this exercise include:

Reaching out to a maximum number of representatives from business community,

consumer associations, trade associations, labour unions and rights-based

organizations and solicit their feedback on the current state of economy

Based on the feedback from various stakeholders, suggest removal of distortions in

the taxation and expenditure regime

Suggesting compensatory mobilization measures to bridge any revenue gap created

by the removal of tax-related distortions

Creating fiscal space for growth-enhancing and job-oriented infrastructure spending

Mobilizing resources and improving coordination between federal and provincial

governments for more targeted and efficient investments in social sectors, climate

change adaptation and food security

Protecting social sector spending on education, health, clean water supply,

sanitation, women’s empowerment and youth mobilizaton

Revisiting debt management strategy in order to lessen burden on current and

future generations

Thematic Focus of Proposed Budgetary Interventions

Sustainable Development

Job creation

Food security

Industrial competiti

veness

Education

Health Peace & Social Justice

Energy

Boosting Exports

Social Safety Nets

Environmental

sustainability

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

5

5

4. Methodology

This document is the result of in-depth consultations with the business community, economists, representatives of non-governmental organizations, members of Tax Reforms Commission and academia over a period from January to March 2015. Our in-depth interviews included interaction with members of Pakistan Business Council, All Pakistan Business Forum, and sector-specific associations, e.g. auto sector, pharmaceutical sector, dairy, industry and Farmers Association of Pakistan. In order to provide robust policy advice, consistent with macroeconomic fundamentals, SDPI uses a three-layered macro-meso-micro economic model. The top layer is a financial programming model providing a set of key macroeconomic identities and behavioural equations aimed at providing forecasts related to growth, investment, consumption, taxes, government expenditures, exports, imports and current account balance. The middle tier is a dynamic computable general equilibrium (CGE) model which provides forecast related to goods and factor (labour and capital) markets. Finally at the bottom tier we have a microsimulations model which computes the poverty and welfare impact of macroeconomic policies using household income and expenditure survey data.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

6

6

5. Tax Proposals

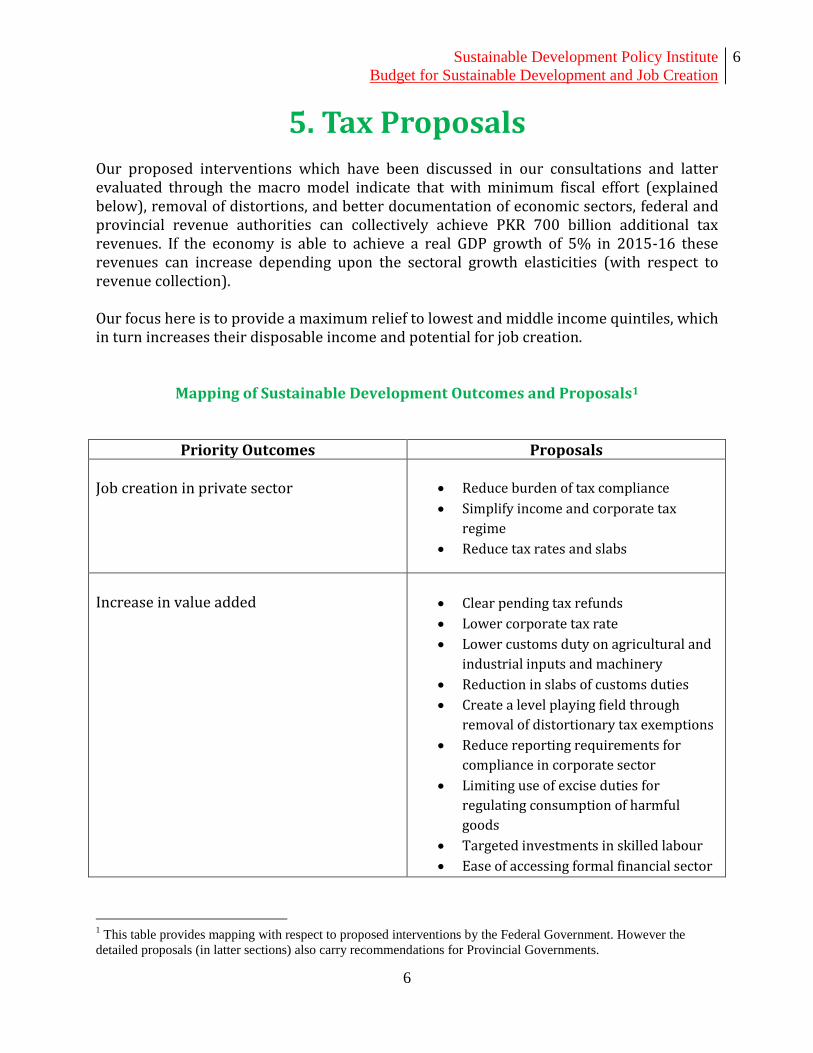

Our proposed interventions which have been discussed in our consultations and latter evaluated through the macro model indicate that with minimum fiscal effort (explained below), removal of distortions, and better documentation of economic sectors, federal and provincial revenue authorities can collectively achieve PKR 700 billion additional tax revenues. If the economy is able to achieve a real GDP growth of 5% in 2015-16 these revenues can increase depending upon the sectoral growth elasticities (with respect to revenue collection). Our focus here is to provide a maximum relief to lowest and middle income quintiles, which in turn increases their disposable income and potential for job creation.

Mapping of Sustainable Development Outcomes and Proposals1

Priority Outcomes Proposals Job creation in private sector

Reduce burden of tax compliance

Simplify income and corporate tax

regime

Reduce tax rates and slabs

Increase in value added

Clear pending tax refunds

Lower corporate tax rate

Lower customs duty on agricultural and

industrial inputs and machinery

Reduction in slabs of customs duties

Create a level playing field through

removal of distortionary tax exemptions

Reduce reporting requirements for

compliance in corporate sector

Limiting use of excise duties for

regulating consumption of harmful

goods

Targeted investments in skilled labour

Ease of accessing formal financial sector

1 This table provides mapping with respect to proposed interventions by the Federal Government. However the

detailed proposals (in latter sections) also carry recommendations for Provincial Governments.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

7

7

Priority Outcomes Proposals for working capital

Boosting Exports Focus on reducing tariff and non-tariff

barriers to trade with neighbouring

countries

Clear pending refunds of exporters

Investing in trade facilitation measures

for both exports and imports

Open more land routes for trading with

Afghanistan, India and Iran and created

integrated customs management units

Reduce customs duty on import of raw

materials and machinery from China and

India. Increase the number of items

allowed for trading at land routes

Social Safety Nets and Social Protection Integrating and strengthening social

safety nets under one umbrella

programme to avoid duplication of

efforts and reduce resource wastage

Replace hidden and cross subsidies with

targeted subsidies

Increasing efficiency of fiscal

instruments for workers welfare (e.g.

Workers Welfare Fund)

Removal of any duplications between

federal and provincial social safety net

programmes

Minimum rural employment guarantee

scheme in pilot districts

Enhanced allocations for skills training

to facilitate mobility

Ensuring compliance of minimum wage

laws and workplace safety standards

Increase allocations for ensuring food

security

Increase allocations for women and

children in conflict areas

Natural resource management and environmental protection

Increase allocations for projects related

to climate change adaptation, disaster

risk reduction and environmental

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

8

8

Priority Outcomes Proposals protection

Rigorous implementation of carbon tax

Reduce customs duty on green

technologies (inputs) for industry

Agriculture Implementation of previously

announced crop & livestock insurance

programme

Exemption from GST for agricultural

inputs such as seeds, fertilzers, and

chemicals.

Food Security Implementation of previously

announced zero hunger programme

Fortified meals for expecting mothers,

breast feeding mothers, and children

below 5 targetted from recipients of

BISP.

5.1. Direct Taxes

In order to avoid the ongoing misrepresentation, the distinction between taxable income of

salaried and non-salaried class should be eliminated. All incomes in excess of minimum

exemption should be taxed at the same rate. The top tax rate for salaried and non-salaried

taxpayers should be brought down to 25%. Already there is a wide margin between

statutory top tax rate and effective tax paid. The top tax rate should be applied to income in

excess of PKR 5,500,000 per annum.

The number of slabs for Association of Persons (AoPs), self employed and salaried persons

should be reduced to 3 for making the overall taxation structure relatively more

progressive. For the benefit of small tax-payers, the exemption limit should be indexed with

annual inflation

Employer organizations should be given a relief particularly during times of economic

slowdown. We therefore recommend linking social security and Employees Old Age Benefit

(EOAB) contributions to growth in key productive sectors of the economy. If the provisional

real GDP growth rate crosses the targeted growth rate, it is then proposed that social

security contribution by employers may be increased by one per cent of salary of insurable

employees. One per cent increase is also recommended in the case of EOAB.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

9

9

Advanced income tax on functions and gatherings is easy to avoid and evade given the lack

of proper documentation. It is recommended that this tax should be removed.

The taxable income on which there is zero% tax rate should remain unchanged during

2015-16. This will help in curtailing tax expenditures

Given the high returns in stock market observed during 2014-15, the tax rates on such

profits should be considered for an upward revision with any exemptions removed.

Similarly the taxation of dividend income may be at 12%. The definition of ‘securities’ under

section 37A of Income Tax Ordinance should include the government’s debt securities

The efficiency of Workers’ Welfare Fund (WWF) needs to be reformed. Equally important is

to better manage welfare schemes under this fund. The operations at WWF should be in line

with predetermined key performance indicators. There should be an alignment with other

social protection programmes such as Benazir Income Support Programme. The rampant

evasion in WWF contributions2 can be checked by putting in place biometric systems

available with NADRA and State Bank of Pakistan. Better fund management will require

expertise in risk assessment by officials at WWF and EOBI

FBR in the past has sent notices to owners of property (above a certain limit) for respecting

their tax liability. Little success has been achieved in this area. It is, therefore, proposed that

persons who own property above a certain limit and are full time residents of Pakistan

should not be allowed to transfer or sell their property if they have not paid past year’s

income tax return. The same treatment should apply to assets such as cars above 800Cc

engine capacity

The withholding tax in telecommunications sector is one of the highest in comparison to

peer economies. A reduction of 5% is recommended.

There is a WHT on cash withdrawal from banks (beyond a certain threshold). The

percentage of WHT may be charged upon telegraphic transfer (outward) of foreign

exchange from Pakistan. It is also proposed that declaration of income should be mandatory

for money remitted outside of Pakistan

At provincial levels, urban property tax needs immediate reform. There are issues related

to: a) valuation (owner-sellers undervalue their property on official documents), b) lack of

motivation / incentive at revenue authorities to improve collections, c) exemptions (e.g.

preferential treatment allowed to owner-occupied property), and d) poor coverage (over

half of urban property in each province goes untaxed).

5.2. Corporate Income Tax

In order to encourage corporatization and job creation, the corporate tax rate should be

lowered to 29%. However a gradual phasing out of exemptions should be initiated

(discussed in section 5).3 This will also incentivize formalization and documentation of

businesses

2 2% of profits of business establishments go to WWF contributions.

3 The Indian general budget 2015-16 envisages a reduction in corporate tax rate from 30 to 25% in the next four

years.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

10

10

The current structure of taxation is a disincentive to corporatize. FBR’s own report co-

authored with a consortium of economic experts states: ‘Public and private limited

companies pay the same tax rates, though the former have slightly more reporting

requirements than the latter. The public limited company pays out its entire net income in

dividends. The shareholders will thus not only pay a corporate income tax, but also a tax on

the dividend income. The effective tax rate in the case of an incorporated business comes to

41.5%. In the non-corporate sector there are two sub-sectors: Associations of Persons

(AoP) and Business individuals. An AoP does not have the limited liability protection but

does face a significantly lower tax rate than a company. In addition, an AoP’s income tax

represents the full and final income tax liability for the individual partners, who then do not

need to make any additional payments for personal income tax. The effective rate of

taxation is 25%. In respect of business individual, it may be said that they are simply

persons who does business as a sole proprietor and does not incorporate their enterprise.

This person does not get any legal protection from liability, and in turn faces tax rate much

lower than either an AoP or a company, since they are taxed only at the individual income

tax rate. Their actual rate comes to 7.25%’.

5.3. Indirect Taxes

The sales tax on prescribed thresholds of monthly electricity bills of retailers located in air

conditioned shopping malls should be uniformly set at 10%.

The sales tax on the purchase of high-end mobile and smart phones (above price/unit PKR

20,000) should be 17%. An excise duty of similar magnitude may also be considered.

All provincial sales tax on services laws should be harmonized.

As an incentive to increase compliance, the threshold level in sales tax may be increased to

PKR 8 million. Furthermore, zero rating (under sales tax) should only be allowed to sectors

which represent consumption of the poorest of the poor. Any zero rating or exemptions

allowed on the grounds of boosting exports, industry or services sectors should be

eliminated. There is robust evidence to suggest that such fiscal incentives (in isolation from

other complimentary policies) have not contributed to increase in productivity or exports.

It is recommended that exemption from GST for selected agriculture inputs may be allowed

to ensure food security and rural development.

In order to restore the confidence of business community (on tax authorities), a deadline of

two months should be placed on clearance of sales tax refunds. For new businesses, sales

tax registration is still a lengthy process and can take up to several months.

The provision of self-assessment and voluntary compliance under the Sales Tax Act 1990

compromises revenue as it is not supported by extensive or randomised audit. Third party

oversight can also help improving audit function at tax authorities.

Federal excise duty (FED) on locally produced cigarettes, may be increased by another 5%.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

11

11

In order to give boost to construction sector and construction related jobs, it is proposed

that FED on cement sector may be modified to 3% on retail price.

FED on international travel in economy class is proposed be increased to PKR 10,000 per

ticket. Similarly for business class FED may be increased to PKR 20,000 per ticket. Services

by chartered flights may be charged FED at 20%.

In view of the ongoing energy crisis, need for conserving environment and maintenance of

road infrastructure it is proposed that locally manufactured cars and imported motor

vehicles should be treated equal and FED charged at 17%.

Maximum general tariff on import may be brought down to 20%. The minimum general

tariff should be 0%. The number of tariff slabs should be brought down to 3. The regulatory

duty on luxury items may be increased by another 5%.

In order to protect environment and conserve energy, it is proposed that for the domestic

consumers adjustable advanced tax on the monthly bill exceeding PKR 50,000 should be

17%.

In order to protect environment, customs duty on import of inputs of alternative and

renewable energy equipment may be brought down to 0%.

In order to check the conspicuous consumption behaviour an adjustable advance tax of 5%

may be imposed on multinational food chains currently operating in Pakistan.

As an incentive to increase compliance, the input tax invoicing of machinery may be brought

in line with accelerated depreciation allowance in income tax.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

12

12

6. Tax Expenditures

A five-year income tax exemption was proposed in Budget 2014-15 for locally grown fruits

in Balochistan, G-B and FATA. As it is difficult to audit the origin of agricultural produce and

hence curtail fraud, therefore it is proposed that this exemption be removed. Any machinery

important for this purpose and region was also allowed exemption from customs duty. This

may be reviewed to assess its contribution in province’s economic development.

The RoI still remains encouraging on most energy projects. It is proposed that tax

exemption allowed to coal mining projects (for power generation) in Sindh be removed. The

dividends from such projects should be taxed at a rate applied to all other power generation

units.

The capital gains tax (CGT) on securities held for any time period should be made uniform.

In view of the improved performance of securities markets in Pakistan, it is proposed that

CGT should be applied at a uniform rate of 17.5%.

The reduction in corporate tax rate, allowed to foreign direct investment in Pakistan, should

be removed. This is prone to misuse by domestic investors. The corporate tax rate should be

the same for both domestic and foreign investors.

The sales tax concessions allowed to five leading export oriented sectors (textile, leather,

carpets, surgical and sports goods) caused a loss of PKR 65 million to FBR collections in

2013-14. There is a vast evidence in recent economic studies that there was no link

between these concessions and export performance. Therefore, it is recommended to

abolish: SRO 809(I)2009, SRO 212(I)/2013, SRO 154 (I)/2013, and SRO 98(I)/2013.

The SROs allowing concessions on sales tax for import of raw materials are being misused

and also need to be urgently revisited and abolished. These particularly include: SRO

1125(I)/2011, and SRO 670(I)/2013.

The development of Gwadar coasts presents encouraging RoI. Therefore, it is recommended

that the tax concessions give to ‘China Overseas Ports Holding Company Limited’ should be

removed.

The reduction in rate of tax withheld on mobile phone charges may be reduced to 10%. The

currently high taxes are promoting the use of Viber and Whatsapp usage to avoid higher

spending. It is ultimately the poor that pay relatively higher for mobile phone usage.

In the case of advance tax on first class, club class and business class air tickets, the

distinction of compliant and non-compliant taxpayer was not implemented by any airline or

travel agent. This distinction may be removed and advanced tax should be increased to

10%.

In the case of advance tax on real estate transactions, the distinction of compliant and non-

compliant tax-payer should be enforced effectively. The advanced tax should be increased

to 5%.

The reduction in rate of tax allowed to Mutual Funds should be removed.

The rate of initial allowance on buildings should be brought down to 8%.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

13

13

Taxpayers registered under Sales Tax Act 1990 are allowed 2.5% tax credit if 90% of their

sales are to persons registered under the same Act. This tax credit is not very efficient in

reducing incidence of informal economy and therefore should be removed.

Certain exemptions were allowed to IT enabled services in order to boost their exports.

These should be phased out given their misuse.

The customs duty exemption allowed for Gwadar (on import of machinery and equipment

for power generation plants, water treatment plants and infrastructure related projects)

may be assessed to check its utility. The concessionary rate of customs duty on import of

machinery and equipment for setting up hotels in Gwadar should be assessed to stop its

misusage.

All exemptions allowed for mineral exploration, mine construction and extraction should be

removed. Similarly all exemptions allowed for Thar Coal fields should be reviewed

considering that Thar Coal is still a nonstarter, and government is focusing on LNG rather

than coal.

In the case of energy projects, first year depreciation allowance of 90% of cost is allowed in

lieu of initial allowance. Private sector power projects are exempt from income taxes. The

dividends of share holders are taxed at a reduced rate. These concessions should be

removed.

A lifetime exemption was allowed to Independent Power Plants (IPPs) under the 1994

power policy. This exemption should be removed. NEPRA has the mandate and authority to

get revisions to agreements (between government and IPPs) enforced.

Following concessions may be removed and if needed may be made part of the gross salary:

1. Compensatory allowance to Pakistani citizen locally recruited at Pakistan Mission

abroad with income exceeding 75 percent of gross salary

2. Flying allowance to PIA, Civil Aviation Authority, Pakistan Army, Pakistan Navy and

Pakistan Air force

3. Conveyance allowance to Provincial Governors, Chiefs of Staff, Pakistan Armed

forces and the Corps Commanders

4. Entertainment allowance to Provincial Governors, Chiefs of Staff, Pakistan Armed

forces and the Corps Commanders

5. Free Rent Residency, as the right given to President of Pakistan, Provincial

Governors, Chiefs of Staff, Pakistan Armed forces.

6. Rent-free accommodation/house-rent allowance to the Ministers of the Federal

government

7. Free/Subsidized food by hotel and restaurants during duty hours to the Ministers of

Federal govt.

8. Free/Subsidized education to children of the Ministers of the federal government

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

14

14

9. Free/Subsidized medical treatment Ministers of federal government

10. Concessional passage by the transporters including Railways, Airlines to the

members of their household and dependents

11. Judicial allowance to Judges of Supreme Court and High court

12. Motor vehicle, housing allowance to civil servants under federal or provincial

governments

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

15

15

7. Tax Administration

All current amnesties should be revisited and phased out. In case of persons who have still not

filed and paid taxes after amnesty, legislation may be appropriately revised in order to allow

liable taxpayers to pay arrears in instalments.

Introducing and maintaining tax credit for certain transactions over a certain time period can

promote documentation of a fast growing informal economy. Tax credits may be allowed for

personal expenditures on private tuition academies, rent of residential space, medical expenses,

legal fee, professional fee (e.g. fee paid to accountants). These tax credits may only be allowed

subject to submission of payment evidence.

Any changes to the online filing should first be pre-tested in focus group environment with tax-

payers across various education levels. The transactions cost of online filing should be

rationalized. Utmost efforts may be made to rationalize the interface between taxpayer and

payee through appropriate use of ICT tools.

Third party evaluation of tax compliance processes should be an annual feature. This should be

undertaken by a strong firm having experience in past evaluations. The services of foreign

consulting firms should be discouraged as local firms have better insight in to ongoing

practices.

The hearing of appeals should be separated from FBR’s core functions. The appeals should be

heard and followed up with a party which has no conflict of interest.

The units within FBR are weakly networked. The missing integration across tax related

information and data implies lack of internal and external validation of tax records. For

example, within the FBR’s Inland Revenue Service, the database for sales tax is not integrated

with database for income tax. Businesses or liable persons can get away with quoting different

turnover numbers on their sales tax and income tax returns.

For correct assessment of tax base across the country, province-wise and district-wise

estimation of incomes by sector is essential. Pakistan Bureau of Statistics should be mandated

to provide: a) estimates of provincial and district-wise GDP, and supply and use tables (for

inter-industry flow of transactions). Similarly, the provincial Bureaus of Statistics (in order to

support collection of GST on services) should conduct a census of services incomes and

establishments.

A law to prohibit benami transactions is long due. The Indian Benami Transactions

(Prohibition) Act 1988 can serve as a good example.

To keep a check on the growing undocumented sector and informal economy, it is proposed

that clause-9 of The Protection of Economic Reforms Act 1992, i.e. secrecy of banking

transaction, should be removed.

Tax authorities lack access to information on assets held by Pakistani residents in foreign

countries. Since 2010 Pakistan has not filed any case with the Swiss government. The Swiss

government under its Return of Illicit Assets Act allows developing countries to recover funds

shifted through dubious means.

Outreach programmes for taxpayers can demonstrate proper utilization of tax resources at

micro level. These outreach programmes, if properly designed, can help the public in

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

16

16

understanding how paying taxes can improve public service delivery in social and

infrastructure sectors.

Prompt grievance redressal mechanisms will help in bridging the high levels of trust deficit

between the state and taxpayers.

Open Budget Initiatives such as one practiced in several commonwealth countries can

strengthen fiscal transparency and overtime enhance taxpayers’ confidence.

The next NFC award should have conditionalities that include improvement in provincial tax

administration. The following reforms / conditions may be announced as part of the federal

budget:

o Ending fragmentation in collection of taxes at the provincial level. For example in the

case of Sindh, taxes are being collected by: a) Excise, Taxation and Narcotics

Departments, b) Board of Revenue, c) Sindh Revenue Board and d) Government of Sindh

directly collecting levies (e.g. electricity duty). Such fragmentation is leading to

excessive administrative costs and evasion (as taxpayers can report different incomes)

o The efficiency of tax collection at provincial levels also needs attention. For example,

Sindh Tax Revenue Mobilization Plan 2014-19 correctly points out that 9 out of the total

15 provincial taxes in Sindh render 99 percent of collected revenues. The remaining 6

taxes only contribute 1 per cent. Such taxes should be reviewed, simplified or

consolidated

o Provincial revenue authorities need to establish a census-based baseline of tax bases for

each of the provincial taxes. The baselines should highlight the current sector-wise tax

gaps, administrative efficiency, and sector-wise effective revenue potential. The

coordination across the provincial revenue collection bodies should also be reviewed

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

17

17

8. Expenditure Management

8.1. Current Expenditures

The size of the federal government needs to be reduced. There are several ministries that

may be merged in order to save taxpayers’ contributions. Furthermore, several attached

departments within the ministries may be merged. This has been done in the past and

should continue as a regular exercise. Facilities such as vehicles and housing allowed to

senior civil servants, judiciary, and military officials should be monetized and indexed with

inflation.

In line with the political manifestos of most political parties, the fragmented governance in

energy sector must end. There should be a single energy ministry for integrated energy

management.

The number of foreign missions and embassies of Pakistan may be reduced. A region

specific approach may be taken where one embassy may be able to take care of a group of

countries.

A revision of Fiscal Responsibility and Debt Limitation Act should put forward: a) bold

targets to cut down the current expenditures, b) medium term plan to manage high debt

levels, and c) protecting social sector expenditures and spending towards environmental

protection and food security.

All new SROs should be first discussed in parliament, relevant standing committees, and

Council of Common Interest

Any supplementary grant which exceeds a certain limit of the approved budget should have

endorsement of standing committee on finance.

There is a need to better resource Ministries of Climate Change and Food Security. It is

proposed that outcomes based budgeting may be introduced in both ministries to keep a

check on Pakistan’s commitments towards Sustainable Development Goals.

In order to save scarce government resources derived through taxation it is important to

diversify the sources of infrastructure financing. The infrastructure that is excessively

financed through foreign aid also leads to Dutch disease effect. We propose tax free bonds

for infrastructure projects. Such bonds should be offered to both local and foreign investors.

8.2. Development Spending

A priority should be given to high growth projects (e.g. energy sector) and projects having

high potential to create future jobs. The Planning Commission (and similarly provincial

Planning & Development bodies) may form a special working group on: a) how to identify

high growth projects within the currently approved portfolio, and b) measures to protect

allocations and disbursements for such projects.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

18

18

All planning and development entities must strengthen their capacity for monitoring and

evaluation in terms of both human and technical expertise. The traditional M&E currently in

practice only involves overseeing of inputs, utilization of resources and products acquired

at the end. There is a need to move towards result based monitoring and evaluation of

projects with emphasis upon outcomes and long-term impact.

Throw forward in PSDP must be reduced through alternate financing modes, such as a)

public private partnerships, b) built to operate & transfer, and c) built to operate & own

schemes. While slashing PSDP following criteria must be adopted; a) projects near

completion should be fully protected, b) contractual binding in projects with foreign donors

must be honoured, and c) development projects with high growth impact should be

protected.

Provinces can rationalize throw forward through: a) avoiding politically driven projects

lacking economic justification, b) avoiding duplication of projects, and c) considering the

closure of new and ongoing projects for which the expense incurred is less than 25%.

Following measures must be taken to minimize leakages in PSDP a) project management

cost in public sector development projects is way too high which must be reduced, b)

dedicated technical professionals must be appointed as project directors in projects instead

of bureaucrats with experience only in civil service, c) consultancy charges must be

rationalized, d) contingencies should be reduced, and e) public sector projects should be

exempted from GST.

Bypassing Planning Commission or provincial planning and development departments in

project approval and award of anticipatory approval must be discouraged. There must be

rigorous abidance of feasibility, appraisal and approval processes. This can be enforced and

strengthened through: a) strong financial and technical appraisal (can be outsourced), b)

social analysis which reflects beneficiary population, dislocation, resettlement and

livelihoods c) economic analysis that estimates EIRR, B/C ratio, NPV and domestic resource

cost, and d) risk analysis that should include time delays, cost variations, design and content

modifications.

It is recommended that the future of the following schemes should be determined through

regular quarterly and annual reviews. Currently, low efficiency is being observed in case of

PM’s Interest Free Loan Scheme, PM’s Business Loan Scheme, PM’s Free Reimbursement

Scheme for Less Developed Areas, PM’s Youth Training Scheme, PM’s Youth Skill

Development Scheme, and PM’s Housing Scheme. The review should be conducted by

independent and internationally renowned experts. There are also overlaps with popular

projects announced by the provincial governments e.g. Punjab Government’s Yellow Cab

Scheme.

The direct, hidden and cross subsidies need to be better targeted for the poorest of the poor.

They should be the ultimate beneficiaries for subsidies. Currently, subsidy operations are

allowed for agriculture (major crops particularly wheat), irrigation, roads and highways,

public higher education, fertilizer, textile, automotive, and energy sectors. Finance Division

should host on urgent basis a high level working group to review and phase out untargeted

subsidies.

Sustainable Development Policy Institute

Budget for Sustainable Development and Job Creation

19

19

In order to promote women’s entrepreneurship particularly in SME sector, it is proposed

that a national programme for advocacy, outreach and special package for women may be

structured. Such a special package should not aim to allow any fiscal incentives, however

may put in place special facilitation mechanisms by SECP, FBR and related institutions.

8.3 Education Sector

Rationalize between, primary, secondary and tertiary education spending across all

provinces. Currently per student expenditure on primary students is far lower than

secondary and tertiary education. In some areas the federal government and provincial

governments spend ten times as much on secondary students as they do on primary

students.

Rationalize the budget allocation between physical infrastructure (capital expenditure) and

teacher capacity building (human development). Currently there is too much focus on

building infrastructure, which is important and should not be ignored. However financing

for improving teacher quality should be a priority

The development budget on education should be given protection by law. The provincial

government may pass a law which ensures that during any fiscal year the allocation for

education will not be diverted elsewhere.

8.4 Health Sector

The customs duty on the import of pharmaceutical items not produced in Pakistan should

be lowered. This particularly applies to life saving drugs and child vaccines which are

widely missing from local markets.

The development budget on health should be given protection by law. The provincial

government may pass a law which ensures that during any fiscal year the allocation for

health will not be diverted elsewhere.

At a provincial level, future financial resource can be saved if there is an enhanced focus on

primary preventive health care - through: allocation of more funds for primary care (at BHU

level), mother and child health care, family planning, and immunization. Enhanced funding

is required to ensure security of polio teams in rural areas.

The health sector governance can further increase - through: decentralization of planning

and budgeting of health related activities at the district government level, improving regular

monitoring, restructuring and strengthening Departments of Health and office of DG Health,

and investment in improving supply chains.

Related Documents