Supply Chain Management Professional SCM Pr n analysis n practice n knowledge n survey n human resource March 2013 Vol. 1—No.2 ` 150 risk management Reviewing RapAgRisk. Page..33 talent When hiring decisions go bad. Page...47 In This Issue Ensuring Food Security guru speak AseAn’ s Supply Chain Challenge. Page...7 Salary Survey Report 2013 Page...42 Evaluating how Agri Supply Chain can evolve to capture Value for the participant

SCMPro March 2013 Edition

Mar 13, 2016

The only enterprise magazine for SCM Professionals.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Supply Chain Management ProfessionalSCMPr n analysis

n practicenknowledgensurveynhuman resource

March 2013 Vol. 1—No.2 `150

risk managementReviewing RapAgRisk.

Page..33

talentWhen hiring decisions go bad.

Page...47

In This

Issue

Ensuring Food Security

guru speakAseAn’s Supply Chain Challenge.

Page...7

Salary Survey

Report 2013Page...42

Evaluating how Agri Supply Chain can evolve to capture Value for the participant

www.scmp.in

...live supply chain

Industry Portal for the Supply Chain Professional

editorial

3SCMPr March 2013

It is with great pleasure I present to you the second issue of SCM PRO. We had barely recovered from the emotional high of the first issue, and we plunged into the second issue. That too at a time when the nation

was looking forward to a budget. The future we were looking at in the first issue is getting defined brick by brick. There is a huge amount of reforms we still need. The time for tokenism is long past gone. Mere tinkering with a few rates or allocating some funds to needed sectors is not enough.

The nation heaved sigh of relief with the budget by the Finance Minister. For once, politics took backstage to economics – but not in full measure. There is cause for hope – tinged with caution. I believe it is not yet time to pop the bubbly. We will watch and bring you our take on these develop-ments.

In the second issue of SCM Pro, we bring you an eclectic mix of articles for your reading.

Food security is of prime importance to a nation’s progress. It is reported that up to 40% of the agri produce gets spoilt as it travels from Farm to Fork. The minister of state for agriculture and food processing industries, Tariq Anwar, pegs the monetary value of this wastage at Rs. 50,000 crores per year. In our special feature issue, we focus on what we can do as sup-ply chain professionals to prevent this colossal wastage – we have a series of articles that focus on various aspects of the Agri Supply Chain.

One of the defining developments in our part of the world is the rise of ASEAN and its impact on India. For our Guru Speak we caught up with Dr. Mahender Singh the CEO and Rector of Malaysian Institute of Supply Innovation in Malaysia. We bring you his views on leveraging supply chain as a platform for growth in ASEAN.

In addition we have an interesting mix of articles carefully selected for your reading pleasure. I hope you enjoy them.

As always, we invite your comments and views on our content. Espe-cially, if you do not agree with the views of our authors, please write in with your views. We encourage healthy debate. And in this debate we see the green shots of a vibrant supply chain community.

Let us build this community together.

Happy Reading.

Executive Editor

Building a VibrantCommunity

Girish V s

Executive Editor

4 SCMPr March 2013

Co

nte

nts

ma

rc

h 2

013

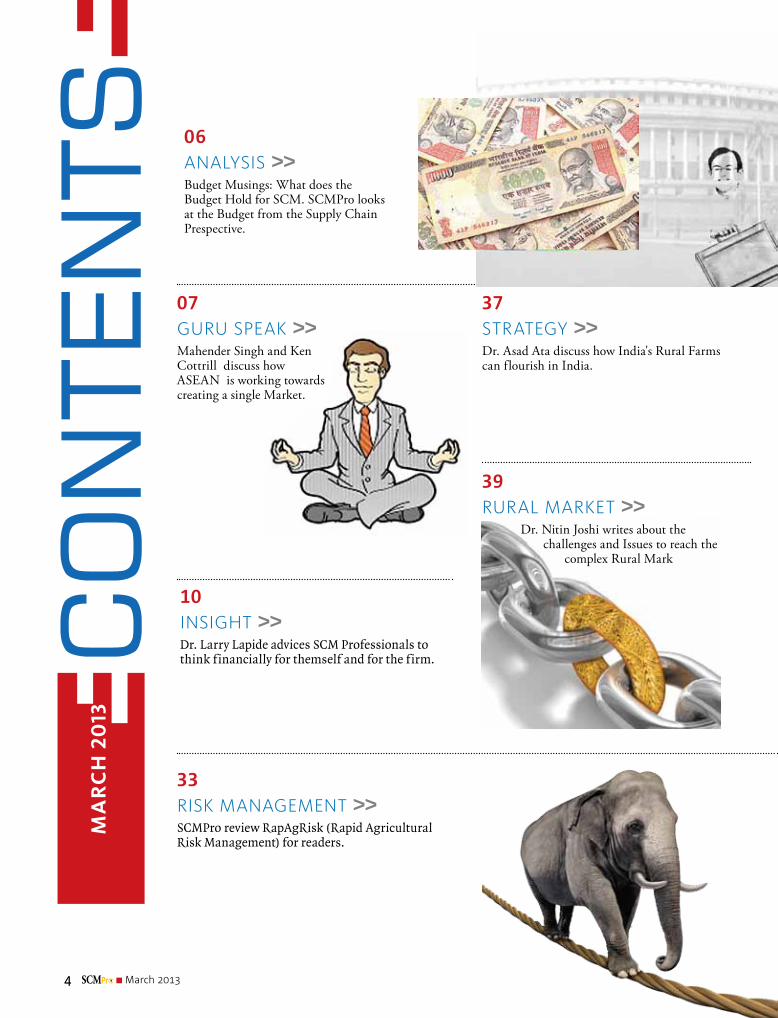

06ANALYSIS >>Budget Musings: What does the Budget Hold for SCM. SCMPro looks at the Budget from the Supply Chain Prespective.

37StrAtegY >>Dr. Asad Ata discuss how India's Rural Farms can flourish in India.

10INSIght >>Dr. Larry Lapide advices SCM Professionals to think financially for themself and for the firm.

4

33rISk mANAgemeNt >>SCMPro review RapAgRisk (Rapid Agricultural Risk Management) for readers.

39rurAL mArket >>

Dr. Nitin Joshi writes about the challenges and Issues to reach the

complex Rural Mark

07guru SpeAk >>Mahender Singh and Ken Cottrill discuss how ASEAN is working towards creating a single Market.

5

50LASt pAge >>Dr. Rakesh Singh writes how India can play an important role in Southeast Asia as a part o ASEAN economic community.

12LeAd StorY

Executive Publisher Jayaram [email protected]

EDITORIALExecutive EditorGirish V [email protected]

Consultant Editor Dr. Rakesh [email protected]

CREATIVE & ProductionHead Shivasankaran [email protected]

advertisingSoney Mathew [email protected]

Rashid [email protected] Media Group211/1, Sona Udyog, Parsi Panchayat Road, Andheri (East), Mumbai -400069 INDIA.

Printed and published by Jayaram Nair on behalf of B2B Media Group. Printed at SAP Print Solutions Pvt. Ltd, 28 Laxmi Ind. Estate, Lower Parel, Mumbai - 400 705, India and published at 211/1, Sona Udyog, Parshi Panchayat Rd., Andheri (E), Mumbai - 400069.

No part of this publication may be reproduced or transmitted in any form or by any means including photocopying or scanning without the prior permission of the publishers. Such written permission must also be obtained from the publisher before any part of the publication is stored in a retrieval system of any nature. No liabilities can be accepted for inaccuracies of any description, although the publishers would be pleased to receive amendments for possible inclusion in future editions. Opinions reflected in the publication are those of the writers. The publisher assumes no responsibilities for return of unsolicited material or material lost or damaged in transit. All correspondence should be addressed to B2B Media Group. All disputes are subject to the exclusive jurisdiction of competent courts and forums in Mumbai only.

ANNUAL SUBSCRIPTION RATE INDIA: `1,800/-

Agri Supply Chain - Enusirng Food Security to the Nation: A well developed Agri Supply Chain is an imperative for the growth of the Sector and ensuirng food security o the nations.

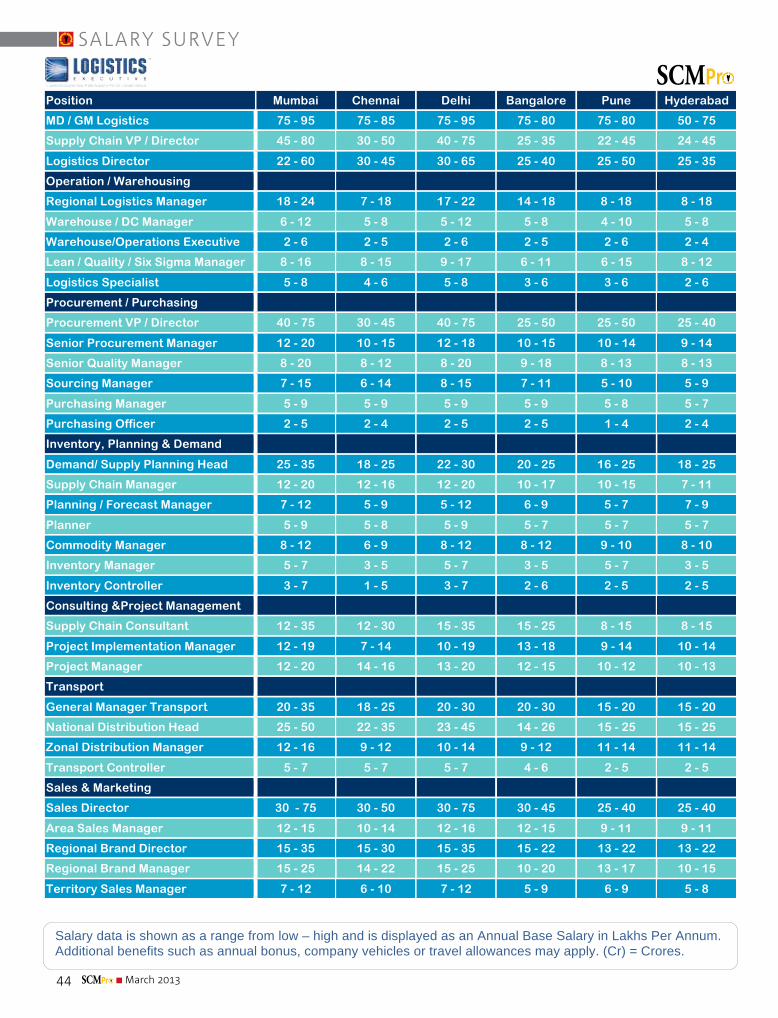

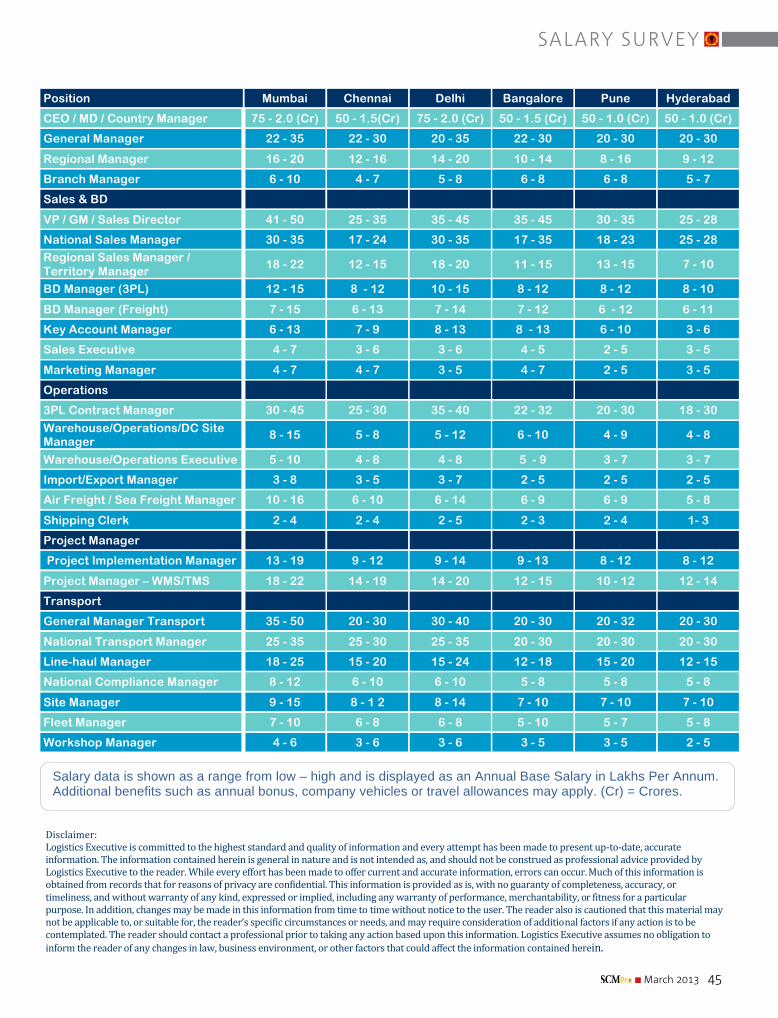

42SALArY SurveY >>Logistics Executive in Conjunction with SCMPro brings to you the second edition of the 2013 Salary Guide report for the Indian Supply Chain and Logistics market.

Accademic Partner

SCMPr

5

47humAN reSourceS >>Making a wrong hiring decision costs money. Its not just a business issue but an economic one too, writes Darryl Judd.

SCMPr March 2013

6 SCMPr March 2013

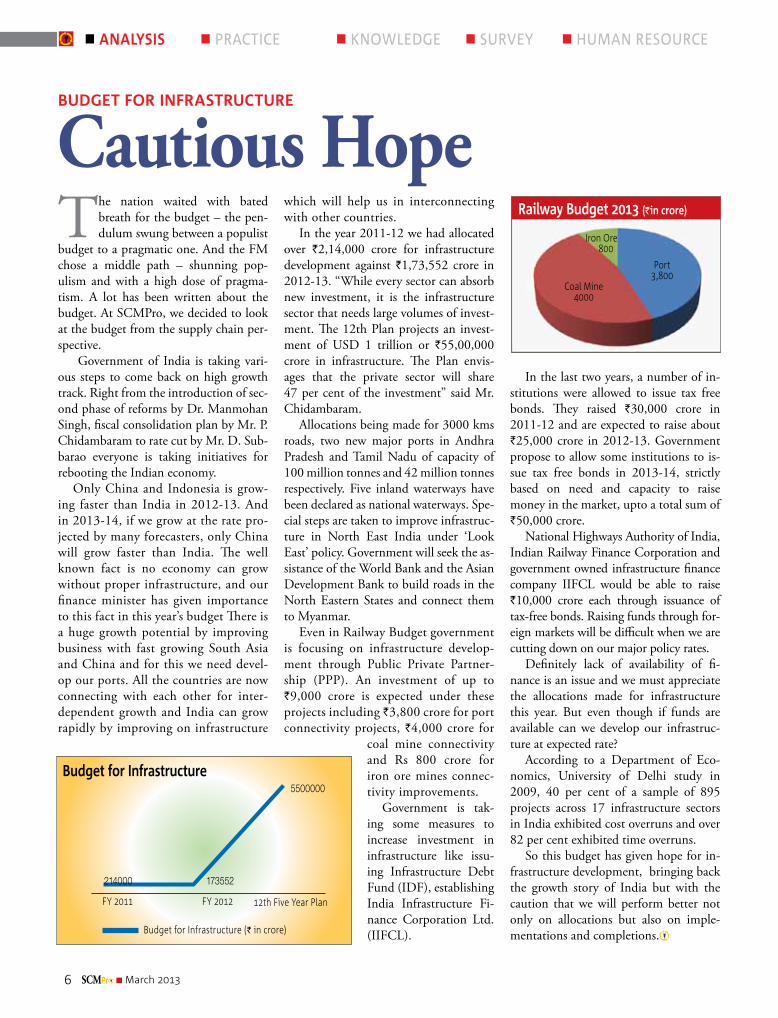

The nation waited with bated breath for the budget – the pen-dulum swung between a populist

budget to a pragmatic one. And the FM chose a middle path – shunning pop-ulism and with a high dose of pragma-tism. A lot has been written about the budget. At SCMPro, we decided to look at the budget from the supply chain per-spective.

Government of India is taking vari-ous steps to come back on high growth track. Right from the introduction of sec-ond phase of reforms by Dr. Manmohan Singh, fiscal consolidation plan by Mr. P. Chidambaram to rate cut by Mr. D. Sub-barao everyone is taking initiatives for rebooting the Indian economy.

Only China and Indonesia is grow-ing faster than India in 2012-13. And in 2013-14, if we grow at the rate pro-jected by many forecasters, only China will grow faster than India. The well known fact is no economy can grow without proper infrastructure, and our finance minister has given importance to this fact in this year’s budget There is a huge growth potential by improving business with fast growing South Asia and China and for this we need devel-op our ports. All the countries are now connecting with each other for inter-dependent growth and India can grow rapidly by improving on infrastructure

which will help us in interconnecting with other countries.

In the year 2011-12 we had allocated over `2,14,000 crore for infrastructure development against `1,73,552 crore in 2012-13. “While every sector can absorb new investment, it is the infrastructure sector that needs large volumes of invest-ment. The 12th Plan projects an invest-ment of USD 1 trillion or `55,00,000 crore in infrastructure. The Plan envis-ages that the private sector will share 47 per cent of the investment” said Mr. Chidambaram.

Allocations being made for 3000 kms roads, two new major ports in Andhra Pradesh and Tamil Nadu of capacity of 100 million tonnes and 42 million tonnes respectively. Five inland waterways have been declared as national waterways. Spe-cial steps are taken to improve infrastruc-ture in North East India under ‘Look East’ policy. Government will seek the as-sistance of the World Bank and the Asian Development Bank to build roads in the North Eastern States and connect them to Myanmar.

Even in Railway Budget government is focusing on infrastructure develop-ment through Public Private Partner-ship (PPP). An investment of up to `9,000 crore is expected under these projects including `3,800 crore for port connectivity projects, `4,000 crore for

coal mine connectivity and Rs 800 crore for iron ore mines connec-tivity improvements.

Government is tak-ing some measures to increase investment in infrastructure like issu-ing Infrastructure Debt Fund (IDF), establishing India Infrastructure Fi-nance Corporation Ltd. (IIFCL).

In the last two years, a number of in-stitutions were allowed to issue tax free bonds. They raised `30,000 crore in 2011-12 and are expected to raise about `25,000 crore in 2012-13. Government propose to allow some institutions to is-sue tax free bonds in 2013-14, strictly based on need and capacity to raise money in the market, upto a total sum of `50,000 crore.

National Highways Authority of India, Indian Railway Finance Corporation and government owned infrastructure finance company IIFCL would be able to raise `10,000 crore each through issuance of tax-free bonds. Raising funds through for-eign markets will be difficult when we are cutting down on our major policy rates.

Definitely lack of availability of fi-nance is an issue and we must appreciate the allocations made for infrastructure this year. But even though if funds are available can we develop our infrastruc-ture at expected rate?

According to a Department of Eco-nomics, University of Delhi study in 2009, 40 per cent of a sample of 895 projects across 17 infrastructure sectors in India exhibited cost overruns and over 82 per cent exhibited time overruns.

So this budget has given hope for in-frastructure development, bringing back the growth story of India but with the caution that we will perform better not only on allocations but also on imple-mentations and completions.

Budget for infrastructure

Budget for Infrastructure

FY 2011

Budget for Infrastructure (` in crore)

FY 2012 12th Five Year Plan

214000 173552

5500000

Cautious Hope Railway Budget 2013 (̀ in crore)

Iron Ore 800

Port 3,800

Coal Mine 4000

n analysis n Practice n knowledge n Survey n human reSource

guru speak

7SCMPr March 2013

Mahender Singh Executive Director MIT Global Scale Network in Asia &Ken Cottrill : Global Communications Consultant MIT Center For Transportation & Logistics

SoutheaSt aSia’S Supply Chain Challenge

Building a Platform for growthThe Stage is Set for Southeast Asia to take its place as a world-leading trading power.

The countries of Southeast Asia are an integral part of the Asian economic miracle. In addition to benefiting from the growth

of China and India, domestic markets in Southeast Asia are expanding and the region is forging stronger links with other develop-ing economies. The Association of Southeast Asian Nations (ASEAN) is actively working on creating a single market that will compete with other international economic commu-nity in terms of its global and regional influ-ence as a trading bloc.

However, if such a vision is to be realized, one of the things that Southeast Asia must focus on is developing world class supply chains. Presently inconsistent quality and availability of transportation infrastructure is impeding the flow of goods in the region, and adding significant cost to logistics op-erations. Cutting-edge supply chain exper-tise can address some of these challenges and drive economic growth.

Located in the heart of a vibrant eco-nomic zone, ASEAN countries have a com-bined population of 600 million people and a GDP of $1.5 trillion. They generate $1.7 trillion worth of trade annually, a figure that is likely to increase significantly if South-east Asian countries maintain projected growth rates of 5 to 6 per cent over the next few years.

ASEAN aims to establish a single market, the ASEAN Economic Community (AEC),

by 2015. Ministers at an AEC Council meeting this May noted that implementa-tion of the AEC blueprint has progressed, particularly in “creating a single market and production base, as well as establishing a competitive economic region.” But more importantly, regardless of whether the target date for creating the new community is met, the goal is indicative of the region’s econom-ic ambitions. Another reason to believe that Southeast Asia is on the cusp of a new era of prosperity is that its expansion is fuelled by several new sources that reinforce its links with regional and global economies. Some of these sources are presented below:

China and India: Together these coun-tries are the engine that drives much of the world’s trade and investment. Accordingly, the exports from ASEAN countries to China and India have almost tripled over the last decade (see Table 1 and Table 2). The volume of trade is expected to climb even further as Chinese and Indian consumers gain more purchasing power and create greater demand for products manufactured in neighboring countries.

Also of note is China’s increasing invest-ment in emerging economies, especially in commodities. ASEAN nations that stand to benefit from these investments include Indonesia (coal, palm oil, and natural gas), Thailand (rubber), and Malaysia (palm oil, natural gas, oil).

Emerging Markets: Southeast Asia will

guru speak

8 SCMPr March 2013 8

benefit from closer ties with other emerging economies, a direct consequence of increas-ing South-South cooperation. In its Asian Development Outlook 2011 report, the Asian Development Bank (ADB) suggests that developing countries should strengthen their “intra” economic links. In the words of Changyong Rhee, ADB’s Chief Economist, “Growing South-South relations at a time of modest growth in industrial economies could be a potential new driver of global growth, but only if these economies become more open to trade and capital flows with each other.”

While world trade has, on average, ex-panded by 16% over the period 2004–2008, Asia’s trade with the Middle East and Latin America has increased by an average of 30% during this time. The region’s trade with oth-er emerging economies stood at 13% of total exports out of Asia in 2008.

As the economic and financial linkages between these emerging economies solidify, the benefits in vital areas including trade, finance, investment, energy and technology will significantly increase. But stronger eco-nomic ties with new partner countries will require Southeast Asia to develop supply chains capable of supporting the increase in international trade volumes.

Sector Based IssuesGrowth in the region will drive demand for sector-based supply chain solutions to ad-dress the needs of different industries.

Construction: According to the ADB, approximately 44 million people are being added to Asia’s urban population every year. Furthermore, there are plans for massive investment in infrastructure development to sustain the economic competitiveness of the region. The ADB estimates that Asia will require about $8 trillion of infrastructure in-vestment during 2010-2020.

Commodities: The region is expected to benefit from robust demand for raw ma-terials from China and India. In partic-ular, rapid urbaniza-tion in both nations will continue to stimulate demand

for commodities, mainly agricultural and energy products.

Manufacturing: A complex web of inte-grated production facilities has developed in the region over recent decades, most notably in the auto industry. The growth in intra-Asian trade has promoted vertical speciali-zation within this network. More foreign direct investment coupled with increasing trade in intermediate goods is expected to further strengthen Southeast Asia’s manufac-turing base and boost growth.

Clouds on the HorizonWhile the outlook appears bright for South-east Asia as a regional and global trading bloc, some difficult hurdles remain. One of the most challenging is poor supply chain infrastructure, which if not addressed, would continue to impede future growth.

The following key issues were laid out by ASEAN Deputy Secretary-General, S. Push-panathan, in a paper presented at the 24th Asia-Pacific Roundtable, Kuala Lumpur, Malaysia, June 2010.

Fragmented roads: Over the last dec-ade, the number of vehicles has doubled in countries such as Indonesia, Vietnam, Cam-bodia, and Myanmar, but the development of respective highway systems has lagged be-hind. The quality and capacity of roads vary greatly from country to country. Singapore boasts fully paved networks, while in Cam-bodia and Lao PDR less than 10% of the highway networks are paved.

A Trans-Asian Highway is under con-struction, and the 38,400 kilometer-route will run through all 10 ASEAN countries when complete. About 97% of the desired length of highway had been built by 2008, but critical links are missing and the quality of some roads is questionable.

Gaps in rail transportation: Over recent years the development of new rail links “has not been substantial” in any of the ASEAN countries except Vietnam, according to Pushpanathan. A flagship project is the Sin-gapore-Kunming Rail Link (SKRL). Sched-uled for completion by 2015, the SKRL line is built on existing national networks and will span seven ASEAN countries. Complet-ing key links in the route will require sub-stantial resources.

Table 1 Exports to China and India% of total exports (average)

Value (USD mil)

ASEAN - 5 2010 15.0 $17,703.1

ASEAN - 5 2000 5.3 $ 2,581.0ASEAN -5 Share of total exports and value of exports to China and India

guru speak

9SCMPr March 2013

Uneven port development: Maritime transportation is crucial to the region’s eco-nomic future and forty-seven designated ports in nine countries form the backbone of the trans-ASEAN port network. Singa-pore and Malaysia’s Port Klang are lead-ing facilities; the remaining gateway ports vary greatly in terms of their cargo handling capabilities.

Air shortfalls: A number of ASEAN member states have invested in airport im-provements, and facilities are generally re-garded as adequate for current traffic levels in capital cities. However, freight handling terminals in some airports do not meet the required standards.

Logistics services represent another im-portant piece of the region’s supply chain puzzle. The ASEAN Roadmap for Integra-tion of Logistics Services Sector aims to lib-eralize these services and related activities to rapidly enhance regional logistics capabili-

ties. The Framework Agreement on Services sets a deadline of 2013 for finalizing com-mitments in this area.

Meanwhile, Southeast Asia’s growing eco-nomic influence is attracting attention from technology vendors. “Supply chain technolo-gies in Southeast Asia are poised to grow on the back of increased requirements for more efficient supply chain operations and end us-ers’ need to reduce logistics costs,” concludes a report published in December 2010 by research firm Frost & Sullivan. The report, 2020 Supply Chain Technology RoadMap; Southeast Asia, looks at the demand for trans-portation management systems (TMS) and warehouse management systems (WMS) in Singapore, Malaysia, Indonesia, and Vietnam.

TMS is the umbrella term for software solutions that manage freight transportation operations, and WMS solutions manage the movement and storage of materials in ware-houses. Both types of software are important

components of supply chain management solution suite. However, the high initial cost of staff training often deters smaller logistics companies from investing in the technology according to the report. Disparities between transportation networks make it difficult to adopt TMS and WMS solutions. Also, “in countries such as Indonesia and Vietnam, advanced telecommunication infrastructure is exclusive to the major cities, making cargo tracking difficult in the rural areas,” says Frost & Sullivan.

Looking ahead, the adoption of TMS will “be driven by the need to remain competi-tive and cater to rising business opportuni-ties from a growing manufacturing base in Southeast Asian countries,” the firm says. It sees demand for WMS coming from large logistics and manufacturing companies, and logistics park developers.

The Way AheadSoutheast Asia is uniquely positioned to benefit from the global shift in economic power from west to east. But if the region is to realize its full potential, a top priority must be the development of world class supply chain fa-cilities and expertise.

The region’s inadequate infrastructure and supply chain services add cost and ham-per goods flows. A 2008 ASEAN study cited by Pushpanathan estimates the logistics costs associated with the intra-ASEAN movement of freight containers as $2.25 billion a year. Transportation, terminal, and access costs account for about 55% of this total, and 45% are attributed to time costs. Imple-menting an ASEAN blueprint for improv-ing the efficiency of distribution networks would reduce logistics costs by roughly $140 million per year according to the study.

Similar efforts are required to build a supply chain talent pipeline. The skills needed to man-age supply chains have changed dramatically over recent decades. Overlay these changes with the specific needs of Southeast Asian businesses, and it becomes apparent that in order to compete effectively in regional and global markets, Southeast Asia must invest in supply chain education and research.

Table 2 China IndiaGrowth potential

n GDP Growth forecast: 2011 - 2016: 9.5% (2000 - 2010: 10.3%)n GDP Per Capita : $ 8,118 in 2016 (2010: $ 4382; 2000: $946)

n GDP Growth forecast: 2011 - 2016: 8.1% (2000 - 2010: 7.3%)n GDP Per Capita : $ 2,110 in 2016 (2010: $ 1,265; 2000: $ 460)

Trade with ASEAN-5

Total: $109.4 bn in 2010(2000: $36.1 bn)

Total: $37. 2 bn in 2010(2000: $ 6.5 bn)

China And India’s growth potential and trade with ASEAN-5

insight

10 SCMPr March 2013

A long time ago I got my doctoral de-gree from the University of Penn-sylvania’s Wharton School of Busi-ness in an area called Operations

Research (O.R.). As a newly minted gradu-ate, I’d explain to people unfamiliar with the discipline that it involved the use of the scientific method and quantitative analysis to solve business problems. I had been trained in decision making, quantitative modeling, and optimization techniques.

When someone would ask what my favour-ite graduate course was, I would carry on ex-citedly about my methodology course. It was taught by a famous professor who delighted students with stories about companies that had successfully used O.R. to solve some of their most pressing business problems. Math applied to the real-world of business—what course content could be better than that? At least that’s what I thought at the time.

Finance is the Language of BusinessFast forward to a recent discussion I had with some colleagues about courses that should be added to a supply chain program. When asked for my opinion, I responded “Introduction to Accounting.” Why accounting and not O.R. methodology? I’ll try to explain below.

During my 35-plus years of business experi-ence, several things have made me realize the importance of accounting and financial reports to understanding what really makes a business tick. Here are several points to consider.

In one of my SCMR column titled “The Operational Performance Triangles,” I pre-sented a triangle that can be used to help con-ceptualize whether a balanced set of operational

performance objectives align to competitive corporate strategies. Two points of the triangle, Efficiency and Asset Utilization, represent those types of performance objectives that directly af-fect a company’s income statement and balance sheet, respectively. (The third point on the tri-angle represents Customer Response objectives that do not directly affect financial reports). My point in that column was that supply chain pro-fessionals need to understand how the first two types of operational objectives—efficiency and asset utilization—relate directly to financials.

Second, my research and experience with Sales and Operations Planning (S&OP) proc-esses has convinced me of the critical impor-tance of translating unit-based operational plans into monetary (i.e., financial) terms. In this way, S&OP teams can maintain the visibility they need to help navigate companies towards achieving financial goals—especially those relat-ed to profitability and Return-on-Assets (ROA).

Third, whenever a large-scale project is to be undertaken, a business case analysis must be developed in financial terms.

Fourth, and lastly, I’m now completely convinced that all future supply chain lead-ers will need to be good business people first and supply chain experts second. For this to happen, they must become conversant in the language of business, which is accounting and financially based.

Luckily for me, I took some elective in-troductory courses in economics and ac-counting during my graduate studies in O.R. While the accounting course involved a lot of painstaking, time-consuming de-tailed calculations on paper (we didn’t have today’s computerized spreadsheet software

This article is an extract from Supply Chain Management Review (www.scmr.com) is reproduced with permission.

Dr. Lapide is a lecturer at the University of Massachusetts’ Boston Campus and is an MIT Research [email protected]

Speak Financially, Get Results

Before a Supply Chain project can be started, executives need to be convinced that it will improve financial performance over the long run. By Larry Lapide.

`

insight

11SCMPr March 2013 11

back then), the hard work helped me better understand the financials of an enterprise. I learned to read balance sheets and income statements while developing an appreciation for the value of corporate assets.

Companies spend a substantial amount of upfront money to build assets to manufacture and distribute supply as well as to deploy in-ventories in anticipation of customer demand. They expect to quickly get returns on their in-vestments. Intel, for example, spends billions of dollars to build semi-conductor fabrication plants. So the company operates them 24/7 to make sure that it is maximizing its long-run ROA on these huge investments. Short-term margin and profit generation alone cannot justify these investments.

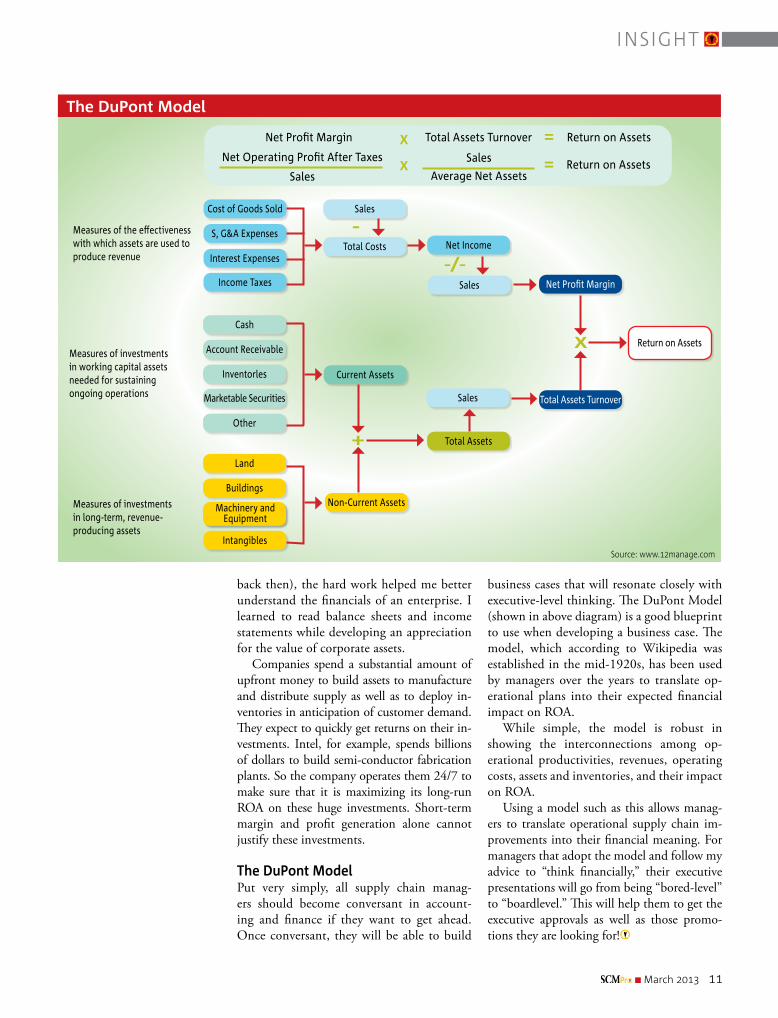

The DuPont ModelPut very simply, all supply chain manag-ers should become conversant in account-ing and finance if they want to get ahead. Once conversant, they will be able to build

business cases that will resonate closely with executive-level thinking. The DuPont Model (shown in above diagram) is a good blueprint to use when developing a business case. The model, which according to Wikipedia was established in the mid-1920s, has been used by managers over the years to translate op-erational plans into their expected financial impact on ROA.

While simple, the model is robust in showing the interconnections among op-erational productivities, revenues, operating costs, assets and inventories, and their impact on ROA.

Using a model such as this allows manag-ers to translate operational supply chain im-provements into their financial meaning. For managers that adopt the model and follow my advice to “think financially,” their executive presentations will go from being “bored-level” to “boardlevel.” This will help them to get the executive approvals as well as those promo-tions they are looking for!

The DuPont Model

Net Profit Margin Total Assets Turnover Return on Assets

Net Operating Profit After Taxes

Sales

Sales

Average Net AssetsReturn on Assets

X

X

==

Cost of Goods Sold

S, G&A Expenses

Interest Expenses

Income Taxes

Cash

Account Receivable

Inventorles

Marketable Securities

Other

Land

Buildings

Machinery andEquipment

Intangibles

Sales

Sales Net Profit Margin

Total Costs Net Income

Current Assets

Sales Total Assets Turnover

Return on Assets

Non-Current Assets

Total Assets

X

+

-/-

Measures of the effectiveness with which assets are used to produce revenue

Measures of investments in working capital assets needed for sustaining ongoing operations

Measures of investments in long-term, revenue-producing assets

-

Source: www.12manage.com

Enabling Food Security to the Nation

Agri Supply ChAin

Agricultural Sector in India is poised to become the reckoning force with well developed Agri Supply Chain Management (ASCM). Girish V.S., Executive Editor explores a way ahead for the sector.

Lead story

12 SCMPr March 2013

Lead story

13SCMPr March 2013 13

Agriculture is the dominant sector of the Indian economy, con-tributing to around 20 per cent of India’s GDP and employing approximately 58 per cent of the Indian Population. Today, India is the second largest producer of food in the world and if

we can back up the agriculture sector, we can easily become the biggest player in the agriculture and food sector. Food security of the nation depends on the continued development of the sector.

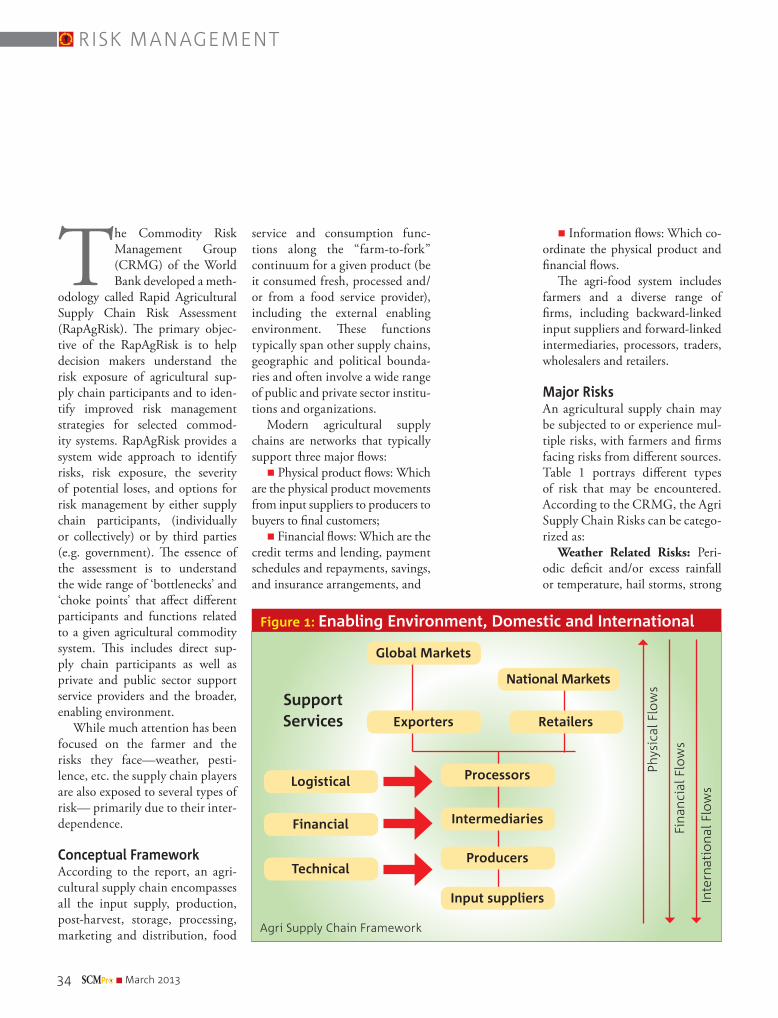

A well developed Agri supply chain is an imperative for the growth of the sector and for food security. Integrated supply chains are one of the most powerful competitive tools in today’s globalizing business economy. For agricultural products, successful supply chain development projects reduce not only the transaction costs but also the institutional barriers that decouple individual links in traditional distribution channels. They allow participants to achieve higher levels of service and to capture sub-stantial added value thereby serving as leverage point both for economic growth and for poverty alleviation. This paper also draws on the experi-ence of the Agri-Chain Competence Center to discuss the critical issues and step-by-step actions necessary to stimulate and support the emer-gence of supply chains in developing countries.

For this issue of SCM Pro, we take a close look at Agri Supply Chains. We then move into “Developing the Business Case For Agri SCM”. A

look at how we can create an Agri supply chain, not as a corporate CSR initiative but as a bottom line oriented and profitable venture that can add value to the nation, the citizen and the corporate involved.

The third issue we focus on is the “Agri Supply Chain—Critical Envi-ronmental & Social Impacts”. In the current economic climate, we need to assess the risks associated with sourcing the primary raw materials and examine what sustainable agricultural practice means. We also examine the tradeoffs between sustainability and the availability of economically viable raw materials. And finally the concept of “Triple Bottom line and ASCM” where we characterize the boundaries of the triple bottom line and the methodologies for reducing upstream impact.

Our next focus is “Building Supply Chain Partnerships”, where we look how customer oriented Agri supply chains have an enormous re-ciprocal effect on each of the successive entities involved in the chain in-cluding quality and/or freshness of products, reduction of product losses during storage and transportation, and how it helps entities in the supply chain generate higher value addition.

We move on to “Collaborating With Global Governments, NGOs, Brokers & Financing Entities”. A critical look at some of the external players who can affect the agri supply chains and the role they play in creating a vibrant Agri Supply Chain. We examine the key impact and concerns including carbon, fertilizers, soil fertility, land use, energy usage, farmer social impacts and food safety regulations.

And finally we look at Agri Supply Chain Risk Management. Due to the increasing spread of risks and massive structural changes in global and national Agri-food systems—farmers, agribusiness firms, and gov-ernments face new challenges in the design of resilient agri supply chain systems. We take a look at a conceptual framework and set of detailed guidelines for conducting systematic assessments of risk and vulnerability within agricultural supply chains - The Rapid Agricultural Supply Chain Risk Assessment developed by the World Bank.

Happy reading.

Enabling Food Security to the Nation

14 SCMPr March 2013

Building a Viable and Sustainable Supply ChainAn Efficient Agri Supply Chain requires specialised abilities for greater returns for all the partners.

lead story

lead story

15SCMPr March 2013 15

Agri Supply chains are complex arrangements that link consumers, retailers, distributors,

marketers (Or middle men as we know them), processors and pri-mary producers. As goods and pro-duce move across the supply chain, they accrue value. One broad clas-sification of Agri Supply Chain is the pre-processing chain—from the farmer to the processor and the post-process chain—from the processor to the consumer. In In-dia, the Agri Supply Chains is frag-mented across both the sections.

The theory behind Agri supply chains inform us that the farmers,

Benefits of Agri Supply Chainn Improved margins for growers and farmersnImproved knowledge of demand and pricesnReduction of product losses during storage and transportation nImproved product quality and /or freshnessnImproved safety of food products nSales can be increased significantly nHigh value added products can be produced

brokers and processors associ-ate themselves through a supply chain, coordinate their value cre-ating activities with one another and in the process create greater value than they can when they operate independently. This in India is often a pipe dream.

Agri Supply chains create syn-ergies in multiple ways. Agri Sup-ply Chains expand traditional markets and increase sales vol-ume for farmers. They have the potential to reduce the delivery cost and increasing the profits to the farmers. In addition they help identify untapped market segment for the produce. In this way, they allow chain members to charge higher prices.

Farmers in India can benefit by joining supply chains. When farmers join a supply chain, they can decide whether they will tar-get their production for upscale, product differentiated markets (like MacDonald’s) or down scale, commodity markets—where the bulk of Indian agri produce are consumed. Agile and innovative Agri-Supply chains allow farmers to improve their profits, realize higher savings, adapt their crops, and supply chain alignment to changing market circumstances. Similarly, competition among chains for good products from farmers, provides an opportunity for farmers to rise above a transac-tional relationship, creating better opportunities for themselves.

In India, the infrastructure connecting the farmer to the

mandi and there on to the other partners in the value chain is very weak. All of these players - the farmers, wholesalers, manufactur-ers, retailers all operate in silos. Lack of adequate demand informa-tion compels the farmer to produce a crop first and then try to sell it. The mantras that brought efficien-cy in manufacturing like—manag-ing financial flow, supply-demand matching, demand forecasting, in-formation sharing, efficient trans-port scheduling are absent from the Indian agriculture sector. The current Agri Supply chain in India has too many intermediaries who distort prices, exploit farmers and prevent produce and other goods from reaching places where de-mand exists

The association of the farmer and the supply chain can take mul-tiple forms and may include co-operative bodies, associating as a trading community, corporate, or contractual tie-ups. Well-designed supply chains are capable of realiz-ing several kinds of captured value for their participants. Each sector of the agricultural sector—fisher-ies, meat and poultry, vegetables and fruits and cereals and grains need a slight modification in the supply chain, but the fundamen-tal drivers of all these remain the same—an ability to understand consumer demand, identify op-portunities and get the produce to the right place at the right time with the required quality. In India, they all share the ineffi-ciencies too.

lead story

16 SCMPr March 2013

Drivers of Agri Supply Chain India is a country with a popula-tion of 1.2 billion. This population contains the celebrated “bottom of the pyramid” as well as the top of the pyramid. These layers of the pyramid have different require-ments from the agri sector. The middle and top of the pyramid are increasingly demanding eco-logical and socio -economic sus-tainability of agricultural produc-tion and are concerned with food safety. The bottom of the pyramid demands that the produce reaches them in daily schedule at lowest possible prices.

To develop an efficient Agri Supply chain requires specialized abilities—Capturing the consumer preferences as they evolve, pack-aging design, process integration and keeping the information flows among all the stakeholders smooth.

Experts advocate adapting one of the three general strategies for or-ganizing Agri Supply Chain: Supply chain differentiation; integral chain and quality assurance. The exact strategy will depend on the local requirements and capabilities of the players.

If specific segments of consum-ers demand specific products, or the local cultural sensitivities de-mand that products be segregated —like vegetarian and non-vegetar-ian products cannot be mixed in a single transport schedule in India. (Reliance retail had to move its non-vegetarian section to a sepa-rate shop!) Under such demands, supply chain differentiation is a good strategy.

As the income levels rise and distances between the producer and consumer increases, supply chain quality becomes very impor-tant. Especially for perishables like fruits, vegetables, fish and meat products. Development and im-plementation of quality assurance concepts in Agri Supply chain with

suppliers and customers, and set-ting up tracking & tracing systems enable agro-processing companies and retailers to assure the quality and safety of food.

In addition as supply chains grow more complex with multiple layers, we need to look at supply chain re-engineering. This rising complexity and the increased competition, will force all stakeholders to seek sources of competitive advantage which are based upon cost reduction, cycle time improvement while at the same

time seek differing value-added and productivity gains and customer value driven initiatives.

There are quite a few innovative ideas from homegrown social enter-prises in this sector. A good example is Jagruti Agro Tech, which focuses on three issues that hurt Indian ag-riculture—lack of farm inputs, lack of customer preference information, and lack of a viable supply chain. Jagruti works with the farmers di-rectly, planning the produce, using information technology to iron out the kinks in the production and supply chain, and connecting the farmer directly to the consumer, thereby increasing the revenue to the farmer and reducing the final price to the consumer.

Developing a viable Agri Supply ChainThere are a few basic approaches to developing a viable agri supply chain. The first is an analysis of the existing system, its commer-cial viability, and the ecosystem it

serves. After this, we can begin the process by examining the adjacent entities in the value chain – can we create a commercially, techni-cally and workable collaboration between these entities. The other elements that need to get atten-tion are: the supply chain should be sensitive to evolving customer preferences, skill development and creating a pool of supply chain specialists who can analyze, plan and implement a winning supply chain solution. This is a grey area

in India with not too many in-stitutes focusing on supply chain management, leave aside agri sup-ply chain management.

Co-operation among the stake holders in the supply chain enables the retailer to convey the customer demand and preferences in time to enable the producer alter his pro-duce to meet the demand. And the sum total efforts of each individual is higher than the individual efforts, getting safe, fresh products to the consumer at a lower price and at the same time ensuring better returns for the farmer.

The Indian farmer is suspicious of any development that disturbs the status quo, but is willing to ac-cept the change if it can be shown to be beneficial. Mr. Radheshyam Chandak of Buldana Urban Co-Op Credit society demonstrated this amply—under the “Gramin Godam Yojana” he has built over 300 godowns in Buldana and all of them are fully utilized by the farm-ers from the region.

Jagruti works with the farmers directly, planning the produce, using information technology to iron out the kinks in the production and supply chain.

As is well known Indian economy till

very recently was pre dominantly

an agrarian economy. Even now

over 60 % of India’s population resides in

villages/ rural areas and is in some man-

ner dependent on the agriculture sector.

It therefore, is indeed heartening that con-

certed attempts are now afoot to ensure

that the Indian farmer/ grower is ensured

optimal realization for his produce being

sold both in the domestic and internation-

al markets. An important pre requisite for

the same is availability of quality produce

at the retail outlets/ market end which

calls for an efficient and reliable supply

chain which is in its infancy in India. It is

also an established fact that a substantial

part of our agricultural produce is wasted

on account of poor handling and lack of

required infrastructure both at the pro-

duction and consumption centers.

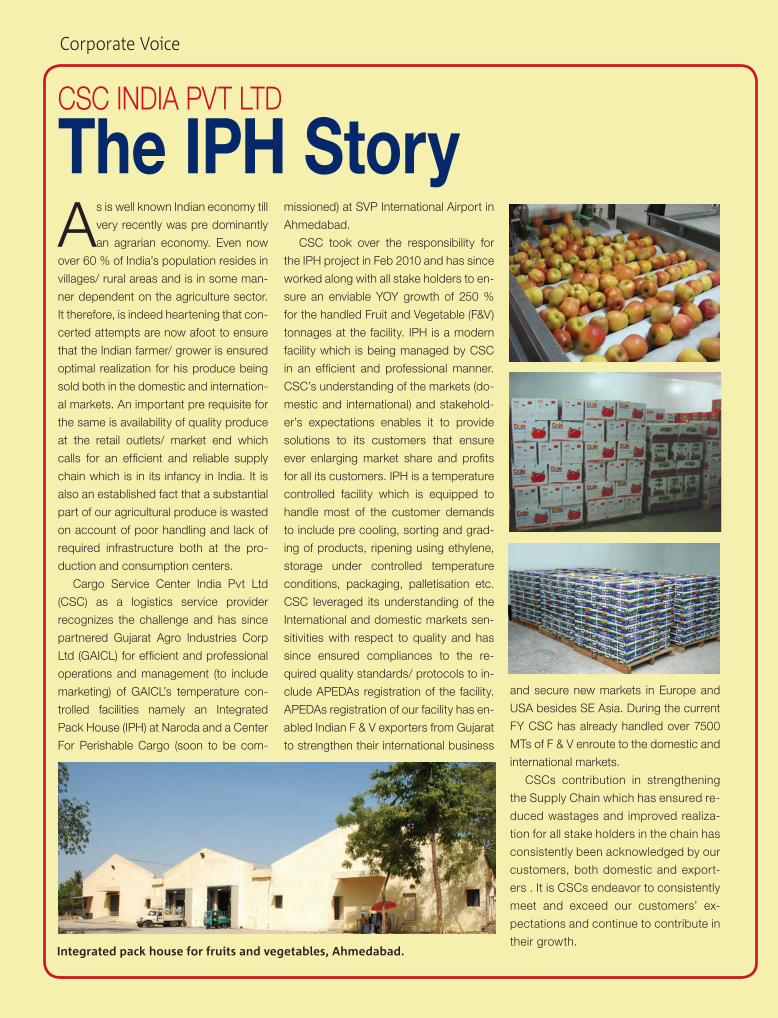

Cargo Service Center India Pvt Ltd

(CSC) as a logistics service provider

recognizes the challenge and has since

partnered Gujarat Agro Industries Corp

Ltd (GAICL) for efficient and professional

operations and management (to include

marketing) of GAICL’s temperature con-

trolled facilities namely an Integrated

Pack House (IPH) at Naroda and a Center

For Perishable Cargo (soon to be com-

missioned) at SVP International Airport in

Ahmedabad.

CSC took over the responsibility for

the IPH project in Feb 2010 and has since

worked along with all stake holders to en-

sure an enviable YOY growth of 250 %

for the handled Fruit and Vegetable (F&V)

tonnages at the facility. IPH is a modern

facility which is being managed by CSC

in an efficient and professional manner.

CSC’s understanding of the markets (do-

mestic and international) and stakehold-

er’s expectations enables it to provide

solutions to its customers that ensure

ever enlarging market share and profits

for all its customers. IPH is a temperature

controlled facility which is equipped to

handle most of the customer demands

to include pre cooling, sorting and grad-

ing of products, ripening using ethylene,

storage under controlled temperature

conditions, packaging, palletisation etc.

CSC leveraged its understanding of the

International and domestic markets sen-

sitivities with respect to quality and has

since ensured compliances to the re-

quired quality standards/ protocols to in-

clude APEDAs registration of the facility.

APEDAs registration of our facility has en-

abled Indian F & V exporters from Gujarat

to strengthen their international business

and secure new markets in Europe and

USA besides SE Asia. During the current

FY CSC has already handled over 7500

MTs of F & V enroute to the domestic and

international markets.

CSCs contribution in strengthening

the Supply Chain which has ensured re-

duced wastages and improved realiza-

tion for all stake holders in the chain has

consistently been acknowledged by our

customers, both domestic and export-

ers . It is CSCs endeavor to consistently

meet and exceed our customers’ ex-

pectations and continue to contribute in

their growth.

Corporate Voice

CSC INDIA PVT LTD The IPH Story

Integrated pack house for fruits and vegetables, Ahmedabad.

18 SCMPr March 2013

A Business Case for Agri Supply Chain Management

Agri Supply Chain Should not be restricted to the CSR initiatives of a few large corporates. It is time to develop a business case for ASCM.

lead story

lead story

19SCMPr March 2013 19

A Business Case for Agri Supply Chain Management Agri Supply Chains are

struggling to attract investors in India. Any investment that comes

in has shades of Corporate Social Responsibility (CSR) attached to them. It is true, Agri Supply Chain programs provide chain entities with that feel-good aura

of social responsibility – that they are doing something for the farm-ers and probably as a proof that they are model corporate citizens. However, it’s time ASCM should develop a business case for the better returns for all the partners involved in the value chain.

But does a business case exist

for establishing Agri Supply Chain? Liberalization, globalization and ever increasing consumer demand across the world create compulsive arguments for export of a wide va-riety of higher margin agricultural products from India. These include, but are not limited to organically grown products, fishery products, exotic fruits and vegetables, and off-season fresh fruits and vegetables to open up new opportunities for our farmers and agri-businesses.

The market for Indian agri pro-duce is undeniable. What we lack is the ability to move the product from the farm to the fork – a serious lack of an integrated supply chain. It is very clear that global market standards are very stringent. Con-sumers in developed countries and in urban areas in India and other developing economies demand fresh, safe and nutritional food, excellent quality and just-in-time delivery. This presents major chal-lenges to Indian farmers and busi-nesses since we lack state-of-the-art technologies and infrastructure. These new developments puts pres-sure on the supply chains and any flaws in the system are magnified many times.

The supply chain of the day is a linear structure, where farm-ers, middlemen, processors, dis-tributors and retail outlets forms a short-term partnerships independ-ent from the other members of the

lead story

20 SCMPr March 2013

chain. This is a highly inefficient model that restricts the player’s ability to respond to changes in supply and demand. Since none of these partnerships are for the longer term, they tend to limit productivity improvements and re-strict innovation, creating wasteful processes and environmental deg-radation.

Supply chain management is a powerful tool to integrate farmers, processors, distributors and retail outlets. Through such integrated Agri Supply chains, producers in developing countries like India can get access to demand and price information to fine tune their pro-duction and processing. However, developing cross-border supply chains is complex, and requires in-formation and expertise about how to build chains. For a cross border Agri Supply chain to reap its po-tential benefits, all the chain part-ners should commit themselves and ensure free flow of information across the chain. The advantages of an Agri Supply chain are numer-ous—like the reduction of product losses, increase in sales, reduction of transaction costs, a better con-trol of product quality and safety and the dissemination of technol-ogy, capital and knowledge among the chain partners.

An efficient Agri Supply chain development not only benefits the immediate stakeholders but also stimulates economic, social and sustainable development in the country. Development of the in-stitutional infrastructure for Agri Supply chain plays an important role in creating an enabling envi-

ronment for development. This might even take the form of a public private partnership (PPP) sharing experiences, risks and bot-tlenecks. In India, supply chain de-velopment is often hampered due to lack of support from the govern-ment and other statutory bodies.

Building Supply ChainsBuilding a supply chain requires consistent commitment, compe-tencies and resources of all the en-tities involved. This is not an easy task. The first step is to develop the right chain organization. And if

the chain extends beyond national borders, special care is required as differences in culture and business practices can have large influences in chain performance and the col-laboration between the players.

An efficient Agri Supply chain development begins with an analy-sis of the existing flow of goods and information along the chain, and the ecosystem - product flow, exchange levels, forces affecting the operation of the supply chain such as governmental policies, etc. This will lead to the identification of po-tential supply chain partners, their

function, role and contribution to the value chain.

It has been observed that the success of a supply chain depends on the chain leader. The chain lead-er should act as the supply chain manager. The chain leader has to be accepted by every member of the chain. If this does not happen, the chain is bound to create bottle-necks and eventually breakdown, with disastrous consequences for every one concerned.

The chain partners should set the parameters such as flexibility, efficiency, innovation, responsive-

ness, cost and information flow etc. that will be used to measure the performance of their chain.

Supply Chain Management and its BenefitsThe question we need to answer is—does all of these make business sense? An efficient Supply chain yields lower transaction costs and increased margins. but due to mul-tiple activities and layers involved it demands a multidisciplinary ap-proach and sustainable trade rela-tions. Supply chain partnerships are based on inter-dependence, trust, open communication and mutual benefits.

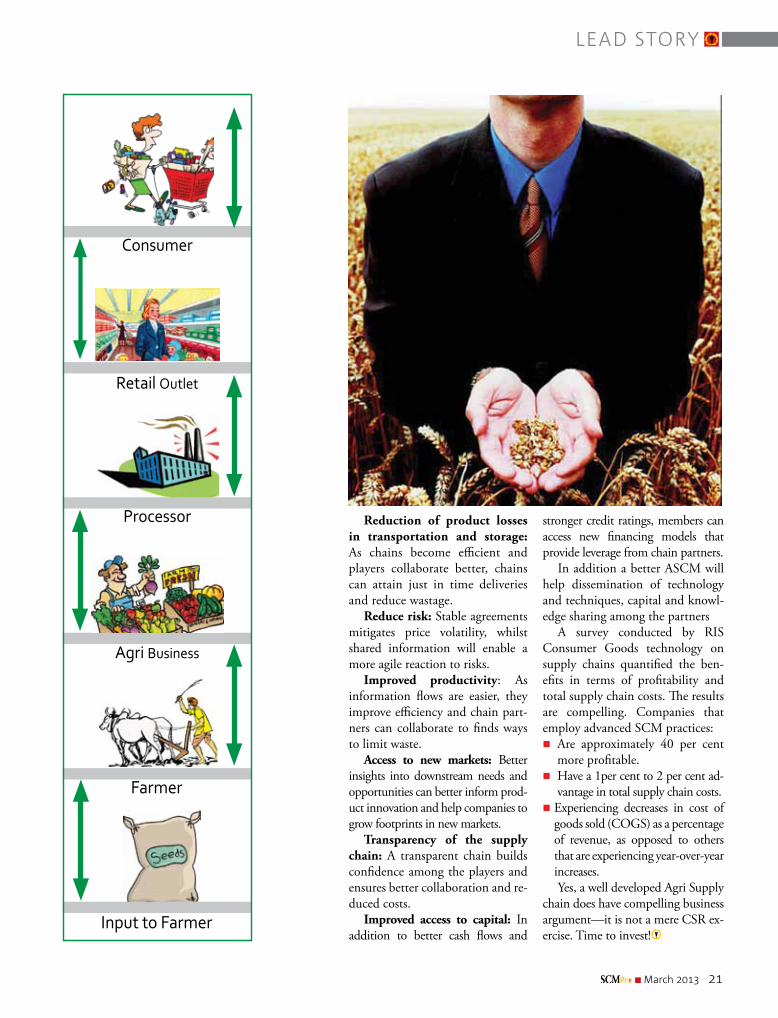

The generic benefits of an agri supply chain are:

Increasing of sales: Efficient chains can lower the total cost of goods, spurring demand and increase in sales.

A transparent chain builds confidence among the players and ensures better collaboration and reduced costs.

Consumer Goods Segment

COGS % of revenue

Year over Year Change in COGS

Total Supply Chain Costs % of revenue

Profitability

Mature SCM Companies 46.50% -3.20% 8% 23.40%

Immature SCM Companies 50.10% 2.80% 10% 10.90%

lead story

21SCMPr March 2013

Reduction of product losses in transportation and storage: As chains become efficient and players collaborate better, chains can attain just in time deliveries and reduce wastage.

Reduce risk: Stable agreements mitigates price volatility, whilst shared information will enable a more agile reaction to risks.

Improved productivity: As information flows are easier, they improve efficiency and chain part-ners can collaborate to finds ways to limit waste.

Access to new markets: Better insights into downstream needs and opportunities can better inform prod-uct innovation and help companies to grow footprints in new markets.

Transparency of the supply chain: A transparent chain builds confidence among the players and ensures better collaboration and re-duced costs.

Improved access to capital: In addition to better cash flows and

stronger credit ratings, members can access new financing models that provide leverage from chain partners.

In addition a better ASCM will help dissemination of technology and techniques, capital and knowl-edge sharing among the partners

A survey conducted by RIS Consumer Goods technology on supply chains quantified the ben-efits in terms of profitability and total supply chain costs. The results are compelling. Companies that employ advanced SCM practices: n Are approximately 40 per cent

more profitable.n Have a 1per cent to 2 per cent ad-

vantage in total supply chain costs.n Experiencing decreases in cost of

goods sold (COGS) as a percentage of revenue, as opposed to others that are experiencing year-over-year increases.Yes, a well developed Agri Supply

chain does have compelling business argument—it is not a mere CSR ex-ercise. Time to invest!

Input to Farmer

Farmer

Agri Business

Processor

Retail Outlet

Consumer

22 SCMPr March 2013

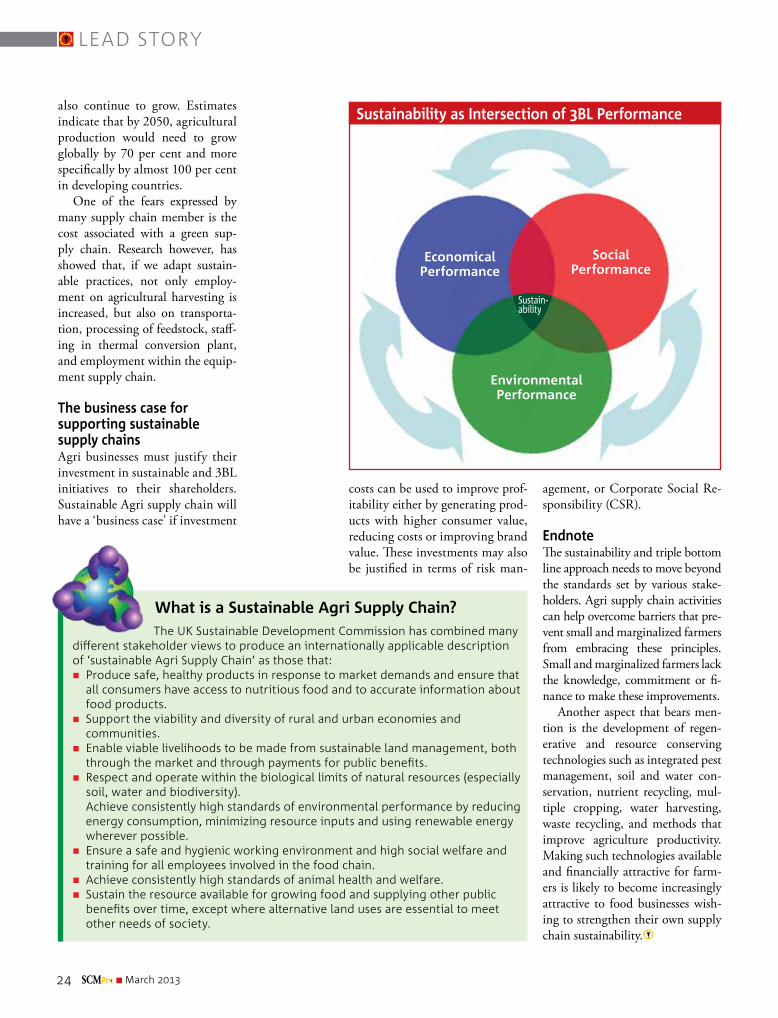

A Triple Bottom LineSustainable business practice needs to have Triple-bottom line (3BL)approach with emphasis on environmental, Social and financial performances.

According to the OECD, Sustainable development refers to development that meets the needs of

the present without compromising the ability of future generations to meet their own needs. Today, sus-tainability is also linked with the implementation of the three pil-lars of sustainable development or

the so-called Triple-Bottom-Line (3BL) with the emphasis on en-vironmental, social and financial performance for the improvement of quality of life of human being. World Business Council of Sus-tainable Development (WBCSD) points out that sustainable devel-opment involves the simultaneous pursuit of economic prosperity,

environmental quality and social equity where companies aiming for sustainability need to perform not against single, financial bottom line but against triple bottom line.

Global warming and the con-cern with climate change have their impact on all aspects of our activi-ties. The world is occupied with creating sustainable business prac-

lead story

Appro Achenvironmental and social impact of ascm

lead story

23SCMPr March 2013 23

manufacturers, retailers, NGOs, governmental and farmers’ or-ganizations is vital in order to raise standards for some supply chains and to enable farmers to adopt more sustainable agricultural prac-tices.

Intersection of Agriculture Supply Chain and SustainabilityAn Agri Supply chain starts from the primary inputs to agriculture and ends when the final produce is sold at the retail outlet. This entire chain is fragmented, and owned by multiple stakeholders, who at times may have divergent objec-tives. Given this state of affairs, we need to take into consideration the role of peasants, small farmers and consumers on improving sustain-able supply chain management in the globalized market.

Sustainability in agri supply chain context means meeting the three challenges of the triple bot-tom line effectively.

Profit—creating avenues for rev-enue and the viability and competi-tiveness of the agricultural sector;

Planet—promoting good envi-ronmental practices;

People—improve the living conditions and economic opportu-nities in rural areas.

Productivity and sustainabilityThe demand for food, feed and biofuel is growing at a very rapid pace. As population increases and as people in economies like India and China start consuming more, this trend will continue. It is esti-mated that the world population will be 9 billion by 2050, up from the current population of 7 bil-lion. In addition, income will in-crease, changing the quantity and composition of food demand. The use of agricultural commodities in the production of biofuels will

tices. The growing attention paid on sustainable supply chain man-agement in different sectors, is yet to percolate into the agriculture sec-tor. This includes the Agri Supply Chains. The need of the hour is to explore opportunities available for agri businesses to enable consumers to buy fresher and more nutritious agri produce, invest in sustainable manufacturing and distribution systems and to develop procure-ment systems based on more sus-tainable forms of agriculture.

Because of globalization, supply chains involve greater use of trans-portation over longer distances, resulting in significant environ-mental damage and a larger carbon footprint. These concerns induce local behaviours that sometimes may not be socially sustainable. These factors are urging stakehold-ers to consider sustainability - due to both rising concern of national and international regulators and an ever-growing attention of end con-sumers on sustainability.

The important factors in de-veloping sustainable supply chains depend on the type of supply chain involved. A far more difficult and elusive parameter is the attitude and role of the individual business to take responsibility for social and environmental performance within supply chain. Trust and adherence to standards are both important to build more sustainable food supply chains. Cooperation among food

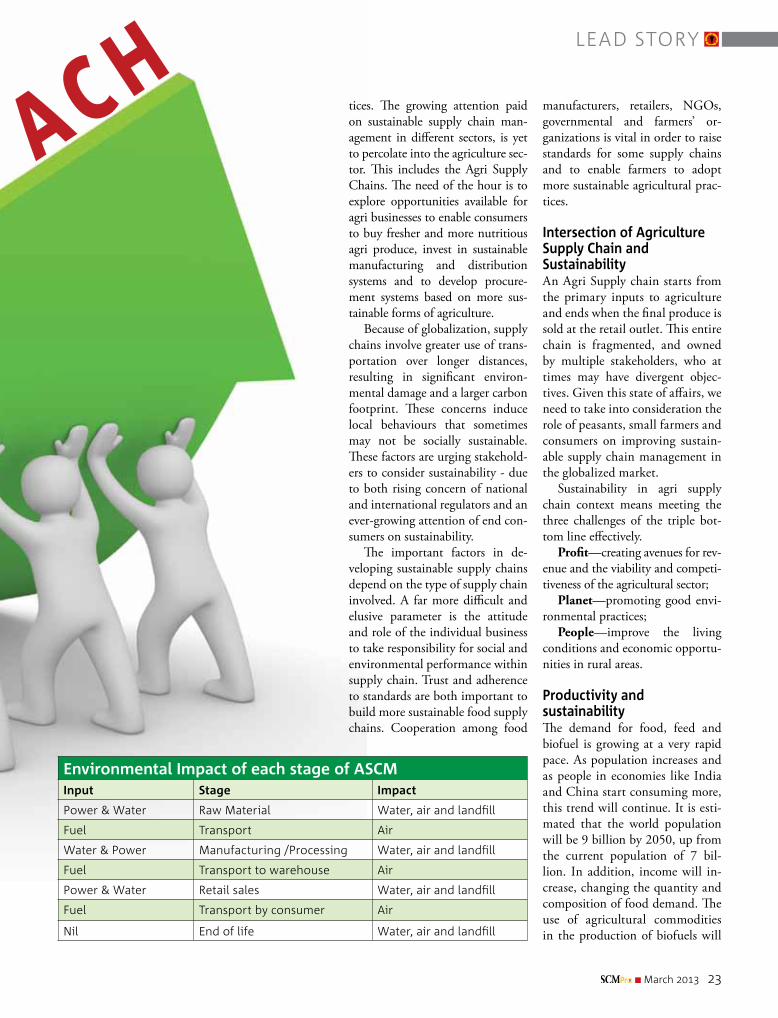

Environmental Impact of each stage of ASCMInput Stage Impact

Power & Water Raw Material Water, air and landfill

Fuel Transport Air

Water & Power Manufacturing /Processing Water, air and landfill

Fuel Transport to warehouse Air

Power & Water Retail sales Water, air and landfill

Fuel Transport by consumer Air

Nil End of life Water, air and landfill

Appro Ach

lead story

24 SCMPr March 2013

also continue to grow. Estimates indicate that by 2050, agricultural production would need to grow globally by 70 per cent and more specifically by almost 100 per cent in developing countries.

One of the fears expressed by many supply chain member is the cost associated with a green sup-ply chain. Research however, has showed that, if we adapt sustain-able practices, not only employ-ment on agricultural harvesting is increased, but also on transporta-tion, processing of feedstock, staff-ing in thermal conversion plant, and employment within the equip-ment supply chain.

The business case for supporting sustainable supply chainsAgri businesses must justify their investment in sustainable and 3BL initiatives to their shareholders. Sustainable Agri supply chain will have a ‘business case’ if investment

costs can be used to improve prof-itability either by generating prod-ucts with higher consumer value, reducing costs or improving brand value. These investments may also be justified in terms of risk man-

agement, or Corporate Social Re-sponsibility (CSR).

EndnoteThe sustainability and triple bottom line approach needs to move beyond the standards set by various stake-holders. Agri supply chain activities can help overcome barriers that pre-vent small and marginalized farmers from embracing these principles. Small and marginalized farmers lack the knowledge, commitment or fi-nance to make these improvements.

Another aspect that bears men-tion is the development of regen-erative and resource conserving technologies such as integrated pest management, soil and water con-servation, nutrient recycling, mul-tiple cropping, water harvesting, waste recycling, and methods that improve agriculture productivity. Making such technologies available and financially attractive for farm-ers is likely to become increasingly attractive to food businesses wish-ing to strengthen their own supply chain sustainability.

Economical Performance

Environmental Performance

Social Performance

Sustain-ability

Sustainability as Intersection of 3BL Performance

What is a Sustainable Agri Supply Chain? The UK Sustainable Development Commission has combined many different stakeholder views to produce an internationally applicable description of ‘sustainable Agri Supply Chain’ as those that:nProduce safe, healthy products in response to market demands and ensure that

all consumers have access to nutritious food and to accurate information about food products.

n Support the viability and diversity of rural and urban economies and communities.

n Enable viable livelihoods to be made from sustainable land management, both through the market and through payments for public benefits.

n Respect and operate within the biological limits of natural resources (especially soil, water and biodiversity).

Achieve consistently high standards of environmental performance by reducing energy consumption, minimizing resource inputs and using renewable energy wherever possible.

n Ensure a safe and hygienic working environment and high social welfare and training for all employees involved in the food chain.

n Achieve consistently high standards of animal health and welfare. n Sustain the resource available for growing food and supplying other public

benefits over time, except where alternative land uses are essential to meet other needs of society.

ClubSCMPro aims to nurture an active community of Supply Chain decision makers, professionals, experts and academicians. The idea is to build a forum where the SCM stakeholders can not only share great ideas on best practices, but can also discuss issues and pain areas affecting supply chain process.

As qualified members, you can avail the following benefits:> Subscriptions to SCMPro, monthly Enterprise magazine> Regular invites to Supply Chain Workshops, Seminars, Conferences, etc> Industry Reports> White Papers> Case Studies> Exclusive invite to the elite annual Black Suit Event

ClubSCMPro m e m b e r r e g i s t r a t i o n o p e n a t w w w. s c m p. i n

ClubSCMPro

Building Supply Chain Partnerships

lead story

26 SCMPr March 2013

lead story

27SCMPr March 2013 27

Built a partnerships to strengthen Supply Chain integration and provide a sustainable competitive advantage for all the chain partners.

The Chartered Institute of Purchasing and sup-ply defines partnership as an “commitment

between two or more parties in a collaborative relationship to create value by striving to achieve shared competitive goals and operational benefit through a spirit of mutual trust and openness.” According to the Global Supply Chain Forum, “A partnership is a tailored business relationship based on mutual trust, openness, shared risk and shared rewards that results in business performance greater than would be achieved by the two firms working together in the absence of partner-ship.” Supply chain management emphasizes collaborative relation-ships between all the stakeholders within a supply chain. No supply chain can exist in isolation. As glo-balization and international trade grows, Agri Supply Chains need to be able to collaborate and extend their sphere of operations across a wider geographical region. An important aspect of implementing a cross border Agri Supply chain management is the formation of strong links between members of the supply chain, however much they are separated by geography. This is easier said than done. For

a long time both practitioners and academics have touted the value of partnerships. The challenge is not identifying the partners; on the contrary, it is to find effec-tive methods for developing the appropriate type of relationship with these partners. The trade en-vironment today is characterized by increased competition, higher customer expectations, faster rates of change, and scarce resources. Partnering provides a way to lever-age the unique skills and expertise of each partner and may also “lock-out” competitors.

Agri supply chain partnerships are essential for the progress and prosperity of the Indian farmer. However, to establish and main-tain genuine partnerships requires a considerable investment of time and resources. It is important to identify the key relationships for which partnering would create exceptional advantages, and to manage their other supplier and customer relationships with appro-priate expectations. The require-ments from an Agri Supply chain differ over the products, nature of customer demand and the time available. So Supply Chain part-nerships too should reflect these requirements.

n A selected range of supply chain activities within short time pe-riod and limited scope.

n A broader range of elements over a longer time frame.

n A firm commitment to a very wide range of elements over in-definite time periods.

Choosing the PartnerWhen it comes to employing even a junior member, firms look to the possible long term benefits of the hire and not the next three months. In a similar way, the Agri Supply Chain partner needs to be evaluated for the longer term ben-efits that will accrue to the entire chain—not just the adjacent two links. This calls for a very high de-gree of understanding of the entire supply chain and its operations.

The first step in determining the best fit for the potential sup-ply chain partner is to identify the attributes that will define the appropriate partners. Many tra-ditional rules of engagement still hold true. These include quality, flexibility, process strengths and competencies, past track record, financial stability, and ability of the people involve. Many experts insist that the purchasing and supply or-ganizations should look into these

lead story

28 SCMPr March 2013

areas deeper before taking a call. An example of this type of deep dive is, rather than just analyze the balance sheet and cash flow state-ments; the suggestion is to assess a supplier’s market share, trends within their industry, their long-term strategic plans, the quality of their management and their com-mitment to research. Each supply chain player needs to become so knowledgeable in supplier op-erations that they know as much about the players across the en-tire value chain as they do about themselves. This necessarily means that every member of the agri sup-ply chain should share their busi-ness plans, capabilities, finances, people and processes with every other member. A tall order given the fragmented nature of the sup-ply chain. The benefit of such sharing can be that as chains ex-pand, these strengths will get each partner extra business, as mem-bers would prefer to do business with known entities than look for new partners.

To properly evaluate a partners potential, members of the larger supply chain must become aware of and consider attributes they may have ignored in the past. Jeff A. Tomko, purchasing senior man-ager for Honda of America Manu-facturing in Marysville, Ohio is reported to have said: “The suppli-ers we want to add to our supply base should have more technology or system capability than we could ever imagine using in the immedi-ate future”

A very important factor that members of an integrated supply chain will look for in their partners is the flexibility to adjust to the ever changing customer demand —an ability to adapt to acceler-ated development. Where does the member’s role in the supply chain begin and end? How did the member contribute in other

in terms of key performance indi-cators, so that the outcomes of the partnership can be monitored and the components can be adjusted as needed. Also each partner must allocate sufficient resources to ad-equately support the relationship.

EndnoteToday, more than ever, supply chain members are building col-laborative relationships with their other supply chain partners in or-der to achieve efficiencies, flexibili-ty, and sustainable competitive ad-vantage. Collaborative activities, such as information sharing, joint relationship effort, and dedicated investments lead to trust and com-mitment. Trust and commitment,

in turn, lead to improved satisfac-tion and performance. And better performance leads to better top, middle and bottom line.

Such collaboration comes at a price. The collaborative relation-ships should provide benefits that compensate for the additional expense associated with such re-lationships. Eventually, members of the supply chain will decide the nature and extent of collaboration —it is not necessary that every member in the chain will have the same deep relationship. Each one will find a workable relation-ship, based on their exposure to the chain.

chains? And a lot more difficult parameter to quantify, but still very important, is management. Evaluating an organization’s man-agement style takes several visits to the members and a detailed re-search on the management, after which one can get an idea on these subjective traits.

Another often overlooked ele-ment in building a supply chain partnership is the cultural affinity between the players—players will find it easier to do business with people who share values, culture and styles.

Building on the PartnershipIt is easier to establish a partner-ship than maintain it. Partner-

ships needs constant working upon and cannot be taken for granted. Once two members en-ter into a partnership, they need to operationalize it. For this they must establish and manage a number of components like a joint planning processes, free in-formation flows, transparency in operating controls, communica-tion links, and equitable sharing of risk and reward. Partnerships are strengthened by trust and commitment, streamlined con-tract style, broad scope of activi-ties, and shared financial invest-ment. It is important that the mutual expectations be expressed

“The suppliers we want to add to our supply base should have more technology or system capability than we could ever imagine using in the immediate future.”

SCMP is a monthly magazine for Supply Chain Professionals for Enterprise Users as well as Service Providers. The magazine contains specialist artcles, news and information designed to update the readers on the developments in supply chain industry. Specialised articles are contributed by the Industry Leaders and Academicians. Besides, there are other updates published to keep the readers keep pace with the Industry. Published in the 1st week of the month, the magazine is distributed to the readers through courier. Currentxly the print copy of the issue is available only for readers based in India. cover Price 1̀50/-

Get Your SubScription now!One year Subscription Rs.1,500/- Two Years Subscription Rs.2,850/-

Name: ...........................................................................................Designation ....................................................................

Company Name: ..............................................................................Industry ..........................................................................

Address ...............................................................................................................................................................................

............................. ...............................................................................City: ..............................................................................

Country:........................................... State: .......................................................... PIN Code: .......... ..........................................................

Tel: ................................................... Mob. .......................................... E-mail: ......................................................................................

DD/Cheque No. ........................................ Bank ..........................................Dated .............................For .̀ .............................................

Your DD/Cheque should be drawn in favour of B2B Media Group

Subscription form alongwith your payment should be sent to:

, 211/1, Sona Udyog, Parsi Panchayat Road, Andheri (East), Mumbai-400 069.

SubScription form

Supply Chain Management Professional

SCMPr n analysisn practicenknowledgensurveynhuman resourceMarch 2013 Vol. 1—No.2 `150

risk managementReviewing RapAgRisk.Page..33 talentWhen hiring decisions go bad.Page...47

In This Issue

Ensuring Food Securityguru speakAseAn’s Supply Chain Challenge.Page...7

Salary Survey Report 2013Page...42

Evaluating how Agri Supply Chain can evolve to capture

Value for the participant

30 SCMPr March 2013

A well established communication network, adequate infrastructure with the willingness to extend credit, research and development and enabling services like markets and mandis is few basic requirements for cross-border Agri Supply chain.

lead story

Transforming the Agri Supply Chain

lead story

31SCMPr March 2013 31

Indian agriculture has the po-tential to create a dominant position for itself in the global markets. To do that we need

to develop a strong, efficient sup-ply chain, that can minimize the post-harvest losses and strengthen the link between farmers, middle-men, processors and retail outlets. That said, Agri supply chains are not self forming. Developing Agri Supply Chains requires concerted effort and commitment from all chain partners. Agri supply chain development creates spin-offs that stimulate social, environmental and sustainable development with-in the region—employment gen-eration, decrease of product losses, etc. Given the fractured nature of Indian Agri Supply Chain, govern-

export their produce to the devel-oped nations.

Public-Private Partnerships Role of Government in agricul-ture markets is on the decline worldwide. It is recognized that efficient markets depend on pro-ducers and market functionar-ies deciding the selling of their produce. Corporate sector has taken over the market operations in most countries. Countries like South Africa and Brazil the gov-ernment has begun withdrawing from markets. In South Africa, agricultural marketing has trans-formed from a controlled envi-ronment to a free system.

Encouraging public private partnership in supply chain is a good way for the government to intervene. Both parties contribute to the development of the Agri Supply Chain and risks are shared The public part can contribute by developing and testing new tech-nologies, tools, models, and instru-ments to improve the performance of the supply chain. The private sector can leverage this knowledge and tools to bring in efficiencies in the supply chain.ment support plays a very impor-

tant role in the development of supply chains to create an enabling environment for agricultural sector development.

Agri Supply Chain develop-ment in India is hostage to these issues. Instead of encouraging free trade in agricultural products, governments resort to tariff and non tariff barriers to movement of agri products. To add to the con-fusion, these governments rarely encourage cross-border supply chain development with policy incentives. The WTO commit-ments on agriculture are nowhere near acceptance. The strict qual-ity standards, subsidies and tariff barriers, food safety norms affect the developing nations ability to

Government’s Role in the Development of Agri Supply Chains

nIdentifying and making public information on agricultural trade bottlenecks.

n Creating adequate infrastructure like transportation, communication and electricity.

n Provide incentives for sustainable use of production resources.

n Provide subsidies where needed in national interest.

n Ensure the availability of information and statistics to facilitate market activity.

n Assembling a body of knowledge on supply chains.

lead story

32 SCMPr March 2013

Cross-border chains Governments, private firms, re-search institutes, international or-ganizations all play an important role in developing cross border sup-ply chains. To develop cross border supply chains, governments need to create awareness among different stakeholders in the chain. Along side, governments need to create the institutional frameworks that will serve as the backbone. In some cases, the government may roll out pilot projects. The Rashtriya Krishi Vikas Yojana is an example of a pi-lot roll out. The results of the pilot can be used to fine tune the models.

Creating Institutional Frameworks India is on the threshold of a fresh agricultural revolution. If this comes about, the quantities which the chain will be required to handle is quite large. The capacity to clean, grade, pack, process and transport would have to expand at a very rapid pace to handle the additional quantities. Clearly, we need to cre-ate institutional frameworks to handle these surges. In India, these institutions are very weak.

Strengthening existing institu-tions or creating new ones can en-courage stakeholders solve supply chain problems jointly. These in-stitutions act as intermediaries and recognize the common interest of an entire sector of the economy. It stimulates demand for knowledge, and matches demand and supply.

Promotion of integrated markets in private/coopera-tive sector Under the APMC act, the State Government is the sole authority which initiates the process of set-ting up of a market commodities, which are regulated and for cer-tain areas, in which the regulation is enforced. This denies the private players any role in the develop-

ment of a market. This leads to a situation where, no player can assess the viability for setting up markets with state of the art facili-ties at competitive cost. We need to include private/corporate sector in setting up of alternative mar-kets, which can operate in parallel to existing markets.

According to a release by the Ministry of Agriculture, The Govt. of Karnataka has inserted a new Chapter in its Karnataka Agricul-tural Produce Marketing (Regula-tion) Act, 1966, to provide for the establishment of ‘National Integrat-ed Produce Markets’ to be owned and managed by the NDDB for the marketing of fruits, vegetables and