FUNDAMENTALS VALUATION SARDA ENERGY & MINERALS LIMITED March 20, 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FUNDAMENTALS VALUATION

SARDA ENERGY & MINERALS

LIMITED

March 20, 2013

ANALYTICAL CONTACT

Ms. Revati Kasture +91-22-6754 3465 [email protected]

BUSINESS DEVELOPMENT CONTACTS

MUMBAI

Mr. R. Suryanarayan +91-22-6754 3602 [email protected]

KOLKATA

Ms. Priti Agarwal +91-33- 40181600 [email protected]

CHENNAI

Mr. V Pradeep Kumar +91-44-2849 7812 [email protected]

AHMEDABAD

Mr. Mehul Pandya +91-79-40265656 [email protected]

NEW DELHI

Ms. Swati Agrawal +91- 11- 2331 8701 [email protected]

BANGALORE

Mr. Dinesh Sharma +91-80-2211 7140 [email protected]

HYDERABAD

Mr. Saikat Roy +91-40-40102030 [email protected]

PUNE

Mr. Rahul Patni +91-20-40009000 [email protected]

CARE EQUITY RESEARCH OFFERS

Independent Research of equities on fundamentals or valuations or both

IPO Grading

White Label Research

Valuation of companies for Institutional Investors, Asset Managers and Corporates

Sector Write-ups for Offer Documents of securities

SARDA ENERGY & MINERALS LIMITED

1 www.careratings.com

EQUIGRADE

Consolidated Financial Snapshot

(Rs. Crores) FY11 FY12 FY13E FY14E

Total Revenues 891 1,108 1,444 1,884

EBITDA 138 168 291 402

PAT 56 84 73 101

Fully Diluted EPS* (Rs.) 15.6 23.4 20.3 28.1

Dividend Per Share (Rs.) 3.0 3.5 3.5 3.5

P/E (x) 6.9 4.6 5.3 3.8

EV/EBITDA (x) 8.4 8.6 4.9 3.1

*Calculated on Current Face Value of Rs.10/- per share

EQUIGRADE – Analytical Power for Investment Decision

SARDA ENERGY & MINERALS LIMITED METALS, POWER & MINERALS

Good Fundamentals, Considerable Upside Potential CMP: 108/ CIV: 1781 Sensex: 19, 008

CARE Equity Research assigns 3/5 on fundamental grade to Sarda Energy & Minerals Limited (SEML) CARE Equity Research assigns a fundamental grade of 3/5 to SEML. This indicates ‘Good Fundamentals’. SEML is an integrated steel and ferro alloys producer with diversification plans into power and natural resources. The company is primarily engaged in the manufacturing and selling of pellets, sponge iron, steel billets, wire rods, wire and ferro alloys from its plant located at Raipur, Chhattisgarh. The operations of the facility are supported by 81.5 MW captive thermal power plant and an operational coal mine (production capacity of 1.2 MTPA). The company is further expanding its ferro alloy business, focused primarily at exports and has commissioned a 2x33 MVA ferro alloy plant along with 80 MW captive power plant in Vishakhapatnam in Q4FY13. In an attempt to diversify and also be further self sufficient in terms of raw materials, the company has entered into power and natural resources business through its various subsidiaries and joint ventures. SEML through its subsidiaries has around 1780 MW of total ongoing power projects. The company also has obtained a total of around 10 mining licenses for prospecting, surveying and mining of coal, iron ore and manganese and acquired economic interest in coal mines in Indonesia. However, most of these projects are at early stages of development and currently the company lacks complete backward integration and is exposed to raw material price volatility. On the operational front, SEML has also taken steps to improve its efficiency by setting up a 0.6 MTPA iron pellet plant, a coal washery at its operational coal mine and fly ash brick manufacturing facilities for waste management. Valuation CARE Equity Research values equity shares of SEML at a Current Intrinsic Value (CIV) of Rs.178 per share. The valuation is arrived at by using the EV/EBITDA valuation methodology. We have assigned an EV/EBITDA multiple of 4.15 times to the consolidated 1-yr forward EBITDA of Rs.402 crore. At the Current Market Price (CMP) of Rs.108 per share; the CIV results in a valuation grade of 5/5, indicating the shares of SEML have ‘Considerable Upside Potential’.

March 20, 2013

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 2

EQUIGRADE

Midsized, integrated steel and ferro alloy manufacturer primarily focused on domestic market;

increased capacity of ferro alloys to help boost exports

Sarda Energy & Minerals Ltd (SEML) is a midsized integrated steel, power and ferro alloys producer. The

company is engaged in the manufacturing and selling of pellets, sponge iron, steel billets, wire rods, wire, wire

ferro alloys and power primarily in the domestic market. SEML’s plant is located at Raipur, Chhattisgarh. The

company has its own captive coal mines with a production capacity of 1.2 million tons per annum (MTPA) and

captive power plant (81.5 MW). The company also has an iron ore mine with a production capacity of 1.5

MTPA however; currently the same is not operational due to Maoists issues in the areas. While, revenues for

the steel business are primarily from domestic market, SEML is a leading exporter of ferro alloys and enjoys

the status of Star Export House from the Ministry of Commerce. The company is set to commission a

greenfield ferro alloys plant of 2x33 MVA capacity backed by captive power plant of 80 MW in Visakhapatnam

in Q4FY13 under its subsidiary Sarda Metals and Alloys Ltd. (SMAL). The company plans to export major

quantity of ferro alloy produced at this plant. Post this plant getting operational the company’s ferro alloy

production capacity will increase to 200,000 MTPA.

Chart 1: Current Installed Capacity

Note: Iron Ore mine is currently not operational Source: Company and CARE Equity Research

FUNDAMENTAL GRADE Good Fundamentals 3/5

Power (81.5MW)

(200,000 MTPA)

p.a)

SARDA ENERGY & MINERALS LIMITED

3 www.careratings.com

EQUIGRADE

Chart 2: Domestic sales constitute bulk of total revenues currently

Source: Company and CARE Equity Research

While, over the last three years i.e. FY09 to FY12 SEML witnessed a strong growth in its steel revenues

(Compound Annual Growth Rate (CAGR) of 59.9 per cent), this was mainly on account of new pellet and steel

wire rods capacity coming on stream, which lead to a volume growth of 15 per cent and blended realization

growth of 29 per cent (due to change in product mix). During the same period domestic finished steel and

steel raw materials industry witnessed a growth of 8.95 per cent. With no new capacity additions in steel

business over the next few years and also limited scope for further increase in capacity utilization, we believe

the growth rate in steel business for SEML will taper down to around 8 - 9 per cent. This growth would be

primarily supported by the overall growth in finished steel consumption in India. CARE Research foresees the

domestic finished steel consumption in India to grow at a CAGR of around 6.7 per cent in the next five years

from about 69 million (mn) tonnes in FY11 to around 103 mn tonnes by FY16. On the other hand, ferro alloy

business is expected to drive the volume growth for the company on the back of increased capacity.

Shift in product mix towards higher value products coupled with increased efficiency due to pellet plant

and coal washery to help improve EBITDA margin going ahead

In order to move up the value chain and have better control over costs SEML adopted a strategy to produce

higher value products and improve cost efficiencies. The company set up wire rods capacity in FY10 in order

to improve profitability. Rolled steel products (wire rods) command higher per ton value as compared to

sponge iron ore. As a result of which, contribution of rolled products increased from 4.3 per cent in FY10 to

86.2% 86.5% 89.4%

13.8% 13.5% 10.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

FY10 FY11 FY12

Domestic Exports

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 4

EQUIGRADE

32.2 per cent in FY12. The company also put up a 0.6 MTPA pelletisation plant to convert iron fines into

pellets (substitute for iron lump in sponge iron production) in order to reduce costs, as the cost of iron ore

fines are lower by at least around Rs.4000 per ton as compared to iron ore lumps. Further, the company also

set up a 0.96 MTPA coal washery in order to improve the quality of coal. We believe that foray into higher

value products with increased efficiency due to pellet plant and coal washery and revenues from sale of coal

middling (which directly flow into EBITDA) will help improve profitability. We expect the company’s EBITDA

margin to improve from 15.2 per cent in FY12 to 20.1 per cent in FY13 and further to 21.4 per cent in FY14.

Chart 3: Contribution of steel in revenue has increased due to setting up of wire rods capacity

Source: Company and CARE Equity Research

Raw material price continues to impact SEML given the lack of complete backward integration

While SEML meets about 80% of its current coal requirements from captive mines at Raigarh, Chattisgarh

(production of ~1.2 MTPA), the company is still not self sufficient for its requirements of iron ore and

manganese ore and relies on open market procurements for the same. Further, currently there is no long-

term linkage for manganese ore, which is largely imported at prevailing international prices. However, to

tide over the variability as a result of procurement of these from the market, the company has executed

several licenses in Chhattisgarh, Goa and Madhya Pradesh, most of which are still in initial stages of

prospecting and pending various clearances and permissions. Hence, at present, the company continues to

rely on open market purchases which hamper its profitability as compared to some of its fully integrated

peers.

Ferro Alloy Sponge Iron SteelManganese

Ore and CoalPower Pellets

FY10 ₹ 196.8 ₹ 278.4 ₹ 23.7 ₹ 10.6 ₹ 46.5 ₹ -

FY11 ₹ 391.4 ₹ 258.4 ₹ 224.1 ₹ 41.6 ₹ 27.0 ₹ 3.6

FY12 ₹ 362.0 ₹ 347.1 ₹ 382.4 ₹ 5.8 ₹ 46.0 ₹ 42.5

₹ -

₹ 50.0

₹ 100.0

₹ 150.0

₹ 200.0

₹ 250.0

₹ 300.0

₹ 350.0

₹ 400.0

₹ 450.0 In Crores.

SARDA ENERGY & MINERALS LIMITED

5 www.careratings.com

EQUIGRADE

Table 1: Most of the domestic mines are currently under early development stage

Note: Mg. Ore refers to manganese ore

Source: Company and CARE Equity Research

Fungible business model helps cushion profitability margins

Like most sponge iron manufacturing companies, SEML too has a flexible model, wherein company can

trade off between selling sponge iron & power OR processing into billets or wire rods. Such trade off is

triggered by spot rates of power. As billets/wire rods making involves significant power usage, companies

can opt for selling power rather than processing into billets/wire rods. We believe such flexible business

model will help the company to cushion its profitability margins from volatility in metal prices.

Chart 4: In FY10, the company chose to sell higher sponge iron as compared to billets

Source: Company and CARE Equity Research

Segment Holding Co.

% share of SEML

Capacity/ Reserve

Status

Mines India (Raigarh) Coal Standalone - 280 MT Operational.

Production rate of 1.2 MTPA. India (Rajnandgaon) Iron Ore Standalone - 20 MT Operations suspended. India (Chhattisgarh) Iron Ore Standalone - 230 MT Prospecting license & forest

clearance received. India (Goa) Iron Ore Standalone - 3 MT Mining license obtained India (Balaghat) Mg. Ore Standalone - To be

ascertained Prospecting license / Reconnaissance Permit received

India (Goa) Mg. Ore Standalone - 6 MT Mining license received India (Chhattisgarh) Coal SPV 20.6 36 MT Allotted, clearances awaited

200

250

300

350

400

450

500

550

600

0.00

0.05

0.10

0.15

0.20

0.25

0.30

FY08 FY09 FY10 FY11 FY12

mn

Kw

h

mn

to

ns

Sponge Iron (LHS) Steel Billets (LHS) Power (RHS)

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 6

EQUIGRADE

Diversification into power generation and international natural resources through subsidiaries route;

gearing to remain at moderate levels

In order to reduce its dependence on its core metals business SEML is currently in process of developing

power projects of total 1,780 MW and has also acquired economic interest in a coal mine in Indonesia

(having reserves of 300 MTPA) through its wholly owned subsidiary Sarda Global Ventures Pte. Ltd.

(SGVPL). However, most of its power projects including 1,320 MW and 350 MW power plants in state of

Chhattisgarh are currently at early stage of development and as on March 31, 2012, SEML had only invested

around Rs.73 crores cumulatively in the power projects. For its coal mines in Indonesia, the subsidiary

SGVPL has got the mining license, environmental and forest clearance and is currently acquiring land for the

mines. The company expects the Indonesian mine to be operational by 2013.

While, SEML has large expansion plans in place (including various thermal and hydro power projects,

Indonesian coal mine, Chhattisgarh coal mines), given the spaced out timelines of execution, coupled with

good cash generation from the core steel and ferro alloy business (post stabilization of pellet plant and

commissioning of the new ferro alloy plant) the company’s net debt-equity levels are expected to decline

from 1.18 times at the end of FY12 to around 0.84 times by the end of FY14.

SARDA ENERGY & MINERALS LIMITED

7 www.careratings.com

EQUIGRADE

Table 2: Current status of power projects and Indonesian Coal Mine

Source: Company and CARE Equity Research Note: SMAL- Sarda Metals and Alloys Ltd, PPL- Parvatiya Power Ltd, MBPCL- Madhya Bharat Power Corporation Ltd, CHPLLP- Chhattisgarh Hydro Power LLP, SEL- Sarda Energy Ltd, SHPPL- Sarda Hydro Power Pvt.Ltd, SRELLP- Shri Ram Electricity LLP, SGVPL- Sarda Global Venture Pte Ltd, SHP- Small Hydro Project

Segment Holding Co.

% share of SEML

Capacity Status

Power Projects Raipur Thermal Standalone - 81.5 MW

(Captive) Operational.

Vishakhapatnam Thermal SMAL 100% 80 MW (Captive)

To be commissioned in Q3FY13.

Loharkhet (Uttarakhand)

SHP PPL 51% 4.8 MW Operational.

Rongnichu, (Sikkim) Hydro MBPCL 58.48% 96MW Civil construction under progress. To be commissioned by July 2015.

Gullu, Rehar, Mand, Jelha, (Chhattisgarh)

SHP CHPLLP 60.92% 24MW, 24MW, 24MW, 5MW

Civil construction under progress.

Chattisgarh Thermal SEL 100% 1320 MW

Land acquisition in progress, environmental clearance awaited

Kotaiveera, Ganeshpur, (Chhattisgarh)

SHP SHPPL 60% 24MW, 9 MW

Statutory clearances awaited

Chattisgarh Thermal SRELLP 51% 40 MW Techno-economic study under way

Indonesia (Sumatra) Coal SGVPL 100 300 MT Mining license, environmental clearance, forest clearance obtained. Land acquisition in process. Expect commissioning in 2013

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 8

EQUIGRADE

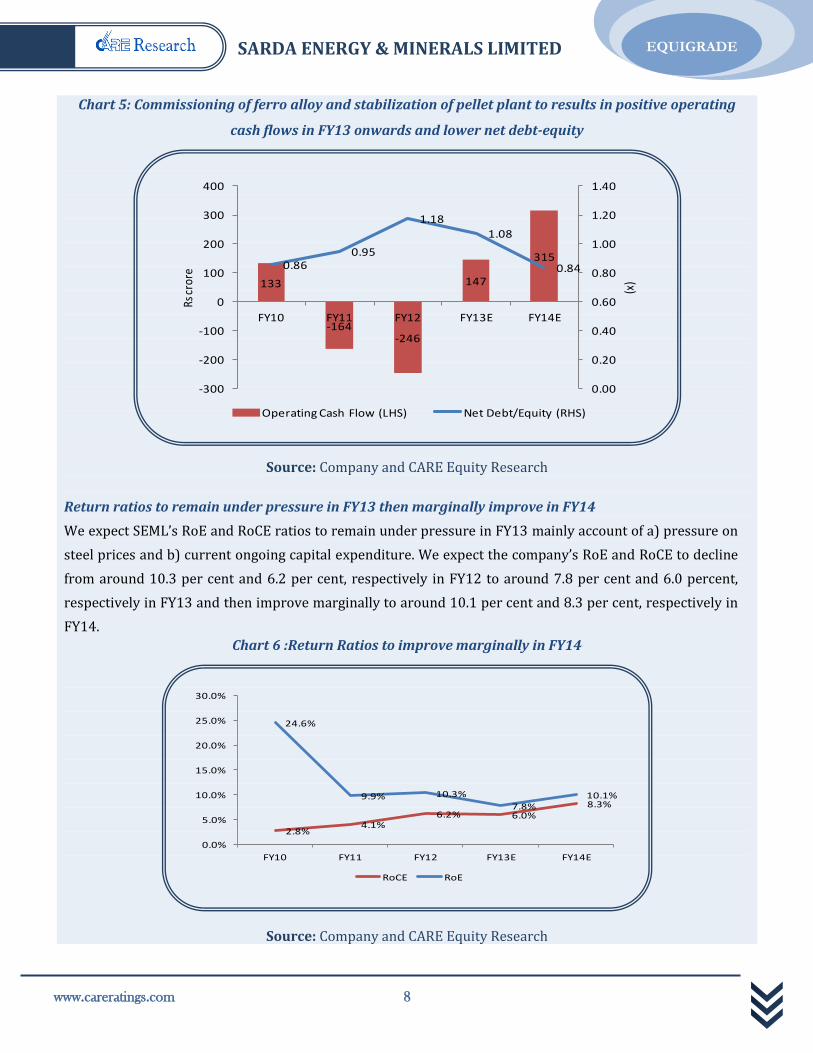

Chart 5: Commissioning of ferro alloy and stabilization of pellet plant to results in positive operating

cash flows in FY13 onwards and lower net debt-equity

Source: Company and CARE Equity Research

Return ratios to remain under pressure in FY13 then marginally improve in FY14

We expect SEML’s RoE and RoCE ratios to remain under pressure in FY13 mainly account of a) pressure on

steel prices and b) current ongoing capital expenditure. We expect the company’s RoE and RoCE to decline

from around 10.3 per cent and 6.2 per cent, respectively in FY12 to around 7.8 per cent and 6.0 percent,

respectively in FY13 and then improve marginally to around 10.1 per cent and 8.3 per cent, respectively in

FY14.

Chart 6 :Return Ratios to improve marginally in FY14

Source: Company and CARE Equity Research

133

-164-246

147

3150.86

0.95

1.18

1.08

0.84

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-300

-200

-100

0

100

200

300

400

FY10 FY11 FY12 FY13E FY14E

(x)

Rs c

rore

Operating Cash Flow (LHS) Net Debt/Equity (RHS)

2.8%4.1%

6.2% 6.0%8.3%

24.6%

9.9% 10.3%

7.8%10.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

FY10 FY11 FY12 FY13E FY14E

RoCE RoE

SARDA ENERGY & MINERALS LIMITED

9 www.careratings.com

EQUIGRADE

Experienced promoters and in compliance with the listing agreement 49

SEML has experienced promoters and top management with its promoters and directors having more than

two decades of experience in the industry. The company has ten members in the Board, with four of them

being in executive positions, and six of them being Non-Executive and Independent Directors.

The Board has formed four sub-committees for audit, remuneration, shareholders/investor’s grievance, and

corporate governance. As per the annual report, the same is in compliance with the listing agreement of the

stock exchanges.

Table 3: SEML: Board of Directors

Source: Company and CARE Equity Research

Name Designation Category of Director Mr. K. K. Sarda Promoter Promoter, Executive & Non Independent Mr. G. K. Chhanghani Whole Time Director Executive & Non Independent

Mr. Pankaj Sarda Whole Time Director Executive & Non Independent

Mr. G. D. Mundra Whole Time Director Executive & Non Independent

Mr. Rakesh Mehra Director Independent Mr. A. K. Basu Director Independent Mr. P. R. Tripathi Director Independent Mr. G. S. Sahni Director Independent Mr.. Lakshminarayanan Director Independent Mr.Balakrishnan Director Independent

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 10

EQUIGRADE

CARE Equity Research assigns a valuation grade of 5/5 to SEML

CARE Equity Research values equity shares of SEML Ltd. at a Current Intrinsic Value (CIV) of Rs. 178 per

share. The valuation has been arrived using EV/EBITDA valuation methodology. We have assigned an

EV/EBITDA multiple of 4.15 times to the one year forward consolidated EBITDA of Rs. 402 crores. While, in

past the company has traded at higher EV/EBITDA multiple; five year average one year forward rolling

EV/EBITDA multiple of 10.4 times, however, during the same period SEML earned an average Return on

Equity of around 18.3 percent, which going ahead (for FY13 – FY17) is expected to be much lower at around

10.3 per cent. While assigning the EV/EBITDA multiple of 4.15, we have discounted for the decline in RoE as

well the future growth in profits, which is expected to be lower at around 7 – 8 per cent.

Table 4 SEML: Valuation snapshot

Source: CARE Equity Research

The following ongoing power projects and mining projects have not been valued, while arriving at the above

CIV, since they are still at a nascent stage of development. Any positive material development in these

projects will provide further upside to SEML’s valuation over the currently assigned CIV of Rs. 178 per

share.

Table 5 List of projects excluded

Source: CARE Equity Research

VALUATION GRADE Considerable Potential Upside 5/5

1-year Forward EBITDA 402

Assigned EV/EBITDA x 4.15

Implied EV (Rs.cr) (a) 1,670

Less: Net Debt (Rs.cr) (b) 1,032

Implied Equity Value (a-b) 638

No. of Shares (crores) 3.6

CIV per share 178

Name of subsidiary/JV Segment Capacity Subsidiary/JV % Stake Sarda Energy Ltd Thermal Power 1320 MW Subsidiary 100.0 Madhya Bharat Power Corp Thermal Power 96 MW Subsidiary 58.5 Chattisgarh Hydro Power LLP Hydro Power 77 MW Subsidiary 60.9 Sarda Hydro Power Pvt. Ltd Hydro Power 24 MW Subsidiary 60.0 Shree Ram Elec. LLP Thermal Power 40 MW Subsidiary 51.0 Madanpur South Coal Ltd Coal Mine 36 MTPA Joint Venture 20.6

SARDA ENERGY & MINERALS LIMITED

11 www.careratings.com

EQUIGRADE

At the current market price (CMP) of Rs.108 per share, the CIV of Rs.178 per share results in a valuation

grade of 5/5, indicating equity shares of SEML have ‘Considerable Upside Potential’.

Chart 7: SEML: One-year forward rolling price bands

Source: Capitaline and CARE Equity Research

-80

20

120

220

320

420

520

620

5-Apr-07 5-Apr-08 5-Apr-09 5-Apr-10 5-Apr-11

Rs/

sha

re

1-yr fwd rolling P/E

1x 4x 7x 10x 13x Price

0

500

1000

1500

2000

2500

3000

3500

4000

5-Apr-07 5-Apr-08 5-Apr-09 5-Apr-10 5-Apr-11

Rs C

rore

1-yr fwd rolling EV/EBITDA

4x 6x 8x 10x 12x EV

0

100

200

300

400

500

600

700

800

5-Apr-07 5-Apr-08 5-Apr-09 5-Apr-10 5-Apr-11

Rs/

sha

re

1-yr fwd P/B

0.5x 1.0x 1.5x 2.0x 2.5x Price

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 12

EQUIGRADE

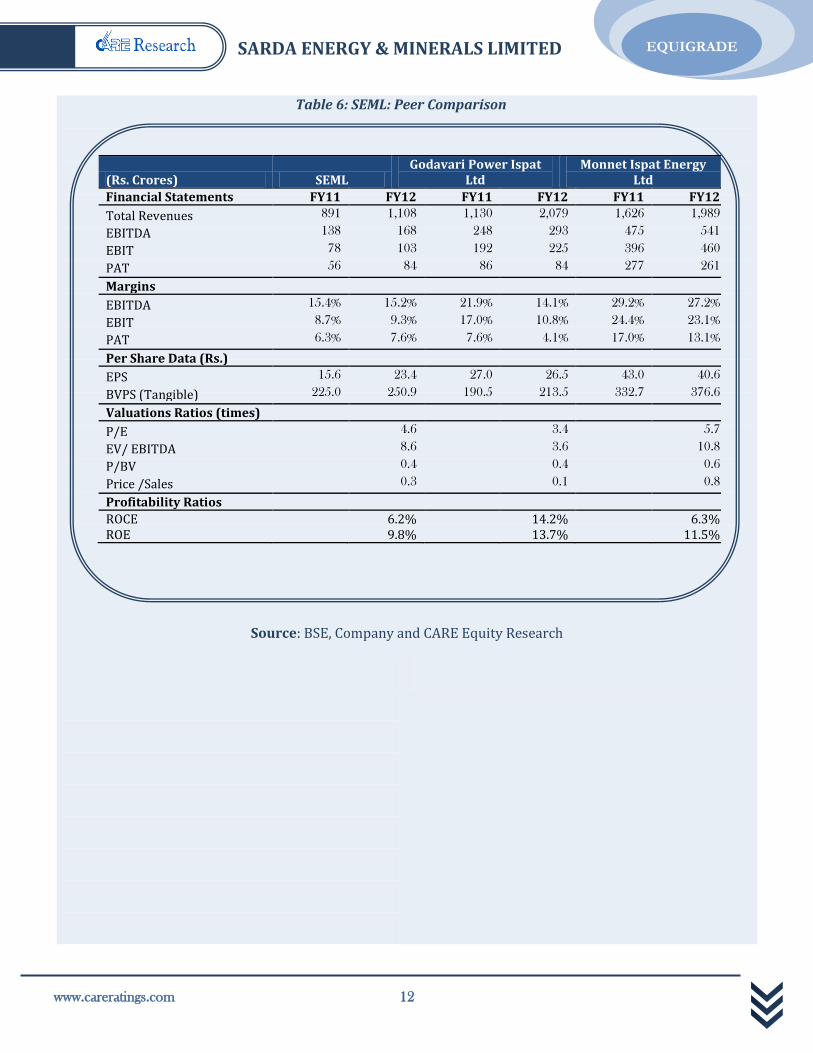

Table 6: SEML: Peer Comparison

Source: BSE, Company and CARE Equity Research

(Rs. Crores) SEML Godavari Power Ispat

Ltd Monnet Ispat Energy

Ltd

Financial Statements FY11 FY12 FY11 FY12 FY11 FY12

Total Revenues 891 1,108 1,130 2,079 1,626 1,989

EBITDA 138 168 248 293 475 541

EBIT 78 103 192 225 396 460

PAT 56 84 86 84 277 261

Margins

EBITDA 15.4% 15.2% 21.9% 14.1% 29.2% 27.2%

EBIT 8.7% 9.3% 17.0% 10.8% 24.4% 23.1%

PAT 6.3% 7.6% 7.6% 4.1% 17.0% 13.1%

Per Share Data (Rs.)

EPS 15.6 23.4 27.0 26.5 43.0 40.6

BVPS (Tangible) 225.0 250.9 190.5 213.5 332.7 376.6

Valuations Ratios (times)

P/E

4.6

3.4

5.7

EV/ EBITDA

8.6

3.6

10.8

P/BV

0.4

0.4

0.6

Price /Sales

0.3

0.1

0.8

Profitability Ratios

ROCE

6.2%

14.2%

6.3% ROE 9.8% 13.7% 11.5%

SARDA ENERGY & MINERALS LIMITED

13 www.careratings.com

EQUIGRADE

Sarda Energy & Minerals Ltd (SEML) earlier known as Raipur Wires & Steel Limited was incorporated in 1973 by the

Mumbai based Tejpaul Group. The Sarda group purchased Raipur Wires & Steel Limited in 1979 and renamed it as

Raipur Alloys & Steel Ltd (RASL). Further, in August 2007, the company rechristened itself as SEML post the merger

of Chhattisgarh Electricity Company Ltd (CECL) with RASL.

SEML is an integrated steel (manufacturing products across the value chain i.e. sponge iron, iron pellets, billets, ingots,

wire rods, TMT bars) and ferro alloy manufacturer and exporter. The company also has an operational coal mine to

support the raw material requirements for steel manufacturing and power generation.

The steel manufacturing facilities and coal mines are primarily located at Raipur & Raigarh, respectively in

Chhattisgarh state. Ferro alloy facility which is focused towards exports (commissioned in Q4FY13) is located at

Vishakhapatnam.

SEML through its subsidiaries and joint ventures has also invested in various power generation projects (thermal,

hydro and solar), which are at various stages of development and a coal mine in Sumatra region of Indonesia. SEML

also has obtained around a total of 10 licenses from the state and central government bodies for surveying,

prospecting & mining of iron and manganese ore.

COMPANY BACKGROUND

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 14

EQUIGRADE

Table 7: Operational capacity and ongoing projects

Segment Holding Co. % share of SEML

Capacity/ Reserve

Status

Mines Indonesia (Sumatra)

Coal SGVPL 100% 300 MT Mining license, environmental clearance, forest clearance obtained. Land acquisition in progress. Expected commissioning in FY14.

India (Raigarh) Coal Standalone - 280 MT Operational. Production rate of 1.2 MTPA.

India (Rajnandgaon)

Iron Ore Standalone - 20 MT Operations suspended.

India (Chhattisgarh) Iron Ore Standalone - 230 MT Prospecting license & forest clearance received.

India (Goa) Iron Ore Standalone - 3 MT Mining license obtained India (Balaghat) Mg. Ore Standalone - To be ascertained Prospecting license /

Reconnaissance Permit received India (Goa) Mg. Ore Standalone - 6 MT Mining license received India (Chhattisgarh) Coal SPV 20.6 36 MT Allotted, clearances awaited

Power Projects Raipur Thermal Standalone - 81.5 MW

(Captive) Operational.

Vishakhapatnam Thermal SMAL 100% 80 MW (Captive) To be commissioned in Q3FY13. Loharkhet (Uttarakhand)

SHP PPL 51% 4.8 MW Operational.

Rongnichu, (Sikkim) Hydro MBPCL 58.48% 96MW Civil construction under progress. To be commissioned by July 2015.

Gullu, Rehar, Mand, Jelha, (Chhattisgarh)

SHP CHPLLP 60.92% 24MW, 24MW, 24MW, 5MW

Civil construction under progress.

Kotaiveera, Ganeshpur, (Chhattisgarh)

SHP SHPPL 60% 24MW, 9 MW Statutory clearances awaited

Chhattisgarh Thermal SEL 100% 1,320 MW Land acquisition in progress, environmental clearance awaited

Raigarh, Chhattisgarh

Pithead Thermal

Standalone - 350 MW

Metals Raipur Sponge Iron Standalone - 360,000 TPA Operational Steel - 240,000 TPA Operational Wire Rod - 180,000 TPA Operational Wire Drawing - 30,000 TPA Operational Pellets - 600,000 TPA Operational Ferro alloy Standalone - 82,500 TPA Operational Ferro alloy

SMAL 100% 66,000 TPA To be commissioned in Q3FY13.

Waste recycling Raipur Fly ash bricks Standalone - 960,000 Operational

Note: SMAL- Sarda Metals and Alloys Ltd, PPL- Parvatiya Power Ltd, MBPCL- Madhya Bharat Power Corporation Ltd, CHPLLP- Chhattisgarh Hydro Power LLP, SEL- Sarda Energy Ltd, SHPPL- Sarda Hydro Power Pvt.Ltd, SRELLP- Shri Ram Electricity LLP, SGVPL- Sarda Global Venture Pte Ltd, SHP- Small Hydro Project

SARDA ENERGY & MINERALS LIMITED

15 www.careratings.com

EQUIGRADE

The Indian steel industry ranks fifth in the world with a crude steel production capacity of 89 mn tonnes in FY12.

Integrated steel producers contributed to 55 per cent of the total crude steel production while the rest was

contributed by secondary producers. During the period from FY98 to FY01, steel production witnessed a marginal

growth of 3 per cent CAGR. However, during FY02 to FY08, owing to boom in the infrastructure and automobile

sectors, the industry witnessed a sharp turnaround and registered a CAGR of 13 per cent.

Domestic steel consumption to grow at a CAGR of 6.7 percent during FY12– FY16

Despite the gloom in the advanced economies and the European countries, domestic finished steel industry

continued to register a strong growth during FY03 to FY11. Amid a sharp slowdown in the global demand (in the

aftermath of the global financial crisis during FY09), the domestic finished steel industry along with China strongly

contributed in the recovery in the global demand for the finished steel industry. Going ahead, CARE Research

estimates the domestic finished steel consumption to grow at a Compound Annual Growth Rate (CAGR) of around

6.7 per cent during period FY12-FY17.

Structure of Indian steel Industry

Source: CARE Research

Global finished steel production to witness steady growth in demand

CARE Research expects the global steel demand to grow at a CAGR of 3.2 percent from about 1484 mn tonnes in

CY11 to about 1788 mn tonnes in CY14. Despite an expected slowdown in Chinese demand, China is likely to

continue its dominance in the global metals demand followed by India and the other emerging economies. CARE

Research expects global supply of steel will continue to adjust itself with the change in global demand. Global steel

production is likely to increase at a CAGR of around 2 percent during CY11 to CY14. However, being in a surplus

SNAPSHOT OF THE INDUSTRY

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 16

EQUIGRADE

situation, any increase in global steel capacity is likely to negatively impact the capacity utilization rate and the

prices of finished steel products

Trends in global finished steel:

Capacities & Capacity utilization Production and Demand

Source: CARE Research

Sectors driving the domestic demand for the steel industry

During FY03 to FY11, domestic steel consumption has almost doubled up, growing at a CAGR of about 9.5 percent

from 34 mn tonnes to 69 mn tonnes. The Indian steel industry has been closely following the robust growth in

demand by increasing the domestic capacity at an almost similar pace from 40 mn tonnes to about 80 mn tonnes

during the same period. Domestic steel production also increased at a CAGR of 7.5% from 37 mn tonnes to 66 mn

tones.

Sectoral demand for long products (FY11) Sectoral demand for long products (FY15E)

Source: CARE Research

SARDA ENERGY & MINERALS LIMITED

17 www.careratings.com

EQUIGRADE

Consolidated Income Statement

(Rs Crores) FY09 FY10 FY11 FY12 FY13E FY14E

Operating Income 949 528 891 1,108 1,444 1,884 EBITDA 224 81 138 168 291 402

Depreciation and amortisation 28 41 60 65 96 128

EBIT 196 40 78 103 195 275

Interest 1 0 36 72 107 149

PBT 159 159 93 79 108 144

Ordinary PAT (After minority interest) 133 144 72 88 73 101

PAT (After minority interest) 129 80 56 84 73 101

Fully Diluted Earnings Per Share* (Rs.) 37.8 23.4 15.6 23.4 20.3 28.1

Dividend, including tax 10 10 11 13 13 13

* Calculated based on ordinary PAT on Current Face Value of Rs. 10/- per share

Consolidated Balance Sheet

(Rs Crores) FY09 FY10 FY11 FY12 FY13E FY14E

Tangible Net worth (incl. Minority Interest) 525 677 834 957 1,018 1,106

Debt (incl. Preference Shares) 744 622 782 1,139 1,293 1,255

Deferred Liabilities / (Assets) 28 29 36 50 50 50

Capital Employed 1,297 1,328 1,653 2,146 2,360 2,411

Net Fixed Assets, incl. Capital WIP, net of reval reserve 714 906 1,097 1,413 1,317 1,189

Investments 377 211 198 379 379 379

Loans and Advances 107 73 146 194 194 194

Inventory 100 152 259 227 379 487

Receivables 23 23 53 44 62 81

Cash and Cash Equivalents 37 63 16 80 261 377

Current Assets, Loans and Advances 266 311 473 544 896 1,139

Less: Current Liabilities and Provisions 60 100 115 190 232 297

Total Assets 1,297 1,328 1,653 2,146 2,360 2,411

Ratios based on Consolidated Financials

FY09 FY10 FY11 FY12 FY13E FY14E

Growth in Operating Income 51.8% -44.4% 68.9% 24.4% 30.3% 30.5%

Growth in EBITDA 32.2% -63.7% 69.3% 22.3% 73.0% 38.3%

Growth in PAT 9.0% 8.9% -50.1% 22.4% -17.5% 38.8%

Growth in EPS 7.8% -38.0% -33.6% 50.1% -13.1% 38.8%

EBITDA Margin 23.6% 15.4% 15.4% 15.2% 20.1% 21.4%

PAT Margin 13.6% 15.1% 6.3% 7.6% 5.0% 5.4%

RoCE 16.0% 2.8% 4.1% 6.2% 6.0% 8.3%

RoE 27.8% 13.6% 7.7% 9.8% 7.8% 10.1%

Net Debt-Equity (times) 1.3 0.9 1.0 1.2 1.1 0.8

Interest Coverage (times) 340.3 253.9 3.9 2.3 2.7 2.7

Current Ratio (times) 4.4 3.1 4.1 2.9 3.9 3.8

Inventory Days 50 124 125 88 120 120

Receivable Days 9 16 22 14 16 16

Price / Earnings (P/E) Ratio 6.9 4.6 5.3 3.8

Price / Book Value(P/BV) Ratio

0.5 0.4 0.4 0.4

Enterprise Value (EV)/EBITDA 8.4 8.6 4.9 3.1

Source: Company, CARE Equity Research

FINANCIAL ANALYSIS

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 18

EQUIGRADE

CARE EquiGrade Grid (CEG)

Through CEG, CARE Equity Research addresses two critical factors considered by an investor while investing in a particular

company’s equity shares:

1. Fundamentals: Whether the company is fundamentally sound with respect to its business, its financial position, its

management and its prospects.

2. Valuation: What is the Current Intrinsic Value (CIV) of the stock and how it compares vis-a-vis its Current Market Price

(CMP).

These factors are answered assigning quantitative grades to both these parameters. CEG is the snapshot of ‘Fundamental Grade’

and ‘Valuation Grade’ assigned by CARE Equity Research.

Fundamental Grade

This grade represents how sound the company is fundamentally, vis-à-vis other listed companies in India. This grade captures:

1. Business Fundamentals and Prospects

2. Financial Soundness

3. Management Quality

4. Corporate Governance Practices

The grade is assigned on a five-point scale as under:

CARE Fundamental Grade Evaluation

5/5 Strong Fundamentals

4/5 Very Good Fundamentals

3/5 Good Fundamentals

2/5 Modest Fundamentals

1/5 Weak Fundamentals

Valuation Grade

This grade represents the potential value in the company’s equity share for the investor over a 1-year period. The Current

Intrinsic Value (CIV) or the price arrived by CARE Equity Research on fundamental basis is compared with the Current Market

Price (CMP) of the stock and the grade is assigned based on the gap between CIV and CMP of the stock.

The grade is assigned on a five-point scale as under:

CARE Valuation Grade Evaluation

5/5 Considerable Upside Potential (>25% upside from CMP)

4/5 Moderate Upside Potential (10-25% upside from CMP)

3/5 Fairly Priced (+/-10% from CMP)

2/5 Moderate Downside Potential (10-25% downside from CMP)

1/5 Considerable Downside Potential (>25% downside from CMP)

Grading determination is a matter of experienced and holistic judgment, based on relevant quantitative and qualitative

factors of the company in relation to other listed companies.

EXPLANATION OF GRADES

SARDA ENERGY & MINERALS LIMITED

19 www.careratings.com

EQUIGRADE

DISCLOSURES

Each member of the team involved in the preparation of this grading report, hereby affirms that there

exists no conflict of interest that can bias the grading recommendation of the company.

This report has been sponsored by the company.

DISLCLAIMER

This report is prepared by Credit Analysis & REsearch Limited [CARE]. CARE has taken utmost care to ensure

accuracy and objectivity while developing this report based on information available in public domain or from

sources considered reliable. However, neither the accuracy nor completeness of information contained in this

report is guaranteed. Opinions expressed herein are our current opinions as on the date of this report.

CARE’s valuation of the security is mainly based on company-specific fundamental factors. Equity prices are

affected by both fundamental factors as well as market factors such as – liquidity, sentiment, broad market

direction etc. The impact of market factors can distort the price of the security thereby deviating from the

intrinsic value for extended period of time. CARE EquiGrade on a security should not be construed as

recommendation to buy, sell or hold a security; also it is not a comment on the suitability of the investment to

the reader. The subscriber / user assume the entire risk of any use made of this report or data herein. CARE

specifically states that it or any of its divisions or employees do not have any financial liabilities whatsoever to

the subscribers / users of this report. This report is for personal information only of the authorised recipient

in India only. This report or part of it should not be reproduced or redistributed or communicated directly or

indirectly in any form to any other person, especially outside India or published or copied for any purpose.

Published by Credit Analysis & REsearch Ltd., 4th Floor Godrej Coliseum, Off Eastern Express

Highway, Somaiya Hospital Road, Sion East, Mumbai – 400 022.

CARE is not responsible for any errors or omissions in analysis/inferences/views or for results obtained from

the use of information contained in this report and especially states that CARE (including all divisions) has no

financial liability whatsoever to the user of this product. This report is for the information of the intended

recipients only and no part of this report may be published or reproduced in any form or manner without

prior written permission of CARE.

SARDA ENERGY & MINERALS LIMITED

www.careratings.com 20

EQUIGRADE

Credit Analysis & REsearch Ltd. (CARE) is a full-service rating company that offers a wide range of rating and

grading services across sectors. CARE has an unparallel depth of expertise. CARE Ratings methodologies are in

line with the best international practices.

CREDIT ANALYSIS & RESEARCH LTD

HEAD OFFICE |Mr. R Suryanarayan | Cell: +91-9867365827| Tel: +91-22-6754 3602 | E-mail: [email protected] | 4th Floor, Godrej Coliseum, Somaiya Hospital Road, Off Eastern Express Highway, Sion (East), Mumbai - 400 022 | Tel: +91-022- 6754 3456 | E-mail: [email protected] | Fax: +91-022- 6754 3457

KOLKATA | Ms. Priti Agarwal | Cell: +91-98319 67110 | Tel: +91-33- 4018 1600/ 1602 | E- mail: [email protected] | 3rd Flr., Prasad Chambers (Shagun Mall Bldg), 10A, Shakespeare Sarani, Kolkata -700 071

CHENNAI | Mr. V Pradeep Kumar | Cell: +91 9840754521 | Tel: +91-44-2849 7812/2849 0811 | Fax: +91-44-2849 0876 | Email: [email protected] | Unit No. O-509/C, Spencer Plaza, 5th Floor, No. 769, Anna Salai, Chennai - 600 002

AHMEDABAD | Mr. Mehul Pandya | Cell: +91-98242 56265 | Tel: +91-79-40265656 | Fax: +91-79-40265657 | E-mail:[email protected] | 32, Titanium, Prahaladnagar Corporate Road, Satellite, Ahmedabad - 380 015.

NEW DELHI | Ms. Swati Agrawal | Cell: +91-98117 45677 | Tel: +91- 11- 2331 8701/ 2371 6199 | E-mail: [email protected] | 3rd Floor, B -47, Inner Circle, Near Plaza Cinema, Connaught Place, New Delhi - 110 001.

BENGALURU | Mr. Dinesh Sharma | Cell: +91-9900041975| Tel: +91-80-22117140 |

E-mail: [email protected] | Unit No. 8, I floor, Commander's Place, No. 6, Raja Ram Mohan Roy Road, (Opp. P F Office), Richmond Circle, Bangalore - 560 025.

HYDERABAD | Mr. Saikat Roy | Cell: +91-9820998779| Tel: +91-40-40102030 | E-mail: [email protected] | 401, Ashoka Scintilla | 3-6-520, Himayat Nagar | Hyderabad - 500 029.

PUNE | Mr. Rahul Patni | Cell: +91-78754 33355 | Tel: +91-20- 4000 9000 | E-mail: [email protected] | 9th Floor, Pride Kumar Senate, Plot No. 970, Bhamburda, Senapati Bapat Road, Shivaji Nagar, Pune - 411 015.

JAIPUR | Mr. Rahul Jain| Cell: +91 – 9314921496 | Tel: +91-0141-4020213/14 | E-mail: [email protected] | 304, Pashupati Akshat Heights, Plot No. D-91, Madho Singh Road, Near Collectorate Circle, Bani Park, Jaipur - 302016.

ABOUT US

Related Documents