SOUTHERN AFRICAN POWER POOL 1 The Southern African Power Pool www.sapp.co.zw SAPP Experience in Regional Integration And Power Pooling Dr. Lawrence Musaba & Mr. Musara Beta Coordination Centre Manager Chief Market Analyst iPAD East Africa Dar es Salaam, TANZANIA 11-13 August 2009

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SOUTHERN AFRICAN POWER POOL1

The Southern African Power Pool

www.sapp.co.zw

SAPP Experience in Regional Integration And Power Pooling

Dr. Lawrence Musaba & Mr. Musara Beta

Coordination Centre Manager Chief Market Analyst

iPAD East Africa

Dar es Salaam, TANZANIA

11-13 August 2009

SOUTHERN AFRICAN POWER POOL2

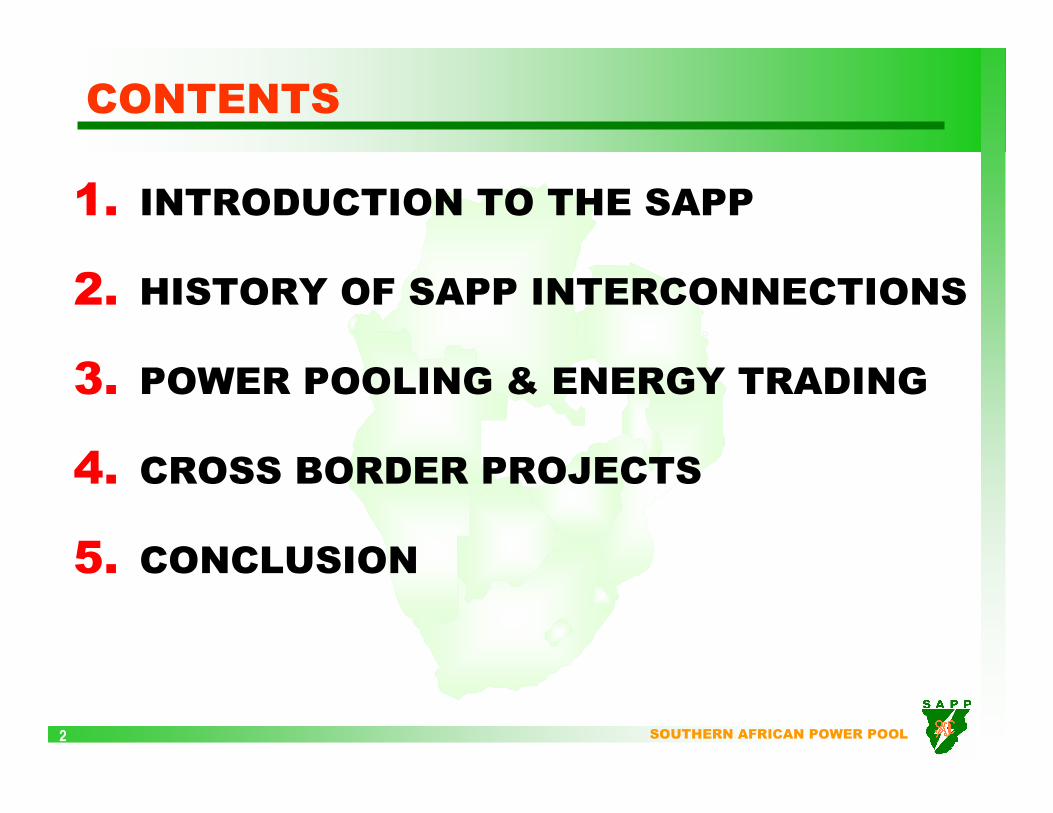

1. INTRODUCTION TO THE SAPP

2. HISTORY OF SAPP INTERCONNECTIONS

3. POWER POOLING & ENERGY TRADING

4. CROSS BORDER PROJECTS

5. CONCLUSION

CONTENTS

SOUTHERN AFRICAN POWER POOL3

1. INTRODUCTION TO THE SAPP

DR CongoTanzania

Zambia

Angola Malawi

Zimbabwe

MozambiqueBotswanaNamibia

South AfricaLesotho

Swaziland

� 12 SADC Member

Countries

� 230 Million people

� Regional Average

Electricity growth

rate 4.6% p.a.

1.1 Geographic

SOUTHERN AFRICAN POWER POOL4

� The SAPP was created in August 1995 through the signing of the Inter-Governmental MOU.

� The Aim was to optimise the use of available energy resources in the region and support one another during emergencies.

� 12 SADC Members:� 9 Operating Members� 3 Non-Operating Members

1.2 SAPP Creation and Aim

SOUTHERN AFRICAN POWER POOL5

The SAPP Vision is to:

� Facilitate the development of a competitive electricity market in the Southern African region.

� Give the end user a choice of electricity supply.

� Ensure that the southern African region is the region of choice for investment by energy intensive users.

� Ensure sustainable energy developments through sound economic, environmental & social practices.

1.3 SAPP Vision

SOUTHERN AFRICAN POWER POOL6

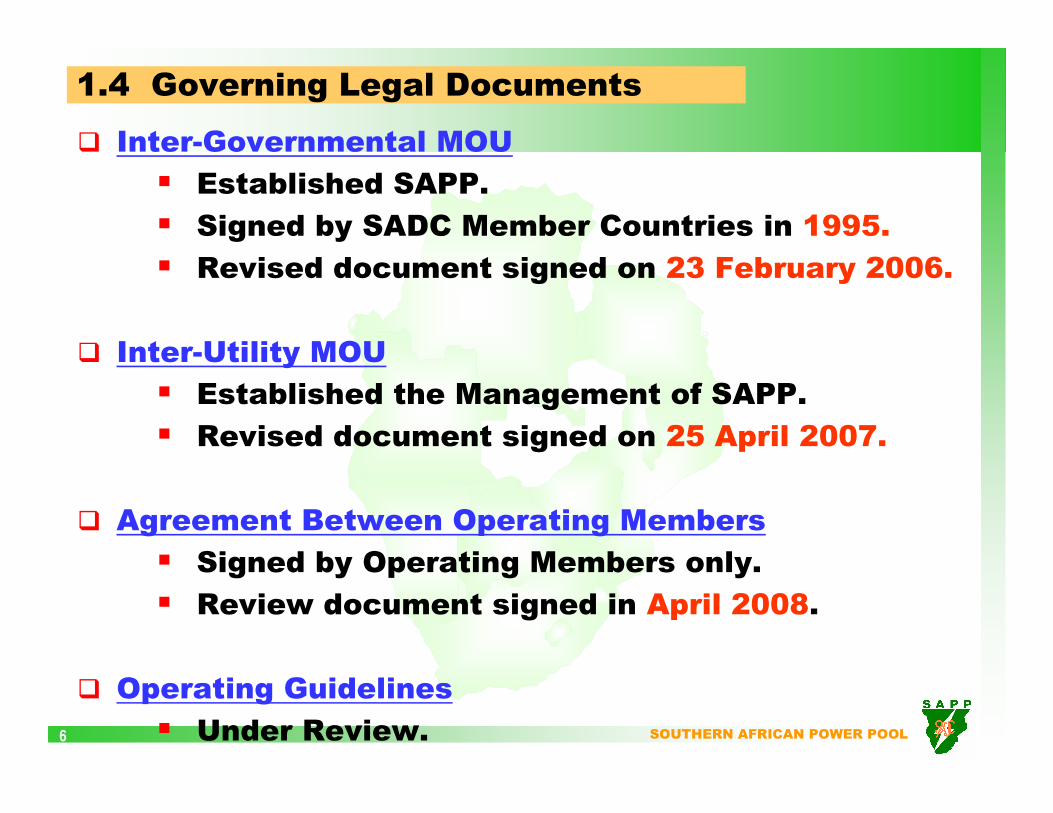

1.4 Governing Legal Documents

� Inter-Governmental MOU

� Established SAPP.

� Signed by SADC Member Countries in 1995.

� Revised document signed on 23 February 2006.

� Inter-Utility MOU

� Established the Management of SAPP.

� Revised document signed on 25 April 2007.

� Agreement Between Operating Members

� Signed by Operating Members only.

� Review document signed in April 2008.

� Operating Guidelines

� Under Review.

SOUTHERN AFRICAN POWER POOL7

1.5 Management & Governance Structure

SADC-DISSADC-DIS

Executive CommitteeExecutive Committee

Management CommitteeManagement Committee

Planning Sub-

Committee

Planning Sub-

Committee

Operating Sub-

Committee

Operating Sub-

Committee

Coordination Centre Board

Coordination Centre Board

Coordination Centre

Coordination Centre

Environmental Sub-

Committee

Environmental Sub-

Committee

Markets Sub-

Committee

Markets Sub-

Committee

SOUTHERN AFRICAN POWER POOL8

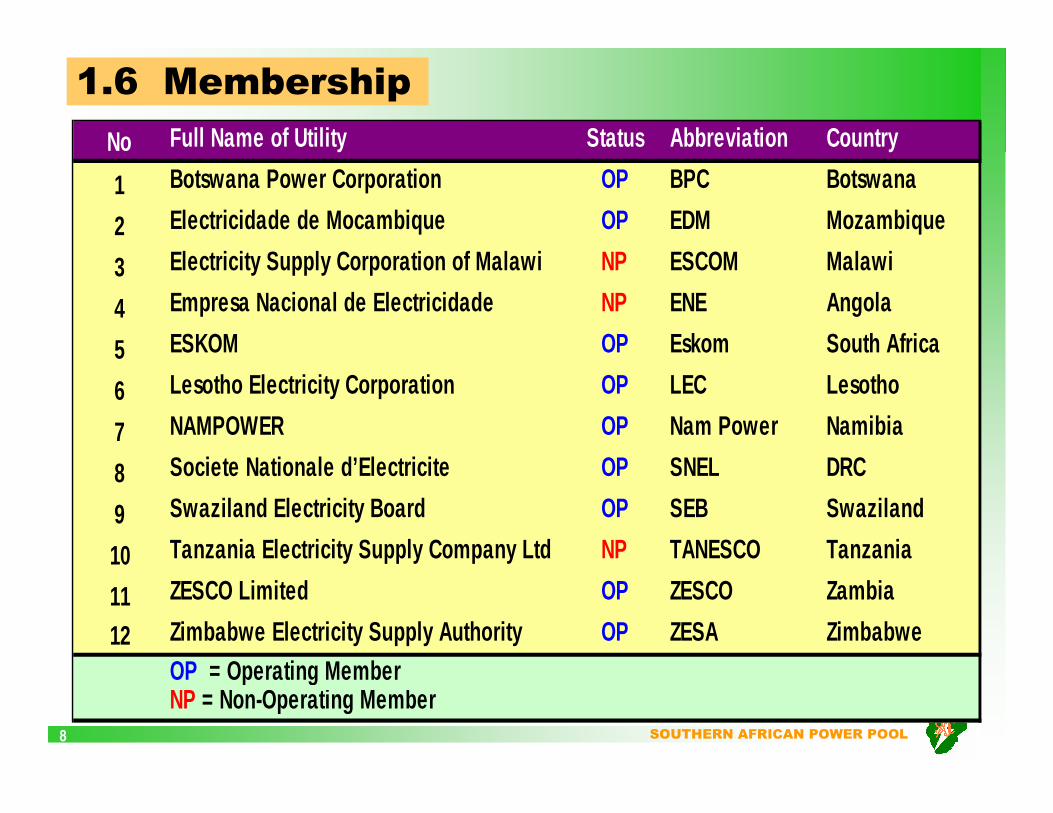

No Full Name of Utility Status Abbreviation Country

1 Botswana Power Corporation OP BPC Botswana

2 Electricidade de Mocambique OP EDM Mozambique

3 Electricity Supply Corporation of Malawi NP ESCOM Malawi

4 Empresa Nacional de Electricidade NP ENE Angola

5 ESKOM OP Eskom South Africa

6 Lesotho Electricity Corporation OP LEC Lesotho

7 NAMPOWER OP Nam Power Namibia

8 Societe Nationale d’Electricite OP SNEL DRC

9 Swaziland Electricity Board OP SEB Swaziland

10 Tanzania Electricity Supply Company Ltd NP TANESCO Tanzania

11 ZESCO Limited OP ZESCO Zambia

12 Zimbabwe Electricity Supply Authority OP ZESA ZimbabweOP = Operating MemberNP = Non-Operating Member

1.6 Membership

SOUTHERN AFRICAN POWER POOL9

1950s: DRC-Zambia500kV HVDC 1700km

1x220kV AC

1960s: Zambia – Zimbabwe

2x330kV AC

1975: Mozambique – South Africa

533kV HVDC – 1400km

DRCDRC

TanzaniaTanzania

AngolaAngola

ZambiaZambia

MalawiMalawi

MozambiqueMozambique

ZimbabweZimbabwe

BotswanaBotswana

NamibiaNamibia

South AfricaSouth Africa

SwazilandSwaziland

LesothoLesotho

1.2 Historic2. HISTORY OF SAPP INTERCONNECTIONS

SOUTHERN AFRICAN POWER POOL10

Thermal Southern Network

DRC

Tanzania

Angola

Zambia

Malawi

Mozambique

Zimbabwe

Botswana

Namibia

South Africa

Swaziland

Lesotho

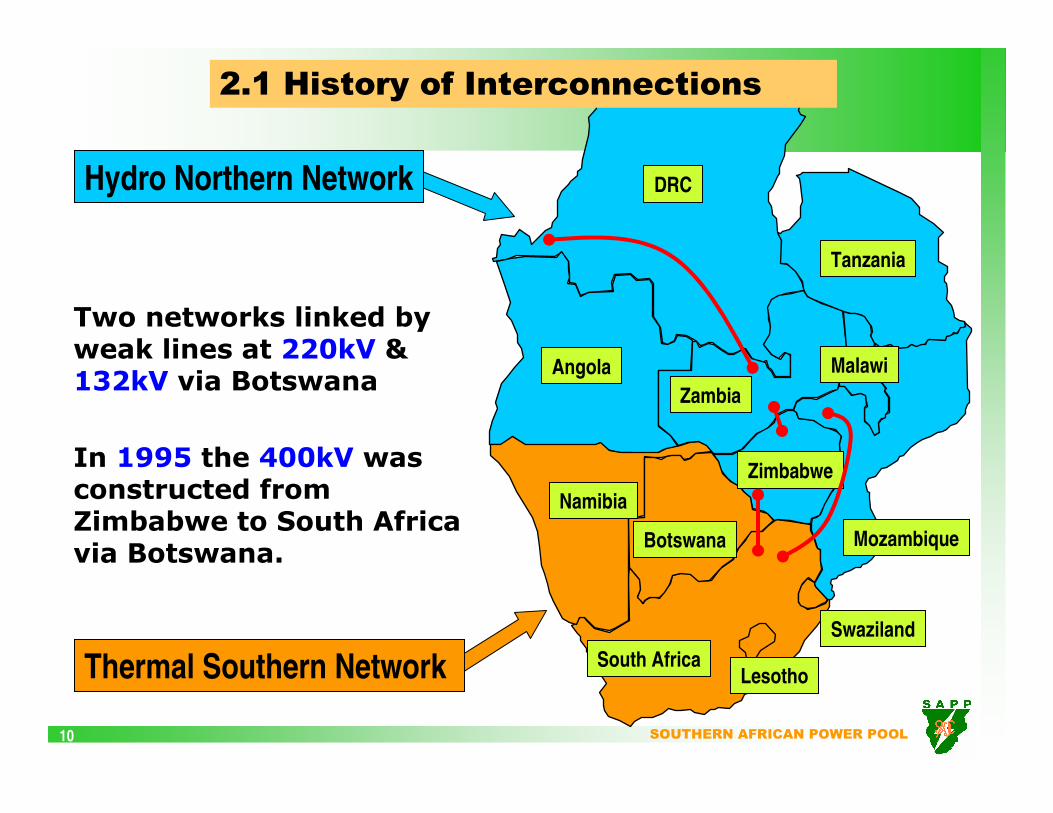

Hydro Northern Network

Two networks linked by weak lines at 220kV & 132kV via Botswana

In 1995 the 400kV was constructed from Zimbabwe to South Africa via Botswana.

2.1 History of Interconnections

SOUTHERN AFRICAN POWER POOL11

� The interconnection of the northern and southern networks created a platform for regional trade and cooperation.

� In 1995, the Ministers responsible for energy in the Southern African Development Community (SADC) signed Inter-Government MOU that lead to the creation of a power pool under the name, Southern African Power Pool(SAPP).

2.1 History of Interconnections

SOUTHERN AFRICAN POWER POOL12

2.2 Completed Interconnections

Since 1995, the following transmission lines have been commissioned by the SAPP:

1. The 400kV Matimba-Insukamini Interconnector linking Eskom of South Africaand ZESA of Zimbabwe in 1995.

2. The 330kV Interconnector between Mozambique and Zimbabwe was commissioned in 1997.

3. BPC Phokoje substation was tapped into the Matimba line to allow for Botswana’s tapping into the SAPP grid at 400kV in 1998.

SOUTHERN AFRICAN POWER POOL13

4. Restoration of the 533kV DC lines between Cahora Bassa in Mozambique and Apollo substation in South Africa was completed in 1998.

5. 400kV line between Camden in South Africavia Edwaleni in Swaziland to Maputo in Mozambique in 2000.

6. 400kV line between Arnot in South Africa and Maputo in Mozambique in 2001.

7. 400kV line between Aggeneis in South Africaand Kookerboom in Namibia in 2001.

8. 220kV line from Zambia to Namibia in 2007.

2.2 Completed Interconnections

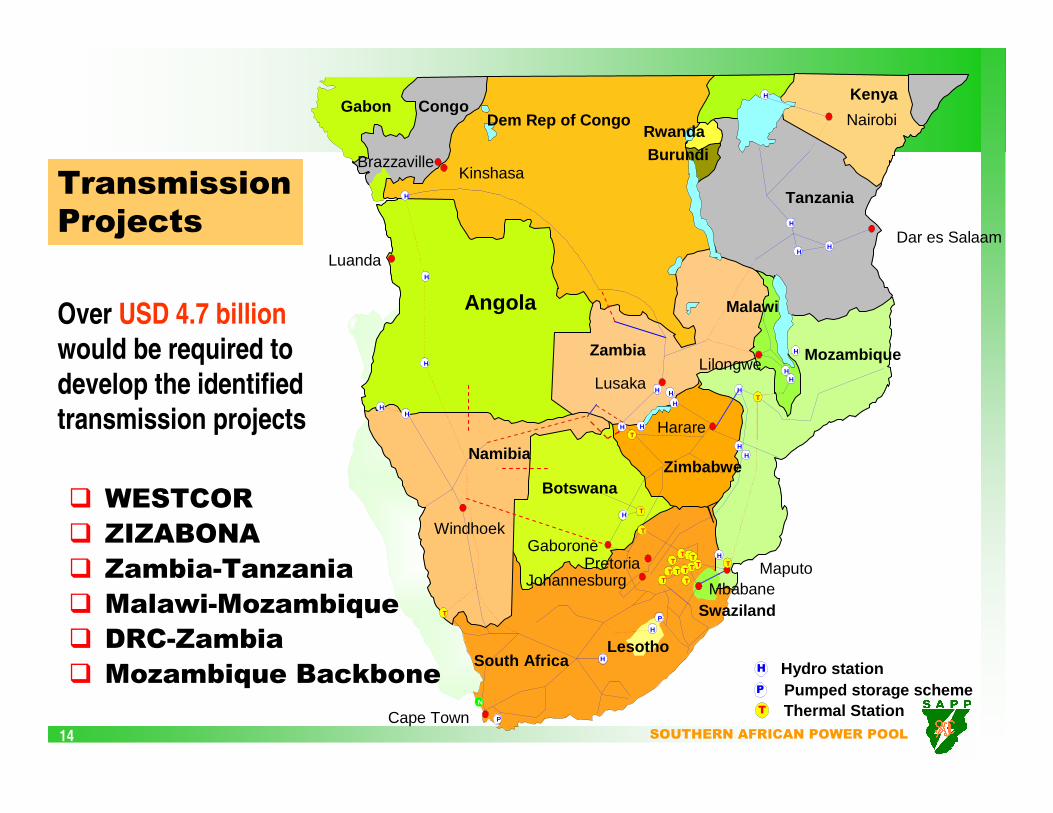

SOUTHERN AFRICAN POWER POOL14

� WESTCOR

� ZIZABONA

� Zambia-Tanzania

� Malawi-Mozambique

� DRC-Zambia

� Mozambique Backbone

Over USD 4.7 billion

would be required to

develop the identified

transmission projects

Transmission

Projects

Dem Rep of CongoCongoGabon

Luanda

Windhoek

Lusaka

Harare

Lilongwe

Nairobi

Dar es Salaam

GaboronePretoria

Johannesburg

Cape Town

MaputoMbabane

KinshasaBrazzaville

Angola

Tanzania

Kenya

Mozambique

South Africa

Swaziland

Lesotho

Namibia

Zambia

BotswanaZimbabwe

Malawi

RwandaBurundi

H

H

H

H

H

H

H

H

H

HH

H

H

HH

H

P

H

H

T

T

T

T

T

T TT

TTTTT T

T

T

HH

H

TH

P

N

HH

H

T

Hydro stationPumped storage schemeThermal Station

P

SOUTHERN AFRICAN POWER POOL15

3. POWER POOLING AND ENERGY TRADING

� Linking utilities electricity production facilitates the dispatch of excess capacity from one system to another.

� Thus the output from different power plants is pooled, scheduled according to increasing marginal cost, and dispatched according to merit order to meet demand.

� The benefits and platform created by power pooling include:

1. Increased security and reliability of supply� Provision of emergency support� Sharing spinning reserve capacity� Balancing generation mix (74% coal, 20% hydro, 4%

nuclear, 2% gas/diesel)

2. Improved sector investment environment� Aggregation of individual power markets� Improved access to creditworthy� Diversification

3.1 Power Pooling

SOUTHERN AFRICAN POWER POOL16

3. Reduced operating costs� Merit order dispatching� Balancing non-coincidental peak-loads� Optimization of generation resources

4. Reduced & deferred investment costs� Advantage of economies of scale� Reduced total reserve requirements (SAPP has

managed from 20% to 10%)� Postponed investments in new peak power

capacity� Reduced investment in hydro system

3.1 Power Pooling - 2

SOUTHERN AFRICAN POWER POOL17

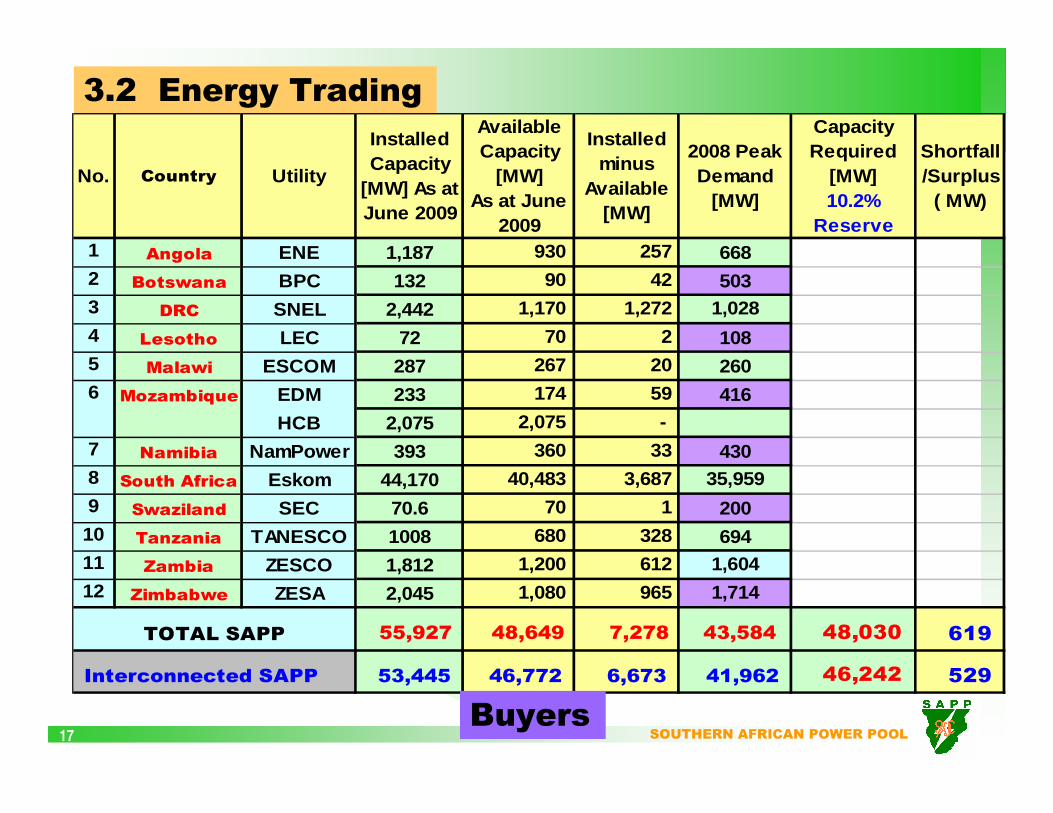

3.2 Energy Trading

No. Country Utility

Installed Capacity

[MW] As at June 2009

Available Capacity

[MW] As at June

2009

Installed minus

Available [MW]

2008 Peak Demand

[MW]

Capacity Required

[MW] 10.2%

Reserve

Shortfall /Surplus

( MW)

1 Angola ENE 1,187 930 257 6682 Botswana BPC 132 90 42 5033 DRC SNEL 2,442 1,170 1,272 1,0284 Lesotho LEC 72 70 2 1085 Malawi ESCOM 287 267 20 2606 Mozambique EDM 233 174 59 416

HCB 2,075 2,075 - 7 Namibia NamPower 393 360 33 4308 South Africa Eskom 44,170 40,483 3,687 35,9599 Swaziland SEC 70.6 70 1 20010 Tanzania TANESCO 1008 680 328 69411 Zambia ZESCO 1,812 1,200 612 1,60412 Zimbabwe ZESA 2,045 1,080 965 1,714

55,927 48,649 7,278 43,584 48,030 619

53,445 46,772 6,673 41,962 46,242 529 Interconnected SAPP

TOTAL SAPP

Buyers

SOUTHERN AFRICAN POWER POOL18

� Energy trading has been facilitated by the fact that some members have excess power supply and others are in a deficit.

� Balancing supply and demand is done via energy trading arrangements:

3.2 Energy Trading - 2

� Bilateral contracts� Bilateral contracts

PREVIOUSLYPREVIOUSLY

� Bilateral contracts

� Short-Term Energy Market (STEM) - 2001

� Post STEM (Balancing Market) - 2002

� Bilateral contracts

� Short-Term Energy Market (STEM) - 2001

� Post STEM (Balancing Market) - 2002

CURRENTCURRENT

� Bilateral contracts

� Day-Ahead Market (DAM) - 2008

� Ancillary Services Market - 2009

� Balancing Mechanism - 2008

� Bilateral contracts

� Day-Ahead Market (DAM) - 2008

� Ancillary Services Market - 2009

� Balancing Mechanism - 2008

FUTUREFUTURE

SOUTHERN AFRICAN POWER POOL19

� Bilateral trading has been increasing year by year.

� Demand in the SAPP is rising by 3% annually.

� Small reduction in 2004 – rehabilitation projects

- 5,000 10,000 15,000 20,000

2002

2003

2004

2005Y

ear

Energy Traded in GWh

3.3 Bilateral Trading

SOUTHERN AFRICAN POWER POOL20

96

210

200

950

100

1,370

400

150

110

100

80

796

1,390

918

230

2,500

3,375

793

770

700

280

5,875

0 1,000 2,000 3,000 4,000 5,000 6,000

Eskom-SEB

Eskom-BPC

Eskom-Nampower

Eskom-EDM

Eskom-LEC

HCB-ESKOM

HCB-ZESA

Eskom-ZESA

SNEL -ZESA

SNEL-ESKOM

ZESCO -ESKOM Energy (GWh)Capacity (MW)

Negotiated Utility Contracts HCB supply (hydro) – 1770 MWESKOM supply (thermal) – 1706 MW

SAPP Bilateral Agreements - 2003

SOUTHERN AFRICAN POWER POOL21

96

210

200

950

100

1,370

250

150

110

100

80

868

1,606

1,045

230

2,500

1,800

793

770

700

280

5,875

0 1,000 2,000 3,000 4,000 5,000 6,000

Eskom-SEB

Eskom-BPC

Eskom-Nampower

Eskom-EDM

Eskom-LEC

HCB-ESKOM

HCB-ZESA

Eskom-ZESA

SNEL -ZESA

SNEL-ESKOM

ZESCO -ESKOM Energy (GWh)Capacity (MW)

HCB supply (hydro) - 1770 MW, ESKOM supply (thermal) -1706 MW

Bilateral Contracts - 2005

SOUTHERN AFRICAN POWER POOL22

2008 Bilateral Contracts in SAPP

96

210

200

120

100

250

1370

100

150

40

45

40

40

950

270

0 200 400 600 800 1000 1200 1400

Eskom-SEC

Eskom-BPC

Eskom-NamPower

Eskom-EdM

Eskom-LEC

HCB-ZESA

HCB-Eskom

SNEL-ZESA

SNEL-Eskom

ZESA-NamPower

EdM-BPC

EdM-NamPower

EdM-SEC

Eskom -MOZAL

HCB-EdM

Capacity [MW]

SOUTHERN AFRICAN POWER POOL23

� There has been no energy trading on the

short-term energy market (STEM) from June

2007 due to:

� Lack of power supply in the market

� Constrained transmission paths.

� Bilateral trading has however continued.

3.4 STEM Trading

SOUTHERN AFRICAN POWER POOL24

STEM TRADING: Supply & Demand

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2001 2002 2003 2004 2005

Year

Ene

rgy

in G

WhSupply Demand

SOUTHERN AFRICAN POWER POOL25

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2001 2002 2003 2004 2005

Energy Traded [GWh] Monetary Value [US$x1000]

STEM TRADING: Energy Traded & Cost

0.41 Usc/kWh

0.39 Usc/kWh

0.50 Usc/kWh 0.74

Usc/kWh

1.08 Usc/kWh

SOUTHERN AFRICAN POWER POOL26

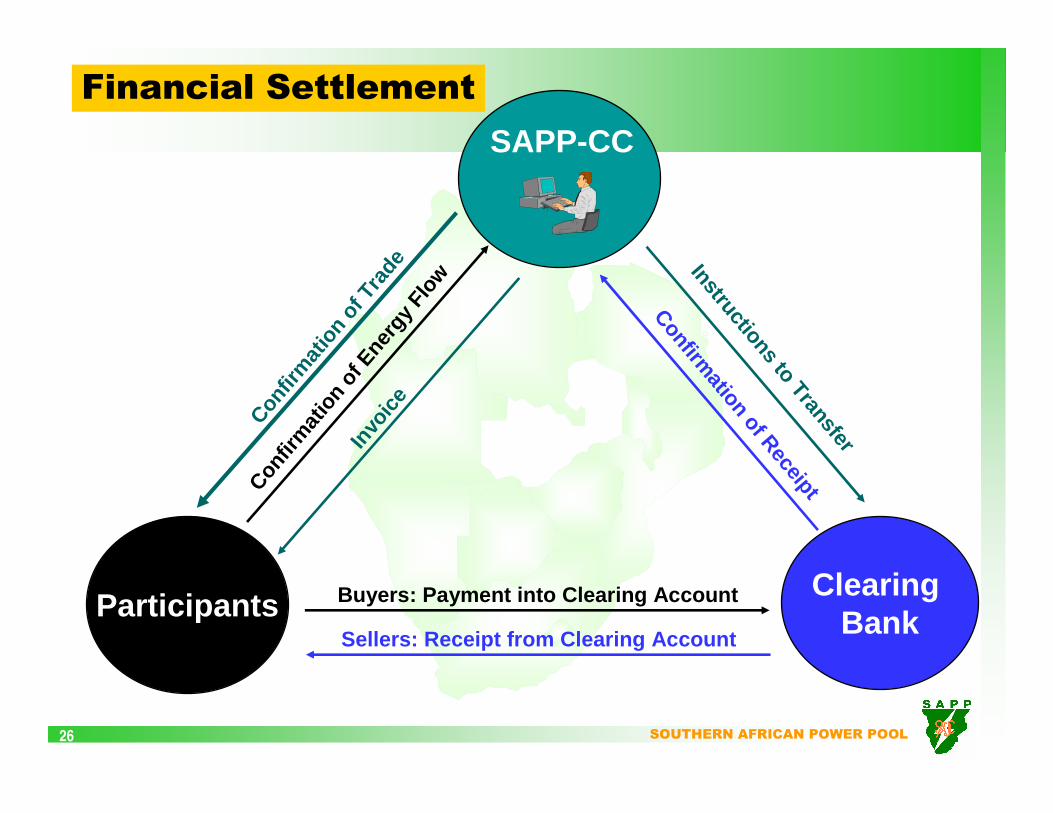

Clearing BankParticipants Buyers: Payment into Clearing Account

Confirmation of ReceiptCon

firm

atio

n of

Tra

de

SAPP-CC

Confir

mat

ion

of E

nerg

y Fl

ow

Invo

ice

Sellers: Receipt from Clearing Account

Instructions to Transfer

Financial Settlement

SOUTHERN AFRICAN POWER POOL27

GOALS of the SAPP DAM design:� Establish an efficient and competitive marketplace� Ensure that consumers benefit from the market

METHODOLOGY:� Development of consistent market mechanisms.� Efficient price signals for the procurement and

transmission of electricity.� Assurance of fair and open access to the

transmission system. � Optimization of generation & transmission capacity.

Goals and Methodology

3.5 SAPP Competitive Market

SOUTHERN AFRICAN POWER POOL28

� Supports an auction-trading model

� All sales & demand bids are aggregated at a fixed time

� The balance price is valid for all trades

� Tool for managing grid congestion

� System price (no grid congestion)

� Area prices (if transmission capacity is exceeded)

DAM Features

SOUTHERN AFRICAN POWER POOL29

SAPP believes that the creation of a competitive ma rket would:

� Help to optimise the use of regional resources

� Assist in determining the correct electricity price in the pool

� Send signals for investments and real time utilization of existing assets; transmission, generation and consu mption.

� Enable the demand side to respond to the supply sid e price signals.

� Designing a market is not simply a matter of copy a nd paste exercise, but hands on experience is necessary to know possible solutions of practical problems.

Advantages of a Competitive Market

SOUTHERN AFRICAN POWER POOL3030

Institutional

Framework

Project preparation,

structuring &

implementation

capability

• Project Preparation, Structuring/Implementation• Currently not at the required standard• No understanding of bankability• No regional coordinated planning/execution

• Institutional Framework• SAPP mandate & structure inappropriate• SADC historical focus on politics• No institution accountable for delivery

• Regulatory Framework• No clarity on cross-border trade• No clarity on cost pass through• No framework to encourage competition• No security of supply

• Weak project sponsors/ developers• No capacity to implement• Need to be reconstituted

• Transaction advisors role

Dependence On

PPAs To Get

Projects

Finance

• Market in each country too small relative to size of projects• Offtaker

• Single buyer model – only utility• Credibilty/ creditworthiness • Impact on balance sheet • Need energy intensive private users

• Dominant Role of Eskom as Major Buyer

• Ratings downgrade • Reduced borrowing capacity • Inability to enter into PPAs

• Risk allocation (currency risk, etc)• Complex negotiations, learning curve

• Too long to close PPAs• Too long to financial close• Need standardisation

• Tariff gap

Political

commitment

• Endorsement at Heads of State level• Reduce bureaucracy• Comfort of Govt underwriting

• Lack of a Project Champion• Strong oversight & accountability

• Low Tariffs• Tariff gap • Need govt underwriting

Progress (Years) towards financial close

Rollin

g

Priorities

4. MAJOR ISSUES AFFECTING CROSS-

BORDER PROJECT CLOSURECompleteness

(relative to checklist)

SOUTHERN AFRICAN POWER POOL31

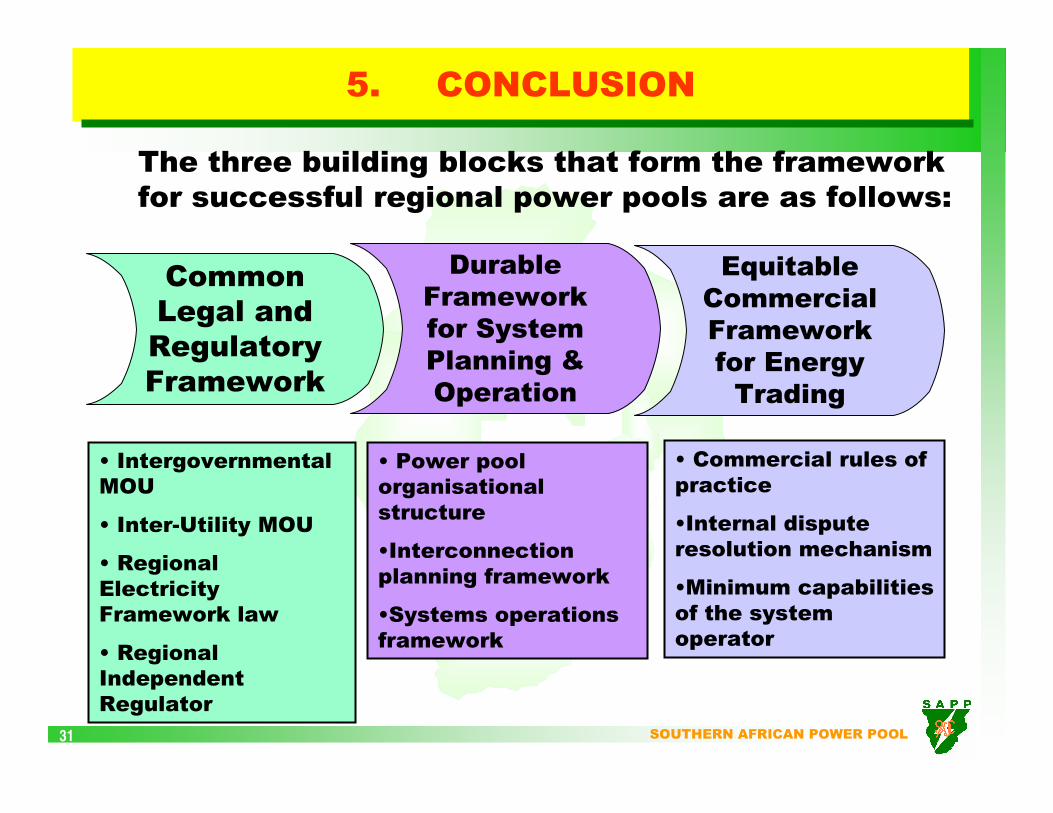

5. CONCLUSION

Common

Legal and

Regulatory

Framework

• Intergovernmental

MOU

• Inter-Utility MOU

• Regional

Electricity

Framework law

• Regional

Independent

Regulator

Durable

Framework

for System

Planning &

Operation

• Power pool

organisational

structure

•Interconnection

planning framework

•Systems operations

framework

Equitable

Commercial

Framework

for Energy

Trading

• Commercial rules of

practice

•Internal dispute

resolution mechanism

•Minimum capabilities

of the system

operator

The three building blocks that form the framework

for successful regional power pools are as follows:

SOUTHERN AFRICAN POWER POOL32

THANK YOU

Related Documents