Samuel M. Bwalya, Ezekiel Phiri, Kelvin Mpembamoto Zambia Revenue Authority, Lusaka, Zambia How non-state actors lobby to influence budget outcomes in Zambia

Samuel M. Bwalya, Ezekiel Phiri, Kelvin Mpembamoto Zambia Revenue Authority, Lusaka, Zambia How non-state actors lobby to influence budget outcomes in.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Samuel M. Bwalya, Ezekiel Phiri, Kelvin Mpembamoto

Zambia Revenue Authority, Lusaka, Zambia

How non-state actors lobby to influence budget outcomes in

Zambia

Outline • Introduction • Objectives of the paper• Evolution and Nature of non-state organization in

Zambia– Definition and overview– Nature of state-business relations– Importance of state business relations

• Overview of national budget process – Budget process– Budget institutions– Actors

• How non-state actors influence budget outcomes– Data and methods– Formal lobbying by non-state actors– Lobbying through the media

• Conclusions

Introduction

There is sizeable political economy and public choice literature on lobbying and specifically on fiscal decision-making especially on developed countries and Latin America, scanty on Sub-Saharan Africa.

The literature suggests that the budget process, actors and budget institutions matter a lot in determining fiscal outcomes and fiscal performance.

However, there is little information on how budget outcomes (fiscal policy) are produced, and how non-state actor seek to influence them.

Interested to examine how budget processes and institutions can be strengthen to promote fiscal governance and adoption of pro-poor tax and expenditures policies and programs

Since budget outcomes are political outcomes, political economy framework of analysis may be useful to extend this paper

Objectives• The paper was set out to; • Examines whether and how non-state actors

influence tax policy and public expenditures in Zambia

• Determine which lobbying channels and strategies are more effective in influencing budget outcomes

• Assesses the extent to which lobbying by non-state actors could improve pro-poor budget outcomes

• Distil recommendations on how state-business relations can be strengthened to promote fiscal governance and sustainability

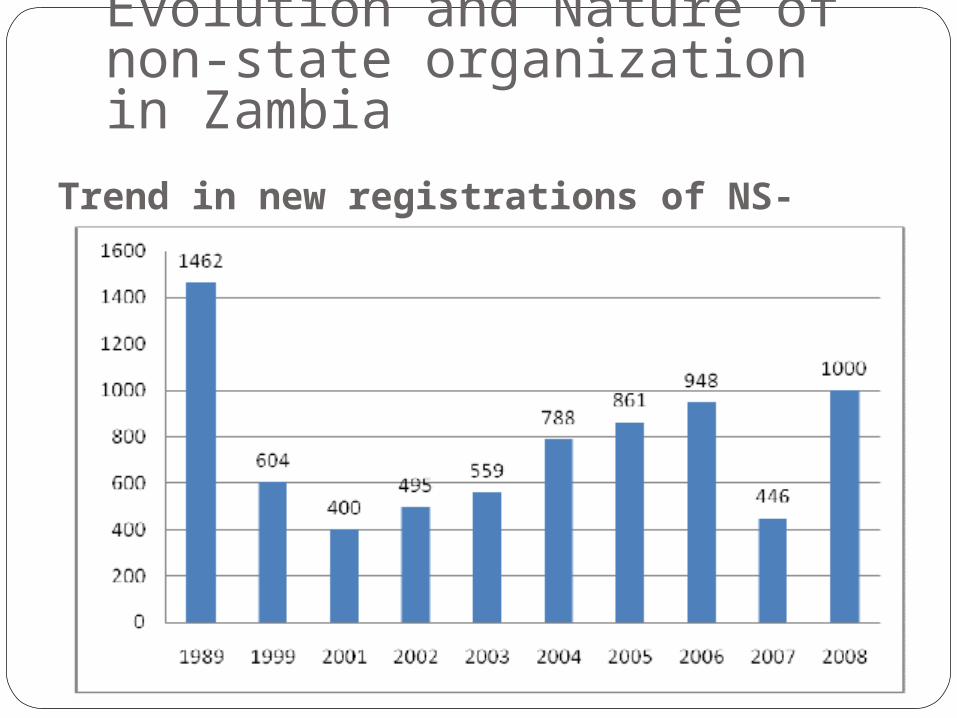

Evolution and Nature of non-state organizations in Zambia

• Significant growth in registration of Non-state actors after political and economic liberalization

• We distinguish two major types: – State-Business Relations

• The Zambia Business Council (ZBC) • Zambia Business Forum ( ZBF)

– State-Civil Society Relations• NGOCC ( coordinating Committee)• The Civil Society for Poverty Reduction (CSPR) • Other civil society networks/coalitions

Evolution and Nature of non-state organization in Zambia

Trend in new registrations of NS-Actors (1989-2008)

New registration of Non-state actors(1998—2008)

State-Business RelationsThe Zambia Business Council as the apex

bodyChaired by the President or his economic advisorThree cabinet ministers, business associationsMeet quarterlyAnnual event of business forum with Zambia

Business Advisory Council (ZIBAC) in attendanceThe Zambia International Business Advisory

CouncilPresident (chair)Economic advisor to the presidentInternational Business AdvisorsZBF (Observer)Meet once and reviews the Private Sector

Development Review Program

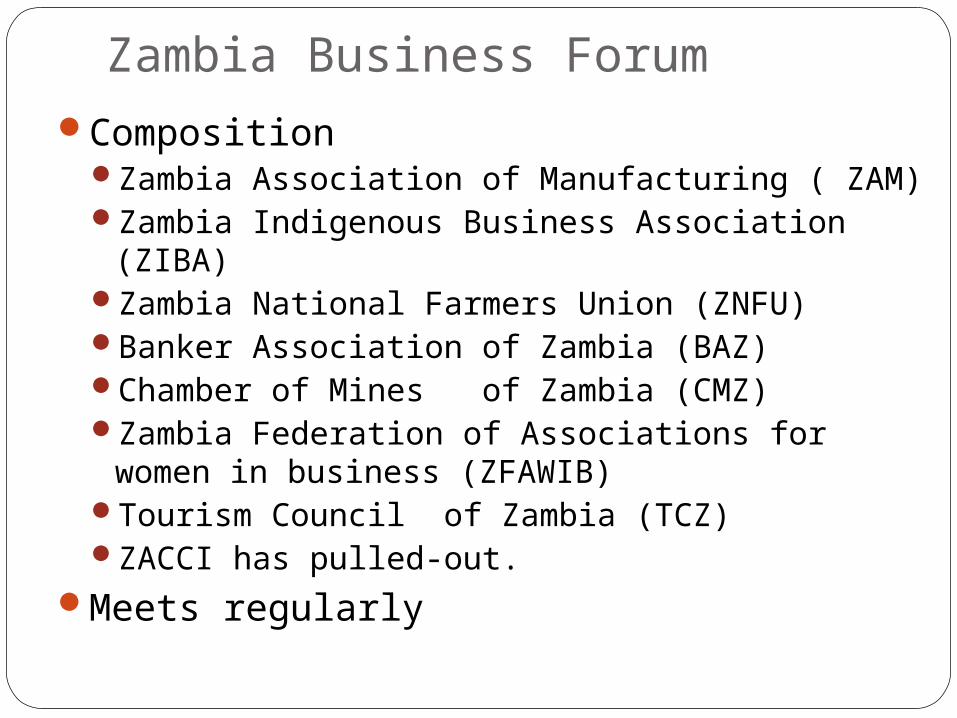

Zambia Business ForumComposition

Zambia Association of Manufacturing ( ZAM)Zambia Indigenous Business Association (ZIBA)Zambia National Farmers Union (ZNFU)Banker Association of Zambia (BAZ)Chamber of Mines of Zambia (CMZ)Zambia Federation of Associations for women in

business (ZFAWIB)Tourism Council of Zambia (TCZ) ZACCI has pulled-out.

Meets regularly

ZIBA

ZFAWIB

CMZ

BAZ

TCZ

ZACCICMZCMZCMZ

ZFAWIB

CMZ

ZFAWIB

CMZ

ZFAWIB

CMZ

TCZ

ZFAWIB

CMZ

THE PRESIDENT

Zambia Business CouncilZBF, MOFNP, MoCTI, MACC,MTC,ZDA

ZIBAC

Zambia Business Forum

ZAMZNFUTCZ

ZFAWIB

CMZ

ZIBA

State-Business RelationsSummary of SBRs in Zambia

Have become quite effective in dialoguing with Govt. especially in the last two decades

SBRs are increasingly being perceived as mutually beneficial, although not in all cases

Business associations effectively lobby to influence fiscal policy in their favor using various channels

The ZIBAC independent advisory (business think-tank)Helps moderate proposals from business associations and

provides benchmarking information to government.The PSD reform program is an example of successful

engagementReviews the PSD reform program annually, advises the

President

Civil Society for Poverty Reduction

Formed in 2000 as an anti-poverty advocacy network

Comprises over 140 non-governmental organizations

Has a network councils that meets annuallyHas board of directors, provincial teams, and an

active secretariatQuite effective in PRSP and FNDP preparationNot so effective in influencing implementation of

FNDP and PRSP programs Not quite able to effectively monitor

implementation and hold govt. accountable to its Plans

Civil Society for Poverty Reduction

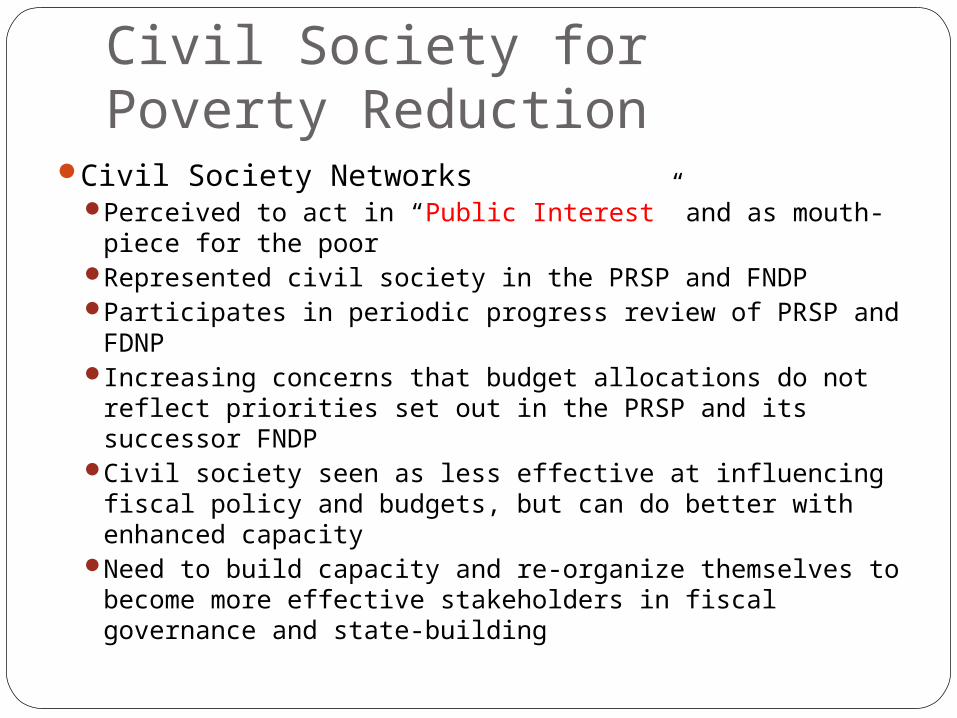

Civil Society Networks Perceived to act in “Public Interest” and as mouth-piece

for the poorRepresented civil society in the PRSP and FNDPParticipates in periodic progress review of PRSP and FDNP Increasing concerns that budget allocations do not reflect

priorities set out in the PRSP and its successor FNDPCivil society seen as less effective at influencing fiscal

policy and budgets, but can do better with enhanced capacity

Need to build capacity and re-organize themselves to become more effective stakeholders in fiscal governance and state-building

Is there scope and role for non-state actors in the budget process?

• Do non-state actor influence fiscal policy decision-making?– Is there scope for their effective participation?– What lobbying strategies do they use? – What outcomes have they influenced?

• Do they influence broader fiscal outcomes?– Promote fiscal transparency and accountability – Contribute to state-building (fiscal-social contract)

• Do they contribute to adoption of more pro-poor tax and expenditure policies/programs?

The National Budget process

• The budget is a policy document and tool for allocating public resources

• Budget decisions are political decisions (institutions, actors, incentives, etc )

• Both state and non-state actors seek to influence budget outcomes in their preferred direction

• Fiscal policy and budgets are important instruments for redistribution of public resources (benefits/losses)

Budget Process ctd• Main actors in the budget process

– Bureaucrats– The Cabinet (President & Line Ministers)– Legislators– Non-state actors

• Firms, individuals, civil society, business groups, donors etc

– Potentials sources of problems• Political business cycles: elections cycles• Common pool problems, state actors lack the

incentive to ensure wise use fiscal resources, • Institutional rigidities make budget allocations

and adjustments difficult, • Politicians may hide their inefficiencies in these

rigidities

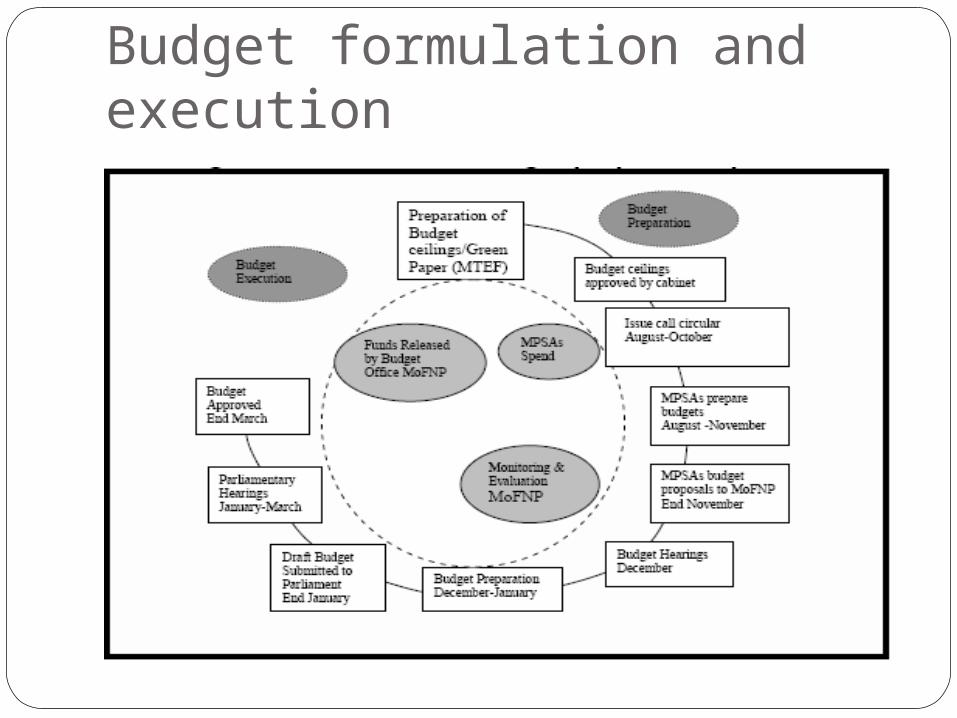

Budget preparation processParliament

Ministry of FinanceMinister (MoFNP)

CabinetPresident/Minister

Economic performance & monitoring comttee

Tax policy Committee

Income Tax Sub-CommitteeCustoms and Excise

Sub-CommitteeVAT Sub-Committee

Committee on Expenditure

Budget formulation and execution

Do non-state actors influence the budget

Data and MethodsTracked tax policy proposals submitted

throughout budget process, Identified proposals approved, reviewed, and dropped

at each budget stage tracked new proposals introduced at each budget stage

To help detect elements of informal lobbyingTo identify policy reversals (through statutory instruments)

Analyzed the composition of approval committees and representation of non-state actors

Largely used 2008 budget proposals and outcomes Tracked lobbying activity as captured in the

mediaFrom 2006—2008 ( daily papers—daily mail, times, and

post)

Some key findings: Lobbying activity11 business and professional associations

accounted for largest number of tax proposals (53.8%) in 2008

8 submissions from Government departments accounted for (22.1%)

16 from individual private corporations (16.1%)

1 Civil society and 6 individuals had each 4% of tax proposals

A submission can contain several tax and expenditure proposals

We look at the number of proposals submitted

Formal lobbying to influence the budget

Tax proposals submitted by tax type

State and Non-State Actors

Income Taxes

Value Added Taxes

Customs & Excise

Non-tax revenues

Total number of proposals

Professional Assocn 47 38 49 0 134

Companies 5 6 29 0 40

Government 23 11 21 0 55

CSOs 7 2 1 0 10

Individuals 5 0 2 3 10

Total 87 57 102 3 249

The most effective lobby in terms of success rate Interest groups No. of

Submission(a)

Total no. of proposals(b)

successfulproposals(c)

Success rate (%)e=c/b

Professional 11 134 12 1.5

Companies 16 40 3 7.5

Government 8 55 12 21.8

CSOs 1 10 8 80.0

Individuals 3 10 0 0

Total 42 249 36 14.5

The most effective lobby in terms of number of tax proposals adopted

Which actors were the most effective lobbies?

• In relative terms, civil society had highest success rate of (80 %), followed by govt (21.8%) and companies (7.5%)

• In absolute terms, professional and business associations though with lower 1.5% success rate, had more tax proposals adopted (need to compare revenue impacts)

• Individuals had lowest success rate, their proposals were often poorly formulated and justified

• Overall relative success rate in 2008 was 14.5% • It appears that this formal mechanism is working

well but needs to be enhanced through capacity building

Which tax proposals adopted were pro-poor?

Highest no. of proposals were on VAT (26.3%), with 80 % of these seeking to reduce the VAT rate: Were largely pro-poor especially if suppliers passed-on

the benefit to consumer by reducing prices (??)Poorly targeted as everyone benefits

Second highest no. of proposals adopted were on direct taxes, esp. payroll taxes and were largely pro-poor

Proposals on customs and excise had low success rate of 6.9% but directly benefited firms,

Some customs revenue measures adversely affected mining companies and cotton exporters (export levy)

Preliminary estimates of revenue implicationsImportant to look at revenue implications

and redistribution effectsWe are mining data on actual revenue

impacts for 2008

VAT revenue loss =US $ 58 million PAYE revenue loss=US $K14.1 million Customs and excise loss =US $.26 million Customs other measure(gains)=US$3.2 millionTax measures in the 2008 budget were by and

large pro-poor.

Lobbying activity captured in print media• 2775 newspapers transcribed from 3285

editions between 2006 and 2008 inclusive • 269 stories related to tax and expenditure

issues– 160 on tax policy; – 109 on expenditure issues

• Pattern suggests civil society are more reactive rather than proactive

• Partly due to lack of expertise to engage in formal budget process of lobbying

Articles and stories on tax and expenditure covered by print media 2006-2008

Total number of proposals published by tax type

Expenditure policy proposals published in print media 2006-2008

Concluding remarks• Zambia Business Council is a critical organizational

arrangement for fostering state-business relations , but needs a legal and Institutional framework to be effective and sustainable

• ZBF is strategic for private sector, but also needs to hold as stable coalition to be effective

• The arrangement through which non-state actor make budget submissions is important and should be strengthened

Firms preferred to lobby unilaterally for firm specific concessions ( customs and excise)

• Proposals channeled through government departments had greater chance of being adopted (public officers critical actors)

• Civil society and govt. had highest success rates in lobbying, but submitted fewer proposals than professional and business association

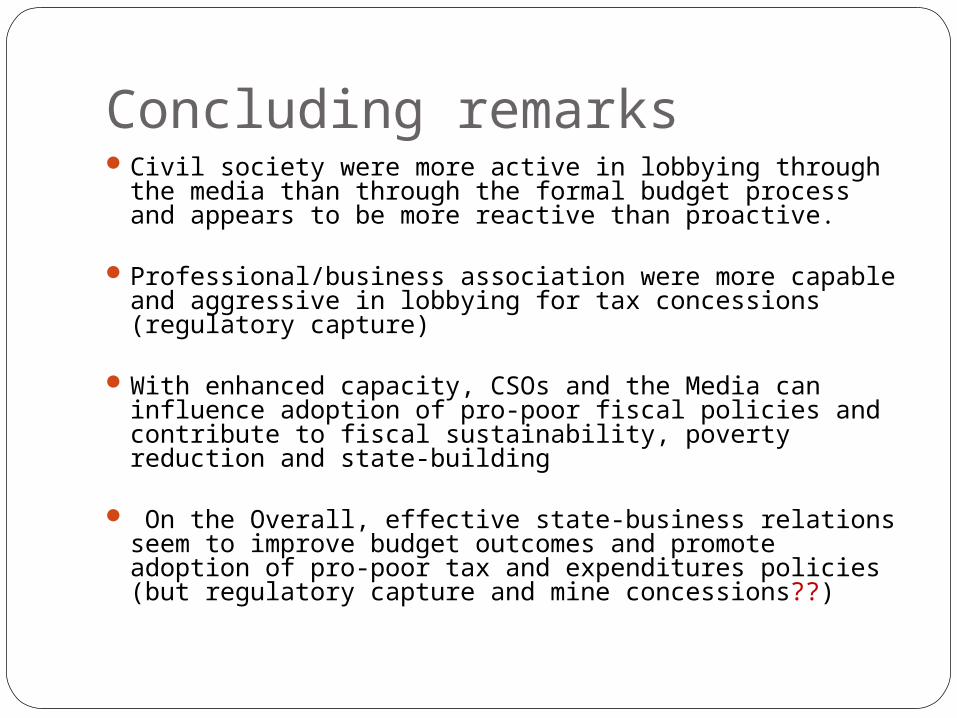

Concluding remarks Civil society were more active in lobbying through the

media than through the formal budget process and appears to be more reactive than proactive.

Professional/business association were more capable and aggressive in lobbying for tax concessions (regulatory capture)

With enhanced capacity, CSOs and the Media can influence adoption of pro-poor fiscal policies and contribute to fiscal sustainability, poverty reduction and state-building

On the Overall, effective state-business relations seem to improve budget outcomes and promote adoption of pro-poor tax and expenditures policies (but regulatory capture and mine concessions??)

Final thoughts

Develop a formal (estimable) model to analyze fiscal policy decision-making more empirically to specifically

identify factors that explain why some non-state actors become more success at influencing fiscal outcomes than others;

determine whether such influence improves the adoption of more socially optimal (pro-poor) fiscal policies and programs;

examine how non-state actors build effective coalition to influence fiscal policy outcomes; and

explore data requirements/source /availability

Thanks

Related Documents