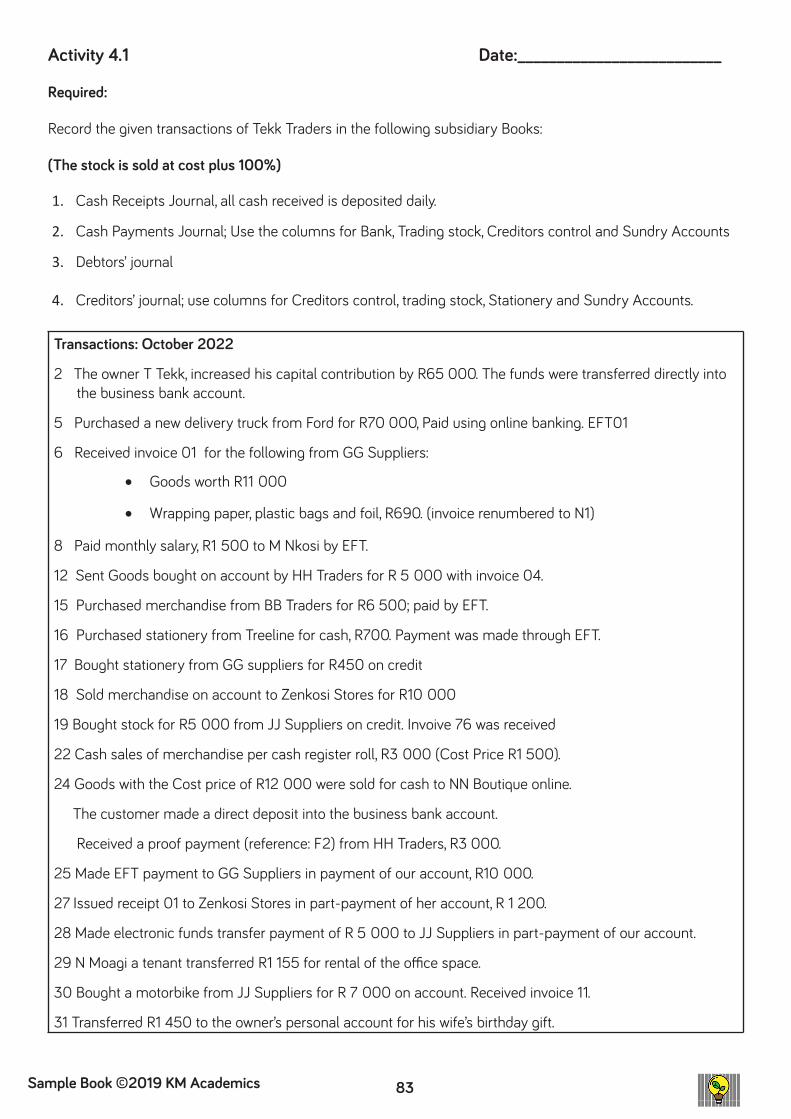

Simplified Accounting M.E. MOKOENA | T.S. KUBHEKA | B. KHOZA Workbook & Activities | Learner’s Book | Sample Book Grade 9 | CAPS Second Edition

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Simplified Accounting

M.E. MOKOENA | T.S. KUBHEKA | B. KHOZA

Workbook & Activities | Learner’s Book | Sample Book

Grade 9 | CAPS

Second Edition

Sample Book ©2019 KM Academics

Image CreditsVectors by Vecteezy (https://www.vecteezy.com)

Simplified Accounting - Grade 9 Second Edition First published 2019

Compiled, Edited and Quality Assured under: KM Academics Copyright 2019 KM Academics

All rights reserved under international copyright law.

Contents and/or cover may not be reproduced in wide or in part in any form without the express written consent or permission of the publisher.

Also by same authors:• Financial Literacy For All Grade 8 (Activities & Workbook)• Financial Literacy For All Grade 9 (Activities & Workbook)• Simplified Accounting Grade 8 (Activities & Workbook)• Simplified Accounting Grade 9 (Activities & Workbook)• Financial Literacy - Learner Support Material - Grade 9 (Sponsored by SAICA)

KM Academics (PTY) LTDReg No.: 2019/330255/07VAT Reg: 4280291446

Physical Address:4526 Krokodile StreetDawn Park Ext 42Boksburg1459

Cell: 084 331 9567 / 072 747 3612 / 073 697 0356 Email: [email protected]: kmacademics.co.za

3Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

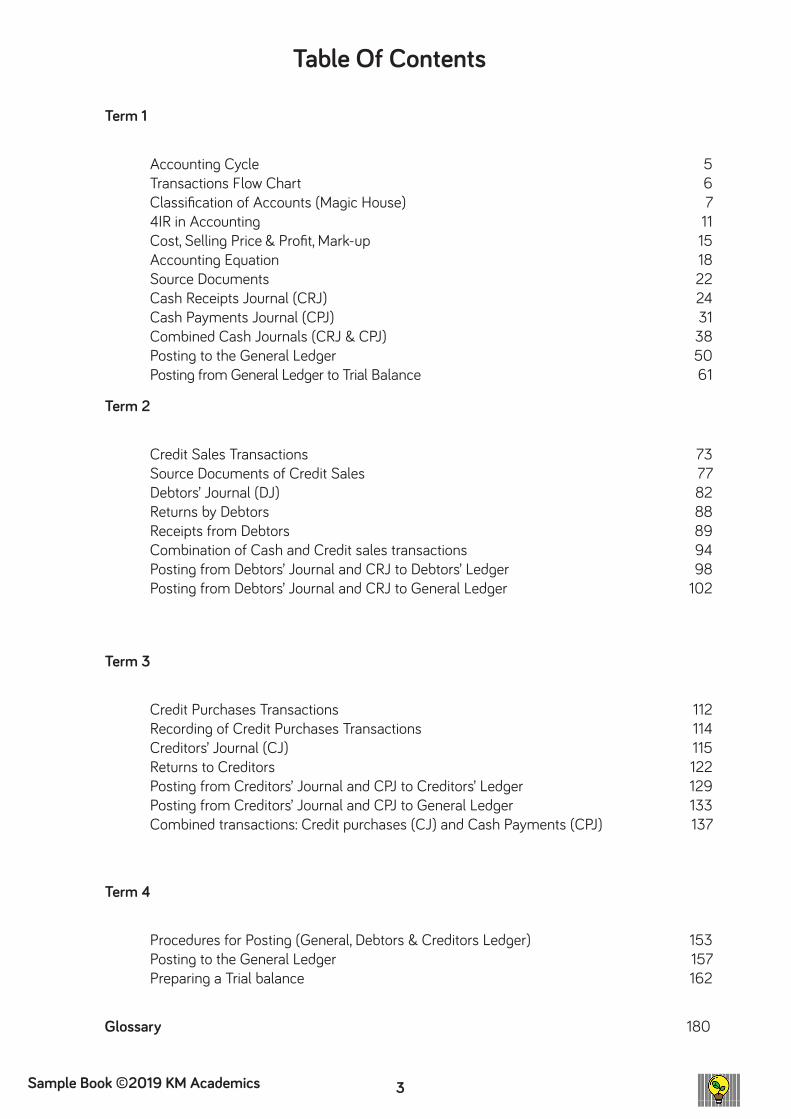

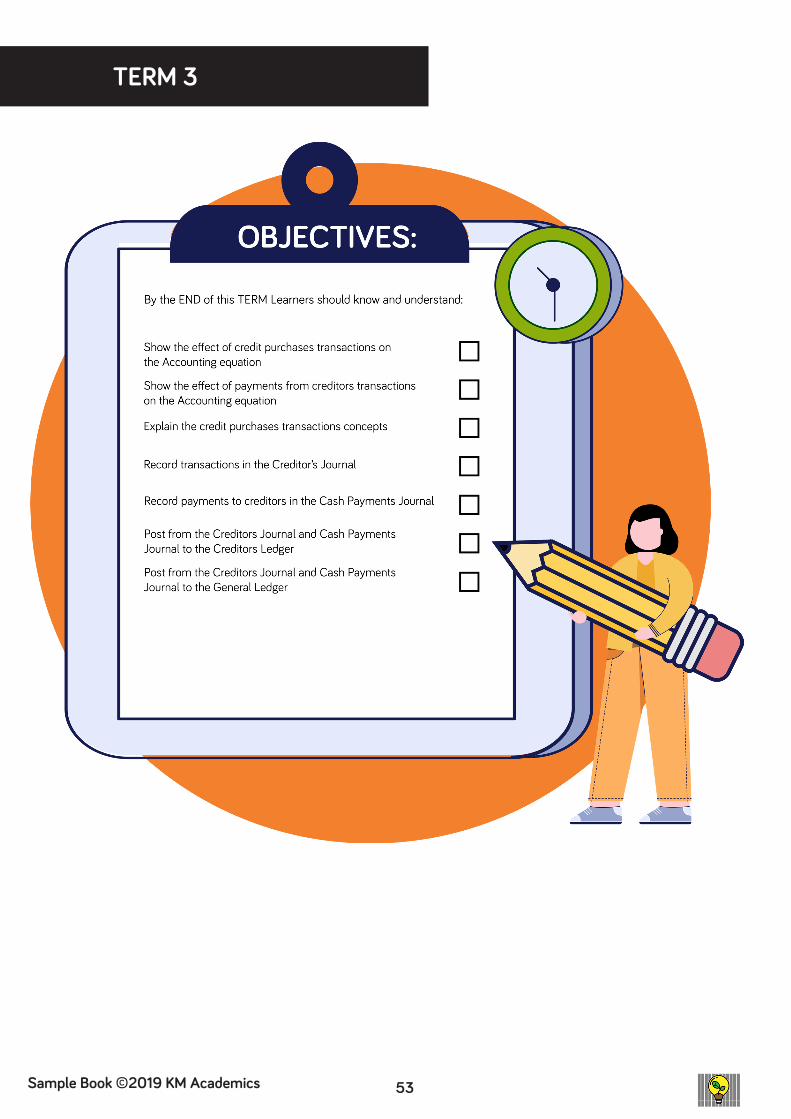

Term 1

Accounting Cycle 5 Transactions Flow Chart 6 Classification of Accounts (Magic House) 7 4IR in Accounting 11 Cost, Selling Price & Profit, Mark-up 15 Accounting Equation 18 Source Documents 22 Cash Receipts Journal (CRJ) 24 Cash Payments Journal (CPJ) 31 Combined Cash Journals (CRJ & CPJ) 38 Posting to the General Ledger 50 Posting from General Ledger to Trial Balance 61

Term 2

Credit Sales Transactions 73 Source Documents of Credit Sales 77 Debtors’ Journal (DJ) 82 Returns by Debtors 88 Receipts from Debtors 89 Combination of Cash and Credit sales transactions 94 Posting from Debtors’ Journal and CRJ to Debtors’ Ledger 98 Posting from Debtors’ Journal and CRJ to General Ledger 102

Term 3

Credit Purchases Transactions 112 Recording of Credit Purchases Transactions 114 Creditors’ Journal (CJ) 115 Returns to Creditors 122 Posting from Creditors’ Journal and CPJ to Creditors’ Ledger 129 Posting from Creditors’ Journal and CPJ to General Ledger 133 Combined transactions: Credit purchases (CJ) and Cash Payments (CPJ) 137

Term 4

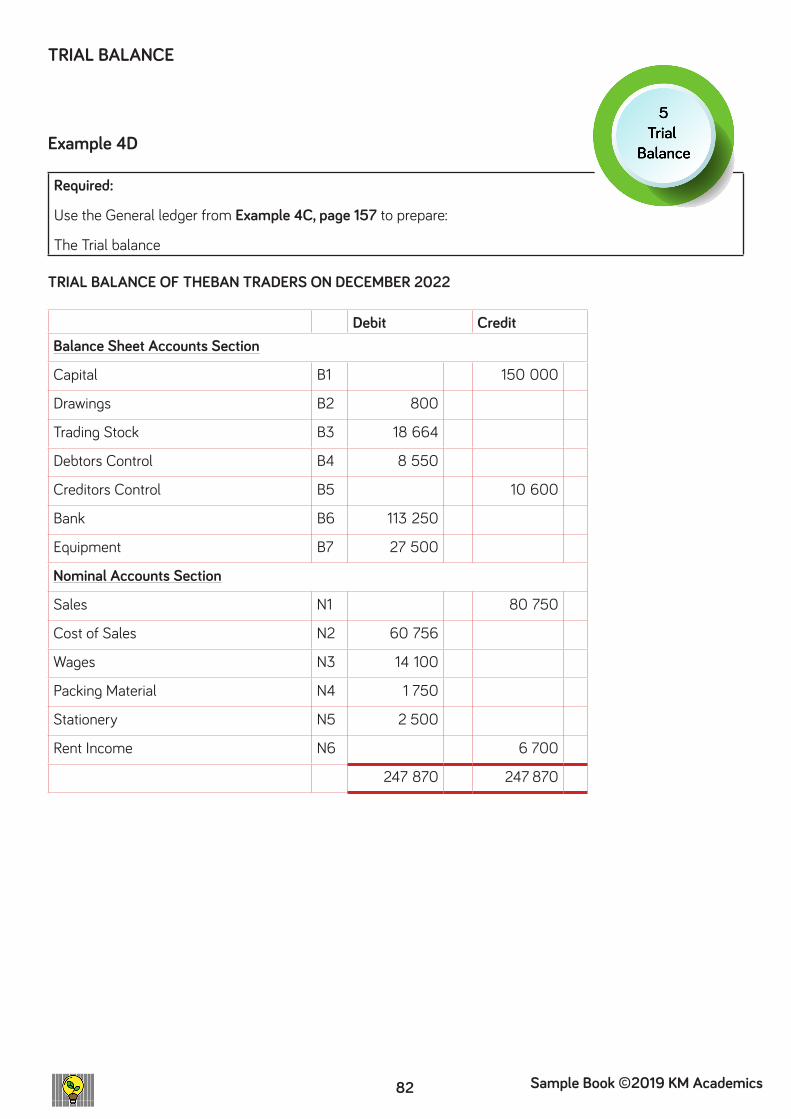

Procedures for Posting (General, Debtors & Creditors Ledger) 153 Posting to the General Ledger 157 Preparing a Trial balance 162

Glossary 180

Table Of Contents

4 Sample Book ©2019 KM Academics

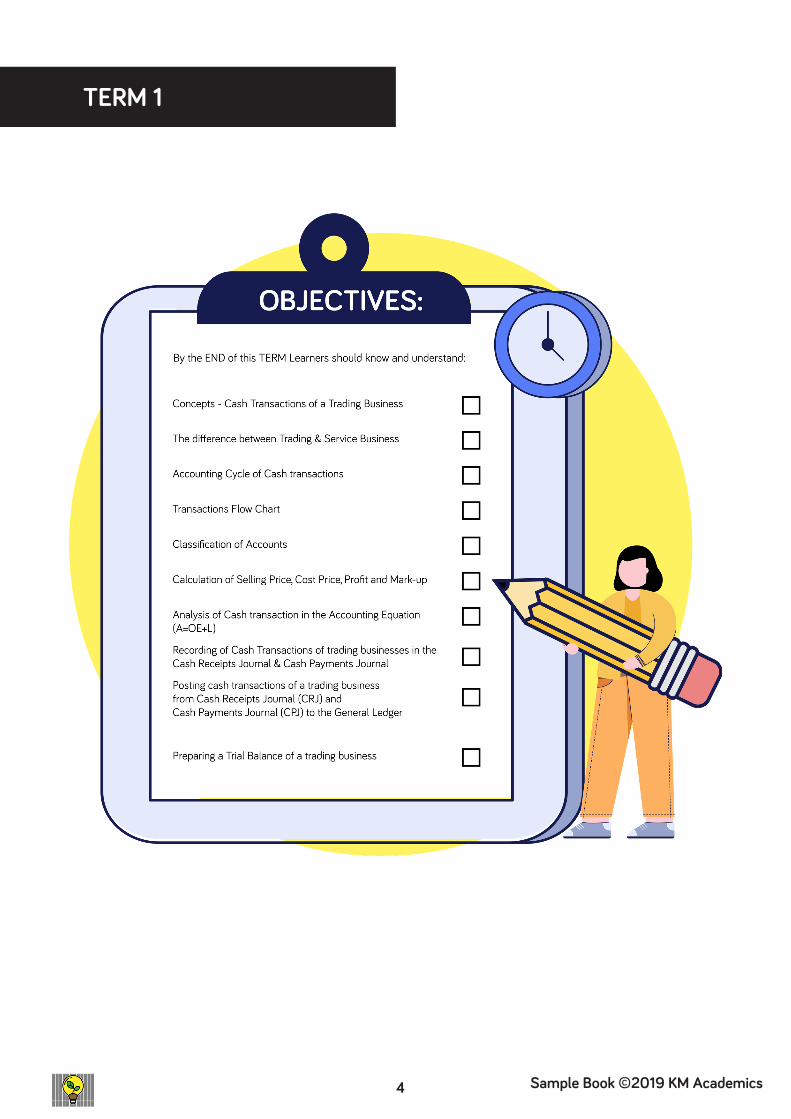

TERM 1

5Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

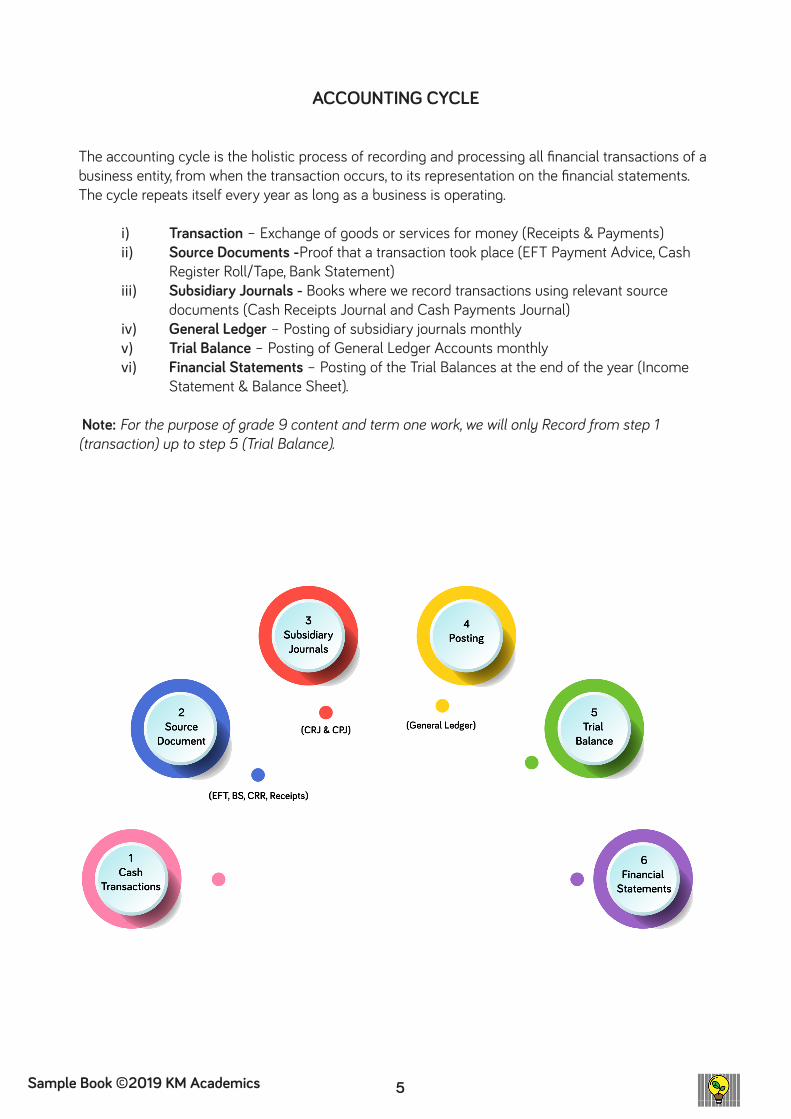

ACCOUNTING CYCLE

The accounting cycle is the holistic process of recording and processing all financial transactions of a business entity, from when the transaction occurs, to its representation on the financial statements.The cycle repeats itself every year as long as a business is operating.

i) Transaction – Exchange of goods or services for money (Receipts & Payments)ii) Source Documents -Proof that a transaction took place (EFT Payment Advice, Cash

Register Roll/Tape, Bank Statement)iii) Subsidiary Journals - Books where we record transactions using relevant source

documents (Cash Receipts Journal and Cash Payments Journal)iv) General Ledger – Posting of subsidiary journals monthlyv) Trial Balance – Posting of General Ledger Accounts monthlyvi) Financial Statements – Posting of the Trial Balances at the end of the year (Income

Statement & Balance Sheet).

Note: For the purpose of grade 9 content and term one work, we will only Record from step 1 (transaction) up to step 5 (Trial Balance).

6 Sample Book ©2019 KM Academics

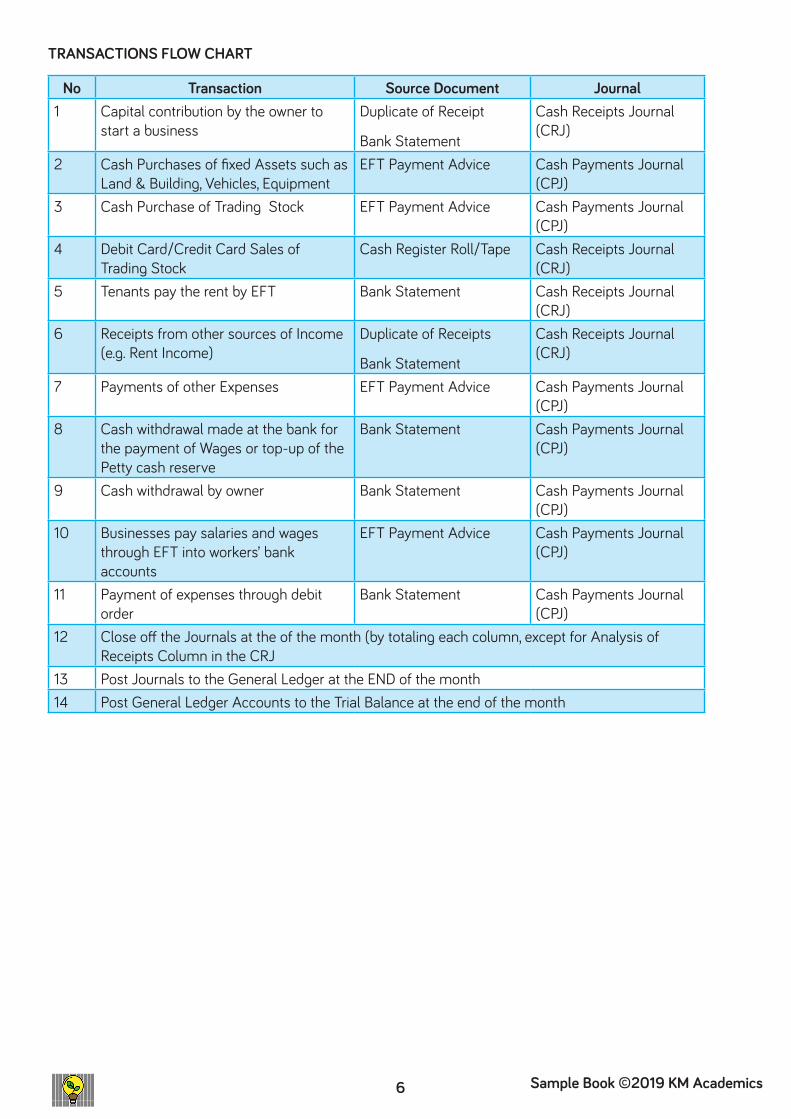

TRANSACTIONS FLOW CHART

No Transaction Source Document Journal1 Capital contribution by the owner to

start a businessDuplicate of Receipt

Bank Statement

Cash Receipts Journal (CRJ)

2 Cash Purchases of fixed Assets such as Land & Building, Vehicles, Equipment

EFT Payment Advice Cash Payments Journal (CPJ)

3 Cash Purchase of Trading Stock EFT Payment Advice Cash Payments Journal (CPJ)

4 Debit Card/Credit Card Sales of Trading Stock

Cash Register Roll/Tape Cash Receipts Journal (CRJ)

5 Tenants pay the rent by EFT Bank Statement Cash Receipts Journal (CRJ)

6 Receipts from other sources of Income (e.g. Rent Income)

Duplicate of Receipts

Bank Statement

Cash Receipts Journal (CRJ)

7 Payments of other Expenses EFT Payment Advice Cash Payments Journal (CPJ)

8 Cash withdrawal made at the bank for the payment of Wages or top-up of the Petty cash reserve

Bank Statement Cash Payments Journal (CPJ)

9 Cash withdrawal by owner Bank Statement Cash Payments Journal (CPJ)

10 Businesses pay salaries and wages through EFT into workers’ bank accounts

EFT Payment Advice Cash Payments Journal (CPJ)

11 Payment of expenses through debit order

Bank Statement Cash Payments Journal (CPJ)

12 Close off the Journals at the of the month (by totaling each column, except for Analysis of Receipts Column in the CRJ

13 Post Journals to the General Ledger at the END of the month14 Post General Ledger Accounts to the Trial Balance at the end of the month

7Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

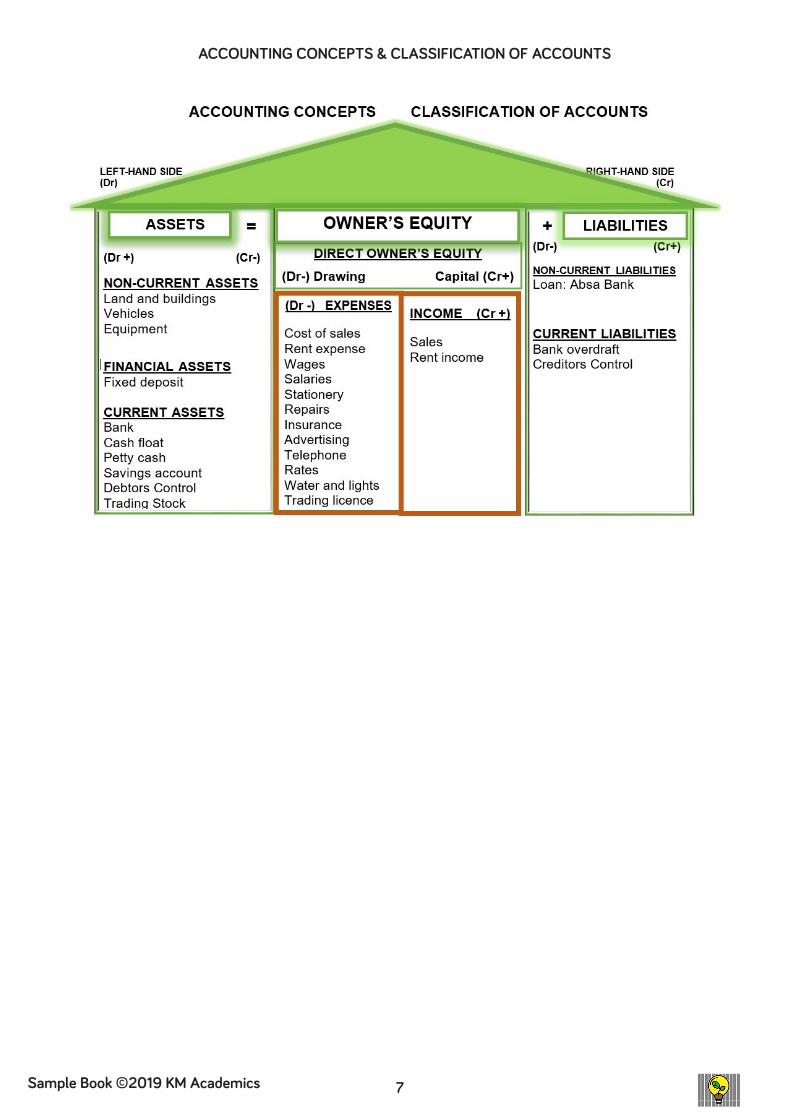

ACCOUNTING CONCEPTS & CLASSIFICATION OF ACCOUNTS

8 Sample Book ©2019 KM Academics

Grade 8 Revision Work DATE:______________________

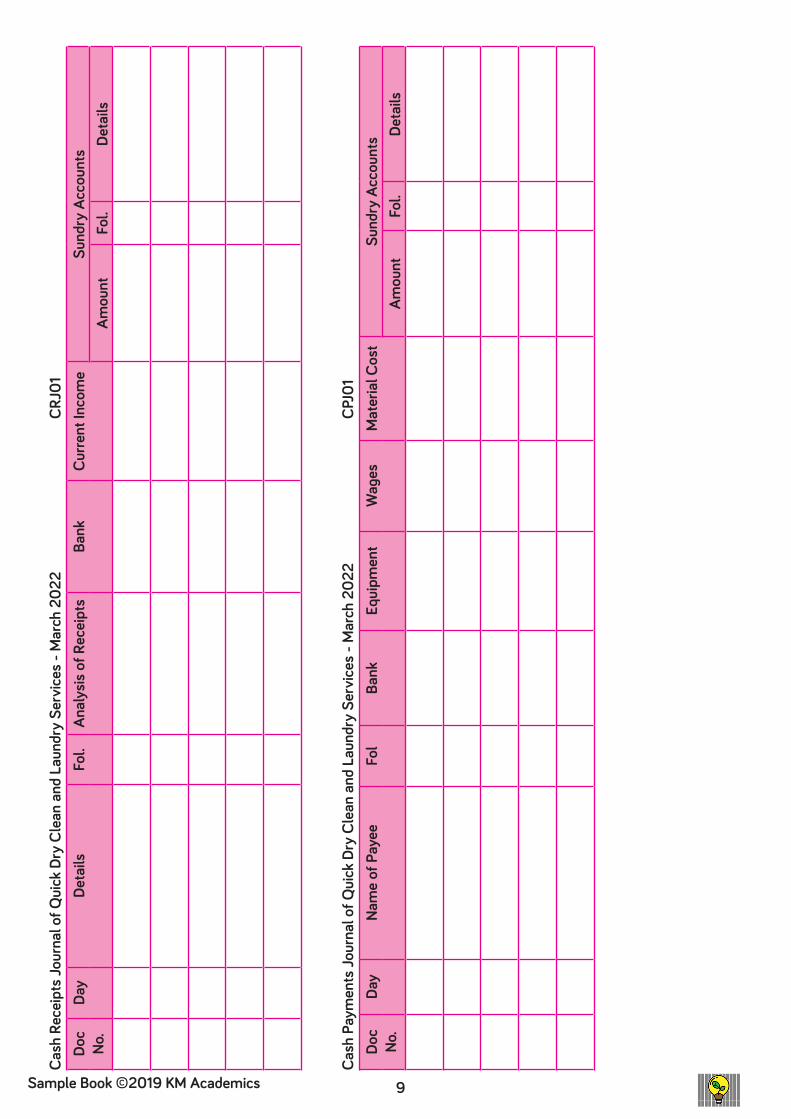

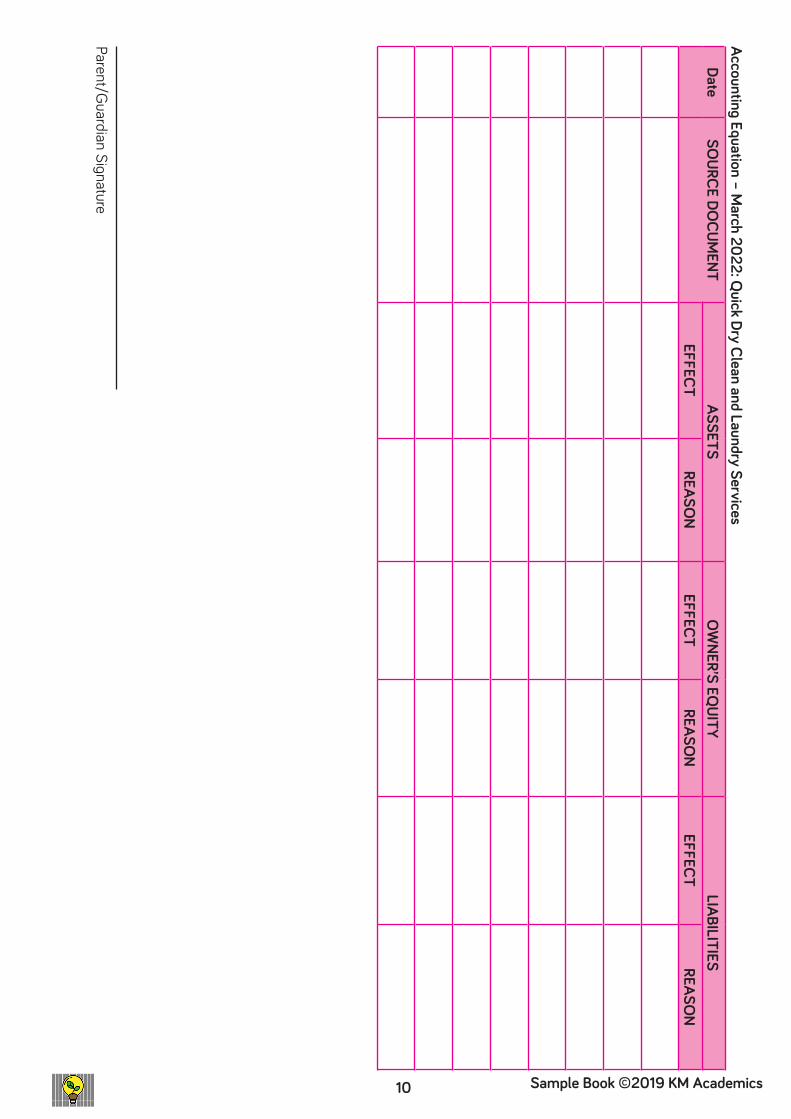

Angel Khanyile started a Dry Clean and Laundry service business “Quick Dry Clean and Laundry”.

Required:1. Record the following transaction in the Cash Receipts Journal of “Quick Dry Clean and Laundry Service

for the month of March 2022. Open columns for Analysis of Receipts, Bank, Current Income and Sundry Accounts.

2. Record the following transaction in the Cash Payment Journal of “Quick Dry Clean and Laundry Service for the month of March 2022. Open columns for Bank, Equipment, Wages, Material Cost and Sundry Accounts.

3. Analyse the transactions on the Accounting Equation4. Close the Journal off at the end of the month

Transactions: March 2022 – Quick Dry Clean and Laundry Services

On the 1st of March Ms. Angel Khanyile electronically transferred R 250 000 as her Capital contribution. On the 3rd of March she purchased dry clean machines amounting to R 60 000 from Fistos Machines and paid by EFT01. On the 5th she received R 11 200 for Services Rendered as per cash register tape and on the same day she received R 5000 via EFT from Xolile Tshabalala who is Renting part of the building for her salon business. On the 6th of March she bought Material Cost from Plastic World for R 1 500 and paid by EFT. On the 10th she made an EFT to pay weekly Wages to S. Sankey, R 2 500. On the 15th she received R 12 000 for Services Rendered as per cash register tape. On the 25th the debit order amounting to R 3 500 for owner’s private car insurance with OUTsurance came through as per bank statement.

9Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

Cash

Rec

eipt

s Jo

urna

l of Q

uick

Dry

Cle

an a

nd L

aund

ry S

ervi

ces

- Mar

ch 2

022

CRJ

01Do

cNo

.Da

yDe

tails

Fol.

Anal

ysis

of R

ecei

pts

Bank

Curre

nt In

com

eSu

ndry

Acc

ount

sAm

ount

Fol.

Deta

ils

Cash

Pay

men

ts Jo

urna

l of Q

uick

Dry

Cle

an a

nd L

aund

ry S

ervi

ces

- Mar

ch 2

022

CPJ

01Do

cNo

.Da

yNa

me

of P

ayee

Fo

lBa

nkEq

uipm

ent

Wag

esM

ater

ial C

ost

Sund

ry A

ccou

nts

Amou

ntFo

l.De

tails

10 Sample Book ©2019 KM Academics

Accounting Equation – March 2022: Q

uick Dry Clean and Laundry ServicesDate

SOURCE DO

CUMENT

ASSETSO

WNER’S EQ

UITYLIABILITIES

EFFECTREASO

NEFFECT

REASON

EFFECTREASO

N

Parent/Guardian Signature

11Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

CONCEPTS OF FOURTH INDUSTRIAL REVOLUTION (4IR) in Accounting:

The impact of 4IR in the Accounting and Auditing profession27 January 20224IR (Fourth Industrial Revolution) is upon us and we can no longer place it in the back seat. We as professionals are now being forced to embrace, adapt and adopt these changes in order to remain relevant in our ever-changing digital world. If there is one thing that the global COVID-19 pandemic has highlighted, it is just how quickly the world can transform and just how much technology is integrated in our everyday lives – both private and work life.The pandemic has forced companies to rapidly move to remote working and often rely solely on advanced technology and digital infrastructure to keep them afloat. Professor Klaus Schwab, Founder and Executive Chairman of the World Economic Forum, said; “New technologies will dramatically change the nature of work across all industries and occupations.” This is certainly true, and the Auditing and Accounting profession is no exception.Some emerging technologies brought forth by the 4IR are already wide-spread and fully integrated in our industry. For example, many Accounting software packages now have built-in reporting solutions that produce financial statements and perform repetitive record keeping more efficiently and accurately using Robotic Process Automation. In the Auditing profession, data analytics tools are more commonly used to extract volumes of data from the client’s records and apply advanced analytical checks to provide deeper insight into trends and patterns identified and highlight exceptions uncovered using the entire population of entries as opposed to sampling.Block-chain technology is said to be the next incredible breakthrough that will transform the Accounting and auditing profession, making financial record-keeping less costly, more reliable, and more accurate. Block-chain technology records transactions in a distributed ledger. Thus far, the technology has proven to be highly secure. The one appealing feature of block-chain technology is its ability to eliminate an intermediary, such as a bank, to verify a transaction.Block-chain operates through a secure peer-to-peer network. When a new transaction is initiated, all participants in this network who have an identical copy and real-time access to the block-chain ledger, communicate and verify the validity of the transaction before being entered into the block-chain. Once a transaction is added, it is encrypted and cannot be deleted or modified. To bring this back to Accounting, this technology is being explored to be used as a digital ledger whereby transactions from both buyer and seller can be recorded in real-time on one system and all the participants in the transaction have access to the ledger and can validate the details of the transaction before it is recorded. Think of it as one big spreadsheet that keeps track of a transaction from supply chain to consumer consumption in one ledger with minimal human intervention. Block-chain eliminates chances of human manipulation and reduces the need for reconciliation and third part confirmation of existence and accuracy of the transaction.In recent years, we have seen several disheartening headlines relating to corruption in the political environment and unethical conduct within our profession. With the recent scandals such as Steinhoff and VBS, it is clear to see that there is a dire need for financial record transparency among stakeholders. This emerging technology has the potential to address the issue of trust and speed up Auditing processes.

IS THERE A NEED FOR ACCOUNTANTS AND AUDITORS IN THE NEAR FUTURE?The emerging technologies are most certainly going to replace several repetitive tasks we now do. However, the answer to the question of whether the robots will take your job is dependent on your willingness to adapt and evolve along with the technology. I believe companies will still need CAs, however the role we play will transform. As automation becomes more and more of a reality, the role of an Accountant will transform into an advisory role which will require the competence to analyse, interpret and use the output produced by these technologies and feed into operational and strategic decisions. Auditors will not be erased by the rise of AI and Blockchain but rather these technologies will generate opportunities to enhance audit execution and leave more time to analyse data and provide quality, value-adding feedback and recommendations to clients.

12 Sample Book ©2019 KM Academics

The Fourth Industrial Revolution (4IR) represents a fundamental change in the way we live, WORK and relate to one another. It is a new chapter in human development, enabled by extraordinary technology advances commensurate with those of the first, second and third industrial revolutions.

Parent/Guardian Signature

All these technological advances are still in the infant stage, however the impact it is expected to make cannot be ignored. What Accountants and auditors need to do is prepare and equip themselves for the future. In order to remain competitive, we need to evolve and adopt an innovative mindset. We need to be alert to these technological changes, invest and commit to continuous learning to improve our digital intelligence and solutions.

Lilly MollelAudit Manager, Johannesburg

1.1. In your own words, explain Fourth Industrial Revolution (4IR)

________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________

1.2. How will the Block-chain software assist the Accounting and Auditing profession? ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________

1.3. Write a short paragraph about how 4IR is affecting and will affect the Accounting related professions? ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________

1.4. What is your advice to existing and aspiring Accounting related professionals in order for them to remain relevant with all changes that are brought about by technological developments?

________________________________________________________________________________ ________________________________________________________________________________ ________________________________________________________________________________

13Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

Parent/Guardian Signature

Activity A DATE:________________________

Mention as many as possible points with regard to impact of COVID-19 with reference to our Country’s:

1. Education _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________

2. Economy _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________

3. Financial Sector _______________________________________________________________________________________________ _______________________________________________________________________________________________ _______________________________________________________________________________________________

IMPACT OF COVID-19 IN OUR EDUCATION, ECONOMY & FINANCIAL SECTORS

On the 5th of March 2020, the National Institute for Communicable Diseases confirmed the first suspected case of COVID-19. Since then, there has been a rapid increase in the number of positive cases reported in our country and globally. Number of COVID-19 related deaths are been confirmed daily. Ordinary citizens, politi-cians, business people, doctors, nurses have lost lives due to COVID-19. Countries were forced to embark on hard lock-down regulations in response to COVID-19 in trying to save lives. Businesses closed down, people lost their jobs and economic activities went down globally.

14 Sample Book ©2019 KM Academics

Introduction

Looking back…

In Grade 8 you have learnt about bookkeeping of a service business.A service business is a business that earns income by providing a service to clients. Examples of service businesses are a barber shop, hair salon/ hairdresser, shoe repair, cleaning services, appliances repair, property developer, Auditors, Architects, plumbing business, spa treatment, dry cleaners, etc.All these businesses obtain income by rendering a service.

Looking forward…In Grade 9 you are going to learn about a trading business.

Trading businesses are businesses that Buy goods with the purpose of Reselling them at a higher Price in order to earn profit.

Examples of trading businesses are clothing stores, food chain stores, fast foods outlets, hardware, furniture stores and so on.Another name for a trading business is a retail business.

How a trading business operatesA trading business buys goods at a certain price and sells them at a higher price.The difference between the purchase price and the selling price is the business’ income or profit.The profit forms part of the Owner’s equity. The profit percentage is also referred to as the ‘profit mark-up’.

• Cost price + profit mark-up = selling price

15Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

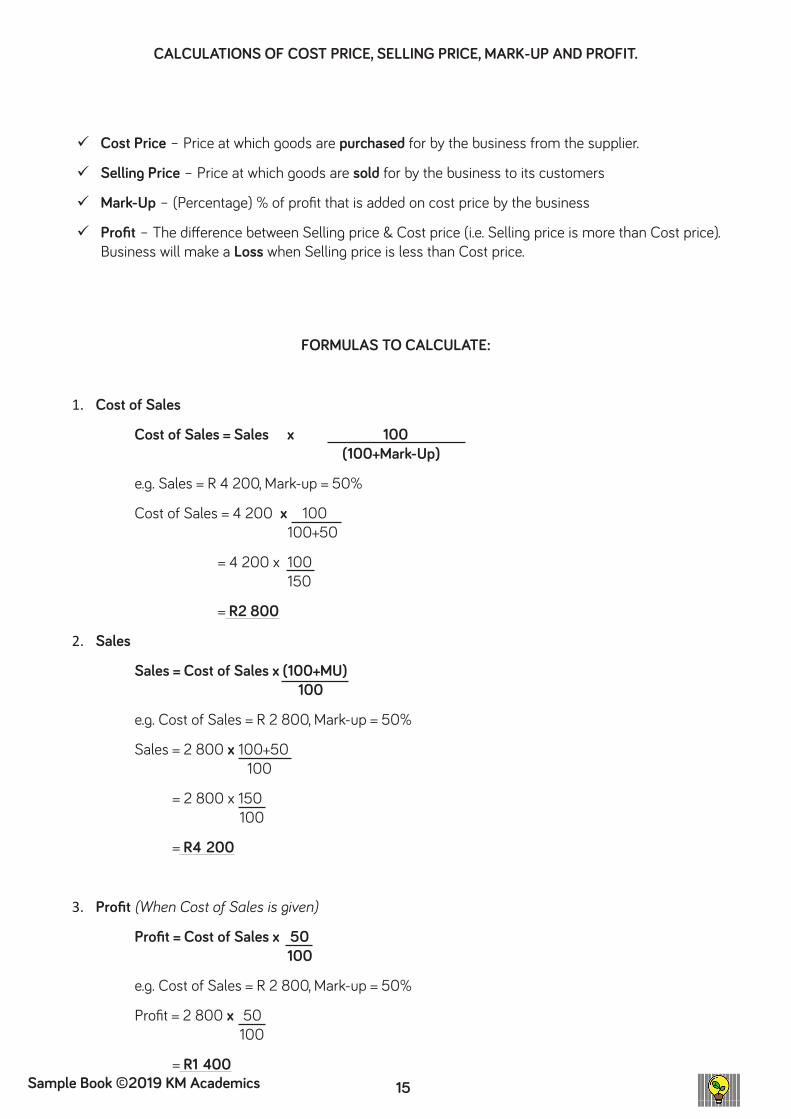

CALCULATIONS OF COST PRICE, SELLING PRICE, MARK-UP AND PROFIT.

Cost Price – Price at which goods are purchased for by the business from the supplier.

Selling Price – Price at which goods are sold for by the business to its customers

Mark-Up – (Percentage) % of profit that is added on cost price by the business

Profit – The difference between Selling price & Cost price (i.e. Selling price is more than Cost price). Business will make a Loss when Selling price is less than Cost price.

FORMULAS TO CALCULATE:

1. Cost of Sales

Cost of Sales = Sales x 100 (100+Mark-Up)

e.g. Sales = R 4 200, Mark-up = 50%

Cost of Sales = 4 200 x 100 100+50

= 4 200 x 100 150

= R2 800

2. Sales

Sales = Cost of Sales x (100+MU) 100

e.g. Cost of Sales = R 2 800, Mark-up = 50%

Sales = 2 800 x 100+50 100

= 2 800 x 150 100

= R4 200

3. Profit (When Cost of Sales is given)

Profit = Cost of Sales x 50 100

e.g. Cost of Sales = R 2 800, Mark-up = 50%

Profit = 2 800 x 50 100

= R1 400

16 Sample Book ©2019 KM Academics

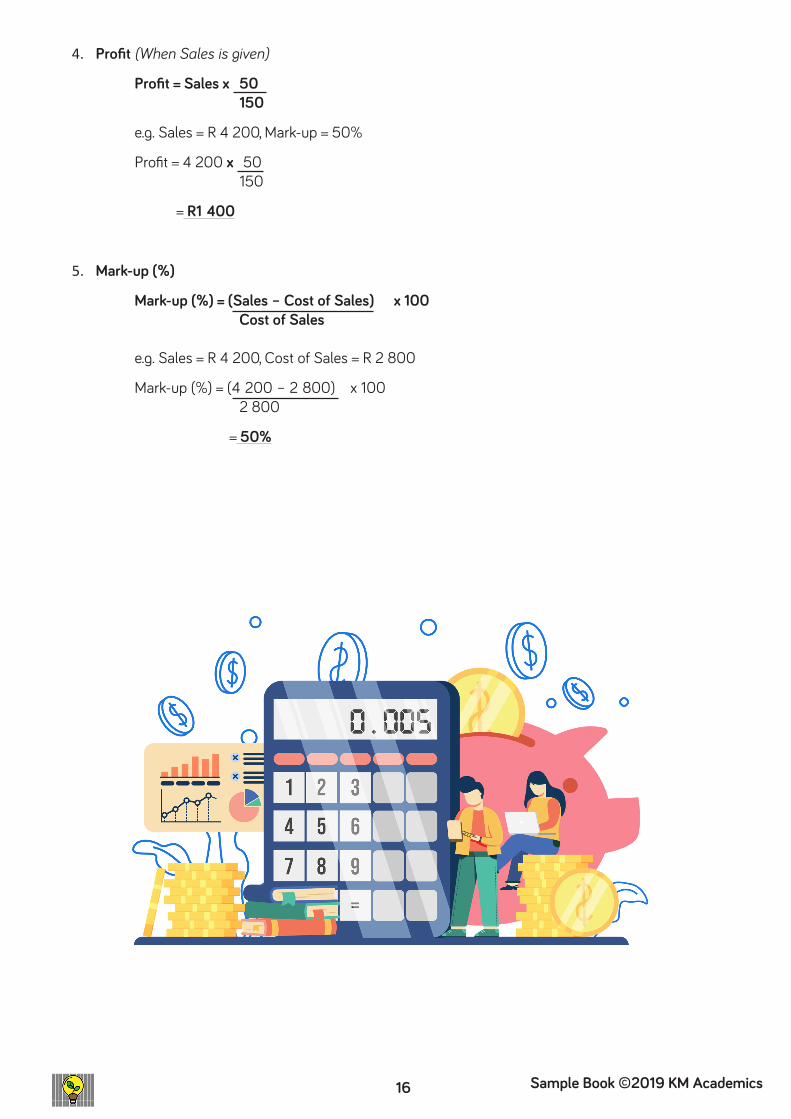

4. Profit (When Sales is given)

Profit = Sales x 50 150

e.g. Sales = R 4 200, Mark-up = 50%

Profit = 4 200 x 50 150

= R1 400

5. Mark-up (%)

Mark-up (%) = (Sales – Cost of Sales) x 100 Cost of Sales e.g. Sales = R 4 200, Cost of Sales = R 2 800

Mark-up (%) = (4 200 – 2 800) x 100 2 800

= 50%

17Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

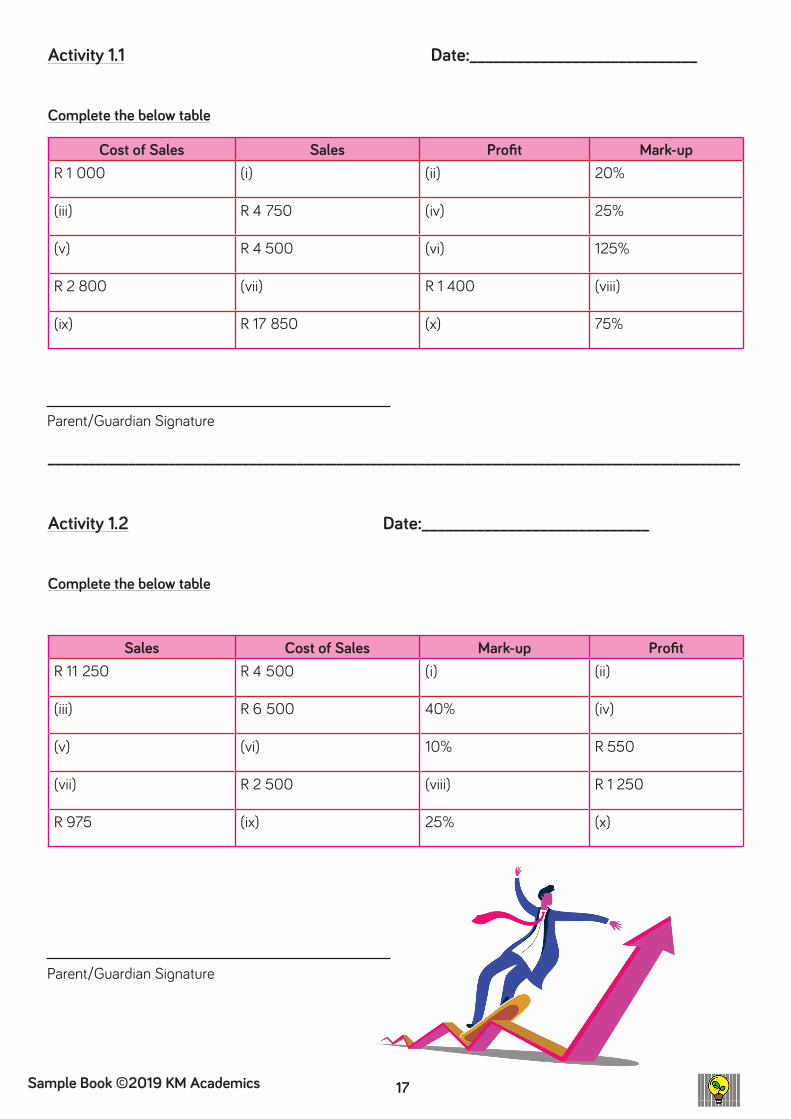

Activity 1.1 Date:_____________________________

Complete the below table

Cost of Sales Sales Profit Mark-upR 1 000 (i) (ii) 20%

(iii) R 4 750 (iv) 25%

(v) R 4 500 (vi) 125%

R 2 800 (vii) R 1 400 (viii)

(ix) R 17 850 (x) 75%

_______________________________________________________________________________________________________

Activity 1.2 Date:_____________________________

Complete the below table

Sales Cost of Sales Mark-up ProfitR 11 250 R 4 500 (i) (ii)

(iii) R 6 500 40% (iv)

(v) (vi) 10% R 550

(vii) R 2 500 (viii) R 1 250

R 975 (ix) 25% (x)

Parent/Guardian Signature

Parent/Guardian Signature

18 Sample Book ©2019 KM Academics

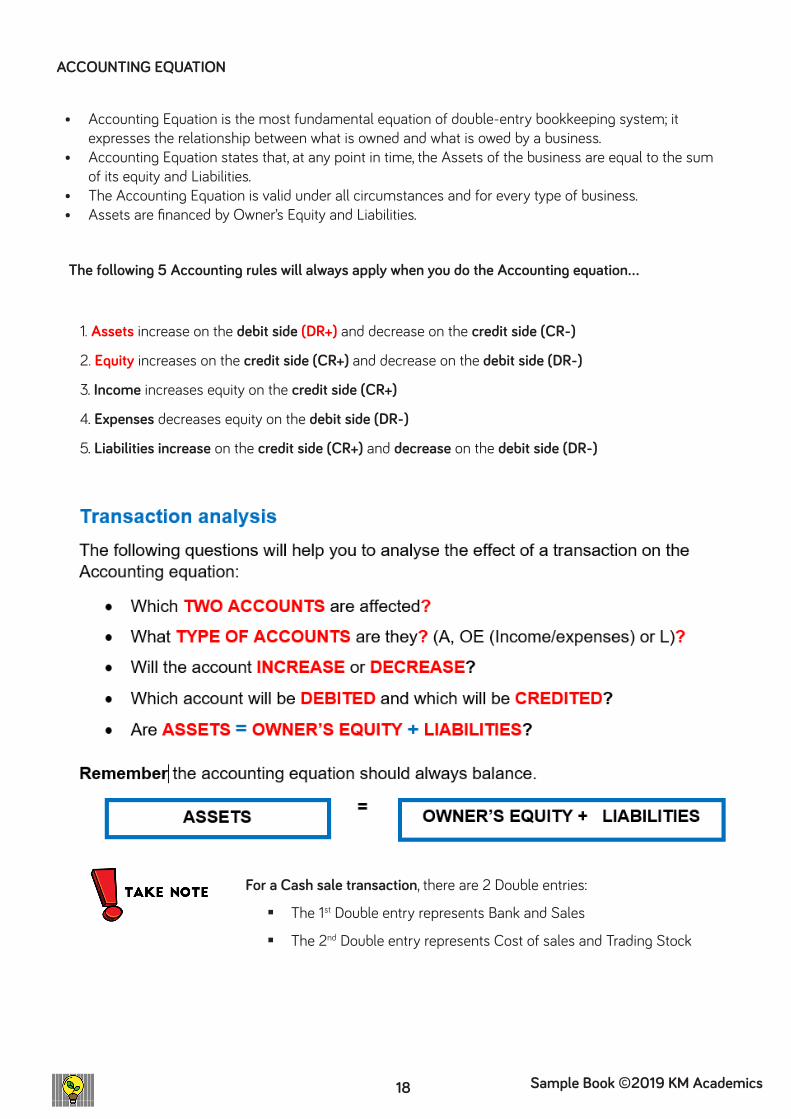

The following 5 Accounting rules will always apply when you do the Accounting equation…

1. Assets increase on the debit side (DR+) and decrease on the credit side (CR-)

2. Equity increases on the credit side (CR+) and decrease on the debit side (DR-)

3. Income increases equity on the credit side (CR+)

4. Expenses decreases equity on the debit side (DR-)

5. Liabilities increase on the credit side (CR+) and decrease on the debit side (DR-)

ACCOUNTING EQUATION

For a Cash sale transaction, there are 2 Double entries:

The 1st Double entry represents Bank and Sales

The 2nd Double entry represents Cost of sales and Trading Stock

• Accounting Equation is the most fundamental equation of double-entry bookkeeping system; it expresses the relationship between what is owned and what is owed by a business.

• Accounting Equation states that, at any point in time, the Assets of the business are equal to the sum of its equity and Liabilities.

• The Accounting Equation is valid under all circumstances and for every type of business.• Assets are financed by Owner’s Equity and Liabilities.

19Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

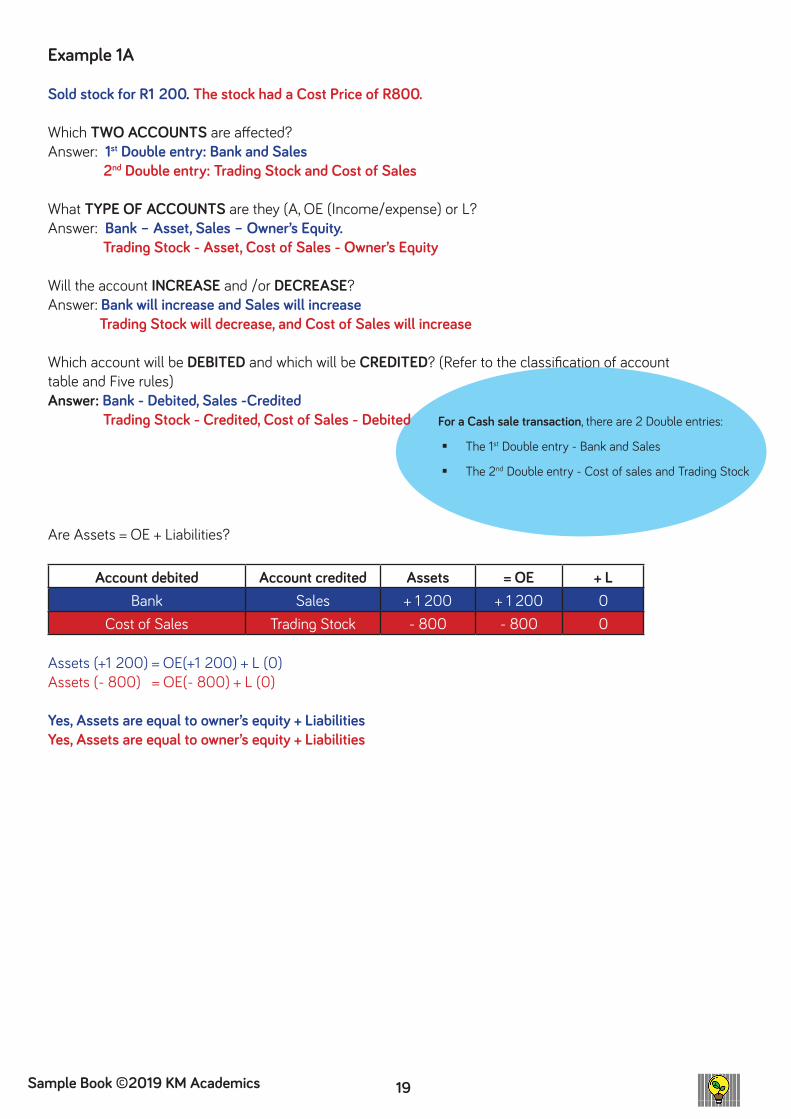

Example 1A Sold stock for R1 200. The stock had a Cost Price of R800.

Which TWO ACCOUNTS are affected?Answer: 1st Double entry: Bank and Sales 2nd Double entry: Trading Stock and Cost of Sales

What TYPE OF ACCOUNTS are they (A, OE (Income/expense) or L?Answer: Bank – Asset, Sales – Owner’s Equity. Trading Stock - Asset, Cost of Sales - Owner’s Equity

Will the account INCREASE and /or DECREASE?Answer: Bank will increase and Sales will increase Trading Stock will decrease, and Cost of Sales will increase

Which account will be DEBITED and which will be CREDITED? (Refer to the classification of account table and Five rules)Answer: Bank - Debited, Sales -Credited Trading Stock - Credited, Cost of Sales - Debited

Are Assets = OE + Liabilities?

Account debited Account credited Assets = OE + LBank Sales + 1 200 + 1 200 0

Cost of Sales Trading Stock - 800 - 800 0

Assets (+1 200) = OE(+1 200) + L (0)Assets (- 800) = OE(- 800) + L (0)

Yes, Assets are equal to owner’s equity + LiabilitiesYes, Assets are equal to owner’s equity + Liabilities

For a Cash sale transaction, there are 2 Double entries:

The 1st Double entry - Bank and Sales

The 2nd Double entry - Cost of sales and Trading Stock

20 Sample Book ©2019 KM Academics

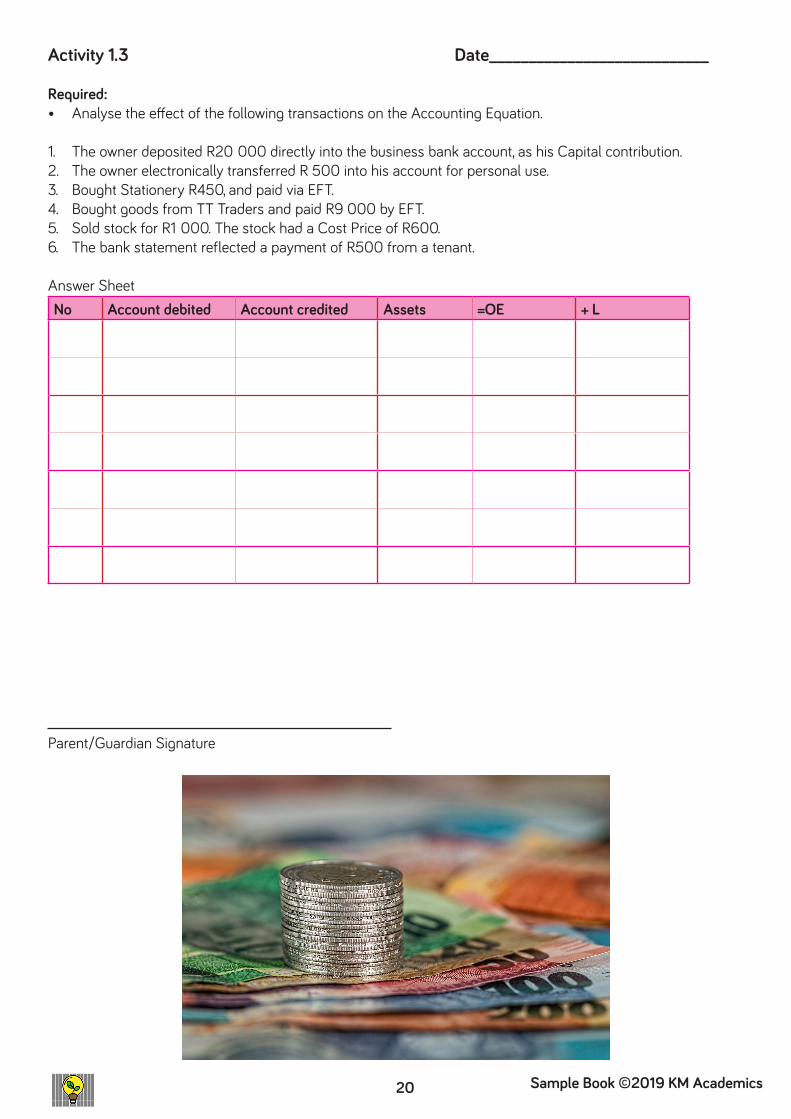

Activity 1.3 Date____________________________

Required:• Analyse the effect of the following transactions on the Accounting Equation.

1. The owner deposited R20 000 directly into the business bank account, as his Capital contribution.2. The owner electronically transferred R 500 into his account for personal use.3. Bought Stationery R450, and paid via EFT.4. Bought goods from TT Traders and paid R9 000 by EFT.5. Sold stock for R1 000. The stock had a Cost Price of R600.6. The bank statement reflected a payment of R500 from a tenant. Answer SheetNo Account debited Account credited Assets =OE + L

Parent/Guardian Signature

21Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

Activity 1.4 Date____________________________

Required:• Analyse the effect of the following transactions on the Accounting Equation.

1. The owner deposited R60 000 directly into the business bank account, as his Capital contribution. 2. The owner electronically transferred R 2 000 into her account for personal use. 3. Bought Packing Material R620, and paid via EFT. 4. Bought Equipment from B Technologies and paid R16 000 by EFT.5. Cash sales according to Cash Register Roll, R1 500 (mark-up on cost 50%)6. The bank statement reflected a payment of R900 from Mr Mkhize the new tenant. Answer SheetNo Account debited Account credited Assets =OE + L

Parent/Guardian Signature

22 Sample Book ©2019 KM Academics

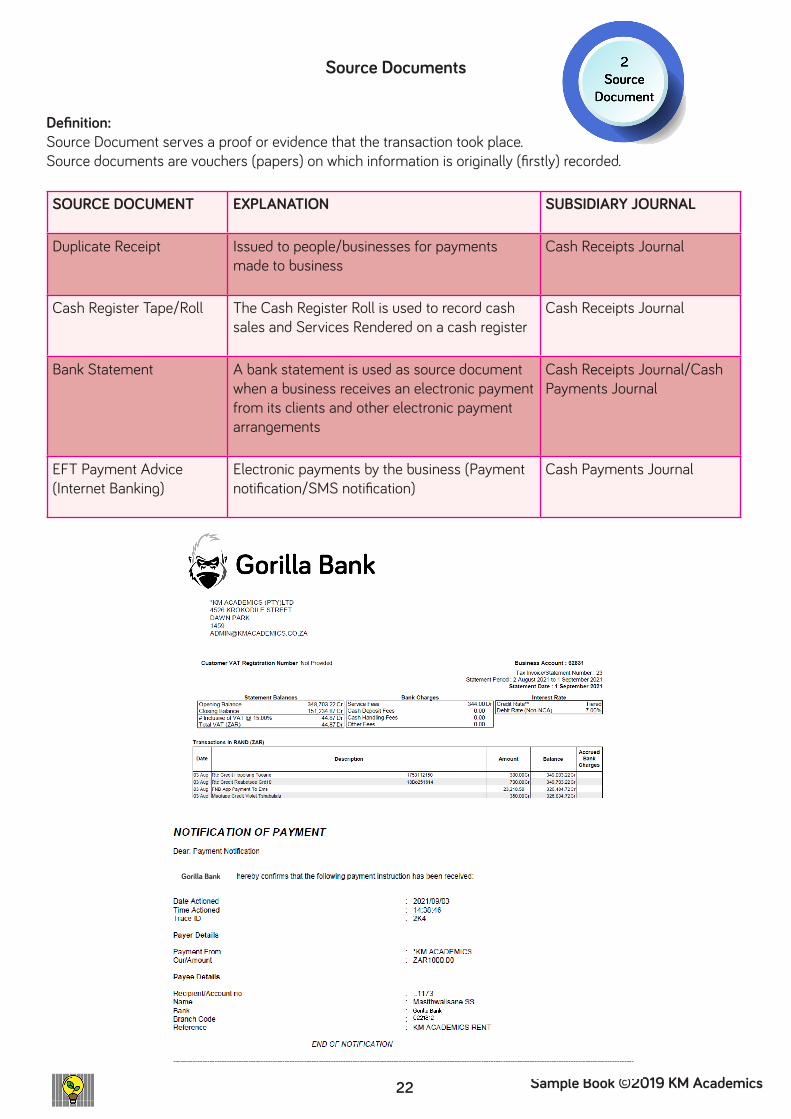

Source Documents

Definition:Source Document serves a proof or evidence that the transaction took place.Source documents are vouchers (papers) on which information is originally (firstly) recorded.

SOURCE DOCUMENT EXPLANATION SUBSIDIARY JOURNAL

Duplicate Receipt Issued to people/businesses for payments made to business

Cash Receipts Journal

Cash Register Tape/Roll The Cash Register Roll is used to record cash sales and Services Rendered on a cash register

Cash Receipts Journal

Bank Statement A bank statement is used as source document when a business receives an electronic payment from its clients and other electronic payment arrangements

Cash Receipts Journal/Cash Payments Journal

EFT Payment Advice(Internet Banking)

Electronic payments by the business (Payment notification/SMS notification)

Cash Payments Journal

Gorilla Bank

23Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

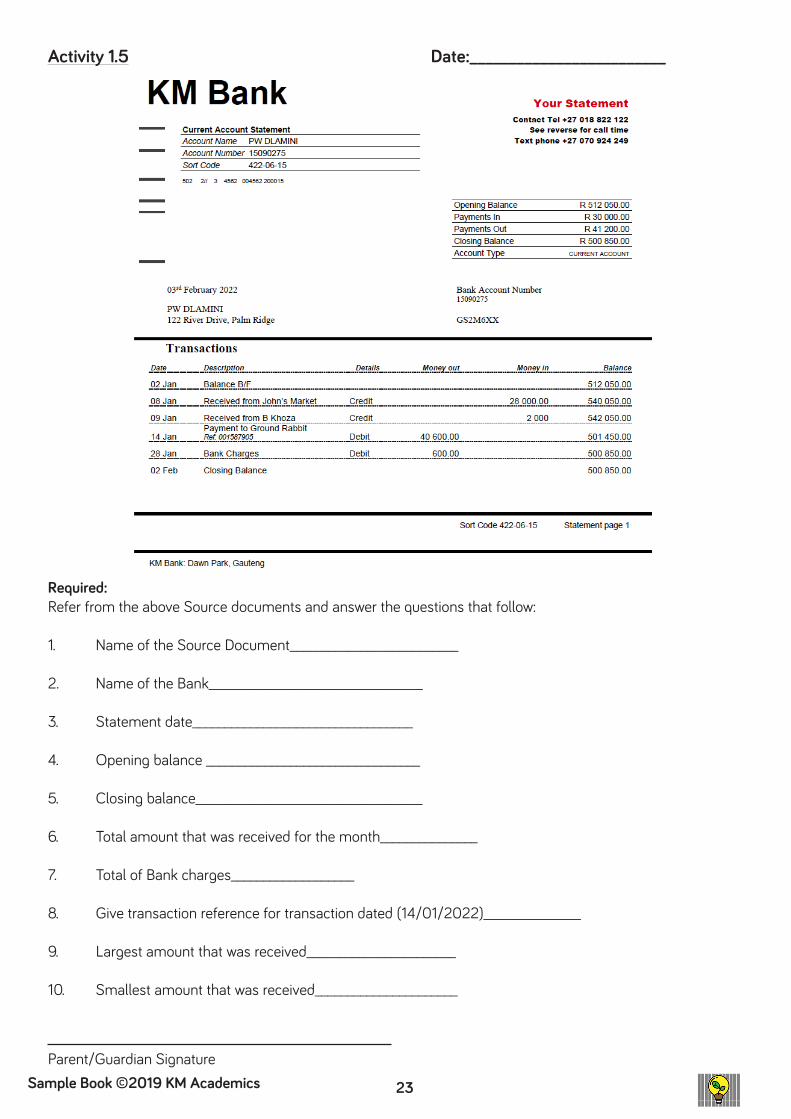

Required:Refer from the above Source documents and answer the questions that follow:

1. Name of the Source Document__________________________

2. Name of the Bank_________________________________

3. Statement date__________________________________

4. Opening balance _________________________________

5. Closing balance___________________________________

6. Total amount that was received for the month_______________

7. Total of Bank charges___________________

8. Give transaction reference for transaction dated (14/01/2022)_______________

9. Largest amount that was received_______________________

10. Smallest amount that was received______________________

Activity 1.5 Date:_________________________

Parent/Guardian Signature

24 Sample Book ©2019 KM Academics

CASH JOURNALS (Step 3 in the Accounting Cycle)

• Cash Journals are journals used to record ALL Cash transactions (inflow and outflow of cash) of the business.

• Movement of cash

Analysis of Cash Journals Transactions:

• Identify the source document and source document number.

• Identify the journal.

• Identify the accounts (Bank will always be ONE of the Accounts).

• Provide for the relevant columns in the journal. (Format of Journals)

• Record the transaction in the journal.

• Check whether the concept of double entry principle is applied correctly.

• Close off the journal at the end of the month. (Total)

CASH RECEIPTS JOURNAL

• Cash Receipts Journals is used to record ALL the monies received by the business from different sources (Capital Contribution, Sales, Rent Income, etc)

• Close off the Journal at the END of each month and Post all Accounts to the General Ledger

• Source documents for CRJ transactions includes, CRR, CRT, Duplicate Receipt, Bank Statement (BS)

25Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

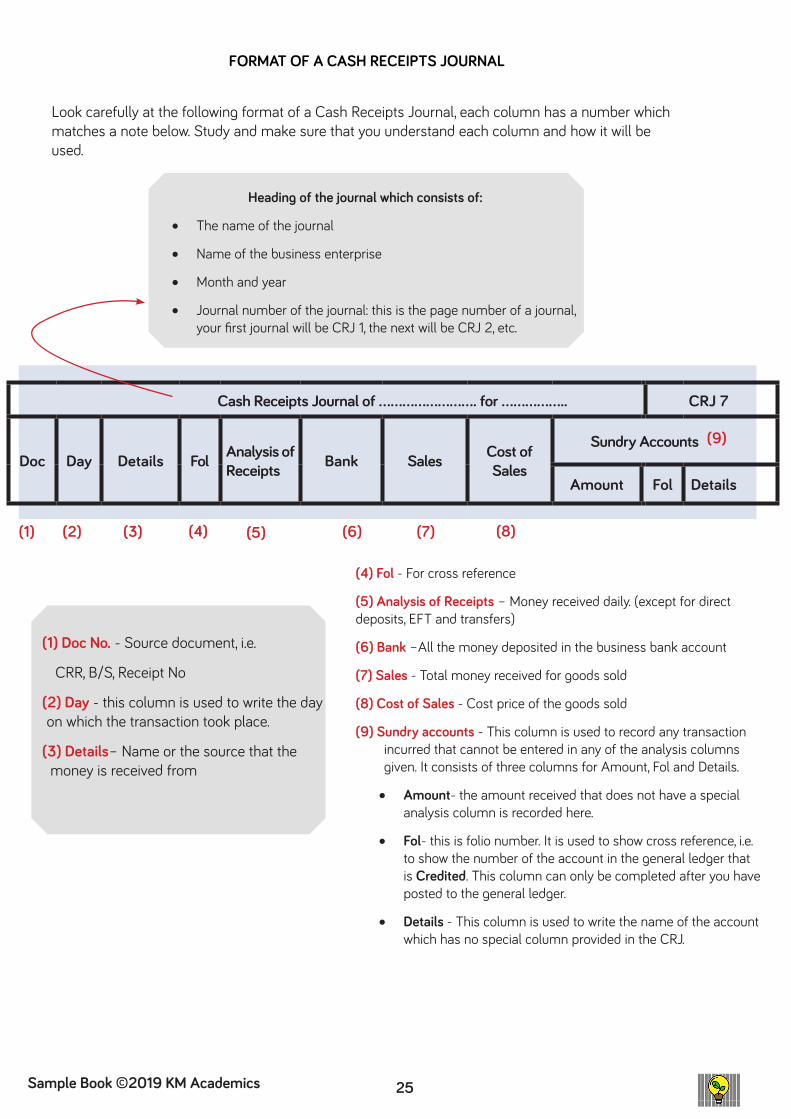

FORMAT OF A CASH RECEIPTS JOURNAL

Look carefully at the following format of a Cash Receipts Journal, each column has a number which matches a note below. Study and make sure that you understand each column and how it will be used.

Cash Receipts Journal of ……………………. for …………….. CRJ 7

Doc Day Details Fol Analysis of Receipts Bank Sales Cost of

Sales

Sundry Accounts

Amount Fol Details

Heading of the journal which consists of:

• The name of the journal

• Name of the business enterprise

• Month and year

• Journal number of the journal: this is the page number of a journal, your first journal will be CRJ 1, the next will be CRJ 2, etc.

(1) Doc No. - Source document, i.e.

CRR, B/S, Receipt No

(2) Day - this column is used to write the day on which the transaction took place.

(3) Details– Name or the source that the money is received from

(4) Fol - For cross reference

(5) Analysis of Receipts – Money received daily. (except for direct deposits, EFT and transfers)

(6) Bank –All the money deposited in the business bank account

(7) Sales - Total money received for goods sold

(8) Cost of Sales - Cost price of the goods sold

(9) Sundry accounts - This column is used to record any transaction incurred that cannot be entered in any of the analysis columns given. It consists of three columns for Amount, Fol and Details.

• Amount- the amount received that does not have a special analysis column is recorded here.

• Fol- this is folio number. It is used to show cross reference, i.e. to show the number of the account in the general ledger that is Credited. This column can only be completed after you have posted to the general ledger.

• Details - This column is used to write the name of the account which has no special column provided in the CRJ.

(1) (2) (3) (4) (5) (6)

(9)

(7) (8)

26 Sample Book ©2019 KM Academics

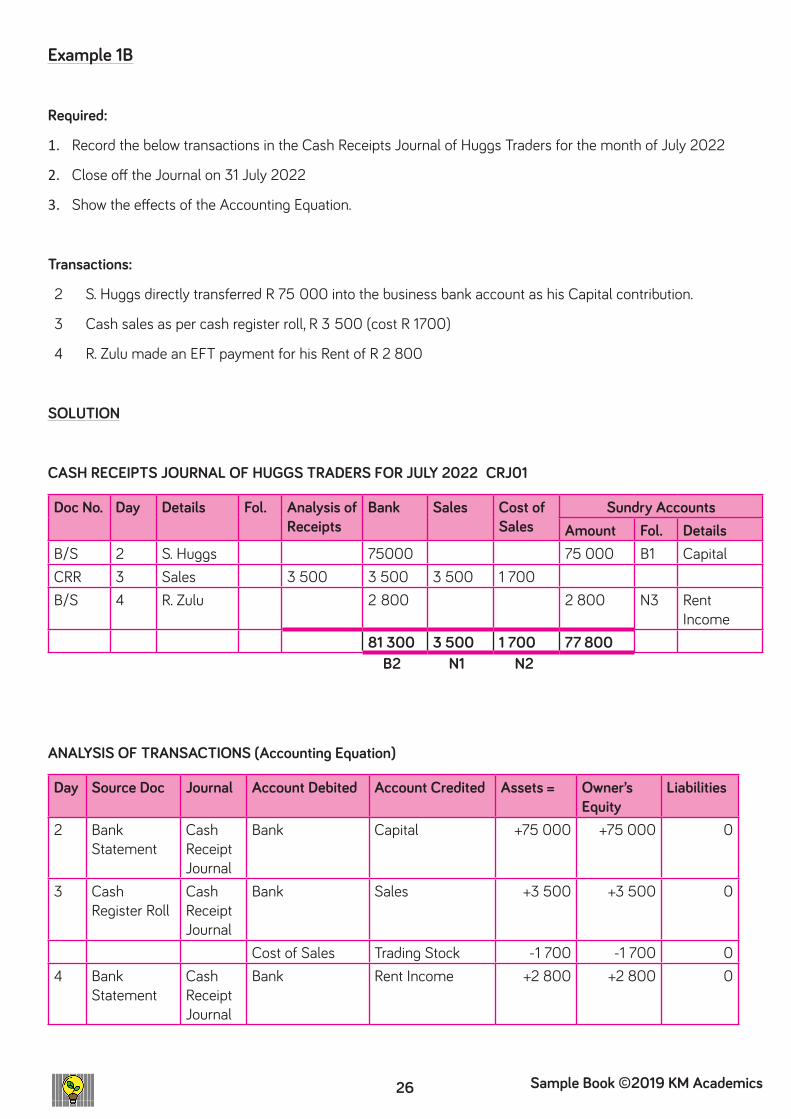

Example 1B

Required:

1. Record the below transactions in the Cash Receipts Journal of Huggs Traders for the month of July 2022

2. Close off the Journal on 31 July 2022

3. Show the effects of the Accounting Equation.

Transactions:

2 S. Huggs directly transferred R 75 000 into the business bank account as his Capital contribution.

3 Cash sales as per cash register roll, R 3 500 (cost R 1700)

4 R. Zulu made an EFT payment for his Rent of R 2 800

SOLUTION

CASH RECEIPTS JOURNAL OF HUGGS TRADERS FOR JULY 2022 CRJ01

Doc No. Day Details Fol. Analysis of Receipts

Bank Sales Cost of Sales

Sundry Accounts Amount Fol. Details

B/S 2 S. Huggs 75000 75 000 B1 CapitalCRR 3 Sales 3 500 3 500 3 500 1 700B/S 4 R. Zulu 2 800 2 800 N3 Rent

Income81 300 3 500 1 700 77 800

B2 N1 N2

ANALYSIS OF TRANSACTIONS (Accounting Equation)

Day Source Doc Journal Account Debited Account Credited Assets = Owner’s Equity

Liabilities

2 Bank Statement

Cash Receipt Journal

Bank Capital +75 000 +75 000 0

3 Cash Register Roll

Cash Receipt Journal

Bank Sales +3 500 +3 500 0

Cost of Sales Trading Stock -1 700 -1 700 04 Bank

StatementCash Receipt Journal

Bank Rent Income +2 800 +2 800 0

27Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

Activity 1.6 Date:_________________________

Required:

1. Record the below transactions in the Cash Receipts Journal of KM Academics for the month of August 2022

2. Close off the Journal on 31 August 2022

3. Show the effects of the Accounting Equation.

Transactions:

1 The owner, S. Mokoena deposited R 50 000 directly into the bank account of the business as his Capital contribution.

4 T. Tommy made an EFT payment for his Rent of R 3 500

10 Credit card sales of goods as per cash register roll, R 4 500 (cost R3 000)

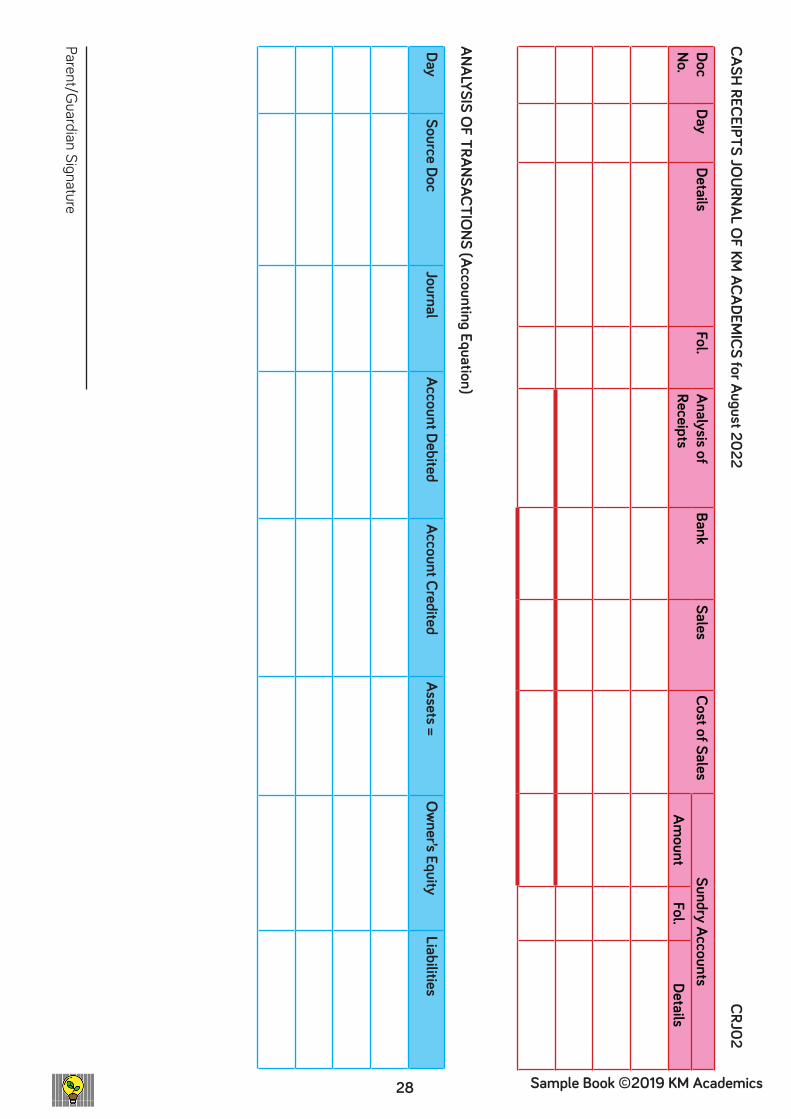

28 Sample Book ©2019 KM Academics

CASH RECEIPTS JOURNAL O

F KM ACADEM

ICS for August 2022

CRJ02

Doc No.

DayDetails

Fol.Analysis of Receipts

BankSales

Cost of SalesSundry Accounts

Amount

Fol.Details

ANALYSIS OF TRANSACTIO

NS (Accounting Equation)

DaySource Doc

JournalAccount Debited

Account CreditedAssets =

Owner’s Equity

Liabilities

Parent/Guardian Signature

29Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

Activity 1.7 Date____________________________Cash Receipts Journal

Piet started a business on 1 January 2022 trading as Inkosi stores. He appointed you to be the bookkeeper of his business.You are required to:• Record the following transactions of Inkosi stores in the Cash Receipts Journal for January 2022.• Make provision for the following columns: Analysis of Receipts, Bank, Sales, Cost of Sales, Debtors Control

and Sundry Accounts.• Close off Journal on 31 January 2022.• Show effect of the transactions on the Accounting Equation. Use the table providedNB: Goods are sold at cost plus 100%.

Transactions: January 20221. Owner directly deposited R40 000 into the business bank account as Capital contribution. Debit card Sales of merchandise as per Cash Register Tape, R 2 500.17. Zulu M transferred R800 into the business bank account for commission.25. Goods sold for cash, R2 000, as per cash register tape

30 Sample Book ©2019 KM Academics

Cash Receipts Journal of _______________________________________________ for _____________________________ CRJ 1DocNo.

DayDetails

FolAnalysis of Receipts

BankSales

Cost of Sales

Sundry AccountsAm

ountFol

Details

Accounting EquationSource docum

entG

eneral LedgerAccounting Equation

Account debitedAccount Credited

Assets=

Owner’s equity

+Liabilities

Parent/Guardian Signature

31Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

TERM 2

32 Sample Book ©2019 KM Academics

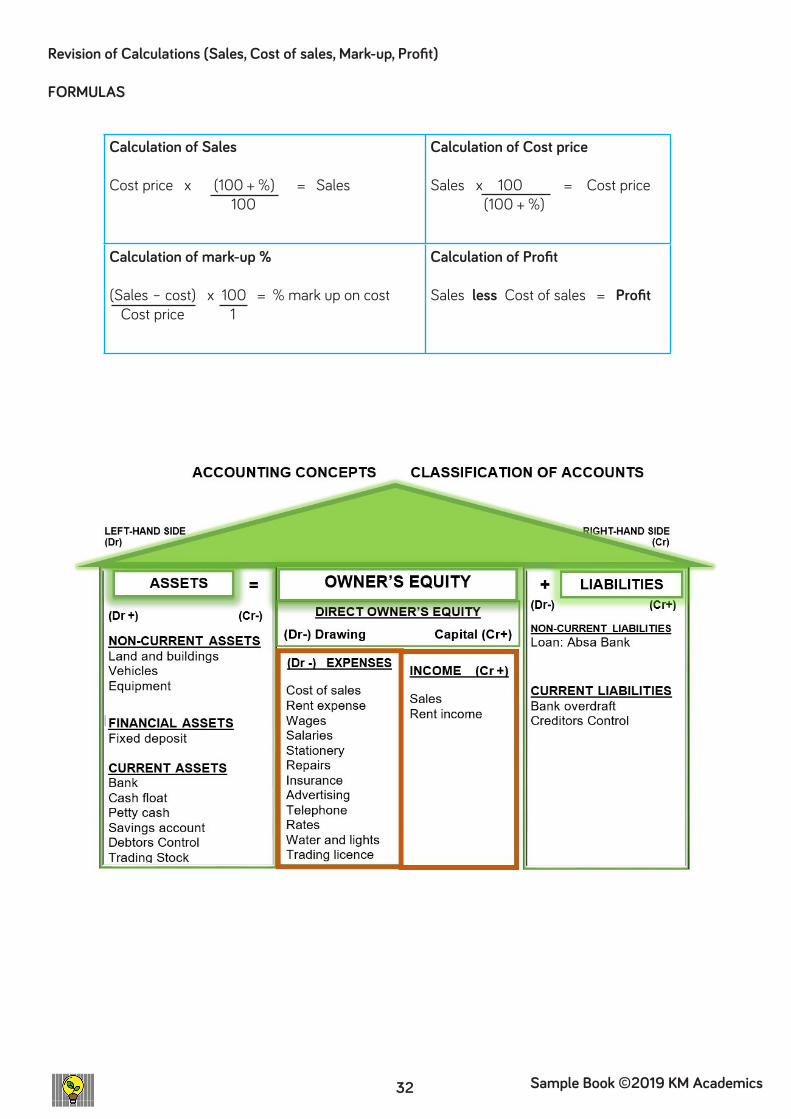

Calculation of Sales

Cost price x (100 + %) = Sales 100

Calculation of Cost price

Sales x 100 = Cost price (100 + %)

Calculation of mark-up %

(Sales – cost) x 100 = % mark up on cost Cost price 1

Calculation of Profit

Sales less Cost of sales = Profit

Revision of Calculations (Sales, Cost of sales, Mark-up, Profit)

FORMULAS

33Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

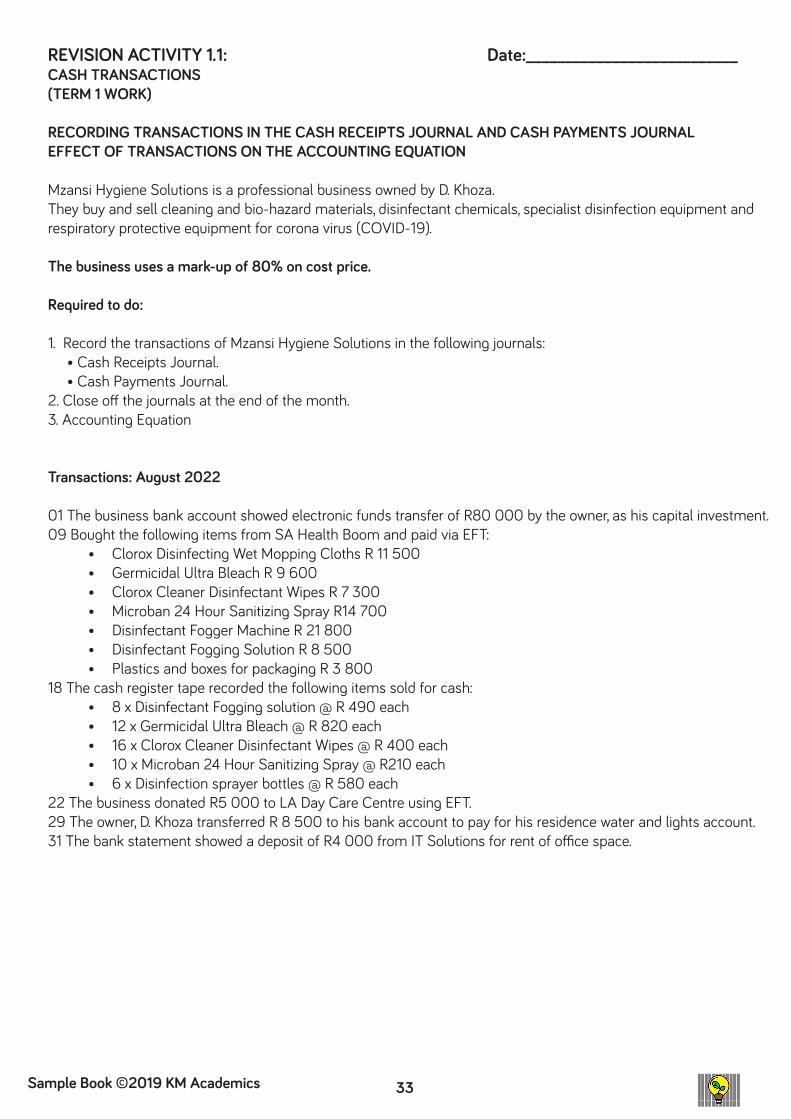

REVISION ACTIVITY 1.1: Date:___________________________CASH TRANSACTIONS (TERM 1 WORK)

RECORDING TRANSACTIONS IN THE CASH RECEIPTS JOURNAL AND CASH PAYMENTS JOURNALEFFECT OF TRANSACTIONS ON THE ACCOUNTING EQUATION

Mzansi Hygiene Solutions is a professional business owned by D. Khoza. They buy and sell cleaning and bio-hazard materials, disinfectant chemicals, specialist disinfection equipment and respiratory protective equipment for corona virus (COVID-19).

The business uses a mark-up of 80% on cost price.

Required to do:

1. Record the transactions of Mzansi Hygiene Solutions in the following journals: • Cash Receipts Journal. • Cash Payments Journal.2. Close off the journals at the end of the month.3. Accounting Equation

Transactions: August 2022

01 The business bank account showed electronic funds transfer of R80 000 by the owner, as his capital investment. 09 Bought the following items from SA Health Boom and paid via EFT:

• Clorox Disinfecting Wet Mopping Cloths R 11 500• Germicidal Ultra Bleach R 9 600 • Clorox Cleaner Disinfectant Wipes R 7 300 • Microban 24 Hour Sanitizing Spray R14 700• Disinfectant Fogger Machine R 21 800• Disinfectant Fogging Solution R 8 500• Plastics and boxes for packaging R 3 800

18 The cash register tape recorded the following items sold for cash: • 8 x Disinfectant Fogging solution @ R 490 each • 12 x Germicidal Ultra Bleach @ R 820 each • 16 x Clorox Cleaner Disinfectant Wipes @ R 400 each • 10 x Microban 24 Hour Sanitizing Spray @ R210 each • 6 x Disinfection sprayer bottles @ R 580 each

22 The business donated R5 000 to LA Day Care Centre using EFT.29 The owner, D. Khoza transferred R 8 500 to his bank account to pay for his residence water and lights account. 31 The bank statement showed a deposit of R4 000 from IT Solutions for rent of office space.

34 Sample Book ©2019 KM Academics

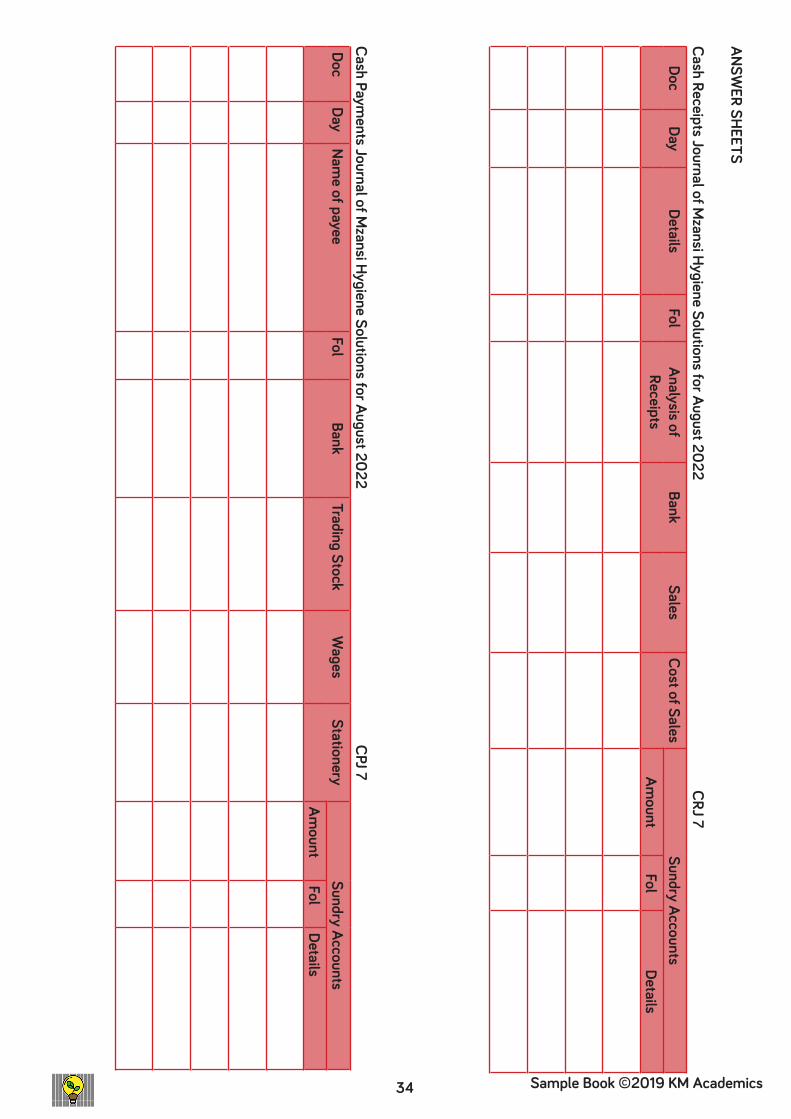

ANSWER SHEETS

Cash Receipts Journal of Mzansi Hygiene Solutions for August 2022 CRJ 7

DocDay

DetailsFol

Analysis of Receipts

BankSales

Cost of SalesSundry Accounts

Amount

FolDetails

Cash Payments Journal of M

zansi Hygiene Solutions for August 2022 CPJ 7Doc

DayNam

e of payeeFol

BankTrading Stock

Wages

StationerySundry Accounts

Amount

FolDetails

35Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

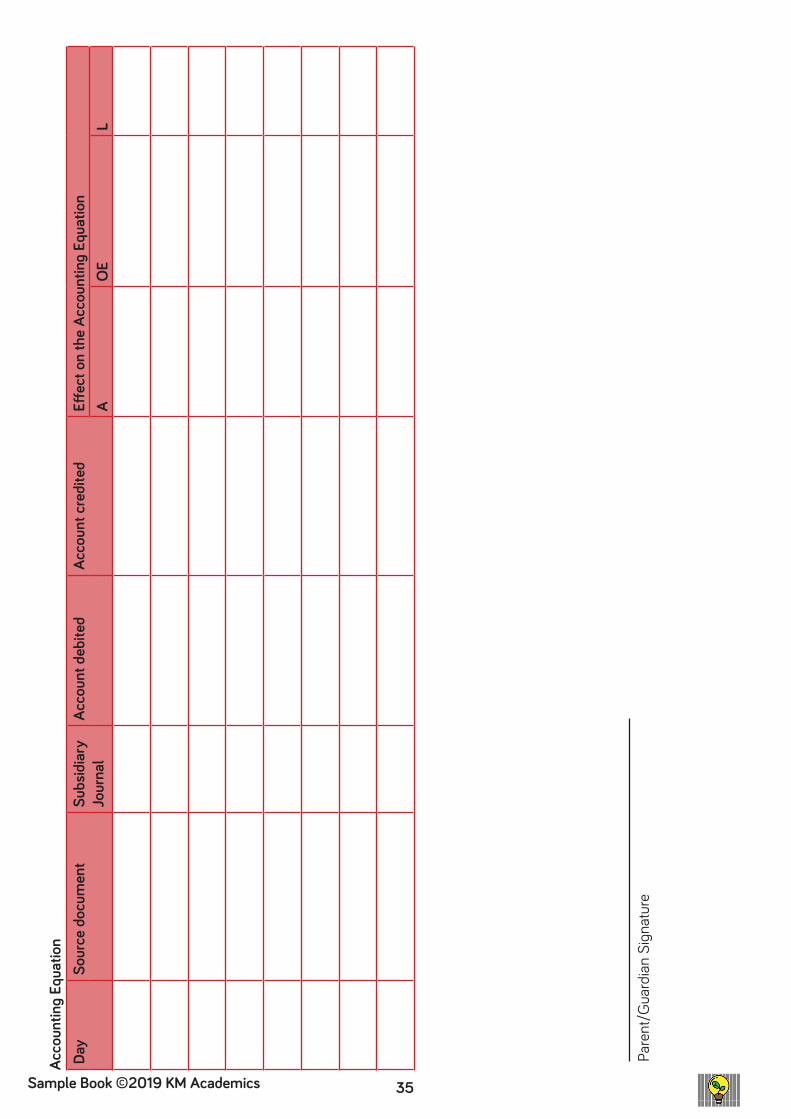

Acco

untin

g Eq

uatio

nDa

ySo

urce

doc

umen

tSu

bsid

iary

Jo

urna

lAc

coun

t deb

ited

Acco

unt c

redi

ted

Effec

t on

the

Acco

untin

g Eq

uatio

nA

OE

L

Pare

nt/G

uard

ian

Sign

atur

e

36 Sample Book ©2019 KM Academics

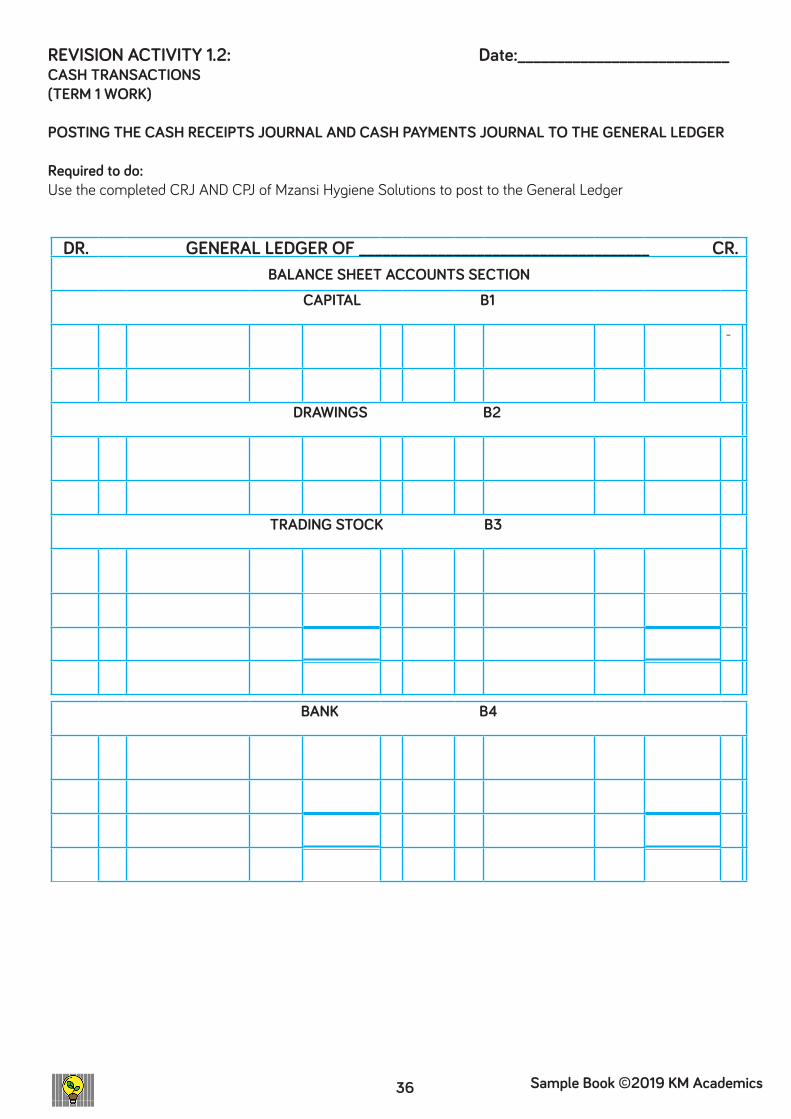

REVISION ACTIVITY 1.2: Date:___________________________CASH TRANSACTIONS (TERM 1 WORK)

POSTING THE CASH RECEIPTS JOURNAL AND CASH PAYMENTS JOURNAL TO THE GENERAL LEDGER

Required to do:Use the completed CRJ AND CPJ of Mzansi Hygiene Solutions to post to the General Ledger

DR. GENERAL LEDGER OF _____________________________________ CR.BALANCE SHEET ACCOUNTS SECTION

CAPITAL B1

-

DRAWINGS B2

TRADING STOCK B3

BANK B4

37Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

NOMINAL ACCOUNTS SECTION

SALES N1

COST OF SALES N2

RENT INCOME N3

DONATIONS EXPENSE N4

Parent/Guardian Signature

38 Sample Book ©2019 KM Academics

REVISION ACTIVITY 1.3: Date:___________________________CASH TRANSACTIONS (TERM 1 WORK)

PREPARING THE TRIAL BALANCE

Required to do:Use the completed General Ledger of Mzansi Hygiene Solutions to prepare the Trial Balance

TRIAL BALANCE OF __________________________________________________________DETAILS FOL DEBIT CREDITBALANCE SHEET ACCOUNTS SECTION

NOMINAL ACCOUNTS SECTION

Parent/Guardian Signature

39Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

CREDIT SALES (DEBTORS)

NEW TERMINOLOGY

• Credit: an arrangement made by a customer with the business to pay later for goods purchased.

• Creditworthy: when a person is able to pay the account, and can be trusted.

• Credit limit: maximum amount a customer can spend on account

• Credit agreement: legally binding contract between a customer and the business

• Credit score: is used by businesses to determine general credit risk, your payment history and ability to repay your debts on time.

• Debtor: a person who owes money to the business.

• Debtors’ journal: The journal where all transactions of sales on credit are recorded. (Third step in the Accounting Cycle)

• Debtors’ Control Account: is an account that simply tracks any amounts owed to the business. A summary of all Debtors’ balances.

• Invoice: A document issued to customers when goods are sold on credit. The business keeps the duplicate as a source document. National Credit Act: the law that regulates the granting of credit and protects both the customer and the business

The purpose of National Credit Act is:

• To educate consumers on the responsibilities of borrowing

• To ensure that money that is borrowed or lent out can be paid back.

• To protect consumers who are unfairly treated by businesses.

• To provide debt counseling processes to consumers who cannot find a solution to repay their debts.

Credit agreement specifies the following:• Credit limit – the maximum amount the debtor can owe on a specific date.

• Payments terms/Credit terms – how long can the debtor pay his/her account.

• Incentives or rewards – can give the debtor discount for early payment.

• Penalties – can charge the debtor interest for late payment.

40 Sample Book ©2019 KM Academics

Main objective of the National Credit Act:

• Aims at credit providers granting credit in a responsible way.

• Consumers not committing to more than what they can afford

• Educating consumers to make informed choices.

What does it mean to buy goods on credit?

Buying on credit means that a customer buys and receives goods now without making a payment immediately. Payment will be made at a later stage. This is also known as buying on account.

• Note that only people who are able to pay their accounts (creditworthy) are allowed to buy on credit. They will sign a credit agreement with terms of credit.

• All credit providers must comply with the (NCA) - National Credit Act

• When a business allows customers to buy on credit, customers are called Debtors.

• A debtor is a person who owes money to the business.

• A new account called Debtors Control, an Asset is created.

• Debtors Control is a summary of balances of all debtors in the business.

• The credit sales transaction is recorded in the Debtors Journal.

• The source document used to write up the Debtors Journal is the Duplicate Invoice. When the business sells goods on credit, the customer receives the original invoice and the business retains the Duplicate Invoice as the source document

41Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

Activity 2.1 Date:______________________ CREDIT SALES CONCEPTS

1. Explain the following concepts 1.1 Credit limit __________________________________________________________________________________________________

__________________________________________________________________________________________________

1.2 A debtor __________________________________________________________________________________________________

__________________________________________________________________________________________________1.3 National Credit Act (NCA) __________________________________________________________________________________________________

__________________________________________________________________________________________________1.4 Creditworthy __________________________________________________________________________________________________

__________________________________________________________________________________________________1.5 Credit agreement __________________________________________________________________________________________________

__________________________________________________________________________________________________

2. Answer the following questions: 2.1 Name and explain the first THREE STEPS in the accounting cycle of a credit sale transaction.

2.2 In which subsidiary journal is credit sales transaction recorded? ______________________________________

2.3 Which source document is issued by the business when goods are sold on credit? ________________________________________________________

2.4 What is the purpose of the National Credit Act? Mention THREE _______________________________________________________________________________________________

_______________________________________________________________________________________________

_______________________________________________________________________________________________

Name of Step Explanation

Step 1:

Step 2:

Step 3:

Parent/Guardian Signature

42 Sample Book ©2019 KM Academics

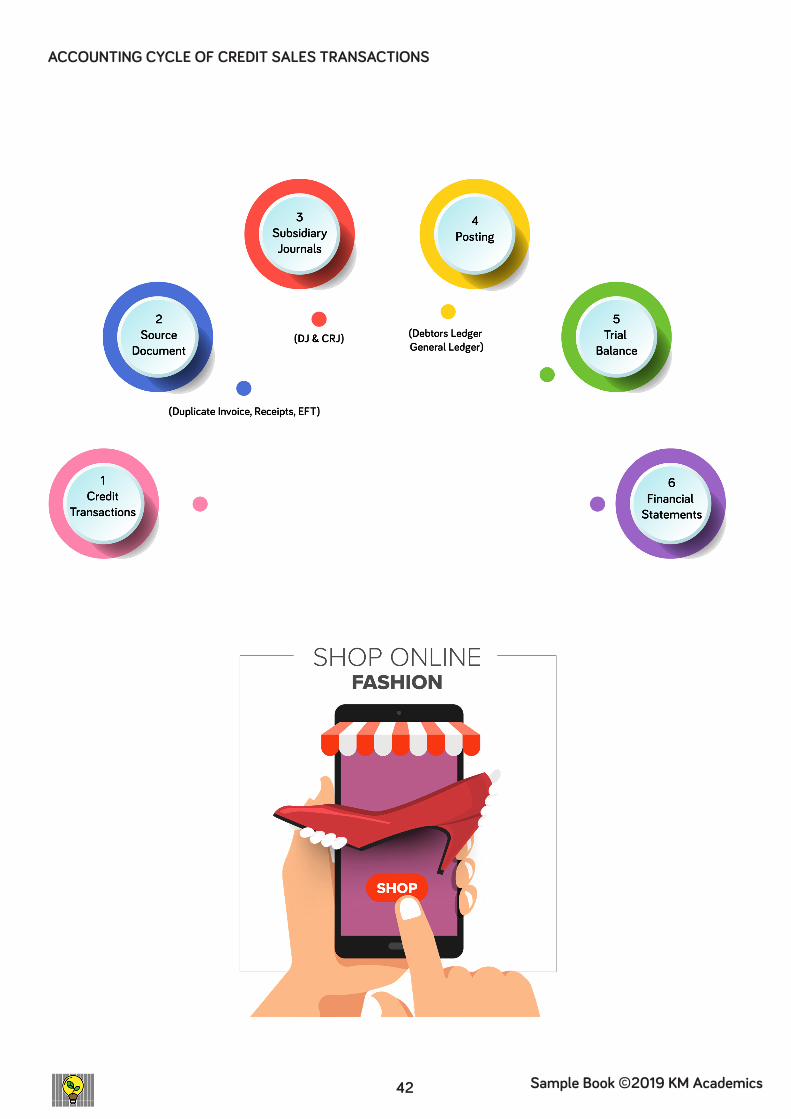

ACCOUNTING CYCLE OF CREDIT SALES TRANSACTIONS

43Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

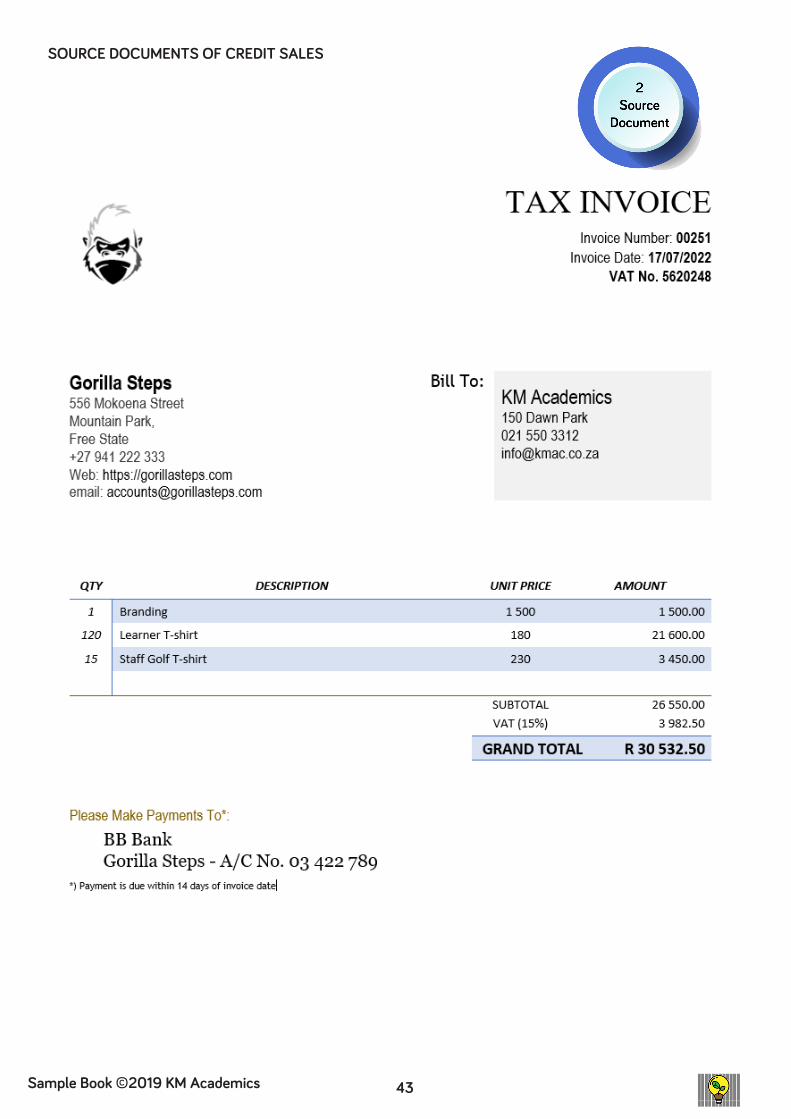

SOURCE DOCUMENTS OF CREDIT SALES

44 Sample Book ©2019 KM Academics

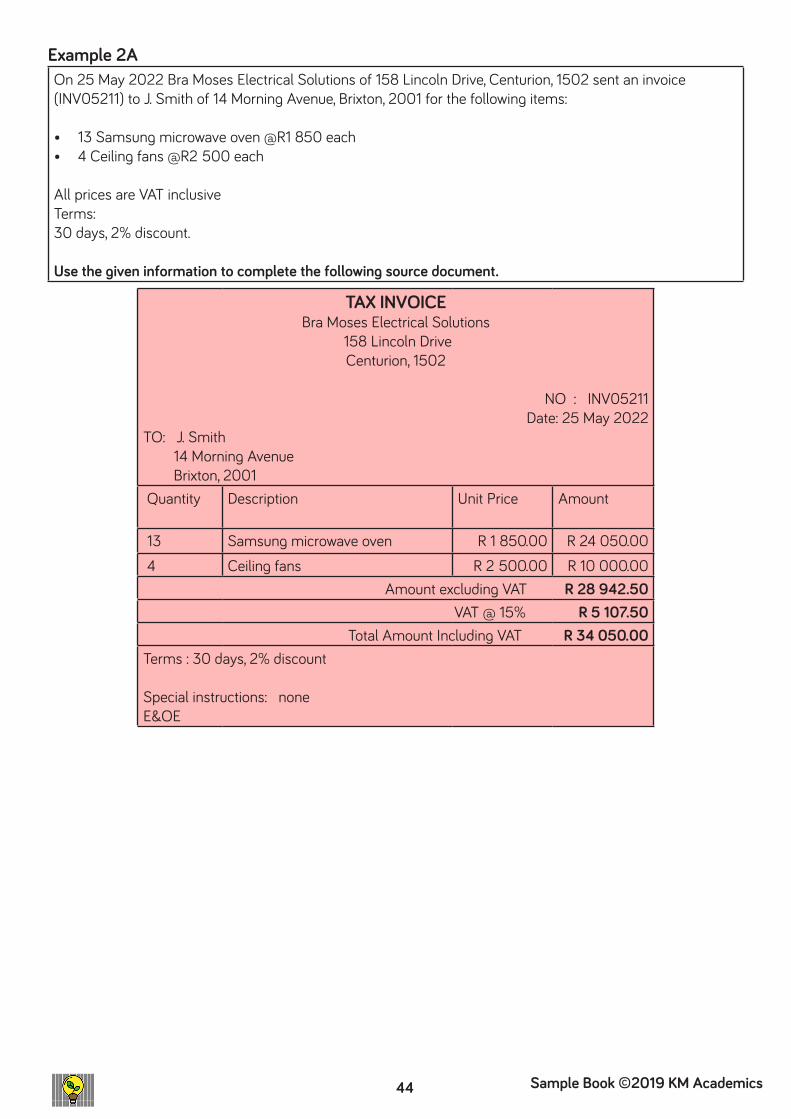

Example 2A On 25 May 2022 Bra Moses Electrical Solutions of 158 Lincoln Drive, Centurion, 1502 sent an invoice (INV05211) to J. Smith of 14 Morning Avenue, Brixton, 2001 for the following items:

• 13 Samsung microwave oven @R1 850 each• 4 Ceiling fans @R2 500 each

All prices are VAT inclusiveTerms:30 days, 2% discount.

Use the given information to complete the following source document.

TAX INVOICEBra Moses Electrical Solutions

158 Lincoln Drive Centurion, 1502

NO : INV05211Date: 25 May 2022

TO: J. Smith 14 Morning Avenue Brixton, 2001 Quantity Description Unit Price Amount

13 Samsung microwave oven R 1 850.00 R 24 050.00 4 Ceiling fans R 2 500.00 R 10 000.00

Amount excluding VAT R 28 942.50VAT @ 15% R 5 107.50

Total Amount Including VAT R 34 050.00 Terms : 30 days, 2% discount

Special instructions: none E&OE

45Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

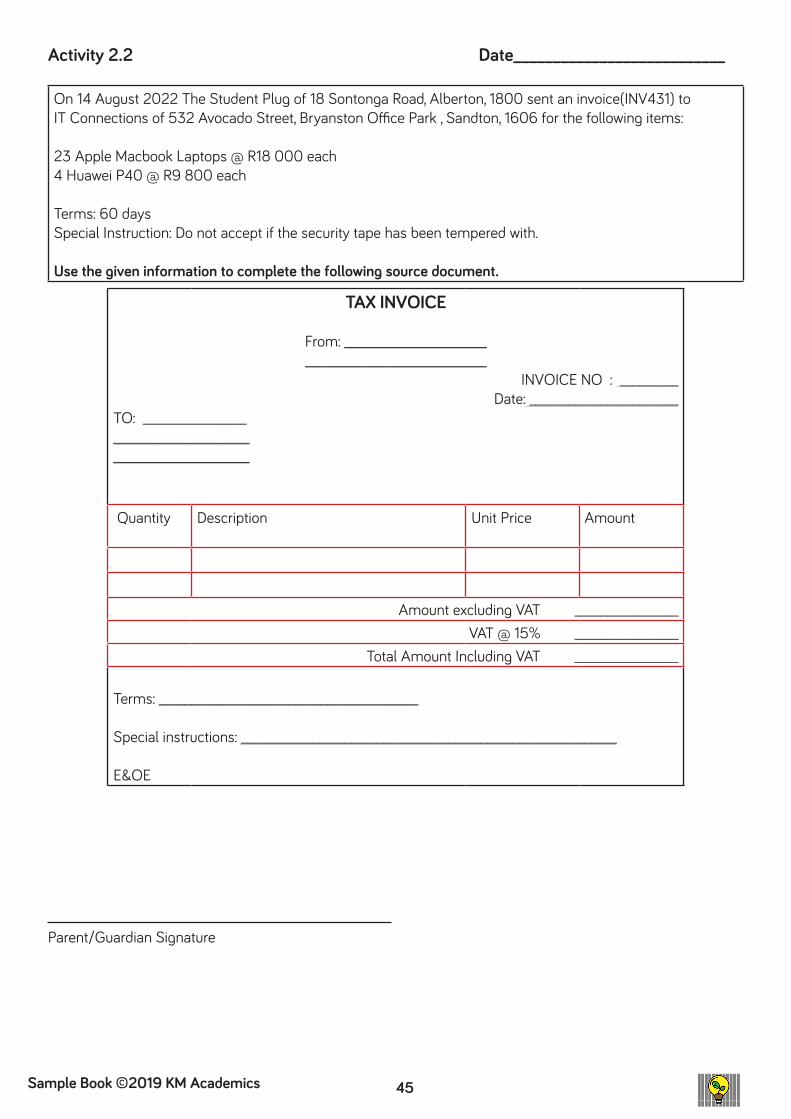

Activity 2.2 Date___________________________ On 14 August 2022 The Student Plug of 18 Sontonga Road, Alberton, 1800 sent an invoice(INV431) to IT Connections of 532 Avocado Street, Bryanston Office Park , Sandton, 1606 for the following items:

23 Apple Macbook Laptops @ R18 000 each4 Huawei P40 @ R9 800 each

Terms: 60 daysSpecial Instruction: Do not accept if the security tape has been tempered with.

Use the given information to complete the following source document.

TAX INVOICE

From: __________________________________________________

INVOICE NO : _________Date: _______________________

TO: __________________________________________________________

Quantity Description Unit Price Amount

Amount excluding VAT ________________VAT @ 15% ________________

Total Amount Including VAT ________________

Terms: ________________________________________

Special instructions: __________________________________________________________

E&OE

Parent/Guardian Signature

46 Sample Book ©2019 KM Academics

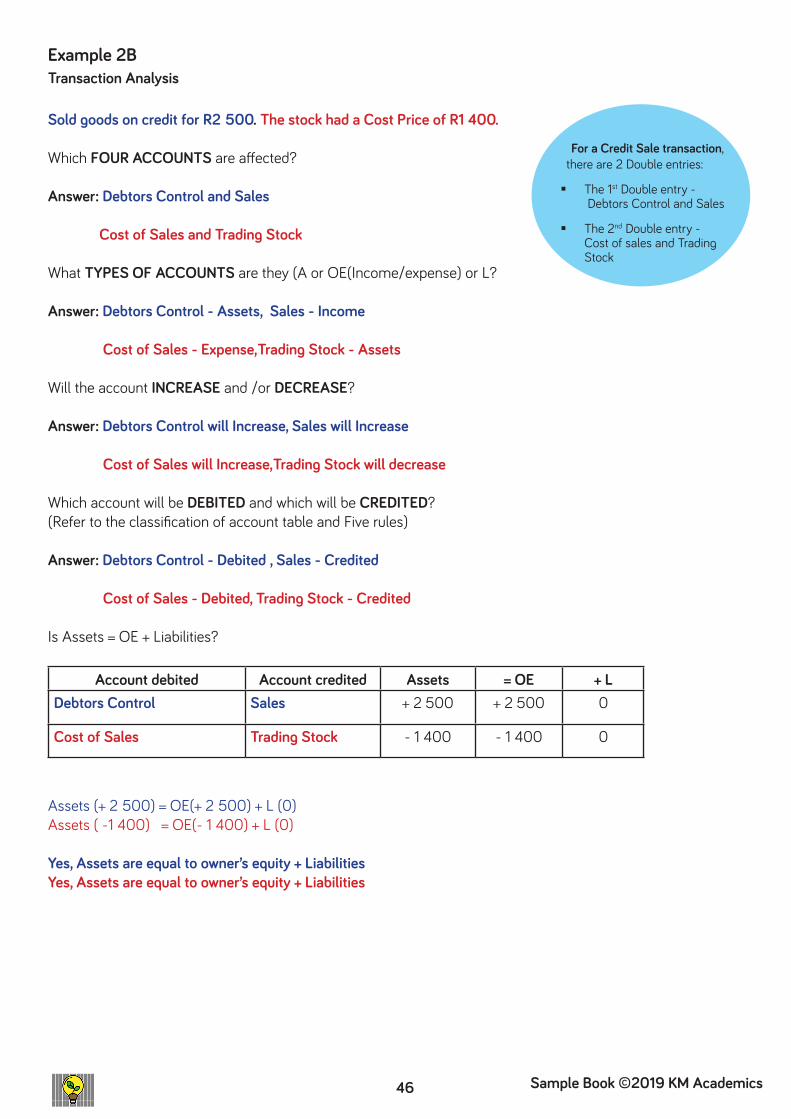

Example 2B Transaction Analysis Sold goods on credit for R2 500. The stock had a Cost Price of R1 400.

Which FOUR ACCOUNTS are affected?

Answer: Debtors Control and Sales

Cost of Sales and Trading Stock

What TYPES OF ACCOUNTS are they (A or OE(Income/expense) or L?

Answer: Debtors Control - Assets, Sales - Income

Cost of Sales - Expense,Trading Stock - Assets

Will the account INCREASE and /or DECREASE?

Answer: Debtors Control will Increase, Sales will Increase

Cost of Sales will Increase,Trading Stock will decrease

Which account will be DEBITED and which will be CREDITED? (Refer to the classification of account table and Five rules)

Answer: Debtors Control - Debited , Sales - Credited

Cost of Sales - Debited, Trading Stock - Credited

Is Assets = OE + Liabilities?

Account debited Account credited Assets = OE + LDebtors Control Sales + 2 500 + 2 500 0

Cost of Sales Trading Stock - 1 400 - 1 400 0

Assets (+ 2 500) = OE(+ 2 500) + L (0)Assets ( -1 400) = OE(- 1 400) + L (0)

Yes, Assets are equal to owner’s equity + LiabilitiesYes, Assets are equal to owner’s equity + Liabilities

For a Credit Sale transaction, there are 2 Double entries:

The 1st Double entry - Debtors Control and Sales

The 2nd Double entry - Cost of sales and Trading Stock

47Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

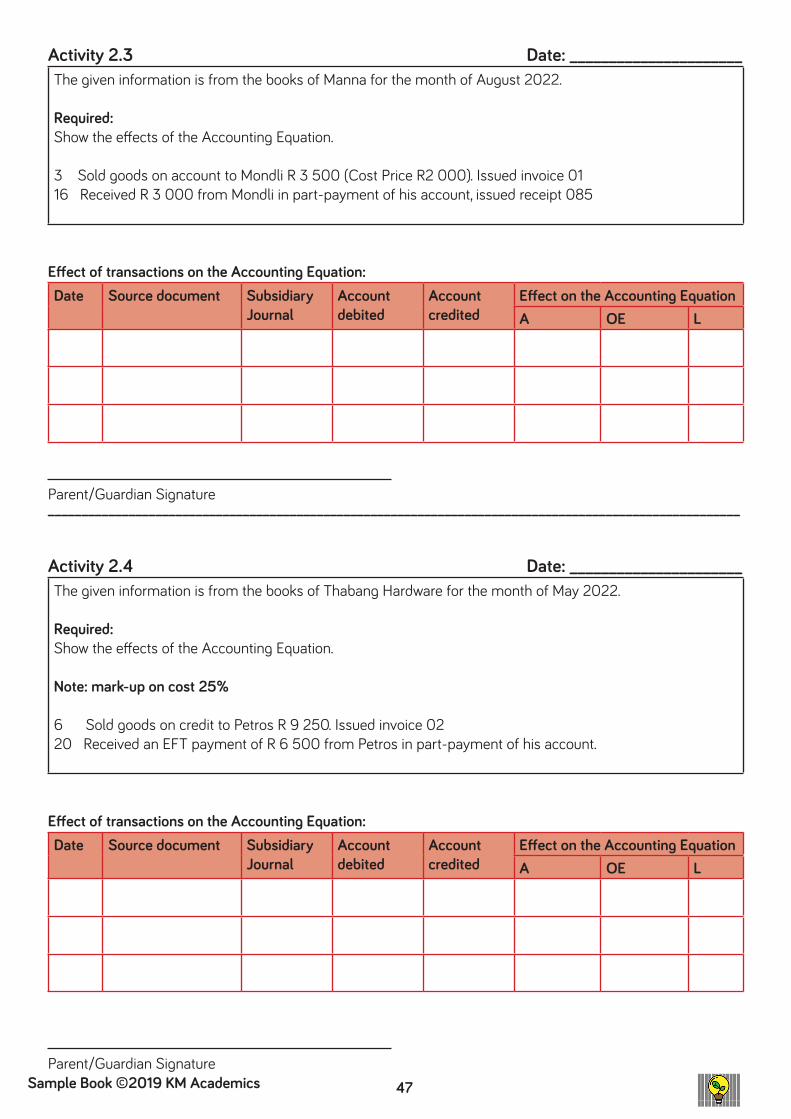

Activity 2.3 Date: ______________________The given information is from the books of Manna for the month of August 2022.

Required:Show the effects of the Accounting Equation.

3 Sold goods on account to Mondli R 3 500 (Cost Price R2 000). Issued invoice 0116 Received R 3 000 from Mondli in part-payment of his account, issued receipt 085

Effect of transactions on the Accounting Equation:Date Source document Subsidiary

JournalAccount debited

Account credited

Effect on the Accounting EquationA OE L

_______________________________________________________________________________________________________

Activity 2.4 Date: ______________________The given information is from the books of Thabang Hardware for the month of May 2022.

Required:Show the effects of the Accounting Equation.

Note: mark-up on cost 25%

6 Sold goods on credit to Petros R 9 250. Issued invoice 0220 Received an EFT payment of R 6 500 from Petros in part-payment of his account.

Effect of transactions on the Accounting Equation:Date Source document Subsidiary

JournalAccount debited

Account credited

Effect on the Accounting EquationA OE L

Parent/Guardian Signature

Parent/Guardian Signature

48 Sample Book ©2019 KM Academics

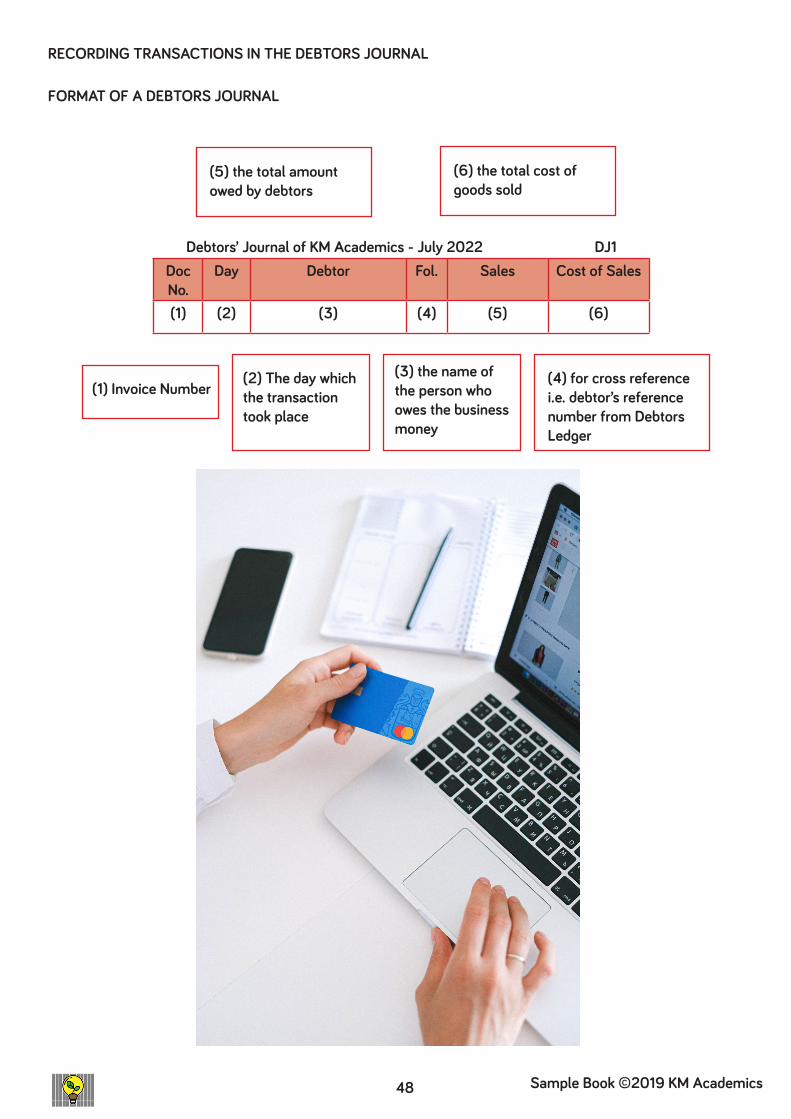

RECORDING TRANSACTIONS IN THE DEBTORS JOURNAL

FORMAT OF A DEBTORS JOURNAL

Debtors’ Journal of KM Academics - July 2022 DJ1Doc No.

Day Debtor Fol. Sales Cost of Sales

(1) (2) (3) (4) (5) (6)

(1) Invoice Number(2) The day which the transaction took place

(3) the name of the person who owes the business money

(4) for cross reference i.e. debtor’s reference number from Debtors Ledger

(5) the total amount owed by debtors

(6) the total cost of goods sold

49Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

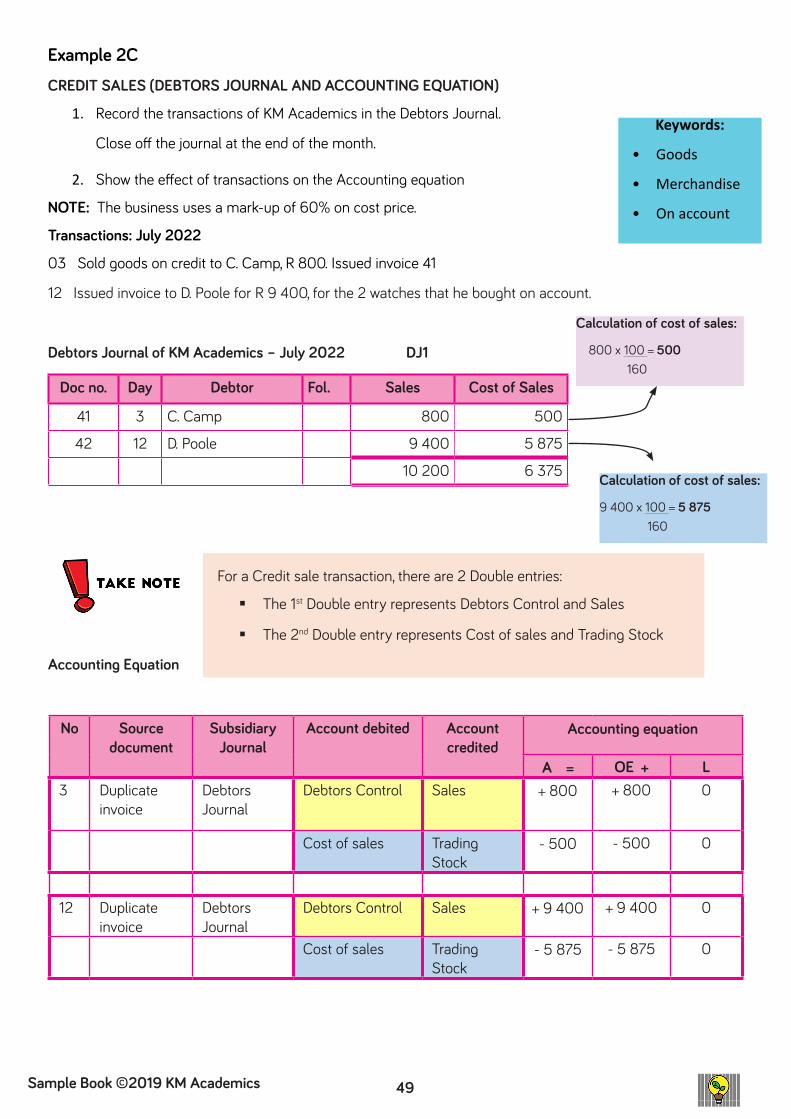

Example 2C CREDIT SALES (DEBTORS JOURNAL AND ACCOUNTING EQUATION)

1. Record the transactions of KM Academics in the Debtors Journal.

Close off the journal at the end of the month.

2. Show the effect of transactions on the Accounting equation

NOTE: The business uses a mark-up of 60% on cost price.

Transactions: July 2022

03 Sold goods on credit to C. Camp, R 800. Issued invoice 41

12 Issued invoice to D. Poole for R 9 400, for the 2 watches that he bought on account.

Debtors Journal of KM Academics – July 2022 DJ1

Doc no. Day Debtor Fol. Sales Cost of Sales

41 3 C. Camp 800 500

42 12 D. Poole 9 400 5 875

10 200 6 375

For a Credit sale transaction, there are 2 Double entries:

The 1st Double entry represents Debtors Control and Sales

The 2nd Double entry represents Cost of sales and Trading Stock Accounting Equation

No Source document

Subsidiary Journal

Account debited Account credited

Accounting equation

A = OE + L3 Duplicate

invoiceDebtors Journal

Debtors Control Sales + 800 + 800 0

Cost of sales Trading Stock

- 500 - 500 0

12 Duplicate invoice

Debtors Journal

Debtors Control Sales + 9 400 + 9 400 0

Cost of sales Trading Stock

- 5 875 - 5 875 0

Keywords:

• Goods

• Merchandise

• On account

Calculation of cost of sales:

9 400 x 100 = 5 875 160

Calculation of cost of sales:

800 x 100 = 500 160

50 Sample Book ©2019 KM Academics

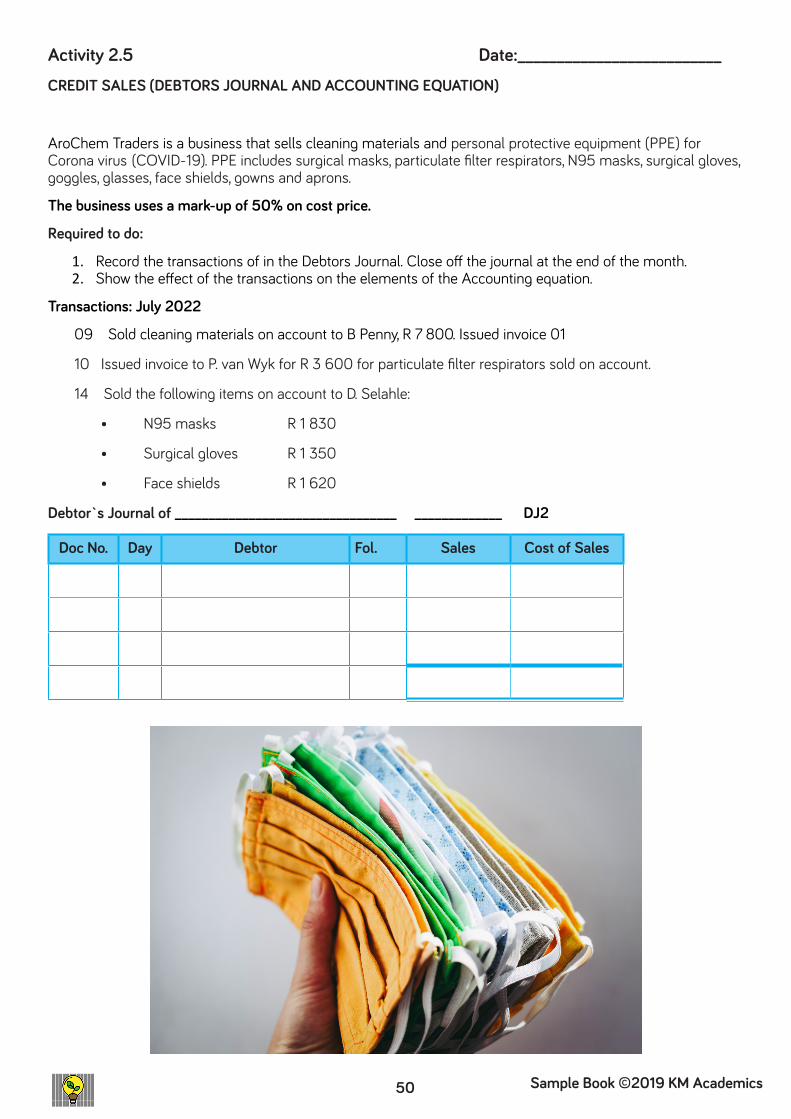

Activity 2.5 Date:__________________________CREDIT SALES (DEBTORS JOURNAL AND ACCOUNTING EQUATION)

AroChem Traders is a business that sells cleaning materials and personal protective equipment (PPE) for Corona virus (COVID-19). PPE includes surgical masks, particulate filter respirators, N95 masks, surgical gloves, goggles, glasses, face shields, gowns and aprons.

The business uses a mark-up of 50% on cost price.

Required to do:

1. Record the transactions of in the Debtors Journal. Close off the journal at the end of the month.2. Show the effect of the transactions on the elements of the Accounting equation.

Transactions: July 2022

09 Sold cleaning materials on account to B Penny, R 7 800. Issued invoice 01

10 Issued invoice to P. van Wyk for R 3 600 for particulate filter respirators sold on account.

14 Sold the following items on account to D. Selahle:

• N95 masks R 1 830

• Surgical gloves R 1 350

• Face shields R 1 620

Debtor`s Journal of _________________________________ _____________ DJ2

Doc No. Day Debtor Fol. Sales Cost of Sales

51Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

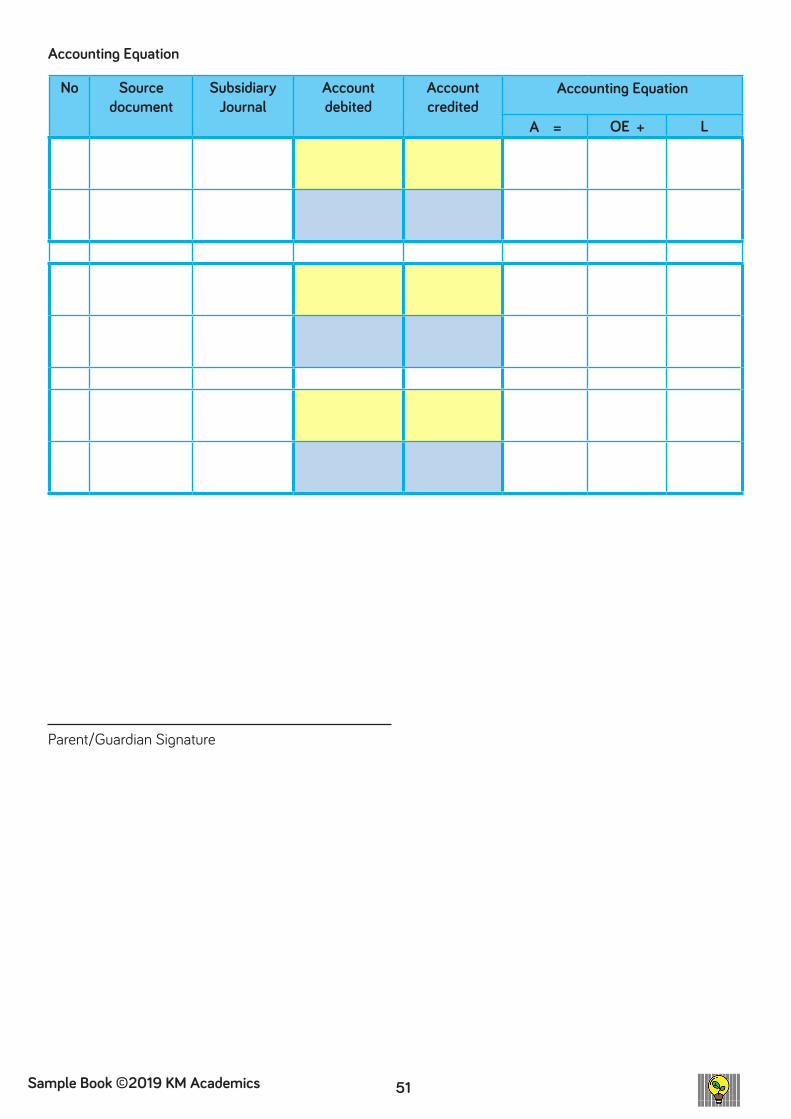

Accounting Equation

No Source document

Subsidiary Journal

Account debited

Account credited

Accounting Equation

A = OE + L

Parent/Guardian Signature

52 Sample Book ©2019 KM Academics

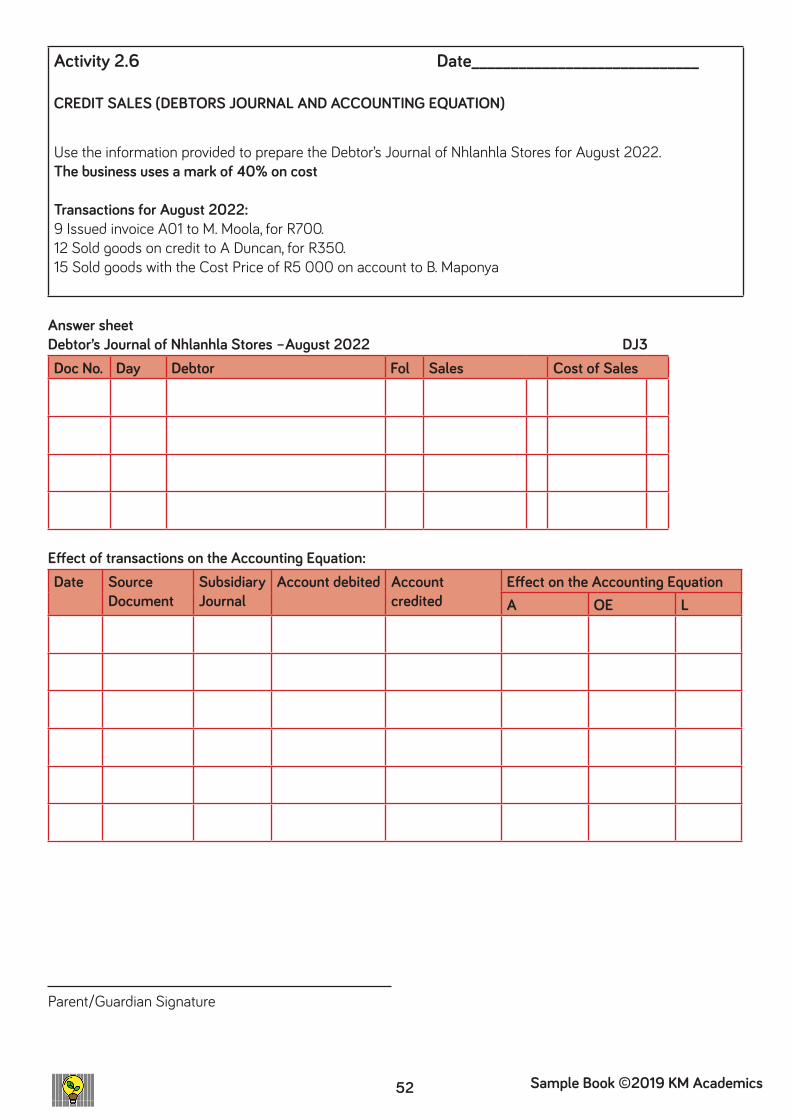

Activity 2.6 Date_____________________________

CREDIT SALES (DEBTORS JOURNAL AND ACCOUNTING EQUATION)

Use the information provided to prepare the Debtor’s Journal of Nhlanhla Stores for August 2022.The business uses a mark of 40% on cost

Transactions for August 2022:9 Issued invoice A01 to M. Moola, for R700. 12 Sold goods on credit to A Duncan, for R350. 15 Sold goods with the Cost Price of R5 000 on account to B. Maponya

Answer sheetDebtor’s Journal of Nhlanhla Stores –August 2022 DJ3Doc No. Day Debtor Fol Sales Cost of Sales

Effect of transactions on the Accounting Equation:Date Source

DocumentSubsidiary Journal

Account debited Account credited

Effect on the Accounting EquationA OE L

Parent/Guardian Signature

53Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

TERM 3

54 Sample Book ©2019 KM Academics

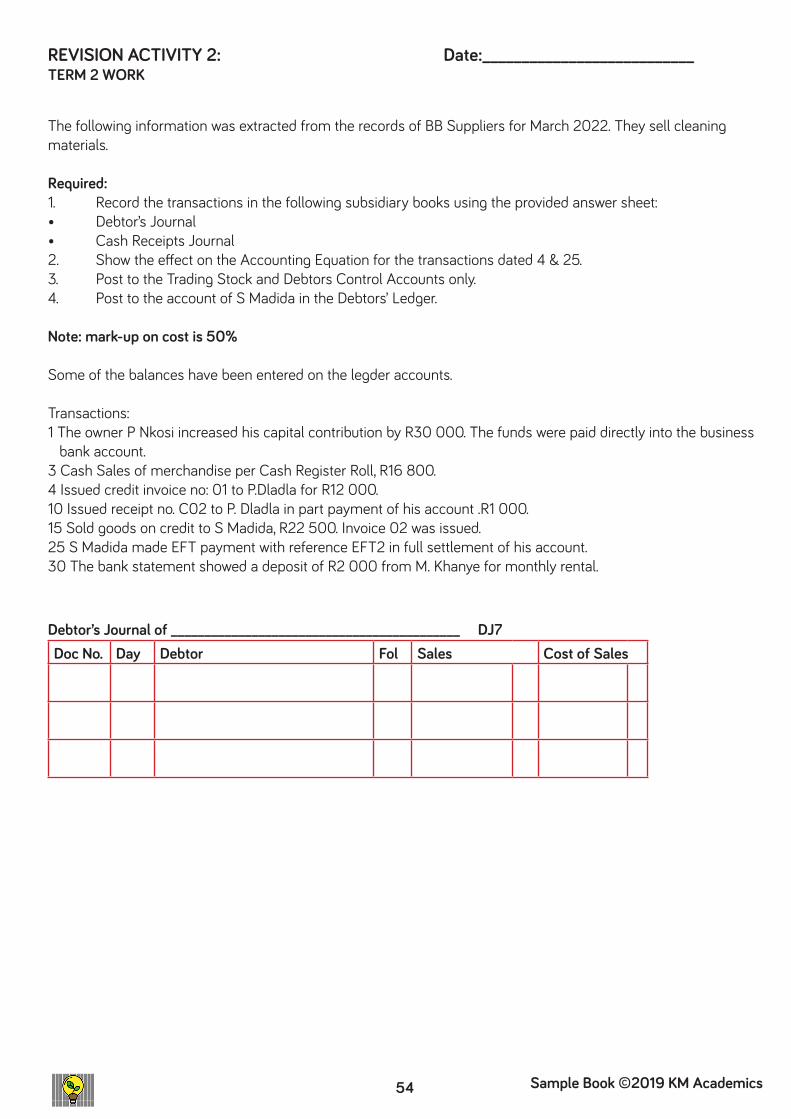

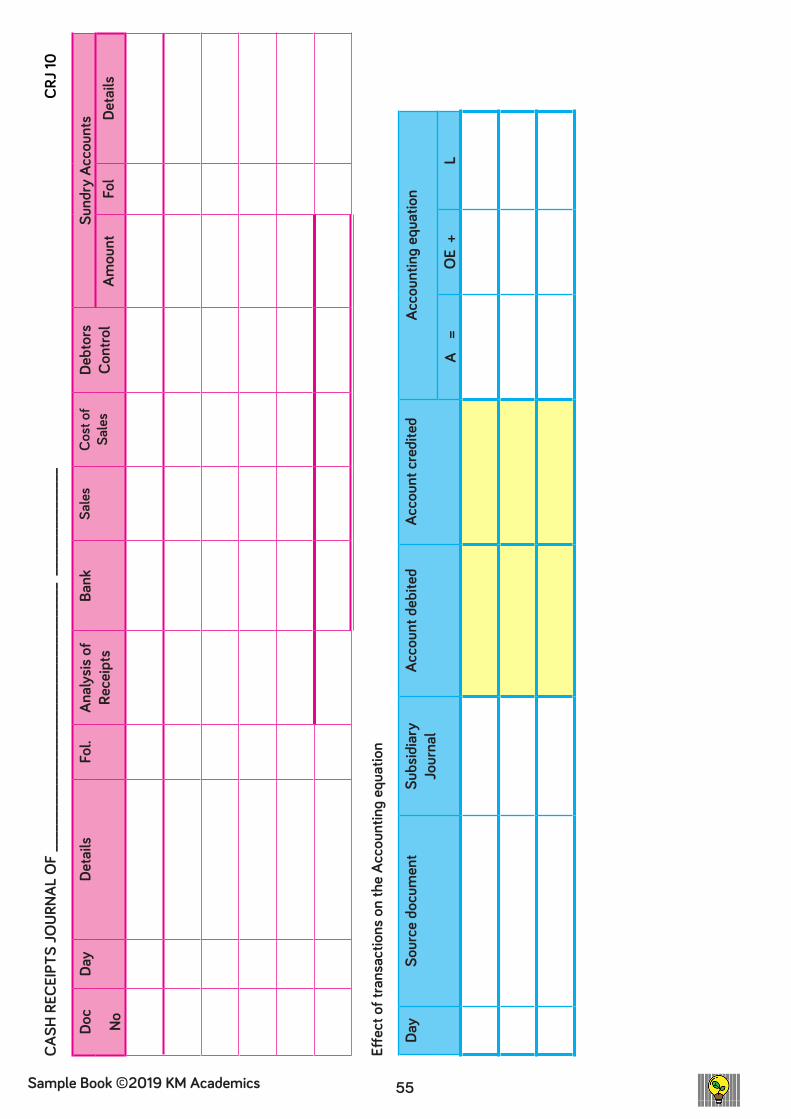

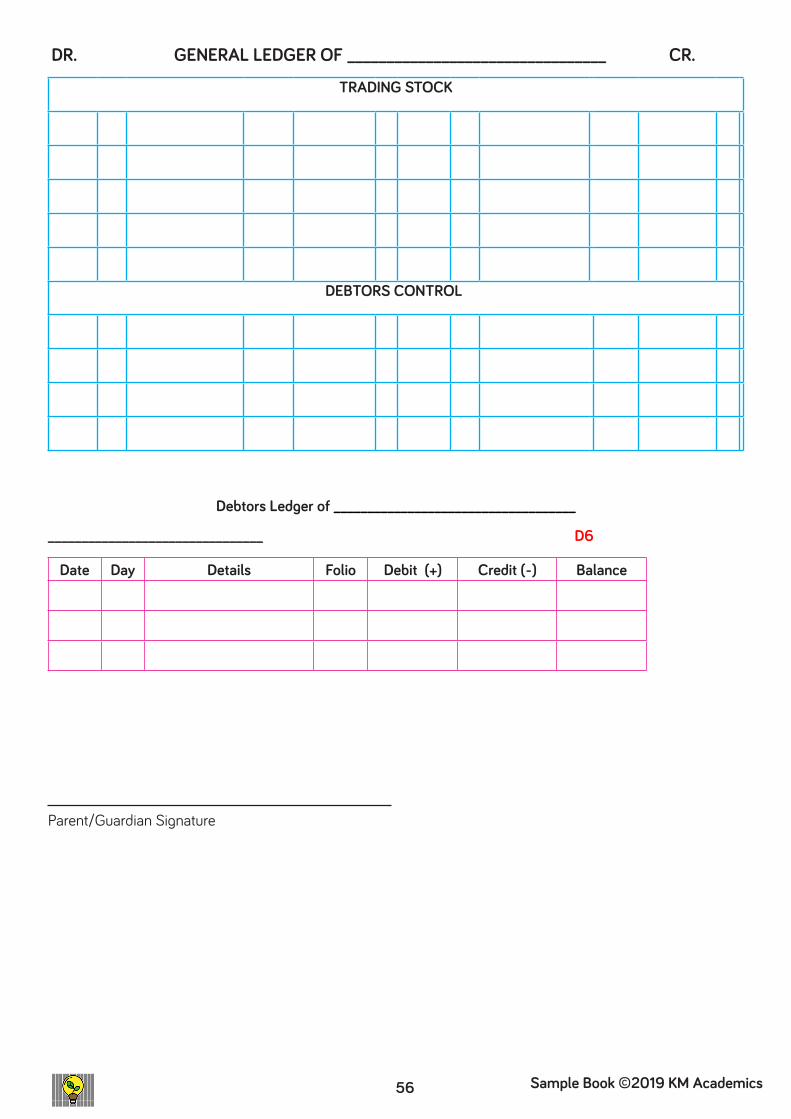

The following information was extracted from the records of BB Suppliers for March 2022. They sell cleaning materials.

Required:1. Record the transactions in the following subsidiary books using the provided answer sheet:• Debtor’s Journal• Cash Receipts Journal2. Show the effect on the Accounting Equation for the transactions dated 4 & 25.3. Post to the Trading Stock and Debtors Control Accounts only.4. Post to the account of S Madida in the Debtors’ Ledger.

Note: mark-up on cost is 50%

Some of the balances have been entered on the legder accounts.

Transactions:1 The owner P Nkosi increased his capital contribution by R30 000. The funds were paid directly into the business bank account.3 Cash Sales of merchandise per Cash Register Roll, R16 800. 4 Issued credit invoice no: 01 to P.Dladla for R12 000.10 Issued receipt no. C02 to P. Dladla in part payment of his account .R1 000.15 Sold goods on credit to S Madida, R22 500. Invoice 02 was issued.25 S Madida made EFT payment with reference EFT2 in full settlement of his account.30 The bank statement showed a deposit of R2 000 from M. Khanye for monthly rental.

REVISION ACTIVITY 2: Date:___________________________TERM 2 WORK

Debtor’s Journal of ___________________________________________ DJ7Doc No. Day Debtor Fol Sales Cost of Sales

55Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

CASH

REC

EIPT

S JO

URNA

L O

F __

____

____

____

____

____

____

____

____

____

__ _

____

____

____

___

CR

J 10

Doc

No

Day

Deta

ilsFo

l.An

alys

is of

Re

ceip

tsBa

nkSa

les

Cost

of

Sale

sDe

btor

s Co

ntro

lSu

ndry

Acc

ount

sAm

ount

Fol

Deta

ils

Effec

t of t

rans

actio

ns o

n th

e Ac

coun

ting

equa

tion

Day

Sour

ce d

ocum

ent

Subs

idia

ry

Jour

nal

Acco

unt d

ebite

dAc

coun

t cre

dite

dAc

coun

ting

equa

tion

A

=O

E +

L

56 Sample Book ©2019 KM Academics

DR. GENERAL LEDGER OF _________________________________ CR.

TRADING STOCK

DEBTORS CONTROL

Debtors Ledger of ____________________________________

________________________________ D6

Date Day Details Folio Debit (+) Credit (-) Balance

Parent/Guardian Signature

57Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

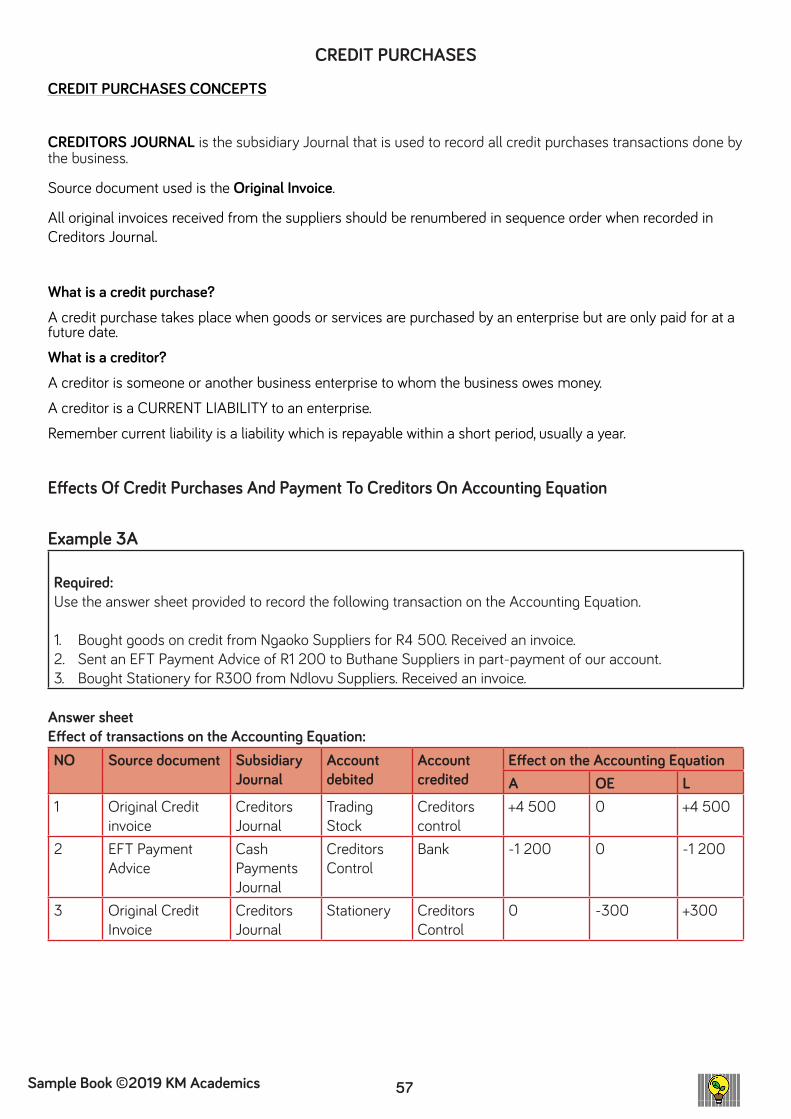

Example 3A

Required:Use the answer sheet provided to record the following transaction on the Accounting Equation.

1. Bought goods on credit from Ngaoko Suppliers for R4 500. Received an invoice.2. Sent an EFT Payment Advice of R1 200 to Buthane Suppliers in part-payment of our account.3. Bought Stationery for R300 from Ndlovu Suppliers. Received an invoice.

Answer sheetEffect of transactions on the Accounting Equation:NO Source document Subsidiary

JournalAccount debited

Account credited

Effect on the Accounting EquationA OE L

1 Original Credit invoice

Creditors Journal

Trading Stock

Creditors control

+4 500 0 +4 500

2 EFT Payment Advice

Cash Payments Journal

Creditors Control

Bank -1 200 0 -1 200

3 Original Credit Invoice

Creditors Journal

Stationery Creditors Control

0 -300 +300

Effects Of Credit Purchases And Payment To Creditors On Accounting Equation

CREDIT PURCHASES

CREDIT PURCHASES CONCEPTS

CREDITORS JOURNAL is the subsidiary Journal that is used to record all credit purchases transactions done by the business.

Source document used is the Original Invoice.

All original invoices received from the suppliers should be renumbered in sequence order when recorded in Creditors Journal.

What is a credit purchase? A credit purchase takes place when goods or services are purchased by an enterprise but are only paid for at a future date.

What is a creditor? A creditor is someone or another business enterprise to whom the business owes money.

A creditor is a CURRENT LIABILITY to an enterprise.

Remember current liability is a liability which is repayable within a short period, usually a year.

58 Sample Book ©2019 KM Academics

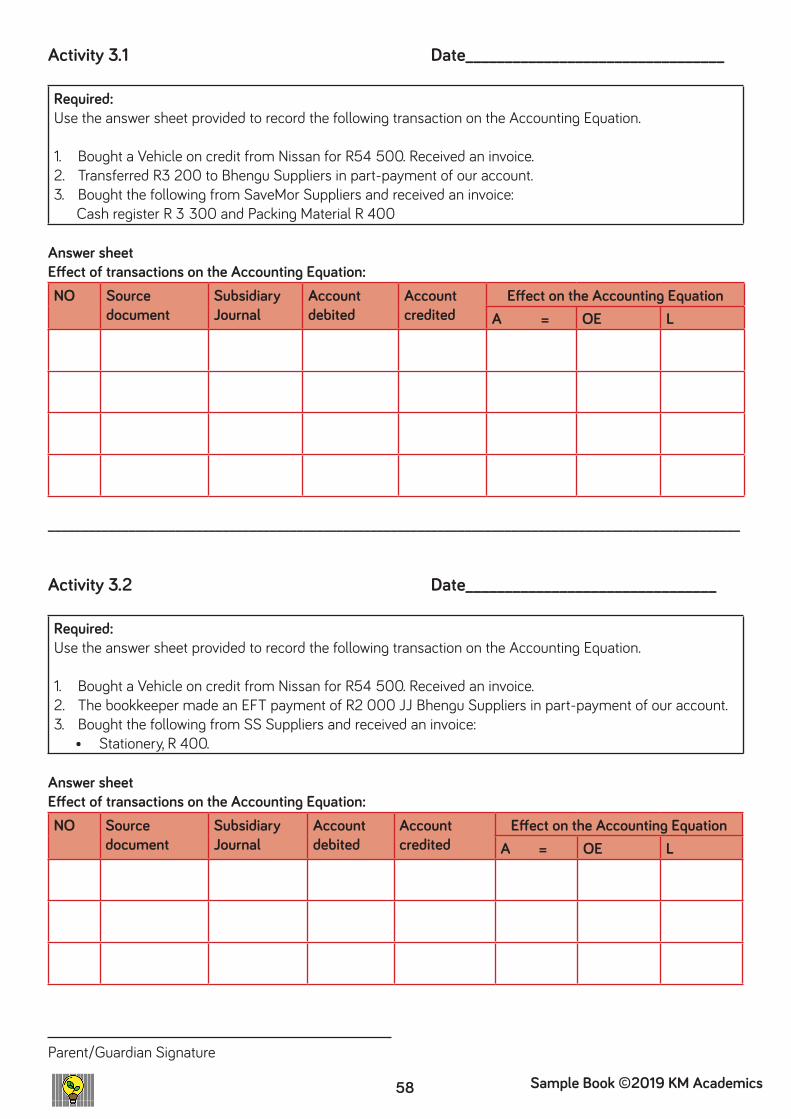

Activity 3.1 Date_________________________________

Required:Use the answer sheet provided to record the following transaction on the Accounting Equation.

1. Bought a Vehicle on credit from Nissan for R54 500. Received an invoice.2. Transferred R3 200 to Bhengu Suppliers in part-payment of our account.3. Bought the following from SaveMor Suppliers and received an invoice: Cash register R 3 300 and Packing Material R 400

Answer sheetEffect of transactions on the Accounting Equation:NO Source

documentSubsidiary Journal

Account debited

Account credited

Effect on the Accounting EquationA = OE L

_______________________________________________________________________________________________________

Activity 3.2 Date________________________________

Required:Use the answer sheet provided to record the following transaction on the Accounting Equation.

1. Bought a Vehicle on credit from Nissan for R54 500. Received an invoice.2. The bookkeeper made an EFT payment of R2 000 JJ Bhengu Suppliers in part-payment of our account.3. Bought the following from SS Suppliers and received an invoice:

• Stationery, R 400.

Answer sheetEffect of transactions on the Accounting Equation:NO Source

documentSubsidiary Journal

Account debited

Account credited

Effect on the Accounting EquationA = OE L

Parent/Guardian Signature

59Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

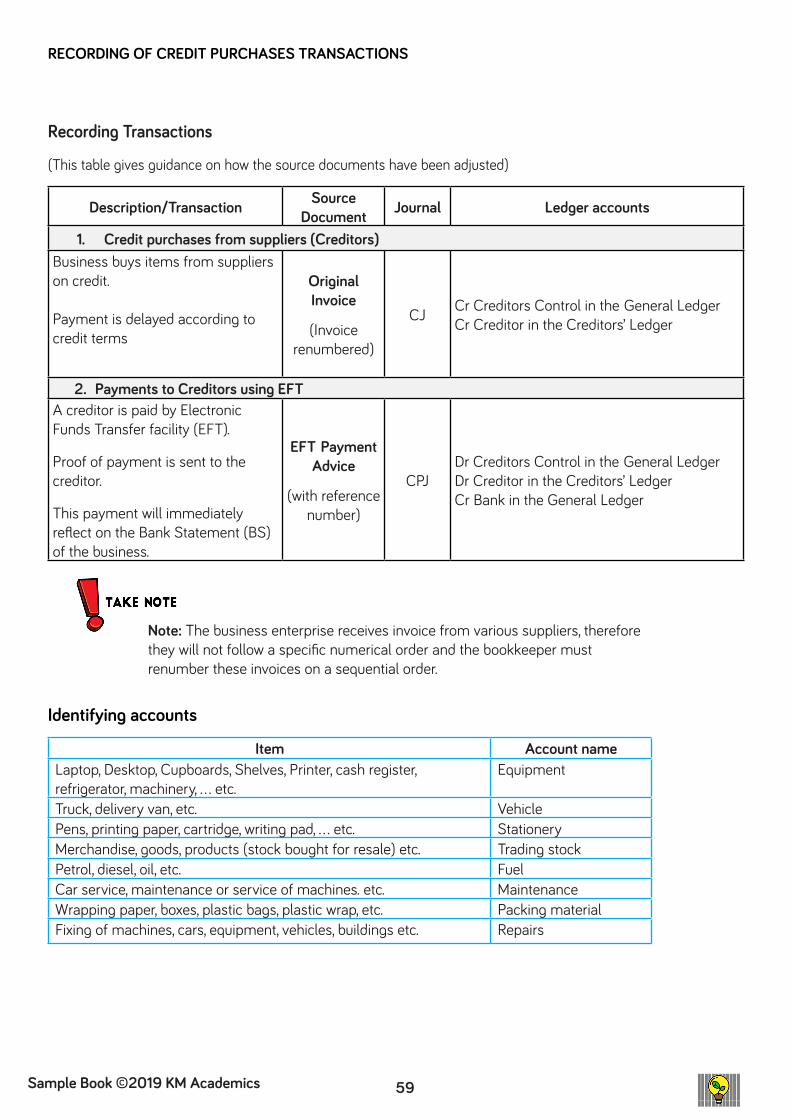

Recording Transactions

(This table gives guidance on how the source documents have been adjusted)

Description/Transaction Source Document Journal Ledger accounts

1. Credit purchases from suppliers (Creditors)Business buys items from suppliers on credit.

Payment is delayed according to credit terms

Original Invoice

(Invoice renumbered)

CJ Cr Creditors Control in the General LedgerCr Creditor in the Creditors’ Ledger

2. Payments to Creditors using EFTA creditor is paid by Electronic Funds Transfer facility (EFT).

Proof of payment is sent to the creditor.

This payment will immediately reflect on the Bank Statement (BS) of the business.

EFT Payment Advice

(with reference number)

CPJDr Creditors Control in the General LedgerDr Creditor in the Creditors’ Ledger Cr Bank in the General Ledger

Identifying accounts

Item Account nameLaptop, Desktop, Cupboards, Shelves, Printer, cash register, refrigerator, machinery, … etc.

Equipment

Truck, delivery van, etc. VehiclePens, printing paper, cartridge, writing pad, … etc. StationeryMerchandise, goods, products (stock bought for resale) etc. Trading stockPetrol, diesel, oil, etc. FuelCar service, maintenance or service of machines. etc. MaintenanceWrapping paper, boxes, plastic bags, plastic wrap, etc. Packing materialFixing of machines, cars, equipment, vehicles, buildings etc. Repairs

RECORDING OF CREDIT PURCHASES TRANSACTIONS

Note: The business enterprise receives invoice from various suppliers, therefore they will not follow a specific numerical order and the bookkeeper must renumber these invoices on a sequential order.

60 Sample Book ©2019 KM Academics

ACCOUNTING CYCLE FOR CREDIT PURCHASES

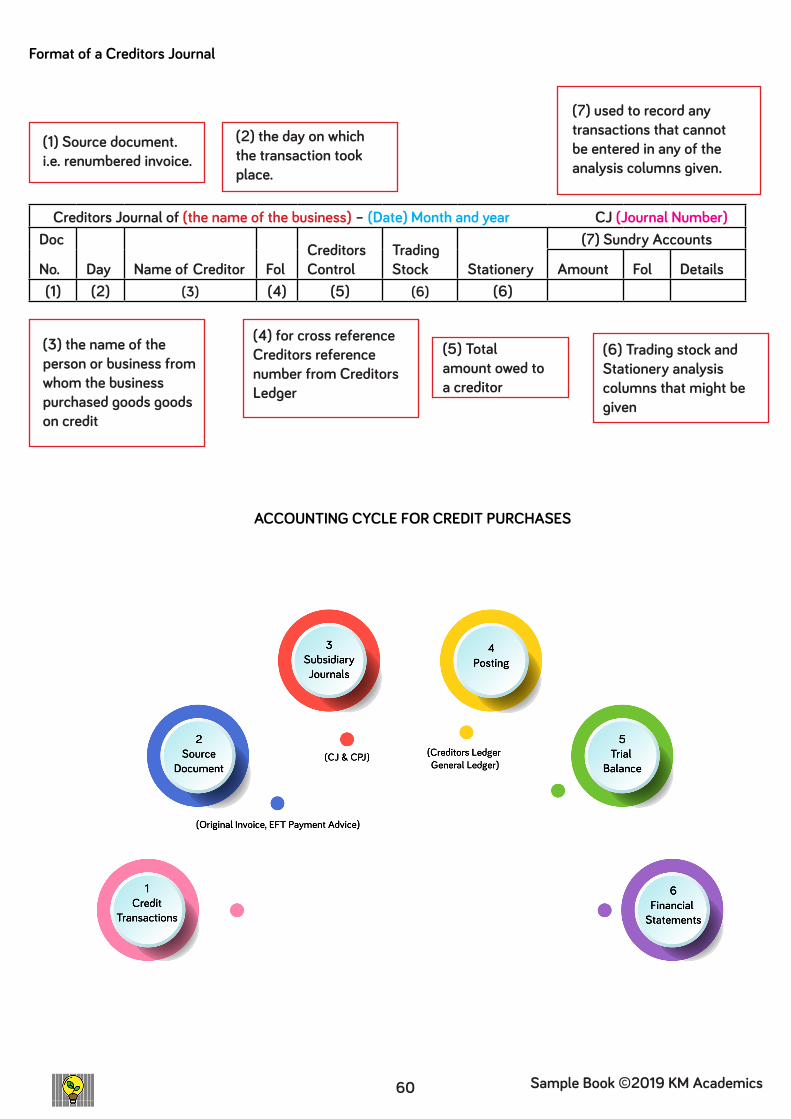

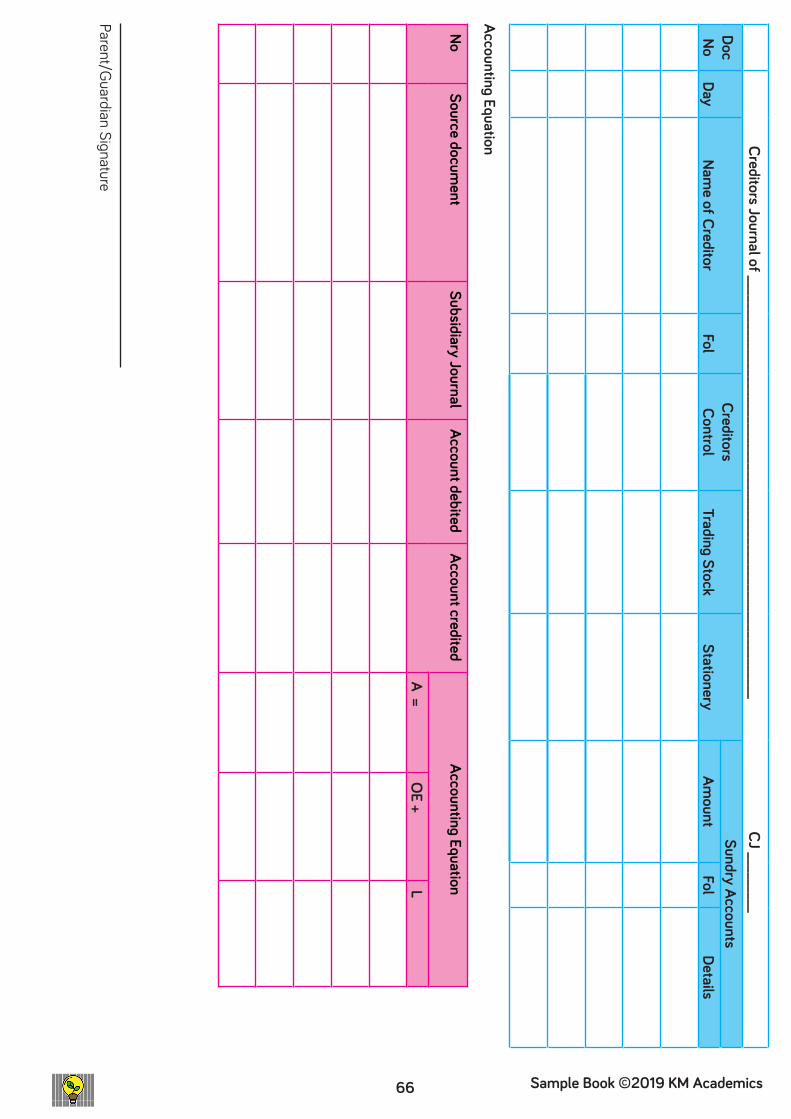

Format of a Creditors Journal

Creditors Journal of (the name of the business) – (Date) Month and year CJ (Journal Number) Doc

No. Day Name of Creditor FolCreditors Control

Trading Stock Stationery

(7) Sundry Accounts

Amount Fol Details (1) (2) (3) (4) (5) (6) (6)

(1) Source document.i.e. renumbered invoice.

(3) the name of the person or business from whom the business purchased goods goods on credit

(4) for cross referenceCreditors reference number from Creditors Ledger

(5) Total amount owed to a creditor

(6) Trading stock and Stationery analysis columns that might be given

(2) the day on which the transaction took place.

(7) used to record any transactions that cannot be entered in any of the analysis columns given.

61Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

ACCOUNTING CYCLE FOR CREDIT PURCHASES

Creditors Journal of (the name of the business) – (Date) Month and year CJ (Journal Number) Doc

No. Day Name of Creditor FolCreditors Control

Trading Stock Stationery

(7) Sundry Accounts

Amount Fol Details (1) (2) (3) (4) (5) (6) (6)

Activity 3.2 Date:____________________________ACCOUNTING CYCLE

Complete the Accounting Cycle for Credit Purchases

Circle the correct letter, i.e 1 b)

1. Transaction

a) Credit Sales

b) Cash Sales

c) Credit Purchases

2. Source Document

a) Duplicate Invoice

b) Original Invoice

c) Duplicate of Receipt

3. Journal

a) Debtors Journal

b) Creditors Journal

c) Cash Receipts

4. Posting to Ledger

a) Debtors Ledger and General Ledger

b) Creditors Ledger and General Ledger

c) General Ledger

Parent/Guardian Signature

62 Sample Book ©2019 KM Academics

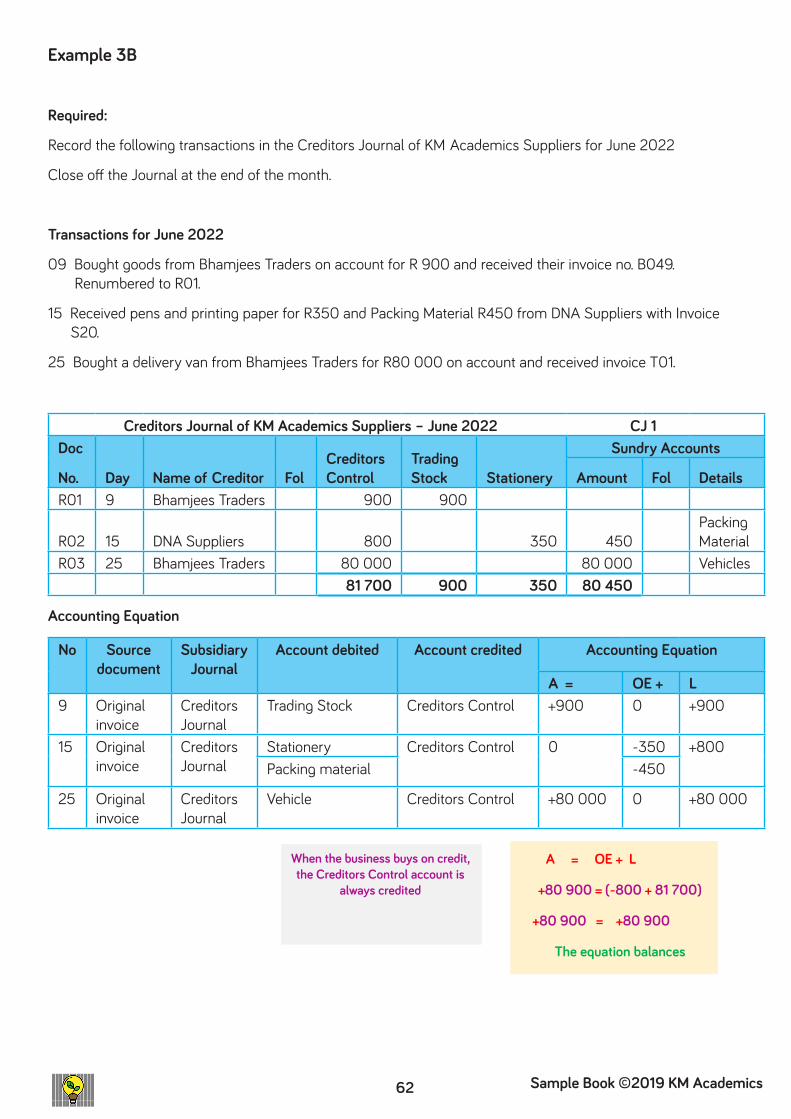

Example 3B

Required:

Record the following transactions in the Creditors Journal of KM Academics Suppliers for June 2022

Close off the Journal at the end of the month.

Transactions for June 2022

09 Bought goods from Bhamjees Traders on account for R 900 and received their invoice no. B049. Renumbered to R01.

15 Received pens and printing paper for R350 and Packing Material R450 from DNA Suppliers with Invoice S20.

25 Bought a delivery van from Bhamjees Traders for R80 000 on account and received invoice T01.

Creditors Journal of KM Academics Suppliers – June 2022 CJ 1Doc

No. Day Name of Creditor FolCreditors Control

Trading Stock Stationery

Sundry Accounts

Amount Fol Details R01 9 Bhamjees Traders 900 900

R02 15 DNA Suppliers 800 350 450 Packing Material

R03 25 Bhamjees Traders 80 000 80 000 Vehicles 81 700 900 350 80 450

Accounting Equation

No Source document

Subsidiary Journal

Account debited Account credited Accounting Equation

A = OE + L9 Original

invoiceCreditors Journal

Trading Stock Creditors Control +900 0 +900

15 Original invoice

Creditors Journal

Stationery Creditors Control 0 -350 +800Packing material -450

25 Original invoice

Creditors Journal

Vehicle Creditors Control +80 000 0 +80 000

A = OE + L

+80 900 = (-800 + 81 700)

+80 900 = +80 900

The equation balances

When the business buys on credit, the Creditors Control account is

always credited

63Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

Activity 3.3 Date:___________________________ Required:

Use the transactions below to prepare the Creditors Journal of ZZ Traders as well as the accounting equation.

Transactions for June 2022

3. Bought goods from DD Suppliers on account for R77 000 and received their invoice no.001. Renumbered to C01.

7. Received Wrapping paper and plastic bags for R5 300 and Stationery R700 from Brookes Traders with Invoice Z80A.

21. Bought a cash register from DD Suppliers for R12 000 on account and received invoice W53.

64 Sample Book ©2019 KM Academics

Creditors Journal of ZZ Traders – June 2022 CJ 2

Doc No

DayNam

e of CreditorFol

Creditors Control

Trading StockStationery

Sundry AccountsAm

ountFol

Details

Accounting Equation

NoSource docum

entSubsidiary Journal

Account debitedAccount credited

Accounting Equation

A =O

E +L

Parent/Guardian Signature

65Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

You are provided with transaction from the books of SS Traders for January 2022. The business buys cell phones on credit.

Required:

1. Record the transactions below in the Creditors Journals provided.

2. Show the effects of the accounting equation.

Transactions: January 2022

4 Bought merchandise from Lawton Suppliers for R81 500. Received their invoice M001 and renumbered it to L01.

9 Bought stationery from LM stationers for R300. Received invoice 02.

15 Received invoice Z44 for R40 000 from TT Motors, for a panel van.

23. Received invoice C33 from Lawton Suppliers for goods bought on credit, R78 900 and photocopying paper R350

Activity 3.4 Date:___________________________ Required:

66 Sample Book ©2019 KM Academics

Creditors Journal of _______________________________________________________________ CJ _________

Doc No

DayNam

e of CreditorFol

Creditors Control

Trading StockStationery

Sundry AccountsAm

ountFol

Details

Accounting Equation

NoSource docum

entSubsidiary Journal

Account debitedAccount credited

Accounting Equation

A =O

E +L

Parent/Guardian Signature

67Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

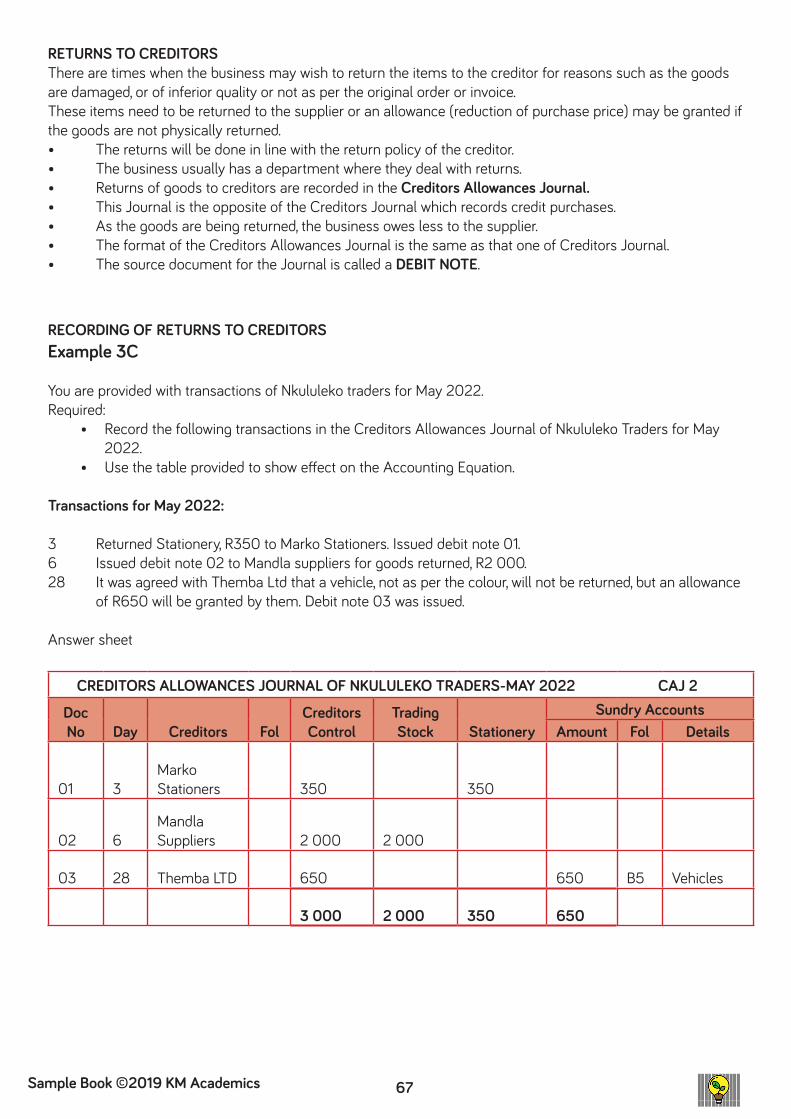

RECORDING OF RETURNS TO CREDITORSExample 3C

You are provided with transactions of Nkululeko traders for May 2022.Required:

• Record the following transactions in the Creditors Allowances Journal of Nkululeko Traders for May 2022.

• Use the table provided to show effect on the Accounting Equation.

Transactions for May 2022:

3 Returned Stationery, R350 to Marko Stationers. Issued debit note 01.6 Issued debit note 02 to Mandla suppliers for goods returned, R2 000.28 It was agreed with Themba Ltd that a vehicle, not as per the colour, will not be returned, but an allowance of R650 will be granted by them. Debit note 03 was issued.

Answer sheet

CREDITORS ALLOWANCES JOURNAL OF NKULULEKO TRADERS-MAY 2022 CAJ 2

Doc No Day Creditors Fol

Creditors Control

Trading Stock Stationery

Sundry AccountsAmount Fol Details

01 3Marko Stationers 350 350

02 6Mandla Suppliers 2 000 2 000

03 28 Themba LTD 650 650 B5 Vehicles

3 000 2 000 350 650

RETURNS TO CREDITORSThere are times when the business may wish to return the items to the creditor for reasons such as the goods are damaged, or of inferior quality or not as per the original order or invoice.These items need to be returned to the supplier or an allowance (reduction of purchase price) may be granted if the goods are not physically returned.• The returns will be done in line with the return policy of the creditor.• The business usually has a department where they deal with returns.• Returns of goods to creditors are recorded in the Creditors Allowances Journal.• This Journal is the opposite of the Creditors Journal which records credit purchases.• As the goods are being returned, the business owes less to the supplier.• The format of the Creditors Allowances Journal is the same as that one of Creditors Journal.• The source document for the Journal is called a DEBIT NOTE.

68 Sample Book ©2019 KM Academics

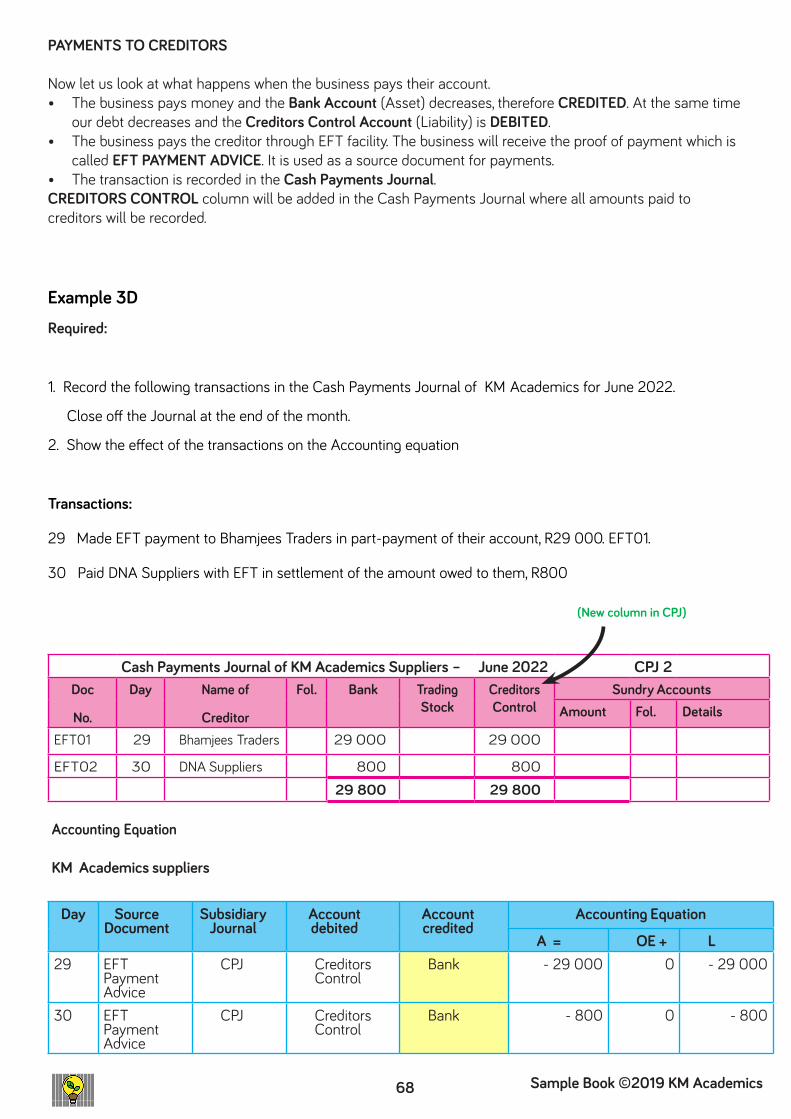

PAYMENTS TO CREDITORS

Now let us look at what happens when the business pays their account.• The business pays money and the Bank Account (Asset) decreases, therefore CREDITED. At the same time

our debt decreases and the Creditors Control Account (Liability) is DEBITED.• The business pays the creditor through EFT facility. The business will receive the proof of payment which is

called EFT PAYMENT ADVICE. It is used as a source document for payments.• The transaction is recorded in the Cash Payments Journal.CREDITORS CONTROL column will be added in the Cash Payments Journal where all amounts paid to creditors will be recorded.

Example 3DRequired:

1. Record the following transactions in the Cash Payments Journal of KM Academics for June 2022.

Close off the Journal at the end of the month.

2. Show the effect of the transactions on the Accounting equation

Transactions:

29 Made EFT payment to Bhamjees Traders in part-payment of their account, R29 000. EFT01.

30 Paid DNA Suppliers with EFT in settlement of the amount owed to them, R800

Cash Payments Journal of KM Academics Suppliers – June 2022 CPJ 2Doc

No.

Day Name of

Creditor

Fol. Bank Trading Stock

Creditors Control

Sundry AccountsAmount Fol. Details

EFT01 29 Bhamjees Traders 29 000 29 000

EFT02 30 DNA Suppliers 800 800

29 800 29 800

Accounting Equation

KM Academics suppliers

Day Source Document

Subsidiary Journal

Account debited

Account credited

Accounting Equation

A = OE + L29 EFT

Payment Advice

CPJ Creditors Control

Bank - 29 000 0 - 29 000

30 EFT Payment Advice

CPJ Creditors Control

Bank - 800 0 - 800

(New column in CPJ)

69Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

TERM 4

70 Sample Book ©2019 KM Academics

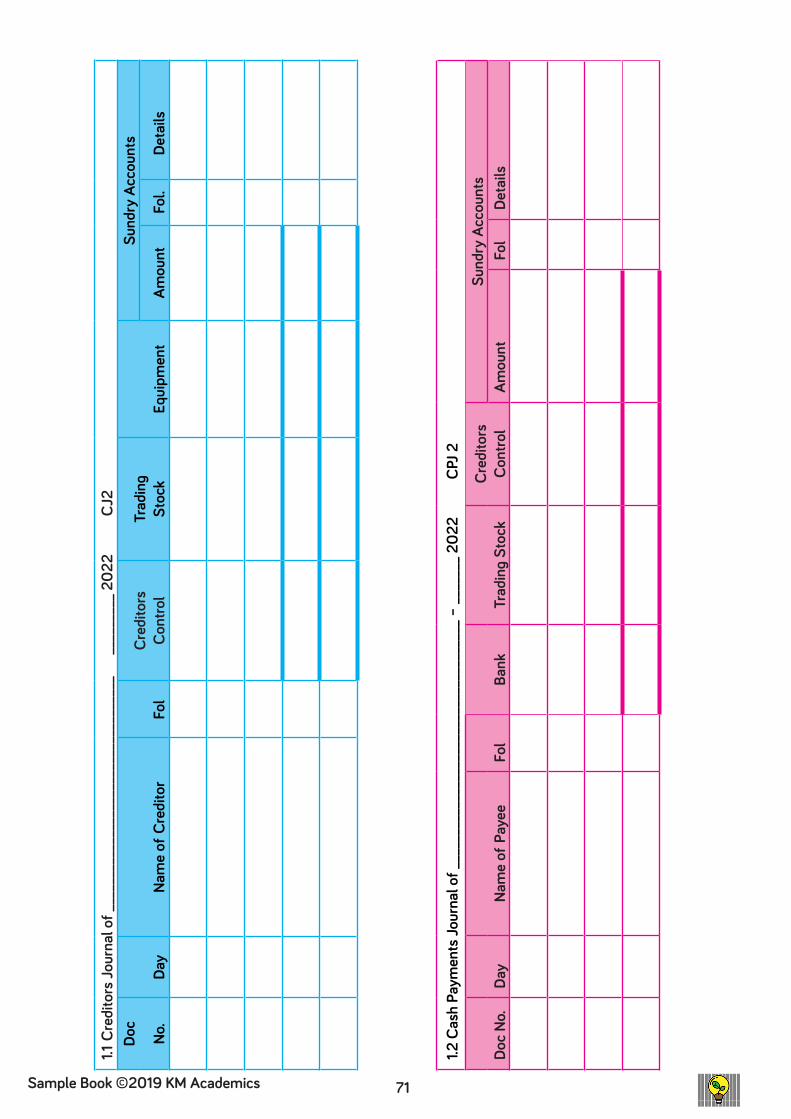

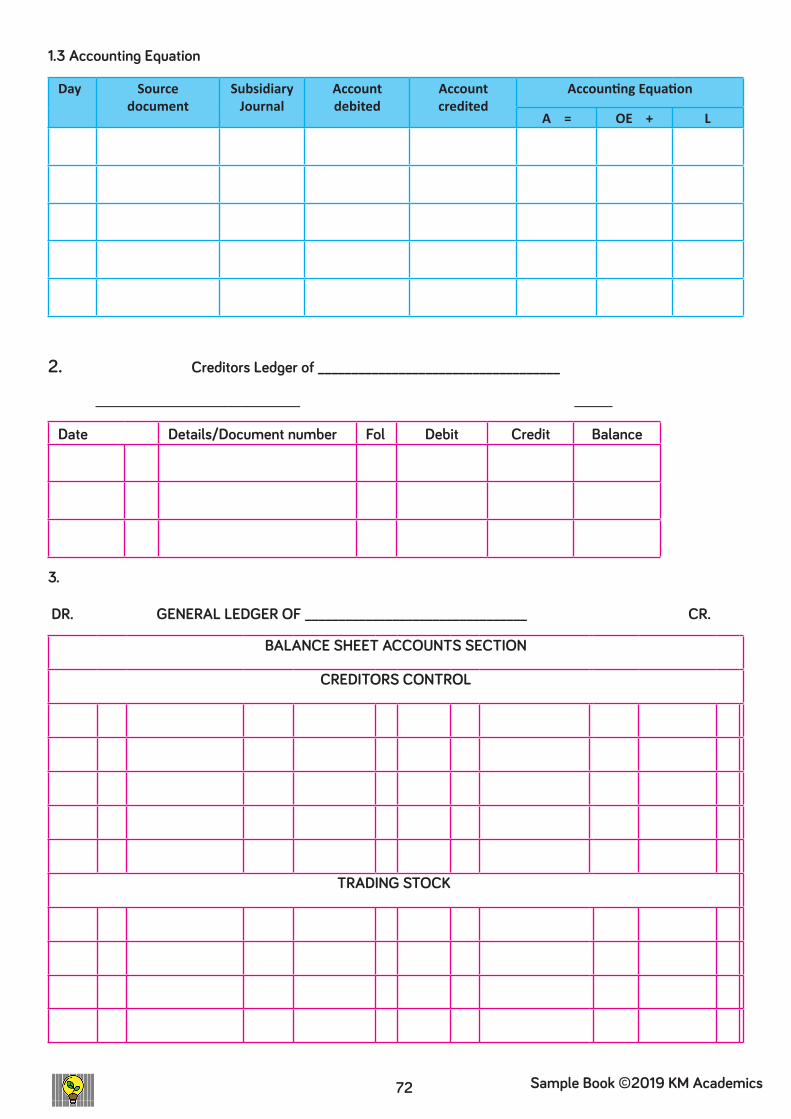

REVISION ACTIVITY 3: Date:___________________________TERM 3 WORK

Required:1. Record the transactions of BBT Suppliers for June 2022 in the following subsidiary journals:

1.1. Creditors Journal with columns for Creditors control, Trading Stock, Stationery and Sundry Accounts.1.2. Cash Payments Journal with columns for Bank, Trading Stock, Creditors Control and Sundry Accounts.1.3 Show the effect of transactions on the elements of the Accounting equation for the transactions dated 16 & 31.

2. Post to the Account of EE Traders in the Creditors Ledger.3. Post to the Trading Stock and Creditors Control Accounts in the General Ledger

Transactions: June 202211. Received invoice 12 (renumbered to 01) from EE Traders for the purchase of the following:

• Merchandise, R 12 800• Acer Laptop, R 3 500

16 Purchased goods on credit from Sponky Suppliers, R 22 000 and received invoice 001.19 Bought Merchandise from Sponky Suppliers for R1 500. Paid using EFT. EFT Payment Advice reference: EFT 1126. Paid part of the amount owing to EE Traders with EFT, R14 400.28. Received stationery on account from Sponky Suppliers with invoice 200, for R895.31. Paid R12 350 using EFT, to Sponky Suppliers in part payment of their account.

71Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

1.1 C

redi

tors

Jour

nal o

f ___

____

____

____

____

____

____

____

____

____

____

_ 202

2

CJ2

Doc

No.

Day

Nam

e of

Cre

dito

rFo

lCr

edito

rs

Cont

rol

Trad

ing

Stoc

kEq

uipm

ent

Sund

ry A

ccou

nts

Amou

ntFo

l. De

tails

1.2 C

ash

Paym

ents

Jour

nal o

f ___

____

____

____

____

____

____

____

____

__ –

____

___ 2

022

CPJ

2

Doc

No.

Day

Nam

e of

Pay

ee

Fol

Bank

Trad

ing

Stoc

kCr

edito

rs

Cont

rol

Sund

ry A

ccou

nts

Amou

ntFo

lDe

tails

72 Sample Book ©2019 KM Academics

1.3 Accounting Equation

Day Source document

Subsidiary Journal

Account debited

Account credited

Accounting Equation

A = OE + L

2. Creditors Ledger of ____________________________________

___________________________ _____

Date Details/Document number Fol Debit Credit Balance

3.

DR. GENERAL LEDGER OF _________________________________ CR.

BALANCE SHEET ACCOUNTS SECTION

CREDITORS CONTROL

TRADING STOCK

73Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

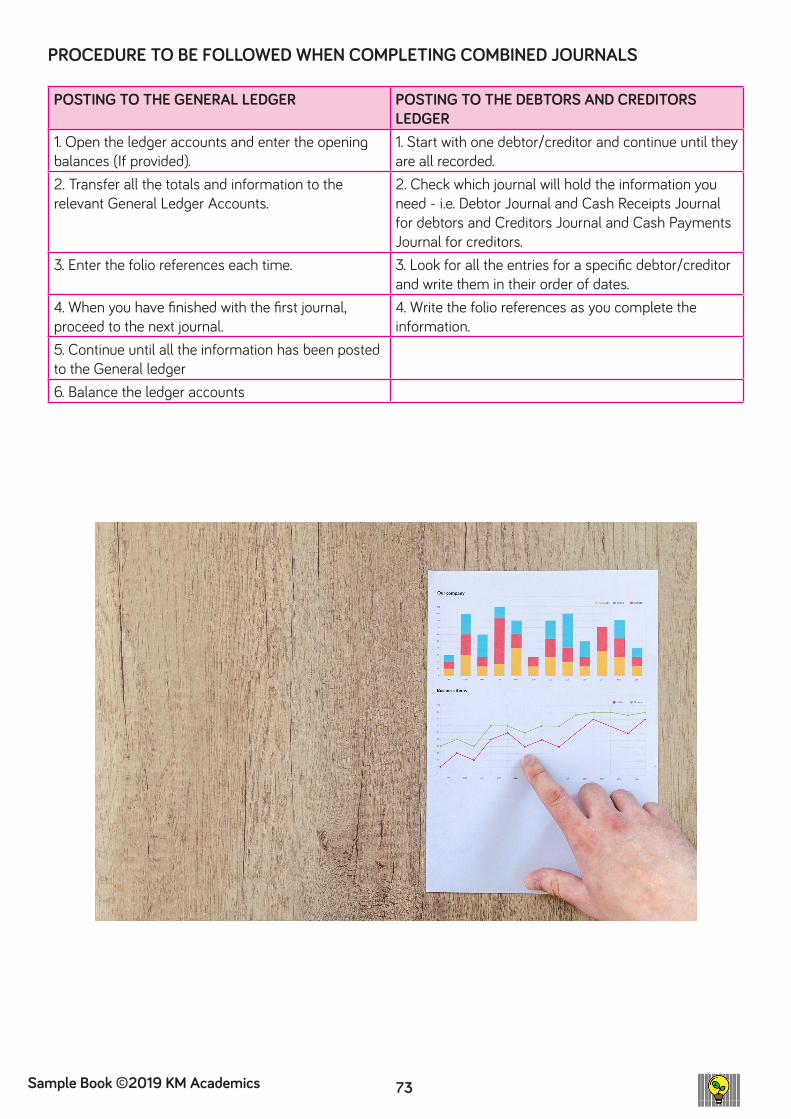

PROCEDURE TO BE FOLLOWED WHEN COMPLETING COMBINED JOURNALS

POSTING TO THE GENERAL LEDGER POSTING TO THE DEBTORS AND CREDITORS LEDGER

1. Open the ledger accounts and enter the opening balances (If provided).

1. Start with one debtor/creditor and continue until they are all recorded.

2. Transfer all the totals and information to the relevant General Ledger Accounts.

2. Check which journal will hold the information you need - i.e. Debtor Journal and Cash Receipts Journal for debtors and Creditors Journal and Cash Payments Journal for creditors.

3. Enter the folio references each time. 3. Look for all the entries for a specific debtor/creditor and write them in their order of dates.

4. When you have finished with the first journal, proceed to the next journal.

4. Write the folio references as you complete the information.

5. Continue until all the information has been posted to the General ledger6. Balance the ledger accounts

74 Sample Book ©2019 KM Academics

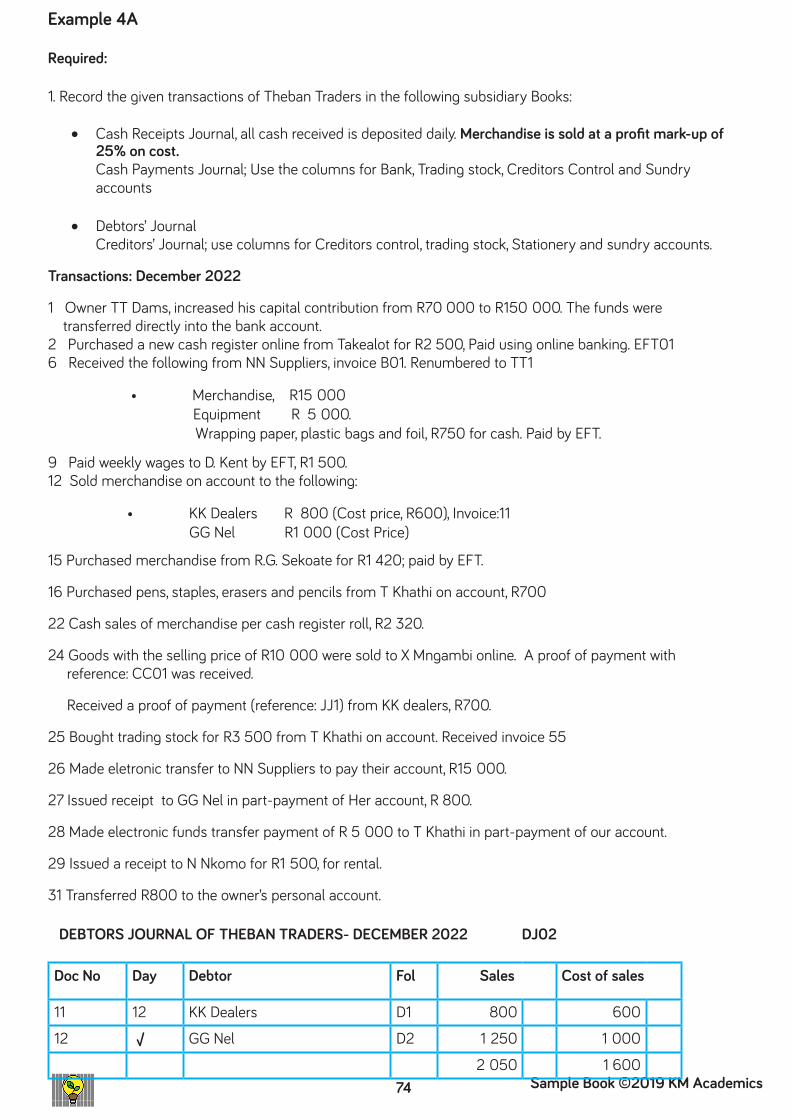

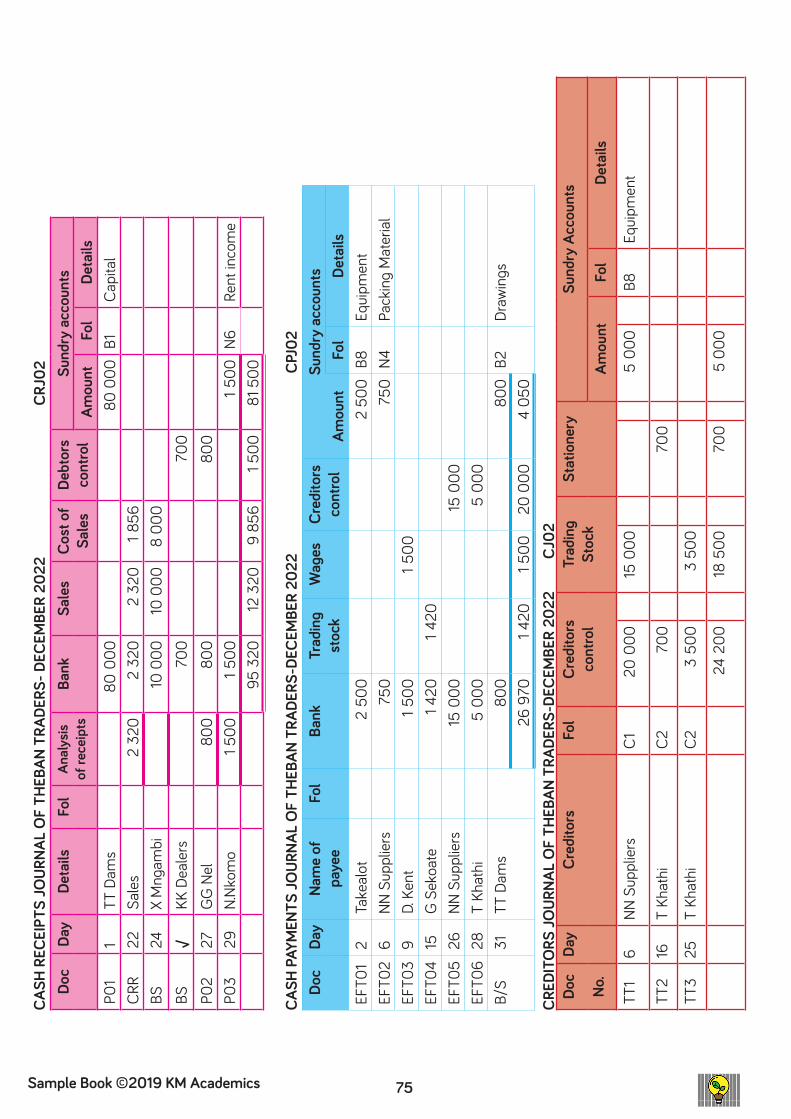

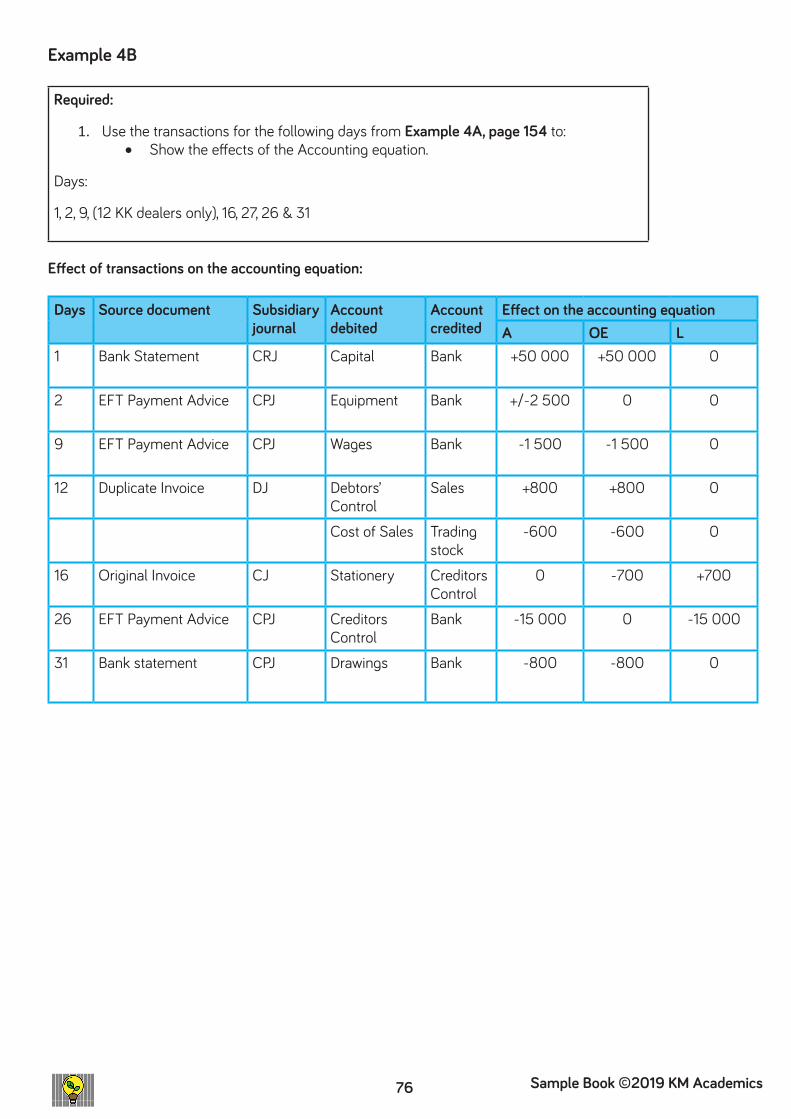

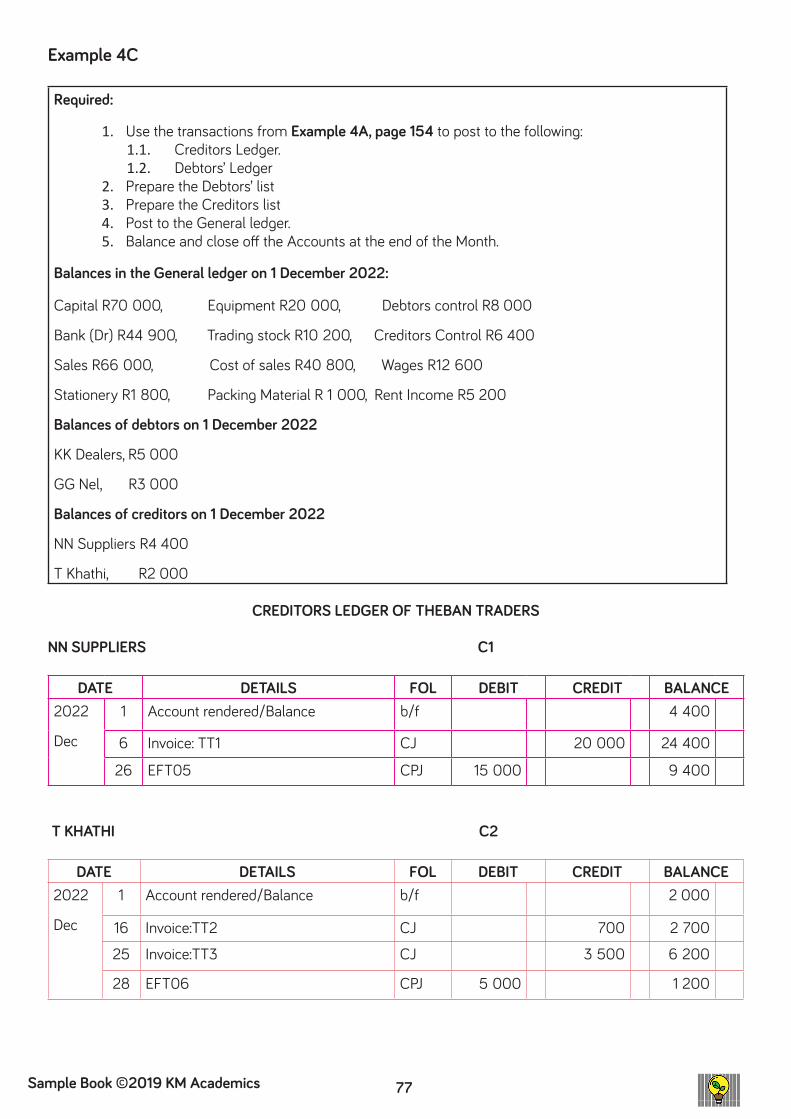

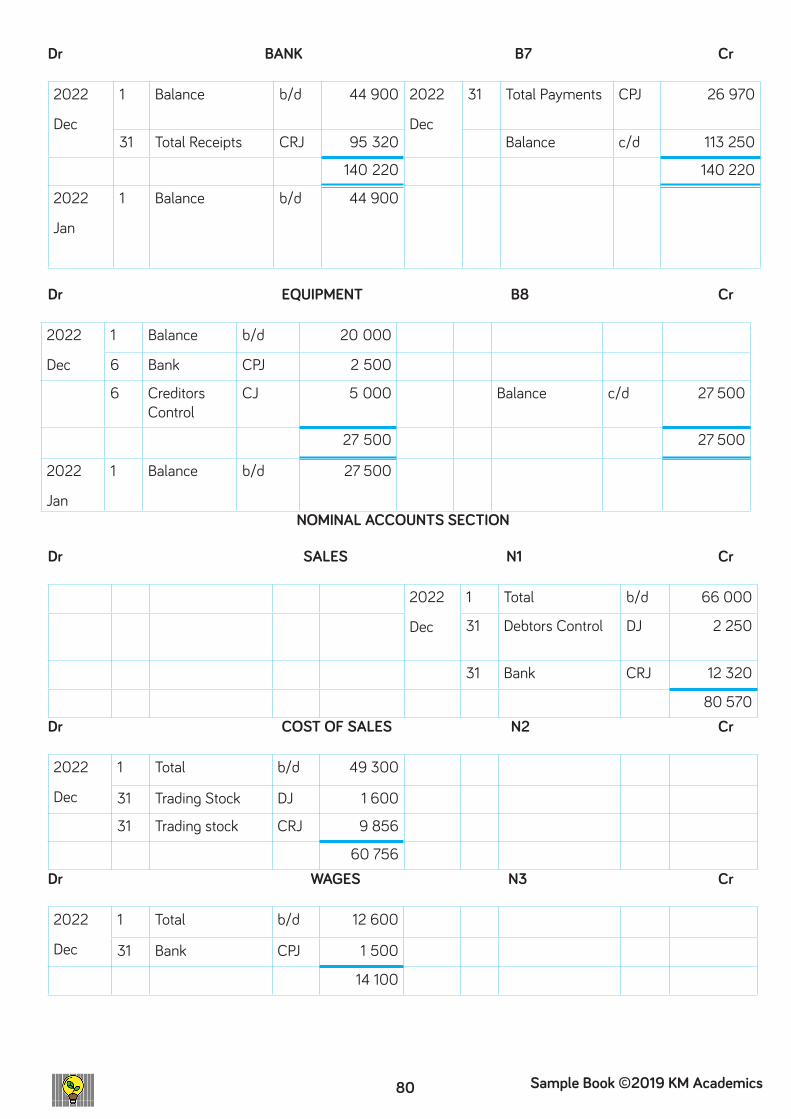

15 Purchased merchandise from R.G. Sekoate for R1 420; paid by EFT.

16 Purchased pens, staples, erasers and pencils from T Khathi on account, R700

22 Cash sales of merchandise per cash register roll, R2 320.

24 Goods with the selling price of R10 000 were sold to X Mngambi online. A proof of payment with reference: CC01 was received.

Received a proof of payment (reference: JJ1) from KK dealers, R700.

25 Bought trading stock for R3 500 from T Khathi on account. Received invoice 55

26 Made eletronic transfer to NN Suppliers to pay their account, R15 000.

27 Issued receipt to GG Nel in part-payment of Her account, R 800.

28 Made electronic funds transfer payment of R 5 000 to T Khathi in part-payment of our account.

29 Issued a receipt to N Nkomo for R1 500, for rental.

31 Transferred R800 to the owner’s personal account.

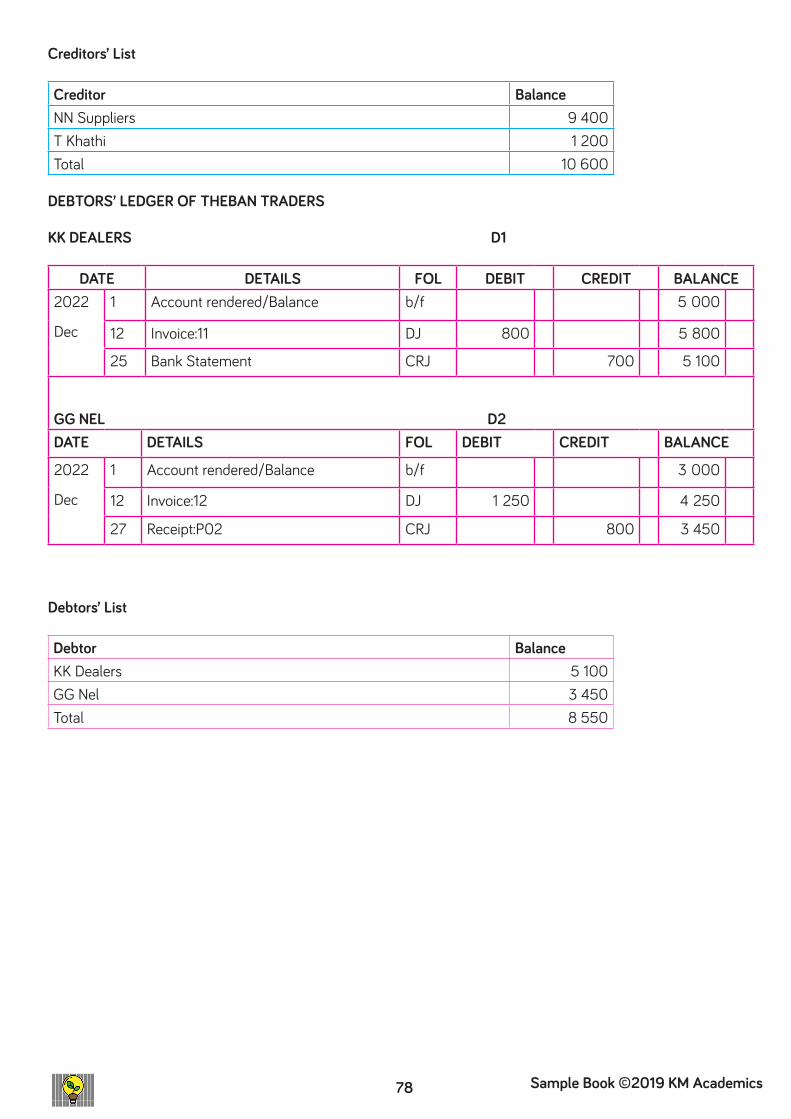

DEBTORS JOURNAL OF THEBAN TRADERS- DECEMBER 2022 DJ02

Doc No Day Debtor Fol Sales Cost of sales

11 12 KK Dealers D1 800 600

12 √ GG Nel D2 1 250 1 000

2 050 1 600

Example 4A

Required:

1. Record the given transactions of Theban Traders in the following subsidiary Books:

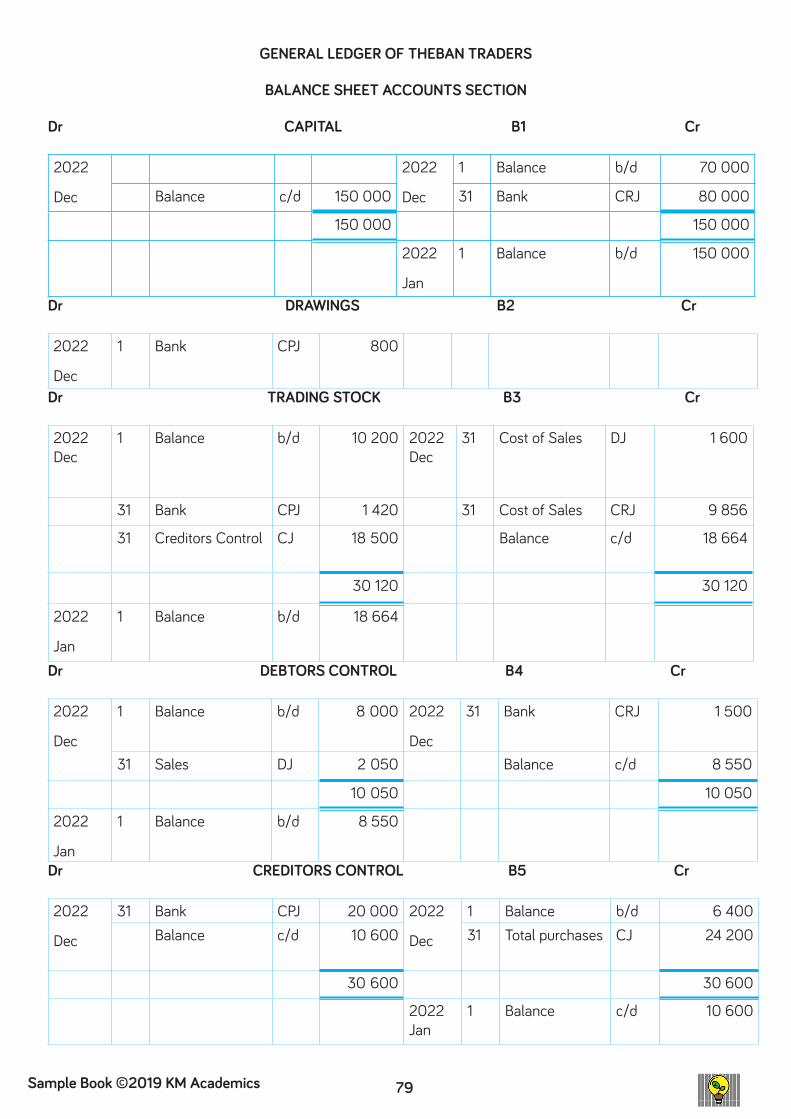

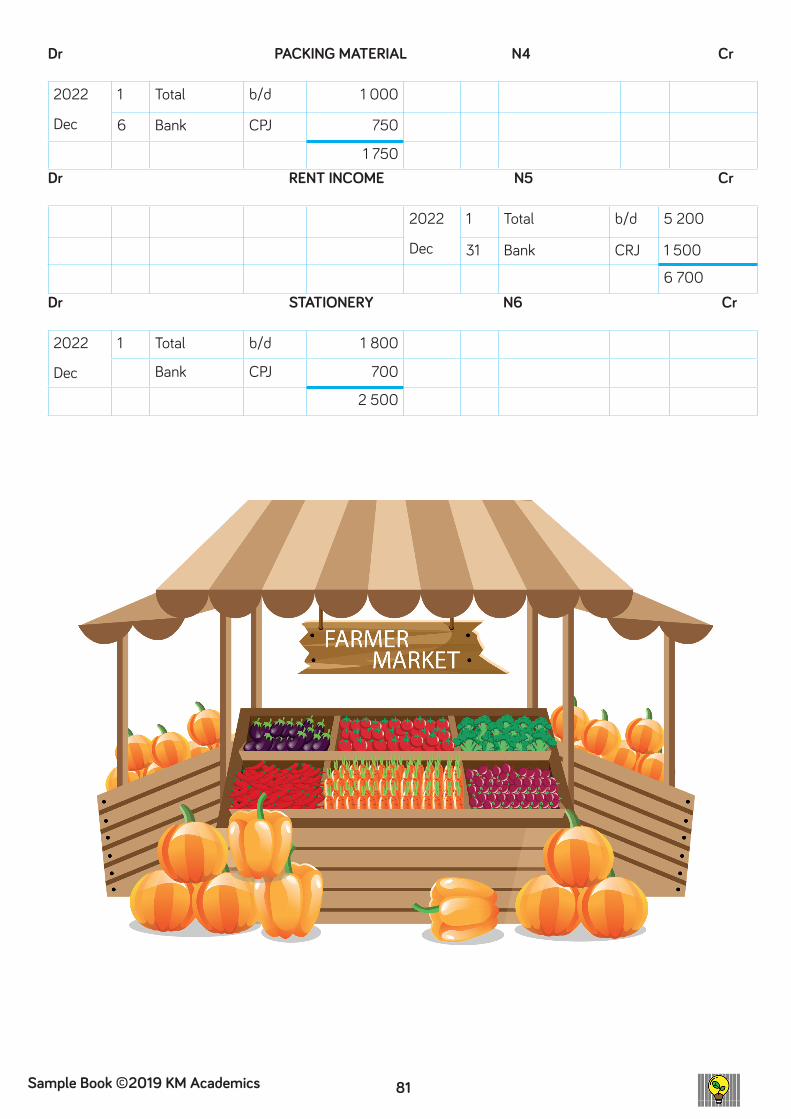

• Cash Receipts Journal, all cash received is deposited daily. Merchandise is sold at a profit mark-up of 25% on cost. Cash Payments Journal; Use the columns for Bank, Trading stock, Creditors Control and Sundry accounts

• Debtors’ Journal Creditors’ Journal; use columns for Creditors control, trading stock, Stationery and sundry accounts.

Transactions: December 2022

1 Owner TT Dams, increased his capital contribution from R70 000 to R150 000. The funds were transferred directly into the bank account. 2 Purchased a new cash register online from Takealot for R2 500, Paid using online banking. EFT01 6 Received the following from NN Suppliers, invoice B01. Renumbered to TT1

• Merchandise, R15 000 Equipment R 5 000. Wrapping paper, plastic bags and foil, R750 for cash. Paid by EFT.

9 Paid weekly wages to D. Kent by EFT, R1 500. 12 Sold merchandise on account to the following:

• KK Dealers R 800 (Cost price, R600), Invoice:11 GG Nel R1 000 (Cost Price)

75Sample Book ©2019 KM Academics Sample Book ©2019 KM Academics

CASH

REC

EIPT

S JO

URNA

L O

F TH

EBAN

TRA

DERS

- DEC

EMBE

R 20

22

CR

J02

Doc

Day

Deta

ilsFo

lAn

alys

is of

rece

ipts

Bank

Sale

sCo

st o

f Sa

les

Debt

ors

cont

rol

Sund

ry a

ccou

nts

Amou

ntFo

lDe

tails

P01

1TT

Dam

s80

000

80 0

00B1

Capi

tal

CRR

22Sa

les

2 32

02

320

2 32

01 8

56BS

24X

Mng

ambi

10

000

10 0

008

000

BS√

KK D

eale

rs70

070

0P0

227

GG

Nel

800

800

800

P03

29N.

Nkom

o1 5

001 5

001 5

00N6

Rent

inco

me

95 3

2012

320

9 85

61 5

0081

500

CASH

PAY

MEN

TS J

OUR

NAL

OF

THEB

AN T

RADE

RS-D

ECEM

BER

2022

CPJ

02Do

cDa

yNa

me

of

paye

eFo

lBa

nkTr

adin

g st

ock

Wag

esCr

edito

rs

cont

rol

Sund

ry a

ccou

nts

Amou

ntFo

lDe

tails

EFT0

12

Take

alot

2 50

02