1 CHAPTER ONE 1.1 Introduction This chapter underlines the background of the study, statement of the problem, formulates the objectives of the study, research questions, and significance of the study as well as delimitations and scope of the study. Furthermore it provides the conceptual framework and definition of terms. 1.2 Background of the Study Financial services industry has been undergoing a profound transformation in the two decades. Rapid changes in the banking environment, increased competition by new players from non banking sector, product innovations, globalization and technological advancement – all these have led to a market situation in which the battle for customers is intense. (Watson et al, 2002) As a consequence, banks have started to offer services through various delivery channels such as mobile banking. In the name of increased customer satisfaction and efficiency, they developed innovative services, products and offered a wide range of services. The delivery of multi channel services forms part of these efforts. For example the provision of banking services being available via mobile phones or personal digital assistants (PDAs), clearly mobile phone banking services forms an important innovation in the banking sector (Weiser, 1991) In Tanzania, mobile phones are the newest technologies that have spread fastest throughout the country with the highest coverage despite of the poor infrastructure. Despite the mobile phone access to and coverage availability to every household, the main reasons of communication are between family members and friends for voice and message services. The mobile phone banking has also showed to be a powerful technical platform for banking services in Tanzania as service delivery channel. Some of the commercial banks have introduced the mobile phone banking services in their products range, which can be delivered to people even in rural areas without banking offices and at low costs. CRDB Bank as one of the commercial banks introduced this product currently named as SIM Banking, but still there is slow adoption of customers toward the product. Despite the bank efforts to provide service through mobile phone banking little is known about factors influencing the adoption of mobile phone banking in

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

CHAPTER ONE

1.1 Introduction

This chapter underlines the background of the study, statement of the problem, formulates the

objectives of the study, research questions, and significance of the study as well as delimitations

and scope of the study. Furthermore it provides the conceptual framework and definition of

terms.

1.2 Background of the Study

Financial services industry has been undergoing a profound transformation in the two decades.

Rapid changes in the banking environment, increased competition by new players from non

banking sector, product innovations, globalization and technological advancement – all these

have led to a market situation in which the battle for customers is intense. (Watson et al, 2002)

As a consequence, banks have started to offer services through various delivery channels such as

mobile banking. In the name of increased customer satisfaction and efficiency, they developed

innovative services, products and offered a wide range of services. The delivery of multi channel

services forms part of these efforts. For example the provision of banking services being

available via mobile phones or personal digital assistants (PDAs), clearly mobile phone banking

services forms an important innovation in the banking sector (Weiser, 1991)

In Tanzania, mobile phones are the newest technologies that have spread fastest throughout the

country with the highest coverage despite of the poor infrastructure. Despite the mobile phone

access to and coverage availability to every household, the main reasons of communication are

between family members and friends for voice and message services.

The mobile phone banking has also showed to be a powerful technical platform for banking

services in Tanzania as service delivery channel. Some of the commercial banks have introduced

the mobile phone banking services in their products range, which can be delivered to people even

in rural areas without banking offices and at low costs. CRDB Bank as one of the commercial

banks introduced this product currently named as SIM Banking, but still there is slow adoption

of customers toward the product. Despite the bank efforts to provide service through mobile

phone banking little is known about factors influencing the adoption of mobile phone banking in

2

Tanzania. It is mobile phone banking as phenomenon which is under investigation in the present

research.

1.3 Statement of the Problem

In the banking industry, bank branches alone are no longer adequate to provide banking services

to cater the increasing needs of demanding customers. Therefore, the provision of banking

services through mobile phone has provided an alternative means to acquire banking services

very convenience and timely to bank customers. Despite all the efforts aimed by CRDB Bank Plc

at developing better mobile phone banking, this system is still unnoticed by large number of the

bank customers. According to the Annual Report of CRDB Bank Plc 2011, the bank has a total

number of customers 1,314,000 but up to now only 18,929 have adopted the product of mobile

phone banking. This brings the basic questions in which there is a need to answer it, what are the

factors influencing customers to adopt mobile banking? Do customers have sufficient knowledge

about mobile phone banking? Therefore in this situation it is important to understand main

factors that make bank customers' to accept and use mobile phone banking. This information can

assist commercial banks including CRDB Bank Plc in building of mobile phone banking services

that the bank customers want to use, thus assist them to attract potential users to use the system.

Research has been conducted on the areas of mobile commerce and mobile banking, with foci on

different factors and contexts. Wu and Wang (2005), in a study on middle class populations,

found that cost had minimal significant impact on the adoption of mobile phone banking;

however it is critical when the technology is first introduced. A study by Wu and Wang (2005)

on the costs of mobile commerce showed that perceived cost had minimal significance when

compared to other variables such as perceived risk, compatibility and perceived usefulness.

Various studies on perceived risk in the context of mobile phone banking (Brown, Cajee, Davies,

& Stroebel, 2003; Walker, 2004) exist, however the perceived risk variable has only been

modeled as a single construct influencing customers to adopt mobile phone banking.

Furthermore, the effects of demographic variables such as race, age, gender, and culture on the

adoption of mobile phone banking was not extensively explored in the above studies. Therefore

this study seeks to explore factors which influence the adoption of mobile phone banking, A case

of Mwanza city of Tanzania and more specifically, the factors limiting the use of the

3

corresponding services available, as research results obtained in other regions and countries may

not be entirely relevant to the Tanzania context due to cultural and behavioral differences as well

as to socio-economic factors.

1.4 Objective of the Study

The main objective of this research is to examine the factors influencing the adoption of mobile

phone banking by customers in Tanzania banking industry. A case of CRDB Bank Plc in

Mwanza city.

Specific objectives: For the general objective to be achieved, the specific objectives that will

guide the research are:

To establish the profile of mobile phone banking users in CRDB Bank at Mwanza city.

To examine how customers at CRDB bank perceive risks in relation to mobile phone

banking in Mwanza city.

To establish what influences customers at CRDB in Mwanza region to trust mobile phone

banking.

To determine how perceived usefulness and perceived ease of use influence the adoption

of mobile phone banking at CRDB Bank in Mwanza city.

1.5 Research Questions

The study will be guided by the following on research questions:

What are the types of users of mobile phone banking in Mwanza city in terms of

demographic characteristics?

What are the main factors influencing the adoption of mobile phone banking by

customers in Mwanza city?

How do customers at CRDB Bank perceive risks with regards to mobile phone banking

in Mwanza city?

What influences customers at CRDB Bank in Mwanza city to trust mobile banking?

How does perceived usefulness and perceived ease of use influence the adoption of

mobile phone banking at CRDB Bank in Mwanza city?

4

1.6 Significance of the Study

The findings of this research may be of potential value to the Banking industry and to other

researchers (e.g. social scientists). Based on the factors found to be influencing user decision on

the adoption of mobile phone banking services, the study may provide recommendations for

banks about changes needed in order to accelerate user adoption of the services offered.

Social scientists may find the results useful for their study of human behavior and motivation,

and how they may affect attitudes towards the adoption and use of an innovative service.

Findings of this study are also expected to serve as a stimulant and stepping stone for future

researchers and academicians by suggesting areas where further studies need to be conducted on

the same or similar topics.

1.7 Delimitation and Scope of the Study

The study will be limited to Mwanza region and specifically to CRDB customers (both retail and

corporate customers) who are users and non users of mobile banking. The study will also be

limited to active bank customers who are users mobile phone banking services. Moreover the

study will be for only bank customers who are resident in Mwanza not less than twelve months.

5

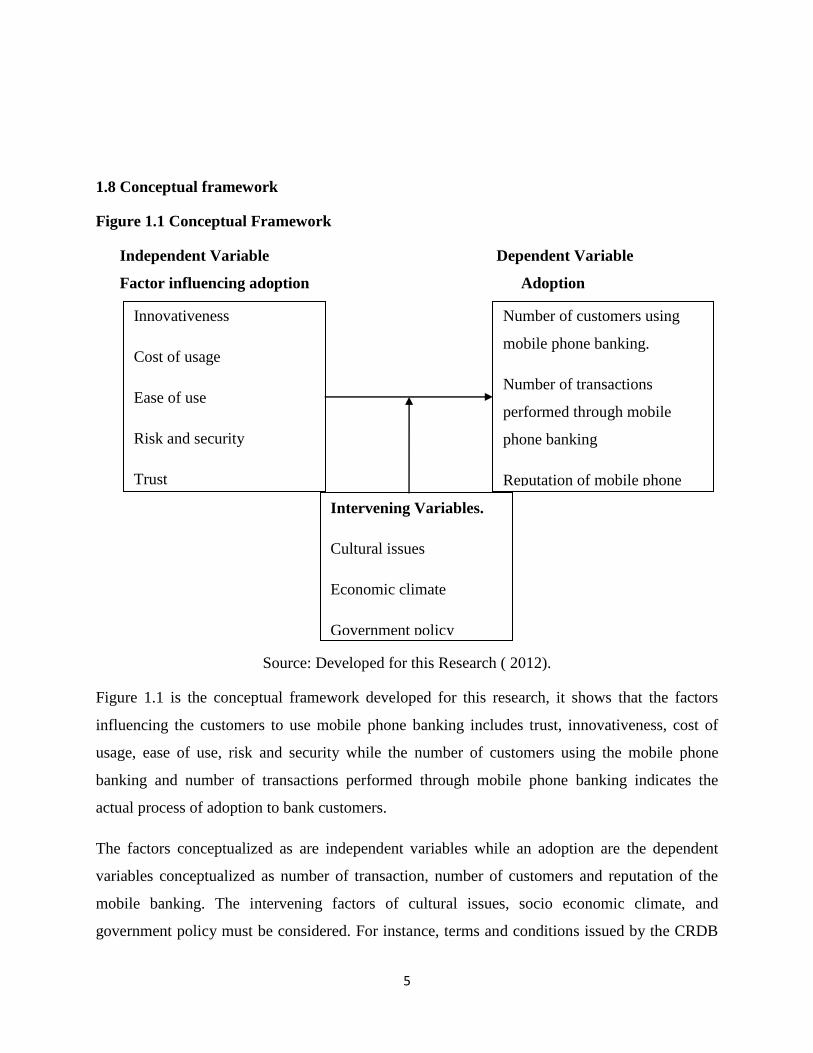

1.8 Conceptual framework

Figure 1.1 Conceptual Framework

Independent Variable Dependent Variable

Factor influencing adoption Adoption

Source: Developed for this Research ( 2012).

Figure 1.1 is the conceptual framework developed for this research, it shows that the factors

influencing the customers to use mobile phone banking includes trust, innovativeness, cost of

usage, ease of use, risk and security while the number of customers using the mobile phone

banking and number of transactions performed through mobile phone banking indicates the

actual process of adoption to bank customers.

The factors conceptualized as are independent variables while an adoption are the dependent

variables conceptualized as number of transaction, number of customers and reputation of the

mobile banking. The intervening factors of cultural issues, socio economic climate, and

government policy must be considered. For instance, terms and conditions issued by the CRDB

Intervening Variables.

Cultural issues

Economic climate

Government policy

Innovativeness

Cost of usage

Ease of use

Risk and security

Trust

Other

Controlling (Proper

Monitoring System and

management.

Number of customers using

mobile phone banking.

Number of transactions

performed through mobile

phone banking

Reputation of mobile phone

banking in the industry

6

bank to its mobile phone banking customers represent the legal context and it may intervene the

customer from joining the service.

In general, Figure 1.1 indicates the relationship between three sets of variables understudy.

1.9 Definition of Key Terms

I. Mobile phone banking

Mobile phone banking means the financial services delivered via mobile networks and

performed on a mobile phone. ( Porteous, 2006)

II. Mobile transactions

Transactions such as remittances and payments delivered via mobile networks and performed on

a mobile phone (Leopoldina, 2005)

III. Retail banking

Retail banking is defined as the banking in which banking institutions execute transactions

directly with consumers, rather than corporations or other banks. Services offered include:

savings and transactional accounts, mortgages, personal loans, debit cards, credit cards, and so

forth ( Tiwari and Buse, 2006).

IV. Banking

An organization, usually a corporation, chartered by a state or federal government, which does

most or all of the following: receives demand deposits and time deposits, honors instruments

drawn on them, and pays interest on them; discounts notes, makes loans, and invests in

securities; collects checks, drafts, and notes; certifies depositor's checks; and issues drafts and

cashier's checks ( Hoggson, N. 1926).

1.10 Conclusion

This chapter has presented the background to the study, statement of research problem and

research objectives. It then provided the significance of the study, scope and delimitation and

definition of key terms. Finally, it explained the conceptual framework for this study.

7

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter reviews the existing literature on factors influencing user behavior in regard to use

and adoption of mobile phone banking services as well as some of the relevant research models

used in Information system (IS) research. In addition, it briefly reviews the research approach of

this study.

2.2 Overview of Mobile Phone Banking

2.2.1 Definition of Mobile Phone Banking

Mobile Phone banking is defined as a business transaction conducted through mobile

communication networks. Mobile phone banking can offer value to consumers through

convenience and flexibility by enabling time and place independence (Venkatesh, 2009).

According to CRDB Bank operating manual, Mobile phone bank is the one which enables its

account holders to carry out banking transactions using their mobile handsets. The product has

been enhanced to enable customers to perform a wide range of banking services on their own

such as

View their account(s) balances

View mini statement showing last four transactions

Pay for utility services such as luku, star times, cable TV.

Transfer funds between own and third party accounts and/or mobile phones

Cash withdrawal by non account holders/ card less from CRDB Bank ATM’s

Top up of mobile phones

And other services such as stop card/cheque, pin change, change of language etc.

Mobile phone banking is an application of mobile commerce which enables customers to access

bank accounts through mobile devices to conduct and complete bank related transactions such as

balancing cheques, checking account statuses, transferring money and selling stocks. ( Kim et al

2009).

8

Luo, Li, Zhang and shin (2010),defined mobile phone banking as an innovative method for

accessing banking services via a channel where by customers interacts with a bank using a

mobile device (e.g. mobile phone or personal digital assistant(PDA)).This is the definition

adopted in this research.

2.2.2 Types of Mobile Phone Banking

Mobile phone banking is implemented through three different technology solutions, namely

browser-based applications, messaging-based applications and client-based applications

(i) The browser-based application

This is an application that is accessed over a network called Wireless Access Protocol (WAP)-

based internet access. This type requires a compatible mobile phone which is WAP-enabled,

used to access banking portals through the Internet. (Kim et al 2009)

(ii) Messaging-Based Applications,

This is an application where by communication is between the bank and the customer, carried

out via text messages. That is a registered customer’s mobile phone number; sends a predefined

command to the bank, and then the bank uses text messages to conduct transactions as per

customer’s request. An example of messaging-based applications is the Unstructured

Supplementary Service Data (USSD). In Tanzania an existing mobile banking applications based

on USSD includes M-PESA (Camner & Sjöblom, 2009).

(iii) Client-Based Applications

This is the special software which is installed in the mobile phone to perform mobile phone

banking services to the customers. An example of a client-based application is what is called the

SIM Toolkit standard (STK) (Tiwari & Buse, 2007).

9

2.2.3 Comparison between traditional banking and mobile phone banking.

Mobile phone banking, this type of service offered by banks actually works the same way as

traditional banking. The major difference lies in the convenience offered by mobile banking

particularly when it comes to making payments, obtaining updated information of the account, or

reconciling account statements. Rather than personally visiting your local bank, you can now

access your account and perform your bank transactions using your mobile phone. But just like

any other customer related services, traditional and online banking has its own shares of benefits

andcdrawbacks.

( i ) Benefits and drawbacks of Mobile Phone Banking

The major benefit one can enjoy with mobile phone banking is convenience because more often

than not, customers can easily complete multiple tasks even without leaving their homes to visit

the local branch of their bank. Efficiency and convenience is what sets apart mobile phone

banking from traditional banking, in mobile phone banking, customers are able to pay their bills,

move deposit, or withdraw money to another account, reconcile multiple bank accounts, and a lot

more related services customers can enjoy in order to expedite their bank transactions even when

they are just at home. It also saves the valuable time of customers which they can use to do other

tasks. In seconds, every bank transaction can be completed and the customer can even print his

or her receipts from his mobile phone for recording purposes. The customer can also enjoy

unlimited access to his or her bank account no matter what the day and time is including holidays

or weekends. In addition to this, even if you are in another country, you can access your account

asclongcascyouchavecacmobilecnetworkcconnection.KKKKKKKKKKKKKKKKKKKKKKKK

KKK

Mobile phone banking can significantly expedite banking transactions and it is also rather cheap

when it comes to bank charges as compared to traditional banking. Most banks with mobile

services offer lesser fees for the service they offer. Besides, banks often have high interest rates

particularly on savings accounts and bank CDs or certificates of deposits and they can also offer

added financial services and other related financial products to its customers. And as for

10

customers, they will not need to buy stamps or envelopes or even rush to the post office to send

in their payments by mail. This lessens the risks for late payments. Customers can also

electronically access their bank statements and reconcile it faster than ever before. (Lugoutte

1996)

The downside to this is that even with all the sophisticated software, security programs and tools

used by mobile banks, there is always a risk for identity theft which can put your account and all

that’s in it in danger of being hacked. The problem actually do not lie on the mobile bank itself

but rather on the users who are not too keen on practicing safety measures in order to safeguards

their account information. Aside from identity theft, different threats related to mobile banking

also include hacking and phishing of mobile bank accounts by expert hackers who are clever

enough to penetrate the user’s personal information.kkkkkkkkkkkkkkkkkkkkkkkkkkkkkkkkkkkk

( ii ) Benefits and Drawbacks of Traditional Banking kkkkkkkkkkkkkkkkkk

Even if convenience and time efficiency is at stake particular for those who love to multi task,

some people still prefer traditional banking methods as compared to Mobile banking services.

For some, security is always the issue that is why they prefer to actually interact with real tellers.

If ever there is a problem, they can easily ask for assistance from a bank representative to sort

out their problems although this can take longer than expected particularly when all hands are

busy with various office tasks. Some people also feel comfortable when they actually see the

money change hands as compared to mobile banking wherein all the proof that they get about

their transactions is the receipt provided to them by the site after completion of a certain

transaction (Ternullo, G 1997).111

2.3 Adoption Theories

According to Doyle (1998), customers are invariably the best source of ideas. Innovations have

commercial value only if they meet the needs of customers better than current product.

Innovative customers are those individuals who are at the forefront in buying new products or

11

applying new ideas. But before customers can adopt an innovation, they must learn about it. This

learning is called the adoption process (Rogers, 1995) and consists of five stages as follows:

Awareness: first the individual is exposed to innovation but lacks complete information about it

Interest: next the individual becomes interested in the new ideas and seeks additional

information about it.

Evaluator: individual mentally applies the innovation to his present and anticipated the future

situation and then decides whether or not to try.

Trial: the individual makes full use of the innovation

Adoption: the individual decides to continue the full use of innovation.

The literature on the adoption of innovation and specifically adoption of mobile banking can be

found in a broad range of academic research. These studies suggest that customers adoption of

mobile banking technology may be related to number of factors, associated with characteristics

of customers (Ajzen and Fishbein, 1980; Chang and Cheung, 2001; Rogers, 1995; Davis, 1985).

This study concentrates on personal characteristics (Demographic and Behavior of the Adopters).

Since Davis Technology Acceptance Model has been proved as reliable and valid model in

explaining information system acceptance and usage it will be used in this study too.

2.3.1 Theory of Reasoned Action (TRA)

This is a model studied from social psychology, which is concerned with the determinants of

consciously intended behaviors. It is composed of attitudinal, social influences, and intention

variables to predict behavior. TRA hypothesized that the individual’s behavioral intention to

perform a behavior is jointly determined by the individual’s attitude toward performing the

behavior and subjective norm, which is the overall perception of what relevant others think the

individual should or should not do.

The importance of attitude toward performing behavior and subjective norm to predict

behavioral intention will vary by behavioral domain. For behaviors in which attitudinal or

12

personal based influence stronger (e.g. purchasing something for personal consumption only),

attitude toward performing behavior will be the dominant predictor of behavior intention and

subjective norm will be of little or no predictive efficacy. While for behaviors in which

normative implications are strong (e.g. purchasing something that others will use), subjective

norm should be the dominant predictor of behavior intention and attitude toward performing the

behavior will be of less importance (Ajzen and Fishbein, 1980).

The theory of reasoned action also hypothesized that behavior intention is the only direct

antecedent of actual behavior. Behavior intention is expected to predict actual behavior

accurately if three boundary conditions specified by Fishbein and Ajzen (1975) can be hold:

(a)the degree to which the measure of intention and behavioral criterion correspond with respect

to their levels of specificity of action, target, context, and timeframe; (b) the stability of

intentions between time of measurement and performance of behavior; and (c) the degree to

which carrying out the intention is under the volitional control of the individual.

The TRA has been successfully applied to a large number of situations to predict the

performance of behavior and intentions. For example, TRA predicted turnover, education, and

breast cancer examination.

2.3.2 Theory of Planned Behavior (TPB)

Ajzen (1985) extended the theory of reasoned action by including other construct called

perceived behavioral control, which predicts behavioral intentions and behavior. The extended

model is called the Theory of Planned Behavior. Perceived behavioral control reflects belief

regarding access to the resources and opportunities needed to affect a behavior.

Perceived behavioral control appears to encompass two components. The first is facilitating

conditions, which reflects the availability of resources needed to perform a particular behavior.

This might include access to the time, money and other specialized resources. In fact, as

supporting technological infrastructures become easily and readily available, mobile banking

will become more feasible. Accordingly, the government can play an intervention and leadership

role in the diffusion of innovation. The second component is self efficacy, which is, being

13

confident of the ability to behave successfully in the situation. An individual with the self

assured skill to use a technology is more inclined to adopt to mobile banking. Self efficacy then

refers to comfort with using the innovation.

TPB has been successfully applied to various situations in predicting the performance of

behavior and intentions, such as predicting user intentions to use a new software, to perform to

perform breast self examination, to avoid caffeine, to perform unethical behavior, and to

understand wastepaper recycling.

2.3.3 Technology Acceptance Model

It was proposed by Fred David in 1985. This is an information system theory that models how

users come to accept and use a technology. TAM focuses on IS use based on social psychology

theory and has a valid and reliable instruments. As defined by Davis the two basic determinants

are perceived usefulness and perceived ease of use are instrumental in explaining the user

intention and behavior towards the use of new technology.

Perceived usefulness is defined as the degree to which a person believes that using a particular

system would enhance his/her job performance while perceived ease of use is defined as the

degree to which a person believes that using a particular system would be free from efforts. A

system high in perceived usefulness, in turn, is the one for which a ser believes in the existence

of a positive use-performance relationship. All else being equal, an application perceived easier

to use than another is more likely to be accepted by users.

2.3.4 Triandis model

The model assumes an attitude intention behavior relationship, by taking into account the

important constructs such as habit, social factors and facilitating conditions. It postulates that the

probabilility of performing an act is a function of habit, intention to perform the act and

facilitating conditions. The intention of performing a particular behavior is a function of the

perceived consequences, social factors (including norms, roles, and the self concept) and affect.

Triandis model has been widely adopted in the studies of social and health behavior, and

consumer behavior (Chang and Cheung, 2001)

14

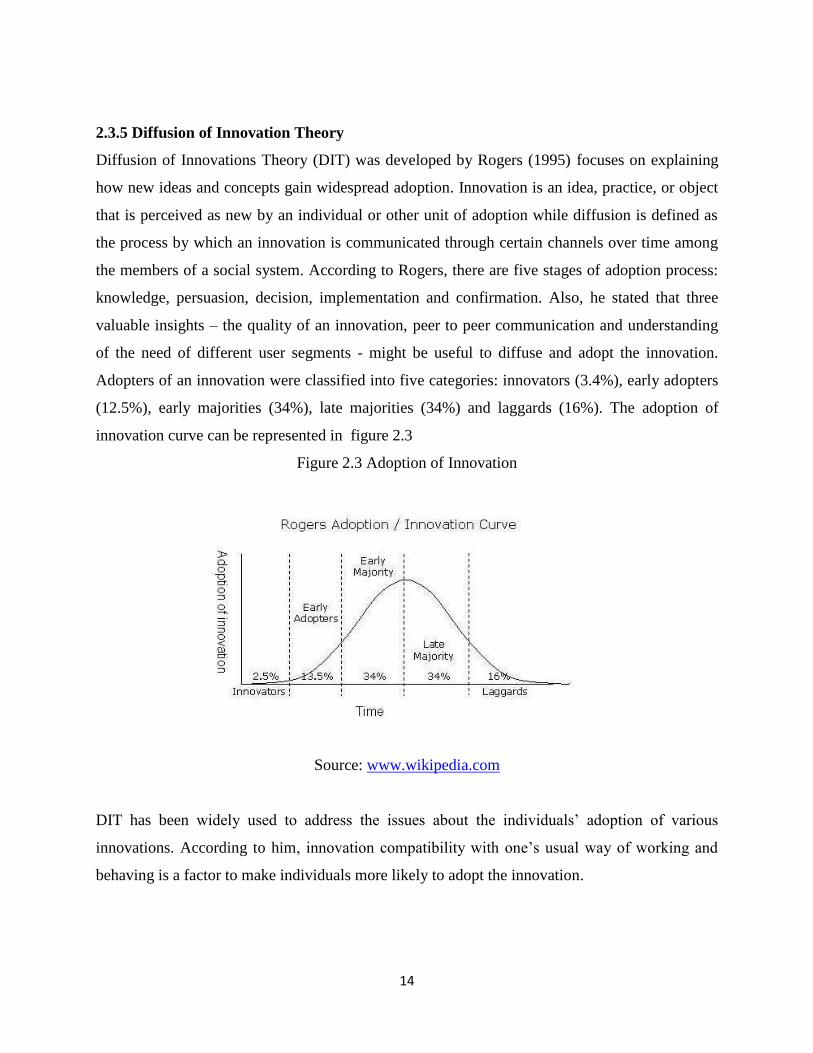

2.3.5 Diffusion of Innovation Theory

Diffusion of Innovations Theory (DIT) was developed by Rogers (1995) focuses on explaining

how new ideas and concepts gain widespread adoption. Innovation is an idea, practice, or object

that is perceived as new by an individual or other unit of adoption while diffusion is defined as

the process by which an innovation is communicated through certain channels over time among

the members of a social system. According to Rogers, there are five stages of adoption process:

knowledge, persuasion, decision, implementation and confirmation. Also, he stated that three

valuable insights – the quality of an innovation, peer to peer communication and understanding

of the need of different user segments - might be useful to diffuse and adopt the innovation.

Adopters of an innovation were classified into five categories: innovators (3.4%), early adopters

(12.5%), early majorities (34%), late majorities (34%) and laggards (16%). The adoption of

innovation curve can be represented in figure 2.3

Figure 2.3 Adoption of Innovation

Source: www.wikipedia.com

DIT has been widely used to address the issues about the individuals’ adoption of various

innovations. According to him, innovation compatibility with one’s usual way of working and

behaving is a factor to make individuals more likely to adopt the innovation.

15

2.4 Adoption of Mobile Phones in Tanzania

When comparing recent adopters and those who have used mobile banking for a longer period of

time, demographically National Survey Data, 2010 found that there is no substantial difference

in who has been using mobile phone banking over time. Tanzanian mobile phone banking users

tend to already have access to banking services. Some 63 percent of mobile phone banking users

reported currently having a banking account.

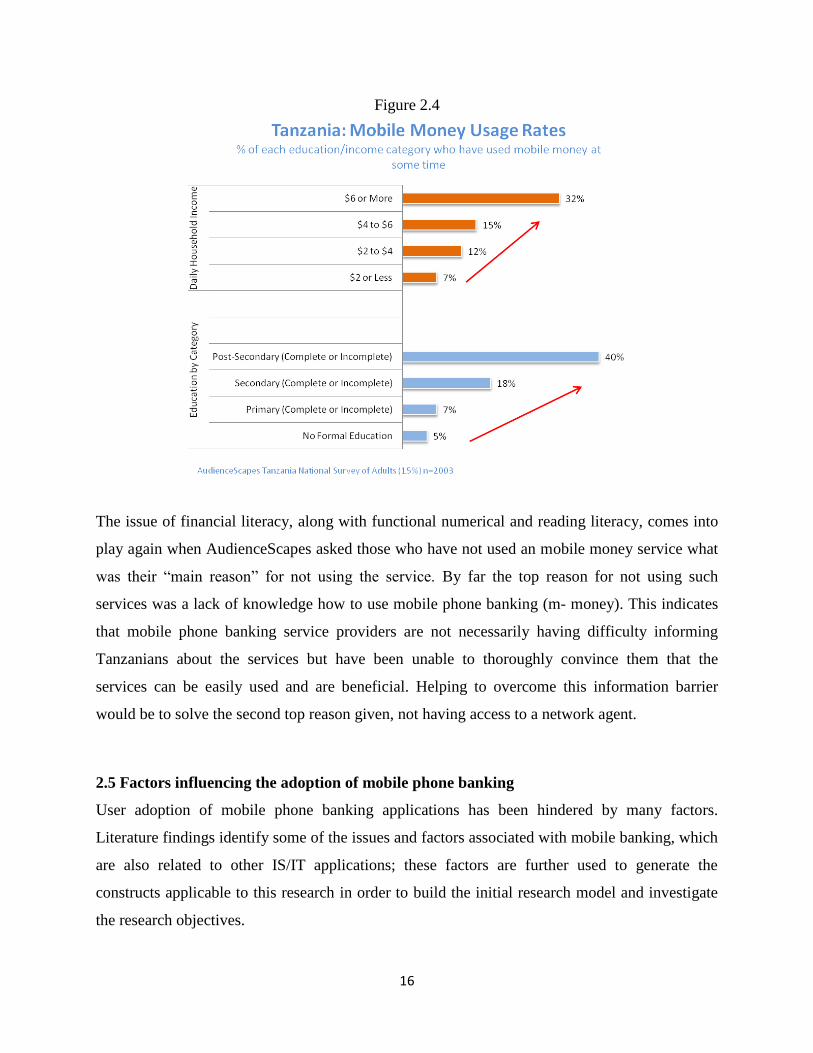

From figure 2.4 If we compare the take up rates between the currently banked and unbanked we

see that there is a very large gap between those who have experience with banking services and

those without This highlights the importance of financial literacy and its influence on mobile

banking adoption, especially of formal banking practices, as those Tanzanians who currently

have a bank account are exponentially more likely to have used (36 percent) mobile banking

compared to those who do not have an account (5 percent). This gap in mobile phone banking

adoption is larger between those who have experience with formal banking services than

informal banking services.

16

Figure 2.4

The issue of financial literacy, along with functional numerical and reading literacy, comes into

play again when AudienceScapes asked those who have not used an mobile money service what

was their “main reason” for not using the service. By far the top reason for not using such

services was a lack of knowledge how to use mobile phone banking (m- money). This indicates

that mobile phone banking service providers are not necessarily having difficulty informing

Tanzanians about the services but have been unable to thoroughly convince them that the

services can be easily used and are beneficial. Helping to overcome this information barrier

would be to solve the second top reason given, not having access to a network agent.

2.5 Factors influencing the adoption of mobile phone banking

User adoption of mobile phone banking applications has been hindered by many factors.

Literature findings identify some of the issues and factors associated with mobile banking, which

are also related to other IS/IT applications; these factors are further used to generate the

constructs applicable to this research in order to build the initial research model and investigate

the research objectives.

17

(i) Perceived Usefulness

The perceived usefulness is a prominent factor which is widely used in explaining consumer

behavior in a recent Mobile phone banking adoption model studies. According to Davis (1989),

the perceived usefulness of a system is defined as the extent to which individuals believe that

using the new technology will enhance their task performance. There is extensive research in the

Information Systems and Mobile phone banking that provides evidence of the significant effect

of perceived usefulness on usage or adoption intention. Therefore, perceived usefulness will

influence user intention to accept or adopt mobile phone banking. Recently numbers of empirical

studies have provided support that perceived usefulness is the primary predictor of Mobile phone

banking adoption and it captures the perceived benefits associated with using mobile banking.

This construct assess the extrinsic characteristics of mobile banking as well as shows how mobile

phone banking can help the users to achieve task-related goals, such as effectiveness and

efficiency (Wei et al., 2008). It is also believed that one who believes mobile phone banking to

be useful and convenient will have positive attitudes towards using Mobile phone banking.

(ii) Perceived Ease of Use

According to Davis (1989), the perceived ease of use for a system is defined as the degree to

which an individual believes that using a particular technology will be free of effort. The

perceived ease of use has been incorporated as an important factor in adopting mobile phone

banking. Many prior empirical studies have demonstrated that perceived ease of use has a

positive influence to adopt mobile phone banking. Thus, perceived ease of use reflects the

perceived efforts in using mobile phone banking. A number of empirical studies tested ease of

use as a predominant determinant of intention to adopt (Agarwal et al 1997). Some found that

this construct exerting a mediation effect. It is one of the major behavioral beliefs influencing

user intention to technology acceptance in both original and the revised TAM models.

Furthermore, one who perceives Mobile phone banking technology to be easy to use will have

positive attitudes towards using Mobile phone banking.

(iii)Personal Innovativeness

Personal Innovativeness is defined as the willingness of an individual to try out any new

information systems. The personal innovativeness is expected to have a strong influence to adopt

18

innovation such as mobile banking (Bhatti, 2007). Innovative individuals have been also found

to be dynamic, communicative, curious, venturesome, and stimulation–seeking. It has been

recognized that highly innovative individuals are active information seekers about new ideas.

Given the relative infancy of the mobile services it is appropriate to test innovativeness as an

influencing variable under new circumstances.

(iv) Perceived Trust

According to Rousseau et. al. (1998), trust is defined as “a psychological state comprising the

intention to accept vulnerability based upon positive expectations of the intentions or behavior of

another”. Perceived Trust is an important construct which is affecting consumer behavior and it

determines the success of Mobile phone banking. Trust is important because it helps consumers

overcome perceptions of uncertainty and risk, and helps build appropriate favorable expectations

of performance and other desired benefits. Furthermore, for trust to exist, consumers must

believe that the sellers have the ability and motivation to reliably deliver goods and services of

the quality expected by the consumers.

(v) Perceived Cost

Perceived Cost is the essentials in the setting up and delivery of Mobile phone banking. Unlike

others constructs, the perceived cost is also an important consideration for consumers to decide

whether to use Mobile phone banking or not. Wei et al., 2009 stated that cost factor is one of the

reasons that could slow down the development of Mobile phone banking. He also mentioned that

cost factor may consist of initial purchase price such as hand set fee, ongoing usage cost such as

subscription fee, service fee and communication fee, and maintenance cost or upgrade cost. In

this study, Perceived cost construct has been incorporated and defined as the extent to which an

individual believes that using mobile phone banking is costly.

(vi) Subjective norms

A person’s subjective norm is determined by his or her perception that salient social referents

think he/she should or should not perform a particular behavior. That person is motivated to

comply with the referents even if he/she does not favor the behavior. The referents may be

superiors (e.g., parents or teachers) or peers (e.g., friends or classmates). In the theory reasoned

19

action (Ajzen and Fishbein, 1980) and theory planned behavior (Ajzen, 1985) social influence is

modeled as subjective norms on behavioral intention. Though the effect of subjective norms on

intention is inconclusive, from prior research there is a significant body of theoretical and

empirical evidence regarding the importance of the role of subjective norm on technology use,

directly or indirectly.

(vii) Perceived Behavioral Control

According to the theory of planned behavior, perceived behavioral control is defined as

individual perceptions of how easy or difficult it is to perform a specific behavior. The perceived

behavior is an important determinant of behavioral intentions by reducing perception of control,

confidence, and effortlessness in executing a behavior. Pedersen (2005) argued that Perceived

Behavioral Control reflects the internal and external constrains on behavior, and is directly

related to both intention to use and actual use of Mobile phone banking services. Behavioral

control has been shown to have an effect on key dependent variables such as intention and

behavior in a variety of domains. A significant number of researches in mobile phone banking

have highlighted the importance of Perceived Behavioral Control by demonstrating its influence

on key dependent variables.

(viii) Facilitating Conditions

Facilitating conditions is defined as the external environment of helping users overcome barriers

and hurdles to use a new IT or Mobile banking (J.C.Gu Et Al., 2009). Users will perceive mobile

phone banking service when they will feel how easy or difficult it is to perform a specific

behavior.

(ix) Self-Efficacy

Self-Efficacy is an important component of perceived behavioral control and refers to an

individual’s belief in his/her capacity to perform a behavior Self-efficacy develops from multiple

sources of information that include in particular vicarious experience and verbal persuasion.

(Khalifa & Cheng 2002).

20

(x) Attitude towards Use

Attitude towards using the system is defined as ‘the degree of evaluative affect that an individual

associate with using the target system in his job’. (Davis et al., 1989) have modified this

definition somewhat. They argue that information systems will be useful in general if they

‘contribute to accomplishing the end-user’s purpose. According to the TRA, the most important

determinant of a person’s behavior is behavioral intention. Behavioral intention is defined as the

strength of one’s intention to perform a specified behavior. A person’s intention to perform a

behavior is a combination of (1) the attitude towards performing the behavior and (2) his or her

subjective norm. Attitudes can be defined as the positive or negative feelings a person has

towards performing a target behavior. If a person perceives that the outcome from performing a

behavior is positive, then he or she will have a positive attitude towards performing the behavior.

Likewise, if a person perceives that the outcome from performing a behavior is negative, he or

she will have negative attitudes towards performing the behavior.

2.6 Empirical Literature Review

Several studies have been conducted on adoption of mobile phone banking. This section

discusses recent studies on the topic.

Wambari (2009) conducted a study on mobile phone banking in developing countries such as

Tanzania, Kenya; the objective of the study was to understand and appreciate the concept and

potential of mobile phone banking and analyze its impact on the customers in developing

countries. However, the study found weaknesses on the security and applications updating in

mobile phone banking. Regulatory barriers set by Tanzania investment centre and central bank

on these services was least concern that the customers had. Slow speed in customer adoption,

data quality and lack of interoperability were other challenges facing the mobile phone banking

users.

The study has been elaborated that the adoption and use of mobile phones is product of a social

process, embedded in social practices such as SMEs Practices which leads to some economic

benefits. The community defines the style of mobile phone use e.g. In urban areas over 73 % of

mobile phone usage is for business purposes while over 70 % of mobile phone usage in the rural

areas is for social communication.

21

Wambari’s findings was biased because it only included samples from developing countries

urban centers such as Nairobi, Dar es salaam etc

Secondly, the study did not look into the details of the cultural impact of the Mobile phone

banking technology which therefore can be grounds for related research.

Shi Yu (2009) conducted the study which identifies and investigates the factors which influence

customers’ decision to use a specific form of mobile phone banking, and specifically focuses on

the evaluation of SMS-based mobile banking in the context of New Zealand.

The model attempts to identify the features of the service, the features of the environment and

those user characteristics that underline usefulness and ease of use, and which may provide an

insight of what influences user perceptions in the case of SMS-based mobile banking.

From This study, It was found that two context specific variables (service speed and service

awareness through advertising) may be important determinants of the success of SMS banking; it

was also shown that, in line with prior results about other geopolitical locations, customers are

more likely to adopt SMS banking if they were comfortable and confident in their ability to use

the service.

Furthermore, the results suggest that compatibility may be a significant factor in the use or

adoption of mobile banking. Banks should therefore build and design functions and mobile

banking services in a way that is consistent and fits with customers’ past experience. Banks can

send customers surveys and receive feedback in order to develop services and functions which

would satisfy customers’ further demands.

Masinge K (2010) aimed to investigate the factors influencing the adoption of mobile phone

banking by the Bottom of the Pyramid (BOP) in South Africa. The study focused on the effect

of the following factors:

• Perceived usefulness of mobile phone banking service;

• Perceived ease of use of the mobile phone banking service;

• Perceived cost of mobile phone banking service; and

22

• Customer’s trust in the mobile phone banking service provider (from three perspectives: banks,

mobile network providers and the wireless network infrastructure);

• Perceived risk (divided into five facets: performance risk, financial risk, social risk, time risk

and security/privacy risk) associated with mobile phone banking services.

The results were able to show that perceived usefulness has a significant impact on the adoption

of mobile phone banking by the BOP. People at the BOP will adopt mobile phone banking

services when the value and benefit of mobile phone banking is evident. The current users of

mobile phone banking services perceived mobile phone banking as useful. The results show that

the people at the BOP will adopt mobile phone banking when it is perceived to be easy to use.

The current users of mobile phone banking services perceived mobile phone banking to be easy

to use. The perceived ease of use variable has a significant positive relationship with perceived

usefulness. This implies that the easier it is to use mobile phone banking, the more it will become

useful. Hence, it is of paramount importance to develop mobile phone banking services with

valuable functionality, as well as mobile devices with visible screens and usable keypads.

The results also shows that perceived cost is a significant factor influencing the adoption of

mobile phone banking on the BOP, thereby making perceived cost a barrier for users of mobile

phone banking. The people who are not interested in using mobile phone banking perceived

mobile phone banking to be costly. People at the BOP will adopt mobile phone banking when it

is perceived to be affordable. The results show that people at the BOP (Bottom of Pyramid) will

adopt mobile phone banking services when the mobile service providers (both the banks and

mobile network provider) are perceived to be trustworthy. Customer’s trust of mobile service

providers has a direct effect on the customer’s loyalty. Trust has a negative significant

correlation with perceived risk, and trust can play a role in mitigation of risk. The results show

perceived risk had no effect on the adoption of mobile banking services by the Bottom of

Pyramid.

In summary, most of these studies have been conducted in developed countries and used

questionnaire for data collection. Moreover the effects of demographic variables such as race,

age, gender and culture on adoption of mobile banking was not intensively explored. Some

demographic variables may have indirect interrelation effects between the variables. In other

23

words the cognitive propensity of individuals to risk differs across culture. This means that the

customers’ acceptance of mobile phone banking may be influenced by cultural differences. It

would be of interest to explore the geographic effect, such as in rural areas, where it takes much

longer and is more costly to access the nearest banking facilities. Therefore this research will use

both quantitative (questionnaire) and qualitative (interviews) approaches to examine the factors

affecting the adoption of mobile phone banking in Tanzania banking sector - case of CRDB in

Mwanza city.

24

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

This chapter outlines the method that will be used for the study and adopts the following

structure: research design, area of study, target population, sampling and sampling techniques,

source of data and data collection methods, data analysis, ethical consideration and conclusion.

3.2 Research Design

Research design is the conceptual structure within which research is conducted; it constitutes the

blue print for the collection, measurement and analysis of data (Kothari,2006).There are three

different types of case study depending on the nature and purpose of the study, namely:

exploratory, descriptive and casual.

Exploratory research design is suitable for exploratory studies whose main emphasis is to

formulate a problem for precise investigation or developing a working hypothesis from an

operational point of view. The major emphasis is on the discovery of ideas and insight; as such

the research design appropriate for such studies must be flexible to consider different aspects of a

problem (Saunders, et.al, 2000)

In descriptive research design, the major emphasis is on determining the frequency with which

something occurs or the extent to which two variables co vary. It is typically guided by an initial

hypothesis (Churchill, 2000).Descriptive studies are also concerned with specific predictions,

narrations of facts and characteristics concerning individuals, groups or situation.

While Causal research design is suitable for studies whose major emphasis is on determining

causal and effect relationship. Causal studies typically take the form of experiments, since

experiments are best suited to determine cause and effect.

This study will employ a descriptive type of design because a descriptive study pre-supposes

much prior knowledge about the phenomenon being studied. Another reason is that in descriptive

25

studies, the researcher must be able to define clearly as to what he want to measure and must find

adequate methods for measuring it.

3.3 Geographic Area of the Study

The study will be conducted in Mwanza region at one of the big branch of CRDB bank located

along Kenyatta road in Mwanza (Mwanza branch). The study will also be conducted at three

other branches of the bank namely; Nyerere, Nyanza and Bugando composing of customers from

both eight Districts of Mwanza Region. The study will mainly focus on the Customer Care

Department of the bank in order to establish factors affecting the adoption of mobile phone

banking for CRDB Bank customers. This area is chosen by the researcher because it is more

convenient in terms of financial constraints.

3.4 Target population

According to Zikmund (2003, p. 369) a population is any complete group of people, companies,

hospitals, stores, college students or the like that share some set of characteristics. . According to

the Internal Annual Report of CRDB Bank Plc, there are 1,314,000 customers for 71 Branches in

Tanzania, where Mwanza is having about 30,517customers. For the purposes of this study, the

population is estimated to be 20,000 customers, but only 300 customers have adopted the mobile

phone banking service in CRDB Bank Plc in Mwanza region .

3.5 Sample Size

Sample size refers to the specific size of the group or groups being studied in your research. The

intended sample size is the number of participants planned to be included in your study. This

number is not arbitrary and sample size is usually determined by using a power analysis

(Zikmund, 2003). The achieved sample size is the number of participants that are actually

enrolled in or complete the study. Generally, the larger the sample size, the more reliable the

study results are, and the more likely it is that the results can be generalized to other people.

Sample size is an important feature of any empirical study in which due to constraints on time

and resources, researcher will not be able to cover the entire population.

26

Three criteria usually will need to be specified to determine the appropriate sample size: the level

of precision, the level of confidence or risk and the degree of variability in the attributes being

measured ( Milaoulis and Michener, 1976).

There are several approaches to determining the sample size. One approach is to use the entire

population as the sample only when it is less than 100 units, although cost considerations make

this impossible for large populations. Another approach is to use statistical or published tables

which provides the sample size for given set of criteria, if this assumption cannot be met then the

entire population may need to be surveyed (Bartlett, Kotrlik & Higgins, 2001) A third way is

using formulas ,where there are formulas for finite population and infinite population. Taking

cost and time into consideration (Yamane, 1967 p.886) provides a simplified formula to calculate

sample sizes, as follows:

n = N/ 1+N(e)2

Equation 3.5

Where; n = sample size,

N= the population size, and

e = is the level of precision if 5%, e = 0.05

A random sample on the other hand is defined by Huysamen (1994:39) as a drawing process in

which each member of the population has equal chance of being part of the sample and each

sample of any size has the same chance of being chosen.

In this study the Yamane formula was used to determine the sample size of 171 respondents from

the population of 300 customers who adopted the mobile phone banking services in Mwanza

region.

3.6 Sampling techniques

Sampling methods are like models which guide researchers on a step by step fashion to conduct

sampling. These methods are divided into two broad categories: probability sampling and non

probability sampling. Probability sampling is that for each sampling unit of the population you

27

can specify the probability that the unit will be included in the sample. In the simplest case all

the units have the same probability of being included in the sample. In non – probability

sampling, there is no way of specifying the probability of each unit’s inclusion in the sample, and

there is no assurance that every unit has some chance of being included. The researcher uses the

subjective methods such as personal experience, convenience, expert judgment and so on to

select the elements in the sample. (Frankfort and Nachmias, 1996).

According to Doherty (1994) Probability sampling includes the following

(i) Simple random sampling: Elements are chosen at random so that each element has an

equal chance of selection. For example, elements are chosen from a hat or ideally, from a

table of random numbers in a statistics textbook. They can also be generated by

computer.

(ii) Systematic sampling: The first element is chosen at random. Subsequent elements are

chosen using a fixed interval (e.g., every tenth element) until you reach the desired

sample size.

(iii)Stratified sampling: The population to be sampled is divided into homogenous groups

based on characteristics you consider important to the indicators being measured, such as

youth that are sexually active. A simple random or systematic sample is then chosen from

each group.

(iv) Cluster sampling: First, a simple random sample of clusters is chosen from a sampling

frame. Examples of clusters are schools, health facilities and youth clubs. Then, a simple

random sample of individuals within each cluster is selected.

(v) Multi-stage sampling: This is like cluster sampling, but with several stages of sampling

and sub-sampling. This method is usually used in large-scale population surveys.

And Non probability sampling includes:

(i) Convenience sampling: A sample is drawn on the basis of opportunity. For example, the

sample could include youth attending a school activity, service providers attending a

conference or parents attending a school event.

(ii) Quota sampling: A sampling frame is defined in advance of data collection and a sample

is chosen from this list, but not at random.

(iii)Snowball sampling: Data is collected from a small group of people with special

characteristics, who are then asked to identify other people like them. Data is collected

28

from these referrals, who are also asked to identify other people like them. This process

continues until a target sample size has been reached, or until additional data collection

yields no new information. This method is also known as network or chain referral

sampling.

According to Neuman, (2000), the simple random sampling method is the easiest method of

sampling on which other types are modeled. In this simple random sampling, a researcher

develops an accurate sampling frame; select elements from the sampling frame then allocate the

exact element that was selected for inclusion in the sample.

In this study the researcher utilized the simple random sampling method by obtaining a list of

customers and Personnel of CRDB Bank in Mwanza region who are mobile phone users and

then select randomly two respondents from each strata by the procedure of lottery. The selected

persons are included in a sample.

3.7 Sources of Data and Data Collection Instruments

3.7.1 Sources of data

According to Krishnaswami, (2003) the sources of data may be classified into two categories,

primary sources and Secondary sources.

(i) Primary Data

Primary sources are original sources from which the researcher directly collects data which have

not been previously collected. Thus primary data are data collected by the researcher from the

field. This is the first hand information. Observation, questionnaire and interview are common

research tools used to collect primary data. In this study data will be collected by using Interview

and Questionnaires distributed to respondent.

(ii) Secondary Data

Secondary sources are sources containing of data that had been collected from sources,

interpreted and compiled. Thus secondary data are those data obtained from the literature reports

and statements sources, these are the data that have already been collected by other people for

some other purposes. They are second hand information used by the researcher. Secondary data

29

include both raw data and publish one (Saunders et al, 2000).In this study secondary data will

come from official records regarding budgeting.

The methods of collecting primary and secondary data differ since primary data are to be

originally collected, while in case of secondary data the nature of collection work is merely that

of compilation. (Kothari, 2004). During the study both primary and secondary data collection

methods will be used. Primary data collection methods that will be used include questionnaires

and interviews. Secondary data collection methods that will be used is documentary review.

3.7.2 Data Collection Instruments

In this study primary data is collected through questionnaires and interviews while secondary

data was collected through documentary review.

( i) Questionnaire

A questionnaire is a set of questions which are usually sent to the selected respondents to answer

at their own convenient time and return back the filled questionnaire to the researcher (Kothari,

2004). The reasons for using questionnaires are that they cover large sample at low cost, and they

are free from bias. Both closed- ended and open- ended questions in English language will be

used because of the unavailability of many technological words in Swahili grammar like mobile

banking. The questionnaire will can be used to produce large quantities of structured data which

is about basic socio- biographical information covering age, sex, income, educational

background of the CRDB Bank customers. Appendix A shows the details of the questionnaire

used for this study.

( ii ) Interview

Interview is also a tool of data collection that involves presentation of oral verbal and then

obtaining response from the respondent. This method will be conducted through personal

interview and if possible telephone interviews (Kothari, 2004).This method will be used

specifically for the key informants who cannot express their responses in written language.

Since the topic involves seeking information from CRDB Bank customers and personnel it will

use unstructured interviews since it enable to get relevant information without restriction, more

clarification about the issue from the respondent and respondent understands the question

30

properly. Respondents were taped during the interviews for richer research access to the

discussion.

( iii ) Documentary Review

These are written material that contains information relevant to mobile banking. Hence various

documents will be examined such as books, journals, verbal communication and other supporting

documents that will assist to make up findings of the study.

3.8 Data Analysis

Data analysis in simple terms, it is the process of checking and counting the frequency and

distribution of a phenomenon under investigation (May, 2001). Data for this research were both

in quantitative and qualitative nature and as such, their analysis were conducted along the

quantitative and qualitative frames of reference.

(i) The Quantitative Data Analysis

The quantitative data analysis is intended to inform the study about the statistical position of the

problem and about what is available to address it. Quantitative data collected for this study were

summarized into frequency distributing, figures, graphs, tables and percentages.

Punch, (2000) admits that the quantitative data analysis involves statistics. This means that data

are reflected in the numerical values and are also summarized into diagrams and tables.

In this study, the quantitative data analysis method was utilized to analyze data which were

obtained through the content analysis and the first part of both the questionnaires and interviews.

(ii) The Qualitative Data Analysis

Qualitative data are difficult to analyze. The major thrust of the analytic technique recommended

for use during data collection was data reduction; seeking to make the data mountain manageable

through summary and coding (Robson, 1993).

31

In order to easy the problem of complexity of analyzing the qualitative data, this study utilized

the process which was contributed by Creswell (1998).

Phase I: The researcher’s own experience of the phenomenon

In this regard, the researcher own experience of the problem was obtained from relevant

literature regarding factors influencing the adoption of mobile phone banking..

Phase II: The statement by the respondents about the phenomenon

This means what the respondents said when they were exposed to the questionnaire about the

mobile banking

Phase III: The grouping of the statements

This is called the categorization of the information wherein the researcher continues to look for

similar themes of the context and group them in their respective categories. In this way similar

responses were reflected in the tables so that they could be easily measurable.

Phase IV: seeking the convergent and the divergent perspectives about the phenomenon

This step required the researcher to relate categories to the perspective or the objective of the

mobile banking adoption in order to identify the supporting and non supporting statements. This

was easily achieved through colouring with different markers.

3.9 Reliability and Validity of Research Design

(i) Reliability

Reliability can be defined as the degree to which measurements are free from error and therefore

yield consistent results. Operationally, reliability is defined as the internal consistency of a scale

which assesses the degree to which the items are homogeneous (Easteby-smith et al., 1991).

Reliability can be assessed by the following questions

i. Will the measure yield the same result on other occasions?

ii. Will similar observation be reached by other observers?

32

iii. Is there transparency in how sense was made from raw data?

In order to ensure there is reliability of data in this study, uniform questionnaire will be used to

collect data for all the respondents, before conducting the main survey, a pre-testing (pilot study)

was conducted on the questionnaire. According to Zikmund (2003, p. 359), a pre-testing study

provides an opportunity for the researcher to determine whether the respondents had any

difficulty understanding the questionnaire. The pre-test affords an opportunity to check whether

there are any ambiguous or biased questions. Moreover, all the collected data about this research

is processed and analyzed uniformly.

(ii) Validity

Validity is concerned with whether the findings are really about what they appear to be about.

Validity is defined as the extent to which data collection methods accurately measure what they

were intended to measure ( saunders and thornhill, 2003).

In research, validity has two essential parts: internal and external. Internal validity encompasses

whether the results of the study (e.g. mean difference between treatment and control groups) are

legitimate because of the way the groups were selected, data was recorded or analysis performed.

For example, a study may have poor internal validity if testing was not performed the same way

in treatment and control groups or if confounding variables were not accounted for in the study

design or analysis. External validity, often called “generalizability”, involves whether the results

given by the study are transferable to other groups (i.e. populations) of interest (Last, 2001). In

this study researcher maximized reliability and validity of the research findings.

33

3.10 Ethical Considerations

This research as an academic or professional setting has taken into consideration the following to

address the ethical matters in a research process:

Ethical approval of the research was granted by the letter from the director of postgraduate

studies at St. Augustine University of Tanzania before the commencement, also obtained

permission of the CRDB Bank Plc to conduct research that is involving them.

Confidentiality is constantly maintained so that it would not cause either physical or emotional

harm to the respondents, with more emphasize on being careful when asking questions during

interviews. It does not take the responses out of the context.

Fair consideration is given when objectivity and subjectivity is involved in this research and not

taking advantage of easy access of group of people simply because of easy to access as this may

make choice of the subject not benefit this research.

Results obtained are accurately presented what was actually obtained or what were told and the

subjects should know whether research results will be anonymous or not.

When all ethics are adhered accordingly, it will make the researcher to receive primary data

accurately and hence enable to make analysis and findings of the study.

3.11 Problems and Limitations in the Research

Whilst every effort made by the researcher to make this study as comprehensive as possible

certain limitations and problems were present:

Questionnaires was designed in English language and focused on users who are inexperienced or

one time users of mobile banking who found the questions difficult to understand hence answers

of these questions may be inaccurately.

The number of respondents was lower than was hoped for, because of difficulty in advertising

the questionnaire due to this, the results are less statistically significant.

34

This study will be carried out for a short period of time because the requirement is to do so as to

follow the deadline of the academic calendar of St.Augustine University of Tanzania. Time

constraint may affect both, the quality and quantity of the data collected during the study.

Lack of adequate funds for conducting the study may affect the quality and quantity of data

collected during the study. This may hamper the researcher to conduct the study effectively.

Local empirical literature on factors affecting customer services in the banking sector in

Tanzania is lacking. As a result, the researcher will have to use literature from other sources

countries.

35

CHAPTER FOUR

DATA ANALYSIS AND DISCUSSION OF FINDING

4.1 Introduction

This chapter analyses the responses and represents the research findings from the data collected

from the survey. The data collected is ordinal, quantitative and numerical, thus data analysis is

based on a quantitative method. The outputs are generated using the SPSS package.

The chapter aims to access the factors influencing the adoption of mobile phone banking by

customers in Mwanza city. The following research objectives guided the investigation and they

form the leasis for presentation and discussions of the collected findings: to establish the profile

of mobile phone banking users in CRDB Bank at Mwanza city, to examine how customers at the

bank perceive risks in relation to mobile phone banking in Mwanza city, to establish what

influences CRDB Bank customers to trust mobile banking in Mwanza city, to determine how

perceived usefulness and perceived ease of use influence the adoption of mobile banking at

CRDB Bank in Mwanza city .

This chapter therefore presents the finding of the study, gives a discussion of finding and makes

inferences leased on the findings regarding their contribution to the researcher problem. The

chapter is structured as follows. First, the background information of the respondents is given.

This includes personal information relating to category of respondents, age, gender, educational

level, occupation and income level. Next, data relating to specific research objectives is given

and the discussion of the findings is presented. The chapter closes with overall summary from

research objectives / questions.

36

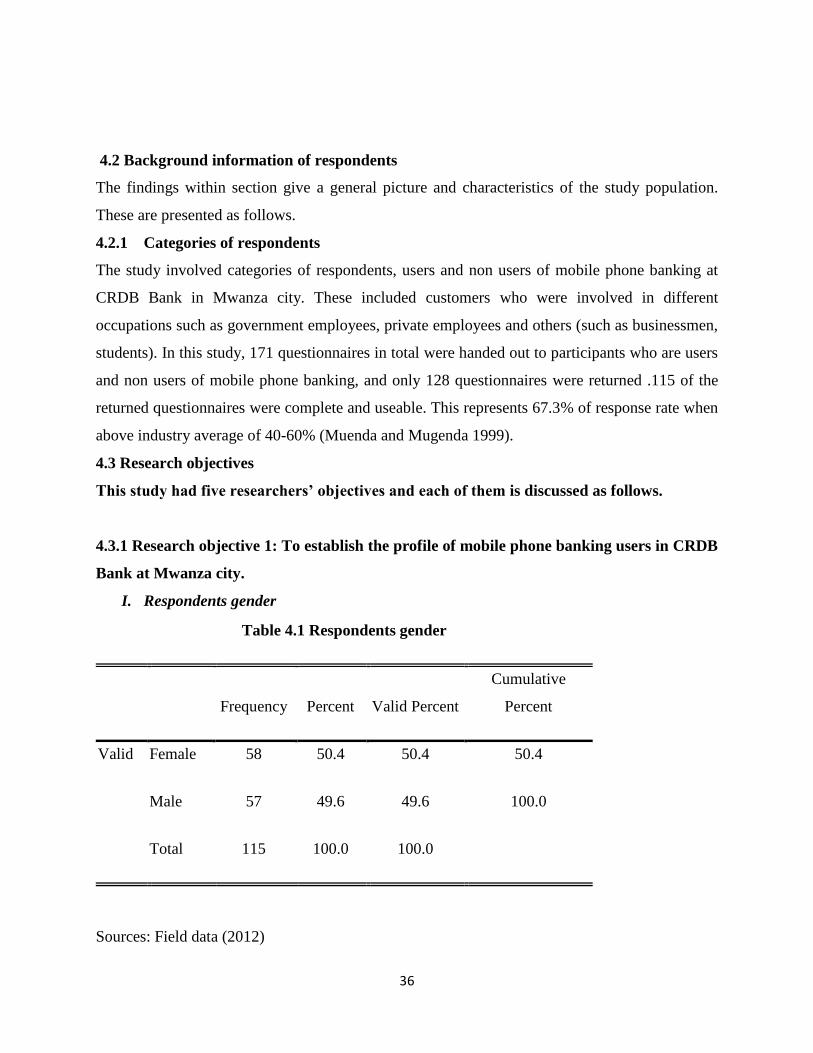

4.2 Background information of respondents

The findings within section give a general picture and characteristics of the study population.

These are presented as follows.

4.2.1 Categories of respondents

The study involved categories of respondents, users and non users of mobile phone banking at

CRDB Bank in Mwanza city. These included customers who were involved in different

occupations such as government employees, private employees and others (such as businessmen,

students). In this study, 171 questionnaires in total were handed out to participants who are users

and non users of mobile phone banking, and only 128 questionnaires were returned .115 of the

returned questionnaires were complete and useable. This represents 67.3% of response rate when

above industry average of 40-60% (Muenda and Mugenda 1999).

4.3 Research objectives

This study had five researchers’ objectives and each of them is discussed as follows.

4.3.1 Research objective 1: To establish the profile of mobile phone banking users in CRDB

Bank at Mwanza city.

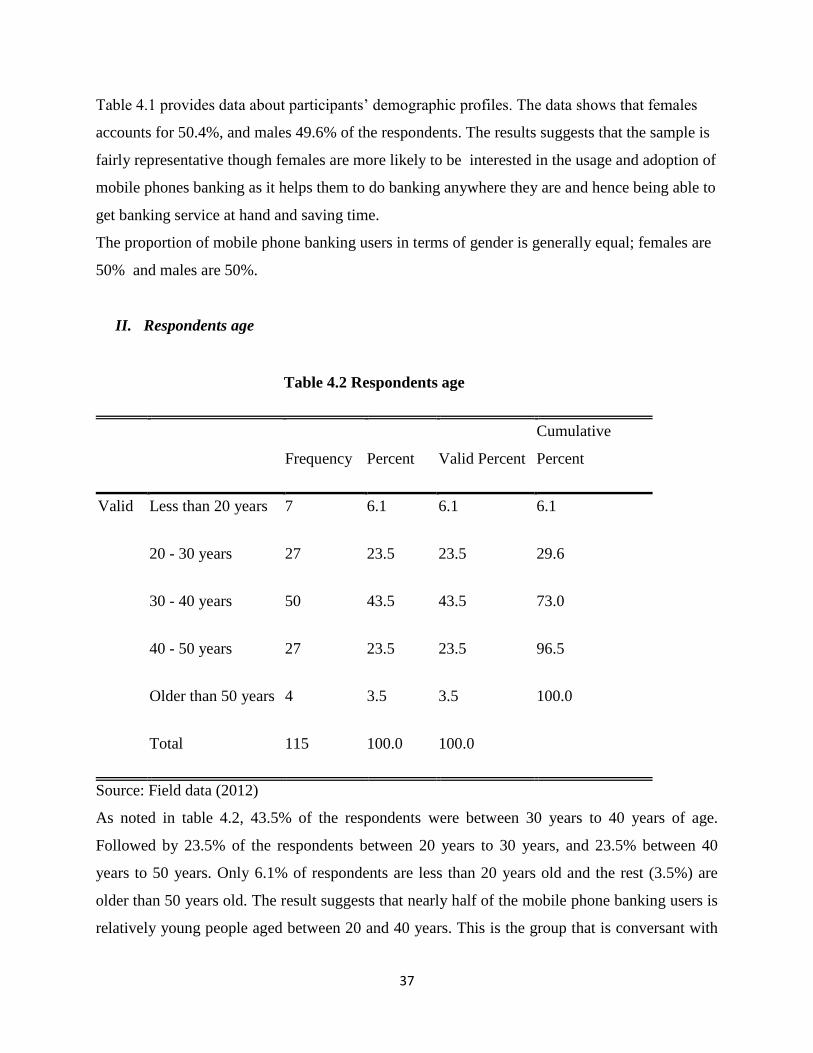

I. Respondents gender

Table 4.1 Respondents gender

Frequency Percent Valid Percent

Cumulative

Percent

Valid Female 58 50.4 50.4 50.4

Male 57 49.6 49.6 100.0

Total 115 100.0 100.0

Sources: Field data (2012)

37

Table 4.1 provides data about participants’ demographic profiles. The data shows that females

accounts for 50.4%, and males 49.6% of the respondents. The results suggests that the sample is

fairly representative though females are more likely to be interested in the usage and adoption of

mobile phones banking as it helps them to do banking anywhere they are and hence being able to

get banking service at hand and saving time.

The proportion of mobile phone banking users in terms of gender is generally equal; females are

50% and males are 50%.

II. Respondents age

Table 4.2 Respondents age

Frequency Percent Valid Percent

Cumulative

Percent

Valid Less than 20 years 7 6.1 6.1 6.1

20 - 30 years 27 23.5 23.5 29.6

30 - 40 years 50 43.5 43.5 73.0

40 - 50 years 27 23.5 23.5 96.5

Older than 50 years 4 3.5 3.5 100.0

Total 115 100.0 100.0

Source: Field data (2012)

As noted in table 4.2, 43.5% of the respondents were between 30 years to 40 years of age.

Followed by 23.5% of the respondents between 20 years to 30 years, and 23.5% between 40

years to 50 years. Only 6.1% of respondents are less than 20 years old and the rest (3.5%) are

older than 50 years old. The result suggests that nearly half of the mobile phone banking users is

relatively young people aged between 20 and 40 years. This is the group that is conversant with

38

technology and hence more likely to be interested with mobile phone banking. Thus should focus

on this age group.

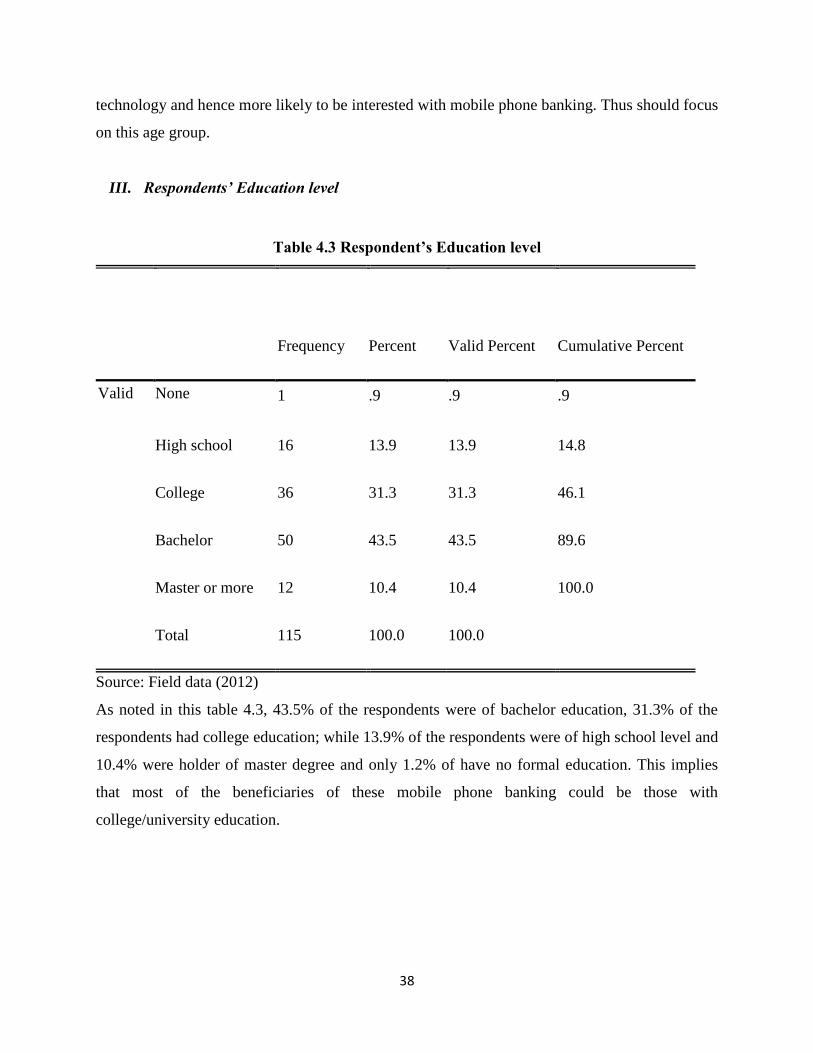

III. Respondents’ Education level

Table 4.3 Respondent’s Education level

Frequency Percent Valid Percent Cumulative Percent

Valid None 1 .9 .9 .9

High school 16 13.9 13.9 14.8

College 36 31.3 31.3 46.1

Bachelor 50 43.5 43.5 89.6

Master or more 12 10.4 10.4 100.0

Total 115 100.0 100.0

Source: Field data (2012)

As noted in this table 4.3, 43.5% of the respondents were of bachelor education, 31.3% of the

respondents had college education; while 13.9% of the respondents were of high school level and

10.4% were holder of master degree and only 1.2% of have no formal education. This implies

that most of the beneficiaries of these mobile phone banking could be those with

college/university education.

39

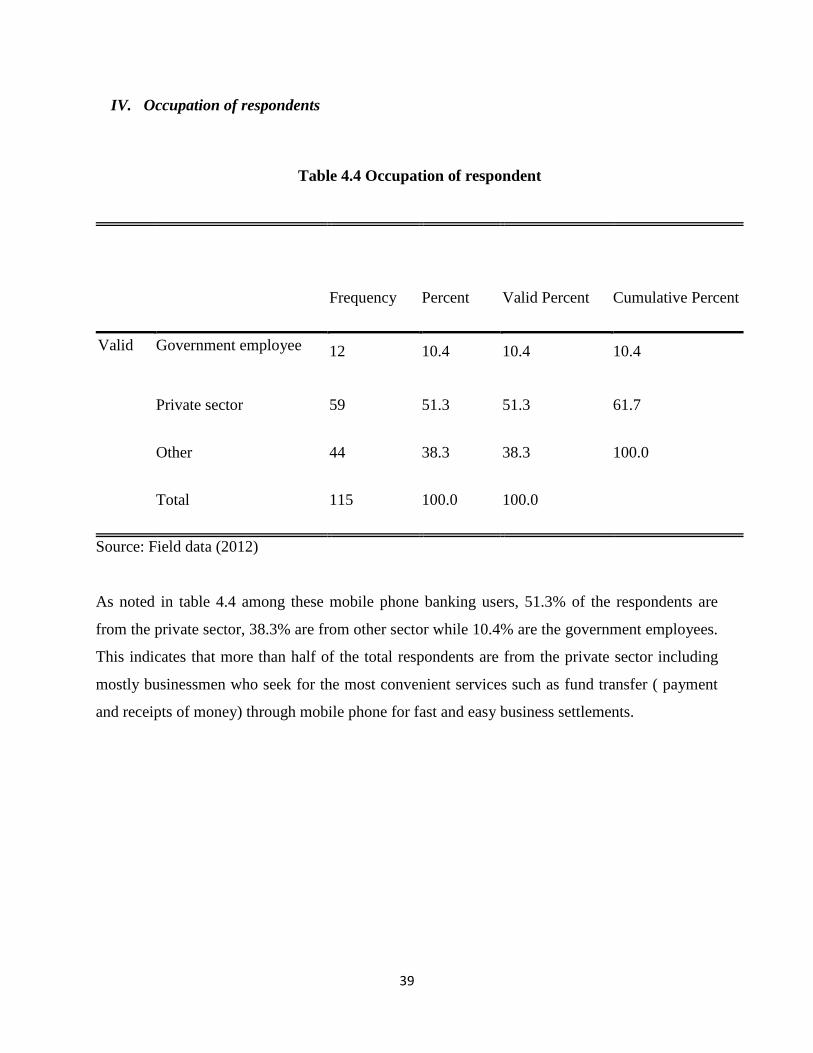

IV. Occupation of respondents

Table 4.4 Occupation of respondent

Frequency Percent Valid Percent Cumulative Percent

Valid Government employee 12 10.4 10.4 10.4

Private sector 59 51.3 51.3 61.7

Other 44 38.3 38.3 100.0

Total 115 100.0 100.0

Source: Field data (2012)

As noted in table 4.4 among these mobile phone banking users, 51.3% of the respondents are

from the private sector, 38.3% are from other sector while 10.4% are the government employees.

This indicates that more than half of the total respondents are from the private sector including

mostly businessmen who seek for the most convenient services such as fund transfer ( payment

and receipts of money) through mobile phone for fast and easy business settlements.

40

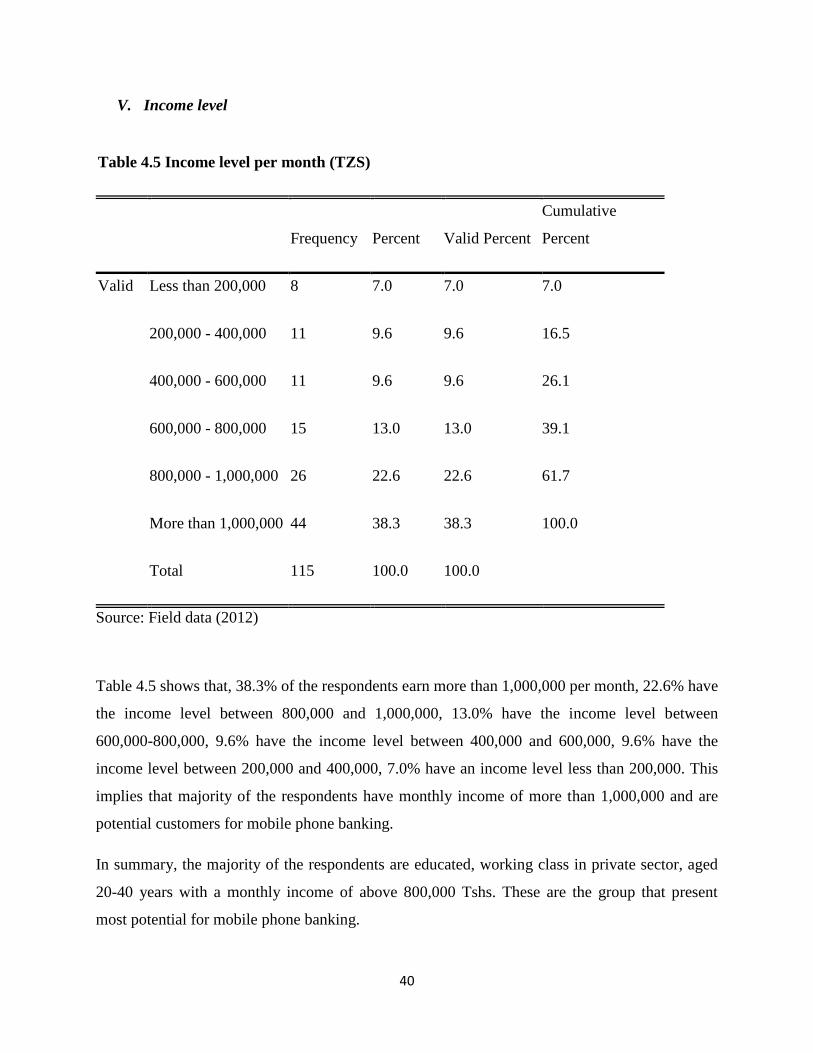

V. Income level

Table 4.5 Income level per month (TZS)

Frequency Percent Valid Percent

Cumulative

Percent

Valid Less than 200,000 8 7.0 7.0 7.0

200,000 - 400,000 11 9.6 9.6 16.5

400,000 - 600,000 11 9.6 9.6 26.1

600,000 - 800,000 15 13.0 13.0 39.1

800,000 - 1,000,000 26 22.6 22.6 61.7

More than 1,000,000 44 38.3 38.3 100.0

Total 115 100.0 100.0

Source: Field data (2012)

Table 4.5 shows that, 38.3% of the respondents earn more than 1,000,000 per month, 22.6% have

the income level between 800,000 and 1,000,000, 13.0% have the income level between

600,000-800,000, 9.6% have the income level between 400,000 and 600,000, 9.6% have the

income level between 200,000 and 400,000, 7.0% have an income level less than 200,000. This

implies that majority of the respondents have monthly income of more than 1,000,000 and are

potential customers for mobile phone banking.

In summary, the majority of the respondents are educated, working class in private sector, aged

20-40 years with a monthly income of above 800,000 Tshs. These are the group that present

most potential for mobile phone banking.

41

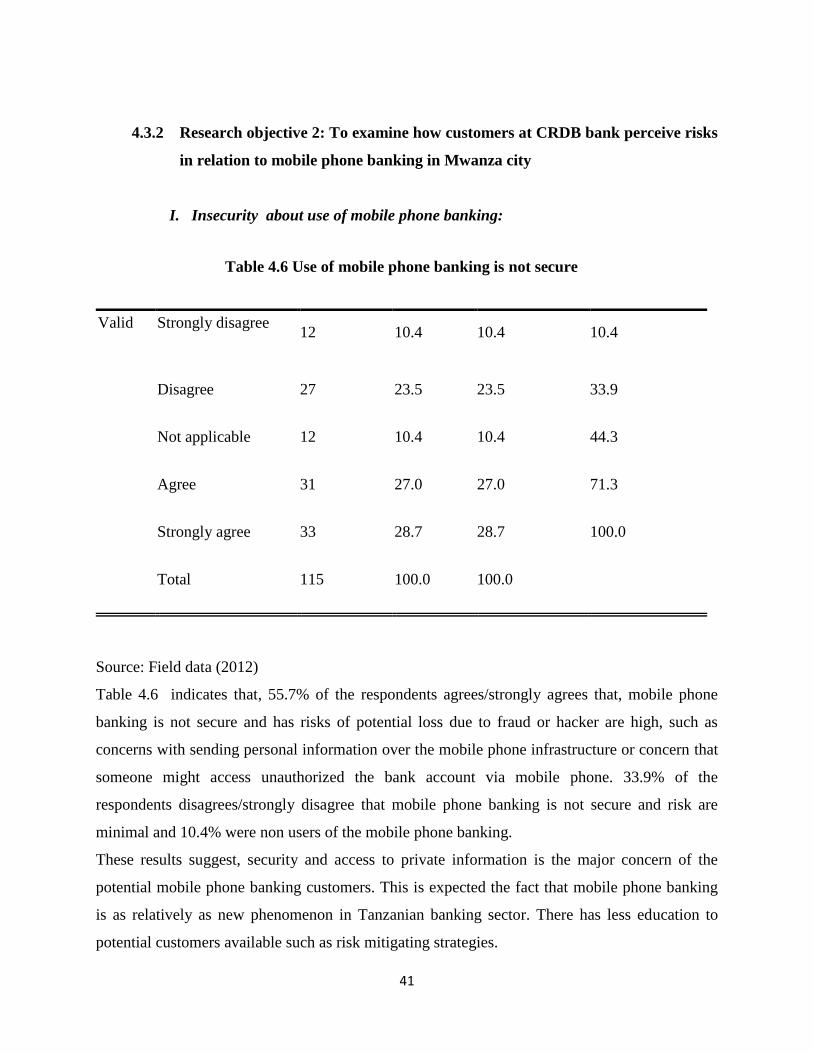

4.3.2 Research objective 2: To examine how customers at CRDB bank perceive risks

in relation to mobile phone banking in Mwanza city

I. Insecurity about use of mobile phone banking:

Table 4.6 Use of mobile phone banking is not secure

Valid Strongly disagree 12 10.4 10.4 10.4

Disagree 27 23.5 23.5 33.9

Not applicable 12 10.4 10.4 44.3

Agree 31 27.0 27.0 71.3

Strongly agree 33 28.7 28.7 100.0

Total 115 100.0 100.0

Source: Field data (2012)

Table 4.6 indicates that, 55.7% of the respondents agrees/strongly agrees that, mobile phone

banking is not secure and has risks of potential loss due to fraud or hacker are high, such as

concerns with sending personal information over the mobile phone infrastructure or concern that

someone might access unauthorized the bank account via mobile phone. 33.9% of the

respondents disagrees/strongly disagree that mobile phone banking is not secure and risk are

minimal and 10.4% were non users of the mobile phone banking.

These results suggest, security and access to private information is the major concern of the

potential mobile phone banking customers. This is expected the fact that mobile phone banking

is as relatively as new phenomenon in Tanzanian banking sector. There has less education to

potential customers available such as risk mitigating strategies.

42

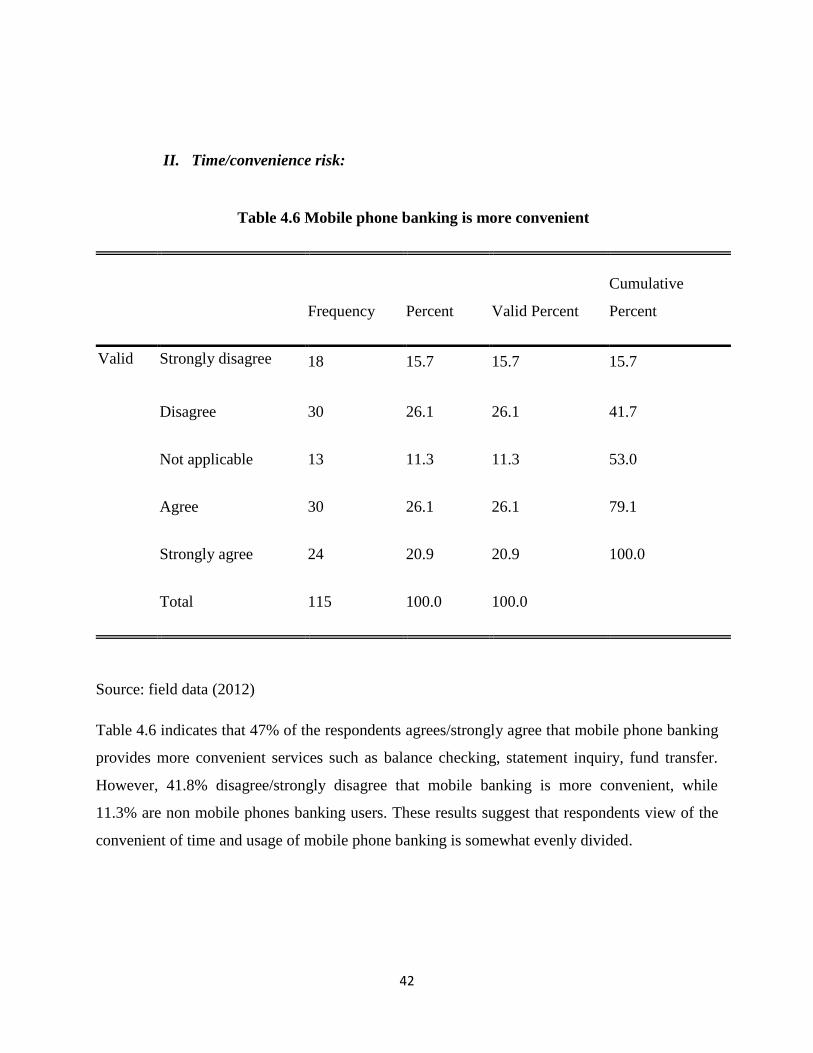

II. Time/convenience risk:

Table 4.6 Mobile phone banking is more convenient

Frequency Percent Valid Percent

Cumulative

Percent

Valid Strongly disagree 18 15.7 15.7 15.7

Disagree 30 26.1 26.1 41.7

Not applicable 13 11.3 11.3 53.0

Agree 30 26.1 26.1 79.1

Strongly agree 24 20.9 20.9 100.0

Total 115 100.0 100.0

Source: field data (2012)

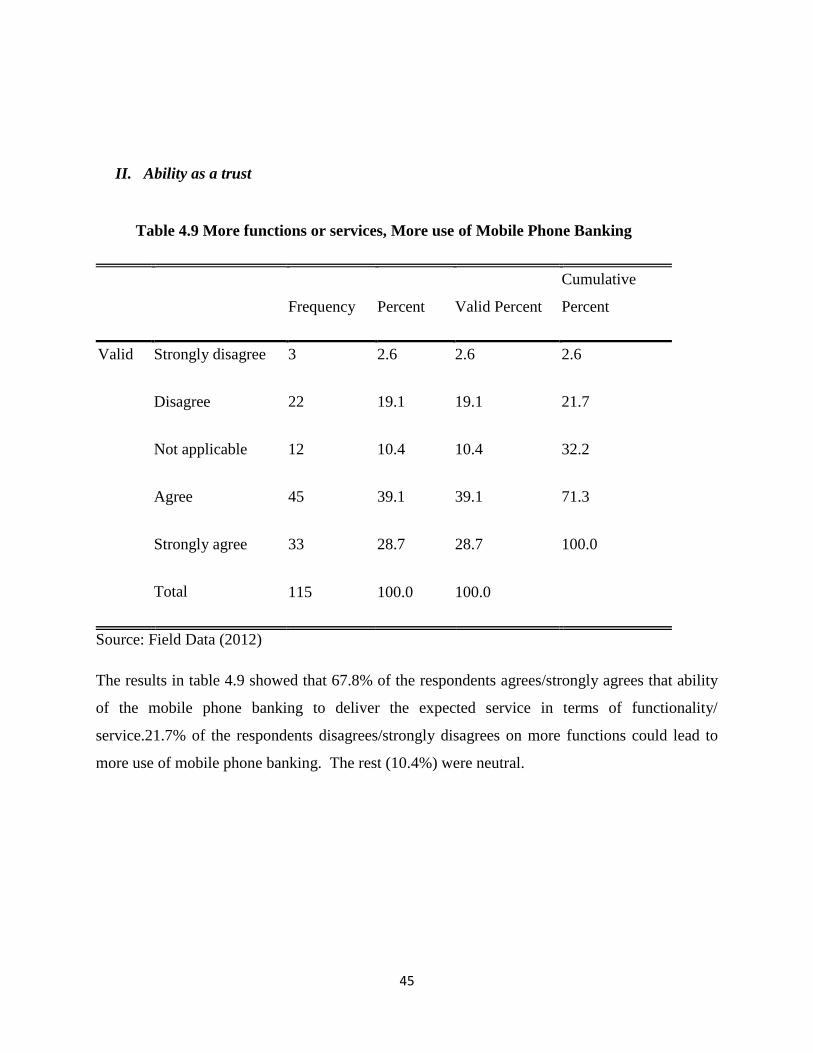

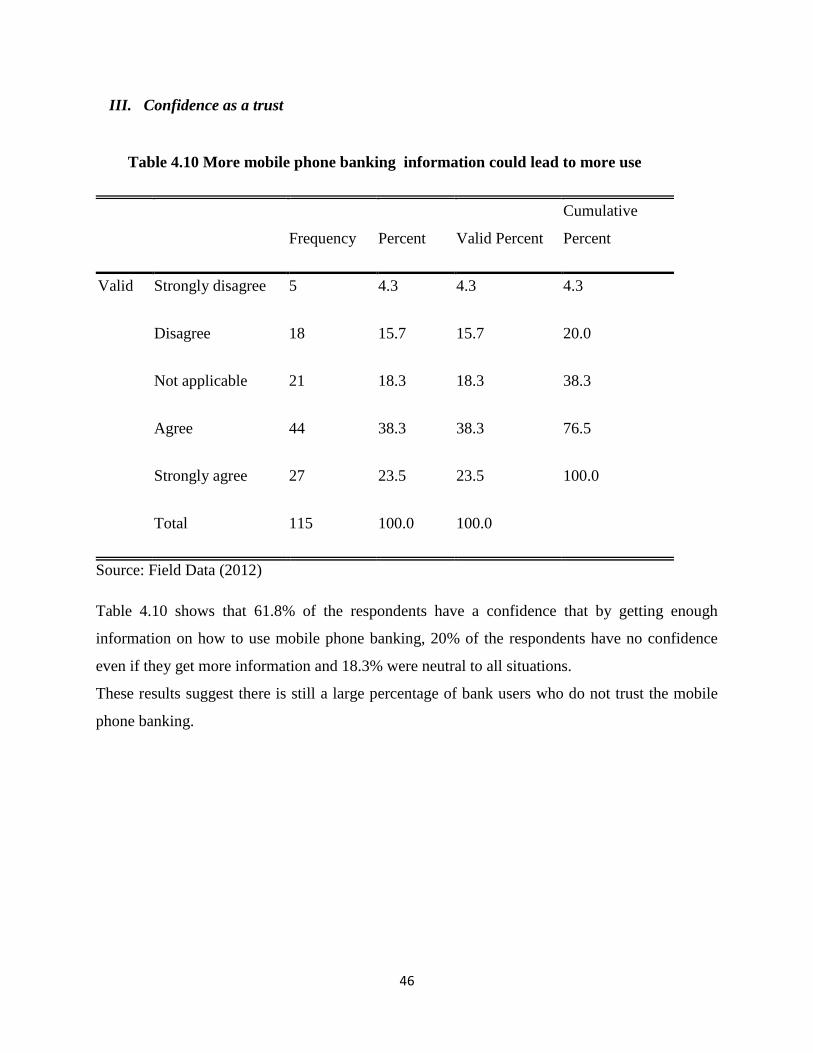

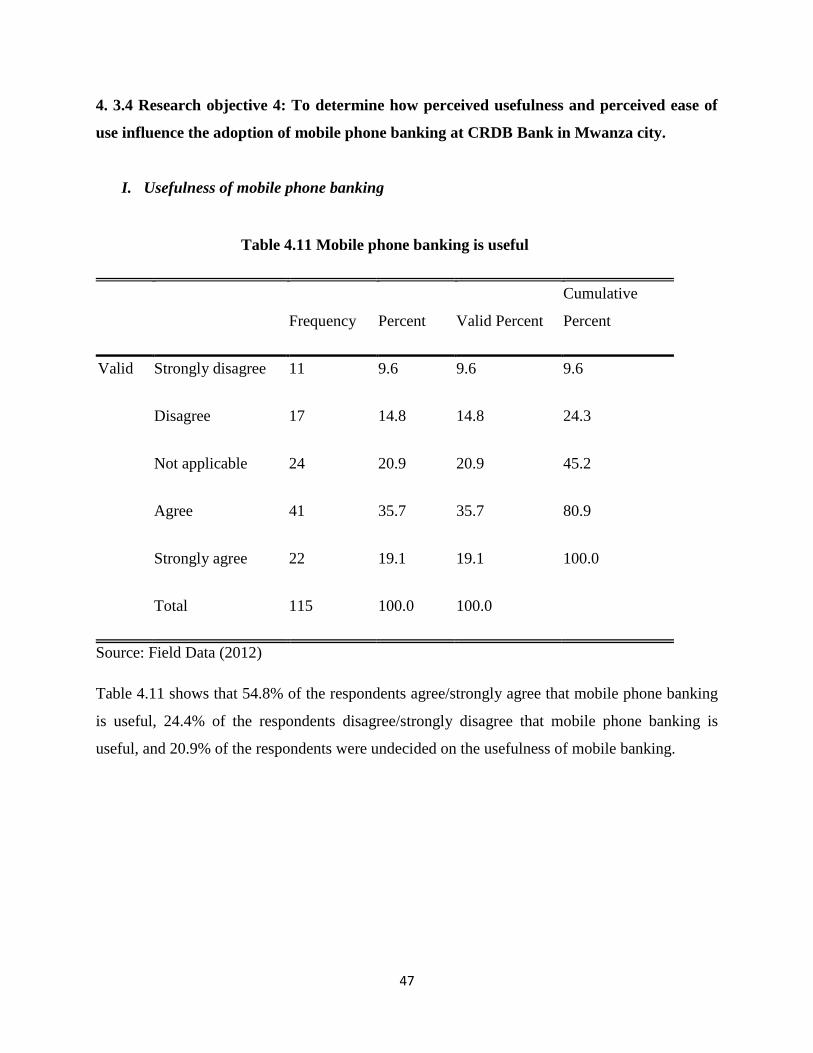

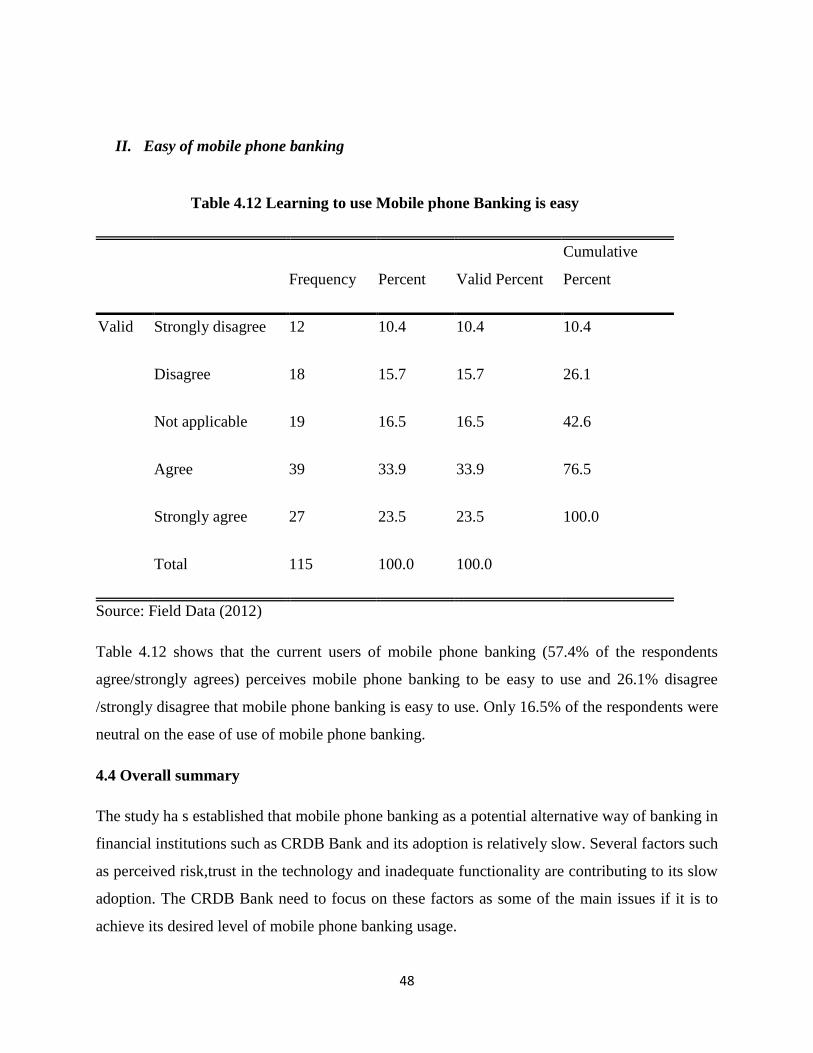

Table 4.6 indicates that 47% of the respondents agrees/strongly agree that mobile phone banking