SAHULAT A Journal of Interest Free Microfinance 5 Contributors Dr. Waquar Anwar Dr. Rafiquz Zaman Dr. Magda Ismail Abdel Mohsin Datuk Syed Othman Alhabshi Zainab Fida Ahsan Shri Bhagat Nin Dr. Narwade Sunil Mamata Patra Dr Radhakrushna Panda Harasankar Adhikari Dr Seema P. Salgaonkar Vol. 4 June 2016 No. 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Regd. No. : DELENG/2012/43962

SAHULATA Journal of Interest Free Microfinance

International Board of Advisors

M. Najatullah Siddiqi M. Umer ChapraIndia and USA Saudi ArabiaFormer Professor of Economics Research AdvisorKAAU, Jeddah, Saudi Arabia Islamic Development Bank, Jeddah

Zubair Hasan Mabid al JarhiMalaysia UAEProfessor of Economics Dubai Islamic Bank, UAEINCIEF, Kaula Lumpur, Malaysia

M. Obaidullah Rodney WilsonSaudi Arabia UKIslamic Development Bank, Jeddah Professor, Durham University, UK

Shashi Bhushan Waquar AnwarIndia IndiaNandi Foundation JIH, Delhi, Hyderabad, India India

Editor Najmul Hoda

Assistant Editor Mridu Kamal

Sahulat Microfinance Society Regd. Office: E-89, Darussalam Building, Flat No- 403, Near Hari Kothi, Alshifa Hospital Road, Abul Fazal Enclave Part-1, Jamia Nagar, Okhla, New Delhi-110025 (India)

` 150/-

SAHULATA Journal of Interest Free Microfinance

5Contributors

Dr. Waquar Anwar

Dr. Rafiquz Zaman

Dr. Magda Ismail Abdel Mohsin

Datuk Syed Othman Alhabshi

Zainab Fida Ahsan

Shri Bhagat Nitin

Dr. Narwade Sunil

Mamata Patra

Dr Radhakrushna Panda

Harasankar Adhikari

Dr Seema P. Salgaonkar

Vol. 4 June 2016 No. 1

Guidelines for Authors

A Journal of Interest Free Microfinance is a research based refereed journal. To begin with, it is published twice a year – in January and June. It is brought out by the Sahulat Microfinance Society, New Delhi, India. Sahulat welcomes contributions from all interested scholars all over the world. The areas of special interest for the journal are: Economic Development of Minorities; Poor People and Economically Weaker Sections of the Society; Financial Sector; Co-operative Effort and Co-operative Movement; Commercial Banking; Interest Free Finance; Microfinance and Interest Free Microfinance. The sole purpose of the journal is to encourage free and frank discussion on the issues of concern in these areas so as to develop them as scientific disciplines.

The manuscripts submitted for publication should be typed double spaced. The manuscripts may be submitted in duplicate or through email. If submitted by mail, soft copy may also be sent on a compact disc. No bibliographical reference should be inserted within the text. Instead, all references must be cited at the end of the text as end notes, which should be consecutively numbered. The style of citation in the end notes should be as follows:

Mehta, S. K., Mishra, H. G. and Singh, A. (2011). Role of Self-help Groups in Socio-Economic Change of vulnerable poor of Jammu Region. International Conference on Economics and Finance Research, IPEDR.4, 519-23.

Mummidi, T. (2009). Women and Income Generating Activities: Understanding Motivations by prioritizing Skill, Knowledge and Capabilities. RUME working paper series. Marseiiie, 1, 6-29.

When reference to the same work follows without interruption ibid followed by the page number may be used; when interrupted by other notes, author’s last name, short form of the title, and Op. Cit. followed by page number may be used. Tables, maps and diagrams may be placed appropriately within the text or numbered consecutively and placed in an appendix at the end of the article after the end notes.

The Editor reserves the right to make editorial revisions.

All correspondence relating to editorial matters may be addressed to [email protected]

Submission of an article for publication in this journal implies that it has neither been submitted elsewhere nor published. It is the policy of the Sahulat Journal not to republish the articles that have been published before. The books for review may be forwarded to the editor in duplicate. However, the books shall be reviewed in the order in which they have been received.

1

ISSN 2319-2941

SAHULATA Journal of Interest Free Microfinance

A Bi-annual Publication of Sahulat Microfinance Society devoted to scientific investigation of issues involved in the

development of poor people in India and abroad.

Editor Najmul Hoda

Assistant Editor Mridu Kamal

Sahulat Microfinance Society Regd. Office: E-89, Darussalam Building, Flat No- 403,

Near Hari Kothi, Alshifa Hospital Road, Abul Fazal Enclave Part-1, Jamia Nagar, Okhla,

New Delhi-110025 (India)

2

Sahulat: A Journal of Interest Free Microfinance is to provide a forum for academic dialogue in a spirit of free enquiry without indulging in personal insults and affronts. Accuracy of facts, responsibility of their interpretations, conclusions drawn and all other opinions expressed in the papers are the exclusive domain of authors. They do not necessarily reflect the view of the Journal, or its editor or the Sahulat Microfinance Society. All materials published in this Journal are accepted and published in good faith for academic dialogue and promotion of knowledge only. The Journal with its editor and other functionaries and Sahulat Microfinance Society bear no responsibility, whatsoever, in this connection.

3

In the name of ALLAHThe Most BeneficentThe Most Merciful

4

Printer and Publisher:Arshad Ajmal, on behalf of Sahulat Microfinance SocietyPrinted by : Drishti Printers, 9810529858, 9810277025 Printed at : Star Print o Bind, F-31, Okhla Industrial Area, Phase-1, New DelhiPublished from: E-89, Darussalam Building, Flat No- 403, Near Hari Kothi, Alshifa Hospital Road, Abul Fazal Enclave Part-1, Jamia Nagar, Okhla, New Delhi-110025 (India)

5

SAHULATA Journal of Interest Free Microfinance

Vol. 4 June 2016 No. 1

CONteNtSARtiCleSAlternative Interest Free Economic System: Dr. Waquar Anwar 11Goals, Challenges and Road Map

Co-operatives and the Need for their Dr. Rafiquz Zaman 23Growth in India

Hybrid Model of Zakah, Waqf, Dr. Magda Ismail A. Mohsin, 27Qard-Hassan & Islamic Finance for a Prof. Syed Othman AlhabshiJust and Sustainable Microfinance

The Role of Zakah and Awqaf in Zainab Fida Ahsan 47Community Development: Rules, Applications and Suggested Framework

CASe StUDYA Study of Socio-Economic Impact Shri Bhagat Nitin and 63of SHGs on Women from Dr. Narwade SunilMarginalised Social Groups

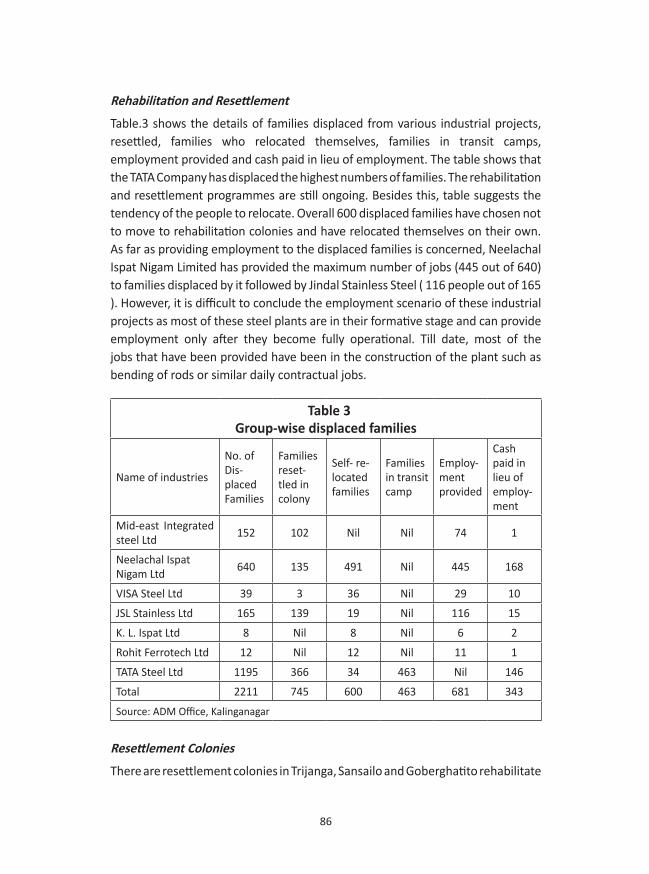

Industrialisation and Socio-Economic Mamata Patra 79Status Tribals: A Study of Kalinganagarin Odisha

Return on Investment of the Self Help Group Dr. Radhakrushna Panda 107Enabled Micro Enterprises in Odisha

Urban Affiliation and Wellbeing: Study Harasankar Adhikari 119of Female Domestic Workers of Kolkata

Women Entrepreneurship and Micro Dr. Seema P. Salgaonkar 133Finance: A Case study of Goa

6

CONtRiBUtORS tO tHe CURReNt iSSUe

Dr. Waquar AnwarFinancial Advisor, Jamaat-e-Islami Hind, Dawat Nagar, Abul Fazal Enclave - 1, Jamia Nagar, New Delhi, IndiaEmail: [email protected]

Dr. Rafiquz ZamanIAS (Rtd.) Vice Chancellor,Assam Rajiv Gandhi University of Co-operative Management, Sivasagar, Assam, India Email: [email protected]

Dr. Magda ismail Abdel Mohsin Associate Professor, International Centre for Education in Islamic Finance (INCEIF), The Global University of Islamic Finance, Kuala Lumpur, Malaysia Email: [email protected]

Prof. Datuk Dr. Syed Othman Alhabshi Chief Academic Officer, International Centre for Education in Islamic Finance (INCEIF), The Global University of Islamic Finance, Kuala Lumpur, MalaysiaEmail: [email protected]

Zainab Fida Ahsan Graduate student,International Centre for Education in Islamic Finance (INCEIF), The Global University of Islamic Finance, Kuala Lumpur, MalaysiaEmail: [email protected]

Shri Bhagat Nitin Research Scholar, Department of Economics, Hyderabad Central University, Hyderabad, Telangana, India

Dr. Narwade SunilProfessor, Department of Economics, Dr. Babasaheb Ambedkar Marathwada University, Aurangabad, Maharashtra, IndiaEmail: [email protected]

Mamata PatraAssistant Professor, Political Science, Bhuban Women’s Degree College, Bhuban, Dhenkanal, Odisha, IndiaEmail: [email protected]

Dr Radhakrushna PandaSenior Research and Documentation Expert, National Institute of Development Innovation (NIDI),Plot No-693, Near Kalinga Stadium, Nayapali, Bhubaneswar, IndiaEmail: [email protected]

Harasankar AdhikariSocial WorkerMonihar Housing Co-operative Society, Flat No-7/2, 1050/2, Survey Park, Calcutta, India Email : [email protected]

Dr Seema P. SalgaonkarAssociate Professor, Political Science, Government College of Arts,Science & Commerce, Khandola – Marcela, Goa, IndiaEmail: [email protected]

77

editorial

It is indeed a great pleasure in presenting the fifth issue of this special journal that covers the various dimensions of the interest-free cooperative microfinance model. Continuing with our past issues, we carefully selected articles that were original, unique and relevant to the basic objective of the journal.The entries have substantially increased in a small period of years given the fact that the overall research in this area is still limited. In addition to this, we are also overwhelmed by some real empirical evidence-based articles.

The journal is still trying to find a full-time editor in absence of which the processing of articles suffer. This was the reason we could not publish the December issue. We hope to end our search soon and find a qualified editor who can deftly handle the responsibilities.

This volume consists of nine articles selected from more than a score of submissions received. The articles cover diverse issues in the microfinance sector in India. The common thread among all the articles is that the researchers focus on identifying a possible solution or highlight the best practice in the field.

The first article has highlighted the four goals of alternative system as need fulfillment, respectable source of earning, equitable distribution of income and wealth and growth and stability and also identified the challenge faced from within and outside. The author has eloquently suggested road map for the future actions.

The second article explores the historical development of cooperative sector in India. It lists the success stories and also highlights the challenges faced by this sector. It highlights the current legal infrastructure available for the growth of cooperative sector in India.

The third article proposes a hybrid model as a tool to eradicate poverty and maintain financial stability. The author basically advocates categorization of the society on the basis of needs. The allocation of zakah/charity or interest free loan may be decided on this categorization.

The fourth article discusses the role of Zakah and Waqf in community development. It argues that the instruments of Zakah and Waqf can effectively provide a paradigm in the achievement of equitable distribution of wealth and its healthy circulation. To substantiate this claim, the author discusses a Singapore waqf modal and also suggests some reforms in Islamic asset management.

The fifth article explores the role of SHGs in socio-economic development of women from marginalized communities. The empirical evidence from Washim

8

of Vidharbha region famously known for highest number of farmer suicides in Maharashtra suggest that women from marginalized groups were comparatively less benefiting from the SHG movement and hence the author suggests that women bank should be established in each block and regular inspection of SHGs should be undertaken by Gram Sabhas along with provision of housing loans.

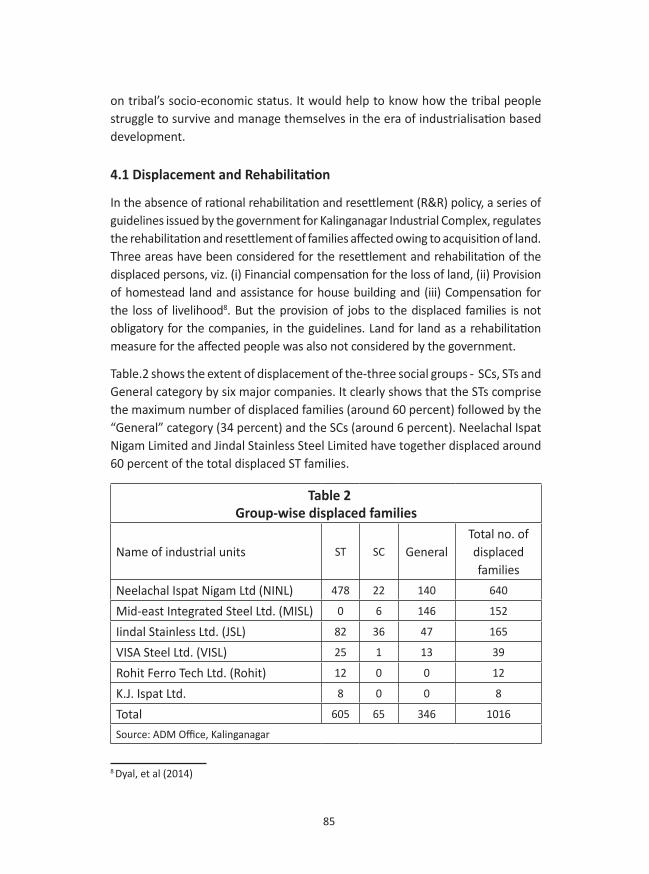

The sixth article investigates the impact of Industrializationon socio economic condition of tribals of Kalinganagar district in Orissa. It also traces the vulnerability faced by the community due to displacement and other exploitations. This study also highlights the responses of local people towards developmental projects and socio-economic and environmental impact of industrialization.

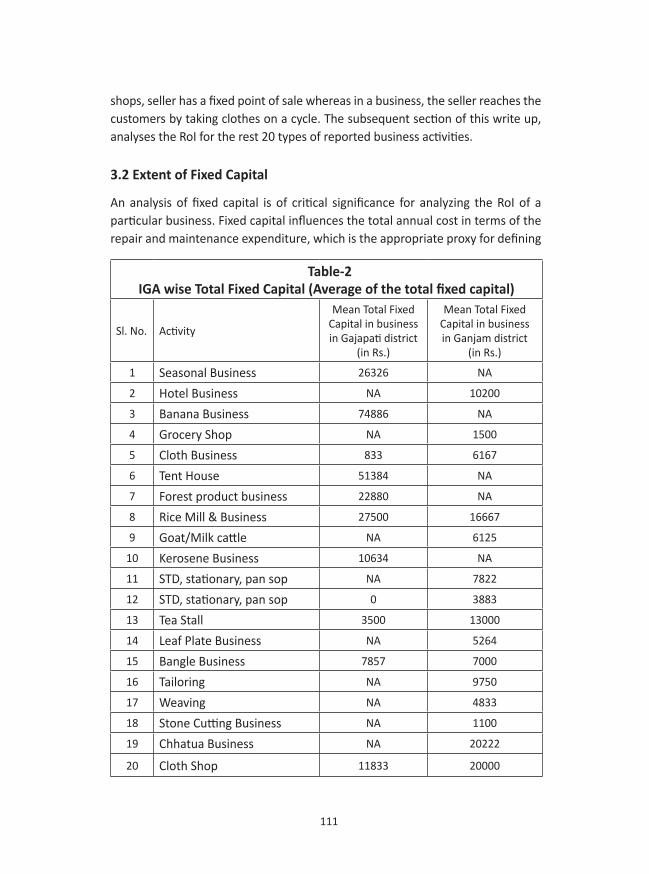

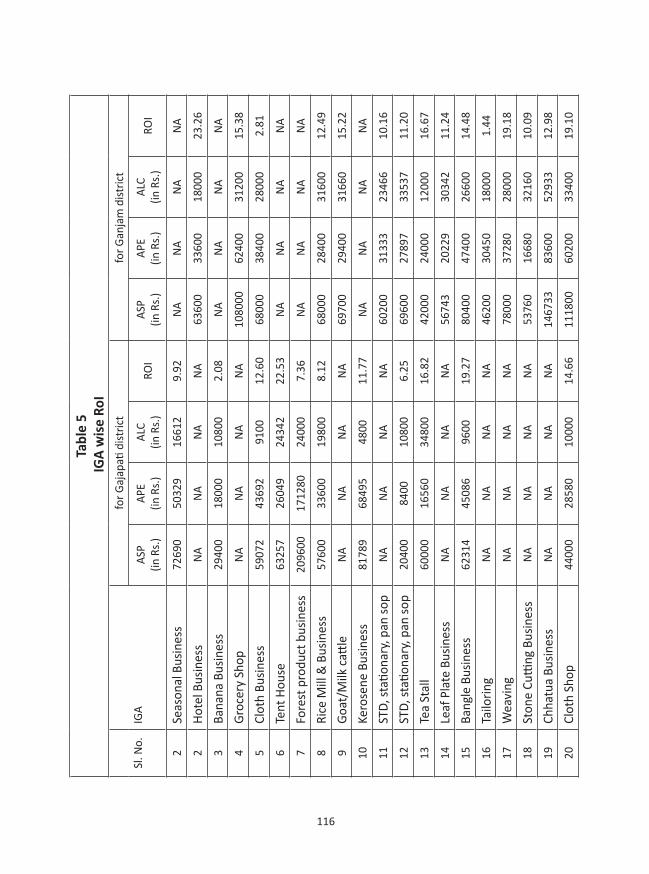

The seventh article examines the return on investment generated by the SHGs engaged in pursuing different economic activities either on individual basis or as a group with the assistance of bank loans and investment made in their micro enterprises. The authors analyse the primary data obtained from 200 SHG led micro enterprises operating in Ganjam and Gajapati districts in Odisha to understand the return on investment of SHG led business activities.

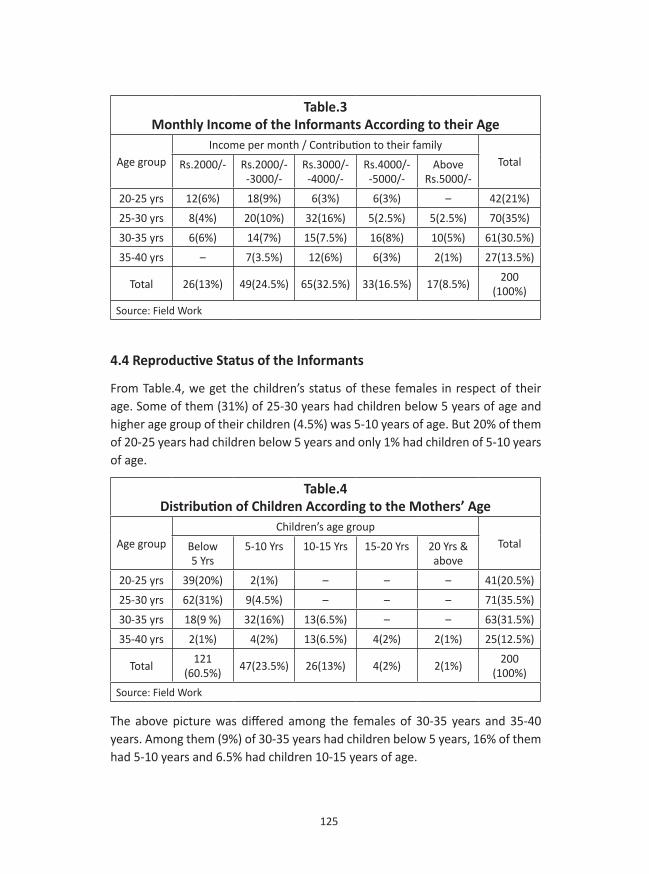

The eightharticle studies the impact of urban affiliation and wellbeing on female domestic workers of Kolkata. The study suggests that there are evidences that domestic workers life has quite improved however lack of employment certainty and social security makes them quite vulnerable to loss of job in case of ill health and other inevitable conditions. The author suggests some retirement scheme and secular education should be provided so that their safety and security is insured at elderly days.

The ninth article examines stimulus provided by micro financing in growth of women entrepreneurship skills. The data is obtained from in-depth personal interviews with members of women self-help group.While noting the challenges faced by women self-help groups in their entrepreneurial activities the study suggests that micro financing helps these women improve their entrepreneurial skills making them more independent and confident.

We welcome your feedback and also your contributions in the form of research articles, best practices, white papers, book-reviews or technical notes. You may send your queries for submission or request for a copy of the journal to [email protected]

Najmul HodaEditor

9

ARtiCleS

1010

11

Alternative interest Free economic System: Goals, Challenges and Road Map

Dr. Waquar Anwar1

This paper is based on the assumption that Interest Free Economic System is a desired alternative. This assumption is the natural corollary of the assumption that states that the conventional economic system based on interest is very harmful and there is a need for an alternative system. Any detailed discussion on this assumption-within-assumption is beyond the scope of this write-up. But a rich literature is available on the desirability of interest free economic system as well as the undesirability of the conventional system. However, some reflections of these issues will by default crop up in this article.

Our task at hand is one step ahead. It requires unfolding the goals of such an alternative system and delineating the steps required for realising those goals. A goal cannot be realised without facing the challenges and obviating its consequences that may crop up in the process. Further, a clear idea about the road map and a blueprint will also be required. So the intent is to develop a model that can do both - describe the disease and prescribe the medicine. A description of Islamic economics, as such, is also not intended in these lines. However, its contours can be felt between the lines!

Our methodology of discussion will be to first visit the writing of renowned Islamic economists and find what goals they have proposed and then proceed further. I shall, for this purpose, be referring to the writings of Dr. M. Umer Chapra and Dr. Mohammad Nejatullah Siddiqi.

1. Goals of an islamic economic System

Dr. M. Umer Chapra, in his book “Islam and Economic Challenges,” has discussed the goals of an Islamic Economic System from different aspects. First, he talks about what an economic system should ensure? What it should do and what

1 Financial Advisor, Jamaat-e-Islami Hind, New Delhi

11

12

not? Then he proceeds to describe the conventional interest based system and the Islamic interest free system, concluding with the failure of the former and the success of the latter.

Dr. Chapra says that an economic system should ensure:2

1. Need Fulfilment;

2. Respectable Source of Earning;

3. Equitable Distribution of Income and Wealth; and

4. Growth and Stability. [Chapra, 1992, p. 210]

While describing money and banking system he says that:

A. The system should not:

- Promote Inequalities

- Lead to Conspicuous Consumption

- Bring Unemployment

- Result in Unhealthy Monetary Expansion to the detriment of all [Chapra, 1992, p. 201]

B. Instead the system should:

- Support Need Satisfaction

- Lead to High Rate of Employment

- Result in broad-based Ownership of Means of Production [Chapra, 1992] [Ibid, p. 201]

Dr. Chapra after describing Maqasid Al-Shari’ah (Higher Objects of Islamic Law) links the goals of economy to fulfilment of the objects and opines that only that market may be considered optimum which is in harmony with, or not at least in conflict with, the Maqasid. Chapra says, “The Islamic worldview and strategy are blended together into a consistent whole and there is complete harmony between them.” [Ibid, p. 201-202] In his opinion an economy attains total efficiency when it achieves three goals: 1.Efficient employment of total potential of scarce human and material resources; 2. Stability; and 3. Sustainable rate of future growth.

2 Chapra, Islam and the Economic Challenge (1992), The Islamic Foundation and The International Institute of Islamic Thought, p. 210

12

13

He further warns that equitable distribution of income and wealth should not affect the following four factors:

- Motivation to Work

- Saving

- Investment

- Undertaking Enterprise [Chapra, 1992, p. 3] [Ibid, p. 3]

One may refer to the thoughts and works of Dr. Mohammad Nejatullah Siddiqi in his book as well as his website3. He talks about two positive traits of the economy [justice (adl) and equity (ihsan)], stressing the need of obviating two negative traits [oppression (zulm) and corruption (fasad)].

“The desired state of the world is free of oppression (zulm) and corruption (fasad) and full of justice (‘adl)…. Its hallmark is justice and equity and elimination of oppression and corruption while ensuring need fulfilment and sustainability.”4]

Dr. Siddiqi has also defined, and distinguished between justice and equity.

“Justice is largely perceived in terms of equivalence (in exchange transactions) and reciprocity (in social relationship). But equity (ihsan) is urged on top of justice and is defined as giving more than is due according to the standards of equivalence and reciprocity to ensure with dignity for all…. There are persons in society who are weak, invalid, poor, etc. so they have little to give. But they must receive in order to survive. Hence exchange and reciprocity is no good for them…. That is what equity envisages.”5

In other words, justice is treating equally and with fairness while equity is bringing some benefit or preventing some disutility (mafasid). It means rendering to others even more than their due. It is benevolence along with justice.

Dr. Siddiqi has prescribed remedies and suggested goals for achieving the same. He has specially talked about, inter alia, discouraging interest and gambling and promoting production based economy.

3 www.siddiqi.com/mns4 [Islamic Economics between Aspirations And Realities, http://www.siddiqi.com/mns/ISLAMIC_ECONOMICS_BETWEEN_ASPIRATIONS_AND_REALITIES_.htm]5 [Siddiqi, Riba, Bank Interest and the Rationale of its Prohibition, Markazi Maktaba uislami Publishers (Delhi), 2004, p. 24]

13

14

“Reducing the role of debt and eliminating gambling from financial markets should, therefore, be on top of the agenda for Islamic economics.”6

“Islamic Economics looks at production as a life sustaining activity. It aspires to promote a type of economy that sustains life for all, the weak and the poor included. It does not equate life sustaining productive activity with profit making activity. It is also aware of the limits to growth that ecological and environmental considerations impose on us.”7

“The key to Islamic economics lies in positioning the Islamic vision in place of the Anglo Saxon economic vision. But the Islamic economic vision has to be universal and contemporary not chauvinistic and medieval. As we move in that direction we may be pleased to discover we have good company from amongst modern economists in the West and East. The search for a more humane political economy is now universal. The challenge is, who leads the way.”8

It is true that ‘the search for a more humane political economy is now universal.’ It is also true that a majority of goals described above are also universally accepted. However, Islamic approach has certain characteristics which we are repeating hereunder for the purpose of highlighting so that our discussions ahead may become more meaningful.

1. Reducing the role of debt and eliminating gambling

2. Production based economy

3. Savings based economy resulting in investment wherefrom

Another very important goal of an interest free economic system is that wealth created should permeate all ranks and files of the economy and it should remain in circulation. One may refer to the verse of the Qur’ān that tells us the basic reason of this goal.

“And what Allah restored to His Messenger from the people of the towns - it is for Allah and for the Messenger and for [his] near relatives and orphans and the [stranded] traveller - so that it will not be a perpetual distribution

6 [Future of Islamic Economics, http://www.siddiqi.com/mns/future_of_islamic_economics.html]7 [Risk Management in an Islamic Framework, http://www.siddiqi.com/mns/RiskManagementInAnIslamicFramework.htm]8 [International Workshop on Islamic Political Economy in Capitalist Globalization: An Agenda for Change, http://www.siddiqi.com/mns/nature.html]

14

15

among the rich from among you. And whatever the Messenger has given you - take; and what he has forbidden you - refrain from. And fear Allah; indeed, Allah is severe in penalty.” [Al-Qur’ān 59:7]

This verse has a particular historical reference to an event in Madinah. But the message of keeping wealth in circulation so that it may not remain in the hands of the rich alone is universal.

One can imagine a production based economy with least dependence on debt and high reliance on savings based investments wherein wealth created is not allowed to circulate only between upper strata of the society. Obviously the fruits of such an economic development will seep into all the fibres of the economy in all pervading fashion.

2. Challenges

A changeover to, even a move towards, interest free economy from conventional interest based economy will throw three types of challenges: (i) Natural challenges; (ii) Resistance from Stakeholders of the existing system; and (iii) Self Inflicted Problems.

Any system in vogue, whatever level of ills it may contain, cannot be thoroughly contaminated. It must be serving some purpose otherwise it would have been thrown into the dustbin. A completely bad thing cannot see the day of light even for some hours of a day. The whole idea of revolutionary changes makes no sense. Changes have to be evolutionary in nature. This step by step approach demands that questions arising at every stage are addressed logically and seriously.

Interest free economic system demands that all premiums on debts without any counterpart be prohibited. Conventional economy has been running on interest for the last more than two centuries and almost all economic transactions are contaminated by it. Answer to the following issues will be required for replacing the existing system by the desired system. These are genuine, rather natural, challenges.

● Developments in conventional economics which are agreeable to Islamic economics

● Developments in conventional economics which are not agreeable to Islamic economics

15

16

● The ills of debt based economy including deficit financing.

● The possibilities of deploying capital in joint ventures on equity financing basis.

● The need and products of Islamic finance based on equity financing in production based economies as against those in rentier economies.

● The limits and conditions of current expenditure based on future income for individuals, families, corporate houses and nations.

● The pros and cons of the existing monetary system and the method and impact of creating money and bringing it to circulation, suggesting remedies based on the principles of equity and justice.

In addition to the above issues that require some research work based on empirical studies, there is another issue that interest free economic system, for all practical purposes, is another name for an Islamic economic system. There are persons who are averse to this idea. An interesting development is that most of such persons, groups and nations have agreed to the idea of Islamic finance because they get easy and low cost money in this name but when it comes to anything more Islamic than that, they get scared. It is a challenge for the proponents of Islamic economics to convince the world at large that this alternative is universal and it serves all.

2.1 Resistance from Stakeholders of the existing System

The conventional interest based economic system is serving the powerful persons, families and nations who are in minority but they sway the world of economics and finance. It serves them, and serves well. The vast and badly hit majority that is at the receiving end of the ill impacts of the system is either voiceless or unable to rise to the occasion. Such stakeholders may include rich people, big bankers, resourceful corporations and powerful governments. Their resistance is inevitable but this does not mean that the task ahead is insurmountable. Theirs is not a homogeneous entity as such and they are also members of the same society and are serving it from their specific sides. With conscious efforts, serious research and unambiguous practices of the alternative system, the tide can be changed and made favourable.

2.2 Self inflicted Problems

16

17

Self inflicted wounds are more painful than others. It is an irony that interest free economics has been hit hard, rather below the belt, by its sister Islamic Banking and Finance Industry. The latter was supposed to be an offshoot of the former but with the passage of time it has assumed the role of game-changer, if not game-spoiler.

A very basic object of interest free economics is to reduce the role of debt in finance. Initially this object was kept in mind but with passage of time things have taken turn differently, if not u-turn. I shall be quoting Dr. Siddiqi in support of this charge sheet on this assault from the most unexpected corner.

“The thing to worry about is not the phenomenon of Islamic Banking and Finance emerging as the chief embodiment of the idea of Islamic economics but the particular form Islamic finance has assumed: Debt-financing.”9

The reason behind this strange phenomenon is that the Islamic Finance industry started making copies of existing finance products, with its own brand, of course. Following long quote is self-speaking:

“The few Islamic banks that had come up by the end of the seventies of the last century did not depend on brand name ‘Shariah Advisories’ for getting business. All that came during the eighties when, feeling the wind had started blowing the familiar way, giants of the conventional financial industry like City, HSBC, ANB AMRO…entered the field of Islamic finance…. Each and every contract currently used by Islamic financial institutions is certified by a Shariah scholar, often a team of scholars. Barring a few exotic speculative products like Debt Default Swaps, every product currently available in the conventional financial markets is also available or can be readily made available in the Islamic financial market.”

“The contributions to the subject prior to induction of murabaha in late seventies of the last century all revolved around the principle of sharing. Even after admitting a number of other debt creating modes such as ijarah and salam/istisna into the Islamic financial arrangements it was emphasized they had to have only a limited scope. The addition of ‘trade based modes of finance’ had the backing mostly of Shariah scholars, not of trained economists.”10

9 [A Vision for the Future of Islamic Economics, http://www.siddiqi.com/mns/AVisionForTheFutureOfIslamicEconomics.htm]10 [Islamic Economics between Aspirations and Realities http://www.siddiqi.com/mns/ISLAMIC_ECONOMICS_BETWEEN_ASPIRATIONS_AND_REALITIES_.htm]

17

18

The solution could have come from trained economists or in association with the Shariah scholars. But alas!

“…whatever economic talent was forthcoming during the last thirty years was absorbed, largely, into the Islamic finance industry which had little time for theoretical niceties.”11

Dr. Siddiqi has placed himself in the category of those “who complain that Islamic economics proper has been submerged under the stormy waters of Islamic finance endangering its distinct identity….”

This is a painful story and, instead of prolonging it, I would close it with the description of the need for course correction in the Islamic bond industry, i.e. sukuk.

“What makes some of the sukuk debt instruments is inclusion of murabaha receivables into the package of assets against which sukuk are issued and the commitment to redeem them at their face value at some future date, regular periodical returns being paid in between. There is no difference, in effect, between this and a sum of money lent for an interval being serviced by periodical payment covering the interval.”12

3. Road Map

A description of challenges, particularly the last part above appears to be dampening. But no, the situation is not that bad. Conventional economics has inflicted far reaching injuries and there appears to be no way out as if the economics today has reached a dead end. A search for an alternative economics is on. There is no reason why this interest free alternative will not be considered if it is found to be the panacea. The task in hand is to present it with a clear road map and put it into practice wherever possible. A debate done in proper fashion is surely bound to be noticed.

11 [Future of Islamic Economics, http://www.siddiqi.com/mns/future_of_islamic_economics.html]12 [A Note on Sukuk and their Role in Islamic Finance, http://www.siddiqi.com/mns/NoteOnSukuk.htm]

19

Dr. Nejatullah Siddiqi has prescribed a road map of five strategic changes required for the purpose as under:

1. Family, rather than market as the starting point in economic analysis

2. Cooperation playing a greater role in the economy, complementing competition

3. Debt playing a subsidiary rather than the dominant role in financial markets

4. Interest and interest-bearing instruments playing no role in money creation and monetary management

5. Maqasid based thinking supplanting analogical reasoning in Islamic economic jurisprudence13

In the current economic thinking an individual as an economic agent faces the market where he has to face competition on an impersonal basis. The idea of making family as the primary economic agent has an altogether different connotation. Family is a place where love, care and compassion take place. It is not impersonal as the market. Thus, this could be the beginning of co-operation instead of competition in the economy.

The role of debt can be reduced but it cannot be ended altogether. With abolition of interest the trading of debt documents will vanish in the thin air. It is possible only when equity financing is encouraged in a big way. Equity financing would mean an atmosphere of risk sharing.

Risk management is an important aspect of the road map of interest free economic system. This would begin with abolishing the system whereby the financier is able to play a win-win game, immunizing himself from any monetary risk by shifting it to the producer. Further all scope of buying and selling risk is required to be blocked. The culture of risk sharing and equity financing cannot be ushered in without treading this path.

Gambling, which is a zero sum game, needs to be disallowed. There is no scope of any type of gaming in interest free economic system. Buying risk too is a form of gambling which cannot find a place in this alternative to the conventional system.

13 [A Vision for the Future of Islamic Economics http://www.siddiqi.com/mns/AVisionForTheFutureOfIslamicEconomics.htm]

20

The case of derailment of Islamic banking can be resolved and brought back to the desired main track. For example, Dr. Siddiqi has suggested ways and means of ending the malaise of excessive debt creation in the present day trade based finance practiced by Islamic banks. He says “The deposit money received by Islamic banks on the basis of mudaraba should be advanced on the same basis (of profit-sharing) to investors who would then finance productive enterprises directly or on the basis of murabaha, ijara, salam/istisna, etc.”14 This suggestion implies the separation of commercial banking and investment banking in a special way. Investment making institutions would not be allowed to accept deposits from the public. They either seek funding on mudaraba basis through banks or sell shares collecting funds on the basis of shirkah. Deposit taking banks, on the other hand, will manage the payments mechanism only.” This is an attempt of course correction by separating purely financial transactions from business transactions.

The tendency of Islamic banks to provide alternative financing products akin to the existing conventional products needs to be checked. This leads to the demand on the Shariah experts to adjust the features of the existing products by permutation and combination so that some analogy with a past Shariah decree of any school of jurisprudence may be found. There is a need to supplement this qias (analogy) based method of jurisprudence with Maqasid approach. Objects of Islamic law are defined. Hence any law making exercise should pass through this litmus test.

The idea of parallel window for Islamic financing products under conventional banking umbrella is obnoxious. This is a defeatist tendency whereby an alternative system is made a subordinate of the system it was supposed to replace. It is a case of losing the battle in the beginning itself.

Some aspects of the road map may be country specific. In respect of India, the following submissions are made in view of its characteristic features of being a democratic country with fast developing production based economy and large number of Muslims in minority:

A major portion of the features of interest free economy can be practiced. Enterprising persons have good scope of business opportunities. Arrangement for equity based finances on the mode of venture capital or angel finance can

14 [Risk Management in an Islamic Frameworkhttp://www.siddiqi.com/mns/RiskManagementInAnIslamicFramework.htm]

21

be made within the existing laws of the land. Only problem faced will be in collection of public deposits because Reserve Bank of India will not permit that, in the existing rules and laws. India is a democratic country where efforts for opening avenues for public deposits under interest free mode can be done and we understand that it is being done in a manner that is suitable in democracies.

● There is scope of risk sharing mode of finance under the umbrella of state level and multi state level cooperative laws. Efforts are being made to keep the scope open and widen its base.

● Many regional communities are running activities for providing interest free capital on charitable basis, i.e. qarz hasan mode. Their efforts may be praised but the need of the hour is activities within the scope of the existing laws so that they can be replicated at other places. One cannot build any movement on the basis of such private exercises.

● There is a serious effort spearheaded by well-meaning persons for liaison work in favour of Islamic banking in India. A separate effort in favour of interest free economy is required primarily because the scope of economy is much wider than that of banking or finance. Further, the practices in the name of Islamic banking need course correction that can only be done from a more serious academic effort. So Islamic banking too requires the check and balance of interest free economics so that it may not become a misnomer.

A movement in favour of the alternative interest free economic system is required. We will not be alone in this. Dr. Siddiqi says

“The current endeavours of other faith-based communities, also of non-religious but well intentioned people, to escape from tyranny of ideologies by making economics serve humane objectives, deserve our involvement at the local as well as the global level.” [Ibid]

“As we move in that direction we may be pleased to discover we have good company from amongst modern economists in the West and East. The search for a more humane political economy is now universal. The challenge is who leads the way.”15

One can locate some serious groups and individuals, both activists and academicians who are working in the fields of alternative and development

15 [International Workshop on Islamic Political Economy in capitalist globalization:an agenda for change, http://www.siddiqi.com/mns/nature.htm]

22

economics for eradication of poverty and economic development. Some of them may have to be convinced about the vices of interest based economy and satisfied about the worth including feasibility of an interest free economy. However, their work, particularly in collecting empirical data and developing theoretical base for providing a respectable life to the common man is very much common with the Maqasid based interest free economics. To name a few, for example, we may collect information about the Alternative Economic Survey Group of Delhi or noble prize winners like Amartya Sen and Angus Deaton, and their associate Jean Dreze. Amartya Sen did work on human rights, inequality and poverty and studied causes of famine, providing solution to these problems. Angus Deaton’s analysis and consequent measurement of consumption, poverty and welfare and his focus on household surveys and individual data enabled him to get the coveted award and international recognition. Jean Dreze has the distinction of being co-authors of several books of the two economists. This Belgium-born Indian economist has done remarkable work in the fields of hunger, child health and education. Their importance lies in empirical analysis, an area where academics related to interest free economics have much to learn. We may not only sympathise with these developmental economists but also associate with them and become wiser in the process.

22

23

Co-operatives and the Need for their Growth in india

Dr. Rafiquz Zaman1

Father of the Nation, Mahatma Gandhi laid emphasis on development of Co-operatives. According to him, “Co-operation is the gateway to economic freedom”. The first Prime Minister of India, late Pandit Jawaharlal Nehru once said, “Ensure me a good Panchayat, a good School and a good Co-operative Society, I will ensure you the Ramrajya.”

The establishment of network of Registrar Cooperative Societies (RCS) started in different States of India, soon after Independence. For instance, in most states including Assam, RCS at State Capital, District RCS at District Headquarter and Assistant RCS at Sub-division Headquarter have been established. A good number of Junior & Senior Inspectors, Sub-Registrars are available to look into activities related to Co-operatives. The structured layers of Co-operation department are meant for the service of the people.

In fact, in Assam, the first Co-operative was formed in 1904 at Jorhat. Today, the number of Co-operative Societies in Assam is 7906 with a membership of 4.6 lakhs. It includes Apex, District and Primary level co-operative societies (Source: Statistical Hand Book, Assam, 2012). This development in over 110 years does not augur well. Clearly, it indicates snail’s pace in co-operative movement in Assam. The scenario in most of the states in India is similar to that of Assam, if not better.

Amul started its journey way back in 1948. In over 60 years, it has become a giant in its growth. Two leaders, Verghese Kurien and Tribubhavan Das Patel are primarily responsible in leading Amul to its present status. Kurien provided all sorts of technical expertise whereas T. D. Patel organized the farmers at the village level to rear buffaloes to produce milk. Farmers formed strong co-operatives which were the roots of Amul. Any apex level organization with strong roots is not susceptible to any kind of adversaries. This is our learning from the success story of Amul.

One of the concerns by many people of the country is that this successful model has not been replicated so far. It is, of course, partly true. But there are dairy co-

1 Indian Administrative Services (Rtd.). Vice Chancellor, Assam Rajiv Gandhi University of Co-operative Management, Sivasagar, Assam, India

24

operatives in Karnataka, Madhya Pradesh and elsewhere functioning successfully with strong roots at village level. These societies are not publicized much.

Successful co-operatives in sectors, other than dairy, are also present in different parts of the country. In Bhopal, in addition to a dairy co-operative viz. ‘Sanchi’, ‘Vindhya Herbals’ is a successful Madhya Pradesh State Minor Forest Produce (Trading & Development) Co-operative Federation Ltd. This Apex level federation has 60 district unions and 1066 primary co-operative societies catering to about 1.6 million families of forest produce gatherers. In Karnataka there is ‘Yeshashvini Co-operative Farmers Health Care Scheme’ for all the members of the co-operative. Through this the member’s family can avail ‘Cashless surgeries’ on payment of nominal annual premium. This scheme is implemented by the department of Co-operation only. Total number of surgeries and members benefitted (till 3.10.2013) are as follows:

No. of surgeries Members (in lakh)

2003-04 9, 047 16.01

2013-14 31, 277 24.68

It is possible to identify many more sporadic examples of successful schemes of Co-operatives in the country.

The concern of Central and State Governments in India for adequate development of Co-operatives is apparent. After 2004, co-operation got special attention. Central Government set up a Committee for this purpose. In fact, 97th Amendment of the constitution is specifically for giving new shape to the cooperative movement. It declared the formation of co-operative as a fundamental right of citizens and ensured full autonomy to co-operatives without depending on Govt. funding.

Government of India has identified ‘Development of Co-operatives in India’ as a priority area. This concern is also reflected in United Nations Organisation. UNO had declared 2012 as the International Year of Co-operatives. Along with other nations of the world, India also celebrated it throughout the year. It is realized that co-operatives are less vulnerable in adversaries even in days of economic breakdown, because of improved system of information exchange and bonding. In fact, solutions for many problems of agriculture like mechanization, lies in co-operation. Forest can expect better management of collection of Minor Forest Produce through co-operatives. Vindhya Herbals is an excellent example in this regard. Dairies can be successful only through co-operatives.

25

It appears that ‘Co-operatives’ is now at the crossroad. There is a huge opportunity before us. In the days of globalization and liberalization, co-operatives can be a savior for disadvantaged and marginalized families. Otherwise, income divide may push them farther away from the benefits of growth.

There are clearly three functions in the department of co-operation. The first one is Regulation which is to be performed by RCS and its subordinate officials. Another function is Facilitation of formation of the Co-operatives through promotion. The third and the most important one is Education, found to be the weakest link among the three. Unless we educate farmers properly and also create professional managers in Co-operative management, the pace of co-operatives may remain tardy.

Assam Government through the establishment of ‘Assam Rajiv Gandhi University of Co-operative Management (ARGUCOM)’ by an Act in 2010 had taken a very bold step in this regard. Victor Hugo once said, ‘Nothing in this world is more powerful than an idea whose time has come’. This idea of setting up a ‘University of Co-operative Management’ is certainly novel and the university can become the fulcrum for growth of co-operatives through capacity building.

This specialized University is a teaching, residential, non-affiliated University. There is no provision for distance education. The University stands on four pillars viz. Education, Research, Training and Promotion, (ERTP). The University aims to fulfill the needs of youth, farmers, co-operators, officials (regulators) etc. in the co-operative sector. The University would endeavor to change the mindset of people to adhere to the principles of co-operatives in order to start enterprises for self sufficiency.

The University had already started its under graduate course in Co-operative Management to award degree namely BBA (Co-operation) on 1st July, 2013. The course is trimester based according to the suggestions from IIM-Ahmedabad, as the architect of academic framework of the University.

The syllabus for BBA (Co-op.) has been specially designed in consultation with different resource persons. The model for the syllabus is a dynamic one with a provision to incorporate or delete topics according to the requirement of the syllabus. One significant provision is the requirement of each student to spend one trimester to study the functioning of a co-operative enterprise in any part of India. The purpose is to enhance the capacity of the students to be successful entrepreneurs or professional managers primarily, in the co-operative sector.

26

More programmes like MBA and Masters, are introduced in the University after due consultation with IIM-Ahmedabad.

University of Co-operative Management is a higher academic platform. It is possible to showcase the successful stories of co-operative in any part of the country through research or case studies as learning material for the students and farmers. National Fisheries Development Board (NFDB), Hyderabad has sponsored 11 trainings, to be conducted by the University. Through these programmes 315 fishermen have been trained. Under Rashtriya Krishi Vikas Yojana (RKVY) programme also 1563 farmers have been trained.

The need for proper education and training to the farmers is paramount before selling a scheme to them. Construction of rural godowns by the societies is now promoted both by Government and other agencies. But managing a godown by the society involves many aspects. Godown is not simply a room with four walls. Unless proper training is provided to the farmers in advance, the scheme is bound to fail. For this reason, atleast 5 to 7 percent of the fund within the scheme must be kept reserved for training of the farmers on these management aspects.

There are other aspects in the functioning of Co-operatives. Sharing of experiences by different groups of farmers can be of great help. Moreover, apparently a Co-operative Society may look good on its face. But the inner functioning may not be that healthy. There may be problems in management, administration, finances and even profit sharing. It may be necessary to conduct surveys or document case studies of such societies to find out solutions to such problems. These documents can become the backbone of learning in the University. Students and trainees will be highly benefitted from such exercises.

Finally, I would like to stress on various technical aspects in the functioning of co-operative societies. No federation can sustainable itself for long in the absence of strong roots both at the district as well as primary level. Government can only promote the formation of co-operatives but it is necessary for farmers to be educated and make informed choices to become self sustained. The less they depend on govt. funding, the better for their growth opportunities. Govt. support should be mainly on regulation (R), education (E) and of course, facilitation (F) aspect.

The greatest challenge lies in integrating R, E & F together with the co-operation of the farmers at different levels. I hope with the change in the legal framework in relation to the functioning of Co-operative Societies and the awakening at both Central & State Govt. levels, the day is not far to see lights in the Co-operative movement of the country.

Hybrid Model of Zakah, Waqf, Qard-Hassan & islamic Finance for a Just and Sustainable

Microfinance

Dr. Magda ismail A. Mohsin1, Prof. Syed Othman Alhabshi 2

Abstract

The failure of interest based programmes, such as micro-finance and anti-poverty programmes, in assisting the destitute, eradicating poverty and reducing income inequality encouraged the authors to study in depth the alternative financial institutions to interest/riba that can solve such problems rather than harming individuals, communities, societies and countries. This raises the question of whether the different Islamic financial institutions can provide microfinance with zero-interest to eradicate poverty and reduce inequalities.

This paper attempts to propose a hybrid model integrating four religious financial institutions to eradicate poverty within a very short period of time in a just manner and in a sustainable way for generations to come. We shall use both primary sources including text from the Quran and the Hadith, and data collected from secondary sources including books, articles and journals besides World Bank reports from the web sites.

The paper intends to create awareness of the meaningful approach of religion in terms of eradicating poverty, reducing inequalities and creating a fair and just society for all, rather than following man-made system which hurt all societies. Moreover, this paper also intends to open the door wider for more researchers and postgraduate students to explore their knowledge in depth on these religious institutions and to adjust them according to the current needs of different societies. We hope to revitalize four neglected Islamic financial institutions and

1 Associate Professor, International Centre for Education in Islamic Finance (INCEIF), The Global University of Islamic Finance/Kuala Lumpur, Malaysia. e-mail: [email protected] Chief Academic Officer, International Centre for Education in Islamic Finance (INCEIF), The Global University of Islamic Finance/Kuala Lumpur, Malaysia. e-mail: [email protected]

27

integrate them into a hybrid model for a promising way to eradicate poverty in a just and ethical manner.

Acknowledgement

This is a paper extracted from a research conducted by the author and the co-author and funded by INCEIF for two years research 2013-2014. The title of the research is: “An Islamic approach to poverty eradication through zakah & waqf based micro-financing (case studies: Malaysia, Egypt & Sudan).

1. introduction

The last decades witnessed many anti-poverty programmes which had been implemented in many countries to eradicate poverty and to empower the poor and the needy through micro-lending. Although some of these anti-poverty programmes succeeded in reducing poverty to some extent, yet they fail to reduce inequality which is quite high in many regions around the world. According to the World Bank statistics of 2012 on Global Issues, more than 80% of the world’s population live in countries where income inequality is very wide. For example 20% of the world’s poorest population account for less than 2% of global income where 20% of the richest account for almost 77% of the world income (World Bank 2008). Besides, almost half of the world specifically over 3 billion live on less than $2.50 a day; 640 million live without adequate shelter; 925 million people suffer from hunger; 400 million have no access to safe water; 270 million have no access to health services; 10.6 million died before they reached the age of 5 and 1 billion are illiterate. Muslim countries are no exception, according to Statistical, Economic and Social Research and Training Centre for Islamic Countries (SESRIC) statistics 27.2% of the Organization of Islamic Cooperation (OIC) population i.e. 351.2 million people, live on less than $1.25aday. Moreover, the various microfinance programmes which are meant to assist the financially excluded people and which started with a very low interest rate between 4% -7%, has recently increased to 20% and in some cases to 50%.

28

The main objective of this paper is to revive four religious institutions which are meant to eradicate poverty, reduce inequalities and narrow the gap between the rich and the poor in an ethical and just manner. These religious institutions are the zakah, waqf, qard-hassan and interest-free institutions which are well known in all holy books that had been sent to man throughout history. Since the Quran is the last holy book which has been sent by Allah, it upholds all these institutions and discusses them in details. These were immediately put in practice by His final messenger (pbuh), the companions and the successors in more than thirteen centuries in the Islamic world. However, within the last century all these institutions had been replaced with man-made systems which led to the negligence of the Islamic institutions in the Islamic world. Consequently an unacceptable scenario, as highlighted above, has prevailed globally. To change this current scenario, it is highly recommended to revive these institutions and to put them in practice again for the benefit of the mankind. This can be achieved by integrating these four institutions i.e. the institutions of zakah, waqf, qard-hassan, and Islamic finance into a hybrid model as an alternative to the current anti-poverty programmes that deal with interest/riba, which is prohibited in the religion. This paper is divided into four sections including the introduction. Section two gives an overview on poverty; section three explains the Islamic approach of poverty eradication, while section four proposes a hybrid model for Islamic Microfinance followed by the conclusion.

2. Overview on Poverty

Currently the role of waqf, zakah, qard-hassan which are meant to eradicate poverty, eliminate riba and create employment for the majority of people in the Islamic world, have been neglected for over a century. Consequently, this has forced almost all Muslim countries to follow the conventional system in eradicating its poverty through many anti-poverty programmes, including the international and the national microfinance programmes, which are based on interest/riba. But instead of eradicating the poverty in some countries it initiated persistent poverty for generations to come due to compound interest.

To overcome this, we believe that the Islamic approach to anti-poverty programmes is the best scheme for eradicating poverty in a just way if zakah, waqf and qard-hassan are integrated into a hybrid model for Islamic microfinance. Accomplishing this will not only eradicate the poverty of the poor and needy, but

29

will shift them to be among the active and well-off members in their societies. The basis for this shifting is found in the Sunnah of the Prophet (pbuh) as narrated by Anas ibn Malik:

“An Ansari (native of Madinah) man approached the Prophet (pbuh) seeking for his generosity. The Prophet (pbuh) instead asked him to bring whatever he has from his home. The man returned with a rug and an old mug. The Prophet (pbuh) then asked his companions seated with him if any of them would buy them. One of the companions offered to pay one dirham. The Prophet (pbuh) then asked if anyone would offer two dirhams and one of them did. He then gave one dirham to the man to buy food for his day and asked him to buy an axe with the other dirham. When he came back with the axe, the Prophet (pbuh) personally fixed a wooden handle to the axe and asked him to get firewood to sell at the market. A few days later, the man met the Prophet (pbuh) and told him he has been getting some fourteen dirhams selling firewood within the last few days". Then Allah’s Messenger said, “This is better for you than begging, for begging would come as a stain on your face on the Day of Resurrection” Narrated by Abu Daud, (H/1398) and al-Termizee (18410).

In the above hadith, the Prophet (pbuh) taught the beggar to earn his livelihood through his own skills in order to make a livingandearn respect in society rather than begging. This is followed by another Hadith of the Prophet (pbuh) as narrated by ibn Hakim ibn Hizam: "The hand that gives is much better than the hand that receives." (Sahih Muslim).

Hence, Islam promotes a developmental approach which enables the poor to use their skills with whatever they have in hand in order to earn their living and be independent of society as long as they are healthy and fit to work. Nevertheless, for those who cannot afford to work due to lack of skills or because of age or health problem, Islam provides regular income from those who have to support those who have not. This income comes from Bait al-Mal/Public Treasury which draws its resources directly from zakah (Alhabshi, 1992). According to the teaching of Islam, zakah is a compulsory due which has to be taken from the rich to be given to the less fortunate on yearly basis. Zakah scheme is a remarkable national annual programme which is meant not only to eradicate poverty, but also to reduce the gap between the rich and the poor and at the same time to eliminate riba from Muslim societies. Beside zakah there is also another national scheme, the waqf scheme; which provides goods and services to societies and which also benefits the less fortunate at large. In addition to these, the Islamic loan, al-qard

30

al-hassan and the Islamic way of finance have great impact on eliminating riba which is the main cause of poverty and all evil corruption in the world.

3. islamic institutions to eradicate Poverty

Islam defines poverty as a state whereby an individual fails to fulfill any of the five basic needs such as protection of religion, protection of physical self, seeking of knowledge and education as well as protection of the family and wealth (M. Kabir, 2010). Moreover, Islam classified poverty according to the differences among people and according to the levels of human abilities. Even though individuals are provided with equal opportunities, Islam acknowledged that their economic status may differ according to their capability and needs which may be divided into three categories:

Category 1: Unhealthy individuals and incapable to work, they lack both skills and the capital.

Category 2: Healthy individuals but lack both the skills and the capital.

Category 3: Healthy and skilled individuals but lack the capital.

For those categories Islam provides four approaches of anti-poverty schemes each according to the above mentioned categories. These schemes are: compulsory scheme/zakah, voluntary scheme/waqf, Islamic Finance Scheme and al-qardal-hassan scheme.

3.1 Compulsory Scheme: Zakah

The basis for this compulsory scheme is stated in the following Quranic verse in Surah al- Surah Al-Taubah (9:103);

Of their goods (wealth), take alms, that so thou mightest purify and sanctify them; and pray on their behalf. Verily thy prayers are a source of security for them: And Allah is One Who heareth and knoweth.

Hence what is Zakah? Zakah is a compulsory due upon all eligible Muslims to give part of their wealth to the state to redistribute it to its recipients.

Literally it means blessing, purification, increase and goodness. Zakah is the third pillar of Islam, it is obligatory upon all Muslims to give part of their wealth

31

and assets once it reaches al-nisab/the minimum or threshold assigned on annual basis or once harvested. It is also important to note that zakah has to be paid from lawful wealth and assets, and cannot be calculated on prohibited or unlawful wealth, such as income from interest, stolen property or wealth acquired or earned through unlawful means. There are two types of zakah, zakah al-Fitrah which has to be given by every Muslim in the month of Ramadan before Eid prayer and zakah on wealth. Zakah on wealth includes more than fourteen types of wealth that man possesses such as livestock, gold, silver currency and jewellery, commercial assets, agriculture, honey and animal products, mining and fishing, rented buildings, plants as well as fixed capital and lately italso includes salary, wages, bonuses, grants, gift and dividend income which if collected and distributed efficiently and according to the teachings of Islam, is more than enough to eradicate total poverty within a very short duration(A. Mohsin, 2013).

Scope of Zakah as Financial tool for Poverty eradication

The recipients of zakah are very clearly stated in the following Quranic verse in Surah al-Tauba (9:60);

"Zakah is for the poor, and the needy and those who are employed to administer and collect it, and the new converts, and for those who are in bondage, and in debt and service of the cause of Allah, and for the wayfarers, a duty ordained by Allah, and Allah is the All-Knowing, the Wise".

As highlighted above zakah is a compulsory financial tool to be given to eight recipients. Although eight recipients of have been mentioned in the above Quranic verse there is a general agreement that the first priority is to be given to eradicate the poverty of the poor, the needy and to assist the debtor (M. Kabir, 2010).As defined by Muslim scholars (al-Qaradawi, 1999) a poor person is a person who is without any means of livelihood and material possessions. The needy isa person who is without sufficient means of livelihood to meet his basic necessities. And the debtor is a person who has financial difficulties in repaying his borrowed loan to meet his basic necessities.

Zakah is an Alternative institution to Riba

One of the objectives of zakah is as an alternative institution to riba (A. Mohsin, 2013) as mentioned in Surat al-Rum, (30:39)

“And that which you give in gift (to others), in order that it may increase

32

33

(your wealth by expecting to get a better one in return) from other people’s property, has no increase with Allah; but that which you give in Zakah seeking Allah’s Countenance, then those they shall have manifold increase.”

Therefore, by giving zakah to these three categories of people they will be prevented from borrowing with interest/riba under any anti-poverty programme to meet their crucial needs.

Zakah for elimination of Corruption

Besides the above objectives of zakah, it is also one of the tools for material and spiritual purification, i.e. elimination of any sort of corruption in a society. For example, with regards to the giver of zakah, it not only purifies his wealth but it purifies his heart from selfishness and from greed for wealth. On the other hand, zakah also purifies the recipient’s heart from envy and jealousy, from hatred and uneasiness; and it fosters in his heart instead, goodwill and warm wishes for the giver. In a large scale zakah purifies the society from any class warfare and suspicion, from ill feelings and distrusts, from corruption and disintegration and from all such evils. Hence, an automatic and an ethical strategy for poverty eradication will be realized on a regular basis through circulating the wealth from the have to the have not in a kindly and ethical manner eliminating all sorts of corruption.

Current Practice of Zakah on Monthly Salaries

At present income is the most important source of taxes today. It includes wages, salaries, rents, profits, dividend and other forms of earnings received in a given period. Therefore, people earning income including salaries cannot be excluded from the payment of zakah. Recently some Muslim countries enacted laws for the collection of zakah on income on obligatory basis such as in Sudan and on voluntary basis such as in Malaysia. Huge amount of money has been collected from this scheme and if managed according to the teachings of Islam it will eradicate poverty within a short duration. (A. Mohsin, 2013).

3.2 Voluntary institution: Waqf

The basis for this voluntary institution is found in the following Quranic verse:

“By no means shall ye Attain righteousness unless Ye give (freely) of that Which ye love” (Al-i-Imran 3:92)

Moreover, the Prophet (s) said: “When a man dies his acts come to an end, except three things, recurring charity, knowledge (by which people benefit),

34

and pious offspring, who pray for him” (Narrated by abu-Hurraira, Sahih Muslim No. 1631).

Historically speaking the institution of waqf, which is voluntary in nature provided goods and services to all categories of people; the poor, needy middle class people and even the rich in terms of shelter, food, cloth, education, health as well as jobs and even providing qard-hassan/ benevolent loan through cash waqf. Similar to the institution of zakah, the institution of waqf is one of the alternative institutions to interest/riba as mentioned in Surat al-Baqarah (2: 276);

Allah will deprive usury of all blessing, but will give increase for deeds of charity…

Parallel to the above mentioned compulsory scheme of zakah by providing voluntary goods and services to the poor and needy in terms of education, training, healthcare, these people will not be forced to borrow from any anti-poverty programmes which lend with riba to meet their basic and crucial needs.

What is Waqf?

In Arabic language, the word means to stop, to withhold the thing. Hence it is a financial charitable institution established by withholding one's property to eternally spend its revenue on fulfilling any need that might arise in the society depending on the choice and conditions made by the founder. Once the property has been declared as waqf, it becomes perpetual, irrevocable and inalienable which means it can never be given as a gift, neither to be inherited nor sold, it belongs to Allah and the waqf property always remains intact while providing perpetual goods and services to the society.

Kinds of Waqf

Waqf can be classified into different kinds based on its purpose or usage. The following is the classification in terms of the waqf property itself. In this case waqf is classified into two, waqf ghair manqul and waqf manqul. Waqf ghair manqul means immovable waqf which includes immovable properties such as land, fields, farms or buildings such as mosques, schools and hospitals, orphanages and agricultural lands. Waqf manqul means movable waqfs which includes movable properties such as cattle and animals, books, crops, weapons, medical instruments, jewellery and cash. Both are important tools for poverty eradication.

35

Scope of Waqf as tool for Poverty eradication

Since waqf is voluntary in nature through centuries, waqf has served its role as poverty eradication tool. Through creating immovable waqf, it serves the beneficiaries in terms of providing them with the much needed goods and services. For example, by creating immovable waqf in the form of agriculture land, schools, hospitals and factory it serves the poor and the needy not only in terms of feeding them, providing them with free education and free treatment but in terms of providing them with jobs too. Through creating movable waqf in terms of cash waqf, it provides funding for many services including the financial support for small entrepreneur, without riba. The most important implication of cash waqf is that it allows continuous accumulation of capital with time as more and more capital will be made into waqf (Alhabshi, 2013). This means that the proceeds of the waqf pool of funds will increase infinitely and which, if managed according to the teachings of Islam, can solve all the above mentioned economic problems.

Current Practice of Waqf

The last two decades has witnessed the revival of the institution of waqf and the creation of cash waqf in almost all Muslim countries and Muslim minority countries. Nine cash-waqf models have been practiced successfully providing many goods and services for the poor and the needy. Among these models are waqf shares model, waqf takaful model, direct model, mobile model, corporate cash waqf model, compulsory model, deposit product model, co-operative model and waqf mutual fund model (A. Mohsin, 2009), which can be adopted easily as anti-poverty programmes.

3.3 islamic Financial institutions

As mentioned earlier the issue of interest/riba is the main cause of persistent poverty in the developing countries (A. Mohsin, April 2014). And since it is not allowed in Islam, Islam provides alternative means of financing as mentioned in the following Quranic verse:

“…Allah hath permitted trade and forbidden usury…” (Surat al-Baqarah2: 276)

Hence, under trade (Alhabshi, 2014) many Islamic financial modes are allowed to finance any activity in the society including financing small entrepreneur through any of the following; murabaha, salam, istisna, mudharabah or musharakah.

36

What is islamic Finance?

Islamic finance is a financing activity that is consistent with the principles of shari'ah/Islamic law where the element of interest/riba is not involved.

Current Practices of islamic Finance

Almost all of the current practices of Islamic finance is done through Islamic banking which is one of the fastest growing sectors at the present time in Muslim and non-Muslim countries. Since the ethical nature of Islamic finance means that businesses should provide some sort of positive benefits to the society in terms of goods and services, its investment has to be done through any lawful financial products mentioned above.

3.4 interest-Free institution: Al-Qard Al-Hassan

This is another tool to eradicate poverty through lending needy people qard-hassan/benevolent loan without any interest/riba. This is the only lending institution which is allowed in Islam in order to assist needy individuals who are facing crucial needs or trying to find lawful living. Since it is more to help others who are in crucial needs, the lender must not expect any return but seeks multiple rewards from His Creator as mentioned in Surat al-Baqarah (2:245):

Who is he That will loan to God A beautiful loan, which God Will double unto his credit And multiply many times?

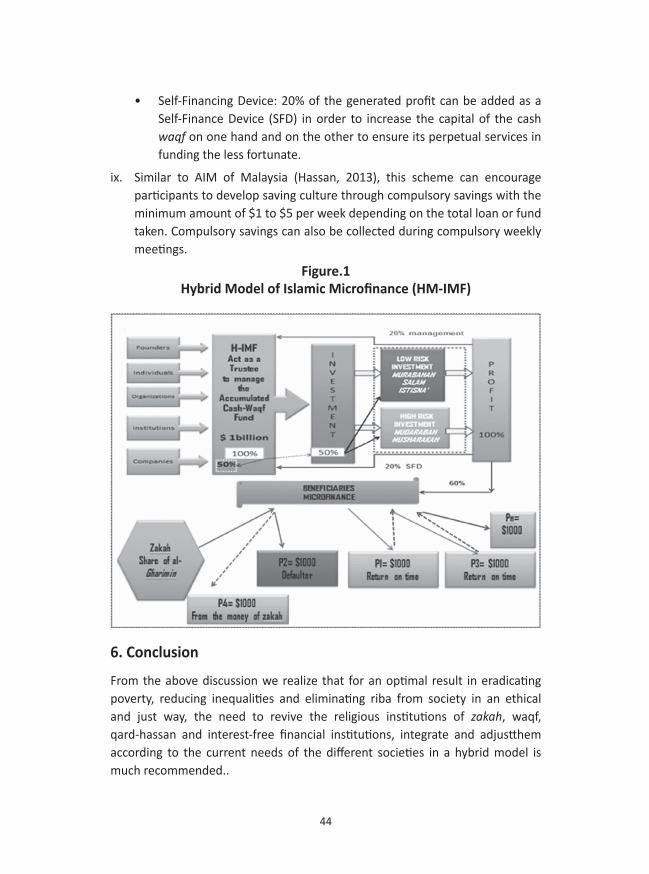

4. Proposal for A Hybrid Model of islamic Microfinance (HM-iMF)

For more than 60 years, the World Bank Group has partnered with governments worldwide, reducing poverty by providing financial and technical help through many anti-poverty programmes. Since 2000, some developing countries have reduced extreme poverty by half, achieving Millennium Development Goals (MDG 1) five years ahead of schedule. However, milestone was not met in much of Africa and South Asia, and a billion people worldwide still live in extreme poverty. Many more experience hunger and are vulnerable to environmental or price shocks (World Bank). Among these anti-poverty programmes is the microfinance programme which is meant to give small loans to low-income

37

individuals who lack access to banking and related services to start their small businesses and to lift them out of poverty. In these programmes, small loans will be given to the poor for the purpose of generating additional income or to expand their business. This is usually done through short term financing and repayment can be made on daily or weekly basis. Additional capital can also be given after the full settlement of the previous loan. In general the main objectives of microfinance programmes are to eradicate poverty and to improve the lifestyle for the regional societies. However, these microfinance programmes have been criticized of its conventional nature which does not suit Muslim countries. The following are some of the criticisms of the conventional approach compared to the Islamic microfinance approach.

islamic Microfinance vs. Conventional Microfinance

Recently some of the microfinance institutions managed to reduce poverty in Muslim countries while others failed. The failure was due to the conventional approach in seeking profit even from the moderate poor through interest based lending, which is prohibited in Islam. The following are some of the differences between conventional microfinance and Islamic microfinance (Al-Harran & others);

• The conventional microfinance assets are interest bearing debts while Islamic microfinance assets consist of diverse types of non-interest financial instruments such as qard-hassan, zakah, cash waqf and Islamic finance.

• The conventional microfinance is more towards enhancing the role of women in society by provide them loan which they have to repay with interest/riba, while Islam empowers women by providing them with regular income from Bait al-Mal/State Treasury.

• Usually the main target for conventional microfinance institutions are those from the moderate poor, thus neglecting the poorest segment of the society whereas this segment is the priority of the Islamic microfinance to tackle them through both zakah and waqf institutions.

• In conventional microfinance framework, the borrower will not receive the whole principal since a portion will be deducted from the beginning as a reserve. Besides, the borrower will have to pay interest for the whole amount that has been borrowed. On the contrary, under the Islamic microfinance the whole process is not acceptable as it is against the Islamic principles.

• In cases of default the conventional institutions will use its power to collect

38

the defaulted amount from the other group members who are essentially poor whereas Islamic microfinance institutions use the share of zakah which is meant for such cases, without harming other groups.

Hybrid Model of islamic Microfinance institution HM-iMF

As mentioned above, Islam provides many anti-poverty schemes each according to individual’s capabilities and needs. For the success of this Hybrid Model of Islamic Microfinance (HM-IMF) we will integrate the above mentioned four schemes, each according to the categories of individual and their needs as mentioned above. Two anti-poverty schemes; zakah & waqf schemes have to be implemented directly as poverty eradicating schemes in order to tackle the basic needs for the first two categories of individuals before joining the HM-IMF. The other two anti-poverty schemes, qard-hassan and Islamic finance scheme have to be implemented after the third category of individuals join the HM-IMF. This will be explained in details as presented below:

Zakah Scheme for Poverty eradication

For individuals who belong to the first category of people mentioned above, i.e. unhealthy and lack both skills and capital due to old age, widowhood or orphanhood; Islam makes it mandatory for the institution of zakah to take care of this category of people in order to provide them with a regular income that covers their basic needs. Doing so will eradicate their poverty and will prevent them from borrowing with riba to meet their crucial needs.

Zakah & Waqf Schemes for Poverty eradication

For the second category of people who are healthy but lack both skills and capital, two schemes have to be implemented to provide them with the funds and the skills before joining the HM-IMF and start their small business. These two schemes are:

• Zakah Scheme: For individuals who fall under this group, zakah has to be given to them in cash and in kind (but for a short duration). This is done by giving them some cash in order to satisfy their basic needs (like for 3-6 months) and giving them in kind to provide them with the tools to start their small business in terms of providing them with necessary equipment and tools such as grass cutters, small boats, sewing machines, food stalls, etcetera.

• Waqf Scheme: Waqf scheme is meant to provide the free training for this

39

category of individuals in order to provide them with the skills to use the above mentioned equipment and tools as well as to teach them how to generate their own income in the future. In addition, a very close monitoring on this group has to be done on daily or on weekly basis for a quick result in eradicating their poverty. In case some individuals from this group fail to generate their own income within the proposed short duration of 6 months, extension of another 6 months can be given to them. For those individuals who succeed in earning their income within this short duration and hope to earn more income, they become eligible to register as participants in the HM-IMF through joining either the Islamic financial scheme or al-qardal-hassan scheme to get more funds to expand their small business.

islamic Finance Scheme for Microfinance