S. Kumars Nationwide Ltd. Investor Presentation Sep. 2005 C lothiers to the Nat ion T oday …t he World Tomorro w SKNL

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Clothiers to the Nation Today…the World Tomorrow

SKNL

S. Kumars Nationwide Ltd.

Investor PresentationSep. 2005

Clothiers to the Nation Today …the World Tomorrow

SKNL

Clothiers to the Nation Today…the World Tomorrow

SKNL

An Overview

Key Strengths

Section 1

Section 2

Section 3

Industry OverviewSection 4

Business Profile

Initiatives & DriversSection 5

Financial ReviewSection 6

Index

Clothiers to the Nation Today…the World Tomorrow

SKNL

An OverviewSection 1

Section 2

Section 3

Section 4

Section 5

Section 6

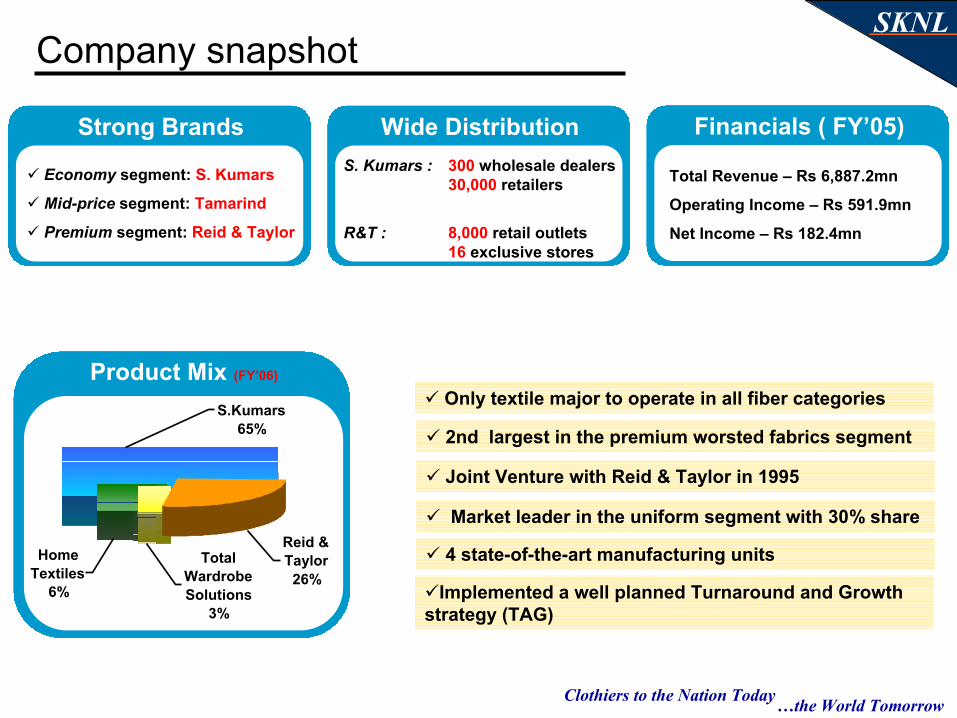

Company snapshot

Financial snapshot

The Journey

Business Profile

Key Strengths

Industry Overview

Initiatives & Drivers

Financial Review

Turnaround -CDR Package

Clothiers to the Nation Today…the World Tomorrow

SKNL

Product Mix (FY’06)

Company snapshot

Strong Brands

Economy segment: S. Kumars

Mid-price segment: Tamarind

Premium segment: Reid & Taylor

Wide DistributionS. Kumars : 300 wholesale dealers

30,000 retailers

R&T : 8,000 retail outlets 16 exclusive stores

Financials ( FY’05)

Total Revenue – Rs 6,887.2mn

Operating Income – Rs 591.9mn

Net Income – Rs 182.4mn

S.Kumars 65%

Reid & Taylor

26%Home

Textiles 6%

Total Wardrobe Solutions

3%

Only textile major to operate in all fiber categories

4 state-of-the-art manufacturing units

2nd largest in the premium worsted fabrics segment

Market leader in the uniform segment with 30% share

Implemented a well planned Turnaround and Growth strategy (TAG)

Joint Venture with Reid & Taylor in 1995

Clothiers to the Nation Today…the World Tomorrow

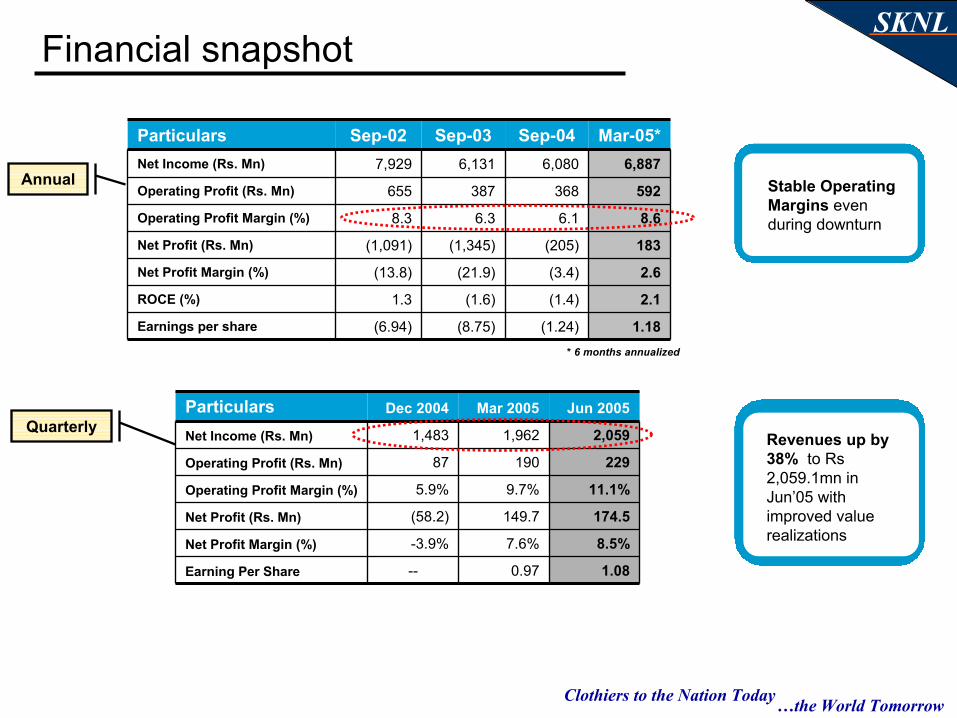

SKNLFinancial snapshot

1.18(1.24)(8.75)(6.94)Earnings per share

2.1(1.4)(1.6)1.3ROCE (%)

2.6(3.4)(21.9)(13.8)Net Profit Margin (%)

183(205)(1,345)(1,091)Net Profit (Rs. Mn)

8.66.16.38.3Operating Profit Margin (%)

592368387655Operating Profit (Rs. Mn)

6,8876,0806,1317,929Net Income (Rs. Mn)

Mar-05*Sep-04Sep-03Sep-02Particulars

1.080.97--Earning Per Share

8.5%7.6%-3.9%Net Profit Margin (%)

174.5 149.7 (58.2)Net Profit (Rs. Mn)

11.1%9.7%5.9%Operating Profit Margin (%)

229 190 87 Operating Profit (Rs. Mn)

2,0591,9621,483Net Income (Rs. Mn)

Jun 2005 Mar 2005 Dec 2004 Particulars

Annual

Quarterly

Stable Operating Margins even during downturn

Revenues up by 38% to Rs 2,059.1mn in Jun’05 with improved value realizations

* 6 months annualized

Clothiers to the Nation Today…the World Tomorrow

SKNL

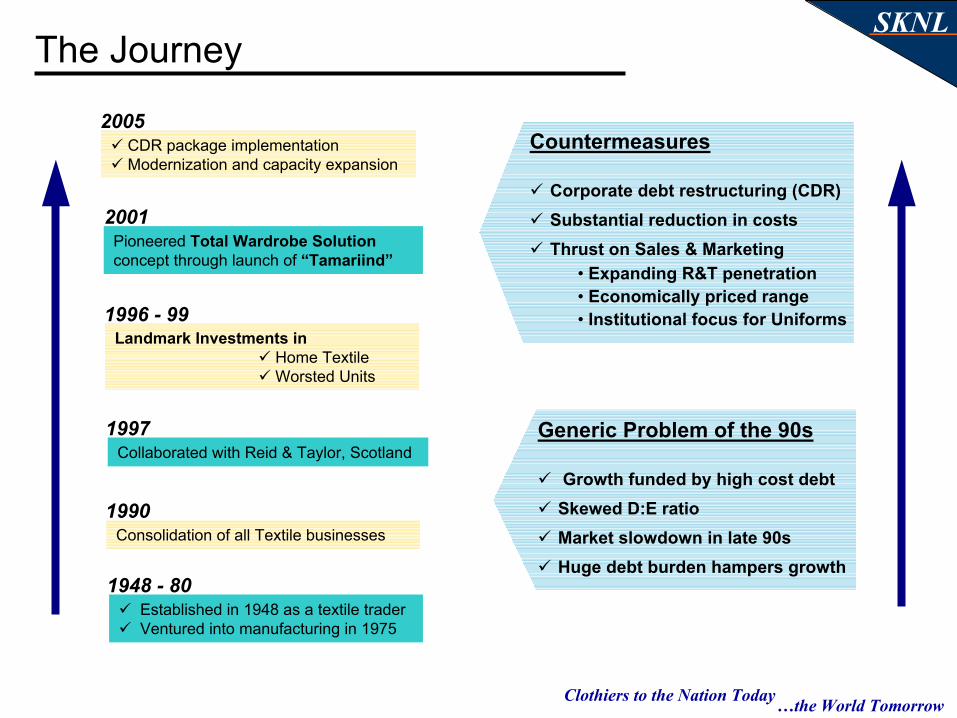

Consolidation of all Textile businesses1990

1997Collaborated with Reid & Taylor, Scotland

1996 - 99Landmark Investments in

Home Textile Worsted Units

2001Pioneered Total Wardrobe Solutionconcept through launch of “Tamariind”

2005CDR package implementationModernization and capacity expansion

1948 - 80Established in 1948 as a textile trader Ventured into manufacturing in 1975

The Journey

Countermeasures

Corporate debt restructuring (CDR)Substantial reduction in costsThrust on Sales & Marketing

• Expanding R&T penetration• Economically priced range• Institutional focus for Uniforms

Generic Problem of the 90s

Growth funded by high cost debtSkewed D:E ratioMarket slowdown in late 90sHuge debt burden hampers growth

Clothiers to the Nation Today…the World Tomorrow

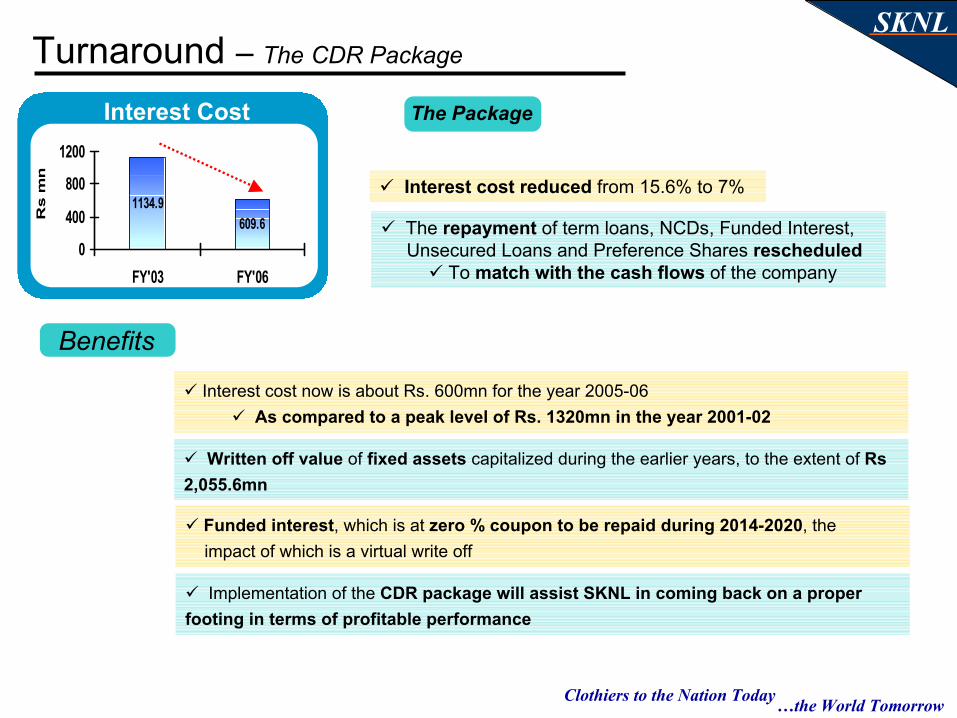

SKNLTurnaround – The CDR Package

Interest cost reduced from 15.6% to 7%1134.9

609.6

0

400

800

1200

FY'03 FY'06

Rs m

n

Interest Cost The Package

The repayment of term loans, NCDs, Funded Interest, Unsecured Loans and Preference Shares rescheduled

To match with the cash flows of the company

Benefits

Interest cost now is about Rs. 600mn for the year 2005-06 As compared to a peak level of Rs. 1320mn in the year 2001-02

Written off value of fixed assets capitalized during the earlier years, to the extent of Rs 2,055.6mn

Funded interest, which is at zero % coupon to be repaid during 2014-2020, the impact of which is a virtual write off

Implementation of the CDR package will assist SKNL in coming back on a proper footing in terms of profitable performance

Clothiers to the Nation Today…the World Tomorrow

SKNL

An Overview

Key Strengths

Section 1

Section 2

Section 3

Industry OverviewSection 4

Business Profile

Initiatives & DriversSection 5

Financial ReviewSection 6

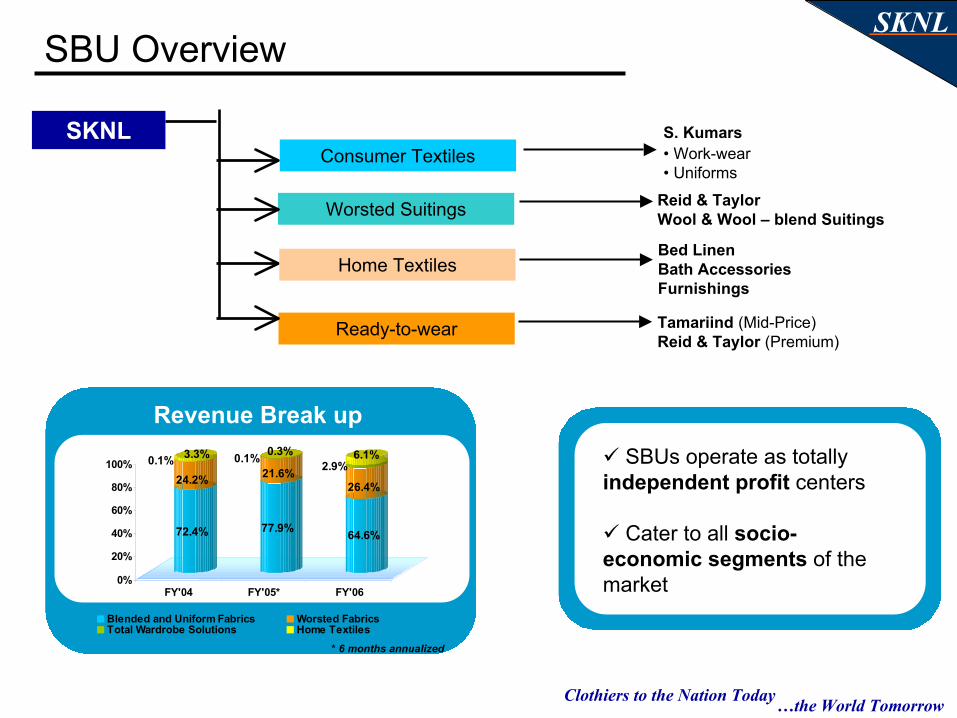

SBU Overview

Consumer Textile

Worsted Suitings

Home Textiles

Ready To Wear

Clothiers to the Nation Today…the World Tomorrow

SKNLSBU Overview

Worsted Suitings Reid & Taylor Wool & Wool – blend Suitings

S. Kumars• Work-wear• Uniforms

Consumer Textiles

Tamariind (Mid-Price)Reid & Taylor (Premium)

Ready-to-wear

Home TextilesBed LinenBath AccessoriesFurnishings

SKNL

SBUs operate as totally independent profit centers

Cater to all socio-economic segments of the market

72.4%

24.2%0.1% 3.3%

77.9%

21.6%0.1% 0.3%

64.6%

26.4%

2.9%6.1%

0%

20%

40%

60%

80%

100%

FY'04 FY'05* FY'06

Blended and Uniform Fabrics Worsted FabricsTotal Wardrobe Solutions Home Textiles

Revenue Break up

* 6 months annualized

Clothiers to the Nation Today…the World Tomorrow

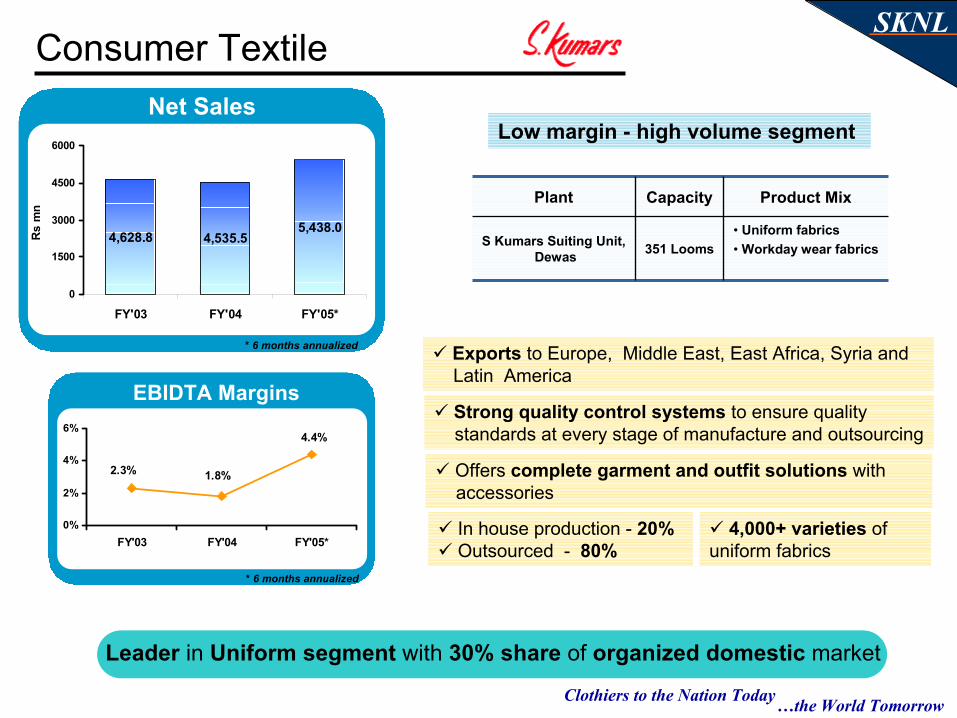

SKNLConsumer Textile

4,628.8 4,535.55,438.0

0

1500

3000

4500

6000

FY'03 FY'04 FY'05*

Rs

mn

Net Sales

* 6 months annualized

EBIDTA Margins

* 6 months annualized

Leader in Uniform segment with 30% share of organized domestic market

• Uniform fabrics• Workday wear fabrics351 LoomsS Kumars Suiting Unit,

Dewas

Product MixCapacityPlant

2.3% 1.8%

4.4%

0%

2%

4%

6%

FY'03 FY'04 FY'05*

Offers complete garment and outfit solutions with accessories

Exports to Europe, Middle East, East Africa, Syria and Latin America

4,000+ varieties of uniform fabrics

In house production - 20%Outsourced - 80%

Low margin - high volume segment

Strong quality control systems to ensure quality standards at every stage of manufacture and outsourcing

Clothiers to the Nation Today…the World Tomorrow

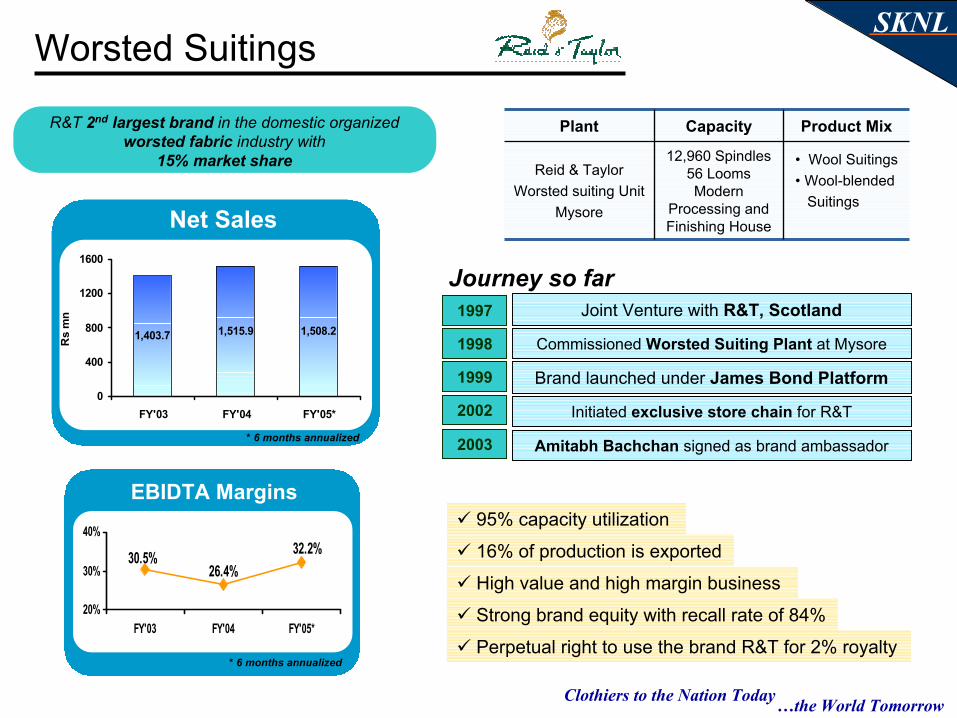

SKNLWorsted Suitings

1,403.7 1,515.9 1,508.2

0

400

800

1200

1600

FY'03 FY'04 FY'05*

Rs

mn

* 6 months annualized

* 6 months annualized

EBIDTA Margins

Net Sales

30.5%26.4%

32.2%

20%

30%

40%

FY'03 FY'04 FY'05*

• Wool Suitings• Wool-blended

Suitings

12,960 Spindles 56 Looms Modern

Processing and Finishing House

Reid & Taylor Worsted suiting Unit

Mysore

Product MixCapacityPlantR&T 2nd largest brand in the domestic organized worsted fabric industry with

15% market share

High value and high margin business

Brand launched under James Bond Platform

Joint Venture with R&T, Scotland

Commissioned Worsted Suiting Plant at Mysore

Strong brand equity with recall rate of 84%

1997

1998

1999

Journey so far

2002 Initiated exclusive store chain for R&T

95% capacity utilization

16% of production is exported

2003 Amitabh Bachchan signed as brand ambassador

Perpetual right to use the brand R&T for 2% royalty

Clothiers to the Nation Today…the World Tomorrow

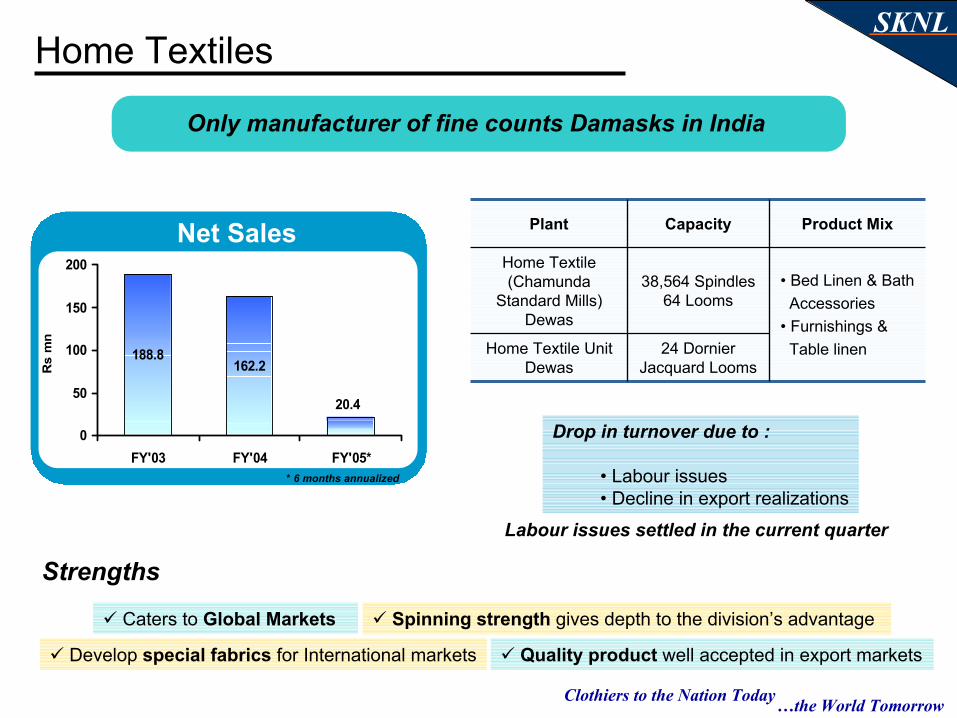

SKNLHome Textiles

Net Sales

188.8162.2

20.4

0

50

100

150

200

FY'03 FY'04 FY'05*

Rs

mn

* 6 months annualized

24 Dornier Jacquard Looms

Home Textile Unit Dewas

• Bed Linen & Bath Accessories

• Furnishings & Table linen

38,564 Spindles 64 Looms

Home Textile (Chamunda

Standard Mills) Dewas

Product MixCapacityPlant

Caters to Global Markets

Develop special fabrics for International markets

Only manufacturer of fine counts Damasks in India

Quality product well accepted in export markets

Drop in turnover due to :

• Labour issues• Decline in export realizations

Labour issues settled in the current quarter

Spinning strength gives depth to the division’s advantage

Strengths

Clothiers to the Nation Today…the World Tomorrow

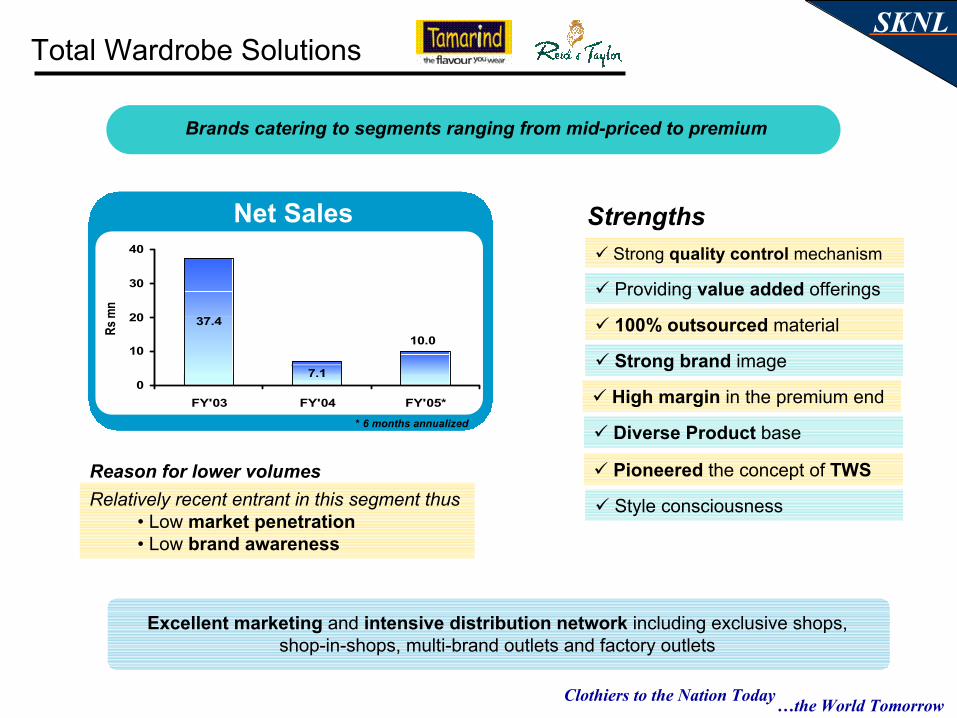

SKNLTotal Wardrobe Solutions

Net Sales

* 6 months annualized

37.4

7.1

10.0

0

10

20

30

40

FY'03 FY'04 FY'05*

Rs m

n

Pioneered the concept of TWS

Brands catering to segments ranging from mid-priced to premium

Diverse Product base

Providing value added offerings

100% outsourced material

Strong brand image

High margin in the premium end

Excellent marketing and intensive distribution network including exclusive shops, shop-in-shops, multi-brand outlets and factory outlets

Strong quality control mechanism

Style consciousnessRelatively recent entrant in this segment thus• Low market penetration• Low brand awareness

Reason for lower volumes

Strengths

Clothiers to the Nation Today…the World Tomorrow

SKNL

An Overview

Key Strengths

Section 1

Section 2

Section 3

Industry OverviewSection 4

Business Profile

Initiatives & DriversSection 5

Financial ReviewSection 6

Strong Brands

Human Capital

Manufacturing

Distribution & Market Reach

Clothiers to the Nation Today…the World Tomorrow

SKNLStrong Brands

#2 in Worsted Fabrics (15% share)• Worsted fabrics• Ready-to-wear

Pioneered Total Wardrobe Solutions in India• Ready-to-wear

Market leader in uniforms (30% share)• Blended fabrics• Workwear• School Uniforms

AchievementsProductsBrand

Clothiers to the Nation Today…the World Tomorrow

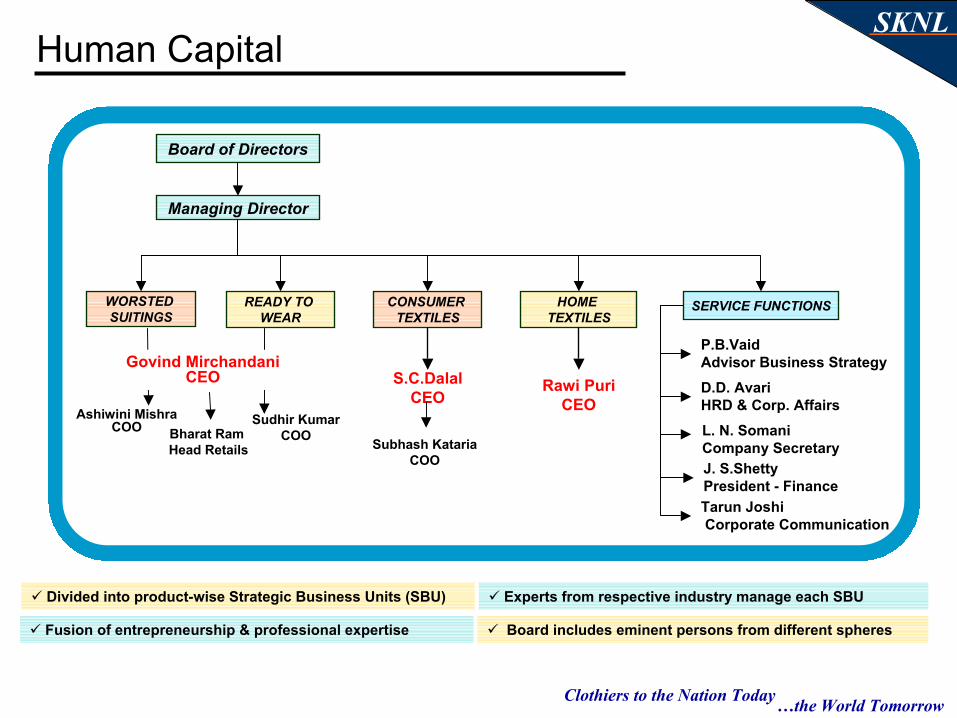

SKNLHuman Capital

Board of Directors

Managing Director

P.B.Vaid Advisor Business Strategy

SERVICE FUNCTIONS

D.D. AvariHRD & Corp. Affairs

J. S.ShettyPresident - FinanceTarun JoshiCorporate Communication

L. N. SomaniCompany Secretary

WORSTED SUITINGS

CONSUMER TEXTILES

READY TO WEAR

Sudhir Kumar COO

S.C.Dalal CEO

Rawi Puri CEO

Subhash Kataria COO

Bharat Ram Head Retails

Govind Mirchandani CEO

Ashiwini Mishra COO

HOME TEXTILES

Divided into product-wise Strategic Business Units (SBU)

Fusion of entrepreneurship & professional expertise Board includes eminent persons from different spheres

Experts from respective industry manage each SBU

Clothiers to the Nation Today…the World Tomorrow

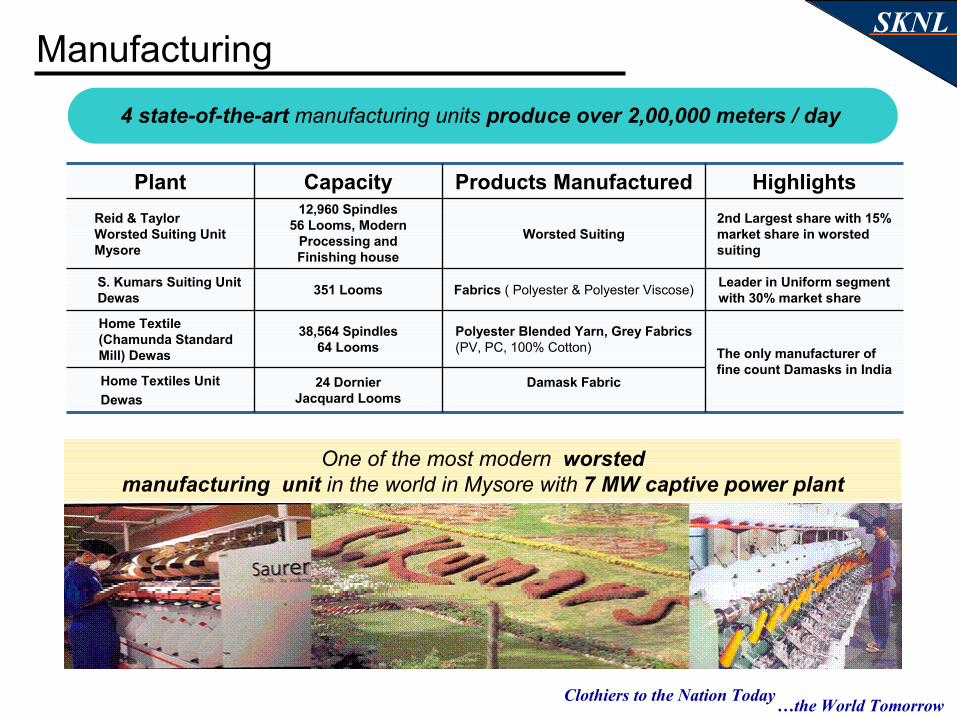

SKNLManufacturing

Damask Fabric

Polyester Blended Yarn, Grey Fabrics (PV, PC, 100% Cotton)

Fabrics ( Polyester & Polyester Viscose)

Worsted Suiting

Products Manufactured2nd Largest share with 15% market share in worsted suiting

12,960 Spindles 56 Looms, Modern

Processing and Finishing house

Reid & Taylor Worsted Suiting Unit Mysore

The only manufacturer of fine count Damasks in India

38,564 Spindles 64 Looms

Home Textile (Chamunda Standard Mill) Dewas

Leader in Uniform segment with 30% market share 351 LoomsS. Kumars Suiting Unit

Dewas

24 Dornier Jacquard Looms

Home Textiles Unit Dewas

Highlights CapacityPlant

4 state-of-the-art manufacturing units produce over 2,00,000 meters / day

One of the most modern worsted manufacturing unit in the world in Mysore with 7 MW captive power plant

Clothiers to the Nation Today…the World Tomorrow

SKNLDistribution & Market Reach

Penetrative distribution network in Domestic & International Markets

• Over 300 dealers & 30,000 retail outlets across 300 cities in India– Network of Agents servicing the mills

• Largest institutional supplier (organized sector)

• Reid & Taylor, Scotland – Channel to Global Markets

– Access to top brands worldwide (Prada, Brioni, Hackett, Dunhill, Kiton etc.)

• Exclusive stores for Reid & Taylor– 16 in operation & 10 under fit outs

Clothiers to the Nation Today…the World Tomorrow

SKNL

An Overview

Key Strengths

Section 1

Section 2

Section 3

Industry OverviewSection 4

Business Profile

Initiatives & DriversSection 5

Financial ReviewSection 6

Overview

Emerging opportunities

Clothiers to the Nation Today…the World Tomorrow

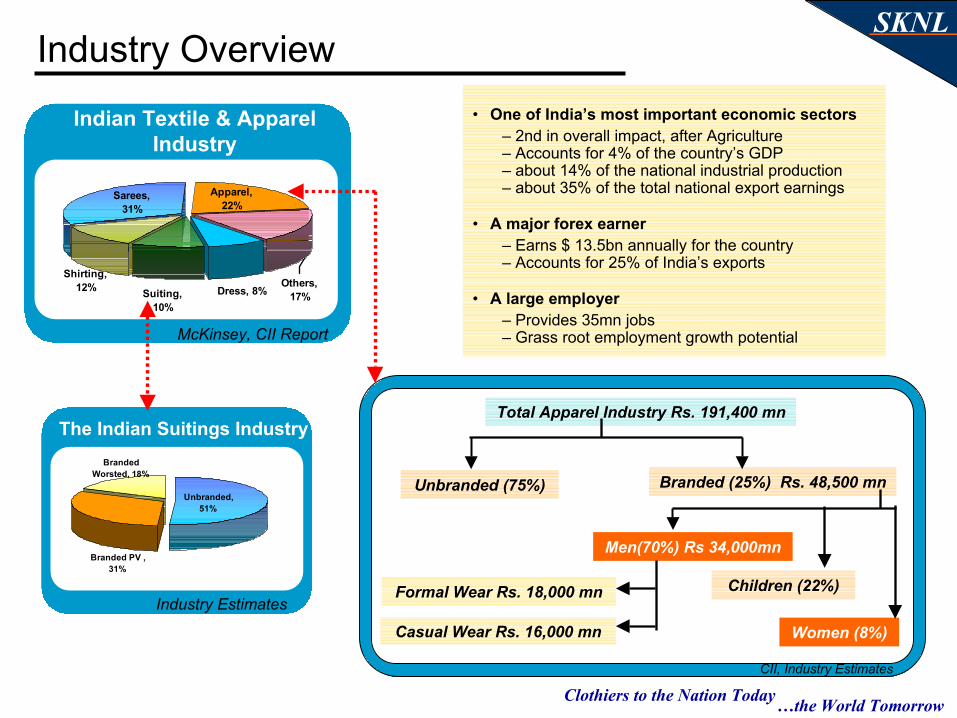

SKNLIndustry Overview

McKinsey, CII Report

Industry Estimates

Others, 17%

Sarees, 31%

Dress, 8%

Apparel, 22%

Shirting, 12% Suiting,

10%

Indian Textile & Apparel Industry

The Indian Suitings Industry

Unbranded, 51%

Branded Worsted, 18%

Branded PV , 31%

CII, Industry Estimates

Total Apparel Industry Rs. 191,400 mn

Unbranded (75%) Branded (25%) Rs. 48,500 mn

Men(70%) Rs 34,000mn

Women (8%)

Children (22%)Formal Wear Rs. 18,000 mn

Casual Wear Rs. 16,000 mn

• One of India’s most important economic sectors– 2nd in overall impact, after Agriculture– Accounts for 4% of the country’s GDP– about 14% of the national industrial production – about 35% of the total national export earnings

• A major forex earner– Earns $ 13.5bn annually for the country– Accounts for 25% of India’s exports

• A large employer– Provides 35mn jobs– Grass root employment growth potential

Clothiers to the Nation Today…the World Tomorrow

SKNL

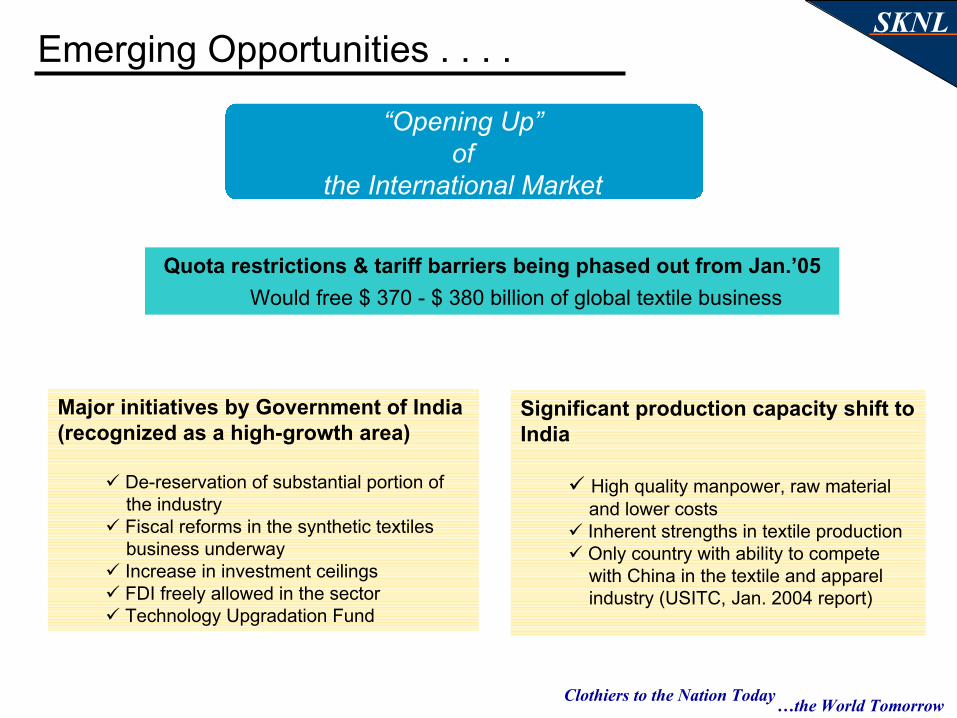

Major initiatives by Government of India (recognized as a high-growth area)

De-reservation of substantial portion of the industryFiscal reforms in the synthetic textiles business underwayIncrease in investment ceilingsFDI freely allowed in the sectorTechnology Upgradation Fund

Significant production capacity shift to India

High quality manpower, raw material and lower costsInherent strengths in textile productionOnly country with ability to compete with China in the textile and apparel industry (USITC, Jan. 2004 report)

“Opening Up” of

the International Market

Emerging Opportunities . . . .

Quota restrictions & tariff barriers being phased out from Jan.’05Would free $ 370 - $ 380 billion of global textile business

Clothiers to the Nation Today…the World Tomorrow

SKNL

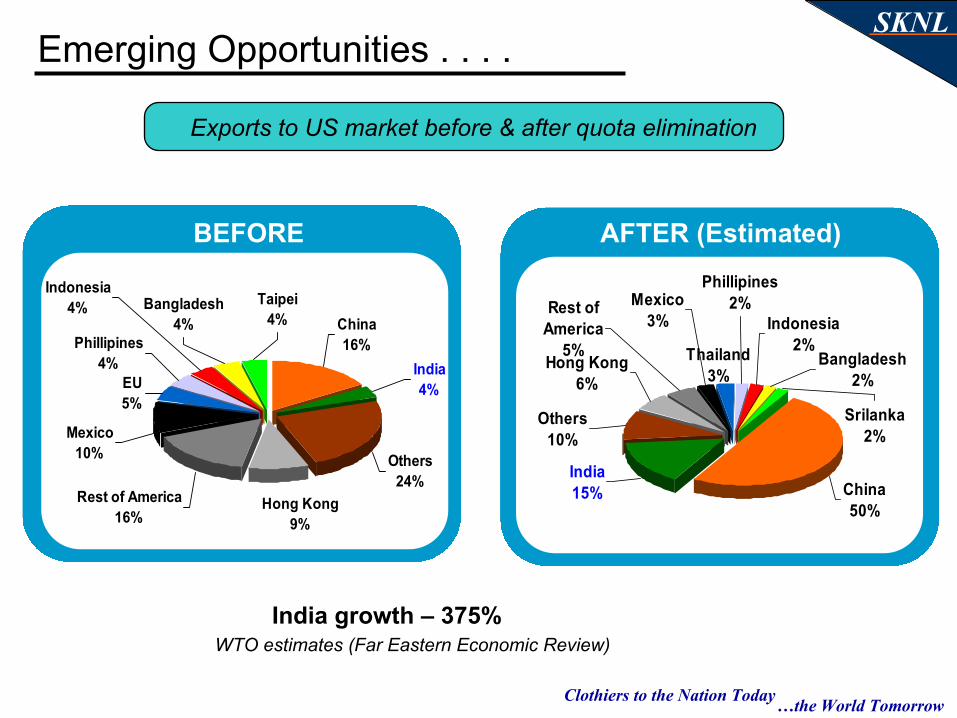

Exports to US market before & after quota elimination

Emerging Opportunities . . . .

China16%

India4%

Others24%

Hong Kong9%

Rest of America16%

Mexico10%

EU5%

Phillipines4%

Indonesia4% Bangladesh

4%Taipei

4%

China50%

India15%

Others10%

Hong Kong6%

Rest of America

5%

Mexico3%

Thailand3%

Phillipines2%

Indonesia2%

Bangladesh2%

Srilanka2%

BEFORE AFTER (Estimated)

India growth – 375%WTO estimates (Far Eastern Economic Review)

Clothiers to the Nation Today…the World Tomorrow

SKNL

An OverviewSection 1

Section 2

Section 3

Industry OverviewSection 4

Business Profile

Initiatives & DriversSection 5

Financial ReviewSection 6

Growth in Existing SBU’s

Key Strengths

Investment Plan

Foray into HVFC

Export Thrust

Growth Drivers (Summary)

Retail Expansion

Strengthening coverage

Clothiers to the Nation Today…the World Tomorrow

SKNL

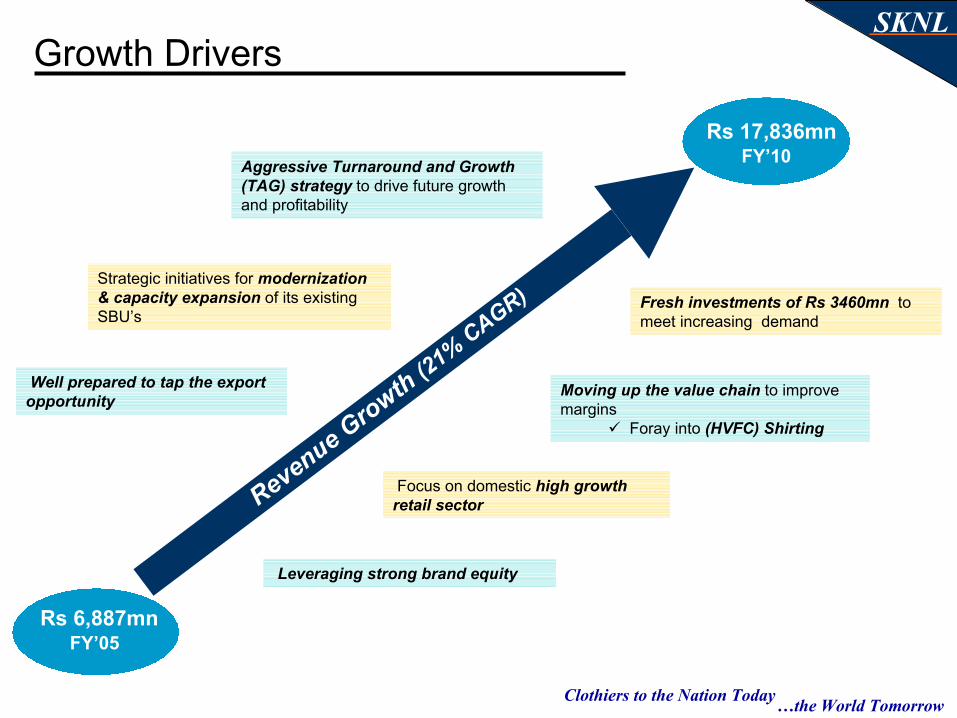

FY’10Rs 17,836mn

FY’05Rs 6,887mn

Growth Drivers

Aggressive Turnaround and Growth (TAG) strategy to drive future growth and profitability

Fresh investments of Rs 3460mn to meet increasing demand

Strategic initiatives for modernization & capacity expansion of its existing SBU’s

Moving up the value chain to improve margins

Foray into (HVFC) Shirting

Well prepared to tap the export opportunity

Focus on domestic high growth retail sector

Leveraging strong brand equity

Revenue Growth (21% CAGR)

Clothiers to the Nation Today…the World Tomorrow

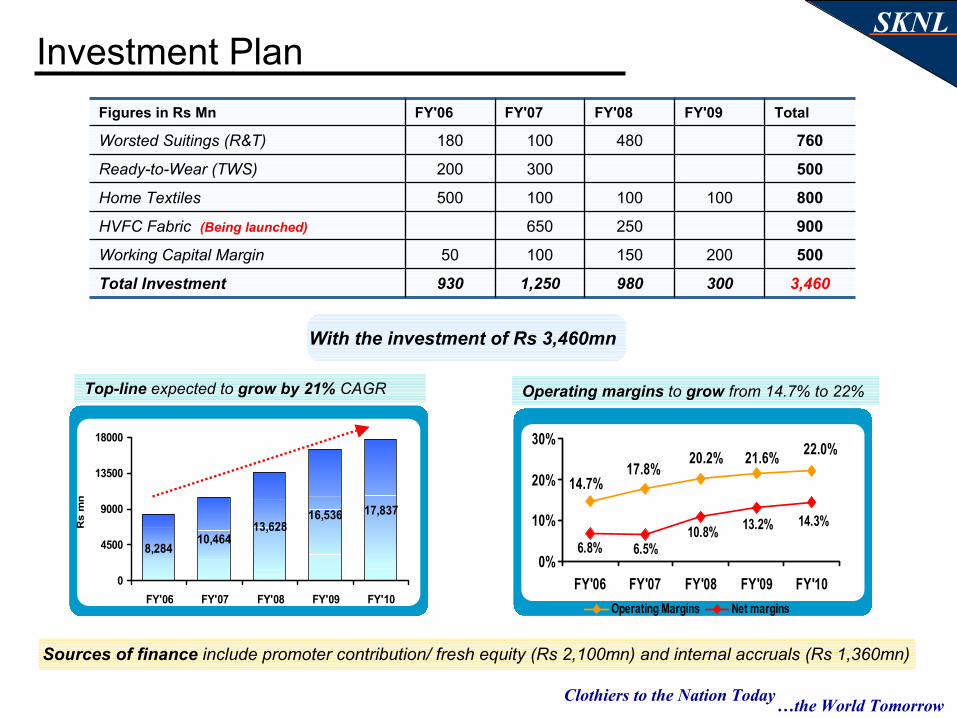

SKNLInvestment Plan

3,4603009801,250930Total Investment

50020015010050Working Capital Margin

900250650HVFC Fabric (Being launched)

800100100100500Home Textiles

500300200Ready-to-Wear (TWS)

760480100180Worsted Suitings (R&T)

Total FY'09FY'08FY'07FY'06Figures in Rs Mn

Sources of finance include promoter contribution/ fresh equity (Rs 2,100mn) and internal accruals (Rs 1,360mn)

With the investment of Rs 3,460mn

Top-line expected to grow by 21% CAGR Operating margins to grow from 14.7% to 22%

10,46413,628

16,536 17,837

8,284

0

4500

9000

13500

18000

FY'06 FY'07 FY'08 FY'09 FY'10

Rs

mn

22.0%

14.7%17.8%

20.2% 21.6%

14.3%13.2%10.8%6.5%6.8%

0%

10%

20%

30%

FY'06 FY'07 FY'08 FY'09 FY'10Operating Margins Net margins

Clothiers to the Nation Today…the World Tomorrow

SKNL

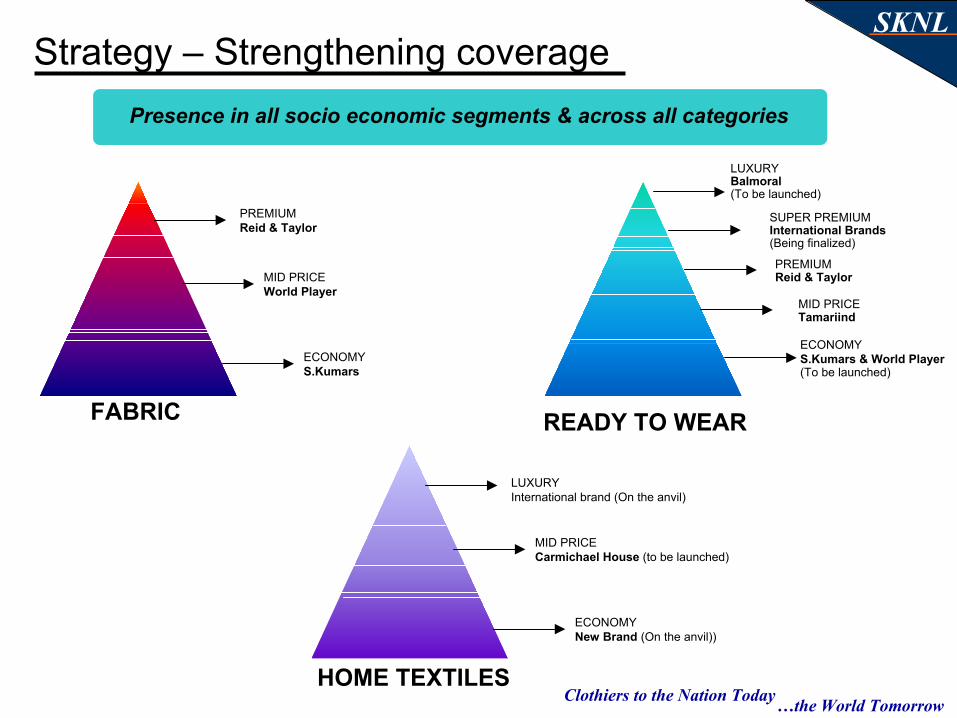

Presence in all socio economic segments & across all categories

MID PRICECarmichael House (to be launched)

ECONOMYNew Brand (On the anvil))

LUXURYInternational brand (On the anvil)

SUPER PREMIUMInternational Brands(Being finalized)

ECONOMYS.Kumars & World Player(To be launched)

LUXURYBalmoral(To be launched)

PREMIUMReid & Taylor

MID PRICE Tamariind

MID PRICEWorld Player

ECONOMYS.Kumars

PREMIUMReid & Taylor

READY TO WEAR

HOME TEXTILES

FABRIC

Strategy – Strengthening coverage

Clothiers to the Nation Today…the World Tomorrow

SKNL

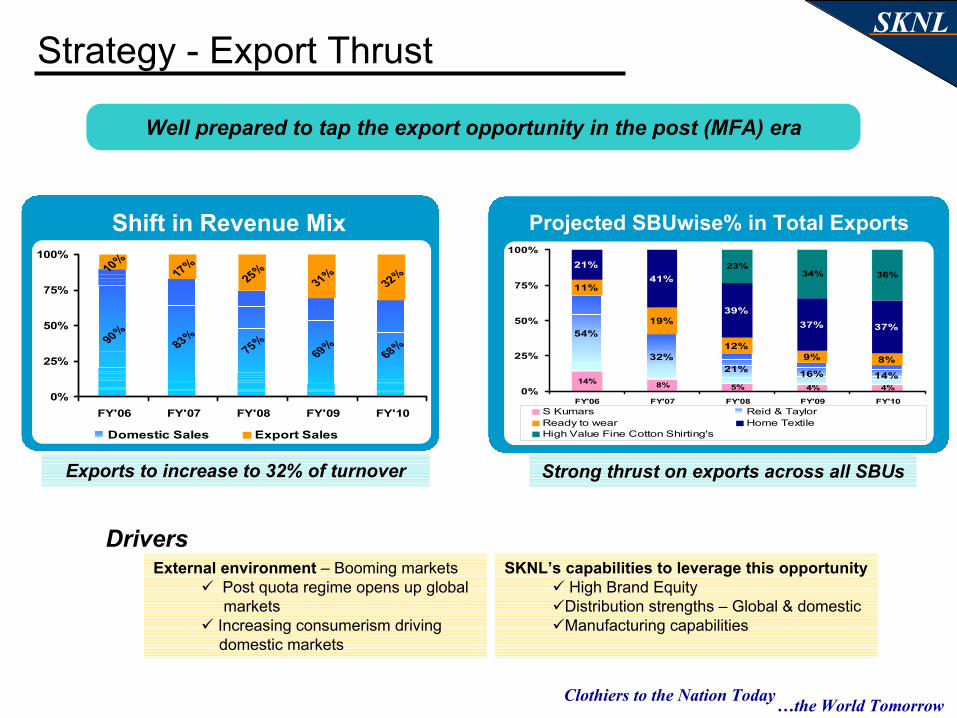

14% 8% 5% 4% 4%

54%

32%21% 16% 14%

11%

19%

12%9% 8%

21%41%

39%37% 37%

34% 36%23%

0%

25%

50%

75%

100%

FY'06 FY'07 FY'08 FY'09 FY'10S Kumars Reid & TaylorReady to wear Home TextileHigh Value Fine Cotton Shirting's

Projected SBUwise% in Total Exports

Strong thrust on exports across all SBUs

Well prepared to tap the export opportunity in the post (MFA) era

Drivers

Shift in Revenue Mix

90%

83%

75%

69%

68%

10%

17%

25%

31%

32%

0%

25%

50%

75%

100%

FY'06 FY'07 FY'08 FY'09 FY'10

Domestic Sales Export Sales

Exports to increase to 32% of turnover

SKNL’s capabilities to leverage this opportunityHigh Brand Equity

Distribution strengths – Global & domesticManufacturing capabilities

External environment – Booming marketsPost quota regime opens up global markets

Increasing consumerism driving domestic markets

Strategy - Export Thrust

Clothiers to the Nation Today…the World Tomorrow

SKNL

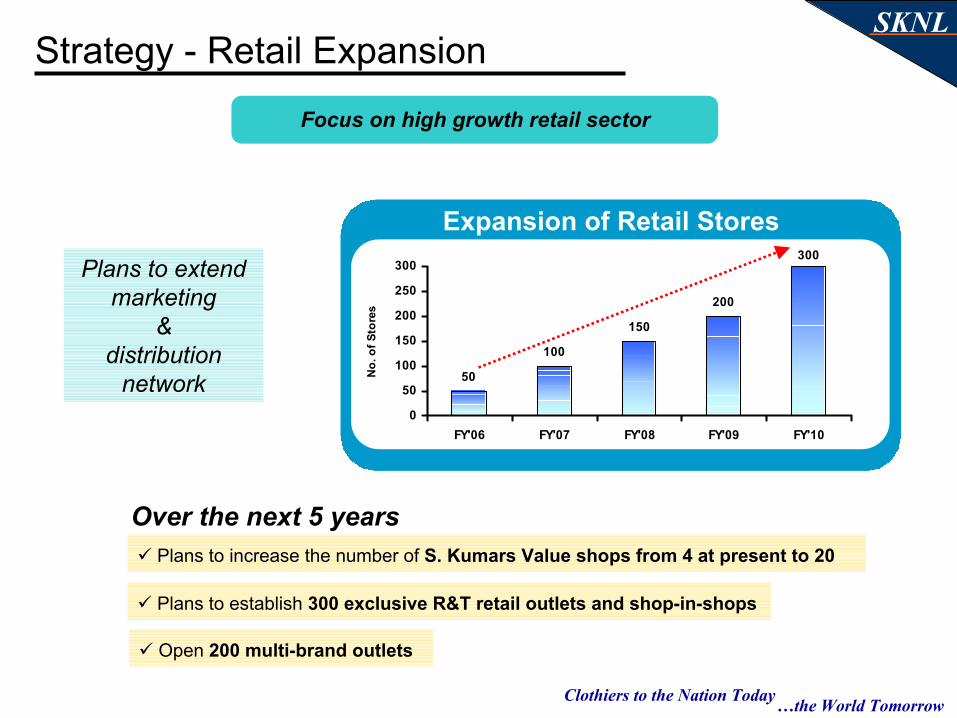

Plans to extend marketing

& distribution

network

Over the next 5 years

50

100

150

200

300

0

50

100

150

200

250

300

FY'06 FY'07 FY'08 FY'09 FY'10

No.

of S

tore

s

Expansion of Retail Stores

Plans to establish 300 exclusive R&T retail outlets and shop-in-shops

Plans to increase the number of S. Kumars Value shops from 4 at present to 20

Open 200 multi-brand outlets

Focus on high growth retail sector

Strategy - Retail Expansion

Clothiers to the Nation Today…the World Tomorrow

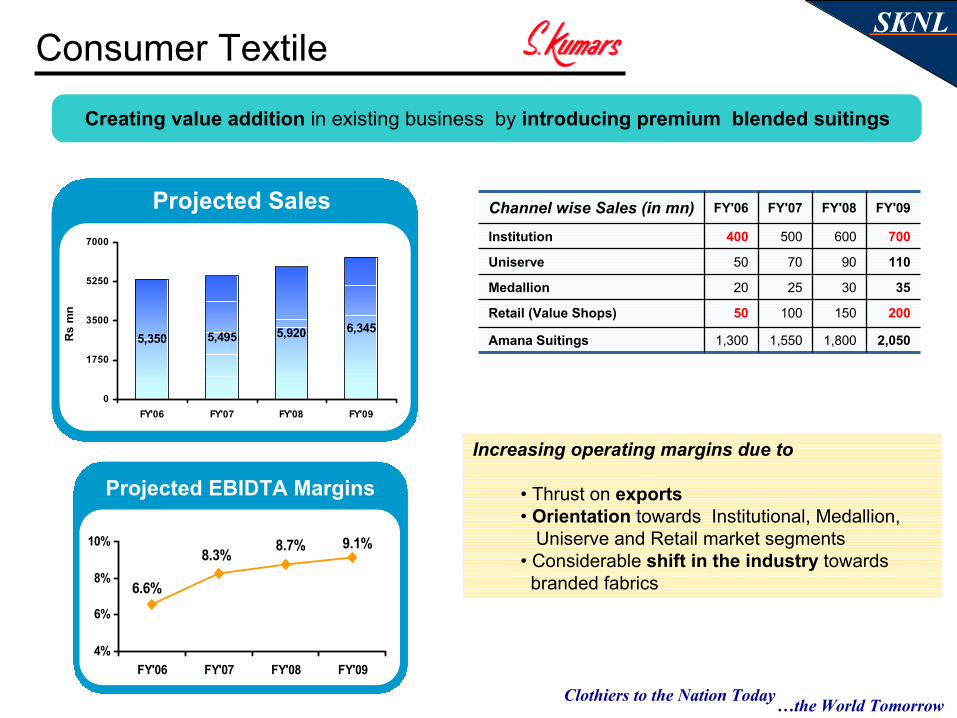

SKNLConsumer Textile

Projected Sales

5,350 5,495 5,920 6,345

0

1750

3500

5250

7000

FY'06 FY'07 FY'08 FY'09

Rs

mn

Projected EBIDTA Margins

2,0501,8001,5501,300Amana Suitings

20015010050Retail (Value Shops)

35302520Medallion

110907050Uniserve

700600500400Institution

FY'09FY'08FY'07FY'06Channel wise Sales (in mn)

6.6%

8.3% 8.7% 9.1%

4%

6%

8%

10%

FY'06 FY'07 FY'08 FY'09

Increasing operating margins due to

• Thrust on exports• Orientation towards Institutional, Medallion,

Uniserve and Retail market segments• Considerable shift in the industry towardsbranded fabrics

Creating value addition in existing business by introducing premium blended suitings

Clothiers to the Nation Today…the World Tomorrow

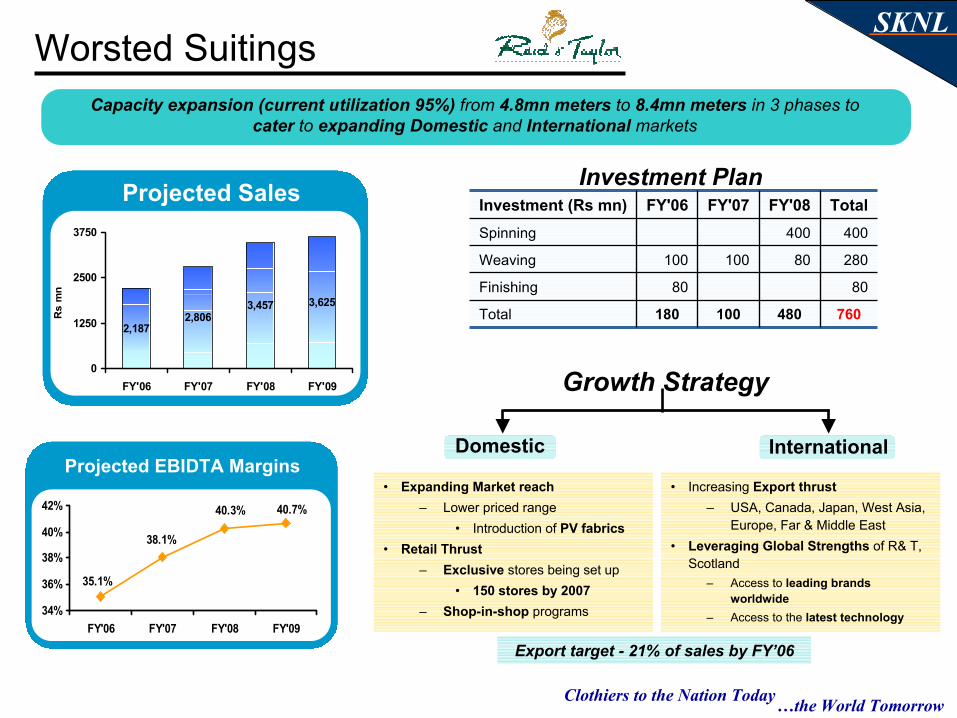

SKNLWorsted Suitings

Projected Sales

2,1872,806

3,457 3,625

0

1250

2500

3750

FY'06 FY'07 FY'08 FY'09

Rs

mn

Projected EBIDTA Margins

760480100180Total

8080Finishing

28080100100Weaving

400400Spinning

TotalFY'08FY'07FY'06Investment (Rs mn)

35.1%

38.1%

40.3% 40.7%

34%

36%

38%

40%

42%

FY'06 FY'07 FY'08 FY'09

Investment Plan

Export target - 21% of sales by FY’06

Capacity expansion (current utilization 95%) from 4.8mn meters to 8.4mn meters in 3 phases to cater to expanding Domestic and International markets

• Expanding Market reach– Lower priced range

• Introduction of PV fabrics• Retail Thrust

– Exclusive stores being set up• 150 stores by 2007

– Shop-in-shop programs

• Increasing Export thrust– USA, Canada, Japan, West Asia,

Europe, Far & Middle East• Leveraging Global Strengths of R& T,

Scotland– Access to leading brands

worldwide– Access to the latest technology

Growth Strategy

InternationalDomestic

Clothiers to the Nation Today…the World Tomorrow

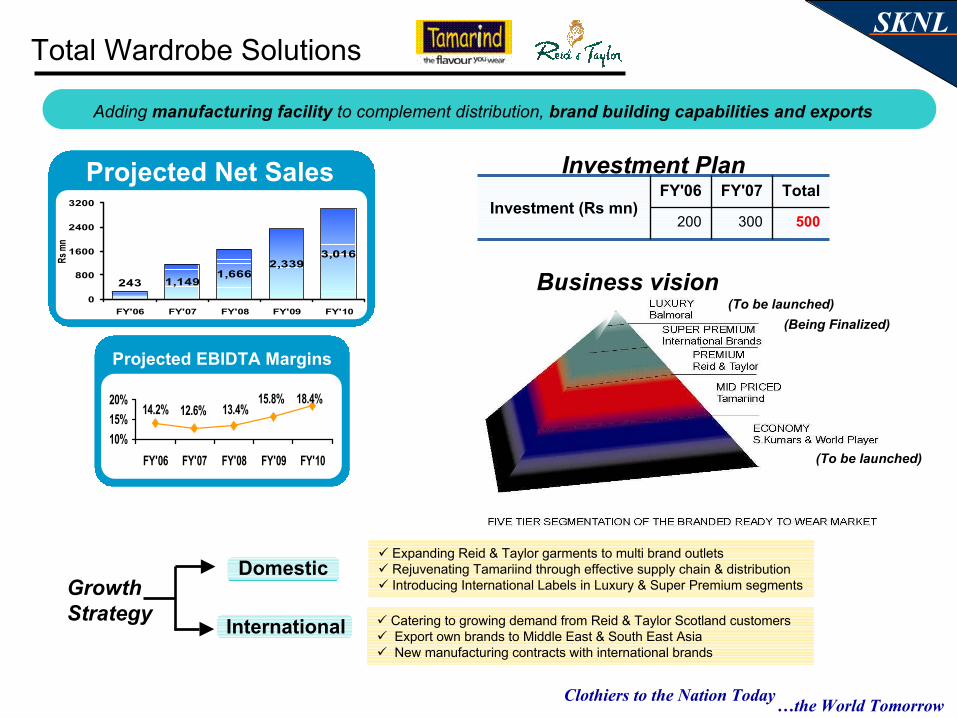

SKNLTotal Wardrobe Solutions

Projected Net Sales

1,1491,666

2,3393,016

2430

800

1600

2400

3200

FY'06 FY'07 FY'08 FY'09 FY'10

Rs m

n

Projected EBIDTA Margins

500300200

TotalFY'07FY'06Investment (Rs mn)

18.4%15.8%13.4%12.6%14.2%

10%15%20%

FY'06 FY'07 FY'08 FY'09 FY'10

Business vision

Investment Plan

(To be launched)(Being Finalized)

(To be launched)

Adding manufacturing facility to complement distribution, brand building capabilities and exports

Expanding Reid & Taylor garments to multi brand outletsRejuvenating Tamariind through effective supply chain & distributionIntroducing International Labels in Luxury & Super Premium segmentsGrowth

Strategy International

Domestic

Catering to growing demand from Reid & Taylor Scotland customersExport own brands to Middle East & South East AsiaNew manufacturing contracts with international brands

Clothiers to the Nation Today…the World Tomorrow

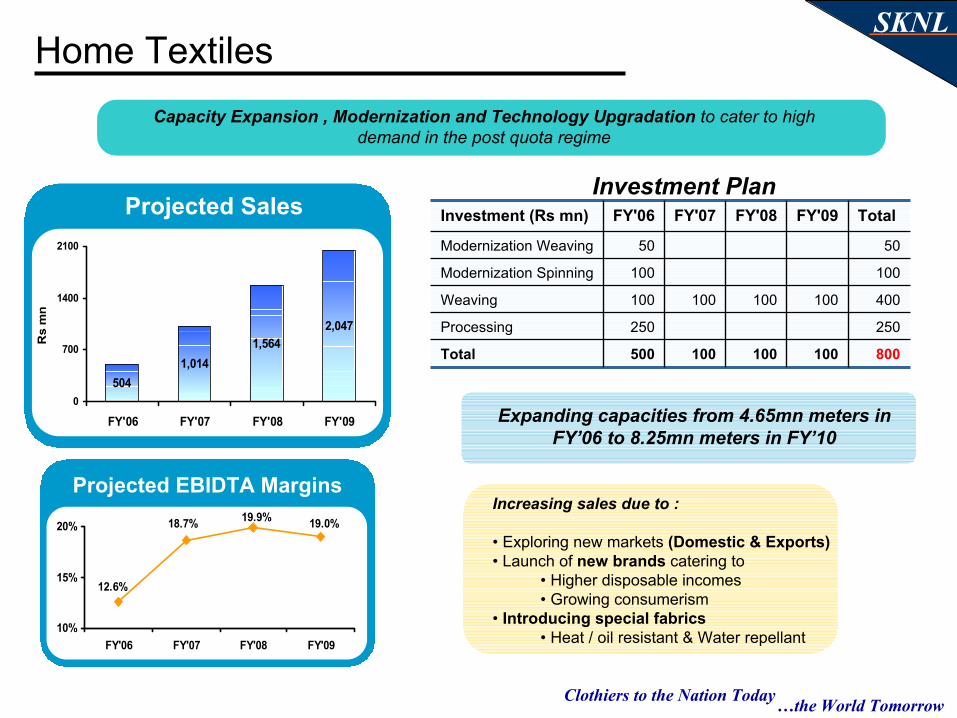

SKNLHome Textiles

Projected Sales

Projected EBIDTA Margins

800100100100500Total

250250Processing

400100100100100Weaving

100100Modernization Spinning

5050Modernization Weaving

Total FY'09FY'08FY'07FY'06Investment (Rs mn)

5041,014

1,5642,047

0

700

1400

2100

FY'06 FY'07 FY'08 FY'09

Rs

mn

19.0%19.9%18.7%

12.6%

10%

15%

20%

FY'06 FY'07 FY'08 FY'09

Investment Plan

Capacity Expansion , Modernization and Technology Upgradation to cater to high demand in the post quota regime

Expanding capacities from 4.65mn meters in FY’06 to 8.25mn meters in FY’10

Increasing sales due to :

• Exploring new markets (Domestic & Exports)• Launch of new brands catering to

• Higher disposable incomes • Growing consumerism

• Introducing special fabrics• Heat / oil resistant & Water repellant

Clothiers to the Nation Today…the World Tomorrow

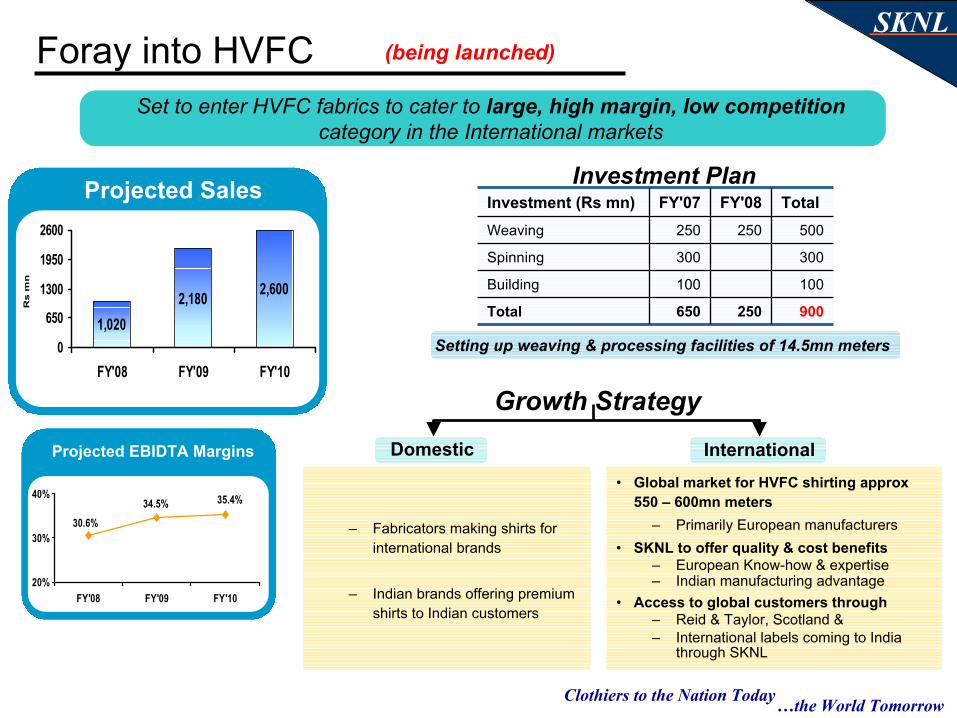

SKNLForay into HVFC

900250650Total

100100Building

300300Spinning

500250250Weaving

Total FY'08FY'07Investment (Rs mn)

Set to enter HVFC fabrics to cater to large, high margin, low competitioncategory in the International markets

Setting up weaving & processing facilities of 14.5mn meters

Investment Plan

(being launched)

Projected Sales

1,0202,180 2,600

0

650

1300

1950

2600

FY'08 FY'09 FY'10

Rs m

n

Projected EBIDTA Margins

35.4%34.5%30.6%

20%

30%

40%

FY'08 FY'09 FY'10

– Fabricators making shirts for international brands

– Indian brands offering premium shirts to Indian customers

• Global market for HVFC shirting approx 550 – 600mn meters

– Primarily European manufacturers• SKNL to offer quality & cost benefits

– European Know-how & expertise– Indian manufacturing advantage

• Access to global customers through– Reid & Taylor, Scotland &– International labels coming to India

through SKNL

Growth Strategy

InternationalDomestic

Clothiers to the Nation Today…the World Tomorrow

SKNL

An Overview

Key Strengths

Section 1

Section 2

Section 3

Industry OverviewSection 4

Business Profile

Initiatives & DriversSection 5

Financial ReviewSection 6

Annual Performance Trend

Quarterly Performance Trend

Clothiers to the Nation Today…the World Tomorrow

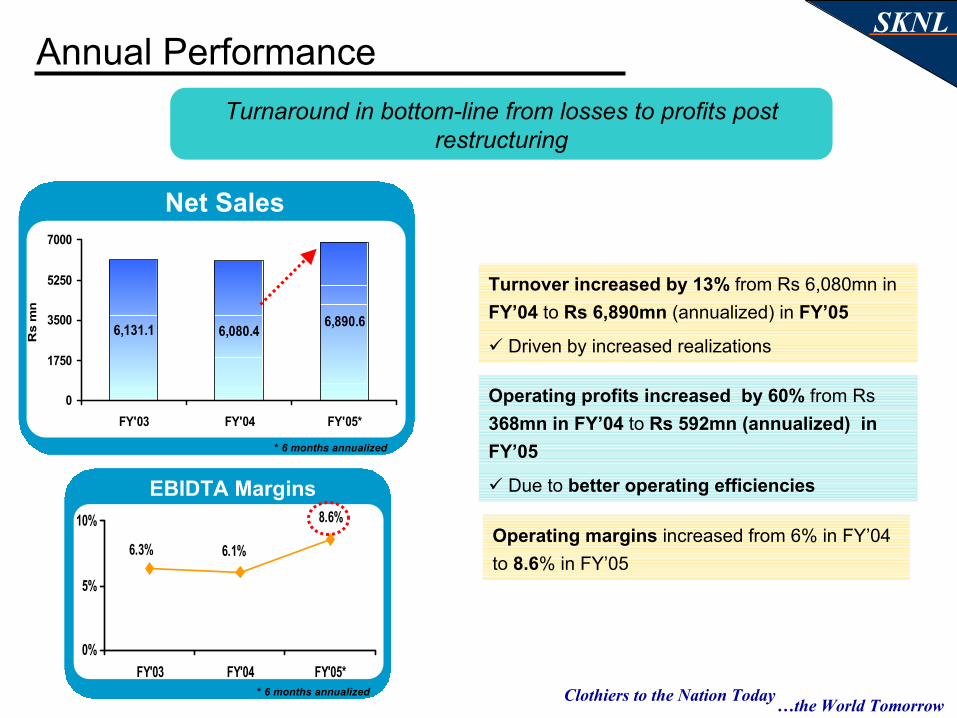

SKNLAnnual Performance

Net Sales

* 6 months annualized

6,131.1 6,080.4 6,890.6

0

1750

3500

5250

7000

FY'03 FY'04 FY'05*

Rs

mn

EBIDTA Margins

* 6 months annualized

6.3% 6.1%

8.6%

0%

5%

10%

FY'03 FY'04 FY'05*

Turnover increased by 13% from Rs 6,080mn in FY’04 to Rs 6,890mn (annualized) in FY’05

Driven by increased realizations

Turnaround in bottom-line from losses to profits post restructuring

Operating profits increased by 60% from Rs 368mn in FY’04 to Rs 592mn (annualized) in FY’05

Due to better operating efficiencies

Operating margins increased from 6% in FY’04 to 8.6% in FY’05

Clothiers to the Nation Today…the World Tomorrow

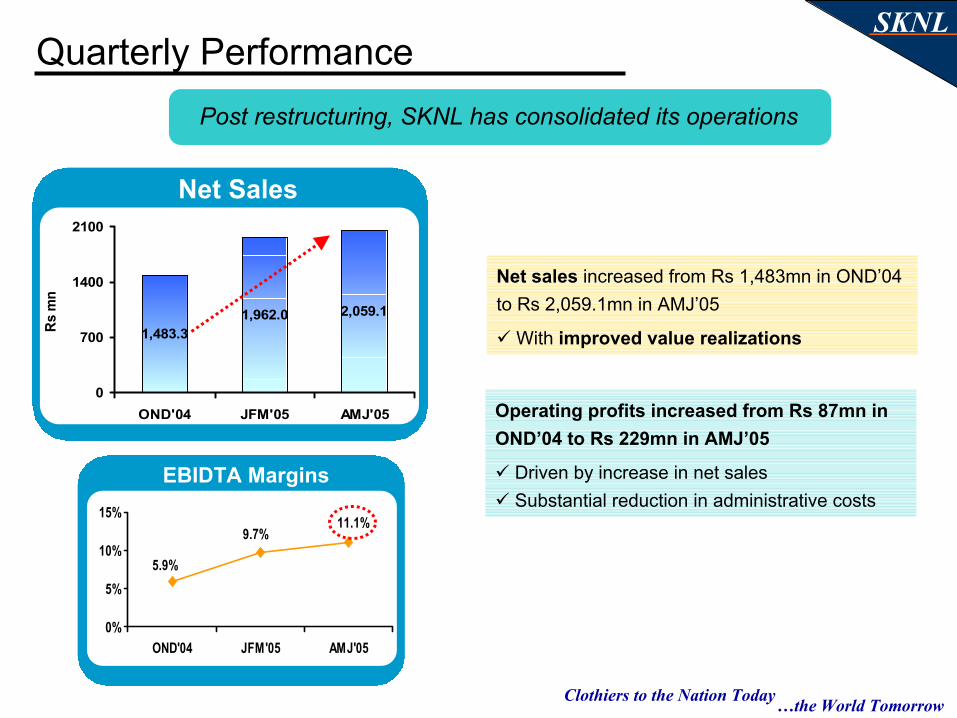

SKNLQuarterly Performance

Net Sales

EBIDTA Margins

5.9%

9.7%11.1%

0%

5%

10%

15%

OND'04 JFM'05 AMJ'05

1,483.31,962.0 2,059.1

0

700

1400

2100

OND'04 JFM'05 AMJ'05

Rs m

n

Net sales increased from Rs 1,483mn in OND’04 to Rs 2,059.1mn in AMJ’05

With improved value realizations

Post restructuring, SKNL has consolidated its operations

Operating profits increased from Rs 87mn in OND’04 to Rs 229mn in AMJ’05

Driven by increase in net salesSubstantial reduction in administrative costs

Clothiers to the Nation Today…the World Tomorrow

SKNL

Annexure

Clothiers to the Nation Today…the World Tomorrow

SKNL

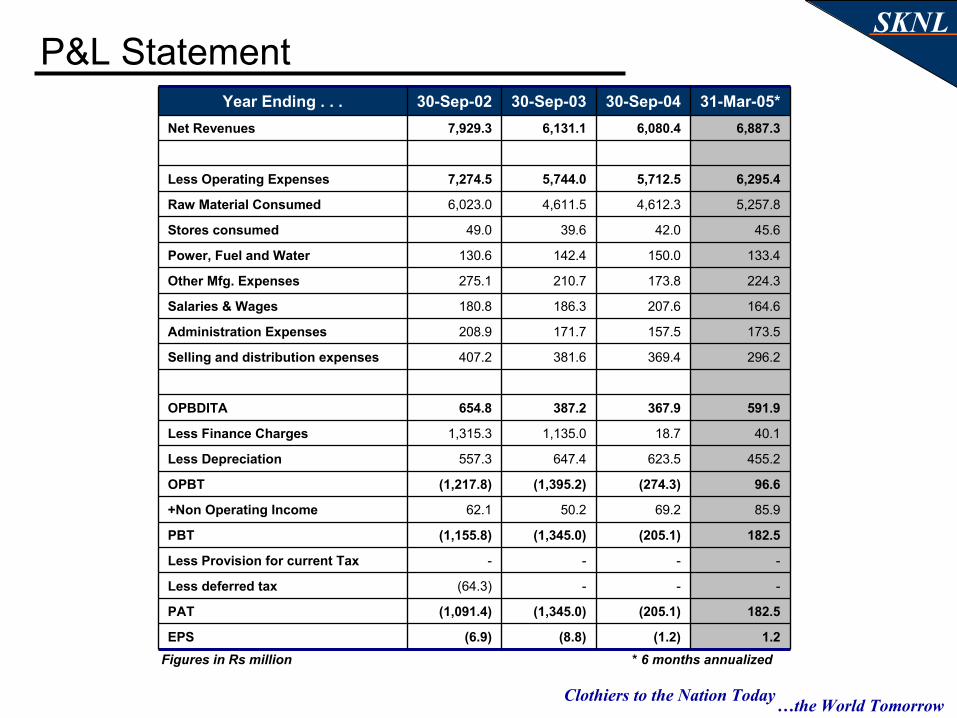

1.2(1.2)(8.8)(6.9)EPS

182.5(205.1)(1,345.0)(1,091.4)PAT

---(64.3)Less deferred tax

----Less Provision for current Tax

182.5(205.1)(1,345.0)(1,155.8)PBT

85.969.250.262.1+Non Operating Income

96.6(274.3)(1,395.2)(1,217.8)OPBT

455.2623.5647.4557.3Less Depreciation

40.118.71,135.01,315.3Less Finance Charges

591.9367.9387.2654.8OPBDITA

296.2369.4381.6407.2Selling and distribution expenses

173.5157.5171.7208.9Administration Expenses

164.6207.6186.3180.8Salaries & Wages

224.3173.8210.7275.1Other Mfg. Expenses

133.4150.0142.4130.6Power, Fuel and Water

45.642.039.649.0Stores consumed

5,257.84,612.34,611.56,023.0Raw Material Consumed

6,295.45,712.55,744.07,274.5Less Operating Expenses

6,887.36,080.46,131.17,929.3Net Revenues

31-Mar-05*30-Sep-0430-Sep-0330-Sep-02Year Ending . . .

P&L Statement

Figures in Rs million * 6 months annualized

Clothiers to the Nation Today…the World Tomorrow

SKNL

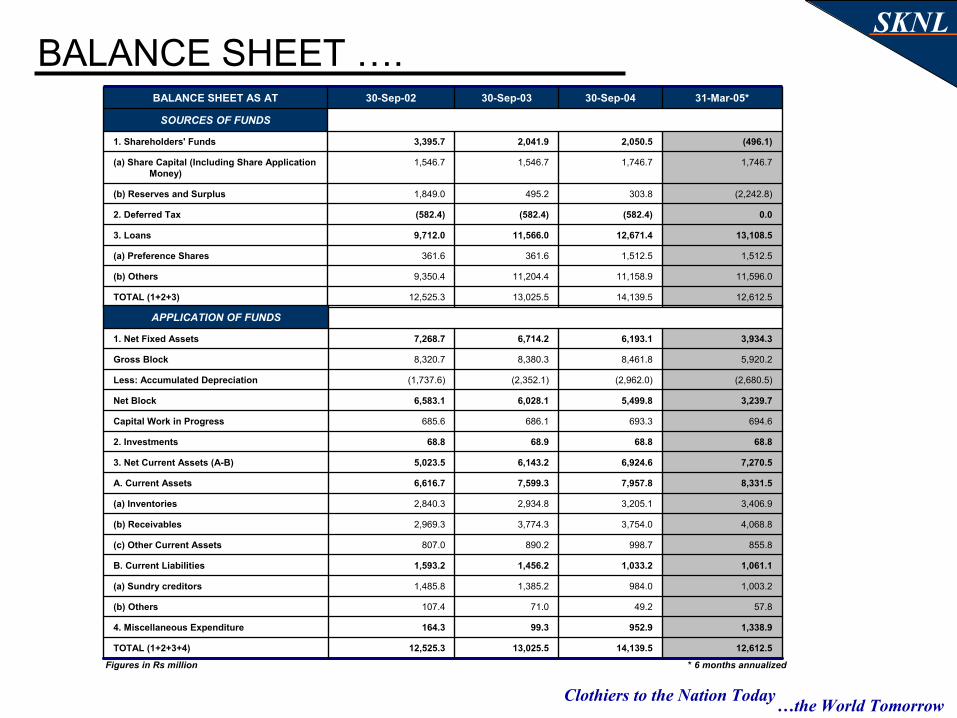

12,612.5 14,139.5 13,025.5 12,525.3 TOTAL (1+2+3)

11,596.0 11,158.9 11,204.4 9,350.4 (b) Others

1,512.5 1,512.5 361.6 361.6 (a) Preference Shares

13,108.5 12,671.4 11,566.0 9,712.0 3. Loans

0.0 (582.4)(582.4)(582.4)2. Deferred Tax

(2,242.8)303.8 495.2 1,849.0 (b) Reserves and Surplus

1,746.7 1,746.7 1,546.7 1,546.7 (a) Share Capital (Including Share Application Money)

(496.1)2,050.5 2,041.9 3,395.7 1. Shareholders' Funds

SOURCES OF FUNDS

31-Mar-05*30-Sep-0430-Sep-0330-Sep-02BALANCE SHEET AS AT

BALANCE SHEET ….

Figures in Rs million * 6 months annualized

12,612.5 14,139.5 13,025.5 12,525.3 TOTAL (1+2+3+4)

1,338.9 952.9 99.3 164.3 4. Miscellaneous Expenditure

57.8 49.2 71.0 107.4 (b) Others

1,003.2 984.0 1,385.2 1,485.8 (a) Sundry creditors

1,061.1 1,033.2 1,456.2 1,593.2 B. Current Liabilities

855.8 998.7 890.2 807.0 (c) Other Current Assets

4,068.8 3,754.0 3,774.3 2,969.3 (b) Receivables

3,406.9 3,205.1 2,934.8 2,840.3 (a) Inventories

8,331.5 7,957.8 7,599.3 6,616.7 A. Current Assets

7,270.5 6,924.6 6,143.2 5,023.5 3. Net Current Assets (A-B)

68.8 68.8 68.9 68.8 2. Investments

694.6 693.3 686.1 685.6 Capital Work in Progress

3,239.7 5,499.8 6,028.1 6,583.1 Net Block

(2,680.5)(2,962.0)(2,352.1)(1,737.6)Less: Accumulated Depreciation

5,920.2 8,461.8 8,380.3 8,320.7 Gross Block

3,934.3 6,193.1 6,714.2 7,268.7 1. Net Fixed Assets

APPLICATION OF FUNDS

Clothiers to the Nation Today…the World Tomorrow

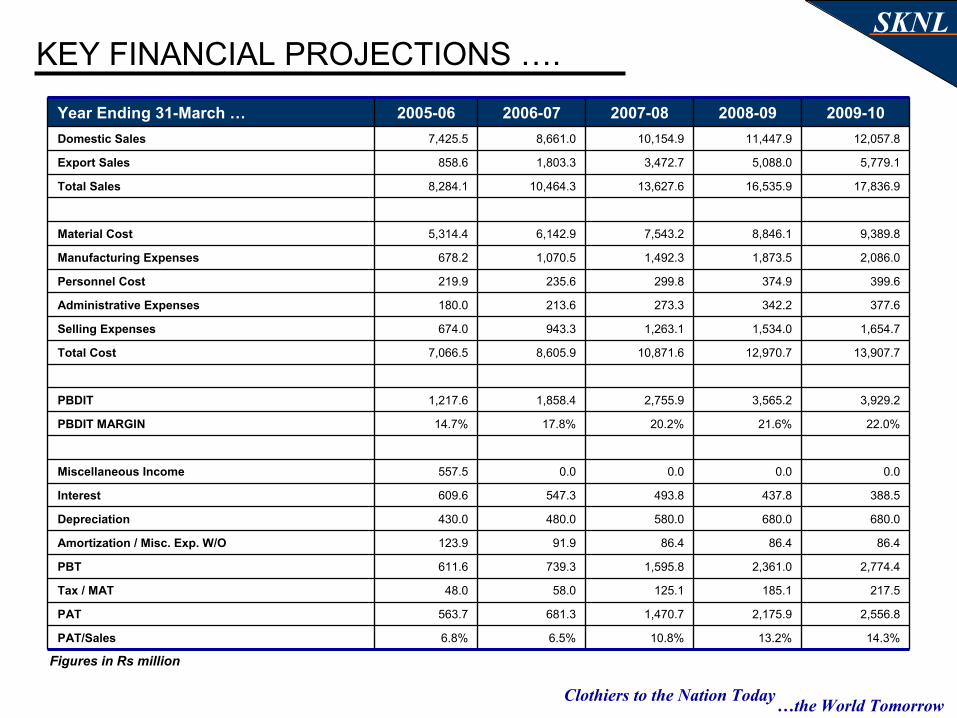

SKNLKEY FINANCIAL PROJECTIONS ….

14.3%13.2%10.8%6.5%6.8%PAT/Sales

2,556.82,175.91,470.7681.3563.7PAT

217.5185.1125.158.048.0Tax / MAT

2,774.42,361.01,595.8739.3611.6PBT

86.486.486.491.9123.9Amortization / Misc. Exp. W/O

680.0680.0580.0480.0430.0Depreciation

388.5437.8493.8547.3609.6Interest

0.00.00.00.0557.5Miscellaneous Income

22.0%21.6%20.2%17.8%14.7%PBDIT MARGIN

3,929.23,565.22,755.91,858.41,217.6PBDIT

13,907.712,970.710,871.68,605.97,066.5Total Cost

1,654.71,534.01,263.1943.3674.0Selling Expenses

377.6342.2273.3213.6180.0Administrative Expenses

399.6374.9299.8235.6219.9Personnel Cost

2,086.01,873.51,492.31,070.5678.2Manufacturing Expenses

9,389.88,846.17,543.26,142.95,314.4Material Cost

17,836.916,535.913,627.610,464.38,284.1Total Sales

5,779.15,088.03,472.71,803.3858.6Export Sales

12,057.811,447.910,154.98,661.07,425.5Domestic Sales

2009-102008-092007-082006-072005-06Year Ending 31-March …

Figures in Rs million

Clothiers to the Nation Today…the World Tomorrow

SKNL

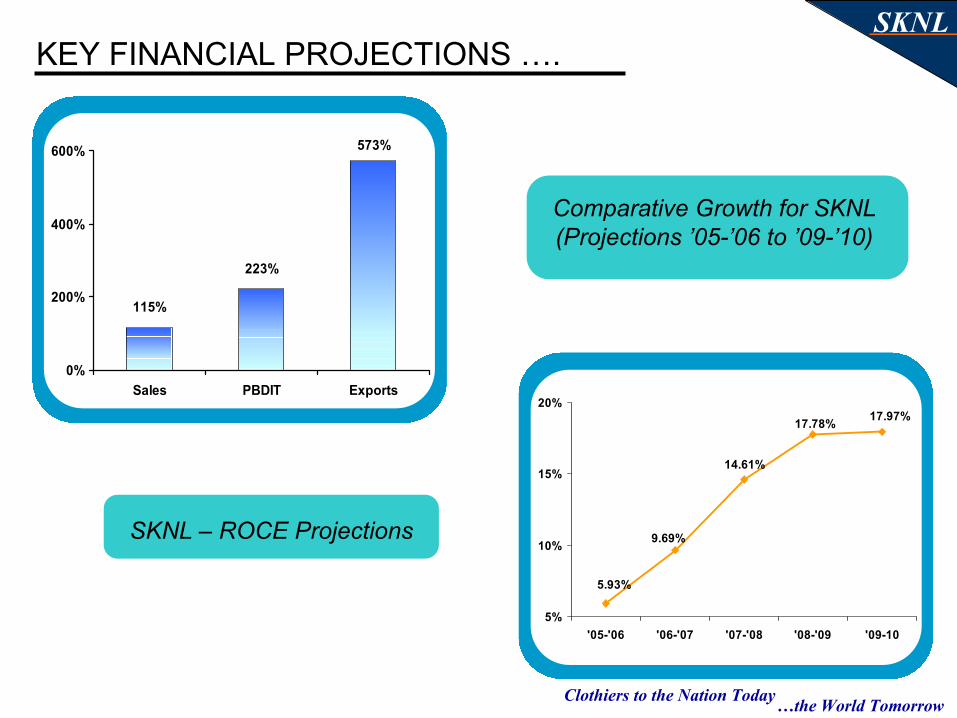

Comparative Growth for SKNL (Projections ’05-’06 to ’09-’10)

SKNL – ROCE Projections

573%

223%

115%

0%

200%

400%

600%

Sales PBDIT Exports

17.97%17.78%

14.61%

9.69%

5.93%

5%

10%

15%

20%

'05-'06 '06-'07 '07-'08 '08-'09 '09-10

KEY FINANCIAL PROJECTIONS ….

Related Documents