Russian uranium mining industry diversification strategy 08.06.2011 Alexander Boytsov, Deputy director general, ARMZ Uranium Holding

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Russian uranium mining industry diversification strategy

08.06.2011

Alexander Boytsov, Deputy director general, ARMZ Uranium Holding

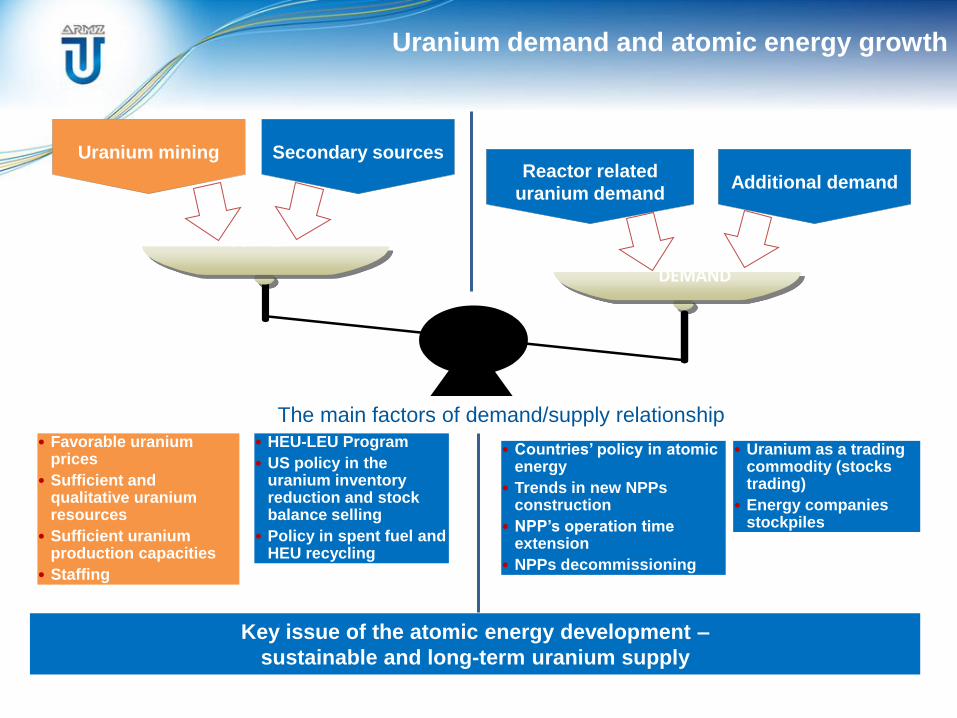

Uranium demand and atomic energy growth

The main factors of demand/supply relationship

Reactor related

uranium demandAdditional demand

Secondary sourcesUranium mining

• Countries’ policy in atomic energy

• Trends in new NPPs construction

• NPP’s operation time extension

• NPPs decommissioning

• HEU-LEU Program

• US policy in the uranium inventory reduction and stock balance selling

• Policy in spent fuel and HEU recycling

• Favorable uranium prices

• Sufficient and qualitative uranium resources

• Sufficient uranium production capacities

• Staffing

• Uranium as a trading commodity (stocks trading)

• Energy companies stockpiles

Key issue of the atomic energy development –

sustainable and long-term uranium supply

SUPPLY

DEMAND

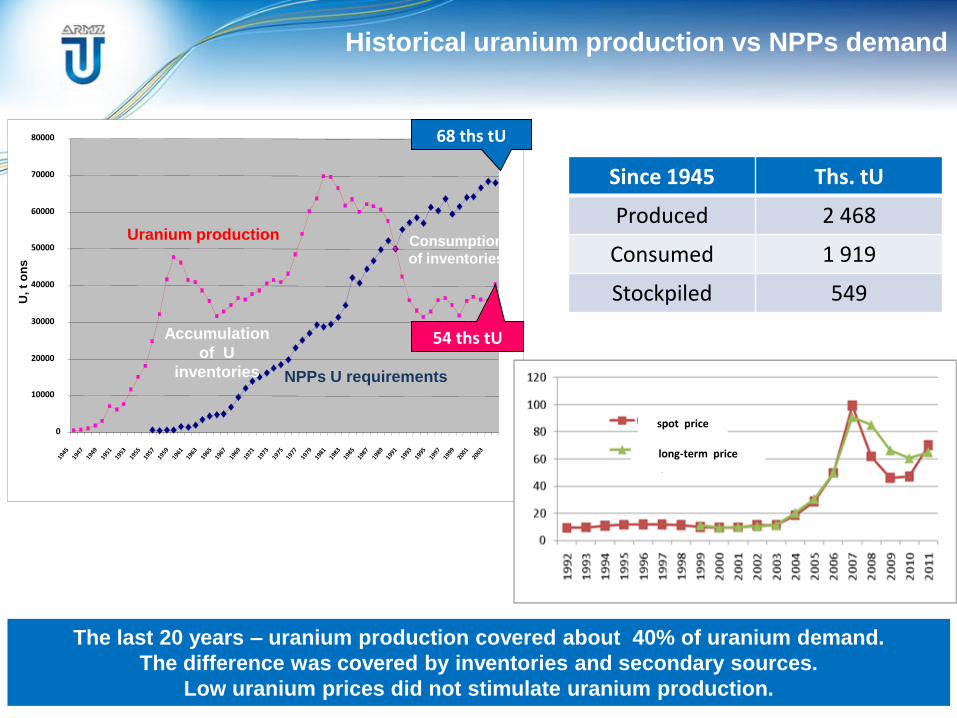

Historical uranium production vs NPPs demand

The last 20 years – uranium production covered about 40% of uranium demand.

The difference was covered by inventories and secondary sources.

Low uranium prices did not stimulate uranium production.

0

10000

20000

30000

40000

50000

60000

70000

80000

U, t

on

s

Accumulation

of U

inventories

Uranium production

NPPs U requirements

68 ths tU

54 ths tU

Consumption

of inventories

Since 1945 Ths. tU

Produced 2 468

Consumed 1 919

Stockpiled 549

0

20

40

60

80

100

120

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

цена спот

цена по долгосрочным контрактам

USD per pound of U3O8

spot price

long-term price

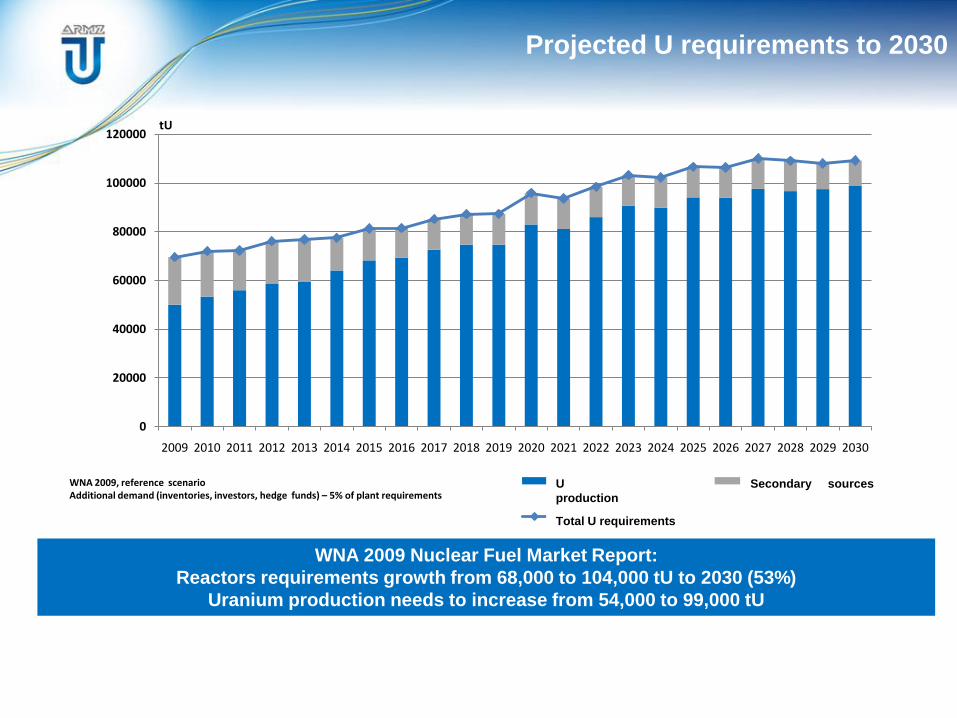

Projected U requirements to 2030

WNA 2009 Nuclear Fuel Market Report:

Reactors requirements growth from 68,000 to 104,000 tU to 2030 (53%)

Uranium production needs to increase from 54,000 to 99,000 tU

0

20000

40000

60000

80000

100000

120000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Добыча урана Вторичные источники

Общие потребности

WNA,2009, средний сценарийДополнительный спрос (складские запасы АЭС, закупки инвестиционныхи хеджевых фондов)—порядка 5% от реакторных потребностей

tU

WNA 2009, reference scenarioAdditional demand (inventories, investors, hedge funds) – 5% of plant requirements

U

production

Secondary sources

Total U requirements

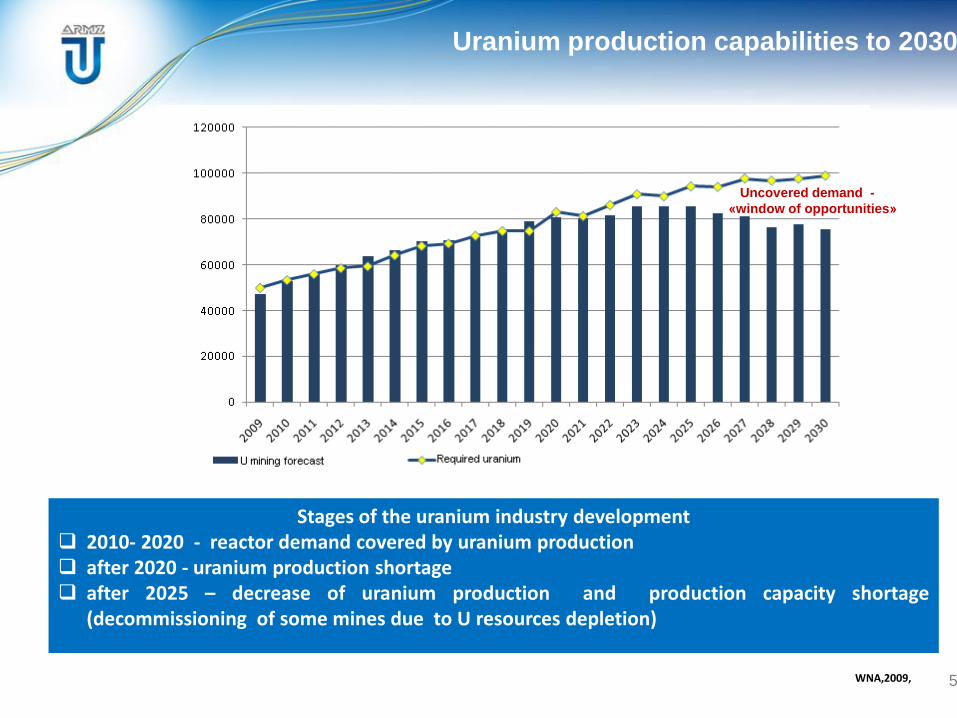

Uranium production capabilities to 2030

5WNA,2009, reference

Stages of the uranium industry development 2010- 2020 - reactor demand covered by uranium production after 2020 - uranium production shortage after 2025 – decrease of uranium production and production capacity shortage

(decommissioning of some mines due to U resources depletion)

Uncovered demand -

«window of opportunities»

tU

production

1679

832

566 545472

296 284 279 276 224

853

0

200

400

600

800

1000

1200

1400

1600

18002260

609 543430 398 392

131 140

0

500

1000

1500

2000

2500

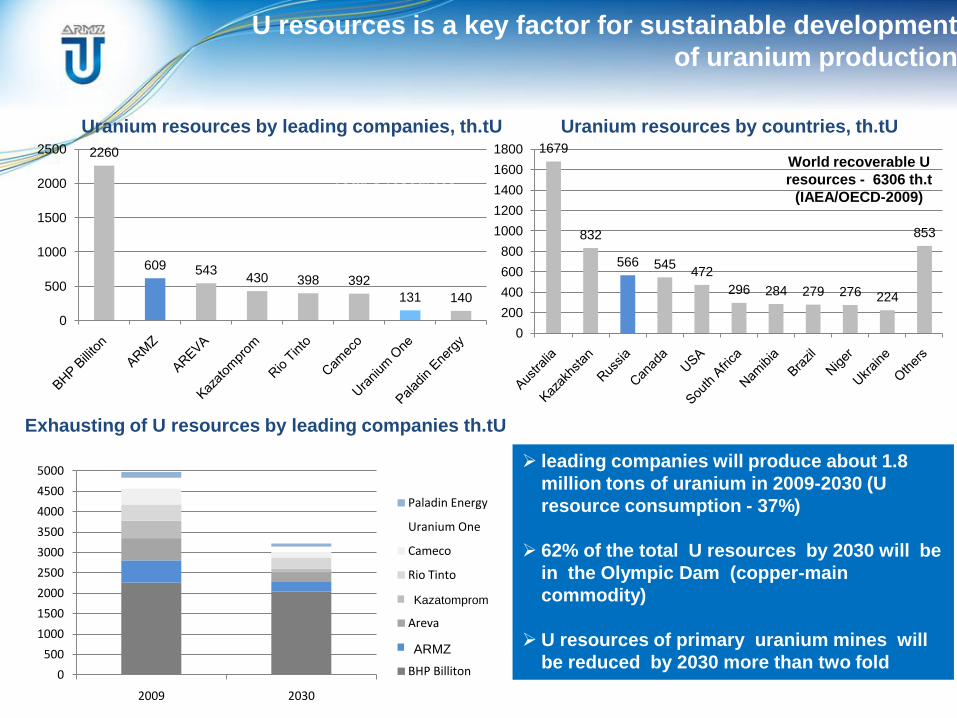

U resources is a key factor for sustainable development

of uranium production

leading companies will produce about 1.8

million tons of uranium in 2009-2030 (U

resource consumption - 37%)

62% of the total U resources by 2030 will be

in the Olympic Dam (copper-main

commodity)

U resources of primary uranium mines will

be reduced by 2030 more than two fold

Uranium resources by leading companies, th.tU Uranium resources by countries, th.tU

Total U resources –

4925 th.t (in-situ)

World recoverable U

resources - 6306 th.t

(IAEA/OECD-2009)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2009 2030

Paladin Energy

Uranium One

Cameco

Rio Tinto

Казатомпром

Areva

АРМЗ

BHP Billiton

Exhausting of U resources by leading companies th.tU

Kazatomprom

ARMZ

World recoverable U

resources - 6306 th.t

(IAEA/OECD-2009)

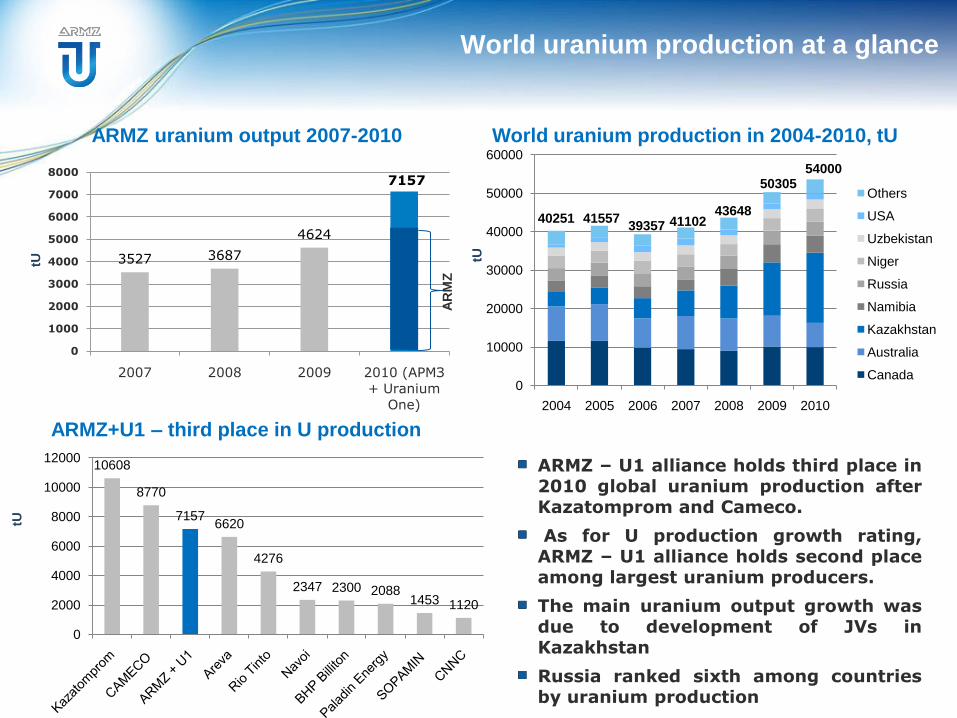

World uranium production at a glance

ARMZ uranium output 2007-2010

ARMZ+U1 – third place in U production

ARMZ – U1 alliance holds third place in2010 global uranium production afterKazatomprom and Cameco.

As for U production growth rating,ARMZ – U1 alliance holds second placeamong largest uranium producers.

The main uranium output growth wasdue to development of JVs inKazakhstan

Russia ranked sixth among countriesby uranium production

3527 3687

4624

0

1000

2000

3000

4000

5000

6000

7000

8000

2007 2008 2009 2010 (АРМЗ

+ Uranium

One)

tU

7157

AR

MZ

tU

10608

8770

71576620

4276

2347 2300 20881453 1120

0

2000

4000

6000

8000

10000

12000

World uranium production in 2004-2010, tU

0

10000

20000

30000

40000

50000

60000

2004 2005 2006 2007 2008 2009 2010

Others

USA

Uzbekistan

Niger

Russia

Namibia

Kazakhstan

Australia

Canada

40251 4155739357 41102

43648

5030554000

tU

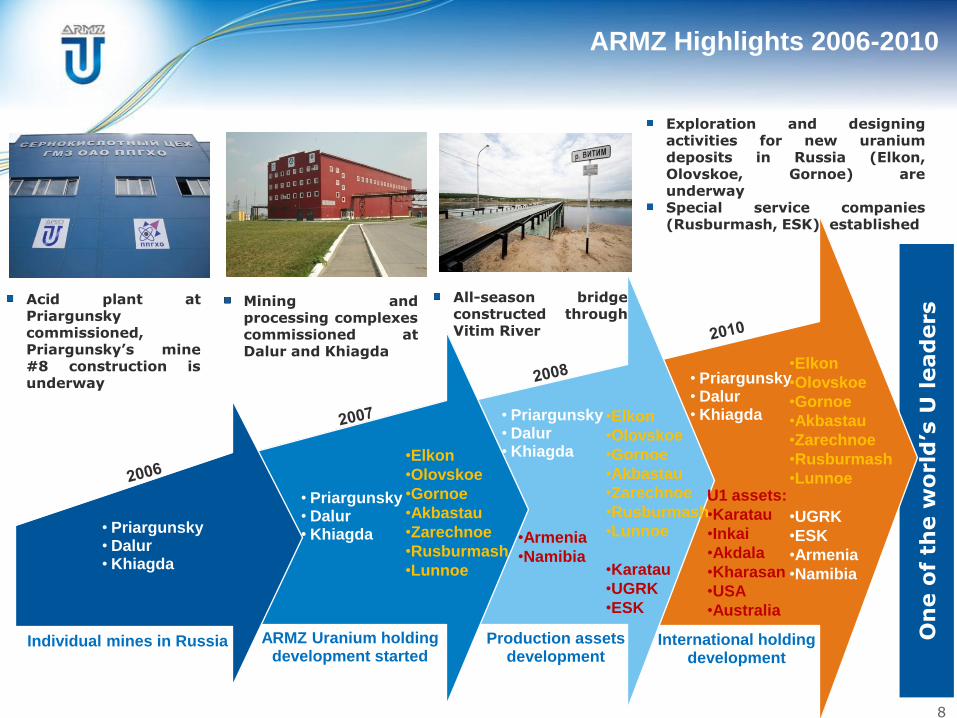

ARMZ Highlights 2006-2010

On

e o

f th

e w

orld

’s U

lead

ers

8

• Priargunsky• Dalur• Khiagda

• Priargunsky• Dalur• Khiagda

Individual mines in Russia ARMZ Uranium holding development started

•Elkon

•Olovskoe

•Gornoe

•Akbastau

•Zarechnoe

•Rusburmash

•Lunnoe

• Priargunsky• Dalur• Khiagda

•Elkon

•Olovskoe

•Gornoe

•Akbastau

•Zarechnoe

•Rusburmash

•Lunnoe

•Karatau

•UGRK

•ESK

•Armenia

•Namibia

Production assets development

• Priargunsky• Dalur• Khiagda

•Elkon

•Olovskoe

•Gornoe

•Akbastau

•Zarechnoe

•Rusburmash

•Lunnoe

•UGRK

•ESK

•Armenia

•Namibia

U1 assets:

•Karatau

•Inkai

•Akdala

•Kharasan

•USA

•Australia

International holding development

Acid plant atPriargunskycommissioned,Priargunsky’s mine#8 construction isunderway

Mining andprocessing complexescommissioned atDalur and Khiagda

All-season bridgeconstructed throughVitim River

Exploration and designingactivities for new uraniumdeposits in Russia (Elkon,Olovskoe, Gornoe) areunderwaySpecial service companies(Rusburmash, ESK) established

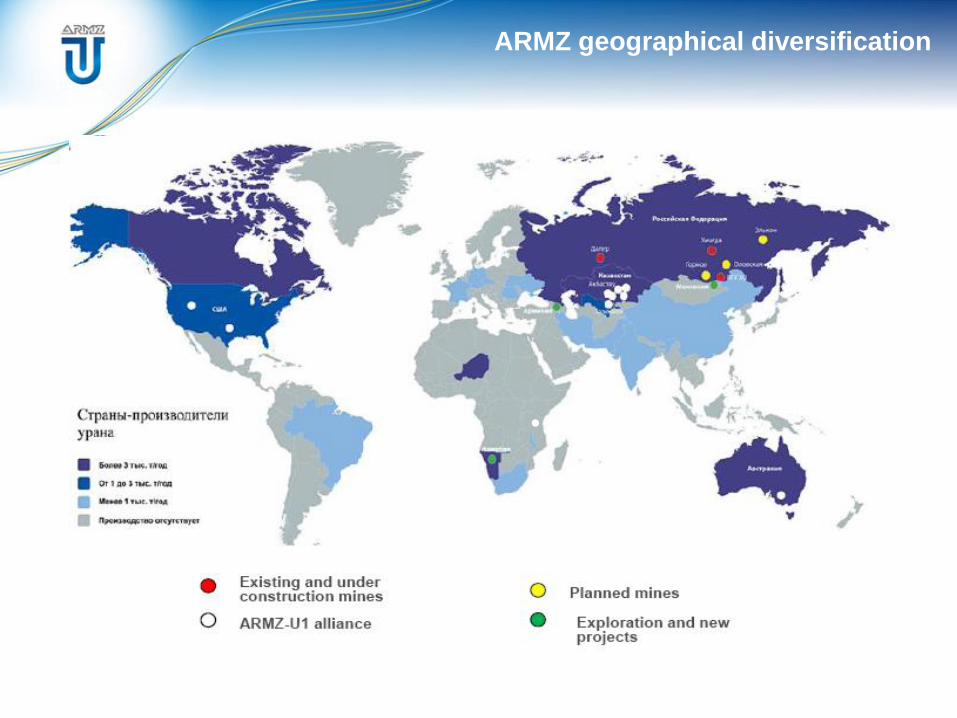

ARMZ geographical diversification

ARMZ projects pipeline

Designing / Exploration

Construction

Exploration / Perspective

10Источник: АРМЗ

ARMZ strategy —through

diversification to world’s leadership

Production

AkbastauZarechnoe

ElkonGornoeOlovskayaLunnoe

Mongolia

Armenia

Namibia

HoneymoonUS ISLN.Kharasan

U1

PriargunskyDalur

KaratauAkdalaS.Inkai

U1

Khiagda

U1

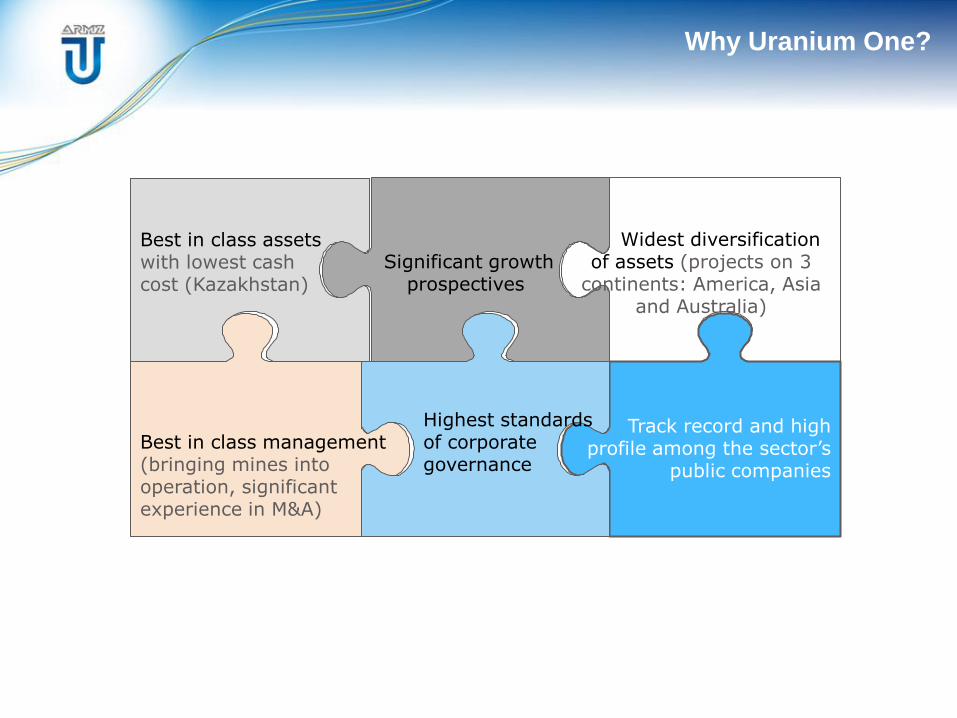

Why Uranium One?

Track record and high profile among the sector’s

public companies

Highest standards of corporate governance

Best in class management (bringing mines into operation, significant experience in M&A)

Best in class assets with lowest cash cost (Kazakhstan)

Significant growth prospectives

Widest diversification of assets (projects on 3

continents: America, Asia and Australia)

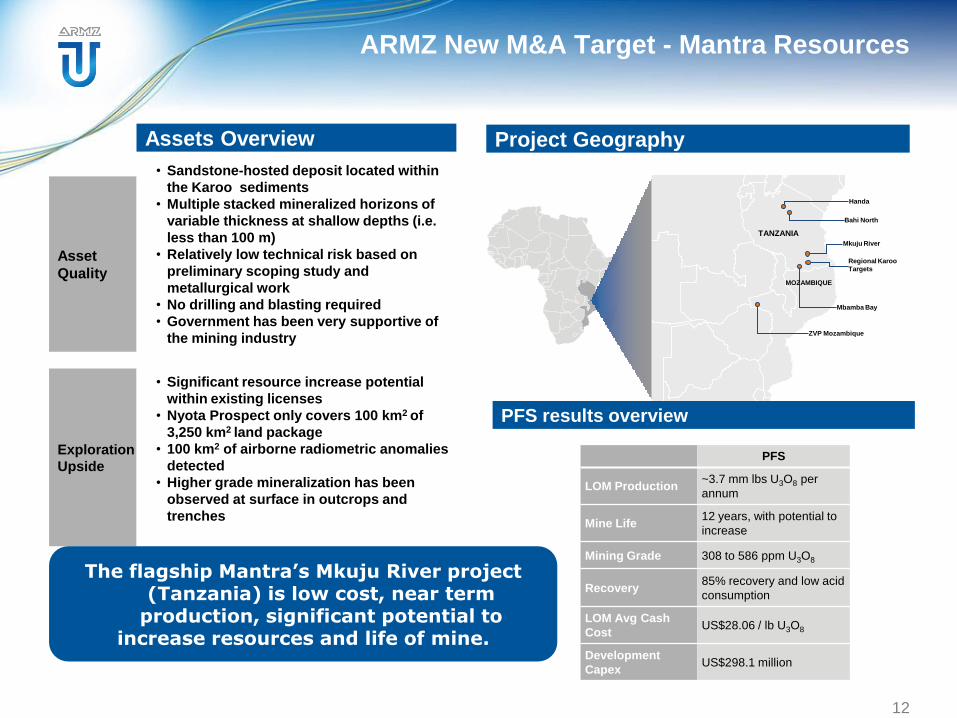

ARMZ New M&A Target - Mantra Resources

Asset

Quality

• Sandstone-hosted deposit located within

the Karoo sediments

• Multiple stacked mineralized horizons of

variable thickness at shallow depths (i.e.

less than 100 m)

• Relatively low technical risk based on

preliminary scoping study and

metallurgical work

• No drilling and blasting required

• Government has been very supportive of

the mining industry

Assets Overview

Exploration

Upside

• Significant resource increase potential

within existing licenses

• Nyota Prospect only covers 100 km2 of

3,250 km2 land package

• 100 km2 of airborne radiometric anomalies

detected

• Higher grade mineralization has been

observed at surface in outcrops and

trenches

PFS

LOM Production ~3.7 mm lbs U3O8 per

annum

Mine Life12 years, with potential to

increase

Mining Grade 308 to 586 ppm U3O8

Recovery85% recovery and low acid

consumption

LOM Avg Cash

CostUS$28.06 / lb U3O8

Development

CapexUS$298.1 million

Handa

Bahi North

Mkuju River

Mbamba Bay

Regional Karoo

Targets

ZVP Mozambique

TANZANIA

MOZAMBIQUE

Project Geography

PFS results overview

12

The flagship Mantra’s Mkuju River project (Tanzania) is low cost, near term

production, significant potential to increase resources and life of mine.

ARMZ – U1 alliance potential

13

ARMZ — Uranium One will be one of the leading global uranium producer. It preliminary ranks second in production volume by 2015.

Further U resources strengthening, especially in the lowest cash cost category.

The increase in market capitalization and the ability to attract investment, using all the market mechanisms.

Excellent potential for further ARMZ – Uranium One growth.

Deal with the Uranium One is the first and most important step in ARMZ strategy

Source: UxC data, ARMZ evaluation

13,0

11,5

9,6

8,5 8,5

3,5

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

Kazatomprom Rosatom plus Uranium One

Areva Cameco Rio Tinto Rosatom 2009 Paladin

Uranium production in 2015, thou tU

ARMZ2009

ARMZ+ U1

ARMZ attributable resources , tU

ARMZ-U1 alliance+ Mantra –first place in U mining

0

100000

200000

300000

400000

500000

600000

700000

800000

Before U1 deal After U1 and Mantra deals

Tanzania

Australia

USA

Kazakhstan

Russia

609 th tU

779 th tU

> 80 USD/kgU

< 80 USD/kgU

> 80

< 80

Resources increased by28% , incl. 68% growth with cash cost < 80 USD/kg U

13.9Mantra

ARMZ strategy – sustainable leadership

Div

ersif

ied

prod

ucer w

ith

w

orld

-cla

ss a

ssets

•Russian uranium deposits

•Effective low-cost uranium production assets abroad

Diversification in prospective non-uranium metals (REE, gold, zirconium, etc.)

Sustainable uranium supplies

Exploration activities over the world

Related Documents