1 Marketing In The Hinterland Saroj Kumar Mohanta Partner, MART

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 1/25

1

Marketing In The Hinterland

Saroj Kumar Mohanta

Partner, MART

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 2/25

Rural Images

Saroj Kumar Mohanta

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 3/25

New Roads

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 4/25

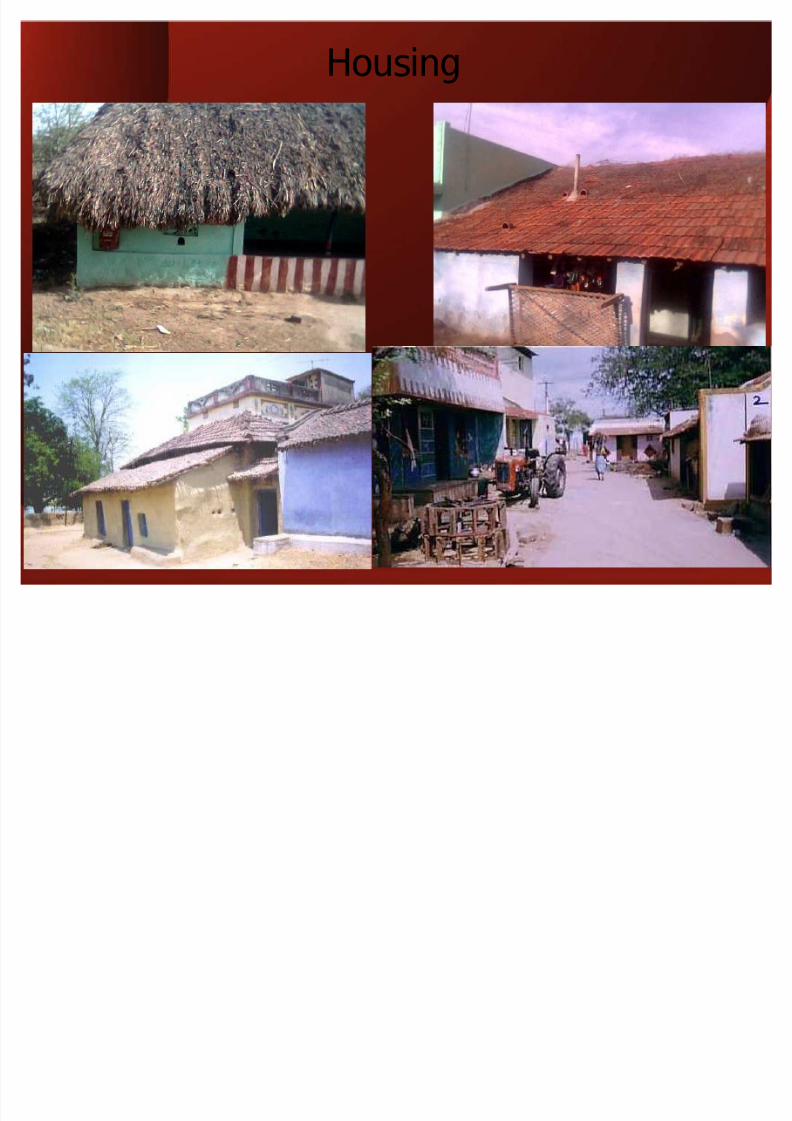

Housing

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 5/25

People

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 6/25

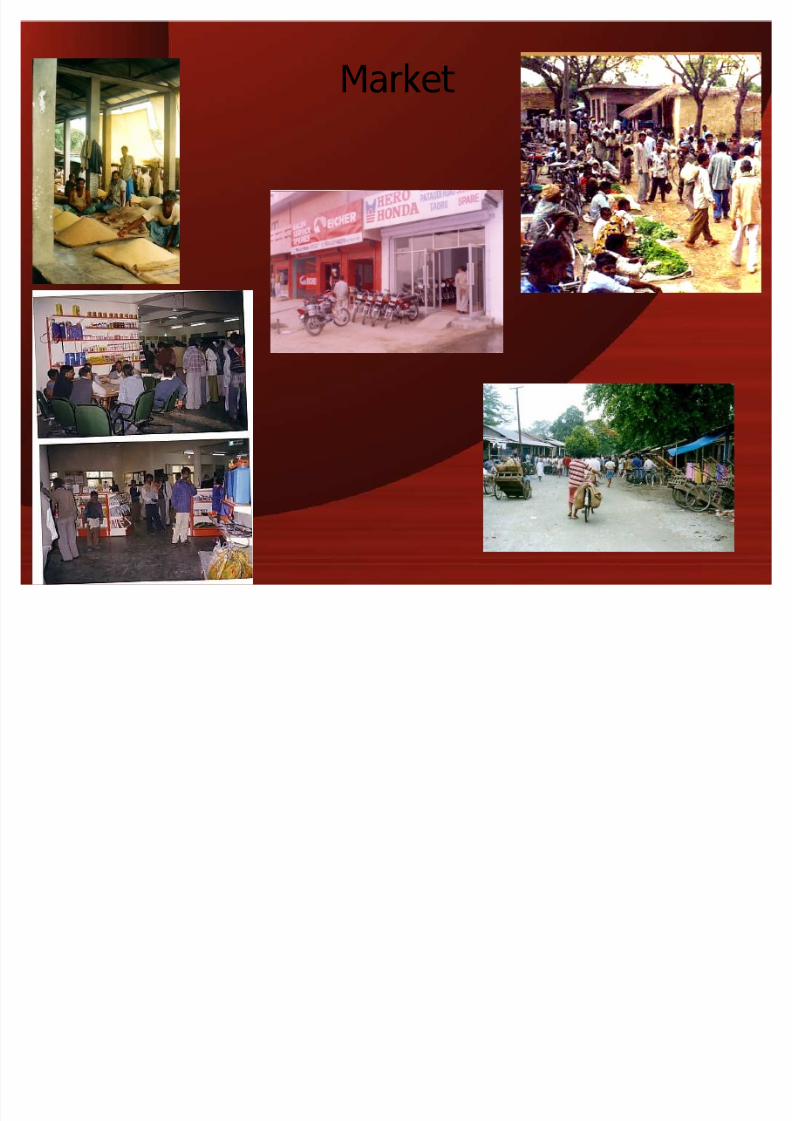

Market

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 7/25

Outlets

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 8/25

Place of Gathering

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 9/25

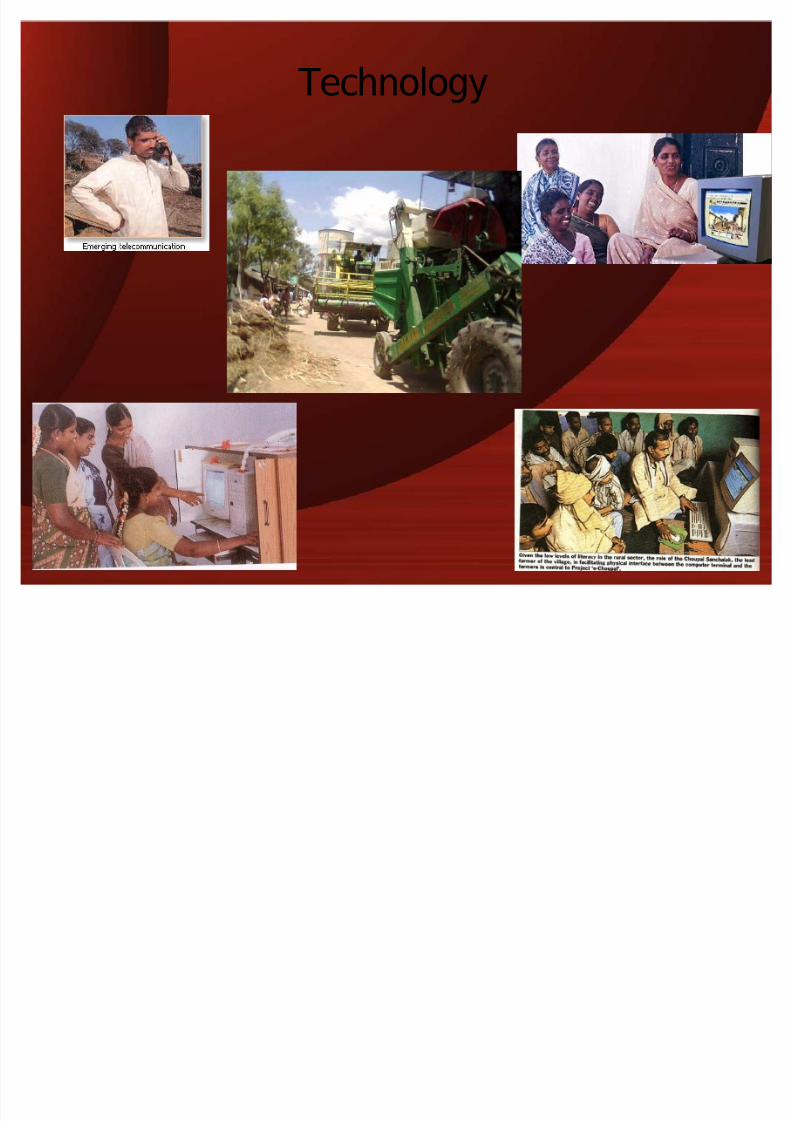

Technology

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 10/25

10

RURAL ECONOMIC STRUCTURE

RURAL ECONOMY

FARM SECTOR NON-FARM SECTOR

AGRICULTURE

ANIMAL HUSBANDRY

HORTICULTURE

FORESTRY

FISHING

INDUSTRIES SERVICES

AGRO-PROCESSING

MANUFACTURING

MINING/QUARRYING

CONSTRUCTION

RETAILING/TRADING

COMMUNITY/SOCIAL SERVICE

TRANSPORT/STORAGE

COMMUNICATION

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 11/25

11

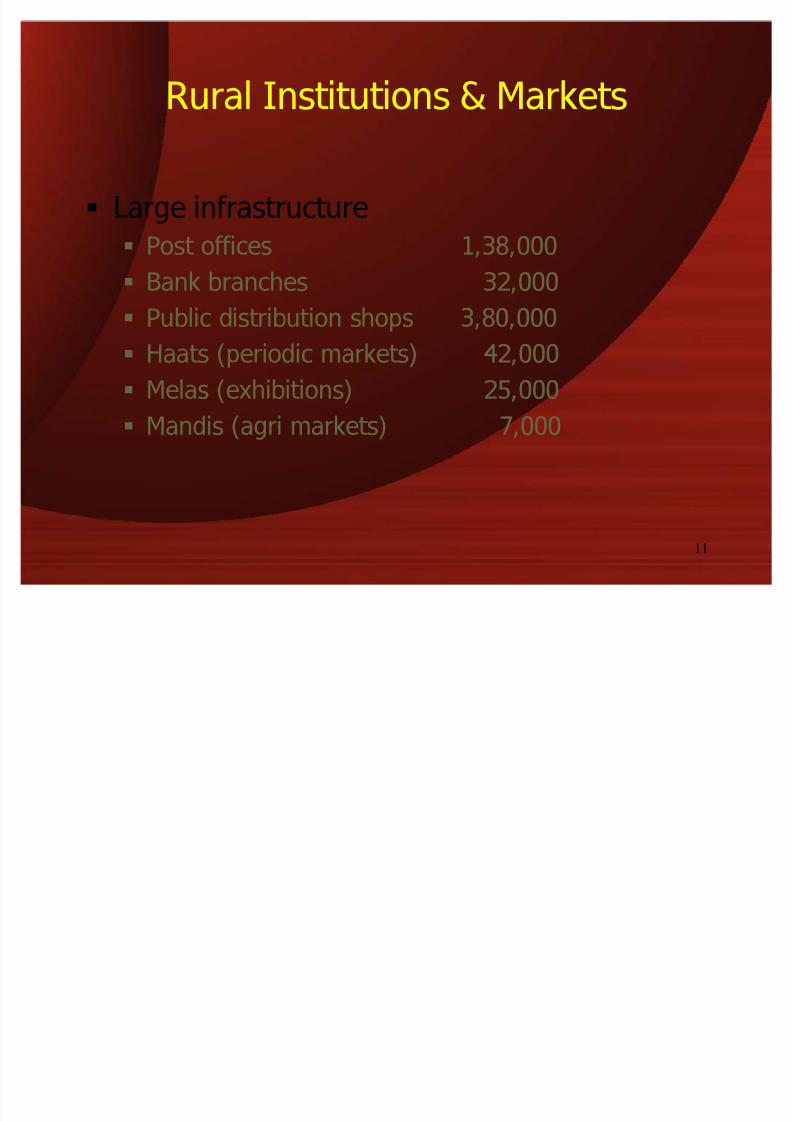

Rural Institutions & Markets

Large infrastructure

Post offices 1,38,000

Bank branches 32,000 Public distribution shops 3,80,000

Haats (periodic markets) 42,000

Melas (exhibitions) 25,000

Mandis (agri markets) 7,000

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 12/25

12

RURAL INFRASTRUCTURE

SOCIAL

Health

137292 sub centres (1 ANM + 1 MHW)

22807 PHCs (medical officer + 14 paramedics ; 6 beds)

3027 CHCs (4 medical specialists + 21 paramedics. 30 beds + X Ray,

labour room, OT, labs)

Education 12,28,501 EDU. INST.

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 13/25

13

RURAL INFRASTRUCTURE

ROAD CONNECTIVITY

49% - <1000; 75% - 1-1500; 78% - > 1500

Pradhan Mantri Gram Sadak Yojna will cover 160000 habitations with

investment of Rs. 60000crores

MEDIA

Radio - 208 Stations - 98.8% population

TV ± DD 1042 transmitters ± 7.5 crore homes

Press ± about 15% of total India

Mobiles ± Over 192 million ««and growing!

ELECTRIFICATION

90% Villages electrified but 48% have access

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 14/25

14

Rural Administrative Structure &Social Structure

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 15/25

15

Rural Administration

Big

village

Small village

Small village

Panchayat

>5000 pop

Elected body

Gram pradhan heads the elected body

Gram sevak is the administration representative

Panchayat empowered to implement programs

Formal body is different from caste panchayats

About 25 panchayats

are administered under

block administration

BDO is in-charge of block administrationRepresentation of panchayats by a pradhan

MLA is chairman in the block

All govt programs are channeled through blocks

to panchayats. Monitoring and control

About 10 blocks are

administered under

District administration

DC is in-charge of District administration

MP is the chairperson in district administraton

DC is incharge of all departments in the district

and also in-charge of all programs

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 16/25

16

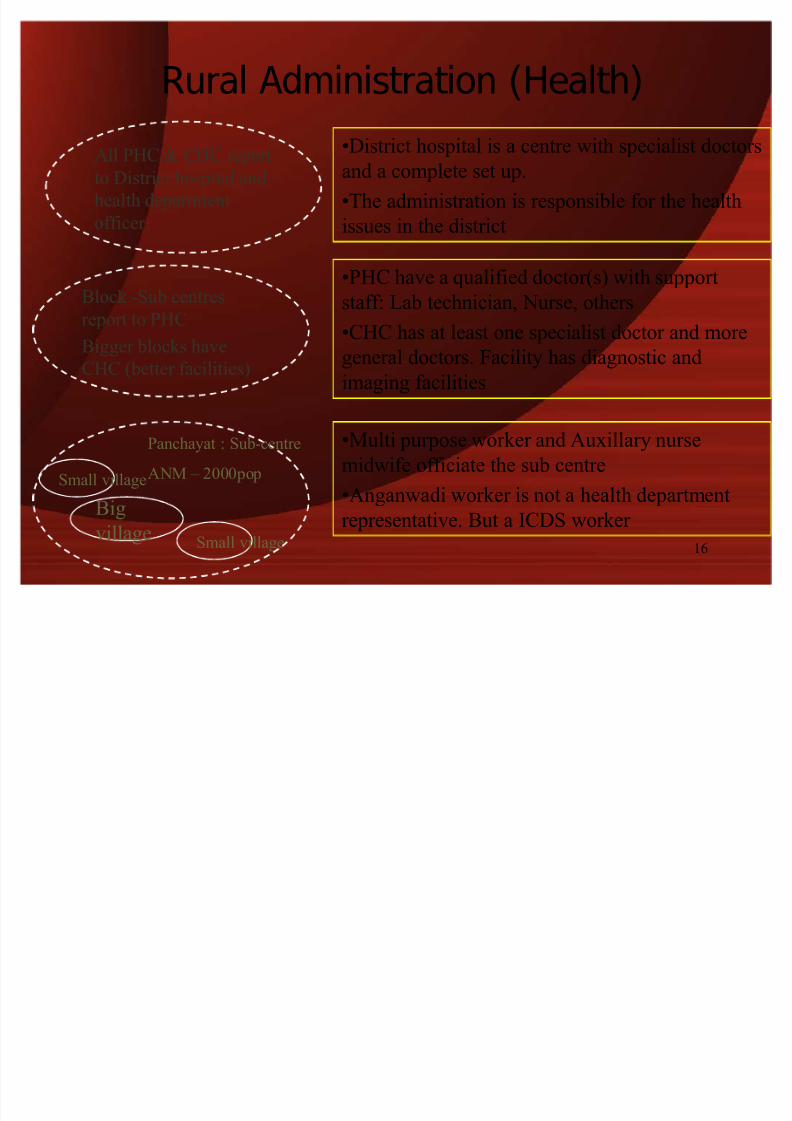

Rural Administration (Health)

Big

village

Small village

Small village

Panchayat : Sub-centre

ANM ± 2000pop

Multi purpose worker and Auxillary nurse

midwife officiate the sub centre

Anganwadi worker is not a health department

representative. But a ICDS worker

Block -Sub centres

report to PHC

Bigger blocks have

CHC (better facilities)

PHC have a qualified doctor(s) with supportstaff: Lab technician, Nurse, others

CHC has at least one specialist doctor and more

general doctors. Facility has diagnostic and

imaging facilities

All PHC & CHC report

to District hospital and

health department

officer

District hospital is a centre with specialist doctorsand a complete set up.

The administration is responsible for the health

issues in the district

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 17/25

17

Close of Session

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 18/25

18

CULTURE SYSTEM LEVELS OF INFLUENCEMACRO

EXO

MESO

MICRO

CUSTOMS

SOCIAL NORMS

CULTURE

EXPERTS

PEER

GROUP

FAMILY

NEIGHBOURSWORK

ATTITUDES,BEHAVIOUR, VALUES,IDEOLOGIES

POINT OFPURCHASE

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 19/25

19

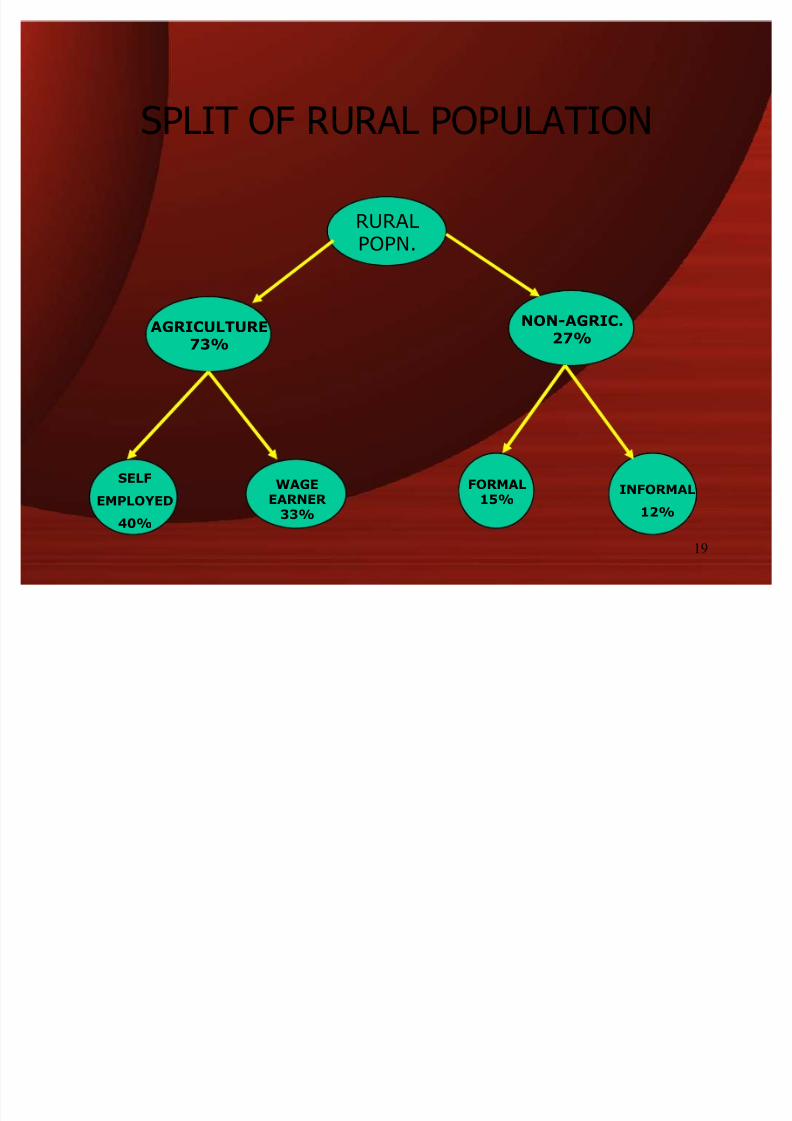

SPLIT

OFRU

RAL

PO

PUL

ATION

RURALPOPN.

AGRICULTURE73%

NON-AGRIC.27%

SELF

EMPLOYED

40%

WAGEEARNER

33%

FORMAL15%

INFORMAL

12%

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 20/25

20

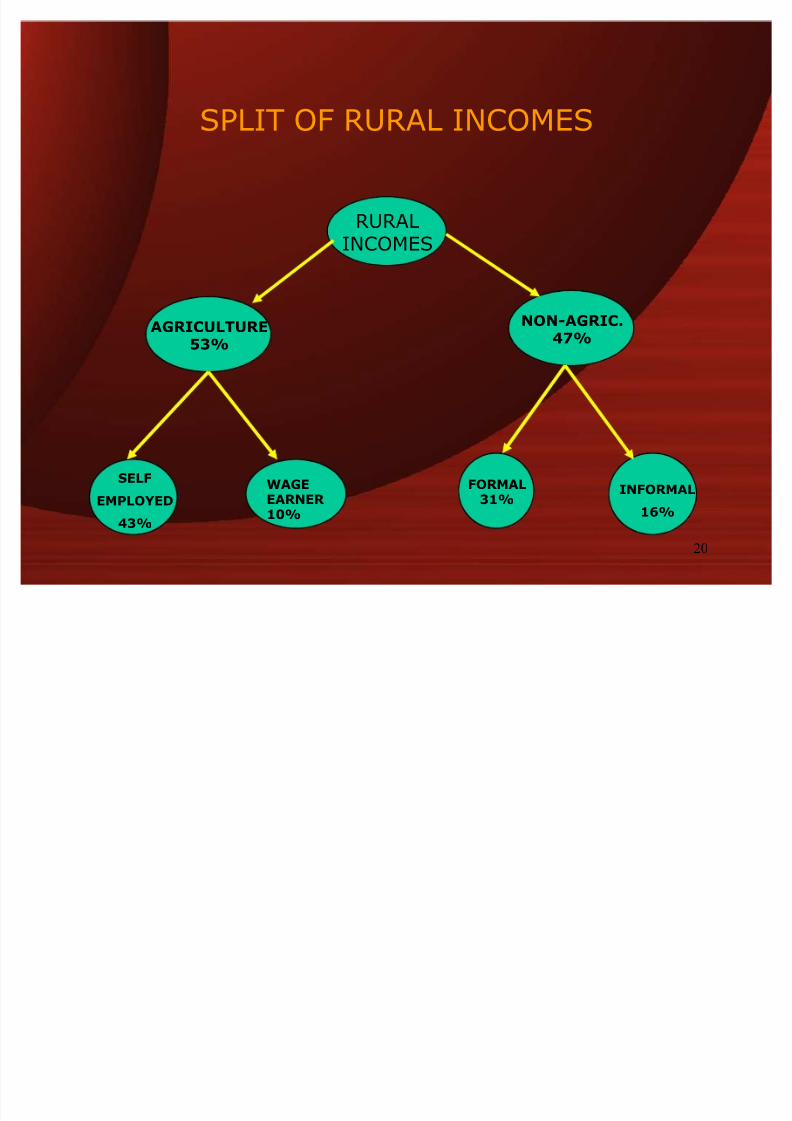

SPLIT OF RURAL INCOMES

RURALINCOMES

AGRICULTURE53%

NON-AGRIC.47%

SELF

EMPLOYED

43%

WAGEEARNER 10%

FORMAL31%

INFORMAL

16%

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 21/25

21

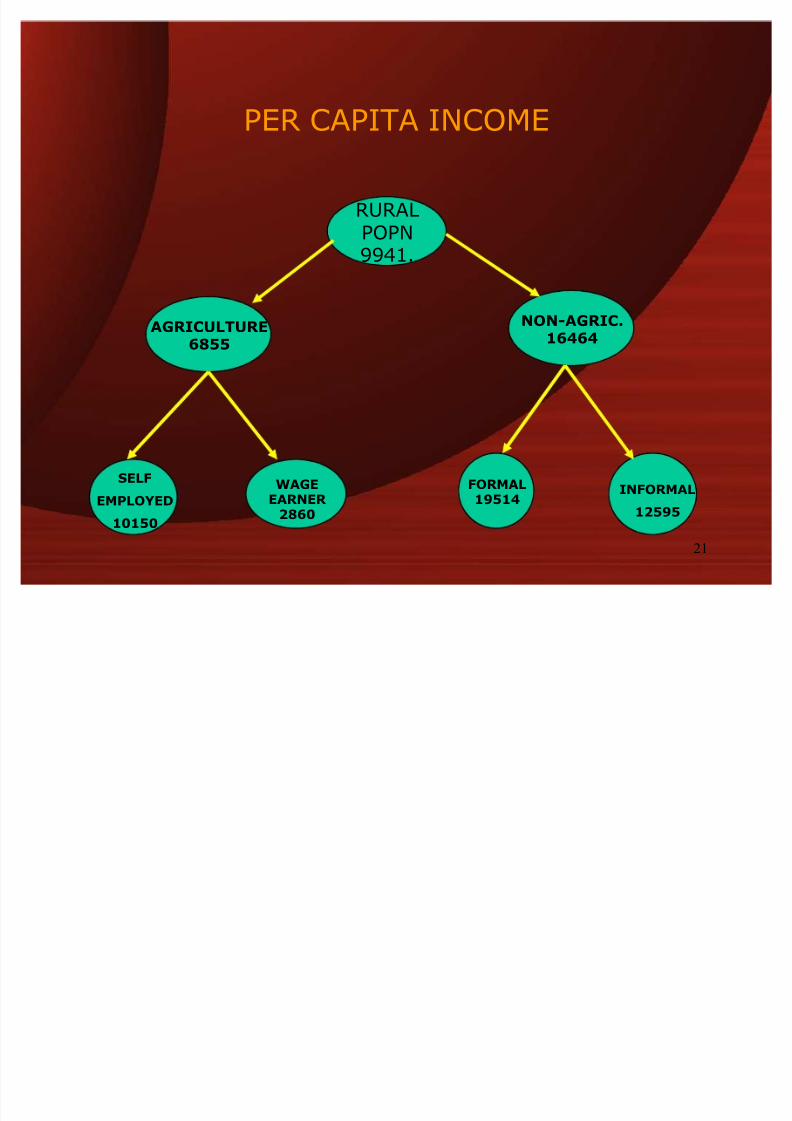

PER CAPITA INCOME

RURALPOPN9941.

AGRICULTURE6855

NON-AGRIC.16464

SELF

EMPLOYED

10150

WAGEEARNER

2860

FORMAL19514

INFORMAL

12595

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 22/25

22

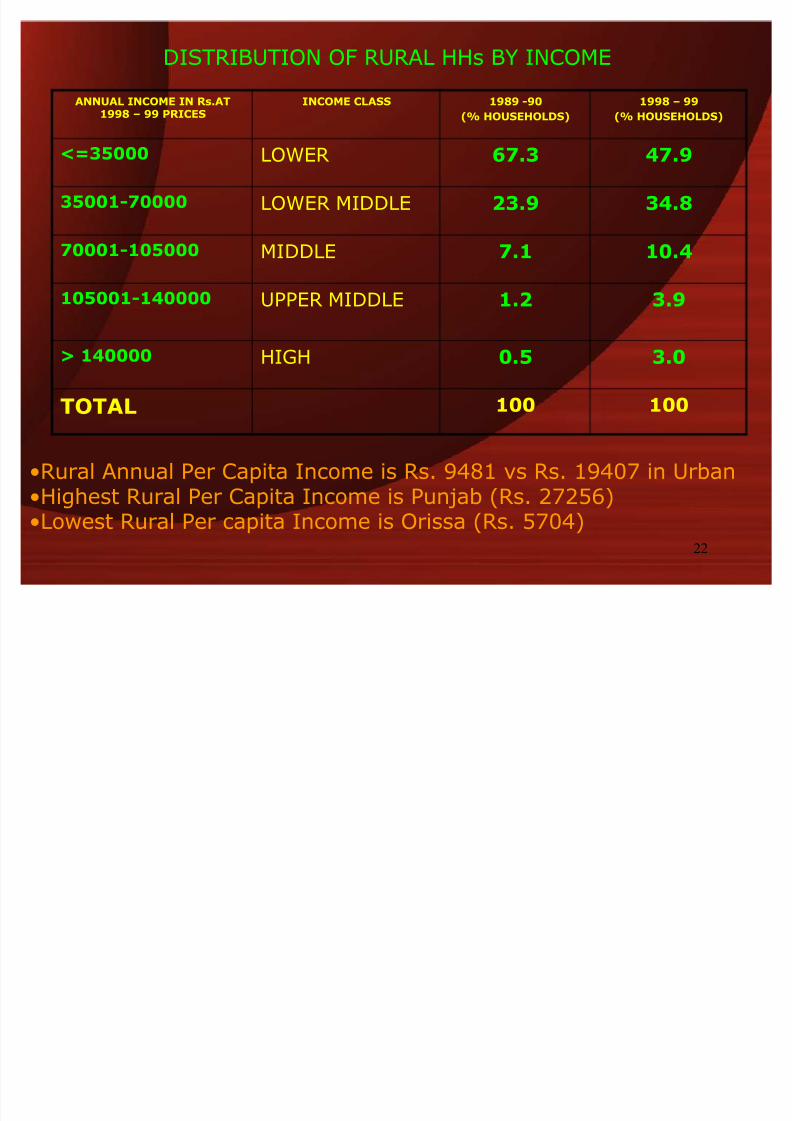

DISTRIBUTION OF RURAL HHs BY INCOME

ANNUAL INCOME IN Rs.AT1998 ± 99 PRICES

INCOME CLASS 1989 -90

(% HOUSEHOLDS)

1998 ± 99

(% HOUSEHOLDS)

<=35000 LOWER 67.3 47.9

35001-70000 LOWER MIDDLE 23.9 34.8

70001-105000 MIDDLE 7.1 10.4

105001-140000 UPPER MIDDLE 1.2 3.9

> 140000 HIGH 0.5 3.0

TOTAL100 100

Rural Annual Per Capita Income is Rs. 9481 vs Rs. 19407 in UrbanHighest Rural Per Capita Income is Punjab (Rs. 27256)Lowest Rural Per capita Income is Orissa (Rs. 5704)

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 23/25

23

Opportunity & Challenges

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 24/25

24

Marketing Opportunities

Low penetration rates in rural

% of rural HH

Durables Urban Rural Total

CTV 30.4 4.8 12.1

Refrigerator 33.5 3.5 12.0

FMCGs Urban Rural Total

Shampoo 66.3 35.2 44.2

Toothpaste 82.2 44.9 55.6

Source: NCAER 2002

8/8/2019 Rural Market Institutions

http://slidepdf.com/reader/full/rural-market-institutions 25/25

25

Marketing Opportunities

R1 - 4%

R2 - 11%

R3 - 37%

R4 - 48%

Low rural consumption in FMCGs (rich HHs)

urban rural

Annual consumption Rs 13,000 Rs 9,400

Rural consumption volumes (R1+R2+R3) Toothpaste 88%

Toothpowder 79%

Shampoo 88%

Related Documents