RURAL BANKING IN INDIA Presented by Sanjiv Kumar Career Point University Kota

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RURAL BANKING IN INDIA

Presented by Sanjiv KumarCareer Point University Kota

Preview

Products of Rural Financing Sources of Rural Finance NABARD

Introduction Organisation Functions/Roles

Challenges in Rural Banking

Products

Various Services offered by the banks to its customers ie Loans, Deposit accounts, insurance etc

The products offered by Rural Banking include:- Agriculture Credits Financial Inclusion MSMEs Deposits

Products of Rural Banking

Banks have introduced a range of products at attractive rates of interests.

Tractor/ Tiller Loan Transformation of Traditional subsistence agriculture

into commercial positionAssist farmers, shift from traditional farming to

mechanized farming for reducing the time and cost of tillage and improve the quality of tillage so as to increase their crop productions through multiple cropping and profitability.

Maximum repayment period 7 to 9 years

Products : Agriculture Credits

Short Term Loan for Cold Storage/Scientific Godowns• Setting up of Cold storage units, warehouses and godowns etc. • Cash Credit limit of working capital to cold storage units for

direct expenses like wages, salaries, electricity charges, fuel and maintenance expenses with a view to promote storing capacity of Agricultural produce and better price realization by the farmers.

Kisan Credit card• To meet the short term credit requirements for cultivation of

crops & Post Harvest Expenses• Consumption requirement of farmer household• Working capital for maintenance of farm assets and activities

allied to agriculture, like dairy animals, inland fishery etc.

Products : Agriculture Credits

Kissan Bhoomi Vridhi Term Loan for 7-10 Years Objective

• To finance the farmers to purchase, develop and cultivate agricultural as well as fallow and waste lands.

Maximum financing amount - Rs. 10.00 lacs for purchase of land.

Single Transaction Term Loan An instant credit for farming community to meet the emergency requirements for Agriculture and Domestic purposes for tiding over temporary financial difficulties.

Products : Agriculture Credits

All Purpose Term Loans To farmers for requirements like Farm Mechanization, Land

Development, Minor Irrigation, Water Conservation, Horticulture, Allied Activities and Other Agriculture related activities etc.

Loans for Women To encourage and empower women beneficiary by offering hassle

free financial assistance at liberal and concessional terms. Both for Farm and Non-Farm activities.

Products : Agriculture Credits

Solar Irrigation Projects

It is cost-prohibitive for the Government to extend grid power to remote areas especially to meet agriculture loads.

The demand for electric energy is far outstripping supply, especially in the agriculture sector

To help farmers to extend grid power to remote areas especially to meet agriculture loads.

.

Products : Agriculture Credits

Financial inclusion is the delivery of financial services at affordable costs to vast sections of disadvantaged and low income groups ie "no frill accounts".

It helps Create a platform to inculcate saving habit, Providing formal credit

avenues, Plug gaps and leaks in public subsidies and welfare programmes.

Various Schemes under financial inclusion are:- No-frills account ,Jan Dhan Yojna EBT – Electronic Benefits Transfer KCC – Kisan Credit Card MUDRA Bank Micro Units Development and Refinance

Agency Bank is a public sector financial institution that provides loans at low rates to micro finance institutions and non-banking financial institutions which then provide credit to MSME's. It was launched by Prime Minister Narendra Modi on 8 April 2015.

Products : Financial Inclusion

MSE-Manufacturing Loans given to enterprises engaged in the manufacture or

production, processing or preservation of goods in general including the following :-

• Printing• Printing and publishing as integrated unit.• Medical Equipment and Ayurvedic Product• Composite unit of Bacon Processing and Piggy Farm• Beedi/Cigarette Manufacturing and other tobacco products.• Manufacture of Bio Fertilizer• Tobacco Processing.

Products : Financing MSMEs

MSE-Services Loans given to enterprises engaged in providing or rendering of

services in general including the following :-• Small Road and Water Transport Operators.• Small Business• Service enterprises engaged in activities, viz,

- Consultancy Services including management services - Seed grading services

- Training-cum-Incubator centre - Educational Institutions - Training Institutes

- Hospitals

Products : Financing MSMEs

• Besides the facilities of opening Current Deposit/Savings Bank Deposit/regular Recurring Deposit and Fixed Deposit accounts, Banks provide a number of well thought out deposit schemes, tailor made to suit different needs of different people - each in its own way maximizing the benefits for the depositor

Products : DEPOSITS

Sources : Rural Finance

• Rural finance is a line of credit specifically intended for the requirements of the agricultural industry. Range from land development to farming equipment. These credit plans are a significant aspect of rural and semi-urban support.

• A number of banks and finance companies have begun to specialize in offering credit to farmers.

• As banks and financial services continue to extend their services into rural India they are generating employment in the vicinity.

Rural Finance

Various Sources of rural finance are:- Nationalised Banks - Regional Rural Banks Private Banks Co-Operative Banks Informal loans (Money Lenders)

Sources of Rural Finance

Nationalized Banks – Regional Rural Banks (RRB/ Gramin) The Government of India, the concerned State Government and

the sponsoring bank, contribute to the share capital of RRBs in the proportion of 50%, 15% and 35%, respectively.

The area of operation of the RRBs is limited to notified few districts in a State

As on date, there are 14,475 rural banks in the country of which 2126 (91%) are located in remote rural areas.

Sources: Rural Finance

Cooperative Banks Credit Cooperatives The Co-operative Credit Structure (CCS) set up to serve the

needs of both short term and long term rural credit in India. Short term credit is provided by three institutions – State Cooperative Banks (SCB) District Central Cooperative Banks (DCCB) Primary Agricultural Credit Societies (PACS)

Long term credit :-Primary Cooperative Agriculture and Rural Development

Banks (PCARDB).ie Land Devp Banks

Sources : Rural Finance

NABARD

RBI resp for all banking and Credit for agriculture and rural development after independence.

More than 70% population was in rural India with agriculture being backbone of economy

RBI was finding it difficult to focus on Credits for Rural as well as Urban develpoment

A committee was constituted to review the arrangements for institutional credit for agriculture and rural development.

On 28 November 1979, the Committee recommended the formation of NABARD to focus on the credit problems of integrated rural development.

The bank came into existence on 12 July 1982

Genesis

NABARD took over:- Agricultural credit functions of RBI Refinance functions of the then Agricultural Refinance and

Development Corporation (ARDC).

NABARD was set up with an initial capital of 100 crore. Consequently GOI and RBI, the paid up capital as on 31 March

2015, stood at 5000 crore with Government of India holding 4,980 crore (99.60%) and Reserve Bank of India 20.00 crore (0.40%).

Genesis

Mission To Promote sustainable and equitable agriculture and rural prosperity

through effective credit support, related services, institution development and other innovative initiatives

Objectives Facilitate credit flow for agriculture , rural infrastructure

and development Promote policies and practices conducive for rural development Institutional development for rural credit system Supervise Rural Financial Institutions E.g. ( Co-operative banks and

Regional Rural Banks) Consultancy Services.

Mission & Objectives

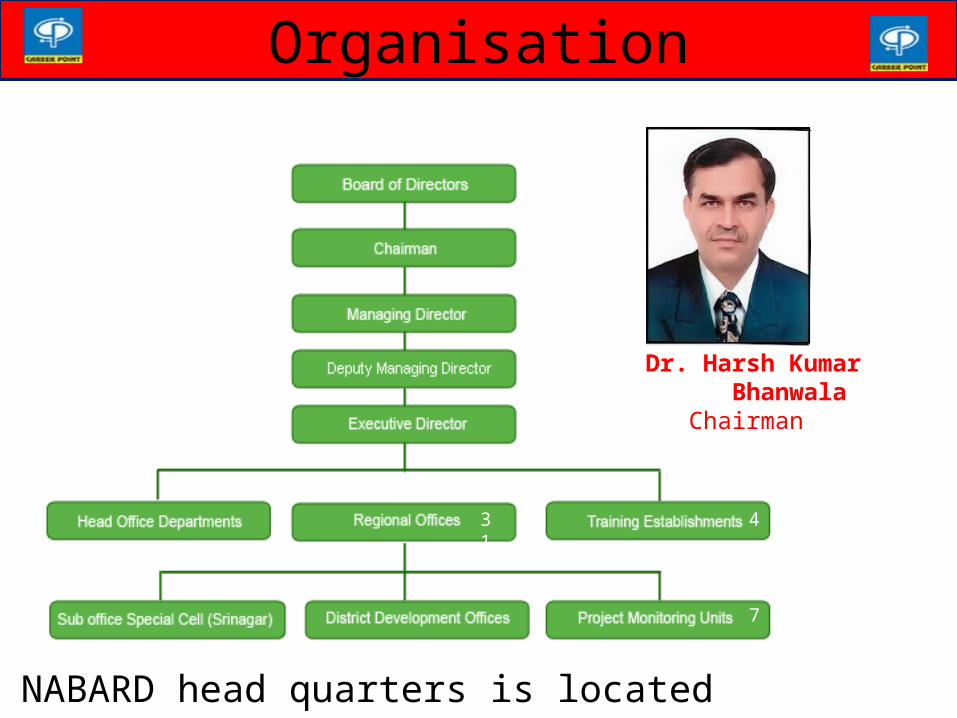

Dr. Harsh Kumar BhanwalaChairman

NABARD head quarters is located at Mumbai

431

7

Organisation

Functions of NABARD

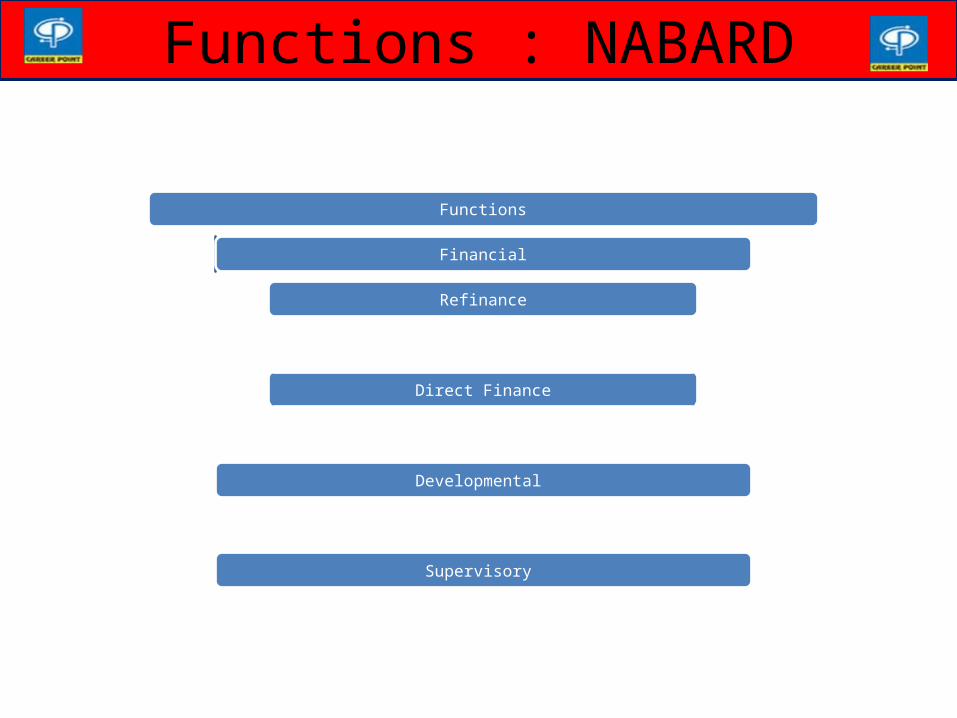

Functions

Financial

Refinance

Direct Finance

Developmental

Supervisory

Functions : NABARD

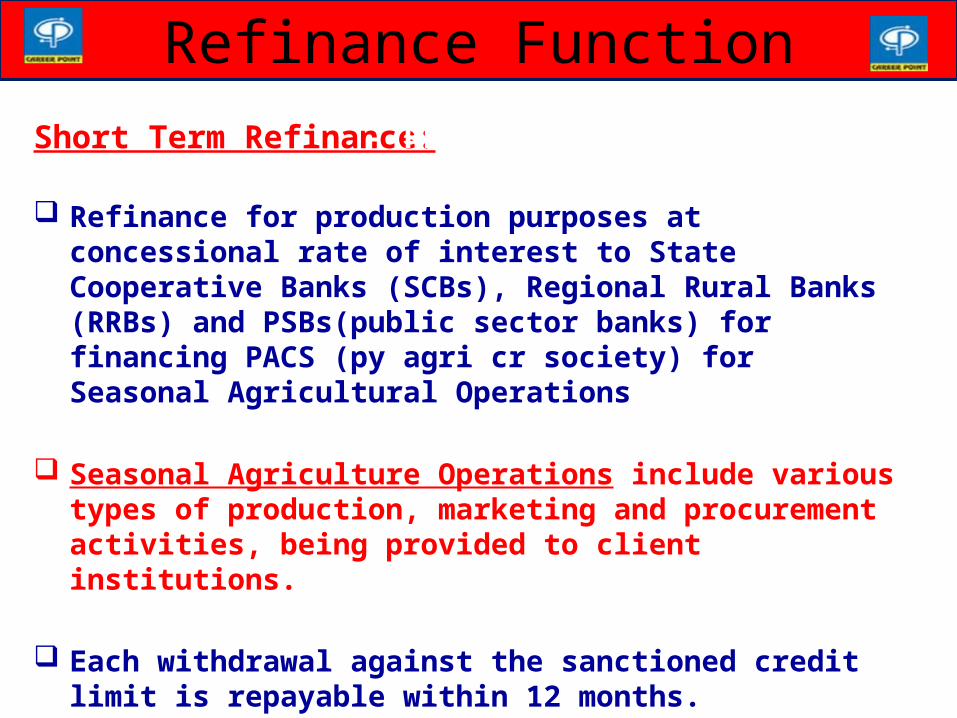

Short Term Refinance:

Refinance for production purposes at concessional rate of interest to State Cooperative Banks (SCBs), Regional Rural Banks (RRBs) and PSBs(public sector banks) for financing PACS (py agri cr society) for Seasonal Agricultural Operations

Seasonal Agriculture Operations include various types of production, marketing and procurement activities, being provided to client institutions.

Each withdrawal against the sanctioned credit limit is repayable within 12 months.

- REFINANCE

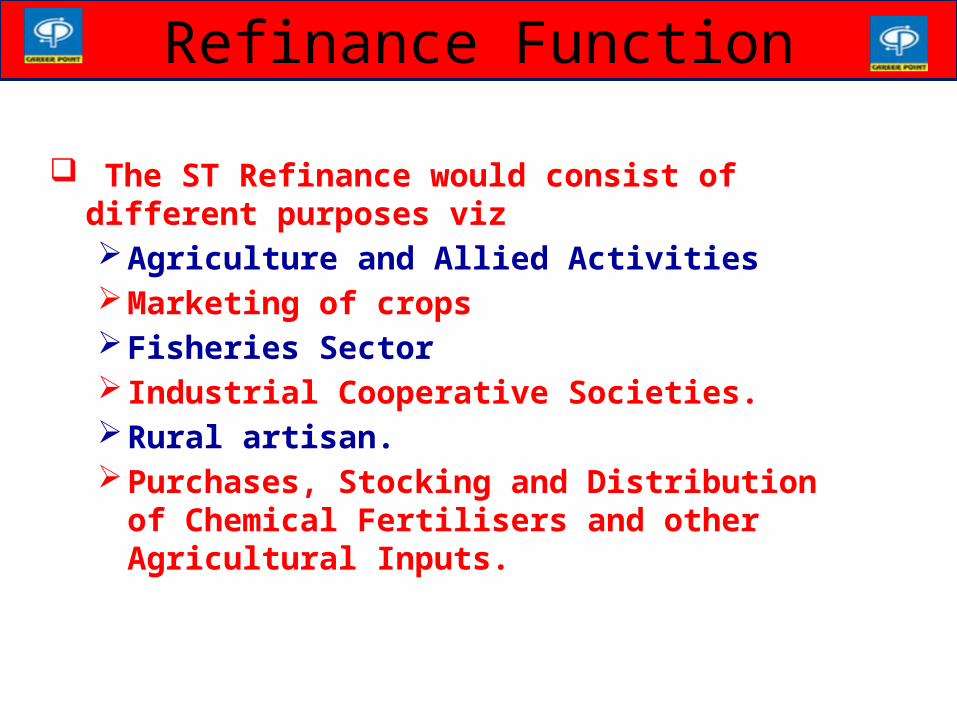

Refinance Function

The ST Refinance would consist of different purposes vizAgriculture and Allied ActivitiesMarketing of crops Fisheries Sector Industrial Cooperative Societies.Rural artisan.Purchases, Stocking and Distribution of Chemical

Fertilisers and other Agricultural Inputs.

Refinance Function

MT Conversion: NABARD provides relief to farmers whose crops are damaged due

to natural calamities by :-Conversion of current short term loans into medium term loansRe-phase / reschedule of existing MT (Conversion) loans.

Consolidated limit sanctioned to RRBs and SCBs in respect of eligible DCCBs.(Distt Co-op Central Bank)

Refinance Function

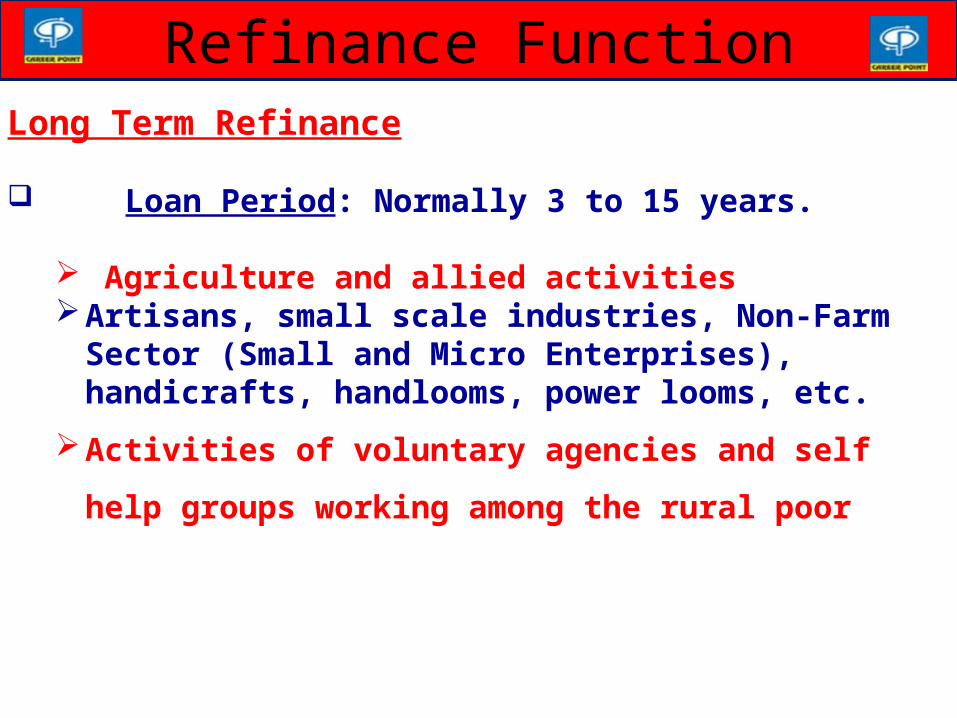

Long Term Refinance

Loan Period: Normally 3 to 15 years.

Agriculture and allied activitiesArtisans, small scale industries, Non-Farm Sector (Small and

Micro Enterprises), handicrafts, handlooms, power looms, etc.

Activities of voluntary agencies and self help groups working

among the rural poor

Refinance Function

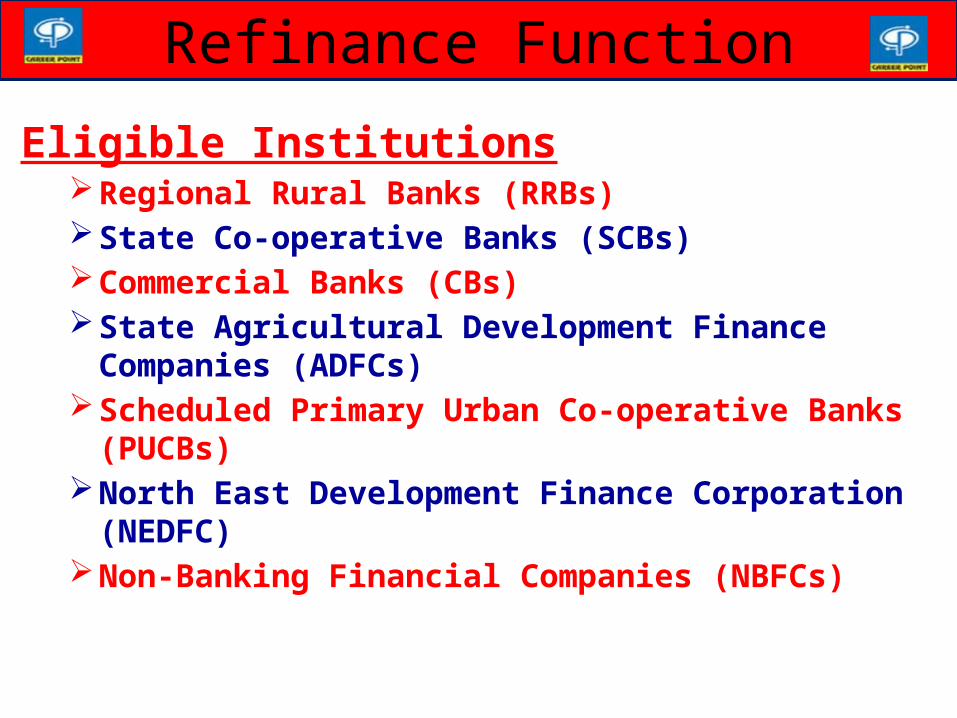

Eligible InstitutionsRegional Rural Banks (RRBs)State Co-operative Banks (SCBs)Commercial Banks (CBs)State Agricultural Development Finance Companies (ADFCs)Scheduled Primary Urban Co-operative Banks (PUCBs)North East Development Finance Corporation (NEDFC)Non-Banking Financial Companies (NBFCs)

Refinance Function

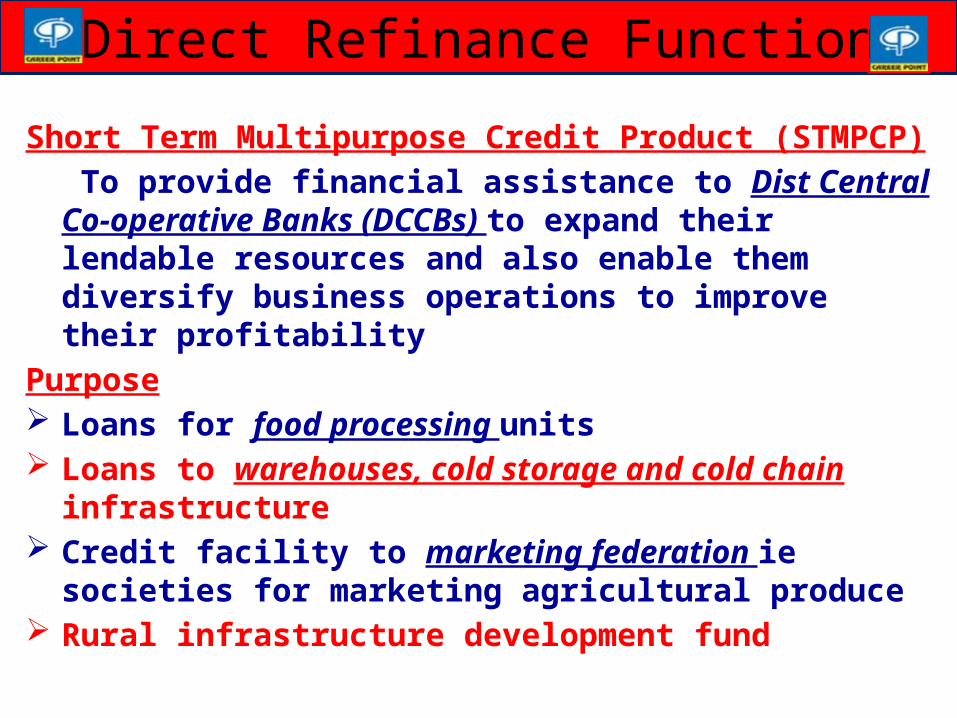

Short Term Multipurpose Credit Product (STMPCP) To provide financial assistance to Dist Central Co-operative Banks (DCCBs) to expand their lendable resources and also enable them diversify business operations to improve their profitability

Purpose Loans for food processing units Loans to warehouses, cold storage and cold chain infrastructure Credit facility to marketing federation ie societies for marketing

agricultural produce Rural infrastructure development fund

Direct Refinance Function

DEVELOPMENTAL FUNCTIONS

Farm sector Non farm sector Financial inclusion Research and development Core banking solution to cooperative banks

Development

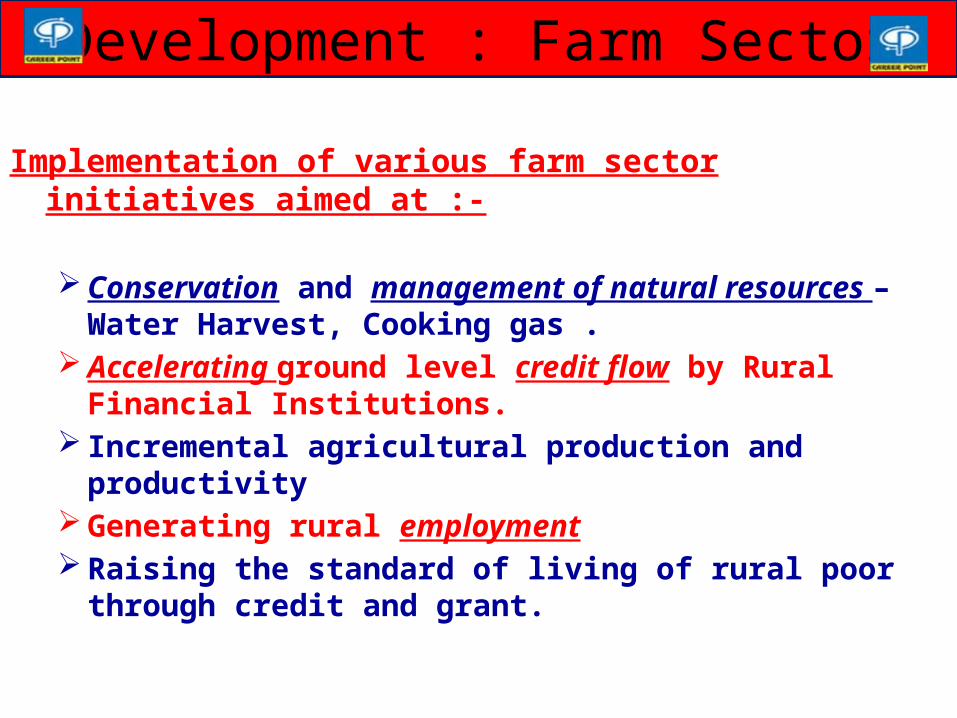

Implementation of various farm sector initiatives aimed at :-

Conservation and management of natural resources – Water Harvest, Cooking gas .

Accelerating ground level credit flow by Rural Financial Institutions. Incremental agricultural production and productivity Generating rural employment Raising the standard of living of rural poor through credit and grant.

Development : Farm Sector

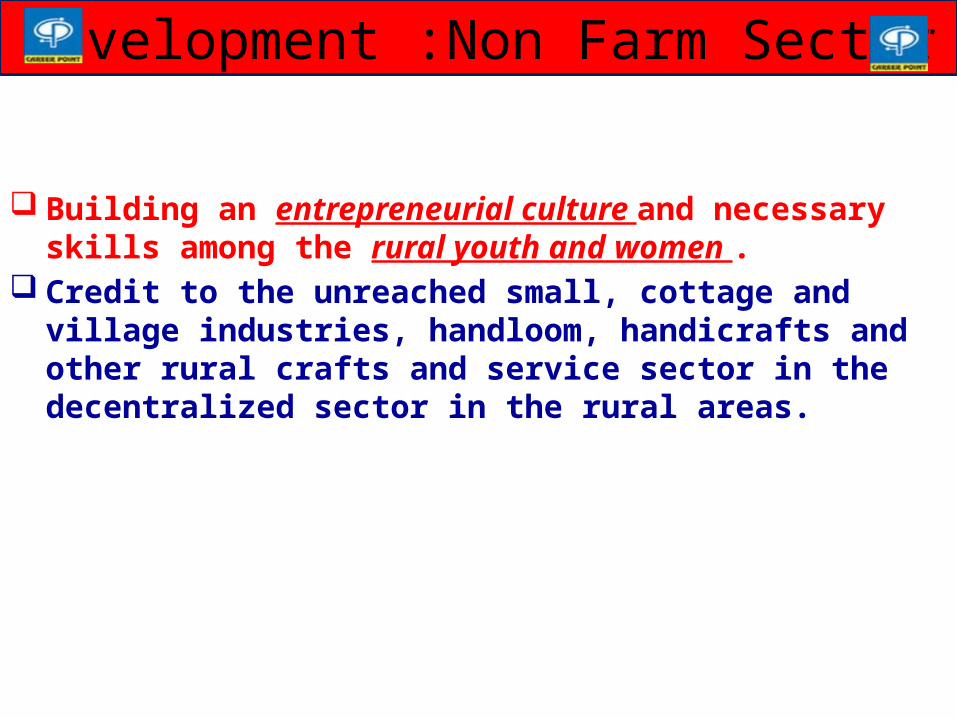

Building an entrepreneurial culture and necessary skills among the rural youth and women .

Credit to the unreached small, cottage and village industries, handloom, handicrafts and other rural crafts and service sector in the decentralized sector in the rural areas.

Development :Non Farm Sector

"The process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups such as weaker sections and low income groups at an affordable cost.”

Two Funds have been established for enhancing financial inclusion Financial Inclusion Fund (FIF)

Financial Literacy Centres & Programmes. Training staff of PACs and RRBs.

Financial Inclusion Technology Fund (FITF). Implementing Core Banking Solution(CBS)-Branch Networking Information and Communication Technology (ICT) . Kisan Credit Cards (KCC)

Financial Inclusion Department (FID) is the nodal department.

Development : Financial Inclusion

R&D Fund• To get to know the problems of agricultural and rural

development through in-depth studies and applied research.

• Utilised for formulating policies on agricultural operations and rural development, facilities for training, dissemination of information and promotion of research by undertaking surveys in the fields of agriculture, rural banking and rural development.

Research & Development

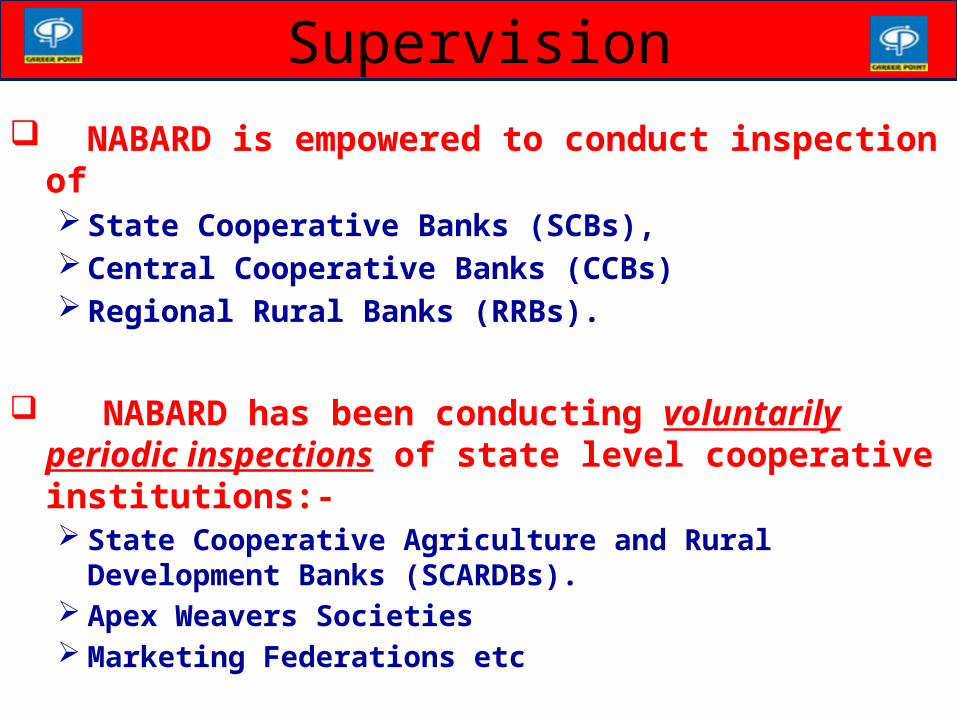

NABARD is empowered to conduct inspection of State Cooperative Banks (SCBs), Central Cooperative Banks (CCBs) Regional Rural Banks (RRBs).

NABARD has been conducting voluntarily periodic inspections of state level cooperative institutions:- State Cooperative Agriculture and Rural Development Banks

(SCARDBs). Apex Weavers Societies Marketing Federations etc

Supervision

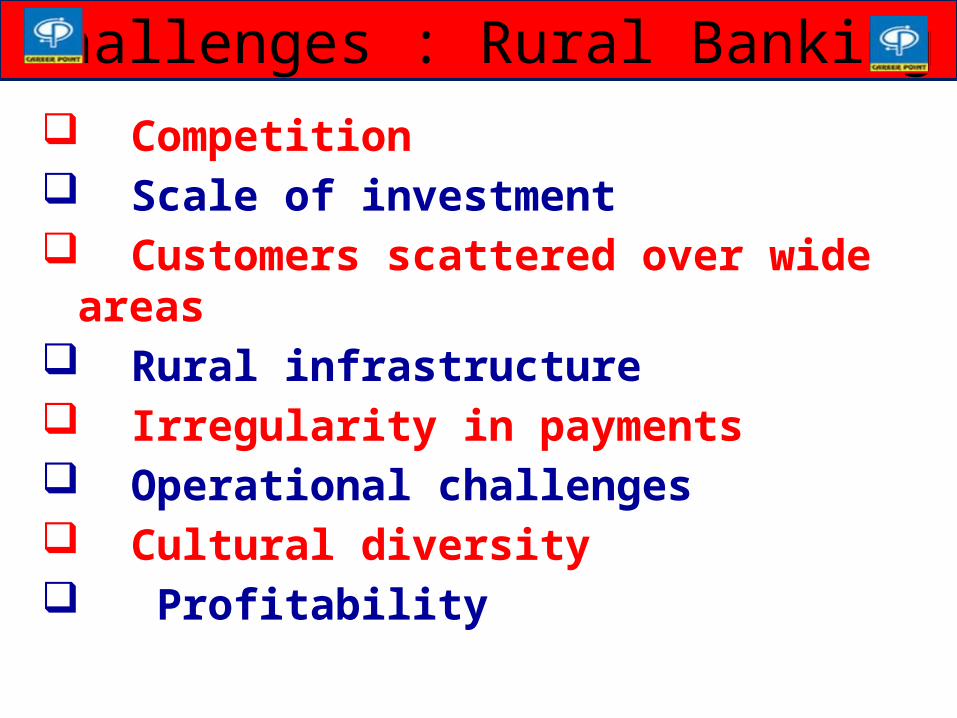

Competition Scale of investment Customers scattered over wide areas Rural infrastructure Irregularity in payments Operational challenges Cultural diversity Profitability

Challenges : Rural Banking

Conclusion

Thank You

Related Documents