FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY / AUGUST 2008 447 Rules-of-Thumb for Guiding Monetary Policy William Poole This article was originally published in the Board of Governors of the Federal Reserve System Open Market Policies and Operating Procedures—Staff Studies, July 1971. It is reprinted here as an addendum to these conference proceedings. Federal Reserve Bank of St. Louis Review, July/August 2008, 90(4), pp. 447-97. tory section outlines the structure of the study so that the reader can see how the various parts fit together. The reader interested only in a summary of the analysis and empirical findings should read this introductory section and then turn directly to the summary in Section V. This sum- mary concentrates on the theoretical analysis while only briefly stating the most important empirical findings. It omits completely the tech- nical details of both the theoretical and empirical work. The reader interested in the technical details should, of course, turn to the appropriate parts of Sections I through IV. Insofar as possible these sections have been written so that the reader can understand any one section without having to wade through all of the other sections. Section I contains the theoretical argument comparing interest rates and the money stock as policy-control variables under conditions of uncer- tainty. The analysis is verbal and graphical, using the simple Hicksian IS-LM model with random terms added. This model is general enough to include both Keynesian and monetarist outlooks, depending on the specific assumptions as to the shapes of the functions. Since the theoretical analysis emphasizes the importance of the relative INTRODUCTION T his study has been motivated by the recognition that the key to understanding policy problems is the analysis of uncer- tainty. Indeed, in the absence of uncertainty it might be said that there can be no policy prob- lems, only administrative problems. It is sur- prising, therefore, that there has been so little systematic attention paid to uncertainty in the policy literature in spite of the fact that policy- makers have repeatedly emphasized the impor- tance of the unknown. In the past, the formal models used in the analysis of monetary policy problems have almost invariably assumed complete knowledge of the economic relationships in the model. Uncertainty is introduced into the analysis, if at all, only through informal consideration of how much difference it makes if the true relationships differ from those assumed by the policymakers. In this study, on the other hand, uncertainty plays a key role in the formal model. Since this study is so long, a few comments at the outset may assist the reader in finding his way through it. The remainder of this introduc- William Poole is a former president of the Federal Reserve Bank of St. Louis. At the time this article was written, he was a senior economist in the special studies section of the division of research and statistics at the Board of Governors of the Federal Reserve System. Joan Walton, Lillian Humphrey, and Debra Bellows provided research assistance. © 2008, The Federal Reserve Bank of St. Louis. The views expressed in this article are those of the author(s) and do not necessarily reflect the views of the Federal Reserve System, the Board of Governors, or the regional Federal Reserve Banks. Articles may be reprinted, reproduced, published, distributed, displayed, and transmitted in their entirety if copyright notice, author name(s), and full citation are included. Abstracts, synopses, and other derivative works may be made only with prior written permission of the Federal Reserve Bank of St. Louis.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 447

Rules-of-Thumb for Guiding Monetary Policy

William Poole

This article was originally published in the Board of Governors of the Federal Reserve SystemOpen Market Policies and Operating Procedures—Staff Studies, July 1971. It is reprinted here asan addendum to these conference proceedings.

Federal Reserve Bank of St. Louis Review, July/August 2008, 90(4), pp. 447-97.

tory section outlines the structure of the study sothat the reader can see how the various parts fittogether. The reader interested only in a summaryof the analysis and empirical findings shouldread this introductory section and then turndirectly to the summary in Section V. This sum-mary concentrates on the theoretical analysiswhile only briefly stating the most importantempirical findings. It omits completely the tech-nical details of both the theoretical and empiricalwork. The reader interested in the technical detailsshould, of course, turn to the appropriate partsof Sections I through IV. Insofar as possible thesesections have been written so that the reader canunderstand any one section without having towade through all of the other sections.

Section I contains the theoretical argumentcomparing interest rates and the money stock aspolicy-control variables under conditions of uncer-tainty. The analysis is verbal and graphical, usingthe simple Hicksian IS-LMmodel with randomterms added. This model is general enough toinclude both Keynesian and monetarist outlooks,depending on the specific assumptions as to theshapes of the functions. Since the theoreticalanalysis emphasizes the importance of the relative

INTRODUCTION

T his study has been motivated by therecognition that the key to understandingpolicy problems is the analysis of uncer-

tainty. Indeed, in the absence of uncertainty itmight be said that there can be no policy prob-lems, only administrative problems. It is sur-prising, therefore, that there has been so littlesystematic attention paid to uncertainty in thepolicy literature in spite of the fact that policy-makers have repeatedly emphasized the impor-tance of the unknown.

In the past, the formal models used in theanalysis of monetary policy problems have almostinvariably assumed complete knowledge of theeconomic relationships in the model. Uncertaintyis introduced into the analysis, if at all, onlythrough informal consideration of how muchdifference it makes if the true relationships differfrom those assumed by the policymakers. In thisstudy, on the other hand, uncertainty plays a keyrole in the formal model.

Since this study is so long, a few commentsat the outset may assist the reader in finding hisway through it. The remainder of this introduc-

William Poole is a former president of the Federal Reserve Bank of St. Louis. At the time this article was written, he was a senior economist inthe special studies section of the division of research and statistics at the Board of Governors of the Federal Reserve System. Joan Walton,Lillian Humphrey, and Debra Bellows provided research assistance.

© 2008, The Federal Reserve Bank of St. Louis. The views expressed in this article are those of the author(s) and do not necessarily reflect theviews of the Federal Reserve System, the Board of Governors, or the regional Federal Reserve Banks. Articles may be reprinted, reproduced,published, distributed, displayed, and transmitted in their entirety if copyright notice, author name(s), and full citation are included. Abstracts,synopses, and other derivative works may be made only with prior written permission of the Federal Reserve Bank of St. Louis.

stability of the expenditures and money demandfunctions, an examination of the evidence onrelative stability appears in Section II.

Given the conclusion of Section II on thesuperiority of a policy operating through adjust-ments in themoney stock, the next question is howthe money stock should be adjusted to achievethe best results. While policymakers generallylook askance at suggestions for policy rules, theonly way that economists can give long-run adviceis in terms of rules. That is to say, the economistis not being helpful at all if he in effect says, “Lookat the rate of inflation, at the rate of unemploy-ment, at the forecasts of the government budgetdeficit, and at other relevant factors, and then actappropriately.” Advice requires the specificationof exactly how policy should be adjusted, and forthis advice to be more than an ad hoc recommen-dation for the current situation, it must involvespecification of how the money stock or someother control variable should be adjusted underhypothetical future conditions of inflation, unem-ployment, and so forth. The purpose of Section IIIis to develop such a rule-of-thumb, or policyguideline, based on the theoretical and empiricalanalyses of Sections I and ll.

A number of technical problems of monetarycontrol are examined in Section IV. After a shortintroduction to the issues, the first part of thissection discusses the relative merits of a numberof monetary aggregates including various reservemeasures, the narrowly and broadly definedmoney stocks, and bank credit. The second partexamines whether policy should specify desiredrates of change of an aggregate in terms of weekly,monthly, or quarterly averages, or in some othermanner. The third part examines in a very incom-plete fashion a few of the problems of adjustingopen market operations so as to reach the desiredlevel of an aggregate.

Finally, Section V consists of a summary ofSections I through IV. To avoid undue repetition,woven into this summary section are a number ofgeneral observations not examined in the othersections.

I. THE THEORY OF MONETARYPOLICY UNDER UNCERTAINTYBasic Concepts

The theory of optimal policy under uncer-tainty has provided many insights into actualpolicy problems (Theil, 1964; Brainard, 1967; Holt,1962; Poole, 1970). While much of this theory isnot accessible to the nonmathematical economist,it is possible to explain the basic ideas withoutresort to mathematics.

The obvious starting point is the observationthat with our incomplete understanding of theeconomy and our inability to predict accuratelythe occurrence of disturbing factors such as strikes,wars, and foreign exchange crises, we cannotexpect to hit policy goals exactly. Some periodsof inflation or unemployment are unavoidable.The inevitable lack of precision in reaching policygoals is sometimes recognized by saying that thegoals are “reasonably” stable prices and “reason-ably” full employment.

While the observation above is trite, itsimplications are not. Two points are especiallyimportant. First, policy should aim at minimizingthe average size of errors. Second, policy can bejudged only by the average size of errors over aperiod of time and not by individual episodes.Because this second point is particularly subject tomisunderstanding, it needs further amplification.

Since policymakers operate in a world thatis inherently uncertain, they must be judged bycriteria appropriate to such a world. Consider theanalogy of betting on the draw of a ball from anurnwith nine black balls and one red ball. Anyoneoffered a $2 payoff for a $1 bet would surely beton a black ball being drawn. If the draw producedthe red ball, no one would accuse the bettor of astupid bet. Similarly, the policymaker must playthe economic odds. The policymaker should notbe accused of failure if an inflation occurs as theresult of an improbable and unforeseeable event.

Now consider the reverse situation from thatconsidered in the previous paragraph. Supposethe bettor with the same odds as above bets on thered ball and wins. Some would claim that the betwas brilliant, but assuming that the draw was not

Poole

448 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

rigged inanyway, thebet, even thoughawinning one,must be judged foolish. It is foolish because, onthe average, such a betting strategy will lead tosubstantially worse results than the oppositestrategy. Betting on red will prove brilliant onlyone time out of 10, on the average. Similarly, aparticular policy action may be a bad bet eventhough it works in a particular episode.

There is a well-known tendency for gamblersto try systems that according to the laws of prob-ability cannot be successful over any length oftime. Frequently, a gambler will adopt a foolishsystem as the result of an initial chance successsuch as betting on red in the above example. Thesame danger exists in economic policy. In fact, thedanger is more acute because there appears to bea greater chance to “beat the system” by applyingeconomic knowledge and intuition. There can beno doubt that it will become increasingly possibleto improve on simple, naive policies throughsophisticated analysis and forecasting and so ina sense “beat the system.” But evenwith improvedknowledge some uncertainty will always exist,and therefore so will the tendency to attempt toperform better than the state of knowledge reallypermits.

Whatever the state of knowledge, there mustbe a clear understanding of how to cope withuncertainty, even though the degree of uncertaintymay have been drastically reduced through theuse of modern methods of analysis. The principalpurpose of this section is to improve understand-ing of the importance of uncertainty for policy byexamining a simple model in which the policyproblem is treated as one of minimizing errorson the average. Particular emphasis is placed onwhether controlling policy by adjusting the inter-est rate or by adjusting the money stock will leadto smaller errors on the average. The basic argu-ment is designed to show that the answer to whichpolicy variable—the interest rate or the moneystock—minimizes average errors depends on therelative stability of the expenditures and moneydemand functions and not on the values of param-eters that determine whether monetary policy isin some sense more or less “powerful” than fiscalpolicy.

Monetary Policy Under Uncertainty ina Keynesian Model1

The basic issues concerning the importanceof uncertainty for monetary policy may be exam-ined within the Hicksian IS-LM version of theKeynesian system. This elementary model hastwo sectors, an expenditure sector and a monetarysector, and it assumes that the price level is fixedin the short run.2 Consumption, investment, andgovernment expenditures functions are combinedto produce the IS function in Figure 1, while thedemand and supply of money functions are com-bined to produce the LM function. If monetarypolicy fixes the stock of money, then the resultingLM function is LM1, while if policy fixes the inter-est rate at r0 the resulting LM function is LM2. Itis assumed that incomes above “full employmentincome” are undesirable due to inflationary pres-sures while incomes below full employmentincome are undesirable due to unemployment.

If the positions of all the functions could bepredicted with no errors, then to reach fullemployment income, Yf , it would make no differ-

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 449

r

r0

LM1

LM2

Yf Y

IS

Figure 1

SOURCE: Originally published version, p. 139.

1 For the most part this section represents a verbal and graphicalversion of the mathematical argument in Poole (1970).

2 Simple presentations of this model may be found in Reynolds(1969, pp. 275-82) and Samuelson (1967, pp. 327-32).

ence whether policy fixed the money stock or theinterest rate. All that is necessary in either caseis to set the money stock or the interest rate sothat the resulting LM function will cut the IS func-tion at the full employment level of income.

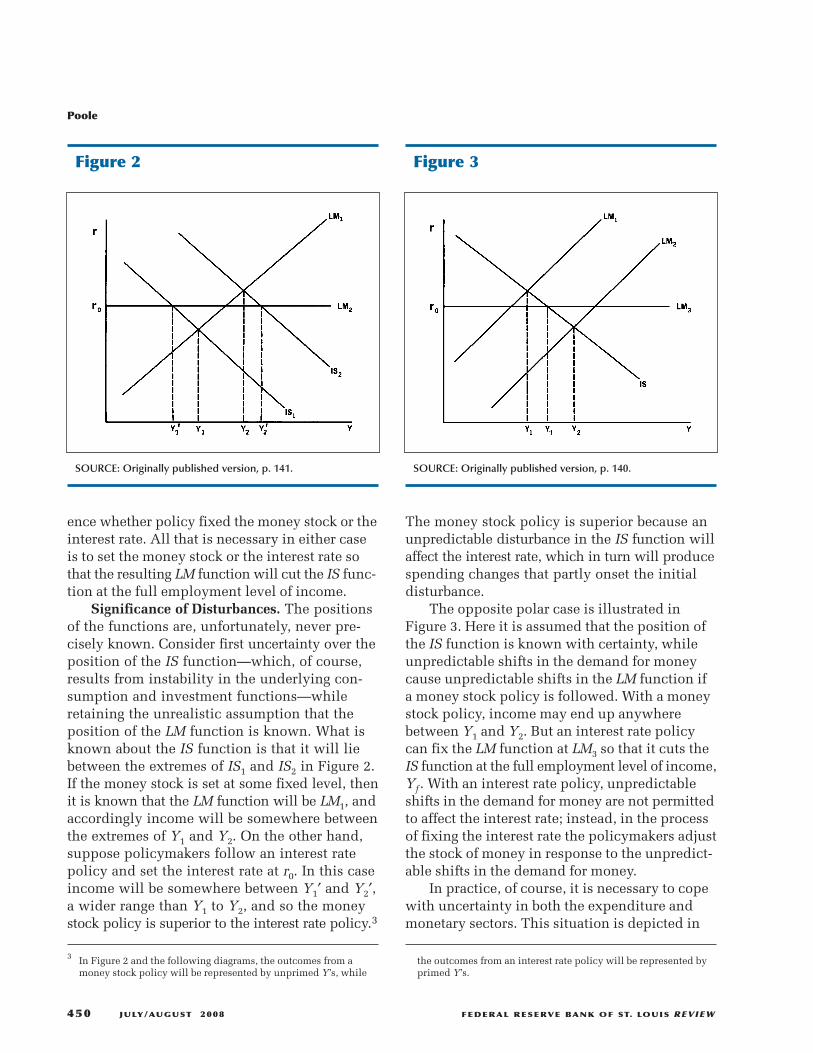

Significance of Disturbances. The positionsof the functions are, unfortunately, never pre-cisely known. Consider first uncertainty over theposition of the IS function—which, of course,results from instability in the underlying con-sumption and investment functions—whileretaining the unrealistic assumption that theposition of the LM function is known. What isknown about the IS function is that it will liebetween the extremes of IS1 and IS2 in Figure 2.If the money stock is set at some fixed level, thenit is known that the LM function will be LM1, andaccordingly income will be somewhere betweenthe extremes of Y1 and Y2. On the other hand,suppose policymakers follow an interest ratepolicy and set the interest rate at r0. In this caseincome will be somewhere between Y1′ and Y2′,a wider range than Y1 to Y2, and so the moneystock policy is superior to the interest rate policy.3

The money stock policy is superior because anunpredictable disturbance in the IS function willaffect the interest rate, which in turn will producespending changes that partly onset the initialdisturbance.

The opposite polar case is illustrated inFigure 3. Here it is assumed that the position ofthe IS function is known with certainty, whileunpredictable shifts in the demand for moneycause unpredictable shifts in the LM function ifa money stock policy is followed. With a moneystock policy, income may end up anywherebetween Y1 and Y2. But an interest rate policycan fix the LM function at LM3 so that it cuts theIS function at the full employment level of income,Yf . With an interest rate policy, unpredictableshifts in the demand for money are not permittedto affect the interest rate; instead, in the processof fixing the interest rate the policymakers adjustthe stock of money in response to the unpredict-able shifts in the demand for money.

In practice, of course, it is necessary to copewith uncertainty in both the expenditure andmonetary sectors. This situation is depicted in

the outcomes from an interest rate policy will be represented byprimed Y’s.

Poole

450 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

Figure 2

SOURCE: Originally published version, p. 141.

Figure 3

SOURCE: Originally published version, p. 140.

3 In Figure 2 and the following diagrams, the outcomes from amoney stock policy will be represented by unprimed Y’s, while

Figure 4, where the unpredictable disturbances arelarger in the expenditure sector, and in Figure 5where the unpredictable disturbances are largerin the monetary sector.

The situation is even more complicated thanshown in Figures 4 and 5 by virtue of the factthat the disturbances in the two sectors may notbe independent. To illustrate this case, considerFigure 5 in which the interest rate policy is supe-rior to the money stock policy if the disturbancesare independent. Suppose that the disturbanceswere connected in such a way that disturbanceson the LM1 side of the average LM function werealways accompanied by disturbances on the IS2side of the average IS function. This would meanthat income would never go as low as Y1, butrather only as low as the intersection of LM1 andIS2, an income not as low as Y1′ under the interestrate policy. Similarly, the highest income wouldbe given by the intersection of LM2 and IS1, anincome not so high as Y2′.4

Importance of Interest Elasticities and OtherParameters. So far the argument has concentratedentirely on the importance of the relative sizesof expenditure and monetary disturbances. Butis it also important to consider the slopes of thefunctions as determined by the interest elastici-ties of investment and of the demand for money,and by other parameters? Consider the pair of ISfunctions, IS1 and IS2, as opposed to the pair, IS3and IS4, in Figure 6. Each pair represents themaximum and minimum positions of the IS func-tion as a result of disturbances, but the pairs havedifferent slopes. Each pair assumes the samemaximum and minimum disturbances, as shownby the fact that the horizontal distance betweenIS1 and IS2 is the same as between IS3 and IS4.For convenience, but without loss of generality,the functions have been drawn so that underan interest rate policy represented by LM2 bothpairs of IS functions produce the same range ofincomes. To keep the diagram from becoming

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 451

4 The diagram could obviously have been drawn so that an interestrate policy would be superior to a money stock policy even thoughthere was an inverse relationship between the shifts in the IS andLM functions. However, inverse shifts always reduce the margin

Figure 4

SOURCE: Originally published version, p. 141.

Figure 5

SOURCE: Originally published version, p. 141.

of superiority of an interest rate policy, possibly to the point ofmaking a money stock policy superior. Conversely, positivelyrelated shifts favor an interest rate policy.

Poole

452 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

Figure 7

SOURCE: Originally published version, p. 141.

Figure 6

SOURCE: Originally published version, p. 141.

Figure 8

SOURCE: Originally published version, p. 143.

Figure 9

SOURCE: Originally published version, p. 143.

too messy, only one LM function, LM1, under amoney stock policy has been drawn. Now con-sider disturbances that would shift LM1 back andforth. From Figure 6 it is easy to see that if shiftsin LM1 would lead to income fluctuations greaterthan from Y1′ to Y2′—which fluctuations wouldoccur under an interest rate policy—then aninterest policy would be preferred regardless ofwhether we have the pair IS1 and IS2, or the pairIS3 and IS4.

The importance of the slope of the LM functionis investigated in Figure 7 for the two LM pairs,LM1 and LM2, and LM3 and LM4. The functionshave been drawn so that each pair representsdifferent slopes but an identical range of distur-bances. It is clear that if shifts in IS1 are smallenough, then an interest rate policy will be pre-ferred regardless of which pair of LM functionsprevails. Conversely, if a money stock policy ispreferred under one pair of LM functions becauseof the shifts in the IS function, then a money stockpolicy will also be preferred under the other pairof LM functions.

The upshot of this analysis is that the crucialissue for deciding upon whether an interest rateor a money stock policy should be followed is therelative size of the disturbances in the expendi-ture and monetary sectors. Contrary to muchrecent discussion, the issue is not whether theinterest elasticity of the demand for money isrelatively low or whether fiscal policy is more orless “powerful” than monetary policy.

To avoid possible confusion, it should beemphasized that the above conclusion is in termsof the choice between a money stock policy andan interest rate policy. However, if a money stockpolicy is superior, then the steeper the LM func-tion is, the lower the range of income fluctuation,as can be seen from Figure 7. It is also clear fromFigure 6 that under an interest rate policy an errorin setting the interest rate will lead to a larger errorin hitting the income target if the IS function isrelatively flat than if it is relatively steep. Butthese facts do not affect the choice betweeninterest rate and money stock policies.

The “Combination” Monetary Policy. Up tothis point the analysis has concentrated on thechoice of either the interest rate or the money

stock as the policy variable. But it is also possibleto consider a “combination” policy that worksthrough the money stock and the interest ratesimultaneously. An understanding of the combi-nation policy may be obtained by further consid-eration of the cases depicted in Figures 2 and 7.

In Figure 8 the disturbances, as in Figure 2,are entirely in the expenditure sector. As wasseen in Figure 2, the result obtained by fixing themoney stock so that LM1 prevailed was superiorto that obtained by fixing the interest rate so thatLM2 prevailed. But now suppose that instead offixing the money stock, the money stock werereduced every time the interest rate went up andincreased every time the interest rate went down.This procedure would, of course, increase theamplitude of interest rate fluctuations.5 But if theproper relationship between the money stock andthe interest rate could be discovered, then theLM function could be made to look like LM0 inFigure 8. The result would be that income wouldbe pegged at Yf . Disturbances in the IS functionwould produce changes in the interest rate, whichin turn would produce spending changes suffi-cient to completely offset the effect on income ofthe initial disturbance.

The most complicated case of all to explaingraphically is that in which it is desirable toincrease the money stock as the interest rate risesand decrease it as the interest rate falls. In Figure 9the leftmost position of the LM function as aresult of disturbances is LM1 when the moneystock is fixed and is LM2 when the combinationpolicy of introducing a positive money-interestrelationship is followed. The rightmost positionsof the LM functions under these conditions are notshown in the diagram. When the interest rate ispegged, the LM function is LM3. If either LM1 orLM2 prevails, the intersection with IS1 producesthe lowest income, which is below the Y1′ level

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 453

5 The increased fluctuations in interest rates must be carefullyinterpreted. In this model the IS function is assumed to fluctuatearound a fixed-average position. However, in more complicatedmodels involving changes in the average position of the IS function,perhaps through the operation of the investment accelerator, interestrate fluctuations may not be increased by the policy being discussedin the text. By increasing the stability of income over a period oftime, the policy would increase the stability of the IS function inFigure 8 and thereby reduce interest rate fluctuations.

obtained with LM3. But in the case of LM2, incomeat Y1 is only a little lower than at Y1′, whereaswhen IS2 prevails, LM2 is better than LM3 by thedifference between Y2 and Y2′. Since the gapbetween Y2 and Y2′ is larger than that between Y1and Y1′, it is on the average better to adopt LM2

than LM3 even though the extremes under LM2

are a bit larger than under LM3.Extensions of Model. At this point a natural

question is that of the extent to which the aboveanalysis would hold in more complex models.Until more complicated models are constructedand analyzed mathematically, there is no way ofbeing certain. But it is possible to make educatedguesses on the effects of adding more goals andmore policy instruments, and of relaxing the rigidprice assumption.

Additional goals may be added to the modelif they are specified in terms of “closer is better”rather than in terms of a fixed target that must bemet. For example, it would not be mathematicallydifficult to add an interest rate goal to the modelanalyzed above, if deviations from a target interestrate were permitted but were treated as beingincreasingly harmful. On the other hand, it isclear that if there were a fixed-interest target,then the only possible policy would be to pegthe interest rate, and income stabilization wouldnot be possible with monetary policy alone.

The addition of fiscal policy instrumentsaffects the results in two major ways. First, theexistence of income taxes and of governmentexpenditures inversely related to income (forexample, unemployment benefits) provides auto-matic stabilization. In terms of the model, auto-matic stabilizers make the IS function steeper thanit otherwise would be, thus reducing the impactof monetary disturbances, and reduce the varianceof expenditures disturbances in the reduced-formequation for income. This effect would be shownin Figure 6 by drawing IS1 so that it cuts LM2 tothe right of Y1′ and drawing IS2 so that it cuts LM2

to the left of Y2′.The second major impact of adding fiscal

policy instruments occurs if both income and theinterest rate are goals. Horizontal shifts in the ISfunction that are induced by fiscal policy adjust-ments, when accompanied by a coordinatedmone-

tary policy, make it possible to come closer to adesired interest rate without any sacrifice inincome stability. An obvious illustration is pro-vided by the case in which the optimal monetarypolicy from the point of view of stabilizing incomeis to set the interest rate as in Figure 5. Fiscalpolicy can then shift the pair of IS functions, IS1and IS2, to the right or left so that the expectedvalue of income is at the full employment level.

If the interest rate is not a goal variable, thenfiscal policy actions that shift the IS functionwithout changing its slope do not improve incomestabilization over what can be accomplished withmonetary policy alone, provided the lags in theeffects of monetary policy are no longer than thosein the effects of fiscal policy. An exception wouldbe a situation in which reaching full employmentwith monetary policy alone would require anunattainable interest rate, such as a negative one.

These comments on fiscal policy have beenpresented in order to clarify the relationshipbetween fiscal and monetary policy. While mone-tary policymakers may urge fiscal action, for themost part monetary policy must take the fiscalsetting as given and adapt monetary policy tothis setting. It must then be recognized that aninterest rate goal can be pursued only at the costof sacrificing somewhat the income goal.6

All of the analysis so far has taken placewithin a model in which the price level is fixedin the short run. This assumption may be relaxedby recognizing that increases in money incomeabove the full employment level involve a mix-ture of real income gains and price inflation.Similarly, reductions in money income belowthe full employment level involve real incomereductions and price deflation (or a slower rateof price inflation). The model used above can bereinterpreted entirely in terms of money incomeso that departures from what was called abovethe “full employment” level of income involve amixture of real income and price changes. Stabi-

6 An interest rate goal must be sharply distinguished from the useof the interest rate as a monetary policy instrument. By a goalvariable is meant a variable that enters the policy utility function.Income and interest rate goals might be simultaneously pursuedby setting the money stock as the policy instrument or by settingthe interest rate as the policy instrument.

Poole

454 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

lizing money income, then, involves a mixtureof the two goals of stabilizing real output and ofstabilizing the price level.

However, interpreted in this way the structureof the model is deficient because it fails to dis-tinguish between real and nominal interest rates.Price level increases generate inflationary expec-tations, which in turn generate an outward shiftin the IS function. The model may be patched upto some extent by assuming that price changesmake up a constant fraction of the deviation ofincome from its full employment level and assum-ing further that the expected rate of inflation is aconstant multiplied by the actual rate of inflation.Expenditures are then made to depend on the realrate of interest, the difference between the nomi-nal rate of interest and the expected rate of infla-tion. The result is to make the IS function, whendrawn against the nominal interest rate, flatter andto increase the variance of disturbances to the ISfunction. These elects are more pronounced: (a)the larger is the interest sensitivity of expendi-tures; (b) the larger is the fraction of price changesin money income changes; and (c) the larger isthe effect of price changes on price expectations.The conclusion is that since price flexibility ineffect increases the variance of disturbances inthe IS function, a money stock policy tends to befavored over an interest rate policy.

II. EVIDENCE ON THE RELATIVEMAGNITUDES OF REAL ANDMONETARY DISTURBANCESNature of Available Evidence

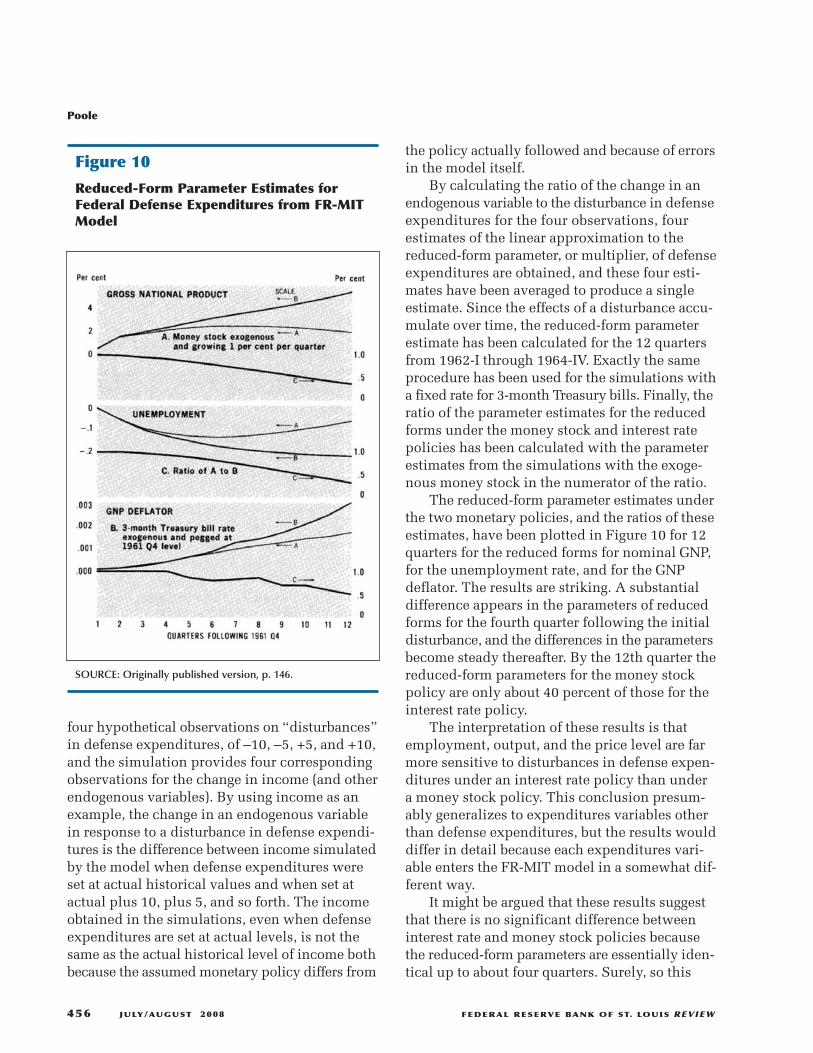

Little evidence is available that directly teststhe relative stability of the expenditure andmoneydemand functions. It is necessary, therefore, toproceed somewhat indirectly. First, simulation ofthe FR-MIT model7 is used to show the probablesize of the effect on gross national product (GNP),the GNP deflator, and the unemployment rate ofan assumed expenditure disturbance. This evi-

dence provides some indication of the extent towhich the impact of an expenditure disturbancedepends on the choice between the money stockand the Treasury bill rate as monetary policy con-trol variables. This evidence bears only on thequestion of what happens if an expenditure dis-turbance occurs, not on the relative stability ofthe expenditure and money demand functions.However, this approach is useful when combinedwith intuitive feelings about relative stability.

The second type of evidence, derived fromreduced-form studies, is more directly related tothe question of relative stability; nevertheless, itis not entirely satisfactory because the studiesexamined were not designed to answer the ques-tion at hand. To supplement these studies byother investigators, there follows a simple test ofthe stability of the demand for money function.

Impact of an Expenditure Disturbance

Simulation of the FR-MIT model providessome insight as to how the size of the impact ofan expenditure disturbance depends on the choiceof the monetary policy instrument. The simula-tion technique is necessary because the FR-MITmodel is nonlinear, making it impossible to obtainan explicit expression for the reduced form.8

However, comparison of two sets of simulationsprovides some interesting results. Except as indi-cated below, the simulations all used the actualhistorical values of the model’s exogenous vari-ables and all simulations started with 1962-I, astarting date selected arbitrarily.

The first set of five simulations assumes anexogenous money stock that grows by 1 percentper quarter, starting with the actual money stockin 1961-IV as the base. To investigate the impactof a disturbance in an exogenous expendituresvariable, the exogenous variable “federal expen-ditures on defense goods” was set in one simula-tion at its actual level minus $10 billion; in anotherat actual minus $5 billion; and in three furthersimulations at actual, actual plus $5 billion, andactual plus $10 billion. This procedure produces

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 455

7 For a general description of the model, see de Leeuw and Gramlich(1968).

8 In a reduced-form equation, an endogenous (that is, simultaneouslydetermined) variable is expressed as depending only on exogenousand predetermined variables (variables taken as given for thecurrent period).

four hypothetical observations on “disturbances”in defense expenditures, of –10, –5, +5, and +10,and the simulation provides four correspondingobservations for the change in income (and otherendogenous variables). By using income as anexample, the change in an endogenous variablein response to a disturbance in defense expendi-tures is the difference between income simulatedby the model when defense expenditures wereset at actual historical values and when set atactual plus 10, plus 5, and so forth. The incomeobtained in the simulations, even when defenseexpenditures are set at actual levels, is not thesame as the actual historical level of income bothbecause the assumedmonetary policy differs from

the policy actually followed and because of errorsin the model itself.

By calculating the ratio of the change in anendogenous variable to the disturbance in defenseexpenditures for the four observations, fourestimates of the linear approximation to thereduced-form parameter, or multiplier, of defenseexpenditures are obtained, and these four esti-mates have been averaged to produce a singleestimate. Since the effects of a disturbance accu-mulate over time, the reduced-form parameterestimate has been calculated for the 12 quartersfrom 1962-I through 1964-IV. Exactly the sameprocedure has been used for the simulations witha fixed rate for 3-month Treasury bills. Finally, theratio of the parameter estimates for the reducedforms under the money stock and interest ratepolicies has been calculated with the parameterestimates from the simulations with the exoge-nous money stock in the numerator of the ratio.

The reduced-form parameter estimates underthe two monetary policies, and the ratios of theseestimates, have been plotted in Figure 10 for 12quarters for the reduced forms for nominal GNP,for the unemployment rate, and for the GNPdeflator. The results are striking. A substantialdifference appears in the parameters of reducedforms for the fourth quarter following the initialdisturbance, and the differences in the parametersbecome steady thereafter. By the 12th quarter thereduced-form parameters for the money stockpolicy are only about 40 percent of those for theinterest rate policy.

The interpretation of these results is thatemployment, output, and the price level are farmore sensitive to disturbances in defense expen-ditures under an interest rate policy than undera money stock policy. This conclusion presum-ably generalizes to expenditures variables otherthan defense expenditures, but the results woulddiffer in detail because each expenditures vari-able enters the FR-MIT model in a somewhat dif-ferent way.

It might be argued that these results suggestthat there is no significant difference betweeninterest rate and money stock policies becausethe reduced-form parameters are essentially iden-tical up to about four quarters. Surely, so this

Poole

456 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

Figure 10

Reduced-Form Parameter Estimates forFederal Defense Expenditures from FR-MITModel

SOURCE: Originally published version, p. 146.

argument goes, mistakes could be discovered andonset within four quarters. There are two diffi-culties with this argument. The first is that theFR-MIT model may overstate the length of thelags and therefore understate the differences inreduced-form parameters for the two policies forthe quarters immediately following a disturbance.But the second and more important reason is thatit may not be easy to reverse the effects of thedisturbance after the disturbance has been dis-covered. With an interest rate policy, a very largechange in the rate might be required to offset theeffects appearing after the fourth quarter, and sucha change might not be feasible, or at least notdesirable in terms of its effects on security marketsand on income in the more distant future.

The numerical results reported above depend,of course, on the FR-MIT model, and this modelis deficient in a number of respects. But anymodel in which, other things being equal, invest-ment and other interest-sensitive expendituresdecline when interest rates rise will show resultsin the same direction.

These results may be extended to analyze thesignificance of errors in forecasting exogenousvariables. Consider an explicit expression for thereduced form for income. Let the exogenous vari-ables such as government expenditures, perhapscertain categories of investment, strikes, weather,population growth, and so forth, be X1, X2, …, Xn,and let the coefficients of these variables be α1, α2,…, αn when the interest rate is the policy instru-ment, and λ1, λ2, …, λn when the money stock isthe instrument. Then the reduced form for incomewhen the interest rate is the instrument is

(1)

where αr is the coefficient of the interest rate andu is the random disturbance. On the other hand,when the money stock is the instrument, thereduced form is

(2)

As discussed in Section II, the disturbance νtmay have either a larger or a smaller variance thanthe disturbance ut. One factor tending to makeνt smaller than ut is that a money stock policy

Y X X X Mn n M= + + +…+ + +λ λ λ λ λ ν0 1 1 2 2

Y X X X r un n r= + + +…+ + +α α α α α0 1 1 2 2

reduces the impact of expenditures disturbances,but another factor, the introduction into thereduced form of money demand disturbances,tends to make νt larger. The net result of thesetwo factors cannot be determined a priori.

But in formulating policy it is not possible toreason directly from equations 1 and 2 becausemany of the Xi cannot be predicted in advancewith perfect accuracy. For scientific purposes expost it may be possible to say that a change inincome was caused by a change in some Xi; forpolicy purposes ex ante this scientific knowledgeis useless unless the change inXi can be predicted.It is necessary to think of each Xi as being com-posed of a predictable part, Xi, and an unpredict-able part, Ei.

For policy purposes the error term in thereduced form includes both the disturbances tothe equation and the errors in forecasting exoge-nous variables. The two types of errors ought tobe treated exactly alike in formulating policy.Equations 1 and 2 can then be rewritten as follows:

(3)

(4)

For policy purposes the error term in the reduced-form equation 3 is the sum of the terms from α1E1tthrough ut and in the reduced-form equation 4the sum of the term λ1E1t through νt.

A systematic study of the importance of theEi terms cannot be made because no formal recordof errors in forecasting exogenous variables existsinsofar as the author knows. However, someinsight into the problem may be obtained by list-ing the variables that must be forecast. Whichvariables have to be forecast depends, of course,on the model being used. The larger econometricmodels generally have relatively few exogenousvariables that raise forecasting problems becauseso many variables are explained endogeneouslyby the model itself. The FR-MIT model has 63

X X Ei i i= +ˆ

Y X X X

r E Ei n n

r

= + + +…++ + + +…+α α α αα α α α

0 1 2 2

1 1 2 2

ˆ ˆ ˆ

� nn nE u+

Y X X X

M E Ei n N

M

= + + +…++ + + +…+λ λ λ λλ λ λ λ

0 1 2 2

1 1 2 2

ˆ ˆ ˆ

� nn nE +ν

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 457

exogenous variables; some of these are relativelyeasy to forecast, but others are subject to consid-erable forecasting error. The latter include suchvariables as exports, number of mandays idle dueto strikes, armed forces, and federal expenditures.Furthermore, this model involves lagged endoge-nous variables in many equations; hence an inac-curate forecast of GNP next quarter will increasethe error in forecasting GNP two quarters into thefuture, which in turn will lead to errors in fore-casting GNP three quarters into the future, and soforth. Errors in forecasting exogenous variables,therefore, produce cumulative errors in forecast-ing GNP in future quarters.

In simpler models the forecasting problem ismore severe. Consider, for example, the oppositeextreme from the large econometric model, thesingle-equationmodel. Convenient representativesof such models are those spawned in the contro-versy over the Friedman-Meiselman paper (1963)on the stability of the money/income relationship.The various definitions of exogenous, or “autono-mous,” spending utilized by the various authorsin this controversy are as follows :

a) Friedman-Meiselman definition: Autono-mous expenditures consist of the “netprivate domestic investment plus the gov-ernment deficit on income and productaccount plus the net foreign balance”(Friedman and Meiselman, 1963, p. 184).

b)Ando-Modigliani definition: Autonomousexpenditures consist of two variables whichenter the reduced form with different coef-ficients. One variable is “property tax por-tion of indirect business taxes” plus “netinterest paid by government” plus “govern-ment transfer payment” minus “unemploy-ment insurance benefits” plus “subsidiesless current surplus of government enter-prises” minus “statistical discrepancy”minus “excess of wage accruals over dis-bursement.” The second variable is “netinvestment in plant and equipment, andin residential houses” plus “exports” (AndoandModigliani, 1965a, pp. 695-96, 702).

c) DePrano-Mayer definition: The basic defini-tion is “investment in producers’ durable

equipment, nonresidential construction,residential construction, federal govern-ment expenditures on income and productaccount, and exports. One variant of thishypothesis subtracts capital consumptionestimates, and the other does not” (DePranoand Mayer, 1965a, p. 739). DePrano andMayer also tested 18 other definitions ofautonomous expenditures (DePrano andMayer, 1965a, pp. 739-40).

d)Hester definition: Autonomous expendi-tures consist of the “sum of governmentexpenditure, net private domestic invest-ment, and the trade balance” (Hester, 1964a,p. 366). Hester also experimented withthree other definitions involving alterna-tive treatments of imports, capital consump-tion allowances, and inventory investment(Hester, 1964a, pp. 366-67).

To a considerable extent the diversity in thesedefinitions is misleading because except for theFriedman-Meiselman definition all the definitionsare in fact rather similar. But whichever definitionis used, it is impossible to escape the feeling thatinaccurate forecasting of exogenous variables islikely to be a major source of uncertainty. Andwhile this discussion has taken place within thecontext of formal models, exactly the same prob-lem plagues judgmental forecasting. Every fore-casting method can be viewed as starting fromforecasts of “input,” or exogenous, variables andthen proceeding to judge the implications of theseinputs for GNP and other dependent, or endoge-nous, variables.

Regardless of what type of model is used, itappears that for the foreseeable future it will benecessary to forecast exogenous variables thatsimply cannot be forecast accurately by usingpresent methods. As a result, it seems very likelythat the error term including forecast errors hasa far smaller variance in equation 4 than in equa-tion 3. Indeed, it might be argued that as a sourceof uncertainty the Ei terms are far more importantthan the u or ν terms, and therefore that thesmaller size of the λi parameters as compared tothe α i parameters is of great importance. If theparameter estimates from the FR-MIT model areaccepted, the standard deviation of the total ran-

Poole

458 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

dom term relevant for policy (that is, includingerrors in forecasting exogenous variables) wouldbe over twice as large under an interest rate policyas under a money stock policy. If this argumentis correct, shifting from the current policy ofemphasizing interest rates to one of controllingthe money stock might cut average errors in half,where errors are measured in terms of the devia-tions of employment, output, and price level fromtarget levels for these variables.

Evidence from Reduced-Form Equations

Additional insight into the relative sizes ofdisturbances under interest rate and money stockpolicies may be obtained by examining the con-troversy generated by the Friedman-Meiselmanpaper on the stability of the money/income rela-tionship (Friedman andMeiselman, 1963). In thispaper equations almost the same as equations 1and 2 above were estimated. The equation corre-sponding to equation 1 differs in that the exoge-nous variables were assumed to consist only of asingle autonomous spending variable, as definedabove. The equation corresponding to equation 2has the same disability for our purposes, but italso did not include an interest rate as a variable.

Before examining the implications of theFriedman-Meiselman findings for this study, itshould be noted that their approach was sharplycriticized in papers by Donald D. Hester (1964a),Albert Ando and Franco Modigliani (1965a), andMichael DePrano and Thomas Mayer (1965a).These critics particularly attacked the Friedman-Meiselman definition of autonomous expendi-tures, and proposed and tested the alternativedefinitions listed above. However, they alsoattacked the single-equation approach and recom-mended the use of large models instead.

The tests of alternative equations must beregarded as inconclusive in terms of which vari-able—the money stock or autonomous spending—is more closely related to the level of income.9

Both approaches achieve values for R2 of 0.98 or0.99 so that the unexplained variance is very smallin both cases. It seems very unlikely that the addi-tion of an interest rate variable to the equationsby using autonomous expenditures as the explana-tory variable, which addition would make theequations correspond to equation 1 above, wouldmake any substantial difference.

From this evidence it appears that ex postexplanations of the level of income are about asaccurate by using autonomous expenditures aloneas are those by using money stock alone. But giventhe inaccuracies in forecasting autonomous expen-ditures, it must be concluded that ex ante expla-nations by using themoney stock are substantiallymore accurate than those with forecasts of autono-mous expenditures. From this evidence, the totalrandom term in equation 4 appears to have asubstantially smaller variance than the total ran-dom term in equation 3.

For the reasons mentioned by the Friedman-Meiselman critics, evidence from single-equationstudies cannot be considered definitive. But nei-ther can the evidence be ignored, especially inlight of the difficulties encountered in the con-struction and the use of large econometric modelssuch as the FR-MIT model.

Evidence on Stability of Demand forMoney Function

One of the shortcomings of the single-equationstudies discussed above is that their authors paidtoo little attention to the stability of regressioncoefficients over time. Consider the followingstatement by Friedman and Meiselman:

The income velocity of circulation of moneyis consistently and decidedly stabler than theinvestment multiplier except only during theearly years of the Great Depression after 1929.There is throughout, including those years, aclose and consistent relation between the stockof money and consumption or income, andbetween year-to-year changes in the stock ofmoney and in consumption or income(Friedman and Meiselman, 1963, p. 186).

This conclusion is based on correlation coef-ficients betweenmoney and income (or consump-

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 459

9 For reasons that need not be explained here, most of this contro-versy was conducted in terms of equations with consumptionrather than GNP as the dependent variable. In the Friedman-Meiselman study, however, results are reported for equations withGNP (Friedman and Meiselman, 1963, p. 227). Such results arealso reported in Andersen and Jordan (1968, p. 17).

tion), but what is relevant for policy is theregression coefficient, which determines howmuch income will change for a given change inthe money stock. In the Friedman-Meiselmanstudy, a table (Friedman and Meiselman, 1963,p. 227) reports the regression coefficient forincome on money as being 1.469 for annual data1897-1958. However, the same table reports regres-sion coefficients for 12 subperiods, some of whichare overlapping, ranging from 1.092 to 2.399.

With a few exceptions, most economistsagree that velocity changes can be explained inpart by interest rate changes.10 Thus, variabilityin the regression coefficients when income isregressed on money is not evidence of the insta-bility of the demand for money function. To obtain

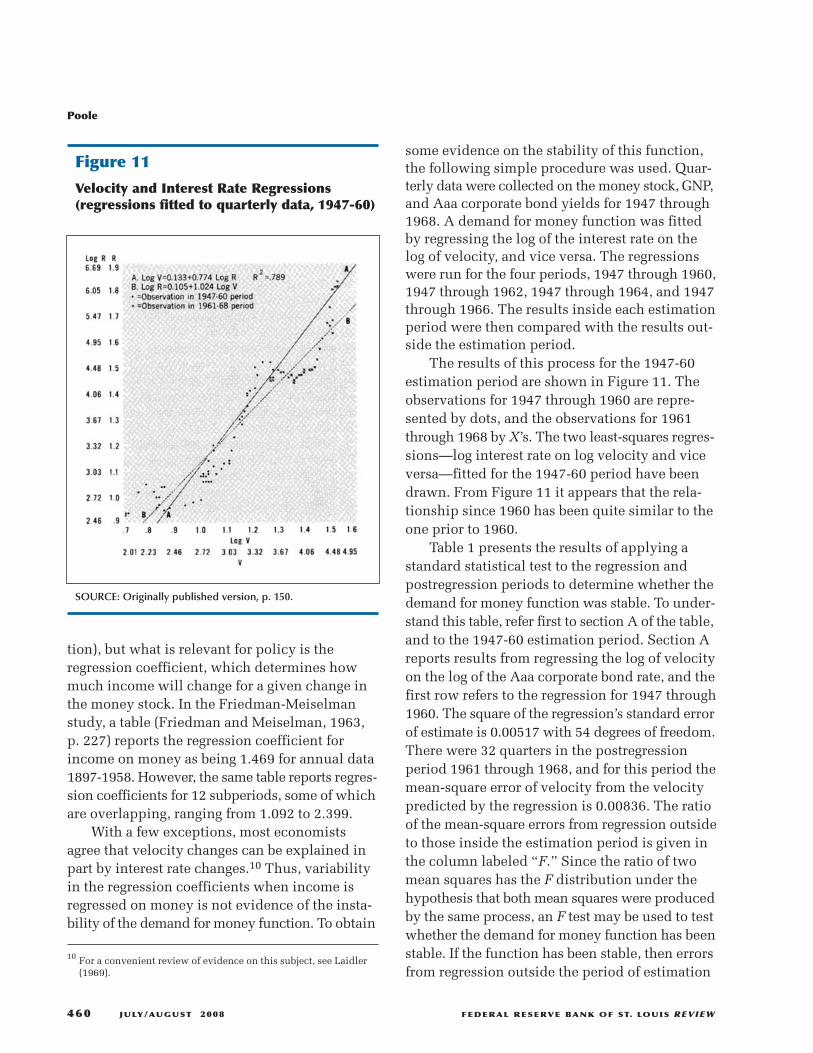

some evidence on the stability of this function,the following simple procedure was used. Quar-terly data were collected on themoney stock, GNP,and Aaa corporate bond yields for 1947 through1968. A demand for money function was fittedby regressing the log of the interest rate on thelog of velocity, and vice versa. The regressionswere run for the four periods, 1947 through 1960,1947 through 1962, 1947 through 1964, and 1947through 1966. The results inside each estimationperiod were then compared with the results out-side the estimation period.

The results of this process for the 1947-60estimation period are shown in Figure 11. Theobservations for 1947 through 1960 are repre-sented by dots, and the observations for 1961through 1968 by X’s. The two least-squares regres-sions—log interest rate on log velocity and viceversa—fitted for the 1947-60 period have beendrawn. From Figure 11 it appears that the rela-tionship since 1960 has been quite similar to theone prior to 1960.

Table 1 presents the results of applying astandard statistical test to the regression andpostregression periods to determine whether thedemand for money function was stable. To under-stand this table, refer first to section A of the table,and to the 1947-60 estimation period. Section Areports results from regressing the log of velocityon the log of the Aaa corporate bond rate, and thefirst row refers to the regression for 1947 through1960. The square of the regression’s standard errorof estimate is 0.00517 with 54 degrees of freedom.There were 32 quarters in the postregressionperiod 1961 through 1968, and for this period themean-square error of velocity from the velocitypredicted by the regression is 0.00836. The ratioof the mean-square errors from regression outsideto those inside the estimation period is given inthe column labeled “F.” Since the ratio of twomean squares has the F distribution under thehypothesis that both mean squares were producedby the same process, an F test may be used to testwhether the demand for money function has beenstable. If the function has been stable, then errorsfrom regression outside the period of estimation

10 For a convenient review of evidence on this subject, see Laidler(1969).

Poole

460 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

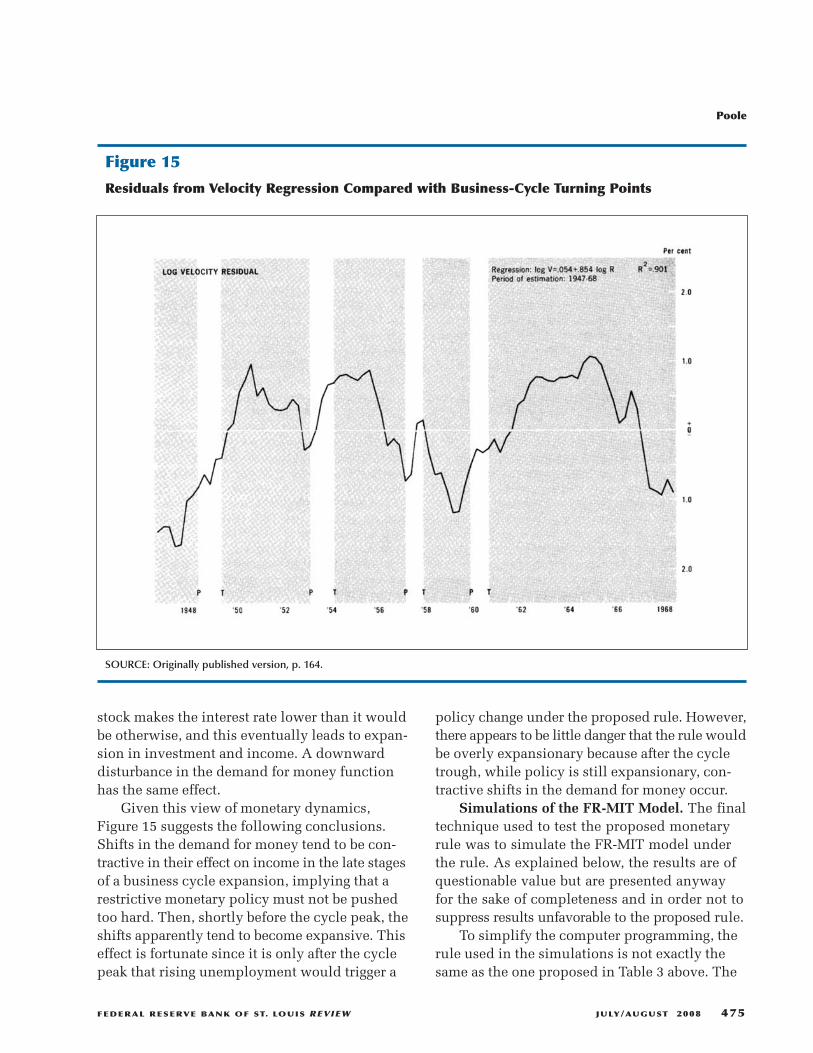

Figure 11

Velocity and Interest Rate Regressions(regressions fitted to quarterly data, 1947-60)

SOURCE: Originally published version, p. 150.

should be, on the average, the same size as theerrors inside the period of estimation. For the1947-60 regression being discussed, F = 1.62 andis significant at the 10 percent level but not atthe 5 percent level.

Looking at Table 1 as a whole it can be seenthat, for three of the regressions, the errors outsidethe period of estimation are not statistically sig-nificantly larger than those inside the period ofestimation. Indeed, for the bond rate regressionfor the 1947-60 period, the errors outside theperiod of estimation were actually smaller, onthe average, than those inside the period of esti-mation. Overall, however, these results taken atface value cast some doubt on the stability of thedemand for money function.

However, there is reason to believe that thereare problems in applying the F test in this situa-tion. The reason is that the residuals from regres-sion exhibit a very high positive serial correlationas indicated by Durbin-Watson test statistics ofaround 0.15 for all of the regressions. What thismeans is that the effective number of degrees offreedom is actually less than indicated in the table,and with fewer degrees of freedom the F ratioscomputed have less statistical significance than

the significance levels reported in the table. Theonly way around this problem is to run a morecomplex regression that removes the serial cor-relation of the residuals, but there is no generalagreement among economists as to exactly whatvariables belong in such a regression. The virtueof the simple regressions of velocity on an inter-est rate and vice versa is that this form has beenused successfully by many investigators startingin 1954 (Latané, 1954).

The appropriate conclusion to be drawn fromthis evidence would seem to be that the relation-ship between velocity and the Aaa corporate bondrate is too close and too stable to be ignored, butnot close enough and stable enough to eliminateall doubts. However, the question is not whetheran ironclad case for a money stock policy existsbut rather whether the evidence taken as a wholeargues for the adoption of such a policy. Whilethere is certainly room for differing interpreta-tions of Figure 11 and Table 1, and of the otherevidence examined above, on the whole all ofthese results seem to point in the same direction.It appears that the money stock rather than inter-est rates should be used as the monetary policycontrol variable.

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 461

Table 1Tests of the Stability of the Demand for Money Function by Using Quarterly Data

Regression Progression

Estimation period (SEE)2 d.f. MSE d.f. F Significance level

A. Log velocity regressed on log Aaa corporate bond yield

1947-60 .00517 54 .00836 32 1.62 .10

1947-62 .00484 62 .00746 24 1.54 .10

1947-64 .00509 70 .00587 16 1.15 >.25

1947-66 .00502 78 .00986 8 1.96 .10

B. Log Aaa corporate bond yield regressed on log velocity

1947-60 .00684 54 .00589 32 1.16* >.25

1947-62 .00614 62 .00723 24 1.18 >.25

1947-64 .00570 70 .01162 16 2.04 .025

1947-66 .00537 78 .02192 8 4.08 .005

NOTE: *MSE < (SEE)2.

III. A MONETARY RULE FORGUIDING POLICYRationale for a Rule-of-Thumb

The purpose of this section is to develop arule-of-thumb to guide policy. Such a rule—notmeant to be followed slavishly—would incorpo-rate advice in as systematic a way as possible. Therule proposed here is based upon the theory andevidence in Sections II and III and upon a closeexamination of post-accord experience.

Individual policymakers inevitably useinformal rules-of-thumb in making decisions.Like everyone else, policymakers develop cer-tain standard ways of reacting to standard situa-tions. These standard reactions are not, of course,unchanging over time, but are adjusted and devel-oped according to experience and new theoreti-cal ideas. If there were no standard reactions tostandard situations, behavior would have to beregarded as completely random and unpredict-able. The word “capricious” is often, and notunfairly, used to describe such unpredictablebehavior.

There are several difficulties with relying onunspecified rules-of-thumb. For one thing, therules may simply be wrong. But an even moreimportant factor, because formally specified rulesmay also be wrong, is that the use of unspecifiedrules allows little opportunity for cumulativeimprovements over time. A policymaker may havean extremely good operating rule in his head andexcellent intuition as to the application of therule but unless this rule can be written downthere is little chance that it can be passed on tosubsequent generations of policymakers.

An explicit operating rule provides a way ofincorporating the lessons of the past into currentpolicy. For example, it is generally felt that mone-tary policy was too expansive following the impo-sition of the tax surcharge in 1968. Unless thelesson of this experience is incorporated into anoperating rule, it may not be remembered in 1975or 1980. How many people now remember theoverly tight policy in late 1959 and early 1960that was a result of miscalculating the effects ofthe long steel strike in 1959? Since the FOMCmembership changes over time, many of the cur-

rent members will not have learned firsthand thelesson from a policy mistake or a policy success10 years ago. If the FOMCmember is not an econ-omist, he may not even be aware of the 10-year-old lesson.

It is for these reasons that an attempt is madein this section to develop a practical policy rulethat incorporates the lessons from past experience.The rule is not offered as one to be followed tothe last decimal place or as one that is good forall time. Rather, it is offered as a guide—or as abenchmark—against which current policy maybe judged.

A rule may take the form of a formal modelthat specifies what actions should be taken toachieve the goals decided upon by the policy-makers. Such a model would provide forecastsof goal variables, such as GNP, conditional onthe policy actions taken. The structure of themodel and the estimates of its parameters would,of course, be derived from past data and in thatsense the model would incorporate the lessonsof the past.

But in spite of advances in modelbuildingand forecasting, it is clear that forecasts are stillquite inaccurate on the average. In a study of theaccuracy of forecasts by several hundred fore-casters between 1953 and 1963, Zarnowitz con-cluded that the mean absolute forecast error wasabout 40 percent of the average year-to-yearchange in GNP (Zarnowitz, 1967, p. 4). He alsoreported, “there is no evidence that forecasters’performance improved steadily over the periodcovered by the data” (Zarnowitz, 1967, p. 5).

Not only are forecasts several quarters aheadinaccurate but also there is considerable uncer-tainty at, and after, the occurrence of business-cycle turning points as to whether a turning pointhas actually occurred. In a study of FOMC recog-nition of turning points for the period 1947-60,Hinshaw concluded that (Fels and Hinshaw, 1968,p. 122):

The beginning data of the Committee’s recog-nition pattern varied from one to nine monthsbefore the cyclical turn…On the other hand,the ending of the recognition pattern variedfrom one to seven months after the turn…With

Poole

462 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

the exception of the 1948 peak, the Committeewas certain of a turning point within sixmonths after the NBER date of the turn. At thedate of the turn, the estimated probability wasgenerally below 50; it reached the vicinity of50 about two months after the turn.

This recognition record, which is as good as thatin 10 widely circulated publications whoseforecasts were also studied in (Friedman andMeiselman, 1963) casts further doubt on the valueof placing great reliance on the forecasts.11

Given the accuracy of forecasts at the currentstate of knowledge,12 it seems likely that for sometime to come forecasts will be used primarily tosupplement a policy-decisionmaking process thatconsists largely of reactions to current develop-ments. Only gradually will policymakers placegreater reliance on formal forecasting models.13

While a considerable amount of work is beingdone on such models, essentially no attention isbeing paid to careful specification of how policyshould react to current developments. Whilesophisticated models will no doubt in time bedeveloped into highly useful policy tools, itappears that in the meantime relatively simpleapproaches may yield substantial improvementsin policy. Given that knowledge accumulatesrather slowly, it can be expected that carefullyspecified but simple methods will be successfulbefore large-scale models will lie. Careful speci-fication of policy responses to current develop-ments is but a small step beyond intuitive policyresponses to current developments. This stepsurely represents a logical evolution of the policy-formation process.

Post-Accord Monetary Policy

That an operating guideline is needed can beseen from the experience since the Treasury–Federal Reserve accord. In order that this experi-ence may be understood better, subperiods weredefined in terms of “stable,” “easing,” or “firming”policy as determined from the minutes of theFederal Open Market Committee. The minutesused are those published in the Annual Reportsof the Board of Governors of the Federal ReserveSystem for 1950 to 1968. The definitions of “sta-ble,” “easing,” and “firming” periods are neces-sarily subjective as are the determinations ofdates when policy changed.14 The dating of pol-icy changes was based primarily on the FOMCminutes, although the dates of changes in thediscount rate and in reserve requirements wereused to supplement the minutes. “Stable” periodsare those in which the policy directive wasunchanged except for relatively minor wordingchanges. In some cases the directive was essen-tially unchanged although the minutes reflectedthe belief that policy might have to be changed inthe near future. While the Manager of the SystemOpen Market Account might change policysomewhat as a result of such discussions, theunchanged directive was taken at face value indefining policy turning points.

More difficult problems of interpretationwere raised by such directives as “unchangedpolicy, but err on the side of ease,” or “resolvedoubts on the side of ease.” Such statements wereused to help in defining several periods duringwhich policy was progressively eased (or tight-ened). For example, in one meeting the directivemight call for easier policy, the next meetingmightcall for unchanged policy but with doubts to beresolved on the side of ease, and a third meetingmight call for further ease. These three meetingswould then be taken together as defining an

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 463

11 For further analysis of forecasting accuracy, see Mincer (1969).

12 The accuracy of forecasts may now be better than in the periodsexamined in the studies cited above. But without a number of yearsof data there would be no way of knowing whether forecasts haveimproved, and so forecasts must in any case be assumed to besubject to a wide margin of error at the present time.

13 It may be objected that great reliance is already placed on forecasts,at least on judgmental forecasts. However, these forecasts typicallyinvolve a large element of extrapolation of current developments.It seems fair to say that in most cases in which conditions forecasta number of quarters ahead differ markedly from current conditions,policy has followed the dictates of current conditions rather thanof the forecasts.

14 The author was greatly assisted in these judgments by Joan Waltonof the Special Studies Section of the Board’s Division of Researchand Statistics. MissWalton, who is not an economist, carefully readthe minutes of the entire period and in a large table recorded theprincipal items that seemed important at each FOMC meeting.Having a noneconomist read the minutes tempered the inevitabletendency for an economist to read either too much or too littleinto the minutes. However, the final interpretation of the minutesrested with the author.

“easing” period. However, unless accompaniedby other FOMC meetings clearly calling for apolicy change, statements such as those callingfor an “unchanged policy with doubts resolvedon the side of ease” were interpreted as not call-ing for a policy change.

Some important monthly economic timeseries for the post-accord period are plotted inFigure 12. The heavy vertical lines representperiods of “stable,” “easing,” and “firming” policyas indicated by “S,” “E,” and “F” at the bottomof the figure. Except for the unemployment rate,the average of each series for each policy periodhas been plotted as a horizontal line.

The two features of the post-accord experi-ence are especially noteworthy. First, decisionsto change policy have been taken about as closeto the time when, in retrospect, policy changeswere needed as could be expected in the light ofexisting knowledge.15 There have been mistakesin timing, but the overall record is impressive.The second major feature of this period is thatpolicy actions, as opposed to policy decisions,have been in the correct direction if policy actionsare defined by either free reserves or interest rates,but not if policy actions are defined in terms ofeither the money stock or bank credit.

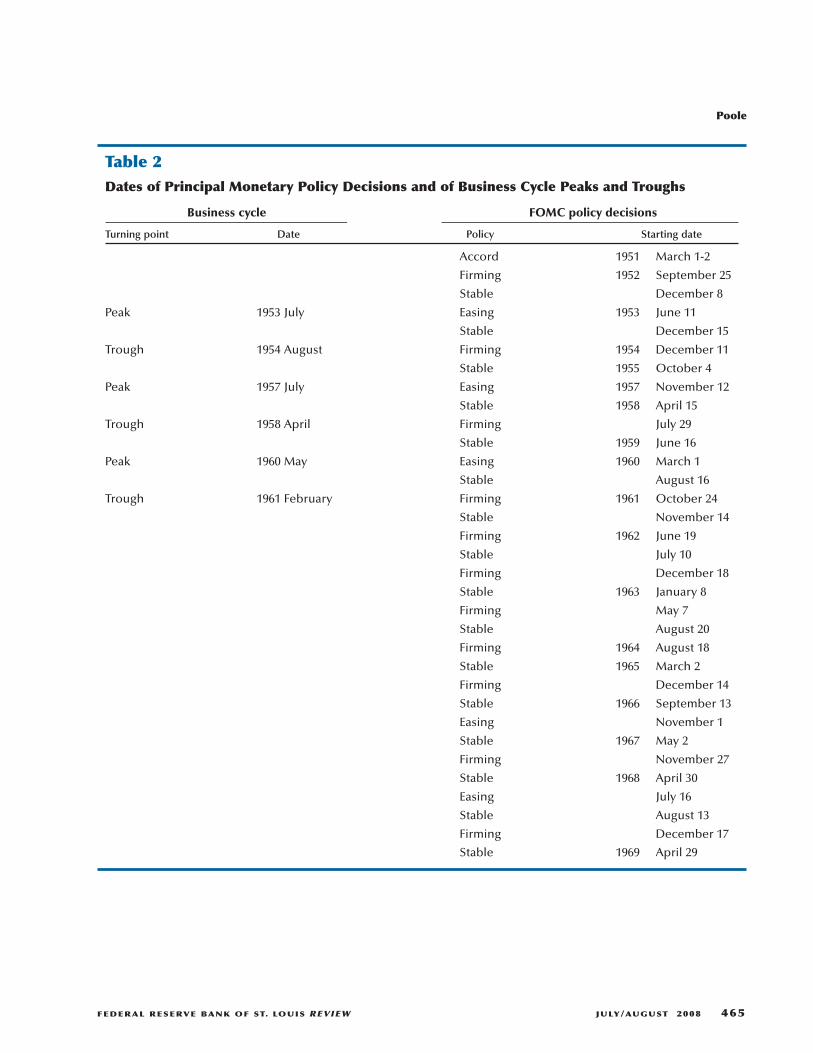

To examine the timing question in moredetail, a useful comparison is that between busi-ness cycle turning points (as defined by theNational Bureau of Economic Research) anddecisions to change policy. The post-accord periodbegins at a time when the U.S. economywas besetby inflation stemming from the war in Korea. thedates of the principal changes in policy and ofthe business cycle peaks and troughs are listedin Table 2. The policy dates are those that definethe beginning of the “stable,” “easing,” and “firm-ing” periods indicated in Figure 12.

The decision to ease policy was made priorto the business cycle peaks of July 1953 and May1960. The decision in 1957wasmade in the fourthmonth following the cycle peak in July, but as canbe seen from Figure 12, the unemployment ratehad not risen very much through October. Given

the amount of uncertainty always present in inter-preting business conditions, this lag must beconsidered to be well within the margin of errorto be expected for stabilization policy. However,the easing policy decision in 1968 was clearly amistake in retrospect but not in prospect giventhe expectations held by the majority of econo-mists that the tax increase would significantlytemper the economic boom.

Firming policy decisions were also generallywell timed. Following the 1953-54 recession,decisions to firm policy in small steps were takenfrom December 1954 to September 1955, as unem-ployment declined to about 4 percent of the laborforce. During the recovery period after the 1957-58recession, firming decisions were taken from July1958 to May 1959. There was also a series of firm-ing decisions taken from the end of 1961 to 1966.Especially noteworthy are those taken fromDecember 1965 to August 1966, in response tothe beginning of inflation associated with theescalation of military activity in Vietnam. Theeasing policy decisions taken in late 1966 andearly 1967 were fully appropriate in light of theeconomic slack that developed in 1967.

Even from the point of view of those whodoubt the importance of fiscal policy, this recordof the timing of policy decisions in the post-accordperiod is remarkably good. The timing recorddoes not suggest that much attention was paid toforecasts, but this lack of attention was perhapsnot unfortunate given the accuracy of forecastsduring the period. From this point of view, theonly real mistake was the easing decision takenin 1968. Of course, those who believe that a steadyrate of growth of the money stock is better thanany discretionary policy likely to be achieved inpractice may read this record as supporting theirthesis. But the post-accord record of the timingof policy decisions is certainly encouraging tothose who believe that the lags in the effects ofpolicy are short enough, and the effects predict-able enough, to make discretionary monetarypolicy a powerful stabilization tool if only deci-sions can be made promptly.

While the System’s performance in the timingof policy decisions has been commendable, thesame cannot be said for the actions taken in

15 For additional views on the timing of Federal Reserve decisions,see Brunner and Meltzer (1964) and Fels and Hinshaw (1968).

Poole

464 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 465

Table 2Dates of Principal Monetary Policy Decisions and of Business Cycle Peaks and Troughs

Business cycle FOMC policy decisions

Turning point Date Policy Starting date

Accord 1951 March 1-2

Firming 1952 September 25

Stable December 8

Peak 1953 July Easing 1953 June 11

Stable December 15

Trough 1954 August Firming 1954 December 11

Stable 1955 October 4

Peak 1957 July Easing 1957 November 12

Stable 1958 April 15

Trough 1958 April Firming July 29

Stable 1959 June 16

Peak 1960 May Easing 1960 March 1

Stable August 16

Trough 1961 February Firming 1961 October 24

Stable November 14

Firming 1962 June 19

Stable July 10

Firming December 18

Stable 1963 January 8

Firming May 7

Stable August 20

Firming 1964 August 18

Stable 1965 March 2

Firming December 14

Stable 1966 September 13

Easing November 1

Stable 1967 May 2

Firming November 27

Stable 1968 April 30

Easing July 16

Stable August 13

Firming December 17

Stable 1969 April 29

Poole

466 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

Figure 12

Post-Accord Monetary Policy

SOURCE: Originally published version, p. 154.

Poole

FEDERAL RESERVE BANK OF ST. LOUIS REVIEW JULY/AUGUST 2008 467

Figure 12, cont’d

Post-Accord Monetary Policy

SOURCE: Originally published version, p. 155.

response to the decisions. In the earlier discussionthe purposely vague terms “easing,” “firming,”and “stable” were used to describe policy deci-sions. These terms were meant to convey thenotions that policymakers wanted, respectively,to accelerate, decelerate, or maintain the pace ofeconomic advance. The question that must nowbe examined is whether policy actions did in facttend to accelerate, decelerate, or maintain thelevel of economic activity.

Policy actions were in accord with policydecisions if these actions are measured by eitherthe 3-month Treasury bill rate or free reserves. Thebill rate rose in “firming” periods, fell in “easing”periods, and tended to remain unchanged in“stable” periods. However, there was some ten-dency for the bill rate to rise in “stable” periodsfollowing “firming” periods, and to fall in “stable”periods following “easing” periods, a pattern notinconsistent with the interpretation of policybeing offered in this study. Similar commentsapply to free reserves.

But the picture is quite different if policyactions are measured by the rate of growth of themoney stock. Careful study of Figure 12 will makethis point clear. The growth rate declined inresponse to the “firming” policy decision in late1952, and again in the “stable” period in early1953. This behavior was, of course, consistentwith the “firming” decision. But the rate of growthdeclined further following the “easing” decisionin June 1953 and remained low until the middleof 1954. The unemployment rate rose rapidlyfrom its low of 2.6 percent at the cycle peak inJuly 1953 to 6.0 percent in August 1954, the cycletrough; the money stock was at the same level inApril 1954, 9 months following the cycle peakand 10 months following the decision to adoptan “easing” policy, as it had been at the peak.

The same pattern that had appeared duringthe 1953-54 recession appeared again at the timeof the 1957-58 recession. The rate of growth ofthe money stock declined in 1957 prior to thecycle peak. (The Treasury bill rate also rose sub-stantially.) But after the decision to adopt an“easing” policy in November 1957, the growthrate of the money stock declined further. FromOctober 1957 to January 1958, the money stock

fell at a 2.9 percent annual rate; from the cyclepeak in July to October it had fallen at a 1.5 per-cent annual rate.

The rate of growth of the money stockincreased substantially in February 1958, and itremained at the higher level during the “stable”policy period April to July. There followed aperiod of “firming” policy decisions from the endof July 1958 to May 1959; however, the averagegrowth rate of the money stock during this periodwas virtually identical to the average in the pre-ceding “stable” period. But in the “stable” periodfrom June 1959 to February 1960, the rate ofgrowth of money, at –2.2 percent, was much lowerthan in the preceding “firming” period. This rateof growth of money can hardly be consideredappropriate in the light of the fact that except forone month the unemployment rate was continu-ously above 5 percent. However, the picture wasconfused by a long steel strike.

The decision to ease policy was taken onMarch 1, 1960, but the rate of growth of themoneystock remained negative until July. The rate ofgrowth of money fell following the “firming”policy decisions of October 1961 and June 1962.In spite of another firming decision in December1962 the rate of growth then increased, and itcontinued to rise during the “firming” period in1963, maintaining the same rate in the following“stable” period. In August 1964, another “firming”decision was taken, and the growth rate trendeddown during the “firming” period from August1964 to February 1965.

During the “stable” period from March toNovember 1965, the Vietnam war heated up. Inthe second half of 1965 the growth rate of moneywas 6.1 percent compared with 3.0 percent duringthe first half. The “firming” policy decision camein December, but the rate of growth of moneyaveraged over 6 percent for the months Decemberthrough April 1966. At this point monetary growthceased. In January 1967 the money stock wasactually less than in May 1966—there havingbeen no increase in the growth rate in the monthsimmediately following the “easing” decision ofNovember 1, 1966.

The growth rate of money then acceleratedduring the “stable” period from May through

Poole

468 JULY/AUGUST 2008 FEDERAL RESERVE BANK OF ST. LOUIS REVIEW

October 1967; for the period as a whole growthaveraged 8.7 percent. In the following “firming”period November 1967 through April 1968, therate of growth of the money stock was lower but itwas still relatively high at 5.1 percent. The growthrate then rose to 9.6 percent in the “stable” periodMay through July 1968 and thereafter fell to a littleless than 6 percent in the July-November 1968period following the “easing” decision of July 16,1968.

There ensued a “firming” period fromDecember 1968 through April 1969. Althoughoriginal figures indicated that monetary growthwas relatively little during this period, a revisionin the money stock series showed that the rateaveraged 5.5 percent for the period as a whole.The rate following April was lower, especially inthe June-December 1969 period, which saw nonet growth in the money stock.

A broadly similar view of the timing of policyactions is obtained from a careful examination ofthe rate of growth of total bank credit. However,as shown in Figure 12, this series is quite erraticand much more difficult to interpret than theseries on the rate of growth of the money stock.

The proper way to interpret these resultswould seem to be as follows. When interest ratesfell in a recession, policy was easier than it wouldhave been if interest rates had not been permittedto fall. But if the money stock was also falling, orgrowing at a below-average rate, policy wastighter than it would have been had money beengrowing at its long-run average rate. Similar state-ments apply to rising interest rates and above-average monetary growth in a boom.

A Monetary Rule

Given the arguments of Sections I and II onthe advantages of controlling the money stock asopposed to interest rates, a logical first step indeveloping a policy guideline is to examine casesclearly calling for ease or restraint. Consider firsta recession. To insure that monetary policy isexpansionary, the rule might be that interest ratesshould fall and the money stock should rise atan above-average rate. This policy avoids twopossible errors.

The first is illustrated in Figure 13. If the ISfunction shifts down from IS1 to IS2 while the LMfunction shifts from LM1 to LM2, the interest ratewill fall from r1 to r2. The shift from LM1 to LM2