NEW ISSUE—BOOK-ENTRY ONLY RATINGS: S&P: "AA+" Moody's: "Aa2" Fitch: "AA" See "RATINGS" In the opinion of Sherman & Howard L.L.C., Bond Counsel, dated as of the date of delivery of the Bonds, assuming continuous compliance with certain covenants described herein, interest on the Bonds is excluded from gross income under federal income tax laws pursuant to Section 103 of the Internal Revenue Code of 1986, as amended to the date of delivery of the Bonds (the "Tax Code"), interest on the Bonds is excluded from alternative minimum taxable income as defined in Section 55(b)(2) of the Tax Code, except that such interest is required to be included in calculating the "adjusted current earnings" adjustment applicable to corporations for purposes of computing the alternative minimum taxable income of corporations, and interest on the Bonds is excluded from Colorado taxable income and Colorado alternative minimum taxable income under Colorado income tax laws in effect on the date of delivery of the Bonds as described herein. See "TAX MATTERS." $204,820,000 REGIONAL TRANSPORTATION DISTRICT (Colorado) Sales Tax Revenue Refunding Bonds (FasTracks Project) Series 2013A Dated: Date of Delivery Due: November 1, as shown below The Bonds are issued and secured pursuant to an Indenture of Trust dated May 16, 2013 (the "Indenture") between the Regional Transportation District (the "District" or "RTD") and The Bank of New York Mellon Trust Company, N.A., as trustee (the "Trustee"). Interest on the Bonds is payable on November 1, 2013 and each May 1 and November 1 thereafter. The Bonds are issuable in registered form and are initially to be registered in the name of Cede & Co., as nominee for The Depository Trust Company, New York, New York ("DTC"), as securities depository for the Bonds. Purchases by beneficial owners of the Bonds are to be made in book-entry form in the principal amount of $5,000 or any integral multiple thereof. Beneficial owners are not to receive certificates evidencing their interests in the Bonds. See "THE BONDS – Book-Entry Form." The Bonds mature, bear interest and are priced to yield as follows: MATURITY SCHEDULE (CUSIP© 6-digit issue number: 759136 (2) ) Maturity (November 1) Principal Amount Interest Rate Yield (1) CUSIP ©(2) 2027 $43,205,000 5.00% 2.92% RW6 2028 45,365,000 5.00 3.03 RX4 2029 47,630,000 5.00 3.13 RY2 2031 19,665,000 5.00 3.25 RZ9 2032 19,550,000 5.00 3.30 SB1 2036 29,405,000 4.25 3.50 SA3 _____________________ (1) This information is provided by the Underwriters. (2) Neither RTD nor the Underwriters take any responsibility for the accuracy of CUSIP numbers, which are included solely for the convenience of the owners of the Bonds. The Bonds are subject to redemption prior to their respective maturity dates as more fully described in "THE BONDS – Prior Redemption." The Bonds are issued for the purpose of refunding, paying and discharging certain of the District's outstanding sales tax revenue bonds as described herein and funding costs of issuance of the Bonds. See "PLAN OF FINANCE." The Bonds are special and limited obligations of the District payable solely from and secured by (a) a non-exclusive first lien upon the revenues received by the District from its 0.4% sales tax, (b) a non-exclusive subordinate lien upon the revenues received by the District from an additional 0.6% sales tax and (c) proceeds of the Bonds and other legally available moneys and investments held in certain funds created under the Indenture. The Bonds do not constitute a general obligation of the District within the meaning of any constitutional or statutory debt limitation or provision and are not payable in whole or in part from the proceeds of ad valorem property taxes. See "SECURITY FOR THE BONDS." The purchase and ownership of the Bonds involve investment risk. Prospective purchasers should give particular attention to the matters discussed under "RISK FACTORS." This cover page contains certain information for quick reference only. It is not a summary of this issue. Investors should read this entire Official Statement to obtain information essential to making an informed investment decision. The Bonds are offered when, as and if executed and delivered and accepted by the Underwriters and subject to the approving legal opinion of Sherman & Howard L.L.C., Denver, Colorado, as Bond Counsel, and to certain other conditions. Hogan Lovells US LLP, Denver, Colorado, and Bookhardt & O'Toole, Denver, Colorado, have acted as Co-Disclosure Counsel to the District in connection with the Official Statement. Certain legal matters will be passed upon for the District by its General Counsel, Marla Lien, Esq., and for the Underwriters by Kutak Rock LLP, Denver, Colorado. First Southwest Company is serving as Financial Advisor to the District in connection with the issuance of the Bonds. It is expected that the Bonds in book-entry form will be available for deposit with delivery to DTC on or about May 16, 2013. MORGAN STANLEY BofA MERRILL LYNCH GEORGE K. BAUM & COMPANY LOOP CAPITAL MARKETS The date of this Official Statement is May 8, 2013. © Copyright 2013, American Bankers Association. CUSIP data herein is provided by Standard & Poor's, CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NEW ISSUE—BOOK-ENTRY ONLY RATINGS: S&P: "AA+" Moody's: "Aa2"

Fitch: "AA" See "RATINGS"

In the opinion of Sherman & Howard L.L.C., Bond Counsel, dated as of the date of delivery of the Bonds, assuming continuous compliance with certain covenants described herein, interest on the Bonds is excluded from gross income under federal income tax laws pursuant to Section 103 of the Internal Revenue Code of 1986, as amended to the date of delivery of the Bonds (the "Tax Code"), interest on the Bonds is excluded from alternative minimum taxable income as defined in Section 55(b)(2) of the Tax Code, except that such interest is required to be included in calculating the "adjusted current earnings" adjustment applicable to corporations for purposes of computing the alternative minimum taxable income of corporations, and interest on the Bonds is excluded from Colorado taxable income and Colorado alternative minimum taxable income under Colorado income tax laws in effect on the date of delivery of the Bonds as described herein. See "TAX MATTERS."

$204,820,000 REGIONAL TRANSPORTATION DISTRICT

(Colorado) Sales Tax Revenue Refunding Bonds

(FasTracks Project) Series 2013A

Dated: Date of Delivery Due: November 1, as shown below

The Bonds are issued and secured pursuant to an Indenture of Trust dated May 16, 2013 (the "Indenture") between the Regional Transportation District (the "District" or "RTD") and The Bank of New York Mellon Trust Company, N.A., as trustee (the "Trustee"). Interest on the Bonds is payable on November 1, 2013 and each May 1 and November 1 thereafter.

The Bonds are issuable in registered form and are initially to be registered in the name of Cede & Co., as nominee for The Depository Trust Company, New York, New York ("DTC"), as securities depository for the Bonds. Purchases by beneficial owners of the Bonds are to be made in book-entry form in the principal amount of $5,000 or any integral multiple thereof. Beneficial owners are not to receive certificates evidencing their interests in the Bonds. See "THE BONDS – Book-Entry Form."

The Bonds mature, bear interest and are priced to yield as follows:

MATURITY SCHEDULE (CUSIP© 6-digit issue number: 759136(2))

Maturity (November 1)

Principal Amount

Interest Rate

Yield (1)

CUSIP©(2)

2027 $43,205,000 5.00% 2.92% RW6 2028 45,365,000 5.00 3.03 RX4 2029 47,630,000 5.00 3.13 RY2 2031 19,665,000 5.00 3.25 RZ9 2032 19,550,000 5.00 3.30 SB1 2036 29,405,000 4.25 3.50 SA3

_____________________ (1) This information is provided by the Underwriters. (2) Neither RTD nor the Underwriters take any responsibility for the accuracy of CUSIP numbers, which are included solely for the convenience of the owners of the Bonds.

The Bonds are subject to redemption prior to their respective maturity dates as more fully described in "THE BONDS – Prior Redemption."

The Bonds are issued for the purpose of refunding, paying and discharging certain of the District's outstanding sales tax revenue bonds as described herein and funding costs of issuance of the Bonds. See "PLAN OF FINANCE."

The Bonds are special and limited obligations of the District payable solely from and secured by (a) a non-exclusive first lien upon the revenues received by the District from its 0.4% sales tax, (b) a non-exclusive subordinate lien upon the revenues received by the District from an additional 0.6% sales tax and (c) proceeds of the Bonds and other legally available moneys and investments held in certain funds created under the Indenture. The Bonds do not constitute a general obligation of the District within the meaning of any constitutional or statutory debt limitation or provision and are not payable in whole or in part from the proceeds of ad valorem property taxes. See "SECURITY FOR THE BONDS."

The purchase and ownership of the Bonds involve investment risk. Prospective purchasers should give particular attention to the matters discussed under "RISK FACTORS."

This cover page contains certain information for quick reference only. It is not a summary of this issue. Investors should read this entire Official Statement to obtain information essential to making an informed investment decision.

The Bonds are offered when, as and if executed and delivered and accepted by the Underwriters and subject to the approving legal opinion of Sherman & Howard L.L.C., Denver, Colorado, as Bond Counsel, and to certain other conditions. Hogan Lovells US LLP, Denver, Colorado, and Bookhardt & O'Toole, Denver, Colorado, have acted as Co-Disclosure Counsel to the District in connection with the Official Statement. Certain legal matters will be passed upon for the District by its General Counsel, Marla Lien, Esq., and for the Underwriters by Kutak Rock LLP, Denver, Colorado. First Southwest Company is serving as Financial Advisor to the District in connection with the issuance of the Bonds. It is expected that the Bonds in book-entry form will be available for deposit with delivery to DTC on or about May 16, 2013.

MORGAN STANLEY BofA MERRILL LYNCH

GEORGE K. BAUM & COMPANY LOOP CAPITAL MARKETS

The date of this Official Statement is May 8, 2013.

© Copyright 2013, American Bankers Association. CUSIP data herein is provided by Standard & Poor's, CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc.

No dealer, salesman or other person has been authorized to give any information or to make anyrepresentation with respect to the Bonds that is not contained in this Official Statement and, if given ormade, such other information or representation must not be relied upon as having been authorized by theDistrict, First Southwest Company (the "Financial Advisor") or the underwriters listed on the coverhereof (collectively, the "Underwriters"). The information contained in this Official Statement is subjectto change, and neither the delivery of this Official Statement nor any sale made after any such deliverycreates any implication that there has been no change since the date of this Official Statement. ThisOfficial Statement does not constitute an offer to sell or the solicitation of any offer to buy, and there is tobe no sale of any of, the Bonds by any person in any jurisdiction in which it is unlawful for such person tomake such offer, solicitation, or sale.

The information set forth herein has been furnished by the District and includes informationobtained from other sources, all of which are believed to be reliable. The information and expressions ofopinion herein are subject to change without notice and neither the delivery of this Official Statement norany sale made hereunder shall, under any circumstances, create any implication that there has been nochange in the affairs of the District since the date hereof. Such information and expressions of opinionare made for the purpose of providing information to prospective investors and are not to be used for anyother purpose or relied on by any other party.

The order and placement of materials in this Official Statement, including the appendices, are notto be deemed a determination of relevance, materiality or importance, and this Official Statementincluding the appendices, must be considered in its entirety. The captions and headings in this OfficialStatement are for convenience only and in no way define, limit or describe the scope or intent, or affectthe meaning or construction, of any provisions or sections of this Official Statement. The offering of theBonds is made only by means of this entire Official Statement.

The Underwriters have provided the following sentence for inclusion in this Official Statement.The Underwriters have reviewed the information in this Official Statement in accordance with, and as partof, their responsibilities to investors under the federal securities laws as applied to the facts andcircumstances of this transaction, but the Underwriters do not guarantee the accuracy or completeness ofsuch information.

In connection with the offering of the Bonds, the Underwriters may overallot or effecttransactions which stabilize or maintain the market price of such Bonds at levels above those which mightotherwise prevail in the open market. Such stabilization, if commenced, may be discontinued at any time.

THESE SECURITIES HAVE NOT BEEN RECOMMENDED BY ANY FEDERAL OR STATESECURITIES COMMISSION OR REGULATORY AUTHORITY. FURTHERMORE, THEFOREGOING AUTHORITIES HAVE NOT CONFIRMED THE ACCURACY OR DETERMINEDTHE ADEQUACY OF THIS DOCUMENT. ANY REPRESENTATION TO THE CONTRARY IS ACRIMINAL OFFENSE.

THIS OFFICIAL STATEMENT IS BEING PROVIDED TO PROSPECTIVE PURCHASERSEITHER IN BOUND PRINTED FORM ("ORIGINAL BOUND FORMAT") OR IN ELECTRONICFORMAT ON THE FOLLOWING WEBSITE: HTTP://WWW.MERITOS.COM. THIS OFFICIALSTATEMENT MAY BE RELIED UPON ONLY IF IT IS IN ITS ORIGINAL BOUND FORMAT OR IFIT IS PRINTED IN FULL DIRECTLY FROM SUCH WEBSITE.

-i-

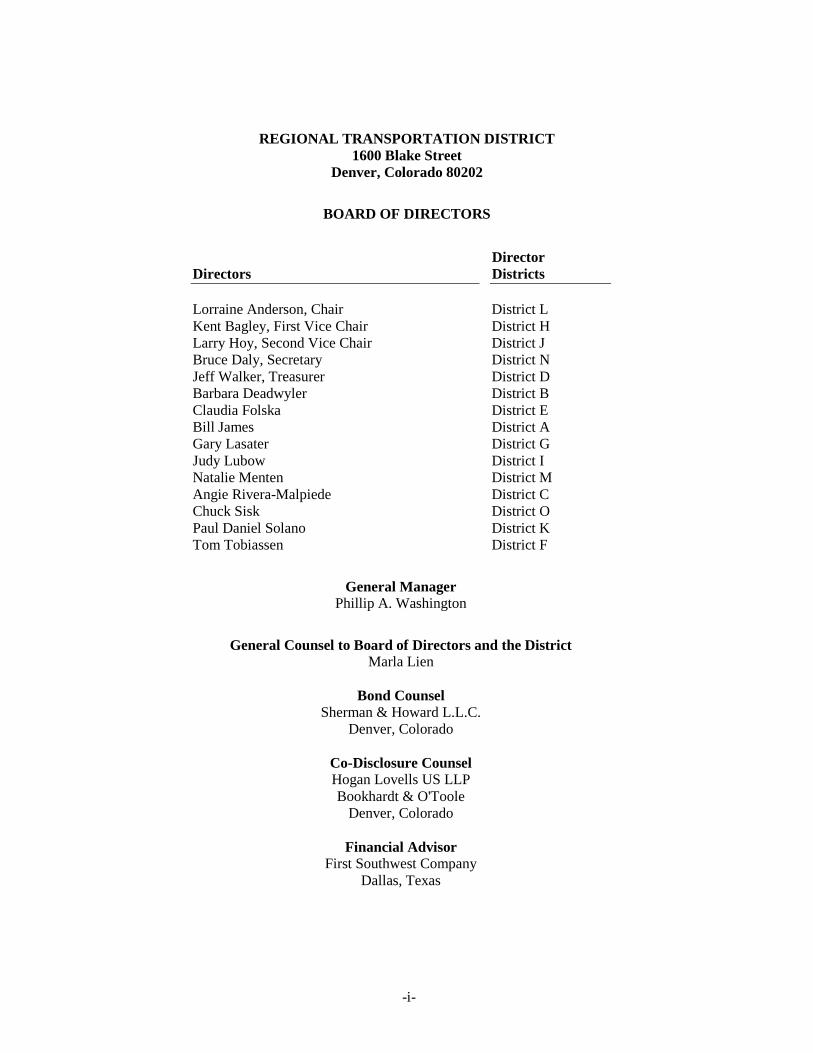

REGIONAL TRANSPORTATION DISTRICT1600 Blake Street

Denver, Colorado 80202

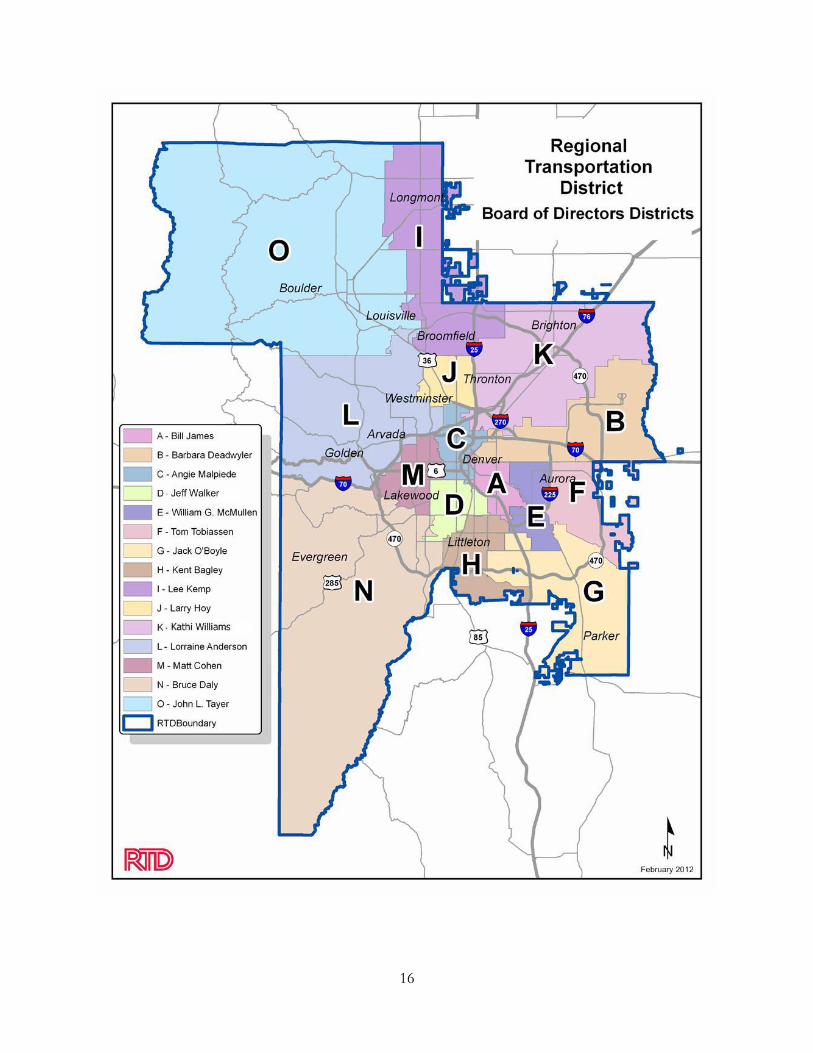

BOARD OF DIRECTORS

DirectorsDirectorDistricts

Lorraine Anderson, Chair District LKent Bagley, First Vice Chair District HLarry Hoy, Second Vice Chair District JBruce Daly, Secretary District NJeff Walker, Treasurer District DBarbara Deadwyler District BClaudia Folska District EBill James District AGary Lasater District GJudy Lubow District INatalie Menten District MAngie Rivera-Malpiede District CChuck Sisk District OPaul Daniel Solano District KTom Tobiassen District F

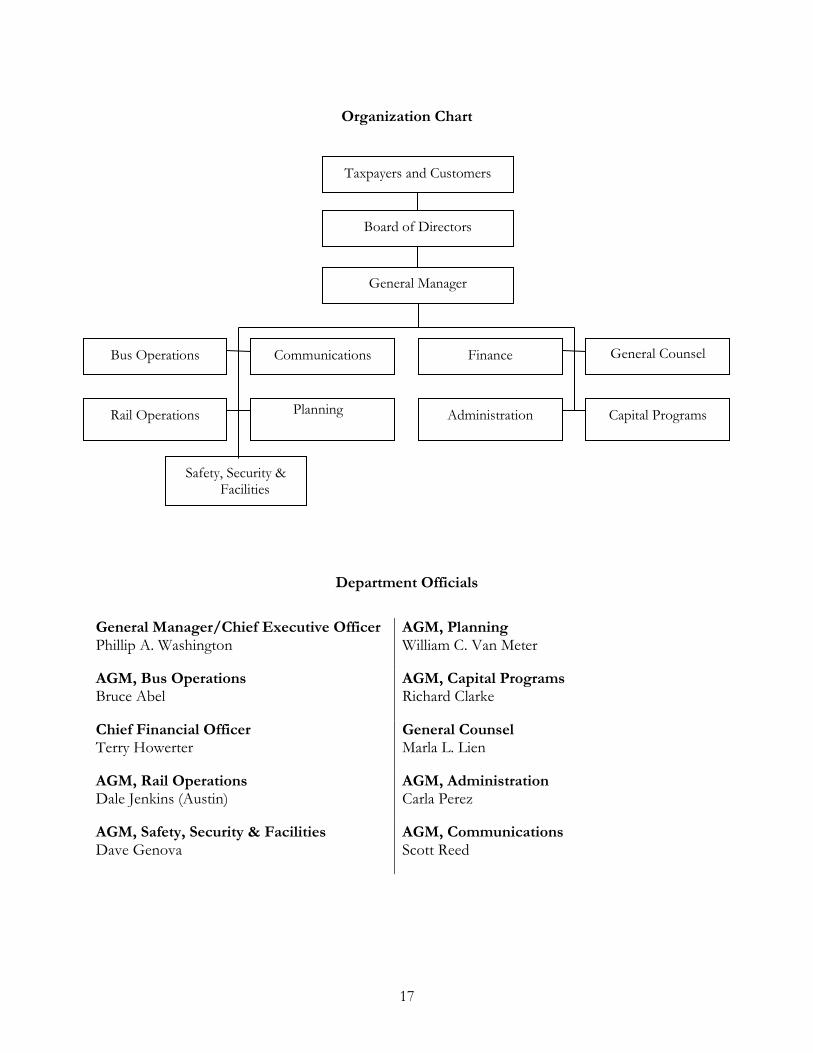

General ManagerPhillip A. Washington

General Counsel to Board of Directors and the DistrictMarla Lien

Bond CounselSherman & Howard L.L.C.

Denver, Colorado

Co-Disclosure CounselHogan Lovells US LLPBookhardt & O'Toole

Denver, Colorado

Financial AdvisorFirst Southwest Company

Dallas, Texas

-ii-

_________________________

TABLE OF CONTENTS_________________________

PageINTRODUCTION ................................................ 1THE BONDS ........................................................ 4

Authority ............................................................ 4Description ......................................................... 4Prior Redemption ............................................... 4Debt Service Requirements................................ 5Payment and Registration .................................. 7Transfer and Exchange....................................... 7Defeasance and Discharge ................................. 7Book-Entry Form ............................................... 8

SECURITY FOR THE BONDS......................... 10Flow of Funds .................................................. 10Debt Service Coverage..................................... 13Additional Securities........................................ 14Events of Default ............................................. 15Bondholders' Remedies.................................... 16

RISK FACTORS ................................................ 16Special and Limited Obligations...................... 17Economic Conditions....................................... 17Effect of Internet Sales..................................... 17Powers Subject to Change by Legislature or

by Initiative................................................... 17No Secondary Market ...................................... 17

PLAN OF FINANCE.......................................... 18General ............................................................. 18Sources and Uses of Funds .............................. 18The Refunding Escrow..................................... 18

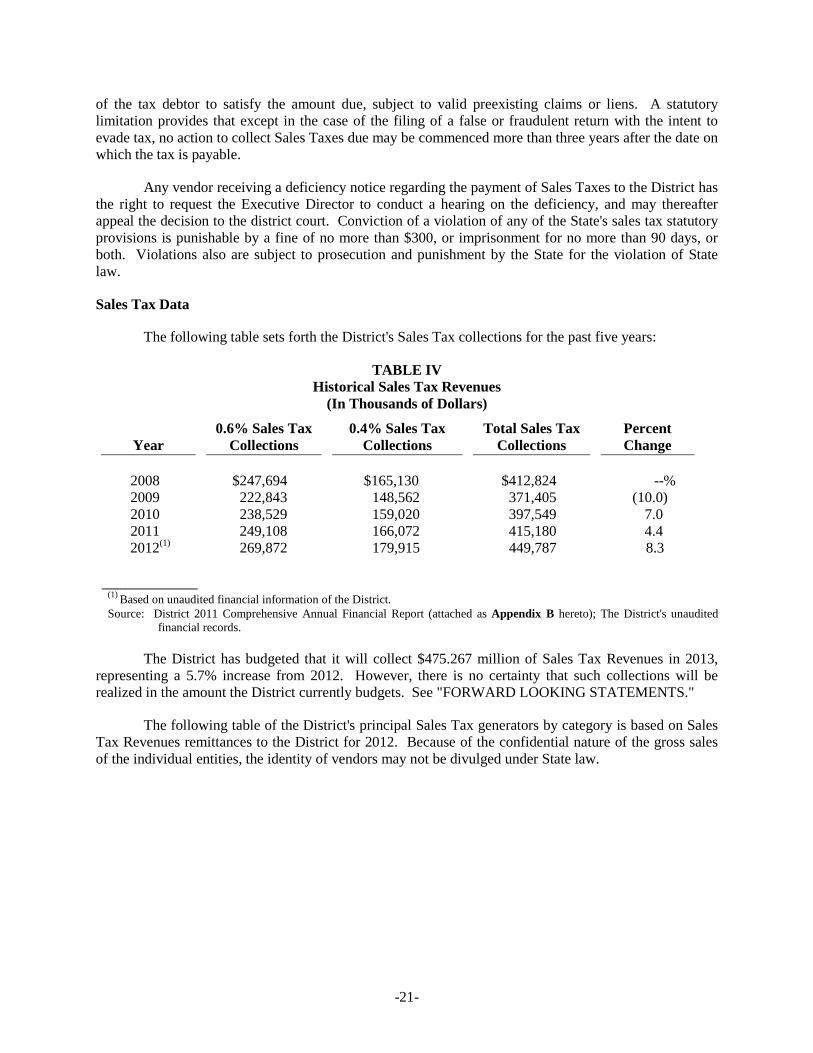

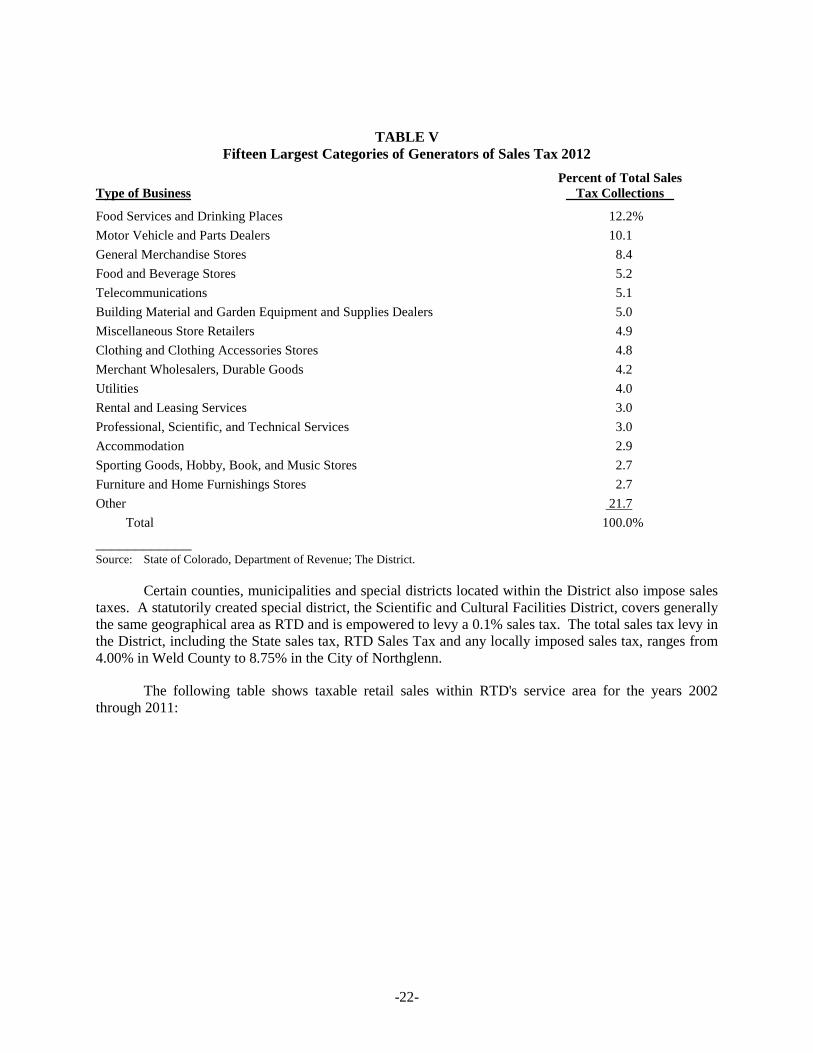

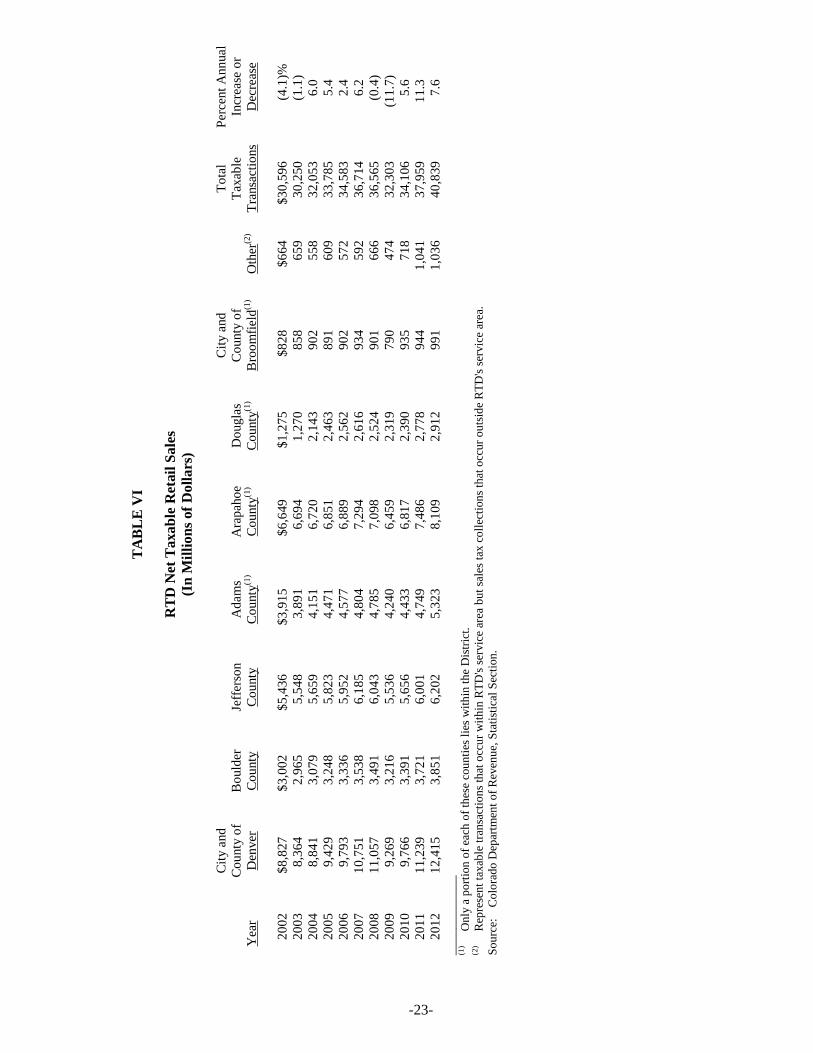

THE SALES TAX .............................................. 19Manner of Collection of the Sales Tax............. 19Remedies for Delinquent Taxes ....................... 20Sales Tax Data ................................................. 21

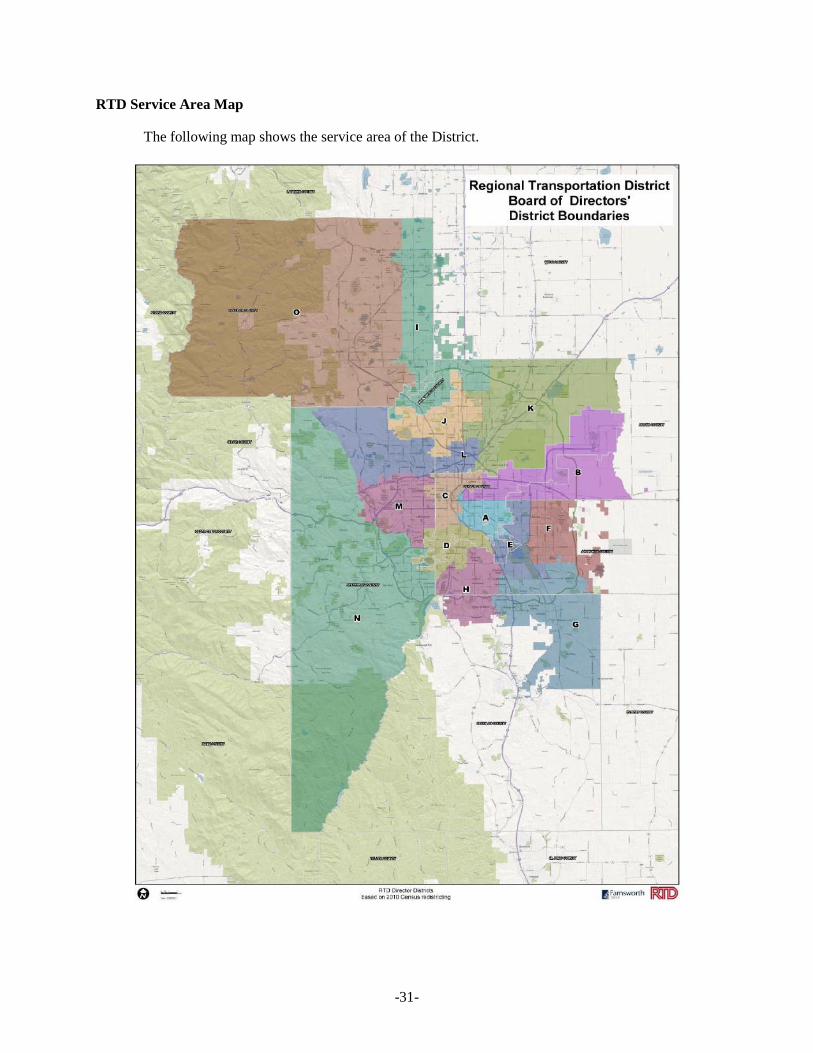

RTD .................................................................... 24General Information......................................... 24Organization..................................................... 24Powers.............................................................. 24Board of Directors............................................ 25Principal Officials ............................................ 26Employee and Labor Relations ........................ 28Retirement Plans .............................................. 28Other Postemployment Benefits ...................... 29Insurance .......................................................... 30Intergovernmental Agreements........................ 30RTD Service Area Map.................................... 31

THE SYSTEM.................................................... 32Fleet Composition ............................................ 32Transit Services................................................ 32Passenger, Maintenance and Administrative

Facilities ....................................................... 34Long-Term Financial Planning ........................ 35

PageFasTracks......................................................... 36

DEBT STRUCTURE OF RTD .......................... 41FINANCIAL INFORMATION

CONCERNING RTD...................................... 44Budget Policy................................................... 44Major Revenue Sources ................................... 45Sales Tax.......................................................... 46Fare Structure................................................... 46Advertising and Ancillary Revenues ............... 48Federal Funding ............................................... 49Investment Income........................................... 50Financial Summary .......................................... 50Management's Discussion and Analysis of

Financial Trends........................................... 53ECONOMIC AND DEMOGRAPHIC

OVERVIEW.................................................... 53FORWARD LOOKING STATEMENTS .......... 53CONSTITUTIONAL REVENUE, SPENDING

AND DEBT LIMITATIONS .......................... 53LITIGATION ..................................................... 54GOVERNMENTAL IMMUNITY ..................... 54CONTINUING DISCLOSURE AGREEMENT 55LEGAL MATTERS ........................................... 56TAX MATTERS ................................................ 56RATINGS........................................................... 58VERIFICATION OF CERTAIN

CALCULATIONS .......................................... 58UNDERWRITING ............................................. 58FINANCIAL ADVISOR.................................... 59FINANCIAL STATEMENTS............................ 59MISCELLANEOUS........................................... 61

APPENDICES:

Appendix A – Form of Continuing DisclosureAgreement .................................... A-1

Appendix B – Regional TransportationDistrict Denver, ColoradoComprehensive AnnualFinancial Report for the FiscalYear ended December 31, 2011and 2010 ........................................B-1

Appendix C – An Economic andDemographic Overview of theDenver Metropolitan Area.............C-1

Appendix D – Form of Bond Counsel Opinion ... D-1Appendix E – Summary of Certain Provisions

of the Indenture..............................E-1

-1-

OFFICIAL STATEMENT

$204,820,000REGIONAL TRANSPORTATION DISTRICT

(Colorado)Sales Tax Revenue Refunding Bonds

(FasTracks Project)Series 2013A

INTRODUCTION

This Official Statement, which includes the cover page and the appendices, provides certaininformation in connection with the offering of $204,820,000 aggregate principal amount of Sales TaxRevenue Refunding Bonds (FasTracks Project), Series 2013A (the "Bonds") of the RegionalTransportation District ("RTD" or the "District"), a public body politic and corporate and politicalsubdivision of the State of Colorado (the "State"), organized and existing under the terms of the RegionalTransportation District Act, Section 32-9-101 et seq., Colorado Revised Statutes, as amended (the "Act").The Bonds are being issued by the District pursuant to an Indenture of Trust, dated May 16, 2013 (the"Indenture") between the District and The Bank of New York Mellon Trust Company, N.A., as trustee(the "Trustee"). Capitalized terms used herein and not otherwise defined shall have the meanings setforth in Appendix E – "SUMMARY OF CERTAIN PROVISIONS OF THE INDENTURE."

At an election held within the District on November 2, 2004 (the "2004 Election"), voters in theDistrict approved a ballot referendum allowing for an increase in the RTD sales tax rate from 0.6% (the"0.6% Sales Tax") to 1.0% effective January 1, 2005. The additional four-tenths of one percent sales taxrate increase approved at the 2004 Election is referred to herein as the "0.4% Sales Tax Increase." Atthe 2004 Election, the District was also authorized to issue debt in the amount of $3.477 billion, with amaximum total repayment cost of $7.129 billion, and a maximum annual repayment cost of $309.738million, with the proceeds of such debt and increased taxes to be spent on the construction and operationof a transit expansion plan known as "FasTracks." The District has issued obligations in the aggregateprincipal amount of approximately $2.492 billion pursuant to the authorization of the 2004 Election.Since the Bonds are being issued to refund the Refunded Bonds (hereinafter defined) at a lower interestrate, the District will not utilize any remaining electoral authorization in connection with the issuance ofthe Bonds. The District has also committed under outstanding agreements to reserve certain amounts ofits electoral authority.

The Bonds are being issued for the purpose of refunding, paying and discharging certain of theDistrict's outstanding sales tax revenue bonds (as further described herein, the "Refunded Bonds") andfunding costs of issuance of the Bonds. See "PLAN OF FINANCE – The Refunding Escrow."

The Bonds are special and limited obligations of the District payable solely from and secured by(a) a non-exclusive first lien upon the revenues generated by the 0.4% Sales Tax Increase (the "0.4%Sales Tax Revenues"), (b) a non-exclusive subordinate lien upon the revenues received by the Districtfrom the 0.6% Sales Tax (the "0.6% Sales Tax Revenues") and (c) proceeds of the Bonds and otherlegally available moneys and investments held in certain funds created under the Indenture, and subjectonly to the provisions of the Indenture permitting application of such amounts for the purposes describedin the Indenture (collectively, the "Pledged Revenues"). The 0.4% Sales Tax Revenues and 0.6% SalesTax Revenues are collectively referred to herein as the "Sales Tax Revenues." The Bonds do not

-2-

constitute a general obligation of the District within the meaning of any constitutional or statutory debtlimitation or provision, and are not payable in whole or in part from the proceeds of ad valorem propertytaxes. See "SECURITY FOR THE BONDS."

The District has previously pledged all of the proceeds from the imposition of the 0.6% Sales Taxto the payment of the following obligations of the District that have a lien on the 0.6% Sales TaxRevenues superior or senior to the lien thereon of the Bonds outstanding as of April 1, 2013 in theaggregate principal amount of $207,355,000: (a) the Sales Tax Revenue Refunding Bonds, Series 2007A;(b) the Sales Tax Revenue Refunding Bonds, Series 2010A; and (c) the Sales Tax Revenue RefundingBonds, Series 2013A (collectively, the "Senior Bonds"). The Senior Bonds were issued pursuant to aSales Tax Revenue Bond Resolution, adopted October 27, 1977, as amended and supplemented (the"Senior Bond Resolution"). See "DEBT STRUCTURE OF RTD" for additional information relating tothe Senior Bonds. The Board has covenanted in the Indenture that no additional securities are to beissued by the District with a pledge of and lien on the 0.6% Sales Tax Revenues that is senior to the lienthereon of the Bonds except for obligations issued by the District to refund Senior Bonds for interestexpense savings as more fully described herein. See "SECURITY FOR THE BONDS – AdditionalSecurities." The Senior Bonds and any such securities issued in the future secured by a lien on the 0.6%Sales Tax Revenues that are senior to the lien thereon of the Bonds are described herein as "Senior Debt"(and more specifically defined in Appendix E herein).

The Bonds are to be secured with a pledge of and lien on the Sales Tax Revenues on a parity withthe following obligations issued and outstanding as of April 1, 2013 in the aggregate principal amount of$1,731,130,000

1(collectively, the "Parity Bonds"): (a) Sales Tax Revenue Bonds (FasTracks Project),

Series 2006A which are the Refunded Bonds; (b) Sales Tax Revenue Refunding Bonds (FasTracksProject), Series 2007A (the "Series 2007A Bonds"); (c) Tax-Exempt Sales Tax Revenue Bonds(FasTracks Project), Series 2010A (the "Series 2010A Bonds"); (d) Taxable Sales Tax Revenue Bonds(FasTracks Project) (Direct Pay Build America Bonds), Series 2010B (the "Series 2010B Bonds");(e) Sales Tax Revenue Bond, Series 2011 (the "RTD TIFIA Bond")1; and (f) Sales Tax Revenue Bonds(FasTracks Project), Series 2012A (the "Series 2012A Bonds"). See "PLAN OF FINANCE – TheRefunding Escrow." The Series 2007A Bonds were issued pursuant to an Indenture of Trust, dated as ofMay 1, 2007, as amended, between the District and The Bank of New York Trust Company, N.A. (nowknown as The Bank of New York Mellon Trust Company, N.A.), as trustee (the "2007 Indenture"). TheSeries 2010A Bonds and the Series 2010B Bonds were issued pursuant to an Indenture of Trust, dated asof November 23, 2010 between the District and The Bank of New York Mellon Trust Company, N.A., astrustee (the "2010A-B Indenture"). The Series 2012A Bonds were issued pursuant to an Indenture ofTrust, dated as of December 20, 2012, between the District and The Bank of New York Mellon TrustCompany, N.A., as trustee (the "2012A Indenture"). The 2007 Indenture, 2010A-B Indenture and the2012A Indenture are referred to collectively herein as the "Parity Indentures." The RTD TIFIA Bondwas issued pursuant to a TIFIA Loan Agreement, dated as of December 1, 2011, between the District andthe United States Department of Transportation, an agency of the United States of America, acting by andthrough the Federal Highway Administrator (the "TIFIA Loan Agreement").

The Bank of New York Mellon Trust Company, N.A. is the successor in interest to The Bank ofNew York Trust Company, N.A., and therefore serves as trustee (the "Senior Debt Trustee") for theSenior Bonds, the four separate series of Parity Bonds (other than the RTD TIFIA Bond) and futureSenior Debt and Parity Bonds. The Indenture requires that any entity that serves as trustee for the SeniorDebt, the Parity Bonds or as trustee for any obligation payable on a parity with the Bonds will also serve

1To date, no draws have been made under the RTD TIFIA Bond. Accordingly, the principal balance outstanding and payable onthe Parity Bonds as of April 1, 2013 was $1,451,130,000. See "DEBT STRUCTURE OF RTD."

-3-

as trustee under the Indenture, and the Senior Debt Trustee therefore has been selected to serve as Trusteefor the Bonds. The District, in accordance with the authority granted by the Act to pledge the Sales TaxRevenues to the payment of securities of the District, has assigned its rights to receive from the ColoradoDepartment of Revenue (the "Department of Revenue") payment of the 0.6% Sales Tax Revenues to theSenior Debt Trustee for the benefit of the owners of the Senior Debt. The District has also assigned to theTrustee its rights to receive payment from the Department of Revenue of the 0.4% Sales Tax Revenuesfor the benefit of the owners of the Bonds and any other securities payable from the 0.4% Sales TaxRevenues, including the Parity Bonds. In each month, after making in full all deposits or paymentsrequired by the Senior Bond Resolution, the Senior Debt Trustee is required to remit any remaining 0.6%Sales Tax Revenues to the Trustee to fund any requirements under the Parity Indentures, the Indentureand the TIFIA Loan Agreement not otherwise funded by the 0.4% Sales Tax Revenues. See "SECURITYFOR THE BONDS – Flow of Funds."

The Board of Directors of RTD (the "Board") has covenanted in the Indenture that no additionalsecurities are to be issued by the District with a pledge of and lien on the 0.6% Sales Tax Revenues or the0.4% Sales Tax Revenues that is superior or senior to the lien thereon of the Bonds, except for obligationsissued by the District to refund, in whole or in part, outstanding Senior Debt, provided that, after theissuance of such refunding bonds, the debt service payable in each Bond Year on all Senior Debt shall notexceed the debt service payable in such Bond Year on all Senior Debt outstanding prior to the issuance ofsuch refunding bonds. The Indenture also permits the District to enter into Senior Financial ProductsAgreements and Senior Credit Facility Obligations in connection with the Senior Debt. Upon satisfactionof certain conditions, the District may also, and expects to, issue additional securities with a pledge of andlien on the Sales Tax Revenues on a parity with the Bonds. See "SECURITY FOR THE BONDS –Additional Securities."

The District has previously pledged the Sales Tax Revenues on a basis subordinate to the Bondsin connection with its P3 Concession and Lease Agreement with Denver Transit Partners and with theissuance of the District’s Subordinate Lien Sales Tax Revenue Bond, Series 2010 (the "DUSPA Bond").See "DEBT STRUCTURE OF RTD" and "THE SYSTEM – FasTracks – Eagle P3 Project."

In connection with the issuance of the Bonds, the District will deliver a Continuing DisclosureAgreement in substantially the form attached as Appendix A. See "CONTINUING DISCLOSUREAGREEMENT."

This Official Statement includes financial, demographic and other information about the District.Prospective purchasers are encouraged to read this Official Statement and the appendices hereto in theirentirety. This Official Statement also contains descriptions of the Bonds, the Indenture and otherdocuments and information pertaining to the Bonds. The description of the Bonds, the Indenture andsuch other documents do not purport to be definitive or comprehensive, and all references to thosedocuments are qualified by reference to those documents. Copies of the above-mentioned documentsmay be obtained from Brenden Morgan, Manager of Debt and Investments, Regional TransportationDistrict, 1600 Blake Street, Denver, Colorado 80202 (303) 299-2313 or at the offices of the District'sfinancial advisor, First Southwest Company, 325 N. St. Paul Street, Suite 800, Dallas, Texas 75201-3852,Attention: Mike Newman (214) 953-8875.

-4-

THE BONDS

Authority

The District is authorized by a resolution (the "Bond Resolution") adopted by the Board to enterinto the Indenture. The Bonds are issued pursuant to the Indenture, the Act and Section 11-57-201 et seq.,Colorado Revised Statutes, as amended. Pursuant to Art. X, § 20(4)(b) of the State Constitution, theBonds may be issued without voter approval for the purpose of refunding the Refunded Bonds at a lowerinterest rate. See "CONSTITUTIONAL REVENUE, SPENDING AND DEBT LIMITATIONS."

Description

The Bonds are dated, mature and bear interest and are subject to the other terms and conditions asdescribed on the cover page hereof.

Prior Redemption

Optional Redemption

The Bonds are subject to redemption prior to their respective maturity dates at the option of theDistrict on November 1, 2023, and on any date thereafter, in any order of maturity and by lot within amaturity (giving proportionate weight to Bonds in denominations larger than $5,000), at a redemptionprice equal to the Make-Whole Price. The Make-Whole Price shall be calculated by a qualified,independent entity appointed by the Chief Financial Officer.

The "Make-Whole Price" means the amount equal to the greater of the following:

(a) 100% of the Amortized Value (as defined below) of the Bonds to be redeemed, plusaccrued and unpaid interest to the date of redemption; or

(b) an aggregate amount equal to the sum of the present values of the remaining unpaidpayments of principal and interest to be paid on the Bonds to be redeemed from and including the date ofredemption to the stated maturity date of such Bonds, discounted to the date of redemption on asemiannual basis at a discount rate equal to the Applicable Tax-Exempt Municipal Bond Rate (as definedbelow) for such Bonds plus zero basis points.

For purposes of determining the Make-Whole Price, the "Amortized Value" will equal theprincipal amount of the Bonds to be redeemed multiplied by the price of such Bonds expressed as apercentage, calculated based on the industry standard method of calculating bond prices, with a deliverydate equal to the date of redemption, a maturity date equal to the stated maturity date of such Bonds and ayield equal to such Bonds' original reoffering yield as set forth on the cover of this Official Statement.

For purpose of determining the Make-Whole Price, the "Applicable Tax-Exempt MunicipalBond Rate" for such Bonds will be the "Comparable AAA General Obligations" yield curve rate for thestated maturity date of such Bonds as published by Municipal Market Data five business days prior to thedate of redemption. If no such yield curve rate is established for the applicable year, the "ComparableAAA General Obligations" yield curve rate for the two published maturities most closely correspondingto the applicable year will be determined, and the "Applicable Tax Exempt Municipal Bond Rate" will beinterpolated or extrapolated from those yield curve rates on a straight-line basis. This rate is madeavailable daily by Municipal Market Data and is available to its subscribers through its internet address:www.tm3.com.

-5-

In calculating the Applicable Tax-Exempt Municipal Bond Rate, should Municipal Market Datano longer publish the "Comparable AAA General Obligations" yield curve rate, then the Applicable Tax-Exempt Municipal Bond Rate will equal the Consensus Scale yield curve rate for the applicable year.The Consensus Scale yield curve rate is made available daily by Municipal Market Advisors and isavailable to its subscribers through its internet address: www.mma-research.com. In the further eventMunicipal Market Advisors no longer publishes the Consensus Scale, the Applicable Tax-ExemptMunicipal Bond Rate will be determined by Morgan Stanley & Co. LLC, as the quotation agent, basedupon the rate per annum equal to the semiannual equivalent yield to maturity of those tax-exempt generalobligation bonds rated in the highest rating category by Moody's Investors Service and Standard & Poor'sRating Services with a maturity date equal to the stated maturity date of such Bonds having characteristics(other than the ratings) most comparable to those of such Bonds in the judgment of the quotation agent.In the event Morgan Stanley & Co. LLC is unable to perform such service, a primary dealer qualified toperform such service may be selected by the RTD's Chief Financial Officer. The quotation agent'sdetermination of the Applicable Tax-Exempt Municipal Bond Rate is final and binding in the absence ofmanifest error.

Notice of Redemption

Notice of the prior redemption of any Bonds shall be given by the Trustee in the name of theDistrict by mailing a copy of the redemption notice by certified or first-class postage prepaid mail, notmore than 60 nor less than 30 days prior to the redemption date to the registered owners of the Bonds tobe redeemed at their addresses as shown on the registration records kept by the Trustee, or in the eventthat the Bonds to be redeemed are registered in the name of the Securities Depository, such notice may, inthe alternative, be given by electronic means in accordance with the requirements of the securitiesdepository. Failure to give such notice by mailing to the registered owner of any Bond or any defecttherein shall not affect the validity of the proceedings for the redemption of any other Bonds.

Any notice of redemption may contain a statement that the redemption is conditioned upon thereceipt of funds on or before the redemption date sufficient to pay the principal of, interest on and anyredemption premium due on the Bonds so called for redemption, and that if such funds are not available,such redemption shall be cancelled by written notice to the registered owners of the Bonds called forredemption in the same manner as the original redemption notice was mailed.

If the Depository Trust Company ("DTC") or its nominee is the registered owner of anyBonds to be redeemed, notice of redemption will only be given to DTC or its nominee as theregistered owner of such Bond. Any failure on the part of DTC or failure on the part of a nomineeof a Beneficial Owner (having received notice from a DTC Participant or otherwise) to notify theBeneficial Owner of any Bond to be redeemed shall not affect the validity of the redemption of suchBond. See "Book-Entry Form" under this caption.

Debt Service Requirements

The Debt Service Requirements of the Bonds, the Parity Bonds (taking into account theanticipated refunding of the Refunded Bonds) and the Senior Bonds are set forth in the following table:

TA

BL

EI

Fis

cal

Yea

rD

ebt

Ser

vice

Deb

tS

ervi

ceR

equ

irem

ents

ofP

arit

yB

ond

sD

ebt

Ser

vice

Req

uir

emen

tsof

the

Bon

ds

Tot

alD

ebt

Ser

vice

Tot

alD

ebt

Ser

vice

Req

uir

emen

tsof

En

din

g1

2/3

1R

equ

irem

ents

ofS

enio

rB

ond

sO

uts

tan

din

gP

arit

yB

ond

s(1)

RT

DT

IFIA

Bo

nd

(2)

Pri

nci

pal

Inte

rest

Tot

alR

equ

irem

ents

ofB

ond

san

dP

arit

yB

ond

sS

enio

rB

ond

s,P

arit

yB

ond

san

dth

eB

ond

s

20

13$

21,

244

,842

$19

,36

1,39

4(3

)$

--$

--$

4,59

2,7

12$

4,59

2,7

12$

23

,954

,106

$4

5,1

98,9

482

014

28

,767

,87

15

9,7

38,4

63

----

10

,020

,46

31

0,0

20,4

63

69

,758

,92

59

8,5

26,7

96

20

152

8,7

69,1

44

59

,742

,86

3--

--1

0,0

20,4

63

10

,020

,46

36

9,7

63,3

25

98

,532

,46

92

016

28

,766

,02

85

9,7

39,9

13

----

10

,020

,46

31

0,0

20,4

63

69

,760

,37

59

8,5

26,4

03

20

172

8,6

24,8

05

59

,741

,11

3--

--1

0,0

20,4

63

10

,020

,46

36

9,7

61,5

75

98

,386

,38

02

018

28

,376

,45

55

9,7

41,2

50

----

10

,020

,46

31

0,0

20,4

63

69

,761

,71

39

8,1

38,1

68

20

191

9,9

80,3

40

59

,740

,32

5--

--1

0,0

20,4

63

10

,020

,46

36

9,7

60,7

88

89

,741

,12

82

020

19

,982

,06

05

9,7

39,9

25

----

10

,020

,46

31

0,0

20,4

63

69

,760

,38

88

9,7

42,4

48

20

211

4,4

95,5

78

59

,741

,87

51

0,8

88,3

88

--1

0,0

20,4

63

10

,020

,46

38

0,6

50,7

25

95

,146

,30

42

022

9,5

83

,950

59

,740

,82

51

0,8

88,3

88

--1

0,0

20,4

63

10

,020

,46

38

0,6

49,6

75

90

,233

,62

52

023

9,5

82

,400

79

,488

,42

51

0,8

88,3

88

--1

0,0

20,4

63

10

,020

,46

31

00,

397

,275

10

9,97

9,6

752

024

9,5

88

,275

79

,492

,52

51

0,8

88,3

88

--1

0,0

20,4

63

10

,020

,46

31

00,

401

,375

10

9,98

9,6

502

025

--7

9,4

93,5

50

19

,484

,11

1--

10

,020

,46

31

0,0

20,4

63

10

8,99

8,1

231

08,

998

,123

20

26--

10

0,49

8,6

501

9,4

81,0

11

--1

0,0

20,4

63

10

,020

,46

31

30,

000

,123

13

0,00

0,1

232

027

--9

4,3

92,6

50

11

,304

,74

74

3,2

05,0

00

10

,020

,46

35

3,2

25,4

63

15

8,92

2,8

591

58,

922

,859

20

28--

93

,343

,87

51

1,3

04,7

47

45

,365

,00

07

,86

0,2

135

3,2

25,2

13

15

7,87

3,8

341

57,

873

,834

20

29--

82

,501

,05

01

1,3

04,7

47

47

,630

,00

05

,59

1,9

635

3,2

21,9

63

14

7,02

7,7

591

47,

027

,759

20

30--

10

6,24

6,4

501

1,3

04,7

47

--3

,21

0,4

633

,21

0,4

631

20,

761

,659

12

0,76

1,6

592

031

--1

26,

325

,775

11

,304

,74

71

9,6

65,0

00

3,2

10

,463

22

,875

,46

31

60,

505

,984

16

0,50

5,9

842

032

--1

22,

664

,850

11

,304

,74

71

9,5

50,0

00

2,2

27

,213

21

,777

,21

31

55,

746

,809

15

5,74

6,8

092

033

--1

34,

631

,025

11

,304

,74

7--

1,2

49

,713

1,2

49

,713

14

7,18

5,4

841

47,

185

,484

20

34--

10

5,90

9,5

001

1,3

04,7

47

--1

,24

9,7

131

,24

9,7

131

18,

463

,959

11

8,46

3,9

592

035

--1

03,

868

,725

11

,304

,74

7--

1,2

49

,713

1,2

49

,713

11

6,42

3,1

841

16,

423

,184

20

36--

10

9,28

3,4

501

1,3

04,7

47

29

,405

,00

01

,24

9,7

133

0,6

54,7

13

15

1,24

2,9

091

51,

242

,909

20

37--

12

6,49

1,0

501

1,3

04,7

47

----

--1

37,

795

,797

13

7,79

5,7

972

038

--5

6,0

30,2

50

11

,304

,74

7--

----

67

,334

,99

76

7,3

34,9

97

20

39--

17

,532

,00

05

0,5

00,7

98

----

--6

8,0

32,7

98

68

,032

,79

82

040

--1

7,5

32,0

00

50

,500

,79

8--

----

68

,032

,79

86

8,0

32,7

98

20

41--

17

,532

,00

05

0,5

00,7

98

----

--6

8,0

32,7

98

68

,032

,79

82

042

--1

7,5

32,0

00

50

,500

,79

8--

----

68

,032

,79

86

8,0

32,7

98

20

43--

17

,532

,00

05

0,5

00,7

98

----

--6

8,0

32,7

98

68

,032

,79

82

044

--1

7,5

32,0

00

50

,500

,79

8--

----

68

,032

,79

86

8,0

32,7

98

20

45--

17

,532

,00

05

0,5

00,7

98

----

--6

8,0

32,7

98

68

,032

,79

82

046

--7

0,7

52,0

00

----

----

70

,752

,00

07

0,7

52,0

00

20

47--

70

,831

,82

3--

----

--7

0,8

31,8

23

70

,831

,82

32

048

--7

0,9

20,2

23

----

----

70

,920

,22

37

0,9

20,2

23

20

49--

71

,015

,80

3--

----

--7

1,0

15,8

03

71

,015

,80

32

050

--7

1,1

16,5

84--

----

--7

1,1

16,5

8471

,116

,58

4T

ota

l$

247

,761

,74

9$

2,6

35,0

50,

176

$5

71,6

81,2

17

$2

04,8

20,0

00

$1

71,9

78,3

49

$3

76,7

98,3

49

$3

,583

,52

9,74

2$

3,8

31,2

91,

492

__

___

___

___

_(1

)D

oes

not

incl

ude

Bu

ild

Am

eric

aB

ond

sub

sid

yex

pec

ted

tob

epa

idb

yfe

der

algo

ver

nm

ent

inco

nn

ecti

onw

ith

the

Ser

ies

201

0BB

ond

s.T

akes

into

acco

unt

the

refu

ndin

gof

the

Ref

und

edB

ond

sd

escr

ibed

in"P

LA

NO

FF

INA

NC

E–

Th

eR

efu

ndin

gE

scro

w."

(2)

Th

isco

lum

nsh

ows

the

Dis

tric

t'ses

tim

ated

deb

tse

rvic

eon

the

RT

DT

IFIA

Bon

das

set

fort

hin

the

TIF

IAL

oan

Agr

eem

ent.

Th

eR

TD

has

issu

edth

eT

IFIA

Bon

dbu

tn

oam

ount

sar

eou

tsta

ndi

ng

atth

isti

me.

Tim

ing

and

size

ofac

tual

dra

ws

und

erth

eT

IFIA

Loa

nA

gree

men

tm

ayca

use

actu

ald

ebt

serv

ice

tova

ryfr

omes

tim

ates

incl

ud

edh

erei

n.

See

"DE

BT

ST

RU

CT

UR

EO

FR

TD

."(3

)In

tere

stin

Fis

cal

Yea

r2

013

onth

eS

erie

s2

012

AB

ond

sw

ill

be

pay

able

from

pro

ceed

sof

the

Ser

ies

20

12A

Bon

ds

dep

osit

edto

the

Cap

ital

ized

Inte

rest

Acc

oun

tof

the

Bon

dF

und

held

und

erth

e20

12A

Ind

entu

re.

Sou

rce:

Th

eF

inan

cial

Ad

viso

r.

-6-

-7-

Payment and Registration

The Bonds are issuable in fully registered form and are initially to be registered in the name ofCede & Co., as nominee for DTC, as securities depository for the Bonds (the "Securities Depository").Purchases by beneficial owners ("Beneficial Owners") of the Bonds are to be made in book-entry form inthe principal amount of $5,000 or any integral multiple thereof. Principal of and final installment ofinterest on the Bonds are payable upon presentation and surrender thereof to, and all other interest ispayable by, the Paying Agent, by check or draft mailed to the registered owners at the addressesappearing on the registration records of the Paying Agent on the 15th day of the calendar month nextpreceding such interest payment date. The Paying Agent may make payments of interest on any Bond bysuch alternative means as may be mutually agreed to by the Paying Agent and the registered owner ofsuch Bond. Notwithstanding the foregoing, so long as the Bonds are registered in the name of DTC or itsnominee, payments to Beneficial Owners are to be made as described in "Book-Entry Form" under thiscaption. The Trustee is acting as Paying Agent under the Indenture.

Neither the District nor the Trustee has any responsibility or obligation for the payment to theparticipants of the Securities Depository ("Participants"), any Beneficial Owner or any other person ofthe principal of or interest on the Bonds.

Neither the District nor the Trustee has any responsibility or obligation with respect to theaccuracy of the records of the Securities Depository or its Participants regarding any ownership interest inthe Bonds or the delivery to any Participant, Beneficial Owner or any other person of any notice withrespect to the Bonds.

Transfer and Exchange

The Bonds are transferable only upon the registration books of the District, which are to be keptfor such purposes at the principal corporate trust office of the Registrar, by the registered owner or his,her or its duly authorized attorney. The registered owner of any Bond or Bonds may also exchange suchBond or Bonds for another Bond or Bonds of authorized denominations. The Registrar may imposereasonable charges in connection with such exchanges and transfers of Bonds, which charges (as well asany tax or other governmental charge required to be paid with respect to such exchange or transfer) are tobe paid by the registered owner requesting such exchange or transfer. In the case of every transfer orexchange, the Registrar is to authenticate and deliver to the new registered owner a new Bond or Bonds ofthe same aggregate principal amount, maturing in the same year and bearing interest at the same perannum interest rate as the Bond or Bonds surrendered. Notwithstanding the foregoing, so long as theBonds are registered in the name of DTC or its nominee, transfers by Beneficial Owners are to be made asdescribed in "Book-Entry Form" under this caption. The Trustee is acting as Registrar under theIndenture.

Neither the District nor the Trustee has any responsibility or obligation with respect to theaccuracy of the records of the Securities Depository or its Participants regarding any ownership interest inthe Bonds or transfers thereof.

Defeasance and Discharge

The Indenture provides the District with the right to discharge the pledge and lien created by theIndenture with respect to any Bonds by depositing in an escrow fund with the Trustee or other depositorysufficient moneys or Federal Securities which are direct obligations of, or obligations the principal of andinterest on which are unconditionally guaranteed by, the United States (or ownership interests in any ofthe foregoing) and which are not callable prior to their scheduled maturities by the issuer thereof, to pay

-8-

when due the Debt Service Requirements on such Bonds at the maturity or redemption thereof. SeeAppendix E – "SUMMARY OF CERTAIN PROVISIONS OF THE INDENTURE – Defeasance."

Book-Entry Form

The following description of the procedures and record keeping with respect to beneficialownership interests in the Bonds, payment of interest and other payments on the Bonds, confirmation andtransfer of beneficial ownership interests in the Bonds and other related transactions is based solely oninformation furnished by DTC.

DTC will act as securities depository for the Bonds. The Bonds are to be issued as fully-registered securities registered in the name of Cede & Co. (DTC's partnership nominee) or such othername as may be requested by an authorized representative of DTC. One fully registered Bond certificateis to be issued for each maturity of the Bonds, each in the aggregate principal amount of such maturity,and is to be deposited with DTC.

DTC, the world's largest depository, is a limited-purpose trust company organized under the NewYork Banking Law, a "banking organization" within the meaning of the New York Banking Law, amember of the Federal Reserve System, a "clearing corporation" within the meaning of the New YorkUniform Commercial Code and a "clearing agency" registered pursuant to the provisions of Section 17Aof the Securities Exchange Act of 1934, as amended. DTC holds and provides asset servicing for over 3.5million issues of U.S. and non U.S. equity, corporate and municipal debt issues, and money marketinstruments (from over 100 countries) that DTC's Participants ("Direct Participants") deposit with DTC.DTC also facilitates the post trade settlement among Direct Participants of sales and other securitiestransactions, in deposited securities, through electronic computerized book-entry transfers and pledgesbetween Participants' accounts. This eliminates the need for physical movement of securities certificates.Direct Participants include both U.S. and non-U.S. securities brokers and dealers, banks, trust companies,clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of theDepository Trust & Clearing Corporation ("DTCC"). DTCC is the holding company for DTC, NationalSecurities Clearing Corporation and Fixed Income Clearing Corporation, all of which are registeredclearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC systemis also available to others, such as both U.S. and non-U.S. securities brokers and dealers, banks, trustcompanies, and clearing corporations that clear through or maintain a custodial relationship with a DirectParticipant, either directly or indirectly ("Indirect Participants"). DTC has a Standard & Poor's rating ofAA+. The DTC Rules applicable to its Participants are on file with the Securities and ExchangeCommission. More information about DTC can be found at www.dtcc.com and www.dtc.org. TheDistrict undertakes no responsibility for and makes no representations as to the accuracy or thecompleteness of the content of such material contained in such websites as described in the precedingsentence, including, but not limited to, updates of such information or links to other internet sites accessedthrough the aforementioned websites.

Purchases of Bonds under the DTC system must be made by or through Direct Participants,which are to receive a credit for the Bonds on DTC's records. The ownership interest of each BeneficialOwner is in turn to be recorded on the Direct and Indirect Participants' records. Beneficial Owners arenot to receive written confirmation from DTC of their purchases. Beneficial Owners are, however,expected to receive written confirmations providing details of the transactions, as well as periodicstatements of their holdings, from the Direct or Indirect Participants through which the Beneficial Ownersentered into the transactions. Transfers of ownership interests in the Bonds are to be accomplished byentries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners.Beneficial Owners are not to receive certificates representing their ownership interests in Bonds, except inthe event that use of the book-entry system for the Bonds is discontinued.

-9-

To facilitate subsequent transfers, all Bonds deposited by Direct Participants with DTC areregistered in the name of DTC's partnership nominee, Cede & Co. or such other name as may berequested by an authorized representative of DTC. The deposit of Bonds with DTC and their registrationin the name of Cede & Co. or such other nominee do not affect any change in beneficial ownership. DTChas no knowledge of the actual Beneficial Owners of the Bonds; DTC's records reflect only the identity ofthe Direct Participants to whose accounts such Bonds are credited, which may or may not be theBeneficial Owners. The Direct and Indirect Participants remain responsible for keeping account of theirholdings on behalf of their customers.

Conveyance of notices and other communications by DTC to Direct Participants, by DirectParticipants to Indirect Participants, and by Direct Participants and Indirect Participants to BeneficialOwners are governed by arrangements among them, subject to any statutory or regulatory requirements asmay be in effect from time to time. Beneficial Owners of the Bonds may wish to take certain steps toaugment transmission to them of notices of significant events with respect to the Bonds, such asredemptions, tenders, defaults, and proposed amendments to the underlying documents. For example,Beneficial Owners of the Bonds may wish to ascertain that the nominee holding the Bonds for theirbenefit has agreed to obtain and transmit notices to Beneficial Owners. In the alternative, BeneficialOwners may wish to provide their names and addresses to the Trustee and request that copies of noticesbe provided directly to them.

Redemption notices are to be sent to DTC. If less than all of the Bonds within an issue are beingredeemed, DTC's practice is to determine by lot the amount of interest of each Direct Participant to beredeemed.

Neither DTC nor Cede & Co. (nor such other DTC nominee) will consent or vote with respect toBonds unless authorized by a Direct Participant in accordance with DTC's MMI Procedures. Under itsusual procedures, DTC mails an omnibus proxy to the District as soon as possible after the record date.The omnibus proxy assigns Cede & Co.'s consenting or voting rights to those Direct Participants to whoseaccounts the Bonds are credited on the record date (identified in a listing attached to the omnibus proxy).

Principal, interest and redemption payments on the Bonds are to be made to Cede & Co. or suchother nominee as may be requested by an authorized representative of DTC. DTC's practice is to creditDirect Participants' accounts upon DTC's receipt of funds and corresponding detail information from theDistrict or the Trustee on payment date in accordance with their respective holdings shown on DTC'srecords. Payments by Participants to Beneficial Owners are governed by standing instructions andcustomary practices, as is the case with securities held for the accounts of customers in bearer form orregistered in "street name" and are the responsibility of such Participants and not of DTC, its nominee, theTrustee or the District, subject to any statutory or regulatory requirements as may be in effect from timeto time. Payment of principal, interest and redemption payments to Cede & Co. (or such other nomineeas may be requested by an authorized representative of DTC) is the responsibility of the District or theTrustee, disbursement of such payments to Direct Participants is the responsibility of DTC, anddisbursement of such payments to the Beneficial Owners is the responsibility of Direct and IndirectParticipants.

DTC may discontinue providing its services as securities depository with respect to the Bonds atany time by giving reasonable notice to the District or the Trustee. Under such circumstances, in theevent that a successor securities depository is not obtained, the Bonds are required to be printed anddelivered.

-10-

The District may decide to discontinue use of the system of book-entry-only transfers throughDTC (or a successor securities depository). In that event, certificates will be printed and delivered toDTC.

The information in this section concerning DTC and DTC's book-entry system has beenobtained from sources that the District believes to be reliable, but neither the District nor theUnderwriters take any responsibility for the accuracy thereof.

SECURITY FOR THE BONDS

The Bonds are special and limited obligations of the District payable solely from and secured bythe Pledged Revenues. The Bonds are not general obligations of RTD. The Bonds are not payable inwhole or in part from the proceeds of general property taxes, nor is the full faith and credit of RTDpledged to pay the Bonds. See Appendix E – "SUMMARY OF CERTAIN PROVISIONS OF THEINDENTURE."

Flow of Funds

The Indenture provides for payments, in the sequence described below, into and out of thefollowing funds held by the Trustee and for the stated purposes.

0.4% Sales Tax Revenues

All amounts received by the Trustee from the 0.4% Sales Tax Revenues are to be deposited to the0.4% Sales Tax Increase Fund. Amounts deposited in the 0.4% Sales Tax Increase Fund are to be appliedeach month by the Trustee to the following purposes in the following order of priority:

Bond Fund. First, from moneys on deposit in the 0.4% Sales Tax Increase Fund, there isto be credited to the Bond Fund, concurrently on a pari passu basis with any payments required to bemade with respect to any parity obligations (including the Parity Bonds), the following amounts:

Interest Payments. Commencing with the month immediately succeeding thedelivery of the Bonds, an amount in equal monthly installments necessary, together with any othermoneys from time to time available therefor from whatever source, to pay the next installment of interestdue on the Bonds then outstanding.

Principal Payments. Commencing with the month immediately succeeding thedelivery of the Bonds, or commencing one year next prior to the first principal payment date of theBonds, whichever commencement date is later, an amount in equal monthly installments necessary,together with any other moneys from time to time available therefor from whatever source, to pay thenext installment of principal (whether at maturity or on a redemption date) due on the Bonds thenoutstanding.

Moneys on deposit in the Bond Fund secure only the payment of the Bonds.

Parity Bond Reserve Funds. Second, from any moneys remaining in the 0.4% Sales TaxIncrease Fund there shall be made any payments required to be made pursuant to any reserve fundsestablished in connection with any parity obligations and concurrently with any repayment or similarobligations payable to any surety provider issuing any reserve fund insurance policy with respect to anyParity Bonds.

-11-

Rebate Fund. Third, and concurrently with any payments required to be made pursuantto any rebate funds established for any parity obligations, from any moneys remaining on deposit in the0.4% Sales Tax Increase Fund, there shall be credited to the Rebate Fund the amount required, if any,until the amount on deposit in the Rebate Fund satisfies the requirements of the Indenture.

Interest on Reserve Fund Insurance Policy Draws on Parity Bonds. Fourth, from anymoneys remaining on deposit in the 0.4% Sales Tax Increase Fund, there shall be paid to any suretyprovider issuing any reserve fund insurance policy with respect to any Parity Bonds, interest on anyamounts drawn under any such reserve fund insurance policy until such interest has been paid in full.

Payment of Subordinate Lien Obligations. Fifth, and subject to the provisions of theIndenture, any moneys remaining on deposit in the 0.4% Sales Tax Increase Fund after the foregoingpayments have been made may be used by the District for the payment of Subordinate Lien Obligations,including reasonable reserves for such Subordinate Lien Obligations and for rebate of amounts to theUnited States Treasury with respect to such Subordinate Lien Obligations, and any Subordinate CreditFacility Obligations and any payments on Subordinate Financial Products Agreements which have a lienon Pledged Revenues subordinate and junior to the lien thereon of the Bonds.

Remaining Revenues. In each month, after making in full the deposits or paymentsrequired from moneys on deposit in the 0.4% Sales Tax Increase Fund, any amounts remaining on depositin the 0.4% Sales Tax Increase Fund are to be remitted by the Trustee to the District free and clear of thelien of the Indenture, unless otherwise directed by the District in writing. See "DEBT STRUCTURE OFRTD" for a description of outstanding and anticipated debt obligations of RTD.

0.6% Sales Tax Revenues

All amounts received by the Senior Debt Trustee from the 0.6% Sales Tax Revenues are to beapplied first as required by the Senior Bond Resolution so long as any Senior Debt remains outstanding.In each month, after making in full all deposits or payments required by the Senior Bond Resolution, anyremaining 0.6% Sales Tax Revenues are to be remitted by the Senior Debt Trustee to the Trustee, free andclear of the lien of the Senior Bond Resolution, for deposit by the Trustee into the 0.6% Sales Tax Fund.Amounts on deposit in the 0.6% Sales Tax Fund are to be applied each month by the Trustee for thefollowing purposes in the following order of priority:

Insufficiency of Moneys on Deposit in 0.4% Sales Tax Increase Fund. First, to the extentthat moneys on deposit in the 0.4% Sales Tax Increase Fund are insufficient in any month to make any ofthe deposits or payments required to be made as set forth above, any moneys on deposit in the 0.6% SalesTax Fund are to be used in such month to make such deposits or payments in the order of priority set forthin "0.4% Sales Tax Revenues" under this caption.

Remaining Revenues. In each month, after making in full the deposits or paymentsrequired by the Indenture from moneys on deposit in the 0.6% Sales Tax Fund, any amounts remaining ondeposit in the 0.6% Sales Tax Fund are to be remitted by the Trustee to the District free and clear of thelien of the Indenture, unless otherwise directed by the District in writing. See "DEBT STRUCTURE OFRTD" for a description of outstanding and anticipated debt obligations of RTD.

The flow of funds under the Indenture is illustrated on the following page:

-12-

Bond Fund

Pay principal and intereston Parity Bonds and Bonds

Parity Bond Reserve Funds

Maintain reserve requirements forcertain Parity Bonds (The Bonds will

not be secured by a reserve fund.)

Rebate Fund

Pay rebate requirements (if any)

Reserve Surety Provider

Pay interest on draws on reservefund insurance policies (if any)

Subordinate Lien Obligations

Pay subordinate lien obligations

RTD

Apply to any legal purpose

Bond Service Account

Pay principal and intereston Senior Debt

Bond Reserve Account

Maintain Senior Debt reserve requirement

Rebate Account

Pay rebate requirement (if any)

BONDS, PARITY BONDS ANDOBLIGATIONS

0.4% Sales Tax Revenues

SENIOR DEBT

0.6% Sales Tax Revenues

RemainingRevenues Reserve Surety Provider

Pay interest on draws on reserve fundinsurance policies (if any)

-13-

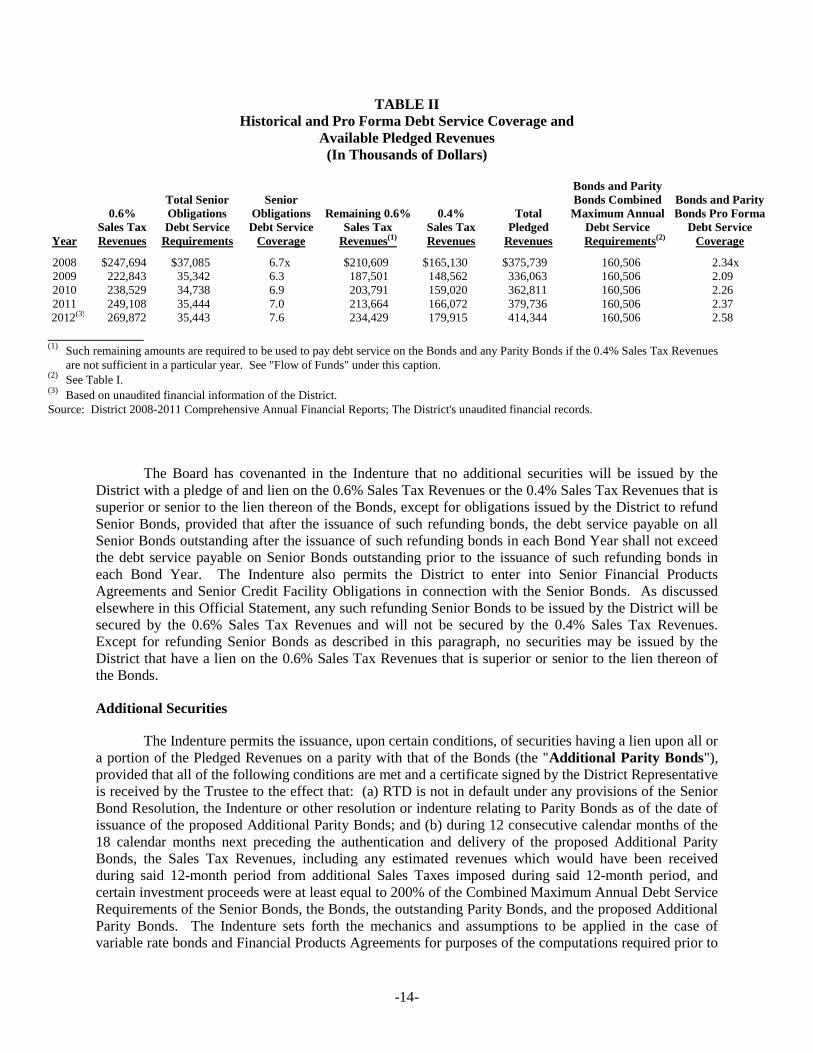

Debt Service Coverage

Based upon the Debt Service Requirements of the Senior Bonds set forth in Table I, theCombined Maximum Annual Debt Service Requirements on the Senior Bonds is $28.769 million (inFiscal Year 2015). Based upon the Debt Service Requirements of the Bonds and Parity Bonds set forth inTable I, the Combined Maximum Annual Debt Service Requirements on the Bonds and Parity Bonds is$160.506 million (in Fiscal Year 2031) and the combined average annual Debt Service Requirements onthe Bonds and Parity Bonds is $102.168 million. Based upon the Debt Service Requirements of theSenior Bonds, the Bonds and the Parity Bonds set forth in Table I, the Combined Maximum Annual DebtService Requirements on the Senior Bonds, the Bonds and the Parity Bonds is $160.506 million (in FiscalYear 2031).

The District collected annual 0.4% Sales Tax Revenues and annual 0.6% Sales Tax Revenues of$179.915 million and $269.872 million, respectively, for 2012, totaling $449.787 million.

If the residual amount ($241.103 million) obtained by subtracting the Combined MaximumAnnual Debt Service Requirements of the Senior Bonds ($28.769 million) from the 2012 annual 0.6%Sales Tax Revenues ($269.872 million) is added to the 2012 annual 0.4% Sales Tax Revenues ($179.915million), the resulting approximation of Pledged Revenues in the amount of $421.018 million would yielda debt service coverage of the Combined Maximum Annual Debt Service Requirements on the Bonds andParity Bonds ($160.506 million) of 2.62x and a debt service coverage of the combined average annualDebt Service Requirements on the Bonds and Parity Bonds ($102.168 million) of 4.12x.

Based on the combined 0.6% Sales Tax Revenues and 0.4% Sales Tax Revenues collected for2012 of approximately $449.787 million, the District's combined maximum annual debt service coverageon the Senior Bonds, the Parity Bonds and the Bonds as set forth in Table I ($160.506 million) would be2.80x. However, as discussed elsewhere in this Official Statement, the Senior Bonds are not secured bythe 0.4% Sales Tax Revenues.

Based solely on the 0.4% Sales Tax Revenues collected for 2012 ($179.915 million), theDistrict's combined maximum annual debt service coverage on the Bonds and Parity Bonds ($160.506million) would be 1.12x and its combined average annual debt service coverage on the Bonds and ParityBonds ($102.168 million) would be 1.76x.

The following table sets forth historical debt service coverage on the Senior Bonds having a lienon the 0.6% Sales Tax that is senior to the lien thereon of the Bonds, the amount of Pledged Revenuesgenerated for the past five years and pro forma historical debt service coverage on the Bonds and ParityBonds based on estimated Combined Maximum Annual Debt Service Requirements on the Bonds andParity Bonds:

[Remainder of page left blank intentionally]

-14-

TABLE IIHistorical and Pro Forma Debt Service Coverage and

Available Pledged Revenues(In Thousands of Dollars)

Year

0.6%Sales TaxRevenues

Total SeniorObligationsDebt Service

Requirements

SeniorObligationsDebt Service

Coverage

Remaining 0.6%Sales Tax

Revenues(1)

0.4%Sales TaxRevenues

TotalPledged

Revenues

Bonds and ParityBonds Combined

Maximum AnnualDebt ServiceRequirements(2)

Bonds and ParityBonds Pro Forma

Debt ServiceCoverage

2008 $247,694 $37,085 6.7x $210,609 $165,130 $375,739 160,506 2.34x2009 222,843 35,342 6.3 187,501 148,562 336,063 160,506 2.092010 238,529 34,738 6.9 203,791 159,020 362,811 160,506 2.262011 249,108 35,444 7.0 213,664 166,072 379,736 160,506 2.372012(3) 269,872 35,443 7.6 234,429 179,915 414,344 160,506 2.58

____________(1)

Such remaining amounts are required to be used to pay debt service on the Bonds and any Parity Bonds if the 0.4% Sales Tax Revenuesare not sufficient in a particular year. See "Flow of Funds" under this caption.

(2)See Table I.

(3)Based on unaudited financial information of the District.

Source: District 2008-2011 Comprehensive Annual Financial Reports; The District's unaudited financial records.

The Board has covenanted in the Indenture that no additional securities will be issued by theDistrict with a pledge of and lien on the 0.6% Sales Tax Revenues or the 0.4% Sales Tax Revenues that issuperior or senior to the lien thereon of the Bonds, except for obligations issued by the District to refundSenior Bonds, provided that after the issuance of such refunding bonds, the debt service payable on allSenior Bonds outstanding after the issuance of such refunding bonds in each Bond Year shall not exceedthe debt service payable on Senior Bonds outstanding prior to the issuance of such refunding bonds ineach Bond Year. The Indenture also permits the District to enter into Senior Financial ProductsAgreements and Senior Credit Facility Obligations in connection with the Senior Bonds. As discussedelsewhere in this Official Statement, any such refunding Senior Bonds to be issued by the District will besecured by the 0.6% Sales Tax Revenues and will not be secured by the 0.4% Sales Tax Revenues.Except for refunding Senior Bonds as described in this paragraph, no securities may be issued by theDistrict that have a lien on the 0.6% Sales Tax Revenues that is superior or senior to the lien thereon ofthe Bonds.

Additional Securities

The Indenture permits the issuance, upon certain conditions, of securities having a lien upon all ora portion of the Pledged Revenues on a parity with that of the Bonds (the "Additional Parity Bonds"),provided that all of the following conditions are met and a certificate signed by the District Representativeis received by the Trustee to the effect that: (a) RTD is not in default under any provisions of the SeniorBond Resolution, the Indenture or other resolution or indenture relating to Parity Bonds as of the date ofissuance of the proposed Additional Parity Bonds; and (b) during 12 consecutive calendar months of the18 calendar months next preceding the authentication and delivery of the proposed Additional ParityBonds, the Sales Tax Revenues, including any estimated revenues which would have been receivedduring said 12-month period from additional Sales Taxes imposed during said 12-month period, andcertain investment proceeds were at least equal to 200% of the Combined Maximum Annual Debt ServiceRequirements of the Senior Bonds, the Bonds, the outstanding Parity Bonds, and the proposed AdditionalParity Bonds. The Indenture sets forth the mechanics and assumptions to be applied in the case ofvariable rate bonds and Financial Products Agreements for purposes of the computations required prior to

-15-

the issuance of Additional Parity Bonds. See Appendix E – "SUMMARY OF CERTAIN PROVISIONSOF THE INDENTURE." The District expects to issue Additional Parity Bonds in late 2013 as describedin "DEBT STRUCTURE OF RTD."

The District may enter into Parity Credit Facility Obligations and Parity Financial ProductsAgreements relating to the Bonds, any Parity Bonds and any Additional Parity Bonds without satisfyingthe above conditions and solely as is determined by the Board to be in the best interest of the District andin accordance with the provisions of the Act and the Constitution and laws of the State; provided that notermination payment required under any such Parity Financial Products Agreements shall be secured by alien on the Pledged Revenues that is senior to or on a parity with the lien thereon of the Bonds.

The Indenture also provides that the District may issue Additional Parity Bonds for the purpose ofrefunding less than all of the Bonds and other Parity Bonds without satisfying the conditions set forth insubparagraph (b) set forth on the preceding page, provided that the debt service payable on all Bonds andother Parity Bonds outstanding after the issuance of such Additional Parity Bonds in each Bond Yeardoes not exceed the debt service payable on all Bonds and other Parity Bonds outstanding prior to theissuance of such Additional Parity Bonds in each Bond Year. See Appendix E – "SUMMARY OFCERTAIN PROVISIONS OF THE INDENTURE."