© UPU 2011 – Tous droits réservés © UPU 2014 – All rights reserved Role and potential of Mobile technologies for Postal Financial Inclusion Alexandre Berthaud – «Financial Inclusion Program Manager» (DCDEV.PARFISD)

Role and potential of mobile technologies for postal financial inclusion

Jul 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© UPU 2011 – Tous droits réservés © UPU 2014 – All rights reserved

Role and potential of Mobile

technologies for Postal

Financial Inclusion

Alexandre Berthaud – «Financial Inclusion Program Manager» (DCDEV.PARFISD)

© UPU 2014 – All rights reserved

Digitize or die?

© UPU 2014 – All rights reserved

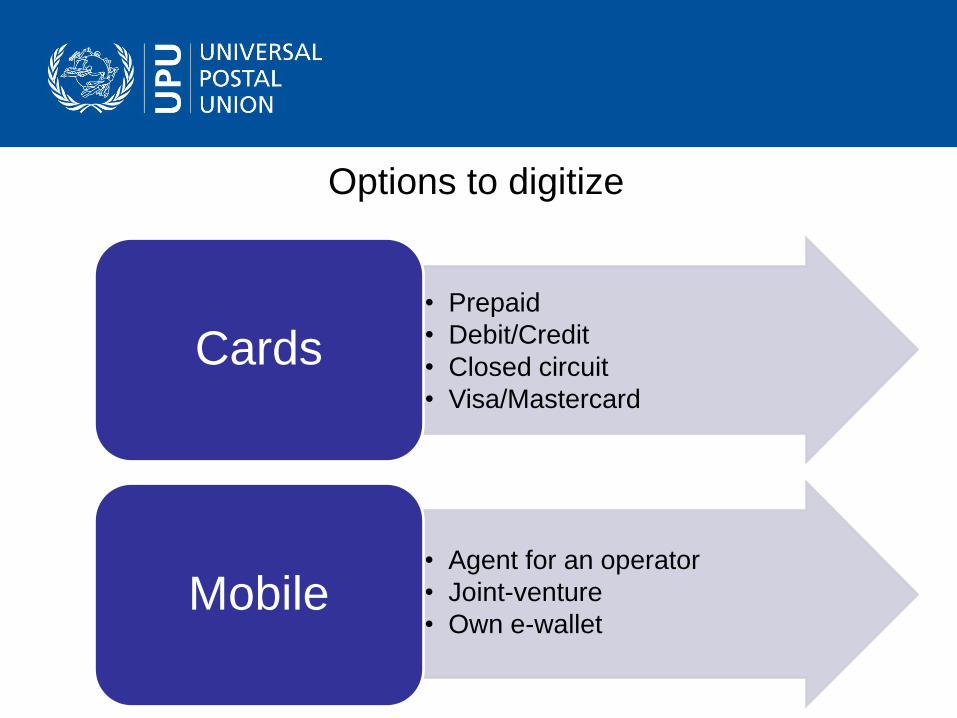

Options to digitize

• Prepaid

• Debit/Credit

• Closed circuit

• Visa/Mastercard

Cards

• Agent for an operator

• Joint-venture

• Own e-wallet Mobile

© UPU 2014 – All rights reserved

Options to digitize

© UPU 2014 – All rights reserved

Options to digitize

© UPU 2014 – All rights reserved

Options to digitize

© UPU 2014 – All rights reserved

Options to digitize

© UPU 2014 – All rights reserved 8

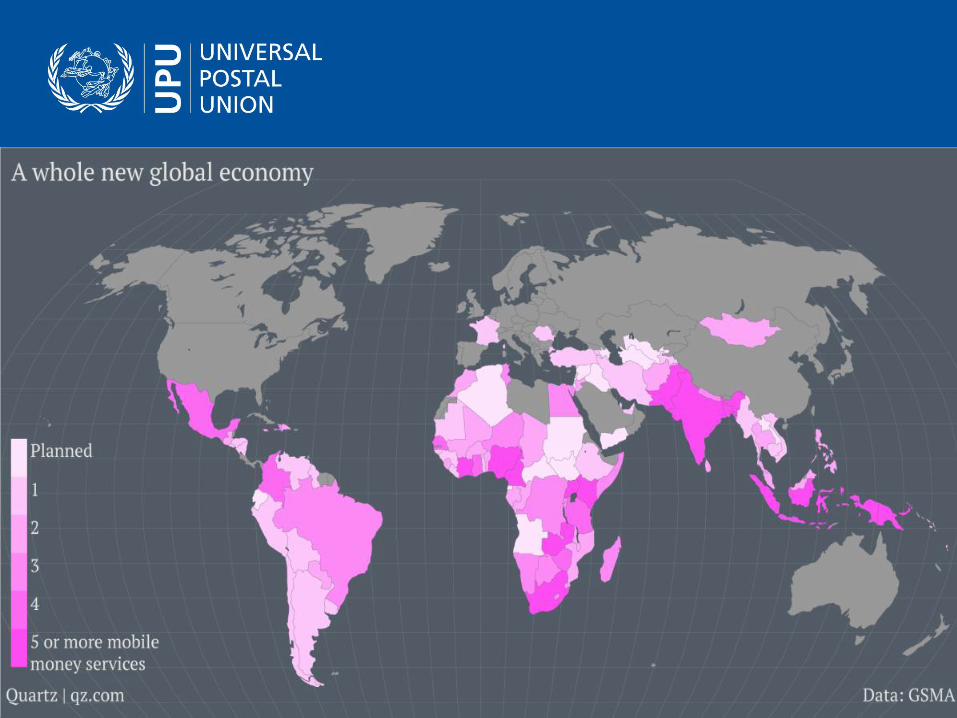

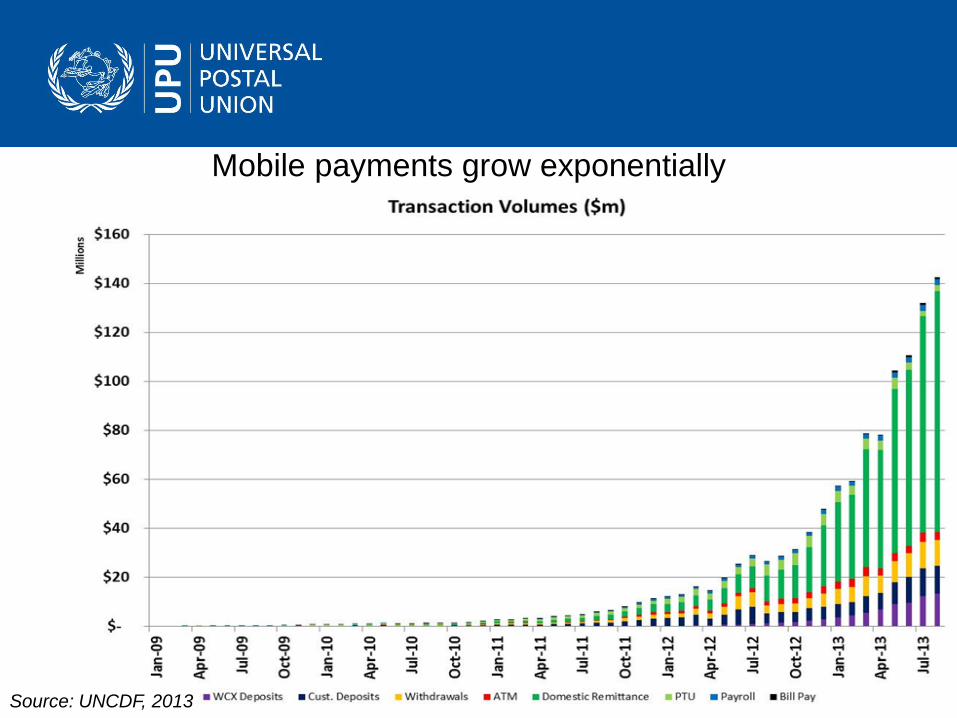

Mobile payments grow exponentially

Source: UNCDF, 2013

© UPU 2014 – All rights reserved

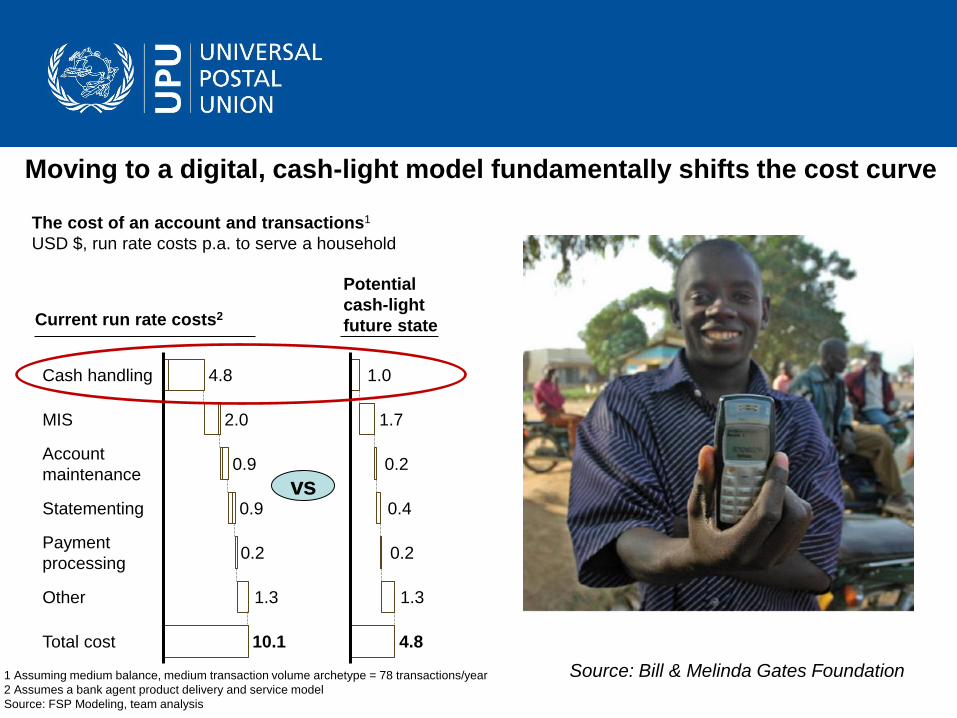

Moving to a digital, cash-light model fundamentally shifts the cost curve

1 Assuming medium balance, medium transaction volume archetype = 78 transactions/year

2 Assumes a bank agent product delivery and service model

Source: FSP Modeling, team analysis

Total cost 10.1

Other 1.3

Payment

processing 0.2

Statementing 0.9

Account

maintenance 0.9

MIS 2.0

Cash handling 4.8

Current run rate costs2

Potential

cash-light

future state

0.2

4.8

1.3

0.4

0.2

1.7

1.0

The cost of an account and transactions1

USD $, run rate costs p.a. to serve a household

vs

Source: Bill & Melinda Gates Foundation

© UPU 2014 – All rights reserved 1

0

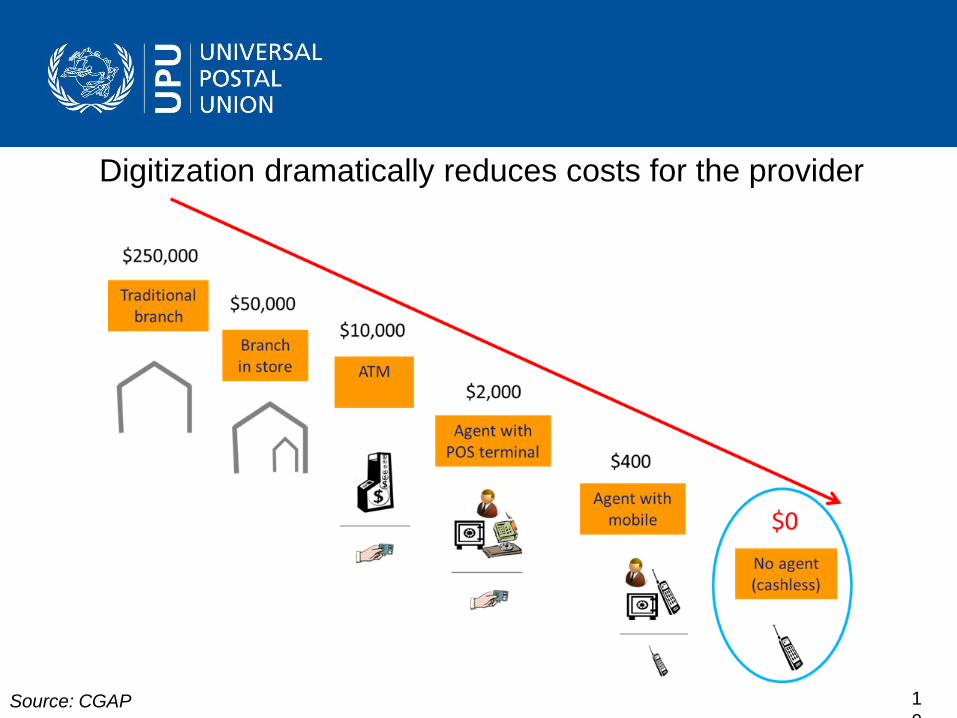

Digitization dramatically reduces costs for the provider

Source: CGAP

© UPU 2014 – All rights reserved 1

1

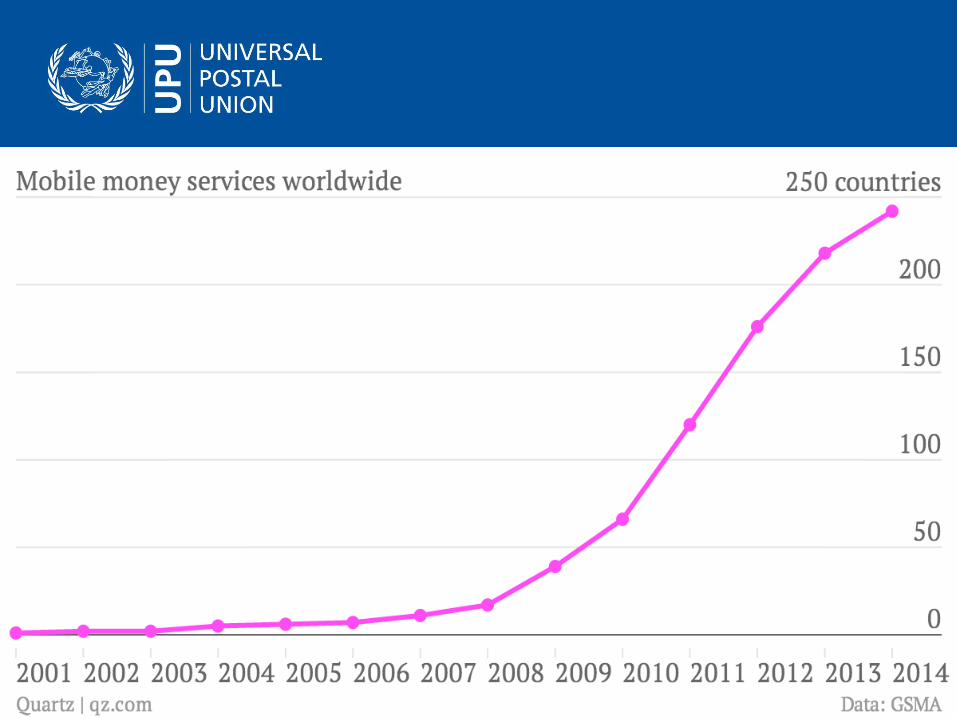

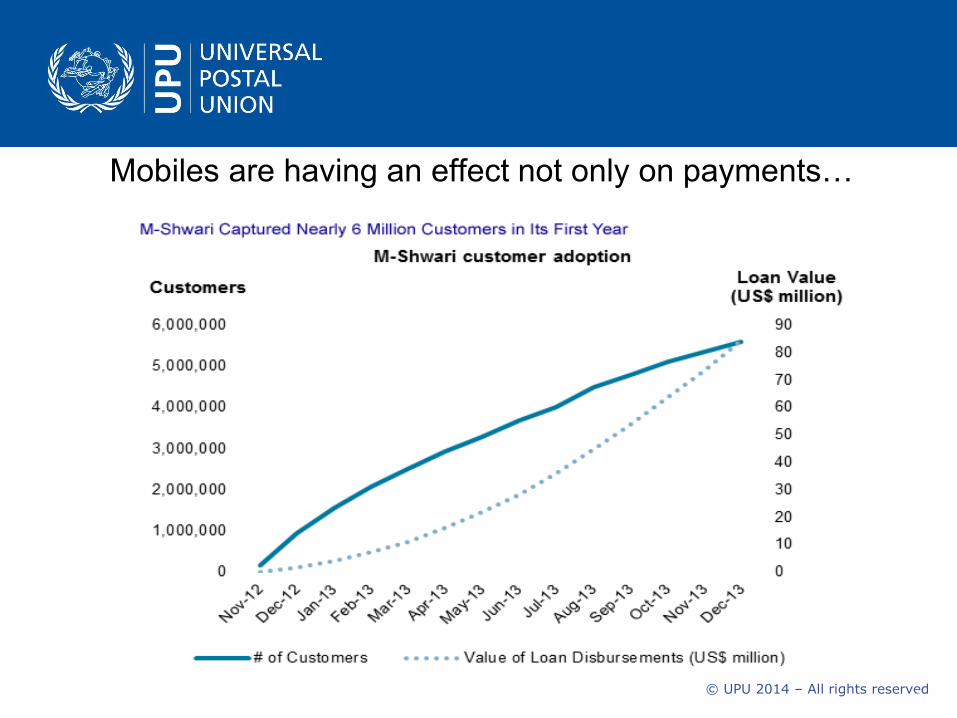

Mobiles are having an effect not only on payments…

© UPU 2014 – All rights reserved 1

2

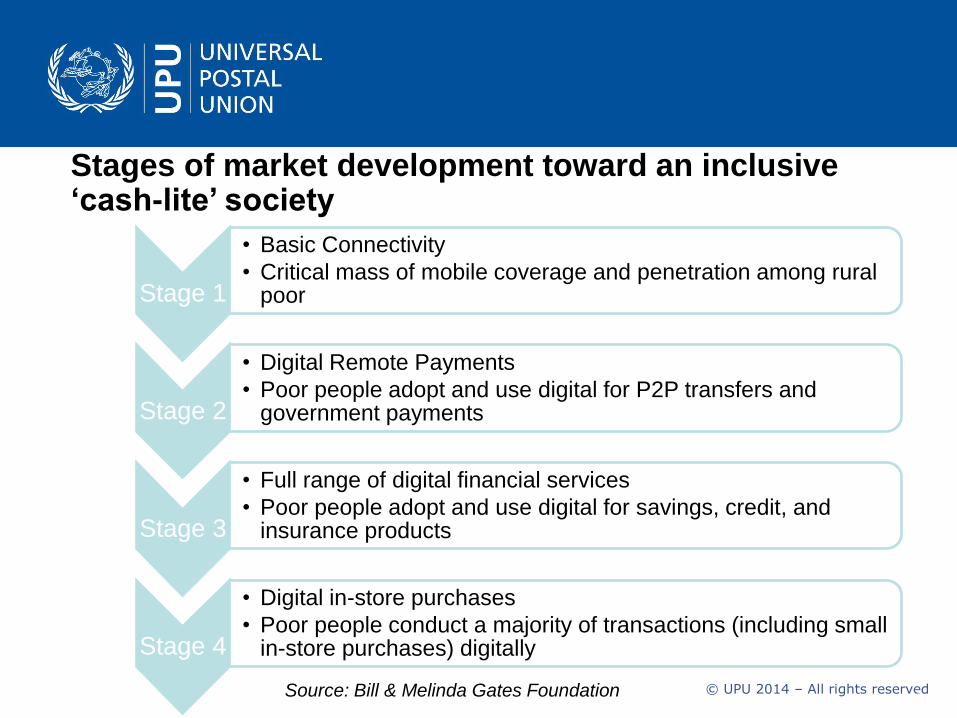

Stages of market development toward an inclusive ‘cash-lite’ society

Stage 1

• Basic Connectivity

• Critical mass of mobile coverage and penetration among rural poor

Stage 2

• Digital Remote Payments

• Poor people adopt and use digital for P2P transfers and government payments

Stage 3

• Full range of digital financial services

• Poor people adopt and use digital for savings, credit, and insurance products

Stage 4

• Digital in-store purchases

• Poor people conduct a majority of transactions (including small in-store purchases) digitally

Source: Bill & Melinda Gates Foundation

© UPU 2014 – All rights reserved

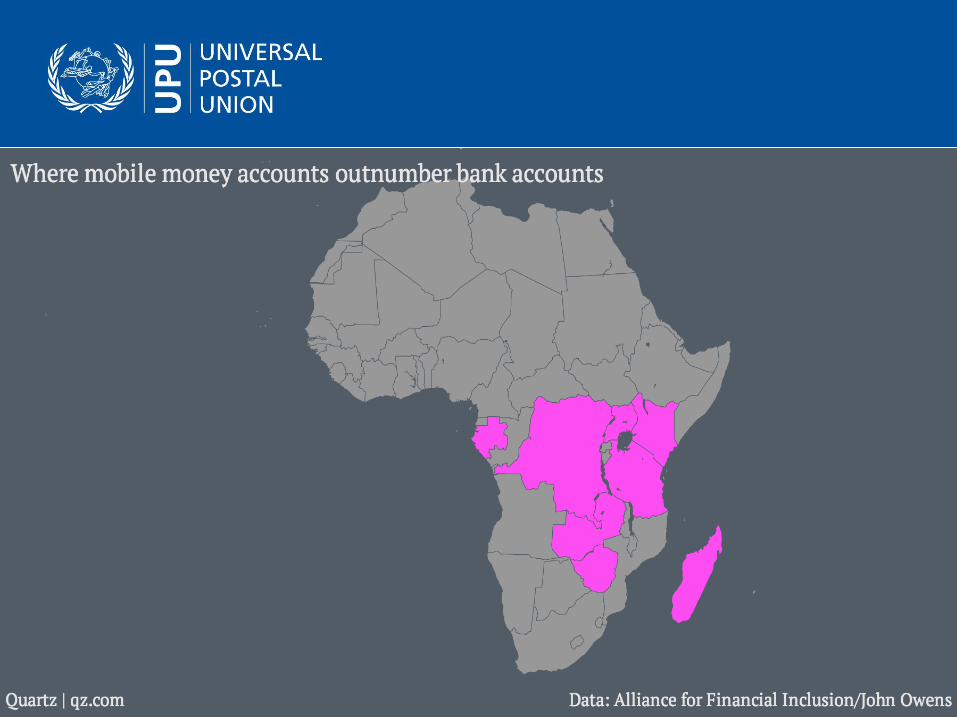

Mobile money and the Post

© UPU 2014 – All rights reserved

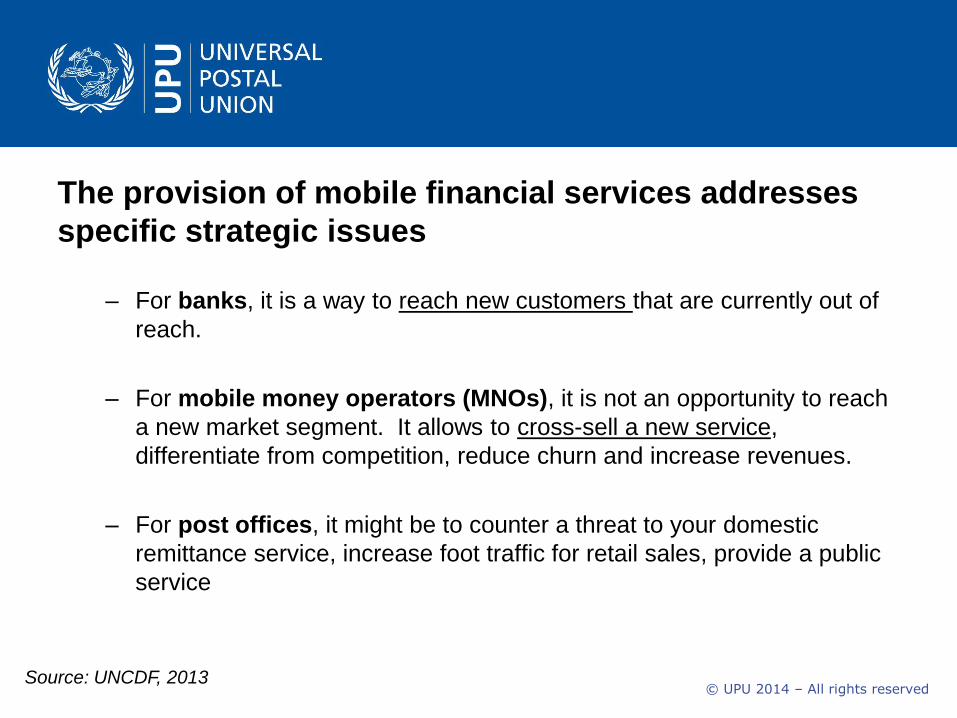

The provision of mobile financial services addresses

specific strategic issues

– For banks, it is a way to reach new customers that are currently out of

reach.

– For mobile money operators (MNOs), it is not an opportunity to reach

a new market segment. It allows to cross-sell a new service,

differentiate from competition, reduce churn and increase revenues.

– For post offices, it might be to counter a threat to your domestic

remittance service, increase foot traffic for retail sales, provide a public

service

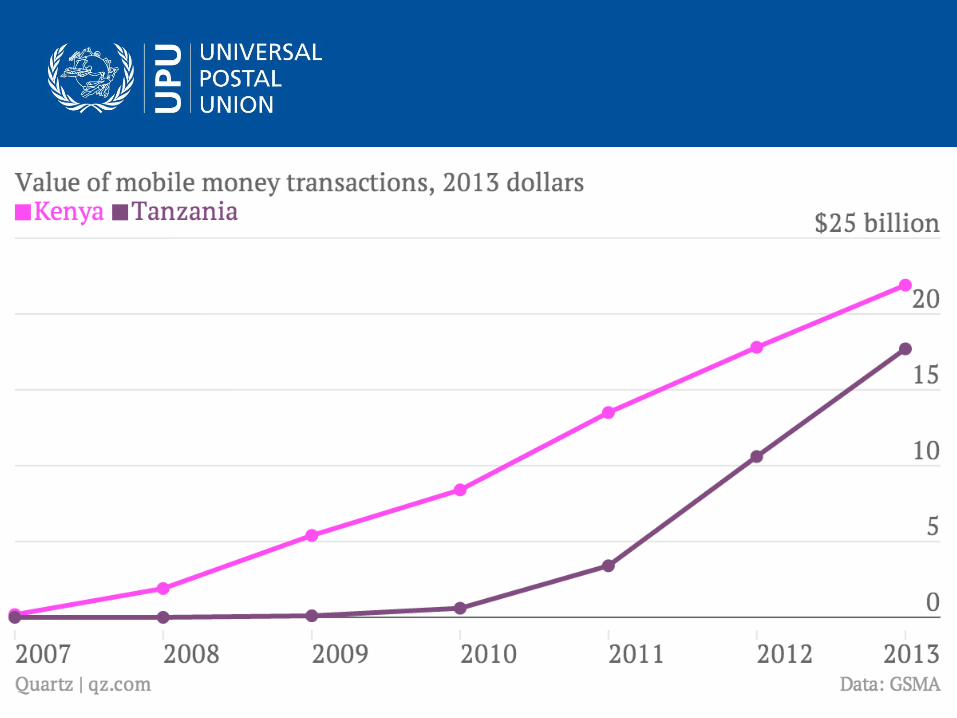

Source: UNCDF, 2013

© UPU 2014 – All rights reserved

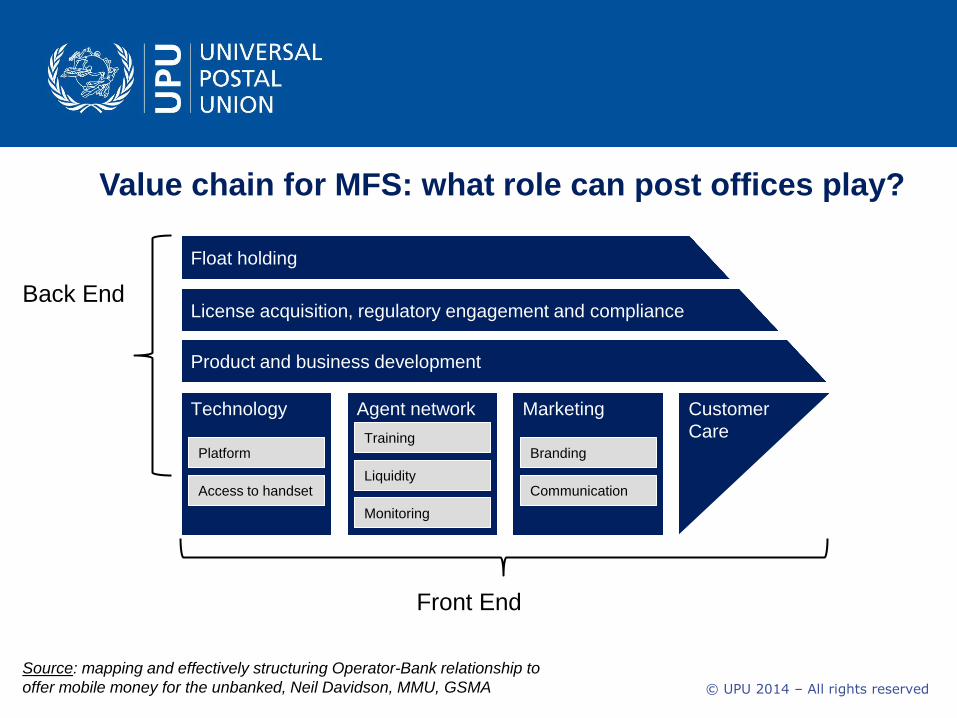

Float holding

License acquisition, regulatory engagement and compliance

Product and business development

Technology Agent network Marketing Customer

Care Platform

Access to handset

Training

Liquidity

Monitoring

Branding

Communication

Front End

Back End

Value chain for MFS: what role can post offices play?

Source: mapping and effectively structuring Operator-Bank relationship to

offer mobile money for the unbanked, Neil Davidson, MMU, GSMA

© UPU 2014 – All rights reserved

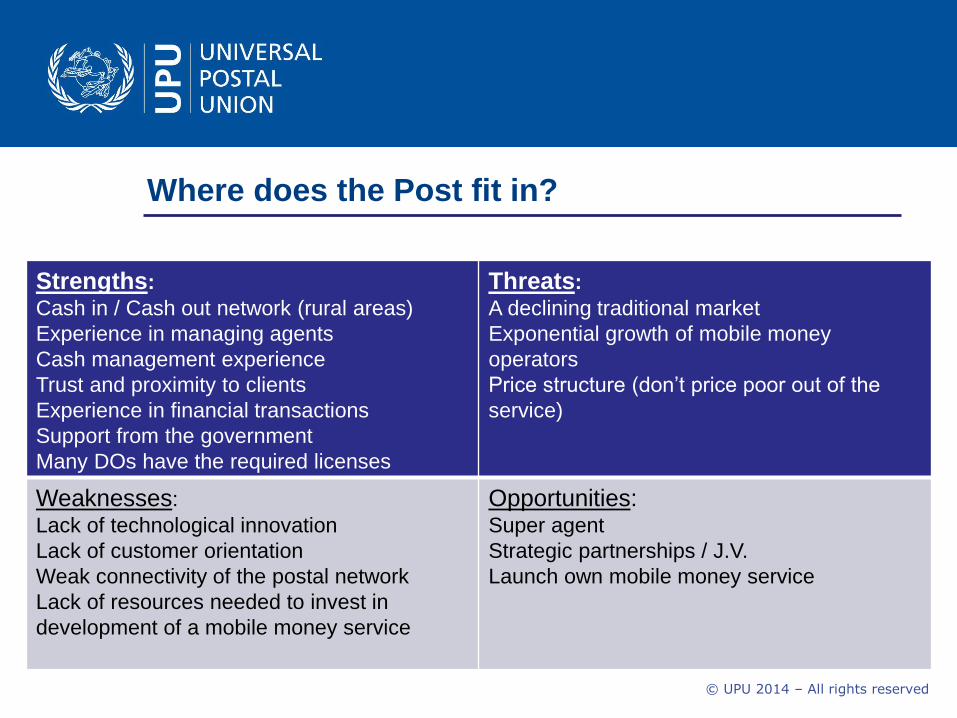

Where does the Post fit in?

Strengths:

Cash in / Cash out network (rural areas)

Experience in managing agents

Cash management experience

Trust and proximity to clients

Experience in financial transactions

Support from the government

Many DOs have the required licenses

Threats:

A declining traditional market

Exponential growth of mobile money

operators

Price structure (don’t price poor out of the

service)

Weaknesses:

Lack of technological innovation

Lack of customer orientation

Weak connectivity of the postal network

Lack of resources needed to invest in

development of a mobile money service

Opportunities: Super agent

Strategic partnerships / J.V.

Launch own mobile money service

© UPU 2014 – All rights reserved

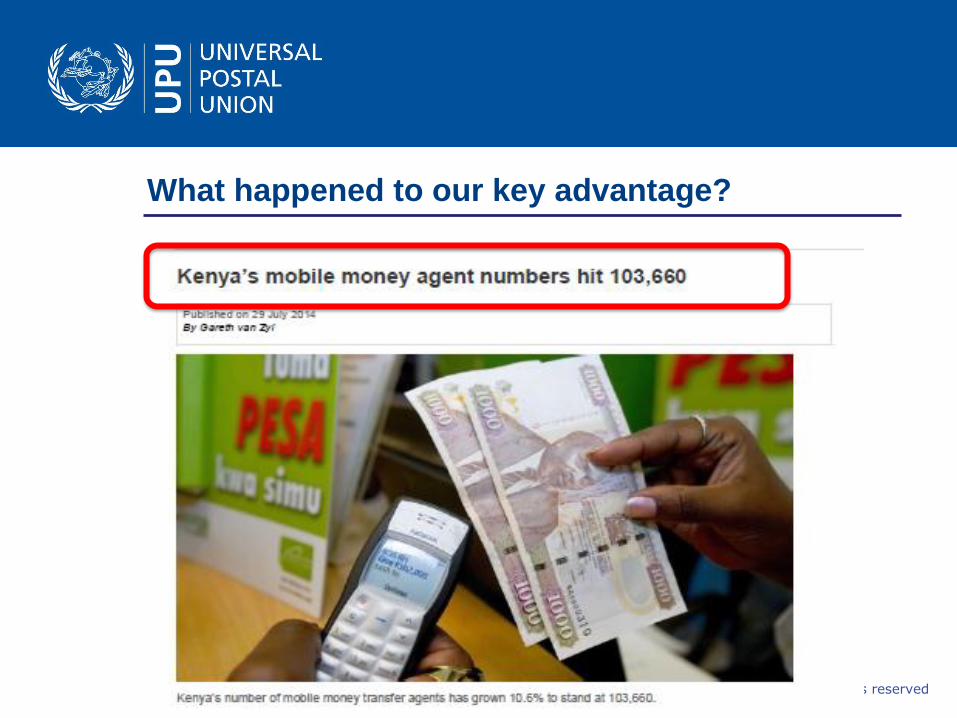

What happened to our key advantage?

© UPU 2014 – All rights reserved

Business Models for

Mobile Postal Financial Inclusion

© UPU 2014 – All rights reserved

• Use mobile technologies to modernize domestic money orders and

connect post offices in rural areas

Business Model A : Connecting POs with Mobiles

© UPU 2014 – All rights reserved

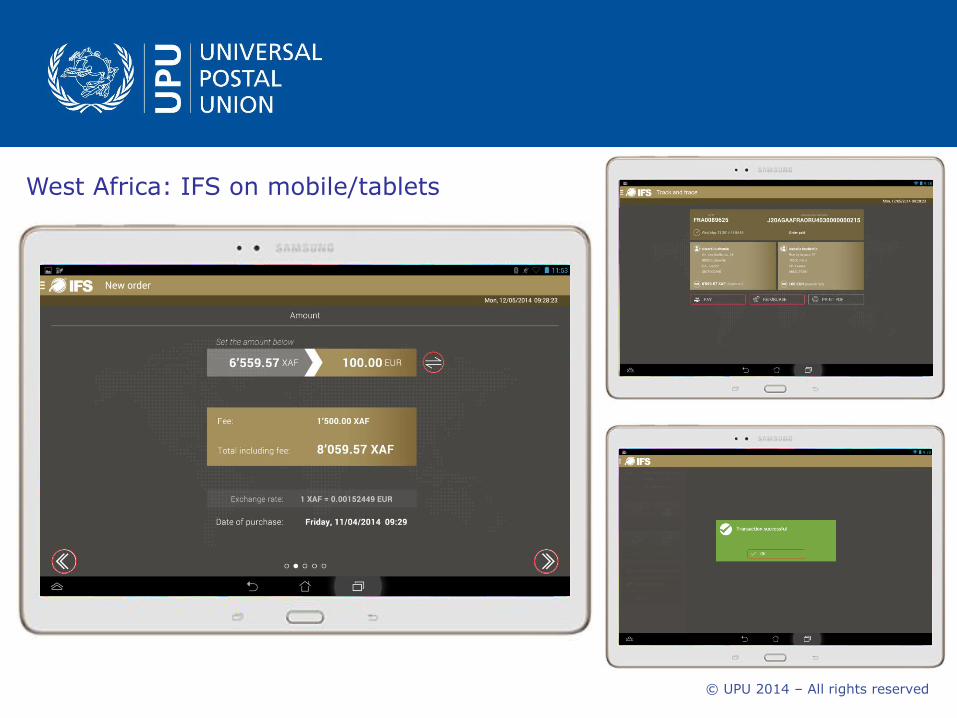

West Africa: IFS on mobile/tablets

© UPU 2014 – All rights reserved

• The Post acts as a cash-merchant for an MNO who wants to

leverage the postal network

• Issue: low fees, high cost

Business Model B : Cash-merchant for mobile

money

© UPU 2014 – All rights reserved

• First mobile money operator in the country

(2009)

• In 2011, 49,000 transactions performed

• Available in post offices + Ecocash agents

• High level of financial exclusion

• 130 post offices (biggest network in the

country)

Burundi: ECOCASH (Partnership between Econet

and Burundi Post)

© UPU 2014 – All rights reserved

• The Post teams up with a mobile operator by bringing the network

and people’s trust

• Shared revenues

Business Model C : Partnership with one/several

Mobile Network Operator

© UPU 2014 – All rights reserved

Service launched in partnership with Tunisiana, Tunisie Telecom, and

Orange launched in 2012 for e-Dinar SMART card holders and mobile

subscribers of the partners

Tunisia: multiple partners

© UPU 2014 – All rights reserved

• The Post builds its own platform that uses MNOs only as pipelines

• Independence to develop its own products

Business Model D : Own Platform independent of

Mobile Network Operators

© UPU 2014 – All rights reserved

• The Post develops its own MNO by leveraging the network of the

Operator

• Allows to link it to Postal financial services

Business Model E :

© UPU 2014 – All rights reserved

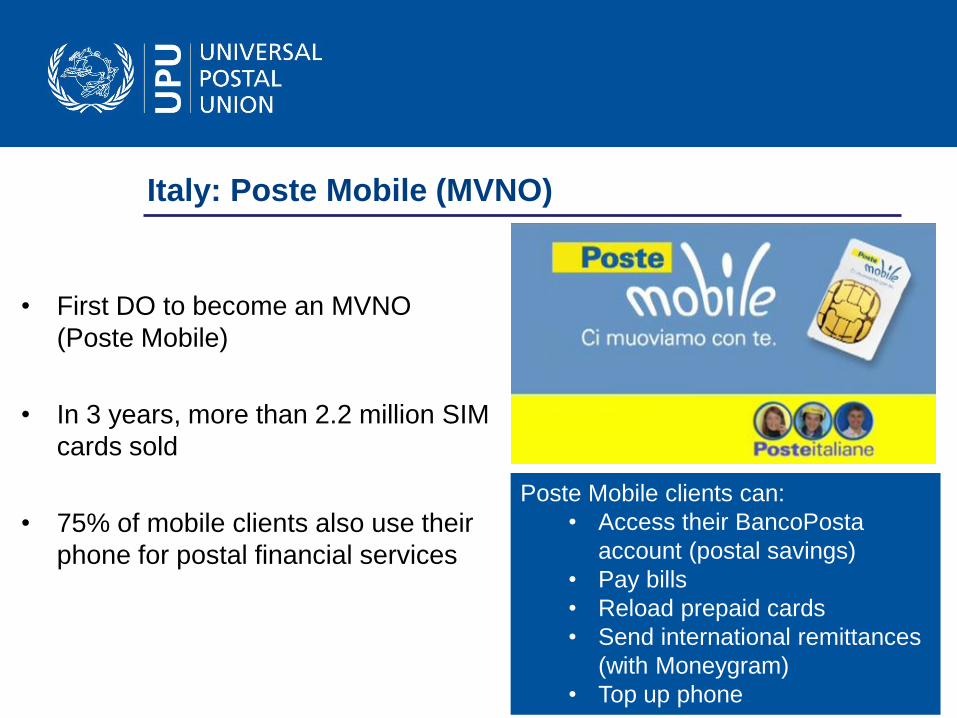

• First DO to become an MVNO

(Poste Mobile)

• In 3 years, more than 2.2 million SIM

cards sold

• 75% of mobile clients also use their

phone for postal financial services

Poste Mobile clients can:

• Access their BancoPosta

account (postal savings)

• Pay bills

• Reload prepaid cards

• Send international remittances

(with Moneygram)

• Top up phone

Italy: Poste Mobile (MVNO)

© UPU 2014 – All rights reserved

What are the challenges?

© UPU 2014 – All rights reserved

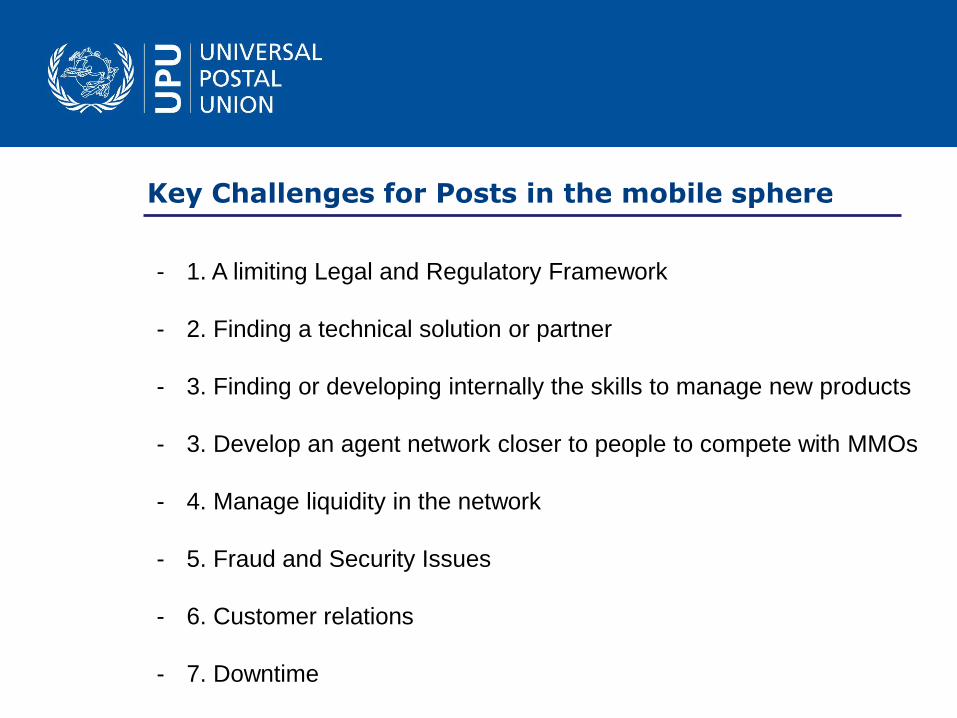

- 1. A limiting Legal and Regulatory Framework

- 2. Finding a technical solution or partner

- 3. Finding or developing internally the skills to manage new products

- 3. Develop an agent network closer to people to compete with MMOs

- 4. Manage liquidity in the network

- 5. Fraud and Security Issues

- 6. Customer relations

- 7. Downtime

Key Challenges for Posts in the mobile sphere

© UPU 2014 – All rights reserved

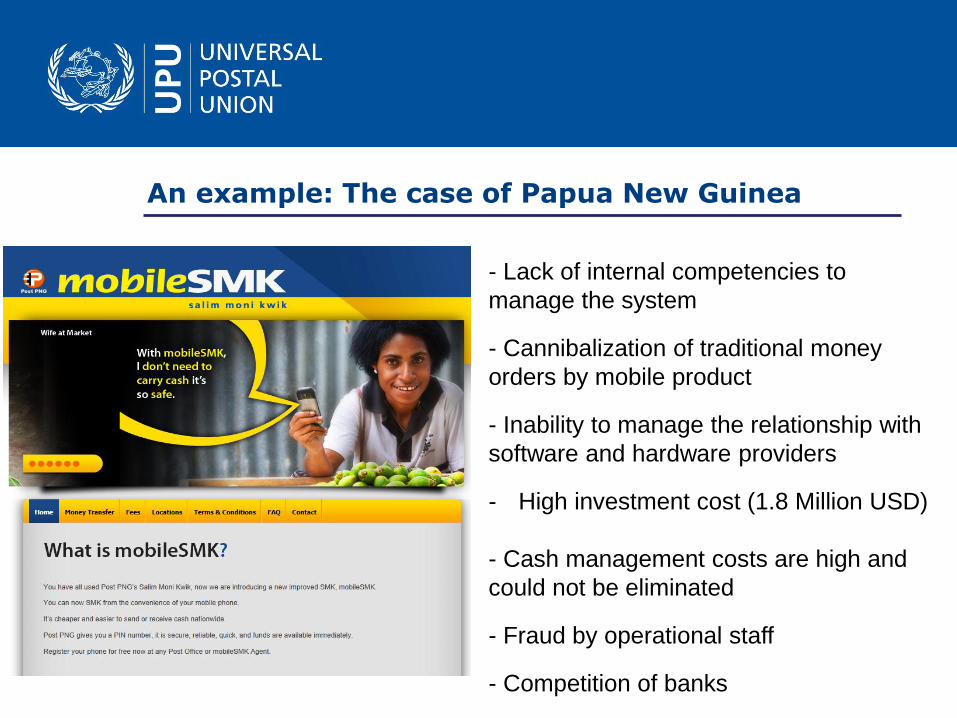

- Lack of internal competencies to

manage the system

- Cannibalization of traditional money

orders by mobile product

- Inability to manage the relationship with

software and hardware providers

- High investment cost (1.8 Million USD)

- Cash management costs are high and

could not be eliminated

- Fraud by operational staff

- Competition of banks

An example: The case of Papua New Guinea

© UPU 2014 – All rights reserved

Conclusions

Mobile money is a growing force that needs to be reckoned with

Postal operators have to carefully consider their strategy to enter this market

Partnerships have to be developed: balance needs to be established between sticking to one’s core competencies and the expected profitability

Coordination between telecoms/postal regulators and central banks is fundamental to ensure growth of the service

Related Documents