Robert McFarlane EVP & Chief Financial Officer Toronto September 11, 2003

Robert McFarlane EVP & Chief Financial Officer Toronto September 11, 2003.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Robert McFarlaneEVP & Chief Financial Officer

TorontoSeptember 11, 2003

2

This presentation and answers to questions contain forward-looking statements about expected future events and financial and operating results that are subject to risks and uncertainties. TELUS’ actual results, performance, or achievement could differ materially from those expressed or implied by such statements. For additional information on potential risk factors, see TELUS’ Annual Information Form, and other filings with securities commissions in Canada and the United States.

TELUS disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

All dollars in C$ unless otherwise specified.

forward-looking statement

3

about TELUS

Leading Canadian pure-play, facilities-based, full-service telecom provider

2nd largest Canadian telco

2003E: Revenues $7.1 to 7.2B

EBITDA $2.75 to 2.85B

FCF $800M to 1B

Enterprise value: ~$17B (equity ~$9B)

Listings: TSX: T, T.A; NYSE: TU

Operating segments: Communications = wirelineMobility = wireless

Executing national growth strategy focused on data, IP & wireless from position of financial strength

4

Communications segment

ILEC: full service in W. Canada and E. Quebec Non-ILEC: focus on data & IP for business in Central Canada

Revenue (2003E) $4.85 to 4.9B

EBITDA (2003E) $2.0 to 2.075B

POPs covered 7.5M

Network Access Lines 4.9M

Local/LD Market Share 96%/78%

Total Internet Subscribers 821K (469K high-speed)

Fibre IP backbone national

Strategic alliance Verizon Communications

5

Mobility segment

31.5M: Cdn. PopulationLicensed POPs

28.3M (90%)Network coverage

Verizon Wireless & NextelStrategic relationships

best in CanadaSpectrum position

only one in CanadaiDEN Mike network

coast to coast 1XCDMA footprint

$750 to 775MEBITDA (2003E)

$2.25 to 2.3BRevenue (2003E)

3.2MSubscribers

Leading Canadian national wireless provider

6

2003 YTD review – consolidated

significant growth in profitability driven by excellent wireless performance & wireline efficiencies

1 Excludes YTD payments under restructuring & workforce reduction initiatives of $202M & $77M for 2003 and 2002, respectively

148M$166M$18MNet Income

$0.42

$0.46$0.04EPS

2.0%$3.51B$3.45BRevenue

15%$1.39B$1.21BEBITDA1

YTD Q2-03 changeYTD Q2-02

7

strong margin expansion evident across both business segments

2003 YTD review – EBITDA margin

38%

26%

34%

41% 40%35%

June YTD EBITDA Margin (total revenue)

Communications ConsolidatedMobility2002 2003 2002 2003 2002 2003

8

2003 YTD review – consolidated

1 Ratio of capex to total revenues

2 EBITDA less capex, cash interest, cash taxes, cash dividends; excludes YTD payments under restructuring & workforce reduction initiatives of $202M & $77M for 2003 and 2002, respectively.

over $600M improvement in free cash flow generation

$606M$445M($161M)Free Cash Flow2

13pts15%28%Capex Intensity1

46%$513M$955MCapex

YTD Q2-03 changeYTD Q2-02

9

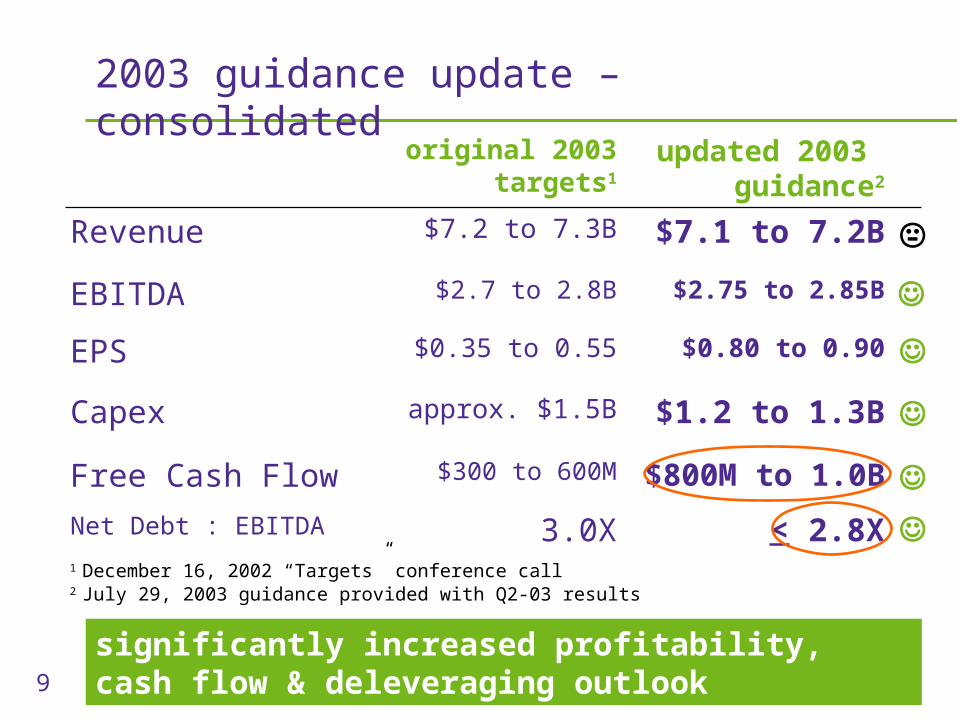

2003 guidance update – consolidated

significantly increased profitability, cash flow & deleveraging outlook

$1.2 to 1.3Bapprox. $1.5BCapex

$800M to 1.0B

$0.80 to 0.90

$2.75 to 2.85B

$7.1 to 7.2B

updated 2003 guidance2

$300 to 600M

$0.35 to 0.55

$2.7 to 2.8B

$7.2 to 7.3B

original 2003 targets1

EPS

Free Cash Flow

EBITDA

Revenue

< 2.8X3.0XNet Debt : EBITDA1 December 16, 2002 “Targets” conference call2 July 29, 2003 guidance provided with Q2-03 results

10

revised 2003 financial outlook – consolidated

2003 guidance implies significant improvement in profitability, cash flow & leverage

$1.2 to 1.3B$1.7BCapex

$800M to 1.0B

$0.80 to 0.90

$2.75 to 2.85B

$7.1 to 7.2B

updated 2003 guidance

($26M)

($0.75)

$2.5B

$7.0B

2002 actuals

EPS

Free Cash Flow

EBITDA

Revenue

< 2.8X3.3XNet Debt : EBITDA

change

0.5X

$400 to 500M

$826M to 1.0B

$1.55 to 1.65

9 to 13%

1 to 3%

11

2003E revenue

2003E EBITDA

ILEC (4%) (1%)

Non-ILEC 9% 72%

Total Communications (2%) 3%

Mobility 13% 43%

Consolidated 2% 11%

2003 implied YoY growth by segment1

latest 2003 guidance implies consolidated revenue & EBITDA growth of 2% & 11%, respectively

1 Uses midpoint of Management guidance for 2003

12

strategic imperatives 2000-2003

Provide integrated solutions

Partner, acquire & divest as necessary

Invest in internal capabilities

Build national capabilities

Focus on growth markets

Going to market as one team

13

build national capabilities

TELUS national infrastructure – 2000

14

build national capabilities

TELUS’ national infrastructure - 2003

15

$5.7B

43%

18%

10%

6%Other

12ME Q2-03

$7.1B

Local Voice

Wireless

Data31%

31%

19%

5%Other

LD

Wireless

12ME Q2-00

Local Voice

23%

Data

14%

LD

TELUSCommunications

TELUSCommunications

TELUSMobility

TELUSMobility

voice focused balanced with growth

focus on growth markets

consolidated revenue profile evolution

16

going to market as one team

strong brand identity established

consistent branding across TELUS

17

18

19

20

2003 corporate priorities

1. Delivering operational efficiency

2. Enhancing wireless performance

3. Improving Central Canada profitability

4. Strengthening financial position

5. Driving improved levels of customer service

6. Reaching a collective agreement

On track?

in progress

deferred Feb/04

21

Achieved $199M in OEP savings YTD 2003

Cumulative annual savings of $349M to June 30, 2003

On track for cumulative savings of $450M in 2003

Cumulative 2004 estimated annual target of $550M

June 2003Actual

2003E

6,500

6,050Staff Reductions

driving $300M in incremental cost reductions in 2003

delivering operational efficiency

operational efficiency program (OEP)

22

TELUS Mobility

Rogers AT&T

BCE Wireless

Microcell

$54

$39$44$45

enhancing wireless performance

continued leadership in ARPU

Source: Company reports

YTD Q2-02

YTD Q2-03 $55

$46$46

$38

significant premium to closest competitor maintained

23

enhancing wireless performance

leading performance in churn

BCE Cingular

2.4%

2.2%

1.6%

2.2%1.7%

1.4% 1.3%

TELUSVerizonAT&T Rogers Nextel

3.3%

SprintPCS

Microcell

3.0%2.6%

T-Mobile

TELUS’ Q2 churn rate is best-in-class

24

enhancing wireless performance

YTD market share of wireless net additions1

Bell

Rogers AT&T

TELUS Mobility34%Other

TELUS Mobility continues to capture healthy share of industry net additions

Aliant

1 Excludes Microcell subscriber losses, and Rogers Wireless’ Q2-03 prepaid adjustmentSource: Company reports, and analyst estimates

25

enhancing wireless performance

how does TELUS Mobility measure up?

Sources: TELUS estimates. Cdn. Statistics - Company Reports; US Statistics - Morgan Stanley1 Projected capex as a % of forecast total revenue. 2 Projected EBITDA less projected Capex divided by projected network revenues

3 Projected wireless penetration gain divided by # of carriers in market. For TELUS, projected net adds divided by projected covered POPs

0.5%0.9%1.2%Penetration gain/carrier3

6 to 83 to 4-No. of carriers in market

53%41%12%Mkt penetration/cov. POPs

11%9%19%(EBITDA – Capex) / net. rev2

21%17%17%Capex intensity1

18%28%43%Annual EBITDA growth rate

33%32%37%EBITDA / network rev.

US Avg 2003

Cdn Avg 2003

TM 2003 guidance

TELUS Mobility is best-in-class operating in a strong 3+ player Canadian wireless industry

26

non-ILEC traction with 7 consecutive quarters of EBITDA improvement

improving Central Canada profitability

non-ILEC revenue and EBITDA

17 16 2031 38

60

105

133117 123

136152

141 139

(6)(23)(30)(36)(37)

(11)(24) (28) (33) (35) (36) (38) (18) (15)

Q1-00 Q2-00 Q3-00 Q4-00 Q1-01 Q2-01 Q3-01 Q4-01 Q1-02 Q2-02 Q3-02 Q4-02 Q1-03 Q2-03

Revenue EBITDA

27

reaching a collective agreement

labour relations update

Federal conciliators announced conclusion of global review between TELUS & the TWU on July 16

60-day negotiating period to begin Nov. 14 with exchange of written proposals

If agreement not reached at end of 60-day period, 21-day ‘cooling off’ period will follow

Process not expected to conclude until early Feb/04

TELUS committed to reaching agreement that balances the needs of all parties

strengthening financial position credit profile

29

TELUS debt structure simplified with 86% of total debt now at TELUS Corporation

Average term to maturity ~6.4 years1

Modest long-term debt maturities until 2006

$499M bank borrowings1 expected to gradually decrease and be paid off by Q1-04

Fixed to floating ratio currently conservative 95%

Foreign currency debt is fully hedged

credit profile

debt overview

1 As at June 30, 2003

30

credit profile

March 2001 – prior to re-organizations

TELUS Corporation (TC)

Tranche A3 $5.0B - 89% utilizedTranche B3 $1.25B - undrawn4

Commercial Paper $0.02B

Interco Notes from subsidiaries $3.15B

612459 B.C. Ltd.

•Upstream guarantees supporting TC

Clearnet Communications Inc (CCI)

•Sr. Discount Notes $1.744B•Interco Notes to TC $0.089B

1 Condensed organizational chart showing only those companies material to the Bank financing. 2 TC, TCI and 612459 B.C. Ltd. provide, where applicable, pledge of shares, upstream guarantees, and assignment of inter-company notes.3 Bank Tranches were secured.4 Tranche B includes notional CP backup of $1.0 B and outstanding L.C.’s at March 31, 2001 of $100 M.

Clearnet PCS Inc. (CPI)

•Interco Notes to TC $0.658B

Clearnet Inc. (CI)

•Interco Notes to TC $0.297B

TELUS Communications Inc. (TCI)

•Upstream guarantees supporting TC•MTN’s•Debentures•Capital leases $0.027B•Commercial Paper $0.974B•Interco Notes to TC $2.106B•Pref. Shares issued to public $0.07B

$1.395B

100%

TELUS Québec

•MTN’s•Mortgage Bonds•Bank- $0.06B

70%

$0.13B

31

Re-organized legal structure to align with business operations and access Clearnet tax losses

Mobility business consolidated into TELE-MOBILE Company partnership in 2001

2002 wind-up of Clearnet Inc. into TELUS Communications Inc. (TCI)

made additional losses available - no cash income taxes payable until 2007

tax-effected loss carryforwards recognized for accounting ~$766M at year-end 2002

credit profile

corporate reorganization activity

32

TELUS Corporation

MaturityBank 1 -Tranche A $1.5B revolver May 2004 -Tranche B $0.6B revolver May 2004C$ 7.5% Notes $1.6B June 2006US$ 7.5% Notes $1.6B June 2007US$ 8.0% Notes $2.6B June 2011

1 At June 30, 2003, Tranche A had outstandings of $499M and Tranche B was undrawn

TELUS Communications Inc.

•MTN’s $0.020B•Debentures $0.988B•Net Sr. Notes to TC $2.3B

TELUS Québec

•Mortgage Bonds $0.030B•MTNs $0.070B

100%

credit profile

June 2003 – post re-organizations

33

Debt Maturity Schedule*

0500

1000150020002500

30003500

H2-03 2004 2005 2006 2007 2008 2009 2010 2011 2012+

C$ millions

* Includes drawn bank credit facilities outstanding at June 30, 2003 of $499 million

credit profile

debt structure - maturities

Bank Facility

34

credit profile

364-day renewal

Renewed $600M 364-day credit facility portion in May 2003

back-up facility

not projected to draw upon

Combined bank facilities now $2.1B

No material changes to terms

New maturity date May 2004 with TELUS option to term-out to May 2005

TELUS’ liquidity position expected to remain >$1B

35

credit profile

credit rating environment

Rating agencies have ‘raised the bar’ post-Enron

proactive orientation with negative bias generally

criticism of agencies (AT&T Canada, WorldCom, Microcell)

telco industry risk premium increased

rating methodology changed/not transparent

time horizon shortened

FCF focus

credit rating committee process & benchmarks became less transparent

36

credit profile TELUS yield spread analysis (1 of 2)

0%

5%

10%

15%

20%

25%

30%

24-M

ay-

01

24-J

un-0

1

24-J

ul-01

24-A

ug-0

1

24-S

ep-0

1

24-O

ct-0

1

24-N

ov-

01

24-D

ec-

01

24-J

an-0

2

24-F

eb-0

2

24-M

ar-

02

24-A

pr-

02

24-M

ay-

02

24-J

un-0

2

24-J

ul-02

24-A

ug-0

2

24-S

ep-0

2

24-O

ct-0

2

24-N

ov-

02

24-D

ec-

02

24-J

an-0

3

24-F

eb-0

3

24-M

ar-

03

24-A

pr-

03

24-M

ay-

03

24-J

un-0

3

24-J

ul-03

24-A

ug-0

3

C$ 7.5% 2006 US$ 7.5% 2007 US$ 8.0% 2011

May 31Credit rating under review

Sep 12Equity offering & debt buyback

Jul 25Moody's downgrade

Jul 29Q2 results & increased disclosure

Jul 8DBRS downgrade

Jul 11S&P downgrade

May 2001 July 2002 Current

rating downgrades caused unprecedented dislocation remedied by results

TELUS C$ & US$ Note Yield Spread Analysis(May 24, 2001 to September 5, 2003)

37

credit profile TELUS yield spread analysis (2 of 2)

C$ 7.5% 2006 US$ 7.5% 2007 US$ 8.0% 2011

Issue Spread 200 bps 243 bps 268 bps May 24, 2001

Peak Spread 1,746 bps 2,826 bps 2,098 bps July 25-26, 2002

Current Spread 176 bps 200 bps 213 bps September 5, 2003

Current Price 106.41 107.75 110.32 September 5, 2003

Current YTM 4.95% 5.18% 6.29%

current credit spreads are below issue spreads

38

$337M equity-funded debt buyback

364-day credit facility renewed

OEP tracking to plan

3rd consecutive year heading to exceed annual profitability guidance

Significant cash tax recoveries

Significant capex reduction

Significant free cash flow generation

credit profile

what’s happened since July 2002?

deleveraging ahead of plan

39

June 2001

Actual

June 2002 Actual

June 2003 Actual

Net Debt ($M) 9,037 9,120 8,039

Net Debt : Capital 59% 59% 55%

Net Debt : EBITDA 3.8x 3.6x 3.0x

FCF1 ($M) (1,044) (692) 580

Parent debt : Total Debt2 79% 85% 86%

Subsequent Rating BBB+/Baa2 BBB/Ba1 BBB/Ba1

credit profile

demonstrated credit improvement

1 12-month trailing Free Cash Flow2 Percentage of total debt at TELUS Corp. (Parent level) - inclusive of bank facility & hedge liability

credit enhanced but rating lower

40

2001 2002

2003E

1 EBITDA less capex, cash interest, cash taxes, cash dividends; excludes restructuring & workforce reduction costs

$(1.35)B

$(26)M

$800 to 1,000M

credit profile improving free cash flow1

41

credit profile

debt reduction ahead of plan($M) original 2003

targetsrevised 2003

guidance

EBITDA1 $2,700 to 2,800 $2,750 to 2,850

Capex ~(1,500) (1,200 to 1,300)

Cash Interest ~(700) ~(630)

Net Cash Tax Recovery (25) to 175 ~165

Cash Dividends ~(175) ~(185)

Free Cash Flow $300 to 600 $800 to 1,000

Working Capital/Other ~0 ~220

Share Issuance2 (non-public) ~70 ~80

Cash Restructuring Costs ~(275) ~(300)

Cash available for debt reduction $100 to 400 $800 to 1,000

1 Before restructuring and workforce reduction costs2 Dividend reinvestment & employee share plans

42

credit profile

2003 guidance – then & now

2.9X to 3.2XOutlook @ Jul-02

$50 to 335Outlook @ Jul-02

$300 to 650Outlook @ Jul-02

2003Net debt : EBITDA

<2.8XOutlook @ Jul-03

$800 to 1,000Outlook @ Jul-03

2003Cash available for debt reduction

$800 to 1,000Outlook @ Jul-03

2003Free Cash Flow

($M)

executing ahead of plan

43

credit profile

credit rating update – changes in 2003

April 16 – Moody’s outlook to ‘stable’ from ‘negative’

May 28 – Fitch outlook to ‘stable’ from ‘negative’

June 16 – DBRS trend to ‘stable’ from ‘negative’

August 8 – S&P outlook to ‘stable’ from ‘negative’

credit ratings are lagging indicators of improvement

44

credit profile

current debt ratings

TELUS Corporation DBRS BBB Stable Trend S&P BBB Stable Outlook Fitch BBB Stable Outlook Moody’s Ba1 Stable Outlook

TELUS Communications Inc. DBRS BBB Stable Trend S&P BBB Stable Outlook Fitch BBB Stable Outlook

TELUS QuébecDBRS BBB Stable Trend S&P BBB Stable Outlook

100%

45

credit profile

BCE & TELUS credit comparison1

rating differential not supported by FCF analysis

*($M) BCE TELUS

2002A 2003E 2004E 2002A 2003E 2004E

Free Cash Flow2 $102 $1,044 $1,248 ($26) $900 $902

Free Cash Flow (less Bell West Put)2 $102 $1,044 $598 ($26) $900 $902

Net Debt $17,620 $17,009 $16,686 $8,390 $7,965 $7,224

FCF/Net Debt 0.6% 6.1% 3.6% -0.3% 11.3% 12.5%

Structure: HoldCo OpCoIssuer Credit Ratings: - Moody's Baa1 Ba1 - S&P A BBB - DBRS A BBB

3 Notch Difference

Notes:

1 Forward-looking estimates from TD securities, except TELUS' 2003E (midpoint of Management guidance); consult appendix for further detail2 Free Cash Flow (FCF) defined as EBITDA less: capex, cash interest, cash taxes and cash dividends

Sources: TD Securities; Company reports

* Disclaimer: TELUS has not yet provided 2004 guidance & does not endorse any particular analysts’ projections

46

2003 outlook leading N.A. telecom performance

11% 5%

3%

0.2%

(18)%

(11)%

TELUS BCE

Sprint

MTS

SBC AT&T

Aliant (3%) (5)%

VerizonBell

South

Projected 2003 EBITDA Growth Rates

Notes: TELUS data based on 2002 actual results & average of 2003 guidance Other 2003 estimates provided by Bloomberg and analyst estimates

(4%)

As at August 28, 2003

47

5%

SBC

Projected 2003 Cash Flow (EBITDA - Capex) Growth Rates

12% 12% 9%

22%

(15)%

(2)%

3%

89%

TELUS BCE SprintMTS BellSouth

Verizon AT&T

Aliant

Notes: TELUS data based on 2002 actual results & average of 2003 guidance Other 2003 estimates provided by Bloomberg and analyst estimates

2003 outlook

leading N.A. telecom performance

As at August 28, 2003

48

summary

Delivering on our strategy:

TELUS Communications – improving efficiencies

– non-ILEC on-track

TELUS Mobility – executing materially ahead of plan

Improved 2003 cash flow & earnings outlook

Generating significant cash flow of $800M to $1B

Continued material debt & leverage reduction

strong & improving investment-grade credit profile

questions?

appendix

52

appendix

BCE & TELUS credit comparison1,4 (1 of 2)

*

* Disclaimer: TELUS has not yet provided 2004 guidance & does not endorse any particular analysts’ projections

($M) BCE TELUS2002A 2003E 2004E 2002A 2003E 2004E

EBITDA $7,215 $7,774 $8,174 EBITDA $2,519 $2,800 $3,038 - capex $3,771 $3,285 $3,282 - capex $1,698 $1,250 $1,300 - cash interest $1,187 $1,243 $1,210 - cash interest $676 $630 $615 - cash taxes $1,042 $1,081 $1,262 - cash taxes $35 ($165) $27 - cash dividends $1,113 $1,122 $1,173 - cash dividends $136 $185 $195Free Cash Flow2 $102 $1,044 $1,248 Free Cash Flow2 ($26) $900 $902 + changes in WC/other ($934) ($210) ($106) + changes in WC/other $220 $195 ($125) - Bell West put option $0 $0 $650 + non-public share issuance $92 $80 $70

- cash restr. costs $274 $300 $90

Free Cash Flow (less Bell West Put)2 $102 $1,044 $598 Free Cash Flow (less Bell West Put)2 ($26) $900 $902

Net Free Cash Flow3 ($832) $834 $492 Net Free Cash Flow3 $12 $875 $757

Excluded: + proceeds from A/R securitization $325 $25 $0 + public share issuance $337 $0 $0

# of share O/S 940.6 940.6 940.6 # of share O/S 345.7 359.1 364.1Price (Sep 2) $30.32 $30.32 $30.32 Price (Sep 2) $26.29 $26.29 $26.29Equity value $28,519 $28,519 $28,519 Equity value $9,088 $9,441 $9,572

Net Debt $17,620 $17,009 $16,686 Net Debt $8,390 $7,965 $7,224

53

appendix

BCE & TELUS credit comparison1,4 (2 of 2)

*($M) BCE TELUS

2002A 2003E 2004E 2002A 2003E 2004E

FCF/Net Debt 0.6% 6.1% 3.6% FCF/Net Debt -0.3% 11.3% 12.5%

Net FCF/Net Debt -4.7% 4.9% 2.9% Net FCF/Net Debt 0.1% 11.0% 10.5%

Structure: HoldCo Structure: OpCoIssuer Credit Ratings: Issuer Credit Ratings: - Moody's Baa1 - Moody's Ba1 - S&P A - S&P BBB - DBRS A - DBRS BBB

Notes:

1 Forward-looking estimates from TD securities, except TELUS' 2003E (midpoint of Management guidance)2 Free Cash Flow (FCF) defined as EBITDA less: capex, cash interest, cash taxes and cash dividends3 TELUS results exclude public share issuance of $337M (2002A) & acc. rec. securitization cash proceeds of $325M (2002A) and $25M (2003E)

BCE results deduct Bell West put option of $650M in 2004E4 TD's FCF derivation modified by exchanging 'changes in working capital' for 'cash dividends'

Sources: TD Securities; Company reports

* Disclaimer: TELUS has not yet provided 2004 guidance & does not endorse any particular analysts’ projections

3 Notch Difference

54

TELUSCorporation

TELUS Communications Inc.

Senior Notes: $3.1B

Subordinated Equity Settled Note: $3.6B

appendix

intercompany financing1 (as at June 30, 2003)

Senior Note: $0.8B

Subordinate Note: $3.2B

1 Excludes net advances owed from TC to TCI of $800M at June 30, 2003.

TELUS Corporation has a net $2.3B senior claim at TCI thereby mitigating structural subordination concerns

55

appendix

TELUS Communications Inc. key metrics

June 30/02 June 30/03(12 months ended)

Net Debt : Total Capitalization 38.6% 31.6%

Net Debt : EBITDA1 2.3X 1.7X

Net Debt ($M) 5,464 4,128

1 Excludes restructuring & workforce reduction costs

Related Documents