ninth edition STEPHEN P. ROBBINS © 2007 Prentice Hall, Inc. © 2007 Prentice Hall, Inc. All rights reserved. All rights reserved. PowerPoint Presentation by Charlie PowerPoint Presentation by Charlie Cook Cook The University of West Alabama The University of West Alabama MARY COULTER Foundations Foundations of Control of Control Chapter Chapter 18 18

Robbins9 ppt18 controlling

Aug 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ninth editionninth edition

STEPHEN P. ROBBINSSTEPHEN P. ROBBINS

© 2007 Prentice Hall, Inc. © 2007 Prentice Hall, Inc. All rights reserved.All rights reserved.

PowerPoint Presentation by Charlie CookPowerPoint Presentation by Charlie CookThe University of West AlabamaThe University of West Alabama

MARY COULTERMARY COULTER

Foundations Foundations of Controlof Control

ChapterChapter

1818

© 2007 Prentice Hall, Inc. All rights reserved. 18–2

L E A R N I N G O U T L I N E L E A R N I N G O U T L I N E Follow this Learning Outline as you read and study this chapter.Follow this Learning Outline as you read and study this chapter.

What Is Control and Why Is It Important?What Is Control and Why Is It Important?• Define control.Define control.

• Contrast the three approaches to designing control Contrast the three approaches to designing control systems.systems.

• Discuss the reasons why control is important.Discuss the reasons why control is important.

• Explain the planning-controlling link.Explain the planning-controlling link.

The Control ProcessThe Control Process• Describe the three steps in the control process.Describe the three steps in the control process.

• Explain why what is measured is more critical than how Explain why what is measured is more critical than how it’s measured.it’s measured.

• Explain the three courses of action managers can take in Explain the three courses of action managers can take in controlling.controlling.

© 2007 Prentice Hall, Inc. All rights reserved. 18–3

L E A R N I N G O U T L I N E (cont’d) L E A R N I N G O U T L I N E (cont’d) Follow this Learning Outline as you read and study this chapter.Follow this Learning Outline as you read and study this chapter.

Controlling Organizational PerformanceControlling Organizational Performance

• Define organizational performance.Define organizational performance.

• Describe the most frequently used measures of Describe the most frequently used measures of organizational performance.organizational performance.

Tools for Organizational PerformanceTools for Organizational Performance

• Contrast feedforward, concurrent, and feedback controls.Contrast feedforward, concurrent, and feedback controls.

• Explain the types of financial and information controls Explain the types of financial and information controls managers can use.managers can use.

• Describe how balanced scorecards and benchmarking are Describe how balanced scorecards and benchmarking are used in controlling.used in controlling.

© 2007 Prentice Hall, Inc. All rights reserved. 18–4

L E A R N I N G O U T L I N E (cont’d) L E A R N I N G O U T L I N E (cont’d) Follow this Learning Outline as you read and study this chapter.Follow this Learning Outline as you read and study this chapter.

Contemporary Issues in ControlContemporary Issues in Control

• Describe how managers may have to adjust controls for Describe how managers may have to adjust controls for cross-cultural differences.cross-cultural differences.

• Discuss the types of workplace concerns managers face Discuss the types of workplace concerns managers face and how they can address those concerns.and how they can address those concerns.

• Explain why control is important to customer interactions.Explain why control is important to customer interactions.

• Discuss what corporate governance is and how it’s Discuss what corporate governance is and how it’s changing.changing.

© 2007 Prentice Hall, Inc. All rights reserved. 18–5

What Is Control?What Is Control?

• ControllingControlling The process of monitoring activities to ensure that The process of monitoring activities to ensure that

they are being accomplished as planned and of they are being accomplished as planned and of correcting any significant deviations.correcting any significant deviations.

• The Purpose of ControlThe Purpose of Control To ensure that activities are completed in ways that To ensure that activities are completed in ways that

lead to accomplishment of organizational goals.lead to accomplishment of organizational goals.

© 2007 Prentice Hall, Inc. All rights reserved. 18–6

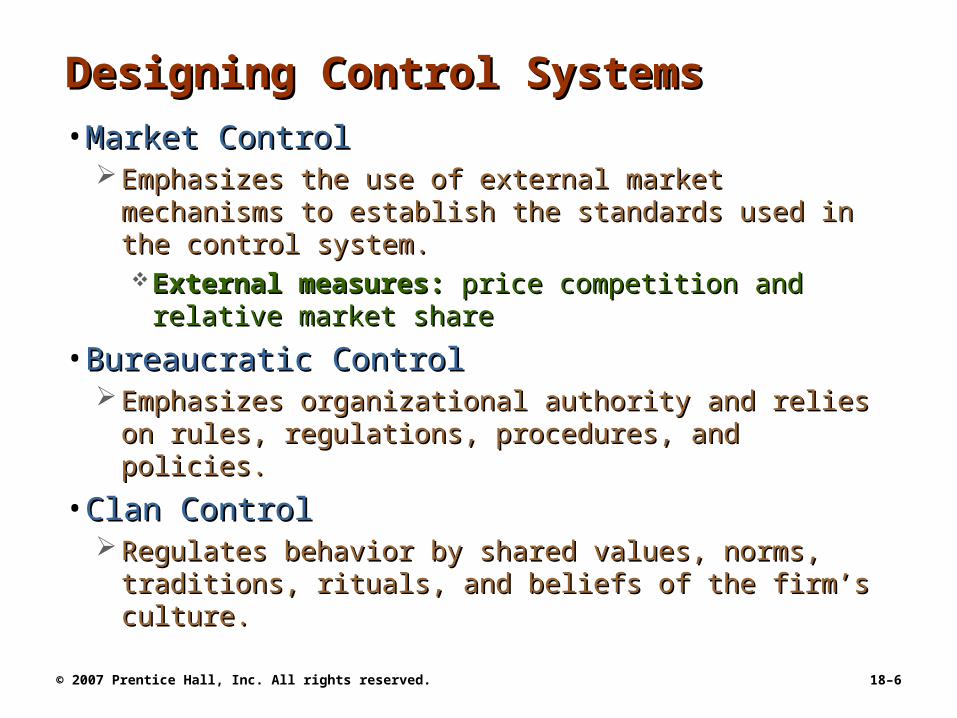

Designing Control SystemsDesigning Control Systems

• Market ControlMarket Control Emphasizes the use of external market mechanisms Emphasizes the use of external market mechanisms

to establish the standards used in the control system.to establish the standards used in the control system.External measures:External measures: price competition and relative price competition and relative

market sharemarket share

• Bureaucratic ControlBureaucratic Control Emphasizes organizational authority and relies on Emphasizes organizational authority and relies on

rules, regulations, procedures, and policies.rules, regulations, procedures, and policies.

• Clan ControlClan Control Regulates behavior by shared values, norms, Regulates behavior by shared values, norms,

traditions, rituals, and beliefs of the firm’s culture.traditions, rituals, and beliefs of the firm’s culture.

© 2007 Prentice Hall, Inc. All rights reserved. 18–7

Exhibit 18–1Exhibit 18–1 Characteristics of Three Approaches to Control SystemsCharacteristics of Three Approaches to Control Systems

Type of ControlType of Control CharacteristicsCharacteristics

MarketMarket Uses external market mechanisms, such as price competition Uses external market mechanisms, such as price competition and relative market share, to establish standards used in and relative market share, to establish standards used in system. Typically used by organizations whose products or system. Typically used by organizations whose products or services are clearly specified and distinct and that face services are clearly specified and distinct and that face considerable marketplace competition.considerable marketplace competition.

BureaucraticBureaucratic Emphasizes organizational authority. Relies on administrative Emphasizes organizational authority. Relies on administrative and hierarchical mechanisms, such as rules, regulations, and hierarchical mechanisms, such as rules, regulations, procedures, policies, standardization of activities, well-procedures, policies, standardization of activities, well-defined job descriptions, and budgets to ensure that defined job descriptions, and budgets to ensure that employees exhibit appropriate behaviors and meet employees exhibit appropriate behaviors and meet performance standards.performance standards.

ClanClan Regulates employee behavior by the shared values, norms, Regulates employee behavior by the shared values, norms, traditions, rituals, beliefs, and other aspects of the traditions, rituals, beliefs, and other aspects of the organization’s culture. Often used by organizations in which organization’s culture. Often used by organizations in which teams are common and technology is changing rapidly.teams are common and technology is changing rapidly.

© 2007 Prentice Hall, Inc. All rights reserved. 18–8

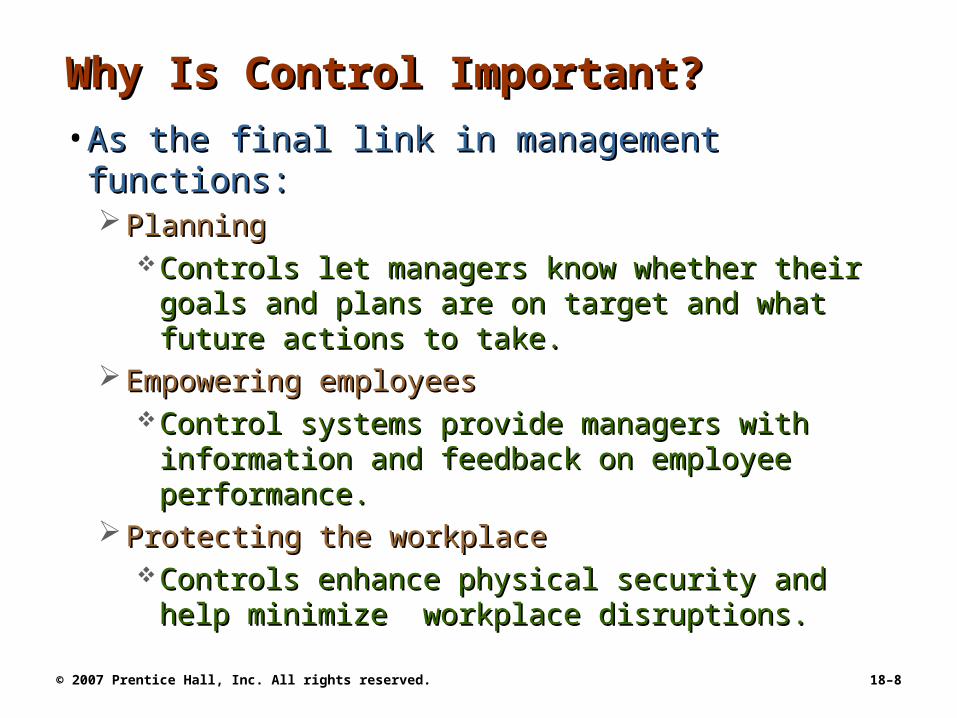

Why Is Control Important?Why Is Control Important?

• As the final link in management functions:As the final link in management functions: PlanningPlanning

Controls let managers know whether their goals Controls let managers know whether their goals and plans are on target and what future actions to and plans are on target and what future actions to take.take.

Empowering employeesEmpowering employeesControl systems provide managers with information Control systems provide managers with information

and feedback on employee performance.and feedback on employee performance. Protecting the workplaceProtecting the workplace

Controls enhance physical security and help Controls enhance physical security and help minimize workplace disruptions.minimize workplace disruptions.

© 2007 Prentice Hall, Inc. All rights reserved. 18–9

Exhibit 18–2Exhibit 18–2 The Planning–Controlling LinkThe Planning–Controlling Link

© 2007 Prentice Hall, Inc. All rights reserved. 18–10

The Control ProcessThe Control Process

• The Process of ControlThe Process of Control

1.1. Measuring actual Measuring actual performance.performance.

2.2. Comparing actual Comparing actual performance against a performance against a standard.standard.

3.3. Taking action to correct Taking action to correct deviations or inadequate deviations or inadequate standards.standards.

© 2007 Prentice Hall, Inc. All rights reserved. 18–11

Exhibit 18–3Exhibit 18–3 The Control ProcessThe Control Process

© 2007 Prentice Hall, Inc. All rights reserved. 18–12

Measuring: How and What We MeasureMeasuring: How and What We Measure

• Sources of Sources of Information (How)Information (How) Personal observationPersonal observation

Statistical reportsStatistical reports

Oral reportsOral reports

Written reportsWritten reports

• Control Criteria Control Criteria (What)(What) EmployeesEmployees

SatisfactionSatisfaction

TurnoverTurnover

AbsenteeismAbsenteeism

BudgetsBudgets

CostsCosts

OutputOutput

SalesSales

© 2007 Prentice Hall, Inc. All rights reserved. 18–13

Exhibit 18–4Exhibit 18–4 Common Sources of Information Common Sources of Information for Measuring Performancefor Measuring Performance

© 2007 Prentice Hall, Inc. All rights reserved. 18–14

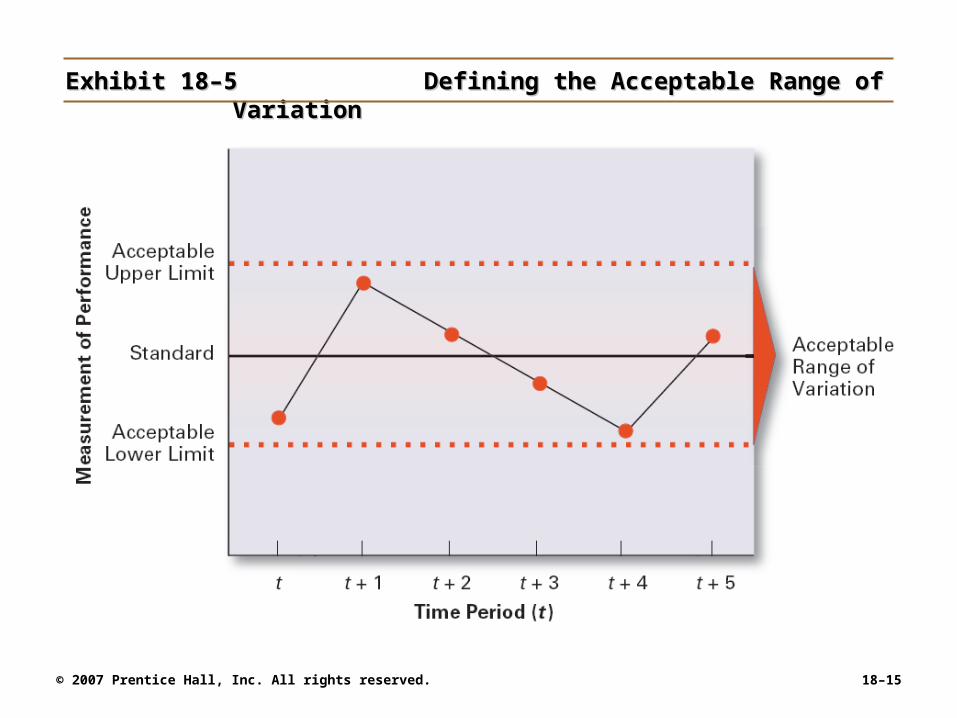

ComparingComparing

• Determining the degree of variation between Determining the degree of variation between actual performance and the standard.actual performance and the standard.

Significance of variation is determined by:Significance of variation is determined by:

The acceptable range of variation from the The acceptable range of variation from the standard (forecast or budget).standard (forecast or budget).

The size (large or small) and direction (over or The size (large or small) and direction (over or under) of the variation from the standard (forecast under) of the variation from the standard (forecast or budget).or budget).

© 2007 Prentice Hall, Inc. All rights reserved. 18–15

Exhibit 18–5Exhibit 18–5 Defining the Acceptable Range of VariationDefining the Acceptable Range of Variation

© 2007 Prentice Hall, Inc. All rights reserved. 18–16

Exhibit 18–6Exhibit 18–6 Sales Performance Figures for July, Sales Performance Figures for July, Eastern States DistributorsEastern States Distributors

© 2007 Prentice Hall, Inc. All rights reserved. 18–17

Taking Managerial ActionTaking Managerial Action

• Courses of ActionCourses of Action ““Doing nothing”Doing nothing”

Only if deviation is judged to be insignificant.Only if deviation is judged to be insignificant.

Correcting actual (current) performanceCorrecting actual (current) performance Immediate corrective action to correct the problem Immediate corrective action to correct the problem

at once.at once.Basic corrective action to locate and to correct the Basic corrective action to locate and to correct the

source of the deviation.source of the deviation.Corrective ActionsCorrective Actions

– Change strategy, structure, compensation scheme, or Change strategy, structure, compensation scheme, or training programs; redesign jobs; or fire employeestraining programs; redesign jobs; or fire employees

© 2007 Prentice Hall, Inc. All rights reserved. 18–18

Taking Managerial Action (cont’d)Taking Managerial Action (cont’d)

• Courses of Action (cont’d)Courses of Action (cont’d)

Revising the standardRevising the standard

Examining the standard to ascertain whether or not Examining the standard to ascertain whether or not the standard is realistic, fair, and achievable.the standard is realistic, fair, and achievable.

– Upholding the validity of the standard.Upholding the validity of the standard.

– Resetting goals that were initially set too low or too high.Resetting goals that were initially set too low or too high.

© 2007 Prentice Hall, Inc. All rights reserved. 18–19

Exhibit 18–7Exhibit 18–7 Managerial Decisions in the Control ProcessManagerial Decisions in the Control Process

© 2007 Prentice Hall, Inc. All rights reserved. 18–20

Controlling for Organizational Controlling for Organizational PerformancePerformance

• What Is Performance?What Is Performance? The end result of an activityThe end result of an activity

• What Is Organizational What Is Organizational Performance?Performance? The accumulated end results of all of the The accumulated end results of all of the

organization’s work processes and activitiesorganization’s work processes and activities

Designing strategies, work processes, and work Designing strategies, work processes, and work activities.activities.

Coordinating the work of employees.Coordinating the work of employees.

© 2007 Prentice Hall, Inc. All rights reserved. 18–21

Organizational Performance Measures Organizational Performance Measures

• Organizational ProductivityOrganizational Productivity Productivity:Productivity: the overall output of goods and/or the overall output of goods and/or

services divided by the inputs needed to generate services divided by the inputs needed to generate that output.that output.

Output: sales revenuesOutput: sales revenues

Inputs: costs of resources (materials, labor Inputs: costs of resources (materials, labor expense, and facilities)expense, and facilities)

Ultimately, productivity is a measure of how efficiently Ultimately, productivity is a measure of how efficiently employees do their work.employees do their work.

© 2007 Prentice Hall, Inc. All rights reserved. 18–22

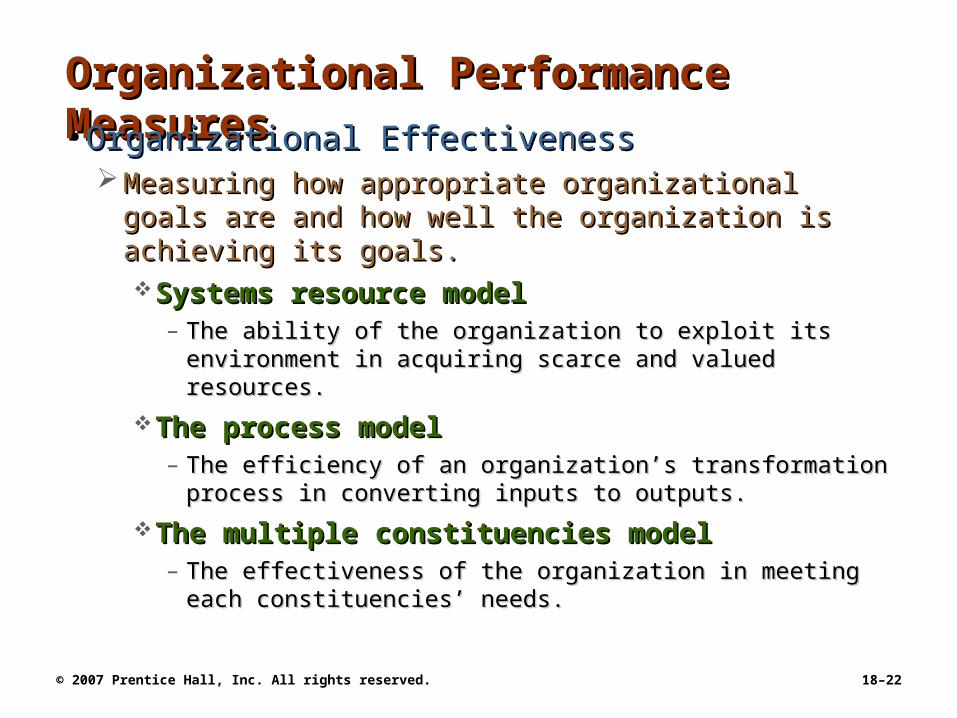

Organizational Performance Measures Organizational Performance Measures

• Organizational EffectivenessOrganizational Effectiveness Measuring how appropriate organizational goals are Measuring how appropriate organizational goals are

and how well the organization is achieving its goals.and how well the organization is achieving its goals.Systems resource modelSystems resource model

– The ability of the organization to exploit its environment in The ability of the organization to exploit its environment in acquiring scarce and valued resources.acquiring scarce and valued resources.

The process modelThe process model– The efficiency of an organization’s transformation process The efficiency of an organization’s transformation process

in converting inputs to outputs.in converting inputs to outputs.

The multiple constituencies modelThe multiple constituencies model– The effectiveness of the organization in meeting each The effectiveness of the organization in meeting each

constituencies’ needs.constituencies’ needs.

© 2007 Prentice Hall, Inc. All rights reserved. 18–23

Industry and Company RankingsIndustry and Company Rankings

• Industry rankings on:Industry rankings on: ProfitsProfits

Return on revenueReturn on revenue

Return on shareholders’ Return on shareholders’ equityequity

Growth in profitsGrowth in profits

Revenues per employeeRevenues per employee

Revenues per dollar of Revenues per dollar of assetsassets

Revenues per dollar of Revenues per dollar of equityequity

• Corporate Culture Corporate Culture AuditsAudits

• Compensation and Compensation and benefits surveysbenefits surveys

• Customer satisfactionCustomer satisfactionsurveyssurveys

© 2007 Prentice Hall, Inc. All rights reserved. 18–24

Exhibit 18–8Exhibit 18–8 Popular Industry and Company RankingsPopular Industry and Company Rankings

© 2007 Prentice Hall, Inc. All rights reserved. 18–25

Tools for Controlling Organizational Tools for Controlling Organizational PerformancePerformance

• Feedforward ControlFeedforward Control A control that prevents anticipated problems A control that prevents anticipated problems beforebefore

actual occurrences of the problem.actual occurrences of the problem.Building in quality through design.Building in quality through design.Requiring suppliers conform to ISO 9002.Requiring suppliers conform to ISO 9002.

• Concurrent ControlConcurrent Control A control that takes place while the monitored activity A control that takes place while the monitored activity

is in progress.is in progress.Direct supervisionDirect supervision: management by walking : management by walking

around.around.

© 2007 Prentice Hall, Inc. All rights reserved. 18–26

Exhibit 18–9Exhibit 18–9 Types of ControlTypes of Control

© 2007 Prentice Hall, Inc. All rights reserved. 18–27

Tools for Controlling Organizational Tools for Controlling Organizational Performance (cont’d)Performance (cont’d)

• Feedback ControlFeedback Control A control that takes place after an activity is done.A control that takes place after an activity is done.

Corrective action is after-the-fact, when the Corrective action is after-the-fact, when the problem has already occurred.problem has already occurred.

Advantages of feedback controls:Advantages of feedback controls:

Provide managers with information on the Provide managers with information on the effectiveness of their planning efforts.effectiveness of their planning efforts.

Enhance employee motivation by providing them Enhance employee motivation by providing them with information on how well they are doing.with information on how well they are doing.

© 2007 Prentice Hall, Inc. All rights reserved. 18–28

Tools for Controlling Organizational Tools for Controlling Organizational Performance: Financial ControlsPerformance: Financial Controls

• Traditional ControlsTraditional Controls Ratio analysisRatio analysis

LiquidityLiquidity

LeverageLeverage

ActivityActivity

ProfitabilityProfitability

Budget AnalysisBudget Analysis

Quantitative standardsQuantitative standards

DeviationsDeviations

• Other MeasuresOther Measures Economic Value Added Economic Value Added

(EVA)(EVA)

Market Value Added Market Value Added (MVA)(MVA)

© 2007 Prentice Hall, Inc. All rights reserved. 18–29

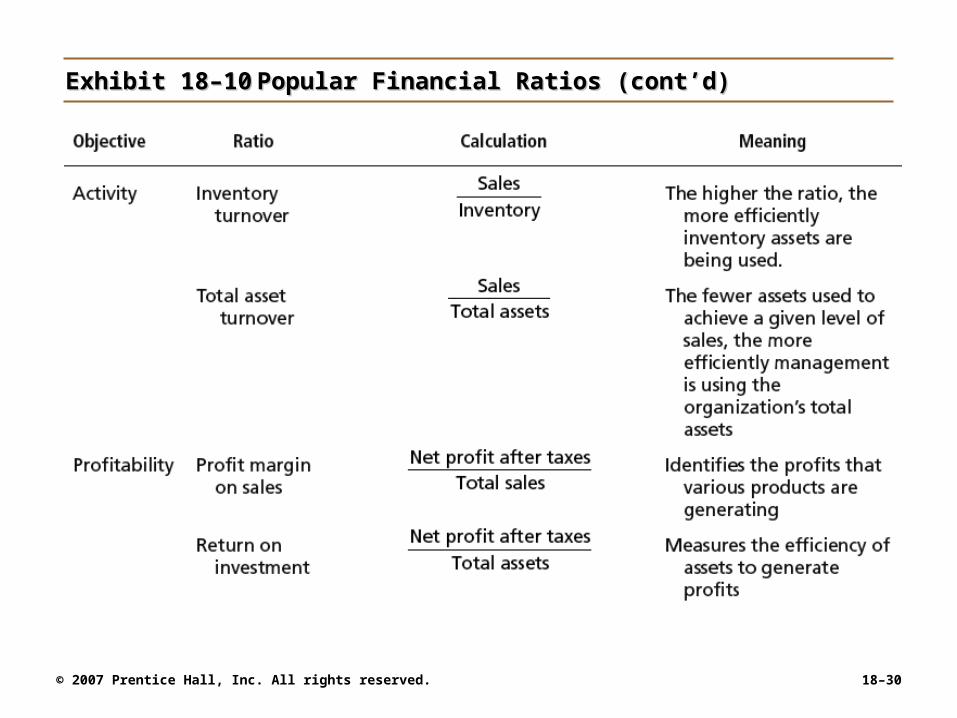

Exhibit 18–10Exhibit 18–10 Popular Financial RatiosPopular Financial Ratios

© 2007 Prentice Hall, Inc. All rights reserved. 18–30

Exhibit 18–10Exhibit 18–10 Popular Financial Ratios (cont’d)Popular Financial Ratios (cont’d)

© 2007 Prentice Hall, Inc. All rights reserved. 18–31

Tools for Controlling Organizational Tools for Controlling Organizational Performance: Financial Controls (cont’d)Performance: Financial Controls (cont’d)

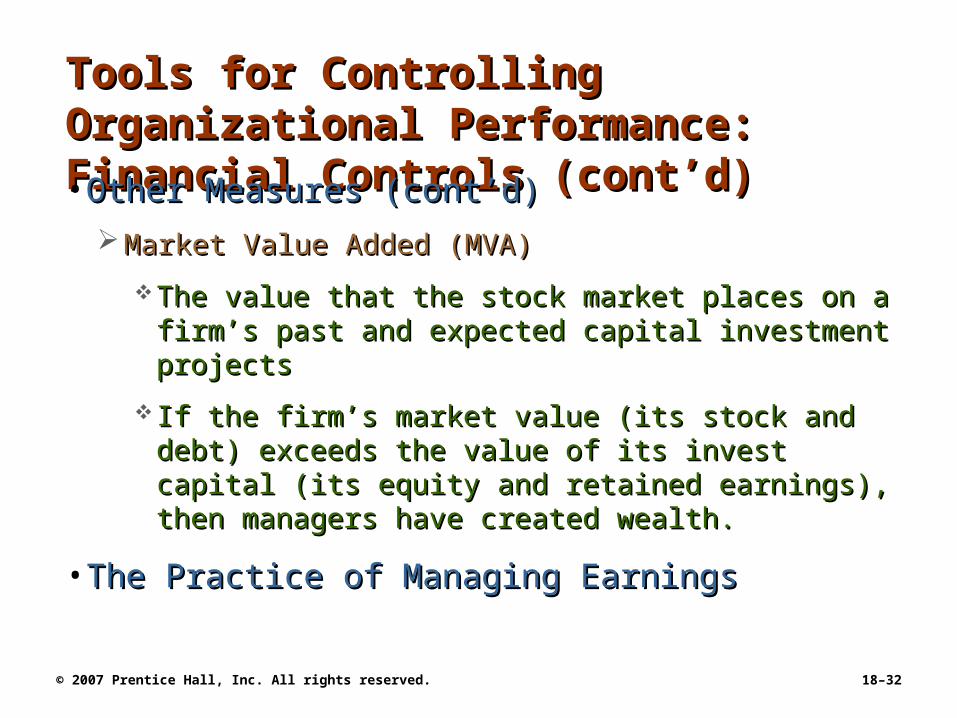

• Other MeasuresOther Measures

Economic Value Added (EVA)Economic Value Added (EVA)

How much value is created by what a company How much value is created by what a company does with its assets, less any capital investments in does with its assets, less any capital investments in those assets: those assets: the rate of return earned over and the rate of return earned over and above the cost of capital.above the cost of capital.

– The choice is to use less capital or invest in high-return The choice is to use less capital or invest in high-return projects.projects.

© 2007 Prentice Hall, Inc. All rights reserved. 18–32

Tools for Controlling Organizational Tools for Controlling Organizational Performance: Financial Controls (cont’d)Performance: Financial Controls (cont’d)

• Other Measures (cont’d)Other Measures (cont’d)

Market Value Added (MVA)Market Value Added (MVA)

The value that the stock market places on a firm’s The value that the stock market places on a firm’s past and expected capital investment projectspast and expected capital investment projects

If the firm’s market value (its stock and debt) If the firm’s market value (its stock and debt) exceeds the value of its invest capital (its equity exceeds the value of its invest capital (its equity and retained earnings), then managers have and retained earnings), then managers have created wealth.created wealth.

• The Practice of Managing EarningsThe Practice of Managing Earnings

© 2007 Prentice Hall, Inc. All rights reserved. 18–33

Controlling Organizational PerformanceControlling Organizational Performance

• Balanced ScorecardBalanced Scorecard Is a measurement tool that uses goals set by Is a measurement tool that uses goals set by

managers in four areas to measure a company’s managers in four areas to measure a company’s performance:performance:FinancialFinancialCustomerCustomer Internal processesInternal processesPeople/innovation/growth assetsPeople/innovation/growth assets

Is intended to emphasize that all of these areas are Is intended to emphasize that all of these areas are important to an organization’s success and that there important to an organization’s success and that there should be a balance among them.should be a balance among them.

© 2007 Prentice Hall, Inc. All rights reserved. 18–34

Information ControlsInformation Controls

• Purposes of Information ControlsPurposes of Information Controls

As a tool to help managers control other As a tool to help managers control other organizational activities.organizational activities.

Managers need the right information at the right Managers need the right information at the right time and in the right amount. time and in the right amount.

As an organizational area that managers need to As an organizational area that managers need to control.control.

Managers must have comprehensive and secure Managers must have comprehensive and secure controls in place to protect the organization’s controls in place to protect the organization’s important information.important information.

© 2007 Prentice Hall, Inc. All rights reserved. 18–35

Information ControlsInformation Controls

• Management Information Systems (MIS)Management Information Systems (MIS)

A system used to provide management with needed A system used to provide management with needed information on a regular basis.information on a regular basis.

Data:Data: an unorganized collection of raw, unanalyzed an unorganized collection of raw, unanalyzed facts (e.g., unsorted list of customer names).facts (e.g., unsorted list of customer names).

Information:Information: data that has been analyzed and data that has been analyzed and organized such that it has value and relevance to organized such that it has value and relevance to managers.managers.

© 2007 Prentice Hall, Inc. All rights reserved. 18–36

Benchmarking of Best PracticesBenchmarking of Best Practices

• BenchmarkBenchmark The standard of excellence against which to measure The standard of excellence against which to measure

and compare.and compare.

• BenchmarkingBenchmarking Is the search for the best practices among Is the search for the best practices among

competitors or noncompetitors that lead to their competitors or noncompetitors that lead to their superior performance.superior performance.

Is a control tool for identifying and measuring specific Is a control tool for identifying and measuring specific performance gaps and areas for improvement.performance gaps and areas for improvement.

© 2007 Prentice Hall, Inc. All rights reserved. 18–37

Exhibit 18–11Exhibit 18–11 Steps to Successfully Implement an Internal Steps to Successfully Implement an Internal Benchmarking Best Practices ProgramBenchmarking Best Practices Program

1.1. Connect best practices to strategies and goals.Connect best practices to strategies and goals.

2.2. Identify best practices throughout the organization.Identify best practices throughout the organization.

3.3. Develop best practices reward and recognition Develop best practices reward and recognition systems.systems.

4.4. Communicate best practices throughout the Communicate best practices throughout the organization.organization.

5.5. Create a best practices knowledge-sharing system.Create a best practices knowledge-sharing system.

6.6. Nurture best practices on an ongoing basis.Nurture best practices on an ongoing basis.

© 2007 Prentice Hall, Inc. All rights reserved. 18–38

Contemporary Issues in ControlContemporary Issues in Control

• Cross-Cultural IssuesCross-Cultural Issues

The use of technology to increase direct corporate The use of technology to increase direct corporate control of local operationscontrol of local operations

Legal constraints on corrective actions in foreign Legal constraints on corrective actions in foreign countriescountries

Difficulty with the comparability of data collected from Difficulty with the comparability of data collected from operations in different countriesoperations in different countries

© 2007 Prentice Hall, Inc. All rights reserved. 18–39

Contemporary Issues in Control (cont’d)Contemporary Issues in Control (cont’d)

• Workplace ConcernsWorkplace Concerns Workplace privacy versus workplace monitoring:Workplace privacy versus workplace monitoring:

E-mail, telephone, computer, and Internet usageE-mail, telephone, computer, and Internet usageProductivity, harassment, security, confidentiality, Productivity, harassment, security, confidentiality,

intellectual property protectionintellectual property protection Employee theftEmployee theft

The unauthorized taking of company property by The unauthorized taking of company property by employees for their personal use.employees for their personal use.

Workplace violenceWorkplace violenceAnger, rage, and violence in the workplace is Anger, rage, and violence in the workplace is

affecting employee productivity.affecting employee productivity.

© 2007 Prentice Hall, Inc. All rights reserved. 18–40

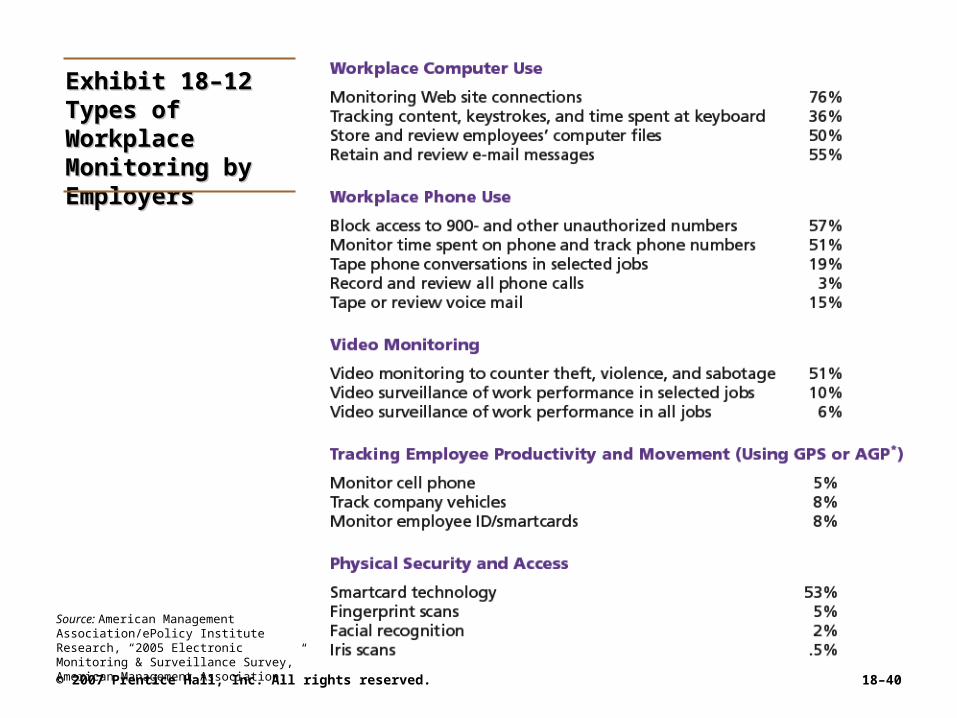

Exhibit 18–12Exhibit 18–12Types of Workplace Types of Workplace Monitoring by Monitoring by EmployersEmployers

Source: American Management Association/ePolicy Institute Research, “2005 Electronic Monitoring & Surveillance Survey,” American Management Association.

© 2007 Prentice Hall, Inc. All rights reserved. 18–41

Exhibit 18–13Exhibit 18–13 Control Measures for Employee Theft or FraudControl Measures for Employee Theft or Fraud

Sources: Based on A.H. Bell and D.M. Smith. “Protecting the Company Against Theft and Fraud,” Workforce Online (www.workforce.com) December 3, 2000; J.D. Hansen. “To Catch a Thief,” Journal of Accountancy, March 2000, pp. 43–46; and J. Greenberg, “The Cognitive Geometry of Employee Theft,” in Dysfunctional Behavior in Organizations: Nonviolent and Deviant Behavior, eds. S.B. Bacharach, A. O’Leary-Kelly, J.M. Collins, and R.W. Griffin (Stamford, CT: JAI Press, 1998), pp. 147–93.

© 2007 Prentice Hall, Inc. All rights reserved. 18–42

Exhibit 18–14Exhibit 18–14 Workplace ViolenceWorkplace Violence

Witnessed yelling or other verbal abuse 42%

Yelled at co-workers themselves 29%

Cried over work-related issues 23%

Seen someone purposely damage machines or furniture 14%

Seen physical violence in the workplace 10%

Struck a co-worker 2%

Source: Integra Realty Resources, October-November Survey of Adults 18 and Over, in “Desk Rage.” BusinessWeek, November 20, 2000, p. 12.

© 2007 Prentice Hall, Inc. All rights reserved. 18–43

Exhibit 18–15Exhibit 18–15 Control Measures for Deterring or Reducing Control Measures for Deterring or Reducing Workplace ViolenceWorkplace Violence

Sources: Based on M. Gorkin, “Five Strategies and Structures for Reducing Workplace Violence,” Workforce Online (www.workforce.com). December 3, 2000; “Investigating Workplace Violence: Where Do You Start?” Workforce Online (www.forceforce.com), December 3, 2000; “Ten Tips on Recognizing and Minimizing Violence,” Workforce Online (www.workforce.com), December 3, 2000; and “Points to Cover in a Workplace Violence Policy,” Workforce Online (www.workforce.com), December 3, 2000.

© 2007 Prentice Hall, Inc. All rights reserved. 18–44

Contemporary Issues in Control (cont’d)Contemporary Issues in Control (cont’d)

• Customer InteractionsCustomer Interactions Service profit chainService profit chain

Is the service sequence from employees to Is the service sequence from employees to customers to profit. customers to profit.

Service capability affects service value which impacts Service capability affects service value which impacts on customer satisfaction that, in turn, leads to on customer satisfaction that, in turn, leads to customer loyalty in the form of repeat business customer loyalty in the form of repeat business (profit).(profit).

© 2007 Prentice Hall, Inc. All rights reserved. 18–45

Exhibit 18–16Exhibit 18–16 The Service Profit ChainThe Service Profit Chain

Source: Adapted and reprinted by permission of Harvard Business Review. An exhibit from “Putting the Service Profit Chain to Work,” by J. L. Heskett, T. O. Jones, G. W. Loveman, W. E. Sasser, Jr., and L. A. Schlesinger. March–April 1994: 166. Copyright (c) by the President and Fellows of Harvard College. All rights reserved. See also J. L. Heskett, W. E. Sasser, and L. A. Schlesinger, The Service Profit Chain (New York: Free Press, 1997).

© 2007 Prentice Hall, Inc. All rights reserved. 18–46

Contemporary Issues in Control (cont’d)Contemporary Issues in Control (cont’d)

• Corporate GovernanceCorporate Governance The system used to govern a corporation so that the The system used to govern a corporation so that the

interests of the corporate owners are protected.interests of the corporate owners are protected.

Changes in the role of boards of directorsChanges in the role of boards of directors

Increased scrutiny of financial reporting (Sarbanes-Increased scrutiny of financial reporting (Sarbanes-Oxley Act of 2002)Oxley Act of 2002)

– More disclosure and transparency of corporate financial More disclosure and transparency of corporate financial informationinformation

– Certification of financial results by senior managementCertification of financial results by senior management

© 2007 Prentice Hall, Inc. All rights reserved. 18–47

Terms to KnowTerms to Know

• controllingcontrolling• market controlmarket control• bureaucratic controlbureaucratic control• clan controlclan control• control processcontrol process• range of variationrange of variation• immediate corrective immediate corrective

actionaction• basic corrective actionbasic corrective action• performanceperformance• organizational organizational

performanceperformance

• productivityproductivity• organizational organizational

effectivenesseffectiveness• feedforward controlfeedforward control• concurrent controlconcurrent control• management by walking management by walking

aroundaround• feedback controlfeedback control• economic value added economic value added

(EVA)(EVA)• market value added market value added

(MVA)(MVA)

© 2007 Prentice Hall, Inc. All rights reserved. 18–48

Terms to Know (cont’d)Terms to Know (cont’d)

• management information management information system (MIS)system (MIS)

• datadata• informationinformation• balanced scorecardbalanced scorecard• benchmarkingbenchmarking• employee theftemployee theft• service profit chainservice profit chain• corporate governancecorporate governance

Related Documents