RESTRICTED RLE COPY Report No. AS- 109 This report was prepared for use within the Bank and its affiliated organizations. They do not accept responsibility for its accuracy or completeness. The report may not be published nor may it be quoted as representing their views. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION ECONOMIC DEVELOPMENT OF PAKISTAN VOLUME II ANNEXES April 26, 1965 South Asia Department Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RESTRICTED

RLE COPY Report No. AS- 109

This report was prepared for use within the Bank and its affiliated organizations.They do not accept responsibility for its accuracy or completeness. The report maynot be published nor may it be quoted as representing their views.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

ECONOMIC DEVELOPMENT

OF

PAKISTAN

VOLUME II

ANNEXES

April 26, 1965

South Asia Department

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

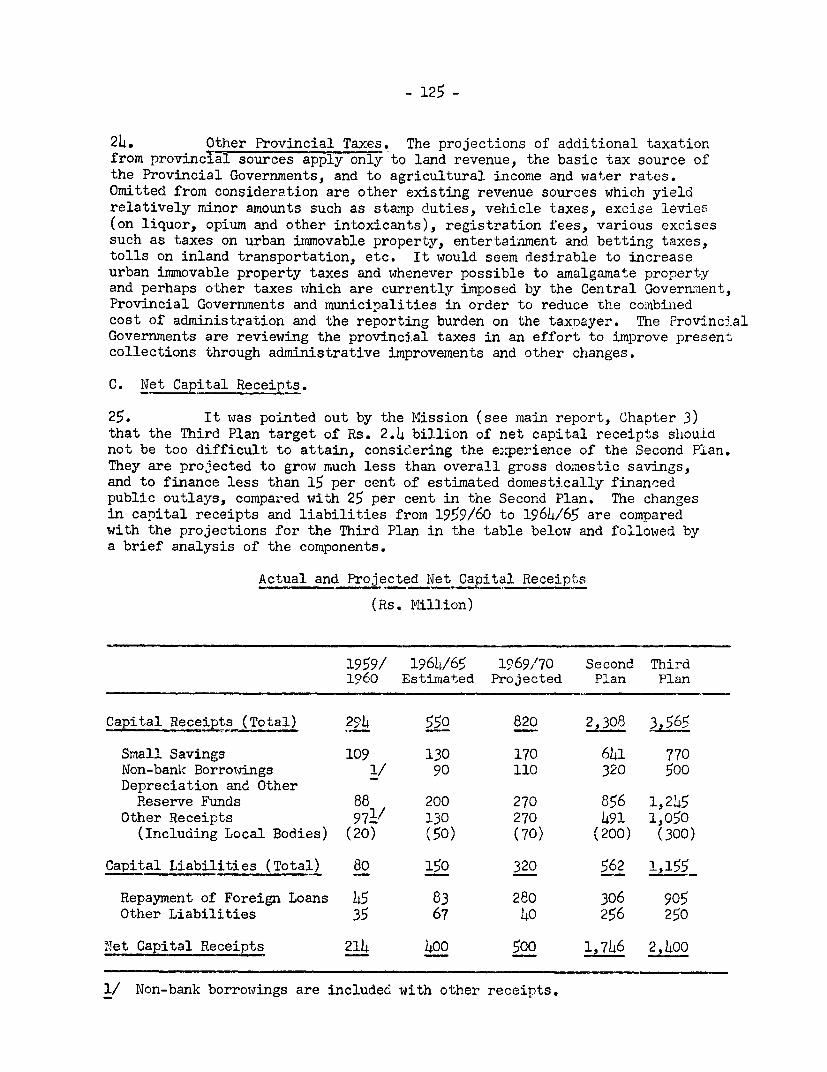

iscl

osur

e A

utho

rized

Pub

lic D

iscl

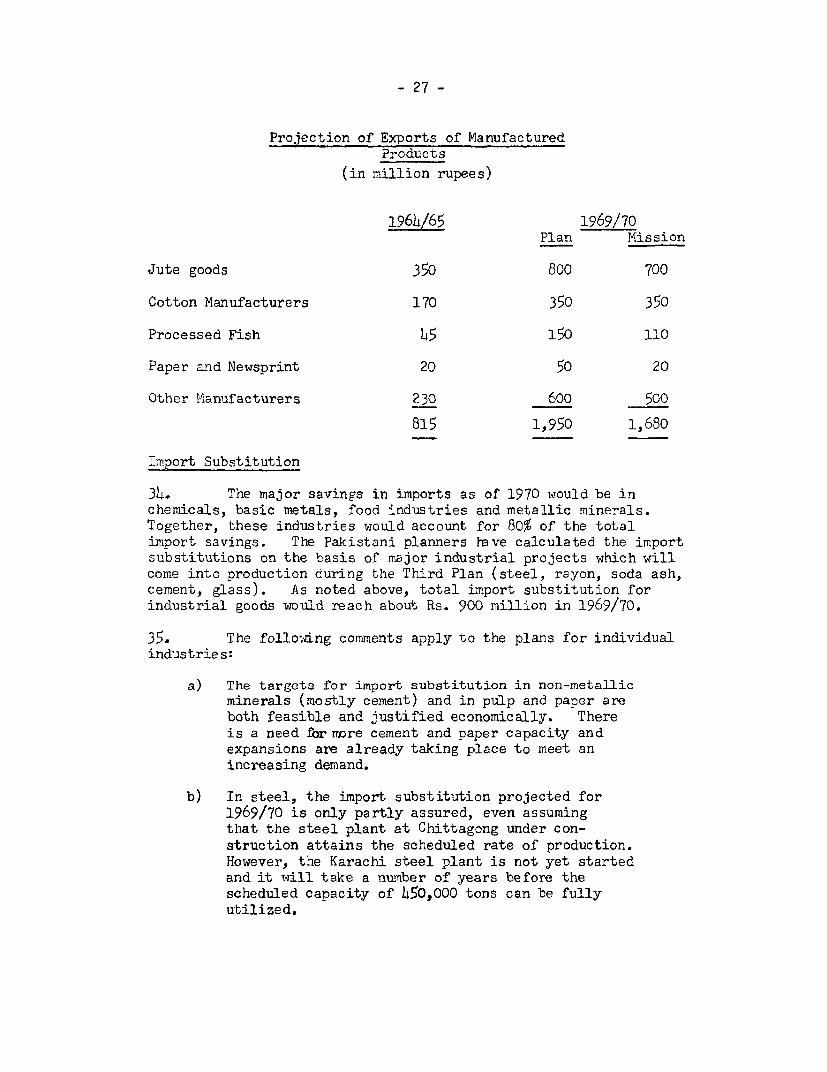

osur

e A

utho

rized

Pub

lic D

iscl

osur

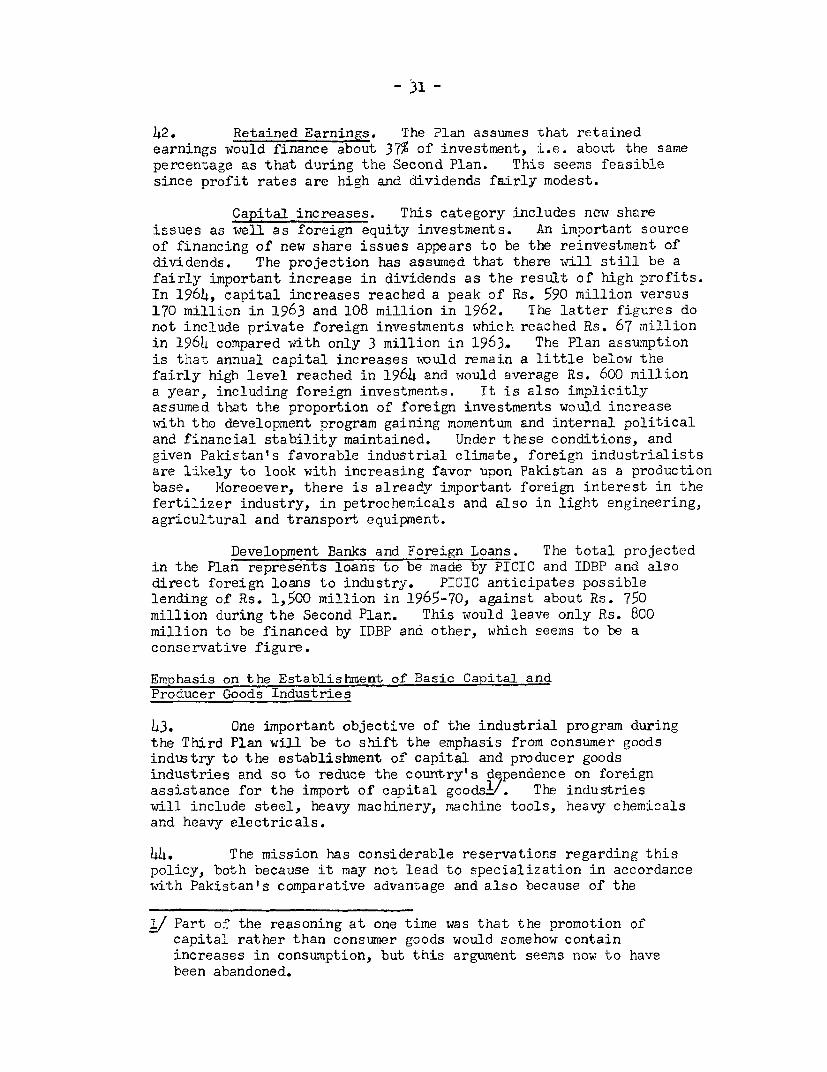

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

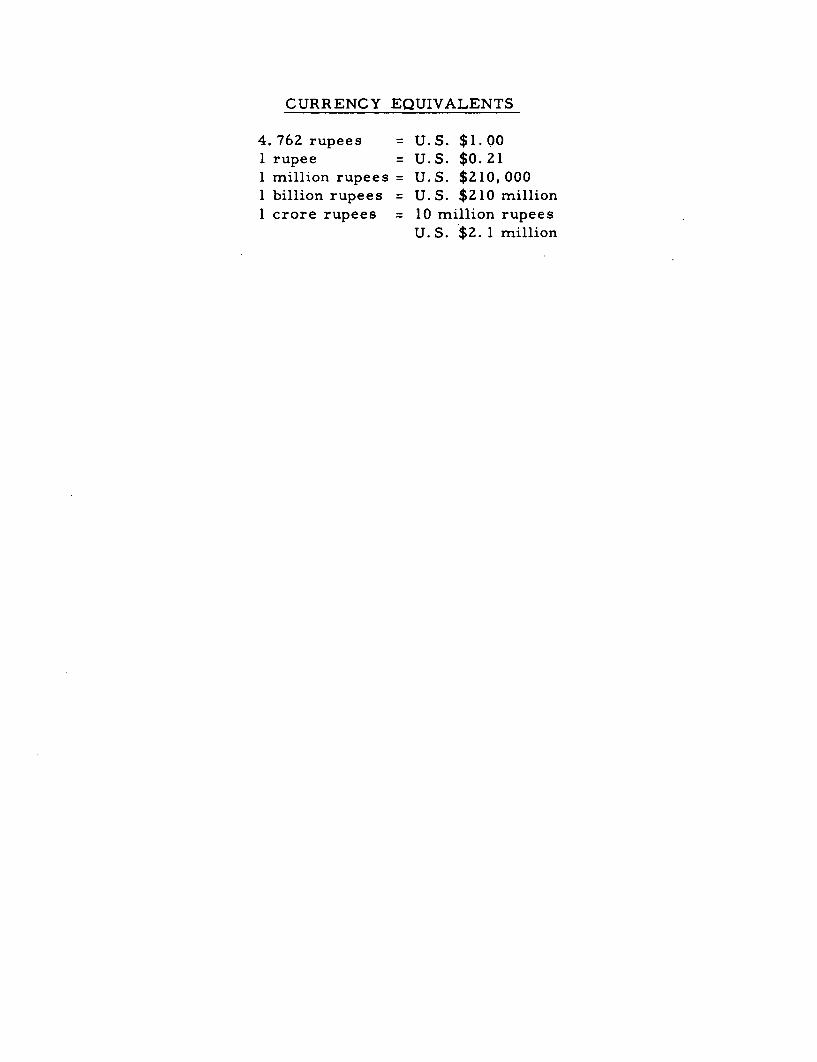

CURRENCY EQUIVALENTS

4.762 rupees = U.S. $1. 00I rupee = U.S. $0. 211 million rupees = U.S. $210,0001 billion rupees = U. S. $210 millionI crore rupees = 10 million rupees

U. S. $2. 1 million

CONTENTS

Page

1. EXPORT FROJECTIONS FOR THE THIRD PLAN 1

2. AGRICULTURE 7

3. IINDUSTRY 19

4. POWER 56

5. TRANSPORT AND COMMUNICATIONS 87

6. SOCIAL SERVICES 95

7. CAPITAL IMARKET 99

8. RECENT TAX CHANGES ADOPTED DURING THESECOND FTVE-YEAR PLAN 102

9. TAX SYSTEM 115

ANNEX 1

EXPORT PROJECTIONS FOR THE THIRD PLAN

Raw Jute.

1. Average raw jute production during the 1950's was about 5.6 riiillionbales a year, moving up from 5.3 during the first half of the decade to 5.9during the second half. Since 1960, production has been as follows:

1960/61 1961/62 1962/63 1963/64 1964/65 Average

Million bales: 4.5 6.9 6.5 5.9 5*5.5/ 5.9

a/ Preliminary estimate.

2. The average for the Second Plan period would thus be unchanged atthe 5.9 figure of the previous five years; this stagnation is the moreremarkable as it implies a continuous decline from the large 1961/62 crop.At the same time, world production has recorded a progressive increase,mainly on account of India.

3. The Second Plan target for raw jute production had been 7.3 millionbales by 1964/65, and the shortfall is now expected to be 25 per cent. Thismust be attributed chiefly to the low price received by farmers relative torice, partly to lack of direct promotion of improvement in cultivation, andpossibly in some degree to emigration. The production target for the ThirdPlan is for 8 million bales by 1969/70, which represents an increase over theaverage Second Plan production by 36 per cent. One-half of this proposed in-crease is to come from additional acreage, made available through reclamationand drainage, and the other half from increased yields.

4. An appropriate price policy could most likely bring jute acreagefrom the present 1.66 million acres close to the 2 million acres target,which at current yields would produce roughly 7 million bales. Better farm-ing methods, seeds and fertilizers are expected to bring production furtherup to 8 million bales. These physical quantities are in no way ambitious bythemselves, but clearly no farmer will be persuaded to put more resourcesinto jute cultivation if the price incentives are lackiag. It may be thatthe continuation of current increases in rice productioon would help to improvethe relative cash value of jute cultivation, but unless the price of rice wrereto drop substantially in the years to come, positive measures will have to betaken to improve the price of jute. This problem is difficult because of thevery large number of growers, and the age-old marketing organization based onthe activity of innumerable small itinerant traders, middle men, country boatoperators, and money lenders. The Jute Marketing Corporation, set up by theCentral Government with the object of stabilizing farm prices through bufferstock operations at the intermediary level, does not appear to have beenoverly successful, although it is reported to have stocked 8 per cent of thecrop last year. The Mission has no information as to what extent this wassimply a commercial purchasing operation.

- 2 -

5. As far as promotion of fertilizer and better seeds is concerned,not much has been done by either Government or by other interested partiesin the past, and the same is true for irrigation. In the opinion of the

Mission, a combined effort of considerable magnitude will be necessary onthe side of production inputs and of price policy to achieve the Plan target

for jute output. In view of the need to keep export prices not only stablebut below the threshold of technological substitution which may become in-

creasingly competitive in the future, and of the need on the other hand to

create a price incentive to the farmer which at present clearly is not avail-able, it would be advisable to seriously consider the abolition of the export

duty as a first step. A thorough study of other suitable resources should

be undertaken as early as possible. Pending tangible indications of sub-stantial change, the Mission visualizes a shortfall by perhaps 5-10 per centfrom the raw jute production target of 8 million bales in 1969/70.

Jute Manufactures.

6. The availability of raw jute for export is the residual of produc-tion after domestic mill consumption, and it cannot be projected before theproduction of jute manufactures is known. Mlore than for other export goods,the limiting factor in jute manufactures is the speed at which productioncapacity can be expanded. The loomage target for the Second Plan had ori-ginally been for a 50 per cent increase to 12,000 looms and was twice revieedupwards during the Plan. Still, just about 10,500 looms are expected to be

operating at the beginning of the Third Plan. The Government is now settinga target to increase this to about 22,000 by 1969/70, including 1,800 broadlooms. This would enable Pakistan to export 600,000 tons of jute fabrics asagainst the present volume of 250,000 toins. The industry considers this tobe possible, given the most favorable conditions for investment, which goconsiderably beyond those presently prevailing. Indirectly, they wouldamount to subsidies advanced through public utilities, to removal of virtu-ally all government controls from the industry, and to extremely favorable

credit facilities. From experience in the past few years, it would notappear to be politically easy to extend all the freedoms requested, becauseof the structure of private capital in the jute industry. This is not to saythat the Mission shares the Government's concern with the conflict of con-centration of wealth with social objectives, but it can foresee polibtical

pressures for a wider social and geographical dispersion of jute mills. Time

is likely to be lost over these issues; and an acceleration in the ordering,shipment and installation of new looms from an annual rate of about 600 per

year in the Second Plan to over 2,500 on average during the Third Plan would

seem to be difficult for purely technical reasons, even in the absence of any

need for government sanctioning of plants.

7. Pakistan's exports of jute fabrics at present constitute about 20per cent of world exports. The proposed increase would imply that Pakistancaptures 58 per cent of the total increase in wqorld demand and would increase

its share to 33 per cent. Although there may be questicns about the industry's

capacity to make such large inroads in world markets, the Mission has no

reason to think that it should be impossible from the marketing point ofview, unless her major competitor, India, were to take drastic steps on theexchange rate side or otherwise, to offset the advantage which Pakistan hasin price as well as in quality. Another contingency would be a slowing downof world demand, brought about by new economies in bulk handling as againstthe use of jute sacking, or by technological competition from syntheticfibers. The most important factor in maintaining and promoting the use ofjute fabrics in the world is to lceep the price stable at a point low enoughto retain and expand markets against synthetic competition. If this can beachieved, much will have been done towards meeting the Plan targets forexport of jute manufactures.

8. The price assumptions made in the projections of earnings by1969/70, implying a slight reduction from present prices for sacking andhessian, and a price of Rs. 1,800 per ton for broad cloth, appear reasonable.However, in the light of the problems to be encountered in the accelerationof production, the Mission thinks that a target of Rs. 800 million from jutemanufacture is more than what can be expected. A reduced target of Rs. 700million might be feasible, implying a 10 per cent reduction from the produc-tion target of 720,000 tons. Even the Rs. 700 million would represent a100 per cent increase over 1964/65, and the Mission feels that the utmosteffort would be required to achieve it.

9. Assuming that the mill offtake of raw jute would be less by about10 per cent than assumed in the Government's projections, this would releaseabout 450,000 bales of raw jute. Such a volume is in the same order ofmagnitude as the shortfall which the Mission thinks is likely to occur in theoutput of raw jute and, therefore, it would still appear feasible to export3.75 million bales. On this basis, a target for earnings of Rs. 750 millionfrom raw jute would not seem to be unreasonable.

Raw Cotton.

10. The volume of Pakistan's cotton exports has in the past fluctuatedwith the crop output, while the export price is governed by factors outsidePakistan's control, such as U.S. farm and cotton export policy. Pakistan'sexports represent only about 4 per cent of total world exports; the qualityof Pakistani cotton is good, and from past experience it appears that evenwith substantial increases in availabilities from one year to another thereis no real difficulty in marketing a growing export surplus, notwithstandingthe fact that part of the volume in recent years has been exported underbilateral trade agreements. An increase in exports from a present trendlevel of close to 1 million bales to a 1969/70 target of 1.25 million baleswould not seem to pose a problem. The price assumption of Rs. 450 per balewould also seem reasonable.

11. Prospects for production of raw cotton are discussed inA n n e x 2, where it is concluded that an output of 3.5 million balesin 1969/70, representing a 45 per cent increase over the present trendlevel, is also a feasible objective. With an assumed domestic disappearanceof about 2.2 million bales, exports could well reach 1.25 million bales andproduce earnings of Rs. 550 million.

12. The production target for 196 4W/6 5 had been 213 million bales. Thiswas already exceeded in 1963/64 with production of around 2.35 millicn bales.In the current year, it is expected that production itill be slightly belowtarget owing to unfavorable weather conditions and floods. However, as inthe case of raw jute, the original price assumptions have proven conserva-tive, and it appears that the price will be at least 10 per cent betterthan expected. Domestic mill consumption increased more slowly than had beenassumed, so that exports now will be about 820,000 bales as against theprojected figure of 650,000 bales. Earnings should therefore be about $84million as against an expected $55 million. After the existing exportduties on raw jute and raw cotton had been reduced from time to time fromthe high level of the Korean boom, the Government decided in July 1964 tofurther reduce them by 50 per cent, to Rs. 10 per bale for both coLiiodi-ties, and to abolish the sales tax on cotton. Expressed as a percentageof the value, the remaining duty represents about 5 per cent in the caseof jute; this reduction is a realistic step but we do not think that byitself it will make the necessary impact on production and export, sincethe long-run prob'em, with Pakistan having a quasi-monopoly, lies deeper,and some day will require more drastic measures. The duty on cotton hadstill been the equivalent of over 15 per cent ad valorem in 1962, and itis now just over 2 per cent. This has certainly been a factor in makinga 100 per cent increase in exports of cotton possible.

Cotton Textiles.

12. Exports of cotton textiles has been disappointing in the SecondPlan, increasing from a level of 80 million yards of cloth to 106 millionyards over five years. It is true that international competition in cottontextiles is difficult, and Pakistan's industry still has difficulty in pro-ducing adequate quality. Her costs are not low and she has had no realincentive to become competitive. For nearly 15 years the domestic markethas been hermetically sheltered; in the first 10 years of this period, pro-duction of cloth increased seven-fold. Since 1961, however, the growthrate has been less than the growth of GNP, which is remarkable in a countrywhere per capita consumption of cloth is only 13 yards per annum, and wherethe income elasticity of demand is no doubt more than unity.

13. The export target for cloth in 1969/70 is modest. Indeed, it isthe same 225 million yards, which had been the target for the end of theSecond Plan. In proportion to total expected output, it is about one-sixth,the same as that prevailing at present with a mill production of 785 millionyards and an export of 106 million yards. The question is whether the

- 5 -

proposed increase of output to 1.4 billion yards by 1969/70 is feasiblewith present domestic market conditions. It would appear that a saturationpoint has been reached in this market two years agosince in the last twoyears domestic consumption increased less than domestic population; thishighly abnormal situation may be partly explained by relative stagnation ofinvestment in the expansion of capacity which is controlled by the Govern-ment. In fact, it is claimed by some sources that installed capacity isfully utilized. However, the Mission believes that the most importantobstacle which may stand in the way to achieving Third lPlan output andexport targets is extreme protection from competition and oligopoly. ThePakistan cotton textile industry is largely equipped with modern machinery;Pakistani factory workers are not less endowed with natural skills than inother countries; management is shrewd but accustomed to easy outlets. Itis a matter for concern that they should still be in need of a total pro-hibition of cotton textile imports and a protective duty of 100 per cent advalorem. The MIission thinks that, with the continuation of these presentarrangements, it is unlikely that costs and prices would become competitive;that incentives to expand output to the targets would be insufficient, andexports would continue to be in need of government compulsion.

14. If it were not for these considerations, the Third Plan targetfor the export of cotton manufactures, namely Rs. 170 million for yarn andRs. 180 million for cloth, with the underlying volume and price assumptions,would appear both practical and feasible.

Fish.

15. Of the Rs. 90 million worth of fish presently exported, abouthalf consisted of traditional exports of fresh river fish from East Pakistanto Calcutta and of dried fish to India, Ceylon and Southeast Asia. Thistype of fish export has not grown very fast and has no great potential. Atarget of Rs. 60 million for the Third Plan, implying a 30 per cent increase,would therefore seem more realistic than the proposed Rs. 100 million. Theother half consists mainly of fresh frozen fish and of shrimp, lobster, etc.,frozen or canned. These items have good market prospects in the U.S.,Europe and possibly in the Far East; but extremely favorable assumptions asto the volume, quality, and price of Pakistan's supply would have to bemade to assume a 200 per cent increase within the next five years. A morelikely assumption would be to double these items from Rs. 45 million toRs 90 million. An additional Rs. 20 million at least could be earned withfish meal, the production of which the M.ission recommends.

Rice.

16. As for raw cotton, the prospects for production of superior riceare very favorable. The Mission accepts the export targets of 400,000 tonseven though this implies a dramatic increase from the present volume of140,000 tons (but the present volume is also three times the volume at thebeginning of the Second Plan). However, it feels that in order to reach

- 6 -

markets other than the Middle East, which has a limited capacity, theassumed price of Rs. 980 per ton is too high. A price of Rs. 850 a tonwould be reasonable for Basmati rice. The assumed price of Rs. 550 forother varieties is less problematical. Therefore, it is felt that earn-ings might reach a level of Rs. 300 million for superior rice, subject tothe condition that the present unsatisfactory procurement and exportarrangements are modified. The Mission thinks that trade in rice shouldbe conducted entirely by private firms. Coarse rice, which is producedmainly in East Pakistan cannot be exported in present circumstances wherePakistan receives wheat under PL 480. In the absence of this factor, itwould be quite possible that Pakistan might become a net exporter; however,several developing countries are presently planning substantially to stepup rice exports; to what extent these efforts would materialize in comingyears is difficult to foresee at this stage. With these two considerationsin mind, the Mission agrees with the Government in considering the exportof coarse rice as too remote a possibility for inclusion in the Plantargets.

Other Exports.

17. As far as paper and newsprint is concerned, the official targetseems to be highly speculative. The assumed increase in both domesticproduction of paper (by 230 per cent) and in domestic consumption (by 210per cent) contairsmargins of guesswork so large that it would be safe notto assume a significant increase in the residual export surplus. For aUlthe other miscellaneous manufactured goods, the Export Promotion Bureau hadpresented detailed targets most of which are strikingly optimistic; theyimplied an annual compound rate of increase of 35 per cent. The PlanningCommission reduced this to 21 per cent, and projected an increase fromRs. 230 million to Rs. 600 million by 1969/70. The iission thinks thatthis is still a very optimistic, though not altogether impossible, target;as a reasonable expectation a figure of Rs. 500 million is suggested.

AGRICULTURE

Introduction

1. The Third Plan calls for a sharp acceleration of growth inthe agricultural sector from the 3.5 percent per year during the SecondPlan to 5 percent per year. The main objectives of the Plan in theagricultural sector are:

(a) to increase the real income of farmers;

(b) to move towards self-sufficiency in food requirementsto the extent compatible with other needs of the economy,aiming at the same time, at improving nutritional standards;

(c) to promote agricultural development on a sound, self-propelling basis by further improvements in agriculturalorganizations and intensified programmes such as thedevelopment of cooperatives, marketing, storage andcredit facilities.

2. To achieve this transformation of agriculture, the highestpriority is being given to rneasures to increase water availability andthe use of fertilizer. The Plan calls for maintaining strong farmincentives and strong support for the entire range of agriculturalprograms. Allocations of public development expenditures for agricultureand water have been roughly doubled over the levels achieved in theSecond Plan and provisions are also being made for a considerableincrease in development credit for financing private on-farm investments.Together these programs amount to over 30 percent of planned developmentoutlays. If the Rural Viorks program is added the percentage rises toabout 35 percent. Provisions have also been rmade for increasing thesupply of essential farm inputs and gradually transferring responsibilitiesto the private sector. Research and extension activities are to bestrengthened further and increased emphasis is to be given to land con-solidation, colonization, range land development, soil conservation andagricultural marketing.

3. Production targets for the principal crops and growth inagricultural GNP are shown in Tables 1 and 2. On the basis of perform-ance during the Second Plan and projected inputs during the Third Plan,the production targets for the major crops appear to be within reach.However, in order to reach an overall growth rate of 5 percent peryear (28 percent in 5 years) in the agricultural sector, the output ofminor crops and livestock will have to be increased considerably abovethe 2.8 percent and 1.9 percent per year growth achieved during theSecond Plan period. There is some evidence that the past growth of minorcrops and livestock may have been understated, but there has beenrelatively little study of these sub-sectors and no positive programfor achieving the planned increases. The mission believes, therefore,that to achieve the projected 5 percent per year growTth rate, some of

- 8 -

the targets for major crops would have to be exceeded by a substantialmargin. This will call for an acceleration of the changes in agriculturewhich were introduced during the First and Second Plans. In additionto the increased level of public development expenditures provided inthe Third Plan, a much greater effort will have to be made to utilizefully the resources of the private sector. This means maximum encourage-ment to private on-farm investments through increased availability ofessential farm inputs at reasonable prices, ircreased farm credit andmaintenance of adequate incentives through a realistic price supportprogram. It also means a more rapid transfer of service and distributionfunctions such as seed and fertilizer distribution, plant protectionservices and mechanized services from overburdened public agencies tothe private sector. This would permit government to concentrate itslimited technical manpower on essential technical services such asresearch, extension and training activities.

Table 1: PRODUCTION TARGETS (1000 tons)

Percentage1964/65 1969/70 IncreaseBenchmark Target Third Plan

Rice 11,000 14,445 31Wheat 4 ,157 5,465 31Maize 505 786 56Other foodgrains 738 770 4

Total foodgrains 16,800 21,466 28

Sugar cane 20,750 28,300 36Oilseeds 1,171 1,806 54Jute (1000 bales) 6,200 8,000 29Cotton (1000 bales) 2,217 3,500 58Tea (million lb) 56 73.5 31.5

Table 2: AGRICULTURAL GNP OF PAKISTANAT FACTOR COST OF 1959/60

(Rs million)

AnnualPercentage

1959/60 1960/61 1961/62 1962/63 1963/64 Growth

Agriculture 16,813 17,285 18,183 18,272 19,366 3.6Major crops 9,634 10,015 10,715 10,606 11i526 4.6Minor crops 2,180 2,229 *2,316 2,381 2,038 2.8Livestock 3,719 3,793 3,868 3,942 14,016 1.9Fishing 1,111 1,137 1,169 1,219 1,255 3.1Forestry 109 111 115 124 131 20.2

Source: Interim Report of the National Income Commission,September 1964, Appendix XIV.

-9-

Sources of Growth

4. Experience during the Second Plan demonstrates clearly thatwater has been the major limiting factor in both West and East Pakistan.In West Pakistan, the problem has been one of trying to spread too littlewater on too much land. In East Pakistan the problem has been too muchwater in the rainy season and not enough in the dry season. This hasresulted in periodic droughts, floods, waterlogging, salinity and con-sequent low yields. The twenty percent increase in water availabilitydeveloped during the Second Plan has been the major growth factor inWest Pakistan. The improvements in flood control and drainage resultingfrom the Coastal E-nbankment Project and other smaller works have beenimportant factors in East Pakistan. With better control of water andreduced crop losses. more intensive cropping has been made possible andfarmers have been in a better position to invest in other inputs such asbetter varieties of seeds, fertilizers and farm machinery.

5. In the Third Plan, public investments in water will be roughlydoubled. Moreover, considerable encouragement is to be given to privatetubewell development in West Pakistm . The low lift pump irrigationprograms in East Pakistan will be accelerated and possibilities forlarge scale sale of small low lift pumps to individual farmers anddevelopment of private tubewells will also be given priority. Majoremphasis is to be given to completion of the Coastal Embankments Projectsand other on-going projects and rapid implementation of a major floodcontrol program for East Pakistan. As a result of these programs,in both wings 5.5 million acres of land will be newly irrigated and21.7 million acres will receive an increased water supply. This isexpected to provide about 35 to 40 percent of the planned increase inoutput and provide the basis for improvements in cropping practices andincreases in other inputs. Achievement of this target will require asharp acceleration in the rate of project preparation and executionin the public sector as well as maximum effort in the private sector.

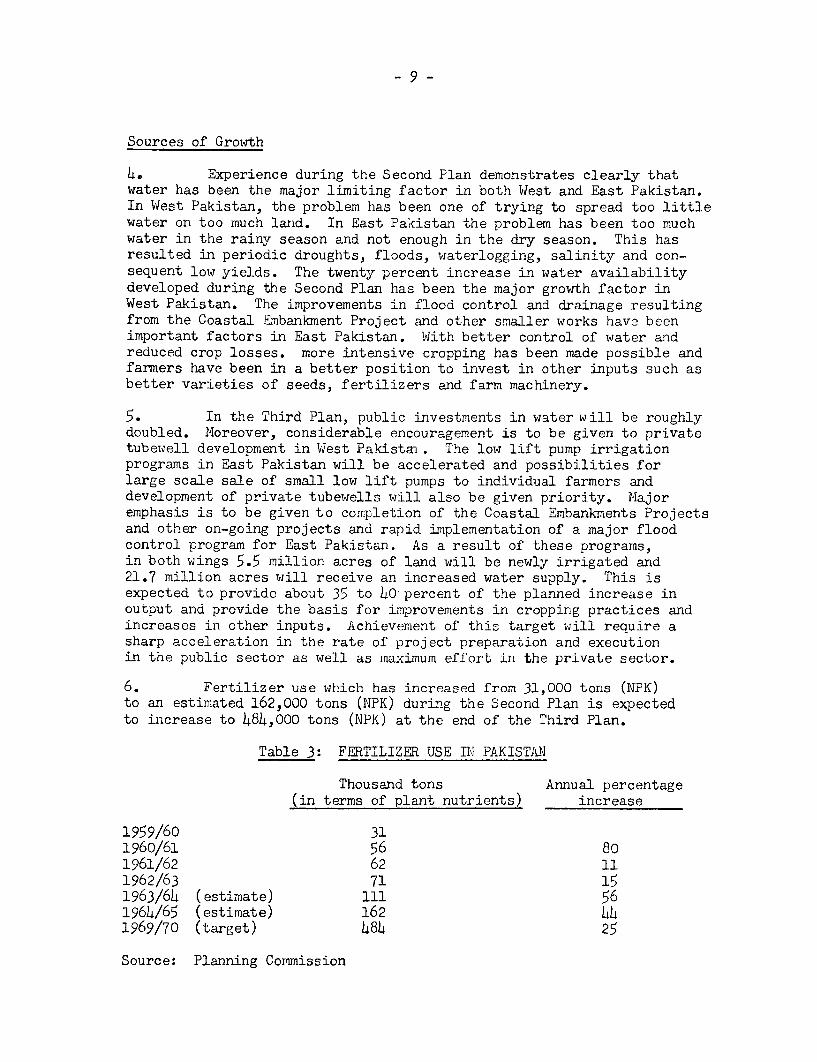

6. Fertilizer use which has increased from 31,000 tons (NPK)to an estimated 162,000 tons (NPK) during the Second Plan is expectedto increase to 484,000 tons (NPK) at the end of the Third Plan.

Table 3: FERTILIZER USE El PAKISTAN'

Thousand tons Annual percentage(in terms of plant nutrients) increase

1959/60 311960/61 56 801961/62 62 111962/63 71 151963/64 ( estimate) 111 561964/65 (estimate) 162 441969/70 (target) 484 25

Source: Planning Commission

- 10 -

The Plan calls for construction of additional fertilizer plants, con-tinuation of subsidies to offset high costs of domestic production,continued imports at a level sufficient to avoid recurrence of currentshortages, and further transfer of distribution to the private sector.Necessary credit arrangements are also to be provided. Fertilizer isexpected to produce about one-third of the planned increase in agricul-tural output. However, since demand is already in excess of domesticoutput, every effort will have to be made to step up imports and toexpedite construction of new plants.

7. Plant protection, improved seed, mechanization, improvedpractices and increased labor inputs are expected to provide the remain-ing 30 percent of the planned increase in output.

8. IWith the planned improvement in water availability and increasein fertilizer use, drought resistant varieties suitable for low fertilityconditions which have been in general use will not produce maximum returns.Fortunately, a number of high yielding varieties suitable for theseimproved conditions have been developed and are in various stages oftesting, multiplication and distribution. Some have already been dis-tributed and have made some impact on yields (e.g. cotton, sugar cane,rice) and can be expected to increase yields substantially as they aredistributed on a wider scale. TwJo promising wheat varieties, a Mexicanand an Australian, are almost ready for mass distribution and could havea dramatic effect on yields. The mission believes that an immediateexpansion and intensification of research activities aimed specificallyat developing high yielding varieties for all of the principal cropsunder different local conditions is essential for continued growthbeyond the Third Plan period. As applications of water and fertilizerincrease over the years, plant varieties will have to be repeatedlychanged to achieve best results.

9. Plant protection activities becorme increasingly important withintensification of production and higher yields. At present the costof the services are almost completely subsidized with the farmerproviding only some labor. On this basis, the government has been ableto provide services on only 12 percent of the cultivated area. Mostof the treatment has been curative rather than preventative. So longas free government services are provided, farmers will tend to avoidexpenditures for routine preventative spraying and dusting in the hopethat government services will be available when needed. However, withthe resources at hand, government has not been able to cope with thedemand and delays have resulted in substantial crop losses. Many of thefarmers would now be prepared to carry out such normal preventativetreatment at their own expense, particularly for orchards, sugar cane,cotton and other high value crops but materials are not readily available.Several private firms have started pilot services in order to meet thisdemand but have been restricted in the imports of materials and equipment.The mission believes that the present target to achieve 19 percent

- 11 -

coverage in 1969-70 is not adequate to achieve the growth projected.In order to achieve a higher coverage the farmers themselves must takeon greater responsibility. This is not possible so long as resourceallocation for plant protection is confined to the public sector. Themission believes that immediate steps should be taken to encouragemaximum private sector participation. This will call for the followingmeasures:

(a) Restricting free public plant protection services to locustcontrol and curative aerial spraying of areas with large scaleinfestation, and technical advice;

(b) Imposing a full charge for all other work, including smallscale curative and all preventative spraying work (most of thiswould be eliminated as rapidly as the private sector cansupply required materials and services);

(c) Liberalizing imports of plant protection materials and equip-ment until such time that local manufacturing can be established.

10. As shown below, the mechanization program c alls for a sharpincrease in government services for land development and private tubewelldevelopment in West Pakistan and low lift pump in East Pakistan.

Table 4: LOW LIFT PUIP IRRIGATION IN EAST PAKISTAIN

No. of Pumps Area Irrigated

1958/59 772 30,0001959/60 1,130 49,00O1960/61 1,267 65,ooo1961/62 1,543 98,0001962/63 2,024 133,0001963/64 2,456 156,ooo

Source: J. Hendry and U Hpu, "East Pakistan Agricultureduring the Third Five-Year Plan," July 196h, p.l5.

Table 5: NUMBER OF PRIVATE TUBEWILLS IN WEST PAKISTANJ/

Number ofPrivate Tubewells Number Installed Durin YearEnd of Year Total Agric. Dept. Private Drillers

1959/60 4,635 1,340 h89 85D1960/61 7,9L0 3,305 817 2,h881961/62 12,196 4,256 1,o40 3,2161962/63 17,600 5,400 1,088 4,2131963/64 24,200 6,400 1,410 4,9901969/70 (target) 70,000

1/ Estimates by Ghulam Mohammad, Senior Economist,Institute of Development Economics.

- 12 -

The Plan also provides for sale of low lift pumps to cultivators,encouraging the use of power tillers in East Pakistan, and expandeddistribution of improved implements. No mention is made of privatesales of tractors and equipment to larger farmers. As in the case ofother input items, the heavy reliance on government subsidized serviceshas limited the scope of development. Scarce foreign exchange has beenreserved for the government sector which has not been able to meet thedemand. Even so the private sector has been active, particularly inWest Pakistan where private well drillers are installing about three-fourths of the 6,000 to 7,000 private wells being installed annually andthe backlog of demand for farm tractors amounts to about 5,000 units ortwo and a half years' allocation of foreign exchange at current licensingrates. The mission believes that government mechanized services can beaugmented to a considerable extent by liberalizing the imports of tractors,pumps, equipment and materials. Moreover, before any substantial increasein the scope of government services, the possibilities of developingprivate sector interest should be carefully considered.

11. Improvement of cultural practices has been progressing slowlybut steadily and can be expected to continue at a somewhat more rapidrate with the use of more water, fertilizer and machinery. In this con-nection, the mission fully agrees with the Plan that there is a need forupgrading the quality of the extension services and providing betterfacilities so as to make them more efficient and effective.

Water Development

12. West Pakistan. The Third Plan calls for a dramatic accelera-tion of the water development program in West Pakistan. By the end ofthe Third Plan, out of a potentialfield availability of 114 millionacre feet it is proposed to develop 86 million acre feet or 75 percentof the total potential. This will require development of 24 millionacre feet as compared to 10.2 million acre feet developed during theSecond Plan. Out of a total conmanded area of 32 million acres in theIndus Basin, of which 27 million acres are presently cropped, about25 million acres will have been reclaimed and/or developed by the endof the Third Plan.

13. Out of the proposed increase of 24 million acre feet, theWater and Power Development Authority (WAPDA) is expected to develop15.8 million acre feet of ground wfater, 11.8 in the northern zone and4.0 in the south; private tubewell developments about 6 million acrefeet mostly in the northern zone; and about 2.2 million acre feet fromadditional river diversions and canal modifications.

1h. Acreage-wise, the development of 20.4 million acres is planned.WA?DA is responsible for 9.8 million acres, 7.3 million in the northernzone and 2.5 million in the south. ADC will complete drainage programsin 5.6 million acres carried over from the Second Plan and privatetubewells are expected to increase water availability on about 5 r,millionacres.

- 13 -

15. Since it will take another two to three years to undertakethe investigations needed for preparing the Master Plan for developmentof the entire Indus Basin, the government proposes to proceed as rapidlyas possible on the development of the sweet water areas where groundwater can be developed economically without prejudicing the developmentof the Basin as a whole. In the meantime, it is proposed to press forwardas rapidly as possible on the engineering of the more difficult areas.

16. At the time the mission was in Pakistan, IJAPDA had beenallocated Rs 2100 million for water development as compared to SecondPlan expenditures of Rs 14W4 million. The allocation has been subsequentlyraised to take care of the program acceleration outlined above. Althoughdetailed breakdowns are not yet available the total allocation for powerand water in West Pakistan has been increased from Rs 3800 million toRs 4370 million. Most of the increase is apparently in the water sector.Total investments would thus be of the order of Rs 2500 million or aboutdouble the expenditures in the Second Plan (exclusive of expenditureson the Indus Replacement Works).

17. On the basis of past performance and the present status ofpreparation of projects the mission doubts whether a development of thismagnitude can be carried out in a five-year period. In any case,considerable effort must be made to bring more schemes to the projectstage. At present, with the exception of the lower Thal Project, noneof the new schemes included in the Third Plan has reached the stage ofdetailed formulation. Moreover, progress on some of the "on-going"projects has been slower than anticipated at least in part because ofinadequate project preparation (e.g. Guddu and GM Barrage projects andSCARP II). A large number of consultants are currently engaged invarious studies which ought to lead to the identification and preparationof projects. Moreover, the Bank has organized a comprehensive study ofwater resources in West Pakistan which should lead to the determinationof a reasonable order of priorities.

18. Meanwhile, the mission believes that there is sufficient scopefor sizable public and private development of groundw7ater in the sweetwater areas and completion of on-going projects to permit a substantialincrease in the rate of water development in West Pakistan during thenext year or two. WAPDA should be prepared to give strong support to theprivate tubewell development by providing electrical connections andtechmical support to assure a maximum level of development.

19. East Pakistan. In East Pakistan the Plan calls for rapidcompletion of on-going projects, initiation of a major flood controlprogram, and a considerable expansion of the low lift pump irrigationprogram. Investments in the water sector will be more than doubled andthe projected irrigation, flood protection and drainage facilities areexpected to bring 1.8 million acres of new land into cultivation andexpand output on 2.7 million acres of presently cultivated land.

- 14 -

20. A large part of the increased output from irrigation isexpected to come from projects wihich have already made substantialprogress in the Second Plan. For example, the Kushtia unit of the GangesKobadak, the Dinajpur Low-lift Pump and Tubewell, the Dacca Demra andthe Chandpur projects which have not yet affected output materiallyare expected to be completed early in the Third Plan. These projectsare expected to bring about 450,000 acres of new land under irrigationand improve yields on an additional 90,000 acres.

21. The major increase is expected, however, from small low liftpump projects. The ADC and EPWAPDA plan to expand their programs toirrigate an additional 750,000 acres and the private sector is expectedto irrigate 240,000 acres mostly with small pumps of 1 cusec or less.Total projected development under these programs is estimated at almost1 million acres.

22. The Coastal Embankments project which has already providedprotection for an estimated 1,400,000 acres will be completed during theThird Plan and improve output on an additional million acres. Aninportant advantage of embankment work is that benefits can be realizedimmediately without a major change in cropping practices and furtherbenefits can be realized as cropping is adjusted to the improved conditions.

23. The Flood Control Plan can also be expected to provide similarimmediate benefits. However, at present the Plan presents only the broadframework and a listing of projects. Considerable engineering andhydrological studies will be required although some individual projectsmay be brought to the execution stage in the next year or two. Studiesby the Krug M4ission, General Hardin, and Professor Thijsse are insubstantial agreement that the problem of floods in East Pakistan is highlycomplex and unusually difficult. All suggest channel improvement andembankment as the practical means of improving conditions and that thesemeans should be developed cautiously with testing and careful observationof each project over a period of years. The reports stress the insatabi-lity of alluvial rivers in delta reaches, the uncertainties of siltation,the great size and power of East Pakistan rivers, ana the economicaspects of protection works. The strategy adopted by East PakistanWAPDA is to carry out construction in stages over the next decade,to observe effects of each project and to adjust plans as necessary.

24. The Bank has undertaken to review all aspects of the waterproblem with the Government of East Pakistan and, if it is considerednecessary, to provide a high level study group to recommend futuredevelopment alternatives. The mission believes, however, that in themeantime, there is sufficient scope for projects which would not prejudicethe direction of future development to achieve the proposed levels ofinvestments. These include completion of on-going projects, low liftpumping in areas protected from floods, and irrigation and drainageprojects in the lower delta where surplus water can be drained to the sea.

- 15 -

Agricultural Administration and Development

25. The public sector program for agricultural development haslagged behind targets set in the Second Plan period. The major reorganiza-tion of agricultural agencies carried out during the first several yearsof the Plan was undoubtedly a disruptive force. On the other hand, theperformance of the farmers has been much better than expected. The sharpincrease in private tubewell development and the unfilled demand fortractors, farm machinery, fertilizers and plant protection services showclearly that farmers have become development minded. The 3.5 percentper year increase in agricultural output which has been achieved duringthe past five years in spite of the limited availability of essentialfarm inputs and the inadequate farm credit system indicate a considerablescope for further acceleration of growth.

26. To date, developmental expenditures for agriculture properhave consisted largely of subsidies for various inputs and expensesassociated with building up a large governmental bureaucracy engaged inlarge part in administering a wide range of services. The purpose ofthe heavy subsidy element was to demonstrate the advantages of theseservices to farmers at a cost which would not be too burdensome to thesmall farmer. Lhe mission believes that the demonstration effect hasnow been accomplished on a wide enough scale so that most farmers areaware of the advantages of fertilizer as well as many of the othersubsidized inputs. Government has not been able to provide a sufficientvolume of fertilizer or services because of foreign exchange shortages,limited budgets and the difficulties of organizing these services onthe scale required. The mission believes that Pakistan could absorb amuch higher level of inputs if a larger share of the supply and servicefunctions were turned over to the private sector and government concen-trated on those areas which cannot be handled by the private sector.These include planning and execution of infrastructure investments suchas irrigation, drainage, flood control, soil conservation, grain storage,support for a commercially oriented credit system; adequate research andextension services; regulatory functions such as establishment andenforcement of standards; and a market support system to ensure adequateproduction incentives. Such a change in the role of government couldbring about a substantial savings in development expenditures andpersonnel currently earmarked for subsidized inputs and services. Thiswould make it possible to provide adequate support both in terms offacilities, funds and personnel for the essential agricultural functionsof government.

27. A basic change of this nature cannot be achieved overnight.Particularly, any reduction of the fertilizer subsidy should be approachedcautiously. The experience of recent reorganizations of agriculturalagencies shows clearly that changes must be introduced gradually andshould take the form of encouraging the private sector and reducing oreliminating functions and modifying government's role as the privatesector develops.

- 16 -

28. In the case of private tubewell development in West Pakistan,private firms are already installing 80 percent of the new wells. TheDepartment of Agriculture initially took the lead in demonstratina theprofitability of tubewell installations but the stage has now been reachedin many areas where the private sector can carry on with technicalguidance, advice and credit. On the other hand, the Department of Agri-culture and ADC continue to provide the oialy heavy tractor servicesavailable and they are not able to keep up with demand. As a consequenceindividual farmers have in some instances attempted to use light andmedium wheeled tractors for land levelling work and ruined their tractors.Moreover, development of new barrage areas such as G.A. and Guddu has beenheld back by the limited capacity of the government tractor pools. Themission believes that more rapid progress would be possible if governmentencouraged the development of private contractors to undertake suchl workrather than to rely solely on governument tractor pools.

29. In the case of fertilizers government has already reduced itsrole to some extent. The recent actions opening up fertilizer distribu-tion to private trade on a limited basis has caused a sharp increase infertilizer sales. A larger increase would have been possible if suffi-cient supplies had been available and if a more active role had beengiven to the private sector. Although the highest priority is beinggiven to measures to increase fertilizer use, fertilizer is currentlyin short supply and can be expected to remain in short supply for sometime since current demand exceeds installed capacity. Purchases werebeing delayed in the hope that fertilizer can be obtained throughcommodity aid sources. Fertilizer could not be obtained through U.S.sources and prospects are that there will be an inadequate supply forspring sowing and summer transplanting and fertilizer sales will probablynot increase at projected rates. This, in turn, will probably delayconstruction of new plants which will mean even larger future importrequirements which would again be limited by foreign exchange scarcities.To break this cycle and to ensure a rapid increase in fertilizer use,there is urgent need for immediate imports of a sufficient quantityto permit full decontrol of fertilizer distribution as well as aneffective extension service.

30. The present capacity of the domestic fertilizer industry is139,000 nutrient tons (including current expansion at Daud Khel andLyallpur), as compared to estimated 196h/65 usage of 160,000 nutrienttons. New plant capacity currently planned to come into production in1968 and 1969 total 203,000 nutrient tons. Additional plants plannedfor the Third Plan period total 185,000 nutrient tons. To the extentthese plants could be completed at an earlier date, substantial foreignexchange resources for fertilizer imports could be saved.

- 17 -

31. Similarly, to achieve projected levels of other inputs, thesupply of farm machinery, small low-lift pumps, plant protection materialsand improved seed will have to be increased at a much faster rate thancan be achieved through government action alone. Immediate steps shouldbe taken to liberalize current restrictions on imports and to encourageactive private sector participation in making essential farm input itemsavailable.

32. While considerable progress has been made in strengthening andexpanding research and extension services, a number of serious gapsremain. In the past water has been the most important limiting factor.As a result of the water development program water is no longer a limitingfactor in many areas. Suitable crop varieties and fertilizer are becomingincreasingly important. This calls for an accelerated research programaimed at developing more high yielding varieties responsive to conditionsof optimum water and fertilizer application. It also calls for a furtherexpansion in extension activities to expedite the transfer of researchresults from the research stations to the better farmers.

33. With the increased intensification of agriculture which iscurrently underway, the cash requirements of farmers for fertilizer,seed, farmn machinery, tubewells and land improvement can be expectedto increase sharply. To date, a substantial part of the investments intubewel'ls and farm machinery has come out of private savings and non-institutional forms of credit. Institutional sources provided aboutRs 120 crores of credit during the Second Plan period, of which about halfwas on medium and long term. This represented about 1.5 percent of theGNP generated in agriculture as compared to officially estimated require-ments of about 25 percent. The Third Plan provides for only a modestincrease in institutional forms of farm credit. "Taccavi loans" (directgovernment loans) will be maintained at about current levels and expend-itures on cooperative credit are to be increased somewhat. The Agricul-tural Development Bank of Pakistan, which has been the principal sourceof agricultural development credit, plans to increase its lendingoperations by about 50 percent in the next five years. The missionbelieves that a much greater increase will be necessary if the objectivesof the Plan are to be realized.

Conclusions

34. In summary, the proposed growth rate of 5 percent per yearduring the Third Plan is extremely ambitious. To achieve this ratean all-out effort will be required. Immediate steps should be takento assure action in the following key areas:

1. Water. A general acceleration of the public water developmentprogram, particularly the preparation of flood control, irrigation,drainage and reclamation projects integrated into the respective provin-cial water resource development plans and maximum encouragement toprivate tubewells and low-lift pump irrigation.

- 18 -

2. Fertilizer. Highest priority to fertilizer imports andconstruction of additional fertilizer plants to prevent recurrence ofcurrent shortages (including timely release of necessary foreign exchangefor fertilizer imports).

3. Strengthening and expanding extension and research activitiesin order to carry out an intensive campaign to stimulate proper use offertilizer (phosphatic as well as nitrogenous fertilizer), plant protec-tion measures, improved seed and improved cultural practices.

4e h. iiaxilnum encouragement to private sector participation in theproduction and distribution of all inpuits with a view toward reducinggovernment's role as rapidly as is consistent with an orderly transitionand acceleration in the use of necessary inputs.

5. 5. A sharp increase in institutional credit to farmers, particularlythe lending activities of the Agricultural Development Bank of Pakistan.

6. Maintaining adequate incentives to farmers through a mnar'ketsupport system aimed at a gradual improvement of the terms of trade.

ANNEX 3

INDUSTRY

GENERAL UIDUSTRIAL SITUATION - SECOND PLAN

1. During the First Plan (1955-196o) production in large andmedium scale industry rose by more than 80%, whereas the Plan targetwas for an increase of 65%. By contrast, with this impressiveshowing, little progress seems to have been made in small industries.

2. It is estimated that during the Second Plan large scalemanufacturing activity will rise by 87%, (13.3% per annum) whereasthe Plan target was for an increase of 65%. Although it isextremely difficult to assess the growth in small scale manufacturingdue to lack of reliable data, it seems that the increase was notabove 14% (2.6% per annum) against a planned increase of 25%.

3. The initial industrialization drive was mainly in textiles.In the Second Plan much slower growth than during the First Plan wasshown, the lead being taken over by petroleum products, chemicalfertilizers and basic metals. These production trends indicate thegradual shift taking place towards more sophisticated industries.In several instances (such as crude steel, sugar, paper, etc.),although production has increased, it has proved difficult to reachPlan targets, which in some cases were placed at a very high level.

Steel production did not get underway since one of the two plantsin the Plan (Karachi) was not started and the other (Chittagong)was not completed.

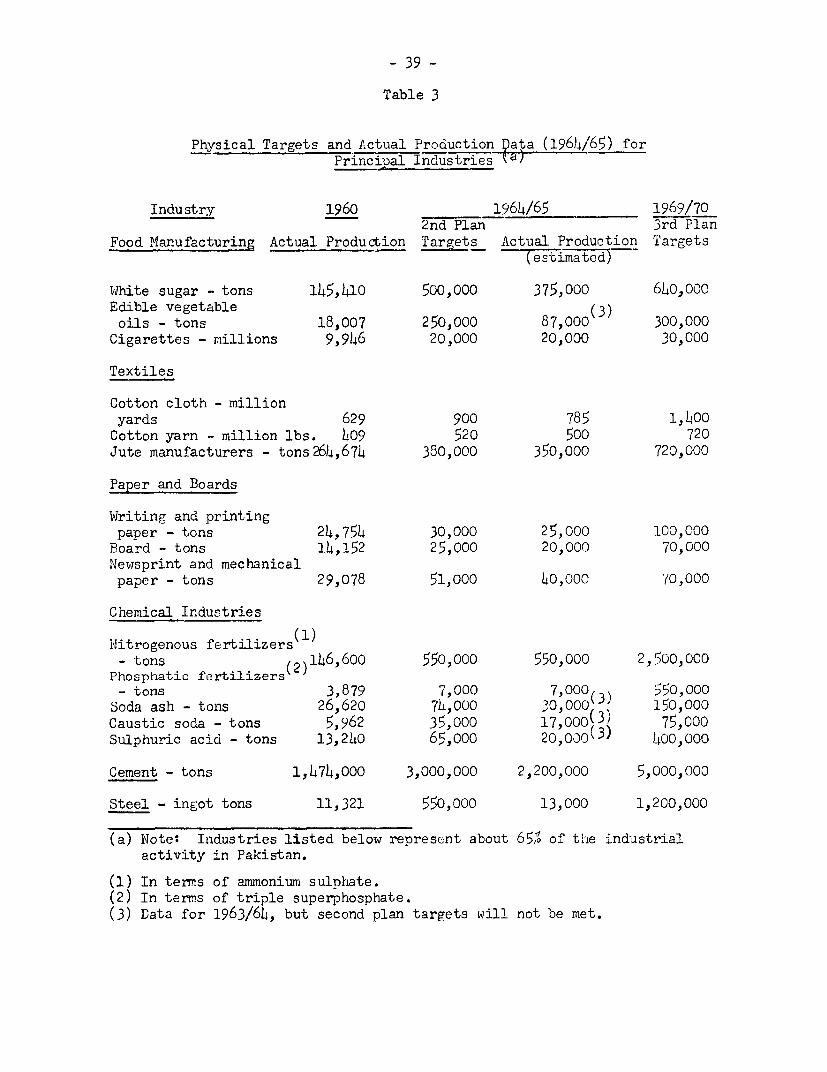

4. Physical production has about reached Plan targets forcigarettes, cotton yarn, nitrogenous fertilizers, but many itemsare lagging, such as white sugar, cotton cloth, all types of paperproducts, soda ash, steel and cement. Cement output is only 2.2million tons against an original Plan target of 3.0 million tons,but here the target may have been unrealistic. However, there isa shortage of cement within the country. Actual production andphysical targets in selected industries are given in Table 3. TheTable shows that for items accounting for 4C% of large scaleindustrial production, Plan targets have not been reached. However,in general the record is impressive.

5. The rapid growth of manufacturing activity has been madepossible by important investments and increased installation ofcapacity,by an improved supply of raw materials, the availability oflong term credit, especially from development banks, and theexistence of an increased demand for manufactured products.

6. Investments in organized industries reached Rs. 5,656million from 1960 to 1965, which is 96% of the Five Year Plan target.Private investment represented about three quarters of the total.Investments were somewhat higher in West Pakistan than in EastPakistan, which absorbed about 45% of total investments.

- 20 -

7. Although many companies are not operating at full capacity,and do not have a high degree of technical capacity, profits remainhigh. While some of the difference in profitability from oneindustry to the other represent varying amounts of capital investedper dollar of product, the degree of competition is also a majorfactor. In fact, the mission found that many companies had littlecompetition. This comfortable position is attributed to the smallsize of the market which allows only a limited number of producersand to the protective policy of high duties and quotas, especiallyfor consumer goods industries, which enjoy average tariffs of about50%. Since value added is often comparatively small and importedmaterials and components carry duties of about 10-12%, the marginof protection on domestic consumer goods production is obviouslyclose to 90% on the average.

8. The main factor hindering the full utilization of existingcapacity, the shortage of industrial raw materials, components andspare parts, has been partly removed. The ratio of licensing torequirements has increased in many sectors, sometimes very signifcantly.In 1964, fifty-one items were placed on the free import 'List and donot require import licenses. The list has been continued for thefirst half of 1965 and it is the stated government policy to maintainit within the limits of foreign exchange availability. As a resultof the liberalization policy, some industrial prices have been reduced,sometimes significantly.

9. In many cases, plant layout and material handling do notpermit the most efficient operations. Modern tooling techniques andmethods, production time standards and quality controls are also notful'ly understood by managers. These shortcomings, together withunder-utilization of capacity, have made much of Pakistani industryhigh cost and many companies (except for jute and sometimes for othertextile industries) are clearly not able to compete effectively ininternational markets.

10. Productivity per employee in many of the factories is belownormal standards for comparable industries elsewhere. This is dueto lack of training, not to any inherent inability of the workers toabsorb training and develop advanced industrial skills. The majorityof factory managers complain about the lack of skilled workers andsupervisors. However, a few of the factories have high productivity,with workers turning out products requiring a high degree of skill.

The Private Sector

11. To enable the development of industries in accordance withtheaims of the Second Five Year Plan, in July 1960 an IndustrialInvestment Schedule was established. The total investment targetwas Rs. 2,181 million, but by June 1963 investments of Rs. 3,151million had been sanctioned, 44% above that originally planned.A Revised Industrial Investment Schedule was issued in 1963. It

- 21 -

provided for the investment of Rs. 1,375 million additional. ByJuly 1964 Rs. 846 million had been already sanctioned and anotherRs. 810 million was expected to be sanctioned by June 1965. TheSchedule has been criticized as rather rigid and politically orregionally motivated. Some of this criticism seems justified.More flexibility in its use would be desirable.

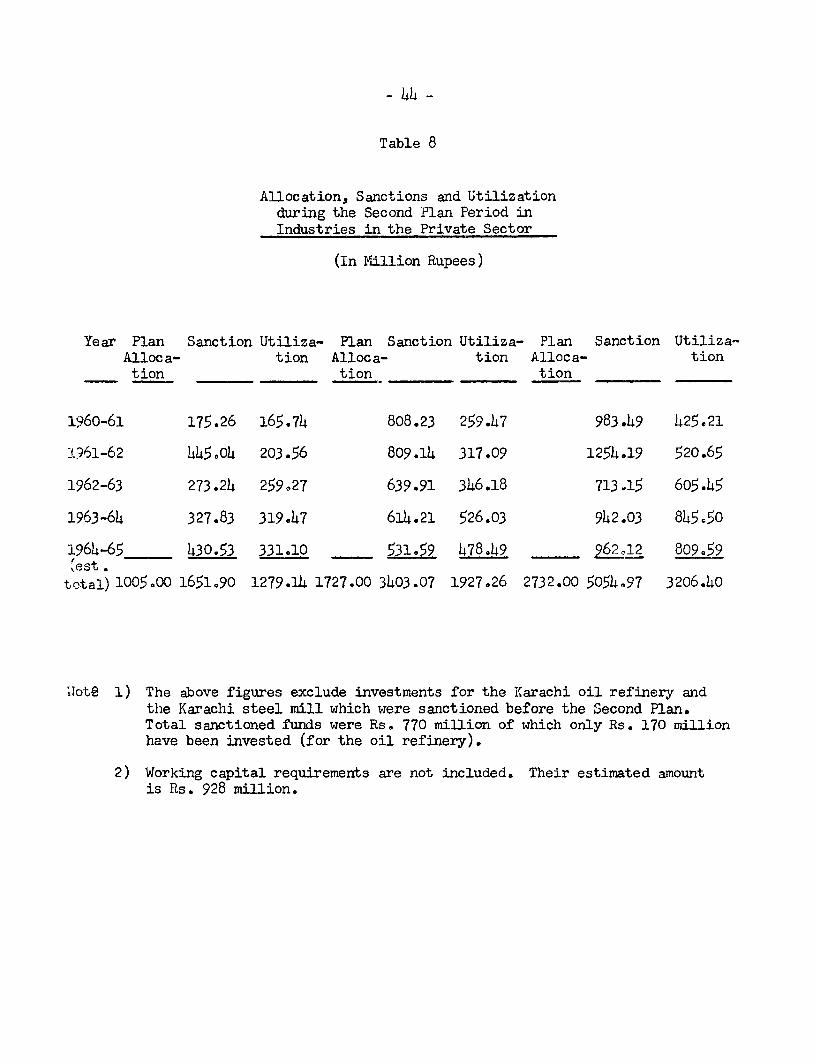

12. There is an inev-itable time lag with obstacles and delaysbetween the sanctioning of projects and the actual investment.Some sanctions are never used, others are revoked. It is estimatedthat for the old and revised Schedules combined, 63% of the totalsanctioned will be utilized by June 30, 1965. The Second Planallocation for the private sector, the amount of projects sanctio,nedand utilized during the Second P'lan period are shown in Table 81/

13. The private sector has done well in terms of investmentsduring the Second Plan. Total industrial investments (includingworking capital) are estimt ed at about Rs, 4,300 million againsta Plan allocation of Rs. 3,780 milliong'. This high level ofinvestments is not entirely reflected in the physical output ofseveral industrial branches which could not reach the Plan targets(see Table 3). This can be explained by a higher cost of invest-ments than originally estimated, but another reason is that the levelof industrial investment was substantially higher in the last twoyears of the Plan than during the first three years, and physicaloutput could not be immediately increased due to the usual lag timebetween construction period and beginning of production.

Industrial Financing

14. The Pakistan Industrial Credit Investment Corporation(PICIC) and the Industrial Development Bank (IDBP) are the two mainsources of medium and long term loans for industry. They provideboth rupees and foreign exchange. Loans from internationalfinancial institutions such as the US Development Loan Fund, theWorld Bank and the International Finance Corporation, or creditsreceived from foreign countries are channelled through theseorganizations.

15. PICIC is a well organized development finance company.Its management and staff are competent and the quality of itstechnical performance is high. Its financial performance is alsosatisfat ory. It has been increasingly profitable--net profitswere sufficient to raise the dividend paid on 1963 earnings from 6%to 7%, while still putting half of net profits in reserves inaccordance with PICICts policy. PICIC's total lending during theSecond Plan may reach about Rs. 750 mil'lion, almost all in foreignexchange. This is about one-sixth of estimated private sectorindustrial investment.

1/ The breakdown of sanctioned investments by industries is shownin Table 9 and the investment sanctioned through differentagencies is shown in Table 10.

2/ The latter figure does not include the Plan provision of Rs.650million for the Karachi steel mill which could not be startedduring the Second Plan period.

- 22 -

16. Some aspects of PICICI.s performance give cause for unease.Firstly, it has done a relatively small amount of underwriting. Ithas thus become primarily a lending, rather than an investing,institution, considerably restricting its role as a stimulator of thecapital marlct. However, very recently PICIC has become more activein underwriting and equity participations. PICIC should make adetermined effort to increase the financing of share capital, both bydirect subscription and by underwriting. In this connection, thegovernment should not delay its approval of more appropriate stand-byand underwriting commissions, so as to make such activitysufficiently attractive not only to PICIC, but also to other Pakistaniinstitutions which might join PICIC. Secondly, the average scale ofPICIC's operations is quite large, the result in part of the line ofdemarcation between PICIC and IDBP operations established by govern-ment. One consequence of this fact is that PICIC has tended tobecome less active in East Pakistan. Another consequence is thata substantial part of PICIC's operations are closely associated withPakistan's largest industrialists. This situation has created forPICIC the image of an institution designed to help the country'slargest industrialists rather than to stimulate new entrepreneurs.The situation can be corrected if appropriate policies are adopted.

17. The present division between the activities of PICIC andof IDBP should be changed. PICIC should be allowed to make smallerinvestments and IDBP to make larger ones. Reduction of thegovernment-established floor on PICIC's operations to, say,Rs. 500,000, would make it possible for PIC1C to be of greater useto medium scale enterprises. As the scale of enterprises isgenerally smaller in East Pakistan, the lowering of PICIC's minimumcommitment would remove one of the obstacles to PICIC's, as yet,limited activities in that Province. However, government shouldalso try to bring better understanding between PICIC and thePakistan Industrial Development Corporation (PIDC), since the latterhas a very large role in East Pakistan. Reduction of PICIC'slending floor should be accompanied by an increase in IDBP'sceiling, thereby making it possible for IDBP to increase itsprofitability. The new ceiling on IDEP's operations could beestablished around the level of, say, Rs. 2,500,0001/. The effectof this measure would be to increase IDBP's opportunities to makelarge scale, and hence more profitable, loans. As a result ofthese steps, there will be some overlap and competition betweenPICIC and IDBP. The industrial growth of Pakistan has now reacheda stage where two development finance companies can work side byside and have a volume of activity large enough to work on aprofitable basis. However, the prospective competition will beharmful, rather than helpful, to both if prospective clients areallowed to play one against the other, or if one institution lowers

1/ Foreign exchange loans are presently limited to Rs. 1.5 million.

- 23 -

standards of appraisal in order to capture business from the other.Accordingly, an understanding should be reached that neitherinstitution will consider investments in enterprises which havebeen rejected on their merits by the other.

18. It is difficult to appraise with exactitude IDBP'scontribution to the economic growth of Pakistan. IDBP is onlythree and one half years old, many of the projects it has financedare still under construction or in the early stages of operation.However, with total loans of Rs. 754 million from August 1961 toDecember 1964, IDBP is becoming, through the sheer volume of itsoperations, an influential stirnulator of industry and is bound tohave a major impact on industrial development.

19. IDBP has aimed at a wide diffusion of credit andbroadening of the base of industrial ownership. Its activity ishelping create a middle-class of entrepreneurs, especially in EastPakistan. The structure of industrial ownership in East Pakistanis overwhelmingly based on small scale enterprises, for whichmedium and long-term credit is of paramount importance. The sameis true of the less developed areas of West Pakistan.

20. The price of IDBP's rapid growth and its penetration tolevels and areas of enterprise not previously reached by institutionalfinance, have been some important weaknesses in the quality of IDBP'swork and in its financial condition. It is not sufficientlyinsulated from political pressire. The quick development of alarge volume of lending, the special efforts being made in EastPakistan and the small average amount of IDBP's loans have given itthe character of an instrument of political and social policy. Assuch, it is often exposed to pressures, particularly from theProvincial Governments which are charged with responsibility forindustrial affairs. These pressures can be partly counteracted bya strong Board with a clear cut business orientation and by anexperienced professional staff, under tough direction, applyinghigh technical standards in the selection of projects.

21. IDBP has reported significant deferrals and arrears asto principal and interest. An examination of past appraisalssuggests that more loans (perhaps 20% of the portfolio) are likelyto be in default, since the enterprises may not be able to generatethe cash necessary for timely repayment.. IDBP appears to bereluctant to collect loans in arrears or to enforce its security,because of the risk of placing the borrower in bankruptcy, perhapsclosing the enterprise, and attracting critical comment in thecommunity.

22. A principal reason for this high level of defaults andarrears is that IDBP's appraisals still leave much to be desired.It is a consequence of the pressure under which IDBP work to lendrapidly, of the inadequate training of its staff, and of the fact

that effective investment-type appraisal is difficult for thesmall enterprises with which so much of IDBPPs operations areconcerned. IDBP has sought to counteract this situation byplacing great emphasis on security, but strict security and othercovenants are not a satisfactory substitute for judgment based onan assessment of financial and technical merits. Also, securityis of little value if IDBP is lenient in enforcing it. Themission believes that IDBP should decide to act firmly to collectdebts in arrears and to make use of its special powers to enforcesecurity.

23. A second matter of concern is IDBPrs capital structure.IDEP has insufficient equity. Its debt-eouity ratio was about19:1 at the beginning of 1964. This is far in excess of the 5:1ratio allowed in the IDBP ordinance. Moreover, IDBP's reservesare growzing at an inadeouate rate, particularly in the light ofrepayment performance.

Public Financed Sector

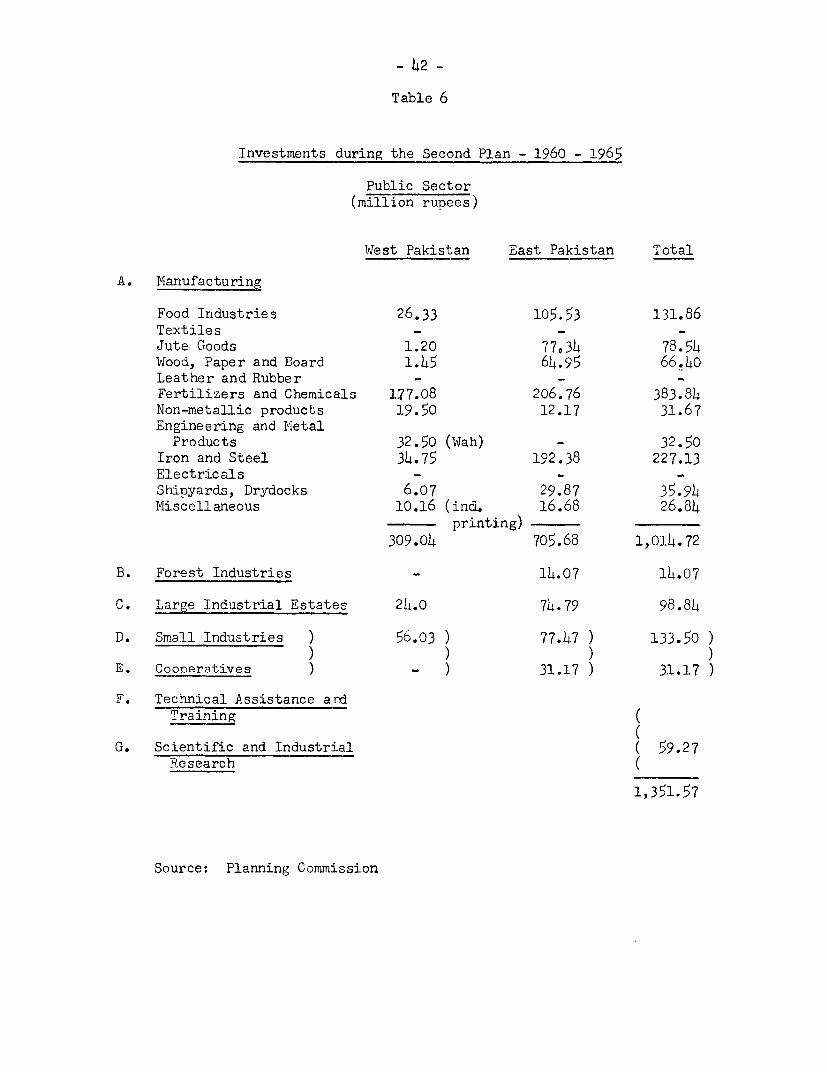

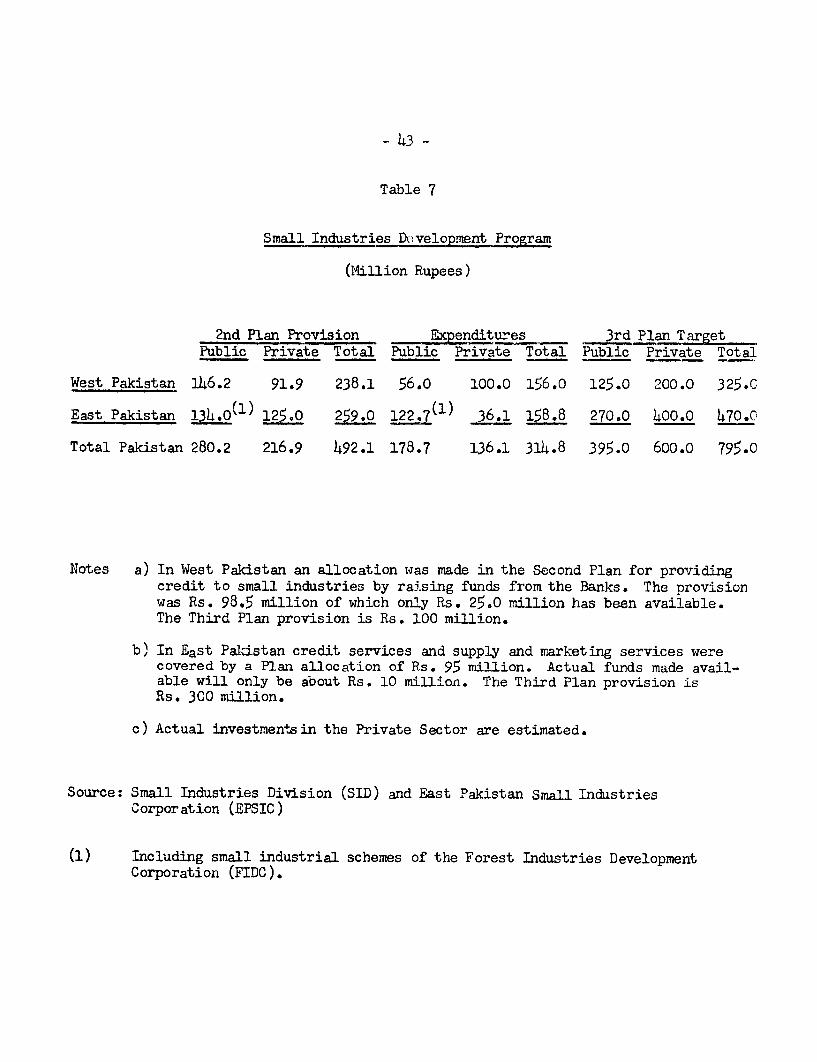

2h. Government investment in large scale industries con-templated in the Second Plan was Rs. 1,076 million (of which Rs.448million was for chemical and fertilizer plants). In addition, theSecond Plan made a provision of Rs. 100 million for the creation oflarge industrial estates in both the Provinces to assist theestablishment of industries. Another provision of Rs. 280 millionwas made to assist the development of small industries throughsmall industrial estates and technical assistance. The totalallocation for the public financed sector was Rs. 1,456 million.Actual investments are estimated at Rs. 1,352 million (Table 6).The main shortfall has occurred in investments for small industrieswhich amounted to Rs. 178.7 million against Rs. 280 million in thePlan (Table 7). The program for small industries is running verymuch behind schedule.

25. Most of the investments have been made by the PIDCwhich have spent Rs. 1,015 million, 70% in East Pakistan. Thereason for larger investments in East Pakistan is because thegovernment considered that the desired level of industrial invest-ment could not be reached by relying only on the limited financialand technical capacity of local private investors. The Wv4estPakistan PIDC has been much less active because the private sectoris rnuch more developed in that Province. During the first fouryears of the Plan, seven projects have been completed by PIDC inEast Pakistan (4 jute mills, 1 sugar mill, one pharmaceuticalfactory and one fertilizer factory). Most of the major schemesowned by EPIDC have a high utilization of capacity, but their costsare rather high and the return on sales and/or 4-nvestriient is lowE/by Pakistan standards. EPIDC itself recognizes that it has stillto make substantial progress to become an efficient organization.

1/ With the exception of the E?IDC jute mills.

- 25 -

However, the mission feels that, especially in East Pakistan,PIDC has played a useful role in promoting new investments in

some fields (such as fertilizers) where private investors werenot forthcoming, at least at the early stage.

26. It is the declared policy of government to disinvestthe PIDC-owned plants if and when private enterprise becomesinterested in the industries offered for sale. However, dis-investments have been relatively small and perhaps the PIDCshould be less reluctant to sell their successful schemes tothe private sector.

TARGETS OF THE THIRD PLAN

27. The industrial sector of the Plan had been programmedonly in a general way when the mission visited Pakistan. InWest Pakistan an inventory had been made of major industrialprojects underway or in the planning stage. In East Pakistanthis analysis was still in progress. A few preliminary studieshave been undertaken for some projects in the chemical andengineering sectors. This work had not yet provided a sub-stantial basis for Plan projections.

28. Based on general projections given to the mission,production by industries producing investment goods and inter-mediate products would increase at 10.6% per annum compared with7.9% for consumer's goods industries. The share of the formerin total industrial output would rise from about 33% in 196h/65to about 36% in 1969/70. The manufacturing sector as a wholewould grow by 9.5% per annum versus 9.2% per annum during theSecond Plan. Large scale industry would grow by 12.1% perannum compared to 13.3% (see Table 10 a). The contribution ofindustry to economic growth during the Third Plan would be about18% as compared i%ith 20%5 in the Second Plan.

29. It is assumed that the relative share of factoryindustries in the total manufacturing output would increase atthe expense of cottage and other small scale industries. Thoughthere would be a higher growth than in the past in the latteractivities (by about 3% a year versus 2.6% during the Second Plan),the share of small scale industries would decline from about 32%of total industry in 1964/65 to 24% in 1969/70. However, theproductivity assumption for small industry are not specificallystated. The basic data available for estimating value added inthis sub-sector are extremely weak. At the present stage, it isdifficult to say whether the small scale industries are expandingor shrinking. The labor productivity in the urban smallindustries has probably increased slightly, but the relative shareof small industries in the total labor force may have decreased.The mission recommends that necessary benchmark data should becollected through a quinquennial census of small and o ttageindustries in both the Provinces.

- 26 -

30. The employment impact of the proposed expansion infactory industries is still under study. It is assumed thatthe measures for employment promotion in organized industriesin the urban areas will continue and include fuller utilizationof existing industrial capacity by the introduction of multipleshifts and removing of handicaps such as non-availability of rawmaterials and spare parts. However, in some industries such aspetrochemicals and steel, it is necessary to use high productivitytechniques. Since the Third Plan stresses the need to developmore capital intensive industries it will be difficult to reconcilethe need to provide more industrial employment opportunities,especially in the urban areas uwith the introduction of industrieswhich are not labor intensive.

Evaluation of Targets

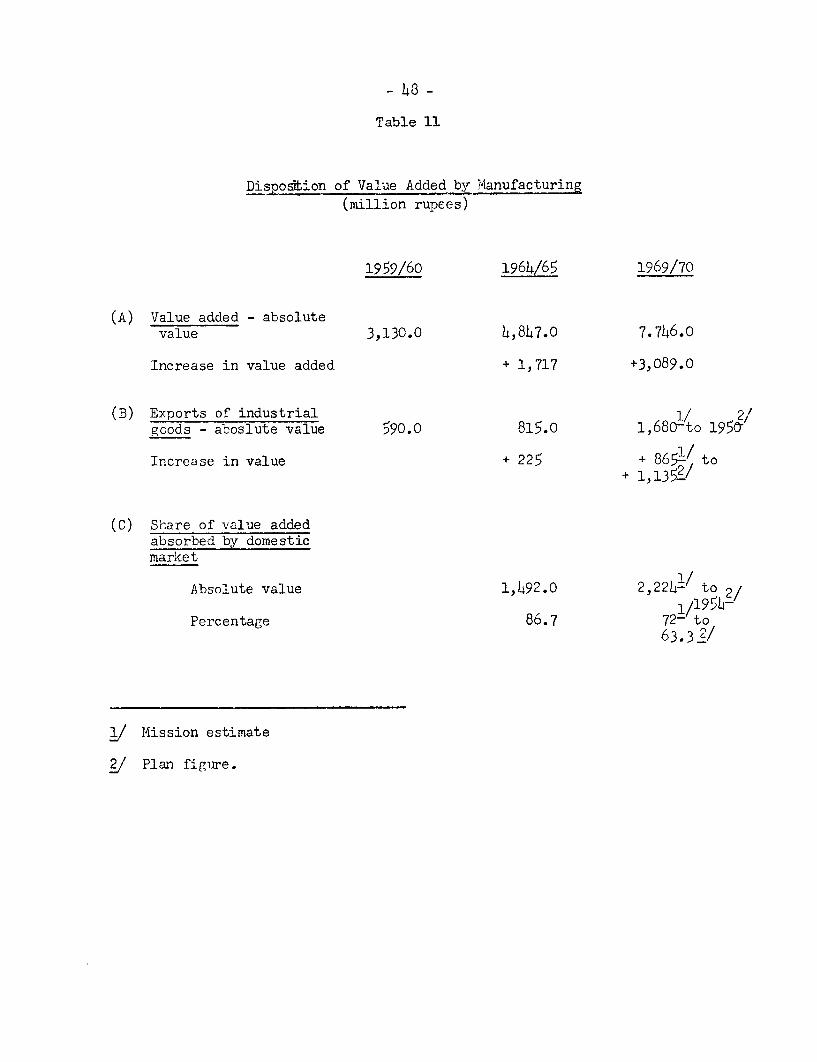

31. Of the total increase of Rs. 3,089 million (see Table11) in value added in manufacturing during the Third Plan, thePlanners expect Rs. 1,954 million to be absorbed by the domesticmarket and Rs. 1,135 to be exported. Rs. 900 million of thedomestic absorption would be import substitution and Rs. 1,054million normal increase in domestic demand. Thus, about two-thirds of the increased industrial production will be directlyrelated to the "international" sector of the economy, i.e.export and import substitution, emphasizing the need forgreater attention to Pakistan's competitive position.

Increase in Exports in Relation to Domestic Demand

32. The above data indicate that 63% of the increase inindustrial production is projected to meet increases in domesticdemand and 37% is for exports. The percentage for the domesticmarket was 87% during the Second Plan. The domestic absorptionof manufactured goods was calculated as a residual between totalplanned increase in industrial output and export projections formanufactures which, in the Plan model, are treated as an independentvariable. This should, of course, be checked by independentestimates of domestic demand for various types of products, butthis had still to be done when the mission was in Pakistan. Suchestimates raise many practical difficulties, and are necessarilysubject to a wide margin of error. An independent check by themission on prospects for exports of manufactured goods by maintypes of industry suggests that the necessary increase indomestic absorption in relation to the production target is under-estimated and that the domestic market would have to take 72%rather than 63% of the increase in industrial production (Table 11).

33. The projected exports of manufactured products, accordingto the Plan and by the mission, are summarized in the followingtable:

- 27 -

Projection of Exports of ManufacturedProducts

(in million rupees)

1964/65 1969/70Plan Mission

Jute goods 350 800 700

Cotton Manufacturers 170 350 350

Processed Fish 4 150 120

Paper and Newsprint 20 50 20

Other Manufacturers 230 600 500

815 1,950 1,680

Import Substitution

34. The major savings in imports as of 1970 would be inchemicals, basic metals, food industries and metallic minerals.Together, these industries would account for 80% of the total

import savings. The Pakistani planners 1-ve calculated the importsubstitutions on the basis of major industrial projects which willcome into production during the Third Plan (steel, rayon, soda ash,cement, glass). As noted above, total import substitution forindustrial goods would reach about Rs. 900 million in 1969/70.

35. The following comments apply to the plans for individualindustries:

a) The targets for import substitution in non-metallicminerals (mostly cement) and in pulp and paper areboth feasible and justified economically. Thereis a need for more cement and paper capacity andexpansions are already taking place to meet anincreasing demand.

b) In steel, the import substitution projected for1969/70 is only partly assured, even assumingthat the steel plant at Chittagong under con-struction attains the scheduled rate of production.However, the Karachi steel plant is not yet startedand it will take a number of years before thescheduled capacity of 45O,000 tons can be fullyutilized.

- 28 -

c) Rightly no provision has been made for importsubstitution by new projects to be completedor started during the Plan in the field oftransport equipment, heavy electricals andmachinery (heavy engineering and machine tools).These projects consitute either pure assemblyoperations with low foreign exchange savings(e.g. transport equipment, electrical machinery)or are not likely to start production during thePlan (i.e. machine tools factories).

d) It is not clear how much of the import sub-stitution projected for chemicals for 1970 iscovered by projects already in operation orunder construction. One item is caustic soda,of which production has started in Lahore.There are projects for petrochemicals based onthe Mari natural gas field and/or utilizing rawmaterials supplied by the Karachi refinery.The economics of manufacturing many of thechemical items suggested are rather doubtfulbecause of the smallness of the local market.Hence, very great efforts will be required toreach the targets set for 1970.

36. Despite the mission's reservations on some of theseindustries, we feel that the target of Rs. 900 million of importsubstitution may occur during the Third Plan, though some of theprojects suggested will not be ready in time to yield importsubstitution by 1969/70. Since import substitution will occuronce the plant is built, whether or not it is economic, one canspeak wJith greater assurance about import substitution capabilitythan about exports.

37. A question that remains is whether the mission's lessoptimistic view of Pakistan's export prospects than those heldby the Planning Commission casts doubt on the feasibility of thegrowth targets in manufacturing. Since the items on which wehave doubts (jute goods and processed fish) probably have a some-what inelastic demand in Pakistan, this would seem to be the case.However, the magnitudes are not large enough to be of major con-cern in relation to total output.

Volume of Investment

38. A summary of fixed investment in manufacturing asprojected in the Plan is presented in the following table:

- 29 -

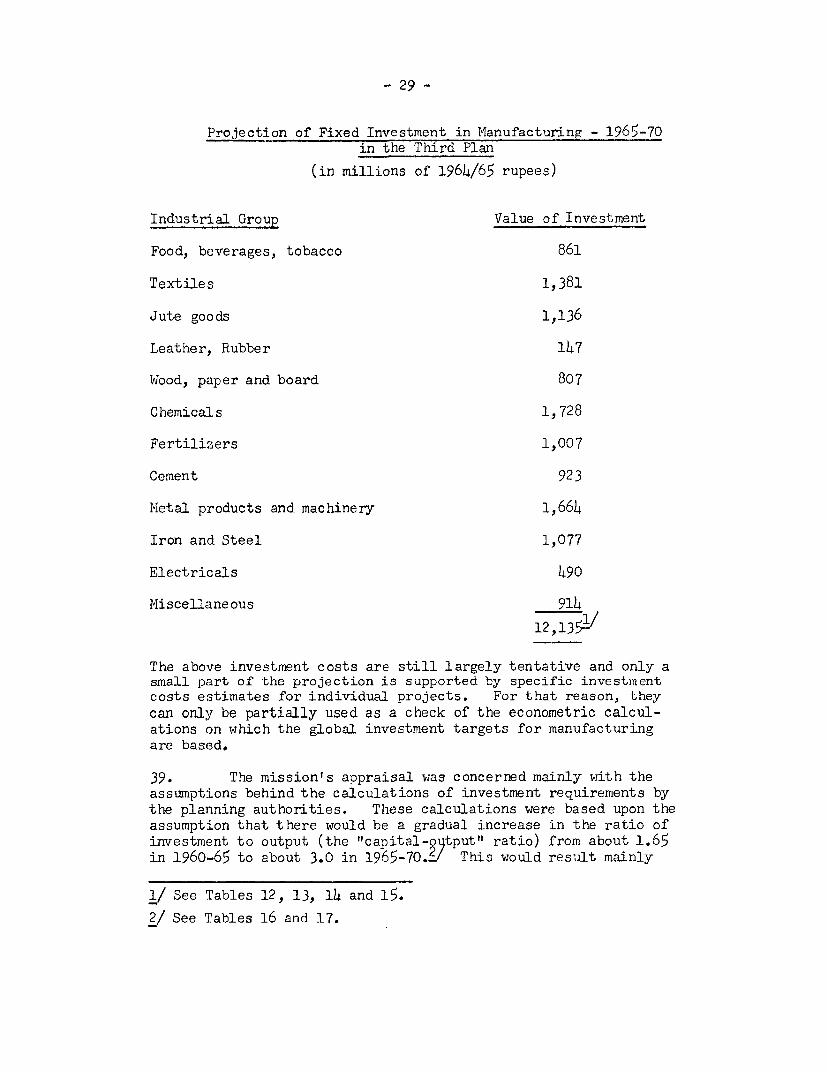

Projection of Fixed Investment in Manufacturing - 1965-70in the Third Plan

(in millions of 1964/65 rupees)

Industrial Group Value of Investment

Food, beverages, tobacco 861

Textiles 1,381

Jute goods 1,136

Leather, Rubber 147

Wood, paper and board 807

Chemicals 1,728

Fertilizers 1,007

Cement 923

Metal products and machinery 1,664

Iron and Steel 1,077

Electricals 490

Miscellaneous 914

12,135-/

The above investment costs are still largely tentative and only asmall part of the projection is supported by specific investmentcosts estimates for individual projects. For that reason, theycan only be partially used as a check of the econometric calcul-ations on which the global investment targets for manufacturingare based.

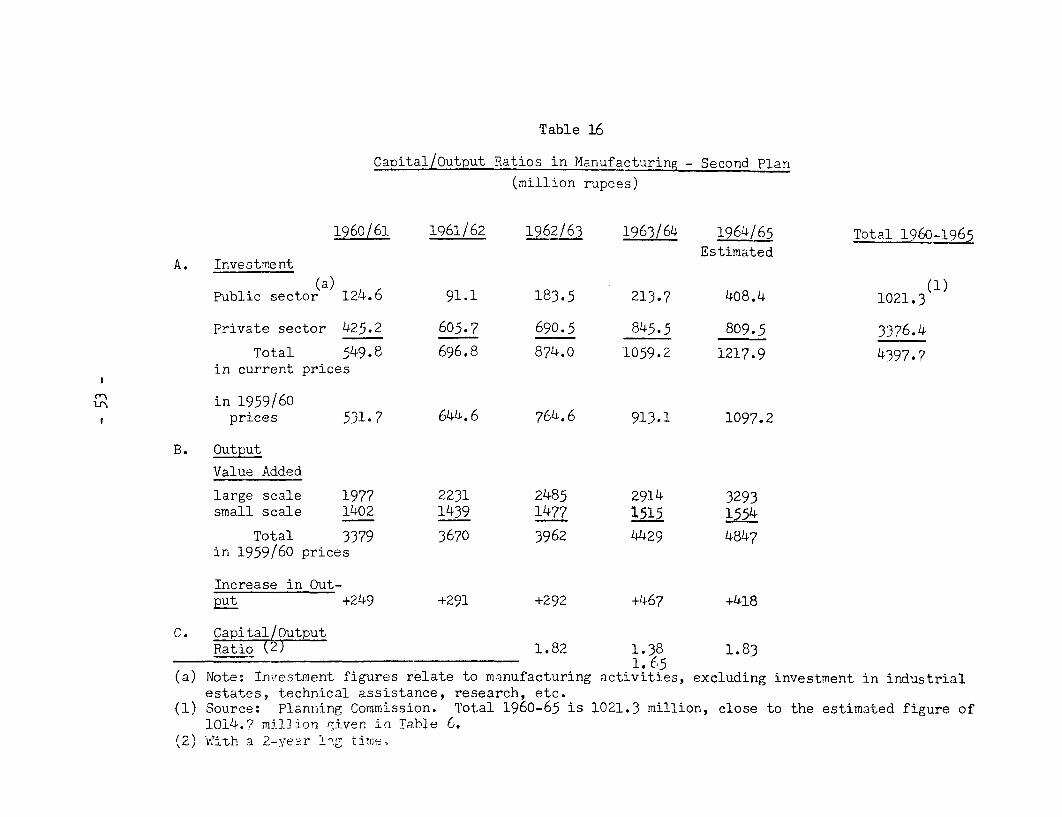

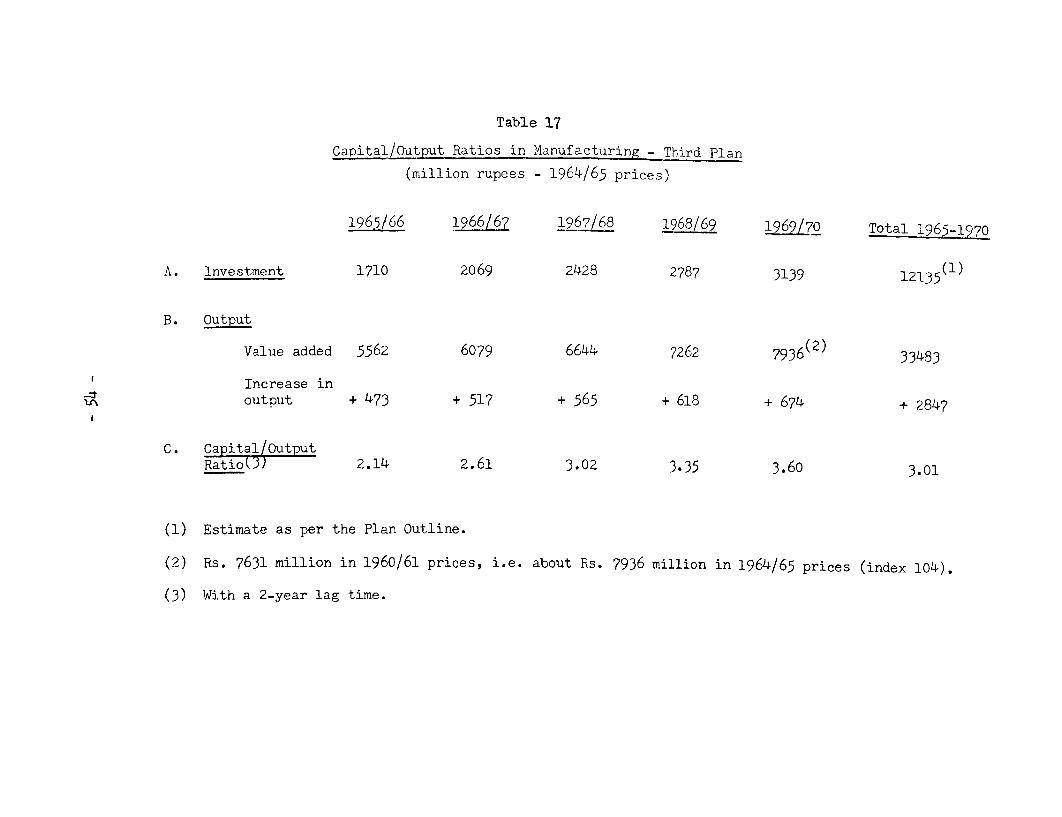

39. The mission's appraisal was concerned mainly with theassumptions behind the calculations of investment requirements bythe planning authorities. These calculations were based upon theassumption that there would be a gradual increase in the ratio ofinvestment to output (the "capital-o itput" ratio) from about 1.65in 1960-65 to about 3.0 in 1965-70.~/ This would result mainly

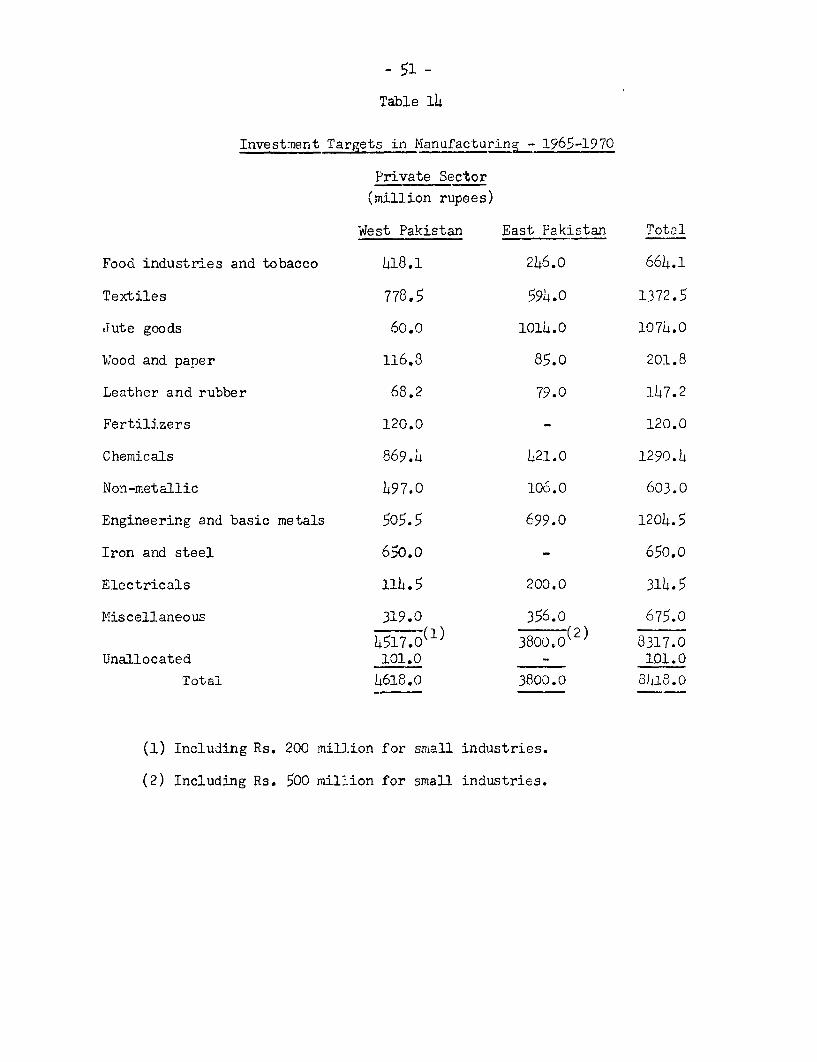

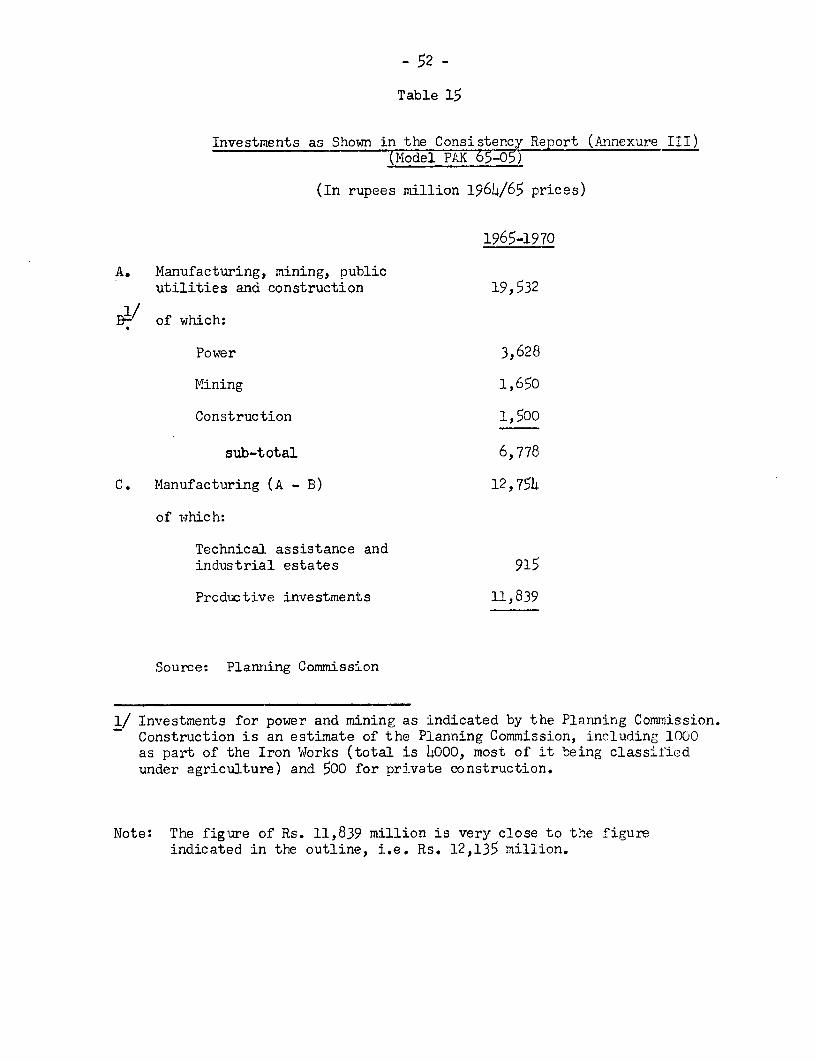

1/ See Tables 12, 13, 14 and 15.2/ See Tables 16 and 17.

- 30 -