-1- UNITED STATES DISTRICT COURT DISTRICT OF CONNECTICUT ______________________________________________X UNITED STATES OF AMERICA, -against- 3:13 cr 00170(HBF) RIVERVIEW SALES, INC. and DAVID LAGUERCIA Defendants. ______________________________________________X SENTENCING MEMORANDUM ON BEHALF OF THE DEFENDANTS RIVERVIEW SALES, INC., AND DAVID LAGUERCIA ALTCHILER LLC Robert Y. Altchiler, Esq. Attorney for the Defendants 111 Saugatuck Avenue Westport, CT 06880 (203) 222-3838 590 Madison Ave., 21 st fl New York, NY 10022 (212) 541.242

Riverview and Laguercia Original Sentencing Memorandum Final Sentencing ROBERT ALTCHILER Memorandum

Dec 29, 2015

Submitted to Scribd in response to ATF post sentencing statement taking a bow for its work in CT, and yet again misleading the public as to who oput the community in danger.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

-1-

UNITED STATES DISTRICT COURT DISTRICT OF CONNECTICUT ______________________________________________X UNITED STATES OF AMERICA,

-against- 3:13 cr 00170(HBF)

RIVERVIEW SALES, INC. and DAVID LAGUERCIA Defendants. ______________________________________________X

SENTENCING MEMORANDUM ON BEHALF OF THE DEFENDANTS RIVERVIEW SALES, INC., AND DAVID LAGUERCIA

ALTCHILER LLC Robert Y. Altchiler, Esq.

Attorney for the Defendants 111 Saugatuck Avenue Westport, CT 06880 (203) 222-3838 590 Madison Ave., 21st fl New York, NY 10022 (212) 541.242

-2-

Introduction

David LaGuercia is a 57-year-old man who stands before this court convicted of

two misdemeanors, both arising from his operating as a Federal Firearms Licensee

(“FFL”). Riverview Sales, Inc. (“Riverview”), the co-defendant, is Mr. LaGuercia’s

company, and stands convicted of a single misdemeanor, also arising from Mr.

LaGuercia’s operating as an FFL. Neither Mr. LaGuercia, nor Riverview, has previously

been convicted of any crime, whether related to any FFL, or otherwise.

Two comprehensive and exhaustive Pre-Sentence Reports (“PSR”s) have been

prepared by the United States Department of Probation (“Probation”), one for Mr.

LaGuercia and one for Riverview. Based on the investigation conducted by Probation,

and its analysis of the information contained in the PSRs, the Probation Officer’s

Evaluation is that a “short period of probation and a financial penalty appear adequate to

address the conduct in the offense of conviction”. (Riverview PSR ¶ 45). We agree and

respectfully request the Court impose a sentence reflecting that evaluation.

As the two reports clearly reflect, the main thrust of this case is Riverview and

Mr. LaGuercia’s failure to properly maintain accurate records required by law. The case

also relates to the use of information or intelligence (information provided by customers,

understanding of regulations, and corrective instructions provided during earlier

inspections, etc.), operational security, staffing, and policies and procedures for the

-3-

operation of its business as an FFL, and as one of the highest volume gun dealers in the

State of Connecticut. More specifically, as to sales volume, as Mr. LaGuercia estimated,

Riverview sold roughly 6,000 guns annually (Riverview ¶32, LaGuercia ¶71). (The exact

number for sales from January 1, 2010 through December 31, 2012 is closer to 17,542.)

The defendants have accepted responsibility for their failures in these areas.

There is no doubt that the defendants failed to comply with a number of the

statutory requirements that govern FFLs and important recordkeeping obligations related

to regulating the firearms industry. The defendants were legally responsible for

Riverview’s compliance with laws and regulations and for the non-ultra vires actions of

employees transacting business in the name of the FFL. Simply put, the defendants failed,

and their violations bring them before this Court for sentencing upon their convictions,

each having pled guilty. Mr. LaGuercia, who has led a predominantly law-abiding life

asks the Court to understand that his transgressions arose from the way he ran his

business, and that he never has and never would, nor has, intentionally put someone at

risk.

The main import of the paperwork requirements of the Gun Control Act is making

sure people who shouldn’t possess guns don’t possess them, and that firearms may be

effectively and efficiently traced. Since becoming an FFL, Mr. LaGuercia had never

failed in either pursuit. More specifically, Mr. LaGuercia has never knowingly permitted

a firearm to be sold to a prohibited person and has never failed to effectively assist any

request for a trace of a weapon. Importantly, the paperwork failures have never impacted

the government’s ability to quickly trace any weapon sold at Riverview.

-4-

The Guidelines

Pursuant to the Guidelines Riverview has a culpability score of 3 (Riverview PSR

¶39), placing it in Zone A, with a corresponding potential fine range of $3,000 to $6,000.

Mr. LaGuercia’s total offense level is 4, with no prior criminal history, which places him

in Zone A under the guidelines. (LaGuercia PSR ¶4). The corresponding guideline range

is 0-6 months and a fine range of $250 to $5,000. Defendants with Zone A sentencing

ranges of 0-6 months are eligible for straight probation, probation with confinement

condition, or a fine as a sole sanction.

The PSRs

The PSR Addenda accurately reflect the defendant’s sentencing objections with

one exception. The defendant requested the reports contain the following:

In Riverview ¶ 26 and ¶ 27, the report address [sic] certain conduct by fired Riverview former employee Kristopher DiBella who admitted selling ammunition to a felon. DiBella was actually accused by that felon and the felon’s wife of repeatedly selling firearms to the wife of that felon for the felon’s possession and use, and repeatedly giving the felon access to firearms at shooting ranges in Connecticut. More specifically, the felon’s wife explained to federal agents that on Father’s Day 2011, DiBella brought firearms to a Connecticut shooting range and allowed the felon to use and shoot a .45 caliber pistol, a 10 mm pistol, a bolt action rifle, and a semi-automatic rifle DiBella said he had built. According to the felon’s wife, this incident occurred well after DiBella had been told her husband was a felon. The ATF acknowledged during the revocation hearings that Mr. LaGuercia was not involved in any of this activity involving the felon and his wife, but cited the sales of ammunition as a grounds for revocation, based on the doctrine of respondeat superior.

-5-

Impact of the Case and Other Factors on the Defendants

Mr. LaGuercia and Riverview have already sustained what might retrospectively

be viewed as a business “Death Penalty” in the form of the revocation of the FFL, on

December 20, 2012, an action that arose from many factors, but was indisputably in

response to the horrific events in Newtown, just days earlier, as well as what appears to

have been an intentional effort to blame Mr. LaGuercia and Riverview for what occurred

at Newtown.1 The revocation and the media strategy crippled Mr. LaGuercia and

Riverview. As Probation explains in its evaluation, the “media attention both the store

and Mr. LaGuercia has received as a result of the shooting…appears unfair and has

played at least some role in the decline of sales. As a result of no longer having the

Federal Firearms License the future of Riverview Sales, Inc. is dim.” (Riverview PSR ¶

45).

Contrary to the repeated efforts to make the defendants a face of the massacre,2

their conduct, Probation’s investigation, and the PSRs demonstrate the unfair nature of

that propaganda, and the apparent business impact it has taken. In concisely explaining

Probation’s findings, the LaGuercia PSR notes that the:

1 According to members of the legal team that represented Mr. LaGuercia during

the revocation proceedings, including the revocation hearing and the four months between the close of the hearing and the December 20 revocation, a full revocation had not been a part of the ongoing negotiations, directed at resolving the administrative case. Rather, according to participants, during the last conversation about an appropriate sanction, a temporary, 90-day shutdown of Riverview seemed to be acceptable to the government.

2 The government’s effort succeeded, in that there are probably as many photos of Riverview Sales in articles about the tragedy at Newtown as there are of Sandy Hook Elementary School or Nancy or Adam Lanza.

-6-

…evidence in this case reveals that Riverview Sales, Inc. was

lacking in regards to the specificity of the record keeping necessary

for the industry, in which they are a part of. As the owner and

operator of Riverview Sales. Inc, Mr. LaGuercia does and should

receive the bulk of the blame for the violations which occurred. Mr.

LaGuercia is the one who has to answer for one of his employees

selling a firearm to a prohibited person and another incident where a

firearm was stolen out of his store, in plain view of other employees

and customers. In regard to the blame, shaming and media attention

Mr. LaGuercia and Riverview Sales, Inc has received as a result of

the shooting on December 14, 2012, the words and reports seem

unjust.

(LaGuercia PSR ¶96).

The evaluation continues:

A broader view [of the relationship between Mr. LaGuercia and

Riverview and the December 14, 2012 horrors] would reveal

individuals throughout the country who purchased firearms from

respected gun stores and then went about their normal day. The fact

that the shooter involved in the December 14, 2012, incident was

provided weapons which were purchased at Riverview Sales, Inc.

should not be a factor when considering the facts/evidence of the

case against the store and Mr. LaGuercia.

-7-

(LaGuercia PSR ¶ 96).

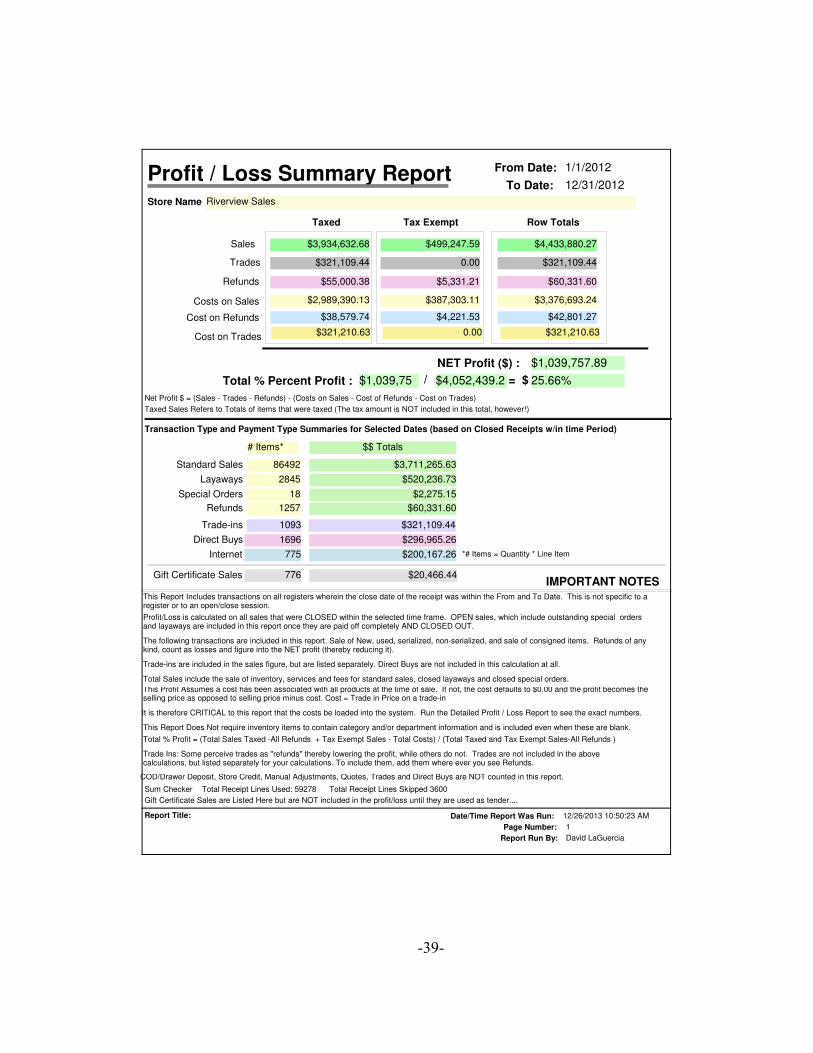

Regardless, the economic impact of the revocation and the media are self-

evident, and unsurprising. In 2011, Riverview’s sales were approximately

$3,654,116.75. In 2012, the last sales year before the revocation, the sales were

approximately $4,433,880.27. In 2013, the first year Riverview operated after the

revocation and Newtown publicity, the sales were approximately $1.483,031.12.

(See Exhibit A-Rough Profit and Loss Estimates 2011-2013). That number

represents an approximate 66.5% decrease in sales.

The defendants have pled guilty and fully accepted responsibility for their

actions. The defendants pled guilty because they are guilty. This memo is

intended to assist the Court in its understanding of certain aspects of the case and

reflected in the Riverview and LaGuercia PSRs. Nothing herein is intended to

dilute the already expressed contrition and acknowledgement of guilt reflected in

the PSRs. For some reason, the government does seem intent to unfairly demonize

Mr. LaGuercia and Riverview, ignoring their cooperation and highlighting non-

criminal conduct. This memorandum is largely directed at the expected

continuation of that effort.

Pending Administrative Proceedings and the Search of Riverview

Indeed, as it happened, it seems there was absolutely no need whatsoever, either

for the warrant executed at Riverview December 20, nor for its execution on that date. At

-8-

the time, Riverview and Mr. LaGuercia, as FFL holders, were obligated to provide the

paperwork eventually seized (no firearms were seized or sought pursuant to the warrant-

only paperwork was seized) upon a simple request from the ATF.

As of December 20, the administrative revocation proceeding was still pending,

as it had been since the close of the hearings in early August, 2012. For the balance of

September, for all of October and November, and then for the first two weeks of

December, the proceeding remained pending. The government cannot dispute that if the

ATF had contacted Mr. LaGuercia on the morning of December 20, and informed him

they needed particular records, whether 4473s, the A&D book, or any other ATF-related

documents, Mr. LaGuercia would have been obligated to provide them immediately,

upon demand.

In January, 2011, Riverview was subject to a compliance inspection by ATF

Industry Operations Investigators. The inspection involved a complete inventory at

Riverview and review of related documents. On June 8, 2011, the Director of Industry

Operations, Boston Field Division issued a Notice of Revocation of Federal Firearms

License, ATF Form 4500(5300.4) to David LaGuercia, dba Riverview Sales. No

restrictions accompanied the Notice, nor did the Notice indicate that the grounds for

revocation warranted any expedited process or special attention. Riverview continued to

conduct its business as an FFL.

Over 13 months later, on July 25 and 27, 2012, with the FFL still in tact and

Riverview still conducting its business, the Director of Industry Operations, Boston Field

Division, issued a revised Notice of Revocation of Federal Firearms License, which

-9-

included allegations that then Riverview employee, Krystopher DiBella, had sold

ammunition to a prohibited person, and that DiBella had allowed a prohibited person to

handle firearms at Riverview. According to the ATF, a criminal investigation of an

individual who admitted to being a felon in possession of firearms, uncovered the fact

that DiBella had sold ammunition to a known felon, and allowed that felon to handle

firearms in the store. That was the first time David LaGuercia learned that DiBella had

engaged in such conduct.

On August 8 and 9, 2012, an informal hearing on the Notice of Revocation was

Held in Boston. Over those two days, both sides presented testimonial and documentary

evidence. When the hearing closed, approximately 18 months after the violations were

discovered, no special conditions were applied, and no emergency revocation occurred.

The FFL remained in tact, and Riverview continued doing business. Four months later,

on December 14, 2012, now approximately 22 months after the violations were

discovered, and more than 17 months after the initial Notice of Revocation was served on

Mr. LaGuercia and Riverview, no action had been taken concerning the revocation

proceedings. The FFL remained in tact and Riverview continued doing business.

Then December 14 came.

Conveniently omitted from the media reports, which began when the government,

on December 20, 2012 apparently leaked the upcoming raid to the media (specifically

Len Bestoff of NBC) more than three hours before the raid took place,

-10-

Len Besthoff !@lennbc 20 Dec 2012 Apparent ATF raid @ store where Lanza bought gun OnlyOn3 #wfsb @ Riverview Gun Sales http://instagr.am/p/Tea9q5oGEy/ Collapse

• Reply • Retweet • Favorite • More • RETWEETS12 • FAVORITE1

• 2:39 PM - 20 Dec 2012 from East Windsor, CT · Details

was the fact that Riverview and Mr. LaGuercia had been actively assisting the

ATF in its ongoing investigation into what had occurred at Sandy Hook and other related

matters.

The government was selectively providing information to the media

Len Besthoff !@lennbc 20 Dec 2012 Sources: Riverview Gun Sales in East Windsor CT sold #NancyLanza at least one of guns used in #Newtown #wfsb Collapse

• Reply • Retweet • Favorite • More • RETWEET1

• 3:51 PM - 20 Dec 2012 · Details

in an attempt to publicly demonize and bury Riverview and Mr. LaGuercia before

they knew what was happening.

-11-

Len Besthoff !@lennbc 20 Dec 2012 #RiverviewGunSales got on radar screen after man with mental issues tried stealing 50 caliber long gun Saturday #wfsb Collapse

• Reply • Retweet • Favorite • More • RETWEET1

• 4:49 PM - 20 Dec 2012 · Details ___________________________________________ Len Besthoff !@lennbc 20 Dec 2012 Upon further investigation, police learned same man with mental issues succesfully stole AR-15 from #RiverviewGunSales 4 days earlier #wfsb Collapse

• Reply • Retweet • Favorite • More • RETWEETS2

• 4:52 PM - 20 Dec 2012 · Details ________________________________________________________________________ Len Besthoff !@lennbc 20 Dec 2012 police say this same man with mental issues stole 11 other weapons from #RiverviewGunSales, found in June 2011 @ father's home #wfsb Collapse

• Reply • Retweet • Favorite • More

4:53 PM - 20 Dec 2012 · Details ________________________________________________________________________

-12-

By the time the warrant was executed Riverview was already being tied to

Newtown, Jordan Marsh and an attack in Hartford. This was no accident. It seems that

the government believed it had an opportunity to undo the staggeringly huge volume of

negative press3 it had received in the last few years, with a high profile prosecution of a

firearms dealer coupled with a concerted media attack related to Newtown. So first they

pursued a search warrant for documents they could have easily had just for the asking,

and then put on a show for the media, while the Attorney General of the United States

met with the Governor of Connecticut and law enforcement officers in Newtown. It

seems the government was intent on showing Connecticut and the country it could do

something about the tragedy that had occurred. The East Windsor Police Department

actively assisted the federal government in its execution of the search warrants4 and in its

effective pursuit of a media strategy designed to cripple Riverview and Mr. LaGuercia

and destroy their names.

This was politics at its worst. The government no doubt viewed the situation as a

difficult problem. Additionally, the government also knew that it was exposed for failing

to prevent a young man with mental problems, who had previously been convicted of

stealing guns, had avoided federal prosecution for those offenses, who had received a

remarkably lenient sentence in connection with those thefts, to repeat his offenses by

3 http://www.cbsnews.com/news/gunrunning-scandal-uncovered-at-the-atf/ http://www.nytimes.com/2012/09/20/us/report-places-blame-in-operation-fast-

and-furious.html?_r=0 http://www.cnn.com/2012/08/02/politics/atf-deputy-director-resigns/index.html http://www.theguardian.com/world/2013/may/13/america-government-associated-

press-phone-records http://thehill.com/blogs/blog-briefing-room/news/190219-gop-members-seek-to-

impeach-holder 4 http://www.nbcnewyork.com/news/local/Federal-Agents-Raid-East-Windsor-

Gun-Shop-Connecticut-Newtown-184370921.html

-13-

stealing weapons again from Riverview. The government also knew that it had permitted

a confessed felon to escape prosecution for charges related to his being a felon in

possession of weapons and ammunition, had allowed the felon’s wife to escape

prosecution for aiding and abetting him, and had permitted the man who sold the firearms

and ammunition to them, who had also sold the Bushmaster to Nancy Lanza, to escape

prosecution altogether. Lastly, the government, in the midst of multiple investigations

related to its gun-walking policies and programs, had permitted the man who sold to the

felon and to Nancy Lanza to sell about 3000 guns between the time the government

learned of his illegal interactions with the felon, and the time the government told Mr.

LaGuercia of those transgressions.

Facing this complex set of circumstances, the government set out to blame Mr.

LaGuercia and Riverview for everything, criminal and non-criminal, and portray them in

the worst possible light.

Riverview and David LaGuercia Assisted the ATF After Newtown

In fact, the ATF fully knew that had they requested any further documents from

Mr. LaGuercia and Riverview, they would have received full cooperation. The ATF’s

experience in the aftermath of Newtown proved that. On December 14, Riverview

received a call from the National Tracing Center looking for a trace on a Sig Sauer 226,

serial number UU676027, a gun apparently used at Sandy Hook. Mr. LaGuercia found

the information and then saw that the purchaser, Nancy Lanza had apparently purchased a

-14-

Bushmaster XM-15, serial number L534858, and followed up with a fax to the National

Tracing Center later that afternoon.

Obviously, Mr. LaGuercia’s assistance alerted the ATF to facts they had not

known up to that point. The Riverview/LaGuercia FFL remained in place, more than 4

full months after the conclusion of the two-day revocation hearings, in which all the

violations cited in the FFL revocation notice had been detailed, in testimony and

documents. The evidence also covered Krystopher DiBella’s interactions with a felon,

something the ATF acknowledged under oath occurred without Mr. LaGuercia’s

knowledge and participation. From the first week of August, 2012, until December 14,

2012, the ATF and United States government had chosen to permit Riverview and Mr.

LaGuercia to continue operating as an FFL.

Two days later, on December 16, ATF Special Agent Brian Higgins contacted

Riverview, informed Mr. LaGuercia he wanted to come to the store to meet, retrieve the

Lanza 4473s, and to make any necessary inquiries concerning Lanza and her purchases.

Again, with the FFL still in place, Mr. LaGuercia and Riverview complied, voluntarily

met with the ATF, Riverview Sales, which was closed at the time, and provided

documents and other information, and all without a warrant. On December 17, SA

Higgins called again, concerning two 4473s for guns unrelated to Sandy Hook, came to

Riverview and took the documents, with nothing less than full cooperation from Mr.

LaGuercia and Riverview.

That same day, December 17, ATF Industry Operation Supervisor Tim Gahm,

informed Jillair Kubish, the ATF Area Supervisor, that the ATF had previously cited

-15-

Riverview for a record keeping violation involving the transfer of the Bushmaster to

Nancy Lanza, during the course of the 2011 ATF Firearms Compliance Inspection of

Riverview Sales. He informed her that Riverview was cited under 27 CFR 478.125(e), 18

U.S.C. 922(m) for having a disposition date that was prior to the authorization date. That

violation was typical of the Riverview violations, in that it was a technical violation of

the law, but endangered no one. Both Gahm and Kubish had appeared for the government

in the revocation proceeding and were fully conversant in the allegations and evidence

presented at the hearing. However, notwithstanding the volume of the allegations cited in

the amended revocation notice, the nature of the evidence presented by the government in

the hearing, and the procedural history of Riverview in connection with ATF inspections,

Riverview’s FFL remained in place, and after December 17 no further ATF requests for

documentation or information were posed to Riverview.

On December 18, with the FFL still in place, the ATF could have come to

Riverview and retrieved all of the documents eventually seized on December 20, without

a warrant, and chose to refrain from doing so. The same is true for the following day,

Wednesday, December 19. For those two days, it appears the government knew it had a

political problem: the ATF had known about Nancy Lanza for months, done nothing

about it, and now they knew her son had used a cited weapon in the massacre. This

should not have been a problem, for there was absolutely no way that a minor technical

citation should have led the ATF to follow up with Mrs. Lanza. However, it apparently

may have influenced the government’s action, and the resulting impact on Riverview and

Mr. LaGuercia.

-16-

Up to that point, Mr. LaGuercia and Riverview were, and would have continued

to be, fully cooperative with the ATF and any of its inquiries.

The ATF Intentionally Concealed Criminal Conduct from David LaGuercia

It seems the government had yet another problem. The ATF had known since the

July of 2011 that the individual who had sold the Bushmaster to Lanza, Krystopher

DiBella, had sold ammunition to a known felon more than once and had allegedly

facilitated the felonious use of firearms by that felon more than once. Beyond the ATF’s

knowledge of those incidents of criminal conduct, the United States Attorney’s office for

the District of Connecticut had known of the allegations against DiBella since August,

2011, and had done nothing to alert Mr. LaGuercia that he continued to employ a person

who was engaging in illegal conduct connected to the sale of ammunition and weapons

involving a felon. (Neither the felon, nor the felon’s wife have ever been prosecuted by

the federal government in connection with the noted conduct.)

As noted in the defendants’ PSR objections, Riverview PSR¶ 26 and ¶ 27, address

certain conduct by DiBella who admitted selling ammunition to a felon. DiBella was

actually accused by that felon and the felon’s wife of repeatedly selling firearms to the

wife of that felon for the felon’s possession and use, and repeatedly giving the felon

access to firearms at shooting ranges in Connecticut. More specifically, the felon’s wife

explained to federal agents that on Father’s Day 2011, DiBella brought firearms to a

Connecticut shooting range and allowed the felon to use and shoot a .45 caliber pistol, a

-17-

10 mm pistol, a bolt action rifle, and a semi-automatic rifle DiBella said he had built.

According to the felon’s wife, this incident occurred well after DiBella had been told her

husband was a felon. The ATF acknowledged during the revocation hearings that Mr.

LaGuercia was not involved in, and did not know of, any of this activity involving the

felon and his wife, but cited the sales of ammunition as a grounds for revocation, based

solely on the doctrine of respondeat superior.

It is somewhat bewildering, if not shocking, that the government has previously

represented to the Court that there is “no evidence to suggest that his [DiBella’s] errors

caused a firearm to be sold to a felon or that he was responsible for knowingly

transferring firearms to prohibited individuals”. The felon and the felons’ wife proffered

to the United States Attorney’s office, and the ATF agents involved in the investigation

were present. According to the investigators, when they first observed the felon, inside

his house with his wife, the felon was wearing a holster. According to the felon’s wife,

she had purchased numerous firearms from DiBella, and had informed DiBella she was

purchasing the weapons because her husband was a felon. According to the felon, he

himself had informed DiBella that he was a felon, and gave that as the reason his wife

had to purchase the weapons. It is difficult to understand how the government could

represent DiBella as being anything less than a rogue employee who knowingly and

repeatedly engaged in illegal conduct. (Apparently during earlier related proceedings, the

government attempted to portray Mr. DiBella as a knave, poorly trained by Riverview,

and who engaged in misconduct largely because he did not know any better.)

On December 16, 2012, upon reviewing the Lanza 4473s, the ATF had to know

-18-

that Mr. DiBella, who up to that point had escaped any charges whatsoever for his

repeated interactions with the felon and his wife, well over a year earlier, was the same

person who sold the Bushmaster to Lanza. Notably, the government had concealed its

knowledge and conclusions concerning DiBella’s interactions with the felon and the

felon’s wife from Mr. LaGuercia, from the time it first learned of them, in July of 2011,

until the late summer of 2012, on the eve of the revocation hearings. Mr. DiBella had

personally sold approximately 3,000 weapons between the time the government learned

he had sold ammunition and weapons to the felon and the felon’s wife, and the time the

ATF decided to inform Mr. LaGuercia of Mr. DiBella’s actions.

What the government had done, was conceal Mr. DiBella’s actions from Mr.

LaGuercia, then later use those actions as a basis for revoking the FFL, all the while

acknowledging Mr. LaGuercia did not know about those actions, did not condone them,

or authorize them. Then government actors knowingly and intentionally set out to destroy

Mr. LaGuercia’s business and his reputation by actively leaking information to the media

about the December 20 raid; about prior thefts from Riverview, which Riverview alerted

police about; about prior thefts by Jordan Marsh, a disturbed man who was back on the

street because of the actions and inactions of federal and Connecticut State authorities;

and about Nancy Lanza and Newtown.

These intentional actions were, in all likelihood, also undertaken to direct

attention away from law enforcement’s inadequacies in their own performance. This was

certainly not the first time the government had used leaks to destroy a

person.5Additionally, the attacks against Mr. LaGuercia were occurring at a time the ATF

5 http://www.azcentral.com/news/articles/2011/11/09/20111109burke-admits-

-19-

and Department of Justice could not afford any further controversies arising from its

investigative failings.6 In fact, on December 17, 2012, the last day the government asked

Mr. LaGuercia for his help, it was widely reported that the family of murdered Border

Patrol Agent Brian Terry was suing seven government employees and a gun shop and its

owner for negligence and wrongful death.7 On December 18, 2012, CBS News continued

the media onslaught against the Department of Justice connected to Operation Fast and

Furious.8The government could not afford another public relations problem, so it decided

to attack Mr. LaGuercia.

The defendants do not know if Mr. DiBella was a part of a formal or informal

ATF gun-walking-type program in Connecticut, even at this late date. What the

defendants do know is that had the ATF informed Mr. LaGuercia of its knowledge that

Mr. DiBella had been selling firearms to the wife of a felon, for their use by the felon;

had they known DiBella was taking firearms to shooting ranges in Connecticut for use by

the felon; had they known DiBella had been selling ammunition to the felon; or had they

know DiBella had been engaging in other illegal conduct connected to the sale of

firearms or ammunition to, or use by, a felon, or by the spouse intending to provide

leaking-whistle-blowers-records.html

6 http://www.cbsnews.com/news/heads-roll-after-fast-and-furious-investigation/ http://online.wsj.com/news/articles/SB1000142412788732371700457815973202

5255610?mg=reno64wsj&url=http%3A%2F%2Fonline.wsj.com%2Farticle%2FSB10001424127887323717004578159732025255610.html

http://www.washingtonpost.com/blogs/post-politics/wp/2013/06/07/manchin-holder-should-consider-resigning/

http://washington.cbslocal.com/2012/12/18/cbs-news-fast-and-furious-gun-found-at-site-where-mexican-beauty-queen-killed/

7 http://www.cbsnews.com/news/brian-terry-family-sues-atf-officials-in-fast-and-

furious/ 8 http://washington.cbslocal.com/2012/12/18/cbs-news-fast-and-furious-gun-

found-at-site-where-mexican-beauty-queen-killed/

-20-

firearms or ammunition to the felon, DiBella’s employment would have been

immediately terminated. Furthermore, we suggest that had the ATF properly informed

Mr. LaGuercia of that severe breach of the law by his employee, acting as an employee,

albeit ultra vires, for the conduct occurring at Riverview, and then in an entirely personal

capacity for his conduct at the shooting ranges, Mr. LaGuercia and Riverview may very

well still have the FFL.

We suggest that, because the ATF knew on July 7, 2011 of DiBella’s conduct,

consisting of multiple violations of the Gun Control Act, and which the ATF believed

occurred from January 2010 to July 2011, but did not inform Mr. LaGuercia of it until on

or about July 25, 2012. The ATF learned of Mr. DiBella’s interactions with the felon and

the felon’s wife on July 7, 2011, as a result of an ongoing investigation. On that date, the

felon and his wife informed the ATF about Krystopher DiBella. At that time, though a

notice of revocation had been served, had Riverview cooperated with the ATF, and

perhaps other government agencies involved in the investigation, the FFL may very well

have been saved.

It is indisputable that retrieving documents from an FFL on December 19, 20 or

thereafter, through the voluntary cooperation, such as the ATF had been receiving from

Riverview and Mr. LaGuercia, would have been easier, taken less manpower, and would

have been more cost-effective and efficient. Such an approach would also have prevented

the media from permanently imprinting David LaGuercia with the mark of the Newtown

massacre. Most importantly, it is clear Mr. LaGuercia and Riverview, if allowed, would

have fully cooperated with the government’s ongoing investigation into the tragedy at

-21-

Newtown. Apparently the government, for its own reasons, felt the warrant was

necessary, but it certainly was not a legal necessity.

As we note above, the charges involved stem from Mr. LaGuercia and

Riverview’s failures to comply with the rigorous FFL requirements that govern the

paperwork that must be maintained in connection with gun sales. As the two reports

clearly reflect, the main thrust of this case is Riverview’s use of information or

intelligence (information provided by customers, understanding of regulations, and

corrective instructions provided during earlier inspections, etc.), operational security,

staffing, and policies and procedures for the operation of its business as an FFL, and as

one of the highest volume gun dealers in the State of Connecticut. More specifically, as

to sales volume, as Mr. LaGuercia estimated, Riverview sold roughly 6,000.00 guns

annually (Riverview ¶32, LaGuercia ¶71). (The exact number for sales from January 1,

2010 through December 31, 2012 is closer to 17,542.)

The Riverview PSR, at ¶96, and referred to above, concisely and accurately notes

that Mr. LaGuercia is the one who ultimately had to answer for DiBella selling a firearm

to a prohibited person, and “another incident where a firearm was stolen [by Jordan

Marsh] out of his store, in plain view of other employees and customers”. But DiBella

and the ATF kept his criminal actions to themselves, for well over a year, and it is clear

that DiBella knowingly broke the law, as a rogue employee, and whose actions

contributed to the revocation, even without Mr. LaGuercia’s knowledge. Jordan Marsh

stole guns from Riverview, which was his victim, not just once, but each time a gun was

stolen. It is an interesting spin on a “blame the victim” theory, that the government

-22-

apparently blames the defendants equally for being victimized multiple times by a

mentally ill young man, who repeatedly stole guns from the defendants. (Furthermore,

the technical nature of the paperwork violations is emphasized by the fact that Mr.

LaGuercia and Riverview, knowing the stolen firearms were already safe and in the

custody of law enforcement, committed violations by not reporting the already safe guns

stolen or missing.)

The Government’s Attempt to Destroy LaGuercia’s Name

The government’s attacks on Mr. LaGuercia also transcended the conduct at issue

in this case into private, defamatory, malicious attacks on him as a gun owner.9

This case and this investigation has never touched upon Mr. LaGuercia’s private conduct,

nor his personal ownership or use of a firearm. Yet, in a brazen, arrogant, self-serving

attempt to connect Mr. LaGuercia’s Second Amendment rights to Riverview’s conduct in

this case and tarnish his name further, the government disseminated information that

contradicted that reality. East Windsor Detective Mathew Carl, whose law enforcement

agency partnered with the ATF and the U.S Attorney’s Office in this case, spoke openly

with the media about Mr. LaGuercia in a nationally distributed story and intentionally

described Mr. LaGuercia as a “very non-caring gun owner.”10 (Emphasis added.)11

9 http://www.cnn.com/2013/04/05/us/connecticut-sandy-hook-gun-

store/index.html http://fox8.com/2013/04/05/no-more-gun-sales-where-sandy-hook-weapon-was-

bought/ http://www.khq.com/story/21895979/store-that-sold-sandy-hook-firearm 10 Id.

-23-

This overt character assassination by the government, in the national media,

was clearly designed to continue the devastating destruction of Mr. LaGuercia’s

reputation.

The message the federal government and its state law enforcement partners

continued to disseminate was that Mr. LaGuercia cared nothing about the safety of

others, either in his capacity as FFL holder, as Riverview Sales owner, or in his personal

capacity as a gun owner. They publicly connected him to Newtown, Jordan Marsh and a

gun attack in Hartford. It is clear the government didn’t care in the least about the

significant negative implications the attacks would have on Riverview or Mr. LaGuercia.

To the contrary, the government overtly sought to destroy Mr. LaGuercia’s name and his

business. The government wanted to show the public that it was protecting it, and that it

knew how to do its job, did it competently, and that any dangers to the public stemmed

from David LaGuercia and Riverview, rather than the government’s failures or

inadequacies. The government’s unwarranted and unjustified attacks invite scrutiny of it

own actions.

Ironically, such examination reveals that Riverview’s security, as faulty as it may

have been, in some ways, reflects the difficulties that exist in regulatory and paperwork

compliance connected to firearms. For example, if the government were to be candid, it

would acknowledge that the Jordan Marsh incident is a manifestation of a lack of

organizational security, staffing, and other controls, that have often to be found lacking in

the government’s own organizational operations connected to firearms. The government

11 The defendants requested the U.S. Attorney investigate a number of law

enforcement leaks related to this case, from the initial tweets about the raid, to the leaks in April, 2013 revealing the administrative findings generated in the revocation proceeding, but were told the investigation was unsuccessful.

-24-

should not put undue blame on the defendants for security failures that pale in

comparison to those committed by the world’s experts in firearms safety.

Riverview’s security failures in connection with the Marsh thefts are not, not

have they ever been, criminal. There is no danger they may reoccur, because Riverview’s

FFL has been revoked. The government’s repeated focus on the thefts is apparently yet

another attempt to unfairly smear Mr. LaGuercia and Riverview, by focusing media

attention on the defendants, and linking them to another potentially dangerous situation.

As noted above, Mr. LaGuercia knew nothing of Mr. DiBella’s interactions with the felon

and the felon’s wife, yet somehow Mr. LaGuercia is to blame. The linkage of Mr.

LaGuercia to an attack in Hartford had nothing to do with him or Riverview.

The government, however, knew all about the DiBella transactions, and did

nothing. The government is clearly holding Mr. LaGuercia to a much higher standard and

much more responsible for “protecting the public” than it does itself.

Earlier last year when the Milwaukee Journal Sentinel exposed a botched

ATF sting in Milwaukee — that included agents hiring a brain-damaged man to promote

an undercover storefront and then arresting him for his work — ATF officials told

Congress the failed Milwaukee operation was an isolated case of inadequate supervision.

It wasn't. The Milwaukee Journal Sentinel reviewed thousands of pages of court records,

police reports and other documents and interviewed dozens of people involved in six

ATF operations nationwide that were publicly praised by the ATF in recent years for

nabbing violent criminals and making cities safer.12

According to the Journal Sentinel, agents with the U.S. Bureau of Alcohol,

12 http://judiciary.house.gov/index.cfm/press-

releases?ContentRecord_id=8EB734E0-9367-4381-9796-E1FC16268CC0

-25-

Tobacco, Firearms and Explosives, used tactics similar to those used in Milwaukee in

every operation, from Portland, Ore., to Pensacola, Fla.

Among the findings:

" ATF agents befriended mentally disabled people to drum up business and later arrested them in at least four cities in addition to Milwaukee. In Wichita, Kan., ATF agents referred to a man with a low IQ as "slow-headed" before deciding to secretly use him as a key cog in their sting. And agents in Albuquerque, N.M., gave a brain-damaged drug addict with little knowledge of weapons a "tutorial" on machine guns, hoping he could find them one. " Agents in several cities opened undercover gun- and drug-buying operations in safe zones near churches and schools, allowed juveniles to come in and play video games and teens to smoke marijuana, and provided alcohol to underage youths. In Portland, attorneys for three teens who were charged said a female agent dressed provocatively, flirted with the boys and encouraged them to bring drugs and weapons to the store to sell. " As they did in Milwaukee, agents in other cities offered sky-high prices for guns, leading suspects to buy firearms at stores and turn around and sell them to undercover agents for a quick profit. In other stings, agents ran fake pawnshops and readily bought stolen items, such as electronics and bikes — no questions asked — spurring burglaries and theft. In Atlanta, agents bought guns that had been stolen just hours earlier, several ripped off from police cars. " Agents pressed suspects for specific firearms that could fetch tougher penalties in court. They allowed felons to walk out of the stores armed with guns. In Wichita, agents suggested a felon take a shotgun, saw it off and bring it back — and provided instructions on how to do it. The sawed-off gun allowed them to charge the man with a more serious crime. " In Pensacola, the ATF hired a felon to run its pawnshop. The move widened the pool of potential targets, boosting arrest numbers. Even those trying to sell guns legally could be charged if they knowingly sold to a felon. The ATF's pawnshop partner was later convicted of pointing a loaded gun at someone outside a bar. According to the reports, instead of a stiff sentence typically handed down to repeat offenders in federal court, he got six months in jail — and a pat on the back from the prosecutor.13

13 http://www.jsonline.com/watchdog/backfire-190528221.html http://media.jsonline.com/documents/2013-01-

31+DEI+CEG+RWG+FJS+to+Jones-ATF+-+Milwaukee.pdf

-26-

This is all to suggest that the government is well aware that sometimes use of

information or intelligence, operational security, staffing, and policies and procedures for

the operation of an FFL, or for the operation of a government agency charged with

maintaining records, keeping track of firearms and other materials, falls short of what the

FFL or the agency intends. This may be true despite repeated warnings or instructions.

For example, the FBI refused to participate in the ATF’s storefront schemes because of

its concerns about use of intelligence, operational security and staffing.14 That, no doubt

would constitute a serious warning to the ATF from another respected law enforcement

agency. As noted below, those concerns came to fruition and put a massive amount of

people at risk. Riverview and Mr. LaGuercia’s actions did not.

Upon investigation of these government activities, it was learned that15flaws in

operational security related to government-operated gun shops included setting up a gun

shops that were easy targets for burglars, and knowingly permitting a man armed with a

gun and threatening to shoot someone walk out of an ATF run shop.16This shines a light

on the government’s unfair attempt to connect Jordan Marsh, a scenario in which the

defendants were victimized, to some form of punishment for the defendants. As reported,

the government had failed miserably in its own attempts to implement proper security at

its own gun shops, allowing guns to be introduced into a community, and putting it at

14 http://oversight.house.gov/wp-content/uploads/2014/01/2013-05-10-Grassley-

DEI-Goodlatte-Sensenbrenner-to-Jones-ATF-Milwaukee-Operation-Fearless.pdf 15 http://www.doi.gov/oig/reports/upload/USPPWeaponsAccountabilityPublic.pdf http://www.mprnews.org/story/npr/138574291 16 http://www.jsonline.com/watchdog/watchdogreports/atfs-fearless-storefront-

had-little-to-ward-off-burglars-im8l7o4-190564791.html; http://www.jsonline.com/watchdog/watchdogreports/atf-agents-conducting-sting-let-man-leave-store-with-gun-gd9vhf8-207807851.html;

-27-

risk. For some, supervising this type of failure warrants a promotion.17Yet a private

citizen, David LaGuercia should be punished because Jordan Marsh successfully stole a

gun, and then was caught trying to steal another. This, of course, occurred after the ATF

and Connecticut state authorities decided Mr. Marsh, who suffered from variety of

psychological issues, should be free after stealing 11 guns from Riverview.

But, according to the government, Riverview and Mr. LaGuercia alone, not the

government, are to blame for Jordan Marsh.

Other reported security failures by the government connected to its own

operations include ATF agents losing track of their own guns,18 and abject lack of

oversight and audit, costing the public millions of dollars (“The ATF's cigarette-selling

stings, like one done in Milwaukee in 2011, were fraught with problems, from misuse of

proceeds to millions of dollars in missing cigarettes, according to a scathing audit by

the Department of Justice's Inspector General. The U.S. Bureau of Alcohol, Tobacco,

Firearms and Explosives could not account for what happened to 2 million cartons of

cigarettes, with a retail value of more than $127 million, according to the auditors. In one

sting — which was done without approval of ATF supervisors — an informant working

for the agents received nearly all of the sting's $5 million in profit, supposedly for

expenses and commissions. But ATF agents could not provide paperwork to support the

informant's expenses. Auditors did not disclose where that operation was conducted.

17 http://www.jsonline.com/watchdog/watchdogreports/atf-leader-who-oversaw-

botched-sting-will-run-phoenix-office-b9943426z1-213728421.html 18 http://www.jsonline.com/watchdog/watchdogreports/atf-agents-lost-track-of-

dozens-of-their-own-guns-reports-show-b99213499z1-247182581.html

-28-

Profits from that operation were deposited into the account of a different ATF sting in

another state, which is a violation of the statutory requirements, the auditors found.”)19

The difficulties in maintaining accurate records and keeping track of firearms and

safe guarding them, cigarettes, and official paperwork are not by any means limited to the

ATF. This is true despite their expertise, training and best intentions.20 A review of the

United States Department of the Interior Inspector General Report on the U.S. Park

Police’ Weapons Accountability Program seems strikingly similar in some ways to

Riverview’s situation, but indisputably more serious in others. (The similarity arises from

Riverview’s repeat ATF inspections, during which it received corrective instructions, as

the USPP did.) The June 27, 2013 report followed a 2008 report, in which the Inspector

General provided 20 recommendations for improvement. That 2008 report found “a

number of weaknesses in USPP’s management and operations that adversely affected the

level of security at national icons and presented other safety concerns.” 21

In 2009, the Inspector General “reviewed the firearms controls of the U.S.

Department of the Interior law enforcement programs, which include USPP.”22

According to the Inspector General “[a] t that time, we found a disconcerting attitude

toward firearms accountability within USPP. In particular, we found that firearms

custodians were unaware of the number of guns in their inventory or of the origin of these

guns, and that guns physically present were not listed on the inventory. We strongly

19 http://www.jsonline.com/watchdog/watchdogreports/atfs-cigarette-stings-had-

serious-lack-of-oversight-audit-finds-b99106474z1-225195342.html; www.justice.gov/oig/reports/2013/a1336.pdf.

20http://www.doi.gov/oig/reports/upload/USPPWeaponsAccountabilityPublic.pdf;http://www.washingtonpost.com/local/park-police-lost-track-of-weapons-inspector-general-report-says/2013/06/27/ac7fc58a-dcf9-11e2-85de-c03ca84cb4ef_print.html

21 Id. 22 Id. at 2.

-29-

recommend that immediate action be taken to establish a professionally responsible

firearms management program at USPP.” 23 According to the report, the probe was

launched in part because of an anonymous tip that Park Police officers were improperly

taking weapons home. Investigators discovered two instances in which that had occurred,

but they found many other troubling examples of mismanagement, according to the

report. Investigators found 1,400 guns that were supposed to have been destroyed or

melted down. An additional 198 handguns donated by the Bureau of Alcohol, Tobacco,

Firearms and Explosives are sitting in a building in Anacostia but don’t show up in

official records. In another instance, the agency in October 2011 sent a list of 18 pistols,

shotguns and rifles it described as lost or stolen to a national database. But it never

launched an internal investigation. The guns, it turned out, had been destroyed or given to

other agencies — or they were still in Park Police possession, according to the report.

One Remington shotgun remains missing. “Commanders up to and including the chief of

police have a lackadaisical attitude toward firearms management,” wrote Mary L.

Kendall, the deputy inspector general. “Historical evidence indicates that the indifference

is a product of years of inattention to administrative detail.”24

According to reporting on the matter, investigators took an unusually harsh tone

in part because they said similar problems found in 2008 and 2009 were never fixed — a

symptom of “the decade-long theme of inaction and indifference” of top Park Police

managers.25 One could think the United States government holds private citizens and

23 Id (emphasis added). 24 Upon this writing, we are unaware of any criminal prosecutions of any USPP

officials for their failures to accurately keep inventories or proper records in connection with firearms.

25 Id.

-30-

FFLs such as Riverview and Mr. LaGuercia to a higher standard and level of scrutiny and

accountability for maintaining required paperwork and records, and for maintaining

security than it does its own agencies. Those agencies are actually law enforcement, are

experts in firearms safety and record keeping, and, as noted above, have their hands full

keeping their own houses in order.26

The reasons these significant government failures are germane to this case are

numerous. First, the government’s own firearms experts’ inability to fulfill their

requirements to complete and maintain required records demonstrates the difficulties that

sometimes arise when honest brokers attempt to fulfill their obligations. As to the United

States Park Police, there seemed to be no attention whatsoever, nor any effective system,

to keeping track of their weapons. There seems to be more than a hint of hypocrisy in the

government’s approach to Mr. LaGuercia, who was an FFL, but had no military, law

enforcement, or management training, like those government supervisors receive.

Apparently, the agents of ATF and the officers of USPP are “very non-caring

gun owners” too.

Next, the government seems to be focusing on blaming the defendants for putting

the community at risk for actions they knew nothing about (DiBella) and for lapses in

security (Marsh), that are non-criminal, and that resulted in the defendants being

26 http://www.washingtonpost.com/local/park-police-lost-track-of-weapons-

inspector-general-report-says/2013/06/27/ac7fc58a-dcf9-11e2-85de-c03ca84cb4ef_story.html (“The U.S. Park Police has lost track of thousands of handguns, rifles and machine guns in what a government watchdog agency concluded is the latest example of mismanagement on a police force trusted to protect millions of visitors to the city’s iconic monuments.”)

-31-

victimized by a person intent upon stealing from them. As noted above, the federal

government has knowingly put weapons in the hands of felons and mentally challenged

people in different parts of the country, something the defendants would never even

contemplate doing. In this case, the government intentionally concealed DiBella’s

conduct from the defendants, allowing DiBella to remain in a position where he could

engage in similar conduct with other felons and other prohibited person, whenever he

liked.

Where was the government’s concern for the safety of the community at that

point? Where was the governments concern that DiBella might have been engaging in

similar conduct with other felons or other prohibited persons? The same questions may

be asked about the felon and the felon’s wife, who both escaped prosecution. The

government has selectively downplayed the dangerousness of Mr. DiBella’s actions,

ignored the government’s own conduct connected to Jordan Marsh, and repeatedly

connected the defendants to Newtown, in order to make Mr. LaGuercia seem worse than

he is.

The above reports concerning ATF operations also reflects the agency’s poor

decision-making in connection with some of its operations. Permitting DiBella to

continue selling weapons and ammunition at Riverview for more than a year, after

learning of his dealings with the felon and the felon’s wife, was an atrocious decision that

put the community at significant risk. It also put the defendants at risk and was then used

by the government in its attempt to revoke the FFL.

Similarly, it seems the government remains unduly focused on Mr. LaGuercia and

-32-

Riverview’s non-criminal conduct related to Jordan Marsh, and his thefts of firearms

from Riverview, and on out-of-state sales, though the government acknowledges the sales

did not violate any law. Mr. Marsh stole guns from Riverview, and it is clear that lax

security played a significant role in at least the theft on video. However, lax security is

not a criminal offense, and some would suggest the main reason, as noted above, Mr.

Marsh was positioned to continue his criminal conduct was due to earlier governmental

failures.27 In fact, those government failures exposed Mr. LaGuercia, himself, to real

danger, when Marsh returned to the store to steal weapons.

The ATF permitted Riverview and Mr. LaGuercia to continue operating as an

FFL after repeated inspections citing numerous violations, because it knew the

community was not at risk as a result of those violations. Riverview was a high volume

dealer, and repeatedly made mistakes in required paperwork over its years of operations.

That the community was not at risk is demonstrated by the length of time that elapsed

between the finding of violations in January, 2011, and the eventual revocation on

December 20, 2012, and the related timing of steps in the process, as described above.

The first time the dangerousness of Riverview’s conduct was suggested was after

Newtown, and it was discovered two weapons had been legally purchased at Riverview.

Up to that point, notwithstanding the number of violations and the full

administrative hearing, no one from the government had suggested Riverview or Mr.

LaGuercia posed a danger to the community. Cynically, the government has manipulated

the DiBella interactions with the felon and the felon’s wife to shield itself and DiBella

(whose relationship with the ATF and government still remains unknown) while using

27 http://www.wfsb.com/video?clipId=8746691&autostart=true

-33-

them to revoke the FFL and as evidence against the defendants in this case. That the

government, in a series of actions, has created the image of Riverview and Mr. LaGuercia

it has, is an absolutely shameful course of hypocrisy.

It just seems that the government has chosen a selective and hypocritical approach

to this case, in an attempt to further taint Mr. LaGuercia. It has gone beyond what is

necessary and appropriate. This is unfortunate, because Mr. LaGuercia has already

suffered enough at the hands of the government.

Sentencing Factors and Argument

Although the federal sentencing guidelines are no longer mandatory, United

States v. Booker, 125 S.Ct. 738 (2005), they are far from moot. The Second Circuit

instructs sentencing courts that their duty is to “consider” the Guidelines. United States v.

Crosby, 397 F.3d 103 (2d Cir., 2005). Anticipating the need to sculpt a new category of

sentences, the Circuit offered the following formulation for sentences imposed in a “non-

Guidelines” manner: “We think it advisable to refer to a sentence that is neither within

the applicable Guidelines range nor imposed pursuant to the departure authority in the

Commission’s policy statements as a `non-Guidelines sentence’ in order to distinguish it

from the term `departure.’” As Crosby noted, there are no bright-line tests for

determining what an appropriate sentence should be; mere “robotic incantations” do not

suffice when weighing the factors a sentencing judge must consider.

Various factors to be considered in imposing sentence are set forth in 18 USCA

-34-

§§ 3553(a). Under §§ 3553(a), the sentencing court must impose a sentence sufficient,

but not greater than necessary, to comply with the purposes set forth in 18 USCA §§

3553(a)(2), which provides that the court, in determining the particular sentence to be

imposed, must consider the need for the sentence imposed to (1) reflect the seriousness of

the offense, to promote respect for the law, and to provide just punishment for the

offense; (2) afford adequate deterrence to criminal conduct; (3) protect the public from

further crimes of the defendant; and (4) provide the defendant with needed educational or

vocational training, medical care, or other correctional treatment in the most effective

manner. Section 3553(a) further provides that in determining the particular sentence to be

imposed, the court must also consider:

* The nature and circumstances of the offense and the history and characteristics of the

defendant.

* The kinds of sentences available.

* The kinds of sentences and the sentencing ranges established for the applicable

category of offense committed by the applicable category of defendant as set forth in the

guidelines issued by the Sentencing Commission and in effect on the date the defendant

is sentenced, or (in the case of a violation of probation or supervised release) the

applicable guidelines or policy statements issued by the Sentencing Commission.

* Any pertinent policy statement issued by the Sentencing Commission that is in effect

on the date the defendant is sentenced.

* The need to avoid unwarranted sentence disparities among defendants with similar

records who have been found guilty of similar conduct.

-35-

* The need to provide restitution to any victims of the offense.

A sentencing court must impose a sentence of the kind, and within the range,

established by the relevant provisions of the Sentencing Guidelines, unless the court finds

that there exists an aggravating or mitigating circumstance of a kind, or to a degree, not

adequately taken into consideration by the Sentencing Commission in formulating the

guidelines that should result in a sentence different from that described. The court, in

determining whether to impose a term of imprisonment, and, if one is to be imposed, in

determining the length of the term, must consider the factors set out in 18 USCA §§

3553(a) to the extent that they are applicable.

The defendants stand before the Court as first time offenders. Both defendants’

convictions stem from their former status as an FFL, a status they no longer possess, and,

by agreement, cannot possess for quite some time. The defendants have been penalized as

a result of related conduct by the revocation of the FFL, which has caused devastating

financial consequences. The defendants have also been paraded before America as a face

of the tragedy at Newtown. Law enforcement officials involved in this case have unfairly

attacked Mr. LaGuercia’s reputation in the national media. The permanence of their

actions cannot be dismissed. This is all to suggest that a significant penalty has already

been imposed.

Because the defendants’ conduct arises from the FFL, there is no chance the

offending conduct may reoccur. The defendants’ lack of criminal history strongly

suggests that experiencing this investigation, prosecution and conviction, along with the

unwarranted media attention, when added to the financial ramifications of the violations,

-36-

in the form of the revocation, is in and of itself more than an adequate punishment for the

crimes at hand.

If that were not enough, Mr. LaGuercia’s age and lack of criminal history provide

the Court with assurance that he poses no risk to the public. See, United States

Sentencing Commission, Recidivism: Criminal History Computation of the Federal

Sentencing Guidelines (2004), Ex. 9 (which shows that those in the age group of 41 to 50

who fall in criminal history category I have an especially low recidivism rate of 6.9%, as

compared to those, for example, in the 36 to 40 years of age bracket who recidivate at a

rate of 12.1% and those under age 21 who recidivate at a rate of 29.5%)28; United States

v. Carmona-Rodriguez, 2005 WL 840464, *5 (S.D.N.Y. 2005) (observing that those

defendants “over the age of 40 . . . exhibit markedly lower rates of recidivism in

comparison to younger defendants.). Additional research performed by the United States

Sentencing Commission also shows that those like Mr. LaGuercia who have no arrests

have an even lower rate of recidivism than those individuals in criminal history category I

who have an arrest history and are “the most empirically identifiable group of federal

offenders who are least likely to offend.” United States Sentencing Commission,

Recidivism and the “First Offender”, May 2004 17.29

28The Sentencing Commission’s report, including Exhibit 9, can be found at:

http://www.ussc.gov/Research_and_Statistics/Research_Publications/2004/200405_Recidivism_Criminal_History.pdf.

29The Report is available at: http://www.ussc.gov/Research_and_Statistics/Research_Publications/2004/200405_Recidivism_First_Offender.pdf

-37-

Conclusion

Based on the above we suggest that a short period of probation, along with the

commitment to refrain from applying for an FFL is “sufficient” to address all of the

sentencing concerns addressed by the Guidelines.

Dated: Westport, CT March 17, 2014 Robert Y. Altchiler

Robert Y. Altchiler, Esq. Attorney for Defendants

Riverview Sales, Inc. and David LaGuercia

111 Saugatuck Avenue Westport, CT 06880 (203) 545.0412 cc: Robert Spector, AUSA (by email)

-38-

EXHIBIT A

Profit / Loss Summary Report From Date:

To Date:

Store Name Riverview Sales

1/1/2013

12/26/2013

Sales

Costs on Sales

NET Profit ($) :

Total % Percent Profit :

IMPORTANT NOTES

Profit/Loss is calculated on all sales that were CLOSED within the selected time frame. OPEN sales, which include outstanding special orders and layaways are included in this report once they are paid off completely AND CLOSED OUT.

This Profit Assumes a cost has been associated with all products at the time of sale. If not, the cost defaults to $0.00 and the profit becomes the selling price as opposed to selling price minus cost. Cost = Trade in Price on a trade-in

It is therefore CRITICAL to this report that the costs be loaded into the system. Run the Detailed Profit / Loss Report to see the exact numbers.

29.15%

$422,970.04

Refunds

$1,285,223.05

$864,215.26

$28,641.15

Cost on Refunds $19,095.19

$197,808.07

$185,338.07

Taxed

$972.19

Tax Exempt

$274.90

This Report Includes transactions on all registers wherein the close date of the receipt was within the From and To Date. This is not specific to a register or to an open/close session.

Taxed Sales Refers to Totals of items that were taxed (The tax amount is NOT included in this total, however!)

Total % Profit = (Total Sales Taxed -All Refunds + Tax Exempt Sales - Total Costs) / (Total Taxed and Tax Exempt Sales-All Refunds )

The following transactions are included in this report. Sale of New, used, serialized, non-serialized, and sale of consigned items. Refunds of any kind, count as losses and figure into the NET profit (thereby reducing it).

Trade-ins are included in the sales figure, but are listed separately. Direct Buys are not included in this calculation at all.

Total Sales include the sale of inventory, services and fees for standard sales, closed layaways and closed special orders.

Total Receipt Lines Used: Total Receipt Lines Skipped38587 1024Sum Checker

COD/Drawer Deposit, Store Credit, Manual Adjustments, Quotes, Trades and Direct Buys are NOT counted in this report.

This Report Does Not require inventory items to contain category and/or department information and is included even when these are blank.

Row Totals

$1,483,031.12

$1,049,553.33

$29,613.34

$19,370.09

Trade-ins $2,185.05

Trade Ins: Some perceive trades as "refunds" thereby lowering the profit, while others do not. Trades are not included in the above calculations, but listed separately for your calculations. To include them, add them where ever you see Refunds.

46

Layaways

Standard Sales

Special Orders

Direct Buys

Cash

Credit Card

Debit Card

Personal Check

Traveler's Check

Store Credit

Transaction Type and Payment Type Summaries for Selected Dates (based on Closed Receipts w/in time Period)

# Items* $$ Totals

70330

909

0

410

$1,467,480.91

$15,071.41

$0.00

$5,678.45 Gift Certificate

0.00

0.00

0.00

0.00

0.00

0.00

0.00

Refunds 914 $29,613.34

*# Items = Quantity * Line ItemInternet 18 $478.80

Gift Certificate Sales $1,750.00

Gift Certificate Sales are Listed Here but are NOT included in the profit/loss until they are used as tender....

19

Trades $2,185.05 0.00 $2,185.05

Net Profit $ = (Sales - Trades - Refunds) - (Costs on Sales - Cost of Refunds - Cost on Trades)

Cost on Trades $1,920.55 0.00 $1,920.55

$422,970. / $1,451,232.7 = $

Report Title: Date/Time Report Was Run: 12/26/2013 10:46:38 AM

1Page Number:

Report Run By: David LaGuercia

-39-

Profit / Loss Summary Report From Date:

To Date:

Store Name Riverview Sales

1/1/2012

12/31/2012

Sales

Costs on Sales

NET Profit ($) :

Total % Percent Profit :

IMPORTANT NOTES

Profit/Loss is calculated on all sales that were CLOSED within the selected time frame. OPEN sales, which include outstanding special orders and layaways are included in this report once they are paid off completely AND CLOSED OUT.

This Profit Assumes a cost has been associated with all products at the time of sale. If not, the cost defaults to $0.00 and the profit becomes the selling price as opposed to selling price minus cost. Cost = Trade in Price on a trade-in

It is therefore CRITICAL to this report that the costs be loaded into the system. Run the Detailed Profit / Loss Report to see the exact numbers.

25.66%

$1,039,757.89

Refunds

$3,934,632.68

$2,989,390.13

$55,000.38

Cost on Refunds $38,579.74

$499,247.59

$387,303.11

Taxed

$5,331.21

Tax Exempt

$4,221.53

This Report Includes transactions on all registers wherein the close date of the receipt was within the From and To Date. This is not specific to a register or to an open/close session.

Taxed Sales Refers to Totals of items that were taxed (The tax amount is NOT included in this total, however!)

Total % Profit = (Total Sales Taxed -All Refunds + Tax Exempt Sales - Total Costs) / (Total Taxed and Tax Exempt Sales-All Refunds )

The following transactions are included in this report. Sale of New, used, serialized, non-serialized, and sale of consigned items. Refunds of any kind, count as losses and figure into the NET profit (thereby reducing it).

Trade-ins are included in the sales figure, but are listed separately. Direct Buys are not included in this calculation at all.

Total Sales include the sale of inventory, services and fees for standard sales, closed layaways and closed special orders.

Total Receipt Lines Used: Total Receipt Lines Skipped59278 3600Sum Checker

COD/Drawer Deposit, Store Credit, Manual Adjustments, Quotes, Trades and Direct Buys are NOT counted in this report.

This Report Does Not require inventory items to contain category and/or department information and is included even when these are blank.

Row Totals

$4,433,880.27

$3,376,693.24

$60,331.60

$42,801.27

Trade-ins $321,109.44

Trade Ins: Some perceive trades as "refunds" thereby lowering the profit, while others do not. Trades are not included in the above calculations, but listed separately for your calculations. To include them, add them where ever you see Refunds.

1093

Layaways

Standard Sales

Special Orders

Direct Buys

Cash

Credit Card

Debit Card

Personal Check

Traveler's Check

Store Credit

Transaction Type and Payment Type Summaries for Selected Dates (based on Closed Receipts w/in time Period)

# Items* $$ Totals

86492

2845

18

1696

$3,711,265.63

$520,236.73

$2,275.15

$296,965.26 Gift Certificate

0.00

0.00

0.00

0.00

0.00

0.00

0.00

Refunds 1257 $60,331.60

*# Items = Quantity * Line ItemInternet 775 $200,167.26

Gift Certificate Sales $20,466.44

Gift Certificate Sales are Listed Here but are NOT included in the profit/loss until they are used as tender....

776

Trades $321,109.44 0.00 $321,109.44

Net Profit $ = (Sales - Trades - Refunds) - (Costs on Sales - Cost of Refunds - Cost on Trades)

Cost on Trades $321,210.63 0.00 $321,210.63

$1,039,75 / $4,052,439.2 = $

Report Title: Date/Time Report Was Run: 12/26/2013 10:50:23 AM

1Page Number:

Report Run By: David LaGuercia

-40-

Profit / Loss Summary Report From Date:

To Date:

Store Name Riverview Sales

1/1/2011

12/31/2011

Sales

Costs on Sales

NET Profit ($) :

Total % Percent Profit :

IMPORTANT NOTES

Profit/Loss is calculated on all sales that were CLOSED within the selected time frame. OPEN sales, which include outstanding special orders and layaways are included in this report once they are paid off completely AND CLOSED OUT.

This Profit Assumes a cost has been associated with all products at the time of sale. If not, the cost defaults to $0.00 and the profit becomes the selling price as opposed to selling price minus cost. Cost = Trade in Price on a trade-in

It is therefore CRITICAL to this report that the costs be loaded into the system. Run the Detailed Profit / Loss Report to see the exact numbers.

25.14%

$814,751.89

Refunds

$3,300,117.11

$2,542,908.57

$53,984.26

Cost on Refunds $38,624.97

$353,999.64

$280,152.56

Taxed

$3,952.42

Tax Exempt

$3,155.47

This Report Includes transactions on all registers wherein the close date of the receipt was within the From and To Date. This is not specific to a register or to an open/close session.

Taxed Sales Refers to Totals of items that were taxed (The tax amount is NOT included in this total, however!)

Total % Profit = (Total Sales Taxed -All Refunds + Tax Exempt Sales - Total Costs) / (Total Taxed and Tax Exempt Sales-All Refunds )

The following transactions are included in this report. Sale of New, used, serialized, non-serialized, and sale of consigned items. Refunds of any kind, count as losses and figure into the NET profit (thereby reducing it).

Trade-ins are included in the sales figure, but are listed separately. Direct Buys are not included in this calculation at all.

Total Sales include the sale of inventory, services and fees for standard sales, closed layaways and closed special orders.

Total Receipt Lines Used: Total Receipt Lines Skipped47566 2973Sum Checker

COD/Drawer Deposit, Store Credit, Manual Adjustments, Quotes, Trades and Direct Buys are NOT counted in this report.

This Report Does Not require inventory items to contain category and/or department information and is included even when these are blank.

Row Totals

$3,654,116.75

$2,823,061.13

$57,936.68

$41,780.44

Trade-ins $355,418.80

Trade Ins: Some perceive trades as "refunds" thereby lowering the profit, while others do not. Trades are not included in the above calculations, but listed separately for your calculations. To include them, add them where ever you see Refunds.

1188

Layaways

Standard Sales

Special Orders

Direct Buys

Cash

Credit Card

Debit Card

Personal Check

Traveler's Check

Store Credit

Transaction Type and Payment Type Summaries for Selected Dates (based on Closed Receipts w/in time Period)

# Items* $$ Totals

58828

3006

2

1328

$3,001,842.37

$492,686.60

$698.00

$207,180.70 Gift Certificate

0.00

0.00

0.00

0.00

0.00

0.00

0.00

Refunds 1060 $57,936.68

*# Items = Quantity * Line ItemInternet 700 $158,889.78

Gift Certificate Sales $20,156.94

Gift Certificate Sales are Listed Here but are NOT included in the profit/loss until they are used as tender....

701

Trades $355,418.80 0.00 $355,418.80

Net Profit $ = (Sales - Trades - Refunds) - (Costs on Sales - Cost of Refunds - Cost on Trades)

Cost on Trades $355,271.30 0.00 $355,271.30

$814,751. / $3,240,761.2 = $

Report Title: Date/Time Report Was Run: 12/26/2013 10:56:13 AM

1Page Number:

Report Run By: David LaGuercia

-41-

EXHIBIT B

-42-

-43-

-44-

Related Documents