1 Risks, Returns, and Optimal Holdings of Private Equity: A Survey of Existing Approaches Andrew Ang Morten Sorensen June 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Risks,Returns,andOptimalHoldingsofPrivateEquity:A

SurveyofExistingApproaches

AndrewAng

MortenSorensen

June2012

2

PolicyRecommendations

Privateequity(PE)investmentsareinvestmentsinprivately‐heldcompanies,

tradingdirectlybetweeninvestorsandnotonorganizedexchanges.Wesummarize

ourfindingsandrecommendationsforinvestmentsinPEasfollows:

1. Standardempiricalapproachesusedtoestimatetheriskandreturnof

standardpublicly‐tradedsecuritiesaredifficulttoapplytoPEinvestment.

ComplicatingfeaturesofPEinvestmentsincludedatalimitations,the

irregularnatureofPEinvestments,andthesampleselectionproblemsthat

typicallyariseinreportedPEdata.Correctingforthesedifficultiesrequires

sophisticatedeconometrictechniques.Naïveanalyses,withoutappropriate

adjustment,maysubstantiallyunderstatePEriskandvolatility,and

exaggerateperformanceestimates.

Recommendation:ReportedestimatesofPEriskandreturnshouldbeinterpreted

withskepticism.Estimatesbasedonsimplestandardmethodologiesfailtomake

correctionsthatarerequiredduetothespecificfeaturesofPEinvestments.Studies

thatdevelopmethodologiestoperformthesecorrectionsarepreliminary,anda

consensusontheappropriateadjustmentshasyettoemerge,butnaïveanalysis

withoutaccountingforbiasesoverstatesPEreturnsandunderstatesPErisk.

2. Commonlyusedfund‐performancemeasure,suchastheIRR,TVPImultiple,

andPME,areproblematic.Thereissubstantialvariationinestimatesofthese

measuresacrossstudiesanddatasources.Themeasurescan,tosomeextent,

bemanipulatedbythetimingandmagnitudesoftheindividualinvestments.

Thesefund‐performancemeasuresuseonlycoarseadjustments,ifany,for

theriskoftheinvestments.Finally,thesemeasuresarenotderivedfrom

underlyingfinancialtheoriesofriskandreturn,makingthemdifficultto

interpretconsistently.

3

Recommendation:Commonlyreportedperformancemeasuresshouldbe

interpretedwithcaution.Theyarenotreturnmeasures.

3. Modelsofassetallocationthattakeintoaccounttransactionscosts,whichare

largeforPE,andilliquidityrisk,whichissubstantialforPE,recommend

modestholdingsofPE.Inthesemodels,rebalancingwillbeinfrequent,so

wideswingsintheholdingsofPEshouldbeexpected,andtheholdingsof

illiquidPEwillbemuchlowerthanpredictedbyassetallocationmodels

assumingthatallassetscanberebalancedwhendesired.

Recommendation:WhendeterminingoptimalPEallocations,assetallocation

modelsmusttakeintoaccounttheinabilitytorebalancePEpositions.Thereshould

begenerallymodestallocationstoilliquidPEinvestments.

4. CurrentPEvehicleshavesubstantialagencyissueswhichpublicequity

vehiclesdonot.WhilethereisheterogeneityinPEcontracts,PEfeesare

largeandconsumeatleastone‐fifthofgrossPEreturns.Incentivefees

accountforlessthanone‐thirdofgeneralpartner(agent)compensation.

Recommendation:Ifanyofthefeespaidtoexternally‐managedPEfundswithGPs

canbebroughtbackin‐housetoinstitutionalassetowners,andifthequalityofthe

PEinvestmentscanbemaintained,therewillbesubstantialsavingstotheasset

owners.

4

Abstract

WesurveytheacademicliteratureabouttherisksandreturnsofPEinvestingand

optimalPEallocations.Empirically,theirregularnatureofPEinvestments

complicatestheestimationandinterpretationofstandardriskandreturnmeasures.

Whilethesecomplicationshaveleadtosubstantialdisparityinperformance

estimatesreportedacrossstudies,naïveanalysisnotaccountingforbiases

overstatesPEmeanreturnsandunderestimatesrisk.AllocationstoPEmusttake

intoaccountsubstantialilliquidityandtransactioncostsandsuggestmodest

optimalholdingsoftheseassets.WhilecurrentcontractsinPEaddressbothmoral

hazardandinformationfrictions,therearesubstantialmanagementand

performancefeesearnedbythePEfirms.

5

I.Introduction

Privateequity(PE)investmentsareinvestmentsinprivately‐heldcompanies,

tradingdirectlybetweeninvestors,notonorganizedexchanges.Theinvestments

aretypicallymadethroughaPEfundorganizedasalimitedpartnershipwiththe

investorasalimitedpartner(LP)andthePEfirmasthegeneralpartner(GP),

overseeingandmanagingtheinvestmentsintheindividualcompanies.Depending

onthetypeofcompaniestheyinvestin,PEfundsaretypicallyclassifiedasbuyout

(BO),venturecapital(VC),orsomeothertypeoffundspecializinginotherilliquid

non‐listedinvestments.BOfundsinvestinmatureestablishedcompanies,using

substantialamountsofleveragetofinancethetransactions.VCfundsinvestinhigh‐

growthstart‐ups,usinglittleornoleverage.Finally,itisnotuncommonforLPsto

alsoinvestdirectlyintoindividualcompanies.Theseinvestmentsareoften

structuredasco‐investmentsintotheportfoliocompaniesalongsidethe

investmentsmadethroughthePEfund.

PEisoftenconsideredadistinctassetclass,anditdiffersfrominvestmentsinpublic

equityinfundamentalways:ThereisnoactivemarketforPEpositions,making

theseinvestmentsilliquidanddifficulttovalue.Theinvestmentsarelong‐term

investments.PEfundstypicallyhavehorizonsoftentothirteenyearsduringwhich

theinvestedcapitalcannotberedeemed.Moreover,partnershipagreements

specifyingthefunds’governancearecomplexdocuments,specifyingtheGPs

compensationasacombinationofongoingfees(managementfees),aprofitshare

(carriedinterest),transactionfees,andotherfees.

ThisarticlesurveystheacademicresearchabouttherisksandreturnsofPE

investingandtheoptimalholdingsofPEinaninvestor’sportfolioalongwitha

reviewofPEcontracts.Researchershavehadlimitedaccesstoinformationabout

thenatureandperformanceofPEinvestments,soresearchinthisareais

preliminaryandofteninconclusive.Researchintomanyimportantaspectsofthese

investments,suchastheperformanceofPEintherecession,thesecondarymarket

6

forLPpositions,andLPs’co‐investments,hasonlyrecentlybegun.Oursurveyonly

coversstudiesofPEdefinedascompaniesownedbyPEfunds.Wedonotconsider

thesubstantialnumberofprivately‐heldandindependentlyownedcompanies,

rangingfromindependentgrocerystoresanddrycleanerstolargefamily‐owned

businesses(seeMoskowitzandVissing‐Jorgensen(2002),Kartashova(2011)and

Faccio,Marchica,McConnell,andMura(2012)).

SectionIIintroducestwoproblemsthatresearchhasencounteredinmeasuringPE

riskandreturns.ThefirstproblemisthestatisticalproblemthatarisesbecausePE

returnsareonlyobservedinfrequently,typicallywithwell‐performingfundsbeing

overrepresentedinthedata.Thismakesitdifficulttoestimatestandardmeasuresof

riskandreturn,suchasCAPMalphasandbetas.Afteraddressingthisproblem,a

secondproblemishowtointerprettheresultingestimates.Standardasset‐pricing

modelsarederivedunderassumptionsthatareappropriatefortraditionalfinancial

markets–withtransparent,liquid,andlow‐frictiontransactions.These

assumptionsareproblematicforPEinvestments,andtheestimatedalphasand

betasneedtobeadjustedtoprovidemeaningfulmeasuresofriskandreturninthe

PEcontext.OnewayofinterpretingtherisksandreturnsofPEinvestments,

especiallyforilliquidityrisk,isforaninvestortoconsiderPEfromaninvestor‐

specificassetallocationcontext.

SectionIIIsummarizestheexistingliteratureontheoptimalallocationofPEin

portfoliosconsistingofpublicliquidpublicequityandilliquidPE.Anewgeneration

ofassetallocationmodelsconsiderstheseissues;thefirstgenerationofasset

allocationapproachesassumedthatassetscanberebalancedwithoutcostatany

time.Theliteraturesonassetallocationincorporatingtransactionscosts,whichare

veryhighforPEinvestment,andsearchfrictions,sincecounterpartiesareoften

hardtofindfortransferringPEinvestments,leadtostrongrecommendationson

optimalholdingsofilliquidPEassets.

InSectionIV,wesurveytheliteratureonPEcontractswithaspecialemphasison

feesandopaqueness.MostPEinvestmentsaremadethroughintermediaries.

7

CurrentPEinvestmentvehiclescannotdisentanglefactorreturnsuniquetothePE

assetclassfrommanagerskill.Furthermore,commonlyusedcontractsmay

exacerbate,ratherthanalleviateagencyissues.

II.EstimatingPrivateEquityRiskandReturn

IIA.DefiningRiskandReturns

Tofixnotationandterminology,itisusefultostartfromthestandardmodelofrisk

andreturn.Fortradedfinancialassets,riskandreturnareusuallymeasuredinthe

contextofthecapitalassetpricingmodel(CAPM)asthe and coefficients

estimatedintheone‐factorlinearregression(theexpectedreturnregression),1

.

Inthisequation, isthereturnearnedbytheinvestorfromperiodt‐1toperiod

t, istherisk‐freerateovertheperiodfromt‐1tot,and isthereturnon

themarketportfolio.Thedefinitionofthereturnearnedonafinancialassetfrom

timet‐1totis

11,

whereCF(t)isthecashflowpaidoutattimet,andP(t)isthemarketpricequotedat

timet,immediatelyafterthepaymentofthecashflow.Fortradedassets,the

expectedreturnregressionisstraightforwardtoestimatebyregressingtheasset’s

observedreturns,sayweekly,onthecorrespondingmarketreturnsoverthesame

periods.

1Thisspecificationassumesthatalphaandbetaareconstantoverthedurationofthedeal.Whileitwouldbeinterestingtoinvestigatethetermstructureoftheriskandreturn,thedatalimitationsandothercomplicationsdescribedherehavepreventedempiricalstudiesofthesedynamics.ThereissubstantialevidencethatalphasandbetasvaryovertimeforlistedequityasAngandKristensen(2012)show.

8

Underappropriateassumptionsaboutinvestors’preferences,suchasconstant

relativeriskaversion(CRRA)ormean‐varianceutility,alongwithassumptions

aboutthemarketenvironment,suchastheabsenceoftransactioncosts,short‐sales

constraints,andtheabilityofinvestorstocontinuouslytradeandrebalancetheir

portfolios,theCAPMmodelspecifiesthateachasset’sexpectedreturnisgivenby

theexpectedreturnregressionwithanalphaequaltozero.Thisimportantresult

hasseveralimplications:Itimpliesthattheappropriatemeasureofriskis ,which

measuresthecorrelationbetweenthereturnontheassetandthereturnonthe

overallmarket(systematicrisk).IntheCAPM,systematicriskistheonlyriskthatis

priced.Idiosyncraticriskisnotpricedbecauseitcanbediversified.Theexpected

returnregressionalsoimpliesthatanasset’sexpectedreturnincreaseslinearlyin .

Finally,itimpliesthatinequilibrium, shouldbezero.Apositive canbe

interpretedasanabnormalpositivereturn.

Followingthislogic,thestandardapproachtoevaluatingrisksandreturnsof

financialassetsproceedsintwosteps:First, and areestimatedusingthe

expectedreturnregression.Second,invokingtheCAPM,theestimated is

interpretedasanabnormalrisk‐adjustedreturn,andthe isinterpretedasthe

systematicrisk.

ForPEinvestments,problemsariseatbothsteps:Atthefirststep,privatelyheld

companiesdonothaveregularlyobservedmarketvalues,bydefinition,andthe

returnsearnedfrominvestinginthesecompaniesareonlyobservedatexit.Hence,

period‐by‐periodreturnsareunavailable,makingitdifficulttoestimatethe

expectedreturnregressiondirectly.Betterperformingprivatelyheldcompanies

mayalsobeoverrepresentedinthedata,creatingsampleselectionproblemsthat

wouldleadthe coefficienttobeoverestimatedandthe coefficienttobe

underestimated.Atthesecondstep,afterestimating and ,itisnotobviousthat

thesecoefficientsappropriatelymeasureexcessreturnsandrisk,respectively.The

assumptionsofliquidandtransparentmarketsunderlyingtheCAPMarefarfrom

therealitiesofPEinvesting.ToreflectactualrisksandreturnsfacingLPinvestors,

9

theestimatedparametersmayrequirevariousadjustmentstoaccountforthecost

ofilliquidity,idiosyncraticrisk,persistence,fundingrisk,etc.

Thelackofregularlyquotedmarketpricesandreturnspresentsafundamental

challengeforempiricalstudiesoftheriskandreturnofPEinvestments.Several

alternativeapproacheshavebeendevelopedusingcompany‐leveldatawith

individualperformanceandvaluationmeasuresandfund‐leveldatawithentire

cash‐flowstreamsbetweenLPsandGPs.Thebenefitsandlimitationsofthese

approachesarediscussednext.

IIB.EstimatesUsingCompany‐levelData

Company‐leveldatacontaininformationaboutinvestmentsbyBOorVCfundsin

individualcompanies.Foreachinvestment,thedatatypicallycontainthenameof

thecompany,theinvestedamount,investmentdate,andtheexitdateandamount.

Suchdataareconfidentialandproprietary,andexistingstudieshaveobtaineddata

throughdirectcontactswithLPsandprofessionaldataproviders.

Franzoni,Nowak,andPhalippou(2012)analyzecompany‐leveldataforBO

investments.Cochrane(2005)andKortewegandSorensen(2010)usecompany‐

leveldataforindividualinvestmentsbyVCsinstart‐ups.TheapplicationtoVC

investingismorechallenging,becausethesampleselectionproblemisparticularly

severefortheseinvestments.

Comparedtofund‐leveldata,company‐leveldatapresenttwoadvantages:First,

therearemanymorecompaniesthanfunds,whichimprovesthestatisticalpowerof

theanalysis.Companiescanbeclassifiedintermsofindustriesandtypes,allowing

foramorenuanceddifferentiationoftherisksandreturnsacrossindustriesand

types,andovertime.Second,investmentsinindividualcompanieshavewell‐

definedreturns.Absentintermediatecashflows,thereturn,asdefinedabove,canbe

calculateddirectlyfromtheinitialinvestmentandthedistributionoftheproceeds

atexit.Aslongasintermediatecashflowsarefewandsmall,asforBOinvestments,

10

thiscalculationprovidesareasonablereturnmeasure.Withmoreintermediatecash

flows,suchasforVCinvestments,thecalculationmaybeperformedseparatelyfor

eachinvestmentround.

Onedisadvantageofcompany‐leveldataisthatthereturnfigurestypicallydonot

subtractmanagementfeesandcarriedinterestpaidbytheLPstotheGPs,andthe

estimatedrisksandreturnsreflectthetotal(grossoffees)risksandreturnsofthe

investments,notthoseearnedbyanLP(netoffees).Translatingbetweennet‐of‐fee

andgross‐of‐feereturnstypicallyrequiresadditionalassumptionsandnumerical

simulations(seeMetrickandYasuda(2010)andFranzoni,Nowak,andPhalippou

(2012)fortwoapproaches).

Continuous‐TimeSpecificationsAtechnicaldisadvantageofcompany‐leveldata

isthatthereturnsaremeasuredoverperiodsofdifferentlengths.Returnsare

measuredfromthetimeoftheinitialinvestmenttothetimeoftheexit,andthe

durationvariessubstantiallyacrossinvestments.Thestandard(discrete‐time)

CAPMmodelisaone‐periodmodel,wheretheperiodmaylastfor,say,aday,a

month,oraquarter.Itdoesnotcompound,however,andallreturnsmustbe

calculatedoverperiodsofthesameduration.

Astandardsolutionistousethecontinuous‐timeversionoftheCAPM,whichdoes

compoundandwhichallowsforacomparisonofrisksandreturnsofinvestmentsof

differentdurations.Campbell,Lo,MacKinlay(1997)provideanextensivediscussion

oftheunderpinningsofthismodel.Inthecontinuous‐timeCAPM,theexpected‐

returnregressionisrestatedinlog‐returns(continuously‐compoundedreturns)as

ln 1 ln 1 ln 1 ln 1 .

Onecomplicationisthattheestimatedinterceptinversionoftheexpectedreturn

equationcannotbeinterpretedasanabnormalreturn,asinthestandarddiscrete‐

timeCAPM.Underspecificassumptionsaboutthewayvolatilityincreaseswiththe

11

durationoftheinvestments,theabnormalreturnscanbecalculatedusingan

adjustmentthataddsthevolatilityasfollows

.

Thisnon‐linearadjustmentleadstohighalphaswhenthevolatilityofindividual

dealsishigh(seeCochrane(2005)andKortwegandSorensen(2011)fordetails

aboutthederivationandimplementationoftheadjustment).Forexample,Cochrane

(2005)reportsanannualvolatilityaround90%,resultinginanestimatedalphaof

32%annually,whichappearsunreasonablyhighcomparedtostudiesusingfund‐

leveldata,raisingdoubtsabouttheappropriatenessoftheassumptionsaboutthe

growthofvolatilitywiththedurationoftheinvestments.

Franzoni,Nowak,andPhalippou(2012)sidestepsthisproblembyestimatingthe

modelafterformingportfoliosofdeals,ratherthanindividualones.This

substantiallylowersthevolatilitiesandreducesthemagnitudeofthisadjustment.It

does,however,reducetheotheradvantagesofusingindividualdeals:inparticular,

itreducesstatisticalpowerandrequiresthemtouseamodifiedIRR(MIRR)

approximationofreturns.

SelectionBiasAnotherprobleminusingcompany‐leveldataissampleselection.

Toillustrate,VCinvestmentsarestructuredovermultiplefinancingrounds,and

better‐performingcompaniestendtoraisemoresuchrounds.Hence,datasetswith

valuationsofindividualVCroundsaredominatedbythesebetter‐performing

companies.Moreover,distressedcompaniesareusuallynotformallyliquidated,and

areoftenleftasshellcompanieswithouteconomicvalue(“zombies”).This

introducesanotherselectionproblemfortheempiricalanalysis.Whenobserving

oldcompanieswithoutnewfinancingroundsorexits,thesecompaniesmaybealive

andwellortheymaybezombies,inwhichcaseitisunclearwhenthewrite‐offof

thecompany’svalueshouldberecorded.ThislatterproblemislesssevereforBO

investments,becausethesemostlyresultinawell‐definedexit(acquisitionorIPO)

orawell‐definedliquidation.

12

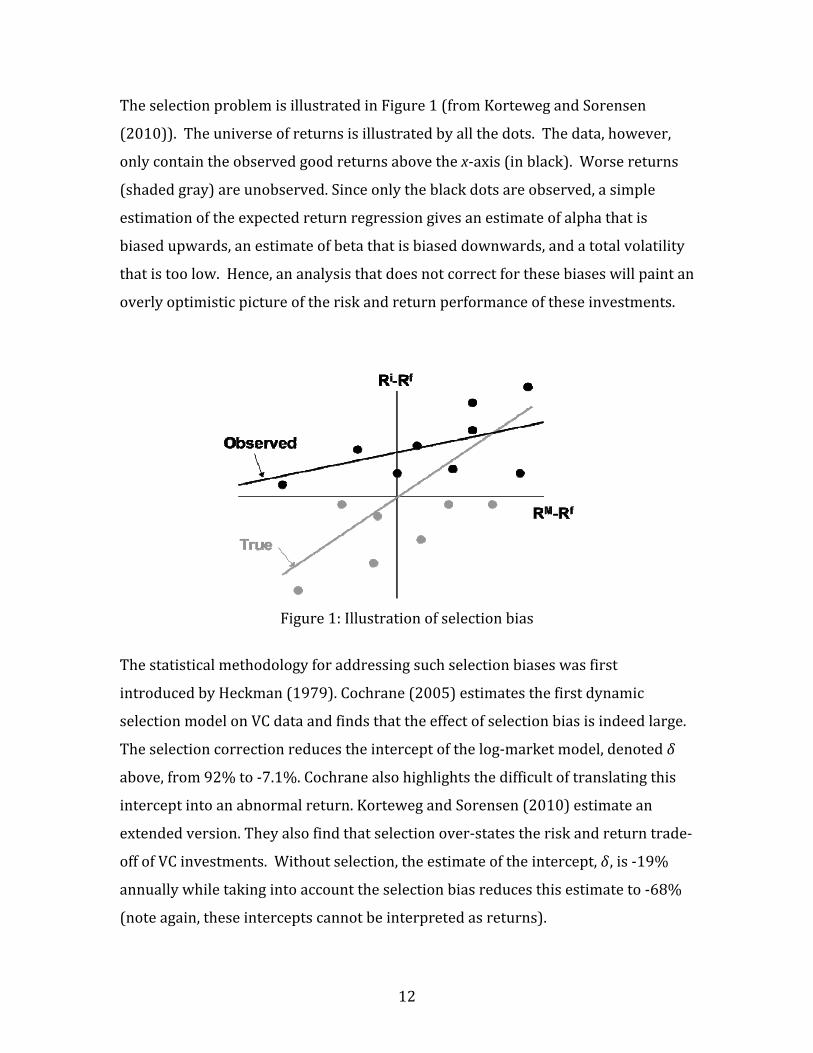

TheselectionproblemisillustratedinFigure1(fromKortewegandSorensen

(2010)).Theuniverseofreturnsisillustratedbyallthedots.Thedata,however,

onlycontaintheobservedgoodreturnsabovethex‐axis(inblack).Worsereturns

(shadedgray)areunobserved.Sinceonlytheblackdotsareobserved,asimple

estimationoftheexpectedreturnregressiongivesanestimateofalphathatis

biasedupwards,anestimateofbetathatisbiaseddownwards,andatotalvolatility

thatistoolow.Hence,ananalysisthatdoesnotcorrectforthesebiaseswillpaintan

overlyoptimisticpictureoftheriskandreturnperformanceoftheseinvestments.

Figure1:Illustrationofselectionbias

Thestatisticalmethodologyforaddressingsuchselectionbiaseswasfirst

introducedbyHeckman(1979).Cochrane(2005)estimatesthefirstdynamic

selectionmodelonVCdataandfindsthattheeffectofselectionbiasisindeedlarge.

Theselectioncorrectionreducestheinterceptofthelog‐marketmodel,denoted

above,from92%to‐7.1%.Cochranealsohighlightsthedifficultoftranslatingthis

interceptintoanabnormalreturn.KortewegandSorensen(2010)estimatean

extendedversion.Theyalsofindthatselectionover‐statestheriskandreturntrade‐

offofVCinvestments.Withoutselection,theestimateoftheintercept, ,is‐19%

annuallywhiletakingintoaccounttheselectionbiasreducesthisestimateto‐68%

(noteagain,theseinterceptscannotbeinterpretedasreturns).

13

Inthecontinuous‐timemodel,theestimated coefficientcanbeinterpretedasthe

CAPMsystematicrisk,withoutadjustments.Cochranefindsaslopeof0.6‐1.9forthe

systematicrisk.Thisfigureseemslow,however.Itincludesestimatesatthe

individualindustrylevelsof,forexample,‐0.1forretailinvestments.

KortewegandSorensen(2010)reportsubstantiallyhigherbetaestimatesof2.6‐2.8,

whichmaybemorereasonableforyoungstartupsfundedbyVCinvestors.They

alsofindsubstantialtimevariationasVCinvestinghasmatured.Theyestimate

alphasovertheperiods1987‐93,1994‐2000,and2001‐2005,andfindthatthe

alphasintheearlyperiodwerepositivebutmodest,thealphasinthelate1990s

wereveryhigh,butthealphasinthe2000shavebeennegative,consistentwith

patternsfoundbystudiesusingfund‐leveldata.

IIC.EstimatesUsingFund‐levelData

Fund‐leveldataaretypicallyobtainedfromLPswithinvestmentsacrossmanyPE

funds.Eachobservationrepresentstheperformanceofanentireportfolioof

investments.Inadditiontoinformationaboutthefund,suchasitstypeandvintage

year,thesedatamaycontainthecashflowstreambetweentheLPandthefundora

performancemeasurecalculatedfromthiscashflowstream(suchastheIRR,TVPI

andPME,asdiscussedbelow).Whenindividualcashflowsareavailable,however,

theyaretypicallynottiedtoindividualportfoliocompanies.

Thereareseveraladvantagestofund‐leveldata:First,fund‐leveldatareflectactual

LPreturns,netoffees,resultinginestimatesoftherisksandreturnsactually

realizedbytheLPs.Thesampleselectionproblemissmaller,sincetheperformance

ofcompaniesthatultimatelyneverproduceanyreturnsfortheinvestingfunds

(zombies)iseventuallyreflectedinthefund‐levelcashflows.Othersampleselection

problemsmayarise,however.Fund‐levelperformanceistypicallyself‐reported,and

betterperformingfundsmaybemorelikelytoreporttheirperformance(as

suggestedbyPhalippouandGottschalg(2009),althoughStucke(2011)arguesthat

14

returnsreportedbyVentureEconomicsunderstateactualperformance).2Still,

theseselectionproblemsarelikelysmallerthantheproblemsthatarisewith

company‐leveldata.Finally,sincefundshavesimilarlifetimes(typicallytenyears),

theexpectedreturnequationcanbeestimateddirectly,avoidingtheproblemswith

thecontinuous‐timelog‐returnspecificationusedforcompany‐leveldata.

Fund‐levelPerformanceMeasuresThemaindisadvantageoffund‐leveldatais

thatitisunclearhowtomeasurethe“return.”Calculatingperiod‐by‐periodreturns,

aspreviouslydefined,requiresassessingthemarketvaluesofthePEinvestment

(P(t)inthereturncalculation)atintermediateperiods.Absentquotedmarket

values,however,thiscalculationisinfeasible.Unfortunately,marketvaluesare

typicallyunavailable,andreportedNAVsarenoisysubstitutesforthesevalues(for

example,ithasbeencustomarytovalueinvestmentsinindividualcompaniesatcost

untilthecompanyexperiencedamaterialchangeinthecircumstances,whichdoes

notcapturesmallerongoingchangesintheprospectsandmarketvaluesofthese

companies).Giventheabsenceofregularlyquotedreturns,severalalternative

measureshavebeenproposed.However,noneofthesemeasuresdefineareturn,as

previouslydefined,andtheirrelationshipstoassetpricingmodelsaresomewhat

tenuous.

InternalRateofReturn(IRR)Anaturalstartingpointistointerprettheinternal

rateofreturn(IRR)ofthecashflowsbetweentheLPandGPasareturnearnedover

thelifeofthefund.DenotingthecashflowattimetasCF(t),andseparatingthose

intothecapitalcallspaidbytheLPtotheGP,denotedCall(t),andthedistributions

ofcapitalfromtheGPbacktotheLP,denotedDist(t),theIRRisdefinedasthe

solutiontotheequation:

1 10,

2AnecdotalevidencefromHarris,Jenkinson,andKaplan(2011)suggeststhatthisbiasmadeVentureEconomicsmoreattractiveforbenchmarkingGPperformance.

15

⇒∑

1

∑1

1.

LjungqvistandRichardson(2003)investigatecash‐flowdatafromalargeLP

investinginfundsraisedin1981‐1993(19VCfundsand54BOfunds).Theyreport

averagefundIRRs(netoffees),combiningPEandVCinvestments,for1981‐1993,

of19.81%,whiletheaverageS&P/500returnis14.1%,suggestingthatPE

investmentsoutperformthemarket.

KaplanandSchoar(2005)usefund‐levelquarterlyperformancemeasuresfrom

VentureEconomicscoveringfor1,090VCandBOfunds,ofwhich746fundswere

fullyormostlyliquidatedatthetimeofthestudy.KaplanandSchoarfindVCandBO

returnsslightlybelowthoseoftheS&P/500indexonanequal‐weightedbasis

(value‐weightedVCfundsperformslightlybetterthantheindex)usingtheirsample

offullyliquidatedfunds.Thevalue‐weightedIRRequals13%.3Extendingthe

sampletomature,butnotliquidatedfunds,raisestheIRRforVCto30%butleaves

itunchangedat13%forBOs,resultinginanoverallaverageIRRof18%.4

FocusingonVCinvestments,BygraveandTimmons(1992)findanaverageIRRof

13.5%over1974‐1989.GompersandLerner(1997),usinginvestmentsofasingle

VCfirm,reportanIRRof30.5%over1972‐1997.

ArecentsurveybyHarris,Jenkinson,andKaplan(2011)summarizestheacademic

studiesusingfund‐leveldatafromvariousdataproviders.5ForBOfunds,they

3AspointedoutbyPhalippouandGottschalg(2009),itisnotobvioushowtovalue‐weightPEfunds.Onepossibilityistoweightbytotalcommittedcapital,butfundsvaryintheirinvestmentspeed,andworseperformingfundsmayinvestmoreslowly,introducingadownwardbiasinvalue‐weightedperformanceestimates.4ThefinalreportedNAVoffundsthatarenotfullyliquidatedistreatedasafinalcashflowinthecalculation.PhalippouandGottschalg(2009)arguethatinterimNAVsmayexaggeratetheactualvalues,leadingtoupward‐biasedperformanceestimates.Incontrast,Stucke(2011)arguesthattheNAVsaresubstantiallybelowactualeconomicvalue,usingVentureEconomicsdata.KaplanandSchoar(2005)andHarris,Jenkinson,andKaplan(2011)usereportedNAVsasstated.5ThesestudiesincludeLjungqvistandRichardson(2003),KaplanandSchoar(2005),PhalippouandGottschalg(2008),andRobinsonandSensoy(2011b).

16

reportweightedaverageIRRsof12.3‐16.9%.ForVCfunds,theweightedaverage

IRRsare11.7‐19.3%.Acrosstimeperiods,BOfundshavehadmorestable

performance,withweightedaverageIRRsof15.1‐22.0%inthe1980s,11.8‐19.3%

inthe1990s,and5.8‐12.8%inthe2000s.VCfundperformancehasmorevolatile

overtime,withweightedaverageIRRsrangingfrom8.6to18.7%inthe1980s,22.9

to38.6%inthe1990s,and‐4.9to1.6%inthe2000s.

OverallthesefiguresrevealsubstantialvariationinIRRsacrossstudiesanddata

sources.Moreover,theIRRisaproblematicmeasureofeconomicperformance.The

IRRisanabsoluteperformancemeasurethatdoesnotcalculateperformance

relativetoabenchmarkormarketreturn.Moreover,theIRRcalculationimplicitly

assumesthatinvestedandreturnedcapitalcanbereinvestedattheIRRrate.Ifa

fundmakesanearlysmallinvestmentwithalargequickreturn,thissingle

investmentcanlargelydefinetheIRRfortheentirefund,regardlessofthe

performanceofsubsequentinvestments.Indeed,Phalippou(2011)suggeststhat

GPsmayactivelymanagetheirinvestmentstoinflatefundIRRs.

TotalValuetoPaid‐inCapitalMultiple(TVPI)Analternativeperformance

measurethatislesssusceptibletomanipulationthantheIRRisthetotal‐value‐to‐

paid‐incapital(TVPI)multiple.Thismultipleiscalculatedasthetotalamountof

capitalreturnedtotheLPinvestors(netoffees)dividedbythetotalamount

invested(includingfees).Formally,theTVPIisdefinedas

∑∑

.

Thiscalculationisperformedwithoutadjustingforthetimevalueofmoney.

WhereastheIRRiscalculatedundertheimplicitassumptionthatcapitalcanbe

reinvestedattheIRRrate,theTVPIiscalculatedundertheimplicitassumptionthat

thecapitalcanbereinvestedatazerorate.Harris,Jenkinson,andKaplan(2011)

reportweightedaverageTVPIsof1.76‐2.30forBOinvestors,and2.19‐2.46forVCs.

Thismultiplevariessubstantiallyovertime,though.ForBOfunds,thereported

17

multiplewas2.72‐4.05inthe1980s,1.61‐2.07inthe1990s,and1.29‐1.51inthe

2000s.ForVCfunds,thereportedmultiplewas2.31‐2.58inthe1980s,3.13‐3.38in

the1990s,and1.06‐1.09inthe2000s.

PublicMarketEquivalent(PME)BoththeIRRandTVPImeasuresareabsolute

performancemeasures.Toevaluateperformancerelativetothemarket,thepublic

marketequivalent(PME)isused.Itiscalculatedastheratioofthediscountedvalue

oftheLP’sinflowsdividedbythediscountedvalueofoutflows,withthediscounting

performedusingrealizedmarketreturns,

∑∏ 1

∑∏ 1

.

KaplanandSchoar(2005)arguethatwhenPEinvestmentshavethesameriskas

thegeneralmarket(abetaequaltoone),aPMEgreaterthanoneisequivalenttoa

positiveeconomicreturnfortheLPs.Thisinterpretationmaybemisleadingwhen

theriskofdistributions(thenumeratorinthePME)isgreaterthantheriskof

capitalcalls(includingmanagementfees,whicharelargelyarisk‐freeliability).

Usingalowerdiscountrateforcapitalcallswouldinflatethedenominatorand

reducethePME.Hence,morecarefullyaccountingfordifferentriskswouldsuggest

thatthePMEmayhavetoexceedonebysomemarginbeforeLPsearnapositive

economicreturn.6

KaplanandSchoar(2005)findaverageequal‐weightedPMEsof0.96.Value‐

weighted,thePMEforVCis1.21andthePMEforBOis0.93.Phalippouand

Gottschalg(2009)usedatafor852fundstocalculateaPMEof1.01(theycallthis

measuretheprofitabilityindexorPI).Thefiguredecreasesto0.88aftervarious

adjustments.

6Additionally,asatechnicalpoint,theCAPMmodelprescribesthatthediscountingshouldbeperformedusingexpectedreturns,notrealizedreturnsasinthePME.Usingtherealizedreturnsdistortsthecalculation(accordingtoJensen'sinequality).

18

Comparingdifferentstudiesanddatasources,Harris,JenkinsonandKaplan(2011)

reportweightedaveragePMEsof1.16‐1.27forBOfunds,and1.02‐1.45forVC

funds.PMEsforBOhavevariedfrom1.03‐1.11inthe1980s,to1.17‐1.34inthe

1990s,and1.25‐1.29inthe2000s.ForVC,thereportedPMEsare0.90‐1.08inthe

1980s,to1.99‐2.12inthe1990s,and0.84‐0.95inthe2000s.The1990swastheVC

decade,andthe2000shasbeentheBOdecade.

RiskMeasuresFund‐leveldataarepoorlysuitedforestimatingtheriskofPE

investing.Few,ifany,academicstudiesattempttousefund‐leveldatatodoso.

Instead,LjungqvistandRichardson(2003)estimateriskbyassigningeachportfolio

companytooneof48broadindustrygroupsandusethecorrespondingaverage

betaforpubliclytradedcompaniesinthesameindustry.Theyreportthatthe

correspondingbetaforpubliclytradedcompaniesis1.08forBOand1.12forVC

investments.NotethatthesebetasdonotadjustforthehigherleverageusedinBO

investmentsrelativetoVCinvestments.Assigningbetas,theyfinda5‐6%premium,

whichtheyinterpretastheilliquiditypremiumofVCinvestments.

KaplanandSchoarstatethatthey“believeitispossiblethatthesystematicriskof

LBOfundsexceeds1becausethesefundsinvestinhighlyleveredcompanies.”They

regressIRRsonS&P/500returns,andfindacoefficientof1.23forVCfundsand

0.41forBOfunds.Aleveredbetaof0.41seemsunreasonablylow.

PersistenceandPredictabilityKaplanandSchoar(2005),Phalippouand

Gottschlag(2009),Hochberg,Ljungqvist,andVissing‐Jorgensen(2010),alongwith

otherstudiesfindevidenceofperformancepersistenceforPEfunds.The

performanceofanearlyfundpredictstheperformanceofsubsequentfunds

managedbythesameGP.ThispersistenceisinterpretedasevidencethatGPsvary

intheirskillsandabilitiestopickinvestmentsandmanagetheportfoliocompanies.

Estimatessuggestthataperformanceincreaseof1.0%forafundisassociatedwith

around0.5%greaterperformancefortheGP’snextfund,measuredeitherinterms

ofPMEorIRR.Formoredistantfunds,persistencedeclines.

19

Duetodatalimitations,studiesthatdocumentpredictabilityinPEreturnsconduct

statisticalanalysisonin‐samplebasis,ratherthanonanout‐of‐samplebasis.In

KaplanandSchoar,forexample,PEfundsinthe“topquartile”dowell,butthese

fundsareidentifiedexpost.Withinafundfamily,fundsoftenhavelifetimesof10

yearsbutoverlaptosomeextent.In‐sampleanalysisusestheultimateperformance

ofapreviousfundtopredicttheperformanceofasubsequentfund,evenifthis

subsequentfundisraisedbeforetheultimateperformanceofthepreviousfundsis

fullyrealized.Thestudiesemployvariousrobustnesschecks,suchasusing

intermediateNAVsinsteadofultimateperformanceorusingtheperformanceof

fundsseveralgenerationsagotopredictfutureperformancetomitigatethis

concern.Still,somerecentresearch,suchasHochberg,LjungvistandVissing‐

Jorgensen(2010)findweakerevidenceofpersistenceusingonlyinformation

availablewhenthenewfundisraised.

IID.SummaryofEmpiricalEvidence

Basedontheexistingevidencefromstudiesusingfund‐leveldata,itseemsearlyfor

apreciseassessmentofhowtheriskofPEinvestingcomparestotheriskof

investinginpubliclytradedequitiesevenintermsofthesemostbasicmetrics.

MeasuringPEriskandreturnsisdifficultbecauseoftheinfrequentobservationsof

fundorcompanyvaluesandselectionbias.Studiesusingcompany‐leveldatathat

accountforselectionbiasfindhighalphasforPEinvestmentsonlyduringthelate

1990s,butnegativealphaspost‐2000.Thepositivealphaestimatesarehardto

interpretintermsofarithmeticreturns,however,becauseoftheveryhighvolatility.

Estimatesofbetasvarysubstantially,rangingashighas3.6forVCinvestments,but

generallyPEbetasarewellaboveone.Studiesusingfund‐leveldatahavefewer

selectionproblems,butstillsufferfromthefactthatnodirectPEreturnsare

observed.Unlikestandardreturnmeasures,fund‐levelIRRs,TVPI,andPME

measurescanbemisleadingandshouldbeinterpretedwithcautiontoinferPE

performance.Intermsofrawperformance,inthewordsofHarris,Jenkinson,and

Kaplan(2011)"itseemslikelythatbuyoutfundshaveoutperformedpublicmarkets

20

inthe1980s,1990s,and2000s."However,duetotheuncertaintyabouttheriskof

privateequityinvestments,itisnotyetpossibletosaywhetherthisoutperformance

issufficienttocompensateinvestorsfortheriskoftheseinvestmentsandwhether

theinvestmentsoutperformonarisk‐adjustedbasis.Finally,thereisevidenceof

persistenceofPEfundreturnsandsome,albeitweakerandlessconsistent,evidence

thatcharacteristicslikefundsizeandpastcapitalraisingspredictPEfundreturns.

III.AssetAllocationstoPrivateEquity

HavingdiscussedthemeasurementofPEreturns,wenowconsideroptimal

allocationstoPE.Thisrequires,ofcourse,asuitablerisk‐returntrade‐offforPE

investmentsaswellascorrelationsofPEreturnswithotherassetsintheinvestor’s

opportunityset.AsSectionIIpointsout,measuringtheseinputsforPEforuseinan

optimizationproblemrequiresspecialconsiderations.Wenowtakeasgiventhese

inputsandfocusonthedimensionofilliquidityriskofPEandhowtoincorporate

illiquidityPEriskintoanoptimalassetallocationframework.Therehavebeen

severalapproachestohandlingilliquidityriskinassetallocation,allofwhichhave

relevanceindealingwithPEallocation.Toputintocontextthesecontributions,we

startwiththecaseofassetallocationwithoutfrictions.

IIIA.FrictionlessAssetAllocation

TheseminalcontributionsofMerton(1969,1971)characterizetheoptimalasset

allocationofaninvestorwithConstantRelativeRiskAversion(CRRA)utility

investinginarisk‐freeasset(withconstantrisk‐freerate)andasetofriskyassets.

TheCRRAutilityfunctionwithriskaversionisgivenby

1

( ) .1

WU W

21

CRRAutilityishomogeneousofdegreeone,whichmeansthatexactlythesame

portfolioweightsarisewhether$10millionofwealthisbeingmanagedor$1billion.

Thismakestheutilityfunctionidealforinstitutionalassetmanagement.

Assumetheriskyassetsarejointlylog‐normallydistributed.Underthecaseofiid

returns,thevectorofoptimalholdings,w,oftheriskyassetsaregivenby

whereisthecovariancematrixoftheriskyassetreturns,isthevectorof

expectedreturnsoftheriskyassets,andrfistherisk‐freerate.Thisisalsothe

portfolioheldbyaninvestorwithmean‐varianceutilityoptimizingoveradiscrete,

one‐periodhorizon.

Therearetwokeyfeaturesofthissolutionthatbearfurthercomment.First,the

Mertonsolutionisadynamicsolutionthatinvolvescontinuousrebalancing.Thatis,

althoughtheportfolioweights,w,areconstant,theinvestor’spolicyisalwaysto

continuouslysellassetsthathaveriseninvalueandtobuyassetsthathavefallenin

valueinsuchawayastomaintainconstantweights.Clearly,thediscretenatureof

PEinvestmentandtheinabilitytotradeitfrequentlymeanthatallocationstoPE

shouldnotbedonewiththestandardMertonmodel.

Second,thecostofemployinganon‐optimalstrategy,forexample,notholdinga

particularassetwhichshouldbeheldinanoptimalportfolio,canbecomparedto

theoptimalstrategyandthecostofholdingthenon‐optimalportfoliodependson

theinvestor’sriskaversion.Thatis,thecostofbearingnon‐optimalweightsis

dependentontheinvestor’sriskpreferences.Thecostsarecomputedusingutility

certaintyequivalents:thecertaintyequivalentcostishowmuchaninvestormustbe

compensatedindollarsperinitialwealthtotakeanon‐optimalstrategybuthave

thesameutilityastheoptimalstrategy.Arelevantcost,whichthesubsequent

literatureexplores,ishowmuchaninvestorshouldbecompensatedfortheinability

11( ),fw r

22

totradeassetslikePEforcertainperiodsoftimeortobecompensatedforbeing

forcedtopayacostwheneveranassetistraded.

IIIB.AssetAllocationwithTransactionsCosts

InvestinginPEincurslargetransactionscostsininitiallyfindinganappropriatePE

managerandconductingappropriateduediligence.Then,therearepotentially

largediscountstotherecordedassetvaluesthatmaybetakenintransferring

ownershipofaPEstakeinilliquidsecondarymarkets.SinceConstantinides(1986),

alargeliteraturehasextendedtheMertonsetuptoincorporatetransactionscosts.

Constantinidesconsidersthecaseofonerisk‐freeandoneriskyasset.Whenthere

areproportionaltransactionscosts,sothatwhenevertheholdingsoftheriskyasset

increase(ordecrease)byv,theholdingoftherisklessassetdecreasesby(1+k)v.

Whentherearetradingcosts,theinvestornowtradesinfrequently.Constantinides

showsthattheoptimaltradingstrategyistotradewhenevertheriskyassetposition

hitsupperandlowerbounds, and ,respectively.Theseboundsstraddlethe

optimalMertonsolutionwheretherearenofrictions.Theholdingsofriskytorisk‐

freeassets,y/x,satisfy

sothatwheny/xlieswithintheinterval thereisnotradeandwheny/xhits

theboundariesoneitherside,theinvestorbuysandsellsappropriateamountsof

theriskyassettobringtheportfoliobacktotheMertonsolution.

Theno‐tradeinterval, ,increaseswiththetransactionscosts,k,andthe

volatilityoftheriskyasset.TransactionscoststosellPEportfoliosinsecondary

marketscanbeextremelysteep.WhenHarvardendowmenttriedtosellitsPE

investmentsin2008,potentialbuyerswererequiringdiscountstobookvalueof

w w

,y

w wx

[ , ]w w

w w

23

morethan50%.7Evenfortransactionscostsof10%,Constantinidescomputesno‐

tradeintervalsgreaterthan0.25aroundanoptimalholdingof0.26forariskyasset

withavolatilityof35%perannum.Thus,PEinvestorsshouldexpecttorebalance

PEholdingsveryinfrequently.

Thecertaintyequivalentcosttoholdingariskyassetwithlargetransactionscostsis

smallformodesttransactionscosts,atapproximately0.2%forproportional

transactionscostsof1%,butcanbesubstantialforlargetransactionscosts—which

isthemorerelevantrangeoftransactionscostsforPEinvestments.For

transactionscostsof15%ormore,therequiredpremiumtobringtheinvestorto

thesamelevelofutilityasthefrictionlessMertoncaseismorethan5%perannum.

Theliteraturehasextendedthisframeworktomultipleassets(see,forexample,Liu

(2004))anddifferenttypesofrebalancingbands.Leland(1996)andDonohueand

Yip(2003)suggestrebalancingtotheedgeofabandratherthantoatargetwithina

band.Others,likePliskaandSuzuki(2004)andBrown,Ozik,andScholtz(2007)

advocateextensionstotwosetsofbands,wheredifferentformsoftradingaredone

attheinnerbandwithmoredrasticrebalancingdoneattheouterband.Inallthese

extensions,theintuitionisthesame:PEinvestmentsshouldbeexpectedtobe

rebalancedveryinfrequently,andtherebalancingbandswillbeverywide.Thecase

oftransactionscostswhenreturnsarepredictableisconsideredbyGarleanuand

Pedersen(2010).ArelatedstudyisLongstaff(2001),whoallowsinvestorstotrade

continuously,butonlywithboundedvariationsothereareupperandlowerbounds

onthenumberofshareswhichcanbetradedeveryperiod.ThismakesLongstaff’s

modelsimilartoatime‐varyingtransactionscost.

Amajorshortcomingofthisliteratureisthatitassumesthattradeinassetsis

alwayspossible,albeitatacost.ThisisnottrueforPE—overashorthorizon,there

maybenoopportunitytofindabuyerandevenifabuyerisfound,thereisnot

enoughtime,relativetotheinvestor’sdesiredshorthorizontoraisecapital,togo

7See“LiquidatingHarvard”ColumbiaCaseWorksID#100312,2010.

24

throughlegalandaccountingprocedurestotransferownership.Animportant

frictionforPEinvestorsinsecondarymarketsisthesearchprocessinfindingan

appropriatebuyer.Theremaybenoopportunitytotrade,evenifdesired,at

considerablediscounts.Thiscaseiswhatthenextliteratureconsiders.

IIIC.AssetAllocationwithSearchFrictions

AsPEinvestmentsdonottradeonacentralizedexchange,animportantpartof

rebalancingaPEportfolioisfindingacounterpartyinover‐the‐countermarkets.

Or,ifmoneyisspunofffromexistingPEinvestments,neworexistingPEfundsmust

befoundtoinvestin.Thisentailsasearchprocess,incurringopportunityandsearch

costs,aswellasabargainingprocess,whichreflectsinvestors’needsforimmediate

trade.Thelatteriscapturedbyatransactionscost,asmodeledintheprevious

section.Theformerrequiresatradingprocessthatcapturesthediscretenatureof

tradingopportunities.

SinceDiamond(1982),search‐basedfrictionshavebeenmodeledbyPoissonarrival

processes.Agentsfindcounterpartieswithanintensity,andconditionalonthe

arrivalofthePoissonprocess,agentscantradeandrebalance.Thisproduces

intervalswherenorebalancingispossibleforilliquidassetsandthetimeswhen

rebalancingarepossiblearestochastic.Thisnotionofilliquidityisthatthereare

timeswhereitisnotpossibletotrade,atanyprice,anilliquidasset.These

particulartypesofstochasticrebalancingopportunitiesareattractiveformodeling

PEinanotherway:theexitinPEvehiclesisoftenuncertain.AlthoughaPEvehicle

mayhaveastatedhorizon,sayof10years,thereturnofcashfromtheunderlying

dealsmaycauselargeamountsofcapitaltobereturnedbeforethestatedhorizon,

orinmanycasesthehorizonisextendedtomaximizeprofitabilityoftheunderlying

investments(ortomaximizethecollectionoffeesbyGPs).

Anumberofauthorshaveusedthissearchtechnologytoconsidertheimpactof

illiquidity(search)frictionsinvariousover‐the‐countermarkets,suchasDuffie,

GarleanuandPedersen(2005,2007).Whiletheseareimportantadvancesfor

25

showingtheeffectofilliquidityriskonassetprices,theyarelessusefulforderiving

assetallocationadviceonoptimalPEholdings.Duffie,GarleanuandPedersen

(2005,2007)consideronlyrisk‐neutralandCARAutilitycasesandrestrictasset

holdingstobe0or1.Garleanu(2009)andLagosandRocheteau(2009)allowfor

unrestrictedportfoliochoice,butGarleanuconsidersonlyCARAutilityandLagos

andRocheteaufocusonshowingtheexistenceofequilibriumwithsearchfrictions

ratherthanonanypracticalcalibrations.Neitherstudyconsidersassetallocation

withbothliquidandilliquidassets.

IIID.AssetAllocationwithStochasticNon‐TradedPeriods

Ang,Papanikolaou,andWesterfield(2011)[APW]solveanassetallocationproblem

withliquidsecurities,correspondingtotradedequitymarketswhichcanbetraded

atanytime,andilliquidsecurities,whichcanbeinterpretedasaPEportfolio.The

investorhasCRRAutilitywithaninfinitehorizonandcanonlytradetheilliquid

securitywhenaliquidityeventoccurs,whichisthearrivalofaPoissonprocesswith

intensity.Inthisframework,thespecialcaseofMertonwithcontinuous

rebalancingisgivenby .Asdecreasestozero,theopportunitiesto

rebalancetheilliquidassetbecomemoreandmoreinfrequent.Themeantime

betweenrebalancingopportunitiesis1/.Thus,indexesarangeofilliquidity

outcomes.

Theinabilitytotradeforstochasticperiodsintroducesanewsourceofriskthatthe

investorcannothedge.Thisilliquidityriskinduceslargeeffectsonoptimal

allocationrelativetotheMertoncase.APWshowthatilliquidityriskaffectsthemix

ofliquidandilliquidsecuritiesevenwhentheliquidandilliquidreturnsare

uncorrelatedandtheinvestorhaslogutility.

ThemostimportantresultthatAPWderiveisthatthepresenceofilliquidityrisk

inducestime‐varying,endogenousriskaversion.Theintuitionisthattherearetwo

levelsofwealththatarerelevantfortheinvestor:totalwealth,whichisthesame

effectasthestandardMertonproblemwheretheriskisthatiftotalwealthgoesto

26

zerotheagentcannotconsume,andliquidwealth.Theagentcanonlyconsumeout

ofliquidwealth.Thus,withilliquidandliquidassets,theinvestoralsocaresabout

theriskofliquidwealthgoingtozero.Thiscanbeinterpretedasasolvency

condition:anagentcouldbewealthybutifthiswealthistiedupallinilliquidassets,

theagentcannotconsume.AlthoughtheCRRAagenthasconstantrelativerisk

aversion,theeffectiveriskaversion—thelocalcurvatureofhowtheagenttradesoff

liquidandilliquidriskinherportfolio—isaffectedbythesolvencyratiooftheratio

ofliquidtoilliquidwealth.Thissolvencyratioalsobecomesastatevariablethat

determinesoptimalassetallocationandconsumption.Thisilliquidityriskcauses

theoptimalholdingsofeventheliquidassettobelowerthantheoptimalholdingof

liquidassetsinapureMertonsetting.

APWderivefivefindingsthatareimportantconsiderationsforinvestinginPE:

1. Illiquidityriskinducesmarkedreductionsintheoptimalholdingsofassets

comparedtotheMertoncase.UnderAPW’scalibrationsforthesamerisk

aversionasa60%riskyassetholding(and40%risk‐freeholding)inthe

Mertoncase,introducinganaveragerebalancingperiodofonceayear

reducestheriskyassetholdingto37%.Whentheaveragerebalancing

periodisonceeveryfiveyears,theoptimalallocationisjust11%.Thus,PE,

whichishighlyilliquid,shouldbeheldinmodestamountsininvestors’

portfolios.

2. Inthepresenceofinfrequenttrading,thefractionofwealthheldinthe

illiquidassetcanvarysubstantiallyandisveryrightskewed.Thatis,

supposetheoptimalholdingtoilliquidassetsis0.2whenrebalancingcan

takeplace.Thentheinvestorshouldexpecttherangeofilliquidholdingsto

varyfrom0.15to0.35duringnon‐rebalancingtimes.Becauseoftheskew,

theaverageholdingstotheilliquidassetwillbehigherthantheoptimal

rebalancingpoint,atsay0.25.Thus,whenanilliquidPEportfoliois

27

rebalanced,theoptimalrebalancingpointistoaholdingmuchlowerthan

theaverageholding.

3. Theconsumptionpolicy(orpayoutpolicy)withilliquidassetsmustbelower

thantheMertonpayoutpolicywithonlyliquidassets.Intuitively,holding

illiquidassetsmeansthatthereisadditionalsolvencyriskthatliquidwealth

goestozeroandconsumptioncannotbefunded.Thus,payoutsoffunds

holdingilliquidassetsshouldbelowerthanthecasewhentheseassetsallare

fullytraded.Asthefractionofilliquidassetsintheportfolioincreases,

consumptionasafractionoftotalwealthdecreases.

4. Thepresenceofilliquidityriskmeansthataninvestorwillnotfullytake

advantageofopportunitiesthatmightlooklikeclosetoan“arbitrage”,for

example,wherecorrelationstotheliquidandilliquidreturnsarenearlyplus

orminusone.Traditionalmean‐varianceoptimizerswithoutconstraints

wouldproduceweightsclosetoplusorminusinfinityinthesetwoassets.

Thisdoesnothappenwhenoneassetisilliquidbecausetakingadvantageof

thisapparentarbitrageinvolvesastrategythatcausestheinvestor’sliquid

wealthtodroptozerowithpositiveprobability.Thus,near‐arbitrage

conditionswhenthereisilliquidityriskarenotexploitedliketheMerton

setting.

5. Finally,thecertaintyequivalentrewardrequiredforbearingilliquidityriskis

large.APWreportthatwhentheliquidandilliquidreturnsarelowly

correlatedandtheilliquidportfoliocanberebalanced,onaverage,once

everyfiveyears(whichisatypicalturnoverofmanyPEportfolios),the

liquiditypremiumisover4%.Forrebalancingonceayear,onaverage,the

illiquiditypremiumisapproximately1%.Thesenumberscanbeusedas

hurdleratesforinvestorsconsideringinvestinginPE.

AnumberofauthorsincludingDai,Li,andLiu(2008),Longstaff(2009),DeRoon,

Guo,andTerHorst(2009),andAngandBollen(2010)alsoconsiderassetallocation

28

wheretheilliquidassetcannotbetradedovercertainperiods.However,inthese

studies,theperiodofnon‐tradingisdeterministic.Incontrast,theAPWframework

hasstochasticandrecurringperiodsofilliquidity.Deterministicnon‐trading

periodsareprobablymoreappropriateforhedgefundinvestmentswherelock‐ups

haveknownexpirations.PEinvestingismoreopenendedandhasrandom,and

infrequent,opportunitiestorebalance.

APWstillmissanumberofpracticalconsiderationsthatthefutureliteratureshould

address.ThemostimportantoneisthatintheMertonsettingintowhichAPW

introduceilliquidity,therearenocashdistributions;allriskyassetreturns(both

liquidandilliquid)arecapitalgains.PEinvestmentsrequirecashflowmanagement

ofcapitalcallsanddistributions.Somead‐hocsimulationshavebeenconductedby

someindustryanalystsonthisissue,likeSiegel(2008)andLeibowitzandBova

(2009),butwithoutexplicitlysolvingoptimalportfolioswithilliquidityrisk.An

extensionofAPWtoincorporatecashflowstreamscouldaddressthis.

IIIE.Summary

TheinabilitytocontinuouslyrebalancePEpositions,potentiallyevenbypaying

transactionscosts,makesoptimalholdingsofilliquidPEinvestmentsverydifferent

fromthestandardMertonframeworkwhichassumesnoilliquidityrisk.Since

transactionscostsinrebalancingPEportfoliosareverylarge,inbothenteringnew

PEpositionsandsellingexistingPEpositions,PEpositionsshouldbeexpectedtobe

rebalancedveryinfrequentlyandinvestorsshouldsetverywiderebalancingbands.

InassetallocationmodelswhereilliquidassetslikePEcanonlybetradeduponthe

arrivalofa(stochasticallyoccurring)liquidityevent,illiquidityriskmarkedly

reducestheholdingsofilliquidassetscomparedtothestandardMertonmodel.For

example,anassetwhichcouldbetradedcontinuouslyintheMertonsettingthatis

heldwitha60%optimalweightwouldhaveanoptimalholdingoflessthan10%ifit

couldberebalancedonlyonceeverytenyears,onaverage.Thecertaintyequivalent

reward,orequivalentlythehurdlerate,forbearingilliquidityriskislarge.Fora

29

typicalPEinvestmentthatcanbetradedonlyonceintenyears,onaverage,the

illiquiditypremiumiswellabove4%.

IV.IntermediaryIssuesinPrivateEquity

Mostcommonly,assetownersmakePEinvestmentsasanLPinafundwhere

investmentdecisionsaremadebyfundmanagersactingasGPs.Thisarrangement

raisespotentialagencyissues.OnecharacteristicofPEinvestmentisthatthe

investmentdecisionsarisingfromsuchmanagementconsiderationsandtherelated

agencyissuesbecomeintrinsicallyintertwinedwithPEperformance.Inpublic

equitymarkets,factorreturnsandactivemanagementcanbeseparatedduetothe

existenceofinvestableindexstrategies.

IVA.AgencyIssues

WhiletheagencyproblemiscentralforPEinvestments,thereisonlyasmall

literatureonoptimaldelegatedportfoliomanagement(seethegoodsurveysbythe

BIS(2003)andStracca(2006)).Thereis,however,alargeliteratureonagency

issuesinstandardcorporatefinancesettings(see,forexample,thetextbookby

Salanie(1997)andBoltonandDewatripont(2005)).Delegatedportfolio

managementisdifferentfromstandardagencyproblemsbecausethe“action”

chosenisgenerallyobserved(theinvestmentsmadebytheGP),butthesetof

actionsisunknown(thefullsetofdealsavailabletotheGP).Incontrast,instandard

moralhazardproblemsthe“action”isunobservable,butthesetofpotentialactions

isusuallyknown.8Thus,littleisknownabouttheoptimaldelegatedportfolio

contract,andtheliteraturehasfew,ifany,specificconclusionsorprescriptions

aboutwhatformtheoptimalPEcontractbetweenLPsandGPsshouldtake.

8Thereareotherreasonsthatmakethedelegatedoptimalportfoliomanagementproblemchallenging.Theagent(fundmanager)cancontrolboththemean,whichistheresponsetothesignalbybuyingagoodstock,andalsothevariance,throughleverage.Inatypicalagencyproblemtheagentcontrolsonlythemean(occasionallythevariance),butnotboth.Incontinuoustime,whichisoftenusedtosolveagencyproblems,diffusiondynamicsareeffectivelyobservableathighenoughfrequencies.

30

PEinvestingisfurthercomplicatedbyhavingtwolevelsofprincipal‐agentrelations

ratherthanjustasingleone:alevelbetweentheLPs(principal)andGPs(agent)

andanotherlevelbetweentheGPsasfundmanagers(principal)anditsunderlying

portfolioofcompanies(agent).Bothlevelsrelyonstrongdirectmonetary

incentives.Apartfromthesemonetaryincentives,however,therelationbetween

LPsandGPsisonewithlimitedinformation,poormonitoring,rigidfeestructures,

andtheinabilitytowithdrawcapital,ordirectlycontrolmanagers.Ononehand,

thesefeaturestendtoheightentensionsbetweentheLPsandGPsandexacerbate,

ratherthanalleviate,agencyissues.Ontheotherhand,thedistancebetweentheLP

andGPmayallowGPstoinvestandmanagecompaniesmorefreely.

Theotherprincipal‐agentrelationbetweenthefundanditsportfoliocompaniesis

onewithstronggovernance,transparentinformationflows,goodincentivesfor

monitoring,andahighalignmentofinterestsbetweenownersandmanagement

(seeJensen(1989)).ThereisstrongevidencethatPEfundsaddsignificantvalue,on

average,tothecompaniesintheirportfolio.ThisliteratureissurveyedbyKaplan

andStromberg(2009).

Theinteractionsbetweenthesetwolayersofprincipal‐agentproblemshavenot

beenfullyexplored.Itisnotinconceivable,though,thatmitigatingtheprincipal‐

agentproblemsattheLP‐GPlevelwouldcomeatthecostofincreasingtheproblems

atthefund‐companylevel.Forexample,greatertransparencyaboutthe

managementofindividualportfoliocompaniesmayinturnleadGPstomanage

thesecompanieswithaneyetowardsmanagingshort‐termearningsexpectations

andsatisfyingpublicexpectationsmorebroadly,aconcernforpubliclytraded

companies,ratherthansimplymanagingcompaniestomaximizetheirtotalvalue.

IVB.PrivateEquityContracts

BecausePEis,byitsnature,private,itisdifficulttoperformsystematiclarge‐sample

studiesofcontractualfeaturesandseehowtheyrelatetoperformance.Gompers

31

andLerner(1999),Litvak(2009),andMetrickandYasuda(2010)examinesmall

samplesofvariousPEcontracts.Severaltentativeconclusionsemerge:

1. PEcontractsarelargelystandardized.Anoften‐quotedfeearrangementisa

managementfeeof2%andacarryof20%.Thereissomevariationinthe

numbers(e.g.,managementfeestendtovarybetween1‐2.5%andcarried

interestvariesbetween20‐35%),butthegeneralstructureiswidelyused.

Additionally,asubstantialpartoftheGPscompensationmaybeintheform

oftransactionfees.PEfeesarehigh.

2. Thereissomevariationinthespecificprovisionsgoverningthecalculation

andtimingofthefeesandcarriedinterest.Forexample,amanagementfee

couldbeflat(oncommittedcapital),decliningoverthelifeofthefund,a

(time‐varyingbutdeterministic)combinationofcommittedandmanaged

capital,orevenanabsoluteamount.

3. Fixedfeeandperformancecomponentsarenotsubstitutesbutcomplements.

Thatis,fundstendtoraiseboththefixedfeeandvariablefeecomponents

(andtheothercompensationcomponents)together.Fundsizetendstobe

positivelycorrelatedwithfees,andKaplanandSchoar(2005),alongwith

othersfindthatsizeisnegativelycorrelatedwithperformance.More

recently,however,RobinsonandSensoy(2011a)investigateanextended

samplewithcontracttermsandperformance,andfindnorelationbetween

net‐of‐feeperformanceandthesizeofthefundorthefees.

4. ThereisadebateabouttheperformancesensitivityofPEcompensation.

MetrickandYasuda(2010)findthatclosetoone‐halfthepresentvalueofGP

compensationarefrommanagementfeesratherthancarriedinterestand

findthistobetrueforbothVCandBOfunds.However,Chungetal.(2011)

pointoutthatasubstantialamountofGPs'performancepayarisesthrough

thecontinuationvalueofraisingfuturefunds,whicharehighlysensitiveto

currentperformance.

5. PEcontractsarecomplexdocuments.Litvak(2009),however,findslittle

relationbetweenopaquenessandtotalcompensation.

32

ThemanagementfeeschargedbyprivateequityandVCfundsarehigh.Accordingto

MetrickandYasuda(2010)suchfeesconsumeatleastone‐fifthofgrossPEreturns.

MetrickandYasudafoundthatoutofevery$100investedwithaVCfund,an

averageof$23ispaidtotheGPsintheformofcarryandmanagementfees.ForBOs,

themeanofthecarryandmanagementfeescomesto$18per$100.

ThehighfeeschargedbyGPspointtothefactthatifaninstitutionalinvestor

wishingtoallocatetoPEcandothisin‐house,thentherearesubstantialsavings

available.Ofcourse,attractingtalentandrunninganin‐housePEshoppresentsa

differentsetofagencyissuesthanout‐sourcingtoPEfundswithGPs.Despitethe

pessimisticviewofreturnsofPEinvestmentstoLPsinSectionII,thehighPEfees

impliesthatifassetownerscancomeclosetocapturinggrossreturns,PEbecomes

muchmoreattractive.

Whileopacitypersedoesnotseemtoberelatedtototalcompensationandreturns,

opacityhasotherimportantknock‐oneffectsforotheraspectsofanassetowner’s

largerportfolio.Complexityandnon‐transparencycanincreaseagencyproblems

andmakeriskmanagementmoredifficult.TheleverageinvolvedinmanyBOfunds

canbemoreexpensive,andisoftenhardertomonitor,thanleveragedonedirectly

bytheassetowner.

IVC.Summary

AgencyissuesarefirstorderproblemsinPEinvestments,unlikeinvestmentsin

publicequity.Indeed,thereisnowaytoseparateactivemanagementfrompassive

managementinPEinvestment.Whilethereislittleliteratureonwhatcontractual

designisoptimalinPEinvestments,existingPEcontractstypicallyassigna

managementfeeof2%andcarryof20%.Thesetranslateintoveryhighfeeswhich

represent20‐25%ofgrossPEreturnsforinvestorspointingtotremendoussavings

forinstitutionalinvestorsifPEinvestmentcanbedoneinhouseassumingthereis

nolossinreturnquality.

33

V.Conclusion

Relativelylittleisknownaboutriskandreturns,assetallocation,andoptimal

contractingforprivateequity(PE)investmentsincontrasttoinvestmentsinlisted,

publicequitymarkets.TheirregularnatureandlimiteddataofPEinvestments

complicatetheestimationandinterpretationofstandardriskandreturnmeasures;

naïvemeasureoverstatePEreturnsandunderstateriskandcommonlyreported

measures(IRR<TVPImultiple,andPME)needtobeinterpretedwithcaution.

Modelsofassetallocationthattakeintoaccounttransactionscostsandilliquidity

risksuggestholdingsofPEshouldbesmallerthantraditionallistedpublicequity.

WhileincentivefeesinPEaddressmoralhazardandinformationagencyproblems,

totalfeesinPEinvestmentsareverylargeandincentivefeesaccountforaminority

oftotalcompensation.

34

Bibliography

Ang,A.,andN.Bollen,2010,LockedUpbyaLockup:ValuingLiquidityasaRealOption,FinancialManagement,39,1069‐1095.

Ang,A.,andD.Kristensen,2012,TestingConditionalFactorModels,forthcomingJournalofFinancialEconomics.

Ang,A.,D.Papanikolaou,andM.Westerfield,2011,PortfolioChoicewithIlliquidAsset,workingpaper,ColumbiaUniversity.

BankofInternationalSettlements,2003,IncentiveStructuresinInstitutionalAssetManagementandTheirImplicationsforFinancialMarkets,BISReport.

Bolton,P,andM.Dewatripont,2005,ContractTheory,MITPress,Boston,MA.

Brown,D.T.,G.Ozik,andD.Scholz,2007,RebalancingRevisited:TheRoleofDerivatives,FinancialAnalystsJournal,September,32‐44.

Bygrave,W.,andJ.Timmons,1992,VentureCapitalattheCrossroads,HarvardBusinessSchoolPress,Boston.

Campbell,J.Y.,A.W.Lo,andA.C.MacKinlay,1997,TheEconomicsofFinancialMarkets,PrincetonUniversityPress,Princeton,NJ.

Chung,J.‐W.,B.A.Sensoy,L.H.Stern,andM.Weisbach,2011,PayforPerformancefromFutureFundflows:TheCaseofPrivateEquity,forthcomingReviewofFinancialStudies.

Cochrane,J.,2005,TheRiskandReturnofVentureCapital,JournalofFinancialEconomics,75,3‐52.

Constantinides,G.M.,1986,CapitalMarketEquilibriumwithTransactionCosts,JournalofPoliticalEconomy,94,842‐62.

Dai,M.,P.Li,andH.Liu,2008,MarketClosure,PortfolioSelection,andLiquidityPremia,workingpaper,WashingtonUniversityinSt.Louis.

DeRoon,F.,J.GuoandJ.TerHorst,2009,BeingLockedUpHurts,workingpaper,TilburgUniversity.

Diamond,P.A.,1992,AggregateDemandinSearchEquilibrium,JournalofPoliticalEconomy,90,891‐894.

35

Donohue,C.,andK.Yip,2003,OptimalPortfolioRebalancingwithTransactionsCosts,JournalofPortfolioManagement,Summer,49‐63.

Driessen,J.,T.‐C.Lin,andL.Phalippou,2011,ANewMethodtoEstimateRiskandReturnofNon‐TradedAssetsfromCashFlows:TheCaseofPrivateEquityFunds,forthcomingJournalofFinancialandQuantitativeAnalysis.

Duffie,D.,N.Garleanu,andL.H.Pedersen,2005,Over‐the‐CounterMarkets,Econometrica,73,1815‐1847.

Duffie,D.,N.Garleanu,andL.H.Pedersen,2007,ValuationinOver‐the‐CounterMarkets,ReviewofFinancialStudies,20,1865‐1900.

Faccio,M.,M.‐T.Marchica,J.J.McConnell,andR.Mura,2012,ReturnsandRiskstoPrivateEquity,workingpaper,PurdueUniversity.

Franzoni,F.,E.Nowak,andL.Phalippou,2012,PrivateEquityPerformanceandLiquidityRisk,forthcomingJournalofFinance.

Garleanu,N.,2009,PricingandPortfolioChoiceinIlliquidMarkets,JournalofEconomicTheory,144,532‐564

Gompers,P.andJ.Lerner,1997,RiskandRewardinPrivateEquityInvestments:TheChallengeofPerformanceAssessment,JournalofPrivateEquity,1,5‐12.

Gompers,P.,andJ.Lerner,1999,AnAnalysisofCompetitionintheU.S.VentureCapitalPartnership,JournalofFinancialEconomics,51,3‐44.

Harris,R.,T.Jenkinson,andS.N.Kaplan,2011,PrivateEquityPerformance:WhatDoWeKnow?workingpaper,UniversityofChicago.

Heckman,J.,1979,SampleSelectionBiasasaSpecificationError,Econometrica,47,153‐62.

Hochberg,Y.,A.Ljungvist,andA.Vissing‐Jorgensen,2010,InformationalHold‐UpandPerformancePersistenceinVentureCapital,workingpaper,NorthwesternUniversity.

Kaplan,S.N.,andAntoinetteSchoar,2005,PrivateEquityPerformance:Returns,Persistence,andCapitalFlows,JournalofFinance,60,1791‐1823.

Kaplan,S.N.,andP.Stromberg,2009,LeverageBuyoutsandPrivateEquity,JournalofEconomicPerspectives,23,121‐46.

Kartashova,K.,2011,ThePrivateEquityPremiumPuzzleRevisited,workingpaper,BankofCanada.

36

Korteweg,A.,andM.Sorensen,2010,RiskandReturnCharacteristicsofVentureCapital‐BackedEntrepreneurialCompanies,ReviewofFinancialStudies,23,3738‐3772.

Lagos,R.,andG.Rocheteau,2009,LiquidityinAssetMarketswithSearchFrictions,Econometrica,77,403‐426.

Leibowitz,M.,andA.Bova,2009,PortfolioLiquidity,MorganStanleyResearch.

Leland,H.E.,1996,OptimalAssetRebalancinginthePresenceofTransactionsCosts,workingpaper,UCBerkeley.

Ljungqvist,A.,andM.Richardson,2003,TheCashFlow,ReturnandRiskCharacteristicsofPrivateEquity,workingpaper,NYU.

Litvak,K.,2009,VentureCapitalPartnershipAgreements:UnderstandingCompensationAgreements,UniversityofChicagoLawReview,76,161‐218.

Liu,H.,2004,OptimalConsumptionandInvestmentwithTransactionCostsandMultipleRiskyAssets,JournalofFinance,54,289‐338.

Lo,A.,W.,H.Mamaysky,andJ.Wang,2004,AssetPricesandTradingVolumeunderfixedTransactionsCosts,JournalofPoliticalEconomy,112,1054‐1090.

Longstaff,F.A.,2001,OptimalPortfolioChoiceandtheValuationofIlliquidSecurities,ReviewofFinancialStudies,14,407‐431.

Longstaff,F.A.,2009,PortfolioClaustrophobia:AssetPricinginMarketswithIlliquidAssets,forthcomingAmericanEconomicReview.

Merton,R.C.,1969,LifetimePortfolioSelectionunderUncertainty:TheContinuousTimeModel,ReviewofEconomicsandStatistics,51,247‐257.

Merton,R.C.,1971,OptimumConsumptionandPortfolioRulesinaContinuousTimeModel,JournalofEconomicTheory,3,373‐413.

Metrick,A.,andA.Yasuda,2010,TheEconomicsofPrivateEquityFunds,ReviewofFinancialStudies,23,2303‐2341.

Metrick,A.andA.Yasuda,2010,VentureCapitalandOtherPrivateEquity:ASurvey,workingpaper,YaleUniversity.

Moskowitz,T.,andA.Vissing‐Jorgensen,2002,TheReturnstoEntrepreneurialInvestment:APrivateEquityPuzzle,AmericanEconomicReview,92,745‐778.

37

Phalippou,L.,2009,BewareWhenVenturingintoPrivateEquity,JournalofEconomicPerspectives,23,147‐166.

Phalippou,L.,2011,AnEvaluationofthePotentialforGPFGtoAchieveAboveAverageReturnsfromInvestmentsinPrivateEquityandRecommendationsRegardingBenchmarking,ReporttotheNorwegianMinistryofFinance.

Phalippou,L.,andO.Gottschalg,2009,ThePerformanceofPrivateEquityFunds,ReviewofFinancialStudies,22,1747‐1776.

Pliska,S.R.,andK.Suzuki,2004,OptimalTrackingforAssetAllocationwithFixedandProportionalTransactionsCosts,QuantitativeFinance,4,233‐43.

Robinson,D.T.,andB.A.Sensoy,2011a,DoPrivateEquityFundManagersEarnTheirFees?Compensation,OwnershipandCashFlowPerformance,workingpaper,DukeUniversity.

Robinson,D.T.,andB.A.Sensoy,2011b,Cyclicality,PerformanceMeasurement,andCashFlowLiquidityinPrivateEquity,workingpaper,DukeUniversity

Salanie,P.,1997,TheEconomicsofContracts:APrimer,MITPress,Boston,MA.

Siegel,L.B.,2008,AlternativesandLiquidity:WillSpendingandCapitalCallsEatYour“Modern”Portfolio,JournalofPortfolioManagement,Fall,103‐114.

Stracca,L.,2006,DelegatedPortfolioManagement:ASurveyoftheTheoreticalLiterature,JournalofEconomicPerspectives,20,823‐848.

Stucke,R.,2011,UpdatingHistory,workingpaper,UniversityofOxford.

Related Documents