P a g e | 1 International Association of Risk and Compliance Professionals (IARCP) 1200 G Street NW Suite 800 Washington, DC 20005-6705 USA Tel: 202-449-9750 w w w .ri s k - co m pl i a nce - a s s o c i a tion . co m Top 10 risk and compliance management related news stories and world events that (for better or for worse) shaped the week's agenda, and what is next Dear Member, “During your working lives, y o u wi l l h a v e to rei n v e n t y o u rse l v es many times. Success and satisfaction will not come from mastering a fix ed body of knowledge but from constant adaptation and creativity in a rapidly changing world.” Who said that? Chairman Ben S. Bernanke, at Bard College at Simon's Rock, Great Barrington, Massachusetts. What else did he say? - The word "graduate" comes from the Latin word for "step." - Another prediction, just as safe, is that p e op l e will ne v er t h el e s s co n t i n u e t o f oreca s t t h e e n d of i n n o v at i o n . A great speech! Read more at Number 1 below. At Number 7 … … I enjoyed another speech: I nternational Association of Risk and Compliance Professionals (I ARCP) ww w.r i sk - co m plia n c e - as socia t i o n .com

Risk management presentation June 3 2013

Oct 30, 2014

International Association of Risk and Compliance Professionals (IARCP)

http://www.risk-compliance-association.com

Every Monday

Top 10 risk and compliance management related news stories and world events

Do you want to receive (at not cost) every Monday the Top 10 risk and compliance management related news stories and world events that (for better or for worse) shaped the week's agenda, and what is next?

You can register at:

http://www.risk-compliance-association.com/Top_10_Risk_Compliance_Management_Stories_Events.html

Receive the New Member Orientation Newsletters

You will have the opportunity to learn (at not cost) what members registered before you have already learned. Understand better risk and compliance management, projects, careers, challenges and opportunities.

You can register at:

http://www.risk-compliance-association.com/New_Member_Orientation_Newsletters.html

http://www.risk-compliance-association.com

Every Monday

Top 10 risk and compliance management related news stories and world events

Do you want to receive (at not cost) every Monday the Top 10 risk and compliance management related news stories and world events that (for better or for worse) shaped the week's agenda, and what is next?

You can register at:

http://www.risk-compliance-association.com/Top_10_Risk_Compliance_Management_Stories_Events.html

Receive the New Member Orientation Newsletters

You will have the opportunity to learn (at not cost) what members registered before you have already learned. Understand better risk and compliance management, projects, careers, challenges and opportunities.

You can register at:

http://www.risk-compliance-association.com/New_Member_Orientation_Newsletters.html

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

P a g e | 1

International Association of Risk and Compliance Professionals (IARCP)

1200 G Street NW Suite 800 Washington, DC 20005-6705 USA Tel: 202-449-9750 www.risk-compliance-assoc

iation.com

Top 10 risk and compliance management related news stories and world events that (for better or for worse)

shaped the week's agenda, and what is next

Dear Member,

“During your working lives, you will have to reinvent yourselves many times.

Success and satisfaction will not come from mastering a fixed body of knowledge but from constant adaptation and creativity in a rapidly changing world.”

Who said that?

Chairman Ben S. Bernanke, at Bard College at Simon's Rock, Great Barrington, Massachusetts.

What else did he say?

- The word "graduate" comes from the Latin word for "step."

- Another prediction, just as safe, is that people will nevertheless continue to forecast the end of innovation.

A great speech! Read more at Number 1 below.

At Number 7 …… I enjoyed another speech:

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 2

“I am very pleased to be here among an audience of professional economists, which is certainly preferable to appearing before an audience of unprofessional economists.”

Who said that?

Sarah Bloom Raskin, Member of the Board of Governors of the Federal Reserve System, at the Society of Government Economists and the National Economists Club, Washington DC.

Well, Sarah … don’t be brutally honest, as professional economists can be as rude as unprofessional economists…

She was brutally honest. She said:

“I like your kind!

Your talents are needed now more than ever as we try to put the tools of the economic profession to work for the common good.

It's easy to be an economist who looks back on crises and crashes and tries to explain why they happened, but much harder to be an economist whose efforts manage to help stop them from happening in the first place.

Economic policymaking, at its best, reflects a continuous struggle to make sure that data and explanations of such data are consistent with real experience.

If we're to engage in this struggle honestly, it's no easy task.

It involves understanding not just the reliability and signal in various data, but also questioning whether the data accords with our understanding of actual experience.

So, to get this right requires many different perspectives, not just on the data but on the underlying realities the data are trying to capture.”

Sara, I like your speech. I agree, to engage in this struggle honestly, it's

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 3

no easy task. I enjoyed you told all these to professional economists. Read more at Number 7 below.Welcome to the Top 10 list.

Best Regards,

George Lekatis President of the IARCPGeneral Manager, Compliance LLC 1200 G Street NW Suite 800, Washington DC 20005, USATel: (202) 449-9750Email: [email protected] Web: www.risk-compliance-association.com HQ: 1220 N. Market Street Suite 804, Wilmington DE 19801, USATel: (302) 342-8828

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 4

Chairman Ben S. BernankeAt Bard College at Simon's Rock, Great Barrington, Massachusetts

Economic Prospects for the Long Run

“Graduation from college is only one step on a journey, but it is an important one and well worth celebrating.”

Consultation PaperOn Draft Implementing Technical Standards

On Additional Liquidity Monitoring Metrics under Article 403(2) of the draft Capital Requirements Regulation (CRR)

EXPLANATORY MEMORANDUM TOTHE FINANCIAL CONGLOMERATES AND OTHER FINANCIAL GROUPS (AMENDMENT) REGULATIONS

These Regulations implement, in part, Directive 2011/ 89/ EU of the European Parliament and of the Council amending Directives 98/78 /EC, 2002/ 87/ EC, 2006/48 /EC and 2009/ 138/ EC (OJ L 326/113 8.12.2011) asregards the supplementary supervision of financial entities in a financial conglomerate.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 5

Who calls the shots? The problem of fiscal dominance

Speech by Dr Jens Weidmann, President of the Deutsche Bundesbank, at the 4th Bank of France - Deutsche Bundesbank Macroeconomics and Finance Conference, Paris.

Solvency I I update for all firms

As part of our commitment to sharing developments in our approach to the implementation of Solvency I I , I thought it would be helpful to write to all firms affected by the Directive to give an update on the current position and what this means for the work that has to be done in the coming months.

As you know, there continues to be significant uncertainty over the timetable and final shape of the Solvency I I regime.

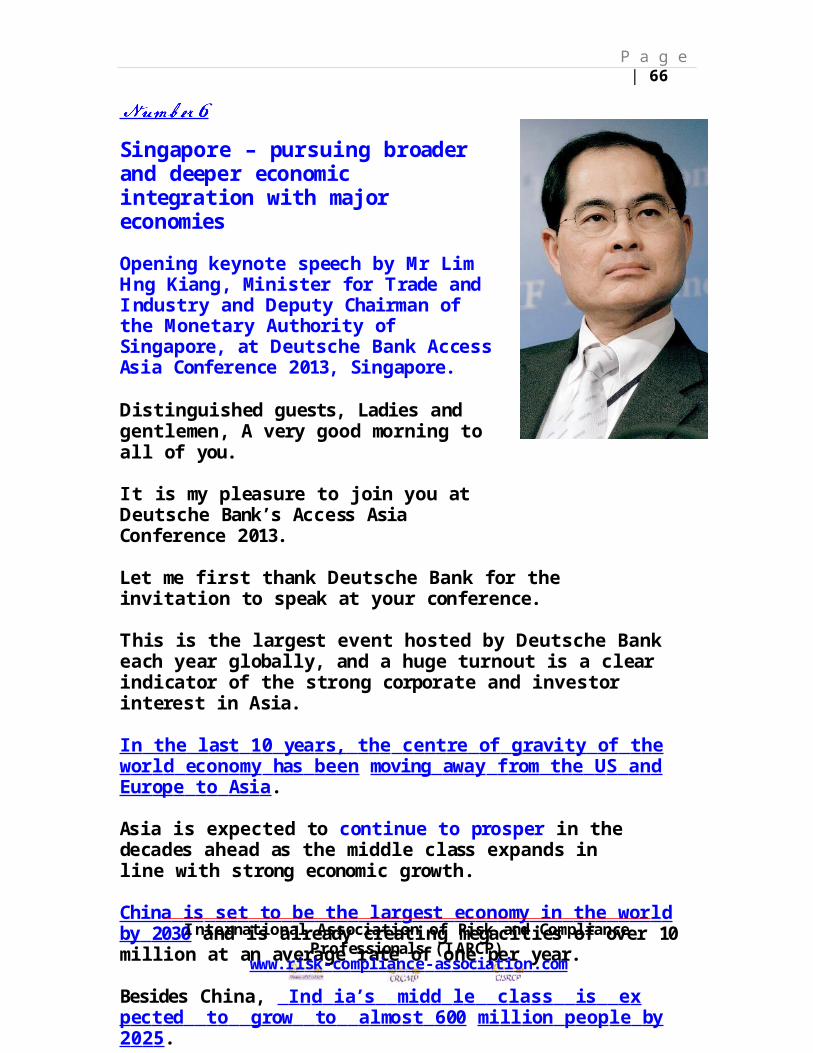

Singapore – pursuing broader and deeper economic integration with major economies

Opening keynote speech by Mr Lim Hng Kiang, Minister for Trade and Industry and Deputy Chairman of the Monetary Authority of Singapore, at Deutsche Bank Access Asia Conference 2013, Singapore.

“In the last 10 years, the centre of gravity of the world economy has been moving away from the US and Europe

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 6

to Asia.

Asia is expected to continue to prosper in the decades ahead as the middle class expands in line with strong economic growth.

China is set to be the largest economy in the world by 2030 and is already creating megacities of over 10 million at an average rate of one per year.

Besides China, Ind ia’s midd le class is expected to grow to almost 600 million people by 2025.

In Indonesia, almost 60 per cent of Indonesian households, in a country of 240 million people, are expected to reach middle-class status by 2020.”

Prospects for a stronger recovery

Speech by Ms Sarah Bloom Raskin, Member of the Board of Governors of the Federal Reserve System, at the Society of Government Economists and the National Economists Club, Washington DC.

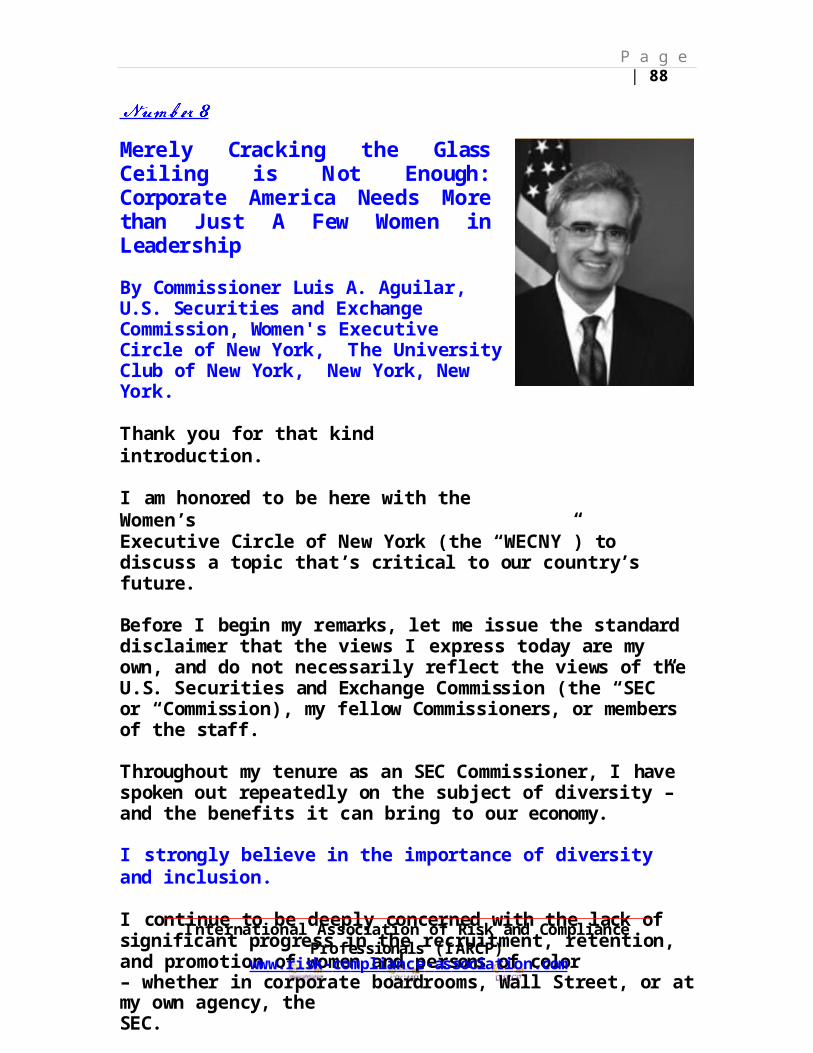

Merely Cracking the Glass Ceiling is Not Enough: Corporate America Needs More than Just A Few Women in Leadership

By Commissioner Luis A. Aguilar, U.S. Securities and Exchange Commission, Women's Executive Circle of New York, The University Club of New York, New York, New York.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 7

The Single Resolution Mechanism – why it is needed

Speech by Mr Benoît Coeuré, Member of the Executive Board of the European Central Bank, at the ICMA Annual General Meeting and Conference 2013, organised by the International Capital Market Association, Copenhagen.

“The financial crisis has highlighted the weaknesses of the institutional framework of Economic and Monetary Union.

The negative feedback loop between banks and sovereigns as well as signs of market fragmentation made European leaders take an extraordinary decision last summer, namely to establish the European Banking Union.”

The Important Role of Immigrants in Our Economy

By Commissioner Luis A. AguilarU.S. Securities and Exchange Commission Remarks at the 2013 Annual GalaGeorgia H ispanic Chamber of CommerceAtlanta, Georgia

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 8

Chairman Ben S. BernankeAt Bard College at Simon's Rock, Great Barrington, Massachusetts

Economic Prospects for the Long Run

Let me start by congratulating the graduates and their parents. The word "graduate" comes from the Latin word for "step."

Graduation from college is only one step on a journey, but it is an important one and well worth celebrating.

I think everyone here appreciates what a special privilege each of you has enjoyed in attending a unique institution like Simon's Rock.

It is, to my knowledge, the only "early college" in the United States; many of you came here after the 10th or 11th grade in search of a different educational experience.

And with only about 400 students on campus, I am sure each of you has felt yourself to be part of a close-knit community.

Most important, though, you have completed a curriculum that emphasizes creativity and independent critical thinking, habits of mind that I am sure will stay with you.

What's so important about creativity and critical thinking?

There are many answers.

I am an economist, so I will answer by talking first about our economic future--or your economic future, I should say, because each of you will have many years, I hope, to contribute to and benefit from an increasingly sophisticated, complex, and globalized economy.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 9

My emphasis today will be on prospects for the long run.

In particular, I will be looking beyond the very real challenges of economic recovery that we face today--challenges that I have every confidence we will overcome--to speak, for a change, about economic growth as measured in decades, not months or quarters.

Many factors affect the development of the economy, notably among them a nation's economic and political institutions, but over long periods probably the most important factor is the pace of scientific and technological progress.

Between the days of the Roman Empire and when the Industrial Revolution took hold in Europe, the standard of living of the average person throughout most of the world changed little from generation to generation.

For centuries, many, if not most, people produced much of what they and their families consumed and never traveled far from where they were born.

By the mid-1700s, however, growing scientific and technical knowledge was beginning to find commercial uses.

Since then, according to standard accounts, the world has experienced at least three major waves of technological innovation and its application.

The first wave drove the growth of the early industrial era, which lasted from the mid-1700s to the mid-1800s.

This period saw the invention of steam engines, cotton-spinning machines, and railroads.

These innovations, by introducing mechanization, specialization, and mass production, fundamentally changed how and where goods were produced and, in the process, greatly increased the productivity of workers and reduced the cost of basic consumer goods.International Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 10

The second extended wave of invention coincided with the modern industrial era, which lasted from the mid-1800s well into the years after World War I I.

This era featured multiple innovations that radically changed everyday life, such as indoor plumbing, the harnessing of electricity for use in homes and factories, the internal combustion engine, antibiotics, powered flight, telephones, radio, television, and many more.

The third era, whose roots go back at least to the 1940s but which began to enter the popular consciousness in the 1970s and 1980s, is defined by the information technology (IT ) revolution, as well as fields like biotechnology that improvements in computing helped make possible.

Of course, the IT revolution is still going on and shaping our world

today. Now here's a question--in fact, a key question, I imagine,

from yourperspective.

What does the future hold for the working lives of today's graduates?

The economic implications of the first two waves of innovation, from the steam engine to the Boeing 747, were enormous.

These waves vastly expanded the range of available products and the efficiency with which they could be produced.

Indeed, according to the best available data, output per person in the United States increased by approximately 30 times between 1700 and 1970 or so, growth that has resulted in multiple transformations of our economy and society.

History suggests that economic prospects during the coming decades depend on whether the most recent revolution, the IT revolution, has economic effects of similar scale and scope as the previous two.

But will it?

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 11

I must report that not everyone thinks so.

Indeed, some knowledgeable observers have recently made the case that the IT revolution, as important as it surely is, likely will not generate the transformative economic effects that flowed from the earlier technological revolutions.

As a result, these observers argue, economic growth and change in coming decades likely will be noticeably slower than the pace to which Americans have become accustomed.

Such an outcome would have important social and political--as well as economic--consequences for our country and the world.

This provocative assessment of our economic future has attracted plenty of attention among economists and others as well.

Does it make sense?

Here's one way to think more concretely about the argument that the pessimists are making:

Fifty years ago, in 1963, I was a nine-year-old growing up in a middle-class home in a small town in South Carolina.

As a way of getting a handle on the recent pace of economic change, it's interesting to ask how my family's everyday life back then differed from that of a typical family today.

Well, if I think about it, I could quickly come up with the Internet, cellphones, and microwave ovens as important conveniences that most of your families have today that my family lacked 50 years ago.

Health care has improved some since I was young; indeed, life expectancy at birth in the United States has risen from 70 years in 1963 to 78 years today, although some of this improvement is probably due to better nutrition and generally higher levels of income rather than advances in medicine alone.International Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 12

Nevertheless, though my memory may be selective, it doesn't seem to me that the differences in daily life between then and now are all that large.

Heating, air conditioning, cooking, and sanitation in my childhood were not all that different from today.

We had a dishwasher, a washing machine, and a dryer.

My family owned a comfortable car with air conditioning and a radio, and the experience of commercial flight was much like today but without the long security lines.

For entertainment, we did not have the Internet or video games, as I mentioned, but we had plenty of books, radio, musical recordings, and a color TV (although, I must acknowledge, the colors were garish and there were many fewer channels to choose from).

The comparison of the world of 1963 with that of today suggests quite substantial but perhaps not transformative economic change since then.

But now let's run this thought experiment back another 50 years, to 1913 (the year the Federal Reserve was created by the Congress, by the way), and compare how my grandparents and your great-grandparents lived with how my family lived in 1963.

Life in 1913 was simply much harder for most Americans than it would be later in the century.

Many people worked long hours at dangerous, dirty, and exhausting jobs--up to 60 hours per week in manufacturing, for example, and even more in agriculture.

Housework involved a great deal of drudgery; refrigerators, freezers, vacuum cleaners, electric stoves, and washing machines were not in general use, which should not be terribly surprising since most urban households, and virtually all rural households, were not yet wired for electricity.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 13

In the entertainment sphere, Americans did not yet have access to commercial radio broadcasts and movies would be silent for another decade and a half.

Some people had telephones, but no long-distance service was

available. In transportation, in 1913 Henry Ford was just

beginning the massproduction of the Model T automobile, railroads were powered by steam,and regular commercial air travel was quite a few years away.

Importantly, life expectancy at birth in 1913 was only 53 years, reflecting not only the state of medical science at the time--infection-fighting antibiotics and vaccines for many deadly diseases would not be developed for several more decades--but also deficiencies in sanitation and nutrition.

This was quite a different world than the one in which I grew up in 1963 or in which we live today.

The purpose of these comparisons is to make concrete the argument made by some economists, that the economic and technological transformation of the past 50 years, while significant, does not match the changes of the 50 years--or, for that matter, the 100 years--before that.

Extrapolating to the future, the conclusion some have drawn is that the sustainable pace of economic growth and change and the associated improvement in living standards will likely slow further, as our most recent technological revolution, in computers and IT, will not transform our lives as dramatically as previous revolutions have.

Well, that's sort of depressing.

Is it true, then, as baseball player Yogi Berra said, that the future ain't what it used to be? Nobody really knows; as Berra also astutely observed, it's tough to make predictions, especially about the future.

But there are some good arguments on the other side of this debate.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 14

First, innovation, almost by definition, involves ideas that no one has yet had, which means that forecasts of future technological change can be, and often are, wildly wrong.

A safe prediction, I think, is that human innovation and creativity will continue; it is part of our very nature.

Another prediction, just as safe, is that people will nevertheless continue to forecast the end of innovation.

The famous British economist John Maynard Keynes observed as much in the midst of the Great Depression more than 80 years ago.

He wrote then, "We are suffering just now from a bad attack of economic pessimism.

It is common to hear people say that the epoch of enormous economic progress which characterised the 19th century is over; that the rapid improvement in the standard of life is now going to slow down."

Sound familiar?

By the way, Keynes argued at that time that such a view was shortsighted and, in characterizing what he called "the economic possibilities for our grandchildren," he predicted that income per person, adjusted for inflation, could rise as much as four to eight times by 2030.

His guess looks pretty good; income per person in the United States today is roughly six times what it was in 1930.

Second, not only are scientific and technical innovation themselves inherently hard to predict, so are the long-run practical consequences of innovation for our economy and our daily lives.

Indeed, some would say that we are still in the early days of the IT revolution; after all, computing speeds and memory have increased many times over in the 30-plus years since the first personal computers came on the market, and fields like biotechnology are also advancing rapidly.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 15

Moreover, even as the basic technologies improve, the commercial applications of these technologies have arguably thus far only scratched the surface.

Consider, for example, the potential for IT and biotechnology to improve health care, one of the largest and most important sectors of our economy.

A strong case can be made that the modernization of health-care IT systems would lead to better-coordinated, more effective, and less costly patient care than we have today, including greater responsiveness of medical practice to the latest research findings.

Robots, lasers, and other advanced technologies are improving surgical outcomes, and artificial intelligence systems are being used to improve diagnoses and chart courses of treatment.

Perhaps even more revolutionary is the trend toward so-called personalized medicine, which would tailor medical treatments for each patient based on information drawn from that individual's genetic code.

Taken together, such advances could lead to another jump in life expectancy and improved health at older ages.

Other promising areas for the application of new technologies include the development of cleaner energy--for example, the harnessing of wind, wave, and solar power and the development of electric and hybrid vehicles--as well as potential further advances in communications and robotics.

I'm sure that I can't imagine all of the possibilities, but historians of science have commented on our collective tendency to overestimate the short-term effects of new technologies while underestimating their longer-term potential.

Finally, pessimists may be paying too little attention to the strength of the underlying economic and social forces that generate innovation in the modern world.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 16

Invention was once the province of the isolated scientist or tinkerer.

The transmission of new ideas and the adaptation of the best new insights to commercial uses were slow and erratic.

But all of that is changing radically.

We live on a planet that is becoming richer and more populous, and in which not only the most advanced economies but also large emerging market nations like China and India increasingly see their economic futures as tied to technological innovation.

In that context, the number of trained scientists and engineers is increasing rapidly, as are the resources for research being provided by universities, governments, and the private sector.

Moreover, because of the Internet and other advances in communications, collaboration and the exchange of ideas take place at high speed and with little regard for geographic distance.

For example, research papers are now disseminated and critiqued almost instantaneously rather than after publication in a journal several years after they are written.

And, importantly, as trade and globalization increase the size of the potential market for new products, the possible economic rewards for being first with an innovative product or process are growing rapidly.

In short, both humanity's capacity to innovate and the incentives to innovate are greater today than at any other time in history.

Well, what does all this have to do with creativity and critical thinking, which is where I started?

The history of technological innovation and economic development teaches us that change is the only constant.International Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 17

During your working lives, you will have to reinvent yourselves many times.

Success and satisfaction will not come from mastering a fixed body of knowledge but from constant adaptation and creativity in a rapidly changing world.

Engaging with and applying new technologies will be a crucial part of that adaptation.

Your work here at Simon's Rock, and the intellectual skills, creativity, and imagination that that work has fostered, are the best possible preparation for these challenges.

And while I have emphasized technological and scientific advances today, it is important to remember that the arts and humanities facilitate new and creative thinking as well, while helping us to draw meaning that goes beyond the purely material aspects of our lives.

I wish you the best in facing the difficult but exciting challenges that lie ahead.

Congratulations.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 18

Consultation PaperOn Draft Implementing Technical Standards

On Additional LiquidityMonitoring Metrics under Article 403(2) of the draft Capital Requirements Regulation (CRR)

1.Responding to this Consultation

The EBA invites comments on all proposals put forward in this paper and in particular on the specific questions summarised in 5.2. Comments are most helpful if they:

- respond to the question stated;

- indicate the specific point to which a comment relates;

- contain a clear rationale;

- provide evidence to support the views expressed/ rationale proposed; and

-describe any alternative regulatory choices the EBA should

consider. Please send your comments to the EBA by email [email protected] by 14.08.2013, indicating the reference‘EBA/CP/2012/18’ on the subject field.

Please note that comments submitted after the deadline, or sent to another e-mail address will not be processed.

Publication of responses

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 19

All contributions received will be published following the close of the consultation, unless you request otherwise.

Please indicate clearly and prominently in your submission any part you do not wish to be publicly disclosed.

A standard confidentiality statement in an e-mail message will not be treated as a request for non-disclosure.

A confidential response may be requested from us in accordance with the EBA’s rules on public access to documents.

We may consult you if we receive such a request. Any decision we make not to disclose the response is reviewable by the EBA’s Board of Appeal and the European Ombudsman.

Data protection

Information on data protection can be found at www.eba.europa.eu under the heading ‘Legal Notice’.

2. Executive Summary

The proposed Capital Requirements Directive/ Regulation (CRR/ CRD) sets out requirements concerning liquidity which are expected to apply from 1 January 2014 and mandates the EBA to prepare draft regulatory/ implementing technical standards (RTS/ITS) in this area.

The EBA has developed these ITS proposals on the basis of the legislative texts for the CRR agreed by the European Parliament and the Council in April 2013, in accordance with the mandate contained in Articles 403(2) of those texts.

These texts will be subject to legal-linguistic review before being formally adopted and the final text published in the Official Journal of the European Union.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 20

The EBA will review the ITS proposals to ensure that they take account of any changes made in the final text of the CRR, as well as to take account of any changes arising out of the consultation process.

Main features of the ITS

This CP contains the EBA proposal in relation to supervisory reporting of additional monitoring metrics for liquidity.

In defining its proposal, the EBA followed the approach developed by theBasel Committee on Banking Supervision (BCBS).

The EBA’s proposed metrics to be covered by this ITS include the following:

- a maturity ladder (template and instructions). This is similar to the contractual maturity mismatch put forward by the BCBS text and provides insight into the extent to which a bank relies on maturity transformation under its current contracts.

It comprises two separate templates (set out in two worksheets), one for contractual flows and one for behavioural flows.

The maturity of the outflows and inflows to be reported in both templates range from open maturity up to greater than 10 years (13 buckets in total).

- some additional monitoring tools (templates and instructions) related to:

o concentration of funding by counterparty: This is similar to the concentration of funding metric put forward by the BCBS, and it allows the identification of those sources of wholesale and retail funding of such significance that their withdrawal could trigger liquidity problems.

It is proposed that institutions report the top ten largest counterparties from which funding obtained exceeds a threshold of 1% of total liabilities, together with information on the counterparty name, counterparty type

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 21

and location, product type, currency, amount received, weighted average and residual maturity.

o concentration of funding by product type: This seeks to collect information about the institution's concentration of funding by product type, broken down into different funding types related to retail and wholesale funding.

It is proposed that institutions report the total amount of funding received from each product category, when it exceeds a threshold of 1% of total liabilities.

o prices for various lengths of funding: This seeks to collect information about the average transaction volume and prices paid by institutions for funding with different maturities ranging from overnight to 10 years.

o rollover of funding: This seeks to collect information about the volume of funds maturing and new funding obtained i.e. ‘roll-over of funding’ on a daily basis over a monthly time horizon.

3. Background and rationale The nature of ITS under EU law

The present draft ITS are produced in accordance with Article 15 of EBA regulation. Paragraph 4 of that same article provides that ITS shall be adopted by means of an EU Regulation or Decision.

According to EU law, EU regulations are binding in their entirety and directly applicable in all Member States.

This means that, on the date of their entry into force, they become part of the national law of the Member States and that their implementation into national law is not only unnecessary but also prohibited by EU law, except in so far as this is expressly required by them.

Shaping these rules in the form of a Regulation would ensure alevel-playing field by preventing diverging national requirements and would ease the cross-border provision of services; currently, an institution

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 22

that wishes to take up operations in another Member State has to apply different sets of rules.

Background and regulatory approach followed in the draft ITS

In January 2013, the Basel Committee on Banking Supervision (BCBS) published its revised text on the liquidity coverage ratio (LCR) and liquidity risk monitoring tools.

These monitoring tools, together with the LCR standard, provide the cornerstone of information that aid supervisors in assessing the liquidity risk of an institution, because they can help competent authorities identify potential liquidity difficulties signaled through a negative trend in the metrics or through an absolute result of the metrics.

The EBA will observe further work conducted by the BCBS in respect of liquidity risk monitoring and consider amendments to its own proposals as necessary.

One such topic may be monitoring tools for intra-day liquidity management.

Within this context, the EBA may consider increasing further the granularity of some of the proposed time buckets covering the period of the first 3 months.

Input from the industry on these last aspects would be welcome.

The CRR provisions related to liquidity reporting translate these BCBS proposals into EU law.

Thus, in addition to the LCR, institutions will have to report to their competent authorities information related to additional metrics.

In this context, the CRR also provides, in Article 403(3)(b), that the EBA shall develop draft ITS to specify the additional liquidity monitoring metrics required to allow competent authorities to obtain a

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 23

comprehensive view of the liquidity risk profile, proportionate to the nature, scale and complexity of an institution's activities.

This CP contains the EBA proposal in relation to supervisory reporting of additional monitoring metrics for liquidity.

In defining its proposal, the EBA followed the approach developed by the BCBS.

The EBA’s proposed metrics to be covered by this ITS include the following:

- a maturity ladder (template and instructions)

o some additional monitoring tools (templates and instructions) related to:

o concentration of funding by

counterparty o concentration of

funding by product type

o prices for various lengths of funding

o rollover of funding

The metric related to the maturity ladder is similar to the contractual maturity mismatch put forward by the BCBS text.

The template developed in the ITS is designed to capture the maturity mismatch of an institution's balance sheet, and as such, is referred to as the ‘maturity ladder’.

These maturity mismatches indicate how much liquidity a bank would potentially need to raise in each of different time bands if all outflows occurred at the earliest possible date.

This metric provides insight into the extent to which the bank relies on maturity transformation under its current contracts.International Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 24

The maturity ladder forms part of the package of ‘monitoring tools’ which the EBA has designed.

The maturity ladder is a monitoring tool which comprises two separate templates (which are set out in two worksheets), one for contractual flows and one for behavioural flows (inflows and outflows).

The contractual flows resulting from legally binding agreements should be reported according to the provisions of these agreements, while the behavioural flows should be based upon a base-case economic scenario used by the reporting institution in its current business planning (the scenario that the institution expects to happen, as opposed to pre-defined stressed conditions).

The maturity of the outflows and inflows to be reported both in the contractual template and the behavioural template range from open maturity up to greater than 10 years (13 buckets in total), which allows all relevant maturities to be captured.

The metrics related to the additional monitoring tools are designed to monitor an institution's liquidity risk that falls outside the scope of the reports on Liquidity Coverage and Stable Funding.

The template on concentration of funding by counterparty, similar to the concentration of funding metric put forward by the BCBS text, allows the identification of those sources of wholesale and retail funding of such significance that their withdrawal could trigger liquidity problems.

Excessive reliance on individual counterparties could lead to the crystallisation of liquidity risk, where the funding relationship to cease during a stress scenario.

It is therefore important to provide templates for reporting on these items, so as to help institutions to identify these risks early and seek funding from a wide range of counterparties.

For the purpose of this ITS, it is proposed that institutions are required to report the top ten largest counterparties from which funding obtained

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 25

exceeds a threshold of 1% of total liabilities, together with information on the counterparty name, counterparty type and location, product type, currency, amount received, weighted average and residual maturity.

The template on funding by product type seeks to collect information about the institution's concentration of funding by product type, broken down into different funding types related to retail and wholesale funding.

Excessive reliance on specific product types could lead to the crystallisation of liquidity risk, were the specific product types proven to be subject to high outflows during a stress scenario.

It is therefore important to provide templates for reporting on these items, so as to help institutions to identify these risks early and seek funding from a wide range of product types.

For the purpose of completing the ITS templates, it is proposed that institutions report the total amount of funding received from each product category, when it exceeds a threshold of 1% of total liabilities.

With regard to the counterbalancing capacity on the assets side, the EBA is considering integrating into the final ITS the template and instructions shown in the appendix of this consultation paper.

This part of the reporting aims at capturing concentrations of assets used to counterbalance outflows and would collect information about the ten largest holdings in those assets issued by a single name.

It is clear that high concentrations may represent a risk of overestimation of the counterbalancing capacity if the markets for the various financial instruments issued by a specific individual issuer fall dry.

Additional information on the issuer/ counterparty location may add insight on interconnectedness.

As part of the total, the template seeks also information on received stand-by liquidity facilities which are seen as part of the counterbalancing capacity by the institution.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 26

Insight in these specific types of concentrations cannot sufficiently be obtained from other templates.

The template on prices for various lengths of funding seeks to collect information about the average transaction volume and prices paid by institutions for funding with different maturities ranging from overnight to 10 years.

Finally, the template on the roll-over of funding seeks to collect information about the volume of funds maturing and new funding obtained i.e. ‘roll-over of funding’ on a daily basis over a monthly time horizon.

As a reminder, please note that Article 403(2) of the draft CRR stipulates that an institution shall report separately to the competent authorities of the home Member State the items subject to liquidity risk reporting in a currency when it has

(i)aggregate liabilities in that currency, different from the single currency used for reporting, amounting to or exceeding 5 % of the institution’s or the single liquidity sub-group’s total liabilities; or

(ii)a significant branch as defined in Article 52 of the CRD in a host Member State using a currency different from the reporting currency.

The present ITS have been developed to provide competent authorities with harmonised information on institutions’ liquidity risk profile, taking into account the nature, scale and complexity of institutions' activities.

As the ITS on additional liquidity monitoring metrics will become part of the general supervisory reporting framework requirements, following the introduction of liquidity requirements, formats have been developed with the aim of ensuring consistency where allowed by the CRR proposed text.

Scope/ level of application and frequency

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 27

The scope and level of application of these ITS seek to be consistent with the scope and level of application of the CRR and of the prudential reporting requirements (COREP), i.e. it applies:

-on a consolidated basis (Article 10(3) of the CRR): to EU parent credit institutions and investment firms and to credit institutions and investment firms controlled by an EU parent financial holding company or by an EU parent mixed financial holding company;

-on an individual basis (Article 5(4) of the CRR) : to all credit institutions and investment firms that are authorised to provide the investment services listed in points 3 and 6 of section A of Annex I to Directive 2004/ 39/ EC.

However, according to Article 7(1) of the proposed CRR text, competent authorities will be allowed to waive in full or in part the application of Part Six of the CRR (Liquidity requirements) to a institution and to all or some of its subsidiaries, if they fulfill a set a predefined conditions, including if the parent institution complies on a consolidated basis with the obligation set forth in Article 401 and 403.

The reporting frequency will be monthly for all monitoring metrics.

Under specific clear and factual criteria, duly framed in the ITS, proportionate to the nature, scale and complexity of an institution's activities, the reporting frequency can be reduced, respectively to a quarterly basis.

These specific criteria relate to the existence of cross-border activities and size of the institution’s balance sheet.

It shall be noted that Article 64 of the CRD related to supervisory powers allows competent authorities to impose additional or more frequent reporting requirements, including reporting on liquidity positions.

For example in periods of stress competent authorities could impose some reporting with a daily frequency.International Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 28

Timing of ITS development and application date

Considering that the EBA is consulting on this reporting for additional metrics at a later stage than for the other reporting requirements, the EBA may consider further the appropriate application date compared to the application date of other reporting requirements (in particular the reporting requirements for liquidity coverage and stable funding).

According to the draft CRR, the EBA is expected to submit these ITS to the European Commission (EC) by 1 January 2014.

The data point model related to the reporting on additional monitoring metrics will be published for consultation in the course of 2013.

4. Draft implementing technical standards on Additional Liquidity Monitoring Metrics under the Capital Requirements Regulation (CRR)

THE EUROPEAN COMMISSION,

Having regard to the Treaty on the Functioning of the European Union, Having regard to Regulation xx/ XX/ EU of the European Parliament and of the Council of [dd mmmm yyyy] on prudential requirements for credit institutions and investment firms [CRR], and in particular to Articles......and 403(3)(b) thereof, [ADDENDUM TO THE LEGAL BASES AS PRESENTED IN CP50 AND SUBSEQUENT CPs ON VARIOUS ASPECTS OF REPORTING]

Whereas:

...[ADDENDUM TO THE RECITALS AS PRESENTED IN CP50 AND SUBSEQUENT CPs ON VARIOUS ASPECTS OF REPORTING](xx)

(xx) Reporting for additional metrics relating to liquidity should comprise a maturity ladder, because this is what would allow the maturity

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 29

mismatch of an institution's balance sheet to be captured; metrics based on the concentration of funding by counterparty and product type, because these metrics identify counterparties and instruments that are of such relevance that withdrawal of funds or declining market liquidity could trigger liquidity problems; metrics based on the prices for various lengths of funding and the rollover of funding because such information will become valuable over time as supervisors would be made aware of changes in funding spreads, volumes and tenors.

(xx) Given that articles 5 to 9 of Regulation xx/ xxx [CRR] specify the level of application of the liquidity coverage, the level and scope of the reporting of that liquidity coverage and on the additional monitoring metrics should be aligned with that, and therefore the reporting on these additional monitoring metrics should be required only at the level of consolidation at which reporting on liquidity coverage is required according to Article 403(3)(a).

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 30

EXPLANATORY MEMORANDUM TOTHE FINANCIAL CONGLOMERATES AND OTHER FINANCIAL GROUPS (AMENDMENT) REGULATIONS

This explanatory memorandum has been prepared by HM Treasury and is laid before Parliament by Command of Her Majesty.

Purpose of the instrument

These Regulations implement, in part, Directive 2011/ 89/ EU of the European Parliament and of the Council amending Directives 98/78 /EC, 2002/ 87/ EC, 2006/48 /EC and 2009/ 138/ EC (OJ L 326/113 8.12.2011) asregards the supplementary supervision of financial entities in a financial conglomerate.

The Prudential Regulation Authority (“PRA”) and the Financial Conduct Authority (“FCA”) are responsible for implementing the majority of the provisions of this Directive.

The Regulations make a limited number of technical and definitional amendments to existing secondary legislation which imposes obligations on the PRA and FCA with regard to their supervisory functions, in particular concerning information sharing and consultation requirements.

Legislative Context

The Financial Conglomerates Directive 2002 (Directive 2002/ 87/EC), provides the framework for the prudential supervision of financial conglomerates involved in both banking and insurance activities, supplementing the relevant banking and insurance sectoral directives by providing additional supervision at the group level.International Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 31

The Financial Conglomerates Directive 2002 was implemented in the UK mainly by rules made by the Financial Services Authority (“FSA” – the predecessor to the PRA and FCA) under the Financial Services and Markets Act 2000 (“FSMA”), but certain provisions which imposed obligations on the supervisory authority, were transposed by the Financial Conglomerates and Other Financial Groups Regulations 2004 (S.I. 2004/1862).

Directive 2011/ 89/ EU is the result of a technical review of the 2002 Directive which was commenced by the European Commission in 2008 and makes changes to the Financial Conglomerates Directive 2002 and the relevant sectoral directives to improve the effectiveness of the current rules.

These Regulations transpose those aspects of Directive 2011/ 89/ EU which require amendments to be made to existing secondary legislation, notably the Financial Conglomerates and Other Financial Groups Regulations 2004 and the Capital Requirements Regulations 2006 (S.I. 2006/ 3221), by the transposition deadline of 10 June 2013.

Most of the Directive provisions are being transposed by rules made by the PRA and FCA.

Those provisions of the Directive which relate to alternative investment fund managers, and which also require amendments to the Financial Conglomerates and Other Financial Groups Regulations 2004, but have a later transposition deadline of 22 July 2013, will be transposed by way of a separate set of Regulations which is due to be made for the purposes of transposing the Alternative Investment Fund Managers Directive (Directive 2011/ 61/EU) by that deadline.

These Regulations also update certain cross-references in the Financial Conglomerates and Other Financial Groups Regulations 2004 to provisions in Part 12 of FSMA, which were amended by the Financial Services and Markets Act 2000 (Controllers) Regulations 2009 (S.I. 2009/ 534) as part of the exercise of transposing the Acquisitions Directive (Directive 2007 /44/EC).

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 32

Policy background - What is being done and why

The aim of Directive 2011/ 89/ EU is to act as a quick fix in response to gaps in conglomerate supervision that were highlighted by the experience of the financial crisis and identified in the review of the Financial Conglomerates Directive 2002 carried out by the European Commission in 2008/2009.

The changes are expected to eliminate the unintended consequences and technical omissions in the relevant sectoral directives (covering the supervision of banking and insurance institutions), and improve the consistency of supervision of group risks.

The changes include amendments to the capital calculation methodology for conglomerates, a requirement to include asset management companies and alternative investment fund managers in the conglomerates identification process, and amendments to the identification threshold triggers, as well as providing for conglomerate stress testing.

Most of these substantive changes will be implemented by amendments to PRA and FCA rules.

However, a limited number of amendments are required to existing secondary legislation which imposes obligations on the PRA and FCA with regard to their supervisory functions in relation to conglomerates.

These mainly concern consequential amendments to consultation and information sharing requirements.

A more fundamental review of the Financial Conglomerates Directive 2002 is currently underway.

The aim of this is to provide a wider-ranging assessment of the the financial crisis.

The European Commission published a progress update report on this review in December 2012.International Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 33

This noted the importance of taking into account the recent and pending changes to sectoral legislation – such as Solvency I I and the Capital Re qu iremen ts Direct ive (“CRD 4”) – as well as the implications of Banking Union proposals for conglomerate supervision.

As a result, the report stated that the Commission does not intend to bring forward legislative proposals in 2013, but will keep the situation under review to determine the appropriate timing for the revision.

Consolidation

There are no current plans to consolidate the amendments to the Financial Conglomerates and Other Financial Groups Regulations 2004 or the Capital Requirements Regulations 2006.

However, the 2004 Regulations are likely to be amended again following the current more fundamental review of the Financial Conglomerates Directive 2002, at which stage further consideration will be given to consolidation.

The Capital Requirements Regulations 2006 are expected to be further amended or replaced as part of the exercise of transposing CRD4 which is due to be adopted later this year.

Consultation outcome

The European Commission undertook a targeted pre-legislative consultation on its review of the Financial Conglomerates Directive in November 2009, prior to issuing its formal proposal in August 2010.

We understand that a UK stakeholder responded but the response was not made public.

Details of the consultation, including published responses, are available at: http://ec.europa.eu/internal_market/consultations/2009/fcd_review_e n.htmInternational Association of Risk and Compliance Professionals

(IARCP)www.risk-compliance-association.com

P a g e | 34

A draft of these Regulations was subject to a public consultation in the document CP12/40: Financial Conglomerates Directive – Technical review amendments, a joint FSA-HM Treasury consultation, which was published on the FSA website on 21 December 2012, and is available at: http://www.fsa.gov.uk/static/pubs/cp/cp12-40.pdf.

The consultation closed on 21 March 2013 and no responses were received concerning the Treasury’s draft Regulations.

The Treasury also consulted the FSA and its successor authorities prior to making these Regulations, which impose obligations directly on the PRA and FCA, and the FSA was content with the draft Regulations.

Guidance

The Treasury is not planning to issue any guidance on these Regulations, which do not impose obligations directly on business.

The PRA and the FCA are due to issue policy statements detailing their final rules implementing other parts of Directive 2011/ 89/ EU.

TRANSPOSITION NOTE FOR DIRECTIVE 2011/ 89/EU

This transposition note sets out the legislation which transposes into UK law Directive 2011/ 89 /EU of the European Parliament and of the Council amending Directives 98/78/ EC, 2002/87/EC, 2006/48/ EC and 2009/ 138/ EC as regards the supplementary supervision of financial entities in a financial conglomerate.

This Directive makes technical amendments to the Financial Conglomerates Directive 2002 (Directive 2002/ 87/ EC), which deals with the supplementary supervision of financial conglomerates, which are groups which carry out significant activities in both the banking/ investment services and insurance sectors.

It also makes consequential amendments to the relevant sectoral directives dealing with the regulation of banks/investment firms and insurance firms.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 35

The Financial Conglomerates Directive 2002 was originally transposed mainly by way of rules made by the Financial Services Authority (the “FSA”) under the Financial Services and Markets Act 2000, and also in part by the Financial Conglomerates and Other Financial Groups Regulations 2004 (SI 2004/ 1862) made by the Treasury.

The new Directive makes technical changes to the Financial Conglomerates Directive 2002, including changes to the conglomerate capital calculations methodology, changes to include asset management companies and alternative investment fund managers within the process for identifying a financial conglomerate, and changes to the application of identification threshold triggers.

The new Directive is being transposed mainly by the way of amendments being made to the rules of the Prudential Regulation Authority (the “PRA”) and (where necessary) the Financial Conduct Authority (the “FCA”), which were established in place of the FSA with effect from 1 April 2013 (when the Financial Services Act 2012 came into force).

These rules continue to be made under the Financial Services and Markets Act 2000 (as amended by the Financial Services Act 2012).

The new Directive includes amendments to Directive 2009/138/EC (“Solvency I I”), whose transposition date is currently delayed.

The FSA has consulted on proposed amendments arising from the new Directive to the draft PRA prudential sourcebook (SOLPRU) which will, in due course, transpose aspects of Solvency I I .

References to these draft PRA H andbook rules are shown in this Transposition Note although SOLPRU will not be made until the transposition of Solvency I I takes place.

The Directive is also being transposed in part by way of amendments being made by the Treasury to the Financial Conglomerates and Other Financial Groups Regulations 2004 and the Capital Requirements Regulations 2006 (SI 2006/ 3221), together with consequential amendments being made to other legislation.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 36

Most of the provisions of this Directive are due to apply from 10

June 2013. Amendments to the Financial Conglomerates and Other

FinancialGroups Regulations 2004 relating to alternative investment fund managers (which apply from 22 July 2013) will be made separately by way of the Regulations being made to transpose the Alternative InvestmentFund Managers Directive (Directive 2011/61/EU).

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 37

Who calls the shots? The problem of fiscal dominance

Speech by Dr Jens Weidmann, President of the Deutsche Bundesbank, at the 4th Bank of France - Deutsche Bundesbank Macroeconomics and Finance Conference, Paris.

1. Introduction

Ladies and gentlemen,

I would like to thank you for the opportunity to speak here

today. Indeed, in springtime there is no better place to be

than Paris.

As Henry Miller put it: “God knows, when spring comes toParis the humblest mortal alive must feel that he dwells in Paradise”.

However, other parts of Europe are currently a long way from Paradise.

Numerous countries are experiencing a severe crisis, and many people are going through a time of great hardship.

Thus, our most important challenge is to overcome the crisis, restore growth and lead Europe back to prosperity – without endangering price stability.

To achieve this objective many difficult and far-reaching decisions have to be taken.

Against this backdrop, conferences such as this one are

essential. After all, scientific research is a central pillar of good

decision-making.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 38

Thus, I would like to thank the Banque de France for hosting this

event. This session of the conference is titled: “Fiscal Policy in a

MonetaryUnion”.

What is a central banker’s role in such a discussion?

Well, Mervyn King once said: “Central banks are often accused of being obsessed with inflation. This is untrue. If they are obsessed with anything, it is with fiscal policy.”

As so often, Mervyn King was right, we central bankers are indeed obsessed with fiscal policy – and German ones quite probably somewhat more so than those of a different nationality.

This obsession is driven by two interrelated observations:

First, high levels of public debt harbour the risk of higher inflation.

Second, sooner or later high levels of public debt are bound to hurt economic growth.

Given the high levels of public debt in many European countries, one would expect a broad consensus in favour of consolidation – and not just among fixated central bankers.

However, the reality is a bit more complex than I just implied.

There are different views on the dangers and merits of public debt.

In fact, we are currently observing a change of mood that has been dubbed the “austerity backlash”.

Some politicians claim that their countries are dying from mere austerity on its own; others convey the impression that the policy of consolidation has reached its limits.

Consequently, they call for it to be postponed.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 39

These “backlashers” argue that in the current economic situation inflationary pressure is only of limited concern.

Along the same lines they argue that consolidation rather than debt hurts growth the most – at least in the short run.

In my speech I would like to discuss these two issues: first, the relationship between public debt and inflation and second, the question of consolidation and growth.

2. Sound public finances as a prerequisite for monetary policy

Public debt and inflation are related on account of monetary policy’s power to accommodate high levels of public debt.

Thus, the higher public debt becomes, the greater the pressure that can be put upon monetary policy to respond accordingly.

Suddenly it might be fiscal policy that calls the shots – monetary policy no longer follows the objective of price stability but rather the concerns of fiscal policy.

A state of fiscal dominance has been reached.

Technically, fiscal dominance refers to a regime where monetary policy ensures the solvency of the government.

The traditional roles are reversed: monetary policy stabilises real government debt while inflation is determined by the needs of fiscal policy.

In the conventional view, fiscal dominance entails the famous“unpleasant monetarist arithmetic”.

In the words of Sargent and Wallace: “…the monetary authority … must try to finance with seigniorage any discrepancy between the revenue demanded by the fiscal authority and the amounts of bonds that can be sold to the public.”

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 40

In their setup, fiscal policy runs a chronic primary deficit which leads to a corresponding increase in the money supply.

As a simple money demand holds in the model, the price level adjusts to establish equilibrium in the money market.

Put more bluntly: the central bank finances government deficits through the printing press.

Recently, however, another concept of fiscal dominance has gained much attention in the academic literature: the fiscal theory of the price level.

According to this theory, fiscal policy can affect inflation even if it does not monetise public debt along the lines of Sargent and Wallace.

In the words of Woodford: “Fiscal dominance manifests itself through pressure on the central bank to use monetary policy to maintain the market value of government debt.”

The main pillar of the fiscal theory rests on the fact that bonds are claims to nominal payoffs.

Now, if governments are unable to raise sufficient real resources, a new direct link arises between current and expected deficits and inflation.

Intuitively, the logic of the fiscal theory can be described as follows: Let us assume additional expenditure, for instance higher transfers, which are not financed by additional taxes but by issuing additional bonds.

Consequently the value of real debt is now higher than the present value of future tax payments.

Households feel richer and thus consume more, causing output and inflation to increase.

Monetary policy has to stabilise real debt to avoid an inflation spiral, with the result that it responds at a rate of less than 1 to 1 to inflation, thereby violating the Taylor principle.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 41

Thus, higher inflation reduces debt in real terms and lower real interest rates reduce the real debt service burden of existing government debt.

In each of the two cases, a regime of fiscal dominance is characterised by higher inflation and probably also more volatile inflation.

Monetary policy is no longer able to control the inflation rate, and therefore welfare losses will occur.

However, the story does not end here.

Remaining within the world of theory, we can continue as follows:

because economic agents are forward-looking, it is quite possible

that theconsequences I have just described could manifest themselves before the economy has entered the regime of fiscal dominance.

Looking ahead, public debt cannot be accumulated forever.

Sooner or later, governments that run large deficits for a long period of time risk hitting a fiscal limit – a point at which government revenues can no longer be increased to stabilise government debt.

This inability to raise revenues might have economic reasons, such as a crossing of the peak of the Laffer curve.

But there might also be political reasons that make it infeasible to raise taxes.

Certainly, the actual fiscal limit is highly uncertain in many ways: it is a probability distribution rather than a point and depends on expectations, shocks and policy measures taken.

And forward-looking agents know: once the government hits the fiscal limit, either an adjustment of fiscal spending or an adjustment of monetary policy needs to occur.

Otherwise debt cannot be stabilised.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 42

And as a consequence, monetary policy might come under pressure to step in and stabilise government debt.

Thus, even if fiscal policy has not yet reached its limit, the economic mechanisms attached to the fiscal theory of the price level might already swing into action.

To be specific: let us assume that agents expect, with some probability, that monetary policy will bear the burden of adjustment and stabilise real government debt through higher inflation.

Once inflation expectations start rising, the same might happen with inflation as well.

Thus, even if the fiscal limit has not been reached, it may still affect inflation.

In other words, how policy makers are expected to cope with the fiscal limit, including their efforts to consolidate, not only affects expectations concerning future policy regimes but can also affect today’s welfare.

Against the backdrop of this theoretical analysis, one thing should be made clear from a monetary policy perspective: policymakers should not assume that they are on safe ground just because inflation expectations are firmly anchored.

Only if agents expect deviations from a “virtuous regime” of monetary dominance to be short-lived – say, because policymakers still enjoy high credibility – will inflation expectations remain well anchored.

However, if agents learn that the deviation is going to last for longer than initially expected, their inflation expectations will change.

And this might happen very suddenly.

3. Hence, the case for consolidation

What conclusion can we draw from this theoretical analysis?

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 43

Well, the right conclusion is that fiscal consolidation is crucially important to keep inflation expectations anchored.

On this basis, one could make a solid case for consolidation.

For it is incumbent on governments to reduce the level of public

debt. Indeed, they have to do this to promote economic growth

and to ensureprice stability.

As Olivier Blanchard put it: we have to get out of the danger zone.

Certainly, over the past three years many countries have made great efforts to consolidate their public finances.

However, the main driver of these efforts was not academic theory but profane market pressure.

As Simon Nixon recently wrote in the Wall Street Journal:

“For euro-zone countries facing high borrowing costs or reliant on international aid to fund their budget deficits, fiscal consolidation wasn’t a choice but a necessity.”

And it still is.

Even so, now that market pressure has eased somewhat, so has the political will to consolidate.

Many argue that consolidation has gone too far and that it will impede growth given the current state of the economy.

But is that a tenable argument against the need to reduce public debt, to get out of the danger zone?

Let us take a closer look at the relationship between consolidation and growth.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 44

4. But will consolidation hurt growth?

To put my view in a nutshell: I see no conflict between consolidation and growth.

And, indeed, there is not much controversy regarding the long-term relationship between consolidation and growth.

Various studies have confirmed that, in the long run, solid public finances have a beneficial effect on growth – and I am not just referring to the Reinhart- Rogoff study that has received some criticism recently.

Cecchetti and others, for instance, also find that high debt levels inhibit potential growth.

Nevertheless, the short-term relationship between consolidation and growth is hotly debated.

And this debate is currently obscuring the consensus on the longer-term effects of consolidation.

This is because the debate relates directly to policy decisions and to their short-term effects on which politicians are very strongly focused.

More specifically, the debate is focusing on the appropriate pace of consolidation in the current circumstances.

The discussion, therefore, is revolving around the size of the fiscal multiplier.

The larger the multiplier, the greater the negative effect consolidation has on short-term growth.

In general, the size of the multiplier depends on a number of factors.

It depends on the specific fiscal and economic situation of the relevant country, including the size of the export sector, the exchange rate regime,

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 45

trust in fiscal sustainability and the concrete design of the consolidation measures.

Recent research has highlighted the fact that the multiplier might also be state-dependent.

This would imply the possibility that the multiplier is larger in a crisis.

One reason for this could be that monetary policy is constrained by the zero lower bound.

Another reason could be that the number of liquidity-constrained households is increasing.

Empirical studies tend to find that multipliers are indeed larger in recessions and in situations where consolidation takes place during a financial crisis.

However, many of these studies suffer from a lack of data as deep recessions tend to be quite rare events.

Moreover, the way in which such studies are set up is often rather basic and fraught with estimation challenges.

Finally, there are also studies which imply that the fiscal multiplier might be smaller when public debt ratios are high and the sustainability of public finances is in doubt.

Now, what does all this tell us about the current situation and the appropriate pace of consolidation?

Blanchard and Leigh, in a recent working paper, suggest that the fiscal multiplier is currently larger than previously thought.

Therefore, they conclude that consolidation would currently be rather costly in terms of growth and more “backloading” would be desirable.

However, the data set from which these results have been obtained is

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 46

rather small.

Once other control variables are included and variation of the country sample is taken into account, the results are no longer robust.

All things considered, the size of fiscal multipliers seems to be subject to considerable uncertainty – both in general and with regard to the current situation.

Consequently, I think we should look beyond the size of the short-term fiscal multiplier when discussing consolidation.

In general, if consolidation is achieved by reducing public spending, for instance, it will enhance potential growth.

In addition, consolidation will foster fiscal sustainability.

In this regard, it is important to consider how financial markets judge a country’s fiscal situation and translate the results in their risk assessment.

There is widespread agreement that the influence of country-specific fiscal characteristics has risen over the course of the crisis.

The current crisis is, to a large extent, a crisis of confidence – financial markets have lost their confidence in the sustainability of public finances.

Against this backdrop, sustained and credible consolidation would send a clear signal.

Also, with regard to political acceptance, I doubt that turning deferment of consolidation into a never-ending story will find more public support than a fairly swift correction.

And this is why I believe that determined consolidation would help convince the markets that the future fiscal position is going to be sound.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 47

This, in turn, would bring down long-term interest rates or ensure that they remain at a low level, which would be beneficial for economic growth.

By delaying consolidation, on the other hand, governments would risk an increase in market uncertainty.

As a consequence, sovereign bond spreads would remain high or go up even further.

5. Conclusion

Ladies and gentlemen High levels of public debt are one of the major economic policy challenges of our times – especially from a central banker’s point of view.

Sustainable public finances are a necessary prerequisite for a stable currency – a prerequisite that monetary policy itself cannot create.

Given that high levels of public debt also hurt economic growth, there is a solid case for consolidation.

True, in the short run, consolidation can dampen growth; that is undisputed.

Nevertheless, a credible commitment to sound public finances will also inspire confidence.

And confidence is what is lacking in the euro

area. Thank you.

International Association of Risk and Compliance Professionals (IARCP)

www.risk-compliance-association.com

P a g e | 48

Solvency I I update for all firms

As part of our commitment to sharing developments in our approach to the implementation of Solvency I I , I thought it would be helpful to write to all firms affected by the Directive to give an update on the current position and what this means for the work that has to be done in the coming months.

As you know, there continues to be significant uncertainty over the timetable and final shape of the Solvency I I regime.

We are very conscious of the implications for the industry of the continuing delays in terms of complexity and cost.

We cannot yet provide the clear timetable but we are acting in two ways to help the UK industry, both in the European negotiation and in our approach to implementation for UK firms.

I will take each of these points in turn.

European timetable

We are actively engaging with European colleagues to support the timely resolution of policy issues.

Earlier this year we invited firms to take part in the long-term guarantees assessment and we submitted data to the European Insurance and Occupational Pensions Authority (EIOPA) at the end of April.

EIOPA is currently analysing data from Member States with a view to preparing a report for European co-legislators in June.