SEATTLE | 206.622.3700 LOS ANGELES | 310.297.1777 www.wurts.com February 2012 RISK ALLOCATION IN THE 21 ST CENTURY

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SEATTLE | 206.622.3700 LOS ANGELES | 310.297.1777 www.wurts.com

February 2012

RISK ALLOCATION IN THE 21ST CENTURY

A G E N D A

2

INVESTMENT APPROACH

SAMPLE RISK DASHBOARD

GOVERNANCE

I N V E S T M E N T A P P R O A C H

3

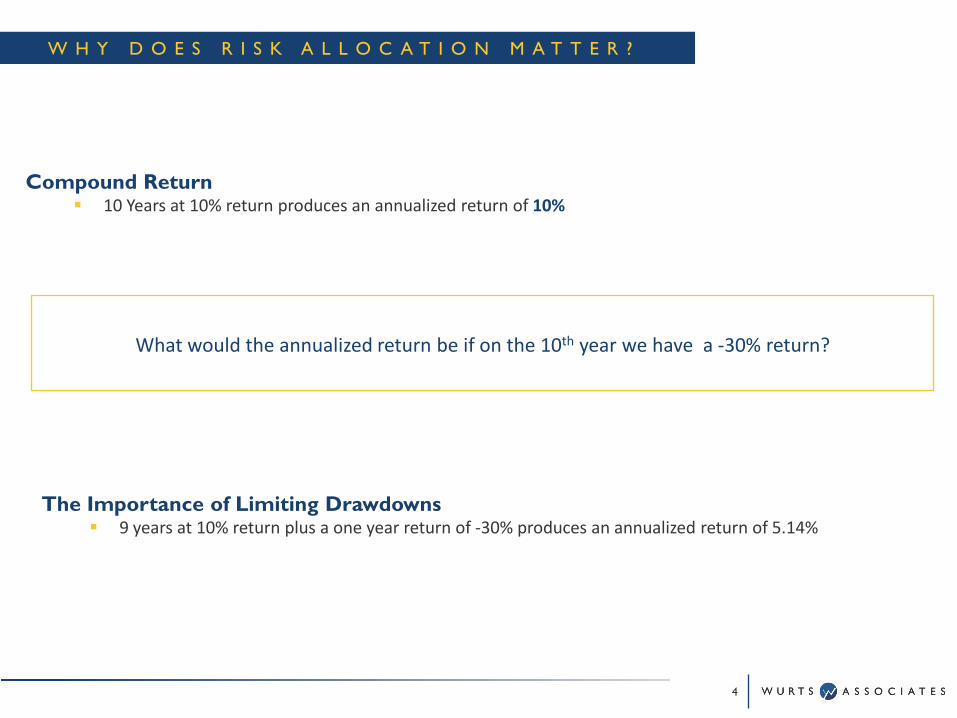

Compound Return 10 Years at 10% return produces an annualized return of 10%

What would the annualized return be if on the 10th year we have a -30% return?

The Importance of Limiting Drawdowns 9 years at 10% return plus a one year return of -30% produces an annualized return of 5.14%

4

W H Y D O E S R I S K A L L O C A T I O N M A T T E R ?

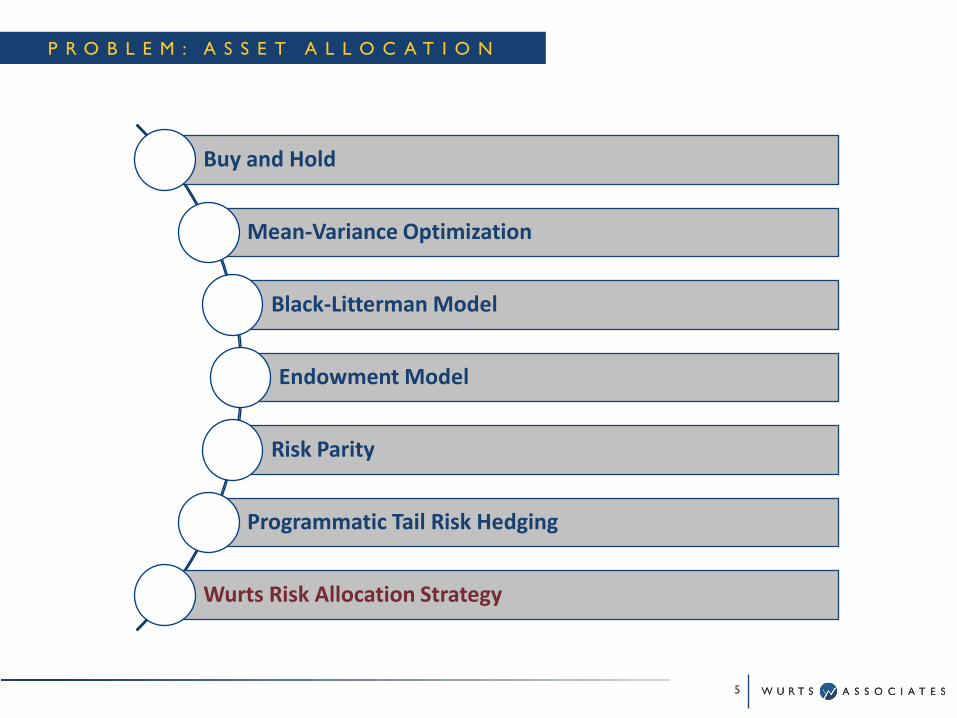

P R O B L E M : A S S E T A L L O C A T I O N

Buy and Hold

Mean-Variance Optimization

Black-Litterman Model

Endowment Model

Risk Parity

Programmatic Tail Risk Hedging

Wurts Risk Allocation Strategy

5

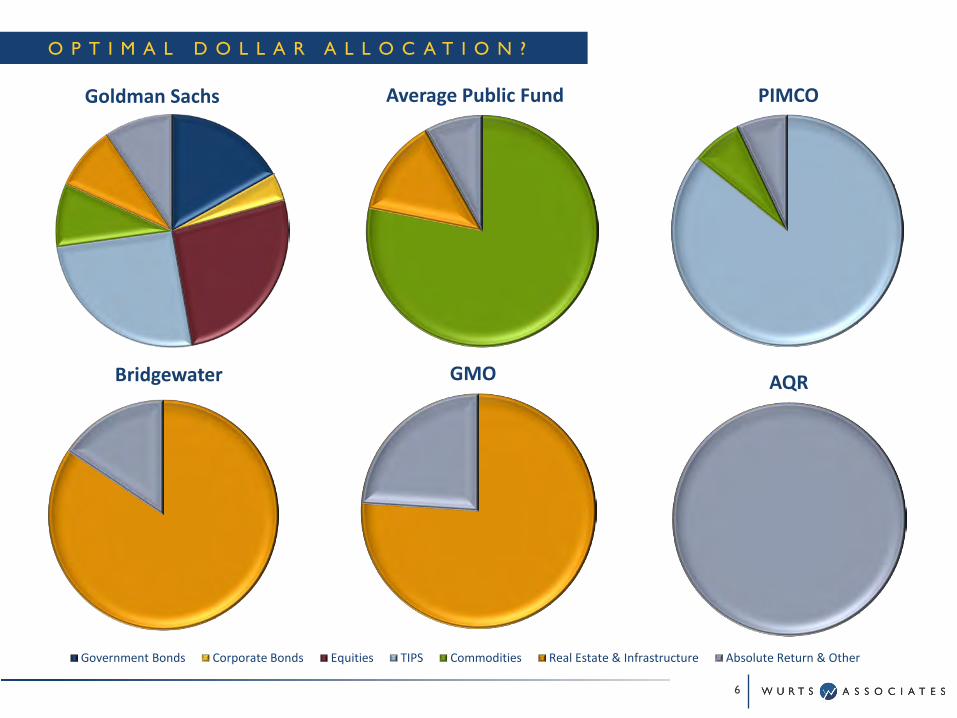

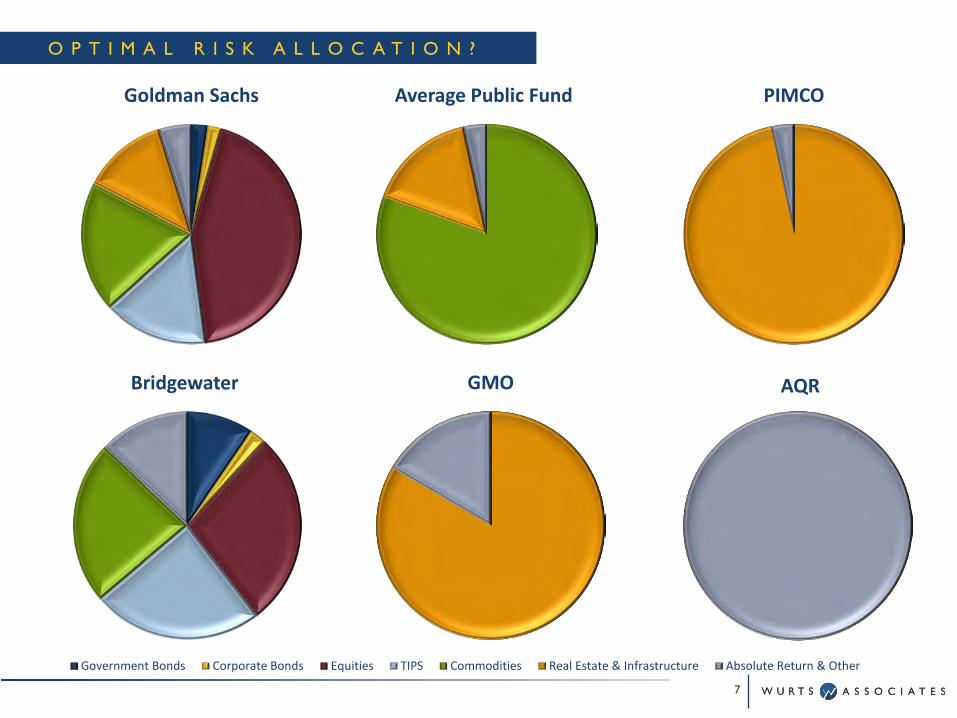

Government Bonds Corporate Bonds Equities TIPS Commodities Real Estate & Infrastructure Absolute Return & Other

O P T I M A L D O L L A R A L L O C A T I O N ?

Average Public Fund

Bridgewater GMO AQR

PIMCOGoldman Sachs

6

Government Bonds Corporate Bonds Equities TIPS Commodities Real Estate & Infrastructure Absolute Return & Other

Average Public FundGoldman Sachs PIMCO

Bridgewater AQRGMO

O P T I M A L R I S K A L L O C A T I O N ?

7

I N V E S T M E N T P R I N C I P L E S

Principles

Valuation

Risk

Diversification

8

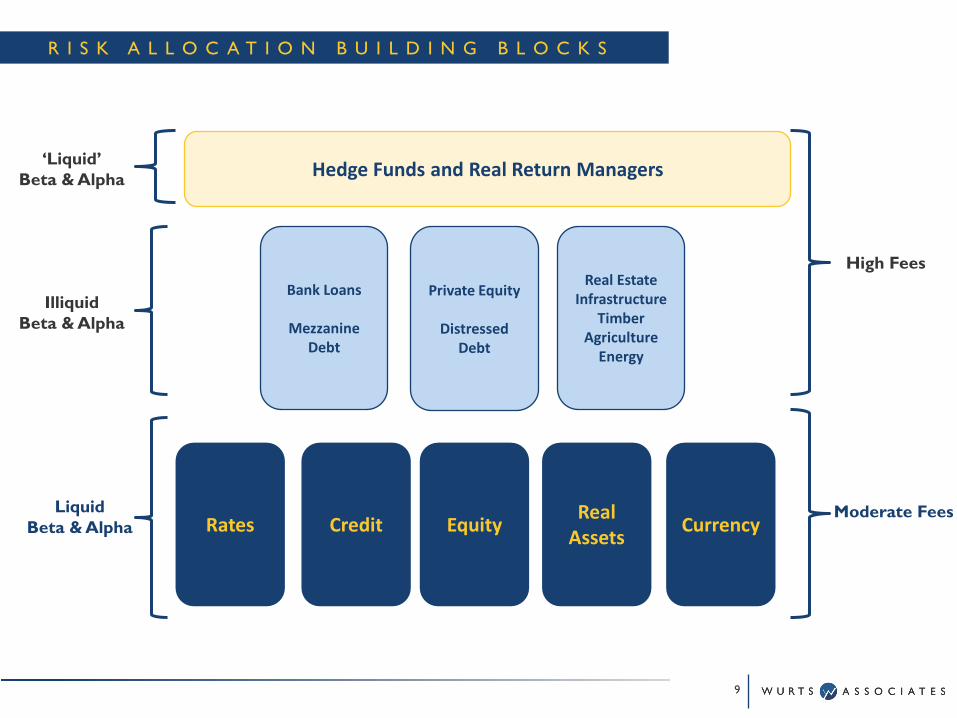

R I S K A L L O C A T I O N B U I L D I N G B L O C K S

‘Liquid’Beta & Alpha

Illiquid Beta & Alpha

Liquid Beta & Alpha

High Fees

Moderate Fees

Hedge Funds and Real Return Managers

Real EstateInfrastructure

TimberAgriculture

Energy

Private Equity

Distressed Debt

Bank Loans

Mezzanine Debt

Rates Credit EquityReal

AssetsCurrency

9

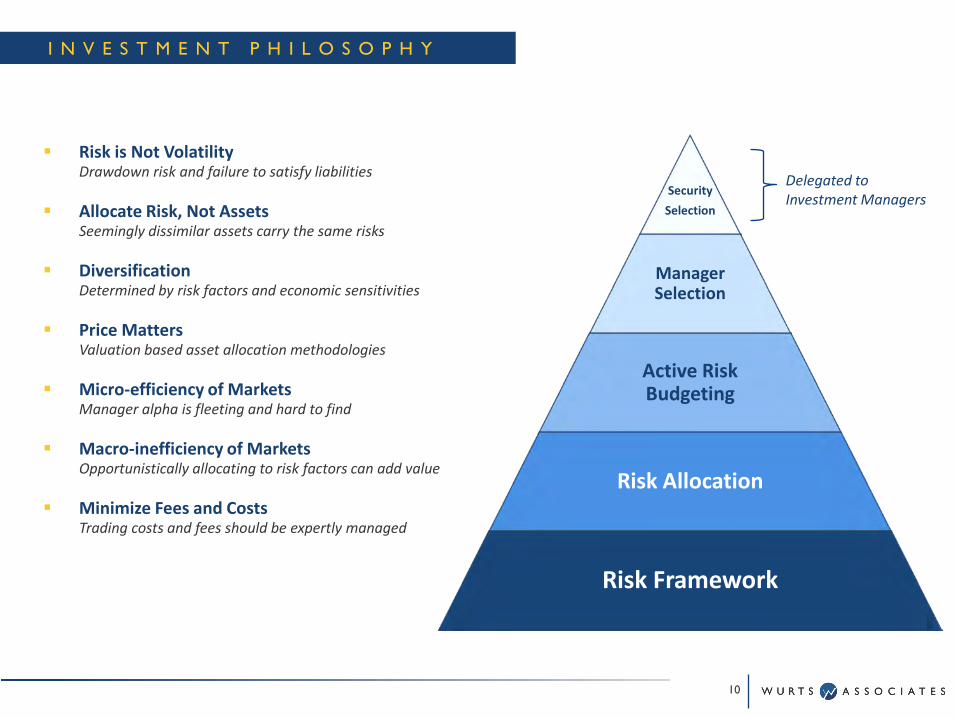

Security

Selection

Manager Selection

Active Risk Budgeting

Risk Allocation

Risk Framework

I N V E S T M E N T P H I L O S O P H Y

Risk is Not VolatilityDrawdown risk and failure to satisfy liabilities

Allocate Risk, Not AssetsSeemingly dissimilar assets carry the same risks

DiversificationDetermined by risk factors and economic sensitivities

Price MattersValuation based asset allocation methodologies

Micro-efficiency of Markets Manager alpha is fleeting and hard to find

Macro-inefficiency of Markets Opportunistically allocating to risk factors can add value

Minimize Fees and CostsTrading costs and fees should be expertly managed

Delegated to Investment Managers

10

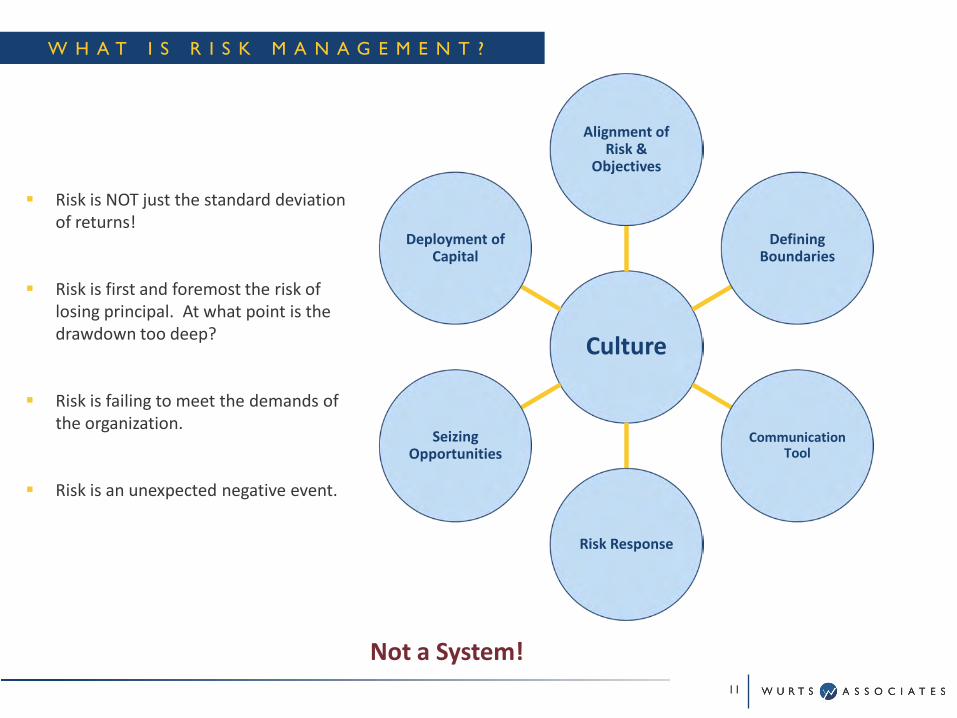

W H A T I S R I S K M A N A G E M E N T ?

Culture

Alignment of Risk &

Objectives

Defining Boundaries

Communication Tool

Risk Response

Seizing Opportunities

Deployment of Capital

Not a System!

Risk is NOT just the standard deviation of returns!

Risk is first and foremost the risk of losing principal. At what point is the drawdown too deep?

Risk is failing to meet the demands of the organization.

Risk is an unexpected negative event.

11

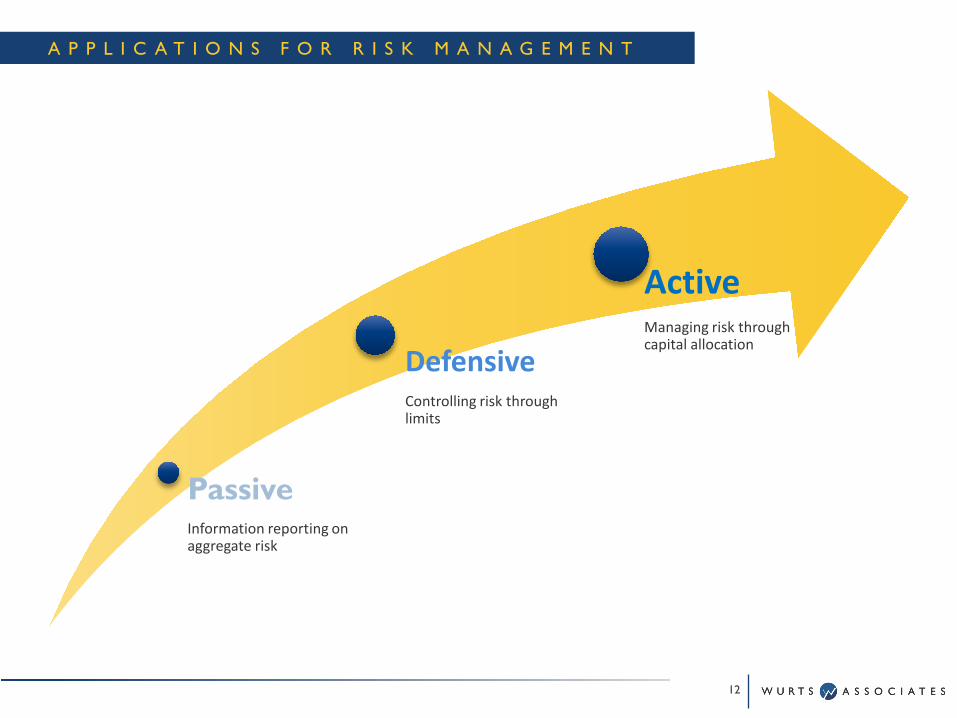

A P P L I C A T I O N S F O R R I S K M A N A G E M E N T

PassiveInformation reporting on aggregate risk

DefensiveControlling risk through limits

ActiveManaging risk through capital allocation

12

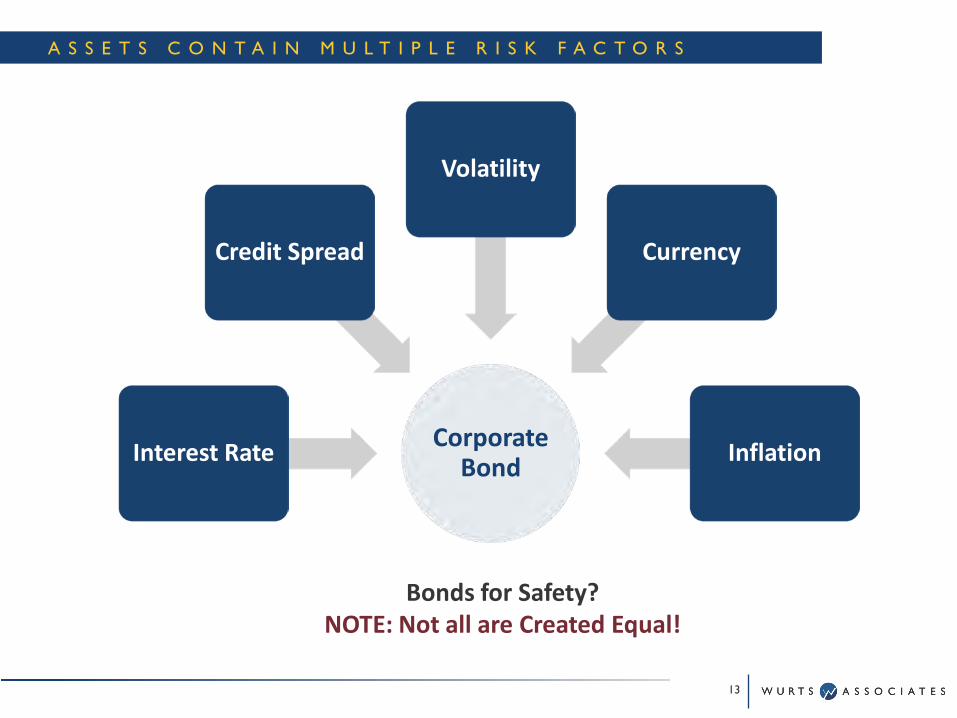

A S S E T S C O N T A I N M U L T I P L E R I S K F A C T O R S

Corporate BondInterest Rate

Credit Spread

Volatility

Currency

Inflation

Bonds for Safety?NOTE: Not all are Created Equal!

13

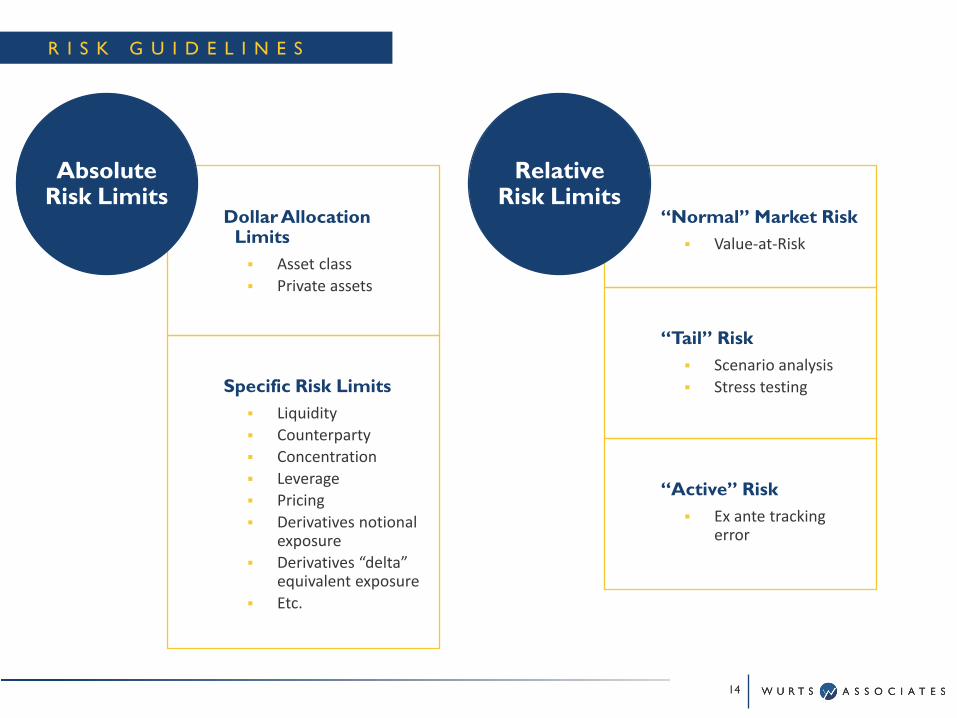

R I S K G U I D E L I N E S

Dollar Allocation Limits Asset class Private assets

Specific Risk Limits Liquidity Counterparty Concentration Leverage Pricing Derivatives notional

exposure Derivatives “delta”

equivalent exposure Etc.

Absolute Risk Limits

“Normal” Market Risk Value-at-Risk

“Tail” Risk Scenario analysis Stress testing

“Active” Risk Ex ante tracking

error

Relative Risk Limits

14

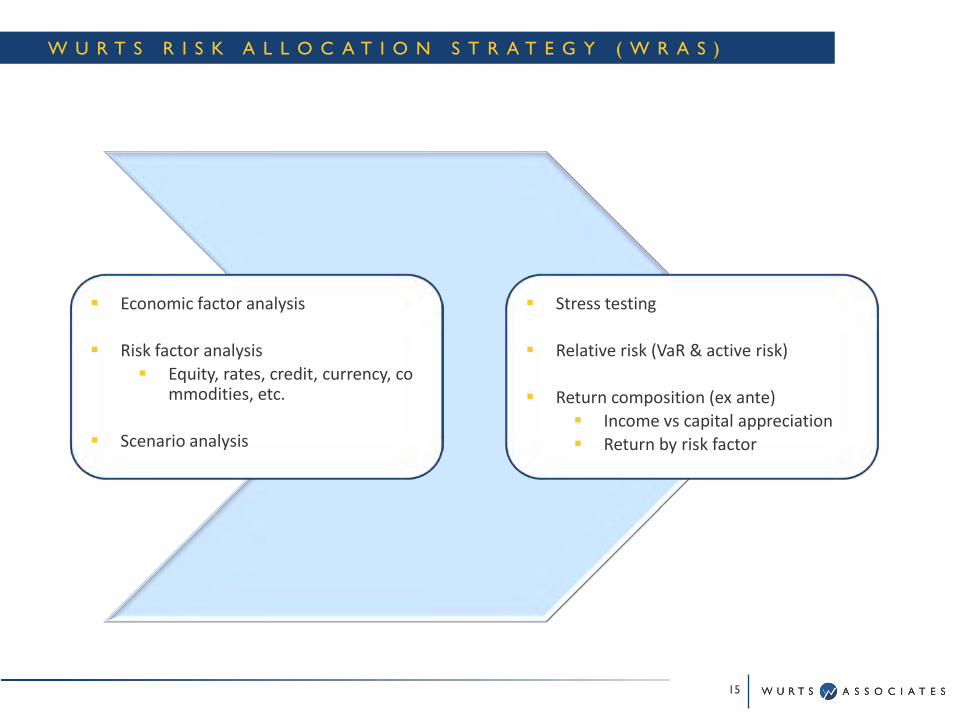

W U R T S R I S K A L L O C A T I O N S T R A T E G Y ( W R A S )

15

Economic factor analysis

Risk factor analysis Equity, rates, credit, currency, co

mmodities, etc.

Scenario analysis

Stress testing

Relative risk (VaR & active risk)

Return composition (ex ante) Income vs capital appreciation Return by risk factor

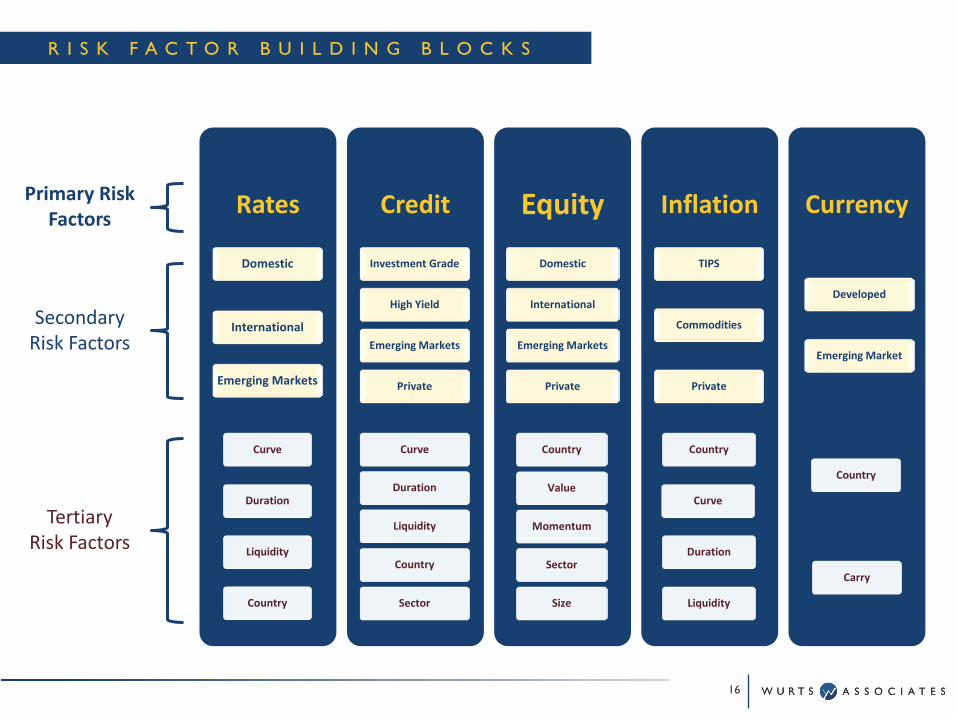

Rates

Domestic

International

Emerging Markets

Curve

Duration

Liquidity

Country

Credit

Investment Grade

High Yield

Emerging Markets

Private

Curve

Duration

Liquidity

Country

Sector

Equity

Domestic

International

Emerging Markets

Private

Country

Value

Momentum

Sector

Size

Inflation

TIPS

Commodities

Private

Country

Curve

Duration

Liquidity

Currency

Developed

Emerging Market

Country

Carry

Primary Risk Factors

Secondary Risk Factors

TertiaryRisk Factors

R I S K F A C T O R B U I L D I N G B L O C K S

16

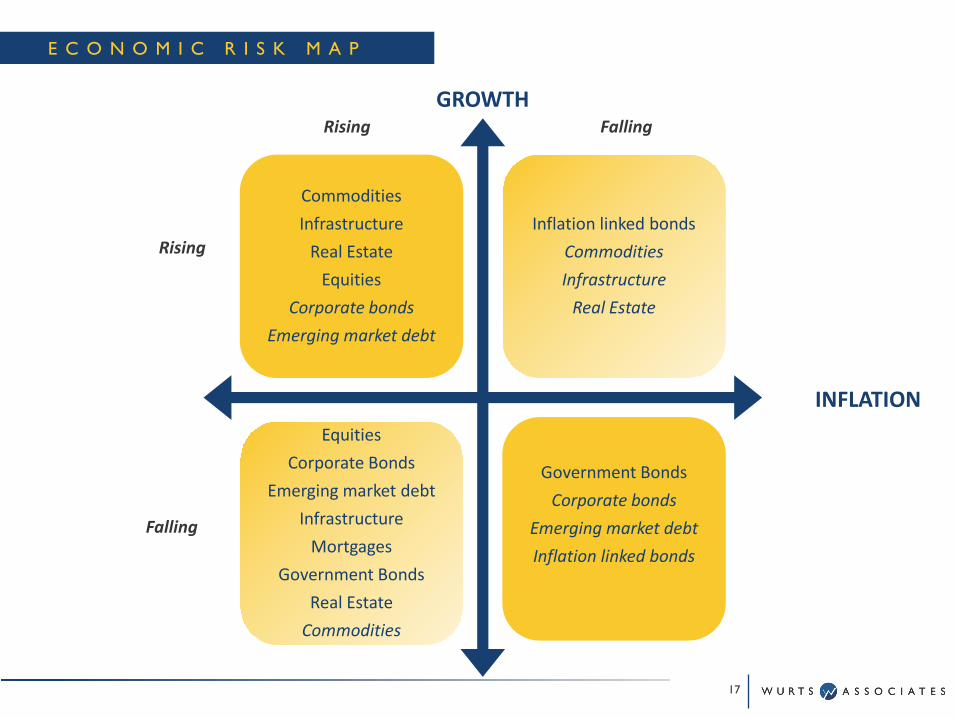

Commodities

Infrastructure

Real Estate

Equities

Corporate bonds

Emerging market debt

Inflation linked bonds

Commodities

Infrastructure

Real Estate

Equities

Corporate Bonds

Emerging market debt

Infrastructure

Mortgages

Government Bonds

Real Estate

Commodities

Government Bonds

Corporate bonds

Emerging market debt

Inflation linked bonds

GROWTHRising Falling

INFLATION

Rising

Falling

E C O N O M I C R I S K M A P

17

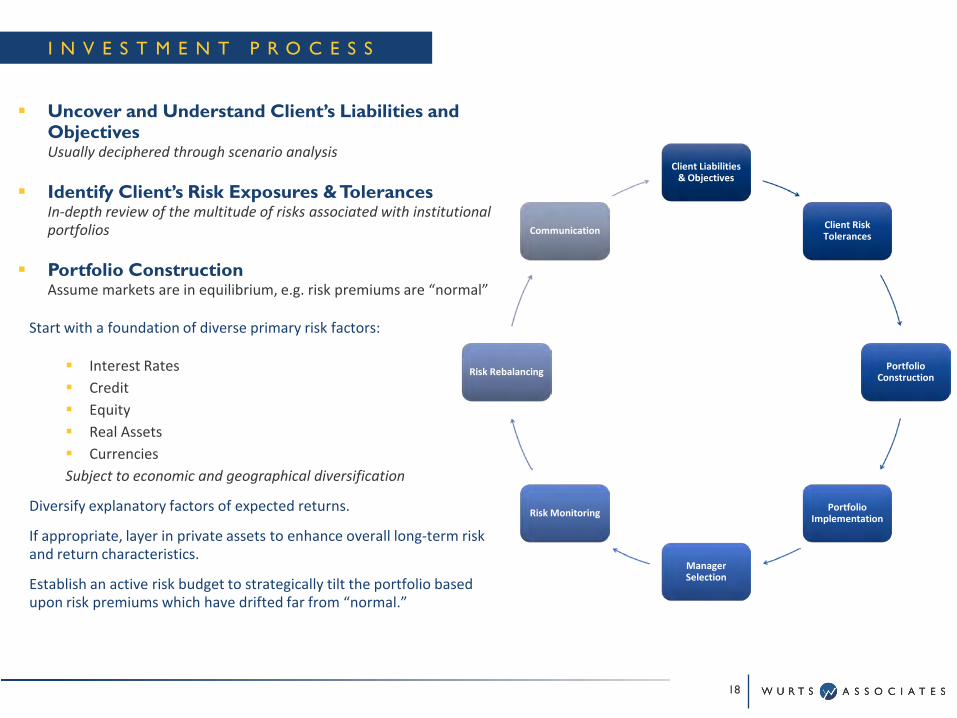

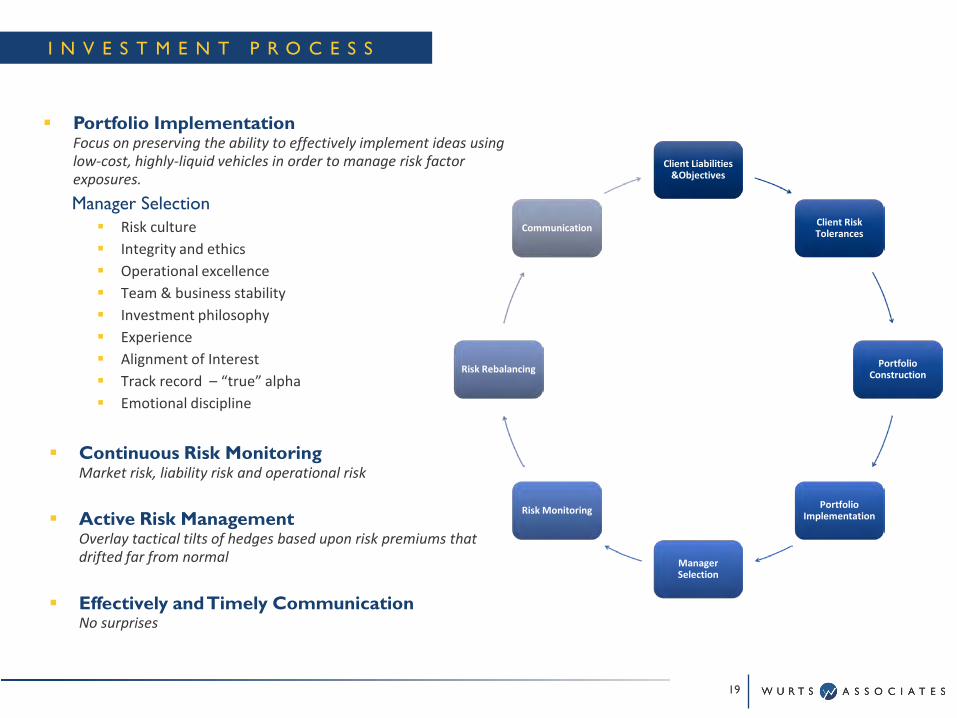

I N V E S T M E N T P R O C E S S

Uncover and Understand Client’s Liabilities and Objectives Usually deciphered through scenario analysis

Identify Client’s Risk Exposures & TolerancesIn-depth review of the multitude of risks associated with institutional portfolios

Portfolio ConstructionAssume markets are in equilibrium, e.g. risk premiums are “normal”

Start with a foundation of diverse primary risk factors:

Interest Rates Credit Equity Real Assets CurrenciesSubject to economic and geographical diversification

Diversify explanatory factors of expected returns.

If appropriate, layer in private assets to enhance overall long-term risk and return characteristics.

Establish an active risk budget to strategically tilt the portfolio based upon risk premiums which have drifted far from “normal.”

Client Liabilities & Objectives

Client Risk Tolerances

Portfolio Construction

Portfolio Implementation

Manager Selection

Risk Monitoring

Risk Rebalancing

Communication

18

I N V E S T M E N T P R O C E S S

Portfolio ImplementationFocus on preserving the ability to effectively implement ideas using low-cost, highly-liquid vehicles in order to manage risk factor exposures.

Manager Selection Risk culture Integrity and ethics Operational excellence Team & business stability Investment philosophy Experience Alignment of Interest Track record – “true” alpha Emotional discipline

Continuous Risk Monitoring Market risk, liability risk and operational risk

Active Risk ManagementOverlay tactical tilts of hedges based upon risk premiums that drifted far from normal

Effectively and Timely Communication No surprises

Client Liabilities &Objectives

Client Risk Tolerances

Portfolio Construction

Portfolio Implementation

Manager Selection

Risk Monitoring

Risk Rebalancing

Communication

19

S A M P L E R I S K D A S H B O A R D

20

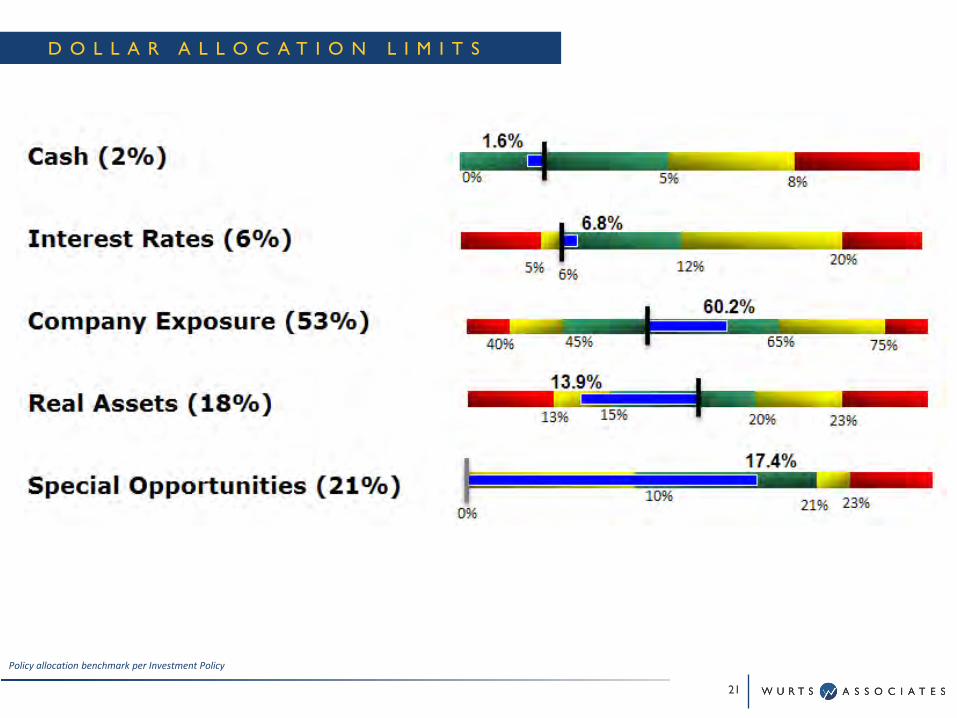

Policy allocation benchmark per Investment Policy

D O L L A R A L L O C A T I O N L I M I T S

21

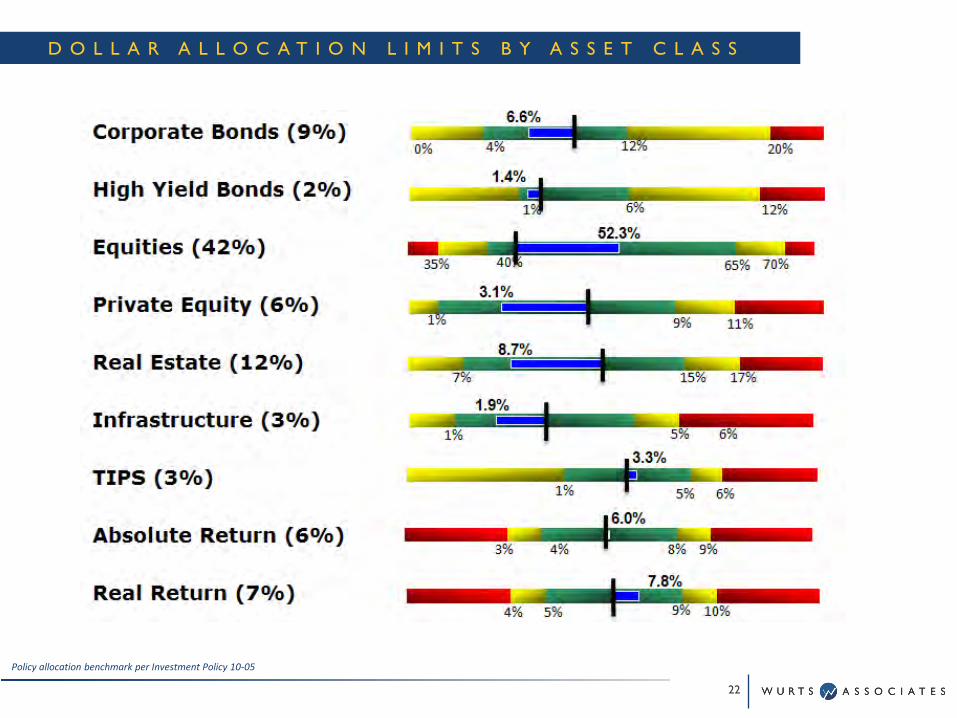

Policy allocation benchmark per Investment Policy 10-05

D O L L A R A L L O C A T I O N L I M I T S B Y A S S E T C L A S S

22

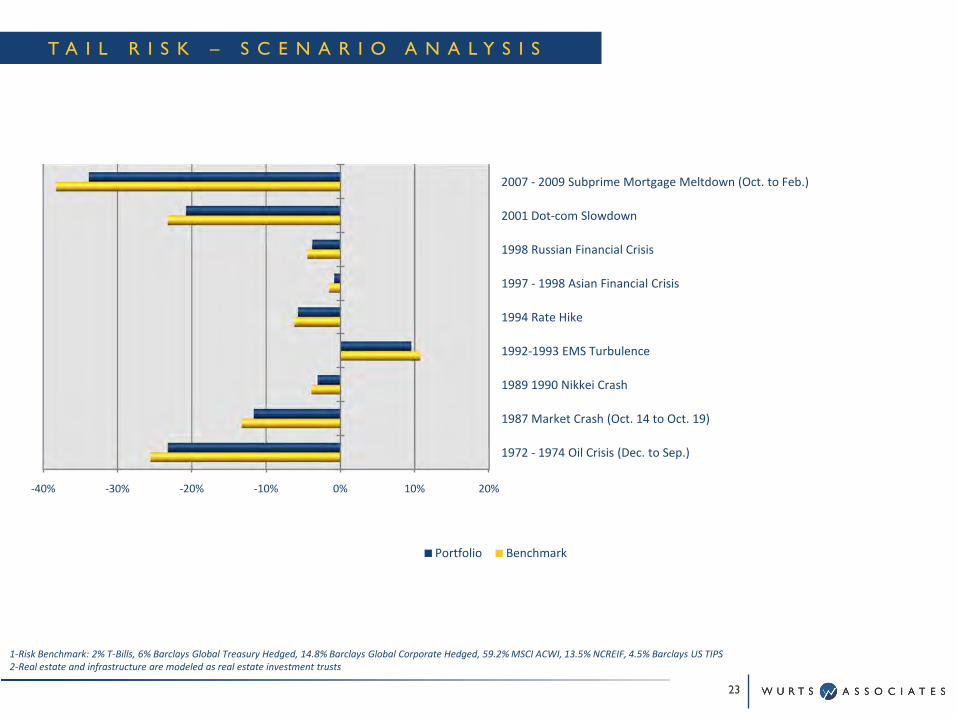

1-Risk Benchmark: 2% T-Bills, 6% Barclays Global Treasury Hedged, 14.8% Barclays Global Corporate Hedged, 59.2% MSCI ACWI, 13.5% NCREIF, 4.5% Barclays US TIPS2-Real estate and infrastructure are modeled as real estate investment trusts

-40% -30% -20% -10% 0% 10% 20%

1972 - 1974 Oil Crisis (Dec. to Sep.)

1987 Market Crash (Oct. 14 to Oct. 19)

1989 1990 Nikkei Crash

1992-1993 EMS Turbulence

1994 Rate Hike

1997 - 1998 Asian Financial Crisis

1998 Russian Financial Crisis

2001 Dot-com Slowdown

2007 - 2009 Subprime Mortgage Meltdown (Oct. to Feb.)

Portfolio Benchmark

T A I L R I S K – S C E N A R I O A N A L Y S I S

23

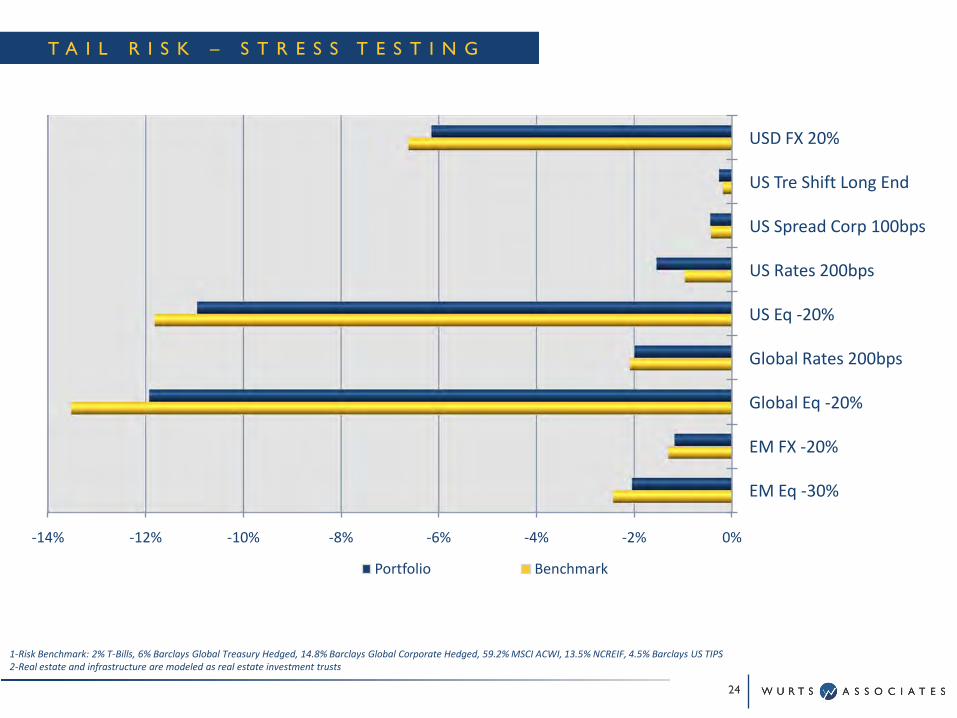

1-Risk Benchmark: 2% T-Bills, 6% Barclays Global Treasury Hedged, 14.8% Barclays Global Corporate Hedged, 59.2% MSCI ACWI, 13.5% NCREIF, 4.5% Barclays US TIPS2-Real estate and infrastructure are modeled as real estate investment trusts

-14% -12% -10% -8% -6% -4% -2% 0%

EM Eq -30%

EM FX -20%

Global Eq -20%

Global Rates 200bps

US Eq -20%

US Rates 200bps

US Spread Corp 100bps

US Tre Shift Long End

USD FX 20%

Portfolio Benchmark

T A I L R I S K – S T R E S S T E S T I N G

24

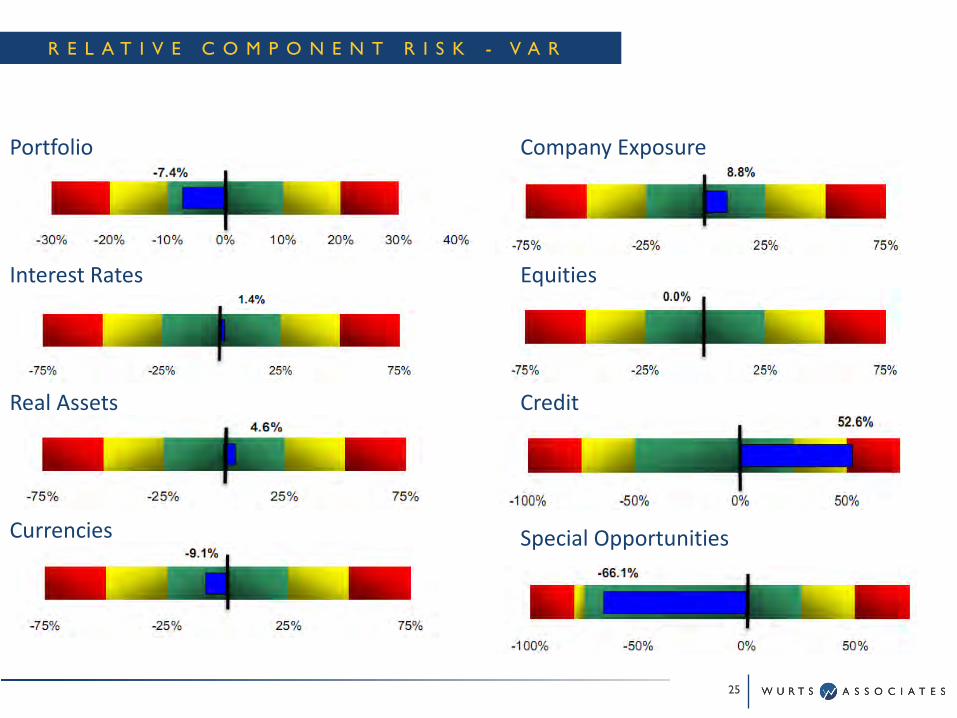

Portfolio

Real Assets

Currencies Special Opportunities

EquitiesInterest Rates

Credit

Company Exposure

R E L A T I V E C O M P O N E N T R I S K - V A R

25

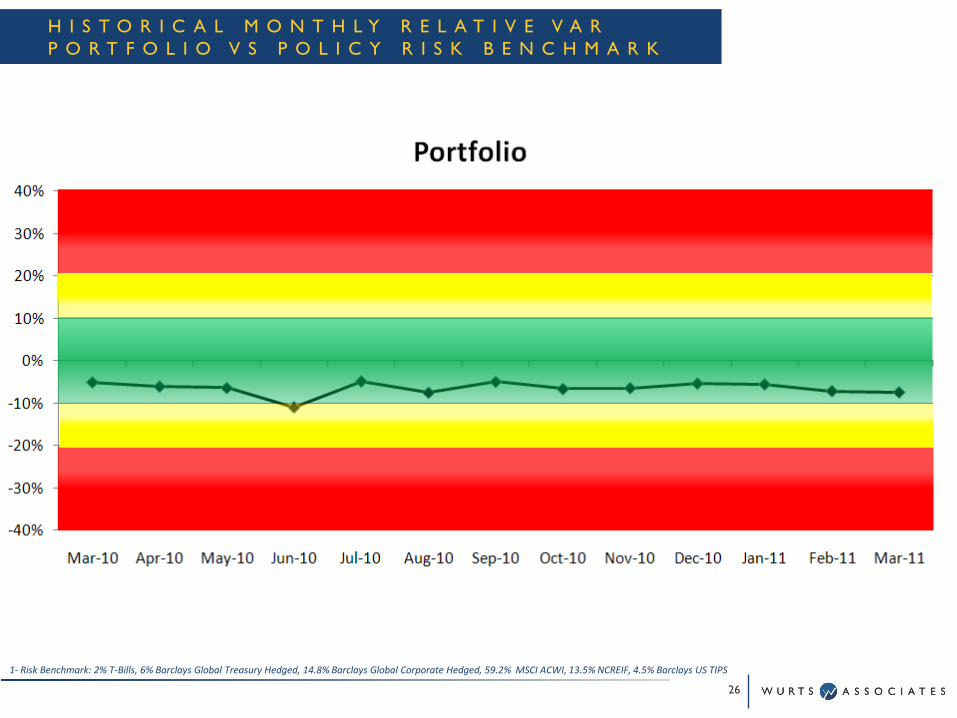

1- Risk Benchmark: 2% T-Bills, 6% Barclays Global Treasury Hedged, 14.8% Barclays Global Corporate Hedged, 59.2% MSCI ACWI, 13.5% NCREIF, 4.5% Barclays US TIPS

H I S T O R I C A L M O N T H L Y R E L A T I V E V A RP O R T F O L I O V S P O L I C Y R I S K B E N C H M A R K

26

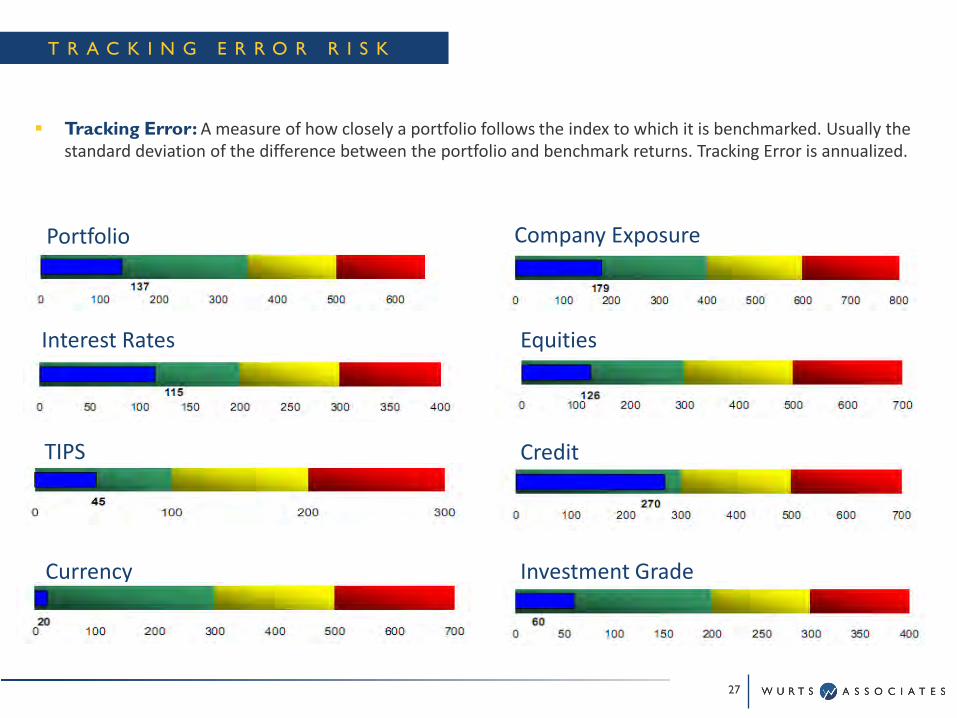

Portfolio

Interest Rates

Company Exposure

TIPS Credit

Investment Grade

Equities

Currency

Tracking Error: A measure of how closely a portfolio follows the index to which it is benchmarked. Usually the standard deviation of the difference between the portfolio and benchmark returns. Tracking Error is annualized.

T R A C K I N G E R R O R R I S K

27

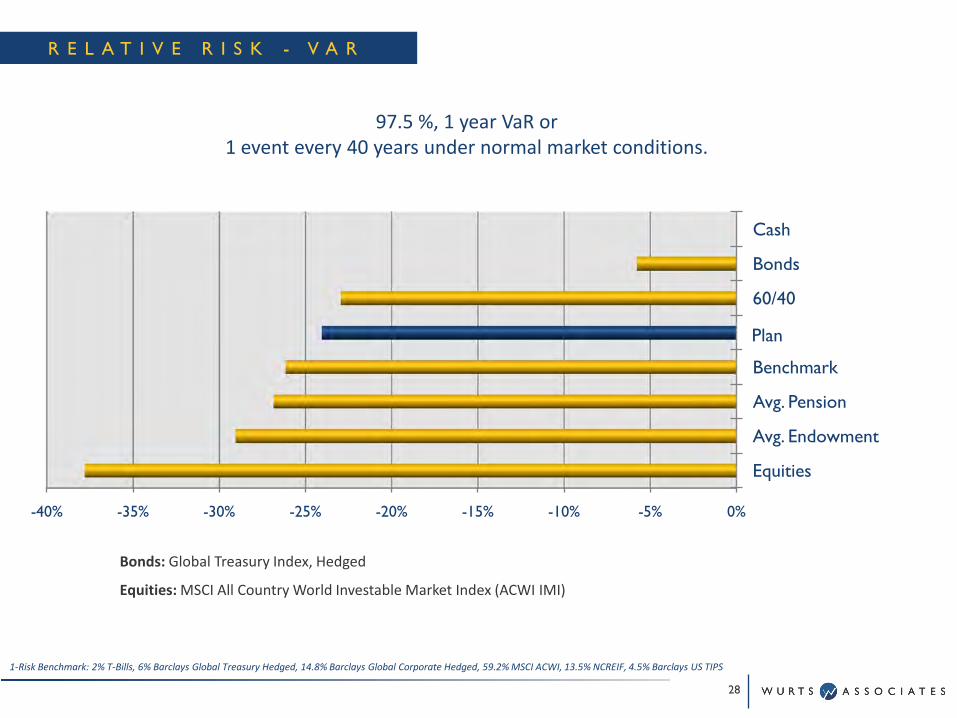

-40% -35% -30% -25% -20% -15% -10% -5% 0%

Equities

Avg. Endowment

Avg. Pension

Benchmark

APFC

60/40

Bonds

Cash

97.5 %, 1 year VaR or 1 event every 40 years under normal market conditions.

Bonds: Global Treasury Index, Hedged

Equities: MSCI All Country World Investable Market Index (ACWI IMI)

1-Risk Benchmark: 2% T-Bills, 6% Barclays Global Treasury Hedged, 14.8% Barclays Global Corporate Hedged, 59.2% MSCI ACWI, 13.5% NCREIF, 4.5% Barclays US TIPS

Plan

R E L A T I V E R I S K - V A R

28

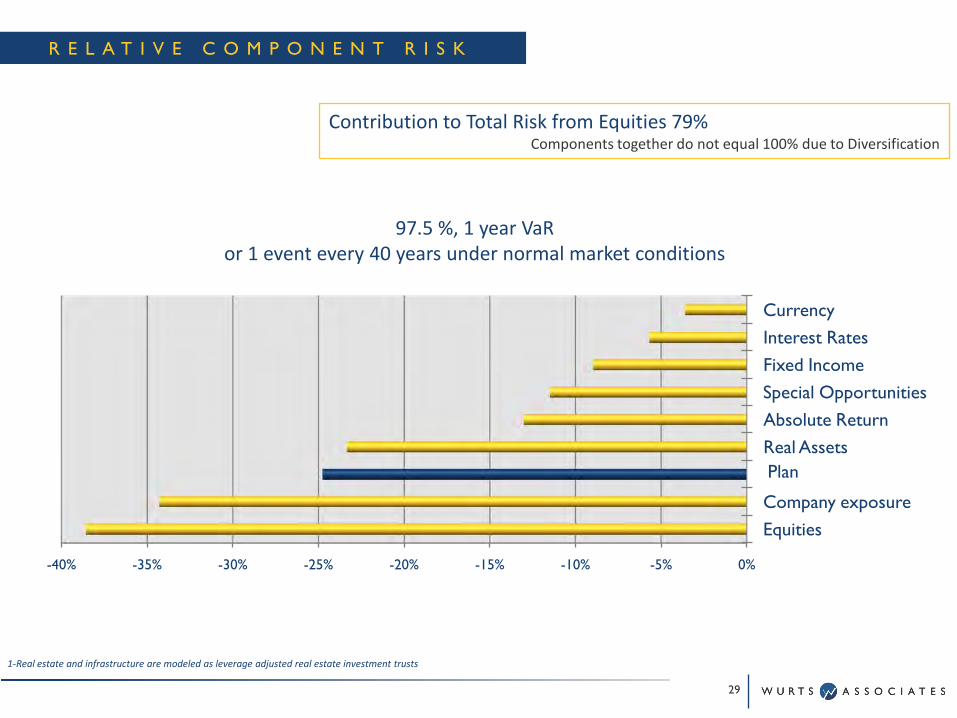

-40% -35% -30% -25% -20% -15% -10% -5% 0%

EquitiesCompany exposureAPFCReal AssetsAbsolute ReturnSpecial OpportunitiesFixed IncomeInterest RatesCurrency

97.5 %, 1 year VaR or 1 event every 40 years under normal market conditions

Contribution to Total Risk from Equities 79%Components together do not equal 100% due to Diversification

1-Real estate and infrastructure are modeled as leverage adjusted real estate investment trusts

R E L A T I V E C O M P O N E N T R I S K

29

Plan

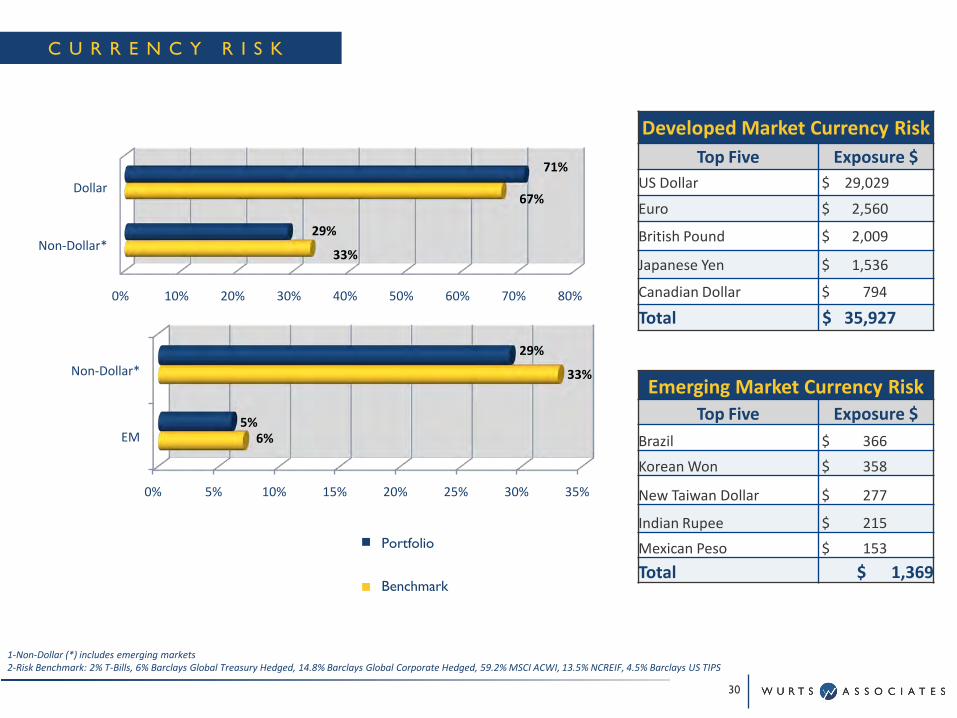

Emerging Market Currency RiskTop Five Exposure $

Brazil $ 366

Korean Won $ 358

New Taiwan Dollar $ 277

Indian Rupee $ 215

Mexican Peso $ 153

Total $ 1,369

Developed Market Currency RiskTop Five Exposure $

US Dollar $ 29,029

Euro $ 2,560

British Pound $ 2,009

Japanese Yen $ 1,536

Canadian Dollar $ 794

Total $ 35,927

1-Non-Dollar (*) includes emerging markets2-Risk Benchmark: 2% T-Bills, 6% Barclays Global Treasury Hedged, 14.8% Barclays Global Corporate Hedged, 59.2% MSCI ACWI, 13.5% NCREIF, 4.5% Barclays US TIPS

0% 10% 20% 30% 40% 50% 60% 70% 80%

Non-Dollar*

Dollar

71%

67%

29%

33%

0% 5% 10% 15% 20% 25% 30% 35%

EM

Non-Dollar*

29%

33%

5%6%

C U R R E N C Y R I S K

30

Portfolio

Benchmark

0%

10%

20%

30%

40%

50%

60%

70%

North America

Europe Pacific EM Asia Other Latin America

EM Europe &

Middle East

DevelopingCountry Exposure $

China $ 491Korea $ 355 Taiwan $ 263 Brazil $ 248India $ 211 South Africa $ 133 Mexico $ 120Israel $ 110Indonesia $ 105Turkey $ 103 Total $ 2,140

1-Risk Benchmark: 2% T-Bills, 6% Barclays Global Treasury Hedged, 14.8% Barclays Global Corporate Hedged, 59.2% MSCI ACWI, 13.5% NCREIF, 4.5% Barclays US TIPS

C O U N T R Y R I S K

31

Portfolio

Benchmark

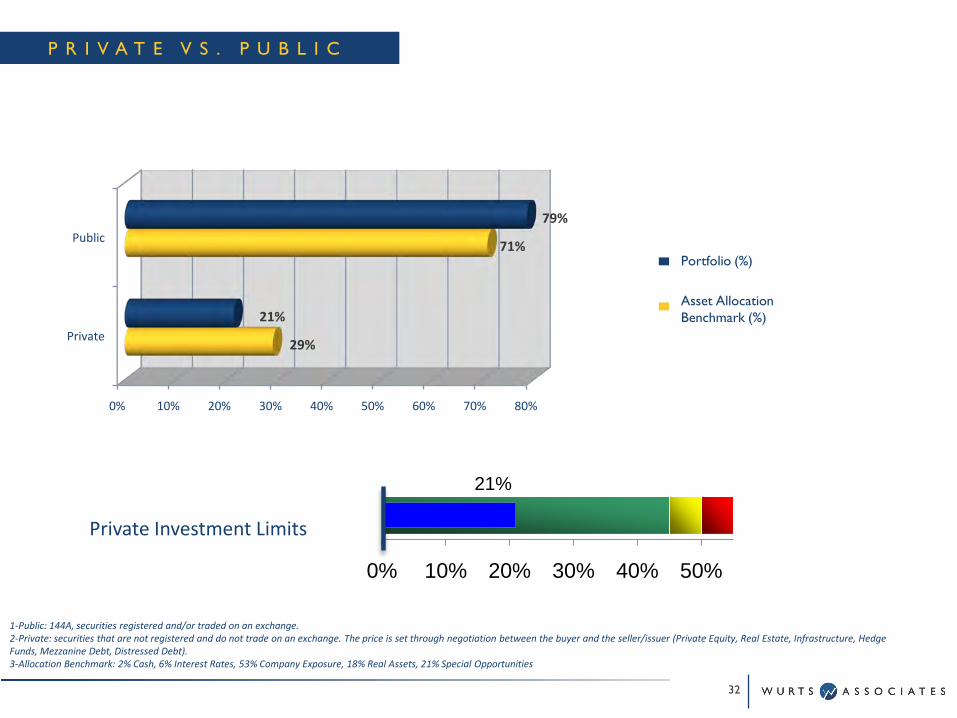

21%

0% 10% 20% 30% 40% 50%

Private Investment Limits

1-Public: 144A, securities registered and/or traded on an exchange.2-Private: securities that are not registered and do not trade on an exchange. The price is set through negotiation between the buyer and the seller/issuer (Private Equity, Real Estate, Infrastructure, Hedge Funds, Mezzanine Debt, Distressed Debt).3-Allocation Benchmark: 2% Cash, 6% Interest Rates, 53% Company Exposure, 18% Real Assets, 21% Special Opportunities

0% 10% 20% 30% 40% 50% 60% 70% 80%

Private

Public

29%

71%

21%

79%

P R I V A T E V S . P U B L I C

32

Portfolio (%)

Asset Allocation Benchmark (%)

8%

0% 10% 20% 30%

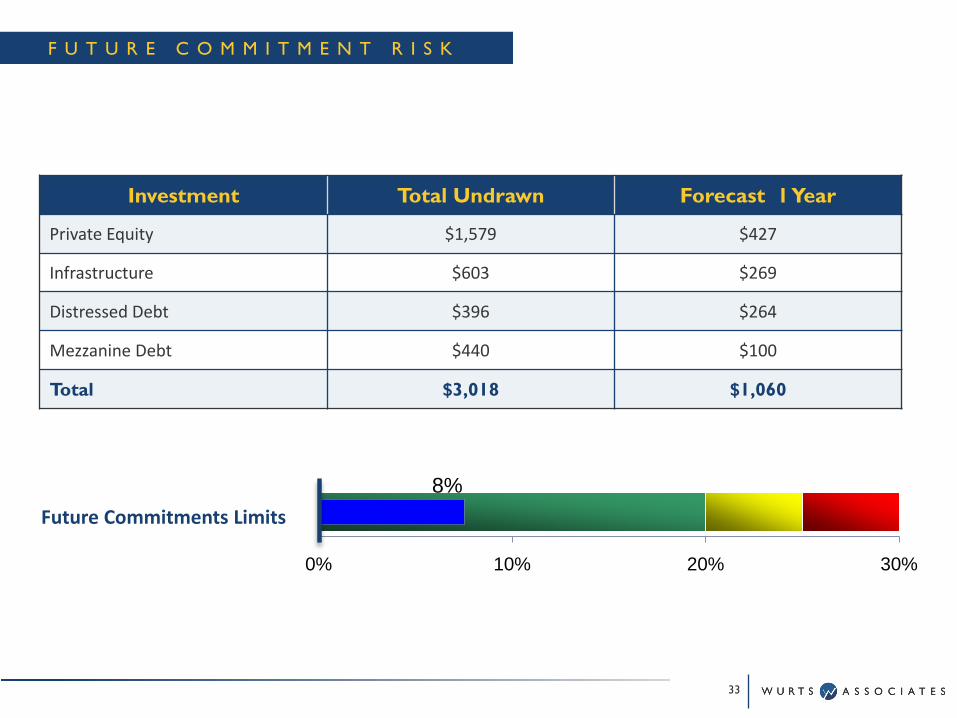

F U T U R E C O M M I T M E N T R I S K

Investment Total Undrawn Forecast 1 Year

Private Equity $1,579 $427

Infrastructure $603 $269

Distressed Debt $396 $264

Mezzanine Debt $440 $100

Total $3,018 $1,060

Future Commitments Limits

33

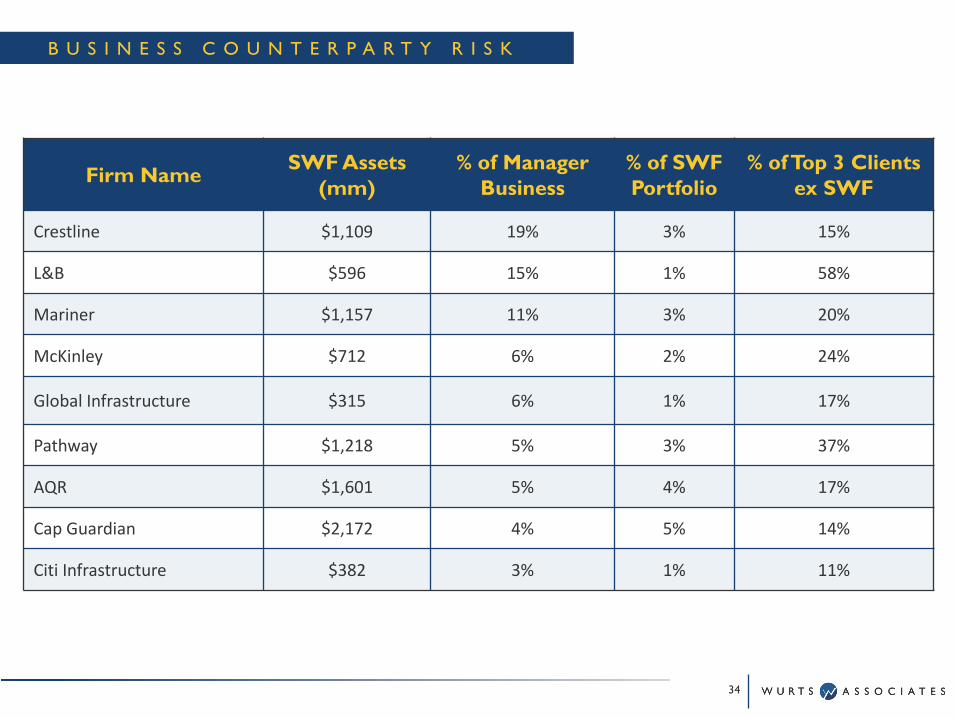

Firm Name SWF Assets (mm)

% of Manager Business

% of SWF Portfolio

% of Top 3 Clients ex SWF

Crestline $1,109 19% 3% 15%

L&B $596 15% 1% 58%

Mariner $1,157 11% 3% 20%

McKinley $712 6% 2% 24%

Global Infrastructure $315 6% 1% 17%

Pathway $1,218 5% 3% 37%

AQR $1,601 5% 4% 17%

Cap Guardian $2,172 4% 5% 14%

Citi Infrastructure $382 3% 1% 11%

B U S I N E S S C O U N T E R P A R T Y R I S K

34

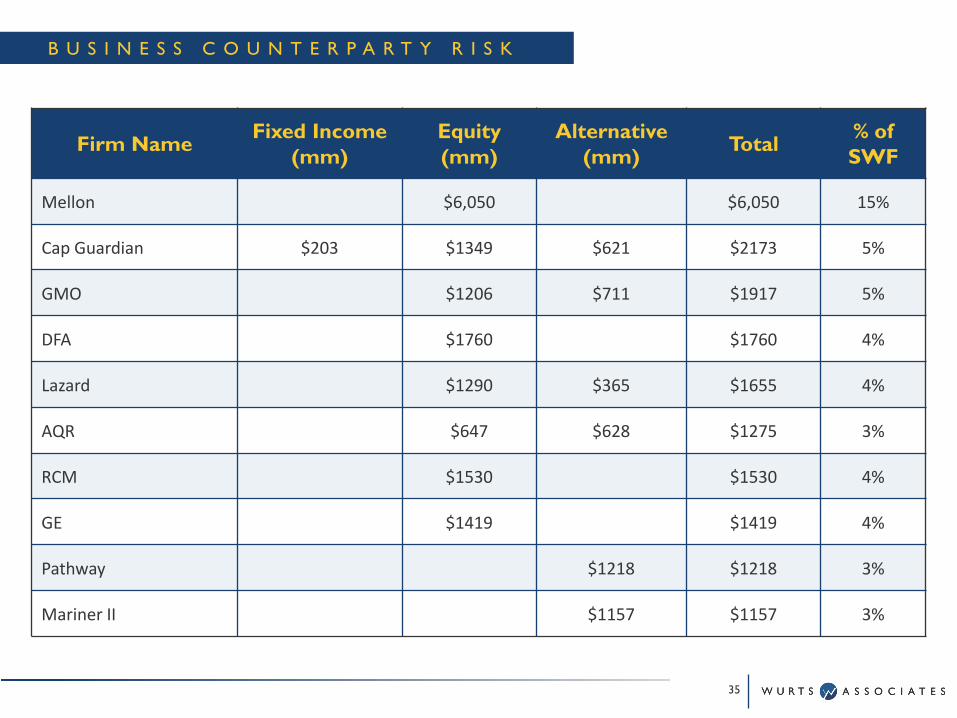

Firm Name Fixed Income(mm)

Equity (mm)

Alternative(mm) Total % of

SWF

Mellon $6,050 $6,050 15%

Cap Guardian $203 $1349 $621 $2173 5%

GMO $1206 $711 $1917 5%

DFA $1760 $1760 4%

Lazard $1290 $365 $1655 4%

AQR $647 $628 $1275 3%

RCM $1530 $1530 4%

GE $1419 $1419 4%

Pathway $1218 $1218 3%

Mariner II $1157 $1157 3%

B U S I N E S S C O U N T E R P A R T Y R I S K

35

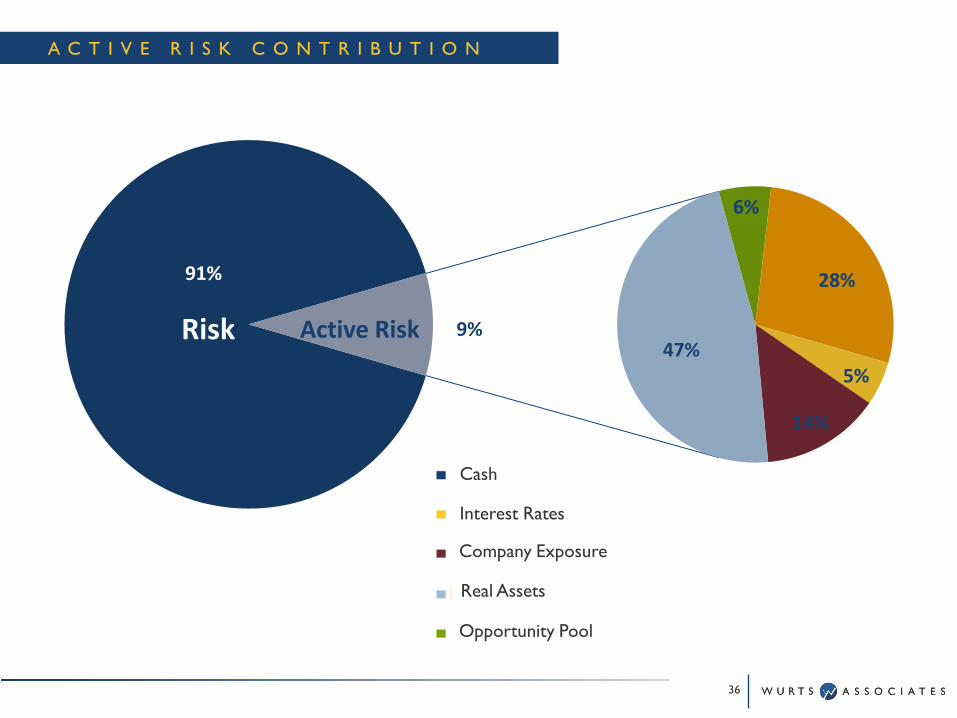

Risk5%

14%

47%

6%

28%

Active Risk 9%

91%

A C T I V E R I S K C O N T R I B U T I O N

36

Cash

Interest Rates

Company Exposure

Real Assets

Opportunity Pool

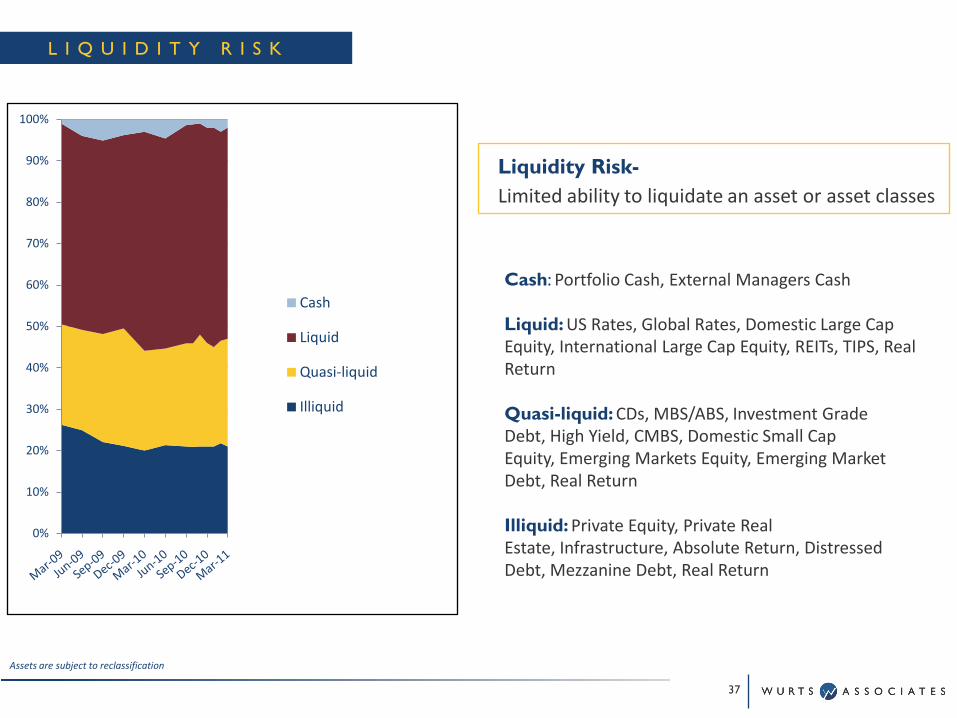

L I Q U I D I T Y R I S K

Liquidity Risk-Limited ability to liquidate an asset or asset classes

Cash: Portfolio Cash, External Managers Cash

Liquid: US Rates, Global Rates, Domestic Large Cap Equity, International Large Cap Equity, REITs, TIPS, Real Return

Quasi-liquid: CDs, MBS/ABS, Investment Grade Debt, High Yield, CMBS, Domestic Small Cap Equity, Emerging Markets Equity, Emerging Market Debt, Real Return

Illiquid: Private Equity, Private Real Estate, Infrastructure, Absolute Return, Distressed Debt, Mezzanine Debt, Real Return

Assets are subject to reclassification

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cash

Liquid

Quasi-liquid

Illiquid

37

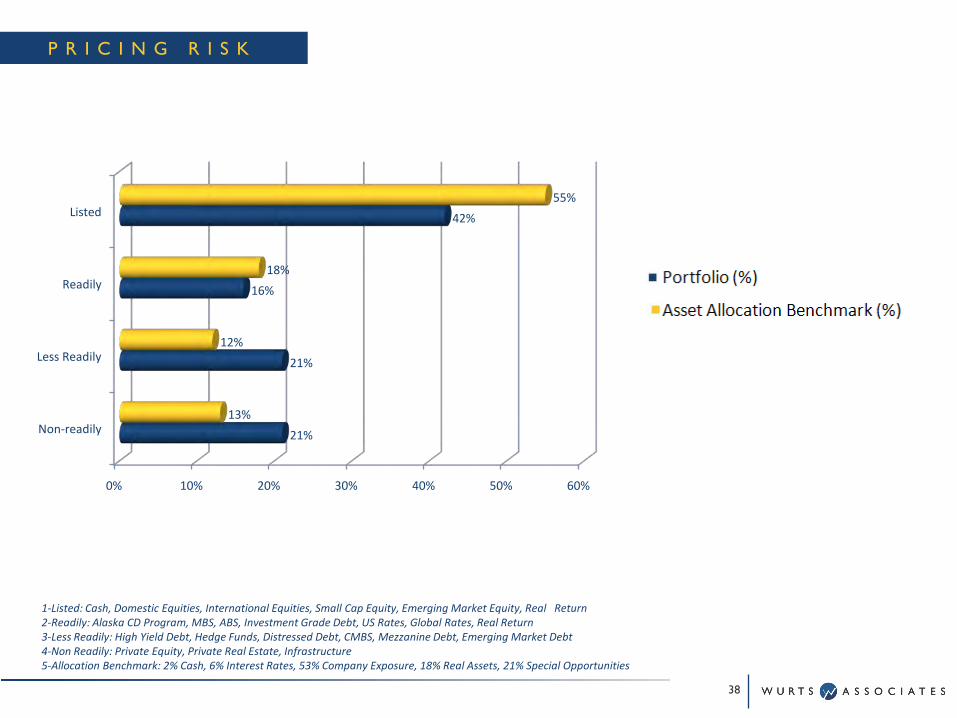

1-Listed: Cash, Domestic Equities, International Equities, Small Cap Equity, Emerging Market Equity, Real Return2-Readily: Alaska CD Program, MBS, ABS, Investment Grade Debt, US Rates, Global Rates, Real Return3-Less Readily: High Yield Debt, Hedge Funds, Distressed Debt, CMBS, Mezzanine Debt, Emerging Market Debt4-Non Readily: Private Equity, Private Real Estate, Infrastructure5-Allocation Benchmark: 2% Cash, 6% Interest Rates, 53% Company Exposure, 18% Real Assets, 21% Special Opportunities

0% 10% 20% 30% 40% 50% 60%

Non-readily

Less Readily

Readily

Listed

21%

21%

16%

42%

13%

12%

18%

55%

P R I C I N G R I S K

38

G O V E R N A N C E

39

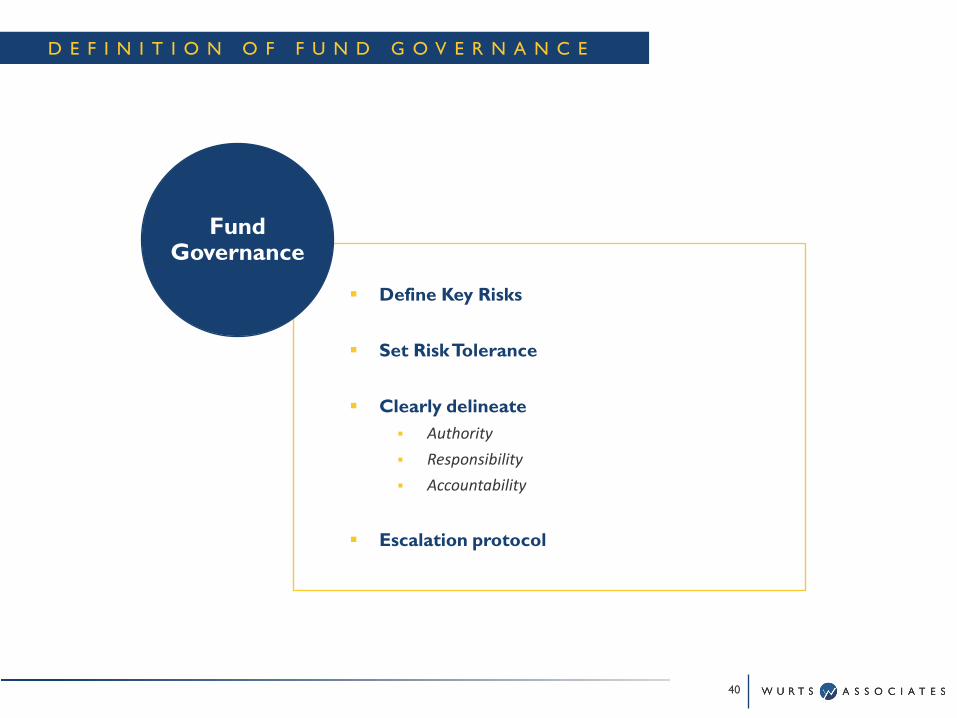

D E F I N I T I O N O F F U N D G O V E R N A N C E

40

Define Key Risks

Set Risk Tolerance

Clearly delineate Authority

Responsibility

Accountability

Escalation protocol

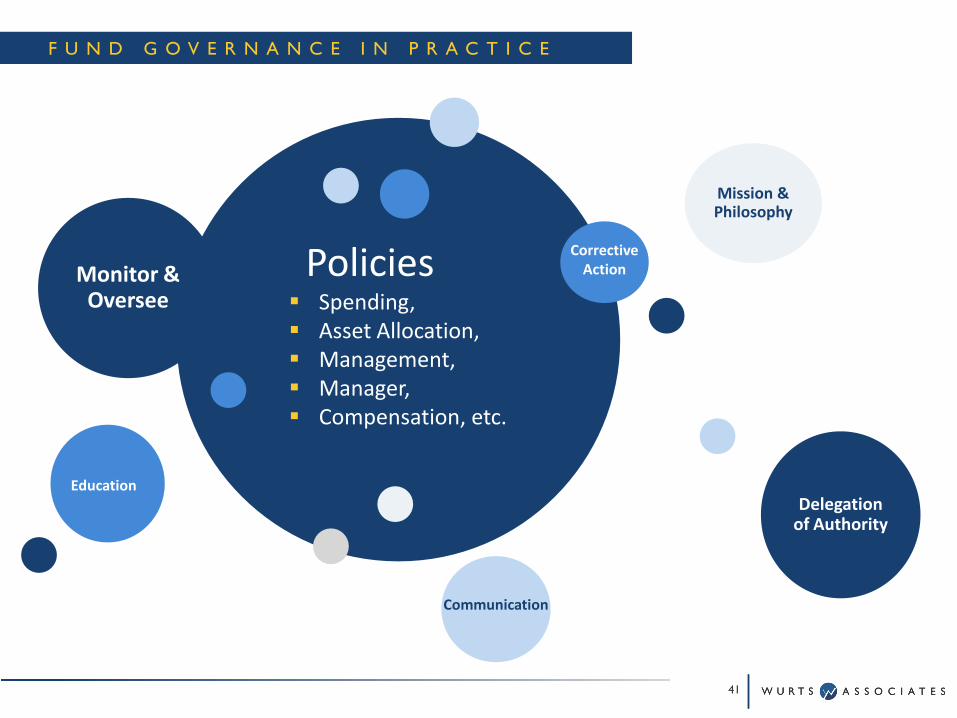

Fund Governance

Monitor & Oversee

Mission & Philosophy

Delegation of Authority

Policies Spending, Asset Allocation, Management, Manager, Compensation, etc.

Education

Communication

Corrective Action

F U N D G O V E R N A N C E I N P R A C T I C E

41

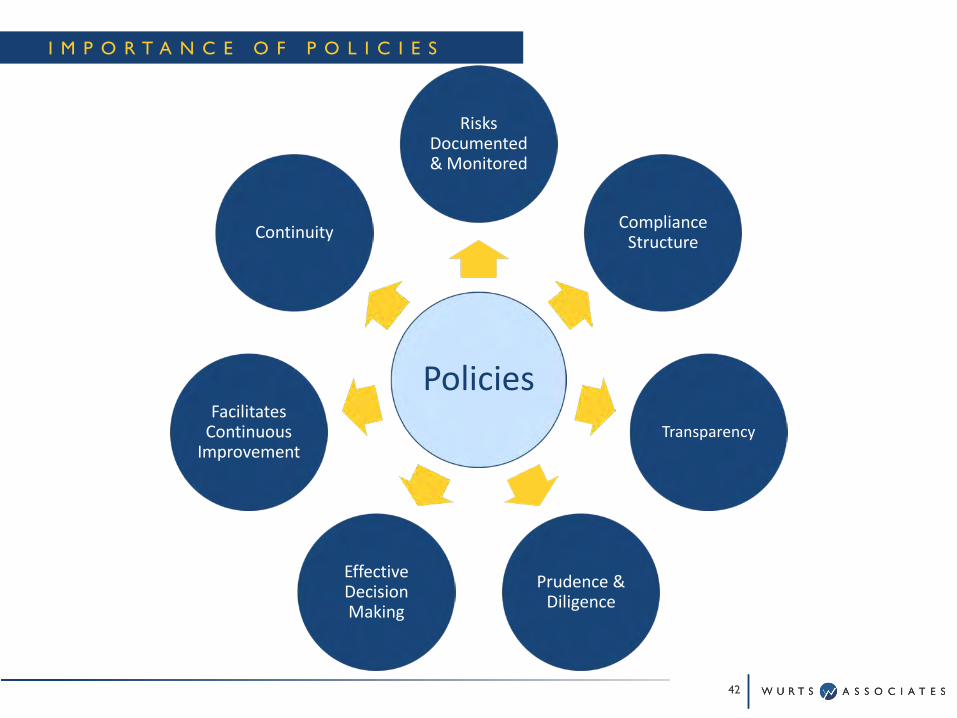

I M P O R T A N C E O F P O L I C I E S

Policies

Risks Documented & Monitored

Compliance Structure

Transparency

Prudence & Diligence

Effective Decision Making

Facilitates Continuous

Improvement

Continuity

42

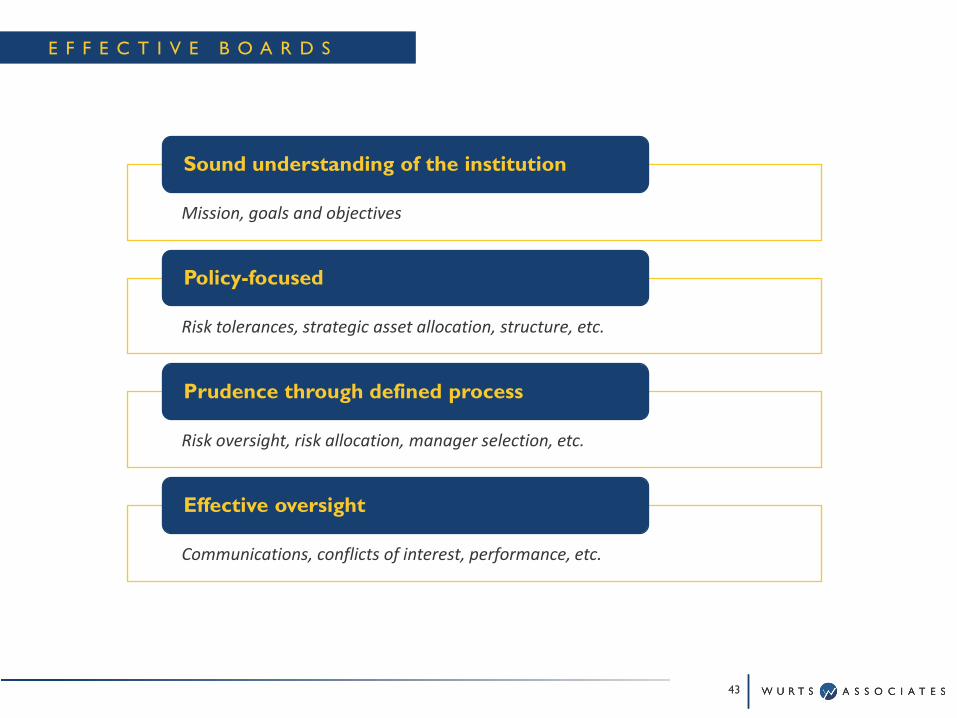

E F F E C T I V E B O A R D S

Mission, goals and objectives

Sound understanding of the institution

Risk tolerances, strategic asset allocation, structure, etc.

Policy-focused

Risk oversight, risk allocation, manager selection, etc.

Prudence through defined process

Communications, conflicts of interest, performance, etc.

Effective oversight

43

Related Documents