Risk Assessment of the Brazilian FX Rate Wagner Piazza Gaglianone Jaqueline Terra Moura Marins Banco Central do Brasil – Departamento de Estudos e Pesquisas

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Risk Assessment of the Brazilian FX Rate

Wagner Piazza Gaglianone

Jaqueline Terra Moura Marins

Banco Central do Brasil – Departamento de Estudos e Pesquisas

The views expressed in this

presentation are those of the

authors and do not necessarily

represent those of the Banco

Central do Brasil or its members.

Disclaimer

2

“Essentially, all models are wrong, but some are useful.”

(George E. P. Box)

The objective of this paper is to investigate a set of FX-rate models and reveal which are more useful for point (and density) forecasting.

The aim is to increase our understanding of the exchange rate dynamics in Brazil from a risk-analysis perspective.

Motivation: Fundamentals may vary in their predictive content at different horizons (or distinct parts of the distribution of the FX-rate).

Introduction

3

• Meese and Rogoff (1983): The Random Walk (RW) paradigm (economic

fundamentals - such as the money supply, trade balance and national income - are of little use in forecasting out-of-sample exchange rates). • Bacchetta and van Wincoop (2006): describe the RW paradigm as: “…the major weakness of international macroeconomics”. • Mark (1995): greater exchange rate predictability at longer horizons. • Kilian and Taylor (2003): exchange rates can be predicted from economic models at horizons of 2 to 3 years, after taking into account the possibility of nonlinear dynamics. • Engel and West (2005): It is not surprising that a RW outperforms fundamental-based models if one treats FX-rate as an asset price within a rational expectation present-value model (and discount factor near one).

Introduction

4

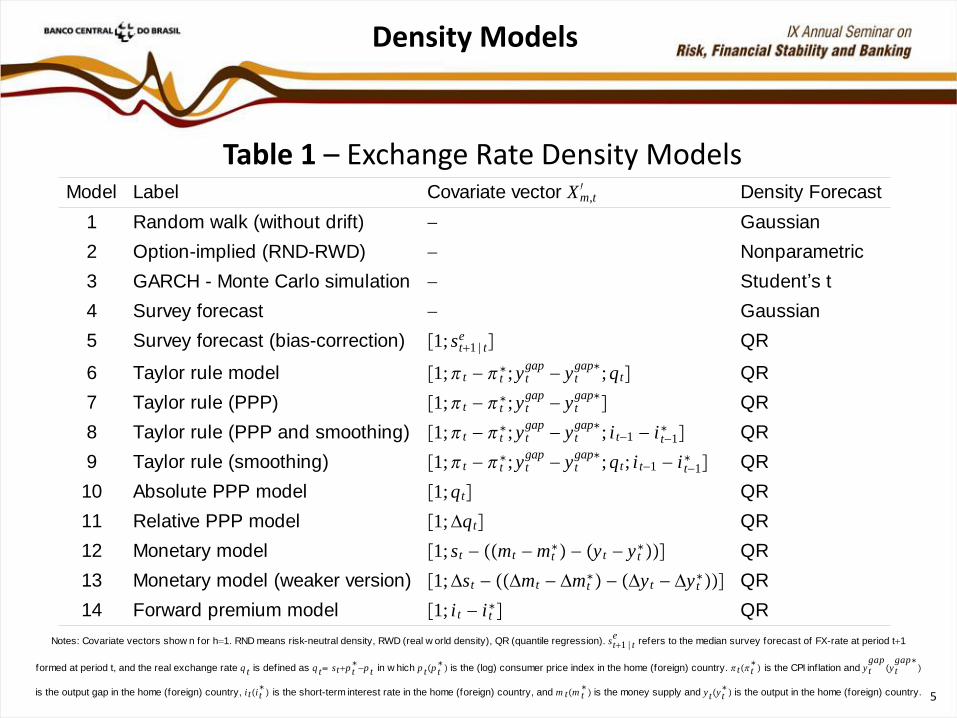

Table 1 – Exchange Rate Density Models

Notes: Covariate vectors show n for h1. RND means risk-neutral density, RWD (real w orld density), QR (quantile regression). st1te

refers to the median survey forecast of FX-rate at period t1

formed at period t, and the real exchange rate q t is defined as q t stp tp t in w hich p tp t

is the (log) consumer price index in the home (foreign) country. tt is the CPI inf lation and yt

gapyt

gap

is the output gap in the home (foreign) country, i ti t is the short-term interest rate in the home (foreign) country, and m tm t

is the money supply and ytyt is the output in the home (foreign) country.

Density Models

Model Label Covariate vector Xm,t Density Forecast

1 Random walk (without drift) Gaussian

2 Option-implied (RND-RWD) Nonparametric

3 GARCH - Monte Carlo simulation Student’s t

4 Survey forecast Gaussian

5 Survey forecast (bias-correction) 1; st1te QR

6 Taylor rule model 1; t t; y t

gap y tgap

;qt QR

7 Taylor rule (PPP) 1; t t; y t

gap y tgap QR

8 Taylor rule (PPP and smoothing) 1; t t; y t

gap y tgap

; i t1 i t1 QR

9 Taylor rule (smoothing) 1; t t; y t

gap y tgap

;qt; i t1 i t1 QR

10 Absolute PPP model 1;qt QR

11 Relative PPP model 1;qt QR

12 Monetary model 1; st mt mt y t y t

QR

13 Monetary model (weaker version) 1;st mt mt y t y t

QR

14 Forward premium model 1; i t i t QR

5

Density Models

Model 1: Random walk (without drift), with Gaussian distribution based on past forecast errors. Model 2: Forward-looking approach based on option prices. Two main steps: (i) obtaining risk-neutral densities (RND); (ii) transforming them into real world densities (RWD). RND represents probabilities that investors would attach to the future asset prices in a world in which they were risk-neutral. If investors are risk-averse, risk premia will drive a wedge between the probabilities inferred from options (RND) and RWD. See Shimko (1993); Vincent-Humphreys and Noss (2012).

6

Density Models

Model 3: AR(1)-GARCH(1,1)-Student’s t, with Monte Carlo simulation. Backward-looking approach with variance reduction techniques. Saliby (1989); Glasserman (2004). Model 4: Survey-based median forecast (Focus), with Gaussian distribution based on past forecast errors. Models 5-14: Economic-driven models based on Molodtsova and Papell (2009), Wang and Wu (2012) and quantile regression. The density forecast of model m takes the form of:

in which (st+h - st) is the h-period change of the (log) exchange rate, and Xm,t contains economic variables used in model m.

7

Forecast Evaluation

Point Forecast Evaluation (location)

- RMSE and Diebold-Mariano (1995) - Pesaran-Timmermann (1992, 2009)

Density Forecast Evaluation (shape)

Global Analysis - Coverage rates (50%, 70%, 90%) - Berkowitz (2001) - LPDS ranking and Amisano-Giacomini (2007)

Local Analysis (backtests) - Kupiec (1995) - Christoffersen (1998) - VQR test (2011)

8

Density Forecasts - Global Analysis

• Coverage Rates: Frequency of FX-rate observations inside a forecast interval (e.g. 70% band formed by conditional quantiles at τ = 0.15 and 0.85).

Objective is to statistically check the equality between the actual and the nominal coverage. Drawback: ignore time dependence and cluster behavior.

• Berkowitz (2001) test: Evaluates the entire density from normalized forecast errors = Φ⁻¹(zt+1), where Φ⁻¹ is the inverse of the standard normal distribution function and zt+1 is the Probability Integral Transform (PIT): where is the density forecast of model m, and st+1 is the observed FX-rate. Null hypothesis:

9

• Log Predictive Density Score (LPDS): LPDS of model m and forecast horizon h is defined by:

where is the (model m) conditional density of FX-rate for period t+h based on the information set available at t.

Such density is evaluated at st+h and (log) averaged along the out-of-sample observations. A higher score implies a better model (Adolfson et al., 2005).

• Amisano-Giacomini (2007) test: Compares the LPDS between two competing models (requiring rolling-window samples). The null hypothesis assumes equal LPDS between model 1 (RW) and m≠1.

Density Forecasts - Global Analysis

10

Density Forecasts - Local Analysis

• Kupiec (1995): Nonparametric test based on the proportion of violations: . The null hypothesis E ( Ht+h ) = (1 – τ) can be tested through a standard LR test.

• Christoffersen (1998): Incorporates time dependence, by assuming that Ht+h follows a first order Markov sequence. The null assumes independence of Ht+h and the “conditional coverage” test is based on unconditional coverage (Kupiec) and independence.

• VQR (2011) test: Previous backtests ignore the magnitude of violations. Gaglianone et al. (2011) propose a Quantile Regression-based test to evaluate Value-at-Risk measures. Under the null that is indeed a conditional quantile of st+h , it follows that α₀(τ) = 0 and α₁(τ) = 1 from

11

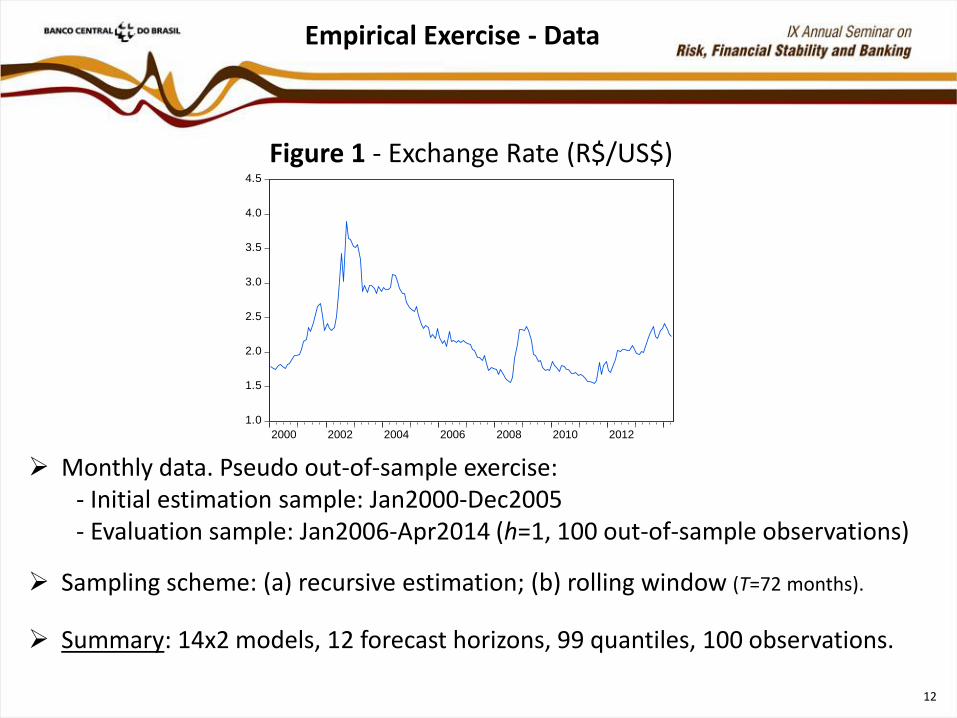

Empirical Exercise - Data

Figure 1 - Exchange Rate (R$/US$) Monthly data. Pseudo out-of-sample exercise: - Initial estimation sample: Jan2000-Dec2005 - Evaluation sample: Jan2006-Apr2014 (h=1, 100 out-of-sample observations)

Sampling scheme: (a) recursive estimation; (b) rolling window (T=72 months).

Summary: 14x2 models, 12 forecast horizons, 99 quantiles, 100 observations.

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2000 2002 2004 2006 2008 2010 2012

12

Point Forecasts

Figure 2 - Point Forecasts from Models 1-4

1.5

2.0

2.5

3.0

3.5

4.0

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Point forecasts from Model 1, recursive estimation

1.5

2.0

2.5

3.0

3.5

4.0

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Point forecasts from Model 2, recursive estimation

1.5

2.0

2.5

3.0

3.5

4.0

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Point forecasts from Model 4, rolling window estimation

1.0

1.5

2.0

2.5

3.0

3.5

4.0

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Point forecasts from Model 3, rolling window estimation 13

Point Forecasts

Does any model "beat" the random walk?

Table 2 - Diebold-Mariano (1995) test of equal accuracy

Notes: P-values in parentheses. Positive statistic means that a model has lower RMSE compared to the RW (model 1a).

Model 1a 2a 3a 4a 5a 6a 7a 8a 9a 10a 11a 12a 13a 14a

h=1 2.16 -1.82 -0.96 -0.60 -0.45 -0.42 -0.75 -1.14 -1.54 -0.73 -1.77 -0.82 -1.71

(0.03) (0.07) (0.34) (0.55) (0.65) (0.68) (0.46) (0.26) (0.13) (0.47) (0.08) (0.41) (0.09)

h=2 1.96 -1.35 -1.13 -0.81 -0.76 -0.41 -0.60 -1.02 -2.00 -1.77 -1.71 -1.39 -2.34

(0.05) (0.18) (0.26) (0.42) (0.45) (0.68) (0.55) (0.31) (0.05) (0.08) (0.09) (0.17) (0.02)

h=3 1.99 -1.35 -1.08 -0.86 -1.11 -0.88 -0.82 -1.40 -1.82 -1.22 -1.59 -1.16 -2.39

(0.05) (0.18) (0.28) (0.39) (0.27) (0.38) (0.41) (0.17) (0.07) (0.22) (0.11) (0.25) (0.02)

h=4 2.17 -1.33 -0.87 -0.89 -1.22 -0.90 -1.02 -1.31 -1.92 -1.13 -1.65 -1.49 -2.03

(0.03) (0.19) (0.39) (0.38) (0.23) (0.37) (0.31) (0.19) (0.06) (0.26) (0.1) (0.14) (0.05)

h=5 2.01 -1.26 -0.39 -1.02 -1.34 -1.10 -1.15 -1.44 -2.29 -0.66 -1.98 -0.99 -1.98

(0.05) (0.21) (0.7) (0.31) (0.18) (0.28) (0.25) (0.15) (0.02) (0.51) (0.05) (0.32) (0.05)

h=6 2.01 -1.32 -0.07 -0.94 -1.43 -1.10 -1.16 -1.44 -2.24 -0.77 -2.18 -0.67 -1.67

(0.05) (0.19) (0.94) (0.35) (0.16) (0.27) (0.25) (0.15) (0.03) (0.45) (0.03) (0.5) (0.1)

h=7 2.19 -1.32 0.13 -1.06 -1.52 -1.30 -1.34 -1.60 -2.24 -0.77 -2.15 -1.01 -1.81

(0.03) (0.19) (0.9) (0.29) (0.13) (0.2) (0.18) (0.11) (0.03) (0.44) (0.03) (0.31) (0.07)

h=8 2.48 -1.34 0.22 -1.02 -1.53 -1.41 -1.50 -1.96 -1.79 -1.16 -1.89 -1.00 -1.92

(0.01) (0.18) (0.82) (0.31) (0.13) (0.16) (0.14) (0.05) (0.08) (0.25) (0.06) (0.32) (0.06)

h=9 2.81 -1.31 0.19 -0.98 -1.71 -1.44 -1.60 -2.09 -1.71 -0.78 -1.62 -0.84 -1.77

(0.01) (0.19) (0.85) (0.33) (0.09) (0.15) (0.11) (0.04) (0.09) (0.44) (0.11) (0.4) (0.08)

h=10 3.41 -1.31 0.22 -1.06 -1.95 -1.59 -1.75 -1.96 -1.47 -1.12 -1.48 -1.18 -1.66

(0) (0.19) (0.82) (0.29) (0.05) (0.12) (0.08) (0.05) (0.15) (0.26) (0.14) (0.24) (0.1)

h=11 3.93 -1.32 0.13 -1.08 -1.64 -1.57 -1.90 -1.59 -1.39 -1.14 -1.36 -1.14 -1.61

(0) (0.19) (0.9) (0.28) (0.1) (0.12) (0.06) (0.11) (0.17) (0.26) (0.18) (0.26) (0.11)

h=12 4.45 -1.35 -0.04 -1.11 -1.78 -1.67 -1.87 -1.80 -1.36 -1.22 -1.35 -1.05 -1.73

(0) (0.18) (0.97) (0.27) (0.08) (0.1) (0.06) (0.07) (0.18) (0.23) (0.18) (0.3) (0.09)

14

Point Forecasts

Can the competing models forecast the direction of change?

Table 3 - Prediction of the direction of change of the FX-rate

Note: The null hypothesis assumes that a model has no power in predicting the directional change of the FX-rate.

Pesaran & Timmermann (1992, 2009) direction of change test (p-value)

Model 1a 2a 3a 4a 5a 6a 7a 8a 9a 10a 11a 12a 13a 14a

h=1 0.00 0.02 0.84 0.24 0.21 0.81 0.21 0.31 0.89 0.99 0.89 0.68 0.23

h=2 0.01 0.07 0.94 0.00 0.63 0.50 0.10 0.33 0.05 0.06 0.12 0.06 0.04

h=3 0.04 0.02 0.81 0.00 0.78 0.51 0.20 0.81 0.20 0.10 0.19 0.40 0.04

h=4 0.07 0.59 0.00 0.19 0.46 0.55 0.31 0.08 0.02 0.40 0.72 0.10

h=5 0.00 0.69 0.00 0.24 0.60 0.83 0.29 0.02 0.51 0.13 0.71 0.02

h=6 0.02 0.63 0.00 0.33 0.92 0.89 0.37 0.02 0.81 0.06 0.46 0.01

h=7 0.00 0.58 0.00 0.15 0.59 0.50 0.19 0.01 0.71 0.01 0.70 0.00

h=8 0.00 0.88 0.00 0.39 0.96 0.99 0.46 0.14 0.00 0.00 0.00 0.00

h=9 0.00 0.76 0.00 0.32 0.59 0.47 0.25 0.11 0.00 0.00 0.00 0.00

h=10 0.00 0.97 0.00 0.06 0.02 0.09 0.10 0.00 0.21 0.00 0.01 0.00

h=11 0.00 0.81 0.00 0.04 0.05 0.18 0.04 0.01 0.00 0.00 0.01 0.00

h=12 0.00 0.89 0.00 0.01 0.20 0.08 0.09 0.00 0.00 0.00 0.00 0.00

15

Density Forecasts

Figure 3 - Conditional Densities for April 2014 (h=1)

0

1

2

3

4

5

6

7

8

9

1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8 2.9

FX-rate for 2014m4, forecast horizon: h1, recursive estimation

M1M2

M3

M4

M5

M6

M7

De

nsit

y

16

Density Forecasts

Table 4 – Selected models from the Global Analysis Horizon Berkowitz test LPDS ranking AG test (stat0)

1 2, 5ab, 6b, 7ab, 8ab, 10ab, 11ab, 12ab, 13ab, 14ab 3ab, 5a, 14b 3b, 14b

2 2, 5b, 6ab, 7ab, 8ab, 9b, 10ab, 11b, 12ab, 13b, 14ab 1b, 3b, 11a, 13a -

3 2, 8b, 9b, 10ab, 12ab, 14ab 1b, 5a, 11ab -

6 8a 1b, 4b, 11a, 13a -

9 8b, 9b 1b, 4b, 11a, 13a -

12 9a 1b, 4ab, 5a 4b

Horizon Coverage rate

1 2, 5ab, 6b, 7ab, 8ab, 9b, 10ab, 11ab, 12ab, 13ab, 14ab

2 3ab, 5ab, 6b, 7ab, 8b, 10b, 11ab, 13ab, 14ab

3 3ab, 5ab, 7ab, 8b, 10ab, 11ab, 12ab, 13ab

6 1b, 3b, 5ab, 6b, 7ab, 8ab, 9b, 10ab, 11ab, 12ab, 13ab, 14a

9 1b, 4b, 5ab, 6ab, 7a, 8ab, 9ab, 10ab, 11ab, 12ab, 13b, 14ab

12 1b, 5ab, 6ab, 7ab, 8ab, 9ab, 10ab, 11b, 12a, 13b, 14ab

17

Density Forecasts

Table 5 - Selected models from the Local Analysis

Note: NP means the minimum number of p-values (above 0.05) to select a given model,

from a total of 9 p-values (3 backtests x 3 quantile levels ) for each part of the density.

Horizon Criteria NP Low quantiles ( 0.1; 0.2; 0.3) High quantiles ( 0.7; 0.8; 0.9)

1 Kupiec, Christ., VQR 9 7ab, 10b, 11a, 13a 5b, 6ab, 7ab, 8ab, 9ab, 10ab, 12b, 13a, 14ab

2 Kupiec, Christ., VQR 8 7b, 11a -

3 Kupiec, Christ., VQR 7 2, 7b -

6 Kupiec, Christ. 4 7a 6a, 9a

9 Kupiec, Christ. 4 - 6a

12 Kupiec, Christ. 4 14a 1b

18

Risk Assessment Exercise

Main Steps:

• Establish (ad-hoc) thresholds for the FX-rate: low (λL) or high (λH). • In the first case, construct a dummy variable Dt+h = 1st+h < λL

to reveal the periods which (ex-post) exhibited a FX-rate below the threshold λL . • Next, for each model m, horizon h, and period t, search for the conditional quantile (and respective quantile level τ*) which is closest to this threshold. • The τ* level represents the (ex-ante) conditional probability that the FX-rate will breach the established limit in the future (h-periods ahead), that is,

19

Risk Assessment Exercise

Figure 4 - Conditional probabilities (h=1) of FX-rate below R$1.55/US$ R$1.60/US$

Figure 5 - Conditional probabilities (h=1) of FX-rate above

R$2.40/US$ R$2.35/US$

0.0

0.2

0.4

0.6

0.8

1.0

2006 2007 2008 2009 2010 2011 2012 2013 2014

0.0

0.2

0.4

0.6

0.8

1.0

2006 2007 2008 2009 2010 2011 2012 2013 2014

0.0

0.2

0.4

0.6

0.8

1.0

2006 2007 2008 2009 2010 2011 2012 2013 2014

0.0

0.2

0.4

0.6

0.8

1.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 20

Conclusions

We evaluate competing FX-rate density models according to its forecasting performance at: (i) different horizons; (ii) distinct parts of the distribution. Overall, no model accounts for the entire density (and all horizons).

Summary of results

• Point forecasts: (i) option-data useful for h=1-3 months; (ii) several models predict the direction

of change (e.g. fundamentals, over 6 months);

• Density forecasts:

- Global analysis: Coverage rates: exclude Gaussian densities;

Berkowitz: options + others (short-run); Taylor rule (medium to long-run);

LPDS ranking: GARCH (h=1,2); survey; PPP and monetary model;

- Local analysis: Risk of FX-rate increase: QR densities (h=1); Taylor rule (h=6,9);

Risk of FX-rate decrease: PPP and monetary models (h=1);

Options (h=3); Forward Premium model (h=12); 21

Conclusions

Results in line with a vast literature reporting the practical difficulty on beating the naive RW (Mark, 2001).

Option-implied density forecasts provide relatively accurate forecasts in the short-run (see also Christoffersen and Mazzotta, 2005; Ornelas et al., 2012).

Correct “direction prediction” appears to cluster at the longer horizons (Cheung, Chinn and Pascual, 2005).

Fundamental relationships (e.g. parity conditions) hold better in the long-run.

Risk assessment: asymmetric response of fundamentals (due to quantile regression) in respect to the selected part of distribution of the FX-rate.

Possible Extensions: (i) extend the set of models; (ii) increase the forecast horizon; (iii) density forecast combination (Hall and Mitchell, 2007; Jore et al., 2010); (iv) alternative risk measures (e.g. expected shortfall); (v) tests of conditional predictive ability (Giacomini and White, 2006).

22

Thank you

More details about the methodology are available at:

http://www.bcb.gov.br/pec/wps/ingl/wps344.pdf

BCB Working Paper Series n.344

Related Documents