RHB PRIVATE EQUITY OPPORTUNITY FUND 1 ANNUAL REPORT 2019 For the financial year ended 31 July 2019

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RHB PRIVATE EQUITY OPPORTUNITY FUND 1

ANNUAL REPORT 2019

For the financial year ended 31 July 2019

1

GENERAL INFORMATION ABOUT THE FUND

Name, Category and Type

Fund Name - RHB Private Equity Opportunity Fund 1

Fund Category - Private equity (close-ended)

Fund Type - Income and growth fund

Commencement Date, Tenure and Maturity Date

The Commencement Date of the Fund was on 28 July 2016. The tenure of the Fund

is 7 years and the Maturity Date of the Fund is on the seventh (7th) anniversary of

the Commencement Date.

Investment Objective, Policy and Strategy

Objective of the Fund

The Fund aims to provide long term^ capital appreciation by investing in the shares

of RHB Private Equity Fund I (“the Company”).

^Note: “long term” in this context refers to a period of 7 years.

Strategy

The Fund will invest principally in the United States Dollar (“USD”) denominated

shares of the Company. The Company is an exempted company with limited

liability incorporated in the Cayman Islands on 3 May 2016 under the company

law of the Cayman Islands. The Company is regulated by the Cayman Islands

Registrar of Companies.

The assets of the Company will be managed by the investment manager of the

Company, i.e. RHB Asset Management Pte Ltd (“RAM Singapore”), a company

incorporated in Singapore on 20 October 2006 to carry out fund management

activities that is regulated by the Monetary Authority of Singapore. RAM

Singapore has appointed NB Alternatives Advisers LLC as the Company’s sub-

investment manager. NB Alternatives Advisers LLC is a limited liability company

incorporated in Delaware and is a registered investment adviser with the United

States Securities and Exchange Commission.

2

The investment objective of the Company is to achieve attractive risk-adjusted

returns on its capital through investments in portfolio investments whose expected

duration is appropriate for the remaining charter life of the Company (a period of

7 years). As the Fund invests at least 95% of Net Asset Value (“NAV”) in the

shares of the Company, the investment strategy employed will be at the Company

level. The Company’s investment strategy is to primarily invest in private equity

and private debt investments, both direct investments and funds, including without

limitation private equity funds, co-investments, secondaries, private debt

investments and semi-liquid private equity investments (i.e. the portfolio

investments). The portfolio investments may consist of private equity investment

or funds managed and operated by various alternative investment managers in

which the Company’s sub-investment manager invests the Company’s assets into.

The Manager may trade in financial derivatives for the purpose of hedging the

Fund’s exposure to the USD denominated shares of the Company.

The Fund’s portfolio will be structured as follows:

At least 95% of

Net Asset Value

- Investments in the shares of RHB Private Equity Fund I.

Up to 5% of

Net Asset Value

- Investments in liquid assets including money market

instruments and Placements of Cash.

Note: Placements of Cash are placements of cash in any deposits or investment

accounts with any financial institution(s) that are not embedded with or linked to

financial derivative instruments.

3

Target Return

This Fund aims to achieve a targeted return of 15%-20% gross internal rate of

return per annum over the 7 years of the Fund.

There is no guarantee that returns targeted in any underwriting process will be

realised or achieved or that an investment strategy will be successful, and actual

returns may be significantly lower than those shown here. Investors should keep

in mind that the securities markets are volatile and unpredictable. There are no

guarantees that the historical performance of an investment, portfolio, or asset class

will have a direct correlation with its future performance.

Investment Policies and Restrictions

The Fund will invest principally in one company, i.e. the shares of RHB Private

Equity Fund I, participate in financial derivatives, invest in money market

instruments and make Placements of Cash with any financial institutions, and any

other investments in line with the Fund’s objective.

In undertaking the Fund’s investments, the Fund must not invest in a fund-of-

funds, a feeder fund or any sub-fund of an umbrella scheme which is a fund-of-

funds or a feeder fund.

Distribution Policy

Subject to the availability of income and at the Manager’s discretion of the best

interests of the Fund and the Unitholders, the Fund will declare income

distributions quarterly.

4

MANAGER’S REPORT

TARGET FUND STRATEGY

The Target Fund has two major strategies, i.e.

(1) investing in direct debt investments by investing into NB Private Equity Credit

Opportunities Fund LP (“NBPECO”), and

(2) investing in private equity investments and/or private debt instruments directly or

through co-investment deals on an opportunistic basis.

NBPECO updates

On 24 June 2019, NBPECO performed a net distribution of United States Dollar

(“USD”)183K to the Fund. The distribution is the result of several realizations in the

portfolio as well as coupon earned from February 2019 through May 2019. In total

NBPECO received in excess of USD170Million(“M”) of proceeds from the realization

of these investments and has paid down a portion of the capital call facility and recycled

the excess proceeds into new investments. In view of this, of the USD13M commitment

allocated by RHB Private Equity Fund I to this fund, RHB Private Equity Fund I has

approximately USD8.5M of commitments to NBPECO remaining unfunded. As of 19

June 2019, NBPECO had called USD486M of investor capital, will have realized

USD340M, and, based on pending and completed investment activity will have

invested and committed a total of approximately USD700M in 24 companies,

representing approximately 66% of NBPECO commitments of USD1,058M. Based on

undeployed capital and recycling provisions, NBPECO now have the ability to call

approximately USD 635M of investor commitments.

As at 31 March 2019, NBPECO’s Net MOIC (Multiple on Invested Capital) was 1.01x

and has generated gross and net Internal Rate of Return (“IRR”) of 5.1% and 0.9%

respectively. The net IRR was impacted by cumulative management fees and fund

expenses. NBPECO held USD467M of investments, which consisted of 35% first lien

loans, 6% second lien loans, 3% 144A bonds, 45% structured preferred investments,

and 11% equity and other investments

As of 31 March 2019, the NBPECO has called USD409M to support cumulative

investments of USD630M. The balance has been funded with the subscription line and

approximately USD24M of recycled proceeds. NBPECO have realised cash proceeds

of approximately USD156M and cash interest of USD33m. NBPECO realised several

large investments in April 2019 and May 2019. If these dispositions and all cash

interest associated with these realizations (in aircraft maintenance repair and overhaul,

specialty consulting, life sciences) are included, NBPECO will have distributed

5

USD308M of cash proceeds, representing a gross IRR of 20.6% and gross MOIC of

1.22x.

Forecasting the development of NBPECO IRRs over the next several months is a

difficult (and perhaps unwise) endeavor. Attempting to define a precise range of returns

for investments NB haven’t made is probably not a great use of time. Based on the

current Net Asset Value (“NAV”) (ignoring future deployment), NB do expect rolling

returns to continue to increase throughout the year as the portfolio matures. Of course,

NB cannot accurately forecast the vagaries of the market and account for all unexpected

idiosyncratic events.

Given NBPECO’s ‘dry powder’ and their disciplined approach to capital deployment,

they approached NBPECO’s Limited Partner Advisory Committee (the “LPAC”) in

February 2019 regarding an extension of NBPECO’s investment period. On 12 April

2019, they received majority consent of the LPAC to extend the investment period of

NBPECO to December 2020. NB expects that the portfolio aims to be deployed in full

by December 2020 and for it to be harvested within RHB Private Equity Fund I’s

charter life.

NB are often asked about the pace of future capital deployment. NBPECO have already

called capital to support their investment in an aerospace concern. While they have

identified several potential investment opportunities, they do not have a definitive

schedule for capital deployment. As such, to provide an approximation of future capital

calls, NB guide investors to assume that the dry powder estimate (approximately

USD635M) is invested ratably over the next six calendar quarters ending in December

2020 (roughly USD100M per quarter). This approximation can swing dramatically (up

or down) depending on prevailing market conditions.

Private Equity – Co-investments

Since inception, total commitments for co-investments of approximately USD12M

have been made, of which almost USD11M have been called. Five transactions have

seen an upward revaluation since the initial investment, these were Project Arch, WM,

Cotton, Cashier and the three CI Capital investments (Indigo, Eucalyptus, Mango) due

to on-plan performance and improvements to business operations. Project Hulk had a

slight downward valuation due to currency movement as the investment was in CAD.

Current portfolio

Project Bluemoon: September 2018, USD2M equity investment into a leading provider

of enterprise systems software that assists large organizations with managing and

optimizing their information technology needs. The lead sponsor is KKR which invests

across a variety of industries globally, with this investment forming part of their

flagship fund with ~USD14b committed capital. Bluemoon is expected to continue to

benefit from a resilient mainframe market and the growth of hybrid IT environments

6

that are increasingly complex and far-reaching. Additional growth upside driven by

better product positioning and cross-selling offerings to existing customers. CY18 total

revenue flat y-o-y due to higher than usual deferral rates in fourth quarter of year 2019,

CY18 consolidated Earnings Before Interest, Tax, Depreciation and Amortisation

("EBITDA") increased 10% Year-on-Year (“YoY”).

Project Cashier: August 2018, USD1M equity investment for the buyout of a leading

provider of Point of Sale (“POS”) terminals and systems as well as a suite of software

and value added solutions. The lead sponsor is Francisco Partners and they are a leading

global private equity firm, which specializes in investments in technology and

technology-enabled services businesses. The firm invests in opportunities where its

deep sectoral knowledge and operational expertise can help companies realize their full

potential. Under the leadership of the Francisco Partners-backed management team, a

significant cost restructuring program is being executed. The cost savings from this

restructuring are expected to be at least 30% above the amount of cost savings

underwritten by Francisco Partners. EBITDA forecast for year 2019 expected to be in

good shape.

Project Hulk: July 2018, USD1.1M equity investment into a top environmental services

company in Canada offering solid waste services, soil remediation and

liquid/hazardous waste services. It is vertically integrated from collection and sorting

to diversion and disposal. Hulk is well positioned to roll-up a highly fragmented

industry with a strong pipeline of accretive add-on acquisitions. There are favourable

environmental service market dynamics that support the base business with opportunity

for margin enhancement. The lead sponsor is BC Partners, they invest across industries,

with a focus on consumer & retail, media & telecom and business services. Hulk closed

an acquisition in November 2018 and is now the fourth largest waste management

player in North America, with a diversified geographical revenue base of ~50% Canada

and ~50% United States (“US”).

Project Indigo: Total USD600K investment commitment, with USD338K capital

previously called in May 2018 had a further USD228K called in December 2018. This

was for equity investment into a sales and marketing agency providing outsourced

sales, marketing and merchandising services to consumer packaged goods (“CPG”)

companies in US. The company is a solid platform asset with a strong foundation and

is well-positioned in the fast-growing small/mid-size CPG segment. The entry

valuation was attractive and at a discount as compared to its peers and below industry

average. The lead investors are CI Capital which have completed 33 platforms and over

240 add-on acquisitions to date representing USD9billion in enterprise value, they

focus on large fragmented industries with favourable consolidation economics,

attractive growth potential and strong cash flow. Indigo has a highly actionable

acquisition pipeline with identified targets with acquisitions completed in May 2018,

June 2018 and September 2018.

7

Project Eucalyptus: May 2018, USD600K investment commitment, with USD338K

capital called for equity investment into an operator of dermatology clinics including

general dermatology, cancer care and cosmetics options with ~30 clinics across 5 states

in US. There is a stable addressable market with strong tailwinds – increasing demand

for services driven primarily by rising occurrence of skin cancer and the aging US.

population together with shortage of dermatologists creates a supply and demand

imbalance. The lead sponsor is CI Capital. Eucalyptus has completed 19 add-on

acquisitions during CI Capital’s ownership, including 9 in the first 9 months of year

2018. It continues to pursue additional add-on acquisitions.

Project Mango: May 2018, USD1.6M investment commitment, with USD925K capital

called for equity investment into a top 3 distributor of specialty chemicals and

ingredients with a North American focus and global supply chain capabilities. Their

clients include those in the coatings, adhesives, sealants, and elastomers (“CASE”),

food, pharma, lab cleaning and other industries. They are one of few companies in the

mid-market that has scale, management sophistication, infrastructure and capital to

consolidate. The lead sponsor is CI Capital. Mango continues to make progress on the

integration of a large, strategic acquisition completed in May 2018. The company has

experienced sales growth as a result of investments in technical talent and added

formulation capabilities.

Project Jewel: April 2018, USD615K equity investment into a cosmetics brand

company that sells primarily through mass and drugstore channels in US. The core

demographic is skewed towards younger, multi-cultural millennial consumers. The

lead investors are Gryphon Investors who have a deep consumer team with a strong

track record in the sector with successful exited deals. They believe there is significant

space to further expand Jewel’s footprint with existing US. retailers and e-commerce,

significant operational improvement / brand positioning enhancement opportunities as

well as a strong historical growth profile. In year 2018, Jewel has been successful at

gaining chain wide distribution at major retailers and has shown traction with Asian

and European retailers. 2018E revenue of USD128M representing ~6% YoY growth

and EBITDA of USD37M representing 8.5% YoY growth.

Project Cotton: July 2017, Euro Dollar (“EUR”)803K equity investment into a Spanish

omni-channel apparel retailer. The co-investment was done alongside PAI Partners in

the recapitalisation of Cotton. The business operates over two thousand points of sale

in 90 countries with three main brands targeting multiple segments. It has a leading

market position in Spain where the sector has experienced a steady recovery. Vertically

integrated chains such as Cotton are expected to continue taking market share. The

company has been refocusing its brands towards core customer groups driving

meaningful ‘Like for Like’ growth across all brands. The company continues to invest

in key assets for brand building and future development: communication, digital, CRM,

loyalty and expansion. Year-to-Date ("YTD") November 2018 sales was EUR802M,

lower than the prior year by 1.1% while its EBITDA was EUR104M, improving 2.6%

vs last year. Net debt stood at 3.1x leverage.

8

Project WM: August 2017, USD1.4M equity investment into a specialty retailer and

distributor of core boating and water recreation products with over 200 stores in the

US and Puerto Rico. The company is the largest retail player in the USD5.5 billion

Recreational Boating Parts & Accessories market. The lead sponsor, Monomoy Capital

Partners targets middle market companies that face significant operational, financial or

market challenges and aims to acquire these companies through complex transactions,

significantly improve their cost structure and product mix to increase cash flow, and

sell them as healthy middle market businesses to financial or strategic buyers as the

economy stabilizes. WM’s fourth quarter of year 2018 sales declined by USD6M from

fourth quarter of year 2017 while its quarterly EBITDA exceeded prior year by

USD4.6M.

Project Arch: September 2017, USD2M equity investment into a B2B provider of

office supplies and other products to large enterprises and small/medium businesses as

well as office supplies retailer with over 1,500 stores in US and Canada. The

transaction was done at a significant discount to comparable distributor businesses. The

experienced lead sponsor for the deal, Sycamore Partners, has a strong track record in

the consumer/retail sector. At transaction close, they have successfully reorganised the

business into three standalone entities. The company is on track with its initial

underwriting plan and Sycamore is confident in executing the identified base case cost

savings as it continues to divest non-core assets. Arch has distributed over 70% of

investment capital due to proceeds from subsidiary sales, restructuring and

recapitalisation. The investment also had a valuation uplift due to on-plan performance.

In September 2018, it agreed to acquire a leading national distributor of workplace

items for a total enterprise value of approximately USD1b.

MARKET REVIEW AND OUTLOOK

Private Equity and Private Debt

NB Asset Allocation Committee maintained its neutral view for private equity and

acknowledges high valuations, but recommends a consistent and disciplined strategic

investment plan.

Unfortunately, NB have nothing insightful or differentiated to say about the credit

markets - at least for now.

At the end of May 2019, US HY spreads stood at 481 basis points (“bps”),

approximately 86bps tighter than December 2018 levels and 30bps wider than March

219. CCC HY has continued to tighten in year 2019, contracting 229bps. Leveraged

loan spreads now stand at 457bps, about 100bps tighter than December 2018 and about

20bps tighter than March 2019; Split B/CCC loans have come in about 17bps for the

year 2019. Through May 2019, the Standard and Poor (“S&P”) is up over 12%, the

Russell up about 11%, and US HY and leveraged loans have notched gains of 7.8%

9

and 5.4%. The Nasdaq Composite Index (“NASDAQ”) is up about 12% through May

2019, after peaking at 8,163 early in the month.

HY gross issuance is flat YoY, and leveraged loan gross issuance is down over 70%;

loan net new issuance (ex-refinancing and repricing) is off 30%. Despite the lack of

new supply, net CLO issuance (USD 54.9b) is up modestly versus the comparable

period in year 2018 (USD 54.7b). Leveraged loan funds have reported 28 consecutive

weeks of outflows; for year 2019, leveraged loan funds have lost about USD16b

(versus +USD10b in the comparable period last year).

NB are not going to opine on implications of the inverted yield curve, ongoing trade

discussions with China, threatened Mexican tariffs, or anti-trust risks to big-tech in the

US. NB are pretty sure that their ability to extract meaningful correlations between

macroeconomic headlines and credit price action is, at best, limited.

Instead, let’s reflect on what’s worked well for NBPECO, what hasn’t worked, and

their thoughts on where they will find value over the next 18 months. In year 2016 and

most of year 2017, NBPECO were able to take advantage of lingering dislocations in

the secondary market, as evidenced by successful trades in companies in the insurance

services and aerospace industries. At the time, position sizes were relatively small as

NBPECO had not held final closes. All of these investments could have been upsized

meaningfully.

NB have done a fantastic job in the structured preferred market, driving exceptional

risk-adjusted returns for investors. NBPECO has invested approximately USD245M in

four preferred instruments. As discussed earlier, they have realised USD127M in a life

sciences company and an aircraft MRO, generating blended gross IRRs north of 20%.

A recent healthcare investment is off to an incredibly strong start, ahead of its synergy

implementation plan with solid top-line numbers. Right now, the operating company

bonds just senior to the preferred are trading at 106-107, implying a 7.8% YTW. And

NB are excited about the prospects of an investment in the midstream sector. NBPECO

are being paid an 8.5% cash dividend in an investment-grade company, and as they

write, the stock is at a 9% discount to conversion parity. Given the structure of the

investment, there are multiple paths for us to win, including a re-rating of the stock.

Investing in structured, unsecured instruments is not something to be taken lightly.

There were several large, well-known funds that splashed preferred capital around

indiscriminately before the year 2008-2009 crisis, and their investors paid the price. As

NB have said before, you can’t entertain these investments unless you love the

businesses. Relying solely on structural protections in preferred investments without

real conviction in the earnings power of the underlying assets is foolish and misguided.

When they make these investments, they spend months picking apart the businesses

with the sponsors and management teams, envisioning every possible bad outcome.

They have turned down dozens of these opportunities and will continue with their

10

persnickety ways. They’ve been around the block a few times and will not forget the

lessons of the past.

It’s not all rainbows and butterflies though. They have taken their lumps in some

smaller names, notably a 2nd lien on a food products company and a security services

company bonds. Fortunately, these positions were sized in proportion to their

conviction levels (quite low), and mark-downs are reflected in the NBPECO’s

performance. They have discussed their largest mistake, a business service firm that

focuses on personalised coupon-printing machines at point of checkout, in numerous

quarterly letters. At this point, the position simply isn’t a key driver of future NBPECO

performance. Over 60% of the NBPECO’s original investment in the company was in

the 1st lien loan; NB sized the 2nd lien loan position to account for a material

probability of impairment. Their initial downside forecasts did not envision a draconian

capitulation in CPG promotional spending and the economically irrational behavior of

a competitor. In short, everything that could go wrong did go wrong, and they, along

with several large creditors, were caught flat-footed by the financial performance of

the firm. It’s far too early to make an accurate assessment of its ultimate recoveries.

The firm’s Japanese and European businesses are performing, and the board and

management have made great strides in stabilizing the US franchise. There are multiple

potential paths for the company, including scenarios where NB recover the majority of

the 1st lien investment.

NB are generally sanguine about the current portfolio, and barring any unforeseen

hiccups, they expect NBPECO IRRs to continue to increase throughout year 2019.

At present, the secondary market is largely unappealing. Names are picked over, and

discounts are simply not large enough to compensate the investors for the risks they

would bear. NB continue to analyze a number of structured investments, but are ever

mindful of asset quality in a frothy market. In these markets, they often hear

competitors lament about ‘nothing to do’ (they catch themselves saying it too). The

reality, however, is quite different - there’s a ton of work to be done. They are actively

researching and monitoring dozens and dozens of credits whose current indicated

trading levels make no sense in the context of absurd capital structures. They will be

more than prepared when these names become actionable. The key is not to complain

about investments they can’t make, but to do the homework to cement their conviction

levels when it’s time to make investments.

While NB see nothing that makes them believe a short-term correction is imminent,

they do see an enormous opportunity set in both primary and secondary investments.

At some point, either they can scoop up loans and bonds at attractive levels or offer

capital to sponsors who must fix real problems irrespective of silly price action.

Markets can change quickly, and no one can systematically predict when or why. NB

keep hearing about the late innings of the credit cycle. It’s an annoying phrase that

pundits like to use in lieu of the following: ‘we really don’t have a clue when it’s going

to turn but ten years of expansion seems quite long, so it stands to reason that something

11

bad is going to happen sooner rather than later.’ NB know one thing: that which causes

the overwhelming majority of investors to re-rate risk is, by definition, unforecastable.

Otherwise, it would already be baked into security prices.

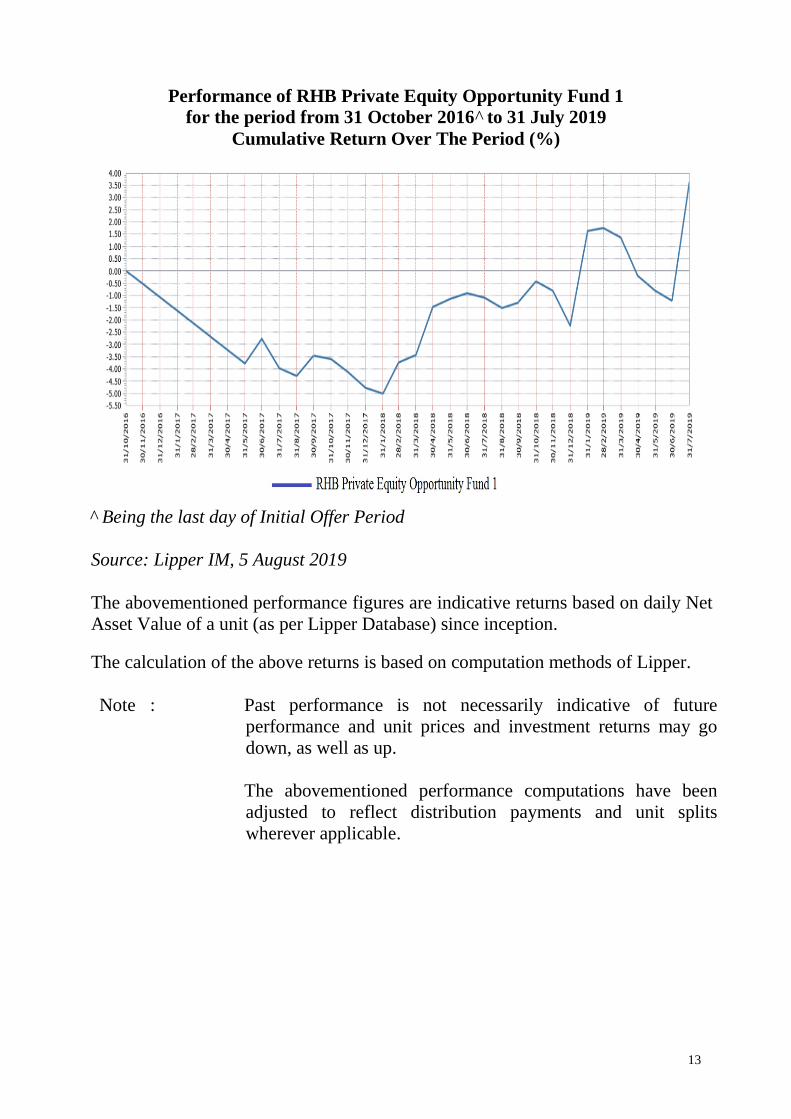

PERFORMANCE REVIEW

During the financial year under review, the Fund has registered a gain of 4.77%* in net

asset value terms. The Fund has not achieved its investment objective during the 12-

month financial year under review as the review period is relatively short compared to

its objective of providing long term (7 years) capital appreciation.

Source: Lipper Investment Management (“Lipper IM”), 5 August 2019

12

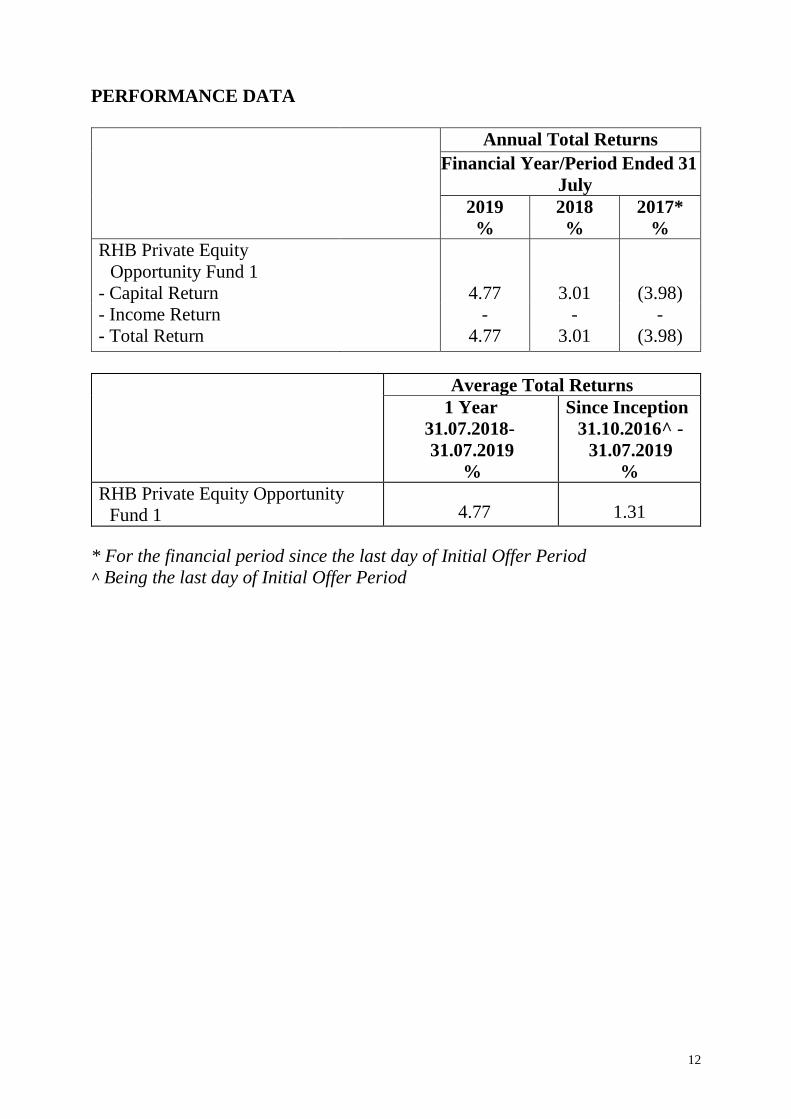

PERFORMANCE DATA

Annual Total Returns

Financial Year/Period Ended 31

July

2019 2018 2017*

% % %

RHB Private Equity

Opportunity Fund 1

- Capital Return 4.77 3.01 (3.98)

- Income Return - - -

- Total Return 4.77 3.01 (3.98)

Average Total Returns

1 Year

31.07.2018-

31.07.2019

%

Since Inception

31.10.2016^ -

31.07.2019

%

RHB Private Equity Opportunity

Fund 1 4.77 1.31

* For the financial period since the last day of Initial Offer Period

^ Being the last day of Initial Offer Period

13

Performance of RHB Private Equity Opportunity Fund 1

for the period from 31 October 2016^ to 31 July 2019

Cumulative Return Over The Period (%)

^ Being the last day of Initial Offer Period

Source: Lipper IM, 5 August 2019

The abovementioned performance figures are indicative returns based on daily Net

Asset Value of a unit (as per Lipper Database) since inception.

The calculation of the above returns is based on computation methods of Lipper.

Note : Past performance is not necessarily indicative of future

performance and unit prices and investment returns may go

down, as well as up.

The abovementioned performance computations have been

adjusted to reflect distribution payments and unit splits

wherever applicable.

14

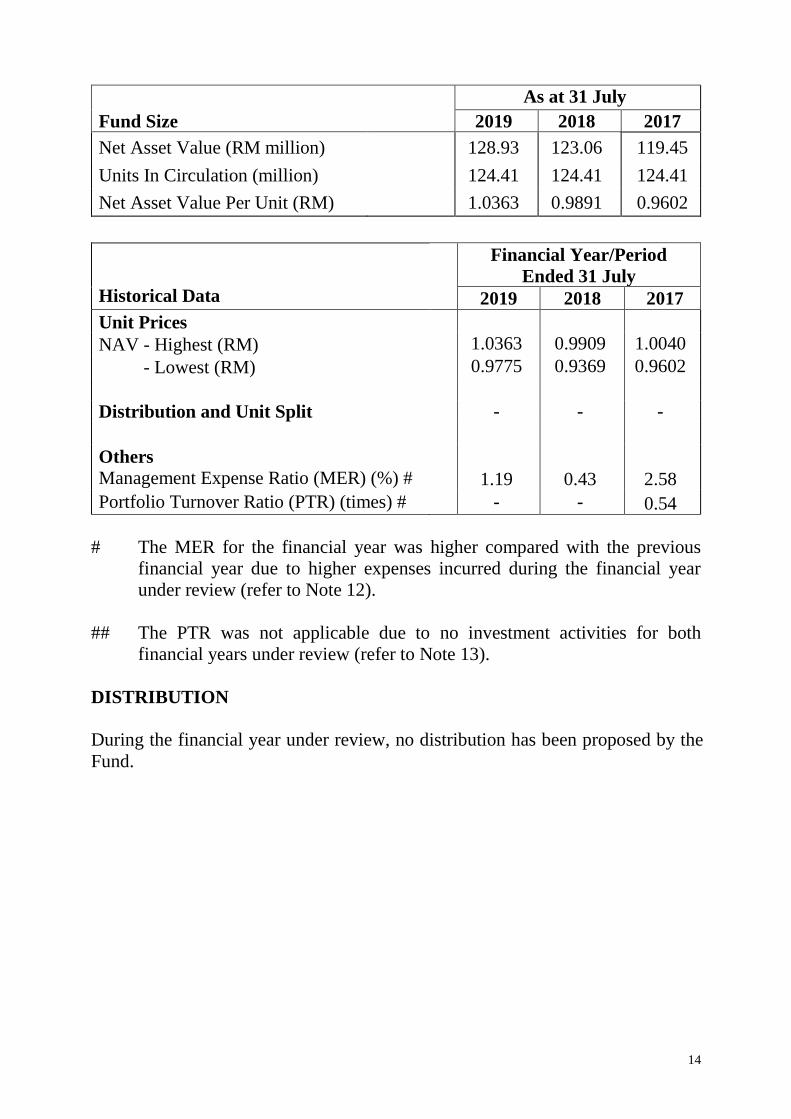

As at 31 July

Fund Size 2019 2018 2017

Net Asset Value (RM million) 128.93 123.06 119.45

Units In Circulation (million) 124.41 124.41 124.41

Net Asset Value Per Unit (RM) 1.0363 0.9891 0.9602

# The MER for the financial year was higher compared with the previous

financial year due to higher expenses incurred during the financial year

under review (refer to Note 12).

## The PTR was not applicable due to no investment activities for both

financial years under review (refer to Note 13).

DISTRIBUTION

During the financial year under review, no distribution has been proposed by the

Fund.

Historical Data

Financial Year/Period

Ended 31 July

2019 2018 2017

Unit Prices

NAV - Highest (RM) 1.0363 0.9909 1.0040

NAV - Lowest (RM) 0.9775 0.9369 0.9602

Distribution and Unit Split - - -

Others

Management Expense Ratio (MER) (%) # 1.19 0.43 2.58

Portfolio Turnover Ratio (PTR) (times) # - - 0.54

15

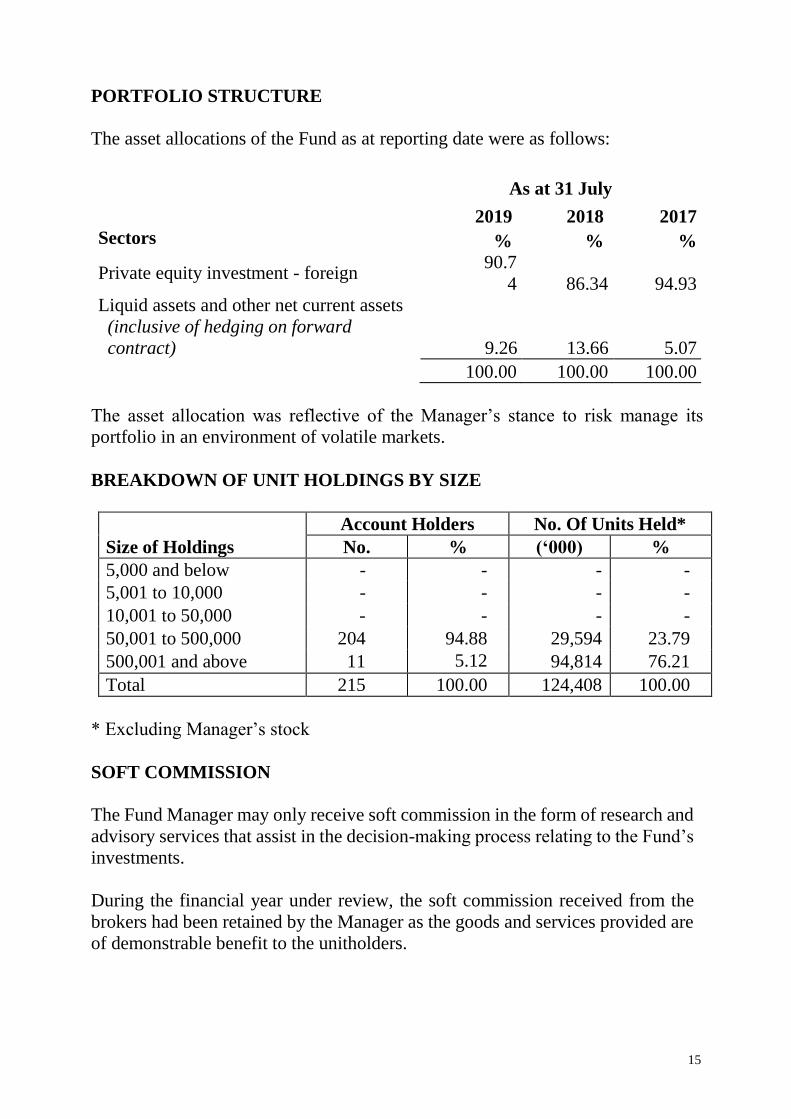

PORTFOLIO STRUCTURE

The asset allocations of the Fund as at reporting date were as follows:

As at 31 July

2019 2018 2017

Sectors % % %

Private equity investment - foreign 90.7

4 86.34 94.93

Liquid assets and other net current assets

(inclusive of hedging on forward

contract) 9.26

13.66

5.07

100.00 100.00 100.00

The asset allocation was reflective of the Manager’s stance to risk manage its

portfolio in an environment of volatile markets.

BREAKDOWN OF UNIT HOLDINGS BY SIZE

Account Holders No. Of Units Held*

Size of Holdings No. % (‘000) %

5,000 and below - - - -

5,001 to 10,000 - - - -

10,001 to 50,000 - - - -

50,001 to 500,000 204 94.88 29,594 23.79

500,001 and above 11 5.12

4 94,814 76.21

Total 215 100.00 124,408 100.00

* Excluding Manager’s stock

SOFT COMMISSION

The Fund Manager may only receive soft commission in the form of research and

advisory services that assist in the decision-making process relating to the Fund’s

investments.

During the financial year under review, the soft commission received from the

brokers had been retained by the Manager as the goods and services provided are

of demonstrable benefit to the unitholders.

16

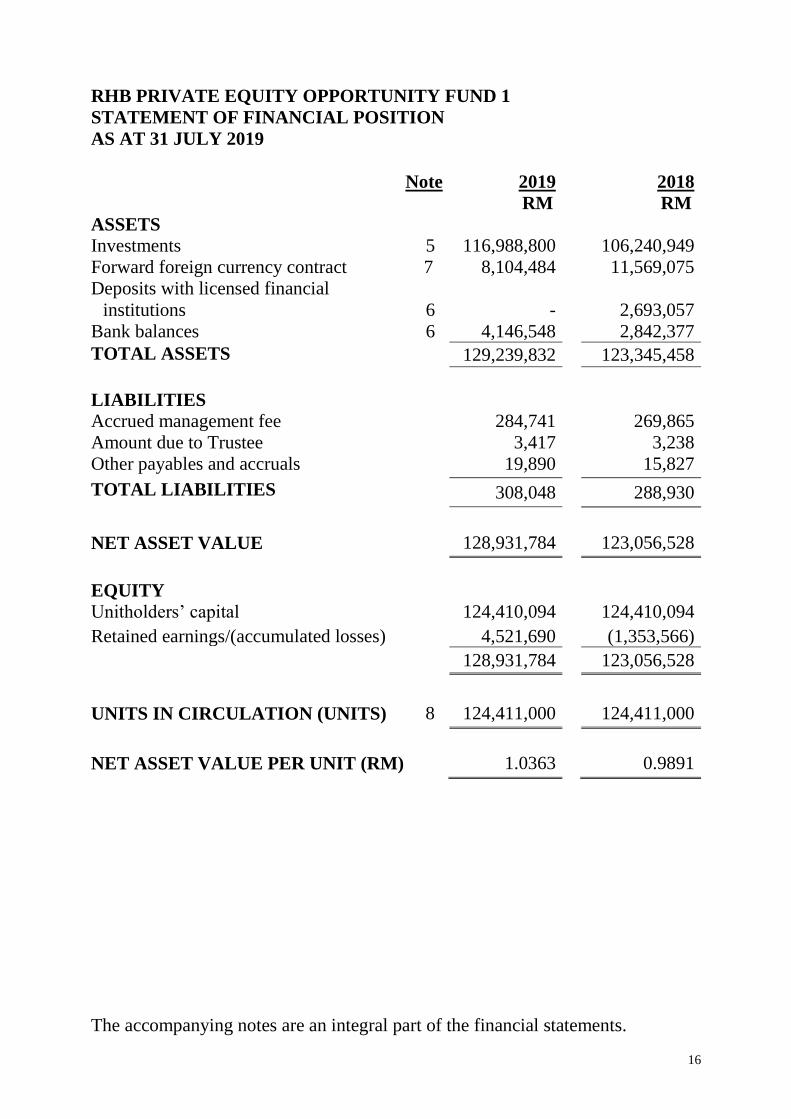

RHB PRIVATE EQUITY OPPORTUNITY FUND 1

STATEMENT OF FINANCIAL POSITION

AS AT 31 JULY 2019

Note 2019 2018

RM RM

ASSETS

Investments 5 116,988,800 106,240,949

Forward foreign currency contract 7 8,104,484 11,569,075

Deposits with licensed financial

institutions 6 -

2,693,057

Bank balances 6 4,146,548 2,842,377

TOTAL ASSETS 129,239,832 123,345,458

LIABILITIES

Accrued management fee 284,741 269,865

Amount due to Trustee 3,417 3,238

Other payables and accruals 19,890 15,827

TOTAL LIABILITIES 308,048 288,930

NET ASSET VALUE 128,931,784 123,056,528

EQUITY

Unitholders’ capital 124,410,094 124,410,094

Retained earnings/(accumulated losses) 4,521,690 (1,353,566)

128,931,784 123,056,528

UNITS IN CIRCULATION (UNITS) 8 124,411,000 124,411,000

NET ASSET VALUE PER UNIT (RM) 1.0363 0.9891

The accompanying notes are an integral part of the financial statements.

17

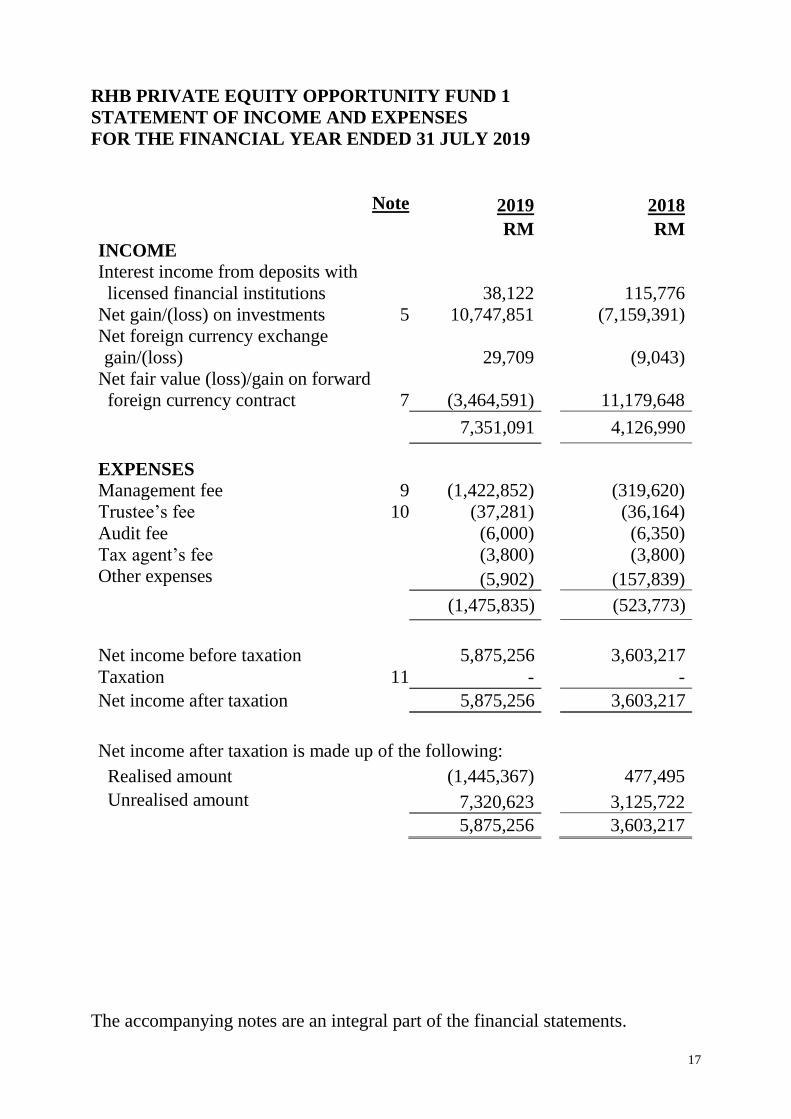

RHB PRIVATE EQUITY OPPORTUNITY FUND 1

STATEMENT OF INCOME AND EXPENSES

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

Note 2019 2018

RM RM

INCOME

Interest income from deposits with

licensed financial institutions

38,122 115,776

Net gain/(loss) on investments 5 10,747,851 (7,159,391)

Net foreign currency exchange

gain/(loss)

29,709 (9,043)

Net fair value (loss)/gain on forward

foreign currency contract

7 (3,464,591) 11,179,648

7,351,091 4,126,990

EXPENSES

Management fee 9 (1,422,852) (319,620)

Trustee’s fee 10 (37,281) (36,164)

Audit fee (6,000) (6,350)

Tax agent’s fee (3,800) (3,800)

Other expenses (5,902) (157,839)

(1,475,835) (523,773)

Net income before taxation 5,875,256 3,603,217

Taxation 11 - -

Net income after taxation 5,875,256 3,603,217

Net income after taxation is made up of the following:

Realised amount (1,445,367) 477,495

Unrealised amount 7,320,623 3,125,722

5,875,256 3,603,217

The accompanying notes are an integral part of the financial statements.

18

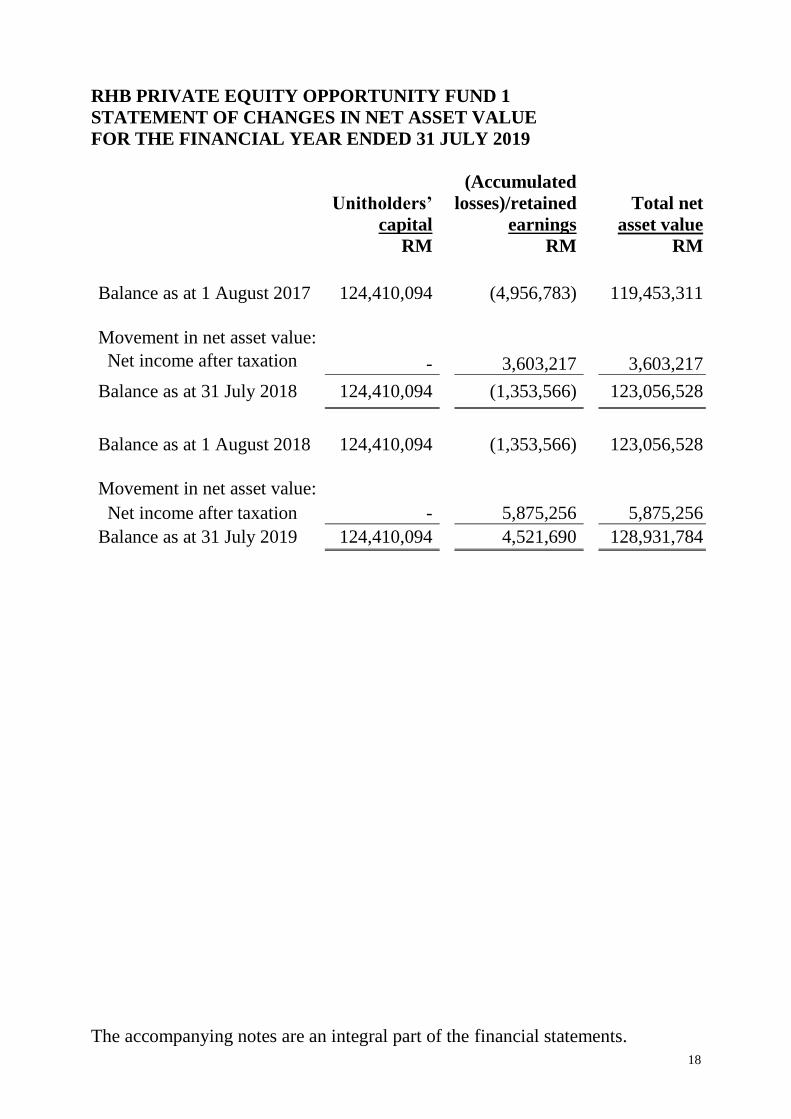

RHB PRIVATE EQUITY OPPORTUNITY FUND 1

STATEMENT OF CHANGES IN NET ASSET VALUE

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

Unitholders’

capital

(Accumulated

losses)/retained

earnings

Total net

asset value

RM RM RM

Balance as at 1 August 2017 124,410,094 (4,956,783) 119,453,311

Movement in net asset value:

Net income after taxation - 3,603,217 3,603,217

Balance as at 31 July 2018 124,410,094 (1,353,566) 123,056,528

Balance as at 1 August 2018 124,410,094 (1,353,566) 123,056,528

Movement in net asset value:

Net income after taxation - 5,875,256 5,875,256

Balance as at 31 July 2019 124,410,094 4,521,690 128,931,784

The accompanying notes are an integral part of the financial statements.

19

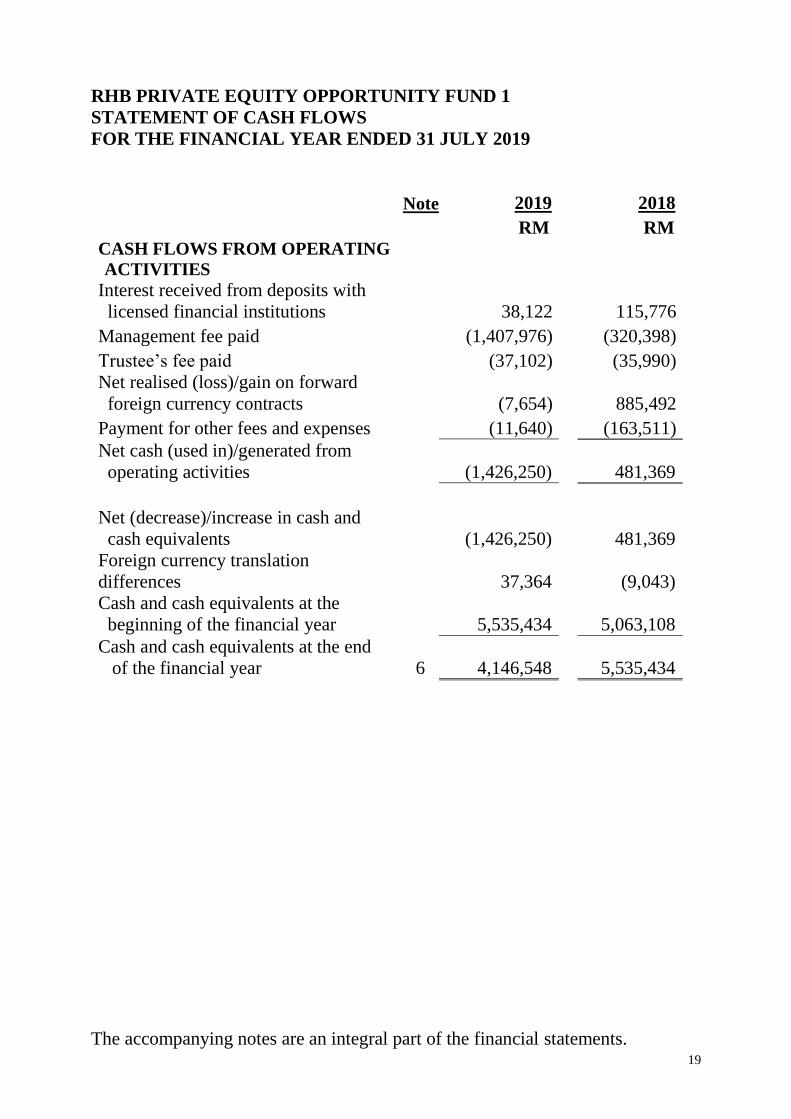

RHB PRIVATE EQUITY OPPORTUNITY FUND 1

STATEMENT OF CASH FLOWS

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

Note 2019

2018

RM RM

CASH FLOWS FROM OPERATING

ACTIVITIES

Interest received from deposits with

licensed financial institutions 38,122

115,776

Management fee paid (1,407,976) (320,398)

Trustee’s fee paid (37,102) (35,990)

Net realised (loss)/gain on forward

foreign currency contracts (7,654)

885,492

Payment for other fees and expenses (11,640) (163,511)

Net cash (used in)/generated from

operating activities

(1,426,250)

481,369

Net (decrease)/increase in cash and

cash equivalents

(1,426,250)

481,369

Foreign currency translation

differences

37,364

(9,043)

Cash and cash equivalents at the

beginning of the financial year

5,535,434

5,063,108

Cash and cash equivalents at the end

of the financial year 6 4,146,548

5,535,434

The accompanying notes are an integral part of the financial statements.

20

RHB PRIVATE EQUITY OPPORTUNITY FUND 1

NOTES TO THE FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

1 THE FUND, THE MANAGER AND THEIR PRINCIPAL ACTIVITIES

The RHB Private Equity Opportunity Fund 1 (hereinafter referred to as “the Fund”)

was constituted pursuant to the execution of a Deed dated 18 July 2016 (hereinafter

referred to as “the Deed”) between RHB Asset Management Sdn Bhd (“the

Manager”) and SCBMB Trustee Berhad (“the Trustee”).

The Fund was launched on 28 July 2016 and will continue its operations until

terminated according to the conditions provided in the Deed. The principal activity

of the Fund is to invest in ‘Permitted Investments’ as defined under the Deed.

The Fund is a feeder fund that invests in the USD denominated shares of one target

fund, i.e. RHB Private Equity Fund I (“the Company”). The Company is an

exempted company with limited liability incorporated in the Cayman Islands on 3

May 2016 under the company law of the Cayman Islands. The Company is

regulated by the Cayman Islands Registrar of Companies.

All investments will be subject to the Securities Commission Malaysia’s (“SC”)

Guidelines on Unlisted Capital Market Products under the Lodge and Launch

Framework, SC requirements, the Deeds, except where exemptions or variations

have been approved by the SC, internal policies and procedures and objective of

the Fund.

The main objective of the Fund is to provide long term capital appreciation by

investing in the shares of one target fund, i.e. RHB Private Equity Fund I.

The Manager, a company incorporated in Malaysia, is a wholly-owned subsidiary

of RHB Investment Bank Berhad, effective 6 January 2003. Its principal activities

include rendering of investment management services, management of unit trust

funds and private retirement schemes and provision of investment advisory

services.

These financial statements were authorised for issue by the Manager on 23

September 2019.

21

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

2.1 Basis of preparation of the financial statements

The financial statements have been prepared under the historical cost convention,

as modified by the financial assets and financial liabilities (including derivative

instruments) at fair value through profit or loss, except as disclosed in the summary

of significant accounting policies, and in accordance with Malaysian Financial

Reporting Standards (“MFRS”) and International Financial Reporting Standards

(“IFRS”).

The preparation of financial statements in conformity with MFRS and IFRS

requires the use of certain critical accounting estimates and assumptions that affect

the reported amounts of assets and liabilities and disclosure of contingent assets

and liabilities at the date of the financial statements, and the reported amounts of

income and expenses during the financial year. It also requires the Manager to

exercise its judgement in the process of applying the Fund’s accounting policies.

Although these estimates and judgement are based on the Manager’s best

knowledge of current events and actions, actual results may differ.

(a) The Fund has applied the following standard and interpretation to the

existing standard for the first time for the financial year beginning on 1

August 2018:

MFRS 9 ‘Financial Instruments’

IC Interpretation 22 ‘Foreign Currency Transactions and Advance

Consideration’

The Fund applied MFRS 9 ‘Financial Instruments’ for the first time in the

2019 financial statements with the date of initial application of 1 August

2018. The standard is applied retrospectively.

In accordance with the transitional provisions provided in MFRS 9,

comparative information for 31 July 2018 was not restated and continued to

be reported under the previous accounting policies governed under MFRS

139. The cumulative effects of initially applying MFRS 9 were recognised

as an adjustment to the opening balance of retained earnings as at 1 August

2018.

The detailed impact of the change in accounting policy on financial

instruments is disclosed in Note 2.2.

Other than that, the adoption of interpretation to the existing standard above

did not have any impact on the current year or any prior period and is not

likely to affect future periods.

22

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.1 Basis of preparation of the financial statements (continued)

(b) The amendments to published standard and interpretation to existing

standard which are relevant to the Fund but not yet effective and have not

been early adopted are as follows:

(i) Financial year beginning on/after 1 August 2019

IC Interpretation 23 ‘Uncertainty over Income Tax Treatments’

(effective 1 January 2019) provides guidance on how to recognise

and measure deferred and current income tax assets and liabilities

where there is uncertainty over a tax treatment.

If an entity concludes that it is not probable that the tax treatment

will be accepted by the tax authority, the effect of the tax

uncertainty should be included in the period when such

determination is made. An entity shall measure the effect of

uncertainty using the method which best predicts the resolution of

the uncertainty.

IC Interpretation 23 will be applied retrospectively.

Annual Improvements to MFRSs 2015 – 2017 Cycle: Amendments

to MFRS 112 ‘Income Taxes’ (effective from 1 January 2019)

clarify that where income tax consequences of dividends on

financial instruments classified as equity is recognised (either in

profit or loss, other comprehensive income or equity) depends on

where the past transactions that generated distributable profits were

recognised. Accordingly, the tax consequences are recognised in

profit or loss when an entity determines payments on such

instruments are distribution of profits (that is, dividends). Tax on

dividend should not be recognised in equity merely on the basis that

it is related to a distribution to owners.

The adoption of the amendments to published standard and interpretation to

existing standard do not give rise to any material impact on the financial

statements of the Fund.

23

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.2 Financial assets

Classification

From 1 August 2018, the Fund classifies its financial assets in the following

measurement categories:

those to be measured subsequently at fair value through profit or loss, and

those to be measured at amortised cost

The Fund classifies its investments based on both the Fund’s business model for

managing those financial assets and the contractual cash flow characteristics of the

financial assets. The portfolio of financial assets is managed and performance is

evaluated on a fair value basis. The Fund is primarily focused on fair value

information and uses that information to assess the assets’ performance and to

make decisions. The Fund has not taken the option to irrevocably designate any

equity securities as fair value through other comprehensive income. The

contractual cash flows of the Fund’s debt securities are solely principal and

interest, however, these securities are neither held for the purpose of collecting

contractual cash flows nor held both for collecting contractual cash flows and for

sale. The collection of contractual cash flows is only incidental to achieving the

Fund’s business model’s objective. Consequently, all investments and derivatives

are measured at fair value through profit or loss.

The Fund classifies cash and cash equivalents at amortised cost as these financial

assets are held to collect contractual cash flows consisting of the amount

outstanding.

Up to 31 July 2018, financial assets are designated as fair value through profit or

loss when they are managed and their performance are evaluated on a fair value

basis.

The Fund designates its investment in private equity investment as financial assets

at fair value through profit or loss at inception.

Derivatives are financial assets at fair value through profit or loss categorised as

held for trading unless they are designated hedges.

Loans and receivables are non-derivative financial assets with fixed or

determinable payments that are not quoted in an active market and have been

included in current assets. The Fund’s loans and receivables comprise cash and

cash equivalents which are all due within 12 months.

24

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.2 Financial assets (continued)

Recognition and measurement

Regular purchases and sales of financial assets are recognised on the trade date -

the date on which the Fund commits to purchase or sell the asset. Financial assets

and financial liabilities at fair value through profit or loss are initially recognised

at fair value.

Financial assets are de-recognised when the rights to receive cash flows from the

investments have expired or the Fund has transferred substantially all risks and

rewards of ownership.

Subsequent to initial recognition, all financial assets at fair value through profit or

loss are measured at fair value. Gains or losses arising from changes in the fair

value of the ‘financial assets at fair value through profit or loss’ category are

presented in statement of income and expenses in the period in which they arise.

Private equity investment are valued based on the last published net asset value per

unit or share of such private equity investment at end of each financial year.

In accordance with the Amended and Restated Private Placement Memorandum

dated 3 July 2017 of the Target Fund, the net asset value and net asset value per

unit of the Target Fund is calculated by the administrator of the Target Fund once

every quarter on the last business day of each quarter. The net asset value per unit

of the Target Fund is published once every quarter and the published price

thereafter will remain the same until the next valuation takes place.

Derivative investments are forward foreign currency contract. Financial derivative

position will be “marked to market” at the close of each valuation day. Foreign

exchange gains and losses on the derivative financial instrument are recognised in

statement of income and expenses when settled or at the date of the statement of

financial position at which they are included in the measurement of the derivative

financial instrument.

Financial assets at amortised cost (2018: loans and receivables) are subsequently

carried at amortised cost using the effective interest method.

25

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.2 Financial assets (continued)

Impairment of financial assets

From 1 August 2018 onwards, the Fund measures credit risk and expected credit

losses using probability of default, exposure at default and loss given default.

Management considers both historical analysis and forward looking information

in determining any expected credit loss. Management considers the probability of

default to be close to zero as these instruments have a low risk of default and the

counterparties have a strong capacity to meet their contractual obligations in the

near term. As a result, no loss allowance has been recognised based on the 12

month expected credit losses as any such impairment would be wholly

insignificant to the Fund.

Until 31 July 2018, for assets carried at amortised cost, the Fund assesses at the

end of the financial year whether there is objective evidence that a financial asset

or group of financial assets is impaired. A financial asset or a group of financial

assets is impaired and impairment losses are incurred only if there is objective

evidence of impairment as a result of one or more events that occurred after the

initial recognition of the asset (a loss event) and that loss event (or events) has an

impact on the estimated future cash flows of the financial asset or group of

financial assets that can be reliably estimated.

Significant increase in credit risk

A significant increase in credit risk is defined by management as any contractual

payment which is more than 30 days past due or a counterparty credit rating which

has fallen below BBB/Baa.

Definition of default and credit-impaired financial assets

Any contractual payment which is more than 90 days past due is considered credit

impaired.

26

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.2 Financial assets (continued)

Write-off

The Fund writes off financial assets, in whole or in part, when it has exhausted all

practical recovery efforts and has concluded there is no reasonable expectation of

recovery. The assessment of no reasonable expectation of recovery is based on the

unavailability of debtor’s sources of income or assets to generate sufficient future

cash flows to repay the amount. The Fund may write-off financial assets that are

still subject to enforcement activity. Subsequent recoveries of amounts previously

written off will result in impairment gains. There are no write-offs/recoveries

during the financial year.

2.3 Financial liabilities

Financial liabilities are classified according to the substance of the contractual

arrangements entered into and the definitions of a financial liability.

Financial liabilities, within the scope of MFRS 139 up to 31 July 2018 and MFRS

9 from 1 August 2018, are recognised in the statement of financial position when,

and only when, the Fund becomes a party to the contractual provisions of the

financial instrument.

Derivatives are financial liabilities at fair value through profit or loss are

categorised as held for trading unless they are designated hedges.

The Fund’s financial liabilities which include accrued management fee, amount

due to Trustee and other payables and accruals are recognised initially at fair value

and subsequently measured at amortised cost using the effective interest method.

A financial liability is de-recognised when the obligation under the liability is

extinguished. Gains and losses are recognised in the statement of income and

expenses when the liabilities are de-recognised, and through the amortisation

process.

27

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.4 Unitholders’ capital

The unitholders’ contributions to the Fund meet the criteria of the definition of

puttable instruments to be classified as equity instruments under MFRS 132

“Financial Instruments: Presentation”. Those criteria include:

the units entitle the holder to a proportionate share of the Fund’s net assets

value;

the units are the most subordinated class and class features are identical;

there is no contractual obligations to deliver cash or another financial asset

other than the obligation on the Fund to repurchase; and

the total expected cash flows from the units over its life are based substantially

on the profit or loss of the Fund.

The outstanding units are carried at the redemption amount that is payable at each

financial year if the unitholders exercise the right to put the units back to the Fund.

Units are created and cancelled at prices based on the Fund’s net asset value per

unit at the time of creation or cancellation. The Fund’s net asset value per unit is

calculated by dividing the net assets attributable to unitholders with the total

number of outstanding units.

2.5 Income recognition

Interest income from deposits with licensed financial institutions is recognised on

an accrual basis using the effective interest method.

From 1 August 2018, interest income is calculated by applying the effective interest

rate to the gross carrying amount of a financial asset except for financial assets that

subsequently become credit-impaired. For credit-impaired financial assets the

effective interest rate is applied to the net carrying amount of the financial assets

(after deduction of the loss allowance).

Up till 31 July 2018, when a loan and receivable is impaired, the Fund reduces the

carrying amount to its recoverable amount, being the estimated future cash flow

discounted at the original effective interest rate of the instrument, and continue

unwinding the discount as interest income. Interest income on impaired loans and

receivables is recognised using the original effective interest rate.

Realised gain or loss on forward foreign currency contracts are measured by the

net settlement amount as per the forward foreign currency contract.

Net income or loss is the total of income less expenses.

28

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.6 Taxation

Current tax expense is determined according to Malaysian tax laws and includes

all taxes based upon the taxable income earned during the financial year.

2.7 Cash and cash equivalents

For the purpose of the statement of cash flows, cash and cash equivalents comprise

bank balances and deposits with licensed financial institutions which are subject

to an insignificant risk of changes in value.

2.8 Presentation and functional currency

Items included in the financial statements of the Fund are measured using the

currency of the primary economic environment in which the Fund operates (the

“functional currency”). The financial statements are presented in Ringgit Malaysia

(“RM”), which is the Fund’s presentation and functional currency.

Due to mixed factors in determining the functional currency of the Fund, the

Manager has used its judgement to determine the functional currency that most

faithfully represents the economic effects of the underlying transactions, events

and conditions and have determined the functional currency to be in RM primarily

due to the following factors:

The Fund maintains cash that is denominated in RM for the purpose of

making settlement of the creation and cancellation.

The Fund’s units are denominated in RM.

The Fund’s significant expenses are denominated in RM.

2.9 Foreign currency translations

Foreign currency transactions in the Fund are accounted for at exchange rates

prevailing at the transaction dates. Foreign currency monetary assets and liabilities

are translated at exchange rates prevailing at the reporting date. Exchange

differences arising from the settlement of foreign currency transactions and from

the translation of foreign currency monetary assets and liabilities are recognised in

statement of income and expenses.

29

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(CONTINUED)

2.10 Segmental information

Operating segments are reported in a manner consistent with the internal reporting

used by the chief operating decision-maker. The operating results are regularly

reviewed by the Manager and the Investment Committee. The Investment

Committee assumes the role of chief operating decision maker, for performance

assessment purposes and to make decisions about resources allocated to the

investment segment based on the recommendation by the Investment & Security

Selection Committee.

2.11 Derivative financial instruments

The Fund’s derivative financial instruments comprise unquoted forward foreign

currency contracts. Derivative financial instruments are initially recognised at fair

value on the date derivative contracts are entered into and are subsequently re-

measured at their fair value.

The fair value of forward foreign exchange contracts is determined using forward

exchange rates at the date of the statement of financial position, with the resulting

value discounted back to present value.

The method of recognising the resulting gain or loss depends on whether the

derivative financial instrument is designated as a hedging instrument, and the

nature of the item being hedged. Derivative financial instruments that do not

qualify for hedge accounting are classified as FVTPL and accounted for in

accordance with the accounting policy set out in Note 2.2.

30

3 FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

The Fund is exposed to a variety of risks, which include market risk, price risk,

interest rate risk, currency risk, credit risk, liquidity risk and capital risk.

Financial risk management is carried out through internal control processes

adopted by the Manager and adherence to the investment restrictions as stipulated

in the Information Memorandum and Unlisted Capital Market Products under the

Lodge and Launch Framework.

Market risk

Market risk is a risk that arises when the prices of investments in the market place

are affected by circumstances such as general market or economic events. These

circumstances, which may be a local or global event, can affect a local market

where the Target Fund is invested in or global markets and subsequently, the value

of the Target Fund’s investments.

Price risk

Price risk is the risk that the fair value of an investment of the Fund will fluctuate

because of changes in market prices.

The Fund is exposed to private equity investment price risk (other than those arising

from interest risk) for its investments of RM116,988,800 (2018: RM106,240,949).

The sensitivity analysis is based on the assumption that the price of the investments

fluctuate by +/(-) 5% with all other variables held constant, the impact on statement

of income and expenses and net asset value is +/(-) RM5,849,440 (2018:

RM5,312,047).

Interest rate risk

Interest rate risk is the risk that the value of the Fund’s investments and its return

will fluctuate because of changes in market interest rates. The Fund’s exposure to

the interest rate risk is mainly confined to short term placements with financial

institutions. The Manager overcomes the exposure by way of maintaining deposits

on short term basis. Therefore, exposure to interest rate fluctuations is minimal.

31

3 FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED)

Currency risk

The Fund invests in the Target Fund which is denominated in United States Dollar

(“USD”). Fluctuations in foreign exchange rate between USD and Ringgit

Malaysia will affect the value of the Fund’s foreign investments when converted to

local currency and subsequently the value of unitholders’ investment. As such, the

performance of the Fund will also be affected by the movements in the exchange

rate between USD and Ringgit Malaysia.

The sensitivity analysis is based on the assumption that the foreign exchange rate

fluctuates by +/(-) 5% with all other variable held constant, the impact on statement

of income and expenses and net asset value is +RM1,369,541/-RM1,330,674

(2018: +/-RM1,219,943).

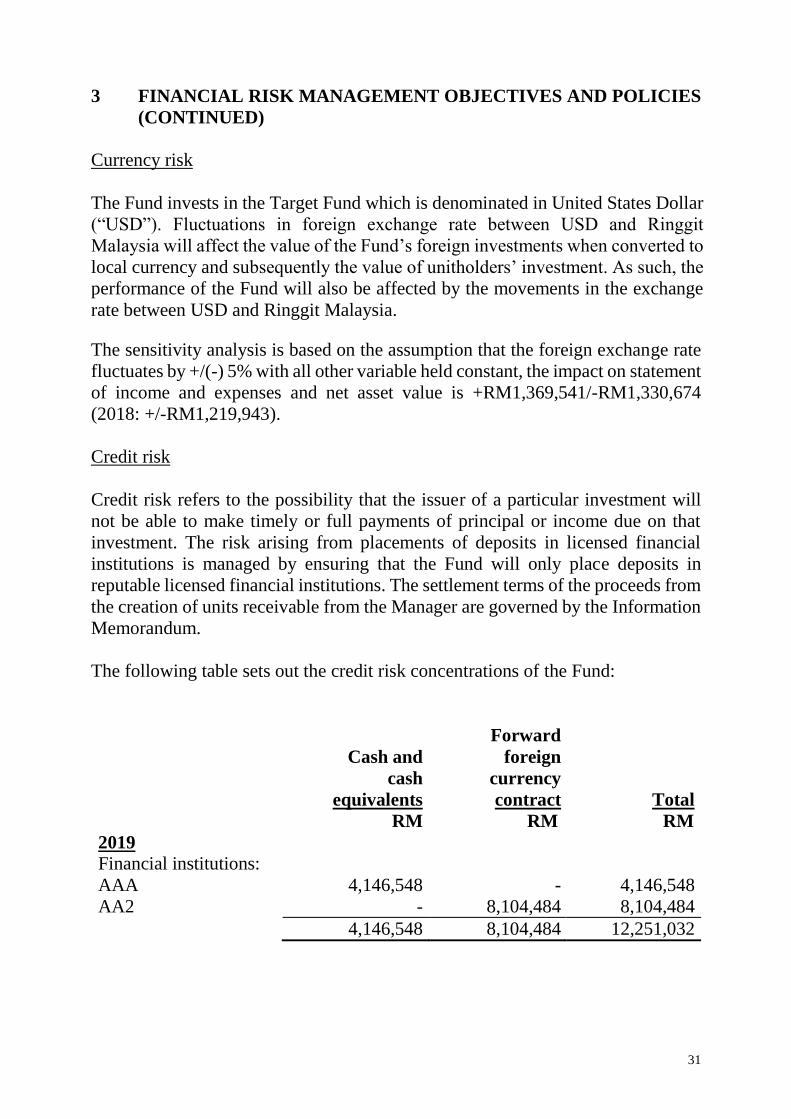

Credit risk

Credit risk refers to the possibility that the issuer of a particular investment will

not be able to make timely or full payments of principal or income due on that

investment. The risk arising from placements of deposits in licensed financial

institutions is managed by ensuring that the Fund will only place deposits in

reputable licensed financial institutions. The settlement terms of the proceeds from

the creation of units receivable from the Manager are governed by the Information

Memorandum.

The following table sets out the credit risk concentrations of the Fund:

Cash and

cash

equivalents

Forward

foreign

currency

contract

Total

RM RM RM

2019

Financial institutions:

AAA 4,146,548 - 4,146,548

AA2 - 8,104,484 8,104,484

4,146,548 8,104,484 12,251,032

32

3 FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED)

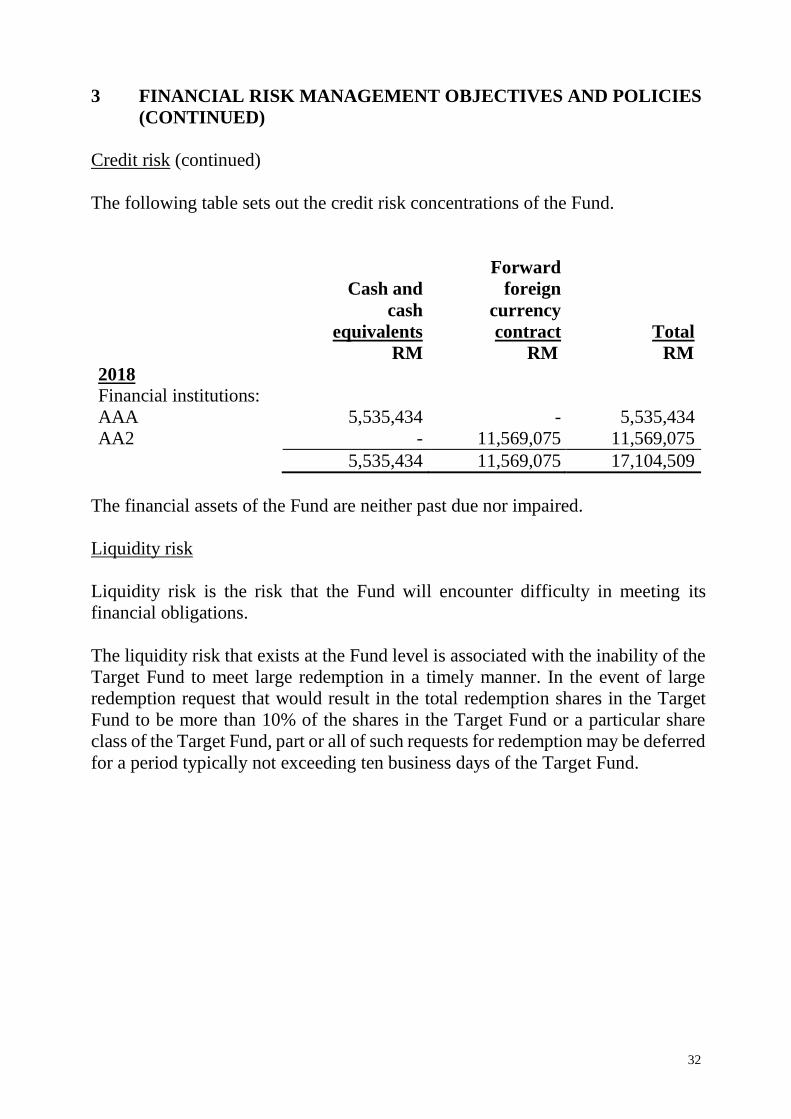

Credit risk (continued)

The following table sets out the credit risk concentrations of the Fund.

Cash and

cash

equivalents

Forward

foreign

currency

contract

Total

RM RM RM

2018

Financial institutions:

AAA 5,535,434 - 5,535,434

AA2 - 11,569,075 11,569,075

5,535,434 11,569,075 17,104,509

The financial assets of the Fund are neither past due nor impaired.

Liquidity risk

Liquidity risk is the risk that the Fund will encounter difficulty in meeting its

financial obligations.

The liquidity risk that exists at the Fund level is associated with the inability of the

Target Fund to meet large redemption in a timely manner. In the event of large

redemption request that would result in the total redemption shares in the Target

Fund to be more than 10% of the shares in the Target Fund or a particular share

class of the Target Fund, part or all of such requests for redemption may be deferred

for a period typically not exceeding ten business days of the Target Fund.

33

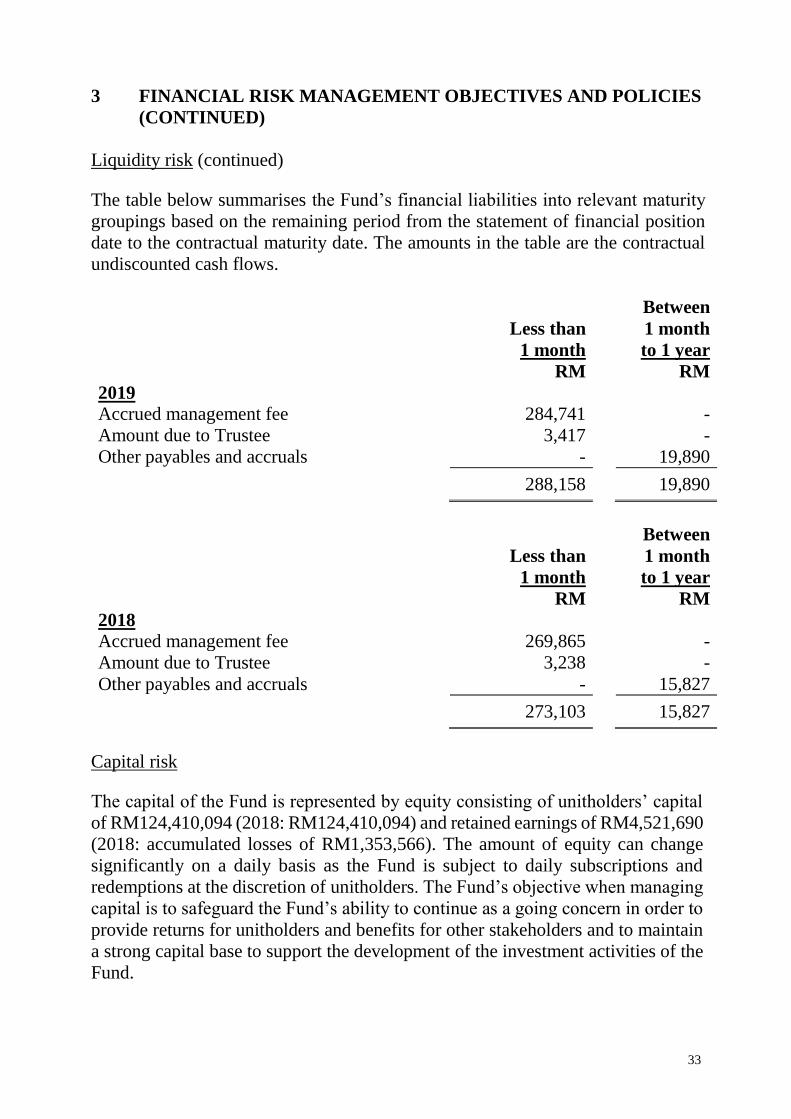

3 FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED)

Liquidity risk (continued)

The table below summarises the Fund’s financial liabilities into relevant maturity

groupings based on the remaining period from the statement of financial position

date to the contractual maturity date. The amounts in the table are the contractual

undiscounted cash flows.

Less than

1 month

Between

1 month

to 1 year

RM RM

2019

Accrued management fee 284,741 -

Amount due to Trustee 3,417 -

Other payables and accruals - 19,890

288,158 19,890

Less than

1 month

Between

1 month

to 1 year

RM RM

2018

Accrued management fee 269,865 -

Amount due to Trustee 3,238 -

Other payables and accruals - 15,827

273,103 15,827

Capital risk

The capital of the Fund is represented by equity consisting of unitholders’ capital

of RM124,410,094 (2018: RM124,410,094) and retained earnings of RM4,521,690

(2018: accumulated losses of RM1,353,566). The amount of equity can change

significantly on a daily basis as the Fund is subject to daily subscriptions and

redemptions at the discretion of unitholders. The Fund’s objective when managing

capital is to safeguard the Fund’s ability to continue as a going concern in order to

provide returns for unitholders and benefits for other stakeholders and to maintain

a strong capital base to support the development of the investment activities of the

Fund.

34

4 FAIR VALUE ESTIMATION

Fair value is defined as the price that would be received to sell an asset or paid to

transfer a liability in an orderly transaction between market participants at the

measurement date (i.e. an exit price).

The fair value of financial assets and liabilities traded in an active market (such as

publicly traded derivatives and trading securities) are based on quoted market prices

at the close of trading on the financial year end date.

An active market is a market in which transactions for the assets or liabilities take

place with sufficient frequency and volume to provide pricing information on an

ongoing basis.

The fair value of financial assets that are not traded in an active market is

determined by using valuation techniques. The Fund uses a variety of methods and

makes assumptions that are based on market conditions existing at each financial

year end date. Valuation techniques used for non-standardised financial instruments

such as options, currency swaps and other over-the-counter derivatives, include the

use of comparable recent transactions, reference to other instruments that are

substantially the same, discounted cash flow analysis, option pricing models and

other valuation techniques commonly used by market participants making the

maximum use of market inputs and relying as little as possible on entity-specific

inputs.

The fair values are based on the following methodologies and assumptions:

(i) For bank balances and deposits with licensed financial institutions with

maturities less than 1 year, the carrying value is a reasonable estimate of fair

value.

(ii) The carrying value less impairment of receivables and payables are assumed

to approximate their fair values due to their short term nature.

35

4 FAIR VALUE ESTIMATION (CONTINUED)

Fair value hierarchy

The Fund adopted MFRS 13 “Fair Value Measurement” in respect of disclosures

about the degree of reliability of fair value measurement. This requires the Fund to

classify fair value measurements using a fair value hierarchy that reflects the

significance of the inputs used in making the measurements. The fair value

hierarchy has the following levels:

Level 1: Quoted prices (unadjusted) in active market for identical assets or

liabilities

Level 2: Inputs other than quoted prices included within level 1 that are

observable for the asset or liability, either directly (that is, as prices) or

indirectly (that is, derived from prices)

Level 3: Inputs for the asset and liability that are not based on observable

market data (that is, unobservable inputs)

The following table analyses within the fair value hierarchy the Fund’s financial

assets at fair value through profit or loss (by class) measured at fair value:

Level 1 Level 2 Level 3 Total

RM RM RM RM

2019

Investments:

- - Private equity

investment - foreign 116,988,800 - - 116,988,800

- Derivative instruments:

- - Forward foreign

currency contract - 8,104,484 - 8,104,484

- 116,988,800 8,104,484 - 125,093,284

36

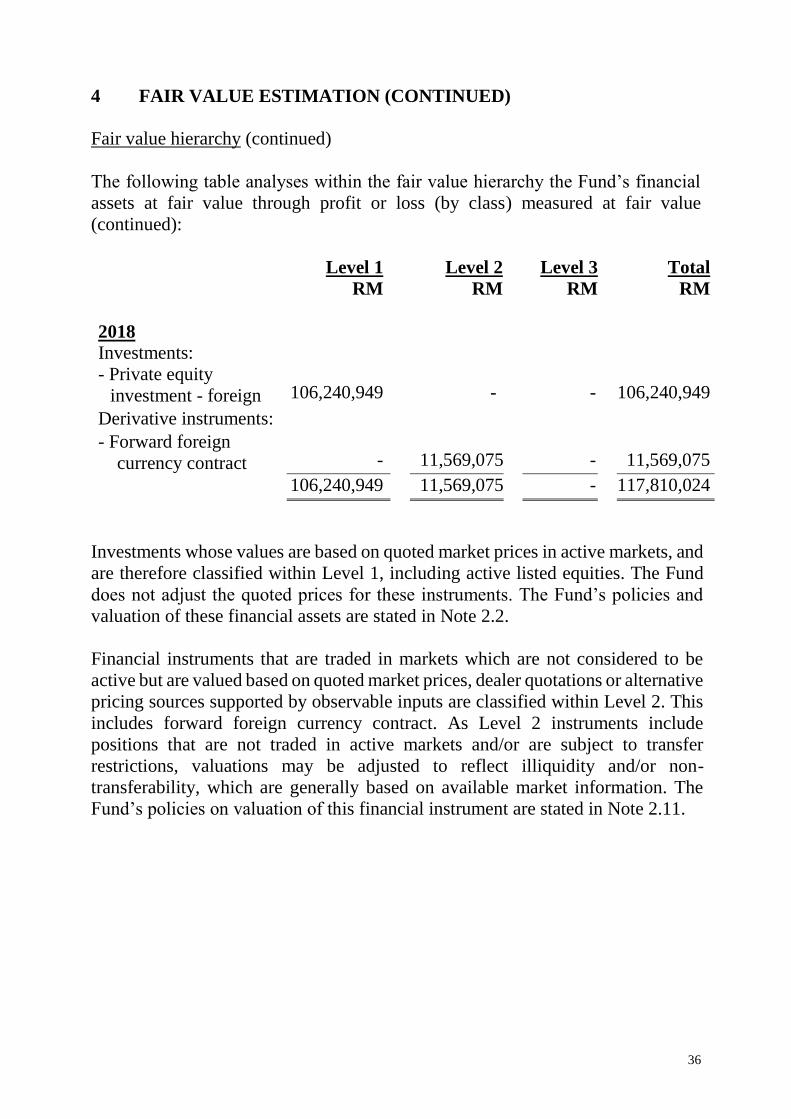

4 FAIR VALUE ESTIMATION (CONTINUED)

Fair value hierarchy (continued)

The following table analyses within the fair value hierarchy the Fund’s financial

assets at fair value through profit or loss (by class) measured at fair value

(continued):

Level 1 Level 2 Level 3 Total

RM RM RM RM

2018

Investments:

- - Private equity

investment - foreign 106,240,949 - - 106,240,949

- Derivative instruments:

- - Forward foreign

currency contract - 11,569,075 - 11,569,075

- 106,240,949 11,569,075 - 117,810,024

Investments whose values are based on quoted market prices in active markets, and

are therefore classified within Level 1, including active listed equities. The Fund

does not adjust the quoted prices for these instruments. The Fund’s policies and

valuation of these financial assets are stated in Note 2.2.

Financial instruments that are traded in markets which are not considered to be

active but are valued based on quoted market prices, dealer quotations or alternative

pricing sources supported by observable inputs are classified within Level 2. This

includes forward foreign currency contract. As Level 2 instruments include

positions that are not traded in active markets and/or are subject to transfer

restrictions, valuations may be adjusted to reflect illiquidity and/or non-

transferability, which are generally based on available market information. The

Fund’s policies on valuation of this financial instrument are stated in Note 2.11.

37

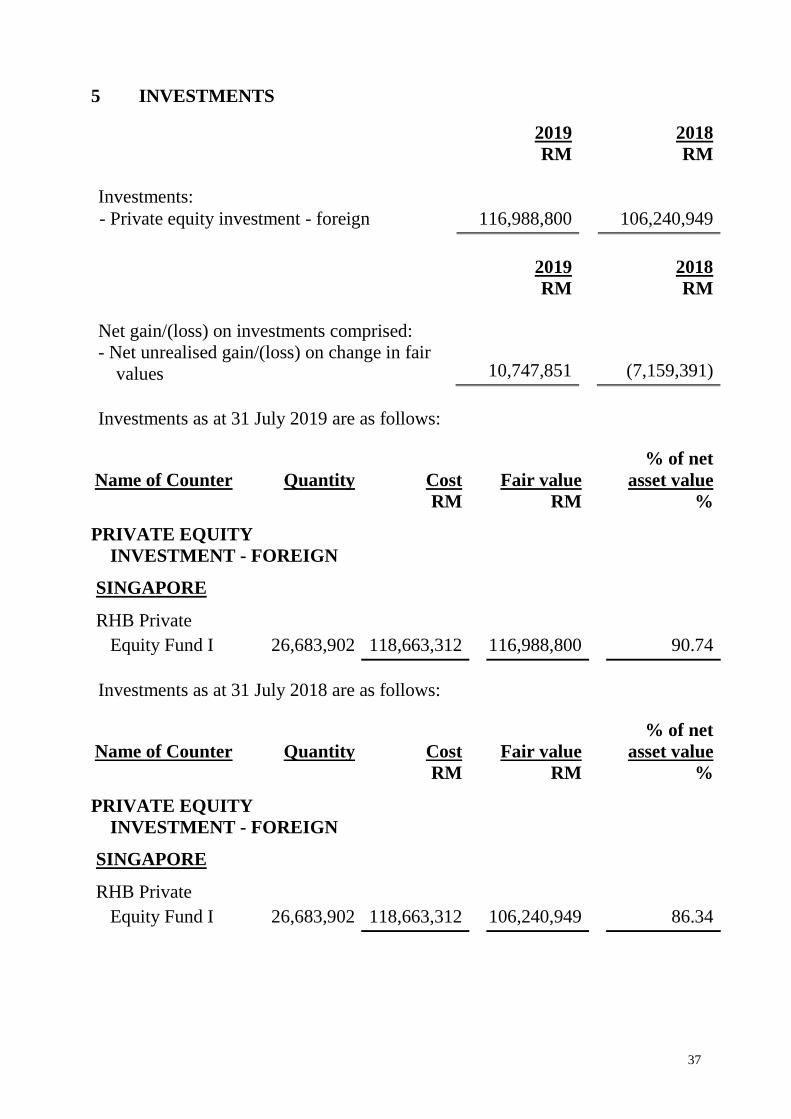

5 INVESTMENTS

2019 2018

RM RM

Investments:

- Private equity investment - foreign 116,988,800 106,240,949

2019 2018 RM RM

Net gain/(loss) on investments comprised:

- Net unrealised gain/(loss) on change in fair

values 10,747,851

(7,159,391)

Investments as at 31 July 2019 are as follows:

Name of Counter Quantity Cost

Fair value

% of net

asset value

RM RM %

PRIVATE EQUITY

INVESTMENT - FOREIGN

SINGAPORE

RHB Private

Equity Fund I 26,683,902 118,663,312

116,988,800

90.74

Investments as at 31 July 2018 are as follows:

Name of Counter Quantity Cost

Fair value

% of net

asset value

RM RM %

PRIVATE EQUITY

INVESTMENT - FOREIGN

SINGAPORE

RHB Private

Equity Fund I 26,683,902 118,663,312

106,240,949

86.34

38

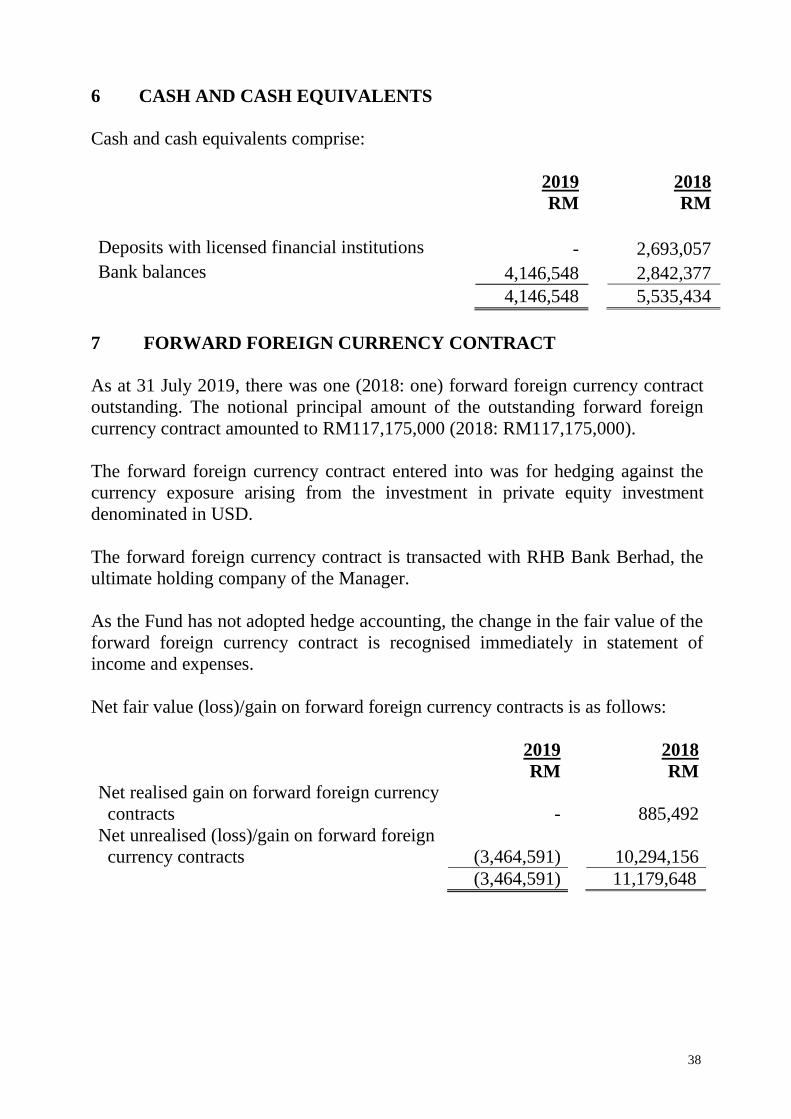

6 CASH AND CASH EQUIVALENTS

Cash and cash equivalents comprise:

2019 2018

RM RM

Deposits with licensed financial institutions - 2,693,057

Bank balances 4,146,548 2,842,377

4,146,548 5,535,434

7 FORWARD FOREIGN CURRENCY CONTRACT

As at 31 July 2019, there was one (2018: one) forward foreign currency contract

outstanding. The notional principal amount of the outstanding forward foreign

currency contract amounted to RM117,175,000 (2018: RM117,175,000).

The forward foreign currency contract entered into was for hedging against the

currency exposure arising from the investment in private equity investment

denominated in USD.

The forward foreign currency contract is transacted with RHB Bank Berhad, the

ultimate holding company of the Manager.

As the Fund has not adopted hedge accounting, the change in the fair value of the

forward foreign currency contract is recognised immediately in statement of

income and expenses.

Net fair value (loss)/gain on forward foreign currency contracts is as follows:

2019 2018

RM RM

Net realised gain on forward foreign currency

contracts

-

885,492

Net unrealised (loss)/gain on forward foreign

currency contracts

(3,464,591)

10,294,156

(3,464,591) 11,179,648

39

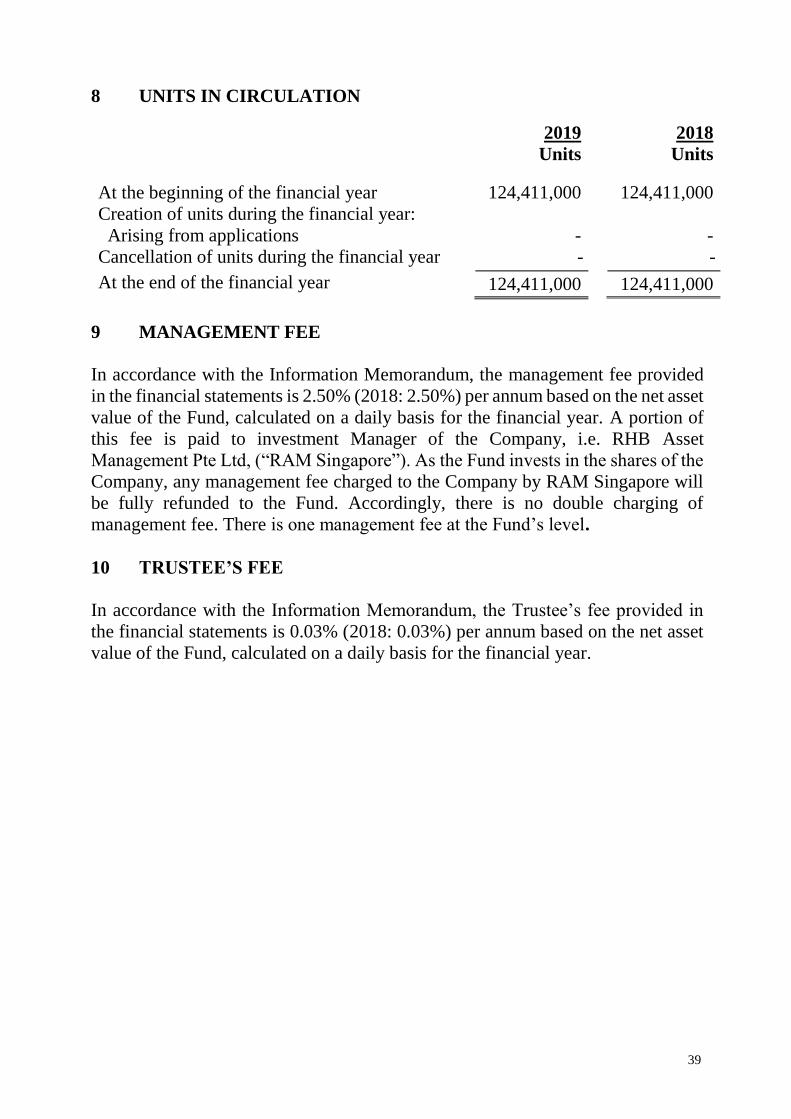

8 UNITS IN CIRCULATION

2019 2018

Units Units

At the beginning of the financial year 124,411,000 124,411,000

Creation of units during the financial year:

Arising from applications - -

Cancellation of units during the financial year - -

At the end of the financial year 124,411,000 124,411,000

9 MANAGEMENT FEE

In accordance with the Information Memorandum, the management fee provided

in the financial statements is 2.50% (2018: 2.50%) per annum based on the net asset

value of the Fund, calculated on a daily basis for the financial year. A portion of

this fee is paid to investment Manager of the Company, i.e. RHB Asset

Management Pte Ltd, (“RAM Singapore”). As the Fund invests in the shares of the

Company, any management fee charged to the Company by RAM Singapore will

be fully refunded to the Fund. Accordingly, there is no double charging of

management fee. There is one management fee at the Fund’s level.

10 TRUSTEE’S FEE

In accordance with the Information Memorandum, the Trustee’s fee provided in

the financial statements is 0.03% (2018: 0.03%) per annum based on the net asset

value of the Fund, calculated on a daily basis for the financial year.

40

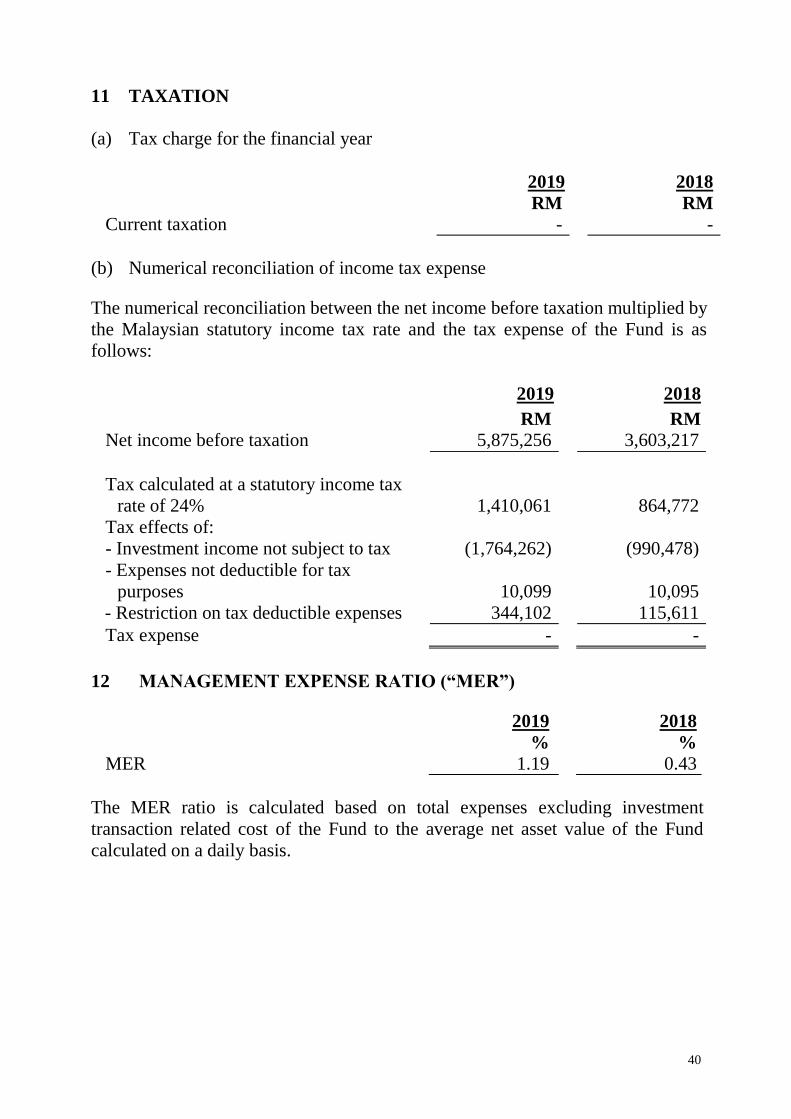

11 TAXATION

(a) Tax charge for the financial year

2019 2018

RM RM

Current taxation - -

(b) Numerical reconciliation of income tax expense

The numerical reconciliation between the net income before taxation multiplied by

the Malaysian statutory income tax rate and the tax expense of the Fund is as

follows:

2019 2018

RM RM

Net income before taxation 5,875,256 3,603,217

Tax calculated at a statutory income tax

rate of 24%

1,410,061

864,772

Tax effects of:

- Investment income not subject to tax (1,764,262) (990,478)

- Expenses not deductible for tax

purposes

10,099

10,095

- Restriction on tax deductible expenses 344,102 115,611

Tax expense - -

12 MANAGEMENT EXPENSE RATIO (“MER”)

2019 2018

% %

MER 1.19 0.43

The MER ratio is calculated based on total expenses excluding investment

transaction related cost of the Fund to the average net asset value of the Fund

calculated on a daily basis.

41

13 PORTFOLIO TURNOVER RATIO (“PTR”)

2019 2018

PTR (times) - -

The PTR ratio is calculated based on average of acquisition and disposals of the

Fund for the financial year to the average net asset value of the Fund calculated on

a daily basis.

14 UNITS HELD BY THE MANAGER AND PARTIES RELATED TO

THE MANAGER

The number of units held by the Manager is as follows:

2019 2018

Units RM Units RM

The Manager 2,726 2,825 2,726 2,696

The units are held beneficially by the Manager for booking purposes. The Manager

is of the opinion that all transactions with the related parties have been entered into

in the normal course of business at agreed terms between the related parties.

Other than the above, there were no units held by Directors or parties related to the

Manager.

The holding company and the ultimate holding company of the Manager is RHB

Investment Bank Berhad and RHB Bank Berhad respectively. The Manager treats

RHB Bank Berhad group of companies including RHB Investment Bank Berhad

and its subsidiaries as related parties.

15 TRANSACTIONS BY THE FUND

There were no transactions by the Fund for the financial year ended 31 July 2019

and 31 July 2018.

42

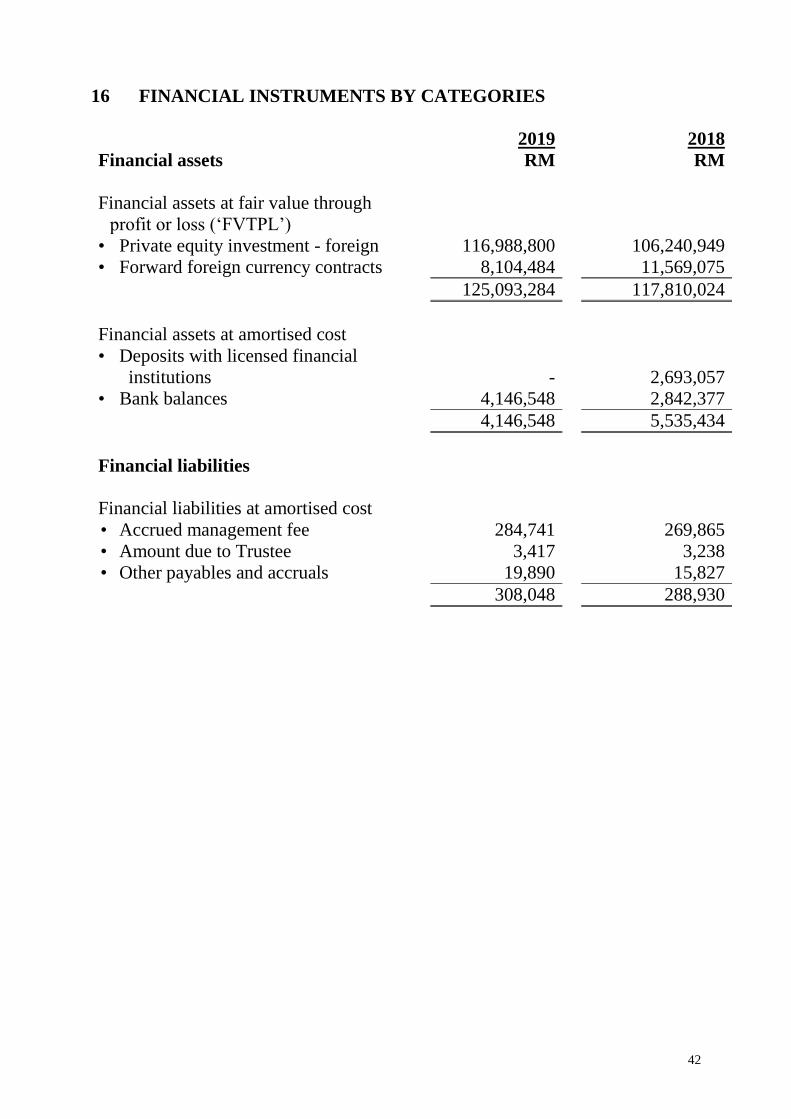

16 FINANCIAL INSTRUMENTS BY CATEGORIES

2019 2018

Financial assets RM RM

Financial assets at fair value through

profit or loss (‘FVTPL’)

• Private equity investment - foreign 116,988,800 106,240,949

• Forward foreign currency contracts 8,104,484 11,569,075

125,093,284 117,810,024

Financial assets at amortised cost

• Deposits with licensed financial

institutions

-

2,693,057

• Bank balances 4,146,548 2,842,377

4,146,548 5,535,434

Financial liabilities

Financial liabilities at amortised cost

• Accrued management fee 284,741 269,865

• Amount due to Trustee 3,417 3,238

• Other payables and accruals 19,890 15,827

308,048 288,930

43

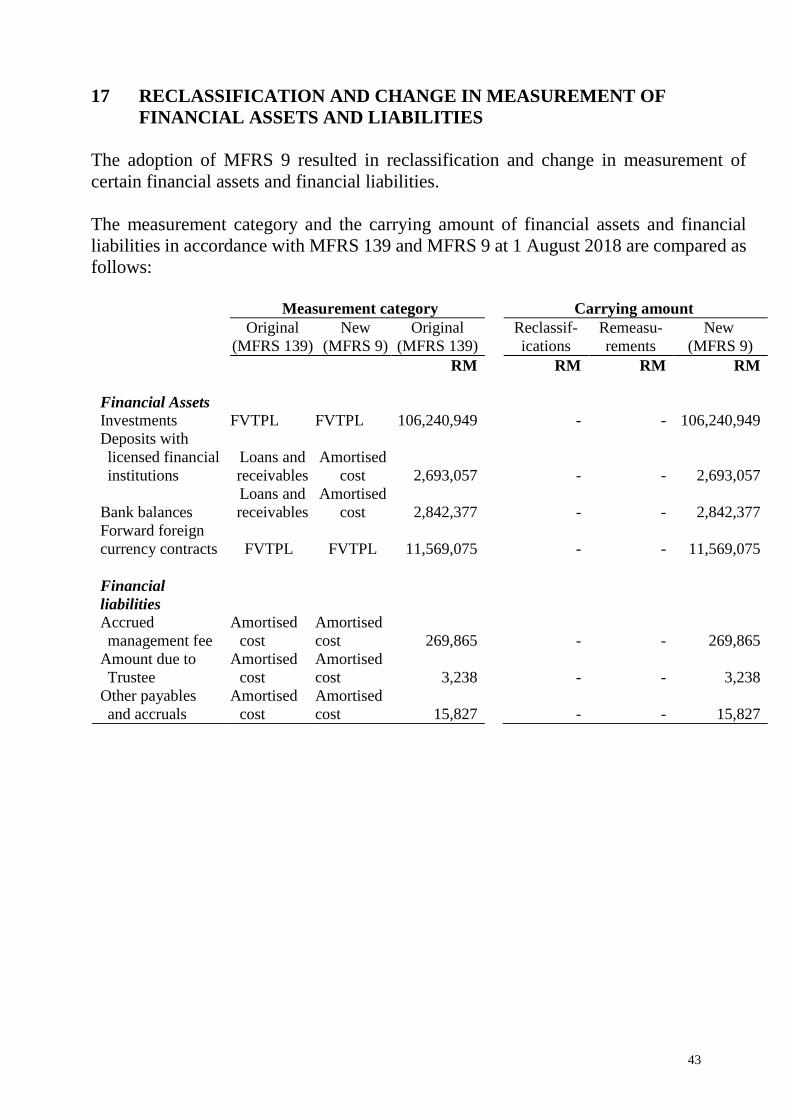

17 RECLASSIFICATION AND CHANGE IN MEASUREMENT OF

FINANCIAL ASSETS AND LIABILITIES

The adoption of MFRS 9 resulted in reclassification and change in measurement of

certain financial assets and financial liabilities.

The measurement category and the carrying amount of financial assets and financial

liabilities in accordance with MFRS 139 and MFRS 9 at 1 August 2018 are compared as

follows:

Measurement category Carrying amount

Original

(MFRS 139)

New

(MFRS 9)

Original

(MFRS 139)

Reclassif-

ications

Remeasu-

rements

New

(MFRS 9)

RM RM RM RM

Financial Assets

Investments FVTPL FVTPL 106,240,949 - - 106,240,949

Deposits with

licensed financial

institutions

Loans and

receivables

Amortised

cost 2,693,057

- - 2,693,057

Bank balances

Loans and

receivables

Amortised

cost 2,842,377

- - 2,842,377

Forward foreign

currency contracts FVTPL FVTPL 11,569,075

- - 11,569,075

Financial

liabilities

Accrued

management fee

Amortised

cost

Amortised

cost 269,865

- - 269,865

Amount due to

Trustee

Amortised

cost

Amortised

cost 3,238

- - 3,238

Other payables

and accruals

Amortised

cost

Amortised

cost 15,827

- - 15,827

44

18 SEGMENT INFORMATION

The Investment & Security Selection Committee of the Manager recommends

strategic resource allocations of the Fund to the Investment Committee of the

Manager (collectively referred to as “Committee”).

The internal reporting provided to the Committee for the Fund’s assets, liabilities

and performance is prepared on a consistent basis with the measurement and

recognition principles of MFRS and IFRS. The Committee is responsible for the

Fund’s entire portfolio and considers the business to have a single operating

segment. The Committee’s asset allocation decisions are based on a single,

integrated investment strategy and the Fund’s performance is evaluated on an

overall basis.

The reportable operating segments derive their income by seeking investments to

achieve the investment objective which commensurate with an acceptable level of

risk within each portfolio. These returns consist of interest and gains on the

appreciation in the value of investments which are derived from Malaysia and

Singapore.

There were no changes in the reportable segments during the financial year.

45

STATEMENT BY MANAGER

We, Sharifatu Laila Syed Ali and Ong Yin Suen, two of the Directors of RHB

Asset Management Sdn Bhd, do hereby state that in the opinion of the Directors

of the Manager, the accompanying statement of financial position, statement of

income and expenses, statement of changes in net asset value, statement of cash

flows and the accompanying notes, are drawn up in accordance with Malaysian