Rewort No. 7869-YU Yugoslavia FinancialSector Restructuring: Policies and Priorities (In TwoVolumes) Volume II: Annexes November 30, 1989 Country Operations Department IV Europe, Middle East and North AfricaRegion FOR OFF:CIAL USE ONLY Document of the WYorld Bank This document has a restricted distribution and may be used by recipients only in the performance of their officialduties. Itscontents maynot otherwise be disclosed withoutWorldBank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Rewort No. 7869-YU

YugoslaviaFinancial Sector Restructuring:Policies and Priorities(In Two Volumes) Volume II: AnnexesNovember 30, 1989

Country Operations Department IVEurope, Middle East and North Africa Region

FOR OFF:CIAL USE ONLY

Document of the WYorld Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

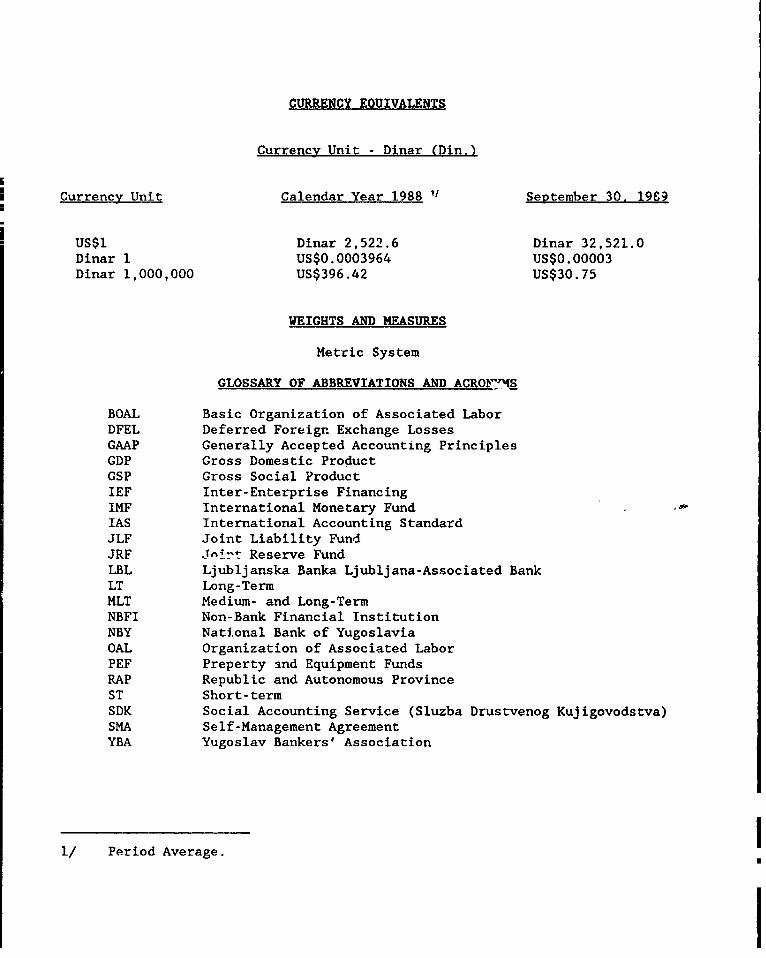

CURRENCY EOUIVALENTS

Currency Unit - Dinar (Din.)

Currency Unit Calendar Year 1988 ' September 30. 19S9

US$1 Dinar 2,522.6 Dinar 32,521.0Dinar 1 US$0.0003964 US$0.00003Dinar 1,000,000 US$396.42 US$30.75

WEIGHTS AND MEASURES

Metric System

GLOSSARY OF ABBREVIATIONS AND ACROrFMS

BOAL Basic Organization of Associated LaborDFEL Deferred Foreigr. Exchange LossesGAAP Generally Accepted Accounting PrinciplesGDP Gross Domestic ProductGSP Gross Social ProductIEF Inter-Enterprise FinancingIMF International Monetary FundIAS International Accounting StandardJLF Joint Liability FundJRF J^n"-'t Reserve FundLBL Ljubljanska Banka Ljubljana-Associated BankLT Long-TermMLT Medium- and Long-TermNBFI Non-Bank Financial InstitutionNBY National Bank of YugoslaviaOAL Organization of Associated LaborPEF Preperty and Equipment FundsRAP Republic and Autonomous ProvinceST Short-termSDK Social Accounting Service (Sluzba Drustvenog Kujigovodstva)SMA Self-Management AgreementYBA Yugoslav Bankers' Association

1/ Period Average.

l~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

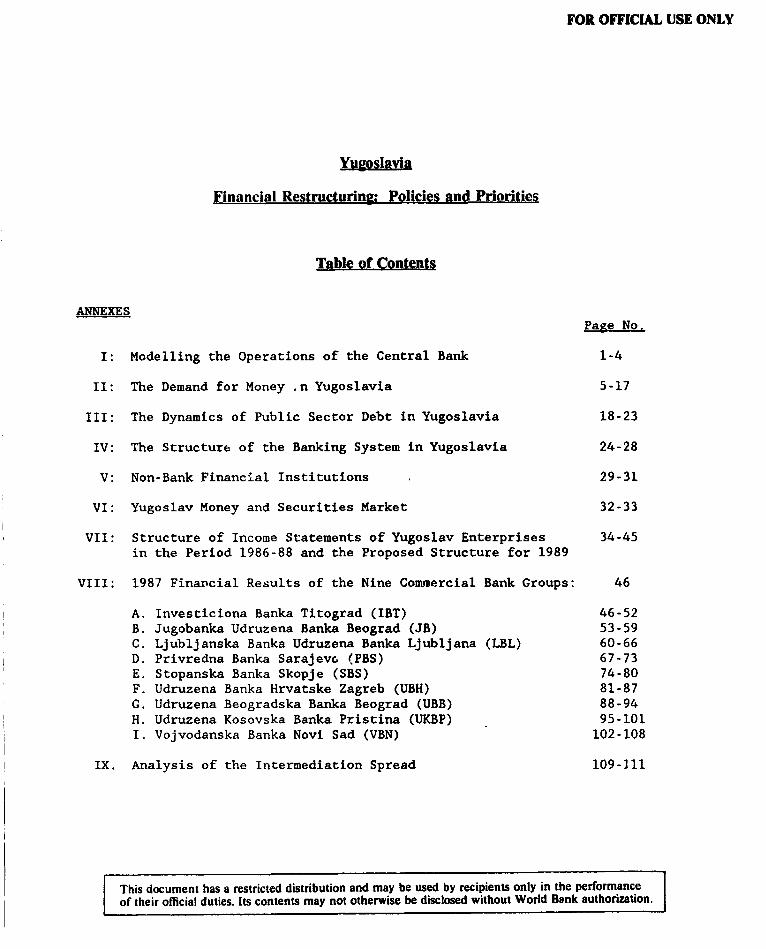

FOR OFFICIAL USE ONLY

Yugoslania

Financial Restructuring: Policies and Priorities

Table of Contents

ANNEXESPage No.

I: Modelling the Operations of the Central Bank 1-4

II: The Demand for Money .n Yugoslavia 5-17

III: The Dynamics of Public Sector Debt in Yugoslavia 18-23

IV: The Structure of the Banking System in Yugoslavia 24-28

V: Non-Bank Financial Institutions 29-31

VI: Yugoslav Money and Securities Market 32-33

VII: Structure of Income Statements of Yugoslav Enterprises 34-45in the Period 1986-88 and the Proposed Structure for 1989

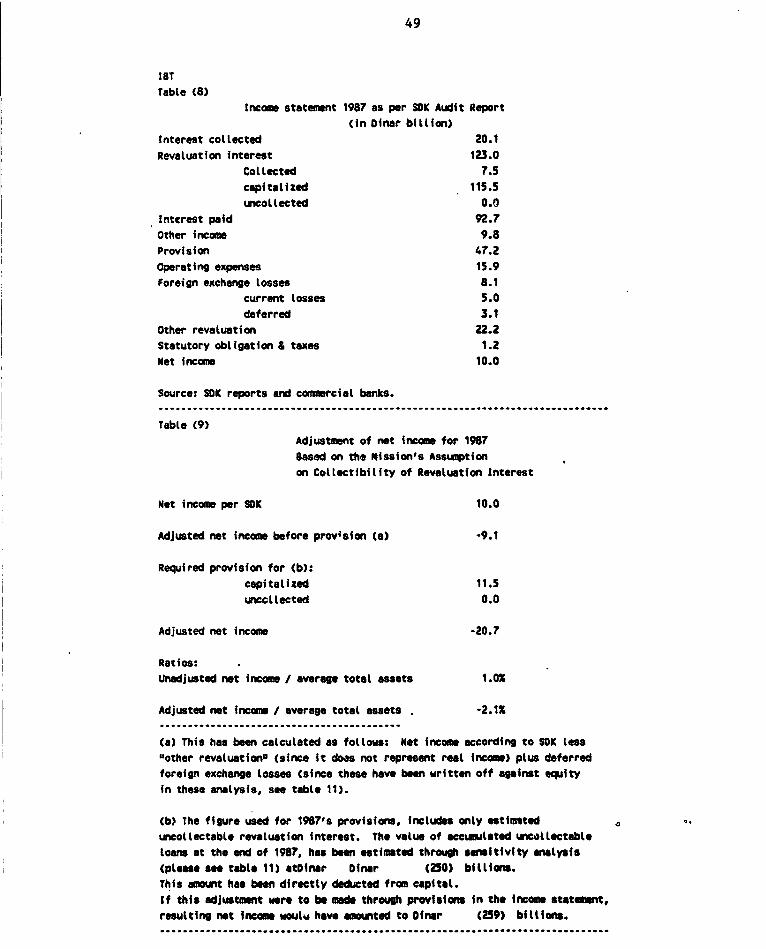

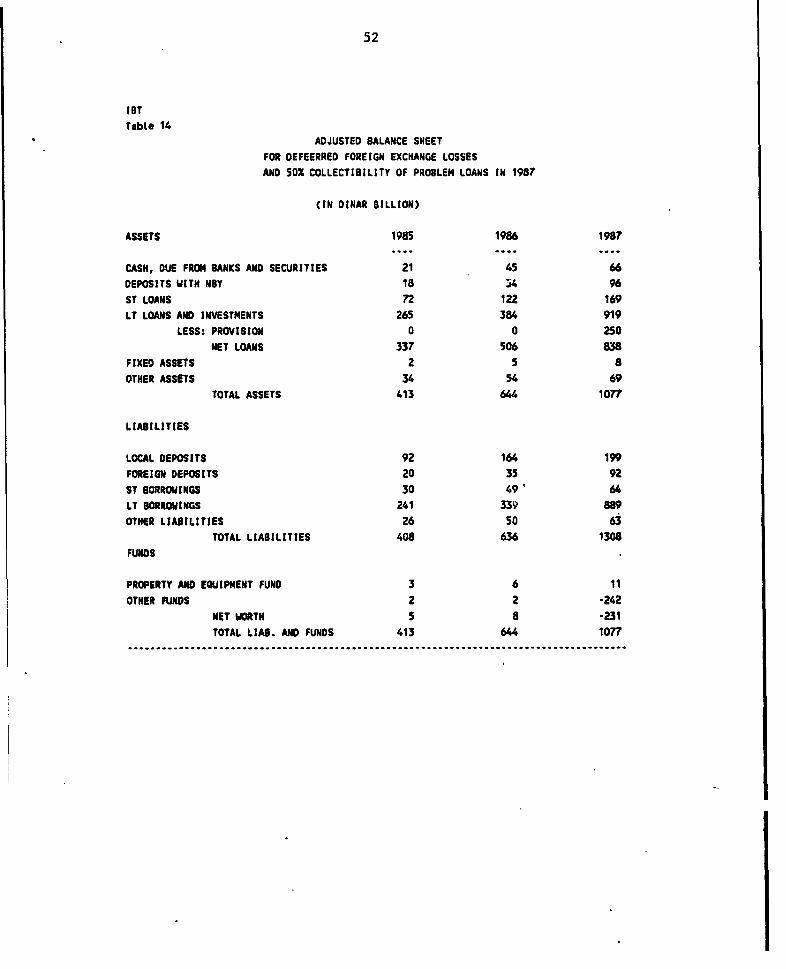

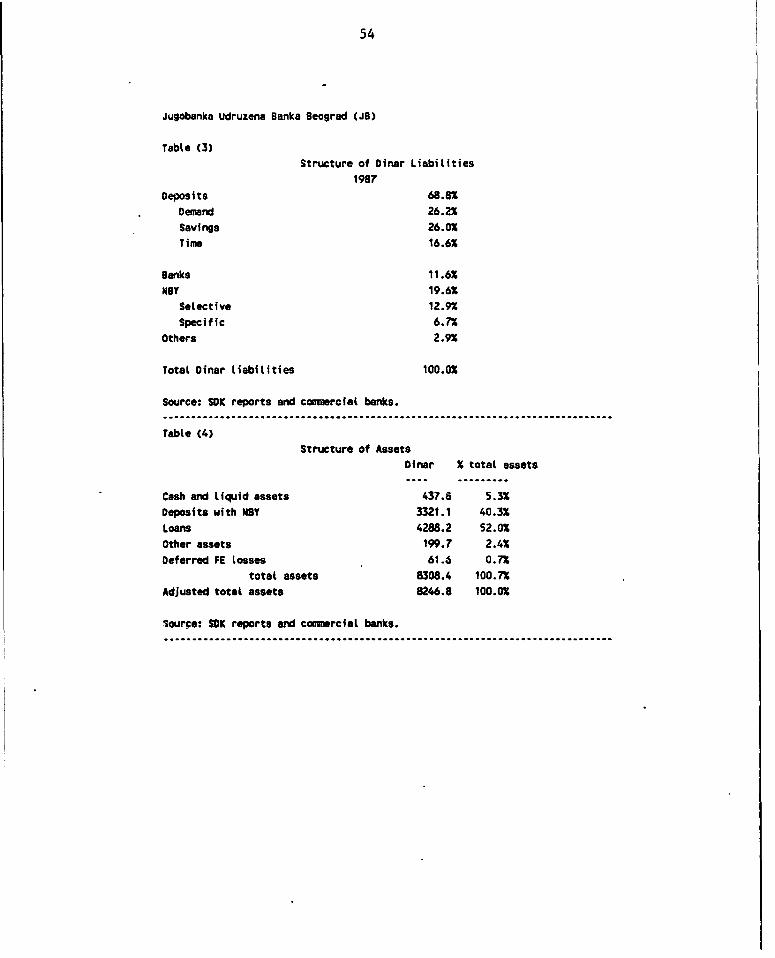

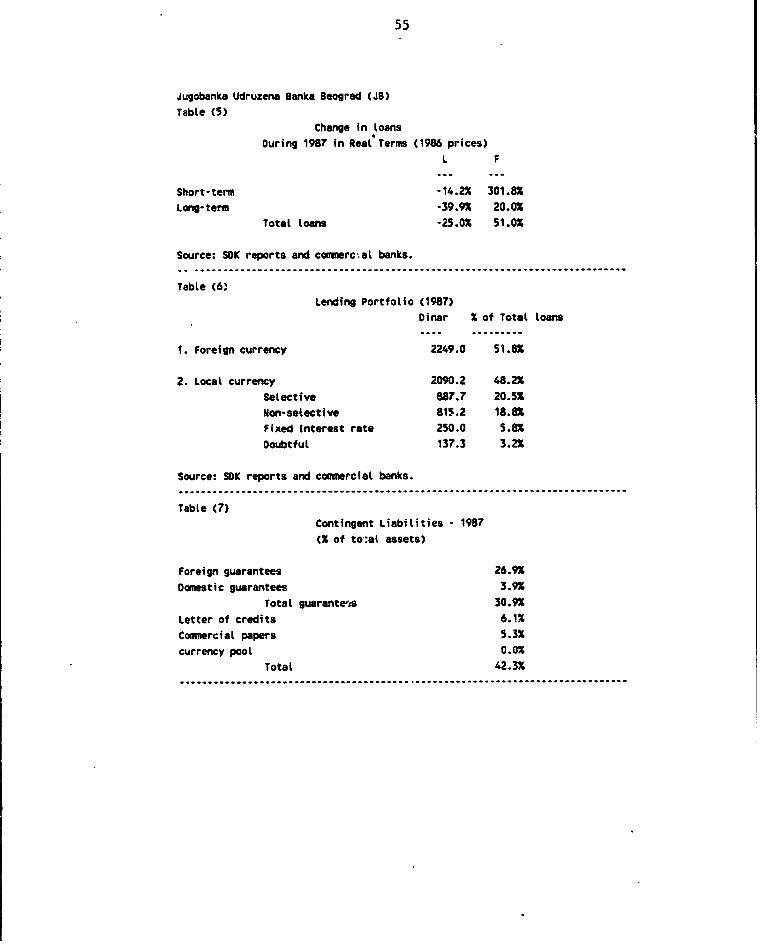

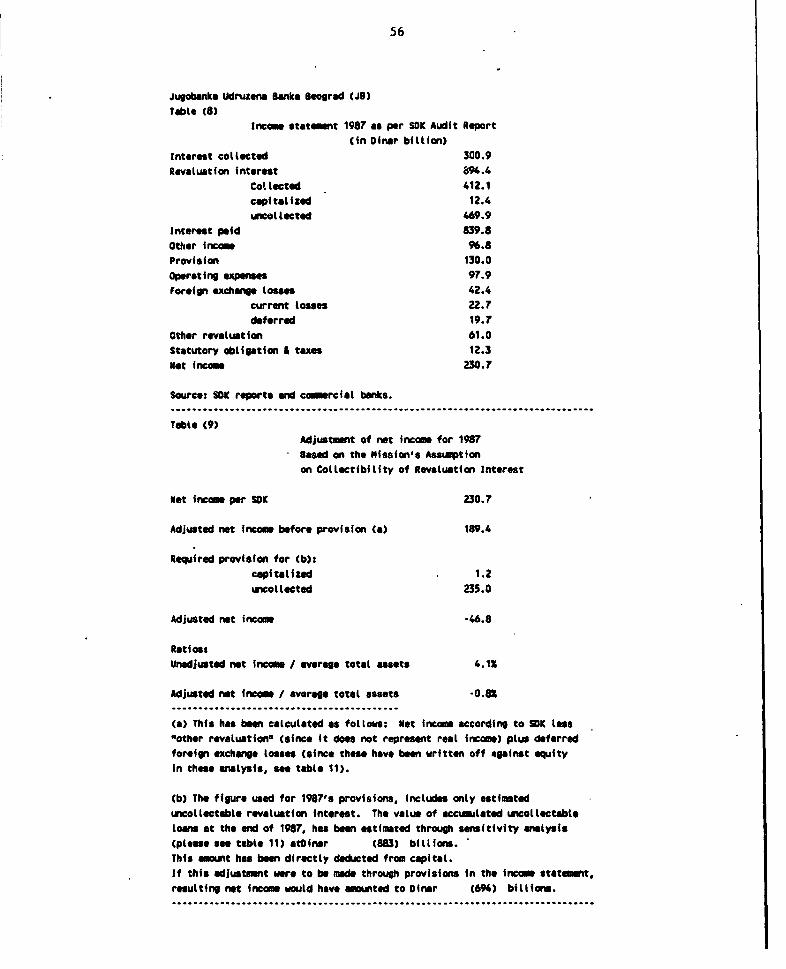

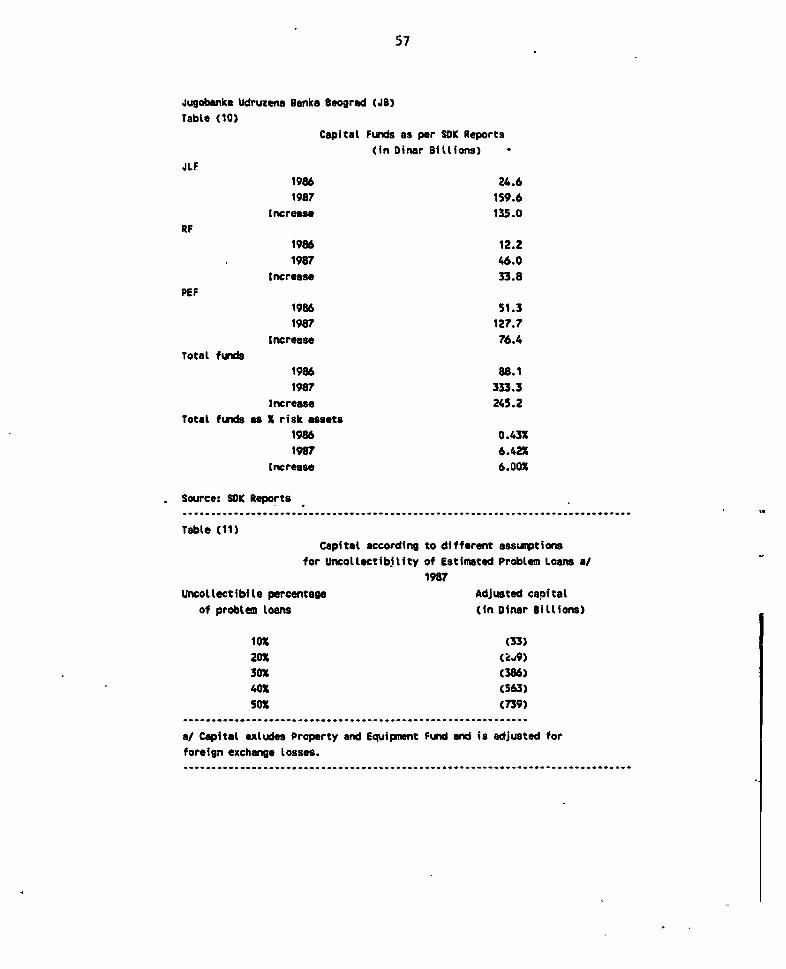

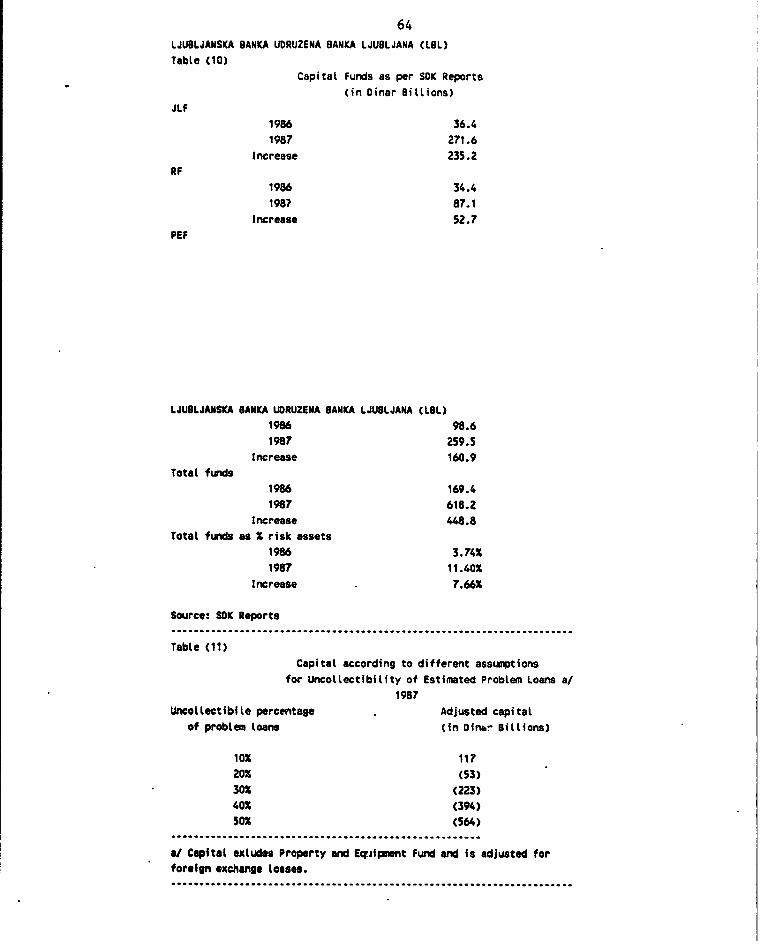

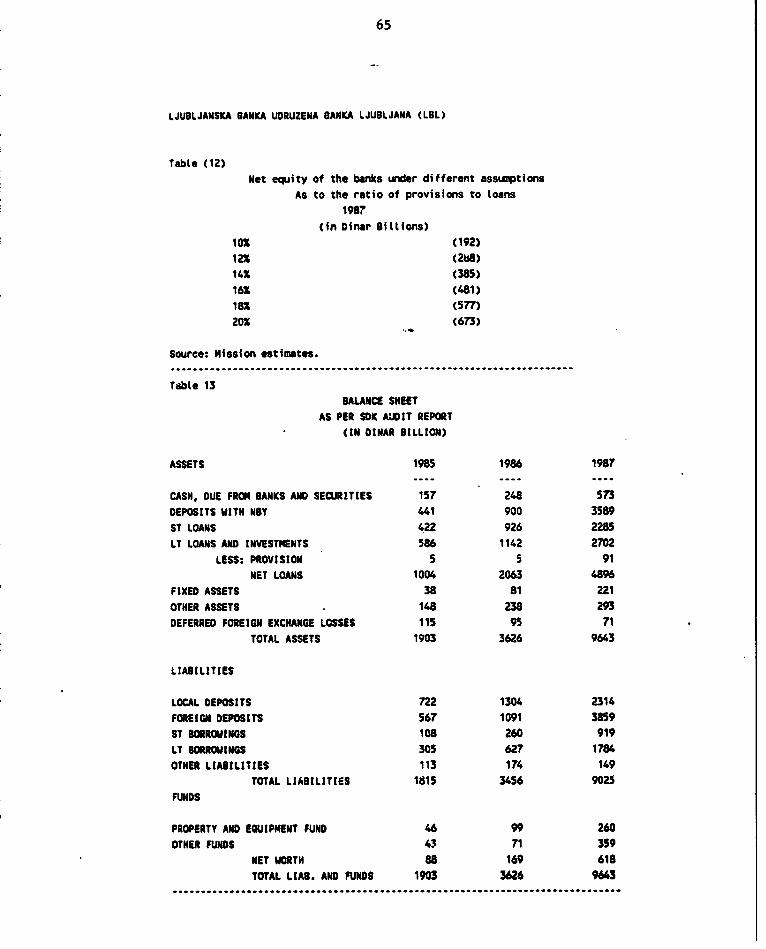

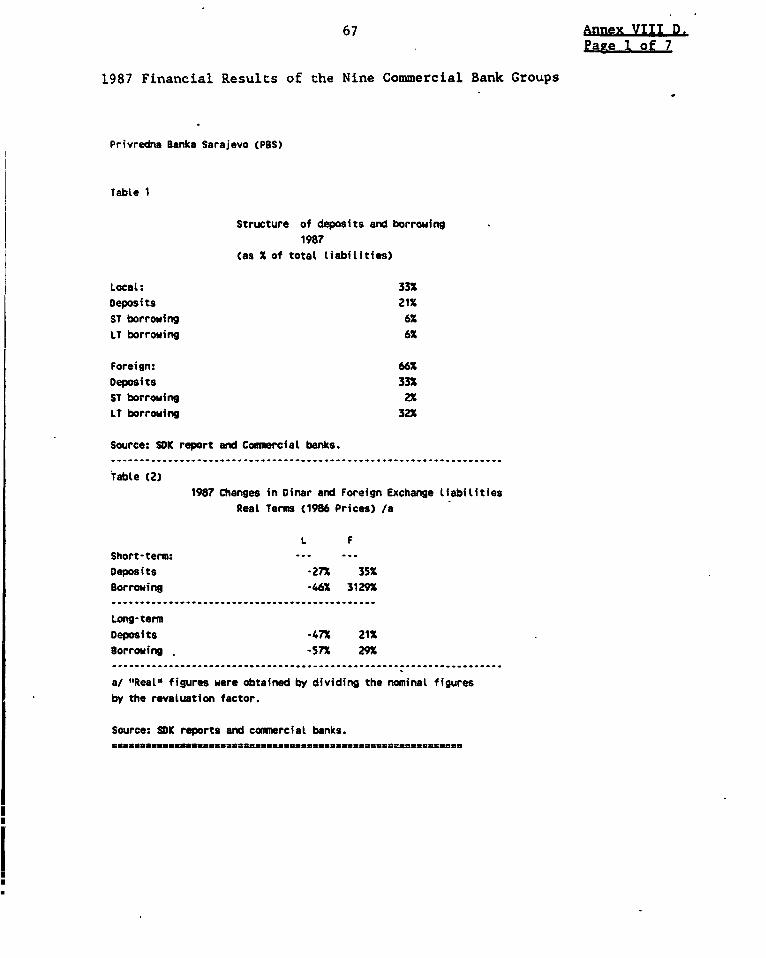

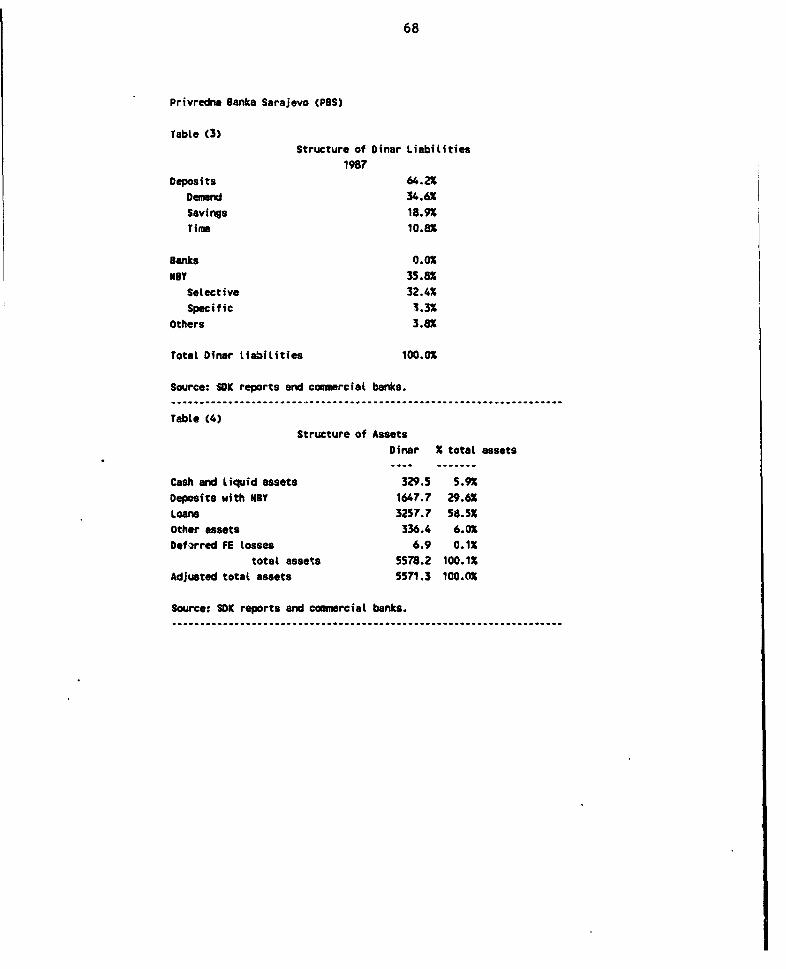

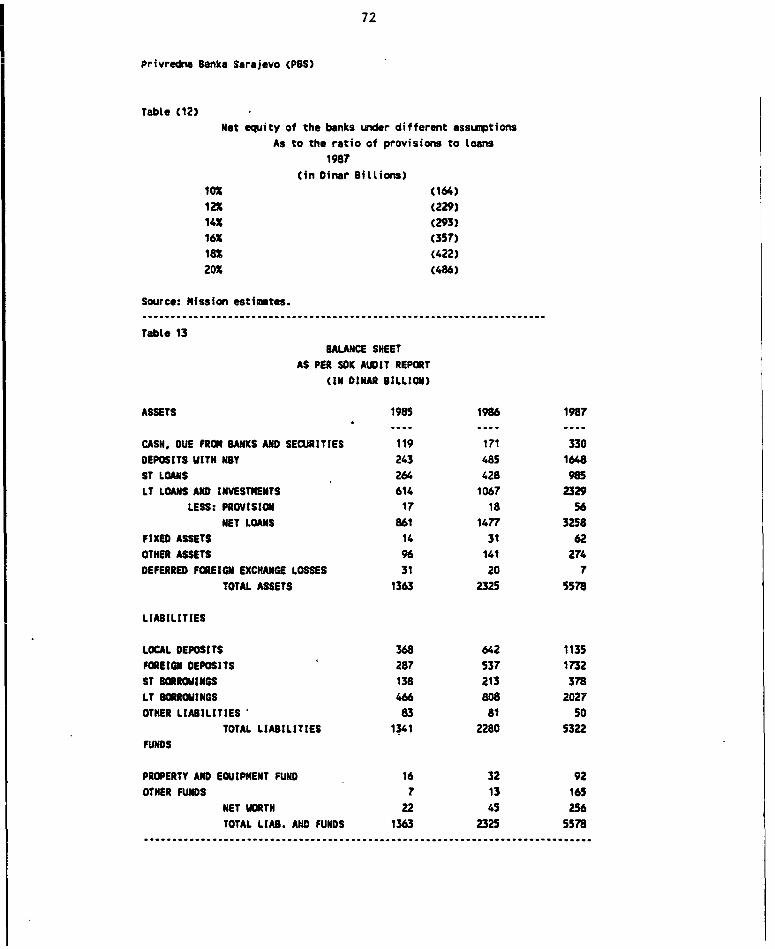

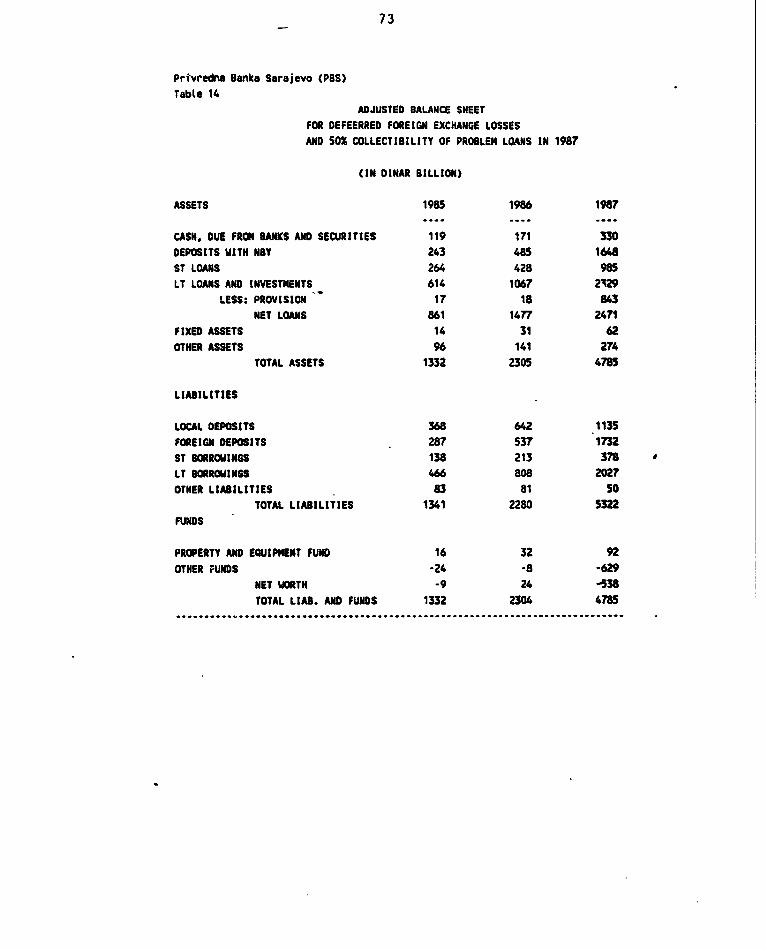

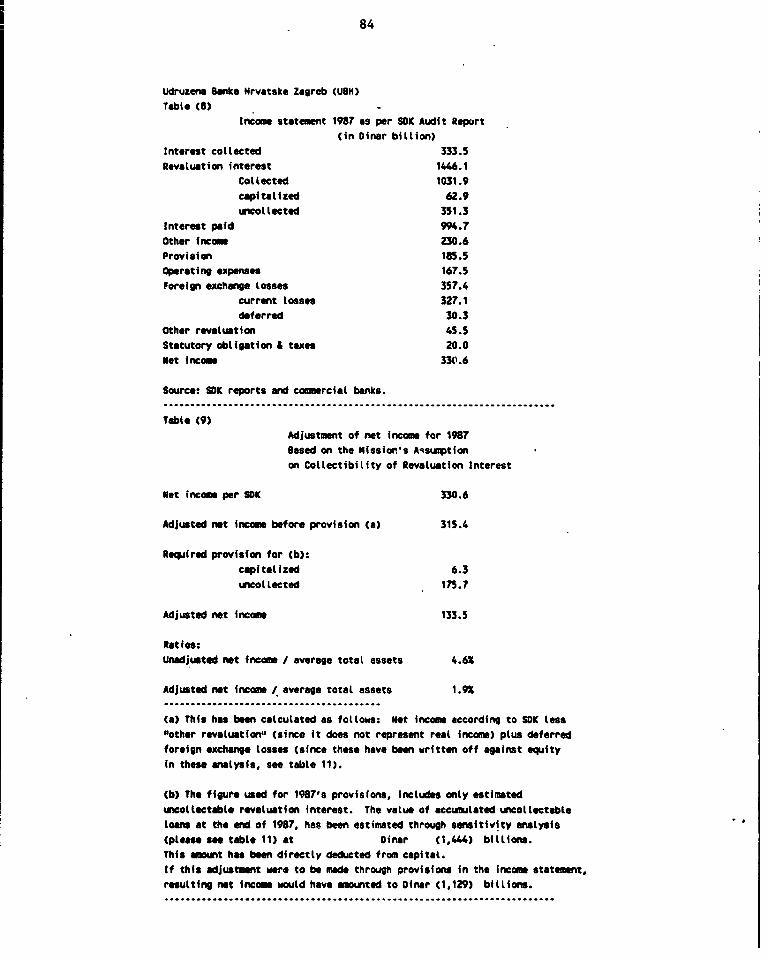

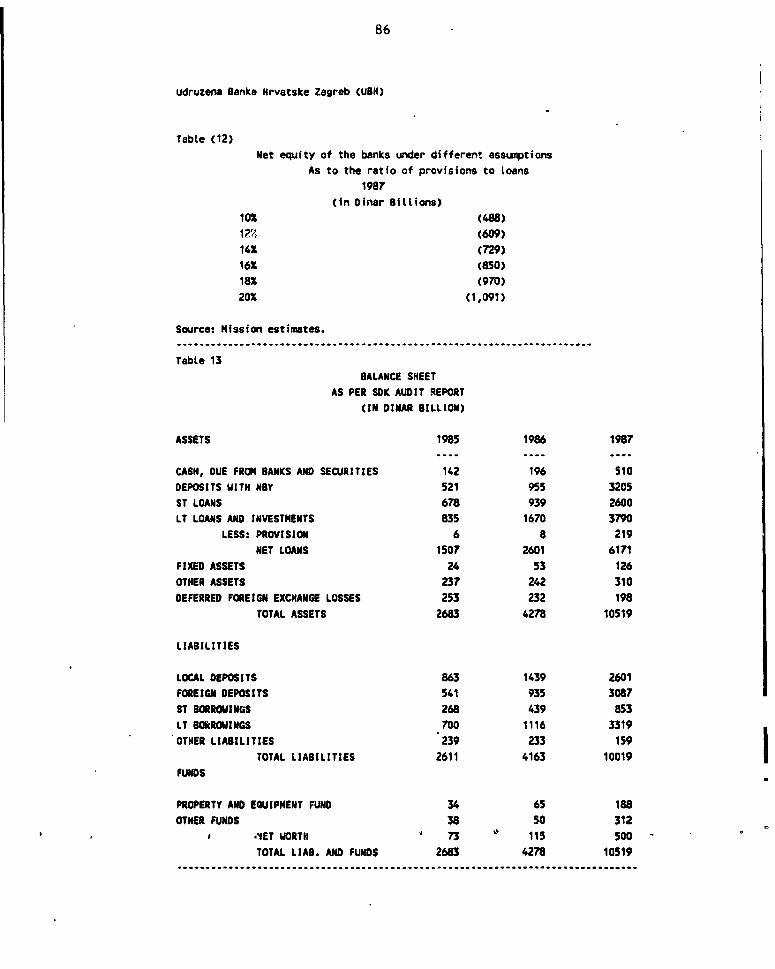

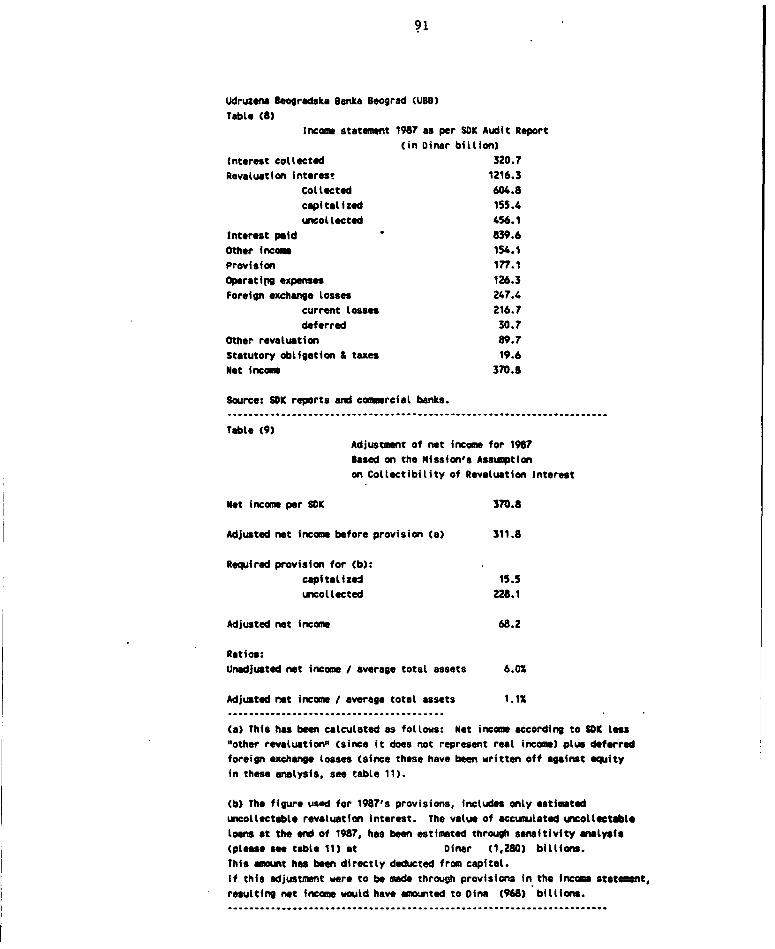

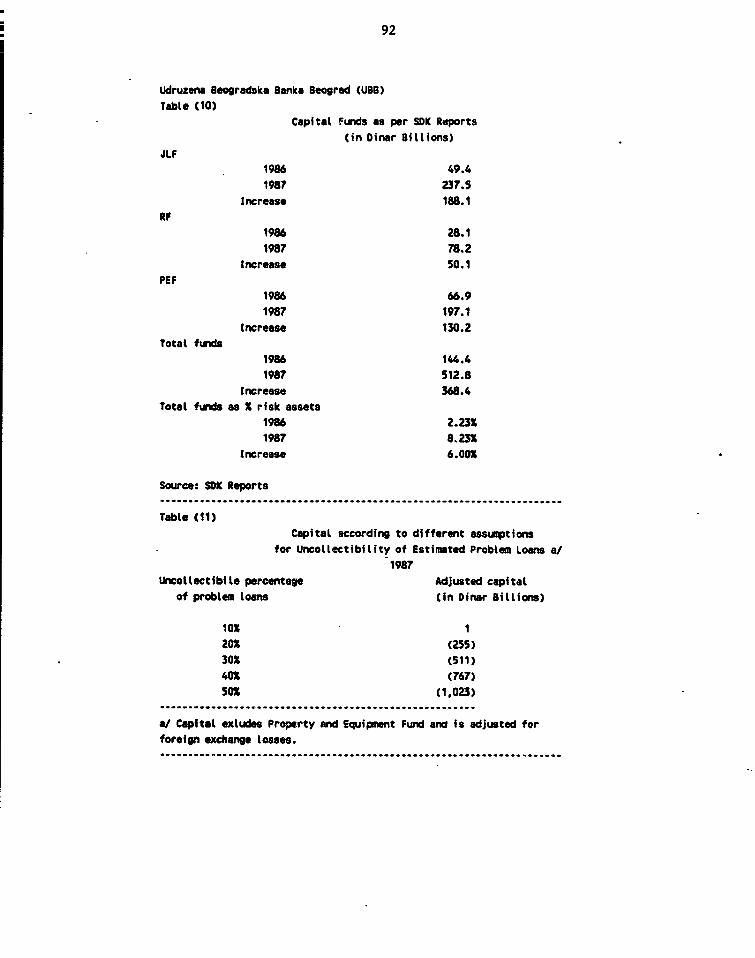

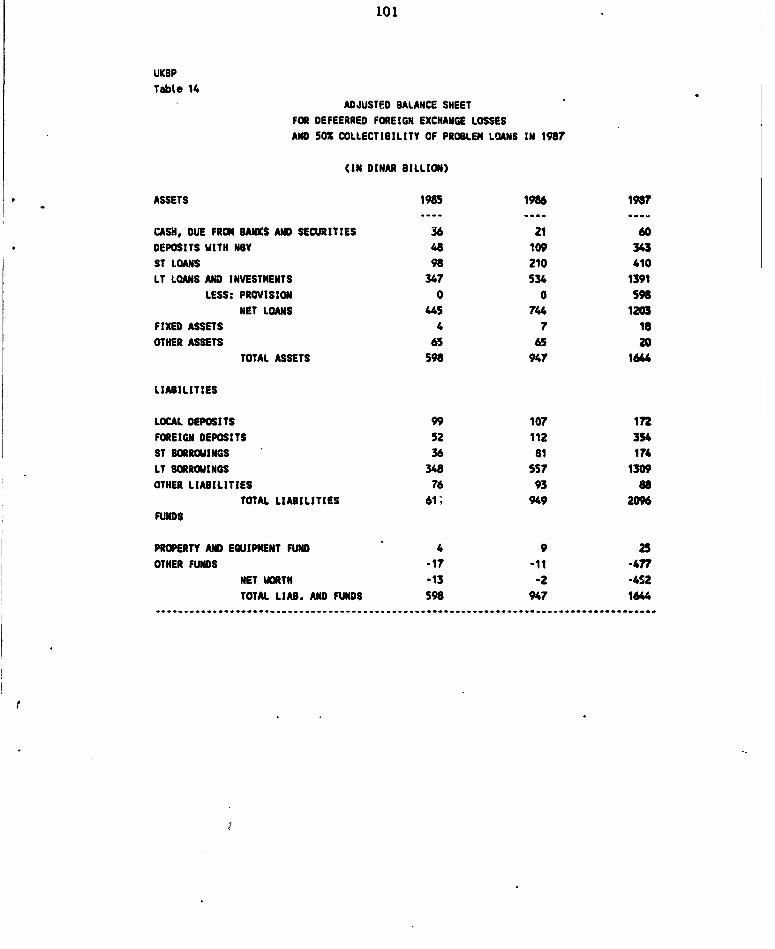

VIII: 1987 Financial Results of the Nine Commercial Bank Groups: 46

A. Investiciona Banka Titograd (IBT) 46-52B. Jugobanka Udruzena Banka Beograd (JB) 53-59C. Ljubljanska Banka Udruzena Banka Ljubljana (LBL) 60-66D. Privredna Banka Sarajevo (PBS) 67-73E. Stopanska Banka Skopje (SBS) 74-80F. Udruzena Banka Hrvatske Zagreb (UBH) 81-87G. Udruzena Beogradska Banka Beograd (UBB) 88-94

H. Udruzena Kosovska Banka Pristina (UKBP) 95-101

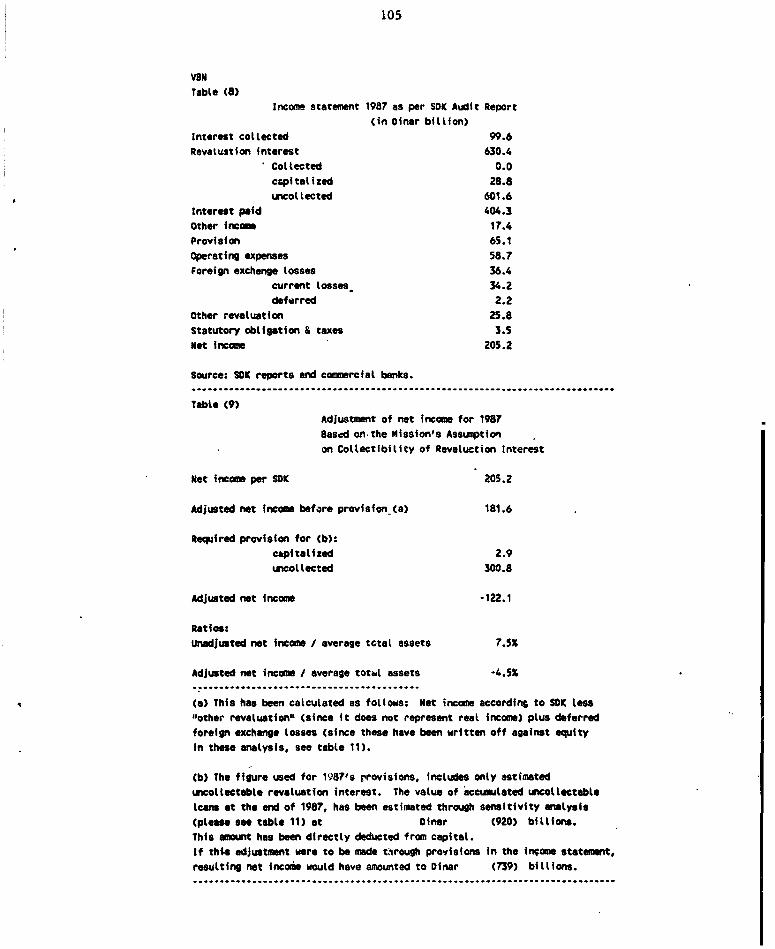

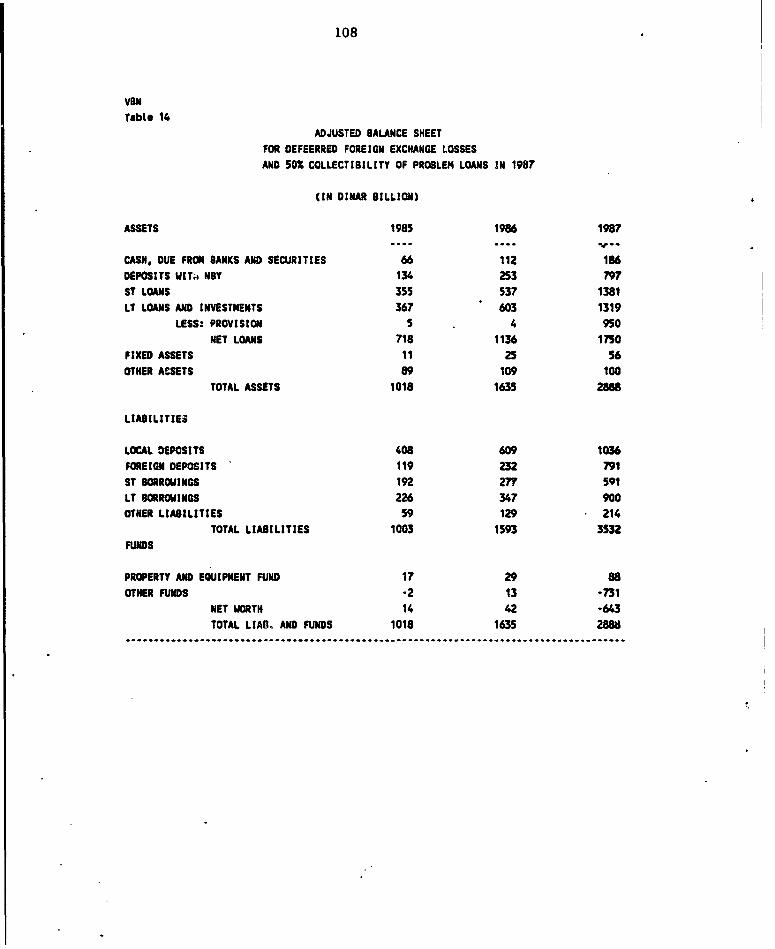

I. Vojvodanska Banka Novi Sad (VBN) 102-108

IX. Analysis of the Intermediation Spread 109-lll

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

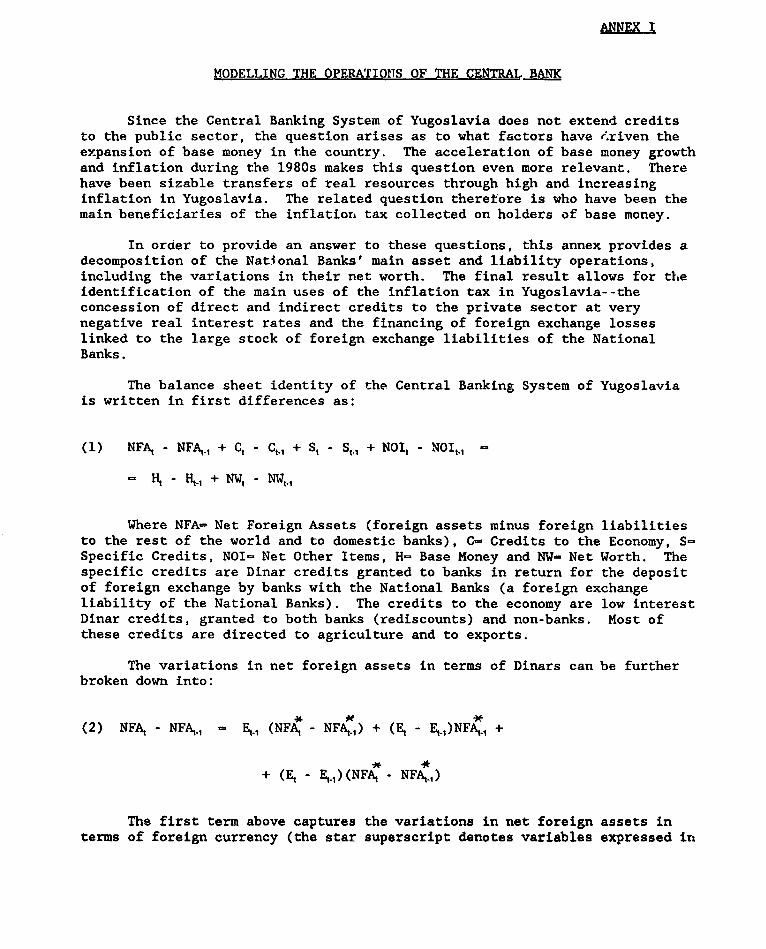

ANNEX I

MODELLING THE OPERATIOlIS OF THE CENTRAL BANK

Since the Central Banking System of Yugoslavia does not extend creditsto the public sector, the question arises as to what factors have ;.riven theexpansion of base money in the country. The acceleration of base money growthand inflation during the 1980s makes this question even more relevant. Therehave been sizable transfers of real resources through high and increasinginflation in Yugoslavia. The related question therefore is who have been themain beneficiaries of the inflation tax collected on holders of base money.

In order to provide an answer to these questions, this annex provides adecomposition of the National Banks' main asset and liability operations,including the variations in their net worth. The final result allows for theidentification of the main uses of the inflation tax in Yugoslavia--theconcession of direct and indirect credits to the private sector at verynegative real interest rates and the financing of foreign exchange losseslinked to the large stock of foreign exchange liabilities of the NationalBanks.

The balance sheet identity of the Central Banking System of Yugoslaviais written in first differences as:

(1) NFA - NFA4., + Ct - Ct, + S, - S,, + NOI, - NOI,., -

- Ht - 1 j + NW, - NWt.,

Where NFA- Net Foreign Assets (foreign assets minus foreign liabilitiesto the rest of the world and to domestic banks), C- Credits to the Economy, S-Specific Credits, NOI- Net Other Items, H- Base Money and NW- Net Worth. Thespecific credits are Dinar credits granted to banks in return for the depositof foreign exchange by banks with the National Banks (a foreign exchangeliability of the National Banks). The credits to the economy are low interestDinar credits, granted to both banks (rediscounts) and non-banks. Most ofthese credits are directed to agriculture and to exports.

The variations in net foreign assets in terms of Dinars can be furtherbroken down into:

(2) NFAt - NFA,.I - E,_1 (NFA4 - NFA.1) + (Et - E,1 )NFA11 +

+ (E, - Et.,)(NFA4 - NFA4.1)

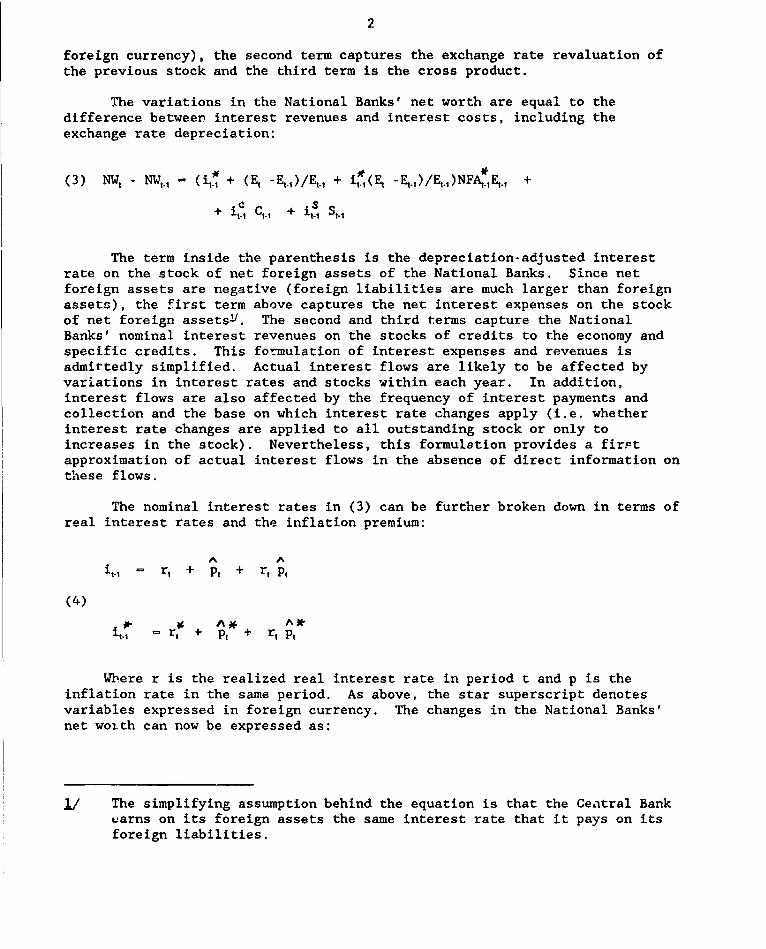

The first term above captures the variations in net foreign assets interms of foreign currency (the star superscript denotes variables expressed in

2

foreign currency), the second term captures the exchange rate revaluation ofthe previous stock and the third term is the cross product.

The variations in the National Banks' net worth are equal to thedifference between interest revenues and interest costs, including theexchange rate depreciation:

(3) NWt - NWt.,, (i,< + (E, -E,.,)/E, + i,(E, -E,,.)/E.,,)NFA,,Et, +

+i, C,, + is s.,

The term inside the parenthesis is the depreciation-adjusted interestrate on the stock of net foreign assets of the National Banks. Since netforeign assets are negative (foreign liabilities are much larger than foreignassets), the first term above captures the net interest expenses on the stockof net foreign assets/. The second and third terms capture the NationalBanks' nominal interest revenues on the stocks of credits to the economy andspecific credits. This formulation of interest expenses and revenues isadmittedly simplified. Actual interest flows are likely to be affected byvar-iations in interest rates and stocks within each year. In addition,interest flows are also affected by the frequency of interest payments andcollection and the base on which interest rate changes apply (i.e. whetherinterest rate changes are applied to all outstanding stock or only toincreases in the stock). Nevertheless, this formulation provides a firstapproximation of actual interest flows in the absence of direct information onthese flows.

The nominal interest rates in (3) can be further broken down in terms ofreal interest rates and the inflation premium:

A it= r, + p, + r, pt

(4)

it, 1 r, + Pt + r, pt

Where r is the realized real interest rate in period t and p is theinflation rate in the same period. As above, the star superscript denotesvariables expressed in foreign currency. The changes in the National Banks'net woith can now be expressed as:

j~/ The simplifying assumption behind the equation is that the Ceatral Bank.arns on its foreign assets the same interest rate that it pays on itsforeign liabilities.

3

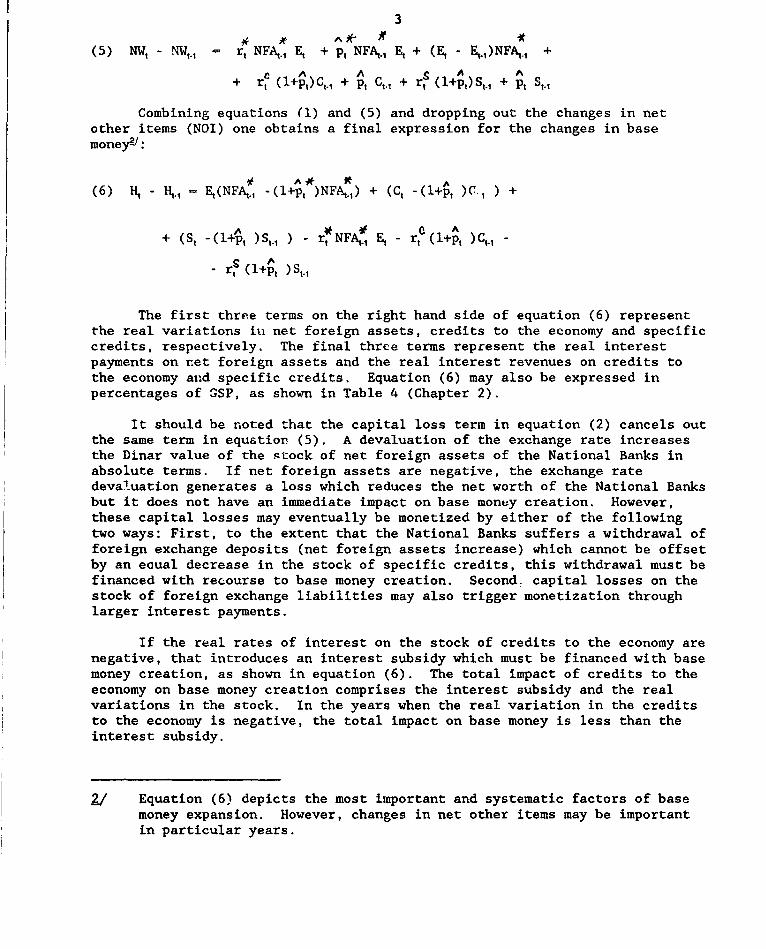

(5) NW, - NW,, rt NFA,, Et + Pt NFAt. E, + (E, - E,.,)NFA,, +

+ rt (l+p,)C, 1 + pt C,, + rs (l+pt)St.1 + ASI

Combining equations (1) and (5) and dropping out the changes in netother items (NOI) one obtains a final expression for the changes in basemoneyJ:

* A* *(6) H, - H, E(NFA,I. (l+Pt )NFAt.1) + (Ct -(l+pt )C.1 ) +

+ (S, -(l+pt )St, ) - rt NFAj E, - rt (l+p, )Ct -

r- (14 ) S,,

The first three terms on the right hand side of equation (6) representthe real variations in net foreign assets, credits to the economy and specificcredits, respectively. The final three terms represent the real interestpayments on ret foreign assets and the real interest revenues on credits tothe economy and specific credits. Equation (6) may also be expressed inpercentages of OSP, as shown in Table 4 (Chapter 2).

It should be noted that the capital loss term in equation (2) cancels outthe same term in equation (5). A devaluation of the exchange rate increasesthe Dinar value of the stock of net foreign assets of the National Banks inabsolute terms. If net foreign assets are negative, the exchange ratedevaluation generates a loss which reduces the net worth of the National Banksbut it does not have an immediate impact on base money creation. However,these capital losses may eventually be monetized by either of the followingtwo ways: First, to the extent that the National Banks suffers a withdrawal offoreign exchange deposits (net foreign assets increase) which cannot be offsetby an ecual decrease in the stock of specific credits, this withdrawal must befinanced with recourse to base money creation. Second. capital losses on thestock of foreign exchange liabilities may also trigger monetization throughlarger interest payments.

If the real rates of interest on the stock of credits to the economy arenegative, that introduces an interest subsidy which must be financed with basemoney creation, as shown in equation (6). The total impact of credits to theeconomy on base money creation comprises the interest subsidy and the realvariations in the stock. In the years when the real variation in the creditsto the economy is negative, the total impact on base money is less than theinterest subsidy.

2.! Equation (6) depicts the most important and systematic factors of basemoney expansion. However, changes in net other items may be importantin particular years.

4

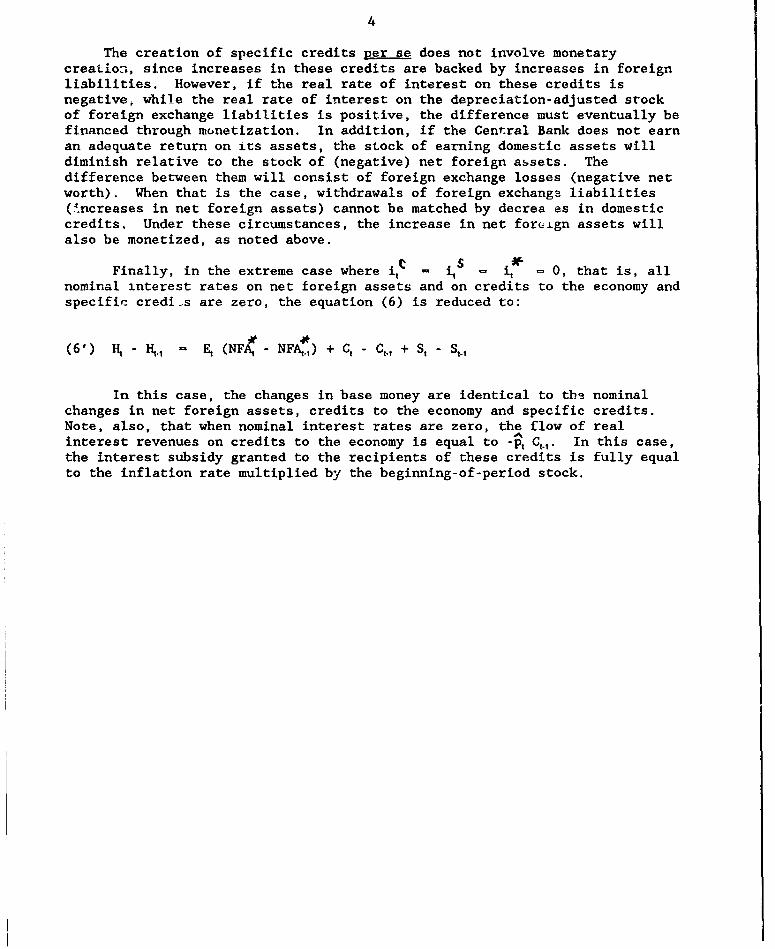

The creation of specific credits per se does not involve monetarycreation, since increases in these credits are backed by increases in foreignliabilities. However, if the real rate of interest on these credits isnegative, while the real rate of interest on the depreciation-adjusted stockof foreign exchange liabilities is positive, the difference must eventually befinanced through monetization. In addition, if the Central Bank does not earnan adequate return on its assets, the stock of earning domestic assets willdiminish relative to the stock of (negative) net foreign assets. Thedifference between them will consist of foreign exchange losses (negative networth). When that is the case, withdrawals of foreign exchang3 liabilities(increases in net foreign assets) cannot be matched by decrea es in domesticcredits. Under these circumstances, the increase in net foreign assets willalso be monetized, as noted above.

V S *Finally, in the extreme case where i t i it i 0, that is, all

nominal interest rates on net foreign assets and on credits to the economy andspecific. credi-s are zero, the equation (6) is reduced to:

(6') H, -Ht1 Et (NFA, -NFAt,) + Ct -Ct + St -S,,

In this case, the changes in base money are identical to the nominalchanges in net foreign assets, credits to the economy and specific credits.Note, also, that when nominal interest rates are zero, the flow of realinterest revenues on credits to the economy is equal to -Pt C,.1. In this case,the interest subsidy granted to the recipients of these credits is fully equalto the inflation rate multiplied by the beginning-of-period stock.

5

THE DEMAND FOR MONEY IN YUGO0LAVIA

1. Spacification

The estimation of the demand for money in Yugoslavia followsstandard practice. The demand for each mo.aetary asset/ is formulated as afunction of real income, the nominal rate of return on alternative financialassets and the expected rate of inflation. The inclusion of the expected rateof inflation is justified because real assets may be relevant alternatives tofixed-income financial assets. In addition, the relationship between interestrates and inflation in Yugoslavia has never been a very close one. As aresult of the determination of the nominal interest rate on deposits bycartel-like agreements among banks, the real rate of interest was negativeduring the entire estimation period. That has increased the importance ofexpected inflation for the estimation of the demand for financial assets.

The dasired real stock of money at period t is, therefore, writtenas:

A(1) log m* bo + b1 log y, + b 2 iTDt + b3 pt + u,

Where m* - desired stock of money, y real income, iTD - nominalinterest rate on time deposits, p - expected inflation and u - random errorterm. The subscripts indicate the period of time. Actual stocks are assumedto adjust to desired levels according to a standard stock adjustment function:

(2) log ;4 - log;.1 - d ( log mn* - log m.1 )

Combining equations (1) and (2) gives:

(3) log m = a. 0 fi a, log y, + a2 iTD, + a3p, + a4 log M. + ut

Where e1 - b, d, i - l..4 and a4 - 1 - d. The a, 's are the short-run coefficients. The long-run coefficients are obtained by dividing theshort-run coefficients by one minus th.e coefficient of the lagged dependentvariable: b1 - a, /( 1 - a 4 ) ; i - 0..3. The semi-logarithmic form impliesvariable inflation and interest rate elasticities along the demand curve. Thedemand for/ currency, sight deposits and time deposits in Yugoslavia wereestimated according to equation (3). The next section discusses the data,while the last section discusses the estimation methods and the results.

1/ Currency, sight deposits and time deposits.

6

? Data

The demands for monetary assets were estimated using quarterlydata for the 1980-87 period. The data on monetary aggregates, interest ratesand prices were centered in the middle of the quarter (February, May, etc)while the income variable was represented by the accumulated flow within thequarter. The data on monetary aggregates are from the quarterly bulletins ofthe National Bank of Yugoslavia. The domestic interest rate used in theestimations is the interest rate on one year time deposits (households' orenterprises' deposits, according to the case). This was the only short-terminterest series available during the estimation period--Deposits with shortermaturities did not exist prior to 1983. The consumer price index was used todeflate the nominal variables and to measure the rate of inflation. Inflationwas measured by the quarterly variations of the CPI. The CPI series are fromthe International Financial Statistics database.

In the case of the households' demand for money, the incomevariable was proxied by the real personal income of households. The series onnominal personal income of the household sector are from the Index?. Thereal income of enterprises was proxied by two alternative variables: theindustrial production index (from the IFS database) and the real revenues ofthe enterprise sector (from the monthly statistical bulletin).

The series on the Central Bank's discount rate are from thequarterly bulletin of the National Bank of Yugoslavia. Data on exchange rates(Dr/US $ and DR/DM) and foreign prices (US and German CPIs) are from theInternational F'nancial Statistics database. Foreign interest rates (on oneyear euro-dollar and euro-mark deposits) a-e from Morgan Guaranty's WorldFinancial Markets.

3. Estimation and Results

3.1 The Demand for Money by Households

A. General Results

The OLS estimates of equation (3) with household data are shown inthe upper half of Table 1. The first and second rows show the estimates ofthe demand for currency and sight deposits, while the third row shows theestimates of the household's demand for Ml. This is a narrow definition of Ml,since it excludes the sight deposits of enterprises. Each demand equation wasestimated with two alternative proxies for domestic inflation. The equations(A) were estimated with current inflation as proxy for expected future

2/ This is actually a series on wage income. Therefore, it is just a proxyfor personal disposable income, since it does not include, for instance,transfers from abroad.

-7-

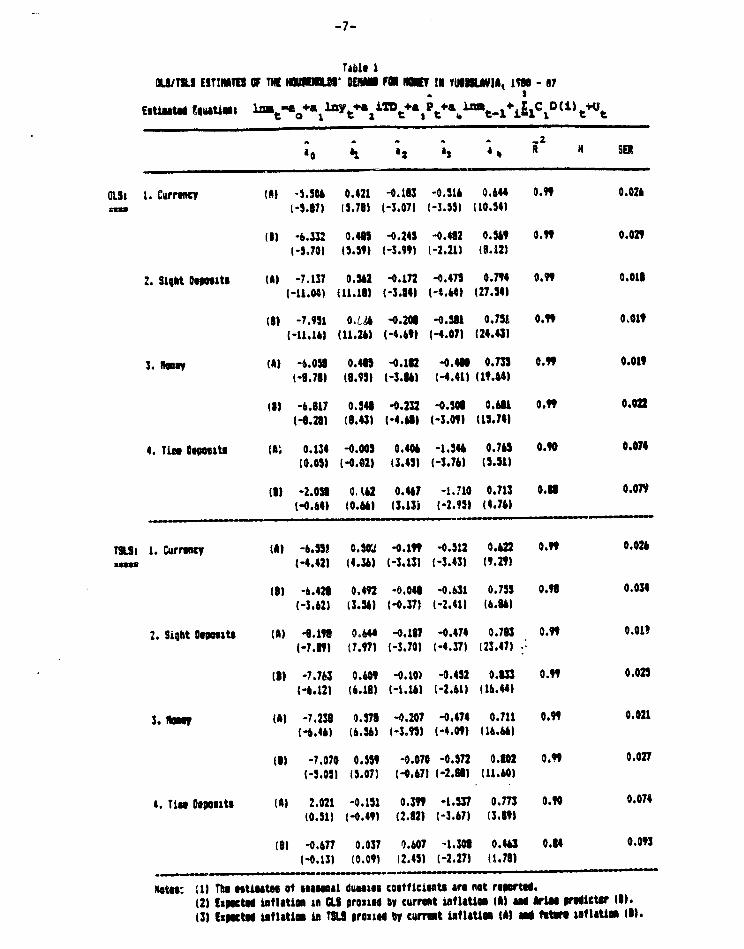

Table IOWJTIU EUTINM OF TN M lWS' DENIS FM NM 1 YUUUV14A 13 - t7

3

Estlaisi EguatU: Im t= + I TDt*ai P t £i I CIt) t t

OLSI I. Cirruc (A) -5.506 0.421 -0.183 -0.516 0.644 0." 0.026( -S.lJ ( 5.78) 1-3.071 1-3.355 l 10.14)

(3) -6.332 0.401 -0.245 -0.432 0.569 O." 0.029

(-I741 (5.59) (-3.99) (-2.21) (1.121

2. Sligt DuOuts (Ai -7.17 I .n2 -o.7n -0.47 0.714 O." o0.01(-11.04) (11.13) (-3.341 ['4.64) (27.54)

(l) -1.951 0.tA -0.20 -0.581 0.751 0." 0.019

(-11.16) (11.26) (-4.69) (-4.07) (24.431

3. (may (A) -6.05 0.415 0.l2 -0.40 0.735 O." 0.019(-8.786 (6.95) (-3.86) (-4.41) (11.64)

(3) -6.817 0.46 -0.232 -0.506 0.681 0.9 0.:22(-8.281 (8.43) (-4.66 (-3.09) (11.41

4. Tin .Dposts (Al 0.134 -0.005 0.406 -1.346 0.765 0." 0.014(0.05) (-0.02) (3.451 (-3.76) (5.51)

(l) -2.06 0, 12 0.467 -1.?10 0.713 0.6 0.07?

(-0.64) (0.66) (3.13i (-2.95) (4.76)

TILS: 1. Currunq (At -6.355 0.Si -0.199 -0.512 0.n22 o.9 0.026=sin (-4.42) (4.36 (-3.13) (-3.43) (9.291

(8) -6.42 0.492 -o.ou -0.631 0.7n5 0.9 0.034(-3.62) (3.36) (-0.371 (-2.411 (6.66)

2. Siqbt Dugo ts (A) -9.1 0.6" -0.137 -0.474 0.76 0.9 0.0.O(-7.69) (7.'1) (-3.70) (-4.37) (23.471

(3) -7.763 0.60 -0.10) -0.452 0.6U3 O." 0.025

(-6.121 (6.198 (-1.16) (-2.61) (16.44)

3. No"i (A) -7.238 0.576 -0.207 -0.474 0.711 0.9 0.021(-6.46) (6.561 1-3.95) (-4.09) (16.66)

(1) -7.070 0.559 -0.070 -0.572 0.802 0.9 0.027(-5.051 (5.07) (-0.67) (-2.66) (11.60)

4. Tis Deposits (6) 2.021 -0.151 0.39 -1.53 o.m 0.90 0.074(0.51) (-0.49) (2.32) (-3.67) (3.69

(9) -0.677 0.037 0.607 -1.308 0.4U 0.64 O.03

(-0.13) (0.091 (2.45) (-2.27) (1.73)

oteo: IIl The estleate at o esmal dustem csttficclmts are not rnoorteu.(2) tspucted ittlatlon .CLY prostue by currst inflatlio (i) and Arim rolct? (I).(3) tsctsd tiflatio In TILS proused by cwv.t Ilatim (A) ad latf u tlatU (3).

8

inflation. The equations (B) make use of ARIMA predictors as proxinc forexpected future inflation-'.

The estimated equatiolis fit very well the data for this period, asshown in Table 1. The estimates are particularly good in the case of currencyand sight deposits. All the coefficients have the expected sign and are verysignificant. Also, the results are not very sensitive to whichever measure ofexpected inflation is used. The long-run income elasticity of the households'demand for Ml is larger than unity, as is frequently the case in developingcountries. The estimated income elasticity for time deposits is notstatistically different from zero. However, low or even negative incomeelasticities for time deposits are not unexpected. Given the wealthconstraint, if the demand for some monetary assets, such as currency and sightdeposits, increase with the number of transactions (proxied by income), thenthe demand 'or at least one asset must fallV.

Tne coefficient of the interest rate on one year time deposits isnegative and significant in the case of currency and sight deposits, and it ispositive and significant in the case of time deposits. Finally, thecoefficient of expected inflation is always negative and significant. Itshould be noted that the coefficients of the inflation rate and the interestrate are the short-run semi-elasticities. Estimates of the average long-runelasticities may be obtained by: First, multiplying the estimated coefficientsby the average inflation and interest rates and, second, dividing the resultby one minus the coefficient of the lagged dependent variable. For instance,in the case of the households' demand for Ml, the long-run interest andinflation elasticities are -0.25 and -0.2, respectively. In the case of thehouseholds' demand for time deposits, the long-run interest and inflationelasticities are +0.6 and -0.8, respectively§. The fact that the inflationelasticity is higher in absolute terms indicates that increasing nominalinterest rates in line with inflation may not be sufficient to prevent areduction in the real demand for time deposits when inflation increases.

i~./ The quarterly variations of the consumer price index in Yugoslavia arebest approximated by a fourth-order auto-regressive stochastic process-AR(4). The inflation predictors used in the demand for money equationsare the one-step-ahead forecasts obtained from the estimation of anAR(4) for the period 1977-87. Although the one-step-ahead forecastswere not obtained from recursive estimation, that does not seem tocreate a serious problem, since the estimates of the auto-regressiveprocess parameters vary very little over different sample periods.

i/ See Friedman,B (1981) and Tobin (1982).

2/ The average interest rate t.nd quarterly inflation rate for the sampleperiod are 36.2 percent and 12.6 percent, respectively. The reportedlong-run elasticities are associated with the (A) equations. Similarresults are obtained with the (B) equations.

9

Risk-averse asset holders may require a risk premium in th- nominal interestrate in compensation for increased inflation uncertainty§.

The lower half of Table 1 presents TSLS estimates of thehouseloldn' demand for monetary assets. In the TSLS estimation, interestrates were considered exogenous for the following reasons: First, interestrates were determined by cartel-like agreements among banks durir.g the wholesample period. In addition, the banks were frequently reluctant to adjustinterest rates to the developments in inflation during this period. Second,the levels at which interest rates were set were sanctioned by accommodatingmonetary policy. Therefore, the main potential source of simultaneity bias inOLS estimates probably lies in the output variable.

Again, each demand equation was estimated with two alternativeproxies for expected inflation. The equations (A) were estimated with currentinflation as a proxy for expected future inflation. In this case, the set ofinstruments used in the TSLS estimation consisted of the Central Bank'sdiscount rate, and the real GNP and interest rates in both Germany and theUS?. Equations (B) were estimated with realized future inflation as a proxyfor expected future inflation. This is a rational expectations procedure--itassumes that the individuals' predictions of inflation are correct on theaverage, and that the individuals do not make systematic prediction errorsover time. In order to avoid the well-known errors-in-variables problem inrational expectations estimation, the realized future inflation wasendogenized in the TSLS estimation and current and past inflation rates wereadded to the instrument set. This procedure ensures the orthogonality betweeninflation and the error term and consistent estimation of the parameters.

The results obtained with TSLS estimation are not very sensitiveto whichever measure of expected inflation is used, as shown in Table 1. Inaddition, the TSLS estimates are quite similar to those obtained throughOLSI. Therefort, the observed decrease in real stocks of currency and sightdeposits held by households in the 1980s seems to be almost fully explained bythe increase in inflation and interest rates during this period. Theestimates of demand for time deposits seem to have less explanatory power, butstill look reasonably good. The fact that time depcosits declined in realterms shows that interest rates were inadequate to compensate for theincreased levels and variance of inflation during this period.

.i./ The alternative way to examine this problem is to test for thesignificance of the variance of inflation in the demand for financialassets. That was not pursued in this study.

1/ In addition to the exogenous independent variables.

.Q/ Except in the case of the demand for currency (and Ml), estimated withrational expectations of inflation. In this case, the interest ratecoefficient is lower and non-significant.

10

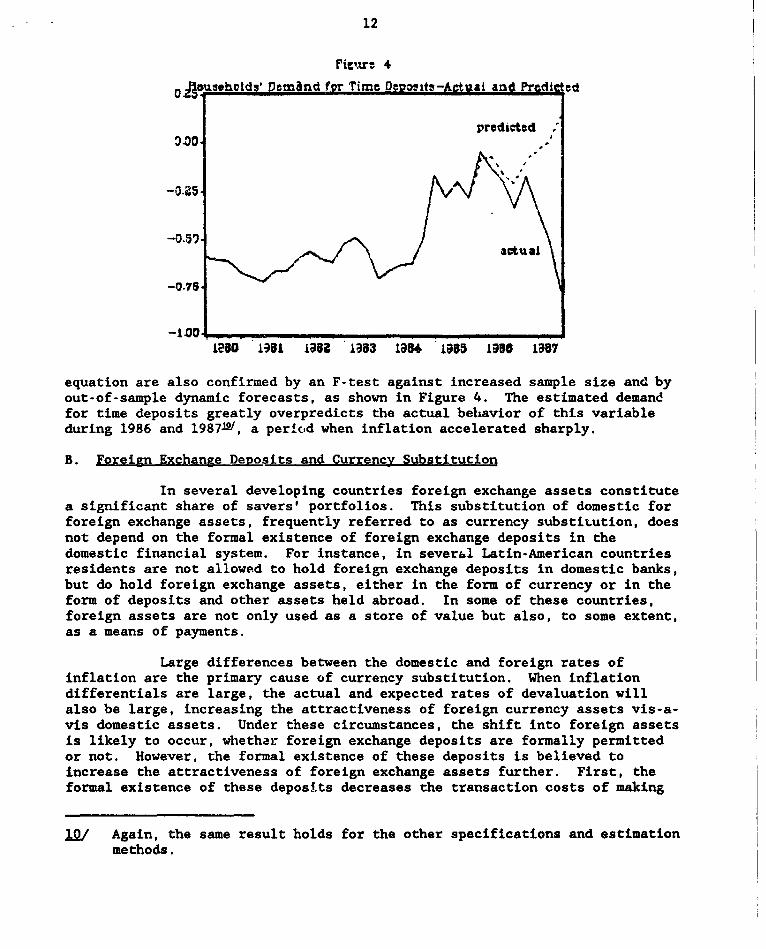

In order to examine the stability of the equations, the end of thesample period was constrained to the last quarter of 1985 and the equationswere reestimated by OLS. The expected inflation variable was proxied by thecurrent inflation rate. These results are shown in Table 2. The demand forcurrency, sight deposits and MI seem to be s over this period, as indicated byTables 1 and 2. The performance of F-tests for stability against increases insample size confirms the existence of stability of the parameters during thisperiod. The stability of the demand equations can also be confirmed throughout-of-sample dynamic forecasts. As shown in Figures 1 through 3, thepredicted values of currency, sight deposits and Ml track very well therealized values of these variables during 1986 and 19871Y.

The results are quite different in the case of time deposits. Asshsown in Tables 1 and 2, the estimated inflation coefficient increasessignificantly when the sample period is extended to 1987, while the interestrate coefficient declines. That may indicate why asset holders starteddemanding a risk premium in nominal interest rates to compensate for increasedinflation uncertainty. The shifts in the parameters of the time deposits

table 2

OLS ESTIMATE9 OF THE HOUSEHOLN' EIBIE FOR HUl, 1990 - 83A ^ 3

Estiutu Equatims t0LFal&nYt+&,iTDt3Pt+a 4 t-iE1 C .) t t

*0 'o a2 63 44 ft SER

1. Currency -5.927 0.453 -0.101 -0.55 0.702 0." 0.025(-3.76) (3.713 (-1.333 (-2.99) (8.14)

2. Sight lignte -6.603 0.521 -0.130 -0.552 0.824 o." 0.019(-5.20) 15.28) (-1.85) (-3.913 (15.12)

3. NI1 -6.50 0.523 -0.125 -0.550 0.160 o.9 0.013(-5.52) (5.57) (-1.97) (-4.05) (12.9)

4. Tin loignte -6.802 0.504 6.560 -0.374 0.439 0.89 0.06o(-1.611 (1.57) (4.29) (-0.67) (2.34)

Notna III The ectltn at s u of sus duan cuttficients ae bt rspated.

2/ The same results hold for the other specifications and methods ofestimation.

11

R"cseholcRo' Demae«d tn CumrenvyActnal and Predicte02.

O.1

-0 \

-0.s

1060 161 196 163 1. 1955 196 1967IM igli ~IM zIN 894 LP8 m

Ftgure a

ffouwhold u D emand ftor ht ObAtAcual and Prdid

I aX~~~~~~50 196 ...6 1...3 194 1..16 16

°M>

-1410 predicted .

_IzaS. .m Iasi. IM ,,9 ,9 , . , ... s I-,

floosel2vds Demanld for Mli-Actual and Predicted

2 D2S >~~~~~~~Z3 prodiotel

10o0 iau iaoz 1983 lU1 9SS l'O0 *m 1"

12

ki.nra 4

0 oassholds' Demand for Timc De;vitz-Actual and Predic ed

predicted

_357~f aotaiRl

-1.00 , .1P5D 13tl 19z 1983 *1984 1935 1950 1987

equation are also confirmed by an F-test against increased sample size and byout-of-sample dynamic forecasts, as shown in Figure 4. The estimated demandfor time deposits greatly overpredicts the actual behavior of this variableduring 1986 and 19872k, a period when inflation accelerated sharply.

B. Foreign Exchange Deposits and Currency Substitution

In several developing countries foreign exchange assets constitutea significant share of savers' portfolios. This substitution of domestic forforeign exchange assets, frequently referred to as currency substiLution, doesnot depend on the formal existence of foreign exchange deposits in thedomestic financial system. For instance, in sever&l Latin-American countriesresidents are not allowed to hold foreign exchange deposits in domestic banks,but do hold foreign exchange assets, either in the form of currency or in theform of deposits and other assets held abroad. In some of these countries,foreign assets are not only used as a store of value but also, to some extent,as a means of payments.

Large differences between the domestic and foreign rates ofinflation are the primary cause of currency substitution. When inflationdifferentials are large, the actual and expected rates of devaluation willalso be large, increasing the attractiveness of foreign currency assets vis-a-vis domestic assets. Under these circumstances, the shift into foreign assetsis likely to occur, whether foreign exchange deposits are formally permittedor not. However, the formal existence of these deposits is believed toincrease the attractiveness of foreign exchange assets further. First, theformal existence of these deposits decreases the transaction costs of making

JQ/ Again, the same result holds for the other specifications and estimationmethods.

13

payments in foreign currency. Second, these deposits frequently yieldinterest rates comparable or even more attractive than those abroad.

In order to examine the exte..t to which the portfolio decisions ofasset holders are affected by expectations of devaluation, the demand fordomestic and foreign exchange deposits by households were formulated asfunctions of income, the nominal interest rate on one year Dinar deposits anda proxy for expected devaluation--a combination of current and laggedquarterly variations of the Dinar/DM exchange rate with polinomiallydistributed weights. The expected inflation is excluded from the equationdue to the high collinearity between the inflation and devaluation rates. Theactual and desired stocks are related by a standard stock adjustment equation,as above. The results are shown in the upper part of Table 3.

The coefficient of the expected devaluation variable appears withthe expected sign (negative for the Dinar deposits and positive for theforeign exchange deposits) and is significant in all the equations!11. Theinterest rate coefficient also appears with the expected sign (negative forsight deposits and for the foreign exchange time deposi-s) in all theequations, although it is not significant in the c-se of the demand for timedeposits. These resuits do suggest that asset holders shift out of Dinardeposits as a result of expectations of higher exchange rate devaluations.The results also show that the real demand for foreign exchange deposits (bothsight and time deposits) are reduced when the i.uterest rate on time depositsincreasesl2.

These results are confirmed by the estimates of the desired ratioof foreign exchange to Dinar deposits as shown in the lower half of Table 31U.The desired ratio of foreign exchange sight deposits to Dinar sight depositsincreases as a result of higher expectations of exchange rate devaluations.The interest rate on Dinar time deposits does not affect the ratio, since itaffects negatively the demand for both Dinar and foreign exchange sightdeposits. The desired ratio of foreign exchange time deposits to Dinar timedeposits also increases as a result of higher expected devaluations anddecreases as a result of increases in the interest rate on Dinar timedeposits. Finally, the same results broadly hold for the ratio of totalforeign exchange deposits to total Dinar deposits. The coefficient of

fl/ The expected devaluation is significant at the 5 percent level in thecase of Dinar and foreign exchange sight deposits and in the case offoreign exchange time deposits. It is significant at the 10 percentlevel in the case of Dinar time deposits.

12J In the comparison of the expected devaluation and interest coefficients.it should be borne in mind that the interest rates are expressed inyearly rates, while the exchange rate devaluations are expressed inquarterly variations.

J,3/ This is the approach followed by Ortiz (1983) in his analysis of theprocess of dollarization in Mexico.

14

expected devaluation is positive and significant and the interest ratecoefficient is negative, although it is not significant. The lack ofsignificance of the interest rate coefficient is not surprising--higherinterest rates on Dinar time deposits reduce not only the demand for foreignexchange deposits but also the demand for Dinar sight deposits.

Table 3

Exlct:d Devaluation and the "Oousenolds 2aana for Dinar and Foreign Currency Deposits

Estisatud Equation: ntm a +a l ny t+a2 iTD t+a 3Et+a4 t-1 +E C D it+t

ao 1 az a3 a4 R SER

-. Sight Deposits:

Ia. Oanrs -6.909 0.544 -0.299 -0.317 0.732 0.99 0.020(-9.57) (9.57) (-5.99) (-2.7)X (20.42)

lb. Foreign Currency 0. 212 -0.017 -0.174 0.933 0.781 0.93 0.045(0.09) (-0.09) (-3.57) (2.88) (7.13)

2. Tice ueOu4ts:

2a. DOnars 2.992 0.220 0.193 -1.079 0.911 0.87 0.098(0.79) (-0.77) (1.49) (-1.86) t4.74)

D. Foreign Cuerency 2.149 -0.205 -0.132 0.856 0.902 8.97 0.050

(1.19) (-1.19) (-1.61) (2.42) (6.68)

3. Ratio of ForeignCurrency Depositsto Oinar Deaosits:

).. Siqht Cenosits e.665 -0.525 0.041 1.209 0.799 0.99 0.047(3.z4) (-3.371 (0.47) (4.12; (14.06)

lb. Tin Deposits 4.719 -0.365 -0.304 1.954 0.675 0.83 0.081(1.08) (-1.09) (-3.47) (4.22) 4.43)

Sc. Total Deposits 5.632 -0.445 -0.11 1.699 0.759 0.97 6.059(1.9 8) (-1.92) (-1.21) (4.85) (7.96)

15

As mentioned above, these results reflect just part of the overallshifts ir. the asset holders' portfoiios. Any observed increase in the stockof foreign exchange deposits is not necessarily accompanied by a reduction inthe demand for Dinar deposits, but may simply reflect the transfer of foreigncurrency previously held outside the banking system into foreign exchangedeposit accounts. By the same token, asset holders may decide to shift out ofDinar deposits and increase their holdings of foreign exchange assets if theyexpect higher future devaluations. However, that can be accomplished byincreasing the holdings of foreign currency or foreign exchange depositsabroad, as opposed to increasing the holdings of foreign exchange deposits inthe domestic financial system.

Nevertheless, these results do suggest that the demand for Dinardeposits decreases as a result of expected devaluations of the domesticcurrency. The shift out of Dinar deposits into foreign exchange deposits irthe asset holders' portfolios is partly offset by the maintenance of realisticinterest rates on Dinar time deposits. However, realistic interest rates onDinar time deposits are not sufficient to interrupt the overall shift intoforeign exchange assets which results from higher inflation and devaluationsof the exchange rate. In paruicular, foreign exchange sight deposits becomevery attractive in a scenario of high inflation and exchange ratedevaluations. The possibility of using these deposits to make payments (or toconvert foreign exchange into Dinars before making final payments in Dinars)allows individuals to economize on the use of Dinar sight deposits furtherwhen inflation increases.

The large differential between inflation rates in Yugoslavia andthe other OECD countries is the primary cause of the large expected exchangerate devaluations and the resulting decrease in the demand for Dinar depositsvis-a-vis the demand for foreign exchange deposits. Therefore, the estimatesof the demand for Dinar assets obtained with expected inflation or expecteddevaluation are fully consistent. These results suggest that substantialprogress irf the mobilization of Dinar resources and in the reduction ofcurrency substitution will depend on progress in reducing inflation. Inaddition, the interest policy has to be realistic in order to prevent furthershifts out of Dinar assets. That means that the interest rate on time deposit!has to compensate asset holders for their expectations of future inflation anlnominal and zeal devaluations. The interest rate on Dinar sight deposits mayalso have to be adjusted to inflation developments, in other to prevent anexcessively negative real return on these deposits. Finally, progress inreducing currency substitution may also be obtained by imposing restrictionson the use of foreign exchange deposits as means of payments. That can beachieved by introducing minimum size requirements for sight deposits inforeign exchange or introducing minimum maturities.

3.2 The Demand for Money by Enterprises

4 reports the estimates of the enterprises' demand for sight andtime deposits. In the case of enterprises, two alternative proxies for outputwere used in the estimations: the industrial production index (equations A)

16

and the real revenues of the enterprises (equations B). The expectedinflation variable was always proxied by the current inflation rate.

The estimation of the enterprises' demand for money produced mixedresults, as shown in Table 4. In the case of sight deposits, the interestrate and the inflation rate coefficients are negative and significant whenintroduced separately, but are never both significant in the sameregressionl4. Also, the output coefficient in the demand for sight depositsis either non-significant or appears significantly with a negative sign.These results may be reflecting shifts in the enterprises' demand for money.For instance, the need for enterprises to hold cash balances for transactionpurposes may have been reduced as a result of the increasing liquidity ofmoney substitutes such as promissory notes. These shifts are likely to becaptured by the output variable, resulting in low or even negativecoefficientsi!/ . Alternatively, the regression results may just reflect thelack of a good proxy for output in the case of enterprises.

In the case of time deposits, the inflation coefficient isnegative and significant, while the interest rate coefficient appears with theexpected positive sign in most regressions but is never significant. Inaddition, the speed of adjustment seems too low, as indicated by thecoefficient of the lagged dependent variable. Again, these results may alsobe affected by the increase in financial transactions among enterprises duringthis period. The interest rates on promissory notes and other inter-enterprise credit agreements probably followed inflation developments moreclosely than the interest rates on time deposits. If that was really thecase, then the increase in inflation must have increased the attractiveness ofpromissory notes and other related instruments at the expense of time depositsin banks, despite the increases in the nominal return on time deposits.Unfortunately, the insufficiency of quarterly series on both the stocks andinterest rates on inter-enterprises' agreements prevents the econometricanalysis of these factors.

14/ Although the relationship between interest rates and inflation was nevertoo close during this period, there remains some degree of collinearitybetween these two variables which could be affecting the t-statistics. IHowever, this problem does not seem to be affecting the estimates of thehouseholds' demand for money.

1i/ This problem has also been observed in other countries. See, forinstance, Garcia and Pak (1978) for the case of the US in the 1970s and WorldBank Report TU-7162 ( External Debt, Sustainable Growth and Fiscal Policy )for the case of Turkey in the 1980s.

17

Table 4: OWTSU ISTINATES OF THE ENTERtISI' DEPMI FOR NW IN YU VIA, 19t - 97a J

..

Out 1. Sight hsats (A) 0.059 0.011 -0.346 - 0.754 0." o.on(0.02) (0.02) (-2.72) - (1.41)

(A) -0.314 o.0n M -0.51 o.m 0.97 0.071-O.09) (0.14) - (-2.04) (9.13)

(Al -1.l71 0.24 -0.2 -0.469 0.M 0." 0.071(-0.37) (0.411 (-2.041 (-1.201 (1.73)

CU) 1.084 -0.53 -0.247 - O.13 0." 0.045(2.73) (-2.43) (-L."9) - (4.12)

(3) 1.33) -0.43 - 4..94 0.174 0." 0.01(3.31) (-3.31 - (-2.49) (6.71)

(II 1.136 -0.523 -0.177 -0.14 0.411 o.9 0.01(3.061 (-2.55) (-1.34) (-2.U1 (4.3)

4. Tin Qosats (A) -2.372 0.M -0.00 -1.37 0.90 O." 0.03(-1.74) (1.731 (-0.14) (-7.42) (11.58)

(3) 0.177 -0.1l3 0.07o -1.324 0.303 0.97 0.03(0.97) (-0.11 (1.11) (-4.15) (11.15)

TSUI 1. Sight Onisto (A) 2.119 -0.443 -0.321 - 0.706 0.9 0.072(0.40 (-0.38) (-2.21) - (4.61)

(A) 0.M -0.030 - -0.791 0.90 0.97 0.07O(0.04) (0. I) - (-1.5 (5.33)

(A) -L.O 0.37 -o.m -o.51 0.327 O.9 o.on(-0.49) (0.52) (-2.05) (-l.%2 (4.9)

(3) 1.203 -0.40 -0.223 - O.U2 0." 0.05(2.41) (-2.34) (-1.010 - (4.30)

(3) 1.4t7 -0.702 - -0.947 0.355 0." 0.042(3.70) (-3.25) - (-2.42) (7.74)

(3) 1.262 -0.593 -0.156 -0.329 0.59 O." 0.041(2.94) (-2.46 (-1.14) (-2.09) (.41U

2. Tin Deposits (A -1.024 0.45 -0.023 -1.33 0.924 0.91 0.033(1.04) (1.04) (-0.30) (-7.24) (3.47)

(6) 0.042 0.015 0.037 -1.341 0.100 0.97 0.033(0.11) (0.12) (0.47) (-6.131 (10.94)

18

Annex III

THE DYNAMICS OF PUBLIC SECTOR DEBT IN YUGOSLAVIA

I. Introduction

The replacement of NBY's foreign exchange losses by a stock of interestbearing bonds issued by the Gevernment constitutes a recognition of vheselosses as public sector debt. Likewise, the interest expense on the stock ofGovernment debt will be recognized as current budgetary expenditures. Thefiscal burden of NBY's restructuring depends on whether the bonds, issued toreplace the losses, are amortized or not. The evolution of the ratios of debtand interest expense to GNP, as well as the ratio of primary surplus (revenuesminus non-interest expenditures), to GNP will depend on the particularfinancing strategy adopted by the Government, as well as on the interest ratespaid an the debt stock and the growth rate of GNP.

This Annex provides an analysis of the evolution of these ratios underthree alternative solutions to the financing of interest and amortizationpayments on the debt stock. The first solution involves the amortization ofthe debt stock over a period of 40 years. In this case, the primary surplushas to be large enough to cover interest expenditures and the amortization ofthe stock of debt over the planned period of amortization. Unier the secondsolution, the stock of bonds is not amortized. In this case, the primarysurplus only has to cover interest expensesi'. In addition, one couldenvisage a third solution, involving a constant debt-output ratio.

2. Debt Dynamics: Primary Surpluses. Real Interest Rates and Output Growth

In the absence of Centrai Bank financing, the Government's budgetconstraint reduces to:

(1) D + (i + E)B E - (BE)

Where D is the nominal primary deficit/surplus, i is the international(Deutsche Mark) nominal interest rate paid on the (Deutsche-Mark denominated)debt stock, B*, and E is the nominal exchange rate (Dinar/Deutsche Mark). Thedots over the variables represent derivatives with respect to time and thepercentage changes (x - x/x). In equation (1) interest payments and the debtstock are stated in terms of Dinars. That is, the stock in Dinars, B, isequal to B*E, and the interest rate is adjusted for the exchange ratedepreciation. The sum of the two terms on the left side of the equationconstitute the nominal deficit. Equation (1) can be expressed in real terms

1/ As mentioned in Chapter VI, a constant real debt stock, as in the secondsolution, could also be achieved by financing the redemption of these(exchange-rate indexed bonds) through issues of inflation-indexed bonds.However, this swap of Dinar for foreign exchange-denominated debt is notconsidered to be adequate since it would generate a currency mismatch inthe banking system.

19

by dividing all the variables by the price level, P, multiplying and dividingthe Interest and the debt terms by the international (Germany) price level,P, and splitting e international nominal interest rate between the real rate,r, and the inflation premium, pal

(2) d + (r' + e)b^e (b-e)

Where d = D/P is the real primary deficit/surplus; b^ - B /P is thereal stock of debt, e - EP-/P is the real exchange rate and b^ the real changesin the stocky. Equation (2) is a linear differential equation in eb. Itshows that changes in the real Dinar value of the debt stock is driven by thereal primary surplus, d, the real interest payments in Deutsche Marks, rb'eand devaltiations of the real exchange rate, eb-e--a capital loss term.

Dividing all the variables in equation (2) by the real GNP, y, andnoting that (eb-)/y - (eb'/y) + y(eb'/y), where y is the rate of growth of realGNP, one obtains:

(3) (eb'/y) - d/y + r'(eb'/y) + e(eb-/y) - y(eb'/y)

Equation (3) shows that the changes in the real debt-output ratio aredetermined by the size of the real primary deficit relative to real GNP, thereal interest payments relative to real GNP, a capital loss term and an outputgrowth factor. Denoting the real debt stock in terms of Dinars as b - eb ,equation (3) can be rewritten as:

(4) (b/y) - d/y + ( r - y ) b/y + e b/y

Equation (4) indicates the three essential factors which drive the debt-output ratio: the primary deficit, the real interest rate-output growthdifferential and the real exchange rate devaluations. If the real exchangerate is kept constant, e G 0, equation (4) reduces to:

(4') (b/y) - d/y + (r' - y ) b/y

Which is a first-order linear differential equation whose generalsolution is:

(5) (b/y)(t) - e (r0dt ( K + (d/y)(t) e ("r.)dt dt )

It is useful to analyze the dynamic properties of the debt-output ratiounder an exchange rate policy which maintains a constant real exchange rate.Discrete adjustments in the real exchange rate produce jumps in the real debt-output ratio but do not affect the dynamic properties of the debt-output ratio(convergence/non-convergence). Of course, a continuous and sustained real

~./ i - r + p' . This formulation assumes perfect foresight, i.e. equalitybetween expected and realized inflation rates.

1/ b G B /P - pb'

20

exchange rats devaluation would affect the dynamic properties of the debt-output ratio, but this possibility is ruled out. Therefore, the sectionsbelow analyze the behavior of the debt-output and the primary surplus-outputratios under the hypothesis of a constant real exchange rate. The lastsection comments on the effects of real devaluations.

2.1. Solution 1: Primary surplus covers interest expenses and theamortization of the stock over a period of 40 years,

The solution to equation (5) is greatly simplified in the particularcases mentioned above. The first solution envisaged by the Yugoslavauthorities involves the generation of a primary surplus (through highertaxes) large enough to cover interest expenses and the amortization of thedebt stock over a period of 40 vears. In this case, the changes in the realstock of debt are determined by the constant yearly real amortizations:

(6) b - - a(t)

Where a(t)--the real amortization at period t--is equal to: b(0)/40,where b(0) is the initial real stock of debt. The solution to thedifferential equation (6) is simply:

(7) b(t) - b(0) - a. t b(0)( 1 - t/40 ) ; t < 40.

Assuming that real output gxows at a constant rate, y, the level of realoutput at period t, y(t), will be equal to y(0)eY'. Therefore, the real debt-output ratio at period t will be equal to:

(8) (b/y)(t) - (b/y)(0) e-Yt ( 1 - t/40 )

The real primary surplus at period t, d(t), is equal to:

(9) d(t, - - rb(t) - a(t)

Substituting the values of a(t) and b(t) and dividing by the real outputat period t one obtains the ratio of primary surplus to output at period t:

(10) (d/y)(t) (b/y)(0) eY' ( -r' + 1/40 ( r t - 1 ))

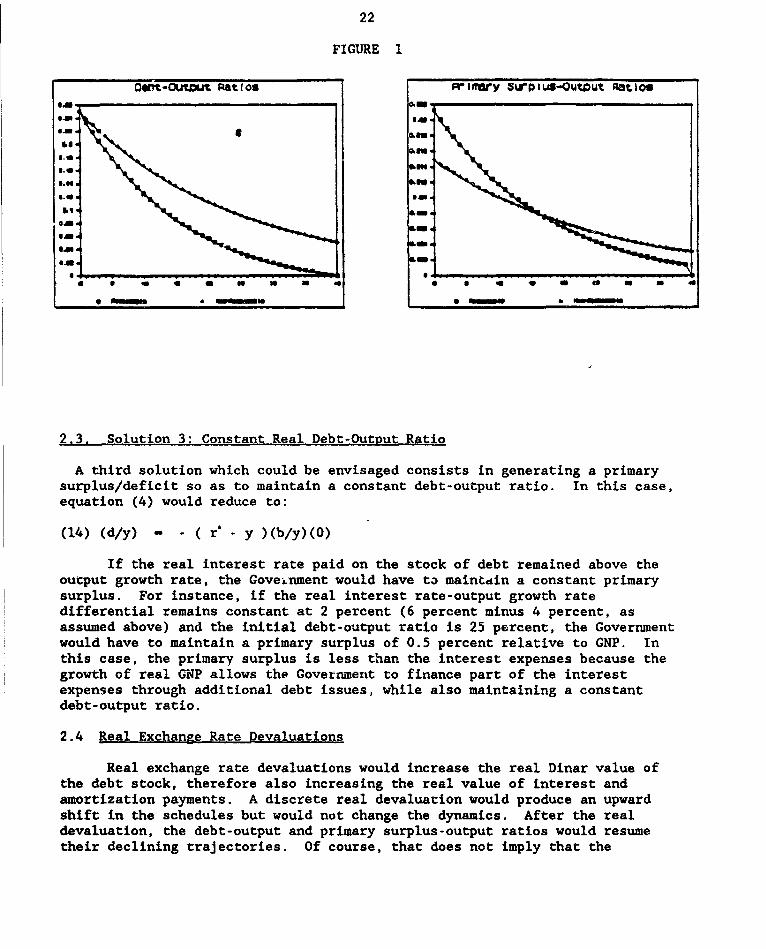

Figure 1 shows the time paths of the ratios of debt to output andprimary surplus to output for an initial real debt-output ratio of 25 percent,a constant real interest rate of 6 percent and a real output growth rate of 4percent. Under this solution, the real debt-output ratio would declinerapidly--approxiamtely 12 percent in just 10 years. The required real primarysurplus would also decline rapidly--from more than 2.1 percent of real GNP inthe first three years to 1.1 percent of real GNP in the same period.

2.2 Solution 2: Primary surplus covers interest expenses

Under the second solution the bonds issued to replace the stock oflosses are not redeemed. This solution consists in a zero real deficit and aconstant overall real debt stock. This is accomplished by setting the primary

A -

deficit at a level equal to the interest expenditures and keeping the stock ofbonds in NBY's balance sheet. The required primary surplus relative to GNPwould be d/y - - r b/y. In this case equation (4') reduces to:

(11) (b/y) - - y (b/y)

Equation (11) is a homogeneous, first-order linear differential equationwith constant coefficient, whose solution is:

(12) (b/y)(t) - (b/y)(0) e-Yt

In this case, the required primary surplus relative to GNP is alsoeasily obtained:

(13) (d/y)(t) - r' (b/y)(0) e-Yt

Figure 1 shows the time paths of the teal debt-output and primarysurplus-output ratios under the same conditions used to illustrate the firstsolution. In the second solution, the real debt-output ratio declines lessrapidly. This is obvious, since in the first solution the real debt stock isbeing amortized, while in the second solution the overall debt stoe~k is keptconstant in real terms and the decline in the real debt-output ratio is onlydlue to the growth of real output. Nevertheless, the compounding of outputgrowth rates over time also produces a significant decline in the debt-outputratio in the second solution--after 40 years the debt-output ratio would bereduced to approximately 5 percent. The prima-y surpluses immediatelyrequired in the second solution would be smaller--between 1.5 and 1.2 percentof GNP in the first five years, compared with 2.1--l.7 percent of GNP in thefirst solution. After the seventeenth year the required primary surplus inthe second solution would become larger than the one required in the firstsolution. However, at this stage the required primary surpluses under eithersolution would be extremely small--less than 0.8 percent of GNP and declining.

It should be noted that the level of real interest rates does notproduce any impact on the time path of the real debt-output ratio under eithersolution. This is because in both cases the primary surplus is adjusted so asto cover the interest expenses on the stock of debt (in the first solution italso covers the amortization of the stock). Therefore, in either case thereal interest rate may be above the output growth rate without causingproblems of divergence!/. However, the level of real interest rates doesaffect the required primary surplus relative to GNP.

i/ As shown in equation (5), if the real interest rate is higher than theoutput ,rowth rate, the debt-output ratio does not converge to anyfinite value.

22

FIGURE 1

CeOtt-OUtWt Rat(O s rrlnry surpus-outout RatLos

C41.~~~~~~~~~~~S

B. - 0.03

161

ILM.

B. _ . . , ,

2.3. Solution 3: Constant Real Debt-Output Ratio

A third solution which could be envisaged consists in generating a primarysurplus/deficit so as to maintain a constant debt-output ratio. In this case,equation (4) would reduce to:

(14) (d/y) - - ( r - y )(b/y)(0)

If the real interest rate paid on the stock of debt remained above theoutput growth rate, the Goveinment would have ta maintdin a constant primarysurplus. For instance, if the real interest rate-output growth ratedifferential remains constant at 2 percent (6 percent minus 4 percent, asassumed above) and the initial debt-output ratio is 25 percent, the Governmentwould have to maintain a primary surplus of 0.5 percent relative to GNP. Inthis case, the primary surplus is less than the interest expenses because thegrowth of real GNP allows the Government to finance part of the interestexpenses through additional debt issues, while also maintaining a constantdebt-output ratio.

2.4 Real Exchange Rate Devaluations

Real exchange rate devaluations would increase the real Dinar value ofthe debt stock, therefore also increasing the real value of interest andamortization payments. A discrete real devaluation would produce an upwardshift in the schedules but would not change the dynamics. After the realdevaluation, the debt-output and primary surplus-output ratios would resumetheir declining trajectories. Of course, that does not imply that the

23

additional fiscal effort that would be required by a real devaluation may beoverlooked. For instance, under the adopted assumptions, the implementationof the second solution would drive the debt-output ratio down to 20 percent inthe fifth year. A real devaluation of 20 percent in that year would drive thedebt-output ratio close to its original value, thus requiring an additionalfiscal effort. In any case, the fiscal adjustment required by the secondsolution is smaller in the early years. That makes it quite atractive,especially one takes into account the need to provide fiscal support to therestructuring of enterprises and banks in the same period.

24

Annex IV

The Bak_ing System In Yu_oslavia

I. The Central Banking System

1. The Institutional Set-up. The central banking system of Yugoslavia(National Banks, for short) comprises the National Bank of Yugoslavia (NBY)and the National Banks of the eight Republics and Autonomous Provinces(NBRAPs). The assets of the National Banks account for approximately30 percent of the total assets of the financial system.!1 The design andconduct of monetary policy in Yugoslavia are carried out by the National Banksthrough a Board of Governors consisting of the Governors of the NBRAPs and theGovernor of the NBY. Decisions of the Board are binding on all the NationalBanks. Until recently, most operational decisions required a unanimous vote;now, however, all decisions are based on a majority vote. In case the Boardfails to reach a decision, the Federal Executive Council makes the finaldecision. The NBY is responsible to the Federal Assembly, whereas the NBRAPsare responsible to the respective assemblies of the Republics and Provinces.

2. Functions. In general, the functional responsibilities of the NationalBanks in Yugoslavia are similar to those of the central banks in othercountries. They are responsible for the design and the implementation ofmonetary and credit policies of the Government. They perform this function inthe context of the annual economic plan o the Government, called the AnnualResolution. Upon approval of the Annual solution by the General Assembly,the Board of the Governors of the NBY decides on the policies and measures toachieve the monetary objectives and targets of the Resolution. Thesedecisions and the Board's recommendations are then submitted to the FederalExecutive Council for approval. When the Board's recommendations areapproved, they are sent back to the NBY for implementation. The NBY theninstructs the NBRAPs as to the manner in which these policies should becarried out.

3. Unlike the central banks in many countries, the National Banks do notengage in direct short-term lending to the Federal Government.V However, theNational Banks have been implicitly extending credit to the Government byassuming the foreign exchange risk on foreign currency deposits collected bythe commercial banks. The latter has created enormous losses for the NationalBanks and has been the major source of base money expansion in Yugoslavia.

4. Noteworthy, with respect to the National Banks' operation, is theirpreoccupation with para-fiscal activities and extending credit on preferential

1/ Including non-bank intermediaries, but excluding the inter-enterprisemarket.

2/ The exception is credit to the army.

25

terms to priority sectors. At the heart of this issue stands the policy ofregional allocation of the benefits of base money creation. In practice,these para-fiscal tasks seem to take priority over the National Banks' task ofconducting a national monetary policy aimed at price stability.

II. The Commercial Banking System

A. Financial Arrangements in the Post-War Period

1. The post-war period has seen a number of profound changes in theYugoslav political and eccnomic system which have been reflected in themechanisms for resource mobilization and allocation and in the structure ofthe financial system. Between 1945-1952, the pre-war market economy wasgradually replaced by a centrally-planned economy in which planning 'DoAiesmade practically all savings and investment decisions, and the Natioial Bankof Yugoslavia (NBY) performed all central and commercial banking operations.Si..ce that time, there have been three stages of increasing decentralization.The first elements of self-management were introduced between 1953-1964,during which time the NBY gradually transferred part of its functions tonewly-established banks, and the Social Accounting Service (SDK) became anindependent institution. A second decentralization was launched throughreforms in 1965, aimed at enlarging the scope of self-management. Banks weretransformed into three types of so-called "business" banks (investment, mixedand commercial) and began to exercise significant influence on the investmentdecisions of enterprises, partly because of the easing of previously imposedcentral planning requirements. Considerable powez was also enjoyed byGovernment bodies, especially at the local and regional level.

2. The period from 1971 to the present began with a major reform program inwhich self-management was extended to all levels of decision-making inassociation with an important transfer of power from the Federal to theRepublican, Provincial and local Governments. In 1971, the productionstructure of the economy was fragmented by splitting existing enterprises intoBasic Organizations of Associated Labor (BOALS). The Law on the Foundationsof the Credit and Banking System was adopted in 1977 and reflected theintention that the "pooling of labor and resources" would become the mkjstimportant instrument for mobilization and allocation of savings in theeconomy. The law replaced existing banks by basic and associated banks, whichwere to be organized and managed as "financiel associations of associatedlabor". It also led to the creation of internial banks as financiai serviceorganizations for BOALS bound together by self-management agreements withinlarger organizations of associated labor. Although significant revisions tothe banking legislation were made in 1985, the Law on the Premises of theBanking and Credit System, which was introduced at the end of that year,helped to maintain the three-tier structure of internal, basic and associatedbanks until recently.

3. Yugoslavia is now in the midst of a policy and legislative reform effortwhich is aimed at achieving a more fundamental restructuring of its economicsystem. The constitution was amended in late 1988. An extensive package ofnew legislation has been introduced, including new laws on enterprises and on

- 26 -

foreign investment (in December 1988), on accounting and on financialoperations (in February 1989) and the new "Law on Banks and other FinancialOrganizations" which was issued on February 17, 1989.

4. Section B of this Annex reviews the main features of the commercialbanking system from 1977 to present day. Section C focusses on the newbanking law and further elements of the legislative framework needed toachieve reform objectives.

B. Institutional Structure of the Financial System from 1977-1989

1. The Commercial Banking System

5. By the beginning of 1988, the commercial banking system consisted ofabout 150 basic, 9 associated, and more than 200 internal banks. The maintask of internal banks was to place in circulation the pooled resources oftheir member enterprises and to channel resources to priorities agreed bythem. The internal bank conducted the BOALs' payments operations and lendingand credit transactions. They were allowed to accepc deposits only from memberBOALS and from the workers within the group. They were not subject tomonetary regulation and some internal banks have therefore been able tosubstantially expand their financing activities and become major participantsin enterprise financing.

6. Basic barks formed the core of the commercial banking system: theyaccepted individual and enterprise deposits and extended short- and long-termfinancing to public and private customers. They were founded, owned andalmost exclusively directed by enterprises and, to a lesser extent, by SocialCommunities of Interest. The larger enterprises were the dominant foundersand also the principal borrowers of the banks.V Ownership of a basic bank bygovernmental bodies was explicitly excluded. Whereas the basic banks weremeant to mobilize resources for the purpose of financing "social production",in a narrower but more critical sense, they aimed at satisfying their foundersdemand for credit at the lowest possible cost. The basic banks were, hence,not truly profit oriented and have been undercapitalized&.

i/ In fact the actual borrowers were not production nor financiallyintegrated entities, but rather the individual basic organizations ofassociated labor (BOALS) which comprised an enterprise.

§/ The equivalent of the banks' equity capital were their reserves: theJoint Liability Fund (JLF), the Fixed Assets Fund, and the Reserve Fund(RF). These funds were made up of the initial contribution of thebanks' founders and contributions from the surpluses of the banks. TheFixed Assets Fund covered expenditures incurred in providing fixedassets needed for the operation of the bank. The JLF was used forwriting off losses. The RF was used to maintain the liquidity of thebank.

- 27 -

7. The law provided that the primary management body of a basic bank wouldbe the assembly. Representatives of the founders made up the banks'assemblies, executive committees, credit committees and supervisingcommittees. Operational managers did not serve on these committees.Furthermore, although the basic banks were legally designed to operatenationwide, their activities were mostly confined to their original regions,partly as a result of their ownership structure. Their numbers did not varysubstantially until 1987 (when seventeen banks in Macedonia, two in Croatia,and one in Vojvodina were merged with other banks in the same RAP).

8. Associated banks were founded and managed by two or more basic banks.Their main function was to pool the resources of basic banks, to undertakeborrowings for large operations, and to handle foreign exchange and creditactivities on behalf of their member basic banks. Unlike basic banks, theywere not permitted to issue checking accounts or accept savings deposits. Theassociated banks were also originally envisaged as nationwide institutions.However, the associated banks have served the interests of the basic bankswhich form their group and primarily of the RAP in which they are located. Atpresent, there is one associated bank in each RAP except for Serbia, which hastwo. With one exception (Jugobanka, one of the banks headquartered inSerbia), the extent of these banks' operating sphere beyond regionalboundaries has been extremely limited. The actual relationship between basicbanks and their associated bank varied among the nine associated bankinggroups and there was a marked difference in the strength of the associatedbanking groups in different RAPs. However, in all cases the associated banksexercised a leadership role, which in part reflected the generally greatermanagerial strength and technological sophistication of the associated banks,and in part the importance of their specialized functions (foreign credit andexchange transactions, larger scale borrowings, guarantees, etc.).

2. Bank Associations and Regulatory Institutions

9. Ail banking organizations were legally required to be members of theAssociation of Yugoslav Banks (YBA), which was in turn represented in theChamber of the Economy. YBA promoted inter-bank co-operation and bankingactivities; provided legal and professional staff assistance to banks; andcooperated with the federal authorities in the formulation of laws on monetaryand banking issues. The cooperation among banks within the YBA was formalizedthrough self-management agreements, and a notable example of these were theagreements on the uniform interest rates on deposits.Y In addition to theYBA, there are three regional bank associations.

10. Basic and associated banks have been supervised by the MBY. They havebeen audited by the Social Accounting Service (SDK). SDK is an autonomousorganization responsible to the Federal, Republican and Provincial assemblies.It operates nationally through a network of branches and performs three types

5/ Based on the agreement of its member banks, the YBA has also managed thedevelopment of the recently approved Common Methodology for investmentselection which is to be applied throughout Yugoslavia.

- 28 -

of operations: it has been the financial auditor of banks and enterprises andsocio-legal entities; it acts as a clearing center for all payments ofenterprises and socio-legal entities (with the exception of socio-politicalcommunities whose payments are undertaken by the central banking system);Vand It collects and publishes statistical information based on the quarterlyreports and annual accounts which all socio-legal entities are obliged toprovide.

WX SDK performs payment services as a bank agent, its balances being aliability to the bank in which the deposits are originally held.

29

Annex V

NON-BANK FINANCIAL INSTITUTIONS

1. In Yugoslavia, a number of non-bank financial intermediaries (NBFIs)have been established, including savings banks and insurance companies. Thusfar, however, their role in the financial system has been limited.

2. Post Office Savings Banks (POSBs). POSBs, like banks, are founded bybasic organizations of associated labor (BOALs) and managed by a boardcomprising representatives of the founders. They are authorised to acceptdeposits from individuals and to make foreign payments on behalf of theirfounders. However, unlike banks, POSBs are not authorised to grant credits,except to their founders and are obliged to deposit th2ir surplus funds inbasic banks within their region. At present, POSBs play a very minor role inthe financial system; their total assets are equivalent to only about 1% ofthe total assets of the associated and basic banks.

3. Savings Banks. In contrast to POSBs, savings banks play an even smallerrole in the financial sector; their number is small and their assets amount toa minute fraction of the assets of POSBs. However, unlike POSBs, they areauthorised to grant credits to households. According to the law, savingsbanks can be established by BOALs and other social/legal entities.

4. Insurance Companies. Insurance companies provide both life insuranceand general and casualty insurance. Like POSBs, the use of their funds isrestricted to deposits in banks only. The funds of the insurance companiescannot be used to purchase money market instruments or to make investments.Total assets of the insurance companies is again a negligible percentage oftotal financial system assets.

5. Self-managed Funds of Associated Labor (SFAL). SFALs are joint or"pooled" funds of enterprises. These are formed, when two or more enterprisescombine their financial resources to finance a "joint venture"; these jointventures are of a contractual rather than equity nature. Typically, one ofthe enterprises in the "pool" would be the lead investor and the otherenterprises in the "pool" would provide financing with both loan and equityfeatures.

6. Thus, for instance, a risk sharing agreement (the contract) might benegotiated whereby the non-lead investor enterprises may have a first claim ora disproportinately large claim (in relation to their financial contribution)on the profits of the joint venture for the duration of the contractualagreement (although the non-lead investor enterprises may be liable for lossesas well). At expiration of the agreement, the lead enterprise typicallybecomes the sole owner of the project (with or without having to pay atransfer price to the other enterprises). Alternatively, the partners maynegotiate to continue the contractual agreement. To a large extent, however,the arrangements are such that the non-lead enterprises will generally have toseek a return on their initial contributions from their share of project

30

profits (during the contract period), rather than from any capital gains atthe termination of the contract.

7. A number of companies interviewed have expressed their unhappyexperience, as non-lead investors, with this form of arrangement. They claimto have limited management control over the new projects (which are normallymanaged by the lead enterprises) and have often received low or negativereturns to their contributions, since many projects are of a developmentalrather than commercial nature (see following section) and also because leadenterprises are not particularly motivated to maximize profits during theperiod of the joint venture agreement, knowing as they do that ownership ofthe joint venture eventually reverts fully to them.

8. Investment Loan Funds (ILFs). Various investment funds have beenestablished by law for the specific purpose of financing projects in theless-developed regions of the country. The most important of these is theFederal Fund for Financing Economic Development of Less-Developed Republicsand Autonomous Regions. Similar funds have also been established at therepublic and local levels. Generally speaking, contributions to thefe fundsare made by enterprises, are obligatory and are channelled through basicbanks. Since 1980, enterprises have been permitted to use up to 50% of theircontributions to the Federal Fund to finance SFAL projects which they havenegotiated with enterprises in less-developed regions. In the 1980s,investment funds have averaged about 2% of GSP per annum.

9. The Yugoslav Bank for International Economic CooReration (YUBIEC).YUBIEC is an export credit and insurance institution, whose main function isto promote Yugoslav exports and to develop economic relations with foreigncountries. Up until 1968, Yugoslavia's export of capital goods was financedby Jugobanka, at that time, a specialized bank for foreign trade. Jugobankaobtained its resources from the NBY and the state. In 1968, Jugobanka'sfunctions were taken over by the Export Credit and Insurance Fund (ECIF),which was established to refinance credits granted by commercial banks for theexport of capital goods and to provide insurance against non-commercial risks.To support these activities, the ECIF obtained its funds from the state andfrom borrowings.

10. In 1979, the functions of ECIF were in turn taken over by the newlyestablished YUBIEC. In addition to the ECIF functions, YUBIEC was assignedadditional export promotion tasks, such as financial cooperation with foreignparties, promotion of joint ventures, financing of preinvestment activities,legal and financial consultancy and the supply of information to founders ofthe bank. The founders of YUBIEC consisted of exporting enterprises, namelyshipbuilders, capital goods manufacturers and capital project contractorsoperating abroad. As of the end of 1988, YUBIEC had a total of 182 members.YUBIEC financed itself by drawing on funds from its members, basic andassociated banks and the NBY. Other sources of funds included foreignborrowings and security issues.

11. In the first half of 1989, the new Law on the Yugoslav Bank forInternational Economic Cooperation was promulgated. Under this Law, YUBIEC isto be transformed into a Joint-stock company and its ownership expanded to

31

include the state and banking institutions, as well as exporter enterprises.The restructured Bank will provide preshipment credits for capital equipmentand ships and grant credits to foreign buyers (buyer's credits) in its ownname and for its own account. It is envisaged that YUBIEC will continue tofund itself through the domestic and international capital markets.

32

Annex VI

Yugoslav Money and Securities Market

The history of the money market in Yugoslavia dates back to 1967, whencertain banks found a necessity for inter-bank transactions and accordinglyorganized a market. Tne money market is utilized by both enterprises (toraise short-term credit) and banks (to meet reserve requirements and to keepwithin credit ceilings).

Reflecting the regional structure of the banking system in Yugoslavia,the money market has developed into a two-tier market. Banks within the sameassociation deal directly with each other, while inter-associationtransactions are conducted primarily at the level of associated banks. Ineffect, banks attempt to satisfy their needs through intra-associationtransactions in the first instance, and inter-association transactions takeplace only as a means of clearing the surpluses and deficits of bankingassociations as a whole.

In 1987, more formal recognition was given to the money market, with theestablishment of the Yugoslav Money and Securities Market (YMSM). The YMSM isphysically located in Belgarde and is organized under the auspices of theYugoslav Bankers Association, on the basis of a self-management agreement (asprovided for by Article 165 of the Law on the Bases of the Credit and BankingSystem). Participants in this market include members (basic and associatedbanks) and non-members (other financial institutions). POSBs, for example,are non-members, but are permitted to deposit funds in and to borrow from themarket, although they are not allowed to engage in the trading of securities.As of November 1987, the number of participants in the market totalled 176.

The YMSM is organized with an Assembly (consisting of representatives ofmembers), a Board of Control (7 members) and an Executive Committee (23members). Members of the Board and the Committee are elected by the Assemblyfor two year terms. The function of the Executive Committee is to implementpolicies adopted by the Assembly, while the function of the Board is tomonitor and supervise the work of the Executive Committee. The Board meetsonce a year, while the Committee meets once or twice a month. Assemblymeetings are held once or twice a year.

The law provides for the YMSM to engage in the following activities:

1. The attraction and lending of idle money resources of banks andother financial organizations.

2. The trading of negotiable short-term securities.

3. The buying and selling of long-term securities.

4. Other transactions related to the speeding up of the circulationof idle money resources and the maintenance of the liquidity ofbanks.

33

The YMSM distinguishes itself from direct inter-bank operations in thatit is more like a bank (a "bank of banks") than a market. The YMSM acceptsdeposits (up to two years in term) from, and makes short-term loans to, banksand POSBs (up to one year in term). With its surplus funds, it also purchasesbills and notes from banks, subject to specific decisions adopted by itsAssembly. It does not, however, issue securities. During periods of tightcredit ceilings, the YMSM provides the banks with a mechanism for off-loadingthe promissory notes in their portfolios and thus lowering their creditexposure.

The law requires that the issue of all promissory notes be backed bygoods and services: i.e. that notes and bills be issued on the basis of "realcommodity-money relationships". In practice, however, the recording,monitorin; and regulatory system has been weak and inadequate (as confirmed byan audit of the Serbian SDK in Belgrade (see Report Incorporating ArrangementsProposed for Regulating the Status and Operation of the Yugoslav Money andSecurities Market, Federal Secretariat of Finance, Belgrade, 20 November,1987). This was one of the major factors leading to the "Agrokomerc" affair,in which a large number of promissory notes were improperly issued and nodetermination was made as to the liquidity and creditworthiness of the issuinginstitution.

Following the "Agrokomerc" affair, attempts have been made to strengthenthe regulation and security of the market. To this end, the YMSM's Assemblyadopted a resolution to regulate the discounting of bills and notes in themarket. This resolution sets out the conditions under which bills and notescan be discounted in the YMSM. Specifically, the market may only accept billsand notes for discounting if such bills and notes have been:

1. purchased by basic banks from their trading partners;

2. issued in accordance with the Law on Securing Payments BetweenUsers of Social Assets;

3. issued with a face amount of not be less than one million dinars;

4. issued with a maturity of not be less than 10 days and no longerthan 60 days;

5. endorsed by the issuing bank and have changed hands at least once(not including the issuing bank) before presentation to themarket.

34

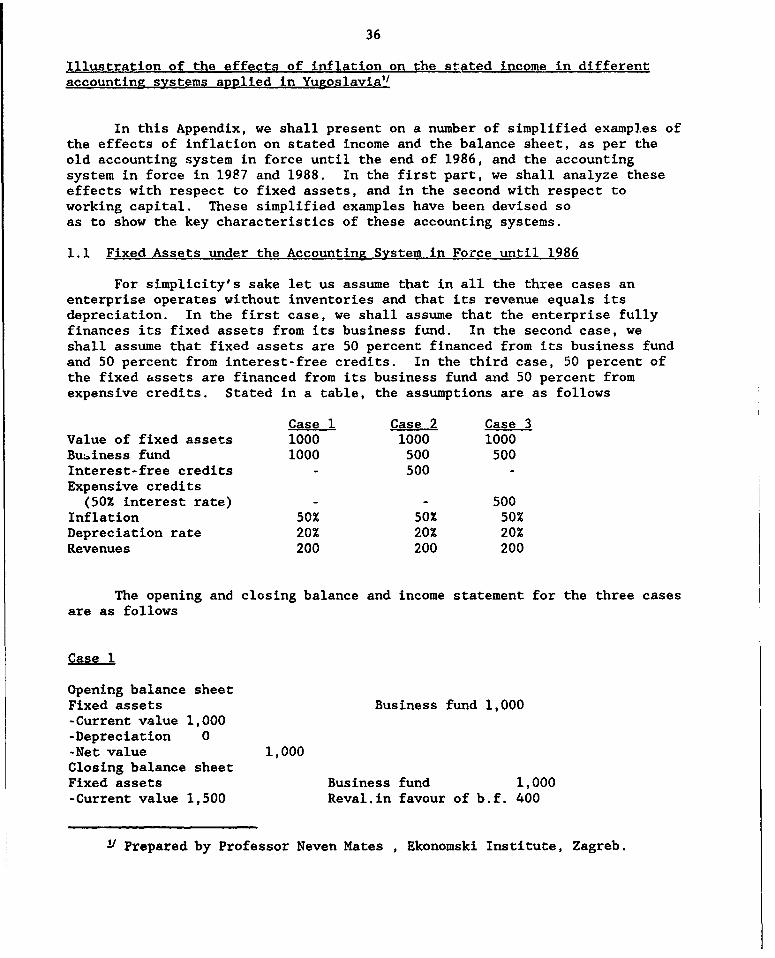

ANNEX VII

Structure of the Income Statements of Yugoslav Enterprises in the

Petiod 1986. 1987-88 and the ProDosed Structure for 1989'

In this Scheme we shall present the structure of the income statementsof Yugoslav firms in three different periods. This is not how thesestatements actually look like; they have been transformed in order to presenttheir logic in a simple manner. This scheme can also be used forunderstanding how revaluation effects are treated on the income statements.

Items to be deducted are in brackets.

Structure up to 1986

1. Revenues, including financial revenues

2. (Cost of goods sold)

3. (Depreciation)

4. Income (1-2-3)

S. (Financial costs)

6. (Taxes and contribution)

---- _--------------

7. Net income (4-5-6)

8. (Personal income, i.e. wages and salaries)

9. (Collective consumption)

_____________a_____

10. Profit or loss (7-8-9)

* Prepared--by Professor N. Mates

35

Structure in 1987 and 1988

1. Revenues, including real financial revenues

2. (Cost of goods sold)

3. (Revaluation of c.o.g.s)

4. (Net revaluation costs)

S. (Revaluation of the business fund, if not covered by the revaluation

surplus)

6. (Depreciat&on)

7. (Revaluation of depreciation)

___________________