chestertonhumberts.com CHESTERTON HUMBERTS RESEARCH BRIEF – SPRING 2012 The Investment Case for UK Agricultural Land RETURN TO THE COUNTRY?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

chestertonhumberts.com

CHESTERTON HUMBERTS RESEARCH BRIEF – SPRING 2012

The Investment Case for UK Agricultural Land

RETURN TO THE COUNTRY?

CHESTERTON HUMBERTS RESEARCH BRIEF2

• AveragefarmlandvaluesinEngland&Walesreachedrecordlevelsin2011andChestertonHumbertsforecaststhattheywillincreasebyanaverageof6%perannumoverthenextfiveyears

• Growthinfarmlandvalueshasoutpacedequitiessincetheearlynoughtiesandresidentialpropertysince2007

• Overa5and10yearperiod,ruralpropertytotalreturnsoutperformedequitiesby690bpsand960bpsrespectively

• UKagriculturalincomegrowthoverthepastdecadewasoverthreetimeshigherthantheEU27average

Thecaseforinvestingintheagriculturalsectorisbecomingincreasinglycompelling.Agriculturallandisatangibleassetwhichoffersportfoliodiversificationopportunities,andthereislowcorrelationbetweenyieldsforfarmlandandthoseforothermainstreamassets.Thishasbeenofparticularrelevanceduringthepost-globalrecessionyearswhenagriculturallandhasperformedwellincontrasttotheuncertaintysurroundingthemoreestablishedassetclasses.Moreover,farmlandinvestmentshavehistoricallyprovidedaneffectivehedgeagainstinflationandrepresentarenewableresourceunlike,forexample,oilandpreciousmetals.

TheUKadditionallyofferstaxplanningincentivesassociatedspecificallywithagriculturallandwhichfurtherenhancetheattractivenessofthesector.Theserelateprincipallytoincometax,capitalgainstaxandinheritancetax.Furthermore,theUKpropertysystemistransparentandofferscleartitleto

owners,withinastablepoliticalandeconomicenvironment.

Investorinterestinagriculturallandhasincreasedsincetheglobalrecessionwithwealthyindividuals(forinvestmentandlifestylepurposes),privateequityfunds,institutionsandspecialistagri-fundsallrepresentedalthoughthemajorityoffarmlandtransactionsareaccountedforbyfarmerslookingtoexpandoperationsand,inthecurrentenvironment,takeadvantageofhighsoftcommodityprices.ForeignpurchasershavebenefittedfromtherelativeweaknessofSterlingoverthepastfewyears.

Accessingthemarketcanbedifficult,however,asthereiscurrentlyashortageofavailablelandandaround25%ofdealswhichtakeplacearetransactedoff-market.Transactionvolumein2011wassimilartothatrecordedin2010andwasalittleunder5%higherthanthe10yearannualaverage.

return to the country? The Investment Case for UK Agricultural Land

Thecombinationofagrowingpopulation,risingsoftcommoditypricesandthedrivetofindsustainablealternativefuelsourcesisplacinggrowingpressureonthesupplyofagriculturallandwhichinturnisattractingincreasinginvestorinterest.Thisreportexaminestheperformanceoftheagriculturalsectorovertimeandassessesitslongertermprospects.

AGRICULTURAL LAND AS AN INVESTMENT ASSET CLASS

INTRODUCTION

Agriculturallandisatangibleassetwhichoffersportfoliodiversificationopportunities,andthereislowcorrelationbetweenyieldsforfarmlandandthoseforothermainstreamassets.

CHESTERTON HUMBERTS RESEARCH BRIEF 3

Institutions

Private Equity Funds

Agri-Funds

Private individuals/Family Offices

Farmers62%

22%

8%

5%3%

Source:RICS&ChestertonHumbertsResearch

Figure1:UKfarmlandpurchasersbytype:2008-11

0

100

200

300

400

500

600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source:Defra/RICS

Figure2:reportedfarmlandtransactions

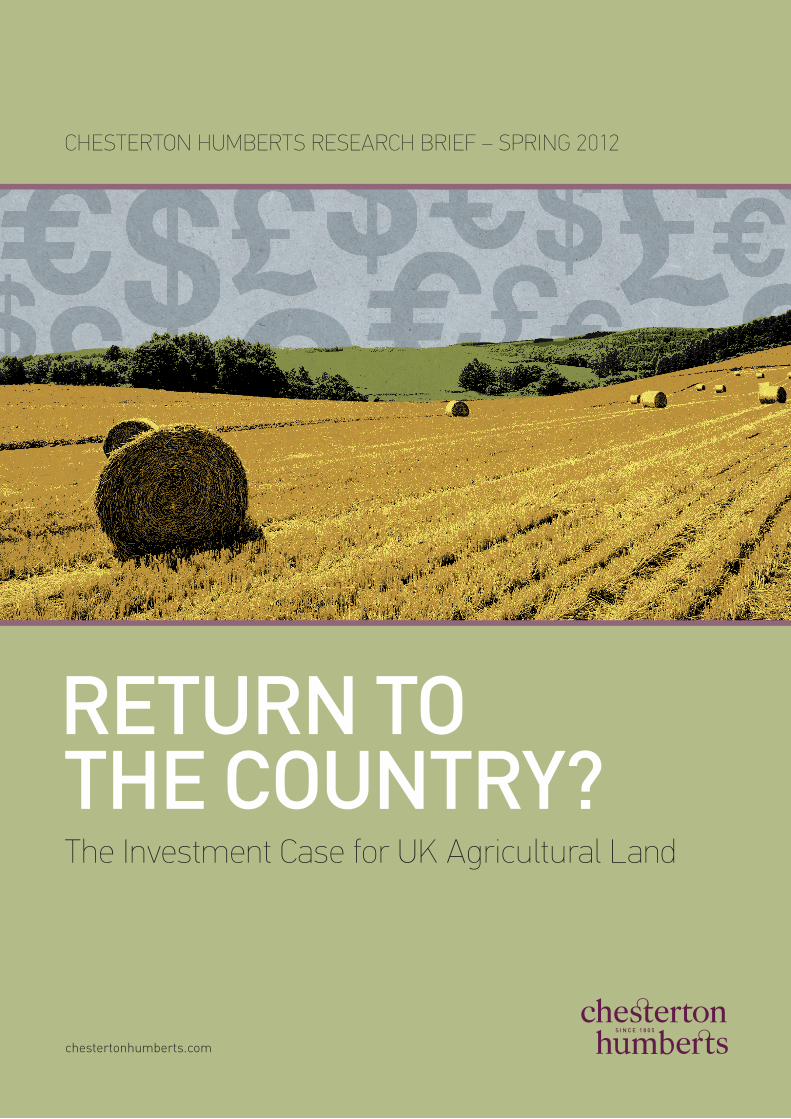

AccordingtotheIPDRuralPropertyInvestmentIndex,thesectorintheUKhasdeliveredsuperiortotalreturnscomparedtocommercialproperty,residentialpropertyand

equitiesoverathree,fiveand10yearperiodandhasoutperformedgiltsoverafiveand10yearperiod.

KEY PERFORMANCE INDICATORS

CHESTERTON HUMBERTS RESEARCH BRIEF4

-4.00% -2.00% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00%12.00%

14.00%16.00%

CommercialProperty

10 year5 year3 year1 year

ResidentialProperty

RuralProperty

Gilts

Equities

Source:IPD

Figure3:UKnominaltotalreturns,ungeared,asatend-December2010

AveragefarmlandvaluesinEngland&Waleshavealmostquadrupledsince1995andtheRICSRuralLandMarketSurveyreportedthattheyreachedarecordhighin2011of£20,722perhectare.Yearonyeargrowthof

averagefarmlandvalueshasoutpacedthatofequitiessincetheearlynoughties,residentialpropertysince2007andhasonlybeenovertakenbygoldinthelasttwoyears.

1995

H1

1995

H2

1996

H1

1996

H2

1997

H1

1997

H2

1998

H1

1998

H2

1999

H1

1999

H2

2000

H1

2000

H2

2001

H1

2001

H2

2002

H1

2002

H2

2003

H1

2003

H2

2004

H1

2004

H2

2005

H1

2005

H2

2006

H1

2006

H2

2007

H1

2007

H2

2008

H1

2008

H2

2009

H1

2009

H2

2010

H1

2010

H2

2011

H1

2011

H2

5,000

0

10,000

15,000

20,000

25,000

£ per hectare

Source:Defra/RICS

Figure4:AveragetransactedfarmlandpricesinEngland&Wales

Yearonyeargrowthofaveragefarmlandvalueshasoutpacedthatofequitiessincetheearlynoughties.

CHESTERTON HUMBERTS RESEARCH BRIEF 5

0

50

100

150

200

250

300

350

400

450

19951996

19971998

19992000

20012002

20032004

20052006

20072008

20092010

2011

England & Wales Residential

Farmland Values

10 Year Gilts

FTSE All-Share

Gold

Index: 1995=100

Source:LandRegistry,BoE,RICS

Figure5:GrowthinEngland&Walesfarmlandvaluesvsgrowthofselectedassets

Totalrealincomefromfarming(TIFF)hasbeenvolatileoverthepastfourdecadesbuttrendedupwardsduringthenoughtiesduringwhichperioditmorethandoubledinreal

terms.Overthepastdecadelivestockoutputhascontributedonaveragearound54%oftotalgrossfarmoutputcomparedtocropoutputwhichhasaveragedaround34.5%.

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

£million

Source:Defra

Figure6:TotalrealincomefromUKfarming(TIFF)

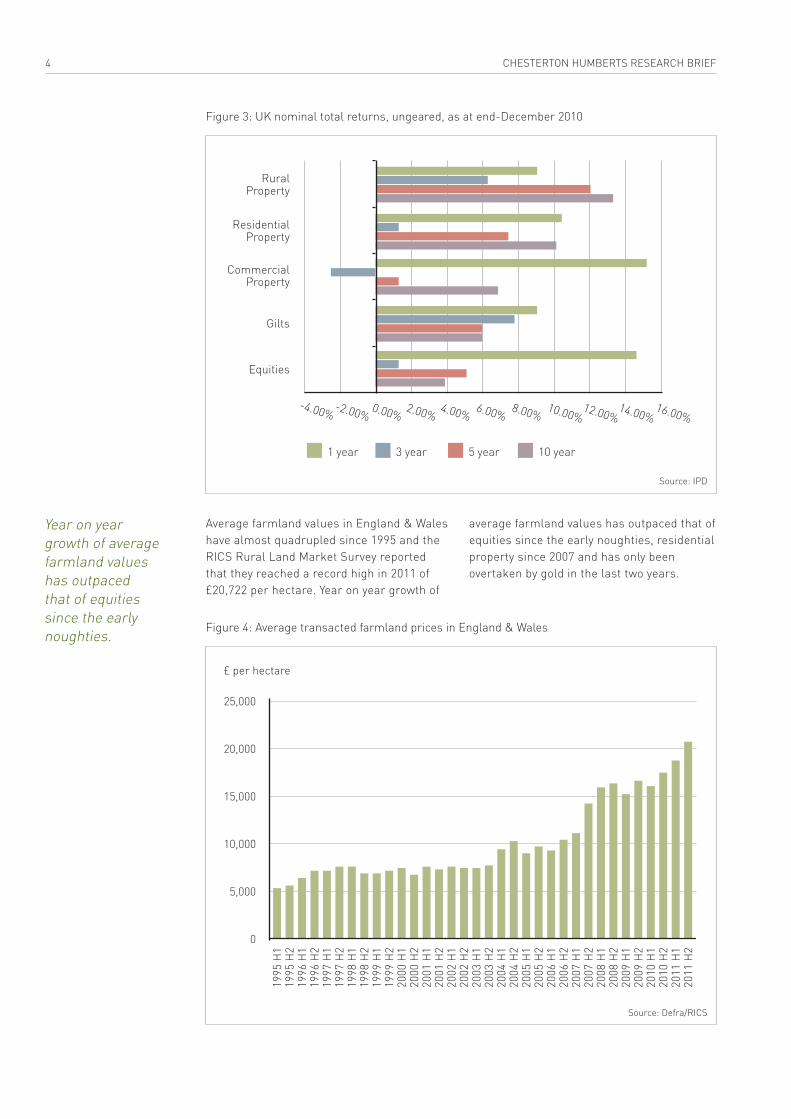

UKagriculturalincomegrowthoverthepastdecadecomparesfavourablywiththerestofEurope.AccordingtoECstatistics,estimated2011incomefromUKagriculturalactivitywasjustunder83%higherthanin

2000,whereasthecorrespondingfigurefortheEU27countrieswas24.5%andfortheEurozonecountriesincomein2011was4.2%lowerthanin2000.

CHESTERTON HUMBERTS RESEARCH BRIEF6

Index: 1995=100

2000 20112000 2002 2003 2004 2005 2006 2007 2008 2009 2010

155

145

135

125

115

105

95

85

75

EU (27 countries) EU area (16 countries) United Kingdom

Source:Eurostat

Figure7:Incomefromagriculturalactivity:UKvsEU27vsEurozone

Note:2011dataareestimates

Thetypeoftenancyagreementcansignificantlyaffectrentalincome.AveragerentsforfarmlandletundertheAgriculturalTenanciesAct1995arecurrentlyover1.75timeshigherthanthoseregulatedbytheAgriculturalHoldingsAct1986andhaverisenby36%forarablelandandby35%forpasturelandbetweenH12009andH22011,whilethecorrespondingincreasesforlandletundertheAgriculturalHoldingsAct1986aremuchlowerat12%and9%respectively.Furthermore,thegapbetweenrentsforfarmlandletundertheAgriculturalTenanciesAct1995comparedtotheAgriculturalHoldingsAct1986haswidenedbymorethan20%sinceH12009.

EfficiencyintheUKagriculturalsectorhasimprovedconsiderablyoverthepastfourdecadesthankstoadvancesintechnology,thegrowthoflarge-scalecapitalintensivefarmsrunbycorporateownersandtheimpactoffarmingpolicychanges,notablytheCommonAgriculturalPolicy(CAP).AccordingtodatafromDefra,totalfactorproductivityforthesectorincreasedby51%between1973and2010.

OUTLOOK

Anumberoffactorspointtoapositivelongtermoutlookfortheagriculturalsector.Increasingaffluenceandchangingpatternsofconsumptionarealreadyleadingtorisingpercapitademandforfoodandtheworld’spopulationcouldreach9.3billion(a35%increase)by2050accordingtoUNmedium

scenarioforecasts.Thiswillplaceincreasingimportanceonagriculturalresourcesandannualglobalconsumptionofwheatandcerealshasalreadyoutstrippedproductioninsixoutofthepast11yearswiththeshortfallhavingtobemadeupfromexistingstocks.

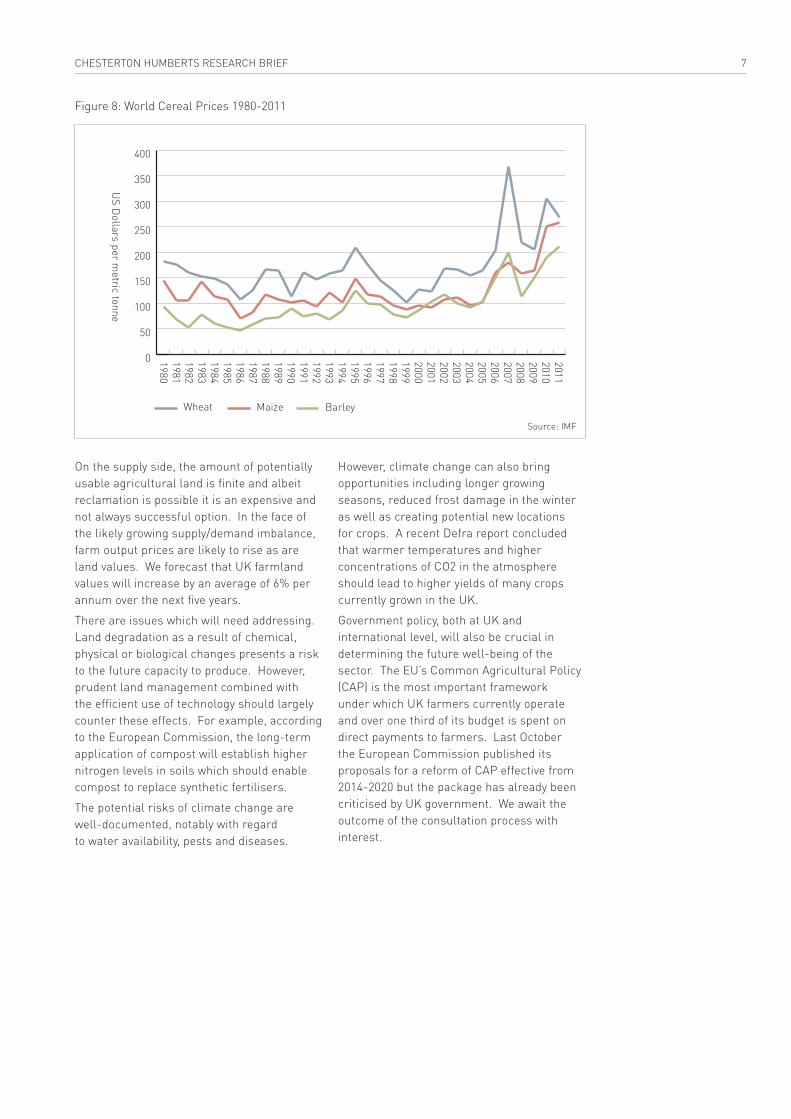

Althoughdisplayingafairdegreeofvolatilityoverthepastthreedecades,worldfoodpriceshavenonethelesstrendedupwardsoverthisperiodandin2011reachedrecordlevels.ThevalueofUKfoodexportshasalsorisenstronglyduringthenoughties(+83%),helpedbytherelativedeclineofSterlingagainstthemajorinternationalcurrenciessince2007.Itishighlylikelythatfoodpriceswillcontinuetotrendupwardsoverthelongertermgiventhemountingpressureonconsumptionfromtheexpandingglobalpopulation.

Technologyadvancesshouldresultinimprovedcropyieldstherebymakingfarmingmoreefficientandprofitableaswellasenablingthefurtherdevelopmentofusefulnon-foodcrops,rangingfromplasticstopharmaceuticalsandbio-fuels.

Theincreasingimportanceofthebio-fuelssectorcanbeseeninitsgrowingshareofUKcropoutputwhichtripledduringthenoughtiesfromaround3%in2000to9.1%in2010.ThereareseveralGovernmentschemesdesignedtopromotegreateruseofrenewableenergysourcesandthe2009RenewableEnergyDirectivehassetatargetofdelivering15%(comparedto3%in2009)oftheUK’senergyconsumptionfromrenewablesourcesby2020.

Technologyadvancesshouldresultinimprovedcropyieldstherebymakingfarmingmoreefficientandprofitableaswellasenablingthefurtherdevelopmentofusefulnon-foodcrops.

CHESTERTON HUMBERTS RESEARCH BRIEF 7

Onthesupplyside,theamountofpotentiallyusableagriculturallandisfiniteandalbeitreclamationispossibleitisanexpensiveandnotalwayssuccessfuloption.Inthefaceofthelikelygrowingsupply/demandimbalance,farmoutputpricesarelikelytoriseasarelandvalues.WeforecastthatUKfarmlandvalueswillincreasebyanaverageof6%perannumoverthenextfiveyears.

Thereareissueswhichwillneedaddressing.Landdegradationasaresultofchemical,physicalorbiologicalchangespresentsarisktothefuturecapacitytoproduce.However,prudentlandmanagementcombinedwiththeefficientuseoftechnologyshouldlargelycountertheseeffects.Forexample,accordingtotheEuropeanCommission,thelong-termapplicationofcompostwillestablishhighernitrogenlevelsinsoilswhichshouldenablecomposttoreplacesyntheticfertilisers.

Thepotentialrisksofclimatechangearewell-documented,notablywithregardtowateravailability,pestsanddiseases.

However,climatechangecanalsobringopportunitiesincludinglongergrowingseasons,reducedfrostdamageinthewinteraswellascreatingpotentialnewlocationsforcrops.ArecentDefrareportconcludedthatwarmertemperaturesandhigherconcentrationsofCO2intheatmosphereshouldleadtohigheryieldsofmanycropscurrentlygrownintheUK.

Governmentpolicy,bothatUKandinternationallevel,willalsobecrucialindeterminingthefuturewell-beingofthesector.TheEU’sCommonAgriculturalPolicy(CAP)isthemostimportantframeworkunderwhichUKfarmerscurrentlyoperateandoveronethirdofitsbudgetisspentondirectpaymentstofarmers.LastOctobertheEuropeanCommissionpublisheditsproposalsforareformofCAPeffectivefrom2014-2020butthepackagehasalreadybeencriticisedbyUKgovernment.Weawaittheoutcomeoftheconsultationprocesswithinterest.

US D

ollars per metric tonne

0

50

100

150

200

250

300

350

400

Wheat Maize Barley

19801981198219831984198519861987198819891990199119921993199419951996199719981999200020012002200320042005200620072008200920102011

Source: IMF

Figure8:WorldCerealPrices1980-2011

Thecontentsofthisreportareintendedforthepurposeofgeneralinformationandshouldnotberelieduponasthebasisfordecisiontakingonthepartofthereader.Althougheveryefforthasbeenmadetoensuretheaccuracyoftheinformationcontainedwithinthisreportatthetimeofwriting,noliabilityisacceptedbyChestertonGlobalforanylossordamageresultingfromitsuse.ReproductionofthisreportinwholeorinpartisnotpermittedwithoutthepriorwrittenapprovalofChestertonGlobal.March2012.

CONTACT

David HebditchHeadofRuralDivisionT:+44(0)1823348290E:[email protected]

Andrew PearceDirectorRuralLincolnT:+44(0)1522516830E:[email protected]

Neil GladwinDirectorRuralTauntonT:+44(0)1823348294E:[email protected]

David PardoeDirectorRuralSalisburyT:+44(0)1722342393E:[email protected]

Christopher JerramDirectorRuralChippenhamT:+44(0)1249444555E:[email protected]

Harry BainesDirectorRuralStamfordT:+44(0)1780758093E:[email protected]

Craig HortonDirectorRuralMarlboroughT:+44(0)1672519111E:[email protected]

Richard SavilleDirectorRuralPetersfieldT:+44(0)1730862043E:[email protected]

Nicholas BarnesHeadofResearchT:+44(0)2030408406E:[email protected]

ChestertonHumbertsisamulti-disciplinarypropertybusinesscoveringResidentialSales&Lettings,Estate/PropertyManagement,International,RuralandCommercialwith70officesworldwide.

ChestertonHumberts’RuralDivisionpridesitselfwiththeexpertisethatitsknowledgeableprofessionalRuralTeamshavegainedovermanyyearsexperienceintheruralpropertysector.ThecombinedspecialismsoftheTeamsrangefrominvolvementwithfarmers,landownersandestateownerstoensuingadviceandworkinestatemanagement,salesandacquisitions,professionalservices(includingvaluation),planningandequestrian.

ShouldyouhaveanyquestionsregardingthisreportorwishforanyotherinformationconcerningtheUKruralpropertymarketpleasedonothesitatetocontactanyofthenameslistedbelow.

Related Documents