Retirement Income 1 Overview & Benefit Options Presented by Jan Hawkins Senior Retirement Benefits Officer Spring 2015

Retirement Income 1 Overview & Benefit Options Presented by Jan Hawkins Senior Retirement Benefits Officer Spring 2015.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Retirement Income

1

Overview & Benefit Options

Presented by Jan HawkinsSenior Retirement Benefits Officer

Spring 2015

Retirement Income

2

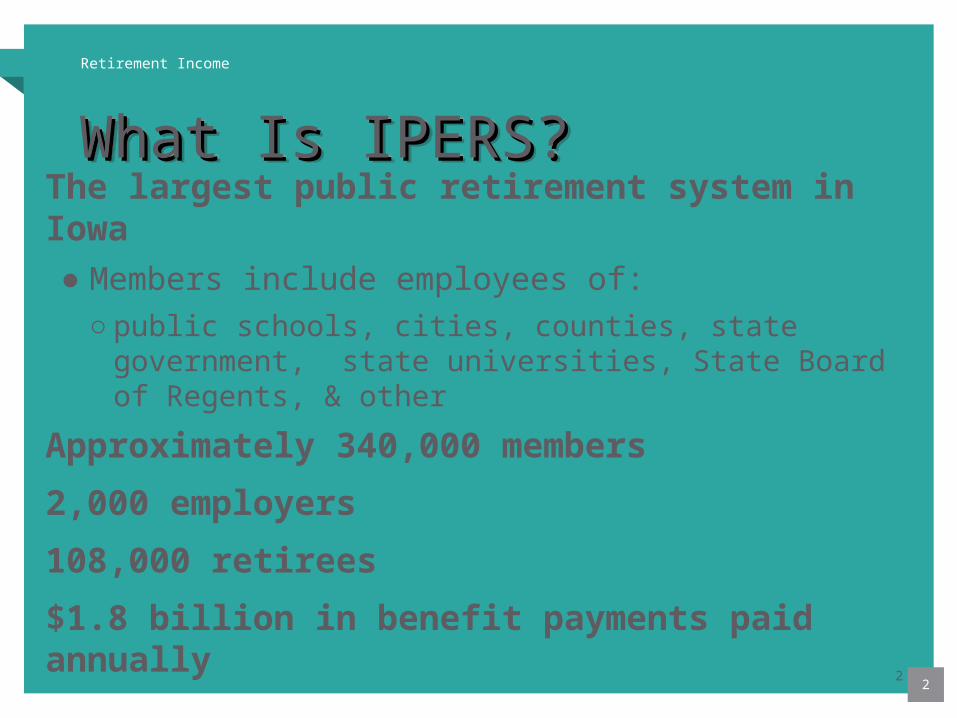

What Is IPERS?What Is IPERS?What Is IPERS?What Is IPERS?The largest public retirement system in Iowa● Members include employees of:

○ public schools, cities, counties, state government, state universities, State Board of Regents, & other

Approximately 340,000 members

2,000 employers

108,000 retirees

$1.8 billion in benefit payments paid annually

2

Retirement Income

3

What Is IPERS? What Is IPERS? What Is IPERS? What Is IPERS?

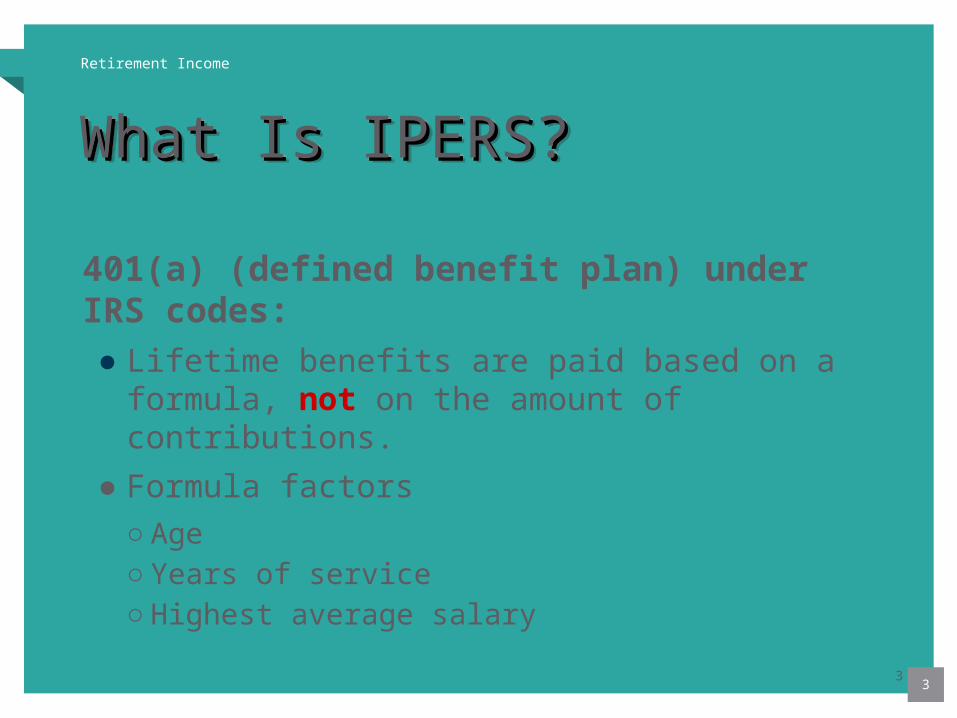

401(a) (defined benefit plan) under IRS codes: ● Lifetime benefits are paid based on a

formula, not on the amount of contributions.

● Formula factors ○ Age○ Years of service○ Highest average salary

3

Retirement Income

6

What’s My Part?What’s My Part?

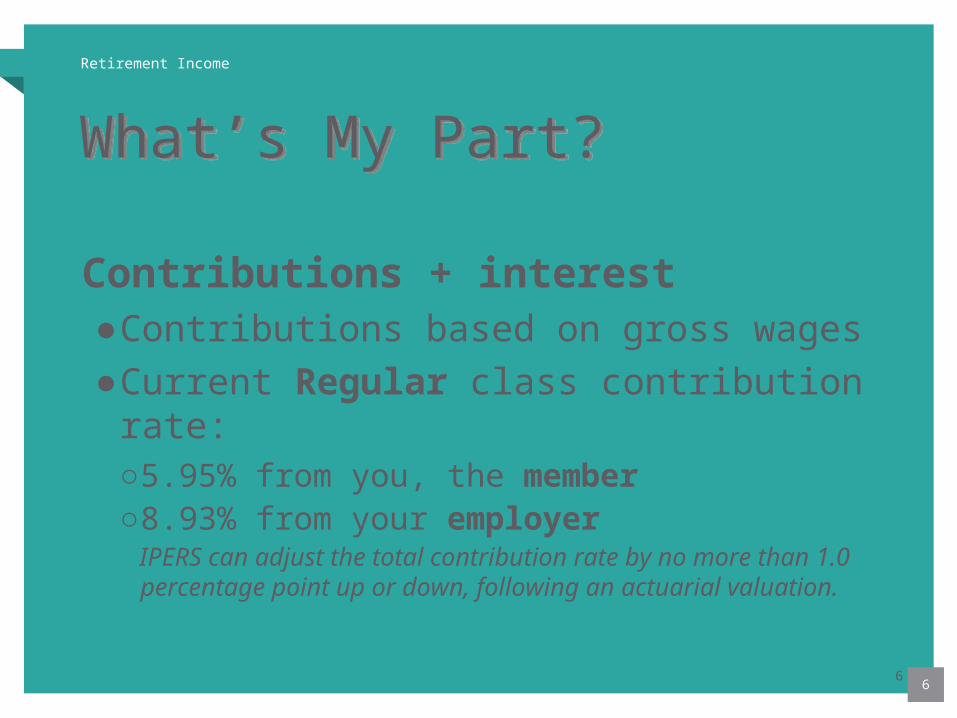

Contributions + interest●Contributions based on gross wages●Current Regular class contribution

rate:○5.95% from you, the member ○8.93% from your employer IPERS can adjust the total contribution rate by no more

than 1.0 percentage point up or down, following an actuarial valuation.

6

Retirement Income

8

What Is “Vesting”?What Is “Vesting”?Vested status is obtained after:

28 quarters (7 years) of reported wages,

or

When wages are reported in the same calendar year age 65 or older is attained

8

Retirement Income

9

VestingVestingEntitles the member to:

○Monthly retirement or disability benefit

○A portion of employer’s investment if refund is taken

andIs required for a service purchase

9

Retirement Income

11

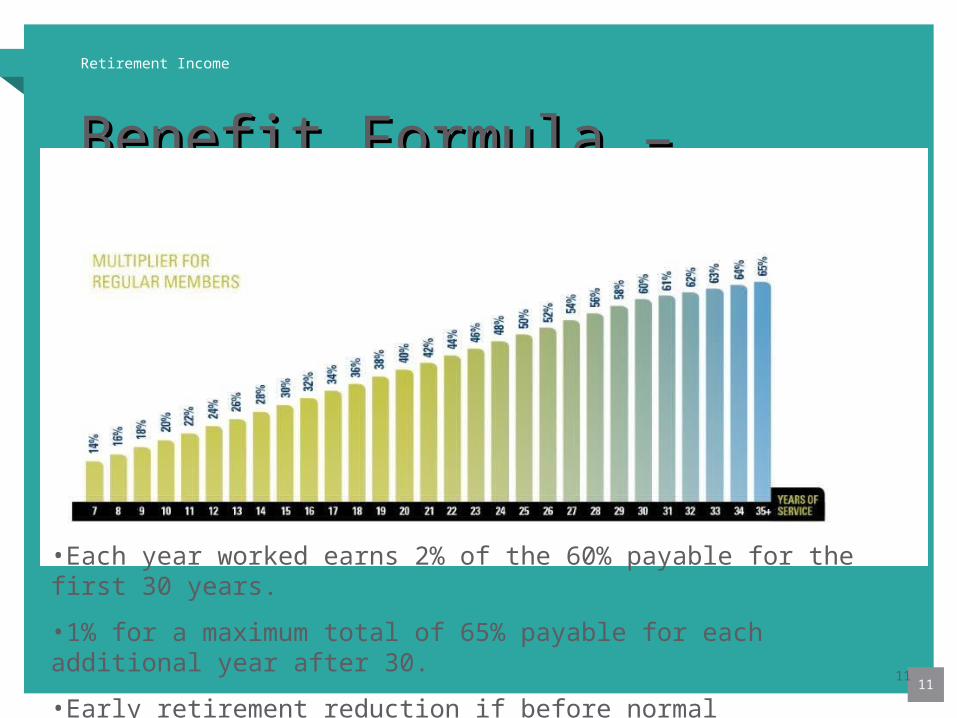

Benefit Formula – Years of Benefit Formula – Years of ServiceService

11

•Each year worked earns 2% of the 60% payable for the first 30 years.

•1% for a maximum total of 65% payable for each additional year after 30.

•Early retirement reduction if before normal retirement.

Retirement Income

12

Rule of 88

Rule of 62/20

Age 65

At least age 62 with 20 or more years of service

Age + Years of service = 88 or greater

Regardless of service

Normal Retirement Age (No Age Reduction)

Normal Retirement Age (No Age Reduction)

12

Retirement Income

13

Reduce 3% a year for portion of service through 06/30/12•From nearest normal retirement eligibility (rule of 88; rule of 62/20;age 65)

Reduce 6% a year thereafter•From age 65

As of July 1, 2012

Early Retirement Age Early Retirement Age ReductionReductionEarly Retirement Age Early Retirement Age ReductionReduction

13

Retirement Income

14

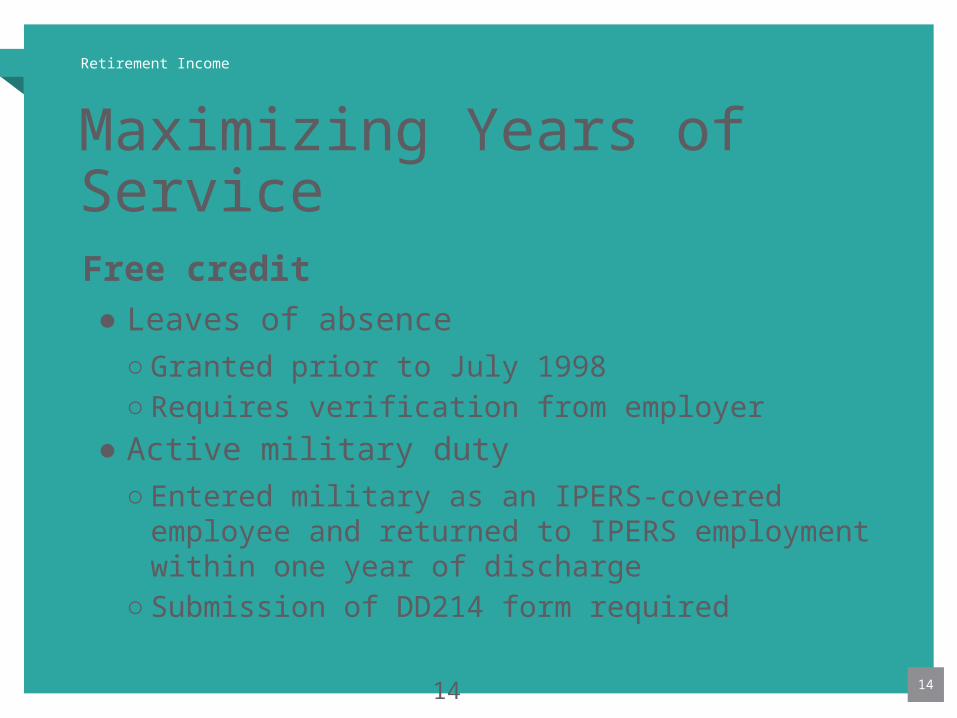

Maximizing Years of ServiceFree credit● Leaves of absence

○ Granted prior to July 1998○ Requires verification from employer

● Active military duty

○ Entered military as an IPERS-covered employee and returned to IPERS employment within one year of discharge

○ Submission of DD214 form required

14

Retirement Income

15

Beginning 01/01/16: Purchasing will take place only during the retirement process.•Increased accuracy of cost•Reduced risk of under- or overpaying

Request an official cost quote when you apply for retirement benefits.•Application for Service Purchase

Service PurchasesService PurchasesService PurchasesService Purchases

15

Retirement Income

16

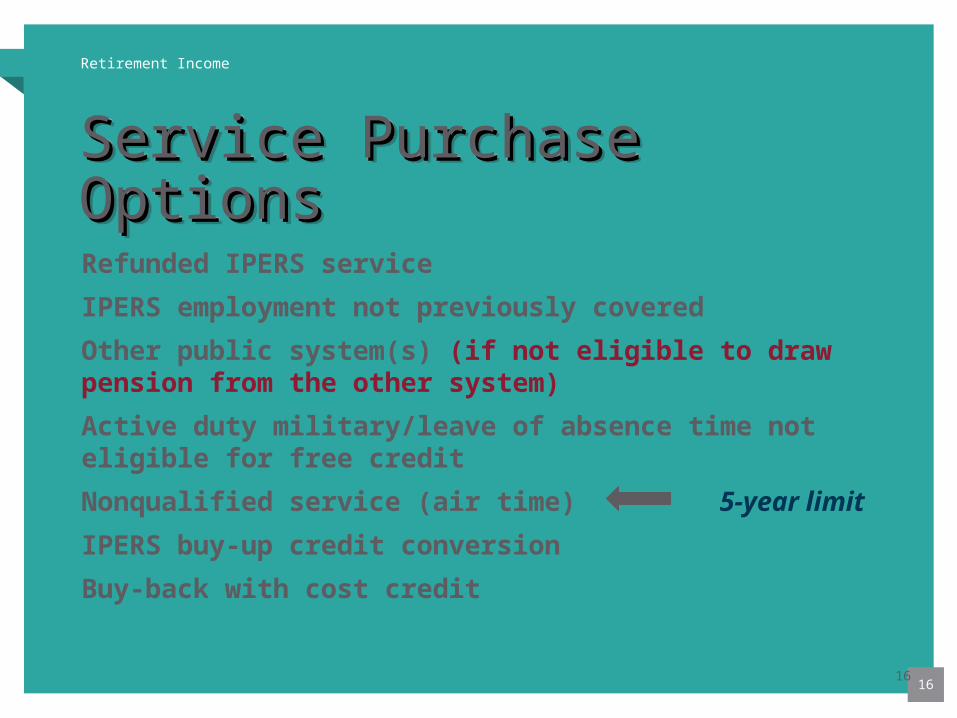

Service Purchase OptionsService Purchase OptionsService Purchase OptionsService Purchase Options

Refunded IPERS service

IPERS employment not previously covered

Other public system(s) (if not eligible to draw pension from the other system)

Active duty military/leave of absence time not eligible for free credit

Nonqualified service (air time) 5-year limit

IPERS buy-up credit conversion

Buy-back with cost credit

16

Retirement Income

17

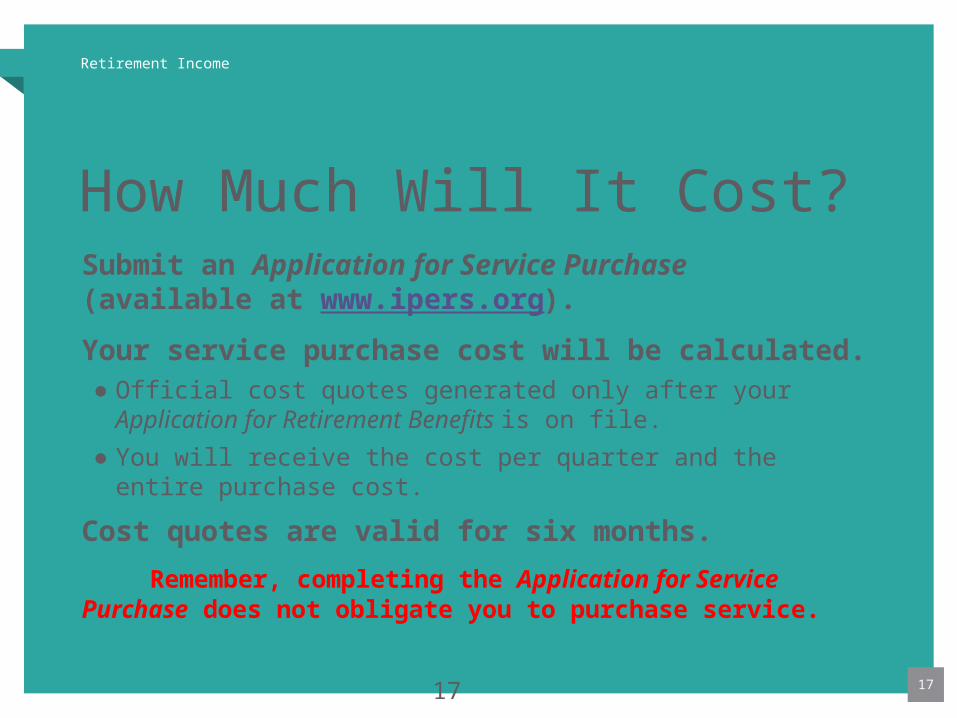

How Much Will It Cost?Submit an Application for Service Purchase (available at www.ipers.org).

Your service purchase cost will be calculated.● Official cost quotes generated only after your Application for

Retirement Benefits is on file.

● You will receive the cost per quarter and the entire purchase cost.

Cost quotes are valid for six months.

Remember, completing the Application for Service Purchase does not obligate you to purchase service.

17

Retirement Income

18

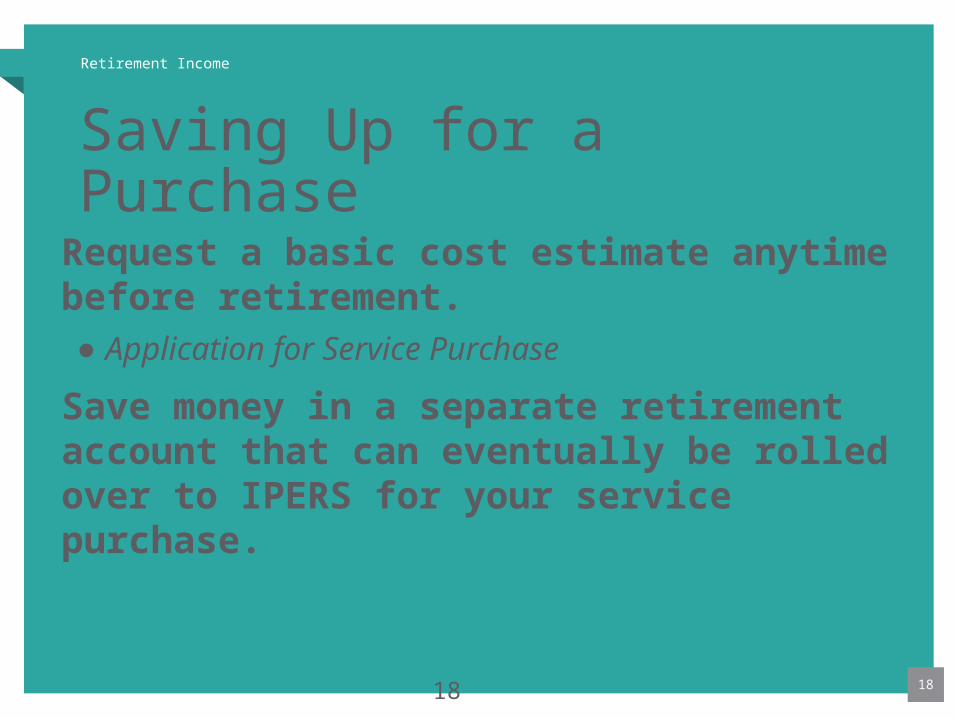

Saving Up for a PurchaseRequest a basic cost estimate anytime before retirement.● Application for Service Purchase

Save money in a separate retirement account that can eventually be rolled over to IPERS for your service purchase.

18

Retirement Income

20

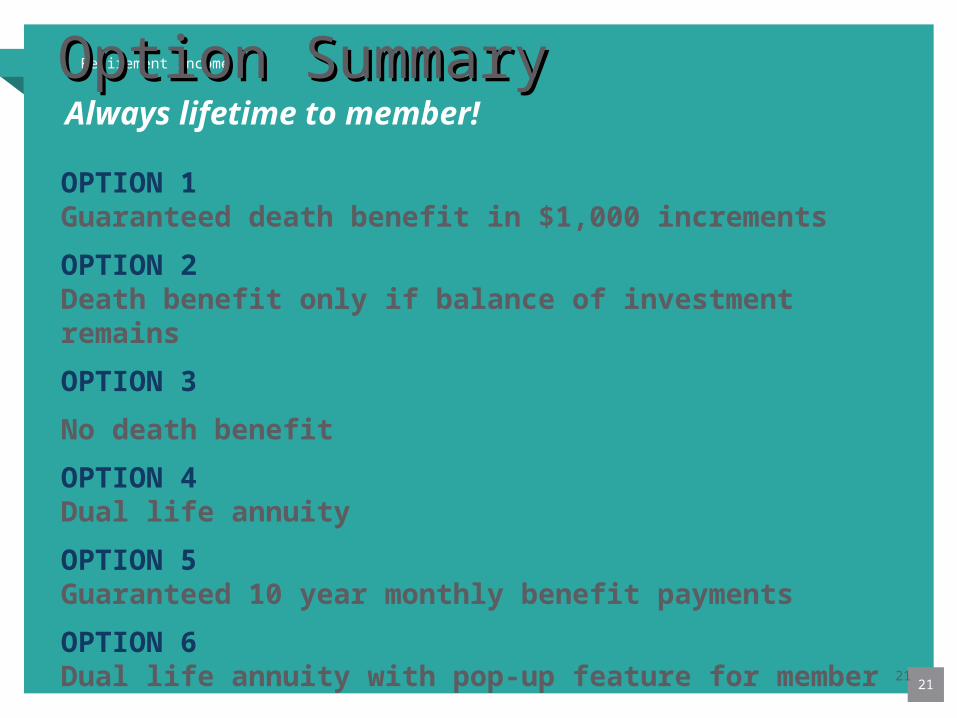

Monthly BenefitMonthly Benefit

Six monthly payment options ● Always lifetime to member

● Different death benefit provisions

IMPORTANT!

Option choice cannot be changed once benefits are paid.

20

Retirement Income

21

Option SummaryOption Summary

OPTION 1 Guaranteed death benefit in $1,000 increments

OPTION 2 Death benefit only if balance of investment remains

OPTION 3

No death benefit

OPTION 4 Dual life annuity

OPTION 5 Guaranteed 10 year monthly benefit payments

OPTION 6 Dual life annuity with pop-up feature for member

Always lifetime to member!

21

Retirement Income

22

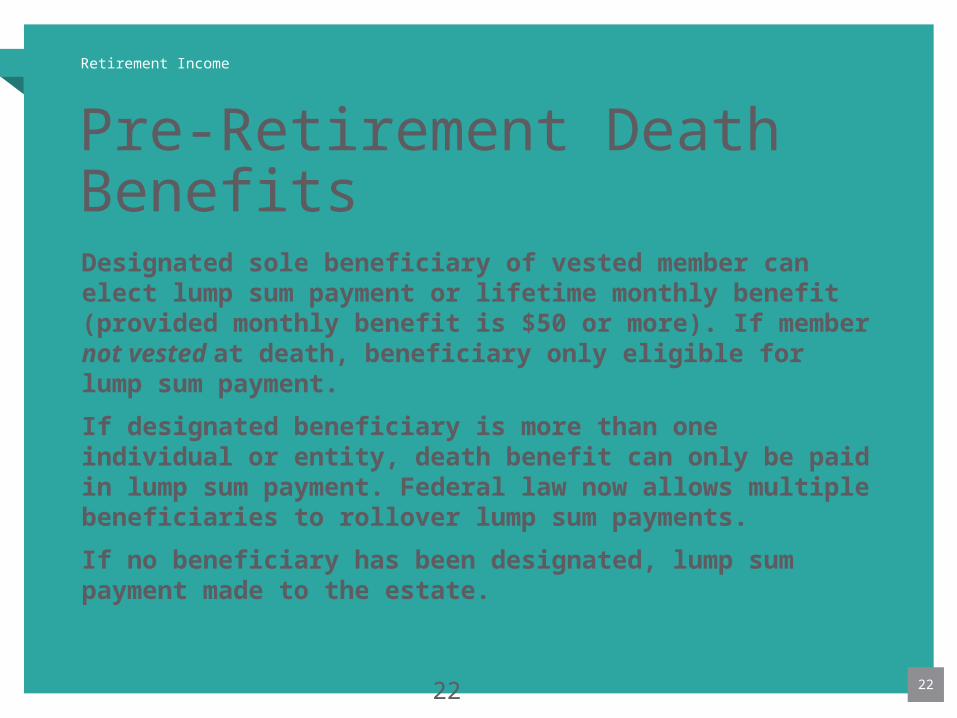

Pre-Retirement Death BenefitsDesignated sole beneficiary of vested member can elect lump sum payment or lifetime monthly benefit (provided monthly benefit is $50 or more). If member not vested at death, beneficiary only eligible for lump sum payment.

If designated beneficiary is more than one individual or entity, death benefit can only be paid in lump sum payment. Federal law now allows multiple beneficiaries to rollover lump sum payments.

If no beneficiary has been designated, lump sum payment made to the estate.

22

Retirement Income

23

Important Facts to Remember!Important Facts to Remember!

Working any time in a month makes you ineligible for benefits that month.

You can get a paycheck in the same month you start IPERS payments.

23

Retirement Income

24

Getting Monthly Benefits StartedGetting Monthly Benefits Started

Must terminate employment unless age 70

Must be age 55 or older● Unless vested and eligible for IPERS disability

benefits, first month of entitlement is month following the month you terminate employment

Must submit completed application

Benefits paid the last business day of month

24

Retirement Income

25

TaxesTaxesBenefit payments are subject to federal and state income tax ● You can request that the tax can be withheld

from monthly benefit payment

1099R mailed each January

For detailed tax information, contact the IRS for publication 575 or consult a tax advisor

25

Retirement Income

26

ReemploymentMust have a bona fide retirement.

It’s your responsibility to contact IPERS if you are returning to an IPERS-covered position.● It’s possible that returning to an IPERS-covered position

will affect your benefit.

Know the Social Security earning limits

26

Retirement Income

27

Bona Fide RetirementTo qualify for a bona fide retirement, you must:

End all service with covered employers, including non-covered service.

File an IPERS benefit application.

Stay out of all employment with a covered employer for one month.

Stay out of all employment in an IPERS-covered position for an additional three months.

27

Retirement Income

28

Reemployment GuidelinesApplies to IPERS-covered employment only

$30,000 earnings limit under age 65 (benefits reduced 50 cents for each dollar earned over the limit)

No earnings limit after age 65

Benefits recomputed upon termination

28

Retirement Income

30

When to Contact IPERSWhen to Contact IPERS

3–5 years from possible retirement for estimates

5–6 months from retirement to obtain application packet

At termination, if before age 55 for additional options

If a disability occurs

30

Retirement Income

31

The purpose of this presentation is to give you a brief overview of IPERS and upcoming law changes.

For detailed information on your account:

Call toll free 1-800-622-3849 or locally at 515-281-0020 Phones are answered by Retirement Benefit Officers from 7:30 am to 5:00 pm Monday through Friday, excluding holidays.

Website: www.ipers.org

• E-mail requests: [email protected]

• Retirement calculators

• Handbook

• Newsletters

• Other important information

Contact us:Contact us:

31

Retirement Income

32

Thank You!

Presented by Jan HawkinsSenior Retirement Benefits Officer

Neither Nationwide® nor any of its representatives give legal or tax advice.

Information provided by Retirement Specialists is for educational purposes only and is not intended as investment advice.

Nationwide Retirement Solutions, Inc. and Nationwide Life Insurance Company (collectively "Nationwide") have endorsement relationships with the National Association of Counties and the International Association of Firefighters-Financial Corporation. More information about the endorsement relationships may be found online at www.nrsforu.com.

Nationwide Retirement Solutions, Inc. and its affiliates (Nationwide) offer a variety of investment options to public sector retirement plans through variable annuity contracts, trust or custodial accounts. Nationwide may receive payments from mutual funds or their affiliates in connection with those investment options. For more detail about the payments Nationwide receives, please visit www.nrsforu.com.

Retirement Specialists are registered representatives of Nationwide Investment Services Corporation, member FINRA. In MI only: Nationwide Investment Svcs. Corporation.

Nationwide, the Nationwide framemark, and On Your Side are service marks of Nationwide Mutual Insurance Company.

©2012 Nationwide Retirement Solutions Inc. All rights reserved.

NRM-6817AO.4 (12/12)

Retirement Income

Retirement Income

35

Retirement Income

36

Retirement Income

37

*Retirement Savings Rule of Thumb, www.debt.org/retirement/how-much-do-i-need-to-save/, accessed Dec. 3, 2012

Retirement Income

38

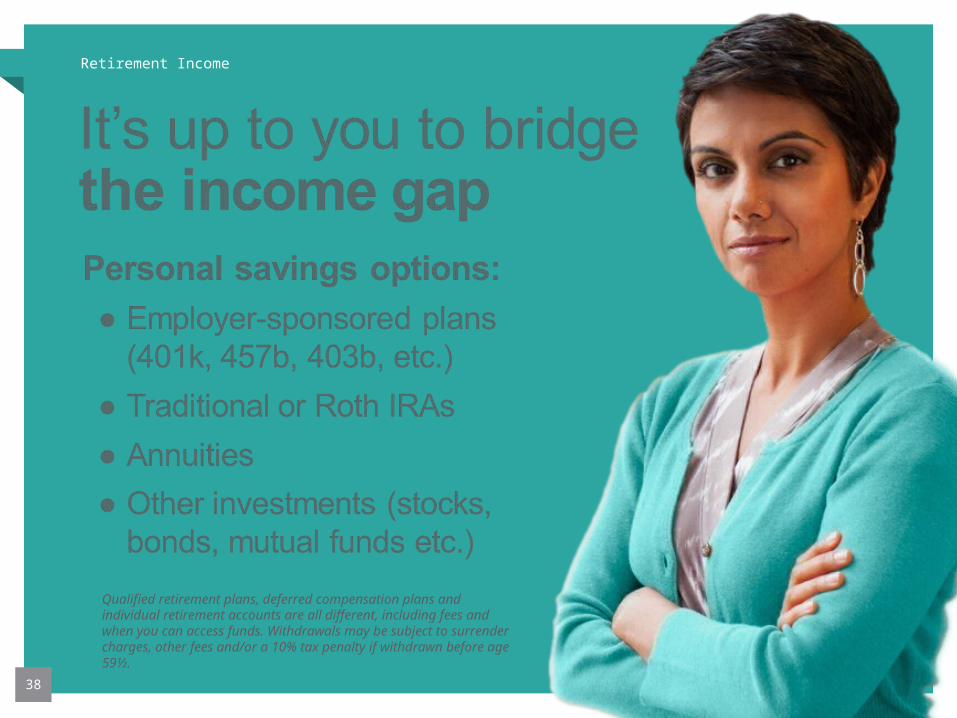

Qualified retirement plans, deferred compensation plans and individual retirement accounts are all different, including fees and when you can access funds. Withdrawals may be subject to surrender charges, other fees and/or a 10% tax penalty if withdrawn before age 59½.

Retirement Income

39

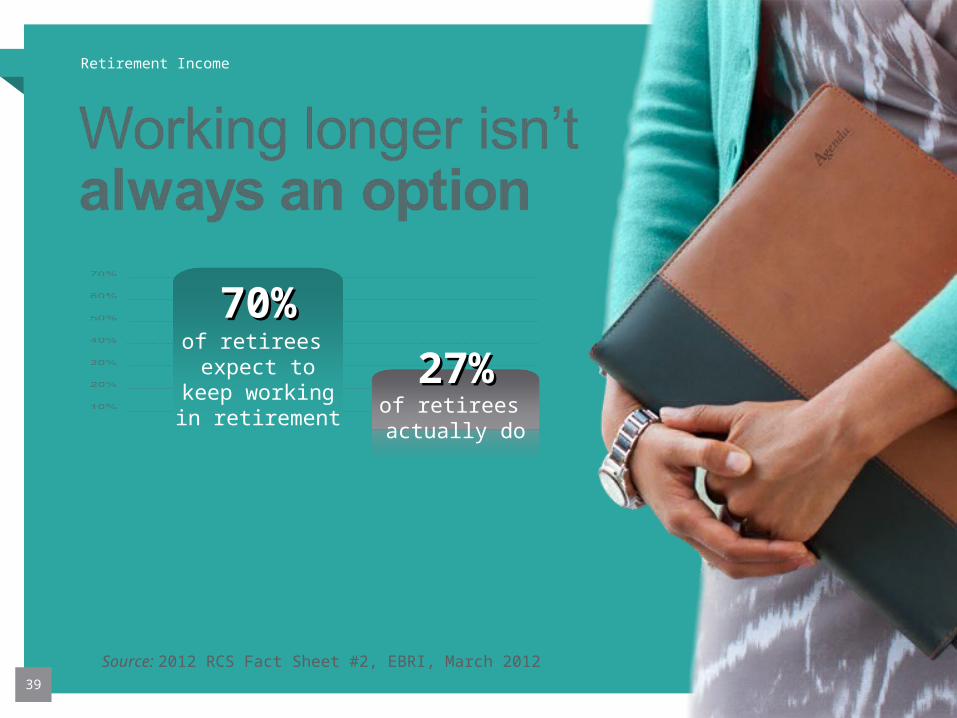

Source: 2012 RCS Fact Sheet #2, EBRI, March 2012

27%27%of retirees actually do

70%70%of retirees

expect to keep working in retirement

Related Documents