Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

• Retailing in India is one of the pillars of its economy and accounts for 14 to 15% of its GDP.

• The Indian retail market is estimated to be US $500 billion and one of the top five retail markets in the world by economic value.

• In 2010 larger format convenience stores and supermarkets accounted for about 4% of the industry.

• Until 2011, Indian Central Government denied FDI in multi brand retail but later announced reforms in November which paved way for retail innovation and competition with multi-brand retailers such as Walmart, Tesco, Carrefour etc.

• As of 2013, India’s retailing industry was essentially owner manned small shops.

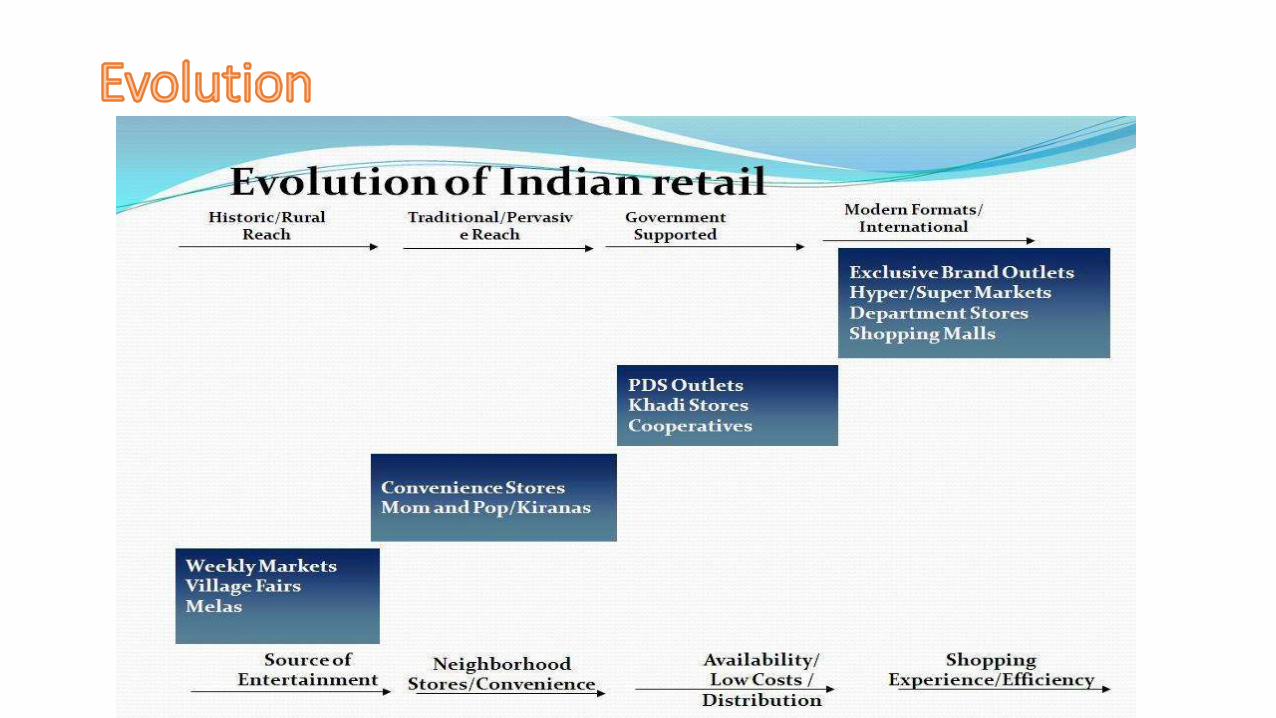

Unorganized Retail Sector:-

• Indian retail is dominated by large number of small retailers consisting of local kirana shops, owner manned general stores, chemists, footwear shops, paan and beedi shops, hand cart hawkers which together make up the so called “unorganized retail”.

• Unorganized retailers normally do not pay taxes and most of them are not even registered for sales tax, VAT or income tax.

Organized Retail Sector:-

• Organized retailing refers to trading activities undertaken by licensed retailers, that is, those who are registered for sales taxes, income taxes, etc.

• These include corporate backed hyper markets and retail chains and also the privately owned large retail business.

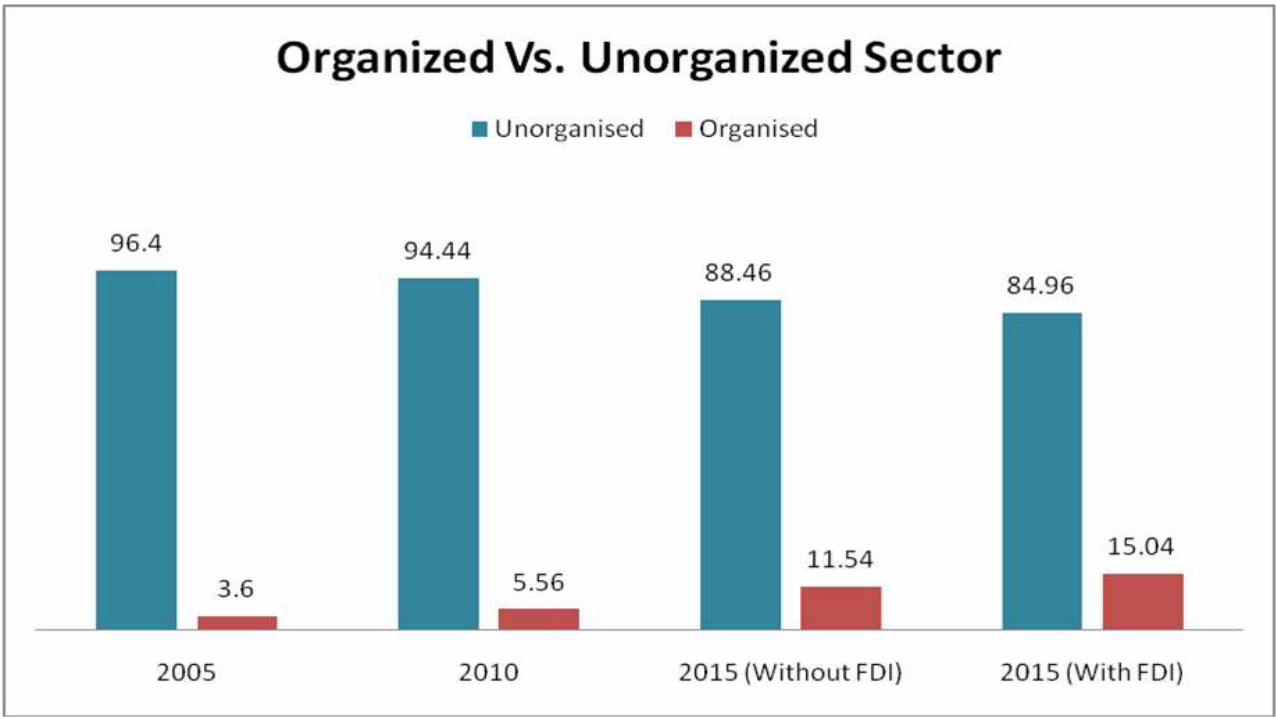

• Organized retail accounts for 7% of India’s roughly US $435 billion retail market and is expected to reach 20% by 2020.

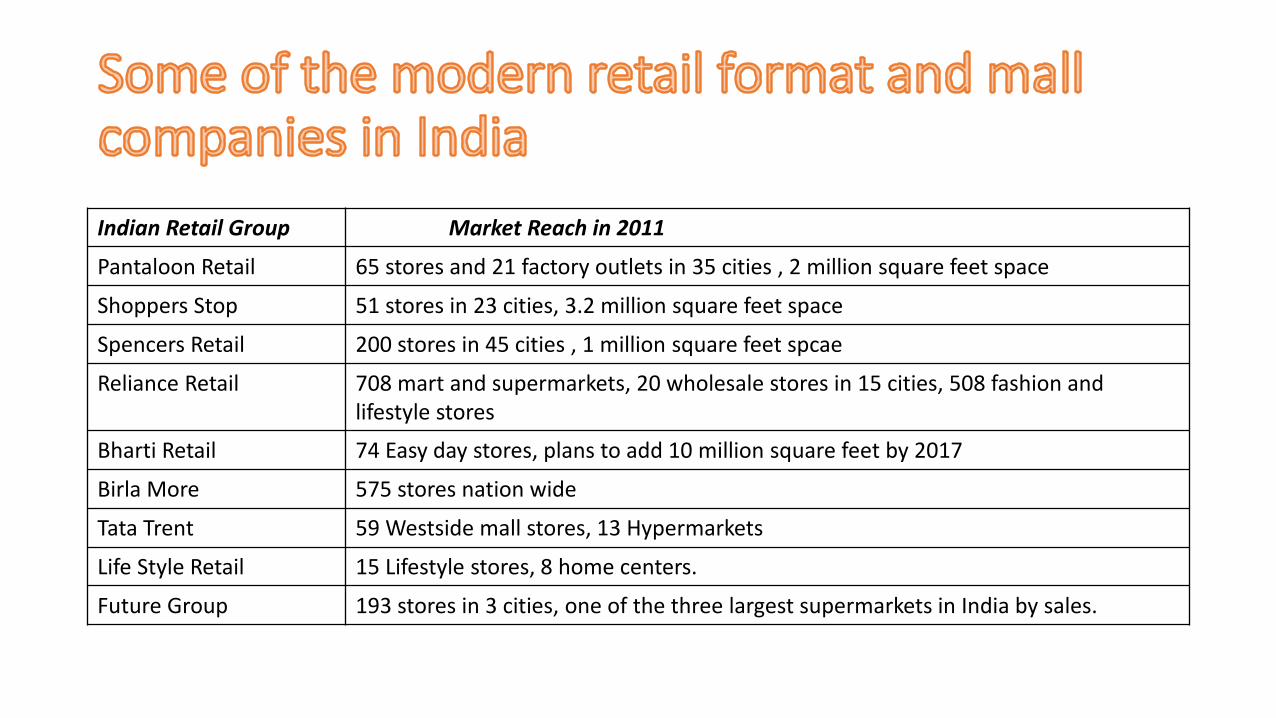

Indian Retail Group Market Reach in 2011

Pantaloon Retail 65 stores and 21 factory outlets in 35 cities , 2 million square feet space

Shoppers Stop 51 stores in 23 cities, 3.2 million square feet space

Spencers Retail 200 stores in 45 cities , 1 million square feet spcae

Reliance Retail 708 mart and supermarkets, 20 wholesale stores in 15 cities, 508 fashion and lifestyle stores

Bharti Retail 74 Easy day stores, plans to add 10 million square feet by 2017

Birla More 575 stores nation wide

Tata Trent 59 Westside mall stores, 13 Hypermarkets

Life Style Retail 15 Lifestyle stores, 8 home centers.

Future Group 193 stores in 3 cities, one of the three largest supermarkets in India by sales.

• The recent proposal of FDI in retail would positively impact the development across the commercial real estate.

• Many retailers are cash strapped and the proposed FDI will provide a bail out for them.

• With the flow of fresh investment into the retail sector, it will trigger investment in real estate both at front end and back end. In front end, retail stores spaces will see investments and in the back end, better quality warehouses could be seen.

• Apartments in residential areas with malls and supermarkets in the vicinity definitely command a higher rate per square foot, due to shopping comfort and convenience.

FDI in multi brand retail:-

• 30% of procurement of manufactured products must be from SMEs

• Minimum investment capital is USD 100 million.

• Minimum of 50% of FDI must be invested in backend infrastructure.

• 50% of the jobs in retail outlet could be reserved for rural youth and a certain amount of farm produce could be required to be procured from farmers.

• Multi brand retail would keep food and commodity prices under control.

FDI in single brand retail:-

• Products to be sold under the same brand internationally.

• Sale of multi branded goods is not allowed, even if procured by the same manufacturer.

• For FDI above 51%, 30% sourcing must be from SMEs

• Consumerism of retail market, any additional product categories to be sold under single brand retail must first receive additional government approval.

• Rising disposable income of Indian middle class.

• Changing consumer preferences and shopping habits.

• Changing Demographics.

• Increase in working population.

• Spurt in urbanization.

• Internet drives awareness and online purchases.

• Easy credit availability a boon for organized retail.

• India’s retailing industry mainly consists of the local mom and pop store, owner manned shops and street vendors.

• Organized retail supermarkets are growing but small, with a market share of 4% as of 2008.

• In 2012 government permitted 51% FDI in multi-brand retail and 100% FDI in single brand retail.

• However a lack of back end warehouse retail infrastructure, as well as state level permits and red tape continues to limit organized retail’s growth in Indian Economy.

• Over 30 regulations such as “signboard licenses” and “anti hoarding measures” have to be complied before a store can open its doors.

• There are taxes for moving goods from state to state and within state.

• Both multi brand and single brand stores in India will have to source nearly a third of their goods from small and medium sized Indian suppliers.

• All multi brand and single brand stores in India must confine their operations to 53 odd cities with a population over one million, out of 7935 towns and cities in India. It is expected that these stores will have full access to over 200 million urban consumers in India.

• Multi brand retailers must have a minimum investment of US$100 million with atleast half the amount to be invested in back end infrastructure, including cold chains, refrigeration, transportation, sorting, packaging and processing to considerably reduce the post harvest loss and to bring remunerative prices to farmers.

Related Documents