1 ISSN 0734–242X Waste Management & Research 2009: 00: 1–13 DOI: 10.1177/0734242X09341073 Los Angeles, London, New Delhi and Singapore http://www.sagepub.com © The Author(s), 2009. Reprints and permissions: http://www.sagepub.co.uk/journalsPermissions.nav Resource recovery from end-of-life tyres in Greece: a field survey, state-of-art and trends A. Karagiannidis, T. Kasampalis Laboratory of Heat Transfer and Environmental Engineering, Department of Mechanical Engineering, Aristotle University of Thessaloniki, Greece Lack of consistent and available information for the entire tyre industry has often hindered adequate understanding of current and future issues that need to be addressed for improving the sustainable end-of-life tyre management. The aim of this paper is to review related best available technologies and techniques for Greece, ranging from simple mechanical processing, up to complex multistep, mechanochemical and/or thermal treatment. End-of-life tyre management guidelines in the form of a manual for supporting future entrepreneurs in this field are also discussed. Extensive data mining, classification and inven- torying was performed, both in the field via questionnaires and in the literature, for the purpose of accurately determining Hellenic conditions, in order to pinpoint encountered problems, propose interventions and determine new entrepreneurship opportunities. Keywords: Hellenic end-of-life tyre management, best available technologies, entrepreneurship, market research Introduction The tyre is a complex and high-technology safety product representing a century of manufacturing innovation, which is still on-going. The tyre comprises many materials out of the very best that the metallurgical, textile and chemical indus- tries can produce. There is no room for even the slightest defect and it is an extremely complex process to develop and manufacture the product. From a materials’ point of view, the tyre is a mixture of synthetic and natural rubber, to which a range of specific substances are added to ensure perform- ance, durability and safety. These include mineral oil, reinforc- ing fillers (carbon black and silica) and vulcanising agents (sul- phur) which act as catalysts to accelerate the vulcanisation process. The technologies utilised to recycle these materials range from the simplest mechanical devices that compress (or cut) to sophisticated and complex multistep mechanochemical and/or thermal treatment set ups. Many of the technologies are flexible and adaptable to different environments (U.S. EPA 2005). The capabilities of many of the individual technol- ogies described can be expanded by linking two or more differ- ent types of systems together to operate in tandem in order to produce a desired product. The most commonly used sys- tems begin with simple mechanical equipment designed to destroy the structure of the tyre. A second level of treatment can be added for further size reduction and to liberate and separate the material components, i.e. the rubber, metal and fluff (Blumenthal 2003). However, the most significant tech- nical disadvantage of a tyre is the three dimensional net- work of sulphur polymer molecules in its chemical struc- ture, which is created by the thermodynamically irreversible reaction of sulphur and rubber molecules, called vulcanisa- tion. The problem is that, after the rubber has used up its useful life, it is difficult to remove the sulphur bonds and de- vulcanise the rubber compound in order to produce a valua- ble recycled material. The tyre is probably one of the best engineered, longest lasting products developed by man. It is designed for per- formance, aesthetics, comfort, control and safety. Scrap tyres are a valuable and viable national resource; the challenge today is to find the best way to utilise them in a wide range of applications. The following work presents the results of a nation-wide field survey conducted in Greece in 2007, aimed to providing a comprehensive inventory with current prac- tices and to facilitate the development of future entrepre- neurship in this field. Corresponding author: Avraam Karagiannidis, Laboratory of Heat Transfer and Environmental Engineering, Department of Mechanical Engineer- ing, Aristotle University Thessaloniki, Box 483, GR-54124 Thessaloniki, Greece. E-mail: [email protected] Received 28 July 2008, accepted in revised form 27 May 2009 Figures 3, 4 appear in color online: http://wmr.sagepub.com Waste Manag Res OnlineFirst, published on September 11, 2009 as doi:10.1177/0734242X09341073

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

ISSN 0734–242XWaste Management & Research

2009: 00: 1–13DOI: 10.1177/0734242X09341073

Los Angeles, London, New Delhi and Singaporehttp://www.sagepub.com © The Author(s), 2009. Reprints and permissions:

http://www.sagepub.co.uk/journalsPermissions.nav

Resource recovery from end-of-life tyres in Greece: a field survey, state-of-art and trendsA. Karagiannidis, T. KasampalisLaboratory of Heat Transfer and Environmental Engineering, Department of Mechanical Engineering, Aristotle University of Thessaloniki, Greece

Lack of consistent and available information for the entire tyre industry has often hindered adequate understanding of currentand future issues that need to be addressed for improving the sustainable end-of-life tyre management. The aim of this paperis to review related best available technologies and techniques for Greece, ranging from simple mechanical processing, up tocomplex multistep, mechanochemical and/or thermal treatment. End-of-life tyre management guidelines in the form of amanual for supporting future entrepreneurs in this field are also discussed. Extensive data mining, classification and inven-torying was performed, both in the field via questionnaires and in the literature, for the purpose of accurately determiningHellenic conditions, in order to pinpoint encountered problems, propose interventions and determine new entrepreneurshipopportunities.

Keywords: Hellenic end-of-life tyre management, best available technologies, entrepreneurship, market research

IntroductionThe tyre is a complex and high-technology safety productrepresenting a century of manufacturing innovation, which isstill on-going. The tyre comprises many materials out of thevery best that the metallurgical, textile and chemical indus-tries can produce. There is no room for even the slightestdefect and it is an extremely complex process to develop andmanufacture the product. From a materials’ point of view,the tyre is a mixture of synthetic and natural rubber, to whicha range of specific substances are added to ensure perform-ance, durability and safety. These include mineral oil, reinforc-ing fillers (carbon black and silica) and vulcanising agents (sul-phur) which act as catalysts to accelerate the vulcanisationprocess.

The technologies utilised to recycle these materials rangefrom the simplest mechanical devices that compress (orcut) to sophisticated and complex multistep mechanochemicaland/or thermal treatment set ups. Many of the technologiesare flexible and adaptable to different environments (U.S.EPA 2005). The capabilities of many of the individual technol-ogies described can be expanded by linking two or more differ-ent types of systems together to operate in tandem in order toproduce a desired product. The most commonly used sys-tems begin with simple mechanical equipment designed to

destroy the structure of the tyre. A second level of treatmentcan be added for further size reduction and to liberate andseparate the material components, i.e. the rubber, metal andfluff (Blumenthal 2003). However, the most significant tech-nical disadvantage of a tyre is the three dimensional net-work of sulphur polymer molecules in its chemical struc-ture, which is created by the thermodynamically irreversiblereaction of sulphur and rubber molecules, called vulcanisa-tion. The problem is that, after the rubber has used up itsuseful life, it is difficult to remove the sulphur bonds and de-vulcanise the rubber compound in order to produce a valua-ble recycled material.

The tyre is probably one of the best engineered, longestlasting products developed by man. It is designed for per-formance, aesthetics, comfort, control and safety. Scrap tyresare a valuable and viable national resource; the challengetoday is to find the best way to utilise them in a wide range ofapplications. The following work presents the results of anation-wide field survey conducted in Greece in 2007, aimedto providing a comprehensive inventory with current prac-tices and to facilitate the development of future entrepre-neurship in this field.

Corresponding author: Avraam Karagiannidis, Laboratory of Heat Transfer and Environmental Engineering, Department of Mechanical Engineer-ing, Aristotle University Thessaloniki, Box 483, GR-54124 Thessaloniki, Greece. E-mail: [email protected] 28 July 2008, accepted in revised form 27 May 2009Figures 3, 4 appear in color online: http://wmr.sagepub.com

Waste Manag Res OnlineFirst, published on September 11, 2009 as doi:10.1177/0734242X09341073

A. Karagiannidis, T. Kasampalis

2

End-of-life-tyre management systems in europeEvery year about 3.2 million tonnes of used tyres (eitherpartly worn or end-of-life tyres) are generated in Europe (seeTable 2), out of which 2.5 million tonnes are end-of-life tyresfor which value recovery has to be maximized. Tyres comingfrom end-of-life passenger cars represent around 10% of thisamount (ETRMA 2008). EU Member States have to be com-pliant with the EU legislation in transposing the Directivesinto local legislation but are also free to set their own nationalinitiatives in order to reach the obligatory EU targets. Regard-ing the development of waste management policies at thenational level, the landfill-of-waste Directive (1999/31/EC) hasbeen a major driver during the past decade. Tyre manufactur-ers are also facing growing environmental pressure from thegeneral public and other stakeholders concerning illegaldumping and historic stockpiles (ETRMA 2008). For all thesereasons, it is in the interest of the tyre industry to continuebeing pro-active and take responsibility collectively for end-of-life tyres treatment.

By June 2008, three different systems were reported withinthe EU for funding end-of-life–tyre management, namely Pro-

ducer Responsibility (PR), tax system and free-market sys-tem (Table 1). The PR scheme, implemented mostly in theform of collective alternative management systems, putsstrong emphasis on the active role that the European tyreindustry can play in the prevention of waste and the promotionof recycling, from the design stages of a tyre up to its ultimateproduction and final treatment. EU countries that have notimplemented the PR scheme currently operate either undernational monopoly or a market-based approach. The firstmethod is under a tax system (where governments are respon-sible for the recovery and recycling of end-of-life tyres whichare thus financed by taxes), while the second method is undera free market system (also including individual PR, schemesand initiatives), where all the operators in the recovery chaincontract under free market conditions and act in compliancewith legislation, which sets the objectives to be met.

It is noteworthy that, since 1992, the trends of the differ-ent recycling and recovery options have significantly evolvedup to 2006 (Table 2), namely: (i) material recycling consider-ably expanded its share from 5% to over 34%; (ii) energyrecovery has increased from 14% to over 31.6%; and (iii)retreading has remained at around 12%. The overall EUrecovery rate also rose in 2006 from 32 to 87% (Table 2).

Many EU countries, such as Austria, Denmark, The Neth-erlands, Germany, France and Sweden are not landfillingtyres any longer. The 2006 recovery rate in Greece was 92%,in Italy 94%, in the UK 93%, whereas in Spain and Irelandthis reached 46% and 18% respectively. It should also benoticed that the most of the 12 new EU members have lowerend-of-life tyre-arisings, with exceptions from Poland, CzechRepublic, Romania and Hungary.

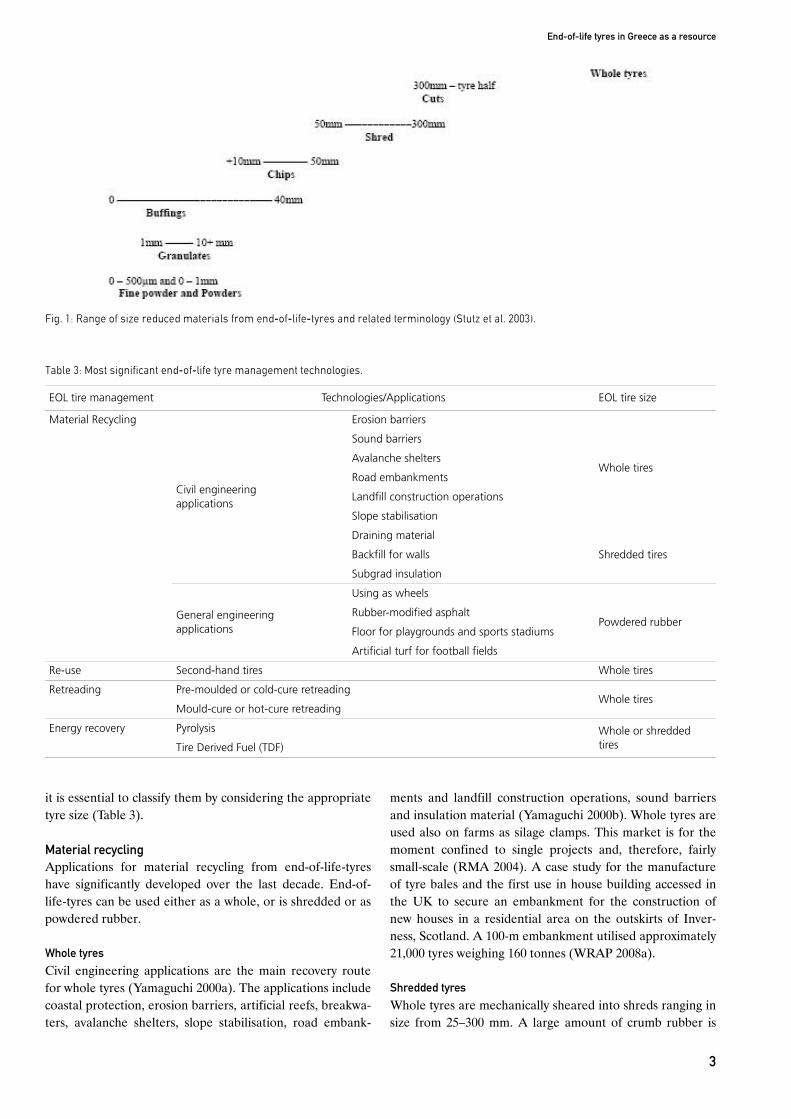

Currently applied technologiesEach material category is comprised of one or more sub-cat-egories (Stutz et al. 2003). Together, the categories and sub-categories create a continuum of size-reduced material from0.01 mm to > 300 mm in size. Each sub-category is presentedas a range as illustrated in Figure 1. The overlap reflects theparticle distribution within the defined size.

Material recycling, re-use, retreading and energy recoveryof end-of-life tyres has become a key challenge facing manycentral and local governments around the world. Therefore,

Table 1: Country-specific implementation of the three main end-of-life management models; the initiation year of specific national systems is also included, when known (ETRMA 2008).

Free market system

PRTax

SystemPreparing

for PR

Spain (2006) √

Portugal (2002) √

France (2004) √

Italy (2007) √

Greece (2005) √

Turkey (2006) √

Cyprus √

UK √

Norway (1995) √

Sweden (1995) √

Finland (1995) √

Germany √

Belgium (2004) √

Netherlands (2003) √

Switzerland √

Austria √

Slovenia √

Croatia √

Denmark √

Slovakia √

Romania (2005) √

Hungary (2006) √

Czech Republic √

Poland (2002) √

Lithuania √

Estonia √

Table 2: End-of-life tyres arising and management in EU-27 in 2006 (ETRMA 2008).

2006 kt %

Arisings 3,238 100

Reuse 110 3.4

Export 185 5.7

Retreading 380 11.7

Material recycling 1,105 34.1

Energy recovery 1,023 31.6

Landfill & Unknown 425 13

Recovery rate 87

End-of-life tyres in Greece as a resource

3

it is essential to classify them by considering the appropriatetyre size (Table 3).

Material recyclingApplications for material recycling from end-of-life-tyreshave significantly developed over the last decade. End-of-life-tyres can be used either as a whole, or is shredded or aspowdered rubber.

Whole tyres

Civil engineering applications are the main recovery routefor whole tyres (Yamaguchi 2000a). The applications includecoastal protection, erosion barriers, artificial reefs, breakwa-ters, avalanche shelters, slope stabilisation, road embank-

ments and landfill construction operations, sound barriersand insulation material (Yamaguchi 2000b). Whole tyres areused also on farms as silage clamps. This market is for themoment confined to single projects and, therefore, fairlysmall-scale (RMA 2004). A case study for the manufactureof tyre bales and the first use in house building accessed inthe UK to secure an embankment for the construction ofnew houses in a residential area on the outskirts of Inver-ness, Scotland. A 100-m embankment utilised approximately21,000 tyres weighing 160 tonnes (WRAP 2008a).

Shredded tyres

Whole tyres are mechanically sheared into shreds ranging insize from 25–300 mm. A large amount of crumb rubber is

Fig. 1: Range of size reduced materials from end-of-life-tyres and related terminology (Stutz et al. 2003).

Table 3: Most significant end-of-life tyre management technologies.

EOL tire management Technologies/Applications EOL tire size

Material Recycling

Civil engineering applications

Erosion barriers

Whole tires

Sound barriers

Avalanche shelters

Road embankments

Landfill construction operations

Slope stabilisation

Draining material

Shredded tiresBackfill for walls

Subgrad insulation

General engineering applications

Using as wheels

Powdered rubberRubber-modified asphalt

Floor for playgrounds and sports stadiums

Artificial turf for football fields

Re-use Second-hand tires Whole tires

Retreading Pre-moulded or cold-cure retreadingWhole tires

Mould-cure or hot-cure retreading

Energy recovery Pyrolysis Whole or shredded tiresTire Derived Fuel (TDF)

A. Karagiannidis, T. Kasampalis

4

used in civil engineering projects, such as playground sur-faces, parking lots, bank stabilization, fill under road surfaceand asphalt modifier, because the scrap tyre chips have prop-erties that road builders find essential: light weight, low earthpressure, good thermal insulation and good drainage proper-ties. Another important attribute is its better damping prop-erty which is good for running vehicles (Adhikari et al. 2000).End-of-life-tyres can be converted into rubber chips for useas attractive horticultural mulch that can assist in retainingnutrients and moisture, thereby helping plant growth andpromoting the conservation of natural resources (WRAP2008b).

Crumb and powdered rubber

After the removal of the steel and fabric components, theremaining rubber is reduced to granular rubber. Applica-tions include moulded rubber products such as wheels forcaddies, dustbins, wheelbarrows and lawnmowers, urban fur-niture and sign posts (U.S. EPA 2005). Crumb and powderedrubber are also to be found as flooring for playgrounds andsports stadiums, while a promising use of crumb rubber is inthe construction of artificial turf, for example, in football fields(Stutz et al. 2003). Rubber-modified asphalt takes advantageof the elasticity and noise absorbing characteristics of the rub-ber (State of California 2003) and can finally be used also asa crack sealant and in repair membranes (Dufton 1995). In2006, a pioneering trial was commissioned at a Nottingham-shire bridleway, UK, which compared a control section ofstandard bridleway construction materials with sectionsincorporating used tyre rubber chips (WRAP 2008c).

Re-use and exportMany used tyres are transported world-wide and can be re-used as second-hand tyres for their originally intended pur-pose. Currently, more than 9% of used tyres are reusedlocally or exported (Blumenthal 2003).

RetreadingRetreading is the process whereby selected and inspectedworn tyres (called casings) receive a new tread (ITRA 2001).Truckers, airlines, construction companies, farmers andpoorer car owners purchase retreads in order to save money.A retreaded tyre costs less to ‘produce’ than a new tyre andsells for less, usually between 30–50% of the comparable newtyre price. However, there is a strong belief among peoplethat retreaded tyres are less safe and have a higher failurerate than new tyres (ITRA 2001). Argos Direct (home deliv-ery arm of retailing giant Argos, UK) has decided to useretreads as part of a drive to reduce its environmental impacton the roads. Currently (2008), 52% of replacement tyres forits commercial fleet are retreads and the company operates afleet of over 750 commercial vehicles in the UK (WRAP2008d). Furthermore, Alltruck (one of the market leaders intruck hire, rental and distribution solutions in the UK andIreland) has found retreaded tyres to be not only extremelyaffordable and reliable but also equally good for the environ-

ment. Alltruck operates a fleet in excess of 1000 vehicles(WRAP 2008e).

Energy recoveryThe rubber component of tyres yields large amounts of energyon combustion. As a comparison, hard coal provides up to29 MJ kg–1 while tyre rubber provides about 32.5 MJ kg–1 ofenergy (Dufton 1995); it should be mentioned at this pointthat the Hellenic browncoal (lignite) is of even lower quality,with a heat value of around 13 MJ kg–1. At present, energyrecovery from end-of-life-tyres can take three forms: (i) co-combustion in existing industrial furnaces; (ii) mono-com-bustion in dedicated incinerators; and (iii) pyrolysis and gasi-fication for fuel as well as material recovery.

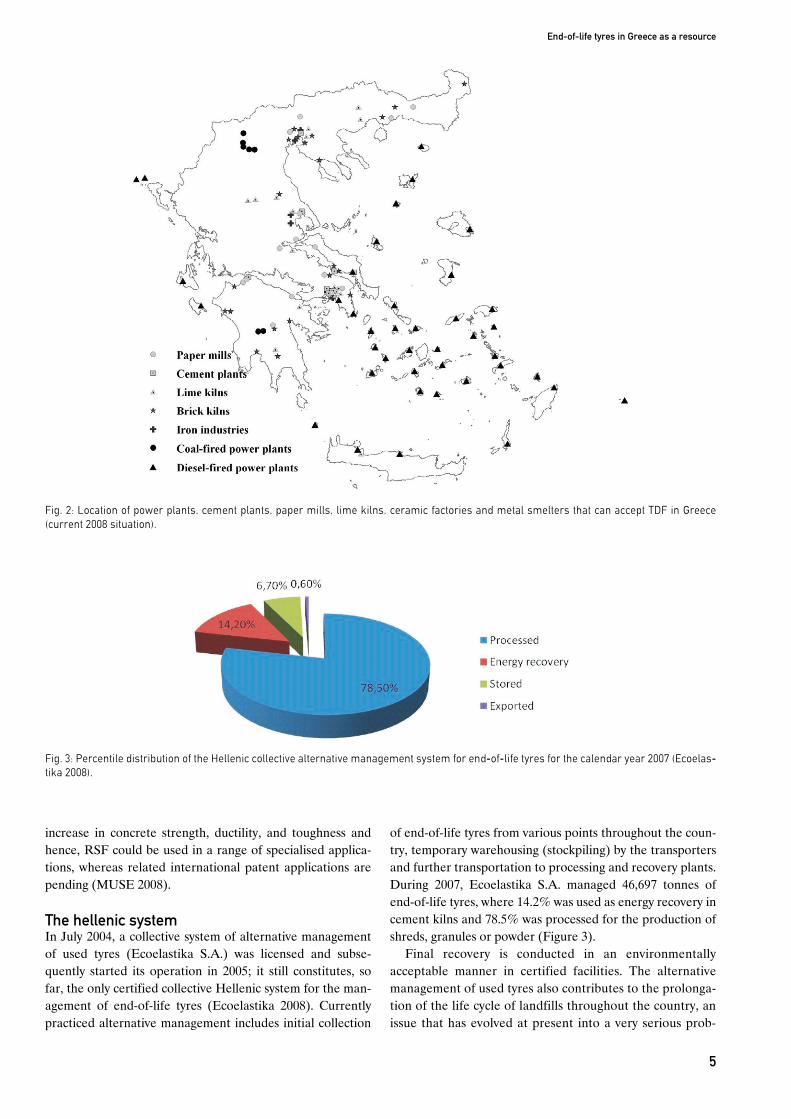

TDF can be used successfully and without significant retro-fitting as a 10–20% supplementary fuel in properly designedsolid fuel industrial combustors (Wellington City Council2003). There are various components to the TDF market suchas: (i) cement kilns; (ii) utility, industrial and pulp and papermill boilers; (iii) dedicated end-of-life tyre to energy andmunicipal waste to energy facilities; and (iv) copper smelters,iron cupola foundries and limekilns (Gray 2004). By June2008, within the EU, there were 250–300 cement works inoperation, which could potentially utilize the equivalent ofthe total number of end-of-life-tyres generated annually. Thelargest use of TDF is for cement production in rotary, fuel-fired kilns and, as shown in Figure 2, there are many suchapplications where TDF could be used in Greece. Figure 2illustrates the location of lignite power plants in Greece, aswell as the location of some other existing industrial facilitiesthat may be considered potential future recipients of TDF,either in the stricter or in the broader sense. In the cementkiln, a mixture of finely ground calcareous (e.g. limestone),argillaceous (e.g. clay, shale) and siliceous (e.g. sand) materialsis heated to 1500–1600°C to produce calcium silicate clinkerwhich is later ground with gypsum to produce cement pow-der. Scrap tyres serve as excellent fuel for this kiln, eitherwhole or shredded, as the very high temperatures and oxidiz-ing atmosphere in the kiln provide for complete combustion.Additionally, the volatilised iron oxide resulting from com-bustion is useful for the cement product, reducing the costsof adding supplemental iron to the feed mix (Gray 2000).

Pyrolysis of end-of-life tyres is the thermal degradation inthe absence of air to produce carbon black (22%), oil (30%),gas (28%), steel (10%) and a small quantity of inorganic slagor ash (5%) (Yongrong et al. 2000). Carbon black is used in awide variety of applications; indeed, one of the major users isthe rubber industry itself (KOPIA 2004). Gasification is thepartial combustion of organics to produce industrial synthe-sis gas, which can itself be used either as fuel or as feedstockin the chemical industry.

One possible market area for recycled steel fibres is thatof concrete construction, where industrially produced steelfibres are replacing re-bars in a range of applications, suchas slabs-on-grade, industrial floors, precast applications andsprayed concrete. The use of RSF in concrete leads to an

End-of-life tyres in Greece as a resource

5

increase in concrete strength, ductility, and toughness andhence, RSF could be used in a range of specialised applica-tions, whereas related international patent applications arepending (MUSE 2008).

The hellenic systemIn July 2004, a collective system of alternative managementof used tyres (Ecoelastika S.A.) was licensed and subse-quently started its operation in 2005; it still constitutes, sofar, the only certified collective Hellenic system for the man-agement of end-of-life tyres (Ecoelastika 2008). Currentlypracticed alternative management includes initial collection

of end-of-life tyres from various points throughout the coun-try, temporary warehousing (stockpiling) by the transportersand further transportation to processing and recovery plants.During 2007, Ecoelastika S.A. managed 46,697 tonnes ofend-of-life tyres, where 14.2% was used as energy recovery incement kilns and 78.5% was processed for the production ofshreds, granules or powder (Figure 3).

Final recovery is conducted in an environmentallyacceptable manner in certified facilities. The alternativemanagement of used tyres also contributes to the prolonga-tion of the life cycle of landfills throughout the country, anissue that has evolved at present into a very serious prob-

Fig. 2: Location of power plants, cement plants, paper mills, lime kilns, ceramic factories and metal smelters that can accept TDF in Greece(current 2008 situation).

Fig. 3: Percentile distribution of the Hellenic collective alternative management system for end-of-life tyres for the calendar year 2007 (Ecoelas-tika 2008).

A. Karagiannidis, T. Kasampalis

6

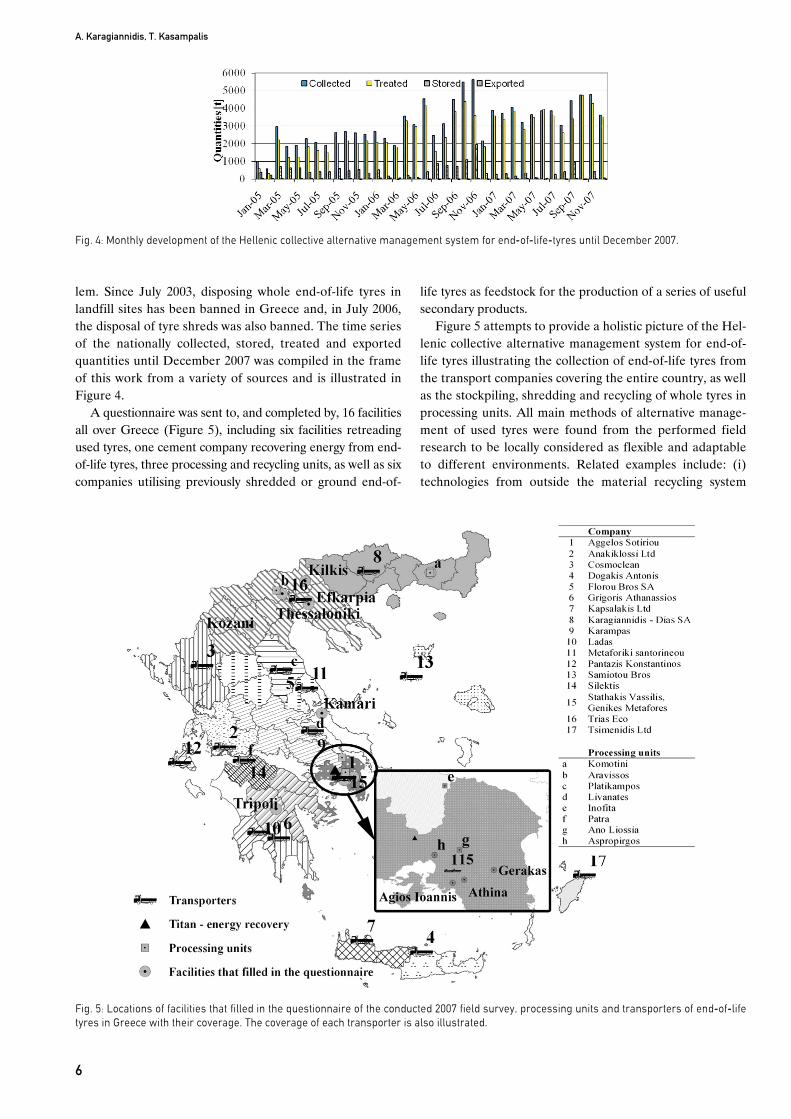

lem. Since July 2003, disposing whole end-of-life tyres inlandfill sites has been banned in Greece and, in July 2006,the disposal of tyre shreds was also banned. The time seriesof the nationally collected, stored, treated and exportedquantities until December 2007 was compiled in the frameof this work from a variety of sources and is illustrated inFigure 4.

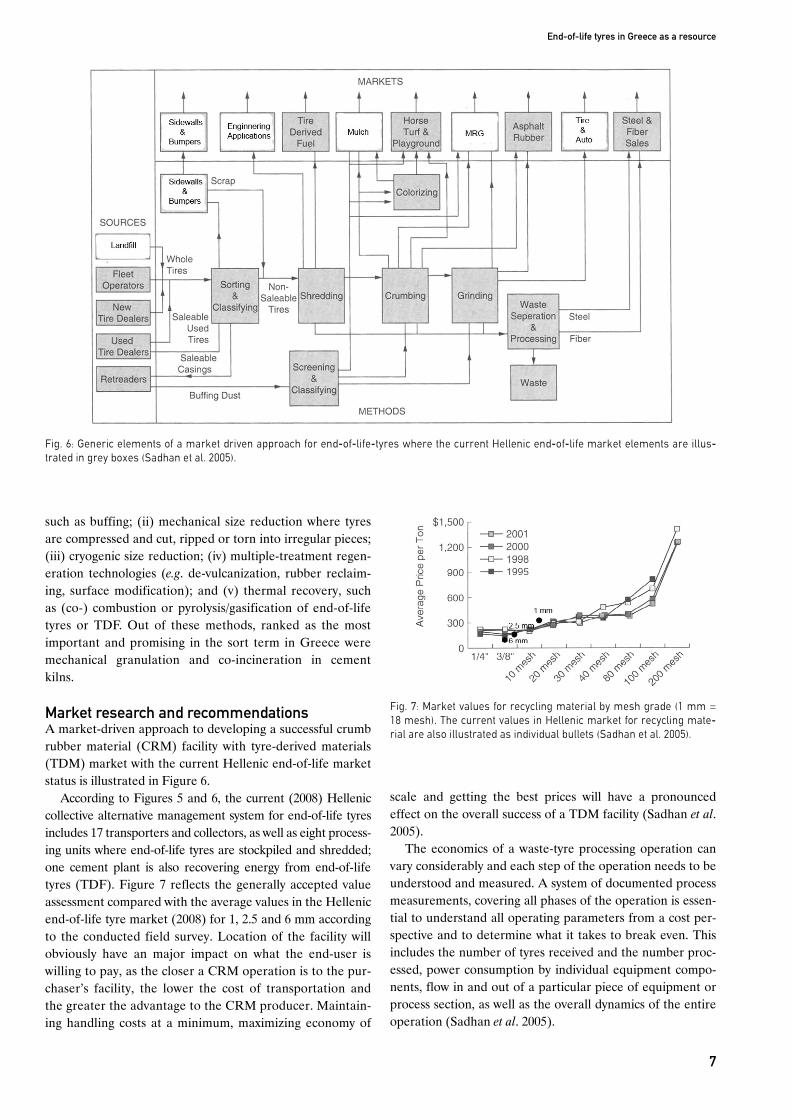

A questionnaire was sent to, and completed by, 16 facilitiesall over Greece (Figure 5), including six facilities retreadingused tyres, one cement company recovering energy from end-of-life tyres, three processing and recycling units, as well as sixcompanies utilising previously shredded or ground end-of-

life tyres as feedstock for the production of a series of usefulsecondary products.

Figure 5 attempts to provide a holistic picture of the Hel-lenic collective alternative management system for end-of-life tyres illustrating the collection of end-of-life tyres fromthe transport companies covering the entire country, as wellas the stockpiling, shredding and recycling of whole tyres inprocessing units. All main methods of alternative manage-ment of used tyres were found from the performed fieldresearch to be locally considered as flexible and adaptableto different environments. Related examples include: (i)technologies from outside the material recycling system

Fig. 4: Monthly development of the Hellenic collective alternative management system for end-of-life-tyres until December 2007.

Fig. 5: Locations of facilities that filled in the questionnaire of the conducted 2007 field survey, processing units and transporters of end-of-lifetyres in Greece with their coverage. The coverage of each transporter is also illustrated.

End-of-life tyres in Greece as a resource

7

such as buffing; (ii) mechanical size reduction where tyresare compressed and cut, ripped or torn into irregular pieces;(iii) cryogenic size reduction; (iv) multiple-treatment regen-eration technologies (e.g. de-vulcanization, rubber reclaim-ing, surface modification); and (v) thermal recovery, suchas (co-) combustion or pyrolysis/gasification of end-of-lifetyres or TDF. Out of these methods, ranked as the mostimportant and promising in the sort term in Greece weremechanical granulation and co-incineration in cementkilns.

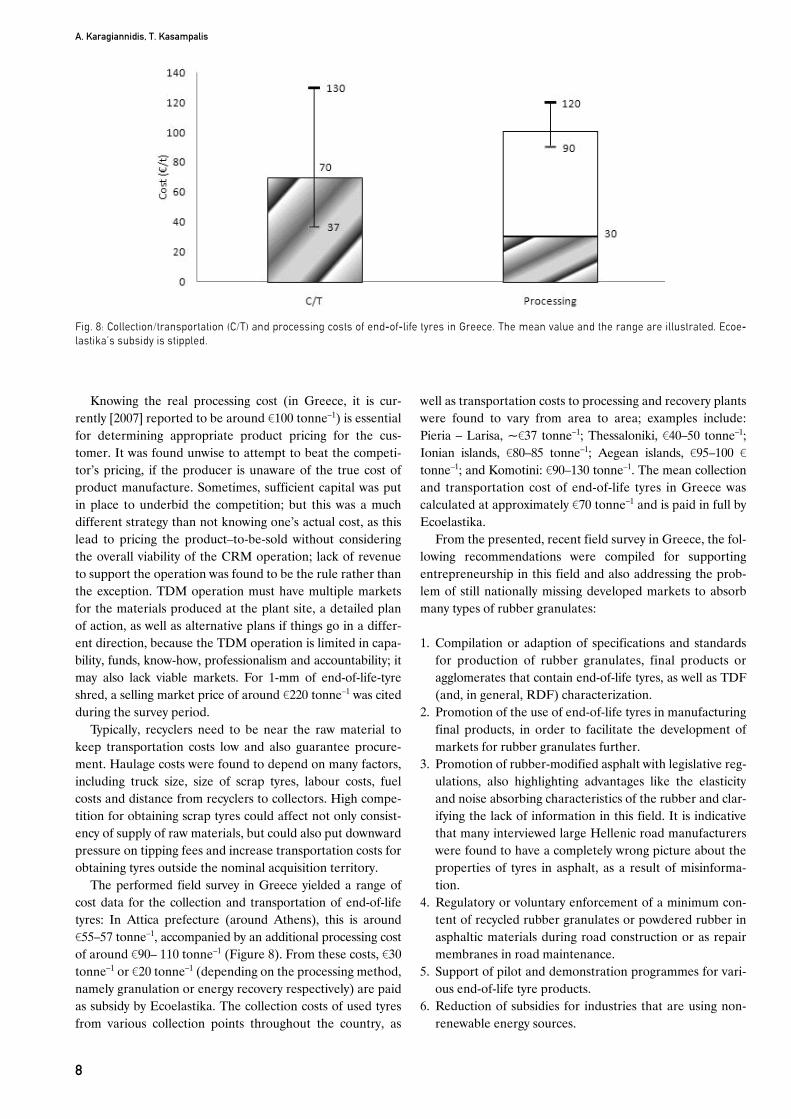

Market research and recommendationsA market-driven approach to developing a successful crumbrubber material (CRM) facility with tyre-derived materials(TDM) market with the current Hellenic end-of-life marketstatus is illustrated in Figure 6.

According to Figures 5 and 6, the current (2008) Helleniccollective alternative management system for end-of-life tyresincludes 17 transporters and collectors, as well as eight process-ing units where end-of-life tyres are stockpiled and shredded;one cement plant is also recovering energy from end-of-lifetyres (TDF). Figure 7 reflects the generally accepted valueassessment compared with the average values in the Hellenicend-of-life tyre market (2008) for 1, 2.5 and 6 mm accordingto the conducted field survey. Location of the facility willobviously have an major impact on what the end-user iswilling to pay, as the closer a CRM operation is to the pur-chaser’s facility, the lower the cost of transportation andthe greater the advantage to the CRM producer. Maintain-ing handling costs at a minimum, maximizing economy of

scale and getting the best prices will have a pronouncedeffect on the overall success of a TDM facility (Sadhan et al.2005).

The economics of a waste-tyre processing operation canvary considerably and each step of the operation needs to beunderstood and measured. A system of documented processmeasurements, covering all phases of the operation is essen-tial to understand all operating parameters from a cost per-spective and to determine what it takes to break even. Thisincludes the number of tyres received and the number proc-essed, power consumption by individual equipment compo-nents, flow in and out of a particular piece of equipment orprocess section, as well as the overall dynamics of the entireoperation (Sadhan et al. 2005).

Fig. 6: Generic elements of a market driven approach for end-of-life-tyres where the current Hellenic end-of-life market elements are illus-trated in grey boxes (Sadhan et al. 2005).

Fig. 7: Market values for recycling material by mesh grade (1 mm =18 mesh). The current values in Hellenic market for recycling mate-rial are also illustrated as individual bullets (Sadhan et al. 2005).

A. Karagiannidis, T. Kasampalis

8

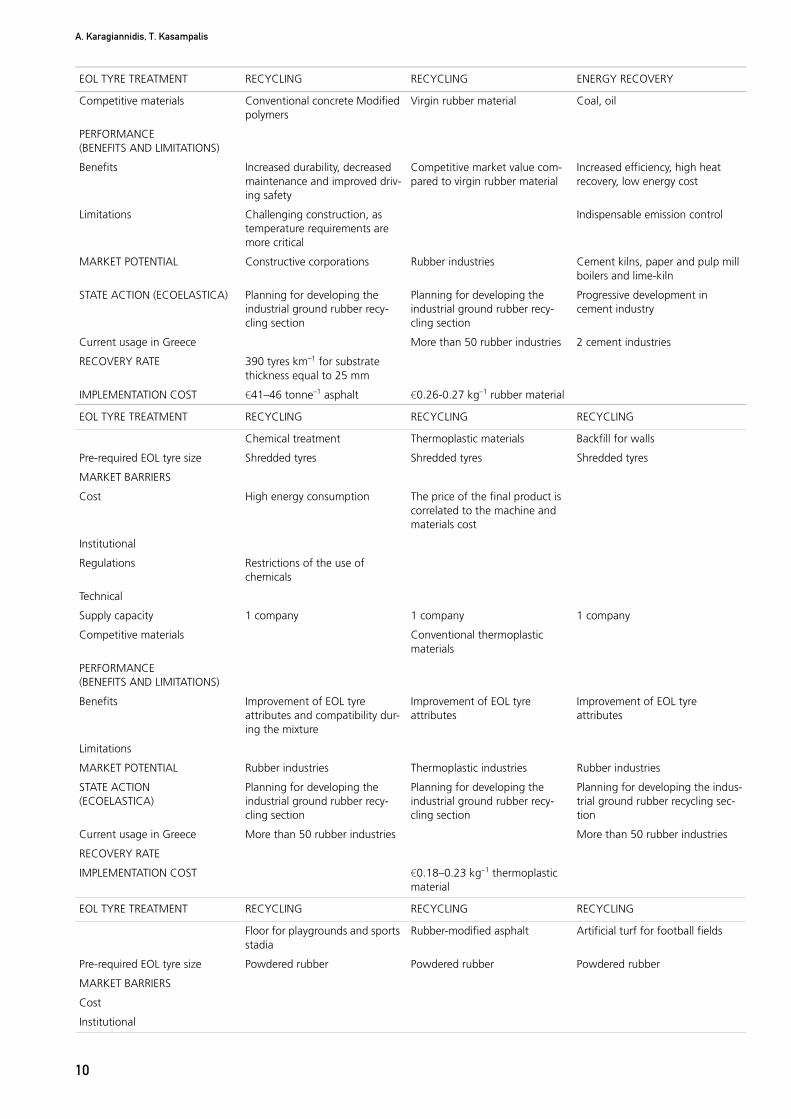

Knowing the real processing cost (in Greece, it is cur-rently [2007] reported to be around €100 tonne–1) is essentialfor determining appropriate product pricing for the cus-tomer. It was found unwise to attempt to beat the competi-tor’s pricing, if the producer is unaware of the true cost ofproduct manufacture. Sometimes, sufficient capital was putin place to underbid the competition; but this was a muchdifferent strategy than not knowing one’s actual cost, as thislead to pricing the product–to-be-sold without consideringthe overall viability of the CRM operation; lack of revenueto support the operation was found to be the rule rather thanthe exception. TDM operation must have multiple marketsfor the materials produced at the plant site, a detailed planof action, as well as alternative plans if things go in a differ-ent direction, because the TDM operation is limited in capa-bility, funds, know-how, professionalism and accountability; itmay also lack viable markets. For 1-mm of end-of-life-tyreshred, a selling market price of around €220 tonne–1 was citedduring the survey period.

Typically, recyclers need to be near the raw material tokeep transportation costs low and also guarantee procure-ment. Haulage costs were found to depend on many factors,including truck size, size of scrap tyres, labour costs, fuelcosts and distance from recyclers to collectors. High compe-tition for obtaining scrap tyres could affect not only consist-ency of supply of raw materials, but could also put downwardpressure on tipping fees and increase transportation costs forobtaining tyres outside the nominal acquisition territory.

The performed field survey in Greece yielded a range ofcost data for the collection and transportation of end-of-lifetyres: In Attica prefecture (around Athens), this is around€55–57 tonne–1, accompanied by an additional processing costof around €90– 110 tonne–1 (Figure 8). From these costs, €30tonne–1 or €20 tonne–1 (depending on the processing method,namely granulation or energy recovery respectively) are paidas subsidy by Ecoelastika. The collection costs of used tyresfrom various collection points throughout the country, as

well as transportation costs to processing and recovery plantswere found to vary from area to area; examples include:Pieria – Larisa, ~€37 tonne–1; Thessaloniki, €40–50 tonne–1;Ionian islands, €80–85 tonne–1; Aegean islands, €95–100 €tonne–1; and Komotini: €90–130 tonne–1. The mean collectionand transportation cost of end-of-life tyres in Greece wascalculated at approximately €70 tonne–1 and is paid in full byEcoelastika.

From the presented, recent field survey in Greece, the fol-lowing recommendations were compiled for supportingentrepreneurship in this field and also addressing the prob-lem of still nationally missing developed markets to absorbmany types of rubber granulates:

1. Compilation or adaption of specifications and standardsfor production of rubber granulates, final products oragglomerates that contain end-of-life tyres, as well as TDF(and, in general, RDF) characterization.

2. Promotion of the use of end-of-life tyres in manufacturingfinal products, in order to facilitate the development ofmarkets for rubber granulates further.

3. Promotion of rubber-modified asphalt with legislative reg-ulations, also highlighting advantages like the elasticityand noise absorbing characteristics of the rubber and clar-ifying the lack of information in this field. It is indicativethat many interviewed large Hellenic road manufacturerswere found to have a completely wrong picture about theproperties of tyres in asphalt, as a result of misinforma-tion.

4. Regulatory or voluntary enforcement of a minimum con-tent of recycled rubber granulates or powdered rubber inasphaltic materials during road construction or as repairmembranes in road maintenance.

5. Support of pilot and demonstration programmes for vari-ous end-of-life tyre products.

6. Reduction of subsidies for industries that are using non-renewable energy sources.

Fig. 8: Collection/transportation (C/T) and processing costs of end-of-life tyres in Greece. The mean value and the range are illustrated. Ecoe-lastika’s subsidy is stippled.

End-of-life tyres in Greece as a resource

9

A newly compiled management review table (see Appendix 1)including classified technical and economic information onthe currently applied end-of-life tyre treatment technologiesin Greece was compiled, as a flexible decision-support toolfor young entrepreneurs and policy makers in this field; itincludes classified and easy-to-use information both for eachapplication of end-of-life tyre treatment including: (i) requiredend-of-life tyre size; (ii) market barriers such as cost, institu-tional, regulatory and technical; (iii) supply capacity; (iv) com-petitive materials; (v) performance benefits and limitations;(vi) market potential; (vii) state action; (viii) current usage;(ix) recovery rate; and (x) implementation cost. This tool hasbeen preliminarily tested already in the field with somestakeholders in the Hellenic end-of-life tyre industry andreceived positive comments; a continuous further validationis planned for the near future. The version presented here isnaturally the original form.

ConclusionsEnd-of-life-tyres represent a serious disposal and environ-mental problem, which can cause several human health haz-ards. Both European and Hellenic legislation have alreadybanned end-of-life tyre landfilling. It is essential that end-of-life tyres are first shredded or granulated, depending on therequired material size, because it is impossible to treat themin their initial shape and vulcanized chemical formation.Transporters should consider a primary shredding at theirown facilities before taking the material to the recyclers.Products generally refer to consumer and industrial goods;they include refined materials, as well as feedstock for energyrecovery.

The end-of-life tyre recovery rate in many EU countries isalready up to 100%; in Greece, some end-of-life tyre treat-

ment options (such as energy recovery of TDF) are still inprogressive development and the largest potential end-of-life tyre treatment market so far is using TDF in cementkilns, with the main associated barriers related to securityof supply and the missing standardization framework forrecovered fuel properties and quality. Rubber-modifiedasphalt is still a nationally unexplored area with manypromising advantages, as this asphalt increases the life-spanof the road surface, reduces noise pollution and increasessafety in wet road conditions. It is still relatively underuti-lised, mostly due to ignorance and lack of awareness of thelocal technical environment and stakeholders; major steps inthis direction are planned. Given the significant amount ofroadwork that is planned up to 2012, this potential applica-tion is particularly appealing, with the sound barrier effectextending not only to the asphalt itself but also to side wallsthat can be made out of end-of-life tyres, thus offering aneven broader market. Furthermore, producing ground rub-ber and recycling it into new rubber products or using it inlandscaping applications is a market with a great potential inGreece, since significant restoration needs are apparent in anumber of degraded sites, including mining areas, old indus-trial grounds and landfills. The currently most commonapplication of rubber granulate is feedstock for the construc-tion of artificial turfs of small football fields, as well as theuse of rubber powder for the construction of wheels fortrash cans; belt conveyors were also found to be manufac-tured in certain cases within local facilities from end-of-lifetyres. It is noteworthy that recovered secondary powder isalso being imported for this purpose, a fact that alone indi-cates significant additional improvement margins of thedomestic system and its potential for further reducing importsas well.

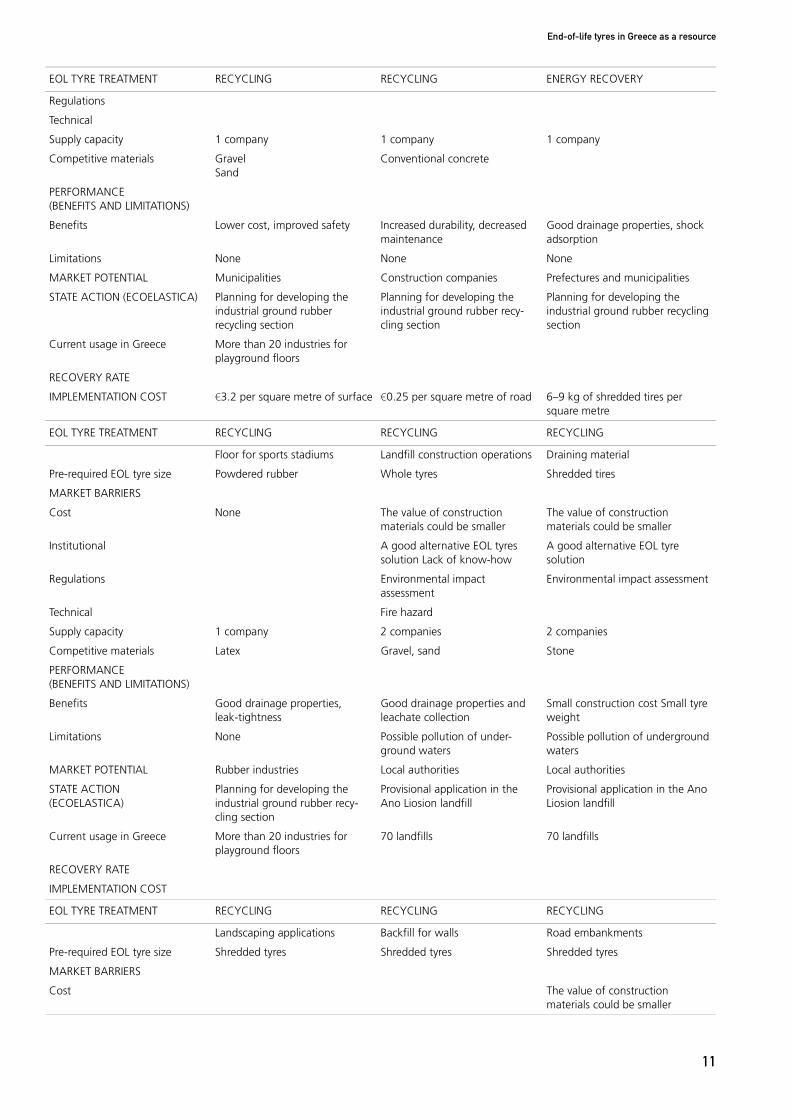

Appendix 1End-of-life tyre management review

EOL TYRE TREATMENT RECYCLING RECYCLING ENERGY RECOVERY

Rubber – modified asphalt New rubber products Tyre-derived fuel (TDF)

Pre-required EOL tyre size Powdered rubber Shredded tyres Whole or shredded tires

MARKET BARRIERS

Cost Mobilisation cost for asphalt rubber production equipment; for small projects, this cost results in greater increase in unit price that may not be fully offset

High energy consumption

Institutional Social concern for possible air pollution due to limited emission control

Regulations Emission control regulations

Technical Not appropriate for using in dense graded asphalt concrete (DGAC) Possible odour emis-sions

Technical know-how

Supply capacity 1 company Various collection points throughout the country

A. Karagiannidis, T. Kasampalis

10

Competitive materials Conventional concrete Modified polymers

Virgin rubber material Coal, oil

PERFORMANCE (BENEFITS AND LIMITATIONS)

Benefits Increased durability, decreased maintenance and improved driv-ing safety

Competitive market value com-pared to virgin rubber material

Increased efficiency, high heat recovery, low energy cost

Limitations Challenging construction, as temperature requirements are more critical

Indispensable emission control

MARKET POTENTIAL Constructive corporations Rubber industries Cement kilns, paper and pulp mill boilers and lime-kiln

STATE ACTION (ECOELASTICA) Planning for developing the industrial ground rubber recy-cling section

Planning for developing the industrial ground rubber recy-cling section

Progressive development in cement industry

Current usage in Greece More than 50 rubber industries 2 cement industries

RECOVERY RATE 390 tyres km–1 for substrate thickness equal to 25 mm

IMPLEMENTATION COST €41–46 tonne–1 asphalt €0.26-0.27 kg–1 rubber material

EOL TYRE TREATMENT RECYCLING RECYCLING RECYCLING

Chemical treatment Thermoplastic materials Backfill for walls

Pre-required EOL tyre size Shredded tyres Shredded tyres Shredded tyres

MARKET BARRIERS

Cost High energy consumption The price of the final product is correlated to the machine and materials cost

Institutional

Regulations Restrictions of the use of chemicals

Technical

Supply capacity 1 company 1 company 1 company

Competitive materials Conventional thermoplastic materials

PERFORMANCE (BENEFITS AND LIMITATIONS)

Benefits Improvement of EOL tyre attributes and compatibility dur-ing the mixture

Improvement of EOL tyre attributes

Improvement of EOL tyre attributes

Limitations

MARKET POTENTIAL Rubber industries Thermoplastic industries Rubber industries

STATE ACTION(ECOELASTICA)

Planning for developing the industrial ground rubber recy-cling section

Planning for developing the industrial ground rubber recy-cling section

Planning for developing the indus-trial ground rubber recycling sec-tion

Current usage in Greece More than 50 rubber industries More than 50 rubber industries

RECOVERY RATE

IMPLEMENTATION COST €0.18–0.23 kg–1 thermoplastic material

EOL TYRE TREATMENT RECYCLING RECYCLING RECYCLING

Floor for playgrounds and sports stadia

Rubber-modified asphalt Artificial turf for football fields

Pre-required EOL tyre size Powdered rubber Powdered rubber Powdered rubber

MARKET BARRIERS

Cost

Institutional

EOL TYRE TREATMENT RECYCLING RECYCLING ENERGY RECOVERY

End-of-life tyres in Greece as a resource

11

Regulations

Technical

Supply capacity 1 company 1 company 1 company

Competitive materials GravelSand

Conventional concrete

PERFORMANCE (BENEFITS AND LIMITATIONS)

Benefits Lower cost, improved safety Increased durability, decreased maintenance

Good drainage properties, shock adsorption

Limitations None None None

MARKET POTENTIAL Municipalities Construction companies Prefectures and municipalities

STATE ACTION (ECOELASTICA) Planning for developing the industrial ground rubber recycling section

Planning for developing the industrial ground rubber recy-cling section

Planning for developing the industrial ground rubber recycling section

Current usage in Greece More than 20 industries for playground floors

RECOVERY RATE

IMPLEMENTATION COST €3.2 per square metre of surface €0.25 per square metre of road 6–9 kg of shredded tires per square metre

EOL TYRE TREATMENT RECYCLING RECYCLING RECYCLING

Floor for sports stadiums Landfill construction operations Draining material

Pre-required EOL tyre size Powdered rubber Whole tyres Shredded tires

MARKET BARRIERS

Cost None The value of construction materials could be smaller

The value of construction materials could be smaller

Institutional A good alternative EOL tyres solution Lack of know-how

A good alternative EOL tyre solution

Regulations Environmental impact assessment

Environmental impact assessment

Technical Fire hazard

Supply capacity 1 company 2 companies 2 companies

Competitive materials Latex Gravel, sand Stone

PERFORMANCE (BENEFITS AND LIMITATIONS)

Benefits Good drainage properties, leak-tightness

Good drainage properties and leachate collection

Small construction cost Small tyre weight

Limitations None Possible pollution of under-ground waters

Possible pollution of underground waters

MARKET POTENTIAL Rubber industries Local authorities Local authorities

STATE ACTION(ECOELASTICA)

Planning for developing the industrial ground rubber recy-cling section

Provisional application in the Ano Liosion landfill

Provisional application in the Ano Liosion landfill

Current usage in Greece More than 20 industries for playground floors

70 landfills 70 landfills

RECOVERY RATE

IMPLEMENTATION COST

EOL TYRE TREATMENT RECYCLING RECYCLING RECYCLING

Landscaping applications Backfill for walls Road embankments

Pre-required EOL tyre size Shredded tyres Shredded tyres Shredded tyres

MARKET BARRIERS

Cost The value of construction materials could be smaller

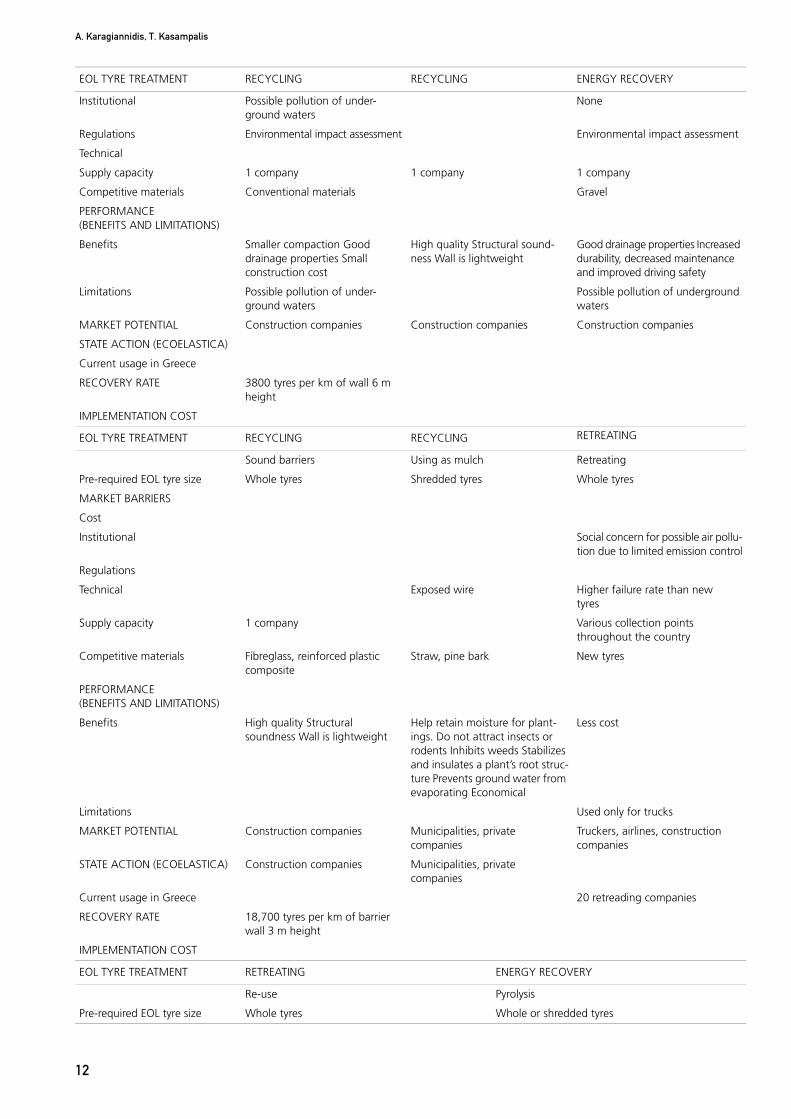

EOL TYRE TREATMENT RECYCLING RECYCLING ENERGY RECOVERY

A. Karagiannidis, T. Kasampalis

12

Institutional Possible pollution of under-ground waters

None

Regulations Environmental impact assessment Environmental impact assessment

Technical

Supply capacity 1 company 1 company 1 company

Competitive materials Conventional materials Gravel

PERFORMANCE (BENEFITS AND LIMITATIONS)

Benefits Smaller compaction Good drainage properties Small construction cost

High quality Structural sound-ness Wall is lightweight

Good drainage properties Increased durability, decreased maintenance and improved driving safety

Limitations Possible pollution of under-ground waters

Possible pollution of underground waters

MARKET POTENTIAL Construction companies Construction companies Construction companies

STATE ACTION (ECOELASTICA)

Current usage in Greece

RECOVERY RATE 3800 tyres per km of wall 6 m height

IMPLEMENTATION COST

EOL TYRE TREATMENT RECYCLING RECYCLING RETREATING

Sound barriers Using as mulch Retreating

Pre-required EOL tyre size Whole tyres Shredded tyres Whole tyres

MARKET BARRIERS

Cost

Institutional Social concern for possible air pollu-tion due to limited emission control

Regulations

Technical Exposed wire Higher failure rate than new tyres

Supply capacity 1 company Various collection points throughout the country

Competitive materials Fibreglass, reinforced plastic composite

Straw, pine bark New tyres

PERFORMANCE (BENEFITS AND LIMITATIONS)

Benefits High quality Structural soundness Wall is lightweight

Help retain moisture for plant-ings. Do not attract insects or rodents Inhibits weeds Stabilizes and insulates a plant’s root struc-ture Prevents ground water from evaporating Economical

Less cost

Limitations Used only for trucks

MARKET POTENTIAL Construction companies Municipalities, private companies

Truckers, airlines, construction companies

STATE ACTION (ECOELASTICA) Construction companies Municipalities, private companies

Current usage in Greece 20 retreading companies

RECOVERY RATE 18,700 tyres per km of barrier wall 3 m height

IMPLEMENTATION COST

EOL TYRE TREATMENT RETREATING ENERGY RECOVERY

Re-use Pyrolysis

Pre-required EOL tyre size Whole tyres Whole or shredded tyres

EOL TYRE TREATMENT RECYCLING RECYCLING ENERGY RECOVERY

End-of-life tyres in Greece as a resource

13

ReferencesAdhikari, B., Maiti, S. (2000) Reclamation and recycling of waste rubber,

Progress in Polymer Science, 25, 909–948.Blumenthal, M. (2003) Factors influencing the use of tire. RCRA Confer-

ence, Washington DC, USA.Dufton, P.W. (1995) Scrap tyres – disposal and recycling options. Rapra

Technology.Ecoelastika S.A. (2008) Alternative management of End of Life Tires.

<http://www.ecoelastika.gr> (4 July 2008).ETRMA. European Tire & Rubber Manufacturers’ Association (2008)

<http://www.etrma.org> (9 May 2008).Gray, T. (2000) Crumb rubber processing in the twenty-first century. Third

Southeast Regional Scrap Tire Management Conference, Atlanta,GA, USA.

Gray, T. (2004) Tire Derived Fuel: Environmental Characteristics and Per-formance. Second Heartlands Regional Waste Tire Conference,Omaha, NB, USA.

ITRA (2001) Understanding Retreading. International Tire & RubberAssociation Foundation.

KOPIA. Korea Plant Industries Association. (2004) Standard Proposal forWaste Tires Pyrolysis Incinerating Plant, Seoul, Korea. From KOPIA(2004) <http://www.kopia.or.kr/eng/main.asp> (4 July 2008).

MUSE (University of Sheffield, UK). Department of Civil and Struc-tural Engineering (2008) <http://www.shef.ac.uk/tyre-recycling/>.

RMA. Rubber Manufacturers Association. (2002) Rubber-ModifiedAsphalt. Washington DC, USA.

RMA. Rubber Manufacturers Association (2004) U.S. Scrap Tire Mar-kets 2003 edition.

Sadhan, K.D., Isayev, A.I. & Khait, K. (2005). Rubber Recycling, Taylor &Francis Group.

State of California, Department of Transportation. (2003) Asphalt Rub-ber Usage Guide. Division of Engineering Services, Materials, Engi-neering and Testing Services-MS#5, Office of Flexible PavementMaterials, Sacramento, CA, USA.

Stutz, J., Donahue Mintzer, S.E. & Cotter, A. (2003) Recycled RubberProducts in Landscaping Applications. Tellus Institute, Resourceand Environmental Strategies, Boston, MA, USA.

UK WRAP. Waste & Resources Action Programme (2008a) Tyres Pro-gramme. From WRP (2008) <ttp://www.wrap.org.uk/document.rm?id=6156>.

UK WRAP. Waste & Resources Action Programme (2008b) TyresProgramme. From WRP (2008) <http://www.wrap.org.uk/wrap_corporate/events/venues/olympia_london.html>.

UK WRAP. Waste & Resources Action Programme (2008c) Tyres Pro-gramme. From WRP (2008) <http://www.wrap.org.uk/construc-tion/tyres/a_new_route/technical_case_study.html>.

UK WRAP. Waste & Resources Action Programme (2008d) Tyres Pro-gramme. From WRP (2008) <http://www.wrap.org.uk/construc-tion/tyres/retread_tyres_on.html>.

UK WRAP. Waste & Resources Action Programme (2008e) Tyres Pro-gramme. From WRP (2008) <http://www.wrap.org.uk/construc-tion/tyres/retread_tyres_on.html>.

U.S. EPA. U.S. Environmental Protection Agency. (2005) Basic Infor-mation. From EPA (2005) <http://www.epa.gov/epaoswer/non-hw/muncpl/tyres/basic.htm> (10 June 2008).

Wellington City Council. (2003) Development of a Regional Waste Recov-ery/Processing Sector. Ministry for the Environment & Ministry ofEconomic Development, Wellington, New Zealand, pp. 19–21.

Yamaguchi, E. (2000a) Applications of Whole Waste Tires. Master ofEngineering thesis, University of Illinois, IL, USA <http://www.p2pays.org/ref/11/10504/html/usa/usewhole.htm> (15 May 2008).

Yamaguchi, E. (2000b) Sound Barrier Wall Containing Recycled Rubberand Plastic. Master of Engineering thesis, University of Illinois,IL, USA: <http://www.p2pays.org/ref/11/10504/html/biblio/html4/msh6.html> (15 May 2008).

Yongrong, Y., Jizhong, C. & Guibin, Z. (2000) Technical Advance on thePyrolysis of Used Tires in China. Department of Chemical Engineer-ing, Zhejiang University, YuQuan Campus, Hangzhou, China.

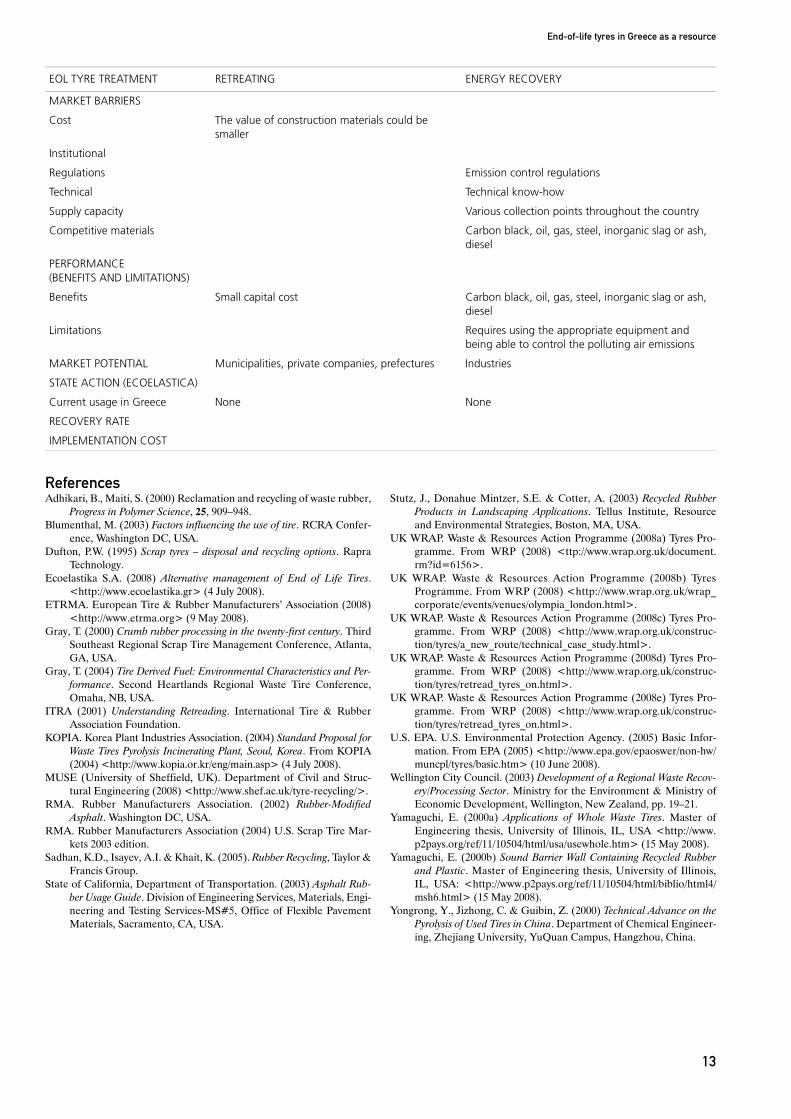

EOL TYRE TREATMENT RETREATING ENERGY RECOVERY

MARKET BARRIERS

Cost The value of construction materials could be smaller

Institutional

Regulations Emission control regulations

Technical Technical know-how

Supply capacity Various collection points throughout the country

Competitive materials Carbon black, oil, gas, steel, inorganic slag or ash, diesel

PERFORMANCE (BENEFITS AND LIMITATIONS)

Benefits Small capital cost Carbon black, oil, gas, steel, inorganic slag or ash, diesel

Limitations Requires using the appropriate equipment and being able to control the polluting air emissions

MARKET POTENTIAL Municipalities, private companies, prefectures Industries

STATE ACTION (ECOELASTICA)

Current usage in Greece None None

RECOVERY RATE

IMPLEMENTATION COST

Related Documents