1

Resource mobilisation through international market

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

To analyze various derivative instruments which are traded in the foreign exchange market.

To study in detail the role of the future and options.

To find out profit/loss position of the option writer and option holder.

To analyze the differences between the instruments traded in “Over the Counter” market and Exchange Traded market.

To understand the viewpoint of various participants of the derivatives market.

To analyze the advantages of hedging funds rather than keeping it idle through case a study of ITC.

2

The word derivative comes from the word ‘to derive’. It indicates that it has no independent value. Derivatives refer to a wide variety of financial instruments or financial contract whose value is derived from the performance of underlying market factors, such as market securities or indices, interest rates, currency exchange rates, and commodity, credit, and equity prices. It is a contract between two parties that specifies conditions. It is basically a betting instrument.

3

•Hedgers – They have an existing exposure. They take up a long or short position in the

derivative to reduce the exposure.

•Speculators – They have no exposure but a strong price belief. They take up long or short

position in the derivative to profit from their price belief knowing fully well that they can loose.

•Arbitragers – These are sophisticated institutions who invest human & physical

infrastructures to discover mispricing. Accordingly they take up simultaneous long & short position with a view to make risk less profit.

4

OTC Exchange Traded

1. Customized 1. Standardized

2. No margin requirement 2. Strict margin requirement

3. Low liquidity 3. Highly Liquid

4. No repricing 4. Repricing is done everyday

5. Less regulatory focus. 5. High regulatory focus

6. Settled by physical delivery mostly 6. Mostly squared off prior to maturity

7. Counter party default risks exist 7. Virtually no counter party default risk

8. Suitable for hedging 8. Suitable for speculation

9. Example: Financial Swaps 9. Example: Futures

5

Derivatives

Futures Options

Call Option Put Option

Swaps Futures

6

A futures contract is a standardized contract between two parties to buy or sell a specified asset of standardized quantity and quality for a price agreed upon today (the futures price or strike price) with delivery and payment occurring at a specified future date, the delivery date. The contracts are negotiated at a futures exchange, which acts as an intermediary between the two parties. The party agreeing to buy the underlying asset in the future, the "buyer" of the contract, is said to be "long", and the party agreeing to sell the asset in the future, the "seller" of the contract, is said to be "short".

7

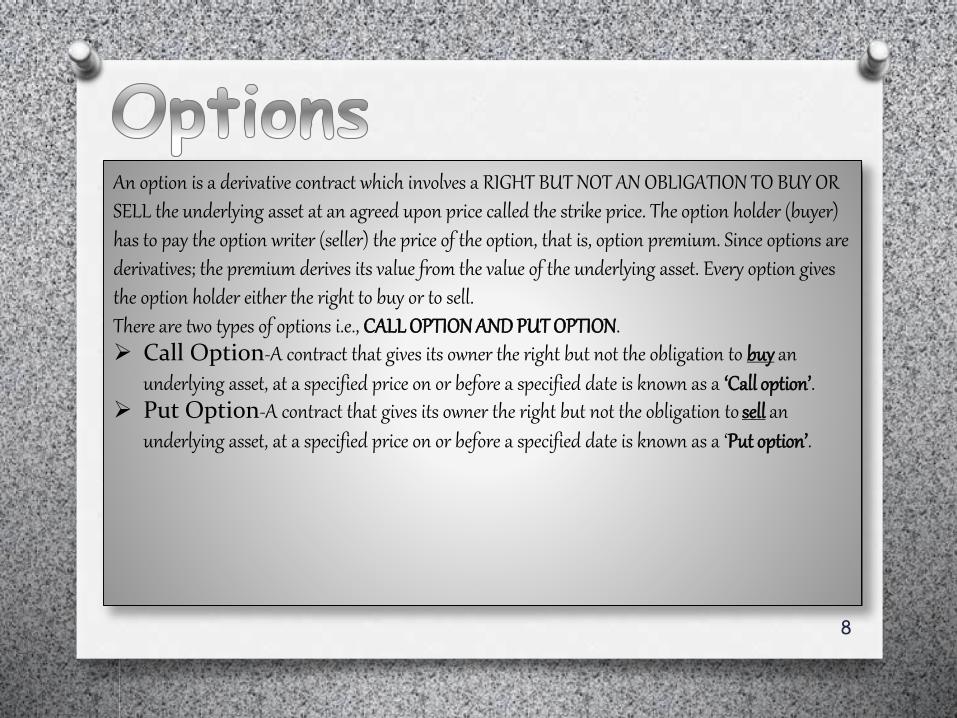

An option is a derivative contract which involves a RIGHT BUT NOT AN OBLIGATION TO BUY OR SELL the underlying asset at an agreed upon price called the strike price. The option holder (buyer) has to pay the option writer (seller) the price of the option, that is, option premium. Since options are derivatives; the premium derives its value from the value of the underlying asset. Every option gives the option holder either the right to buy or to sell. There are two types of options i.e., CALL OPTION AND PUT OPTION. Call Option-A contract that gives its owner the right but not the obligation to buy an

underlying asset, at a specified price on or before a specified date is known as a ‘Call option’. Put Option-A contract that gives its owner the right but not the obligation to sell an

underlying asset, at a specified price on or before a specified date is known as a ‘Put option’.

8

Swaps are transactions which obligates the two parties to the contract to exchange a series of cash flows at specified intervals known as payment or settlement dates. They can be regarded as portfolios of forward contracts. A contract whereby two parties agree to exchange (swap) payments, based on some notional principle amount is called as a ‘Swap’. In case of swap, only the payment flows are exchanged and not the principle amount.

A contract that obligates one counter party to buy and the other to sell a specific underlying asset at a specific price, amount and date in the future is known as a forward contract. Forward contracts are customized with the terms and conditions tailored to fit the particular business, financial or risk management objectives of the counter parties.

9

CASE STUDY OF ITC:ITC is one of the major participants in the derivative market. Most of its foreign currency exposure is hedged using Forward Covers & Options. Hence I have chosen this company to show the advantage of hedging rather than keeping the funds idle.

Scenario I- Hedging is not done Scenario II- Hedging is done through Futures Scenario III- Hedging is done through Options

Source of Information:The data has been taken from Annual Report of ITC and the Expected Spot Rate is from http://www.fedai.org which is complemented by http://www.nseindia.com for Strike Prices.

10

11

As at 31.03.2012 Rate as perFEDAI

Cash Flow on 31.03.2012

Currency Buy (a) Sell (b) Spot Rate (c) Outflow (a*c)

Inflow (b*c) Net (Rs.)

USD 17.93 17.83 54.9950 986.0604 980.5609 (5.4995)

EURO 3.66 3.67 72.5125 265.3958 266.1209 0.7251

GBP 1.84 1.74 88.9175 163.6082 154.7165 (8.8917)

Total Cash Inflow/(Outflow) in case hedging is not done (Rs.) (13.6661)

Figures in million

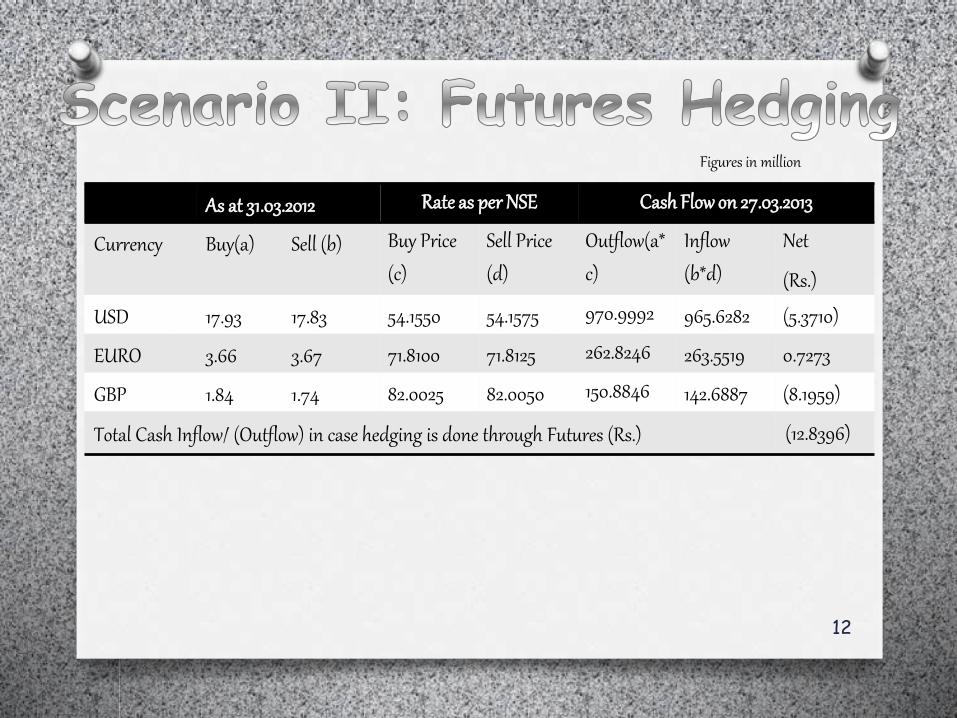

12

As at 31.03.2012 Rate as per NSE Cash Flow on 27.03.2013

Currency Buy(a) Sell (b) Buy Price

(c)

Sell Price

(d)

Outflow(a*

c)

Inflow

(b*d)

Net

(Rs.)

USD 17.93 17.83 54.1550 54.1575 970.9992 965.6282 (5.3710)

EURO 3.66 3.67 71.8100 71.8125 262.8246 263.5519 0.7273

GBP 1.84 1.74 82.0025 82.0050 150.8846 142.6887 (8.1959)

Total Cash Inflow/ (Outflow) in case hedging is done through Futures (Rs.) (12.8396)

Figures in million

13

Particulars Call Option Put Option

Strike Price 54 54

Market Price 1 USD=INR 54.9950

Premium 0.5950 0.4375

Whether exercisable Yes No

Result ITC will gain INR 0.4 per USD. ITC will not exercise the option as the

market price is greater than the Strike

price.

Particulars Workings Amount (Rs.)

Outflow of INR in case of Spot sell 17.93*54.9950 986.0604

Less: Outflow when Call option is exercised 17.93*54.0000 (968.2200)

Less: Premium paid 17.93*0.5950 (10.6684)

Total Cash Inflow/ (Outflow) in case hedging is done through Call Option (Rs.) 7.172

14

Findings from the analysis: We find that hedging is important as it helps to divert risks (diverting risk related to foreign

exchange rate in our case study) by reducing the amount of net outflow from Rs. 13.661 million to Rs. 12.8396 million in case of futures hedging. Thus risk of incurring losses can be mitigated through hedging in the derivatives market.

Moreover since derivatives market is purely based on the expected spot rate which is just an expectation, hence it is exposed to fluctuations. So, the decision of hedging through a derivative instrument depends upon the pros and cons of that instrument.

Related Documents