Research on Online Retailing for Modest Fashion Part 1: Subject Research A thesis submitted to the University of Manchester for the degree of Master of Enterprise (MEnt) in the Faculty of Engineering and Physical Sciences. 2010 Nazihah Ab Mumin School of Materials

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Research on Online

Retailing for Modest

Fashion

Part 1: Subject Research

A thesis submitted to the University of Manchester for the degree of Master of Enterprise (MEnt)

in the Faculty of Engineering and Physical Sciences.

2010

Nazihah Ab Mumin

School of Materials

2

Table of Contents Abstract .............................................................................................................................................. 5

Declaration ......................................................................................................................................... 6

Copyright Statement .......................................................................................................................... 6

Chapter 1: Introduction ...................................................................................................................... 7

Chapter 2: Modesty in Clothing ......................................................................................................... 8

2.1 Introduction ........................................................................................................................ 8

2.2 Background of Modesty in Clothing ................................................................................... 8

2.2.1 History of Modesty ..................................................................................................... 8

2.2.2 History of Fashion ....................................................................................................... 9

2.2.3 Modesty Debate ....................................................................................................... 11

2.2.4 Modesty in Islam ...................................................................................................... 13

2.2.5 Islamic Cosmopolitanism ......................................................................................... 20

2.2.6 Summary .................................................................................................................. 20

2.3 Customer Behaviour ......................................................................................................... 20

2.3.1 Introduction .............................................................................................................. 20

2.3.2 The Theory of Dress and Adornment ....................................................................... 20

2.3.3 Why do women want to dress modestly? ................................................................ 23

2.3.4 Summary .................................................................................................................. 24

2.4 Current issues and trend .................................................................................................. 24

2.5 Chapter Summary ............................................................................................................. 27

Chapter 3: Online Retailing for Modest Clothing ............................................................................. 28

3.1 Introduction ...................................................................................................................... 28

3.2 E-Retailing ......................................................................................................................... 28

3.2.1 Introduction .............................................................................................................. 28

3.2.2 UK online market ...................................................................................................... 28

3.2.3 Online Shopping ....................................................................................................... 30

3.2.4 Summary .................................................................................................................. 31

3.3 Fashion Retailing Online ................................................................................................... 31

3.3.1 Online Fashion Market ............................................................................................. 31

3.3.2 Online Modest Fashion Market ................................................................................ 32

3.3.3 Summary .................................................................................................................. 32

3.4 Customer Behaviour ......................................................................................................... 32

3.4.1 Introduction .............................................................................................................. 32

3

3.4.2 Online Fashion Customer Behaviour ........................................................................ 33

3.4.3 Summary .................................................................................................................. 33

3.5 Website Design Issues ...................................................................................................... 33

3.5.1 Introduction .............................................................................................................. 33

3.5.2 Literature Review ..................................................................................................... 34

3.5.3 The Online Fashion Environment ............................................................................. 35

3.5.4 Competitors websites analysis using the Online Fashion Environment dimension . 36

3.5.5 Results and Discussion ............................................................................................. 40

3.5.6 Summary .................................................................................................................. 40

3.6 E-Marketing and E-Promotion .......................................................................................... 40

3.6.1 Introduction .............................................................................................................. 40

3.6.2 The 7 C’s : The E-Retail Marketing Mix ..................................................................... 40

3.6.3 E-Marketing Promotional Mix .................................................................................. 42

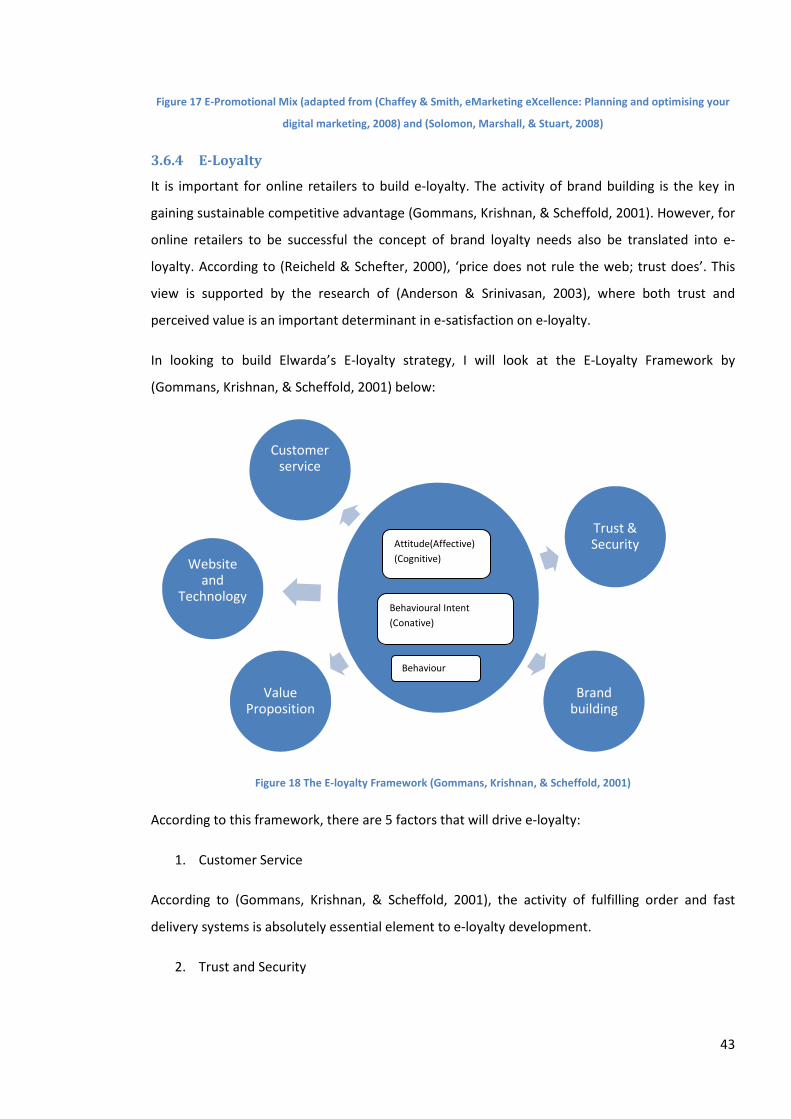

3.6.4 E-Loyalty ................................................................................................................... 43

3.7 Summary .......................................................................................................................... 44

Chapter 4: Research Method ........................................................................................................... 45

Chapter 5: Research Results ............................................................................................................. 48

5.1 Introduction ...................................................................................................................... 48

5.2 Results of research on Modesty ....................................................................................... 48

5.3 Online Retailing for Modest Clothing Results .................................................................. 51

Chapter 6: Discussion and Conclusion ............................................................................................. 58

6.1 Discussion on ‘Modesty in Clothing’ ................................................................................ 58

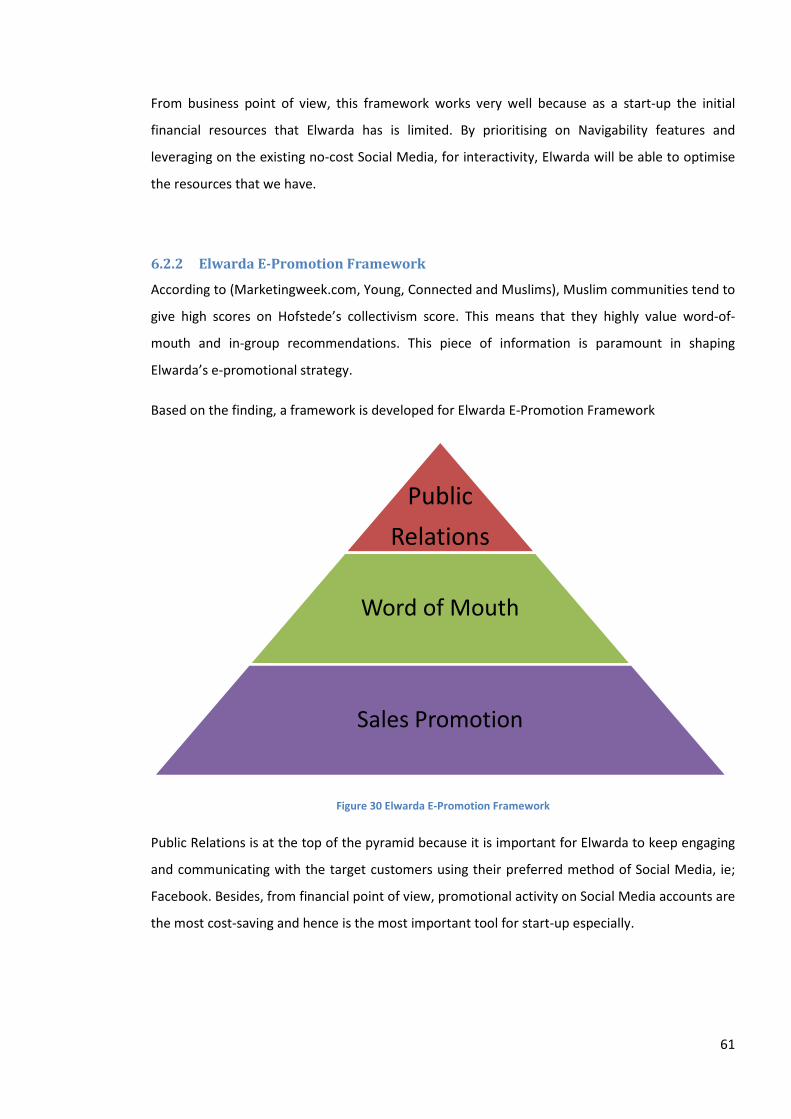

6.2 Discussion on ‘Online Retailing for Modest Clothing’ ...................................................... 60

6.2.1 Elwarda Website Design Framework ....................................................................... 60

6.2.2 Elwarda E-Promotion Framework ............................................................................ 61

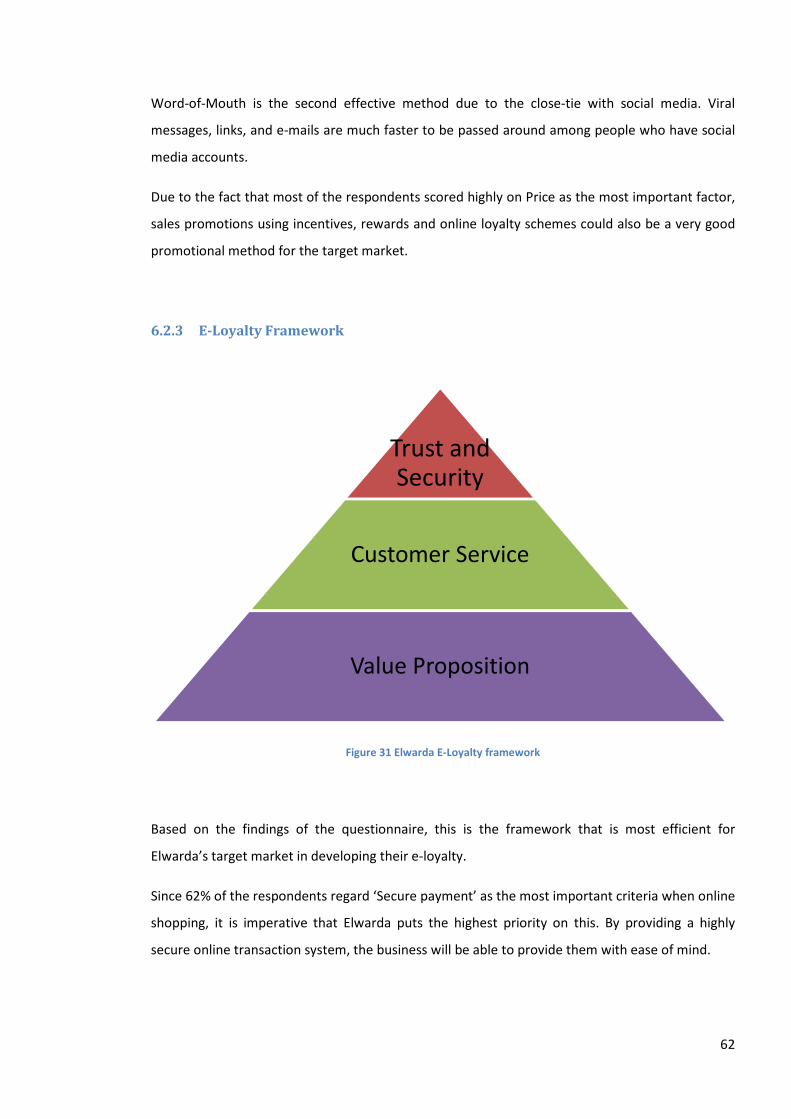

6.2.3 E-Loyalty Framework ................................................................................................ 62

6.3 Summary .......................................................................................................................... 63

Chapter 7: Conclusion and Further Research ................................................................................... 64

Works Cited ...................................................................................................................................... 65

Appendix A: Interview with Jana, Editor of Hijab Style .................................................................... 70

Word Count: 16,338

4

Table of Figures

Figure 1 Abaya .................................................................................................................................. 14

Figure 2 Papers exploring 'hijab'/veil and Islamic fashion ............................................................... 17

Figure 3 Young Indian Girl in Saree .................................................................................................. 22

Figure 4 Indian women in colourful sarees ...................................................................................... 23

Figure 5 Hana Tajima in stylish modest clothing .............................................................................. 25

Figure 6 Hana Tajima ........................................................................................................................ 26

Figure 7 E-commerce and other Home Shopping in the UK by value (£m at retail selling price)

2003-2007 ........................................................................................................................................ 29

Figure 8 bought online in the last 12 months, November 2009 Source: GMI/Mintel (Mintel Report

2010) ................................................................................................................................................ 30

Figure 9 Online Fashion Environment Dimensions, McCormick & Vazquez, 2009 .......................... 35

Figure 10 Maysaa website screenshot ............................................................................................. 37

Figure 11 Analysis of Maysaa website .............................................................................................. 37

Figure 12 Elenany website screenshot ............................................................................................. 38

Figure 13 Analysis of Elenany website ............................................................................................. 38

Figure 14 Losve website screenshot ................................................................................................ 39

Figure 15 Analysis of Losve website ................................................................................................. 39

Figure 16 The 7 C’s : The E-Retail Marketing Mix (Dennis, Fenec h, & Merrilees, 2005) ................. 42

Figure 17 E-Promotional Mix (adapted from (Chaffey & Smith, eMarketing eXcellence: Planning

and optimising your digital marketing, 2008) and (Solomon, Marshall, & Stuart, 2008) ................ 43

Figure 18 The E-loyalty Framework (Gommans, Krishnan, & Scheffold, 2001) ............................... 43

Figure 19 What influences your personal style? .............................................................................. 50

Figure 20 How many times do you shop for Modest Clothing online? ............................................ 51

Figure 21 Research findings: Design of the Website ........................................................................ 52

Figure 22 Research findings: Interactivity of the website ................................................................ 53

Figure 23 Research findings: Secure Payment ................................................................................. 54

Figure 24 Research findings: Price ................................................................................................... 54

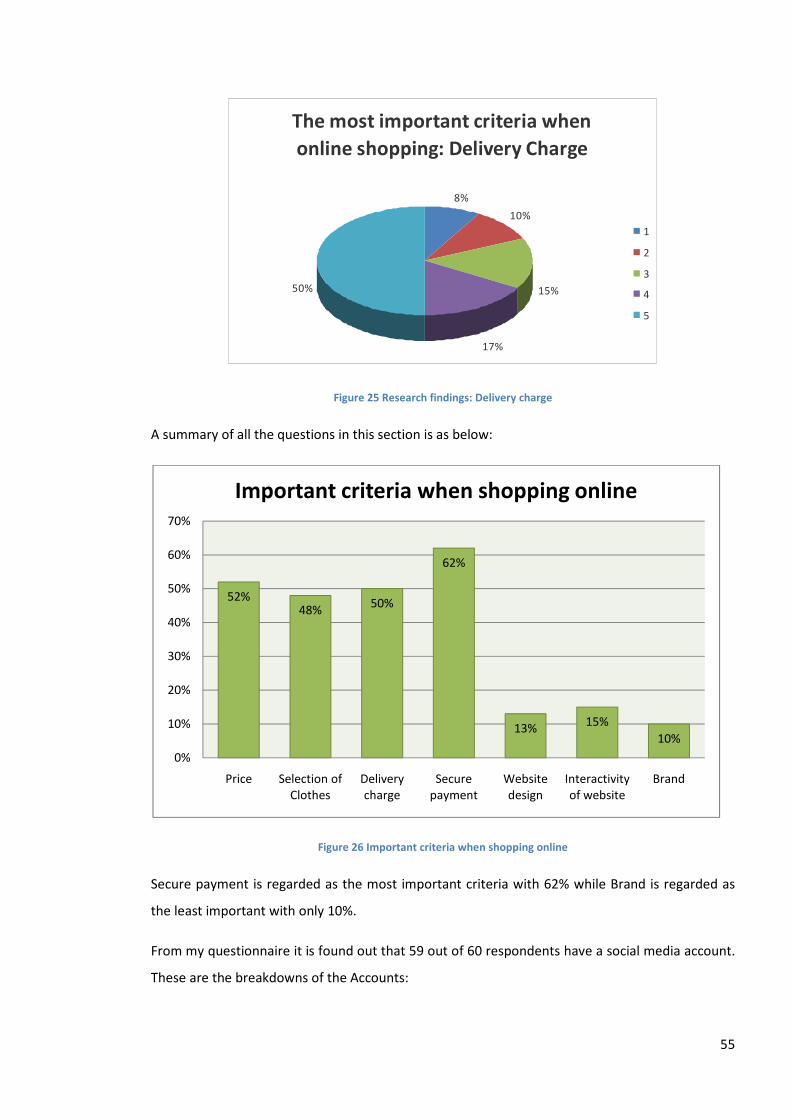

Figure 25 Research findings: Delivery charge .................................................................................. 55

Figure 26 Important criteria when shopping online ........................................................................ 55

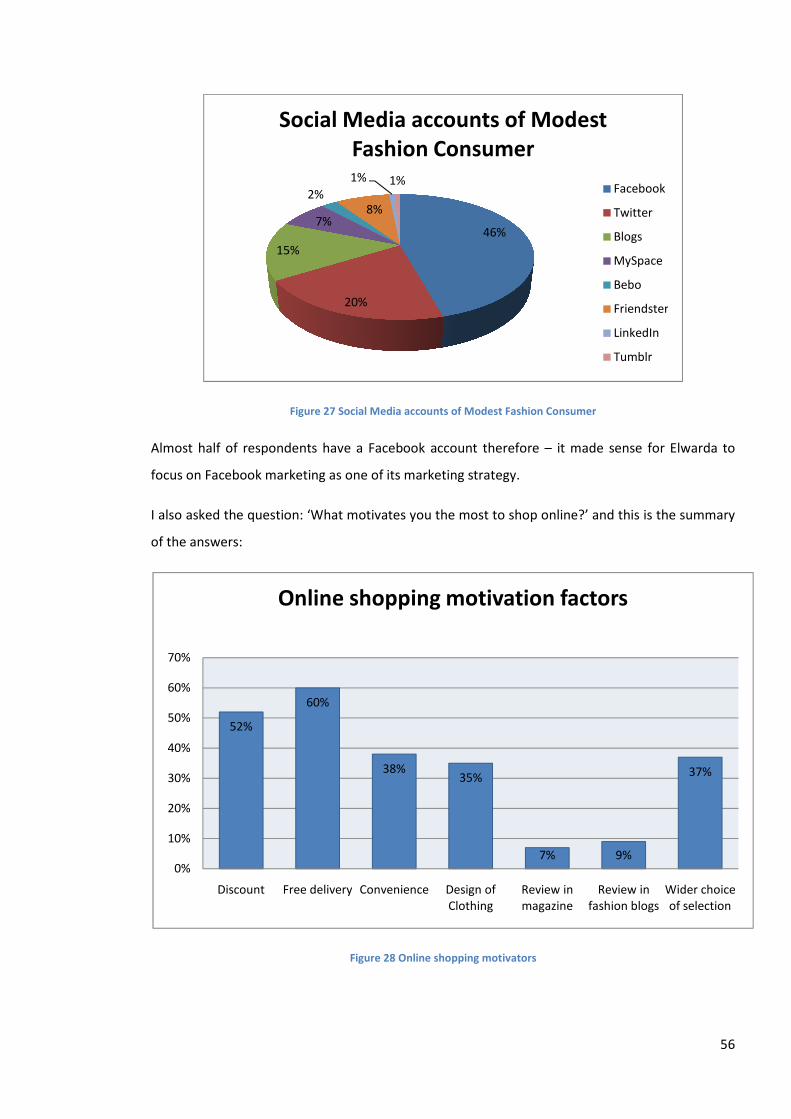

Figure 27 Social Media accounts of Modest Fashion Consumer ..................................................... 56

Figure 28 Online shopping motivators ............................................................................................. 56

Figure 29 Elwarda Website Design Framework ............................................................................... 60

Figure 30 Elwarda E-Promotion Framework .................................................................................... 61

Figure 31 Elwarda E-Loyalty framework........................................................................................... 62

5

Abstract

Modest Fashion industry is a relatively new industry that sprouted out of the effect of

globalisation on Muslim society, especially those who are residing in the Western world. With

market value in the millions, this is an interesting subject matter. Coupled with advancement in

technology that enables efficient online retailing – this is the subject matter that is going to be

researched as part of my business project.

Prepared by:

Nazihah Ab Mumin 20/10/2010

‘Research on Online Retailing for Modest Fashion’

MEnt Textiles and Fashion

The University of Manchester

6

Declaration

No portion of the work referred to in the thesis has been submitted in support of an application

for another degree or qualification of this or any other university or other institute of learning.

Copyright Statement

i. The author of this thesis (including any appendices and/or schedules to this thesis)

owns certain copyright or related rights in it (the “Copyright”) and s/he has given The

University of Manchester certain rights to use such Copyright, including for

administrative purposes.

ii. Copies of this thesis, either in full or in extracts and whether in hard or electronic

copy, may be made only in accordance with the Copyright, Designs and Patents Act

1988 (as amended) and regulations issued under it or, where appropriate, in

accordance with licensing agreements which the University has from time to time.

This page must form part of any such copies made.

iii. The ownership of certain Copyright, patents, designs, trade marks and other

intellectual property (the “Intellectual Property”) and any reproductions of copyright

works in the thesis, for example graphs and tables (“Reproductions”), which may be

described in this thesis, may not be owned by the author and may be owned by third

parties. Such Intellectual Property and Reproductions cannot and must not be made

available for use without the prior written permission of the owner(s) of the relevant

Intellectual Property and/or Reproductions.

iv. Further information on the conditions under which disclosure, publication and

commercialisation of this thesis, the Copyright and any Intellectual Property and/or

Reproductions described in it may take place is available in the University IP Policy

(see http://www.campus.manchester.ac.uk/medialibrary/policies/intellectual-

property.pdf), in any relevant Thesis restriction declarations deposited in the

University Library, The University Library’s regulations (see

http://www.manchester.ac.uk/library/aboutus/regulations) and in The University’s

policy on presentation of Theses

7

Chapter 1: Introduction

This research is part of my business idea, Elwarda, a Modest Fashion Online Retailer. This business

idea stems from my own frustration of the stereotypes of what is deemed as ‘Islamic’ fashion. The

lack of beautiful, modern and contemporary modest clothing is also another motivation for me to

explore the idea of starting the business.

The aim of this project is to find out if there is a need for modern contemporary yet modest

fashion that is linked to Islamic requirement. This question is explored in Chapter 1.

This project also aims to find out the best way to retail this modest clothing online. With the

growing number of online Islamic/Modest clothing retailer, research needs to be done to find out

what they are doing right and what they are doing wrong.

Research is done via both primary and secondary research. Questionnaire has been sent out

online to see whether there is a response for Modest Fashion and to get to know the shopping

habits of the Modest fashion consumer.

Secondary research is done in 2 parts. The first is to look at the existing issues concerning the

Islamic and Modest clothing definition. What is traditionally deemed as Islamic/Modest clothing?

How did it come about? What is the congruence between fashion and faith? Is there a room for

fashion in faith-related sphere? This is tackled in Chapter 2: Modesty in Clothing.

The next secondary research is to look at the ways of how to retail modest clothing online in the

most efficient way. By looking at various papers on online retailing (e-retailing), online marketing

and online promotion (e-marketing and e-promotion) and also into online brand loyalty (e-loyalty)

– a few frameworks for Elwarda business are developed.

8

Chapter 2: Modesty in Clothing

2.1 Introduction

In exploring the idea, I step away from calling the fashion as ‘Islamic’ but rather I use a more

general and neutral term ‘modest’. The reason is twofold: first because I believe there is no one

style that is called ‘Islamic’. Second, I want to explore the possibility for the concept to be

extended outside Muslims.

In understanding the idea of modesty behind clothing and fashion, I will look at the historical

aspects of modesty and fashion from theological and societal point of view.

The theological point of view is important since modest clothing is very closely related to religion

and faith-based decision making.

The societal point of view is to give deeper insights of the evolution of clothing and modesty

throughout human’s existence.

2.2 Background of Modesty in Clothing

2.2.1 History of Modesty

In academia, according to (Thomas, 1899) there’s no satisfactory theory of the origin of modesty.

The assumption of that nakedness is associated with shameness is refuted with the large evidence

that many of natural races are naked and not ashamed of it. (Thomas, 1899). According to

(Harms, 1938) there are 3 fundamental psychological reasons for human dress. These are for

modesty, for adornment, and for protection.

In theology, the earliest depiction of modesty in clothing is revealed in the Quran and also the

Bible, when the first man and woman, Adam and Eve went looking for leaves to cover themselves.

Quranic:

He thus duped them with lies. As soon as they tasted the tree, their bodies became visible to them, and they

tried to cover themselves with the leaves of Paradise. Their Lord called upon them: "Did I not enjoin you

from that tree, and warn you that the devil is your most ardent enemy?"(Quran 7:22)

9

Bibilical:

Then the eyes of both were opened, and they knew that they were naked; and they sewed fig leaves

together and made themselves aprons (7: Genesis 3)

Regarding modesty, theological reference of women’s modesty is also present in the text as

below:

Quranic:

“Tell the believing men to lower their gaze and be modest. That is purer for them. Lo! God is Aware of

what they do. And tell the believing women to lower their gaze and be modest, and to display of their

adornment only that which is apparent, and to draw their veils over their chests, and not to reveal their

adornment.” (Quran 24:30)

Bibilical:

3:1 Likewise, wives, be subject to your own husbands, so that even if some do not obey the word, they may

be won without a word by the conduct of their wives, 2 when they see your respectful and pure conduct.

3 Do not let your adorning be external—the braiding of hair and the putting on of gold jewelry, or the

clothing you wear— 4 but let your adorning be the hidden person of the heart with the imperishable beauty

of a gentle and quiet spirit, which in God’s sight is very precious. 5 For this is how the holy women who

hoped in God used to adorn themselves, by submitting to their own husbands, 6 as Sarah obeyed Abraham,

calling him lord. And you are her children, if you do good and do not fear anything that is frightening. (1

Peter 3:1-6)

It is interesting to note here that from there’s a definite mention of modesty in clothing in the text

of the top 2 world’s largest religion, Christianity with about 2.1 billion follower worldwide

(bbc.co.uk, Christianity) with and Islam with over 1 billion followers. (bbc.co.uk, Islam at a glance,

2009)

2.2.2 History of Fashion

In understanding modest fashion, I want to explore the position it has in the ‘fashion industry’ as

a whole. What does fashion means and how did it come into existence. In identifying these, I

looked at the history of fashion.

There are many theories that come forth to explain fashion and its evolution. These are among of

the theories:

10

Theory of the Leisure Class

Thorstein Veblen (Veblen, 1899/1953), a late nineteenth-century sociologist argues fashion is

used as a ‘tool in the battle for social status’ (Entwistle, 2000).

He also argues that women’s dresses are more influenced by this theory because the role of the

‘bourgeois lady of the house’ is to be a symbol of her master’s wealth and financial ability.

(Entwistle, 2000)

However this theory is very outdated since women nowadays mostly are in a profession

(Entwistle, 2000). This has bring forth considerable change in the way society viewed women and

their fashion style.

The theory of emulation or ‘trickle-down’

This theory argues that styles start at the top of the social class and trickle down to the classes

below who wants to emulate the style of the elites. In order to maintain their status, the elites

keep on changing their style. (Veblen, 1899/1953) and (Simmel, 1904/1971) are the main

proponent of this view.

This theory is however been opposed by (Rouse, 1989) in the occasion where the styles from

working-class or low-status groups such ‘black youth’ have become a trend.

(Partington, 1992) has stronger opinion in saying that working-class women created their own

version of the styles and it is not ‘watered down’ version of the ‘real’ thing.

The theory of Zeitgeist

This theory suggests fashion is influenced by social and political changes.

The examples of the argument that during the economic depression in 1930s the hemlines drop,

and during the economic boom in 1960, the hemlines rise. (Entwistle, 2000). The proponent of

this theory is (Ditcher, 1985)

However, this theory is argued to be over-simplistic by (Wilson, 1985) since history is much more

complex than what is represented. A quantitative study by (Richardson & Kroeber, 1973) proves

that there is no ‘conclusive evidence to suggest that social changes influenced any particular

dimension of the female silhouette’. (Entwistle, 2000)

11

The theory of ‘the shifting erogenous zone’.

One of it is the theory of ‘shifting erogenous zone’. (Laver, 1969/1995). He argues that in 1920’s

the emphasis is on the female’s leg, and in 1930’s is the female’s back. This trend keeps on

changing in order to keep up or keep enticing men’s desire.

However (Polhemus & Proctor, 1978) argued that this is not necessarily the case since the fashion

of combat trousers for women in late 1990’s does not seems to fit the erotic or revealing case.

These are theories that have been used to explain the evolution of ‘fashion’ from mainly Western

point of view. Are these theories sufficient to explain the fashion phenomenon that is more based

in faith?

In the next section I would look at what is defined as ‘modest’ clothing and how does it relate to

Islam.

2.2.3 Modesty Debate

What does it mean to dress modestly? Is more coverage means more modesty? Is it the attitude

of the wearer of the garment or is it the garment itself?

In order to get the a clearer understanding of what is deemed as modest by Muslim women in the

UK, I interviewed Jana Kossabaiti, editor of Hijab Style, an online blog for modest fashion

enthusiasts.

According to her, the traditional or cultural clothing such as abaya, sari or salwar kameez, are

clothing that is mainly worn by the first generation Muslim migrant. The second and third

generation Muslim women no longer wear them, except to go to family event or during special

celebration days. (Interview with Jana: Appendix A).

In an interview done in her paper, Emma Tarlo finds out that her interviewee, Rezia Wahid’s

mother still wears sari as her everyday garment (Tarlo, Islamic Cosmopolitanism, 2007). However,

the second generation Rezia doesn’t wear the traditional garment but rather opts for her own

personal style that is described as “fashionable, Islamic, and distinctive” (Tarlo, Islamic

Cosmopolitanism, 2007). This view is also supported by Jana, a third generation Muslim who’s

studying Medicine in London.

12

The challenge occurs when these women are trying to dress in a conventional Western fashion,

but still adhering to their own concept of modesty. This, according to Jana, that spurred the

modest fashion movement.

However, different cultures have different meanings as to what they mean as modest. In South

India, tightly bonded sari around the body means modesty, even though it bares the midriff.

(Osella & Osella, 2007). For most South Indian, all Western clothing are deemed as immodest,

although it is non-revealing. Similarly, what is modest in Islamic cultures varies from one country

and one culture to the other.

Therefore, is it fair to assume that modest means more coverage?

One of the more highlighted aspects of the modest fashion is the ‘hijab debate’. ‘Hijab’ is a term

most commonly used in Western countries to refer to the head-coverings, or head-scarves that is

worn by most Muslim Women. In academic research, a few theories have been compiled as to

why a Muslim woman wears a hijab: theories of post-colonial resistance, gender performance,

patriarchy, and the rise of global religious movements (Tarlo, Hijab in London: Metamorphosis,

Resonance and Effects, 2007).

The problem with most of these theories is that they ignore the point of view of the wearer of the

‘hijab’. While some Muslim in some countries are unfortunately unable to voice their own

opinion, most Muslim women, especially the ones living in big cities are educated middle to upper

class and they form their own decision when it comes to what they want to wear. And most of

them chose to wear the hijab and described it as empowering (Ruby, 2006)

However, in this paper (Tarlo, Hijab in London: Metamorphosis, Resonance and Effects, 2007),

Tarlo tried to move away from such theories and explored the hijab in context of ‘trans-cultural’

encounters of modern lives in big city. She suggested that that the reason Muslim women

adopted the hijab is shaped by her ‘personal biographic experience’ and is hugely impacted by her

social relationships and surroundings.

On another aspect, we can also look at modesty form gender perspective. What is modest

according to men? What is modest according to women?

When talking about modesty from different gender’s perspective, it brings to mind the view of

(Mernissi, 1987) that the custom of veiling does not stem from Islamic religion, but rather on the

social assumption that women might lead to ‘fitna’ – disorder and chaos therefore they need to

be contained.

13

While this view, according to her is in contrast of the opinion that women are weak and inferior

and need to be hidden, it doesn’t stray from the fact that both arguments centred upon man’s

opinion on what is supposed to be done to women. Either they are weak or a ‘dangerous sexual

beings’ (Kaiser, 1998) – both assumptions led to men’s desire to cloak women.

Looking at things from a different point of view, the fashion industry is also monopolised by men

designers. These men decide what looks are good for women, what is trendy, what is beautiful

and this shaped women’s attitude about what they thing as beautiful and fashionable. It is

possible that this also influences what women think as modest. Assuming that these men designs

to fit what is visually attractive to them, and assuming that men always wants women to be

minimally covered – it means that what is acceptable as modest for women is hugely distorted to

fit what men thinks as modest. And this means, very little clothing!

From these two observations, either to cover or not to cover – both decisions are largely

influenced by men’s opinion on how women should be dressing themselves.

In the next section, I would look at what modesty means from Islamic point of view.

2.2.4 Modesty in Islam

The definition of Islamic fashion is varied and dynamic. The first definition would be concerning

what is worn by Muslims. In this aspect, the Islamic Fashion varies greatly as Muslims are spread

all over the worlds and the clothing they wear is of course influenced by the culture of that

region. If we take the definition of Islamic Fashion as what is decreed in the Quran, we need to

consider the different translation and interpretation of the Quranic order. This is by no means an

easy feat as many Islamic scholars also differed in their opinion of Islamic dresscodes. These

differences in opinion among scholars and ‘hijab-wearers’ responses are documented in a

research by (Ruby, 2006) – “to what extent Muslim women need to cover is a debatable question

among scholars as well as the participants”.

Therefore, in order to decipher the scope of Modesty in Islam, I am going to look at Modestry

from two point of views: 1) The Fashion of the Followers 2) The Quranic interpretation.

First View: The fashion of followers

If we look at the first view and explore Islamic Fashion in terms of its followers, the Muslims, we

can look at these different examples of clothing style from a few different countries.

Islamic Fashion in Britain, for example,

Pakistani, India and the African continent came to the UK with their own styles o

from their culture. The ‘abaya’, and ‘salwar kameez’ is among the examples of clothi

generation Muslims immigrants in the UK.

However, the second generation British Muslims are not following the footsteps of their older

generation. According to Jana, the editor of Hijab Style, (Appendix A

British-born Muslims or the second generation Muslims are looking for ways to integrate their

faith with the Western culture in their clothing.

In the aspect of Islamic fashion, the most

Emma Tarlo wrote 2 papers about ‘hijab’ in London. The first paper, ‘Hijab in London:

Metamorphosis, Resonances and Effects’

Effects, 2007) explored the idea of ‘hijab’ being influenced and affected by ‘trans

space which exposes people to alternative ways of being and in so doing, offers them the

possibility of personal metamorpho

looks at the lives of 3 Muslim women in trying to understand why they wear the ‘hijab’.

Below are a table of various academic papers researching the different issu

Muslim women from all over the world.

Figure 1 Abaya

Islamic Fashion in Britain, for example, is shaped mainly by its immigrants.

Pakistani, India and the African continent came to the UK with their own styles o

from their culture. The ‘abaya’, and ‘salwar kameez’ is among the examples of clothi

mmigrants in the UK.

However, the second generation British Muslims are not following the footsteps of their older

tion. According to Jana, the editor of Hijab Style, (Appendix A: Interview with Jana

born Muslims or the second generation Muslims are looking for ways to integrate their

faith with the Western culture in their clothing.

amic fashion, the most debated topic is concerning the headscarf or ‘hijab’.

Emma Tarlo wrote 2 papers about ‘hijab’ in London. The first paper, ‘Hijab in London:

Metamorphosis, Resonances and Effects’ (Tarlo, Hijab in London: Metamorphosis, Resonance and

explored the idea of ‘hijab’ being influenced and affected by ‘trans

space which exposes people to alternative ways of being and in so doing, offers them the

ity of personal metamorphosis’. The second paper, (Tarlo, Islamic Cosmopolitanism, 2007)

looks at the lives of 3 Muslim women in trying to understand why they wear the ‘hijab’.

Below are a table of various academic papers researching the different issu

Muslim women from all over the world.

14

is shaped mainly by its immigrants. Muslims from

Pakistani, India and the African continent came to the UK with their own styles of dressing, based

from their culture. The ‘abaya’, and ‘salwar kameez’ is among the examples of clothing of first

However, the second generation British Muslims are not following the footsteps of their older

: Interview with Jana), the

born Muslims or the second generation Muslims are looking for ways to integrate their

debated topic is concerning the headscarf or ‘hijab’.

Emma Tarlo wrote 2 papers about ‘hijab’ in London. The first paper, ‘Hijab in London:

etamorphosis, Resonance and

explored the idea of ‘hijab’ being influenced and affected by ‘trans-cultural city as a

space which exposes people to alternative ways of being and in so doing, offers them the

(Tarlo, Islamic Cosmopolitanism, 2007)

looks at the lives of 3 Muslim women in trying to understand why they wear the ‘hijab’.

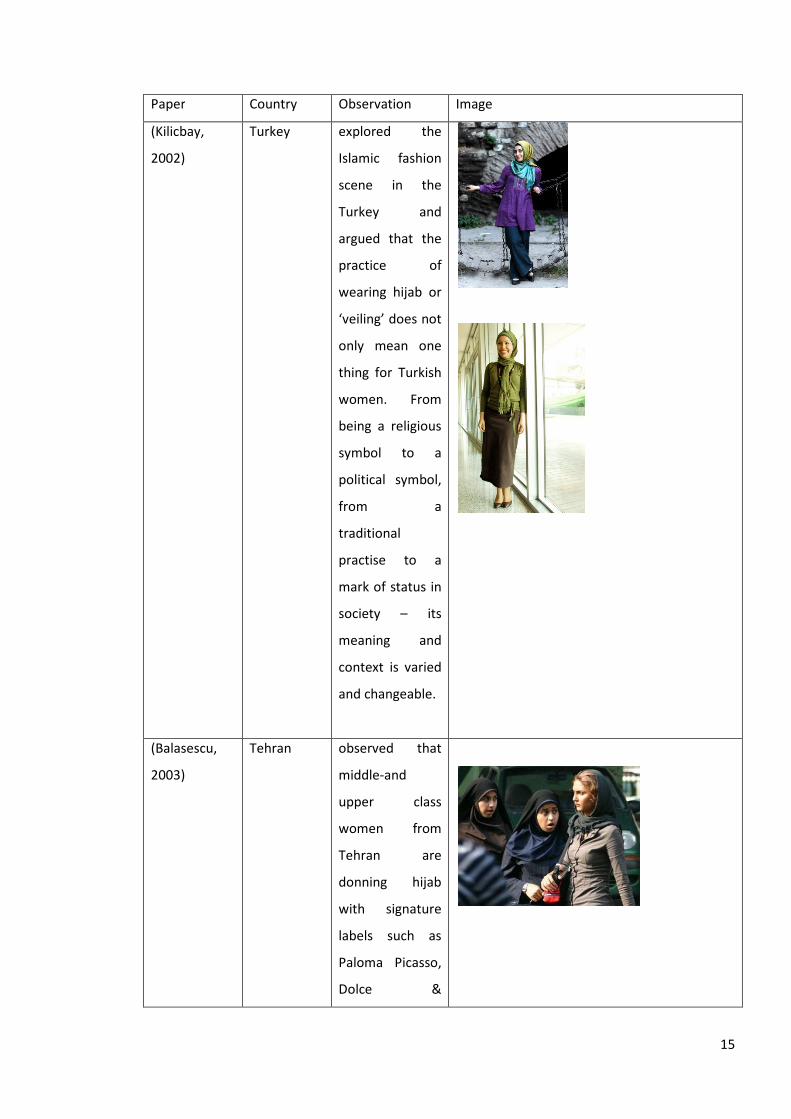

Below are a table of various academic papers researching the different issues and styles of

15

Paper Country Observation Image

(Kilicbay,

2002)

Turkey explored the

Islamic fashion

scene in the

Turkey and

argued that the

practice of

wearing hijab or

‘veiling’ does not

only mean one

thing for Turkish

women. From

being a religious

symbol to a

political symbol,

from a

traditional

practise to a

mark of status in

society – its

meaning and

context is varied

and changeable.

(Balasescu,

2003)

Tehran observed that

middle-and

upper class

women from

Tehran are

donning hijab

with signature

labels such as

Paloma Picasso,

Dolce &

16

Gabbana and

Yves Saint

Laurent

(Brenner,

1996) and

(Jones, 2007)

Java,

Indonesia

and Urban

Indonesia

‘busana

muslimah’

(clothing of the

Muslim women)

Long-sleeved

and floor-length

garments

Loose or fitted

head covering

(Read, 2000) Austin,

Texas

(Moors,

2007)

San’a,

Yemen

“Most San`ani

women appear

in public

completely

covered in black,

often including a

face-veil.”

(Osella &

Osella, 2007)

South India “pardah, or long

and loose salwar

kameezes

carefully teamed

with matching

mafta

(headscarves)”

17

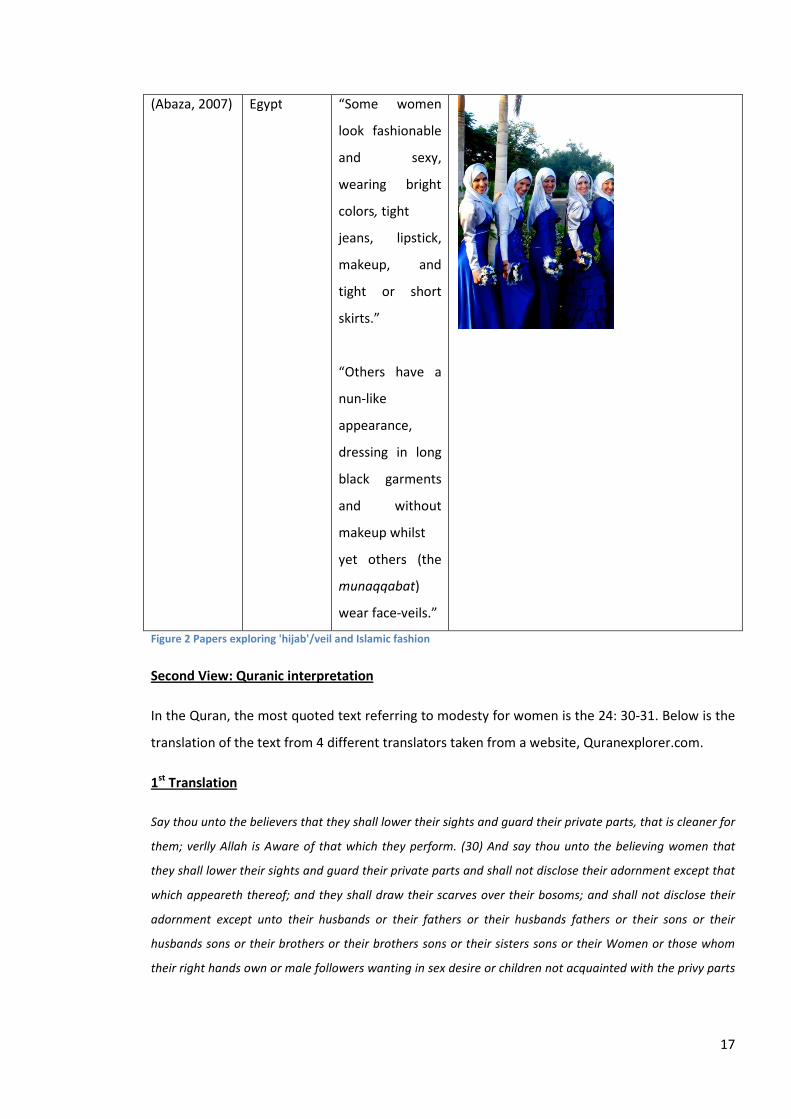

(Abaza, 2007) Egypt “Some women

look fashionable

and sexy,

wearing bright

colors, tight

jeans, lipstick,

makeup, and

tight or short

skirts.”

“Others have a

nun-like

appearance,

dressing in long

black garments

and without

makeup whilst

yet others (the

munaqqabat)

wear face-veils.”

Figure 2 Papers exploring 'hijab'/veil and Islamic fashion

Second View: Quranic interpretation

In the Quran, the most quoted text referring to modesty for women is the 24: 30-31. Below is the

translation of the text from 4 different translators taken from a website, Quranexplorer.com.

1st

Translation

Say thou unto the believers that they shall lower their sights and guard their private parts, that is cleaner for

them; verlly Allah is Aware of that which they perform. (30) And say thou unto the believing women that

they shall lower their sights and guard their private parts and shall not disclose their adornment except that

which appeareth thereof; and they shall draw their scarves over their bosoms; and shall not disclose their

adornment except unto their husbands or their fathers or their husbands fathers or their sons or their

husbands sons or their brothers or their brothers sons or their sisters sons or their Women or those whom

their right hands own or male followers wanting in sex desire or children not acquainted with the privy parts

18

of women; and they Shall not strike their feet so that there be known that which they hide of their

adornment. And turn penitently unto Allah ye all, O ye believers, haply ye may thrive! (31)

- Translation by Abdul Daryabadi (Quranexplorer.com)

2nd

Translation

Tell the believing men to lower their gaze (from looking at forbidden things), and protect their private parts

(from illegal sexual acts). That is purer for them. Verily, Allâh is All-Aware of what they do. (30) And tell the

believing women to lower their gaze (from looking at forbidden things), and protect their private parts (from

illegal sexual acts) and not to show off their adornment except only that which is apparent (like both eyes

for necessity to see the way or outer dress like veil, gloves, head-cover, apron, etc.), and to draw their veils

all over Juyubihinna (i.e. their bodies, faces, necks and bosoms,) and not to reveal their adornment except to

their husbands, or their fathers, or their husband's fathers, or their sons, or their husband's sons, or their

brothers or their brother's sons, or their sister's sons, or their (Muslim) women (i.e. their sisters in Islâm), or

the (female) slaves whom their right hands possess, or old male servants who lack vigour, or small children

who have no sense of the feminine sex. And let them not stamp their feet so as to reveal what they hide of

their adornment. And all of you beg Allâh to forgive you all, O believers, that you may be successful[] (31)

- Translation by Dr. Mohsin (Quranexplorer.com)

3rd

Translation

Tell the believing men to lower their gaze and be modest. That is purer for them. Lo! Allah is aware of what

they do. (30) And tell the believing women to lower their gaze and be modest, and to display of their

adornment only that which is apparent, and to draw their veils over their bosoms, and not to reveal their

adornment save to their own husbands or fathers or husbands' fathers, or their sons or their husbands' sons,

or their brothers or their brothers' sons or sisters' sons, or their women, or their slaves, or male attendants

who lack vigour, or children who know naught of women's nakedness. And let them not stamp their feet so

as to reveal what they hide of their adornment. And turn unto Allah together, O believers, in order that ye

may succeed. (31)

- Translation by Pickthal (Quranexplorer.com)

4th

Translation

Say to the believing men that they should lower their gaze and guard their modesty: that will make for

greater purity for them: and Allah is well acquainted with all that they do. (30) And say to the believing

women that they should lower their gaze and guard their modesty; that they should not display their beauty

and ornaments except what (ordinarily) appear thereof; that they should draw their veils over their bosoms

and not display their beauty except to their husbands, their fathers, their husbands' fathers, their sons, their

19

husbands' sons, their brothers, or their brothers' sons, or their sisters' sons, or their women, or the slaves

whom their right hands possess or male servants free of physical needs, or small children who have no sense

of the shame of sex; and that they should not strike their feet in order to draw attention to their hidden

ornaments. And O ye Believers! Turn ye all together towards Allah that ye may attain Bliss. (31)

- Translation by Yusuf Ali (Quranexplorer.com)

Qur'an 24:30-31

The challenge in understanding the Quranic interpretation stems from the fact that Quran was

revealed in Arabic. For most Muslims who do not understand Arabic, they relied a lot on the

translation of the text. A long and complicated debate has always surrounded the translation of

the Quran. Most of the translators of the Quran are men, as stated in the above examples, and it

is almost impossible to find a woman translator of Quran due to the male dominance in the

traditional Islamic scholar institution. Therefore the biggest challenge concerning the issue of

modesty in Islam nowadays stem from a biased interpretation of the Quran by mainly men-

dominated scholars and institution.

This bias has framed women as ‘threat’, ‘fitnah’ (Hoffman-Ladd, 1987). This allegation has also

brought upon the culture of segregation and separation between men and women.

In fact what happen is men are shunning their responsibility and putting it all upon the women.

When in fact, in the Quran, what first mentioned in the verse concerning modesty is to ask men to

lower their gaze, before ordering women to dress modestly. This shows that the responsibility of

safe-guarding modesty and public safety is upon both men and women, and perhaps more on the

men because they are mentioned first.

Without going too much into the politic of religion, it is clear that there are limited resources in

understanding the Quranic interpretation due to the limitation in translators.

One interesting debate about the Quranic order of modesty is that in one of the translations, it is

ordered for women ‘to cover their bosom’. An interesting observation is put forward by Entwistle

(2000), that professional women wear jackets to go in meeting to cover the breasts as to avoid

sexual glances.

This suggests an innate need for women to cover what is of sexual nature of them to be respected

and treated professionally by men. In this instance, it can be said that this professional women,

also do dress modestly in the context of their professional space.

20

2.2.5 Islamic Cosmopolitanism

What really interests me is the term ‘Islamic Cosmopolitanism’ that is coined by Emma Tarlo in

her paper ‘Islamic Cosmopolitanism: The Sartorial Biographies of Three Muslim Women in

London’. (Tarlo, Islamic Cosmopolitanism, 2007). In this paper, she looked at the life of 3

prominent Muslim women in Britain, and sees what influences their personal style.

What Emma is proposing is that these women are adopting an Islamic Cosmopolitanism approach

in their clothing. Cosmopolitanism linking the ideas of “hybridity, pluralistic dialogue, and

openness to the world of others”. (Tarlo, Islamic Cosmopolitanism, 2007)

Therefore the term Islamic Cosmopolitanism is as interesting ‘term’ that very aptly describes my

target market.

2.2.6 Summary

To define what is ‘modest’ is by no means an easy feat. With limited understanding and research,

this term is still very new in literature. Therefore, I will explore this term by going directly to the

sources – my target market.

2.3 Customer Behaviour

2.3.1 Introduction

In researching the target market, I want to see the main motivation behind the customer

behavior. In order to understand the need of the target market, I need to understand the

underlying motivation behind their action. What motivates them to wear modest clothing? What

are the factors that influenced their decision? In finding the answers I look at the theory of dress

from anthropological point of view. I also asked them a question in my questionnaire to uncover

the reason what influences their dressing style.

2.3.2 The Theory of Dress and Adornment

From anthropological point of view, there are a few theories why human being dress and adorn

themselves:

21

Theory of Protection

One of the most basic is theory is that human being wants to be protected by the natural

elements. (Entwistle, 2000). However, the theory is debatable because as observed in a western

and some non-western cultures, skimpy clothes are still worn in a very cold climate in name of

fashion. This view is argued by (Rouse, 1989) that people survive in extreme environment and

temperatures in limited protection from clothing. This view also seems to overlook the fact that

most styles of clothing are impractical and uncomfortable to the wearer (Polhemus & Proctor,

1978) and (Rouse, 1989).

Theory of Modesty

This theory argues that clothes are

However, this view is contested

‘relative to social context’. What is considered modest in some

cultures.

For example, Hindu women in Kerala finds sleeveless sari blouse and Western dress to be

‘immodest’, while Muslim women in Kerala finds the wearing of sari itself is immodest.

Osella, 2007). The Hindu women might find Western clothing as immodest because of the

unbounded quality of the dress. In the Hindu culture, bondage as represented by the wrapping of

the sari around women’s body is modest and decent. From Muslim point of view, the tightness i

the blouse is indecent because

is theory argues that clothes are worn to cover the sexual body parts

However, this view is contested by (Rouse, 1989) stating that the idea of modesty and shame is

‘relative to social context’. What is considered modest in some cultures

For example, Hindu women in Kerala finds sleeveless sari blouse and Western dress to be

‘immodest’, while Muslim women in Kerala finds the wearing of sari itself is immodest.

Hindu women might find Western clothing as immodest because of the

unbounded quality of the dress. In the Hindu culture, bondage as represented by the wrapping of

the sari around women’s body is modest and decent. From Muslim point of view, the tightness i

the blouse is indecent because it reveals the body shape of the women.

Figure 3 Young Indian Girl in Saree

22

worn to cover the sexual body parts (Entwistle, 2000).

stating that the idea of modesty and shame is

cultures is not the same in other

For example, Hindu women in Kerala finds sleeveless sari blouse and Western dress to be

‘immodest’, while Muslim women in Kerala finds the wearing of sari itself is immodest. (Osella &

Hindu women might find Western clothing as immodest because of the

unbounded quality of the dress. In the Hindu culture, bondage as represented by the wrapping of

the sari around women’s body is modest and decent. From Muslim point of view, the tightness in

it reveals the body shape of the women.

Theory of Display

(Flugel, 1930) argues that clothing as a function of decoration and

the theory of protection and modesty. The argument is that clothes are worn to make us more

sexually attractive, not less.

Theory of Communication

The last theory for clothing and adornment stems from human’s desire to communicate using

symbols (Entwistle, 2000)

This theory is both well

2000).

Again, similar to the theory of fashion that is discussed in section 2.2.2

these theories do not explore the possible influence of faith and religion.

2.3.3 Why do women want

According to (Entwistle, 2000)

why it was neglected is not very clear, however one theory is that sociology tend to ‘focus on

action and rationality’.

Western society viewed body decoration and adornment as of minimal importance and not

worthy of ‘serious analysis’

is not neutral because it includes the idealised version of the subject

Figure 4 Indian women in colourful sarees

argues that clothing as a function of decoration and display is more significant than

the theory of protection and modesty. The argument is that clothes are worn to make us more

sexually attractive, not less.

Theory of Communication

theory for clothing and adornment stems from human’s desire to communicate using

(Entwistle, 2000).

This theory is both well-received by anthropologist on dress and fashion theorists

Again, similar to the theory of fashion that is discussed in section 2.2.2

not explore the possible influence of faith and religion.

do women want to dress modestly?

(Entwistle, 2000), sociology has largely neglected the research of fashion. The reason

why it was neglected is not very clear, however one theory is that sociology tend to ‘focus on

action and rationality’. (Entwistle, 2000). Also, as suggested by (Polhemus & Proctor, 1978)

Western society viewed body decoration and adornment as of minimal importance and not

worthy of ‘serious analysis’. The representation of fashion and dress from

is not neutral because it includes the idealised version of the subject (Entwistle, 2000)

23

display is more significant than

the theory of protection and modesty. The argument is that clothes are worn to make us more

theory for clothing and adornment stems from human’s desire to communicate using

received by anthropologist on dress and fashion theorists (Entwistle,

Again, similar to the theory of fashion that is discussed in section 2.2.2 (History of Fashion), all

not explore the possible influence of faith and religion.

the research of fashion. The reason

why it was neglected is not very clear, however one theory is that sociology tend to ‘focus on

(Polhemus & Proctor, 1978)

Western society viewed body decoration and adornment as of minimal importance and not

. The representation of fashion and dress from historical point of view

(Entwistle, 2000).

24

Fashion also has always been treated with prejudice (Entwistle, 2000). Being associated with

triviality, frivolousness, wastefulness, irrationality and vanity – all these negative attributes did

not help much in the research of fashion from sociology point of view.

The argument that is prevalent when talking about clothing and fashion is that - ironically it

always exclude the ‘body’ ie. the wearer. Many academic articles talked about clothing and

fashion in respect to social culture, political influence, history and such – but rarely, do they go

and ask people on the street why they wear what they wear.

(Entwistle, 2000) covers this topic greatly in her book, the Fashioned Body.

Perhaps this is why there is minimal research done on why women dress they way they dress.

Specifically to my research - why do women dress modestly?

2.3.4 Summary

This section has uncovered that there is not enough resources and research that is done in

understanding the motivation behind how and why women wants to dress themselves in the way

that they do. Therefore, the motivation behind why women want to dress modestly is still left

unexplored in literature and academia.

2.4 Current issues and trend

Fashionability and modesty- Is this a concept that can exist together?

What is fashionable? Does fashionability has an impact on modesty? Does less skin means more

fashionable? Can one be modestly covered, and yet be fashionable?

Fashion such a fleeting concept that changes with time and season. ‘One day you are in, the next

day you are out’, is the quote from the television show ‘Project Runway’ that very aptly described

the whole nature of fashion. Therefore, it is challenging to pin down what really is fashionable?

According to (Balasescu, 2003), the idea that ‘veiling’ is not from a ‘Western’ space - and fashion,

historically belongs to the Western has brought forth the idea that veiling is not fashion. He

however argued that this observation is not accurate.

Maybe the closest concept that can be applied to

being current; being fresh and new. Therefore, if we look at this definition, being fashionable does

not mean being less modest.

The emergence of designers from the Middle East and the Islamic countries has

new dimensions in fashion. When the

exciting to see how the word ‘fashionable’ will evolve.

Maybe the closest concept that can be applied to define what is ‘fashionable

eing fresh and new. Therefore, if we look at this definition, being fashionable does

not mean being less modest.

The emergence of designers from the Middle East and the Islamic countries has

new dimensions in fashion. When the industry is now being influenced by other culture, it is

exciting to see how the word ‘fashionable’ will evolve.

Figure 5 Hana Tajima in stylish modest clothing

25

fashionable’ is the concept of

eing fresh and new. Therefore, if we look at this definition, being fashionable does

The emergence of designers from the Middle East and the Islamic countries has brought forth

industry is now being influenced by other culture, it is

But the question is, how well received will this new designers be? How much will they be able to

impact an industry?

According to an interview by BBC, Hana, a Muslim fashion

fashion wearable and relevant’ to Muslim wome

fashions. bbc.co.uk). The fact is there are many Muslim women nowadays who are not part of the

stereotypes of ‘Muslim women’

of Muslim women who are educated, worldly and

part and parcel of that world. They want

the same time maintaining what’s im

By answering these questions that

working on converging the mainstream fashion with the basic principle of modesty.

Figure 6 Hana Tajima

But the question is, how well received will this new designers be? How much will they be able to

According to an interview by BBC, Hana, a Muslim fashion designer wishes

fashion wearable and relevant’ to Muslim women. (Muslim designers mix hijab with the latest

The fact is there are many Muslim women nowadays who are not part of the

stereotypes of ‘Muslim women’ - oppressed, cloaked in black and silent. There is a g

of Muslim women who are educated, worldly and living in the modern world where fashion is a

art and parcel of that world. They want to participate in that mainstr

the same time maintaining what’s important for them – their identity and their

y answering these questions that the value and design philosophy of Elwarda is shaped. By

working on converging the mainstream fashion with the basic principle of modesty.

26

But the question is, how well received will this new designers be? How much will they be able to

designer wishes to ‘make mainstream

(Muslim designers mix hijab with the latest

The fact is there are many Muslim women nowadays who are not part of the

ppressed, cloaked in black and silent. There is a growing group

living in the modern world where fashion is a

ream fashion idea while at

their identity and their modesty.

the value and design philosophy of Elwarda is shaped. By

working on converging the mainstream fashion with the basic principle of modesty.

27

2.5 Chapter Summary

Modest Fashion is a new and interesting subject matter. Not quite certain of its position in the

traditional/conventional fashion environment, much research still needs to be done in the area of

Modest Fashion.

Academic theories explaining fashion, dress and adornment largely ignores the function of faith –

these left many questions unanswered as a big aspect of my idea of modest clothing is based in

faith.

However, even with the lack of resources and understanding, the modest fashion industry is

growing and these will be explored in the next chapter.

28

Chapter 3: Online Retailing for Modest Clothing

3.1 Introduction

This chapter will explore the concept of E-Retailing, online Market in the UK and online retailing

for fashion in general and online retailing for modest fashion in specific.

By looking at existing competitor’s websites and referring to literature, it is hoped that a

framework could be established as the end result.

3.2 E-Retailing

3.2.1 Introduction

E-Retailing is a short-form for internet retailing; described as the retailing process of goods and

services that is done via the internet.

One of the earliest definitions of e-retailing is:

“a form of shopping in which some form of electronic communications technology is used at the

offering, ordering and/or payment stage” (McGoldrick, 1990)

E-retailing is an activity undertaken by consumers to access retailers’ websites and this may or

may not lead to the final purchase of the products or services (Smith and Chaffey, 2008) In

dissecting this definition, it is clear that the company’s website not only be purely transactional.

3.2.2 UK online market

According to (Mintel Report, E-Commerce, 2010) total e-commerce sales were £17.8 billion (excl

VAT) in 2009, which accounts for 6.6% of all retail sales. It is predicted that the growth from

online sales will outperformed all retail sales, reaching £27 billion (excl VAT) by 2014, by which it

will account for 9.1% of all retail sales.

Sector growth is also very promising with 13% in 2009, a huge difference between the rest of the

retailing sector which stands at 4%.

According to (Mintel Report, E-Commerce, 2010) 90% of those with Internet connections say they

have bought something in the last year. Despite the recession, people were buying more online

29

with 42% saying they have bought more last year compared to 16% who said they have bought

less. (Mintel Report, E-Commerce, 2010).

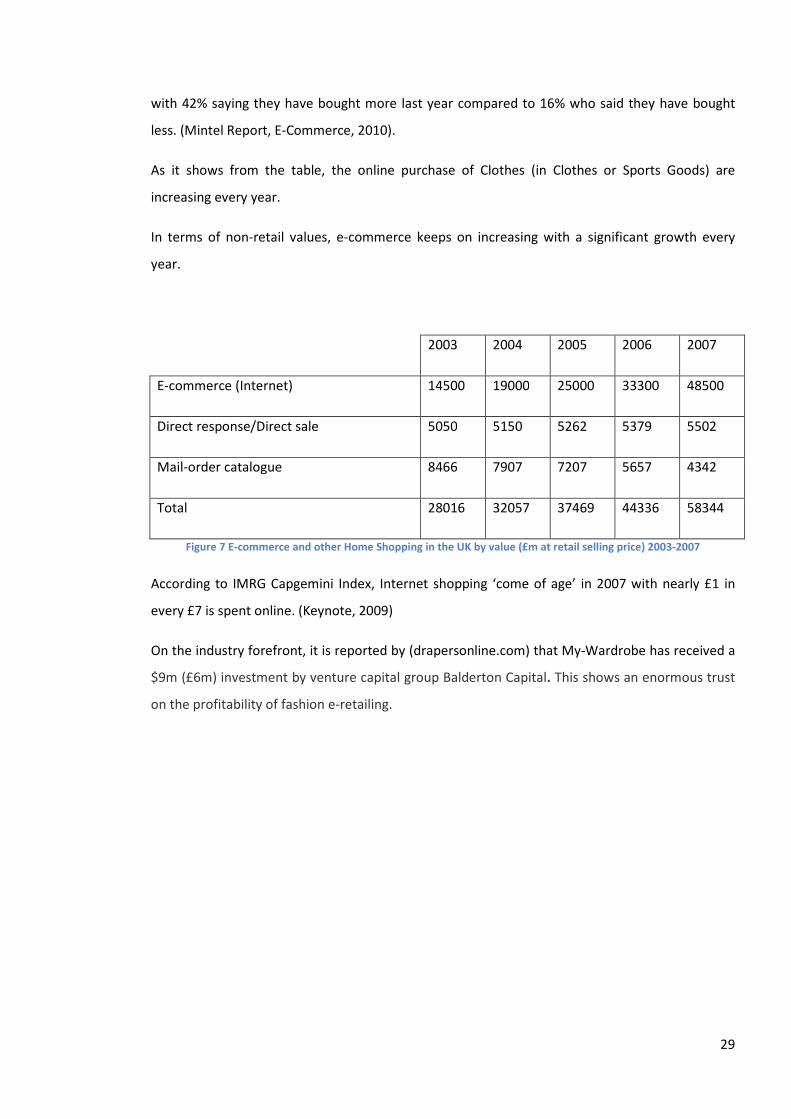

As it shows from the table, the online purchase of Clothes (in Clothes or Sports Goods) are

increasing every year.

In terms of non-retail values, e-commerce keeps on increasing with a significant growth every

year.

2003 2004 2005 2006 2007

E-commerce (Internet) 14500 19000 25000 33300 48500

Direct response/Direct sale 5050 5150 5262 5379 5502

Mail-order catalogue 8466 7907 7207 5657 4342

Total 28016 32057 37469 44336 58344

Figure 7 E-commerce and other Home Shopping in the UK by value (£m at retail selling price) 2003-2007

According to IMRG Capgemini Index, Internet shopping ‘come of age’ in 2007 with nearly £1 in

every £7 is spent online. (Keynote, 2009)

On the industry forefront, it is reported by (drapersonline.com) that My-Wardrobe has received a

$9m (£6m) investment by venture capital group Balderton Capital. This shows an enormous trust

on the profitability of fashion e-retailing.

30

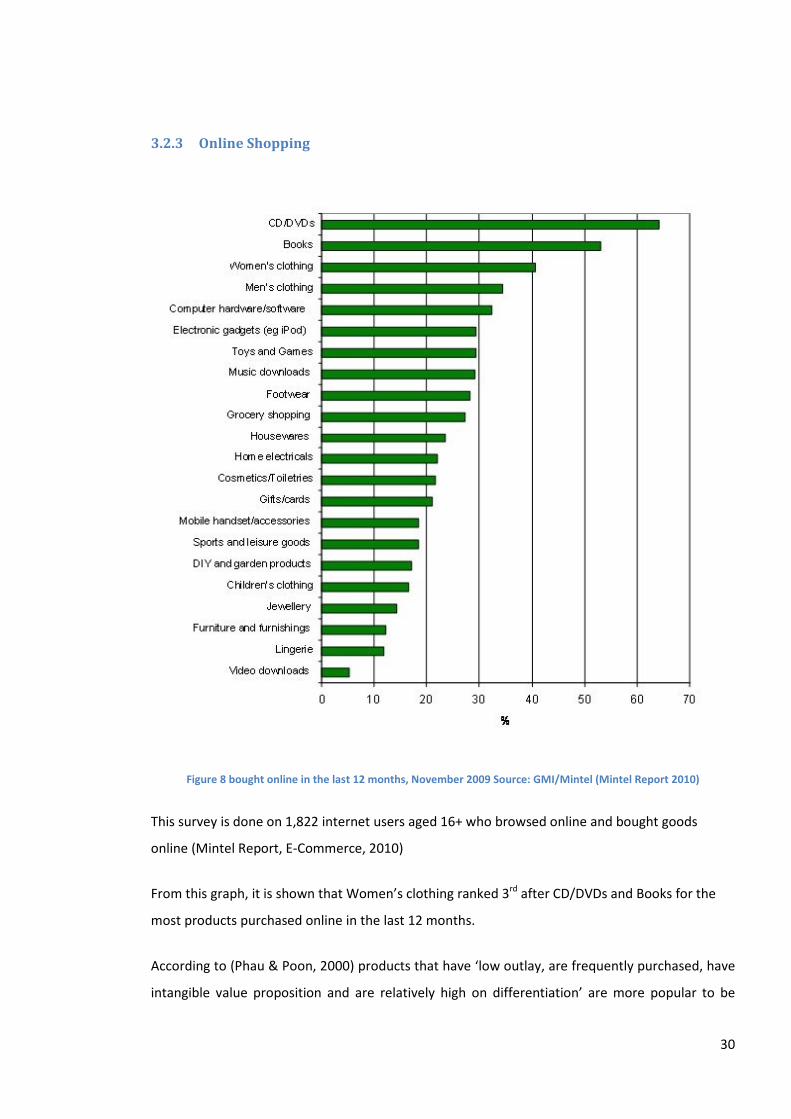

3.2.3 Online Shopping

Figure 8 bought online in the last 12 months, November 2009 Source: GMI/Mintel (Mintel Report 2010)

This survey is done on 1,822 internet users aged 16+ who browsed online and bought goods

online (Mintel Report, E-Commerce, 2010)

From this graph, it is shown that Women’s clothing ranked 3rd after CD/DVDs and Books for the

most products purchased online in the last 12 months.

According to (Phau & Poon, 2000) products that have ‘low outlay, are frequently purchased, have

intangible value proposition and are relatively high on differentiation’ are more popular to be

31

purchased online. This research is supported by the graphs above, where CD/DVDs and Books

being the items that fits the description.

However, this graph contradicts with the research that online shoppers prefer to purchase items

that doesn’t have sizing requirement (Phau and Poon 2000). This might due to the fact that this

research is done in 2000, where there’s limited technology to make purchasing clothing online

viable. With recent software and internet development, fashion retailers has managed to make

shopping for clothes online popular.

3.2.4 Summary

Online commerce or e-commerce is a booming market and is still growing despite the recession.

In the next section, I will look at the online fashion retail industry.

3.3 Fashion Retailing Online

3.3.1 Online Fashion Market

Fashion retailing online has shown a significant growth over the last few years. New online

fashion retailers that keep cropping up is a sign that apparel is significant contributor (Murphy,

1999). According to (Krantz, 1998) in the US and several other countries, apparel has shown to

one of the largest online merchandise categories. The online sales growth in Europe is driven by

multi-channel retailing (Cox, 2002).

Pure-play retailers (clothing retailers that operates purely online without physical store), such as

ASOS and Net-a- Porter has been showing strong growth. The number of online shoppers who

shopped in ASOS for the last 6 months has gone up to 32% from the previous year at the end of

October 2009 (Mintel Report, Fashion Online , 2010). While Net-a-Porter’s sales rose by 20% to

£53.2 million in the half year to August 1, 2009. (Mintel Report, Fashion Online , 2010)

For 2010, Mintel is predicting a growth of 8.2%, bringing the market to a total of £4.27 billion.

(Mintel Report, Fashion Online , 2010)

32

3.3.2 Online Modest Fashion Market

The online modest fashion market is increasing at a rapid speed. Mainly led by Islamic clothing

companies, these online retailers have found a way to tap the opportunity in online retailing.

With the advancement of technology boosted by social media, the modest fashion online retailers

are finding new ways and new markets every day.

From a market research done by JWT (Life and Times of Modern Muslims: Understanding the

Islamic Consumers, 2008), the market for female Islamic clothing is valued at $250 million.

According to Kamarul Aznam, a Malaysian-based managing editor of the bimonthly The Halal

Journal, the global market for modest clothing, assuming that 50% of the worlds’s 1.6 billion

Muslims are dressing modestly – the market is worth at least $96 billion a year. (Young, 2007)

According to him again, as the European countries such as UK and France have higher purchasing

power parity, with estimation of clothing spending $600 per year – the figure could be around $90

million to $450 million a year. (Young, 2007)

Based on that calculation, the 16 million Muslims in the EU Muslim clothing market is estimated

to be worth US$960 million a year to $4.8 billion a year. (Young, 2007)

3.3.3 Summary

Based on the market research above, modest fashion market, geared in the Muslim market seems

to have high potential. This shows that there is a definite interest and gaining awareness of the

modest fashion in the world today.

3.4 Customer Behaviour

3.4.1 Introduction

In developing an effective brand strategy for Elwarda I need to identify the customer behavior of

online modest fashion consumer. Through literature review I managed to characterise the

behaviour of online apparel shoppers. And through my questionnaire I have sharpened the

findings to fit specifically the modest fashion consumers.

33

3.4.2 Online Fashion Customer Behaviour

Research from (Goldsmith & Goldsmith, Buying apparel over the internet, 2002) found out that

online apparel buyers associate positively with buying apparel over the internet. They are also

purchasing more on the internet compared to non-apparel buyers. They were characterized as

being more innovative, knowledgeable and confident in their ability to purchase online.

According to (Phau & Lo, 2004) online apparel shoppers exhibit strong characteristic of

impulsiveness. Supporting this research (Cowart & Goldsmith, 2007) that finds out that it’s the

impulsive shoppers that spend more for apparel online on monthly basis. Although it has to be

note that the result of (Cowart & Goldsmith, 2007) research might not be representative of the

whole online shoppers demographics as the survey is done specifically on college students.

Another bias that might be present is the fact that half of the survey done is on male students.

Another important finding of (Cowart & Goldsmith, 2007) study is that value-conscious consumers

are the most reluctant to shop for apparel online.

3.4.3 Summary

The findings above shone an interesting insight into the online fashion customer behaviour. But I

need to apply the findings with caution to my business ideas since the target market of Elwarda

might behave differently from the behaviour of conventional fashion consumer. The next I will

explore the website design aspects of the e- business.

3.5 Website Design Issues

3.5.1 Introduction

Website is one of the main factors for online retailers. Especially for pure-play retailers (retailers

that only operates online without physical shop), website is the only reference customers can

have about the companies. Multi-channel retailers have better advantage as the physical business

is the starting point of customers, while the online website is deemed as the extension of their

operation.

Therefore, it is imperative for pure-play retailers to get it right when it comes to website design.

This is what I will be researching for my Elwarda business website.

34

I have compiled a list of modest clothing online retailers as part of my research. However, I

focused on a few companies that is closest to my company in terms of their clothing design and

business philosophy.

3.5.2 Literature Review

A research has been done by (Kim & Stoel, 2004) to determine what websites quality actually

contributes to customer satisfaction. Three factors came as the most significant: ‘informational

fit-to-task’, ‘transaction capability’, and ‘response time’.

‘Informational fit-to-task’ are the items that provides information in assisting customer’s task.

While ‘transaction capability’ involves those functions that demonstrate the ability of the website

to deliver its business function and ‘response time’ relates to the load time of the website. (Kim &

Stoel, 2004)

(Yang, Peterson, & Huang, 2001) found that satisfied customers do not really think that the

aesthetic aspect of websites is important.

According to another study, website that is informative and well-organised garners positive

responses from users. However, the website need not be ‘imaginative, exciting and entertaining’.

(Chen, Clifford, & Wells, 2002).

(McCormick & Vazquez, 2009) has analysed the aspects of online fashion retailers websites and

produced a framework called ‘The Online Fashion Environment’. For the purpose of this research,

I will be using this framework to analyse competitor’s websites.

35

3.5.3 The Online Fashion Environment

Website issues Online atmospherics Interactivity

Navigability

• Sitemaps

• Search by:-

• By item

• By

brand/sub-

brand

• Search

engines

• By

style/look/oc

casion

Image

atmospheric

s

• Graphics

• Colour

• Intro-

page/home

page

Value-

added

features

• Suggestions

• Email updates

• Add

on/recommen

dations

• Promotional

offers

Interactive

viewing

• Enlarge

images

• Zoom

• Front, back

and side

views

• 2D and 3D

view

• Product

information

details

Lifestyle

media

• Multi-

media

demos

• Colour

views

• Music

• Catwalk

• Display

models

Fashion

inspiration

• Fashion

photography

• Journalist

text

• Trend

information –

look

books/fashio

n forecasts

• New product

information

• Fashion

advise/blogs

Figure 9 Online Fashion Environment Dimensions, McCormick & Vazquez, 2009

According to the paper by (McCormick & Vazquez, 2009) above are the elements of website that

is existing in online fashion retailers. Website issues, Online Atmospherics and Interactivity are

the three broad categories that are identified.

From further research and readings, it seems that the Website issues have become something of

a standard. This is not the case some 5 years ago, but as e-commerce has grown and more people

are used to visiting websites and purchasing online, a minor lack in any of these factors can easily

make the online retailers look less credible.

Online retailers are expected to have good website designs such as ease of navigability, good

sitemap, and adequate information.

36

Due to the nature of the fashion industry, Online Atmospherics is a relatively more important

than any other industry. Due to the visual nature of clothing and fashion, it is only normal for the

websites to also display such aesthetic and quality on the website. For pure-play fashion retailers,

these are even more important as customers can only judge the clothing as how it is displayed in

the website. Since they are unable to use their sense of touch to judge the clothing, online

shoppers rely heavily on their other sense, visual and audio to make the purchase decision.

3.5.4 Competitors websites analysis using the Online Fashion Environment

dimension

According to (Chaffey, E-Business and E-Commerce Management: strategy, management, and

application, 2002), competitor analysis is especially important in e-commerce due to the ‘dynamic

nature of Internet medium’.

One of the methods to do that is to benchmark. Benchmarking is used to ‘compare e-commerce

services within a market’. (Chaffey, E-Business and E-Commerce Management: strategy,

management, and application, 2002). According to (Chase, 1998) companies should look at

competitor’s sites best practices, worst practices and next practices.

Below is an analysis of Elwarda’s main competitors.

37

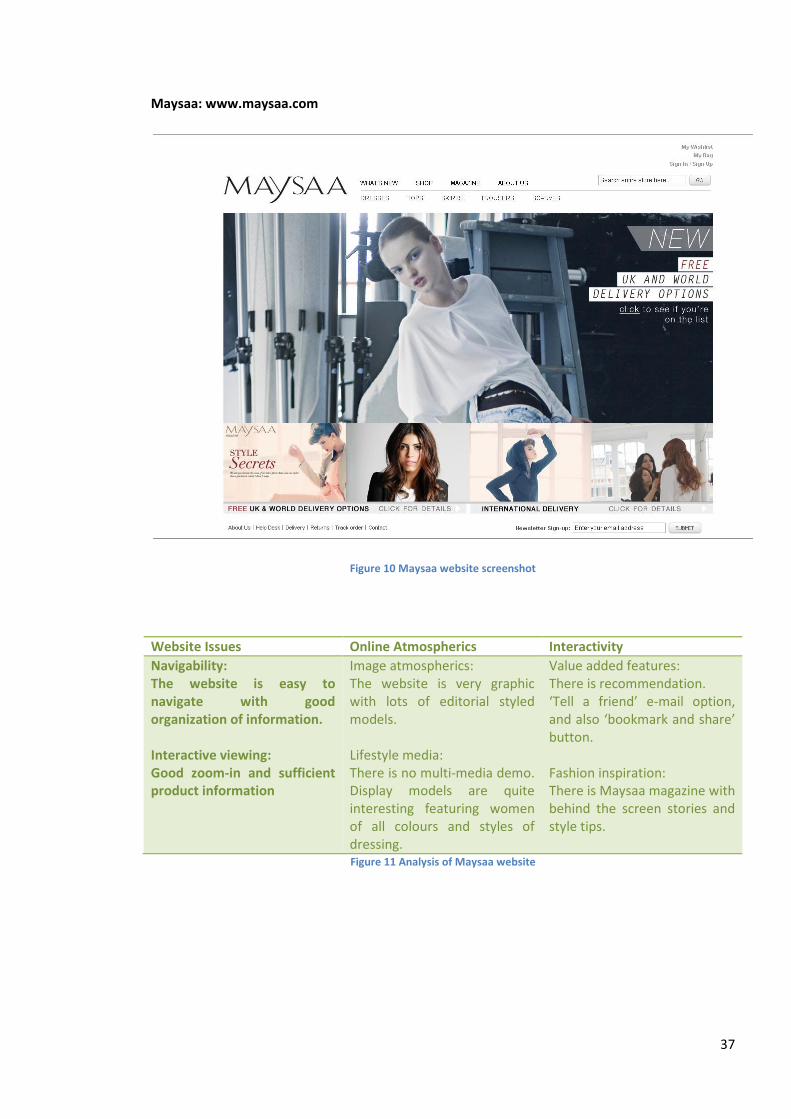

Maysaa: www.maysaa.com

Figure 10 Maysaa website screenshot

Website Issues Online Atmospherics Interactivity

Navigability:

The website is easy to

navigate with good

organization of information.

Interactive viewing:

Good zoom-in and sufficient

product information

Image atmospherics:

The website is very graphic

with lots of editorial styled

models.

Lifestyle media:

There is no multi-media demo.

Display models are quite

interesting featuring women

of all colours and styles of

dressing.

Value added features:

There is recommendation.

‘Tell a friend’ e-mail option,

and also ‘bookmark and share’

button.

Fashion inspiration:

There is Maysaa magazine with

behind the screen stories and

style tips.

Figure 11 Analysis of Maysaa website

38

Elenany: http://www.elenany.co.uk/

Figure 12 Elenany website screenshot

Website Issues Online Atmospherics Interactivity

Navigability: It’s easy to

navigate but too image heavy.

Interactive viewing: The zoom

in function is a bit outdated

compared to the more

instinctive recent zoom in

function. Sufficient product

information.

Image atmospherics:

Very attractive graphics, bright

colours.

Lifestyle media: Sliding images

in home-page. No moving

image of models.

Value added features:

No recommendation.

Fashion inspiration:

No fashion inspiration

Figure 13 Analysis of Elenany website

39

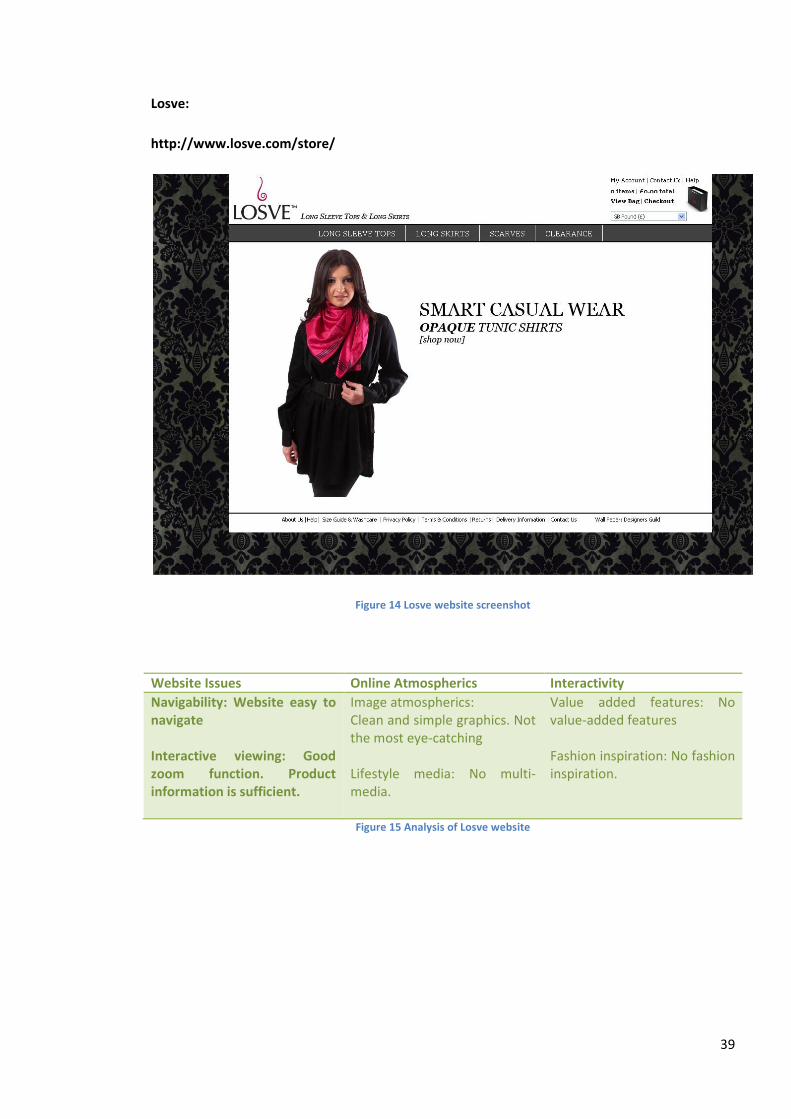

Losve:

http://www.losve.com/store/

Figure 14 Losve website screenshot

Website Issues Online Atmospherics Interactivity

Navigability: Website easy to

navigate

Interactive viewing: Good

zoom function. Product

information is sufficient.

Image atmospherics:

Clean and simple graphics. Not

the most eye-catching

Lifestyle media: No multi-

media.

Value added features: No

value-added features

Fashion inspiration: No fashion

inspiration.

Figure 15 Analysis of Losve website

40

3.5.5 Results and Discussion

Among the three, the best website is Maysaa, with its clean design and eye-catching graphics. To

have a competitive edge, Elwarda could introduce a multi-media element that is missing in

Maysaa’s website.

3.5.6 Summary

From literature it seems that website design does not rank very highly as important to online

fashion consumers. Factors such as information and the overall ability for the business to transact

online are more important.

3.6 E-Marketing and E-Promotion

3.6.1 Introduction

In operating an online fashion retail company, one of the most important aspects is the

marketing. E-marketing is the term used to explain the marketing activities of an online business.

According to (Chaffey, E-Business and E-Commerce Management: strategy, management, and

application, 2002) E-marketing is defined as

‘Achieving marketing objectives through use of electronic communications technology’.

While marketing is defined by the UK’s Chartered Institute of Marketing as:

‘Marketing is the management process responsible for identifying, anticipating and satisfying

customer requirements profitability’

Based from these two explanations, it can be derived that e-marketing is a process of marketing

using the internet and other electronic communications technology in order to meet customer’s

demands in a profitable way.

3.6.2 The 7 C’s : The E-Retail Marketing Mix

The traditional marketing mix 4P’s proposed by (McCarthy, 1960); price, place, product, and

promotion has been the base for all marketing mix used by business organisations. The original

4P’s has been extended and updated to include various elements and to respond to time and

technological change.

41

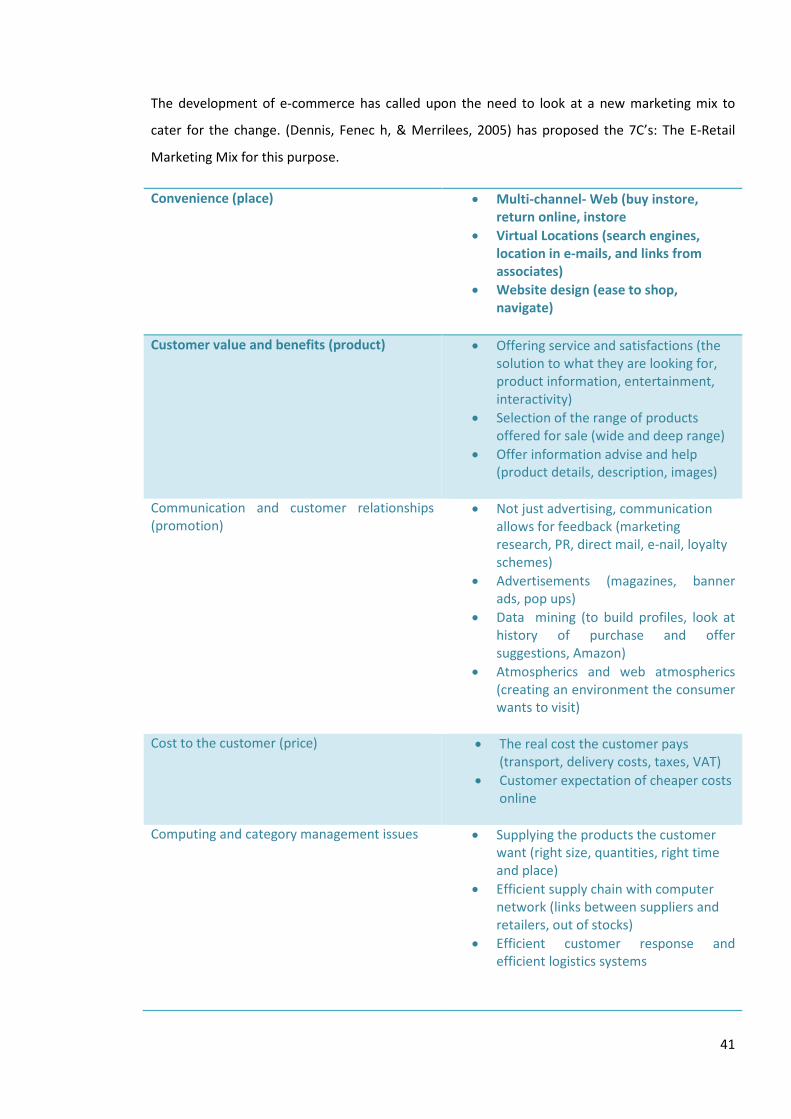

The development of e-commerce has called upon the need to look at a new marketing mix to

cater for the change. (Dennis, Fenec h, & Merrilees, 2005) has proposed the 7C’s: The E-Retail

Marketing Mix for this purpose.

Convenience (place) • Multi-channel- Web (buy instore,

return online, instore

• Virtual Locations (search engines,

location in e-mails, and links from

associates)

• Website design (ease to shop,

navigate)

Customer value and benefits (product) • Offering service and satisfactions (the

solution to what they are looking for,

product information, entertainment,

interactivity)

• Selection of the range of products

offered for sale (wide and deep range)

• Offer information advise and help

(product details, description, images)

Communication and customer relationships

(promotion)

• Not just advertising, communication

allows for feedback (marketing

research, PR, direct mail, e-nail, loyalty

schemes)

• Advertisements (magazines, banner

ads, pop ups)

• Data mining (to build profiles, look at

history of purchase and offer

suggestions, Amazon)

• Atmospherics and web atmospherics

(creating an environment the consumer

wants to visit)

Cost to the customer (price)

• The real cost the customer pays

(transport, delivery costs, taxes, VAT)

• Customer expectation of cheaper costs

online

Computing and category management issues

• Supplying the products the customer

want (right size, quantities, right time

and place)

• Efficient supply chain with computer

network (links between suppliers and

retailers, out of stocks)

• Efficient customer response and

efficient logistics systems