187 CHAPTER- 4 RESEARCH METHODOLOGY 4.1 NEED FOR THE STUDY After gone through the different studies conducted earlier there is a need to make a fresh attempt to understand the policyholder behaviour for purchase of insurance services specially life insurance policies. While reviewing the available literature the need for the study is summarized in the following points: 1. Most of the studies reported in literature were conducted in the area of insurance sector have covered various factors such as cost, value, customer satisfaction, delivery pattern of various policies etc. The proposed study aimed at analyzing on factors influencing policyholders’ decision making behaviour for buying life insurance. 2. Around 80 percent of total population is still uninsured (ICMR-VOICE Planman Consulting Insurance Survey) which shows that there is great potential of life insurance in rural and urban India. The research also developed a new understanding about policyholder buying decisions. Therefore, marketers must revitalize there service marketing strategies. 3. With the largest number of life insurance policies enforced in the world, India's insurance sector accounted for 4.1 per cent of GDP in 2006-07, up from 1.2 per cent in 1999-2000 and further increase is expected which reflect insurance sector has immense potential for growth. This study is better reasoning of policyholder decision making because of the wide size of diversified insurance market running on agent based network. 4. This study presented a new insight to the forthcoming researchers, academician and scholars to understand factors affecting purchase decision of insurance.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 4: Research Methodology

187

CHAPTER- 4

RESEARCH METHODOLOGY

4.1 NEED FOR THE STUDY

After gone through the different studies conducted earlier there is a need to make a

fresh attempt to understand the policyholder behaviour for purchase of insurance

services specially life insurance policies. While reviewing the available literature the

need for the study is summarized in the following points:

1. Most of the studies reported in literature were conducted in the area of insurance

sector have covered various factors such as cost, value, customer satisfaction,

delivery pattern of various policies etc. The proposed study aimed at analyzing on

factors influencing policyholders’ decision making behaviour for buying life

insurance.

2. Around 80 percent of total population is still uninsured (ICMR-VOICE

Planman Consulting Insurance Survey) which shows that there is great

potential of life insurance in rural and urban India. The research also

developed a new understanding about policyholder buying decisions.

Therefore, marketers must revitalize there service marketing strategies.

3. With the largest number of life insurance policies enforced in the world,

India's insurance sector accounted for 4.1 per cent of GDP in 2006-07, up

from 1.2 per cent in 1999-2000 and further increase is expected which reflect

insurance sector has immense potential for growth. This study is better

reasoning of policyholder decision making because of the wide size of

diversified insurance market running on agent based network.

4. This study presented a new insight to the forthcoming researchers, academician and

scholars to understand factors affecting purchase decision of insurance.

Chapter 4: Research Methodology

188

4.2 OBJECTIVES OF THE STUDY

The present study was an in-depth study of micro variables/determinants of

policyholder behaviour. The main purpose of the study was to investigate major

determinants of policyholder behaviour for selecting and buying insurance policy in

Haryana. The main objective of the study was to understand the various external and

internal influences on policyholder decision making. For achieving this main

objective several sub-objectives have been framed:

1. To study the impact of demographic, psychographic and social characteristics

of the sample policyholders on buying decision for purchasing life insurance

policy in Haryana.

2. To identify various needs, motives and stimuli forcing sample policyholders to

buy life insurance policy in Haryana.

3. To identify the gap between policyholder’s perceived benefits and actual

benefits derived from a life insurance policy in Haryana.

4. To find out the dominance of specific determinants on purchase decisions of

sample policyholders for buying life insurance policies in Haryana.

5. To observe the information search process of sample policyholders for buying

an insurance plan in Haryana.

6. To evaluate the factors underlying policyholder perception of rural and urban

policyholders towards the life insurance policies in Haryana.

7. To open new vistas for further researches in Haryana.

4.3 NATURE OF RESEARCH

The adopted research was descriptive in nature as it describes the determinants of

policyholder decision making in general and policyholder behaviour more particular.

The research was an in-depth research of decision making process and study of

factor(s) influencing a purchase decision. This ex post facto research includes survey

and fact finding enquiries.

Chapter 4: Research Methodology

189

This descriptive study was undertaken in order to ascertain and describe the

characteristics of the variables of interest such as age, educational level, job status,

years, work experience, sex compositions, working in the marketing/business system

and such other characteristics. Descriptive study is also undertaken to understand the

characteristics of policyholders that follow certain common practices.

In this study few hypotheses have been also frame and tested since the principle

objective of this work was to find out the impact of demographic, psychographic and

social factors on purchase decisions. For this research a survey of primary sources of

information has been conducted for two reasons. Firstly, analogous situation

(case study) has not been examined as it could have made the scope of the research

very narrow. Secondly, the survey method has the advantages of flexibility and

versatility.

4.4 DATA COLLECTION

The research was basically descriptive in nature but few hypotheses have been tested

for achieving objectives of the research. Therefore both primary and secondary data

have been used. Primary data was collected from selected policy holders through

questionnaires and observations while the secondary data was collected from books,

magazines, news papers, journals, IRDA annual reports, statistical abstract and so on.

Data Required

Primary data was required to know the level of knowledge of sample policyholders,

about different schemes being offered by various insurance corporations to know the

impact of knowledge for selection of a policy and so on to make this study qualitative.

Secondary data was required to study the nature, scope and various types of insurance

policies being opted by policyholders, global insurance practices, development of

insurance sectors in India and global insurance practices in order to make this study

quantitative. The research was designed to find out the determinants of buying

behaviour and policyholders from Haryana were major source of primary data for this

study. The data was collected very carefully as the data increases reliability,

Chapter 4: Research Methodology

190

usefulness, validity, accuracy and importance of statistical analysis. Primary and

secondary data both were collected and used by the researcher for the purpose of

reliability, authenticity and importance of exploratory research.

Primary data: Policyholders from different areas, fields, professions, age groups,

religions and genders have been contacted and interviewed through personal contact

method. Initially the researcher has conducted an informal discussion along with

observation of policyholders and insurance agents only from Gurgaon followed by a

pilot survey and thorough spadework. On the basis of pilot survey conducted in

Gurgaon on 30 policyholders, the researcher has developed a structured

schedule/questionnaire. The Researcher has collected primary data by personally

interviewing policyholders from rural and urban areas with the help of exhaustive

structured schedule/questionnaire consisting 33 questions.

Secondary data: Secondary data was collected from various published books,

reports, web sources, journals, IRDA annual reports, statistical abstract, magazines,

research articles, news papers and printed manuals of the insurance companies. Some

unpublished information has been collected from previous records of insurance

companies. Data was also collected from different units and offices of Insurance

agents.

The questionnaire (schedule): The primary data was collected by personally

interviewing executives with the help of a structured schedule consisting 33 questions.

Where interviewing personally was not possible or allowed, these questionnaires were

distributed to the agents and policyholders in Haryana and collected lately. The

questionnaire consists of open or closed ended questions. The data was collected by

means of a self administrated questionnaire, which was developed in the following stages:

(a) Indentifying variables and developing first draft.

(b) Content validity

(c) Pilot survey

(d) Finalizing the questionnaire

(e) Reliability check

Chapter 4: Research Methodology

191

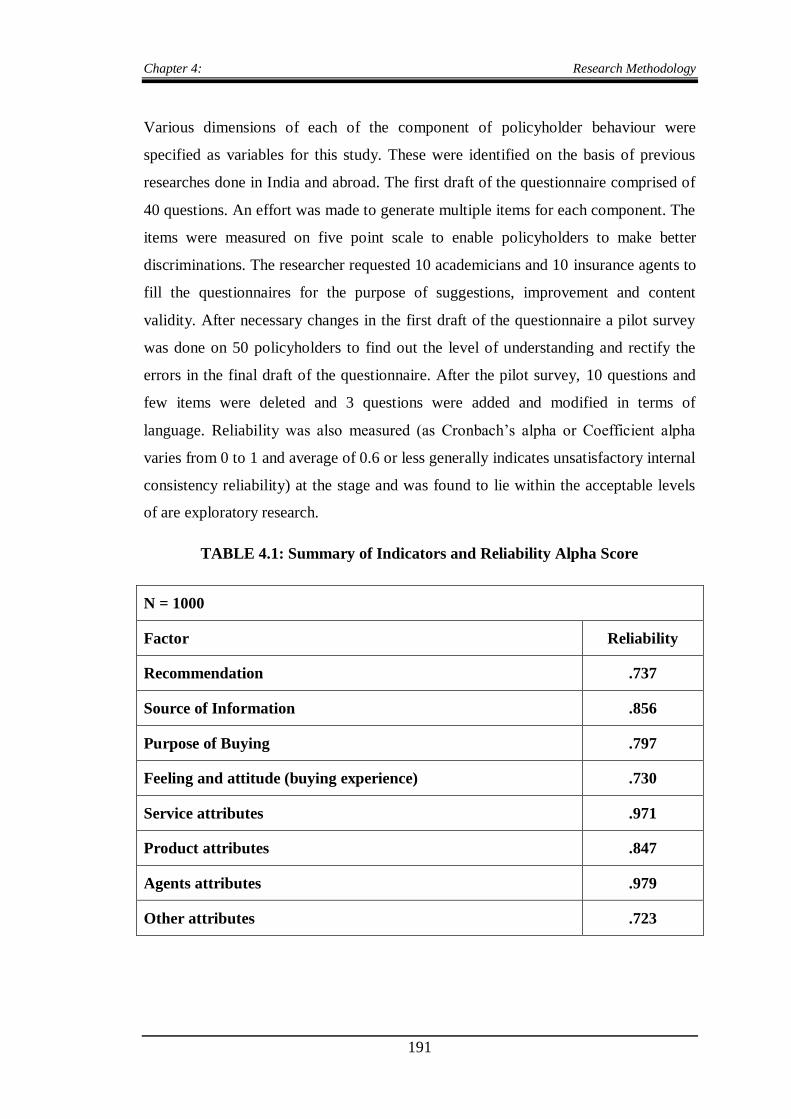

Various dimensions of each of the component of policyholder behaviour were

specified as variables for this study. These were identified on the basis of previous

researches done in India and abroad. The first draft of the questionnaire comprised of

40 questions. An effort was made to generate multiple items for each component. The

items were measured on five point scale to enable policyholders to make better

discriminations. The researcher requested 10 academicians and 10 insurance agents to

fill the questionnaires for the purpose of suggestions, improvement and content

validity. After necessary changes in the first draft of the questionnaire a pilot survey

was done on 50 policyholders to find out the level of understanding and rectify the

errors in the final draft of the questionnaire. After the pilot survey, 10 questions and

few items were deleted and 3 questions were added and modified in terms of

language. Reliability was also measured (as Cronbach’s alpha or Coefficient alpha

varies from 0 to 1 and average of 0.6 or less generally indicates unsatisfactory internal

consistency reliability) at the stage and was found to lie within the acceptable levels

of are exploratory research.

TABLE 4.1: Summary of Indicators and Reliability Alpha Score

N = 1000

Factor Reliability

Recommendation .737

Source of Information .856

Purpose of Buying .797

Feeling and attitude (buying experience) .730

Service attributes .971

Product attributes .847

Agents attributes .979

Other attributes .723

Chapter 4: Research Methodology

192

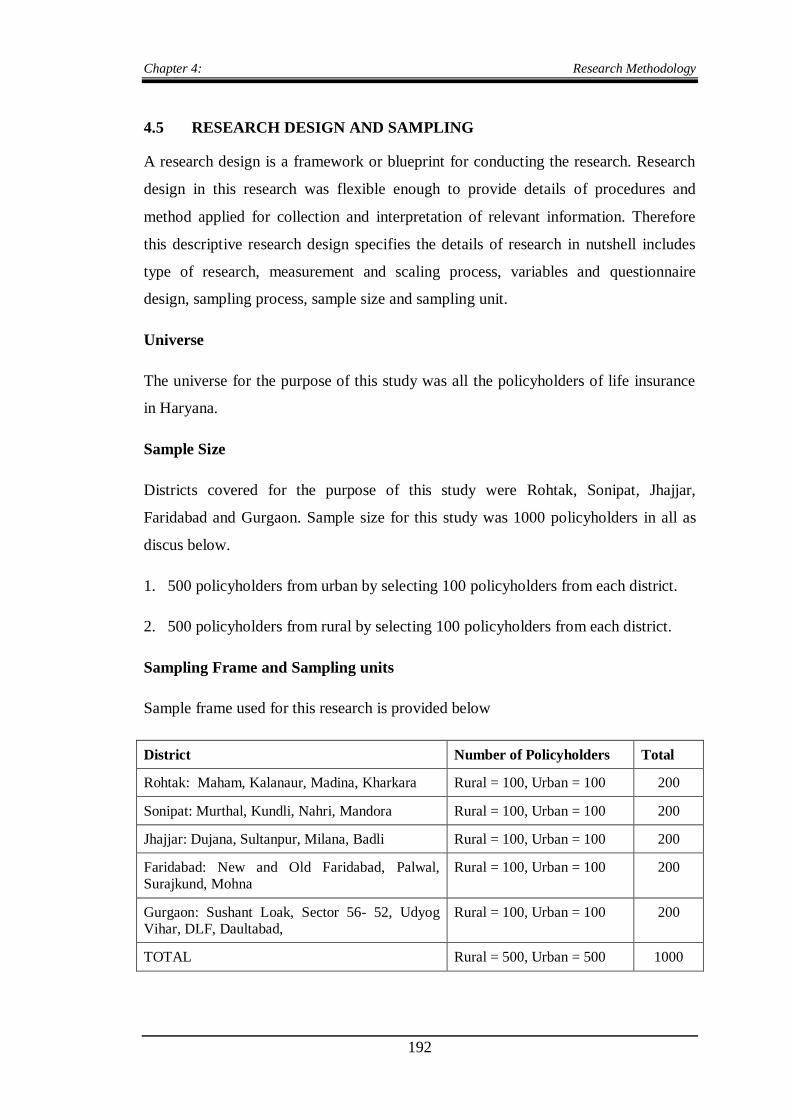

4.5 RESEARCH DESIGN AND SAMPLING

A research design is a framework or blueprint for conducting the research. Research

design in this research was flexible enough to provide details of procedures and

method applied for collection and interpretation of relevant information. Therefore

this descriptive research design specifies the details of research in nutshell includes

type of research, measurement and scaling process, variables and questionnaire

design, sampling process, sample size and sampling unit.

Universe

The universe for the purpose of this study was all the policyholders of life insurance

in Haryana.

Sample Size

Districts covered for the purpose of this study were Rohtak, Sonipat, Jhajjar,

Faridabad and Gurgaon. Sample size for this study was 1000 policyholders in all as

discus below.

1. 500 policyholders from urban by selecting 100 policyholders from each district.

2. 500 policyholders from rural by selecting 100 policyholders from each district.

Sampling Frame and Sampling units

Sample frame used for this research is provided below

District Number of Policyholders Total

Rohtak: Maham, Kalanaur, Madina, Kharkara Rural = 100, Urban = 100 200

Sonipat: Murthal, Kundli, Nahri, Mandora Rural = 100, Urban = 100 200

Jhajjar: Dujana, Sultanpur, Milana, Badli Rural = 100, Urban = 100 200

Faridabad: New and Old Faridabad, Palwal, Surajkund, Mohna

Rural = 100, Urban = 100 200

Gurgaon: Sushant Loak, Sector 56- 52, Udyog Vihar, DLF, Daultabad,

Rural = 100, Urban = 100 200

TOTAL Rural = 500, Urban = 500 1000

Chapter 4: Research Methodology

193

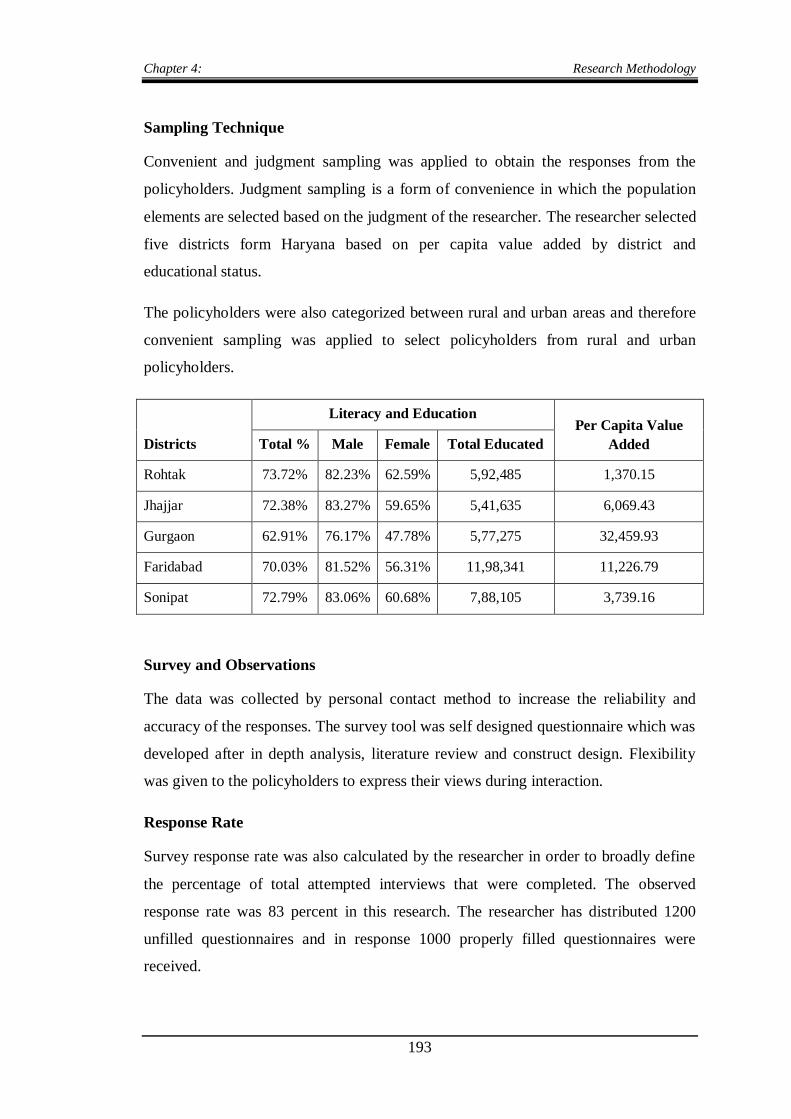

Sampling Technique

Convenient and judgment sampling was applied to obtain the responses from the

policyholders. Judgment sampling is a form of convenience in which the population

elements are selected based on the judgment of the researcher. The researcher selected

five districts form Haryana based on per capita value added by district and

educational status.

The policyholders were also categorized between rural and urban areas and therefore

convenient sampling was applied to select policyholders from rural and urban

policyholders.

Districts

Literacy and Education Per Capita Value

Added Total % Male Female Total Educated

Rohtak 73.72% 82.23% 62.59% 5,92,485 1,370.15

Jhajjar 72.38% 83.27% 59.65% 5,41,635 6,069.43

Gurgaon 62.91% 76.17% 47.78% 5,77,275 32,459.93

Faridabad 70.03% 81.52% 56.31% 11,98,341 11,226.79

Sonipat 72.79% 83.06% 60.68% 7,88,105 3,739.16

Survey and Observations

The data was collected by personal contact method to increase the reliability and

accuracy of the responses. The survey tool was self designed questionnaire which was

developed after in depth analysis, literature review and construct design. Flexibility

was given to the policyholders to express their views during interaction.

Response Rate

Survey response rate was also calculated by the researcher in order to broadly define

the percentage of total attempted interviews that were completed. The observed

response rate was 83 percent in this research. The researcher has distributed 1200

unfilled questionnaires and in response 1000 properly filled questionnaires were

received.

Chapter 4: Research Methodology

194

Data Analysis

The data was collected, processed, edited, tabulated and then interpreted for the purpose

of summarizing the results and findings. The statistical tools were also used to simplify

the raw data like percentages, averages, frequency distribution, mean scores, correlations,

regression and confirmatory factor analysis to find out the crux of the study.

4.6 MEASUREMENT AND SCALING TECHNIQUES

Measurement is a relatively complex and demanding task, especially so when it

concerns qualitative or abstract phenomena. By measurement we mean the process of

assigning numbers to objects or observations, the level of measurement being a

function of the rule under which the numbers were assigned.

Measurement is a process of mapping aspects of a range according to some rule of

correspondence. In measuring we devise some form of scale in the range. Scales of

measurement can be considered in terms of their mathematical properties. For this

study nominal and ordinal scales were used.

For this study Likert scale was developed and five point rating scale was applied

using numerical scores ranging from 1 to 5 for questions. When using this technique it

is important to use consistent scoring therefore the responses were framed from

strongly disagree to strongly agree. In this scale higher scale denotes high

agreeableness of the policyholders.

For construct designing and for reducing set of items, it is important to use multi item

scales specially likert scale. A brief outline of hypothesis statements, variables and

scales developed for the study is provided below:

4.7 HYPOTHESIS

Any assumption cannot be converted into hypothesis without applying statistical

techniques. No empirical research can be complete without testing a primary

hypothesis statement. Statistical tools such as correlations, regression and t-tests were

used for testing hypothesis for the purpose of this research. Following hypothesis

Chapter 4: Research Methodology

195

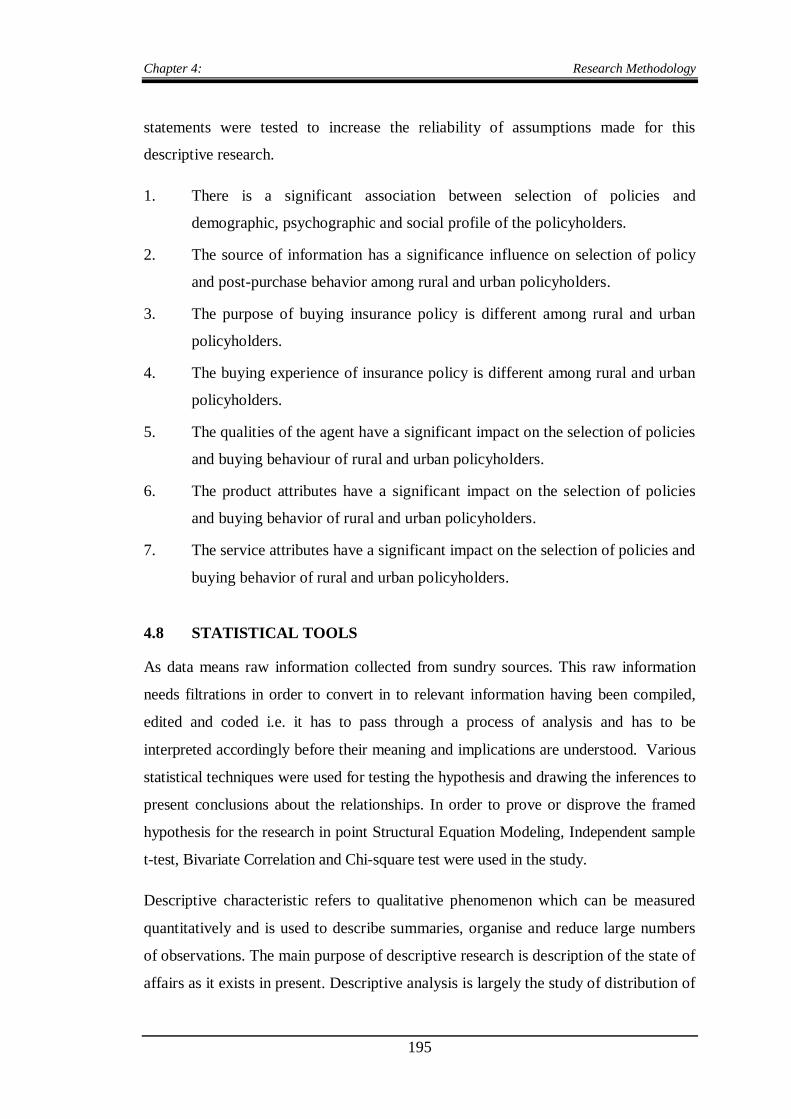

statements were tested to increase the reliability of assumptions made for this

descriptive research.

1. There is a significant association between selection of policies and

demographic, psychographic and social profile of the policyholders.

2. The source of information has a significance influence on selection of policy

and post-purchase behavior among rural and urban policyholders.

3. The purpose of buying insurance policy is different among rural and urban

policyholders.

4. The buying experience of insurance policy is different among rural and urban

policyholders.

5. The qualities of the agent have a significant impact on the selection of policies

and buying behaviour of rural and urban policyholders.

6. The product attributes have a significant impact on the selection of policies

and buying behavior of rural and urban policyholders.

7. The service attributes have a significant impact on the selection of policies and

buying behavior of rural and urban policyholders.

4.8 STATISTICAL TOOLS

As data means raw information collected from sundry sources. This raw information

needs filtrations in order to convert in to relevant information having been compiled,

edited and coded i.e. it has to pass through a process of analysis and has to be

interpreted accordingly before their meaning and implications are understood. Various

statistical techniques were used for testing the hypothesis and drawing the inferences to

present conclusions about the relationships. In order to prove or disprove the framed

hypothesis for the research in point Structural Equation Modeling, Independent sample

t-test, Bivariate Correlation and Chi-square test were used in the study.

Descriptive characteristic refers to qualitative phenomenon which can be measured

quantitatively and is used to describe summaries, organise and reduce large numbers

of observations. The main purpose of descriptive research is description of the state of

affairs as it exists in present. Descriptive analysis is largely the study of distribution of

Chapter 4: Research Methodology

196

one variable. The study provides us with profile of companies, work groups, persons

and other subjects or any multitude of characteristics such as size, composition,

efficiency and preferences.

The sort of analysis may be in respect of one variable (described as unidimensional

analysis), or in respect of two variables (described as bivariate analysis) or in respect

of more than two variables (described as multivariate analysis). In this context we

work out various measures that show the size and shape of a distribution (s) along

with the study or measuring relationship between two or more variables.

Such classification of one or more than one variable can be simple classification or

manifold classification. In manifold classification, we consider two or more attributes

simultaneously and divide the data into a number of classes. When data are collected,

the observations must be organized in such a fashion to allow the researcher to

interpret the data correctly and trace underlying trends. This method is commonly

used to provide grouped data for frequency distributions, measures of central

tendency such as mean, skewness, measure of variability such as the standard

deviation, a numerical index that indicates the average variability of the scores from

the mean.

Statistics Measures: The important statistical measures were used to summaries the

survey/ research data such as frequency distribution, tabulation, measure of central

tendency, measure of asymmetry, measure of dispersion and measure of relationship.

Frequency distribution: Frequency distribution is a summary from the data

presented in class intervals and frequencies.

Measure of central tendency: The central tendency is a single value which is used to

represent an entire set of data. It is a typical value around which most of the other

values cluster. In other words, the tendency of the observations to concentrate around

a central point is known as central tendency. Statistical measures that indicate the

location or positions of a central value to describe the central tendency of the entire

data are called the measures of central tendency. Statistical average or measurement

of central tendency tells us the point about which items have a tendency to cluster.

Chapter 4: Research Methodology

197

Such a measure is considered as the most representative figure for entire mass of data.

Measure of central tendency is also known as statistical averages (Mean, Mode and

Median). In statistics there are various types of measures of central tendency, some of

which can be broadly classified as follows:

1. Mathematical Averages (Arithmetic mean, Harmonic mean and Geometric mean).

2. Positional Averages (Median, Mode, Quartiles, Deciles, Percentiles).

Mean is arithmetical average and is the most popular measure of central tendency and

may be defined as the value which we get by dividing the total of the values of

various given items in a series by total number of items.

Median is the simplest measurement of central tendency and is a widely used

measure. It is used in summarizing the essential features of a series and enabling data

to be compared.

Mode is the most commonly occurring value in a series. Standard deviation

represents total variations in mean.

Measurement of Asymmetry (Skewness): When the data is normally distributed we

get a perfectly bell shaped curve and skewness is altogether absent. Positive skew

represents asymmetry of data set and negative skew also represents heterogeneity

(asymmetry) of data set. Kurtosis is the measure of flat- toppedness of a curve.

Measure of Dispersion: An average can represent a series only as best as a single

figure can, but it certainly cannot reveal the entire story of any phenomenon under

study. In order to measure the scatter of the values of items of a variable in the series

around the true value of average, measures of dispersion such as range, variance,

mean deviation and standard deviation are calculated. The greater the standard

deviation, the greater the magnitude of the values from their mean value. Smaller the

standard deviation, greater the uniformity in the observations made.

The Mean and the Median: Measures of central tendency refer to the summary

measures used to describe the most ‘typical’ value in a set of values. The two most

common measures of central tendency are the median and the mean. The mean of a

Chapter 4: Research Methodology

198

sample or a population is computed by adding all of the observations and dividing by

the number of observations using the following equations:

Population mean = μ = ΣX / N OR Sample mean = x = Σx / n

Where ΣX is the sum of all the population observations, N is the number of population

observations, Σx is the sum of all the sample observations and n is the number of

sample observations. When statisticians talk about the mean of a population, they use

the Greek letter μ to refer to the mean score. When they talk about the mean of

a sample, statisticians use the symbol x to refer to the mean score. As measures of

central tendency, the mean and the median each have advantages and disadvantages.

Some pros and cons of each measure are summarized below. The median may be a

better indicator of the most typical value if a set of scores has an outlier. An outlier is

an extreme value that differs greatly from other values. However, when the sample

size is large and does not include outliers, the mean score usually provides a better

measure of central tendency. Mode is the most commonly occurring value in a series.

Standard deviation represents total variations in mean.

The Standard Deviation: The standard deviation is the square root of the variance.

Thus, the standard deviation of a population is:

σ = √ [ σ2 ] = √ [ Σ ( Xi - μ )2 / N ]

Where σ is the population standard deviation, σ2 is the population variance, μ is the

population mean, Xi is the ith element from the population and N is the number of

elements in the population.

Measure of Relationship: It is important in a study to determine relation between

variables. Different methods can be used for measuring relationship among variables

such as correlation, multiple regression and time series Analysis.

Correlation was used when we have data on two or more than two variables or we

have bivariate/multivariate population. In case of bivariate population, simple

correlation such as Charles Spearman’s coefficient of correlation and Karl Pearson’s

coefficient of correlation, simple regression and two way ANOVA, can be used. In

Chapter 4: Research Methodology

199

case of multivariate population, coefficient of multiple correlation and coefficient of

partial correlation, multiple regression and multi ANOVA, can be used.

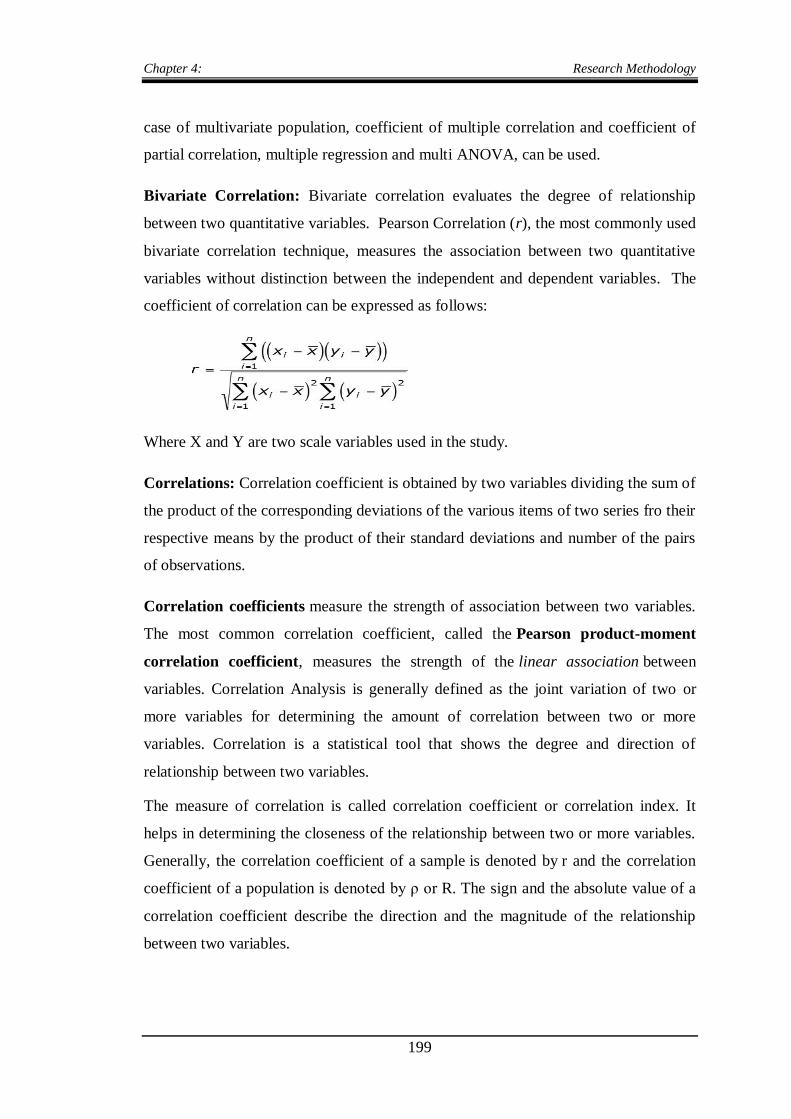

Bivariate Correlation: Bivariate correlation evaluates the degree of relationship

between two quantitative variables. Pearson Correlation (r), the most commonly used

bivariate correlation technique, measures the association between two quantitative

variables without distinction between the independent and dependent variables. The

coefficient of correlation can be expressed as follows:

Where X and Y are two scale variables used in the study.

Correlations: Correlation coefficient is obtained by two variables dividing the sum of

the product of the corresponding deviations of the various items of two series fro their

respective means by the product of their standard deviations and number of the pairs

of observations.

Correlation coefficients measure the strength of association between two variables.

The most common correlation coefficient, called the Pearson product-moment

correlation coefficient, measures the strength of the linear association between

variables. Correlation Analysis is generally defined as the joint variation of two or

more variables for determining the amount of correlation between two or more

variables. Correlation is a statistical tool that shows the degree and direction of

relationship between two variables.

The measure of correlation is called correlation coefficient or correlation index. It

helps in determining the closeness of the relationship between two or more variables.

Generally, the correlation coefficient of a sample is denoted by r and the correlation

coefficient of a population is denoted by ρ or R. The sign and the absolute value of a

correlation coefficient describe the direction and the magnitude of the relationship

between two variables.

Chapter 4: Research Methodology

200

The value of a correlation coefficient ranges between -1 and 1.

The greater the absolute value of a correlation coefficient, the stronger

the linear relationship.

The strongest linear relationship is indicated by a correlation coefficient of -1 or 1.

The weakest linear relationship is indicated by a correlation coefficient equal to 0.

A positive correlation means that if one variable gets bigger, the other variable

tends to get bigger.

A negative correlation means that if one variable gets bigger, the other

variable tends to get smaller.

The Pearson product-moment correlation coefficient only measures linear

relationships. Therefore, a correlation of does not mean zero relationship between two

variables; rather, it means zero linear relationship. (It is possible for two variables to

have zero linear relationship and a strong curvilinear relationship at the same time.)

Product-moment correlation coefficient. The correlation r between two variables is:

r = Σ (xy) / √ [ ( Σ x2 ) * ( Σ y

2 ) ]

Where Σ is the summation symbol, x = xi - x, xi is the x value for observation i, xi is

the mean x value, y = yi - y, yi is the y value for observation i and y is the mean y

value.

The value of r lies between +- 1. Positive values or r indicate positive correlation

between variables whereas negative values indicate negative correlation between

variables. A zero value indicates no correlation between variables. The value of ‘r’

nearer to +1 and -1 indicates high degree of correlation between the two variables.

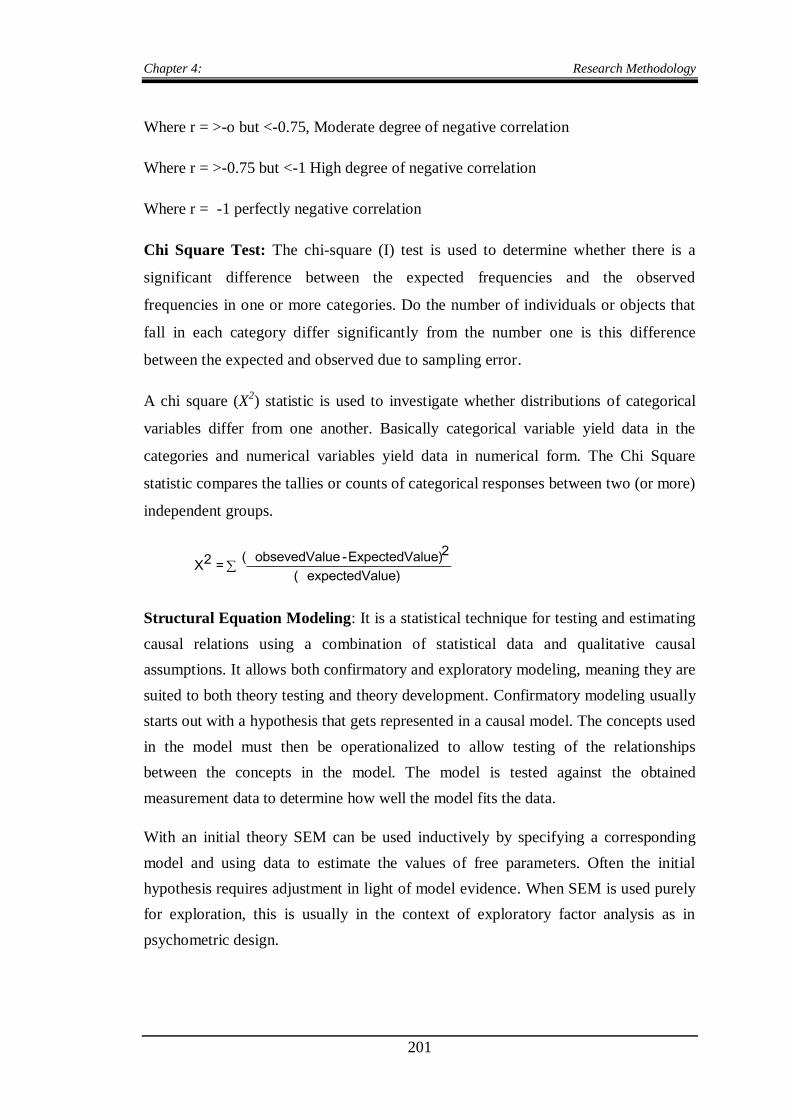

Where r = +1, perfectly positive correlation

Where r = >+0.75 but < +1, High degree of positive correlation.

Where r = > +0 but <+0.75, Moderate degree of positive correlation

Where r = 0 No correlation

Chapter 4: Research Methodology

201

Where r = >-o but <-0.75, Moderate degree of negative correlation

Where r = >-0.75 but <-1 High degree of negative correlation

Where r = -1 perfectly negative correlation

Chi Square Test: The chi-square (I) test is used to determine whether there is a

significant difference between the expected frequencies and the observed

frequencies in one or more categories. Do the number of individuals or objects that

fall in each category differ significantly from the number one is this difference

between the expected and observed due to sampling error.

A chi square (X2) statistic is used to investigate whether distributions of categorical

variables differ from one another. Basically categorical variable yield data in the

categories and numerical variables yield data in numerical form. The Chi Square

statistic compares the tallies or counts of categorical responses between two (or more)

independent groups.

2(obsevedValue -ExpectedValue)2X =(expectedValue)

Structural Equation Modeling: It is a statistical technique for testing and estimating

causal relations using a combination of statistical data and qualitative causal

assumptions. It allows both confirmatory and exploratory modeling, meaning they are

suited to both theory testing and theory development. Confirmatory modeling usually

starts out with a hypothesis that gets represented in a causal model. The concepts used

in the model must then be operationalized to allow testing of the relationships

between the concepts in the model. The model is tested against the obtained

measurement data to determine how well the model fits the data.

With an initial theory SEM can be used inductively by specifying a corresponding

model and using data to estimate the values of free parameters. Often the initial

hypothesis requires adjustment in light of model evidence. When SEM is used purely

for exploration, this is usually in the context of exploratory factor analysis as in

psychometric design.

Chapter 4: Research Methodology

202

Among the strengths of SEM is the ability to construct latent variables: variables

which are not measured directly, but are estimated in the model from several

measured variables each of which is predicted to 'tap into' the latent variables. This

allows the modeler to explicitly capture the unreliability of measurement in the

model, which in theory allows the structural relations between latent variables to be

accurately estimated. Factor analysis, path analysis and regression all represent

special cases of SEM. In SEM, the qualitative causal assumptions are represented by

the missing variables in each equation, as well as vanishing Covariance’s among

some error terms. These assumptions are testable in experimental studies and must be

confirmed judgmentally in observational studies.

Independent Sample T test: In the study the behavior of rural and urban

policyholders is to be considered. The independent samples (or two-sample) t-test is

used to compare the means of two independent samples (rural and urban). The

assumption of the test is:

- The dependent variable is normally distributed.

- The two groups have approximately equal variance on the dependent variable.

The two groups are independent of one another.

The formula for the t-test is a ratio. The top part of the ratio is just the difference

between the two means or averages. The bottom part is a measure of the variability or

dispersion of the scores. The t statistic in the independent sample t test can be

calculated as follows:

Where, x1 and x2 are the means of two independent samples, s1 and s2 are the

standard deviations of the two samples, n1 and n2 are the sample size of the samples.

Software Used: MS Excel, AMOS 18 and SPSS 18 were used for the purpose of data

analysis.

Chapter 4: Research Methodology

203

4.9 RELEVANT VARIABLES STUDIED IN CONSUMER BEHAVIOUR

STUDY

In this study 33 Variables were grouped in two parts of the questionnaire.

Part A of questionnaire consists of general demographic information and Part B of

questionnaire consists of information related to policyholder behaviour. Research was

primarily based on primary data hence significant scales have been used for different

questions. Variables were coded and appropriate scales were assigned for the

variables defined separately. For studying the nature of independent variable and

effect of dependent variables and important dependent variables were selected.

(A) Demographic and life style variables

(B) External Determinants of policyholder behaviour

Sometimes some variables are not directly observable. At the Other times variables

are known to the marketers but their exact nature and relative strength of influence is

not apparent. In these circumstances, it is useful to understand the above mentioned

concepts and how the policyholders behave, so that their decision making process can

be predicted to a reasonable extent. The human mind being as complex as it is, the

understanding of the buying behaviour of the policyholders becomes a continuous

activity of application of various theories and concepts by the marketers. The study of

policyholder behaviour is quite complex, because of many variables involved and

their tendency to interact with and influence each other. These variables are divided

into three major sections that have been identified as the most important general

influences on Policyholder Behaviour. Imagine three concentric circles, one at the

outer most, one in the middle and one at the inner most and they represent the

following:

1. Individual Determinants of Behaviour: The major individual determinants

of Policyholder Behaviour are human mind and its attributes which are

portrayed in middle ring. These variables are personal attributes of a

policyholder and they are influenced by the below stated external factors.

These factors influence policyholders to take decision about the purchase

of insurance product. These determinants are age, education, economic

status, life cycle, personality, attitude, self-concept, religion, language,

motives, motivation, perception and learning and memory.

Chapter 4: Research Methodology

204

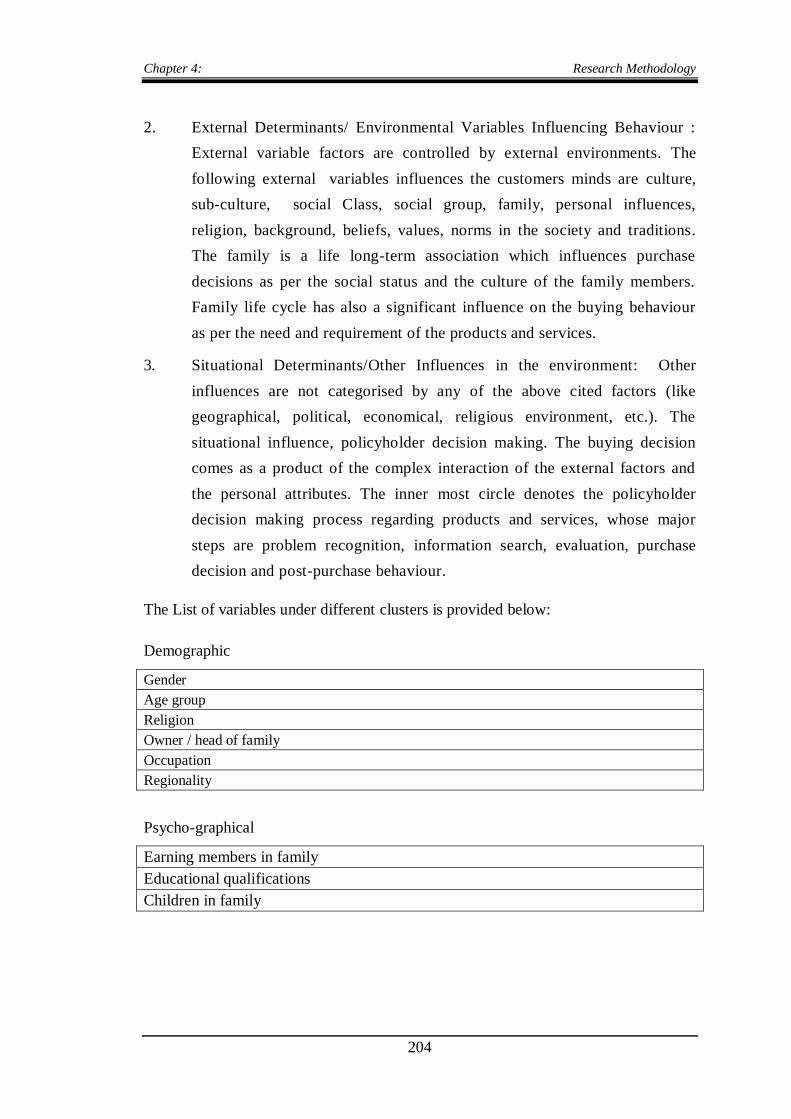

2. External Determinants/ Environmental Variables Influencing Behaviour :

External variable factors are controlled by external environments. The

following external variables influences the customers minds are culture,

sub-culture, social Class, social group, family, personal influences,

religion, background, beliefs, values, norms in the society and traditions.

The family is a life long-term association which influences purchase

decisions as per the social status and the culture of the family members.

Family life cycle has also a significant influence on the buying behaviour

as per the need and requirement of the products and services.

3. Situational Determinants/Other Influences in the environment: Other

influences are not categorised by any of the above cited factors (like

geographical, political, economical, religious environment, etc.). The

situational influence, policyholder decision making. The buying decision

comes as a product of the complex interaction of the external factors and

the personal attributes. The inner most circle denotes the policyholder

decision making process regarding products and services, whose major

steps are problem recognition, information search, evaluation, purchase

decision and post-purchase behaviour.

The List of variables under different clusters is provided below:

Demographic

Gender

Age group

Religion

Owner / head of family

Occupation

Regionality

Psycho-graphical

Earning members in family

Educational qualifications

Children in family

Chapter 4: Research Methodology

205

Life style

Life stage/ Personal status

Income group

Owner’s wealth

Home ownership

Type of vehicle

Type of bank account

Own property

Debit/credit card

Insurer Details

Name of the insurer

Satisfaction level

Amount Insured

Bajaj

ICICI

LIC

HDFC

INGVS

TATAAIG

SBILIFE

BIRLASUNLIFE

RELIANCELIFE

AVIVA

SAHARA

KOTAK

HSBC

MAXNY

METLIFE

AMPSN

SRIRAMLIFE

OTHER

Features of Insurance Policy

C1 = Whole Life Scheme

C2 = Endowment Scheme

C3 = Term Insurance Plan

C4 = Periodic Money Back Plan

C5 = Medical Benefits Linked Insurance

C6 = Children Plan

Chapter 4: Research Methodology

206

C7 = Joint Life Plan

C8 = Capital Market Limited Plan

C9 = Group Schemes

C10 = Social Security

C11 = Education Plan

C12 = Pension Plan

C13 = Growth Plan

C14 = Unit Linked Plan

C15 = Systematic Investment Plan

C16 = Individual Plan

C17 = Money Back Plan

C18 = Special Plan

C19 = Health Plan

C20 = Multiplier Plan

C21 = Plan with Flexible Investment Option

Selection Criteria

A1 = Nobody influenced me, it was my own decision.

A2 = My employer’s suggestion.

A3 = Recommended by family member

A4 = My Friend’s suggestion

A5 = Insurance agent’s suggestion.

A6 = My spouse’s suggestion.

A7= Recommended during advertisement

Sources of Information

B1 = News paper /magazines

B2 = Television

B3 = Internet /E-mails

B4 = Agent

B5 = Office/Workplace Circular/Notices

B6 = Spouse/children

B7 = Friends

B8 = Insurance Experts/advisors

B9 = Word of mouth

B10 = Bankers

B11 = Promotional telephone call/sms

Chapter 4: Research Methodology

207

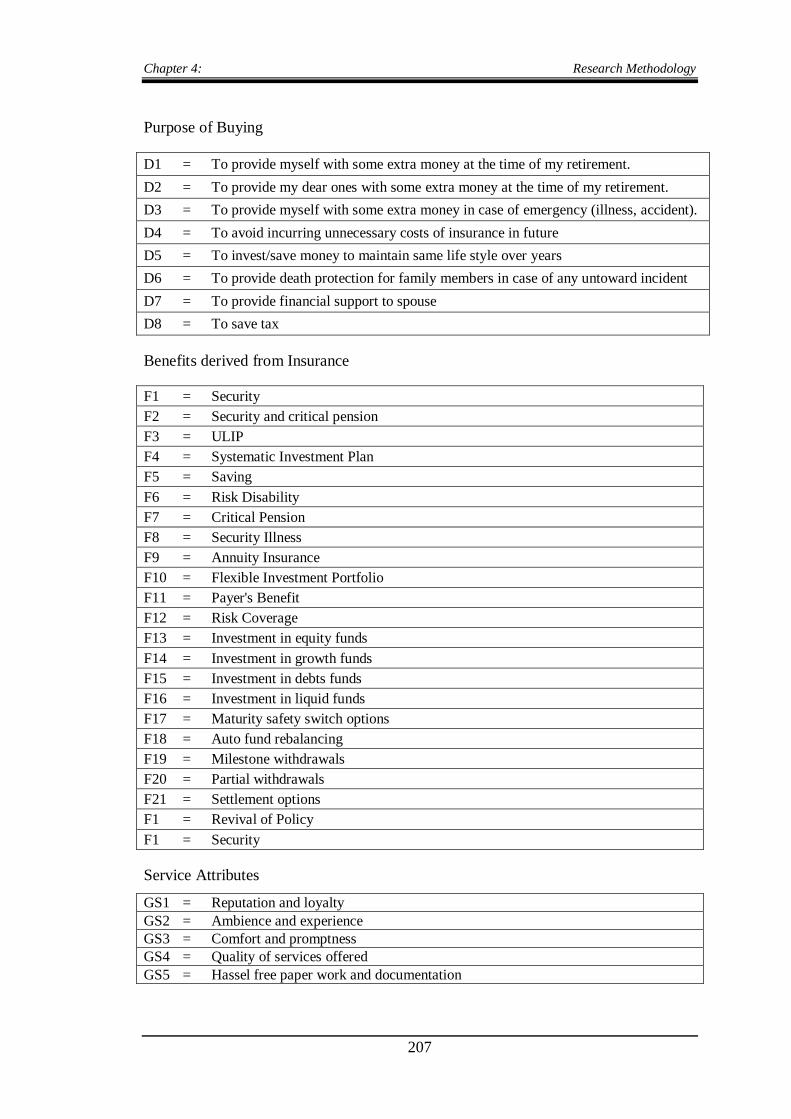

Purpose of Buying

D1 = To provide myself with some extra money at the time of my retirement.

D2 = To provide my dear ones with some extra money at the time of my retirement.

D3 = To provide myself with some extra money in case of emergency (illness, accident).

D4 = To avoid incurring unnecessary costs of insurance in future

D5 = To invest/save money to maintain same life style over years

D6 = To provide death protection for family members in case of any untoward incident

D7 = To provide financial support to spouse

D8 = To save tax

Benefits derived from Insurance

F1 = Security

F2 = Security and critical pension

F3 = ULIP

F4 = Systematic Investment Plan

F5 = Saving

F6 = Risk Disability

F7 = Critical Pension

F8 = Security Illness

F9 = Annuity Insurance

F10 = Flexible Investment Portfolio

F11 = Payer's Benefit

F12 = Risk Coverage

F13 = Investment in equity funds

F14 = Investment in growth funds

F15 = Investment in debts funds

F16 = Investment in liquid funds

F17 = Maturity safety switch options

F18 = Auto fund rebalancing

F19 = Milestone withdrawals

F20 = Partial withdrawals

F21 = Settlement options

F1 = Revival of Policy

F1 = Security

Service Attributes

GS1 = Reputation and loyalty

GS2 = Ambience and experience

GS3 = Comfort and promptness

GS4 = Quality of services offered

GS5 = Hassel free paper work and documentation

Chapter 4: Research Methodology

208

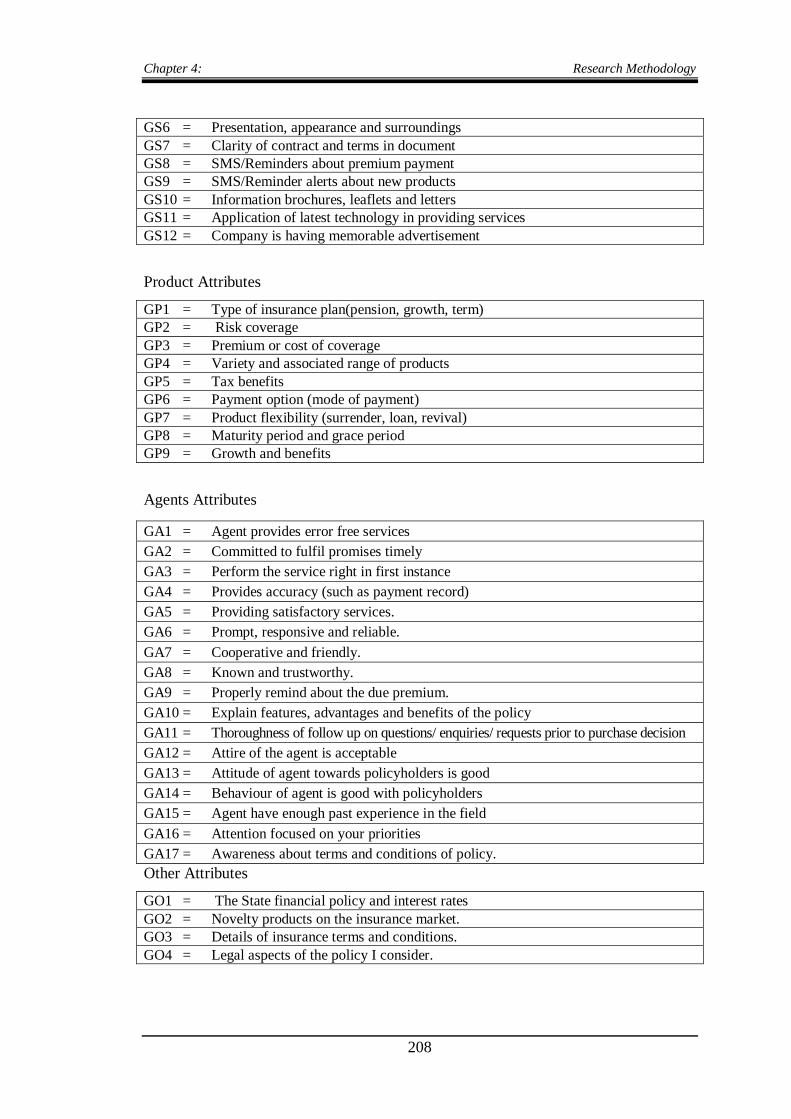

GS6 = Presentation, appearance and surroundings

GS7 = Clarity of contract and terms in document

GS8 = SMS/Reminders about premium payment

GS9 = SMS/Reminder alerts about new products

GS10 = Information brochures, leaflets and letters

GS11 = Application of latest technology in providing services

GS12 = Company is having memorable advertisement

Product Attributes

GP1 = Type of insurance plan(pension, growth, term)

GP2 = Risk coverage

GP3 = Premium or cost of coverage

GP4 = Variety and associated range of products

GP5 = Tax benefits

GP6 = Payment option (mode of payment)

GP7 = Product flexibility (surrender, loan, revival)

GP8 = Maturity period and grace period

GP9 = Growth and benefits

Agents Attributes

GA1 = Agent provides error free services

GA2 = Committed to fulfil promises timely

GA3 = Perform the service right in first instance

GA4 = Provides accuracy (such as payment record)

GA5 = Providing satisfactory services.

GA6 = Prompt, responsive and reliable.

GA7 = Cooperative and friendly.

GA8 = Known and trustworthy.

GA9 = Properly remind about the due premium.

GA10 = Explain features, advantages and benefits of the policy

GA11 = Thoroughness of follow up on questions/ enquiries/ requests prior to purchase decision

GA12 = Attire of the agent is acceptable

GA13 = Attitude of agent towards policyholders is good

GA14 = Behaviour of agent is good with policyholders

GA15 = Agent have enough past experience in the field

GA16 = Attention focused on your priorities

GA17 = Awareness about terms and conditions of policy.

Other Attributes

GO1 = The State financial policy and interest rates

GO2 = Novelty products on the insurance market.

GO3 = Details of insurance terms and conditions.

GO4 = Legal aspects of the policy I consider.

Chapter 4: Research Methodology

209

Post purchase Behaviour

HA1 = Agent shown sound knowledge and efficiency

AG

EN

T

HA2 = Cooperation was extended by the agent

HA3 = Agent has impartial attitude about policies

HA4 = Comfort was created by agent during conversation

HA5 = Agent shown enough respect and support

HA6 = Agent clarified problems on the basis of his past experienced

HA7 = Agent shown individual consideration and maintain confidentiality

HA8 = Less waiting time was given by the agent for advise

HA9 = Agent was easily available to me/policyholders

HB1 = Company have a good reputation in market

PR

OD

UC

T HB2 = The insurer offer additional benefits to loyal customers (payer benefits)

HB3 = For policyholders who buy more products of the same company discount is

offered

HB4 = The policy is designed with policyholders involvement

HB5 = Insurance plan is flexibility to change mode of payment/type of

plan/investment portfolio

HB6 = Company maintain healthy relationship with customers

HC1 = Tax benefits are given according to Law

PA

YM

EN

T

MO

DE

HC2 = Cost/premium of insurance is adequate and affordable.

HC3 = Policy document delivered to me on time

HC4 = Mode of payment is explained properly (a) Yearly (b) half yearly (c)

monthly

HC5 = Mode of premium is explained properly (a) Regular premium (b) single

premium

HD1=Only company I want to associate myself

PO

ST

PU

RC

HA

SE

HD2=Purchase more policies from the same company

HD3=Recommend friends and family the same company and its new offerings

HD4=I will deposit all my due premium on time

Chapter 4: Research Methodology

210

HE1=On-time settlement of the claims/ grievances

CL

AIM

SE

TT

LE

ME

NT

HE2=Easy claim procedure is must

HE3=Satisfactory return of money after maturity

HE4=Adequate return

HE5=Convenient claim intimation and registration

HE6=Hassel free fund value cheque disbursement

HE7=Simple documentation, processing and settlement

Related Documents