Reporting CSR – what and how to say it? Anne Ellerup Nielsen and Christa Thomsen Aarhus School of Business, Denmark Abstract Purpose – This paper seeks to analyse and discuss what organizations say and how they say it when reporting Corporate Social Responsibility. It raises the question whether organizations report consistently on CSR in terms of genres, media, rhetorical strategies, etc. Design/methodology/approach – The analysis takes critical discourse analysis of selected corporations’ CSR reporting, on the one hand, and theories and research on CSR and stakeholder relations, on the other hand, as its starting-point. A model of analysis is proposed which presents discourse as a result of four kinds of challenges facing corporations today. The model serves to establish an ideal typology of CSR concepts and discourses and to analyse these discourses from a modern organizational and corporate communication perspective. Findings – The analysis shows that annual reports are very dissimilar with respect to topics on the one hand and dimensions and discourses expressed in perspectives, stakeholder priorities, contextual information and ambition levels, on the other hand. The paper argues that corporations seem to be wrapped in divergent configurations of interest stemming from different institutional affiliations, such as government, regional institutions and NGOs. Originality/value – The contribution of the paper is to highlight the value of the discourse and the discourse types adopted in the reporting material. By adopting consistent discourse types which interact according to a well-defined pattern or order it is possible to communicate a strong social commitment, on the one hand, and take into consideration the expectations of the shareholders and of the other stakeholders, on the other hand. Keywords Corporate communications, Social responsibility, Reports, Critical thinking Paper type Research paper Introduction In some European countries, including Denmark, governments and legislators recommend that organisations report on their social and environmental activities (cf. the Danish law on Organisational Annual Reporting of 2002) in connection with the general annual report. Claims for transparency and accountability from organizations operating worldwide have pushed organizations to put corporate social responsibility (CSR) on the agenda. This has called for a need to decide how to find a formula for implementing and communicating aspects of responsibility to their stakeholders. However, as there is no established framework – only guidelines – for how to communicate consistently about CSR, many organizations are somewhat unprepared for the task. The lack of a common understanding and terminology in the area of CSR has made it difficult for organizations to develop consistent strategies for reporting on CSR in terms of genres, media, rhetorical strategies, etc. This, coupled with the jungle of discourses, which reign in the domain of CSR, have caused the communication from many organizations to be rather inconsistent. Some organizations have chosen to communicate about their social policy and activities on their corporate websites using distinct and inconsistent concepts for similar issues. Issues such as “safety and work environment” and “work assessment” may figure in reports on environmental The current issue and full text archive of this journal is available at www.emeraldinsight.com/1356-3289.htm Reporting CSR 25 Corporate Communications: An International Journal Vol. 12 No. 1, 2007 pp. 25-40 q Emerald Group Publishing Limited 1356-3289 DOI 10.1108/13563280710723732

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Reporting CSR – what and howto say it?

Anne Ellerup Nielsen and Christa ThomsenAarhus School of Business, Denmark

Abstract

Purpose – This paper seeks to analyse and discuss what organizations say and how they say it whenreporting Corporate Social Responsibility. It raises the question whether organizations reportconsistently on CSR in terms of genres, media, rhetorical strategies, etc.

Design/methodology/approach – The analysis takes critical discourse analysis of selectedcorporations’ CSR reporting, on the one hand, and theories and research on CSR and stakeholderrelations, on the other hand, as its starting-point. A model of analysis is proposed which presentsdiscourse as a result of four kinds of challenges facing corporations today. The model serves toestablish an ideal typology of CSR concepts and discourses and to analyse these discourses from amodern organizational and corporate communication perspective.

Findings – The analysis shows that annual reports are very dissimilar with respect to topics on theone hand and dimensions and discourses expressed in perspectives, stakeholder priorities, contextualinformation and ambition levels, on the other hand. The paper argues that corporations seem to bewrapped in divergent configurations of interest stemming from different institutional affiliations, suchas government, regional institutions and NGOs.

Originality/value – The contribution of the paper is to highlight the value of the discourse and thediscourse types adopted in the reporting material. By adopting consistent discourse types whichinteract according to a well-defined pattern or order it is possible to communicate a strong socialcommitment, on the one hand, and take into consideration the expectations of the shareholders and ofthe other stakeholders, on the other hand.

Keywords Corporate communications, Social responsibility, Reports, Critical thinking

Paper type Research paper

IntroductionIn some European countries, including Denmark, governments and legislatorsrecommend that organisations report on their social and environmental activities (cf.the Danish law on Organisational Annual Reporting of 2002) in connection with thegeneral annual report. Claims for transparency and accountability from organizationsoperating worldwide have pushed organizations to put corporate social responsibility(CSR) on the agenda. This has called for a need to decide how to find a formula forimplementing and communicating aspects of responsibility to their stakeholders.However, as there is no established framework – only guidelines – for how tocommunicate consistently about CSR, many organizations are somewhat unpreparedfor the task. The lack of a common understanding and terminology in the area of CSRhas made it difficult for organizations to develop consistent strategies for reporting onCSR in terms of genres, media, rhetorical strategies, etc. This, coupled with the jungleof discourses, which reign in the domain of CSR, have caused the communication frommany organizations to be rather inconsistent. Some organizations have chosen tocommunicate about their social policy and activities on their corporate websites usingdistinct and inconsistent concepts for similar issues. Issues such as “safety and workenvironment” and “work assessment” may figure in reports on environmental

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1356-3289.htm

Reporting CSR

25

Corporate Communications: AnInternational Journal

Vol. 12 No. 1, 2007pp. 25-40

q Emerald Group Publishing Limited1356-3289

DOI 10.1108/13563280710723732

management, key concepts such as “sustainability” “code of ethics/conduct” and eventhe concept of CSR, of which there is no consensus, appear as main concepts in somecontexts and as sub concepts in other contexts, etc. Our problem statement shall beseen in the light of these observations.

Aim and argumentsTaking critical discourse analysis of selected Danish organizations’ CSR reporting onthe one hand and theories and research on CSR and stakeholder relations on the otherhand as our starting point, we aim to analyze and discuss what organizations say andhow they say it when reporting CSR. Do organizations, for example, report consistentlyon CSR in terms of genres, media, rhetorical strategies, etc.? Is it, for example, possibleto communicate a strong social commitment, while also taking into consideration theexpectations of the shareholders and of the other stakeholders? In order to address thisaim, the following research questions were identified:

RQ1. What can we learn about the way in which companies present themselveswhen reporting CSR? What are their strategies in terms of scope,content/topics, ambition level, etc.? Which concepts and discourses dominate?

RQ2. How can we analyze the strategies for reporting on CSR from a modernorganizational and corporate communication perspective?

Theoretically, we argue that CSR is a contextual concept. Hence, in principle there areno limits to CSR. The definition of CSR as a contextual concept is a big challenge tothe companies. When reporting on CSR they must, for example, be able to manage themutual expectations between the company and the stakeholders. Empirically, weargue that organizations are wrapped in divergent configurations of interest stemmingfrom different institutional affiliations, such as government, regional institutions andNGO’s. In our analysis we draw on data from a Danish case study consisting ofexamples of CSR reporting (extracts from annual reports, social reports, sustainabilityreports, environmental reports, etc.). The case study focuses on the communicationdilemmas following from intersecting dimensions and ambition levels involved in CSRreporting (economic, legal, ethical, and philanthropic considerations for example). Amapping of discourses allows us to establish an ideal typology of CSR concepts anddiscourses and to analyze these discourses from a modern organizational and corporatecommunication perspective.

MethodologyOur analysis is based on Fairclough’s (1995) model of critical discourse analysis. Inparticular, Fairclough views discourse as a social practice, which constitutes socialidentities, social relations and the knowledge and meaning systems of the social world.A given discourse is, however, also constituted by social practice and social structures.Therefore, the social practice of a society is anchored in and oriented towards realmaterial social structures. Ideologies reflect the ideas and assumptions relating to theways in which individual identities, social relations and knowledge systems areconstituted through social practice (Fairclough, 1995). Since, discourse as socialpractice both reproduces and changes the ideas, thoughts and power relations rulingindividual and social interactions, discourse acts ideologically in the social world.

CCIJ12,1

26

Consequently, a critical discourse analysis may contribute to uncovering bothstructures of and changes in the social order.

Fairclough’s discourse analysis model implies that two dimensions are in focus: thatof the communicative event, which is the specific incident of language use, and that ofdiscourse organization, which is the discourse practice in the sense of the speech actsand genres, or discourses, used within a social institution or domain. An analysis of thecommunicative event requires an investigation of the qualities of the text, the discoursepractice in the sense of the production and reception processes, and the wider socialpractice of which the communicative event forms part. As the communicative event isconstituted by and constitutes the discourse practice, the practice cannot beinvestigated without taking into account the communicative event and vice versa. Thecommunicative events used for our analysis are Danish companies’ reporting on CSR.Although our analysis concentrates on formal textual and rhetorical elements such asvocabulary, grammar and meaning relations between sentence and argument types,which construct the discourse and genre characteristics, the analysis does not merelyinvolve the detection of types of discourses, genres and linguistic structures, but is ameans of examining how the text reproduces and restructures the existing discourseorder. Thus, the examination contributes to the initial uncovering of the social worldarticulated in the concepts of CSR.

The analysis of the discourse practice examines how and to what extent the authorcopies his discourse from or changes it with regard to already existing discourses. CSRhas close intertextual relations to business strategy models in general and to societalmodels. For this reason, the present paper considers some of the ideological dimensionsembedded in the set of business strategy discourses as they have unfolded at differentideological stages of society, i.e. the shareholder perspective, the stakeholderperspective and the societal or holistic perspective. Specifically, we analyze the ideasand power relations ruling individual and social interactions, addressing such issues aswhat makes organizations act, how organizations motivate their CSR initiatives, howorganizations interact and how organizations manage the mutual expectationsbetween the organization and the stakeholders.

In the analysis of social practice, text analysis is insufficient on its own as any socialpractice includes both discursive and non-discursive elements. Therefore, sociologicaland cultural dimensions also have to be included, because it reproduces or challengesthe existing discourse order, the communicative event functions as a form of socialpractice. This means that communicative events form, and are formed by, the generalsocial practice through its relation to the discourse order of such general practice. Thisrenders it interesting to investigate the extent to which CSR seems to reproduce thediscourse order of “profit maximation” or, if this is not the case, to investigate whetherit transforms the discourse order to such an extent that a social change towards“corporate citizenship” is realized. A third potential alternative would be that the textreproduces the discourse orders of the shareholder perspective, thus returning to someof the values and thoughts of a traditional society.

The empirical material is based on a case study of selected Danish organizations’CSR reporting (extracts from annual reports, social reports, sustainability reports,environmental reports, etc.). The selected organizations are six large and medium sixedcompanies who are members of the Danish Network of Business Leaders and known asCSR Pioneers in Denmark.

Reporting CSR

27

Theoretical frameworkThe theoretical framework of our paper consists of theories and literature on CSR andstakeholder relations. The theoretical literature typically distinguishes between threedifferent approaches to the question of what organizations are responsible for andmotivated by. The classical view is that “the social responsibility of business is toincrease its profits” (Friedman, 1970). The owners of the company who are supposed tobe interested in profit maximization are the turning point of the decisions made by thecompany. Social responsibility is considered to be primarily the responsibility of thegovernment. This approach also covers companies which primarily consider socialresponsibility as something which contributes to attaining the goals of the company,here in the form of long-term value creation for the owners of the company.

According to the stakeholder perspective companies are not only accountable to theowners of the company, but also to the stakeholders. The argument is thatstakeholders influence the activities of the company and/or are influenced by theactivities of the company (Freeman, 1984). Companies are, for example, accountable topoliticians who can curb the activities of the company by introducing a bill.

The broadest approach to social responsibility is the societal approach in whichcompanies are considered to be responsible to society in general. The view is thatcompanies are part of society. They need a “licence to operate” from society (Committeefor Economic Development, CED, 1971). Today companies representing this approachare characterized as “good corporate citizens” (Waddock, 2004).

Carroll (1991, 1999) boils down the essentials of the three approaches. He considersthe role of companies today as a role which includes four dimensions, i.e. an economic,a legal, an ethical and a philanthropic aspect. Carroll focuses on the stakeholders of thecompany. The problem with the definition is that it is very broad. Social responsibilityis a diffuse and almost non-operational concept, unless organizations learn to “unfoldstakeholder thinking” (Andriof et al., 2003). In this paper, we follow Van Marrewijk(2003) who proposes a distinction between five different ambition levels for socialresponsibility: ”compliance-driven” ”profit-driven” ”caring” ”synergistic” and”holistic”; a distinction which we find relevant with regard to the differentstakeholders of the company.

Freeman (1984, p. 25) defines a ”stakeholder” as “Any group or individual who canaffect or is affected by the achievement of the firm’s objectives”. According to Freemanthe primary stakeholders are those who have a legitimate interest in the company, i.e.investors, employees and customers. Competitors, distributors, local society, interestgroups, media and society are secondary stakeholders. Stakeholder management is aconcept which can be used to understand and manage internal and external changes(Freeman, 1984, p. 52). Freeman distinguishes three different perspectives or levels: therational level, the procedural level and the transactional level. He gives severalexamples to illustrate how the lack of coherence between the goals, strategy andprocesses and the lack of consistency in the messages sent out by the organizationinternally and externally, creates problems in the interaction and communication withthe stakeholders. Freeman stresses that stakeholder management is a voluntaryconcept. However, according to Freeman organizations with an expressed stakeholdermanagement capability develop and implement communication processes with manydifferent stakeholder groups, negotiate with stakeholders about critical issues and aimto sign voluntary agreements with them. The stakeholder model can be used to

CCIJ12,1

28

describe the company, but it can also be used as a means to obtain economic results,stability and growth. Finally, the model can be used normatively – morally orethically – as it shows how companies should treat stakeholders (Donaldson andPreston, 1995).

The European Commission also links CSR to the stakeholder approach. CSR is aconcept whereby companies integrate social and environmental concerns in theirbusiness operations and in their interactions with their stakeholders on a voluntarybasis (EU Commission, 2001, p. 6). The definition is used by leading companies inEurope and is considered as the basis of the European CSR policy. Danish companiestend to focus on the social dimension. Rendtorff (2003, p. 43) explains that ideas aboutsocial responsibility are not as developed in Europe as they are in the USA where thereis ethical legislation. However, in Denmark there is a strong tradition for socialresponsibility and individual concerns, which is seen as a result of the cultural andhistorical heritage and the structure on the labor market. According to Rendtorff thisaspect has led to a situation where the focus is no longer solely on shareholder valueand the bottom line. The different perspectives on CSR are a big challenge to thecompanies. Reporting is a good example of this challenge.

CSR reporting challengesThe emergence of non-financial reporting can be seen as an attempt to increasetransparency with respect to corporate actions concerning social and environmentalissues. A range of certificates and auditing procedures has emerged such as the triplebottom line and sustainability accounting, which goes beyond financial accountingand includes social and environmental performance. In Denmark, for example, theglobal reporting initiative (GRI) has helped some companies become better. However,CSR and CSR reporting are voluntary concepts which weakens the impact of the GRI.In general, much time and effort are spent selecting indicators and producingnon-financial reports. In this context, we find it interesting to investigate whatcompanies actually say and how they say it.

CSR is a contextual concept which fundamentally is a question about the relationsbetween the company and its environment. The concept becomes operational when itmeets the specific stakeholders and their expectations. This meeting opens up apotential conflict as the concept of social responsibility is about ethics and values andcontains an implicit demand for a solution (Thyssen, 2004, p. 127). One question raisedis, for example: is this new agenda beneficial for society (Knudsen, 2006)? Knudsen(2006) states that from a societal perspective it is beneficial that corporations and civilsociety participate in solving problems which governments may be unable to handle.Without active involvement on their part core problems might not be addressed.However, according to Knudsen (2006) a key issue to address from a societalperspective is: who should set priorities? A general assumption is that to the greatestpossible extent, democratically elected representatives should set the overall prioritiesconcerning corporate responsibility initiatives with respect to the environment, humanrights, etc. How else can one ensure that priorities reflect the priorities of the electorate?Another question is how much it is reasonable to ask of companies? Having thisscenario in mind it is interesting to see how companies tacle this dilemma whenreporting on CSR. In principle, there are no limits to social responsibility. Therefore,the main challenge for the organizations is to manage the mutual expectations.

Reporting CSR

29

The company can, for example, do so by entering into a stakeholder dialogue and byadopting specific rules or guidelines for the communication with the stakeholders.These rules may concern reporting standards, deadlines, etc. The form and content ofthe communication depend on contextual elements such as the size of the company, thespecific stakeholder groups, the complexity of the issue, the ambition level and thenature of the engagement specified by the company.

Another challenge consists in motivating CSR initiatives which in practice means thatthe company must be able to explain to internal and external stakeholders why it is logicalor necessary for the company to assume a social responsibility. Being socially responsibleis not evident to companies which operate on ordinary market terms. This explication isimportant in order to be credible. If, for example, CSR initiatives cost money, the companymust be able to explain to the stakeholders – owners/investors, in particular – why theseinitiatives are necessary and in which way they will lead to business privileges.

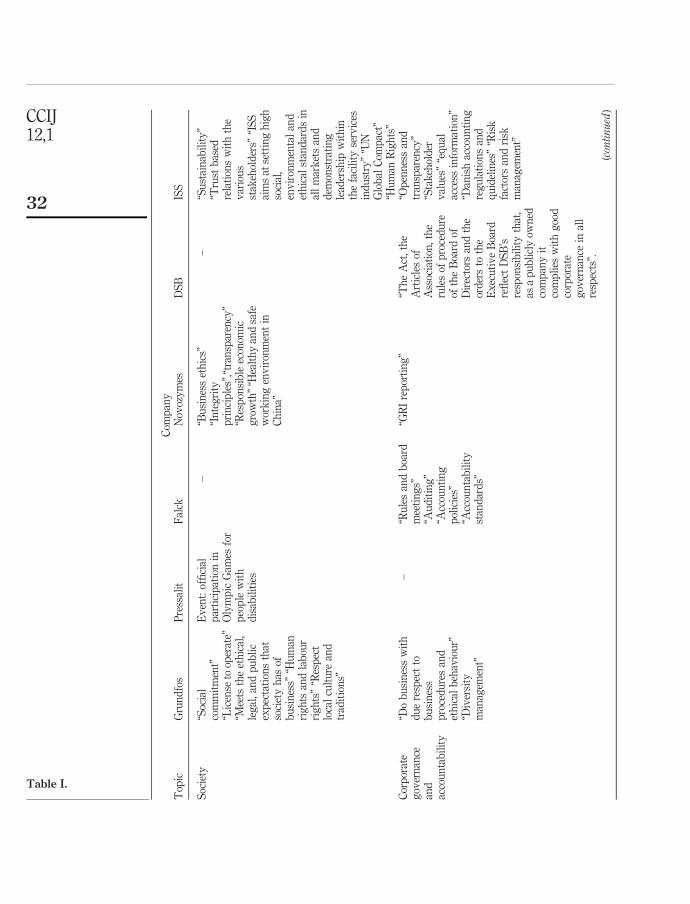

AnalysisIn the following section we shall examine the reporting strategies applied by the sixselected companies in their 2004 annual accounts from a rhetorical and discursive pointof view. Firstly, a semantic topic analysis may serve to point out the CSR issues whichthe reporting companies have emphasized (Table I). This preliminary analysis gives usa rough idea of the reporting companies’ identity and self-understanding as CSRpioneers and CSR caring organizations. Secondly, an analysis of textual and rhetoricalfeatures, such as the use of perspective, priorities, ambition level, etc. will give a morein depth picture of the discourse strategies adopted by the organizations, which allowsus to identify the power relations and the interaction patterns between theorganizations and their stakeholders (Table II). Table III shows our identification of thediscourse types related to each of the CSR topics found in the reports and based on ourinterpretation of the rhetorical features in Table II.

Figure 1 shows our approach which sees discourse as a result of four kinds ofchallenges related to:

(1) globalization;

(2) the role of business in society (people, planet, profit);

(3) the relations to the stakeholders; and

(4) the CSR ambition level of the company.

The annual reports of the six companies are very dissimilar with respect to scope,content, structure, etc. The explanation is that the contexts of the companies aredifferent. As a former division of Novo Nordisk, Novozymes shares, for example, itsearly reporting history with Novo Nordisk (Knudsen, 2006). In 1993 Novo Nordiskmade its first environmental report, and in 1998 the company also began to produce asocial report. In 1999, the social and environmental reports were merged into asustainability report with its annual report. The company now has one integratedreport. Novo Nordisk is the only Danish company with reports in accordance with theGRI. In general, corporate views of the GRI differ. Some use GRI as a source ofinspiration, while others view it as the best available reporting tool.

Table I shows a selection of textual fragments from the annual reports of the sixcompanies categorized according to topics which we consider crucial for the

CCIJ12,1

30

Com

pan

yT

opic

Gru

nd

fos

Pre

ssal

itF

alck

Nov

ozy

mes

DS

BIS

S

Em

plo

yee

s“R

esp

onsi

bil

ity

tow

ard

sou

rem

plo

yee

s”“S

ecu

rew

ork

ing

env

iron

men

t”“W

orld

ofeq

ual

opp

ortu

nit

ies”

Ev

ent:

Gar

den

par

ty(o

pen

ing

ofn

ewg

ard

en)

“Wor

kin

gen

vir

onm

ent”

(in

env

iron

men

tse

ctio

n)

“Ret

enti

onan

dd

evel

opm

ent

ofem

plo

yee

s”“E

mp

loy

eesa

tisf

acti

onan

aly

sis”

“Com

pet

ence

dev

elop

men

tac

tiv

itie

s”

“Par

tici

pat

ion

in“D

enm

ark

’sb

est

wor

kp

lace

surv

ey”

“Hea

lth

and

safe

ty”

“Gen

der

dis

trib

uti

on”

“Loy

alan

dm

otiv

ated

emp

loy

ees”

“tra

inin

gan

dle

arn

ing

”“E

qu

alp

roje

ctab

out

soci

alre

spon

sib

ilit

y”

“Pla

cem

ent

for

the

dis

able

d”

“Eq

ual

opp

ortu

nit

ies”

“Foc

us

onin

div

idu

alca

pac

ity

”“I

SS

isto

day

anem

plo

yer

ofch

oice

for

man

yim

mig

ran

tsan

det

hn

icm

inor

itie

s”.

Loc

alco

mm

un

ity

“Ag

reem

ent

ofp

artn

ersh

ipw

ith

loca

lin

stit

uti

ons

“In

teg

rati

onp

roje

ct:

spon

sors

hip

oflo

cal

spor

tscl

ub

”

––

––

En

vir

onm

ent

“Su

stai

nab

ilit

yw

alk

sh

and

sin

han

d...

”

“Red

uct

ion

and

pre

ven

tion

ofp

ollu

tion

”“C

erti

fied

inac

cord

ance

wit

hth

ein

tern

atio

nal

stan

dar

d”

“Air

pol

luti

on,

noi

cean

dso

ilp

ollu

tion

”

“Ob

ject

ives

for

sust

ain

abil

ity

”“R

ecy

clin

gan

dco

mp

lian

cew

ith

env

iron

men

tal

stan

dar

ds”

“An

env

iron

men

tal-

frie

nd

lyfo

rmof

tran

spor

tw

ith

the

leas

tp

ossi

ble

env

iron

men

tal

imp

act”

(air

pol

luti

on,

noi

seco

nd

itio

ns,

soil

pol

luti

on)

“En

vir

onm

enta

lp

rote

ctio

n”

“Su

stai

nab

led

evel

opm

ent”

“Min

imis

eem

issi

ons

and

effl

uen

ts,

red

uce

,m

anag

ean

dre

cycl

ew

aste

,u

sesa

fep

rod

uct

san

dm

ater

ials

” (continued

)

Table I.Topical analysis

Reporting CSR

31

Com

pan

yT

opic

Gru

nd

fos

Pre

ssal

itF

alck

Nov

ozy

mes

DS

BIS

S

Soc

iety

“Soc

ial

com

mit

men

t”“L

icen

seto

oper

ate”

“Mee

tsth

eet

hic

al,

leg

al,

and

pu

bli

cex

pec

tati

ons

that

soci

ety

has

ofb

usi

nes

s”“H

um

anri

gh

tsan

dla

bou

rri

gh

ts”

“Res

pec

tlo

cal

cult

ure

and

trad

itio

ns”

Ev

ent:

offi

cial

par

tici

pat

ion

inO

lym

pic

Gam

esfo

rp

eop

lew

ith

dis

abil

itie

s

–“B

usi

nes

set

hic

s”“I

nte

gri

typ

rin

cip

les”

,“tr

ansp

aren

cy”

“Res

pon

sib

leec

onom

icg

row

th”

“Hea

lth

yan

dsa

few

ork

ing

env

iron

men

tin

Ch

ina”

–“S

ust

ain

abil

ity

”“T

rust

bas

edre

lati

ons

wit

hth

ev

ario

us

stak

ehol

der

s”“I

SS

aim

sat

sett

ing

hig

hso

cial

,en

vir

onm

enta

lan

det

hic

alst

and

ard

sin

all

mar

ket

san

dd

emon

stra

tin

gle

ader

ship

wit

hin

the

faci

lity

serv

ices

ind

ust

ry”

“UN

Glo

bal

Com

pac

t”“H

um

anR

igh

ts”

Cor

por

ate

gov

ern

ance

and

acco

un

tab

ilit

y

“Do

bu

sin

ess

wit

hd

ue

resp

ect

tob

usi

nes

sp

roce

du

res

and

eth

ical

beh

avio

ur”

“Div

ersi

tym

anag

emen

t”

–“R

ule

san

db

oard

mee

tin

gs”

“Au

dit

ing

”“A

ccou

nti

ng

pol

icie

s”“A

ccou

nta

bil

ity

stan

dar

ds”

“GR

Ire

por

tin

g”

“Th

eA

ct,

the

Art

icle

sof

Ass

ocia

tion

,th

eru

les

ofp

roce

du

reof

the

Boa

rdof

Dir

ecto

rsan

dth

eor

der

sto

the

Ex

ecu

tiv

eB

oard

refl

ect

DS

B’s

resp

onsi

bil

ity

that

,as

ap

ub

licl

yow

ned

com

pan

yit

com

pli

esw

ith

goo

dco

rpor

ate

gov

ern

ance

inal

lre

spec

ts”.

“Op

enn

ess

and

tran

spar

ency

”“S

tak

ehol

der

val

ues

”“e

qu

alac

cess

info

rmat

ion

”“D

anis

hac

cou

nti

ng

reg

ula

tion

san

dq

uid

elin

es”

“Ris

kfa

ctor

san

dri

skm

anag

emen

t”

(continued

)

Table I.

CCIJ12,1

32

Com

pan

yT

opic

Gru

nd

fos

Pre

ssal

itF

alck

Nov

ozy

mes

DS

BIS

S

Bu

sin

ess

stra

teg

y–

“Eco

nom

icsu

stai

nab

ilit

y”

“Bot

tom

-lin

ed

evel

opm

ent”

“Mar

ket

dev

elop

men

t”“p

rod

uct

inn

ovat

ion

”

“Pro

du

ctin

nov

atio

n”

“Aw

ell

exec

ute

dd

eliv

ery

”(p

un

ctu

alit

y)

Mea

sure

men

t“C

erti

fied

toth

eS

ocia

lIn

dex

”–

“Job

sati

sfac

tion

”–

“An

nu

alem

plo

yee

sati

sfac

tion

anal

yse

s”“A

pp

lica

tion

ofB

alan

ced

Sco

reca

rdco

nce

pt”

Sco

pe

ofg

ener

alan

nu

alre

por

t

Ear

nin

gs,

gro

wth

,g

lob

alco

rpor

ate

soci

alre

spon

sib

ilit

y,

env

iron

men

t

Glo

bal

isat

ion

,fi

nan

cial

gro

wth

,fi

nan

cial

,in

nov

atio

nan

dp

rod

uct

s,b

usi

nes

sst

rate

gy

Bu

sin

ess

area

s,R

isk

fact

ors,

fin

anci

alre

vie

w

Su

stai

nab

ilit

y,

wor

ken

vir

onm

ent,

stak

ehol

der

app

roac

h

Ser

vic

es,

Bu

sin

ess

area

s,C

omm

erci

alan

dfi

nan

cial

risk

fact

ors,

Effi

cien

cy(v

alu

es),

cust

omer

sas

stak

ehol

der

s

Cor

por

ate

gov

ern

ance

,cl

ear

stak

ehol

der

app

roac

hin

clu

din

gso

ciet

alco

nce

rn

Ed

itor

ial/

CS

Rþ

––

þ(s

ust

.)–

–S

ocia

lre

por

tþ

––

þ–

–M

enu

onw

ebsi

te“A

bou

tu

s”“D

ocu

men

tati

on”

“Fac

t&

Fig

ure

s”“I

nv

esto

rre

lati

ons”

“Ab

out

us”

”pu

bli

cati

ons”

“In

ves

tor

rela

tion

s”–

Table I.

Reporting CSR

33

Dim

ensi

ons

Dis

cou

rse

elem

ents

Com

pan

yP

ersp

ecti

ve

Sta

keh

old

erp

rior

itie

sC

onte

xt

Am

bit

ion

Nar

rati

ve

scen

ario

Mai

nd

isco

urs

e

Gru

nd

fos

Str

ong

trip

leb

alan

ceap

pro

ach

asa

stri

vin

gp

aram

eter

for

doi

ng

bu

sin

ess

Str

ong

stak

ehol

der

focu

sw

ith

emp

has

ison

emp

loy

ees

and

cust

omer

s

Glo

bal

–n

atio

nal

and

inte

rnat

ion

alm

ark

etle

ader

,st

ron

gC

EO

pro

file

and

loca

lco

mm

itm

ent

Hol

isti

can

dca

red

riv

enIn

div

idu

al,

care

and

soci

etal

com

mit

men

tar

efu

nd

amen

tal

tosu

stai

nab

leth

ink

ing

and

mu

stb

ere

flec

ted

inev

ery

acti

vit

yof

bu

sin

ess

Ind

ivid

ual

care

,so

cial

resp

onsi

ble

and

soci

etal

dis

cou

rse

Pre

ssal

itS

tron

gfo

cus

onp

rofi

tan

dp

eop

lein

aan

org

anis

atio

nal

and

loca

lp

ersp

ecti

ve

Cu

stom

erp

rior

ity

and

emp

loy

eeco

nce

rnL

ocal

–sm

all

com

pan

yw

ith

stro

ng

loca

lro

ots

and

rela

tion

sto

loca

lco

mm

un

ity

net

wor

ks

Pro

fit

and

care

dri

ven

Pro

du

ctin

nov

atio

nan

dg

lob

alm

ark

etor

ien

tati

onar

ek

eyd

riv

ers

inb

usi

nes

s.H

owev

er,

soli

db

usi

nes

sm

ust

incl

ud

est

imu

lati

ng

even

tsfo

rem

plo

yee

san

dlo

cals

Loc

alca

rean

dco

rpor

ate

mot

ivat

ion

dis

cou

rse

Fal

ckS

tron

gp

rofi

tp

ersp

ecti

ve

wit

hen

vir

onm

enta

lis

sues

asp

art

ofth

est

rate

gy

Inv

esto

ran

dp

ub

lic

cust

omer

orie

nta

tion

Inte

rnat

ion

alco

mp

any

,w

ith

nat

ion

alro

ots

and

nat

ion

alle

ader

pos

itio

n

Com

pli

ance

and

pro

fit

dri

ven

Gro

wth

and

dev

elop

men

tar

eca

nal

ised

thro

ug

hin

tern

atio

nal

exp

ansi

onan

dst

aff

trai

nin

g.

Pol

itic

alri

skfa

ctor

sd

ue

tosu

bm

issi

onto

pu

bli

cre

gu

lati

onar

eim

por

tan

tto

bea

rin

min

d

Glo

bal

isat

ion

dis

cou

rse,

Ris

kan

dco

mp

lian

ced

isco

urs

e

(continued

)

Table II.Rhetorical features

CCIJ12,1

34

Dim

ensi

ons

Dis

cou

rse

elem

ents

Com

pan

yP

ersp

ecti

ve

Sta

keh

old

erp

rior

itie

sC

onte

xt

Am

bit

ion

Nar

rati

ve

scen

ario

Mai

nd

isco

urs

e

Nov

ozy

mes

Tri

ple

per

spec

tiv

e,ec

onom

ic,

env

iron

men

tal

and

soci

alis

sues

inte

gra

ted

inth

eov

eral

lb

usi

nes

sst

rate

gy

Str

ong

stak

ehol

der

focu

s:cu

stom

er,

emp

loy

ee,

shar

ehol

der

san

din

ves

tors

Glo

bal

–n

atio

nal

and

inte

rnat

ion

alm

ark

etle

ader

,y

oun

gco

mp

any

Car

ean

dsy

ner

gis

tic

dri

ven

Eco

nom

icg

row

this

OK

bu

tco

nd

itio

ned

.G

row

thm

ust

go

han

din

han

dw

ith

the

env

iron

men

tal

and

hu

man

con

cern

.CS

Ris

par

tof

the

over

all

bu

sin

ess

stra

teg

y

Soc

ieta

lan

db

usi

nes

sd

riv

end

isco

urs

e

DS

BS

tron

gfo

cus

onp

rofi

tp

ersp

ecti

ve

Str

ong

shar

ehol

der

and

inv

esto

ror

ien

tati

on

Nat

ion

wid

eop

erat

oran

dn

atio

nal

tran

spor

tle

ader

wit

hm

onop

olis

tic

pos

itio

n

Com

pli

ance

and

pro

fit

dri

ven

Ear

nin

gst

abil

ity

,m

ark

etd

evel

opm

ent,

qu

alit

yan

def

fici

ency

are

key

dri

ver

san

dd

eter

min

eto

get

her

wit

hle

arn

ing

and

hig

hsk

ille

dem

plo

yee

sas

the

succ

ess

rate

ofb

usi

nes

s

Pri

mar

ily

bu

sin

ess

dri

ven

dis

cou

rse

ISS

Bal

ance

dap

pro

ach

bu

tw

ith

ap

rofi

tfo

cus

Str

ong

stak

ehol

der

focu

sw

ith

emp

has

ison

shar

ehol

der

san

din

ves

tors

Glo

bal

–n

atio

nal

lead

erin

the

pri

vat

ecl

ean

ing

ind

ust

ry,l

ong

his

tory

Com

pli

ance

and

pro

fit

dri

ven

Th

est

akeh

old

erap

pro

ach

isth

ek

eyd

riv

erfo

rd

oin

gb

usi

nes

s.IS

Sis

atr

ansp

aren

tco

mp

any

,ad

opti

ng

rule

san

dre

gu

lati

ons

acco

rdin

gto

inte

rnat

ion

alan

dn

atio

nal

stan

dar

ds

and

pre

-em

pts

risk

fact

ors

offi

nan

cial

,m

anag

eria

lan

dcu

ltu

ral

nat

ure

Pri

mar

ily

bu

sin

ess

dri

ven

dis

cou

rse

Table II.

Reporting CSR

35

considerations of companies’ reporting on CSR. The figure also indicates whether theannual reports are supplemented by separate social reports, editorials containing CSRissues and in which menu the reports are situated on the companies’ corporatewebsites. Our motivation for including these elements in our analysis is that theysignal the priority given to CSR by the companies we investigate.

In Table II the four dimensions in our analysis model are presented on the basis ofthe content and rhetorical elements of the reports in the left columns following the“company” column of Table II, while the right columns present the basic narrativescenario of the companies’ CSR reporting which allows us to discern the way the

Discourse orderSocial responsibility

Topic Profit maximation Discourse types

Employees Working resource Individual self-developmentLocal communitya Local partnershipsEnvironment Compliance Environmental-friendlySociety Stakeholder commitment Social commitmentCorporate governancea Financial accounting Ethical behaviour discourseMeasurementa CSR measurementCorporate web site structure Investor relations discourse Personal relations discourse

Note: aTopics which are absent in some of the reports

Table III.Discourseorders/discourse types

Figure 1.Analysis model

PERSPECTIVE

People Profit Planet

C

O

N

T

E

X

T

Marketposition

Global/Local

CEO/history

A

M

B

I

T

I

O

N

STAKEHOLDERS

Employees Customers

Suppliers Media NGO’s

Low

Middle

High

discourses

discourses

discourses

CSR

Reporting

discourse

universe

discourses

Shareholders

CCIJ12,1

36

companies stage the CSR issue and thereby construct the main discourse related to thisissue. Our analytical approach is thus to give the reader insight into our own process ofanalysis by illustrating our step-by-step interpretation of the reporting material withdue respect to contextual elements.

On the basis of our two-step analysis above showing how the companies in our casestudy stage the issue of CSR in terms of CSR topics, context and ambition, we are ableto discern a set of binary discourse patterns connected to each of the CSR topics, whichwe identify as discourse types. These discourse types reveal the angle from which thecompanies present the CSR topics in their reporting. If we choose the employee topic, itappears that the company may first and foremost consider their employees as aworking resource rather than as a group of individuals who work and perform in orderto constitute and develop their own self-identity. Society may be approached by thecompany as a power and control instance, putting pressure on the company in terms ofspecific stakeholder needs and demands to which the company has to respond in orderto prevent potential conflicts, but society may also be approached as an economic,social and political environment which in metaphorical terms constitutes thecompanies’ “family” to whom they have an obligation to care for the weakest ones bydemonstrating good corporate citizenship and so forth. The third step of our analysisbelow allows us to scrutinize two types of social orders: profit maximation and socialresponsibility referred to as discourse orders in correspondence to Fairclough (1995).

In order to clarify and demonstrate how the above discourse orders function and aretextually and rhetorically staged, we will take a closer look at the ways in which thetopic of employees and society are approached in the reports of Grundfos. A quickglance at Grundfos’ reporting material indicates that the company seems to be highlyconcerned with social aspects of employees and of society in general. Through the useof linguistic and rhetorical features, Grundfos demonstrates an overall caring andresponsible approach to dealing with people in general. In the editorial from the socialreport, the initial statement of the Managing Director Lars Aagaards is:

We are responsible towards our employees and the communities that surround us. This iswhy we are convinced that as a company we have a social responsibility. At Grundfos wedevelop standards and go beyond the expected in our commitment as a socially responsiblecompany.

Apart from the concrete use of the concept of “social responsibility” concepts such as“commitment” and “beyond the expected” seem to reveal that Grundfos has explicitlychosen to pinpoint the issue of CSR as a fundamental part of the company’s businessstrategy. The presentation of the employee topic is approached with significantconcern for the human aspects of the working life as is shown by the following quote:

Our employees are people – human beings – with ideas, a sense of commitment, needs,desires, a sense of responsibility, skills and competences and – sometimes – problems. Ouremployees are not just resources like machinery, buildings and capital – on the contrary; byvirtue of its complexity, any human being has numerous potentials. Our employees thriveand demonstrate their satisfaction because their jobs and working conditions provide themwith great opportunities for professional and personal growth and development.

What we note in this example is the way Grundfos describes its human resources byusing terms such as employees’ “needs” “desire” “sense of responsibility” and even“problems” thus showing that the company has explicit consideration for the personal

Reporting CSR

37

dimension of employees. This consideration is further stressed by the strong emphasison argumentative markers such as “not just – on the contrary” where the first point ofview (human resources are considered as machinery, building and capital) is stronglyoverruled and replaced by the contrary point of view (human resources are complexand considered as an individual potential which develops itself through working).

If we move on to the topic of society, we realise that social, societal commitment andresponsibility are equally embedded in Grundfos’ reporting discourse. Firstly, we learnthat “diversity among people is a chance to reveal new possibilities and unknowncompetences”. Secondly, the social report states that Grundfos has always paidparticular attention to “responsibility and social inclusion”. This choice of vocabularysignals that Grundfos is totally aligned to the terminology of the Danish Governmentfor whom the program of “social inclusion” has been on the political agenda for severalyears and to whom the collaboration with pioneer businesses, who can take active partin solving the integration problems due to a high rate of unemployment amongimmigrants, is crucial. Grundfos also demonstrates a similar concern when it comes tothe local community stating that “our global presence must be in harmony with thelocal surroundings and the people whose lives and conditions we have influence on”.The company hereby indicates that doing business constitutes a dilemma in the sensethat it provides power and influence over peoples’ lives and conditions and that thecompany has to act responsibly in order to overcome the conflict which arises from thisdilemma.

In other words, even though Grundfos seems to reflect a highly consistent CSRreporting style, it is possible to detect traces of discrepant discourse elements.However, thanks to the concentration of rhetorical features emphasizing the caring andsocietal perspectives of Grundfos’ reporting strategies, this company may be said tostand out when it comes to communicating social and societal commitment. The CSRreporting of Grundfos thus undeniably articulates a discourse order of genuine socialresponsibility. At the other end of the scale of the CSR reporting companies discussedin our analysis, we note in particular the two service companies, DSB and ISS which, inspite of their acknowledged position as good business practice companies, may beranked at a lower ambition level and at an earlier CSR stage than their Danishcolleagues.

Concluding remarks: reporting consistently on CSRWe have raised the question whether organizations report consistently on CSR in termsof genre, media, rhetorical strategies, etc.

Our case study shows that the annual reports of the six Danish companies are verydissimilar with respect to topics on the one hand and dimensions and discoursesexpressed in terms of perspectives, stakeholder priorities, contextual information andambition levels on the other hand. It is clear that the six companies use differentstrategies for reporting on CSR. CSR relevant topics selected are: employees, localcommunity, environment, society, corporate governance and accountability, businessstrategy, measurement of CSR initiatives. However, some companies focus more onsome topics than on others. We noted that some of the six companies find it relevant tomention how CSR is measured and to present CSR initiatives in the editorial.Furthermore, it appeared that the six companies have different entries to the annualreport (and the social report) on their websites. For some companies the entry is under

CCIJ12,1

38

“About us” for others it is under “Investor relations”. Our analysis documents that thesix companies also use different rhetorical strategies. Some companies focus on profit,whereas others focus on people. Some companies pinpoint customer stakeholders,whereas others pinpoint employee stakeholders. Some companies areglobally-oriented, whereas others are locally-oriented. Some companies have a highCSR ambition level, whereas others have a low ambition level. Consequently, thenarrative scenario and the main discourse vary from one report to another. Ouranalysis of the topics, dimensions and discourses has allowed us to discern a set ofbinary discourse patterns connected to each of the CSR topics, which we haveidentified as discourse types. These discourse types reveal the angle from which thecompanies present the CSR topics in their reporting. Some companies consider aboveall their employees as a working resource, whereas others consider them above all as agroup of individuals who work and perform in order to develop their own self-identity.On the basis of the analysis of discourse types we have scrutinized two types of socialorders, i.e. the public discourse on social responsibility and the business discourse onprofit maximation or strategy referred to as discourse orders in correspondence toFairclough (1995). Our analysis of one of the companies’ reporting material (Grundfos),shows that it is possible to report consistently (in terms of terminology, rhetoricalstrategies, etc.) according to one of the two types of discourse orders, here the publicdiscourse on social responsibility. In other words, in order to report consistently onCSR companies need to use discourse types which represent perspectives pointingmore or less in the same “direction”.

But how can we analyse these differents strategies and discourse orders from amodern organizational and corporate communication perspective? According toCornelissen (2004, p. 9) the future of any one company in today’s society dependscritically on how it is viewed by key stakeholders such as shareholders and investors,customers and consumers, employees and members of the community in which thecompany resides. Thus, companies need to build and nurture relationships withstakeholders, and they must know how to strategically manage and organize activitiesaimed at their stakeholders. Reporting is one of the activities used by companies in astrategic and instrumental manner. It makes sense to contemplate it as a corporatecommunications tool which helps companies to be judged as “legitimate” by most, ifnot all, of their stakeholders in order to survive and prosper. Conceived as a corporatecommunications tool, annual reports and other reports must focus on the organizationas a whole and the task of how an organization is presented to all of its keystakeholders, both internal and external. In this light it is crucial to know how to reportconsistently on CSR. Our contribution has been to highlight the value of the discourseand the discourse types adopted in the reporting material. By adopting consistentdiscourse types which interact according to a well-defined pattern or order it is possibleto communicate a strong social commitment on the one hand and take intoconsideration the expectations of the shareholders and of the other stakeholders on theother hand.

References

Andriof, J., Waddock, S., Husted, B. and Rahman, S.R. (Eds) (2003), Unfolding StakeholderThinking, Greenleaf Publishing, Sheffield.

Reporting CSR

39

Carroll, A.B. (1991), “The pyramid of corporate social responsibility: toward the moralmanagement of organizational stakeholders”, Business Horizons, Vol. 34, pp. 39-48.

Carroll, A.B. (1999), “Corporate social responsibility, evolution of a definitional construct”,Business & Society, Vol. 38 No. 3, pp. 268-95.

Committee for Economic Development (1971), “Social responsibilities of business corporations”,A statement on national policy by the Research and Policy Committee for EconomicDevelopment, June 1971, Committee for Economic Development, New York, NY.

Cornelissen, J. (2004), Corporate Communications, Theory and Practice, Sage, London.

Donaldson, T. and Preston, L.E. (1995), “The stakeholder theory of the corporation: concepts,evidence, and implications”, Academy of Management Review, Vol. 20 No. 1, pp. 65-91.

EU Commission (2001), Greenpaper on Corporate Social Responsibility, EU Commission, Brussel.

Fairclough, N. (1995), Critical Discourse Analysis, Longman, London.

Freeman, R.E. (1984), Strategic Management: A Stakeholder Approach, Pitman, Boston, MA.

Friedman, M. (1970), “The social responsibility of business is to increase its profits”, The NewYork Times Magazine, September, p. 13.

Knudsen, J.S. (2006), “The global reporting initiative in denmark: emperor’s new clothes or usefulreporting too?”, in Morsing, M. and Kakabadse, A. (Eds), Corporate Social Responsibility.Reconciling Aspiration with Application, Palgrave Macmillan, Hampshire, pp. 129-39.

Rendtorff, J.D. (2003), “Værdibaseret ledelse og socialt ansvar. Aspekter af virksomhedernesgode statsborgerskab”, Økonomi og Politik, No. 3, Jurist- og Økonomforbundets Forlag,Copenhagen.

Thyssen, O. (2004), Værdiledelse: om organisationer og etik, Gyldendal, Copenhagen.

Van Marrewijk, M. (2003), “Concepts and definitions of CSR and corporate sustainability:between agency and communion”, Journal of Business Ethics, Vol. 44, pp. 95-105.

Waddock, S. (2004), “Parallel universes: companies, academics, and the progress of corporatecitizenship”, Business and Society Review, Vol. 109 No. 1, pp. 5-42.

Further reading

Frederiksen, J., Honore, C. and Tost, F. (2003), Rapportering om Bæredygtighed, Børse,Copenhagen.

Corresponding authorAnne Ellerup Nielsen can be contacted at: [email protected]

CCIJ12,1

40

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

Dear Dr Anne Ellerup Nielsen, We are delighted to inform you that Reporting CSR – what and how to say it? has been selected for inclusion in Emerald Reading ListAssist; Emerald’s free, unique, peer-reviewed reading list service provided to all Emerald subscribers. These comprehensive, subject-specific reading lists have been compiled by faculty experts and facilitate both teaching and learning, whilst further increasing the dissemination of your work. The service, launched today, is comprised of a collection of 50 reading lists and accompanying editorials, covering subjects across Emerald’s portfolio areas. Each reading list contains 60-80 Emerald articles and has filterable data markers that help the user to refine content searches. These indicators provide information on the article's practical, literary and pedagogical features, allowing for fast, easy and idiosyncratically-led content searches. To find out more please visit the ListAssist area of the Emerald website, or get in touch at [email protected] Kind regards, Anna Young Reading ListAssist Manager Emerald Group Publishing Limited [email protected] http://www.emeraldinsight.com

Data protection:

Emerald Group Publishing Limited is contacting you at the following address - [email protected]

If you prefer not to receive this email, please Unsubscribe.

Mail filter: If your ISP filters incoming email, please add the following email domain to your list of approved senders:

emeraldinsight.com. This will ensure that you receive the alerts and newsletters to which you have

subscribed.

Contact us: If you have any questions or comments regarding this email, please contact: [email protected]

© Emerald Group Publishing Limited | Copyright Info | Site Policies Registered Office: Howard House. Wagon Lane, Bingley, BD16 1WA, UK, Registered in England No. 3080506, VAT No.

GB 665 3593 06 http://www.emeraldinsight.com

Related Documents