Copyright © 2016 Burkert Valuation Advisors, LLC. All rights reserved. Do not duplicate or copy without permission. If you are here for … REPORT WRITING: THE FINAL FRONTIER IN BV PRODUCTIVITY You’re in the right place!

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright © 2016 Burkert Valuation Advisors, LLC.All rights reserved. Do not duplicate or copy without permission.

If you are here for …

REPORT WRITING: THE FINAL FRONTIER IN BV PRODUCTIVITY

You’re in the right place!

Copyright © 2015 Thought Leaders IP, Inc. & Rod Burkert All Rights Reserved. Do not duplicate or distribute without permission. Visit PracticeBuilderAcademy.com.

REPORT WRITING: THE FINAL FRONTIER IN BV PRODUCTIVITY

Rod Burkert, CPA, CVA, ABV

I am the founder of Burkert Valuation Advisors. I’ve reinvented my practice several times after going solo in July 2000. In my latest iteration, I have built a mobile consulting firm by leveraging social media and my professional network. Since March 2010, I have worked a “traditional practice” while traveling full time throughout the United States and Canada in an RV with my wife and our dogs.

who am i

where my reports are written

i’m direct & to the point no offense intended

i run fast tell me when to brake

Copyright © 2015 Thought Leaders IP, Inc. & Rod Burkert All Rights Reserved. Do not duplicate or distribute without permission. Visit PracticeBuilderAcademy.com.

REPORT WRITING: THE FINAL FRONTIER IN BV PRODUCTIVITY

why report writing is critical

✦ carries the valuation analysis

✦ reflects on your reputation as a professional

✦ can help establish you as a subject matter expert, if not an authority

✦ way to fight battle in war of fee compression

what makes a good report great

✦ based on solid valuation analysis

✦ tells a story ✓ well written ✓ easy to follow ✓ unbiased

✦ leaves the reader confident in the conclusion

✦ complies with professional standards

puzzle pieces of great report writing

content

layout

grammar

style

WHOWHATWHEN

WHEREWHYHOW

WHO are you writing for

caveat scriptor (writer beware)

✦ biggest factor affecting report length is who you are writing for ✓ informed user: IRS, audit firm ✓ uninformed user: family law judge

✦ a 30-40 page report body should cover it ✓ i will show you how to get there

WHAT should you be writing

focus of report narrative

✦ facts, circumstances, research, judgment, etc. belong in report body

✦ theory belongs in an appendix, regardless of who your reader is

✦ wacc example

focus of report narrative

✦ effect of each section on ✓ projected benefit stream ($) ✓ discount rate / valuation multiple (risk) ✓ growth (%) ✓ discounts and premiums

✦ so that each section supports your estimate of value … not your knowledge of valuation theory

WHEN should you be writing

not when you are tired

WHERE is innovation showing up

14

Valuation Approach - Discounted Cash Flow (“DCF”)

� A DCF Approach yields an indication of value of a business based on the present value of its expected future free cash flows.

� Pursuant to the Operating Agreement, the expected future cash flows of the Joint Venture include the free cash flow available for distribution generated from operations in 2013 and the liquidation value of the Joint Venture at February 28, 2014.

� The present value of Joint Venture’s 2013 free cash flow available for distribution and the liquidation value of the Joint Venture at February 28, 2014 are calculated using a discount rate resulting from a CAPM analysis (see Appendix A for details).

� To calculate the fair market value of the PLD Interest, Duff & Phelps multiplied the fair market value of the Joint Venture’s aggregate equity by 49%.

Valuation Analysis Valuation Approach

Present Value of Free Cash Flow Available

for Distribution

Present Value of Liquidation Free

Cash Flow Value of PLD Interest

2/5/2013 1/1/13 – 12/31/13 2/28/14

Confidential

15

� Duff & Phelps relied on the Joint Venture’s 2013 financial projections and the forecasted balance sheet as of February 28, 2014, as provided by the Client and Company representatives.

� The following key assumptions were used in the DCF analysis:

– Duff & Phelps assumed the resulting free cash flows for the 2013 period would be distributed at December 31, 2013.

– Duff & Phelps assumed the Joint Venture would be fully liquidated at February 28, 2014.

– Duff & Phelps assumed transaction costs equal to 2.5% of recoverable assets in the liquidation analysis.

– Duff & Phelps discounted the resulting free cash flows for the 2013 period and the net asset value resulting from the liquidation analysis at February 28, 2014 using a discount rate range of 11.5% to 13.5% (see Appendix A for details). Due to the relatively short discount period for the free cash flows (representing only 14 months), Duff & Phelps made the following assumptions in its calculation of the discount rate:

» Duff & Phelps utilized the Joint Venture’s current capital structure in the discount rate calculation, as opposed to a target capital structure.

» Duff & Phelps utilized a risk-free rate based on a 14-month treasury yield.

– In connection with a going-concern view of the business (i.e., long term horizon, with corresponding discount rate inputs), Duff & Phelps estimates an appropriate discount rate (weighted average cost of capital) would be in the range of approximately 13% - 16%.

Valuation Analysis Discounted Cash Flow Analysis (continued)

Confidential

16

Valuation Analysis Discounted Cash Flow Analysis (continued)

� The DCF analysis produces a fair market value of the Joint Venture ranging from $10.17 million to $10.34 million, with the midpoint value of approximately $10.26 million.

Discounted Cash Flow Analysis($ in thousands)

Valuation Date2/5/13 12/31/2013 (1) 2/28/2014 (2)

Free Cash Flow $10,241 $1,193

Discount Periods 0.91 1.06

Discount RateDiscount Factor 13.50% 0.89 0.87 Discount Factor 12.50% 0.90 0.88 Discount Factor 11.50% 0.91 0.89

TotalDiscounted FCF $10,174 $9,131 $1,043Discounted FCF $10,257 $9,205 $1,053Discounted FCF $10,342 $9,279 $1,063

(1) Represents the 2013 distributions paid as of or around 12/31/13.(2) Represents the projected cash flow s available from the liquidation analysis as of 2/28/14.

Confidential

17

Valuation Analysis Liquidation Analysis

� The liquidation analysis produces free cash flows of $1.19 million as of February 28, 2014, which, at 100% recovery rates on assets, is effectively the Joint Venture’s Members’ Equity net of assumed transaction costs.

Liquidation Analysis (1)($ in thousands)

2/28/14 Estimated Book Value Recovery

Accounts Receivable $3,000 $3,000

Inventory 8,500 8,500

Prepaid Expenses and Other CA 500 500

Net Fixed Assets 100 100

Other Assets 200 200

Cash and Short Term Investments 2,000 2,000

Recoverable Assets $14,300

Less: Transaction Costs (2) (358)

Net Assets $13,943Face Value of Debt $0 $0Accounts Payable 12,000 (12,000)Accruals & Other Current Liabilities 749 (749)

Liquidation Cash Flows $1,193

(1) Duff & Phelps assumed that in a liquidation, goodwill and intangible value were negligible.(2) Transaction costs are estimated to be 2.5% of recoverable assets.

Note: Per Company representatives, estimated balances as of 2/28/14 include two months of free cash flow (from 1/1/14 - 2/28/14)

Confidential

22

Weighted Average Cost of Capital

Confidential A - 1

Weighted Average Cost of Capital Analysis - Liquidation Analysis

Levered Beta Discount Rate Range Sources and Considerations

Unlevered Beta 0.90 1.10 Selected Public CompaniesDebt % of Capital 0% 0% Current Capital StructureEquity % of Capital 100% 100% Current Capital StructureTax Rate 40.0% 40.0% Blended Federal & State Corporate Income Tax Rate

Levered Beta 0.90 1.10

Levered Cost of Equity

Risk-free Rate 0.15% 0.15% 14-month Treasury yieldLevered Beta 0.90 1.10 See AboveMarket Risk Premium 5.5% 5.5% Duff & Phelps StudySmall Stock Premium 6.10% 7.38% Duff & Phelps Study; SBBI Valuation Edition 2012 Yearbook - Decile 10

Levered Cost of Equity 11.2% 13.6%

Cost of Debt

Cost of Debt 2.6% 2.6% 14-month B Bond RateTax Rate 40.0% 40.0% Blended Federal & State Corporate Income Tax Rate

After-tax Cost of Debt 1.6% 1.6%

Weighted Average Cost of Capital (WACC)

Debt % of Capital 0% 0%Equity % of Capital 100% 100%

Calculated WACC 11.20% 13.58%

Implied Midpoint WACC 12.50%

WHY bother changing

show me the money

HOW do you present it

report roadmap

appearance

✦ do not single space your text

✦ avoid the “zebra” effect

✦ font size 12 is the new 11

✦ most MS fonts are terrible

✦ great tips at typographyforlawyers.com

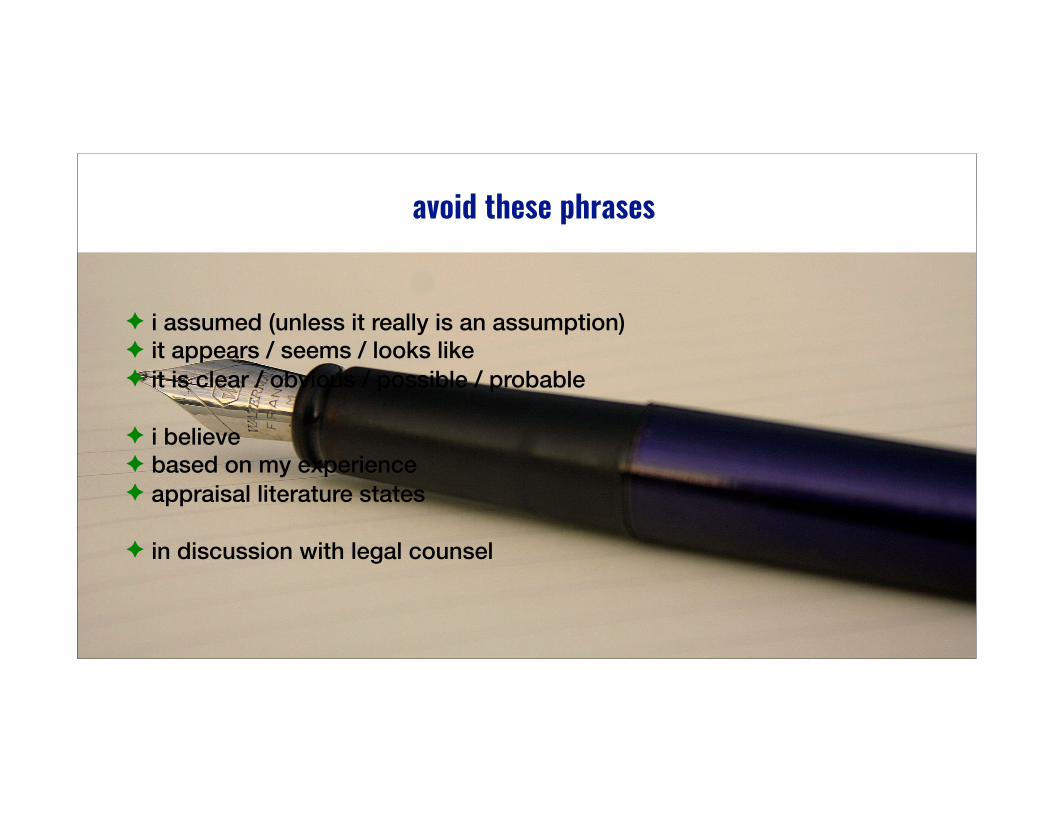

avoid these phrases

✦ i assumed (unless it really is an assumption) ✦ it appears / seems / looks like ✦ it is clear / obvious / possible / probable

✦ i believe ✦ based on my experience ✦ appraisal literature states

✦ in discussion with legal counsel

check for bias

✦ list all of your assumptions

✦ for each one … did it lead to higher/lower value

✦ is there a preponderance of assumptions leading to higher/lower value

✦ can you defend it

final thought

✦ most of us have a pretty good idea how our reports stack up ✓ where we're strong, where we're weak … ✓ and that can change from one report to the next ... ✓ but in general, we know

✦ best ways to improve the quality of a report is to have it reviewed ✓ by a respected peer (for content) ✓ by a technical editor (for grammar)

what is the most valuable thing you got out of today

Rod Burkert Building relationships … Creating value …. Having fun …So you can create a BVFLS practice you’ll love coming to and find success in

Cell: 215-360-6100Skype: rodburkertEmail: [email protected]: sign up at rodburkert.com

Related Documents