The Italian Insurance Market 2016 figures + 3M17 overview

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Italian Insurance Market

2016 figures + 3M17 overview

PwC

Italian insurance market snapshots

The Italian Insurance Market • 2016 figures + 3M17 overview

1

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

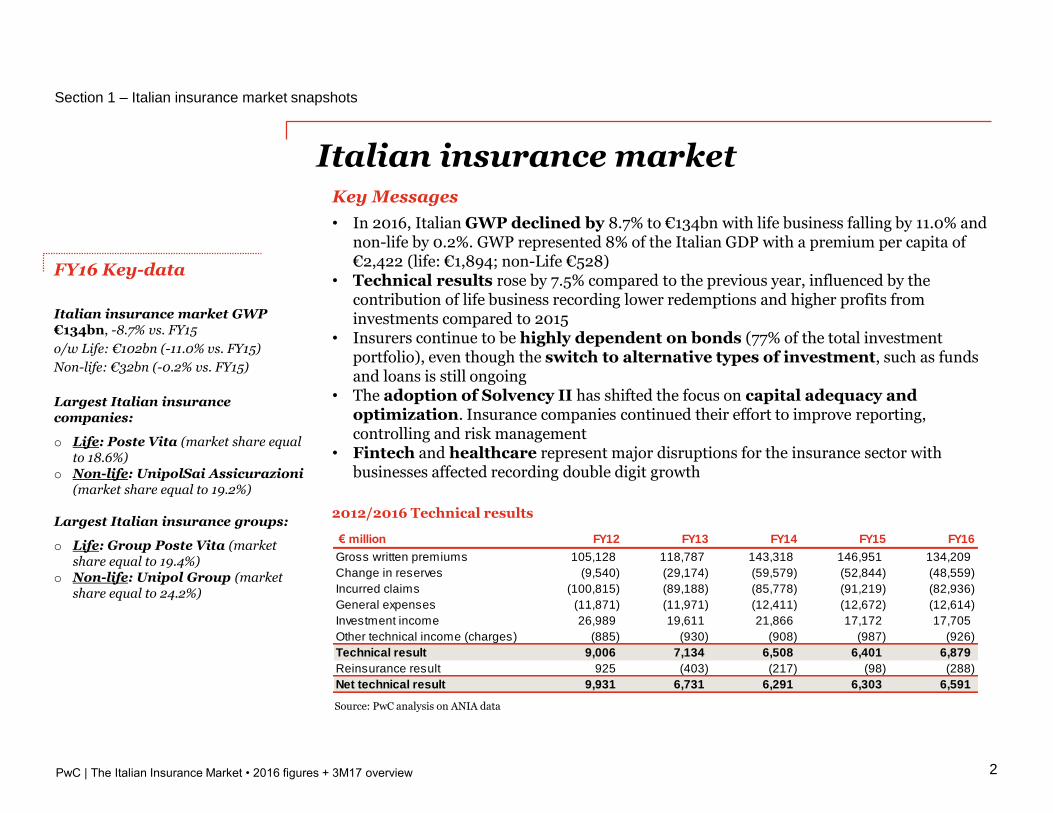

€ million FY12 FY13 FY14 FY15 FY16

Gross written premiums 105,128 118,787 143,318 146,951 134,209

Change in reserves (9,540) (29,174) (59,579) (52,844) (48,559)

Incurred claims (100,815) (89,188) (85,778) (91,219) (82,936)

General expenses (11,871) (11,971) (12,411) (12,672) (12,614)

Investment income 26,989 19,611 21,866 17,172 17,705

Other technical income (charges) (885) (930) (908) (987) (926)

Technical result 9,006 7,134 6,508 6,401 6,879

Reinsurance result 925 (403) (217) (98) (288)

Net technical result 9,931 6,731 6,291 6,303 6,591

Section 1 – Italian insurance market snapshots

2

Italian insurance market

FY16 Key-data

Italian insurance market GWP €134bn, -8.7% vs. FY15

o/w Life: €102bn (-11.0% vs. FY15)

Non-life: €32bn (-0.2% vs. FY15)

Largest Italian insurance companies:

o Life: Poste Vita (market share equal to 18.6%)

o Non-life: UnipolSai Assicurazioni (market share equal to 19.2%)

Largest Italian insurance groups:

o Life: Group Poste Vita (market share equal to 19.4%)

o Non-life: Unipol Group (market share equal to 24.2%)

Source: PwC analysis on ANIA data

Key Messages

• In 2016, Italian GWP declined by 8.7% to €134bn with life business falling by 11.0% and non-life by 0.2%. GWP represented 8% of the Italian GDP with a premium per capita of €2,422 (life: €1,894; non-Life €528)

• Technical results rose by 7.5% compared to the previous year, influenced by the contribution of life business recording lower redemptions and higher profits from investments compared to 2015

• Insurers continue to be highly dependent on bonds (77% of the total investment portfolio), even though the switch to alternative types of investment, such as funds and loans is still ongoing

• The adoption of Solvency II has shifted the focus on capital adequacy and optimization. Insurance companies continued their effort to improve reporting, controlling and risk management

• Fintech and healthcare represent major disruptions for the insurance sector with businesses affected recording double digit growth

2012/2016 Technical results

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

69,715 85,110

110,515 114,950 102,257

35,413

33,690

32,800 32,002

31,953 105,129 118,800

143,315 146,952 134,205

FY12 FY13 FY14 FY15 FY16

€m

illi

on

Life Non-Life

6%

80%

0%

14%

62%

22%

14% 1%

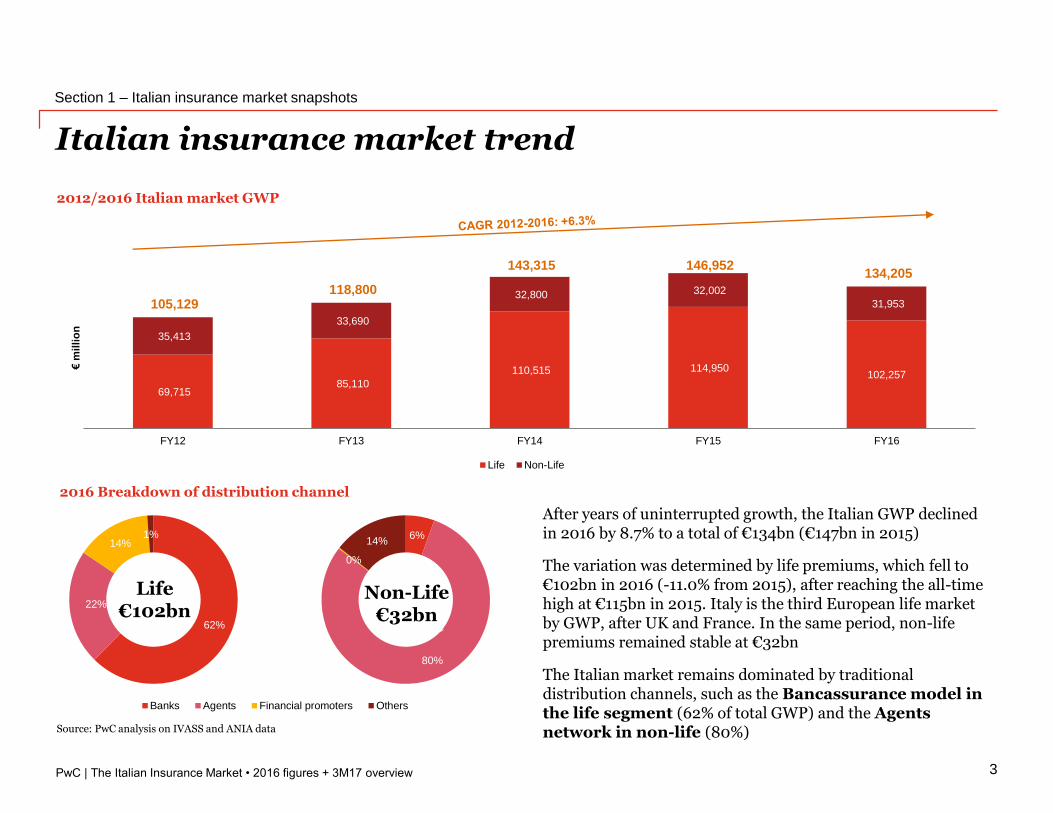

Italian insurance market trend

Section 1 – Italian insurance market snapshots

2012/2016 Italian market GWP

2016 Breakdown of distribution channel

Non-life

Source: PwC analysis on IVASS and ANIA data

After years of uninterrupted growth, the Italian GWP declined in 2016 by 8.7% to a total of €134bn (€147bn in 2015)

The variation was determined by life premiums, which fell to €102bn in 2016 (-11.0% from 2015), after reaching the all-time high at €115bn in 2015. Italy is the third European life market by GWP, after UK and France. In the same period, non-life premiums remained stable at €32bn

The Italian market remains dominated by traditional distribution channels, such as the Bancassurance model in the life segment (62% of total GWP) and the Agents network in non-life (80%)

Life€102bn

Non-Life€32bn

5%

81%

0%

14%

Non-Life market - Breakdown per distribution channel FY14

Banks Agents Financial promoters Others

3

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

19,820

10,437

7,844

5,480 4,587

19,820

18,016

14,947

6,550 6,323

18.6%

9.8%

7.4%

5.1%4.3%

19.4%

17.6%

14.6%

6.4% 6.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

5,000

10,000

15,000

20,000

Mark

et

sh

are

GW

P (€

mil

lio

n)

6,960

5,070

3,731

1,658 1,426

7,737

5,889

4,570

1,974 1,929

19.2%

14.0%

10.3%

4.6% 3.9%

24.2%

18.4%

14.3%

6.2% 6.0%

0%

5%

10%

15%

20%

25%

30%

-

3,000

6,000

9,000

12,000

15,000

Mark

et

sh

are

GW

P (€

mil

lio

n)

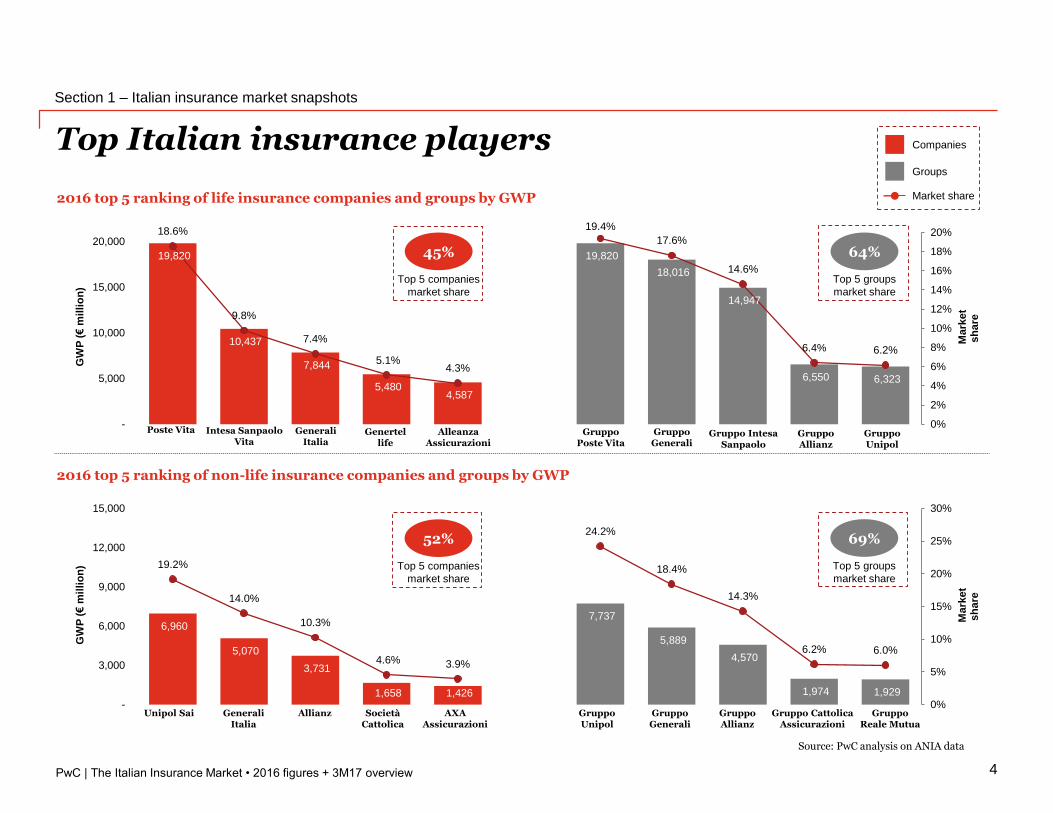

2016 top 5 ranking of life insurance companies and groups by GWP

Top Italian insurance players

Section 1 – Italian insurance market snapshots

4

2016 top 5 ranking of non-life insurance companies and groups by GWP

45%

Top 5 companies

market share

Source: PwC analysis on ANIA data

Poste Vita Genertellife

Intesa Sanpaolo Vita

Generali Italia

AlleanzaAssicurazioni

GruppoPoste Vita

GruppoGenerali

Gruppo Intesa Sanpaolo

GruppoAllianz

GruppoUnipol

Unipol Sai Generali Italia

Allianz AXAAssicurazioni

GruppoUnipol

GruppoGenerali

GruppoAllianz

Gruppo CattolicaAssicurazioni

GruppoReale Mutua

SocietàCattolica

64%

Top 5 groups

market share

52%

Top 5 companies

market share

69%

Top 5 groups

market share

Companies

Groups

Market share

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

Investments

Section 1 – Italian insurance market snapshots

5

2010/1H2017 main 5 European Government Bonds yield to maturity

Source: Bloomberg

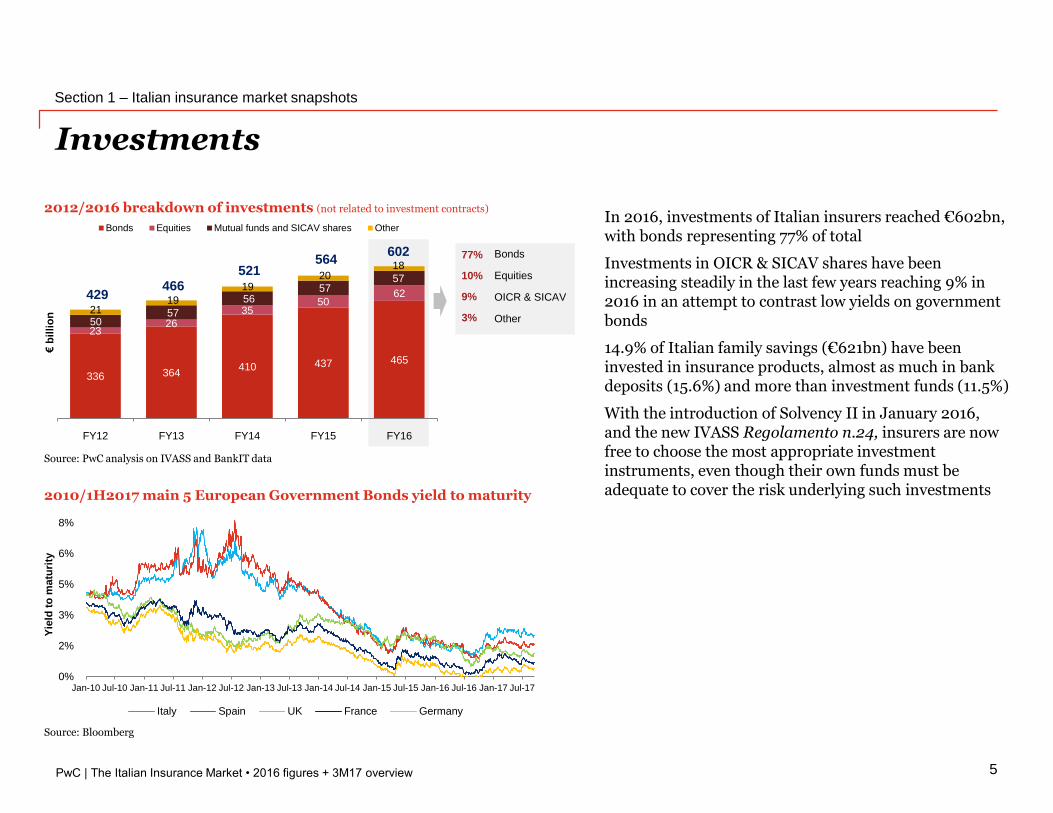

In 2016, investments of Italian insurers reached €602bn, with bonds representing 77% of total

Investments in OICR & SICAV shares have been increasing steadily in the last few years reaching 9% in 2016 in an attempt to contrast low yields on government bonds

14.9% of Italian family savings (€621bn) have been invested in insurance products, almost as much in bank deposits (15.6%) and more than investment funds (11.5%)

With the introduction of Solvency II in January 2016, and the new IVASS Regolamento n.24, insurers are now free to choose the most appropriate investment instruments, even though their own funds must be adequate to cover the risk underlying such investments

0%

2%

3%

5%

6%

8%

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

Yie

ld t

o m

atu

rity

Italy Spain UK France Germany

Source: PwC analysis on IVASS and BankIT data

3%

9%

10%

77%

Other

OICR & SICAV

Equities

Bonds

316 343 389 414 441

166

7574

7676

22 25

35 49

60

26 23

23 25

23

430 466

521 564

601

FY12 FY13 FY14 FY15 FY16

€b

illi

on

Bonds Equities Mutual funds and SICAV shares Other

2012/2016 breakdown of investments (not related to investment contracts)

336 364410 437 465

2326

3550

62

50 57

56 57

57

21 19

19 20

18

429 466

521 564

602

FY12 FY13 FY14 FY15 FY16

€b

illi

on

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

Section 1 – Italian insurance market snapshots

6

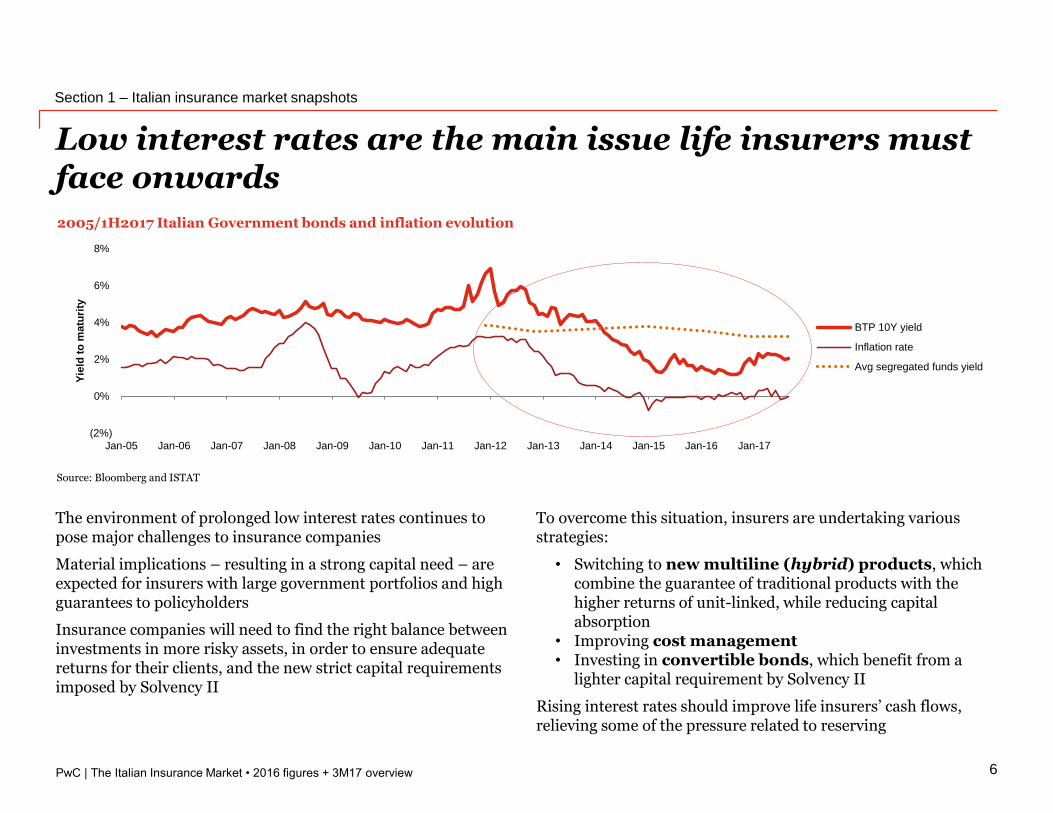

Low interest rates are the main issue life insurers must face onwards

2005/1H2017 Italian Government bonds and inflation evolution

Source: Bloomberg and ISTAT

To overcome this situation, insurers are undertaking various strategies:

• Switching to new multiline (hybrid) products, which combine the guarantee of traditional products with the higher returns of unit-linked, while reducing capital absorption

• Improving cost management• Investing in convertible bonds, which benefit from a

lighter capital requirement by Solvency II

Rising interest rates should improve life insurers’ cash flows, relieving some of the pressure related to reserving

The environment of prolonged low interest rates continues to pose major challenges to insurance companies

Material implications – resulting in a strong capital need – are expected for insurers with large government portfolios and high guarantees to policyholders

Insurance companies will need to find the right balance between investments in more risky assets, in order to ensure adequate returns for their clients, and the new strict capital requirements imposed by Solvency II

(2%)

0%

2%

4%

6%

8%

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Yie

ld t

o m

atu

rity

BTP 10Y yield

Inflation rate

Avg segregated funds yield

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

35,413 33,690 32,800 32,002 31,953

20,190 18,644 17,567 16,642 16,128

FY12 FY13 FY14 FY15 FY16

€m

illi

on

Total Motor

Section 1 – Italian insurance market snapshots

7

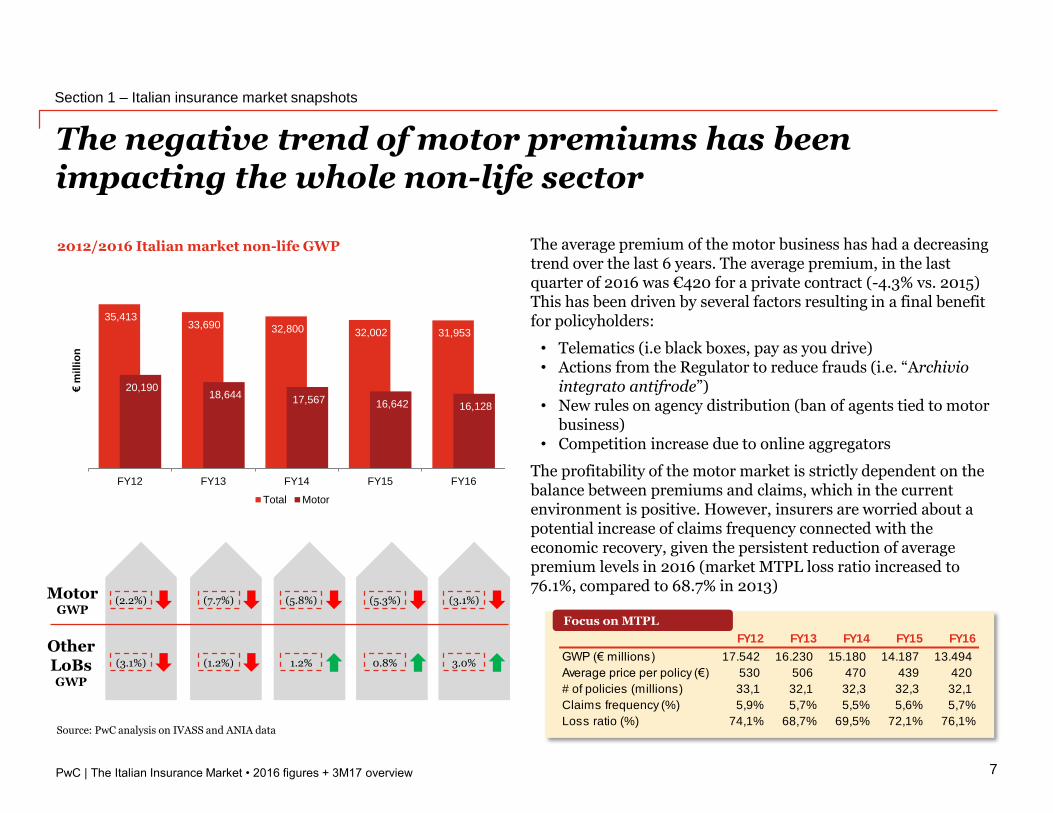

The negative trend of motor premiums has been impacting the whole non-life sector

2012/2016 Italian market non-life GWP

Source: PwC analysis on IVASS and ANIA data

MotorGWP

OtherLoBsGWP

(2.2%) (7.7%) (5.8%) (5.3%)

(3.1%) (1.2%) 1.2% 0.8%

The average premium of the motor business has had a decreasing trend over the last 6 years. The average premium, in the last quarter of 2016 was €420 for a private contract (-4.3% vs. 2015) This has been driven by several factors resulting in a final benefit for policyholders:

• Telematics (i.e black boxes, pay as you drive)• Actions from the Regulator to reduce frauds (i.e. “Archivio

integrato antifrode”)• New rules on agency distribution (ban of agents tied to motor

business)• Competition increase due to online aggregators

The profitability of the motor market is strictly dependent on the balance between premiums and claims, which in the current environment is positive. However, insurers are worried about a potential increase of claims frequency connected with the economic recovery, given the persistent reduction of average premium levels in 2016 (market MTPL loss ratio increased to 76.1%, compared to 68.7% in 2013)

(3.1%)

3.0%

FY12 FY13 FY14 FY15 FY16

GWP (€ millions) 17.542 16.230 15.180 14.187 13.494

Average price per policy (€) 530 506 470 439 420

# of policies (millions) 33,1 32,1 32,3 32,3 32,1

Claims frequency (%) 5,9% 5,7% 5,5% 5,6% 5,7%

Loss ratio (%) 74,1% 68,7% 69,5% 72,1% 76,1%

Focus on MTPL

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

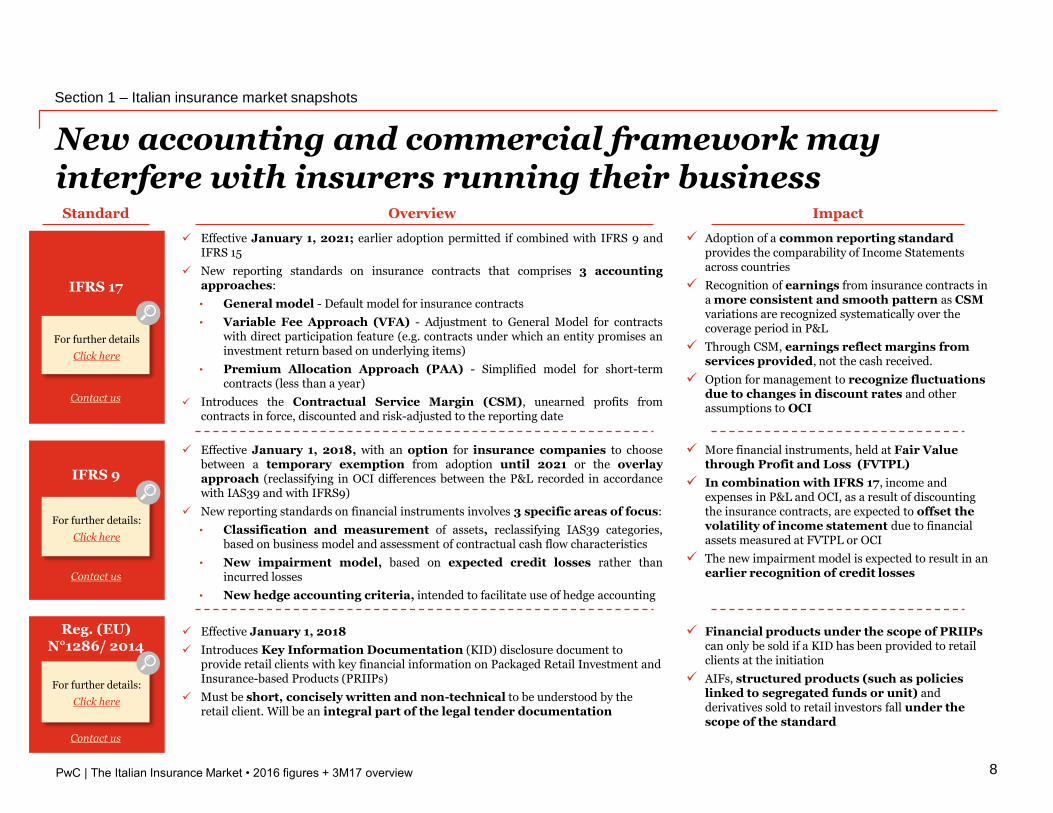

New accounting and commercial framework may interfere with insurers running their business

8

Section 1 – Italian insurance market snapshots

Effective January 1, 2021; earlier adoption permitted if combined with IFRS 9 andIFRS 15

New reporting standards on insurance contracts that comprises 3 accountingapproaches:

• General model - Default model for insurance contracts

• Variable Fee Approach (VFA) - Adjustment to General Model for contractswith direct participation feature (e.g. contracts under which an entity promises aninvestment return based on underlying items)

• Premium Allocation Approach (PAA) - Simplified model for short-termcontracts (less than a year)

Introduces the Contractual Service Margin (CSM), unearned profits fromcontracts in force, discounted and risk-adjusted to the reporting date

Overview Impact

Effective January 1, 2018, with an option for insurance companies to choosebetween a temporary exemption from adoption until 2021 or the overlayapproach (reclassifying in OCI differences between the P&L recorded in accordancewith IAS39 and with IFRS9)

New reporting standards on financial instruments involves 3 specific areas of focus:

• Classification and measurement of assets, reclassifying IAS39 categories,based on business model and assessment of contractual cash flow characteristics

• New impairment model, based on expected credit losses rather thanincurred losses

• New hedge accounting criteria, intended to facilitate use of hedge accounting

Effective January 1, 2018

Introduces Key Information Documentation (KID) disclosure document to provide retail clients with key financial information on Packaged Retail Investment and Insurance-based Products (PRIIPs)

Must be short, concisely written and non-technical to be understood by the retail client. Will be an integral part of the legal tender documentation

Adoption of a common reporting standard provides the comparability of Income Statementsacross countries

Recognition of earnings from insurance contracts in a more consistent and smooth pattern as CSM variations are recognized systematically over the coverage period in P&L

Through CSM, earnings reflect margins from services provided, not the cash received.

Option for management to recognize fluctuations due to changes in discount rates and other assumptions to OCI

Financial products under the scope of PRIIPscan only be sold if a KID has been provided to retail clients at the initiation

AIFs, structured products (such as policies linked to segregated funds or unit) and derivatives sold to retail investors fall under the scope of the standard

IFRS 17

Reg. (EU) N°1286/ 2014

Standard

For further details

Click here

IFRS 9

For further details:

Click here

For further details:

Click here

Contact us

Contact us

Contact us

More financial instruments, held at Fair Value through Profit and Loss (FVTPL)

In combination with IFRS 17, income and expenses in P&L and OCI, as a result of discounting the insurance contracts, are expected to offset the volatility of income statement due to financial assets measured at FVTPL or OCI

The new impairment model is expected to result in an earlier recognition of credit losses

PwC

Italian life insurance market

The Italian Insurance Market • 2016 figures + 3M17 overview

9

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

€ million FY12 FY13 FY14 FY15 FY16

Gross written premiums 69,715 85,110 110,515 114,950 102,257

Changes in technical provisions (10,013) (29,928) (59,967) (53,024) (48,453)

Lapses (Surrenders/ Maturities/ Claims) (75,022) (66,788) (64,577) (71,196) (62,931)

General expenses (3,367) (3,538) (3,812) (3,970) (3,844)

Investment income 25,382 18,409 20,588 15,976 16,657

Other technical income (charges) (222) (325) (381) (388) (328)

Technical result 6,473 2,929 2,369 2,347 3,357

Reinsurance result 388 369 383 312 289

Net technical result 6,861 3,298 2,752 2,659 3,646

4

21

28

4

14

Section 2 – Italian life insurance market

10

Italian life insurance market

2016 # of companies by GWP

GWP

FY16 Key-data

Italian life insurance market GWP

€102bn, -11.0% vs. FY15

Life products distributed mainly through banking channel (62%)

Largest life insurance company:

Poste Vita (market share equal to 18.6%)

Largest life insurance group:

Poste Vita Group (market share equal to 19.4%)

71 insurance companies operating in the life business (71 in 2015)

2012/2016 Life business technical result

Source: ANIA

Key Messages

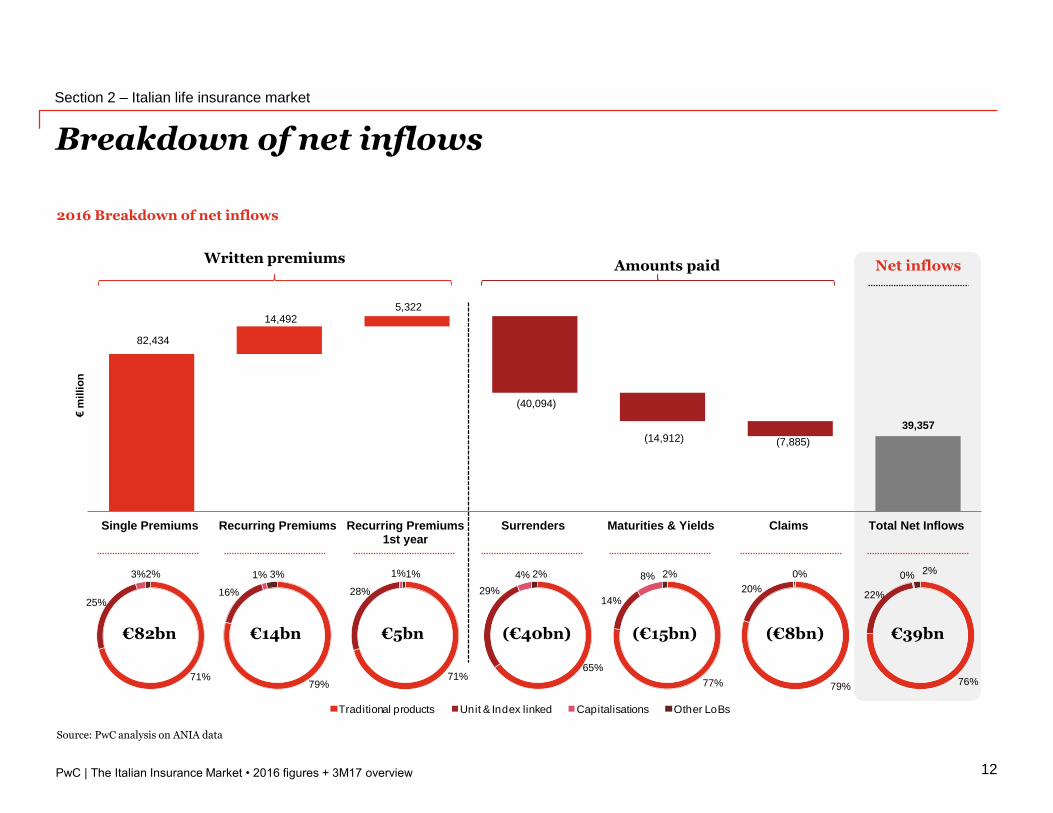

• The GWP of the Italian life insurance market dropped by 11.0%, reaching €102bn and net inflows of €39bn (€44bn in 2015)

• 2016 technical results were positive (€3.4bn), 43.0% higher than 2015 (€2.3bn) due to a recovery in net profits from investments after the negative performance in 2015

• Italian families have invested €621bn of their own savings in life insurance products (14.9% of total savings)

• The market still shows a strong predominance of traditional products (72% vs. 68% in 2015). The low interest rate environment and the introduction of Solvency II still represent strong incentives for insurance companies to boost unit-linked and hybrid contracts; such products, however, showed a slowdown in 2016 after 4 years of constant growth (-24.5% from 2015, compared to a 2011-2015 CAGR of +26%) due to the negative trend of financial market in the first months of 2016

• Life premiums penetration in Italy is 6.1% (premiums/GDP), compared the European average of 2.6% in 2015

• The average Solvency II ratio in the life sector decreased to 210% (266% in 2015)

€5bn€1bn€100m€50m

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

51,235 65,018

82,642 77,953 73,718

18,480

20,092

27,874 36,997 28,539

69,715

85,110

110,515 114,950

102,257

FY12 FY13 FY14 FY15 FY16

€m

illi

on

Traditional contracts Investment contracts

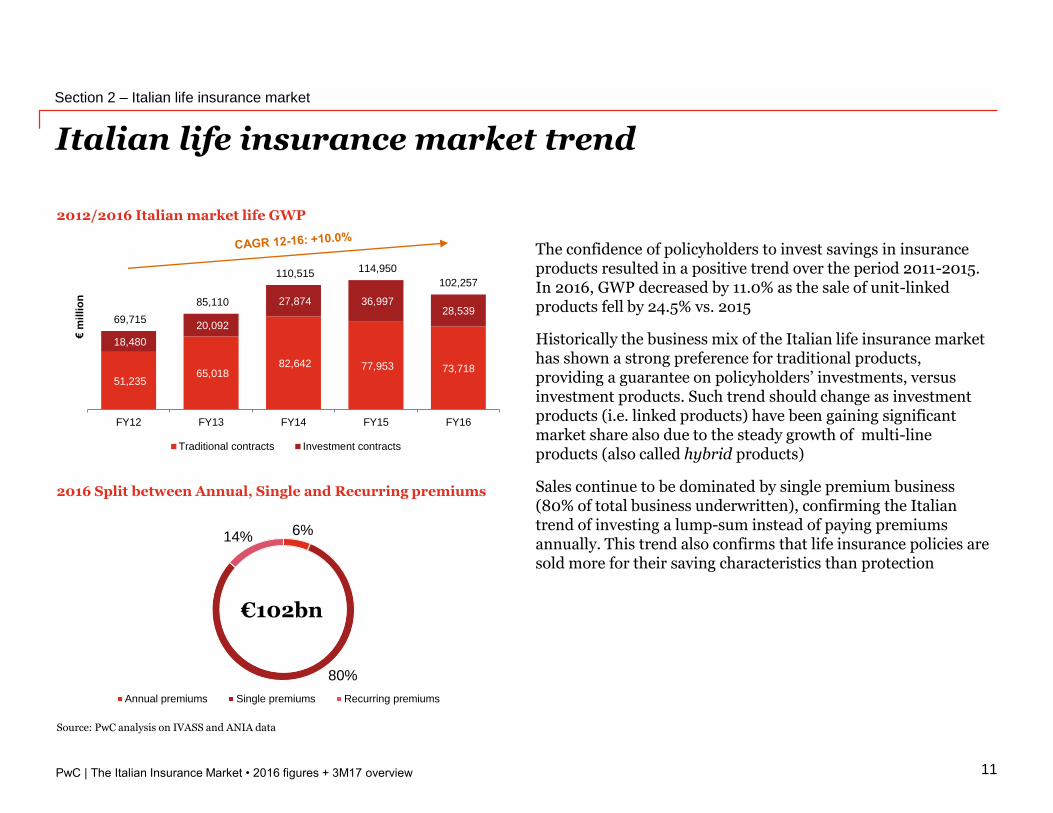

2012/2016 Italian market life GWP

Italian life insurance market trend

Section 2 – Italian life insurance market

11

2016 Split between Annual, Single and Recurring premiums

Source: PwC analysis on IVASS and ANIA data

The confidence of policyholders to invest savings in insurance products resulted in a positive trend over the period 2011-2015. In 2016, GWP decreased by 11.0% as the sale of unit-linked products fell by 24.5% vs. 2o15

Historically the business mix of the Italian life insurance market has shown a strong preference for traditional products, providing a guarantee on policyholders’ investments, versus investment products. Such trend should change as investment products (i.e. linked products) have been gaining significant market share also due to the steady growth of multi-line products (also called hybrid products)

Sales continue to be dominated by single premium business (80% of total business underwritten), confirming the Italian trend of investing a lump-sum instead of paying premiums annually. This trend also confirms that life insurance policies are sold more for their saving characteristics than protection

6%

80%

14%

Annual premiums Single premiums Recurring premiums

€102bn

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

Breakdown of net inflows

41%

46%

9%4%

Traditional products Unit & Index linked Capitalisations Other LoBs

Section 2 – Italian life insurance market

12

2016 Breakdown of net inflows

Written premiumsAmounts paid

Source: PwC analysis on ANIA data

€82bn €14bn €5bn (€40bn) (€15bn) (€8bn)

Net inflows

€39bn

71%

25%

3% 2%

79%

16%

1% 3%

71%

28%

1% 1%

65%

29%

4% 2%

77%

14%

8% 2%

79%

20%

0%

76%

22%

0% 2%

82,434

39,357

(7,885)

(40,094)

(14,912)

14,492 5,322

Single Premiums Recurring Premiums Recurring Premiums1st year

Surrenders Maturities & Yields Claims Total Net Inflows

€m

illi

on

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

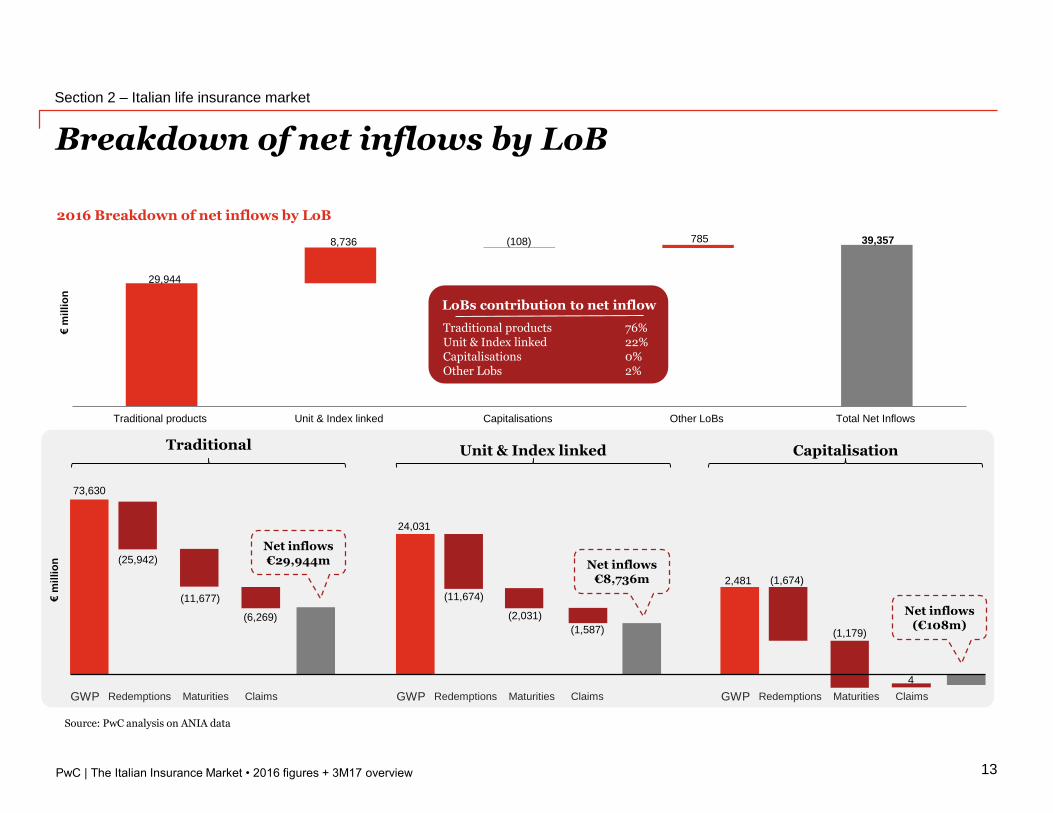

29,944

8,736 (108) 785 39,357

Traditional products Unit & Index linked Capitalisations Other LoBs Total Net Inflows

€m

illi

on

2016 Breakdown of net inflows by LoB

Breakdown of net inflows by LoB

13

Source: PwC analysis on ANIA data

GWP Redemptions Maturities Claims

Net inflows €29,944m

Traditional

73,630

(25,942)

(11,677)

(6,269)

€m

illi

on

Traditional productsUnit & Index linkedCapitalisationsOther Lobs

76%22%0%2%

LoBs contribution to net inflow

GWP Redemptions Maturities Claims

Unit & Index linked

24,031

(11,674)

(2,031)

(1,587)

GWP Redemptions Maturities Claims

Capitalisation

2,481 (1,674)

(1,179)

4

Net inflows €8,736m

Net inflows (€108m)

Section 2 – Italian life insurance market

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

6.05 5.20

4.41 4.76 5.84

17.7%

15.0%

13.2% 13.0%

10.5%

0%

5%

10%

15%

20%

-

1

2

3

4

5

6

7

8

FY12 FY13 FY14 FY15 FY16

Average duration (years) Lapse index (%)

11.1% 9.0% 7.7% 7.8% 6.7%

1.2%

1.3% 1.3% 1.3%

1.3%

5.3%

4.8% 4.2% 3.9%

2.5%

17.7%

15.0%

13.2% 13.0%

10.5%

FY12 FY13 FY14 FY15 FY16

Surrender index (%) Claim index (%) Maturity index (%)

Portfolio lapse index and average duration

Section 2 – Italian life insurance market

14

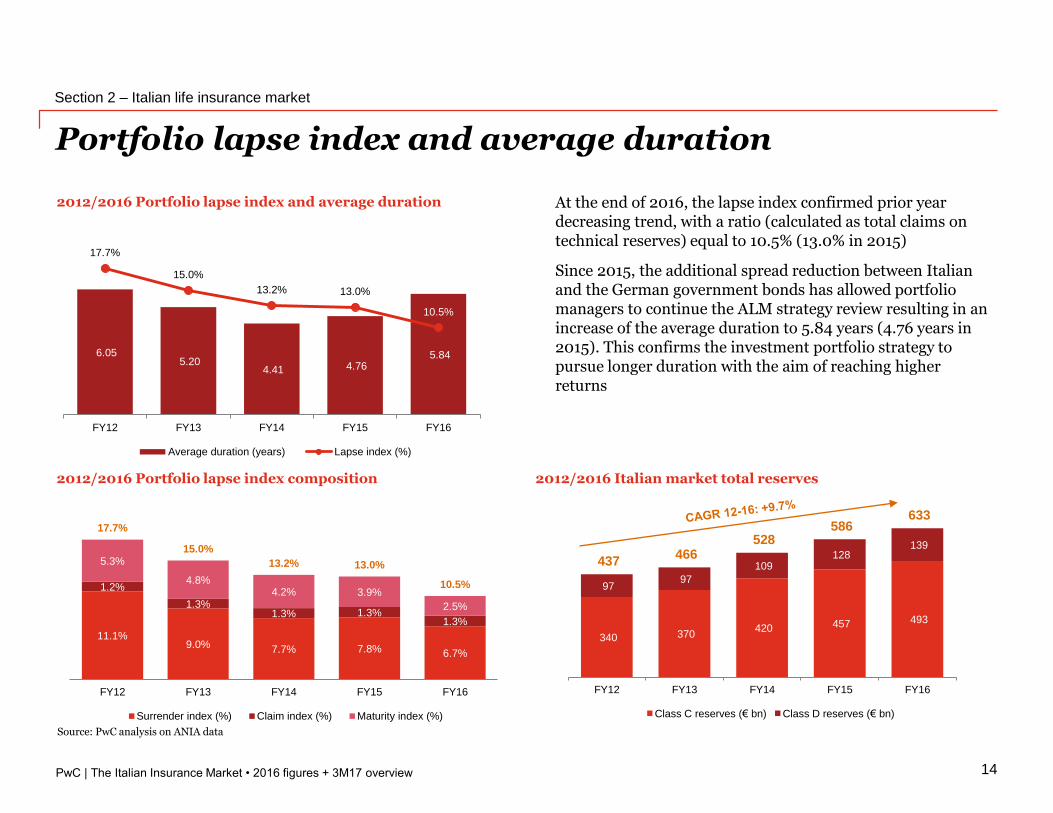

At the end of 2016, the lapse index confirmed prior year decreasing trend, with a ratio (calculated as total claims on technical reserves) equal to 10.5% (13.0% in 2015)

Since 2015, the additional spread reduction between Italian and the German government bonds has allowed portfolio managers to continue the ALM strategy review resulting in an increase of the average duration to 5.84 years (4.76 years in 2015). This confirms the investment portfolio strategy to pursue longer duration with the aim of reaching higher returns

2012/2016 Italian market total reserves

2012/2016 Portfolio lapse index and average duration

2012/2016 Portfolio lapse index composition

Source: PwC analysis on ANIA data

340 370 420 457 493

97 97

109 128

139

437 466

528 586

633

FY12 FY13 FY14 FY15 FY16

Class C reserves (€ bn) Class D reserves (€ bn)

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

62%

34%

4%

Life marketinvestments

Banks

Agents

Financial promoters

Others

2016 Asset allocation of life products

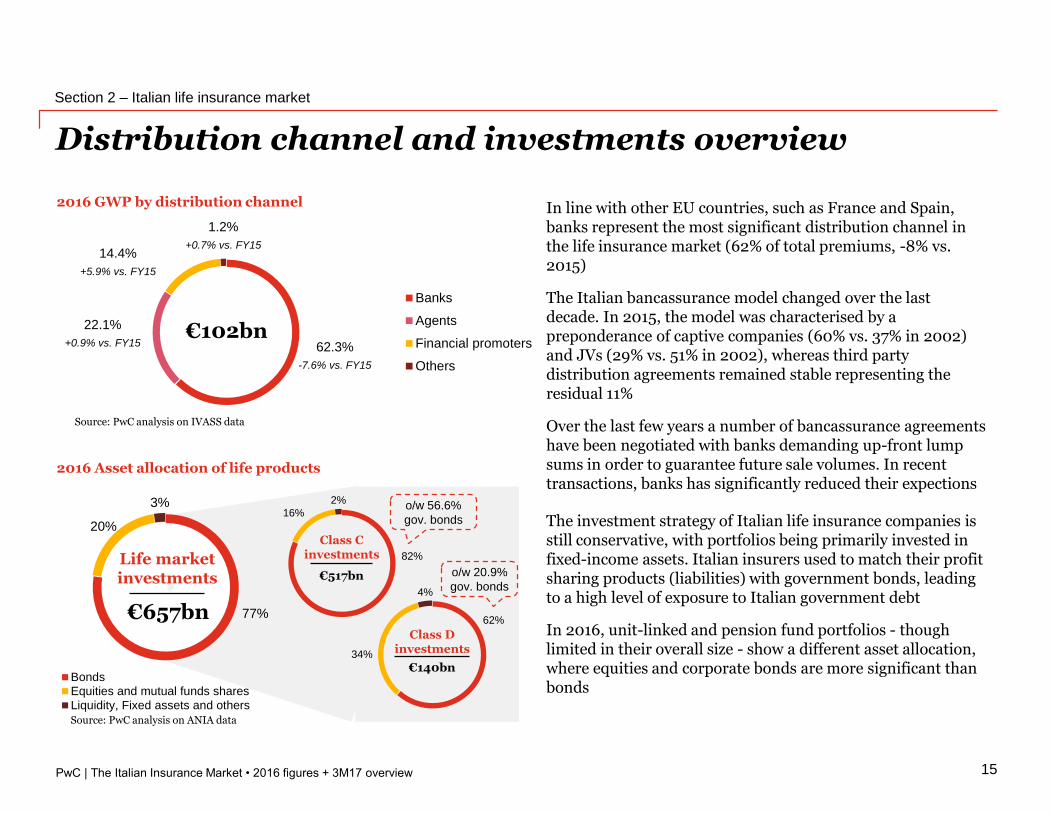

Distribution channel and investments overview

Section 2 – Italian life insurance market

15

Source: PwC analysis on IVASS data

Source: PwC analysis on ANIA data

2016 GWP by distribution channel

€102bn22.1%

+0.9% vs. FY15 62.3%

-7.6% vs. FY15

14.4%

+5.9% vs. FY15

1.2%

+0.7% vs. FY15

€657bnClass D

investments

€140bn

Class Cinvestments

€517bn

61.5%34.2%

4.3%

Bonds

Equities and mutual funds shares

Liquidity, Fixed assets and others

In line with other EU countries, such as France and Spain, banks represent the most significant distribution channel in the life insurance market (62% of total premiums, -8% vs. 2015)

The Italian bancassurance model changed over the last decade. In 2015, the model was characterised by a preponderance of captive companies (60% vs. 37% in 2002) and JVs (29% vs. 51% in 2002), whereas third party distribution agreements remained stable representing the residual 11%

Over the last few years a number of bancassurance agreements have been negotiated with banks demanding up-front lump sums in order to guarantee future sale volumes. In recent transactions, banks has significantly reduced their expections

The investment strategy of Italian life insurance companies is still conservative, with portfolios being primarily invested in fixed-income assets. Italian insurers used to match their profit sharing products (liabilities) with government bonds, leading to a high level of exposure to Italian government debt

In 2016, unit-linked and pension fund portfolios - though limited in their overall size - show a different asset allocation, where equities and corporate bonds are more significant than bonds

82%

16%

2%o/w 56.6%

gov. bonds

o/w 20.9%

gov. bonds

77%

20%

3%

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

14.0%

10.9%

17.6%

66.0%

72.4%

69.2%

20.0%

16.8%

13.3%

FY14

FY15

FY16

Others Banks Financial promoters

59.6% 55.7% 56.7%

40.4% 44.3% 43.3%

FY14 FY15 FY16

Traditional Unit & Index Linked

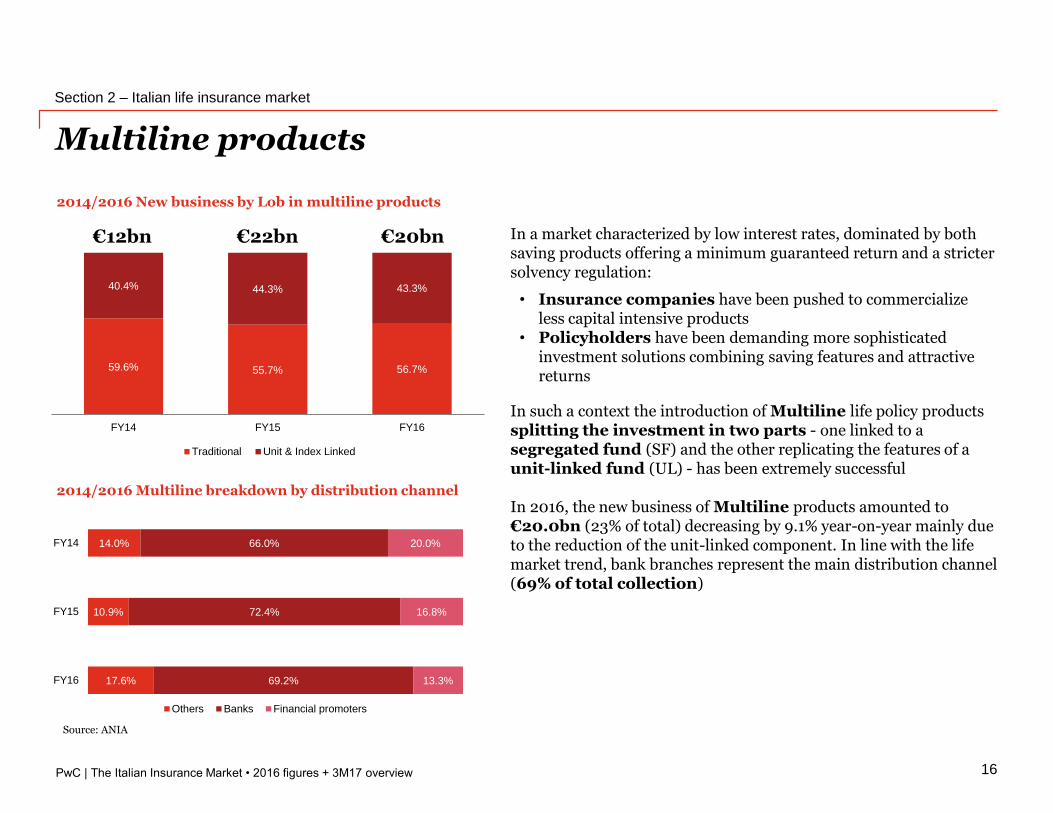

Multiline products

Section 2 – Italian life insurance market

Source: ANIA

16

€22bn In a market characterized by low interest rates, dominated by both saving products offering a minimum guaranteed return and a stricter solvency regulation:

• Insurance companies have been pushed to commercialize less capital intensive products

• Policyholders have been demanding more sophisticated investment solutions combining saving features and attractive returns

In such a context the introduction of Multiline life policy products splitting the investment in two parts - one linked to asegregated fund (SF) and the other replicating the features of a unit-linked fund (UL) - has been extremely successful

In 2016, the new business of Multiline products amounted to €20.0bn (23% of total) decreasing by 9.1% year-on-year mainly due to the reduction of the unit-linked component. In line with the life market trend, bank branches represent the main distribution channel (69% of total collection)

€20bn€12bn

2014/2016 Multiline breakdown by distribution channel

2014/2016 New business by Lob in multiline products

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

4.19% 4.15%

3.61%

3.03% 4.02% 3.37%

3.41%

2.50%

4.02% 3.86%3.81%

3.68%

4.11%

1.99%

1.58%

1.89%

2013 2014 2015 2016

Posta - Valore più ISP Vita - Base sicura

Generali - Gesav Italy - BTP 10y

207253 263 289

8488

108112

29

3352

62

13

148

8

3.91%

3.77% 3.56% 3.24%4.11%

1.99%1.58%

1.89%

2013 2014 2015 2016

Equity

Funds & oth.

Other bonds

Gvmt. bonds

Avg. Segreg. fundsyield

Italy - BTP 10y

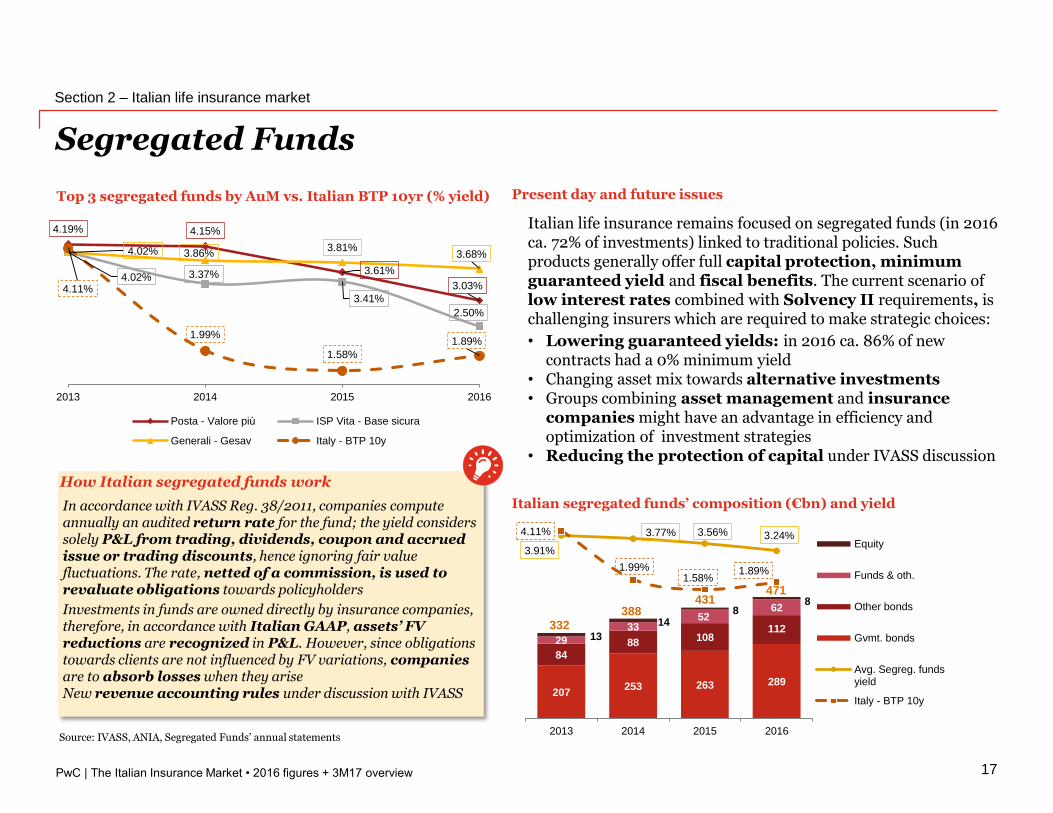

In accordance with IVASS Reg. 38/2011, companies compute annually an audited return rate for the fund; the yield considers solely P&L from trading, dividends, coupon and accrued issue or trading discounts, hence ignoring fair value fluctuations. The rate, netted of a commission, is used to revaluate obligations towards policyholders

Investments in funds are owned directly by insurance companies, therefore, in accordance with Italian GAAP, assets’ FV reductions are recognized in P&L. However, since obligations towards clients are not influenced by FV variations, companiesare to absorb losses when they ariseNew revenue accounting rules under discussion with IVASS

How Italian segregated funds work

Segregated Funds

Section 2 – Italian life insurance market

17

Source: IVASS, ANIA, Segregated Funds’ annual statements

Top 3 segregated funds by AuM vs. Italian BTP 10yr (% yield) Present day and future issues

Italian life insurance remains focused on segregated funds (in 2016 ca. 72% of investments) linked to traditional policies. Such products generally offer full capital protection, minimumguaranteed yield and fiscal benefits. The current scenario of low interest rates combined with Solvency II requirements, ischallenging insurers which are required to make strategic choices:

• Lowering guaranteed yields: in 2016 ca. 86% of new contracts had a 0% minimum yield

• Changing asset mix towards alternative investments • Groups combining asset management and insurance

companies might have an advantage in efficiency and optimization of investment strategies

• Reducing the protection of capital under IVASS discussion

Italian segregated funds’ composition (€bn) and yield

332388

431471

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

Medium bancassurance players

Top underwriters

110%

160%

210%

260%

310%

€- €1,000 €2,000 €3,000 €4,000 €5,000 €6,000 €7,000 €8,000

120%

140%

160%

180%

200%

220%

240%

260%

280%

300%

320%

€- €5,000 €10,000 €15,000 €20,000

Italy – Composite insurers 229%

EU – Life insurers 217%

Italy – Life insurers 210%EU – Composite insurers 210%

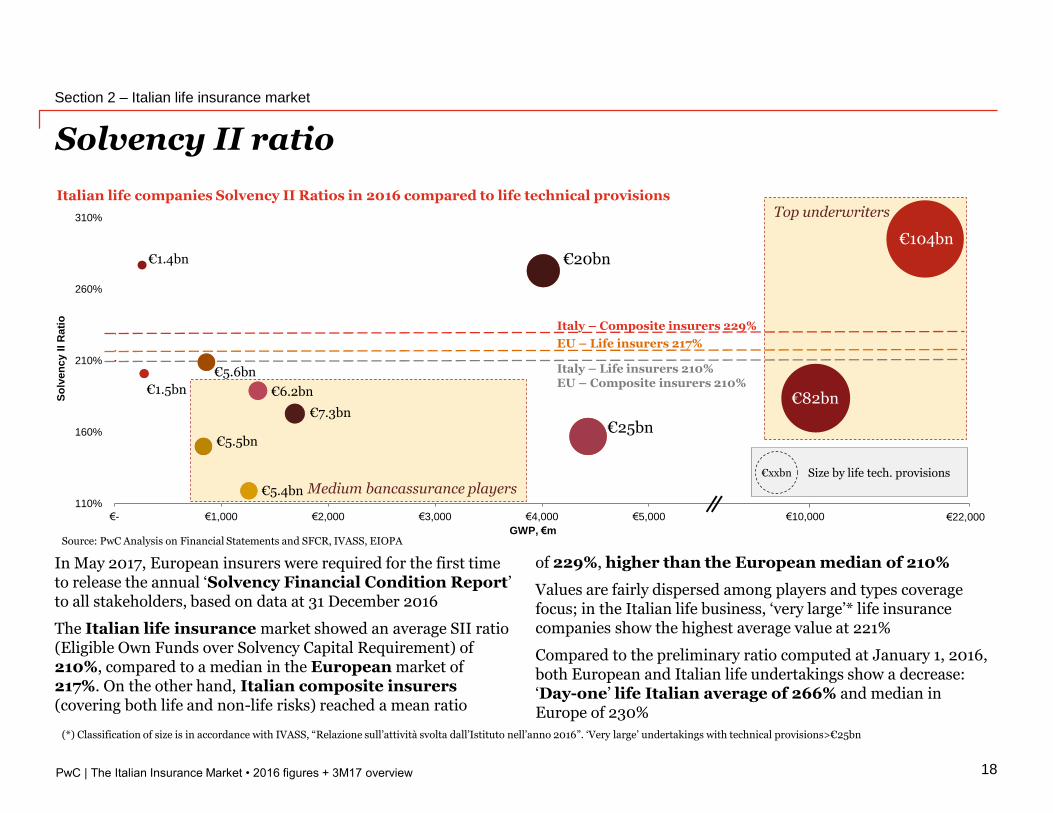

Solvency II ratio

Section 2 – Italian life insurance market

18

In May 2017, European insurers were required for the first time to release the annual ‘Solvency Financial Condition Report’ to all stakeholders, based on data at 31 December 2016

The Italian life insurance market showed an average SII ratio (Eligible Own Funds over Solvency Capital Requirement) of 210%, compared to a median in the European market of217%. On the other hand, Italian composite insurers (covering both life and non-life risks) reached a mean ratio

of 229%, higher than the European median of 210%

Values are fairly dispersed among players and types coverage focus; in the Italian life business, ‘very large’* life insurance companies show the highest average value at 221%

Compared to the preliminary ratio computed at January 1, 2016, both European and Italian life undertakings show a decrease: ‘Day-one’ life Italian average of 266% and median in Europe of 230%

Source: PwC Analysis on Financial Statements and SFCR, IVASS, EIOPA

(*) Classification of size is in accordance with IVASS, “Relazione sull’attività svolta dall’Istituto nell’anno 2016”. ‘Very large’ undertakings with technical provisions>€25bn

GWP, €m

Italian life companies Solvency II Ratios in 2016 compared to life technical provisions

So

lven

cy I

I R

ati

o

€22,000120%

140%

160%

180%

200%

220%

240%

260%

280%

300%

320%

€- €5,000 €10,000 €15,000 €20,000

€104bn

€82bn

€25bn

€20bn

€7.3bn

€6.2bn

€5.4bn

€5.5bn

€5.6bn

€1.4bn

€1.5bn

€xxbn Size by life tech. provisions

€10,000

PwC

Italian non-life insurance market

The Italian Insurance Market • 2016 figures + 3M17 overview

19

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

€ million FY12 FY13 FY14 FY15 FY16

Gross written premiums 35,413 33,690 32,800 32,002 31,953

Earned Premium 35,886 34,441 33,188 32,182 31,847

Incurred claims (25,793) (22,400) (21,201) (20,023) (20,005)

General expenses (8,504) (8,433) (8,599) (8,702) (8,770)

Investment income 1,607 1,202 1,278 1,196 1,049

Other technical income (charges) (663) (605) (527) (599) (598)

Technical result 2,533 4,205 4,139 4,054 3,522

Reinsurance result 537 (772) (600) (410) (578)

Net technical result 3,070 3,433 3,539 3,644 2,945

Section 3 – Italian non-life insurance market

20

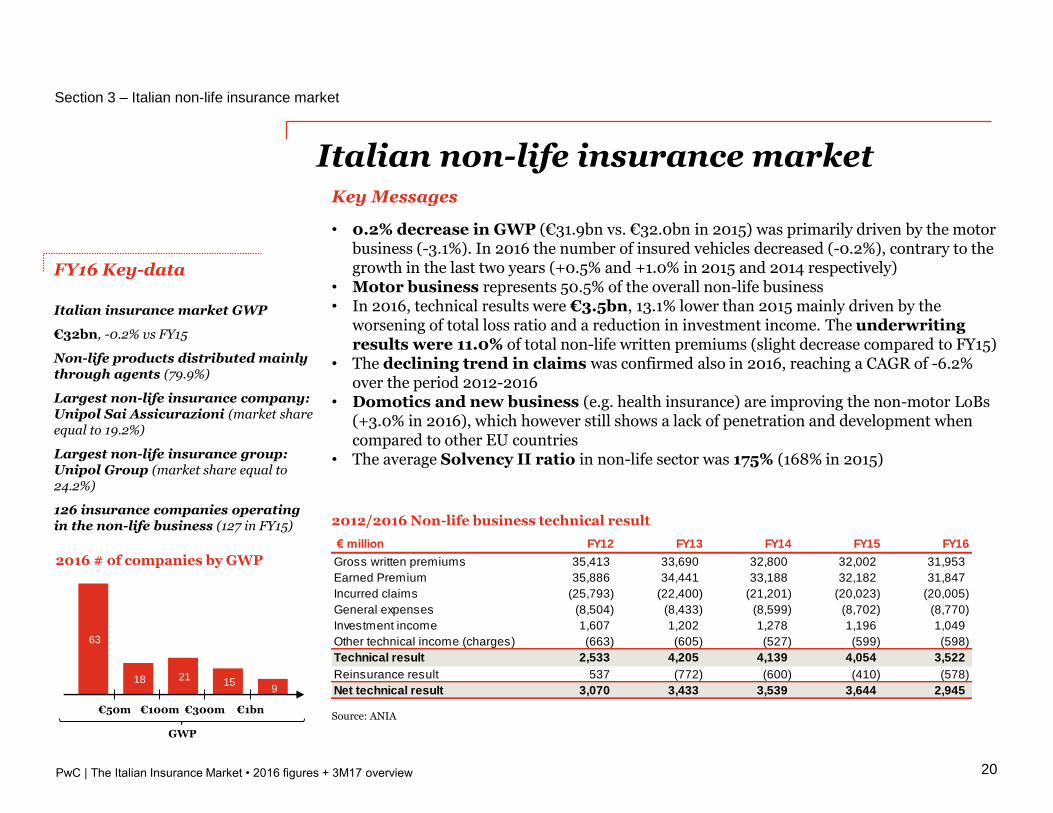

Italian non-life insurance market

FY16 Key-data

Italian insurance market GWP

€32bn, -0.2% vs FY15

Non-life products distributed mainly through agents (79.9%)

Largest non-life insurance company: Unipol Sai Assicurazioni (market share equal to 19.2%)

Largest non-life insurance group: Unipol Group (market share equal to 24.2%)

126 insurance companies operating in the non-life business (127 in FY15)

2016 # of companies by GWP

2012/2016 Non-life business technical result

Source: ANIA

Key Messages

• 0.2% decrease in GWP (€31.9bn vs. €32.0bn in 2015) was primarily driven by the motor business (-3.1%). In 2016 the number of insured vehicles decreased (-0.2%), contrary to the growth in the last two years (+0.5% and +1.0% in 2015 and 2014 respectively)

• Motor business represents 50.5% of the overall non-life business• In 2016, technical results were €3.5bn, 13.1% lower than 2015 mainly driven by the

worsening of total loss ratio and a reduction in investment income. The underwriting results were 11.0% of total non-life written premiums (slight decrease compared to FY15)

• The declining trend in claims was confirmed also in 2016, reaching a CAGR of -6.2% over the period 2012-2016

• Domotics and new business (e.g. health insurance) are improving the non-motor LoBs(+3.0% in 2016), which however still shows a lack of penetration and development when compared to other EU countries

• The average Solvency II ratio in non-life sector was 175% (168% in 2015)

63

18 21 15

9

GWP

€1bn€300m€100m€50m

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

Banks Agents Financial promoters Others

35,413

33,690

32,800 32,002 31,953

FY12 FY13 FY14 FY15 FY16

€m

illi

on

2012/2016 Italian market non-life GWP

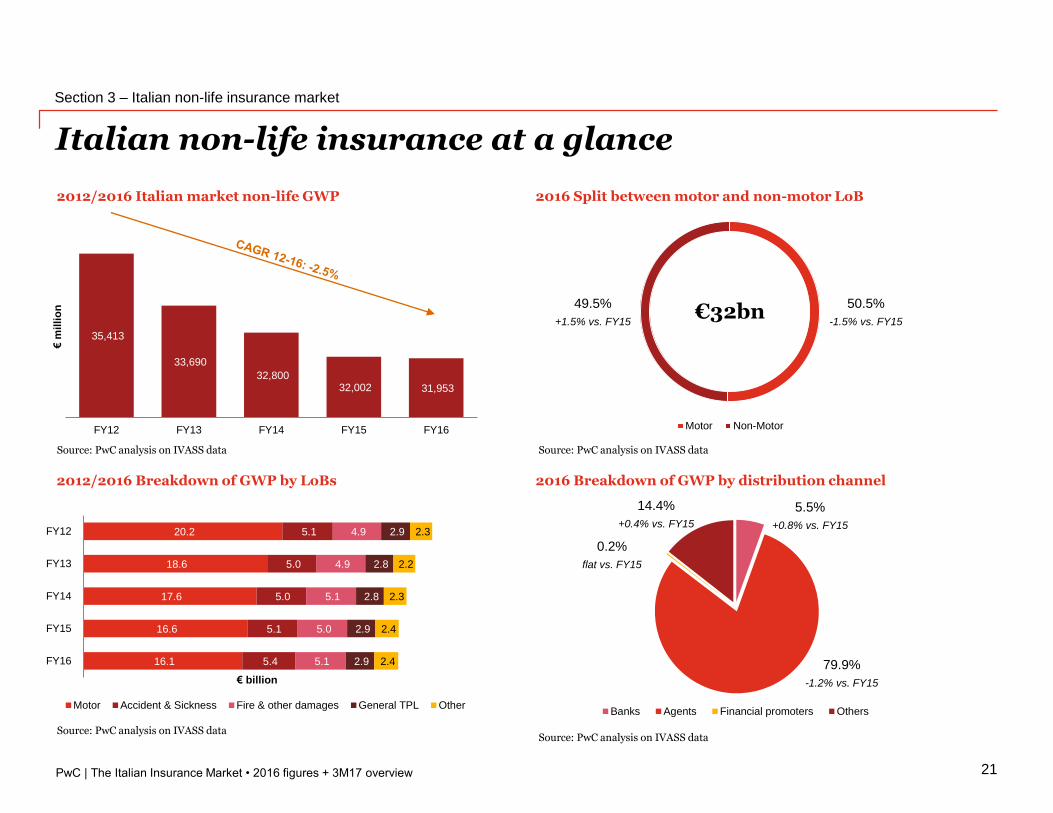

Italian non-life insurance at a glance

Section 3 – Italian non-life insurance market

21

2012/2016 Breakdown of GWP by LoBs

2016 Split between motor and non-motor LoB

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

20.2

18.6

17.6

16.6

16.1

5.1

5.0

5.0

5.1

5.4

4.9

4.9

5.1

5.0

5.1

2.9

2.8

2.8

2.9

2.9

2.3

2.2

2.3

2.4

2.4

FY12

FY13

FY14

FY15

FY16

€ billion

Motor Accident & Sickness Fire & other damages General TPL Other

2016 Breakdown of GWP by distribution channel

Source: PwC analysis on IVASS data

0.2%

flat vs. FY15

79.9%

-1.2% vs. FY15

14.4%

+0.4% vs. FY15

5.5%

+0.8% vs. FY15

Motor Non-Motor

49.5%

+1.5% vs. FY15

50.5%

-1.5% vs. FY15€32bn

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

7.5% 7.7% 7.9% 7.9%7.5%

4.7% 4.8% 4.8% 4.7% 4.4%

FY12 FY13 FY14 FY15 FY16

Motor LoBs Total Non-life market

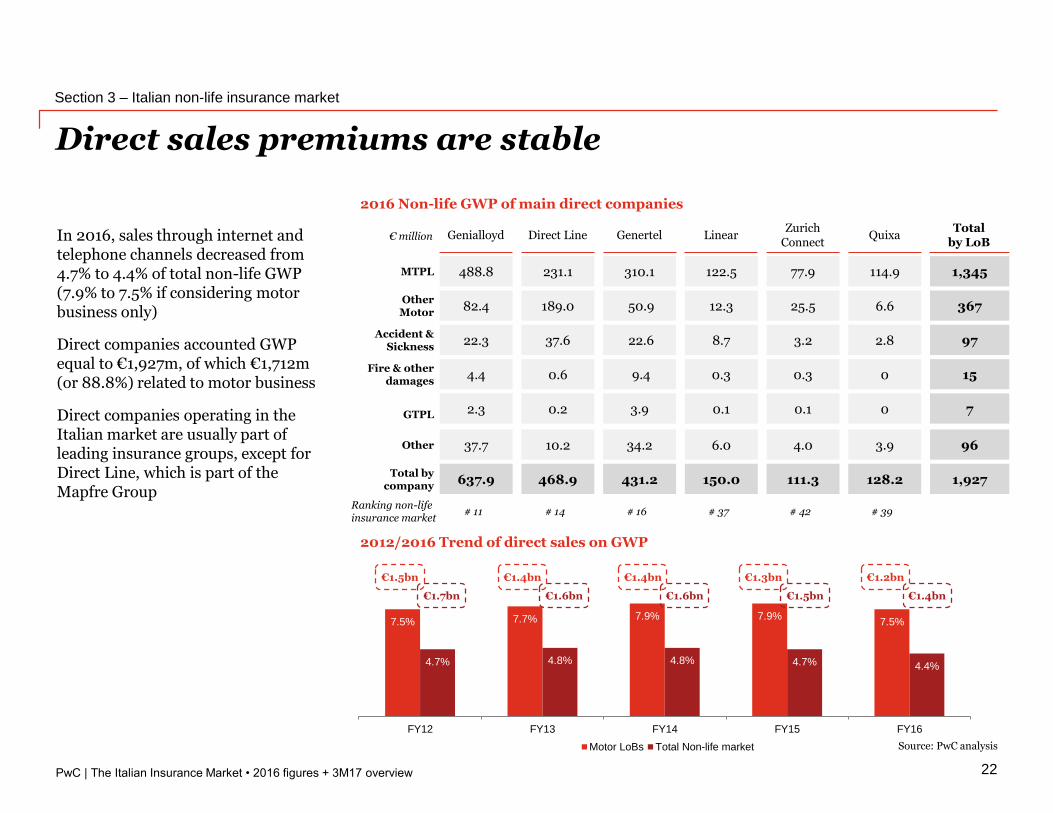

Direct sales premiums are stable

Section 3 – Italian non-life insurance market

22

€ million

MTPL

Other Motor

Accident & Sickness

Fire & other damages

GTPL

Other

Totalby LoB

1,345

367

97

15

7

96

1,927Total by

company

Ranking non-life insurance market

Genialloyd

488.8

82.4

22.3

4.4

2.3

37.7

637.9

# 11

Direct Line

231.1

189.0

37.6

0.6

0.2

10.2

468.9

# 14

Genertel

310.1

50.9

22.6

9.4

3.9

34.2

431.2

# 16

Linear

122.5

12.3

8.7

0.3

0.1

6.0

150.0

# 37

Zurich Connect

77.9

25.5

3.2

0.3

0.1

4.0

111.3

# 42

Quixa

114.9

6.6

2.8

0

0

3.9

128.2

# 39

2016 Non-life GWP of main direct companies

2012/2016 Trend of direct sales on GWP

Source: PwC analysis

In 2016, sales through internet and telephone channels decreased from 4.7% to 4.4% of total non-life GWP (7.9% to 7.5% if considering motor business only)

Direct companies accounted GWP equal to €1,927m, of which €1,712m (or 88.8%) related to motor business

Direct companies operating in the Italian market are usually part of leading insurance groups, except for Direct Line, which is part of the Mapfre Group

€1.5bn

€1.7bn

€1.4bn

€1.6bn

€1.4bn

€1.6bn

€1.3bn

€1.5bn

€1.2bn

€1.4bn

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

24.0% 25.0% 26.2% 27.2% 27.4%

71.9% 65.0% 63.9% 62.2% 62.8%

95.9% 90.1% 90.1% 89.4% 90.3%

FY12 FY13 FY14 FY15 FY16

Expense ratio Loss ratio

35.9% 23.9% 30.5% 11.4% 17.5% 18.6% 30.4% 33.4% 32.4% 21.5% 14.9%

32.8% 25.0% 33.6% 37.7% 37.5% 32.7%

39.9% 66.9% 57.4%

159.4%

11.0%

69.3% 42.2% 60.1% 62.9% 76.1%

15.7%

48.1% 66.0% 41.3% 29.1% 24.8% 32.9%

75.8%90.9% 87.9%

170.9%

28.5%

87.9%72.5%

93.5% 95.2% 97.6%

30.6%

80.9%91.0%

74.9% 66.8% 62.3% 65.5%

Accident Sickness Landvehicles

Railwayrollingstocks

Aircraft Ships Goods intransit

Fire andnaturalforces

Otherdamage toproperty

Motorvehicle +

Shipsliability

Aircraftliability

General TPL Credit Suretyship Financialloss

Legalexpenses

Assistance

Expense ratio Loss ratio

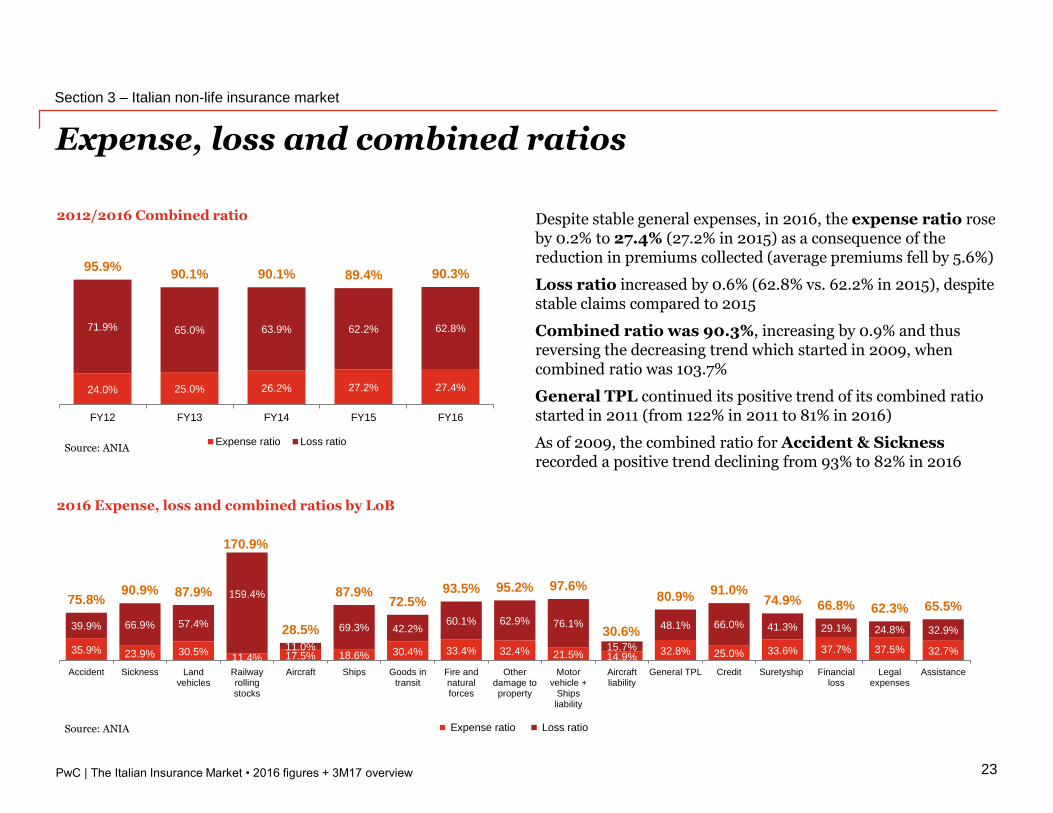

Expense, loss and combined ratios

Section 3 – Italian non-life insurance market

23

2012/2016 Combined ratio

2016 Expense, loss and combined ratios by LoB

Source: ANIA

Source: ANIA

Despite stable general expenses, in 2016, the expense ratio rose by 0.2% to 27.4% (27.2% in 2015) as a consequence of the reduction in premiums collected (average premiums fell by 5.6%)

Loss ratio increased by 0.6% (62.8% vs. 62.2% in 2015), despite stable claims compared to 2015

Combined ratio was 90.3%, increasing by 0.9% and thus reversing the decreasing trend which started in 2009, when combined ratio was 103.7%

General TPL continued its positive trend of its combined ratio started in 2011 (from 122% in 2011 to 81% in 2016)

As of 2009, the combined ratio for Accident & Sicknessrecorded a positive trend declining from 93% to 82% in 2016

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

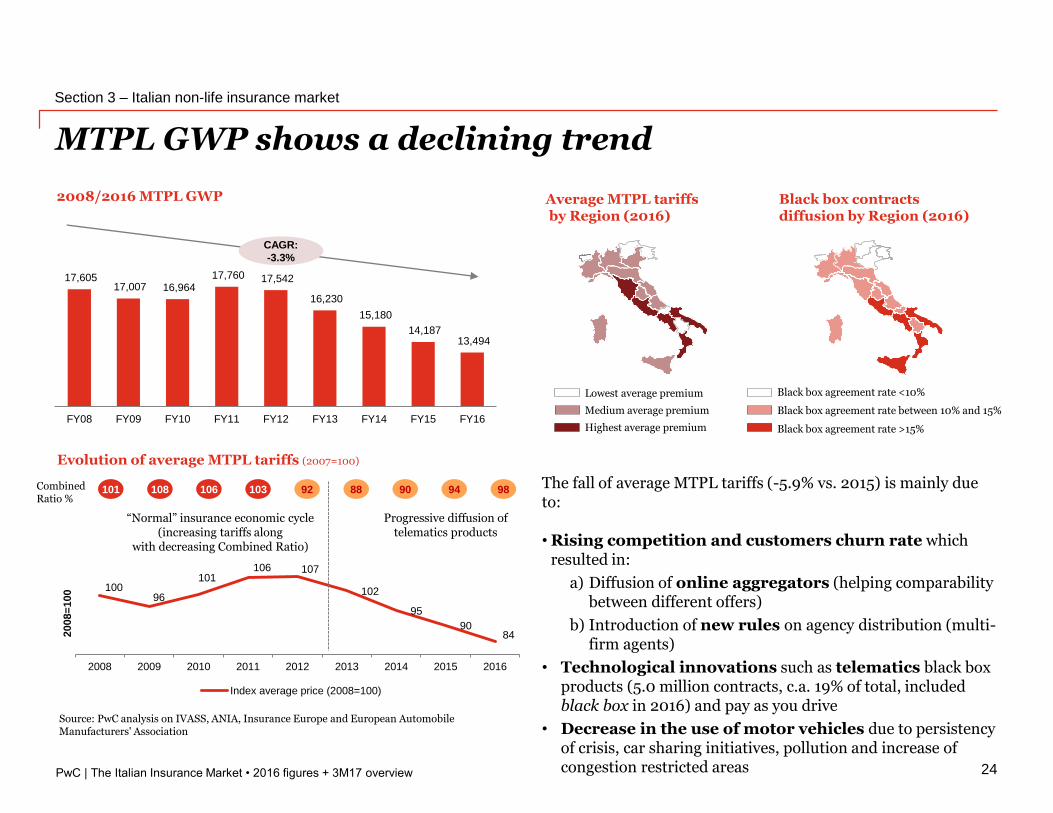

17,605 17,007 16,964

17,760 17,542

16,230

15,180

14,187 13,494

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

100 96

101 106 107

102

95

90 84

2008 2009 2010 2011 2012 2013 2014 2015 2016

2008=

100

Index average price (2008=100)

Section 3 – Italian non-life insurance market

24

MTPL GWP shows a declining trend

Evolution of average MTPL tariffs (2007=100)

The fall of average MTPL tariffs (-5.9% vs. 2015) is mainly due to:

• Rising competition and customers churn rate which resulted in:

a) Diffusion of online aggregators (helping comparability between different offers)

b) Introduction of new rules on agency distribution (multi-firm agents)

• Technological innovations such as telematics black box products (5.0 million contracts, c.a. 19% of total, included black box in 2016) and pay as you drive

• Decrease in the use of motor vehicles due to persistency of crisis, car sharing initiatives, pollution and increase of congestion restricted areas

Source: PwC analysis on IVASS, ANIA, Insurance Europe and European Automobile Manufacturers' Association

101 108 106 103 92 88 90

CAGR:

-3.3%

Combined Ratio %

Progressive diffusion of telematics products

“Normal” insurance economic cycle (increasing tariffs along

with decreasing Combined Ratio)

94

2008/2016 MTPL GWP Average MTPL tariffs by Region (2016)

Black box contracts diffusion by Region (2016)

Black box agreement rate between 10% and 15%

Black box agreement rate <10%

Black box agreement rate >15%

Medium average premium

Lowest average premium

Highest average premium

98

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

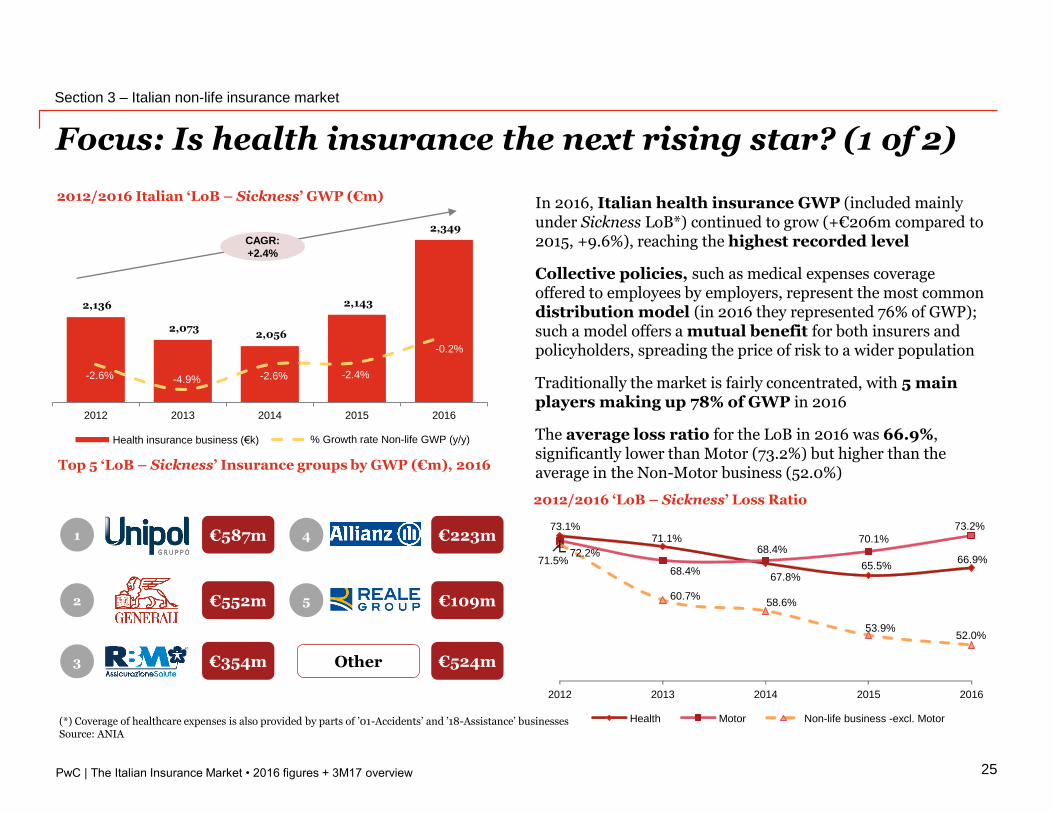

73.1% 71.1%

67.8% 65.5%

66.9% 72.2%

68.4%

68.4% 70.1%

73.2%

71.5%

60.7% 58.6%

53.9% 52.0%

2012 2013 2014 2015 2016

Health Motor Non-life business -excl. Motor

2,136

2,073 2,056

2,143

2,349

-2.6% -4.9% -2.6% -2.4%

-0.2%

2012 2013 2014 2015 2016

Health insurance business (€k) % Growth rate Non-life GWP (y/y)

Focus: Is health insurance the next rising star? (1 of 2)

Section 3 – Italian non-life insurance market

25

2012/2016 Italian ‘LoB – Sickness’ GWP (€m)

Top 5 ‘LoB – Sickness’ Insurance groups by GWP (€m), 2016

2012/2016 ‘LoB – Sickness’ Loss Ratio

Source: ANIA

In 2016, Italian health insurance GWP (included mainly under Sickness LoB*) continued to grow (+€206m compared to 2015, +9.6%), reaching the highest recorded level

Collective policies, such as medical expenses coverage offered to employees by employers, represent the most common distribution model (in 2016 they represented 76% of GWP); such a model offers a mutual benefit for both insurers and policyholders, spreading the price of risk to a wider population

Traditionally the market is fairly concentrated, with 5 main players making up 78% of GWP in 2016

The average loss ratio for the LoB in 2016 was 66.9%, significantly lower than Motor (73.2%) but higher than the average in the Non-Motor business (52.0%)

CAGR:

+2.4%

(*) Coverage of healthcare expenses is also provided by parts of ’01-Accidents’ and ’18-Assistance’ businesses

€587m

€552m

€354m

1

2

3 Other

€223m

€109m

€524m

4

5

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

Focus: Is health insurance the next rising star? (2 of 2)

Section 3 – Italian non-life insurance market

26

Source: “L’innovazione nell’assicurazione salute” - Egea 2016, ISTAT

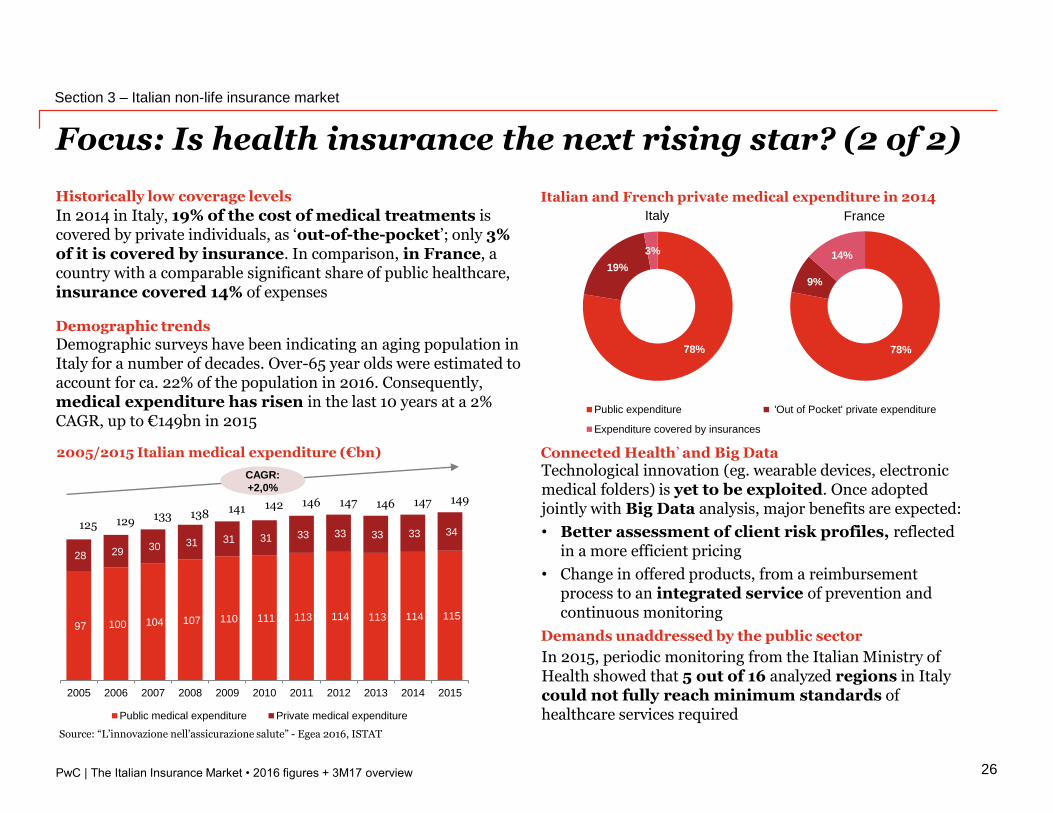

97 100 104 107 110 111 113 114 113 114 115

28 29 30 31 31 31 33 33 33 33 34

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Public medical expenditure Private medical expenditure

CAGR:

+2,0%

125 129 133 138 141 142 146 147 146 147 149

2005/2015 Italian medical expenditure (€bn)

Italian and French private medical expenditure in 2014

Connected Health’ and Big Data

Demands unaddressed by the public sector

Historically low coverage levels

In 2014 in Italy, 19% of the cost of medical treatments is covered by private individuals, as ‘out-of-the-pocket’; only 3%of it is covered by insurance. In comparison, in France, a country with a comparable significant share of public healthcare, insurance covered 14% of expenses

Demographic trends

Demographic surveys have been indicating an aging population in Italy for a number of decades. Over-65 year olds were estimated to account for ca. 22% of the population in 2016. Consequently, medical expenditure has risen in the last 10 years at a 2% CAGR, up to €149bn in 2015

Technological innovation (eg. wearable devices, electronic medical folders) is yet to be exploited. Once adopted jointly with Big Data analysis, major benefits are expected:

• Better assessment of client risk profiles, reflected in a more efficient pricing

• Change in offered products, from a reimbursement process to an integrated service of prevention and continuous monitoring

In 2015, periodic monitoring from the Italian Ministry of Health showed that 5 out of 16 analyzed regions in Italy could not fully reach minimum standards of healthcare services required

78%

19%

3%

Public expenditure 'Out of Pocket' private expenditure

Expenditure covered by insurances

78%

19%

3%

Public expenditure 'Out of Pocket' private expenditure

Expenditure covered by insurances

78%

9%

14%

Public expenditure 'Out of Pocket' private expenditure

Expenditure covered by insurances

Italy France

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

Top underwriters

Solvency II ratio

Section 3 – Italian non-life insurance market

27

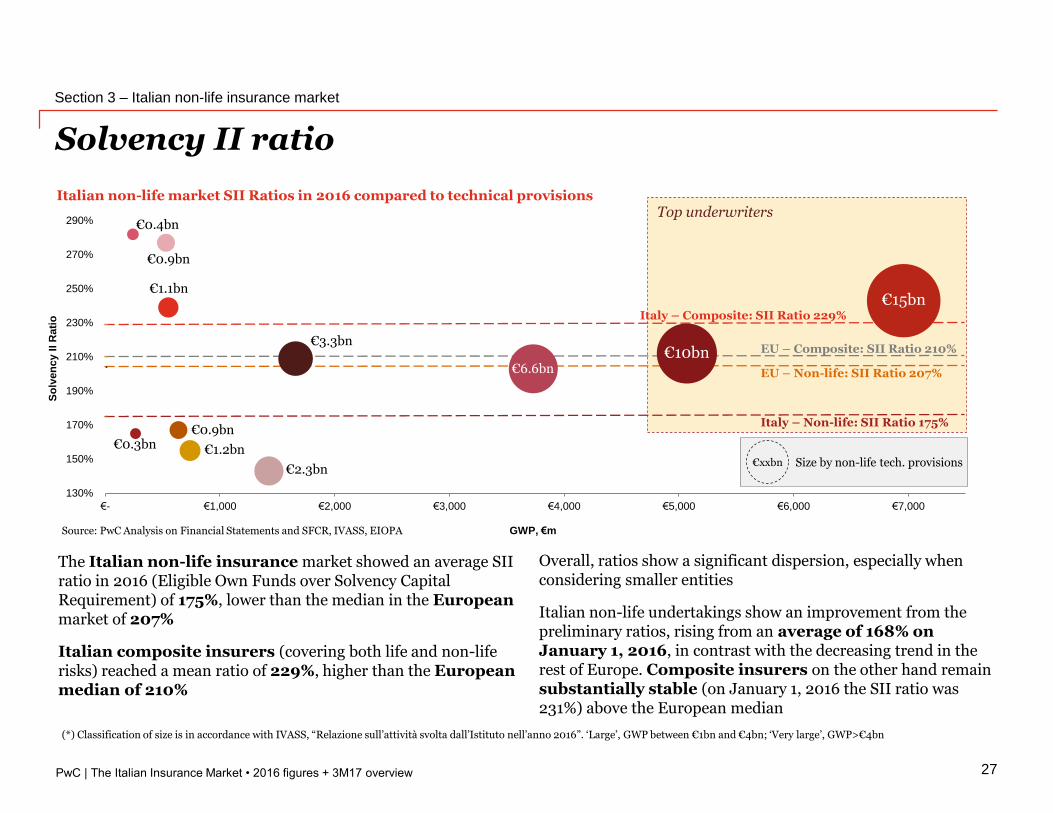

The Italian non-life insurance market showed an average SII ratio in 2016 (Eligible Own Funds over Solvency Capital Requirement) of 175%, lower than the median in the Europeanmarket of 207%

Italian composite insurers (covering both life and non-life risks) reached a mean ratio of 229%, higher than the European median of 210%

Overall, ratios show a significant dispersion, especially when considering smaller entities

Italian non-life undertakings show an improvement from the preliminary ratios, rising from an average of 168% on January 1, 2016, in contrast with the decreasing trend in the rest of Europe. Composite insurers on the other hand remain substantially stable (on January 1, 2016 the SII ratio was 231%) above the European median

Source: PwC Analysis on Financial Statements and SFCR, IVASS, EIOPA

(*) Classification of size is in accordance with IVASS, “Relazione sull’attività svolta dall’Istituto nell’anno 2016”. ‘Large’, GWP between €1bn and €4bn; ‘Very large’, GWP>€4bn

€0.9bn

Italy – Composite: SII Ratio 229%

EU – Composite: SII Ratio 210%

EU – Non-life: SII Ratio 207%

Italy – Non-life: SII Ratio 175%

€0.4bn

€1.1bn

€0.3bn€0.9bn

€1.2bn

€2.3bn

€3.3bn

130%

150%

170%

190%

210%

230%

250%

270%

290%

€- €1,000 €2,000 €3,000 €4,000 €5,000 €6,000 €7,000

€6.6bn

€15bn

€10bn

GWP, €m

So

lven

cy I

I R

ati

o

Italian non-life market SII Ratios in 2016 compared to technical provisions

€xxbn Size by non-life tech. provisions

PwC

3M17 overview & industry outlook

The Italian Insurance Market • 2016 figures + 3M17 overview

28

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

66%

29%

3% 2%

51%

49%

20,297 27,493

31,972 30,331 26,251

8,198

7,967

7,804 7,704 7,746

28,495

35,460 39,776 38,035

33,997

3M13 3M14 3M15 3M16 3M17

€m

illi

on

Life Non-Life

3M17: Insurance market trend update

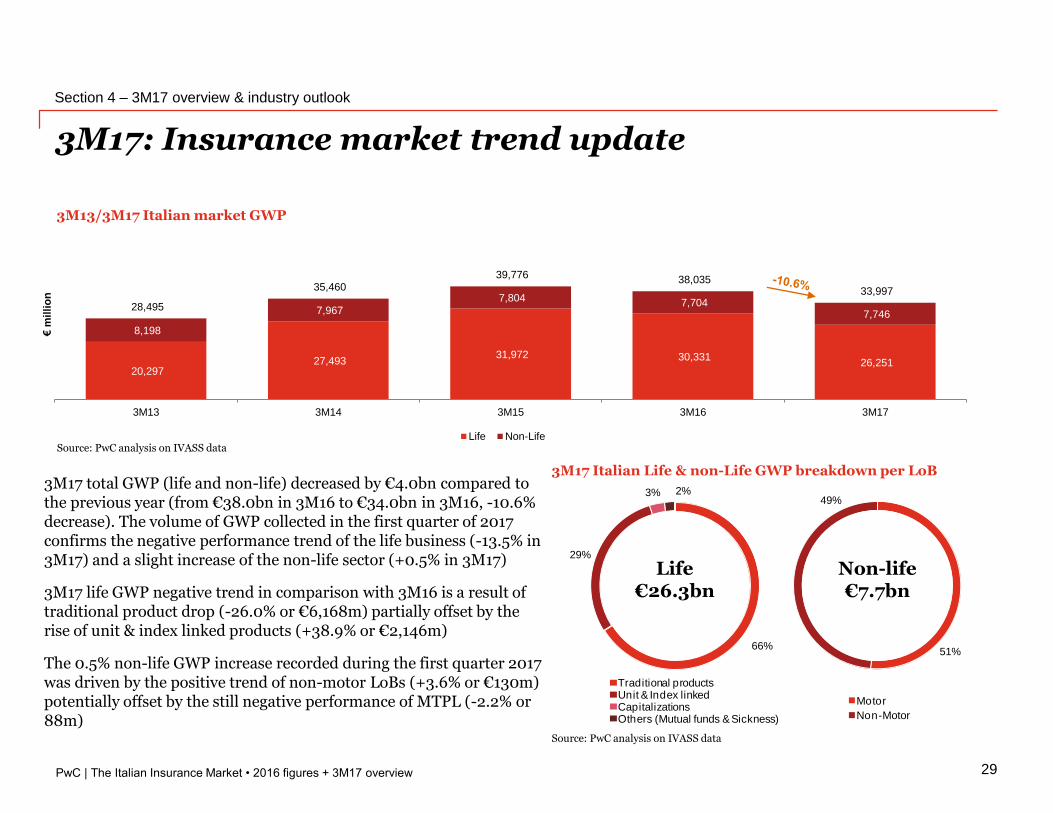

Section 4 – 3M17 overview & industry outlook

29

3M17 Italian Life & non-Life GWP breakdown per LoB

3M13/3M17 Italian market GWP

Life€26.3bn

Non-life€7.7bn

74%

21%

4% 2%

Traditional productsUnit & Index linkedCapitalizationsOthers (Mutual funds & Sickness)

58%

42%

Non-life market - Breakdown per motor and non-motor 3M13

Motor

Non-Motor

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

3M17 total GWP (life and non-life) decreased by €4.0bn compared to the previous year (from €38.0bn in 3M16 to €34.0bn in 3M16, -10.6% decrease). The volume of GWP collected in the first quarter of 2017 confirms the negative performance trend of the life business (-13.5% in 3M17) and a slight increase of the non-life sector (+0.5% in 3M17)

3M17 life GWP negative trend in comparison with 3M16 is a result of traditional product drop (-26.0% or €6,168m) partially offset by the rise of unit & index linked products (+38.9% or €2,146m)

The 0.5% non-life GWP increase recorded during the first quarter 2017 was driven by the positive trend of non-motor LoBs (+3.6% or €130m) potentially offset by the still negative performance of MTPL (-2.2% or 88m)

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

76%

75%

68%

72%

66%

24%

25%

32%

28%

34%

0% 20% 40% 60% 80% 100%

FY13

FY14

FY15

FY16

3M17

Traditional contracts Investment contracts

14,981

4,183

769 364

22,345

3,856

940 354

21,945

8,208

1,403418

23,494

5,519

856 461

17,326

7,665

769 491

Traditional products Unit & Index linked Capitalisations Others (Mutual funds & Sickness)

€m

illi

on

3M13 3M14 3M15 3M16 3M17

3M17: Italian life insurance market update

30

3M13/3M17 Breakdown per channelFY13/3M17 Breakdown per type of policies

Source: PwC analysis on IVASS data

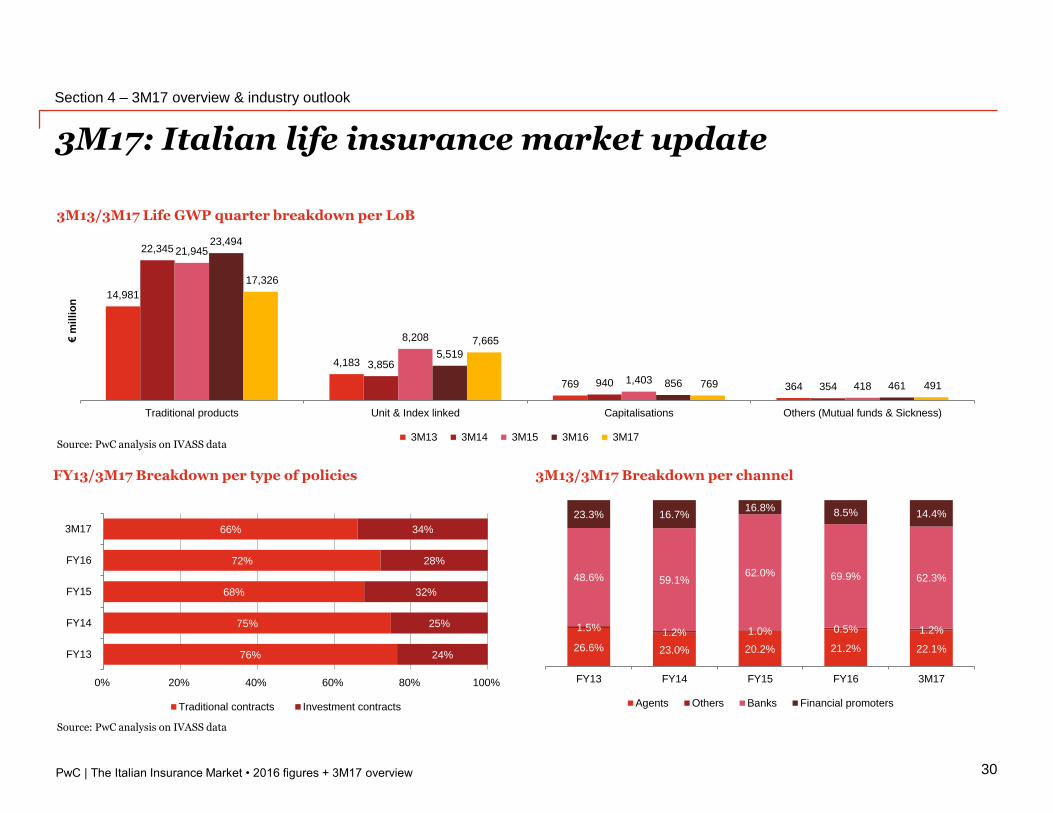

3M13/3M17 Life GWP quarter breakdown per LoB

Section 4 – 3M17 overview & industry outlook

Source: PwC analysis on IVASS data

26.6% 23.0% 20.2% 21.2% 22.1%

1.5% 1.2% 1.0% 0.5% 1.2%

48.6% 59.1% 62.0% 69.9% 62.3%

23.3% 16.7% 16.8% 8.5% 14.4%

FY13 FY14 FY15 FY16 3M17

Agents Others Banks Financial promoters

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

4,790

1,240 994

631 543

4,487

1,285

1,022 621 553

4,240

1,314

1,020 648 582

4,059

1,340 1,054

650 600

3,971

1,422 1,076

657 620

Motor Accident & Sickness Fire & other damages General TPL Other

€m

illi

on

3M13 3M14 3M15 3M16 3M17

3M17: Italian non-life insurance market update

31

3M13/3M17 Breakdown per distribution channel

3M13/3M17 GWP breakdown per main LoB

3M13/3M17 GWP breakdown per motor and non-motor

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

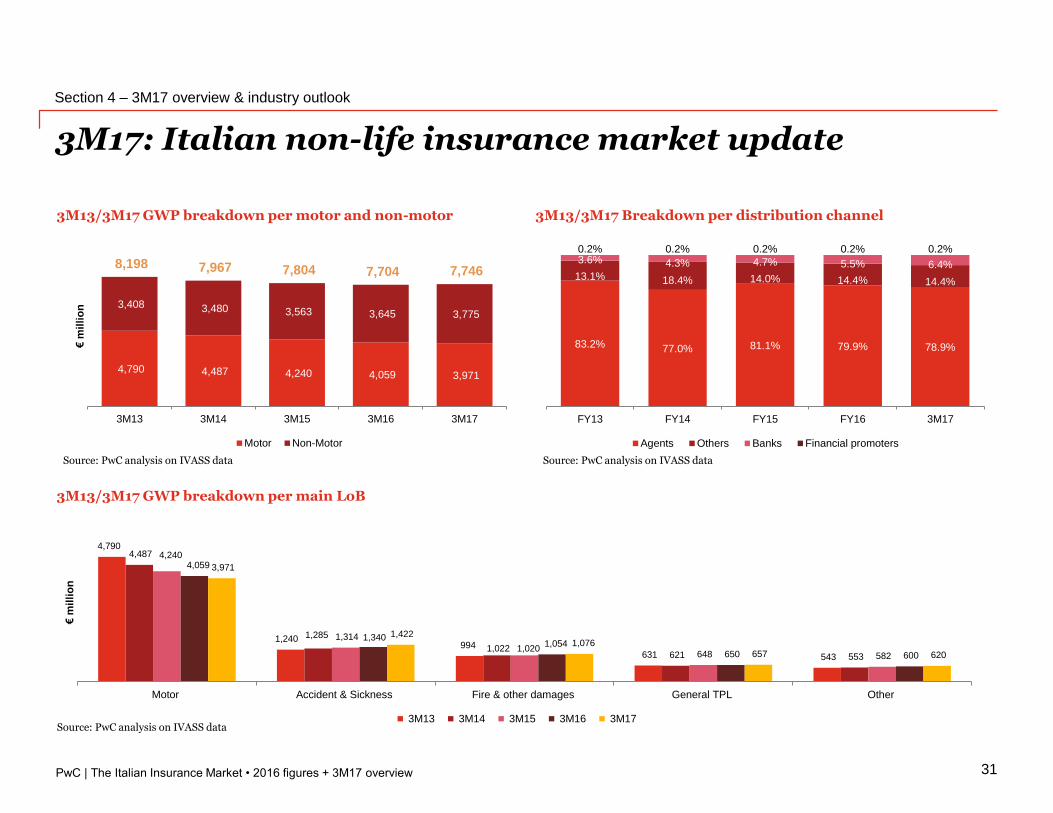

Section 4 – 3M17 overview & industry outlook

4,790 4,487 4,240 4,059 3,971

3,408 3,480 3,563 3,645 3,775

8,198 7,967 7,804 7,704 7,746

3M13 3M14 3M15 3M16 3M17

€m

illi

on

Motor Non-Motor

83.2% 77.0% 81.1% 79.9% 78.9%

13.1% 18.4% 14.0% 14.4% 14.4%

3.6% 4.3% 4.7% 5.5% 6.4%

0.2% 0.2% 0.2% 0.2% 0.2%

FY13 FY14 FY15 FY16 3M17

Agents Others Banks Financial promoters

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

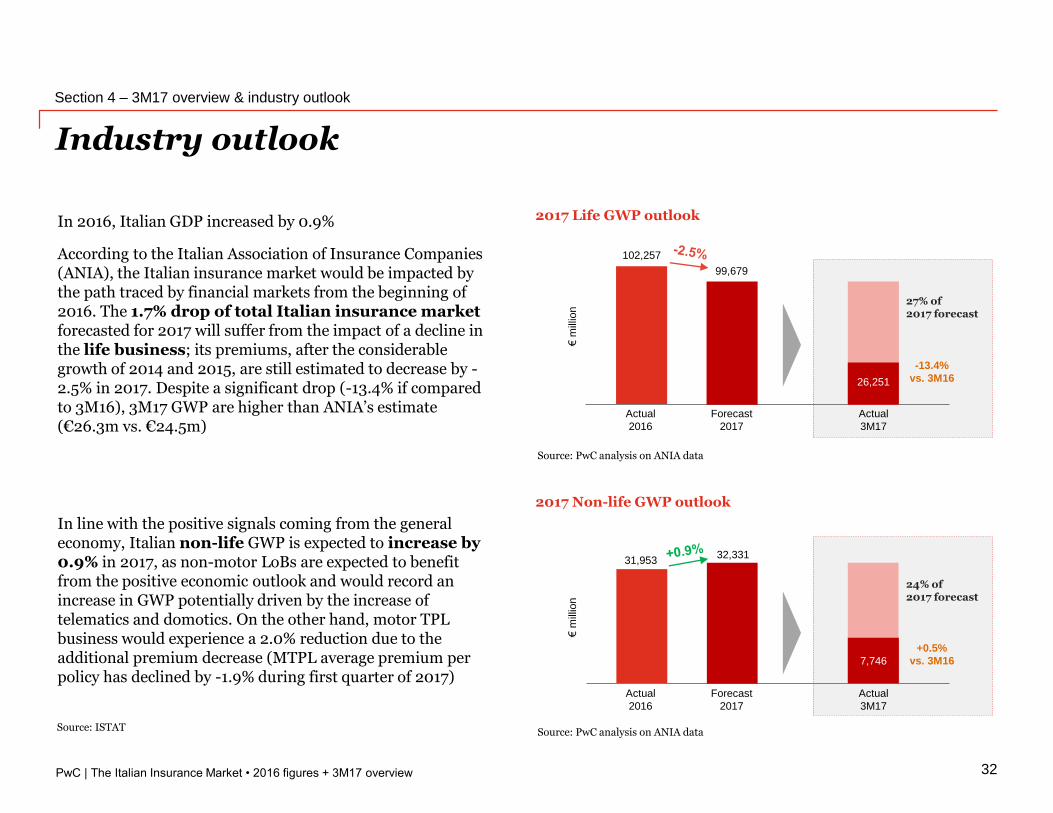

Industry outlook

32

2017 Non-life GWP outlook

2017 Life GWP outlook

Source: PwC analysis on ANIA data

Source: PwC analysis on ANIA data

102,257

99,679

Actual

2016

26,251

Forecast

2017

Actual

3M17

-13.4%

vs. 3M16

€m

illio

n

Actual

2016

Forecast

2017

Actual

3M17

31,95332,331

7,746

+0.5%

vs. 3M16

27% of 2017 forecast

24% of 2017 forecast

€m

illio

n

In 2016, Italian GDP increased by 0.9%

According to the Italian Association of Insurance Companies (ANIA), the Italian insurance market would be impacted by the path traced by financial markets from the beginning of 2016. The 1.7% drop of total Italian insurance marketforecasted for 2017 will suffer from the impact of a decline in the life business; its premiums, after the considerable growth of 2014 and 2015, are still estimated to decrease by -2.5% in 2017. Despite a significant drop (-13.4% if compared to 3M16), 3M17 GWP are higher than ANIA’s estimate (€26.3m vs. €24.5m)

In line with the positive signals coming from the general economy, Italian non-life GWP is expected to increase by 0.9% in 2017, as non-motor LoBs are expected to benefit from the positive economic outlook and would record an increase in GWP potentially driven by the increase of telematics and domotics. On the other hand, motor TPL business would experience a 2.0% reduction due to the additional premium decrease (MTPL average premium per policy has declined by -1.9% during first quarter of 2017)

Section 4 – 3M17 overview & industry outlook

Source: ISTAT

PwC

M&A activity

The Italian Insurance Market • 2016 figures + 3M17 overview

33

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

# Year Target Bidder

Stake

%

Deal Size

(€m)

1 2 01 7 Eu r ov ita A ssicu r a zion i S.p.A Cin v en Pa r tn er s LLP n d n d

2 2 01 6 UNIQA Pr otezion e Societa Rea le Mu tu a di A ssicu r a zion i S.p.A .1 00% 2 9 5

3 2 01 6 Old Mu tu a l Wea lth Ita ly SpA Cin v en Pa r tn er s LLP 1 00% 2 7 8

4 2 01 5 C.B.A . V ita SpA HDI A ssicu r a zion i SpA 1 00% n d

5 2 01 5 ERGO Pr ev iden za SpA Cin v en Pa r tn er s LLP n d n d

6 2 01 4 Ca r ig e V ita Nu ov a A pollo Globa l Ma n a g em en t 1 00% 1 7 0

7 2 01 3 Eu r ov ita A ssicu r a zion i JC Flow er s 8 0% 4 7

8 2 01 2 Ch ia r a V ita Helv et ia Holdin g A G 3 0% 2 3

9 2 01 1 Bipiem m e V ita SpA Cov ea 8 1 % 2 4 3

1 0 2 01 1 BNL V ita SpA Ca r dif A ssicu r a zion i SpA 5 1 % 3 2 5

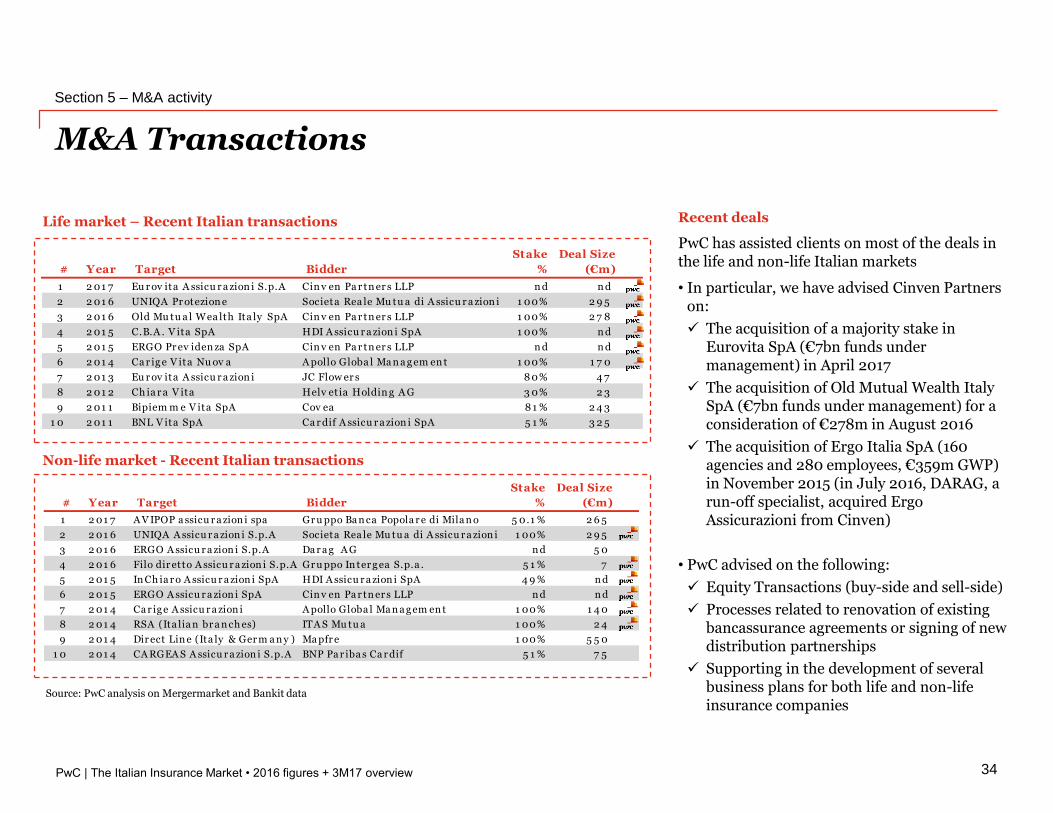

M&A Transactions

Section 5 – M&A activity

34

Life market – Recent Italian transactions

Non-life market - Recent Italian transactions

Source: PwC analysis on Mergermarket and Bankit data

Recent deals

PwC has assisted clients on most of the deals in the life and non-life Italian markets

• In particular, we have advised Cinven Partners on:

The acquisition of a majority stake in Eurovita SpA (€7bn funds under management) in April 2017

The acquisition of Old Mutual Wealth Italy SpA (€7bn funds under management) for a consideration of €278m in August 2016

The acquisition of Ergo Italia SpA (160 agencies and 280 employees, €359m GWP) in November 2015 (in July 2016, DARAG, a run-off specialist, acquired Ergo Assicurazioni from Cinven)

• PwC advised on the following:

Equity Transactions (buy-side and sell-side)

Processes related to renovation of existing bancassurance agreements or signing of new distribution partnerships

Supporting in the development of several business plans for both life and non-life insurance companies

# Year Target Bidder

Stake

%

Deal Size

(€m)

1 2 01 7 A V IPOP a ssicu r a zion i spa Gr u ppo Ba n ca Popola r e di Mila n o 5 0.1 % 2 6 5

2 2 01 6 UNIQA A ssicu r a zion i S.p.A Societa Rea le Mu tu a di A ssicu r a zion i S.p.A .1 00% 2 9 5

3 2 01 6 ERGO A ssicu r a zion i S.p.A Da r a g A G n d 5 0

4 2 01 6 Filo dir etto A ssicu r a zion i S.p.A . Gr u ppo In ter g ea S.p.a . 5 1 % 7

5 2 01 5 In Ch ia r o A ssicu r a zion i SpA HDI A ssicu r a zion i SpA 4 9 % n d

6 2 01 5 ERGO A ssicu r a zion i SpA Cin v en Pa r tn er s LLP n d n d

7 2 01 4 Ca r ig e A ssicu r a zion i A pollo Globa l Ma n a g em en t 1 00% 1 4 0

8 2 01 4 RSA (Ita lia n br a n ch es) ITA S Mu tu a 1 00% 2 4

9 2 01 4 Dir ect Lin e (Ita ly & Ger m a n y ) Ma pfr e 1 00% 5 5 0

1 0 2 01 4 CA RGEA S A ssicu r a zion i S.p.A BNP Pa r iba s Ca r dif 5 1 % 7 5

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

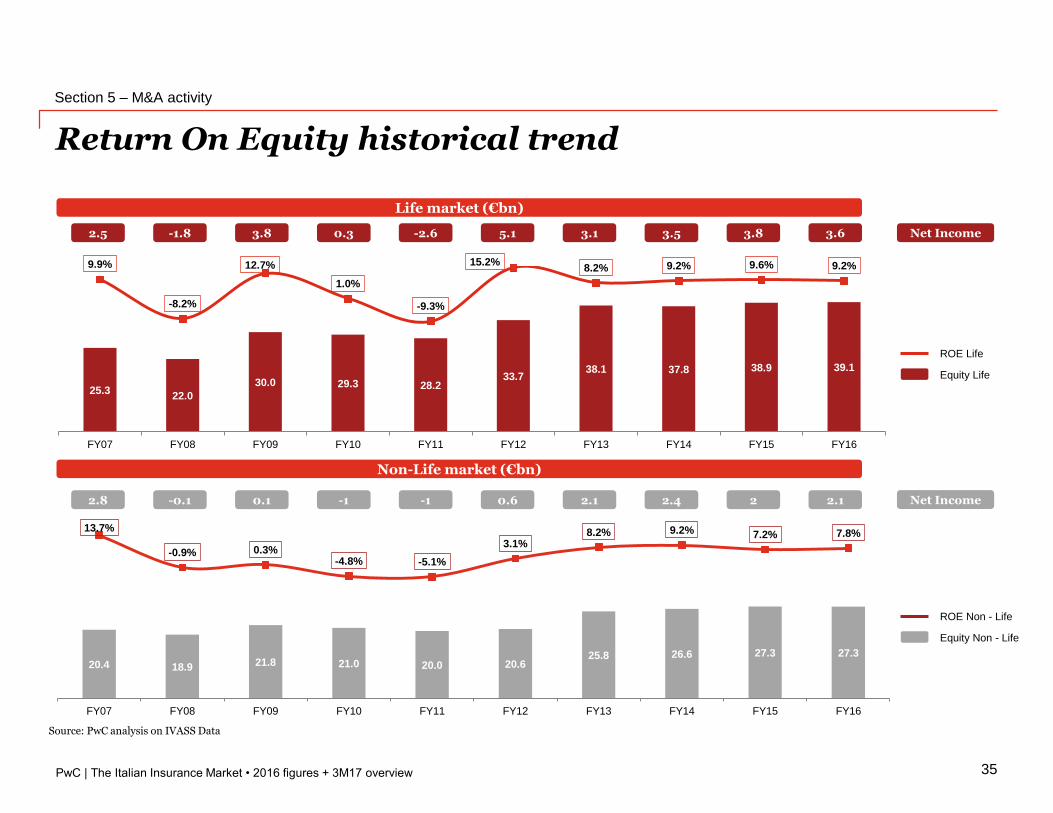

Return On Equity historical trend

Section 5 – M&A activity

35

Source: PwC analysis on IVASS Data

25.322.0

30.0 29.3 28.233.7

38.1 37.8 38.9 39.1

9.9%

-8.2%

12.7%

1.0%

-9.3%

15.2%8.2% 9.2% 9.6% 9.2%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

20.4 18.9 21.8 21.0 20.0 20.625.8 26.6 27.3 27.3

13.7%

-0.9% 0.3%-4.8% -5.1%

3.1%8.2% 9.2% 7.2% 7.8%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Non-Life market (€bn)

2.8 -0.1 0.1 -1 -1 0.6 2.1 2.4 2 2.1

2.5 -1.8 3.8 0.3 -2.6 5.1 3.1 3.5 3.8 3.6 Net Income

ROE Life

Equity Life

Net Income

ROE Non - Life

Equity Non - Life

Life market (€bn)

PwC

The Italian insurance market in the European context

The Italian Insurance Market • 2016 figures + 3M17 overview

36

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

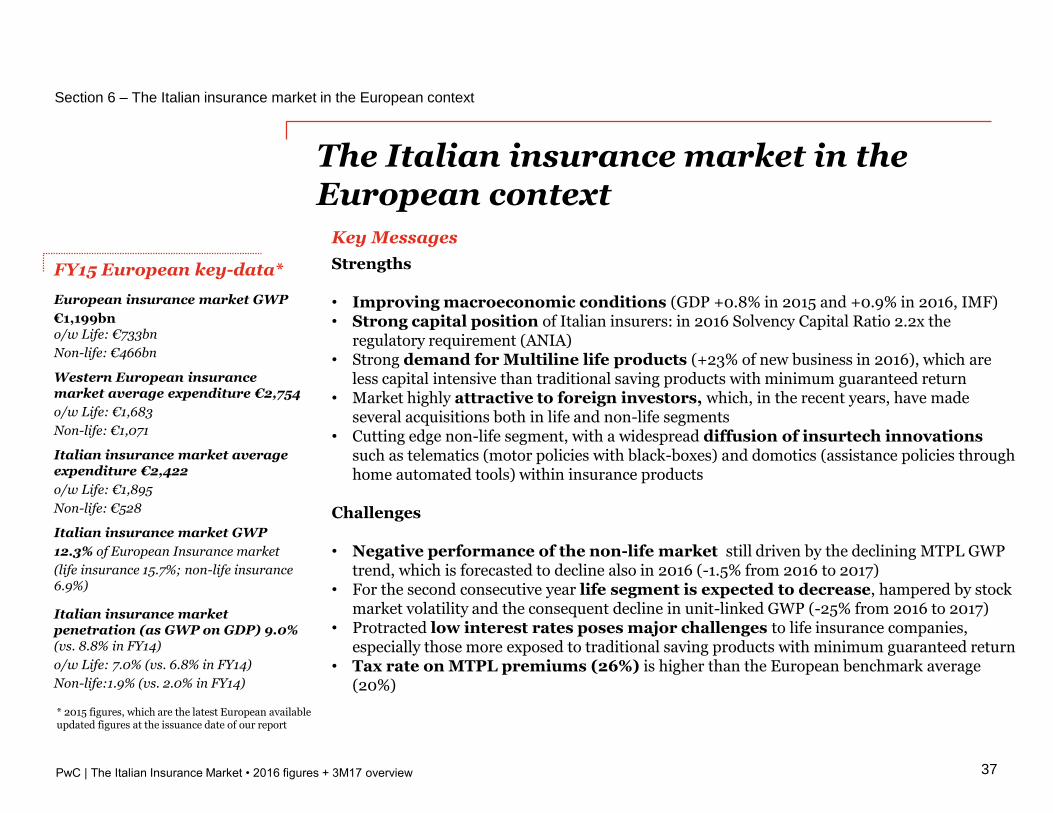

FY15 European key-data*

European insurance market GWP

€1,199bno/w Life: €733bn

Non-life: €466bn

Western European insurance market average expenditure €2,754

o/w Life: €1,683

Non-life: €1,071

Italian insurance market average expenditure €2,422

o/w Life: €1,895

Non-life: €528

Italian insurance market GWP

12.3% of European Insurance market

(life insurance 15.7%; non-life insurance 6.9%)

Italian insurance market penetration (as GWP on GDP) 9.0% (vs. 8.8% in FY14)

o/w Life: 7.0% (vs. 6.8% in FY14)

Non-life:1.9% (vs. 2.0% in FY14)

Section 6 – The Italian insurance market in the European context

37

The Italian insurance market in the European context

Key Messages

Strengths

• Improving macroeconomic conditions (GDP +0.8% in 2015 and +0.9% in 2016, IMF)• Strong capital position of Italian insurers: in 2016 Solvency Capital Ratio 2.2x the

regulatory requirement (ANIA)• Strong demand for Multiline life products (+23% of new business in 2016), which are

less capital intensive than traditional saving products with minimum guaranteed return• Market highly attractive to foreign investors, which, in the recent years, have made

several acquisitions both in life and non-life segments• Cutting edge non-life segment, with a widespread diffusion of insurtech innovations

such as telematics (motor policies with black-boxes) and domotics (assistance policies through home automated tools) within insurance products

Challenges

• Negative performance of the non-life market still driven by the declining MTPL GWP trend, which is forecasted to decline also in 2016 (-1.5% from 2016 to 2017)

• For the second consecutive year life segment is expected to decrease, hampered by stock market volatility and the consequent decline in unit-linked GWP (-25% from 2016 to 2017)

• Protracted low interest rates poses major challenges to life insurance companies, especially those more exposed to traditional saving products with minimum guaranteed return

• Tax rate on MTPL premiums (26%) is higher than the European benchmark average (20%)

* 2015 figures, which are the latest European available updated figures at the issuance date of our report

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

33.7 32.8 32.0

-

67.1 68.3 70.0

-

96.6 98.9 101.1

- 57.2 56.3 57.7 -29.4 29.3 29.5

-

68.8 65.6 70.6 85.1 110.5 114.9

-

118.8 128.9 135.7

-

90.8 93.7 92.7

-

18.3 17.5 14.7

-

25.9 25.2 25.6

-

184.4 175.8 183.4

118.8 143.3 147.0

185.9 197.2 205.7 187.4 192.6 193.8

75.5 73.8 72.4 55.2 54.4 55.1

253.2 241.4 254.0

FY13 FY14 FY15 FY13 FY14 FY15 FY13 FY14 FY15 FY13 FY14 FY15 FY13 FY14 FY15 FY13 FY14 FY15

€m

illi

on

Life market Non-life market

ItalyFrance

Germany

NetherlandsSpain

United Kingdom

-

500

1,000

1,500

2,000

2,500

3,000

3,500

(500) - 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

GW

P -

Lif

e (

€)

GWP - Non-Life (€)

European insurance market

Section 6 – The Italian insurance market in the European context

38

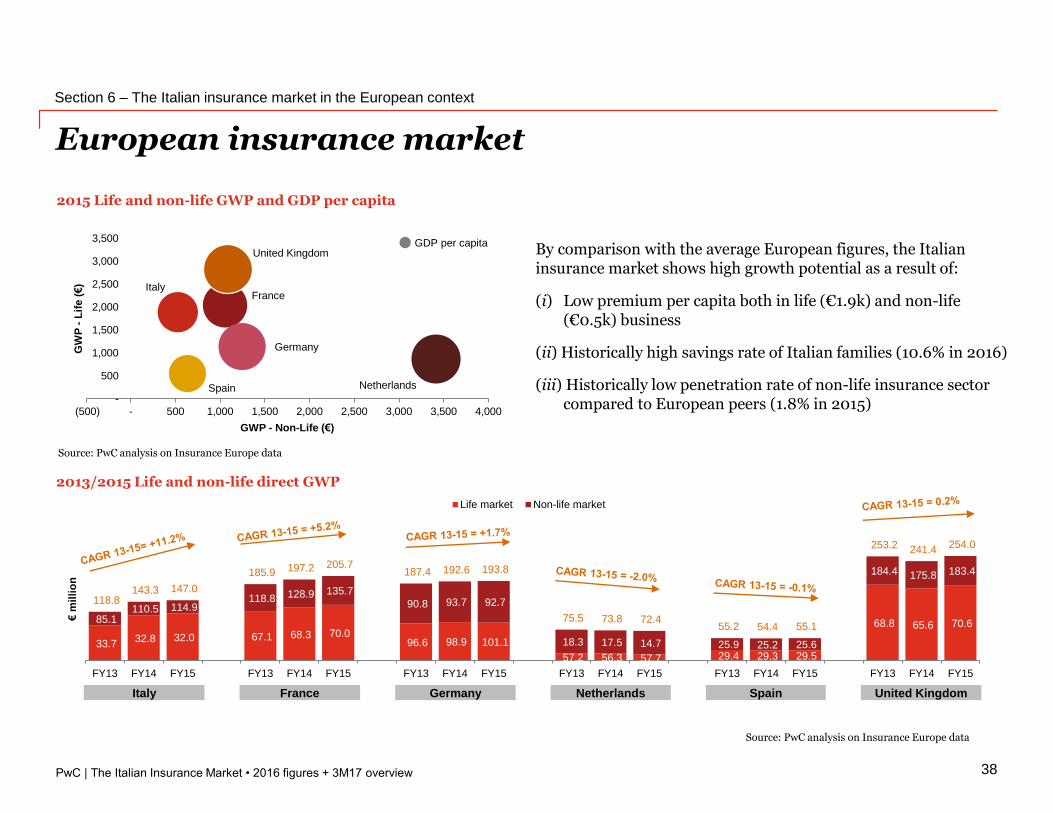

By comparison with the average European figures, the Italian insurance market shows high growth potential as a result of:

(i) Low premium per capita both in life (€1.9k) and non-life (€0.5k) business

(ii) Historically high savings rate of Italian families (10.6% in 2016)

(iii) Historically low penetration rate of non-life insurance sector compared to European peers (1.8% in 2015)

2013/2015 Life and non-life direct GWP

2015 Life and non-life GWP and GDP per capita

Source: PwC analysis on Insurance Europe data

Source: PwC analysis on Insurance Europe data

GDP per capita

France Germany Netherlands Spain United KingdomItaly

PwC | The Italian Insurance Market • 2016 figures + 3M17 overview

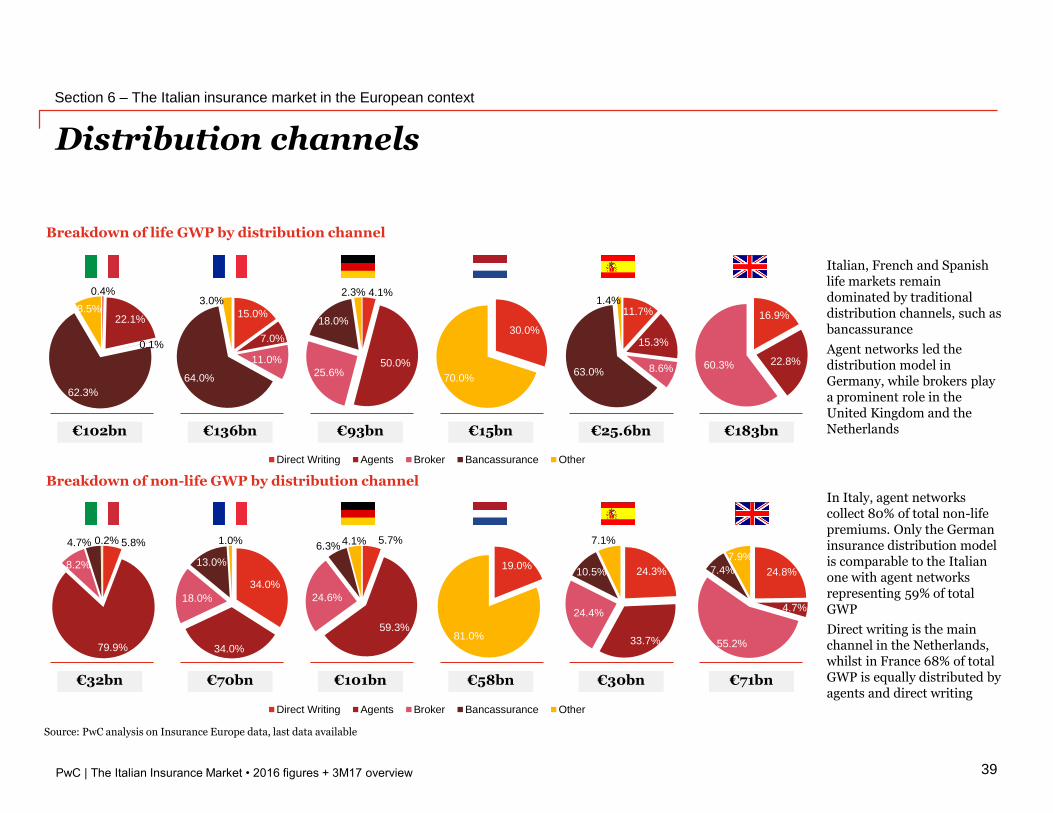

Breakdown of life GWP by distribution channel

Distribution channels

Section 6 – The Italian insurance market in the European context

39

Breakdown of non-life GWP by distribution channel

Source: PwC analysis on Insurance Europe data, last data available

0.4%

22.1%

0.1%

62.3%

8.5% 15.0%

7.0%

11.0%

64.0%

3.0%4.1%

50.0%25.6%

18.0%

2.3%

30.0%

70.0%

11.7%

15.3%

8.6%63.0%

1.4%

16.9%

22.8%60.3%

5.8%

79.9%

8.2%

4.7% 0.2%

34.0%

34.0%

18.0%

13.0%

1.0% 5.7%

59.3%

24.6%

6.3%4.1%

19.0%

81.0%

24.3%

33.7%

24.4%

10.5%

7.1%

24.8%

4.7%

55.2%

7.4%

7.9%

€102bn €136bn €93bn €15bn €25.6bn €183bn

€32bn €70bn €101bn €58bn €30bn €71bn

Italian, French and Spanish life markets remain dominated by traditional distribution channels, such as bancassurance

Agent networks led the distribution model in Germany, while brokers play a prominent role in the United Kingdom and the Netherlands

In Italy, agent networks collect 80% of total non-life premiums. Only the German insurance distribution model is comparable to the Italian one with agent networks representing 59% of total GWP

Direct writing is the main channel in the Netherlands, whilst in France 68% of total GWP is equally distributed by agents and direct writing

15.0%7.0%11.0%64.0%3.0% Direct Writing Agents Broker Bancassurance Other

15.0%7.0%11.0%64.0%3.0% Direct Writing Agents Broker Bancassurance Other

Our contacts

Emanuele GrassoPartner | Financial Services

T: +39 02 7785 372M: +39 348 [email protected]

Gabriele PicutiSenior Associate | Financial Services

M: +39 344 [email protected]

Marco FalcheroAssociate Partner | Financial Services

T: +39 02 7785 951M: +39 335 [email protected]

Davide BigattiSenior Associate | Financial Services

M: +39 340 [email protected]

© 2017 PricewaterhouseCoopers Advisory SpA. All rights reserved. PwC refers to PricewaterhouseCoopers Advisory SpA and may sometimes refer to the PwC

network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes

only, and should not be used as a substitute for consultation with professional advisors.

Related Documents