D2n,Ht S>K CIRCULATING COPY R E S T R I C T E D X T I 3-To TO BE REll TO REPORTS DESK IN GENERAL FILES Report No. TO-278a ONT_ \VZE C) N e p o t N 0. TO-278 This report was prepared for use within the Bank. It may not be published nor may it be quoted as representing the Bank's views. The Bank accepts no responsibility for the accuracy or completeness of the contents of the report. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT APPRAISAL OF PROPOSED THIRD LOAN TO PAKISTAN INDUSTRIAL CREDIT AND INVESTMENT CORPORATION, LIMITED PAKISTAN June Z, 1961 FILE COPY Departmenlt of Technical Operations Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

D2n,Ht S>K CIRCULATING COPY R E S T R I C T E DX T I 3-To TO BE REll TO REPORTS DESK

IN GENERAL FILES Report No. TO-278aONT_ \VZE

C) N e p o t N 0. TO-278

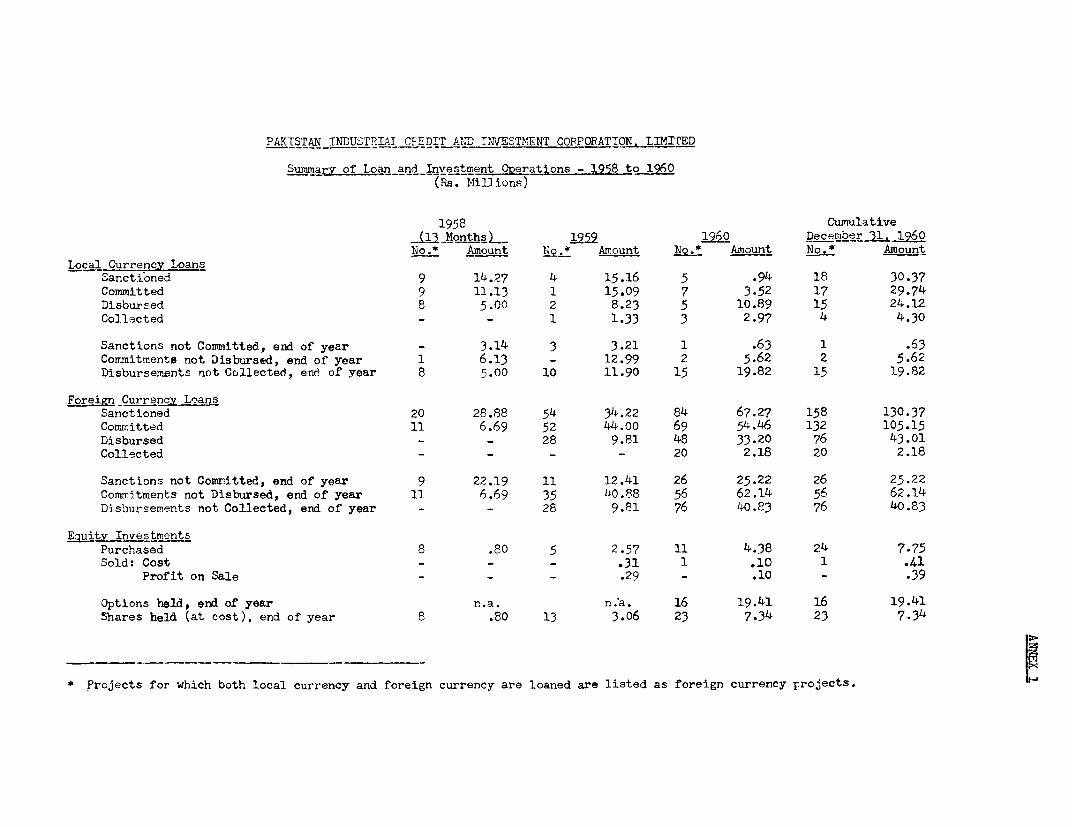

This report was prepared for use within the Bank. It may not be publishednor may it be quoted as representing the Bank's views. The Bank accepts noresponsibility for the accuracy or completeness of the contents of the report.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

APPRAISAL OF PROPOSED THIRD LOAN TO

PAKISTAN INDUSTRIAL CREDIT AND INVESTMENT CORPORATION, LIMITED

PAKISTAN

June Z, 1961

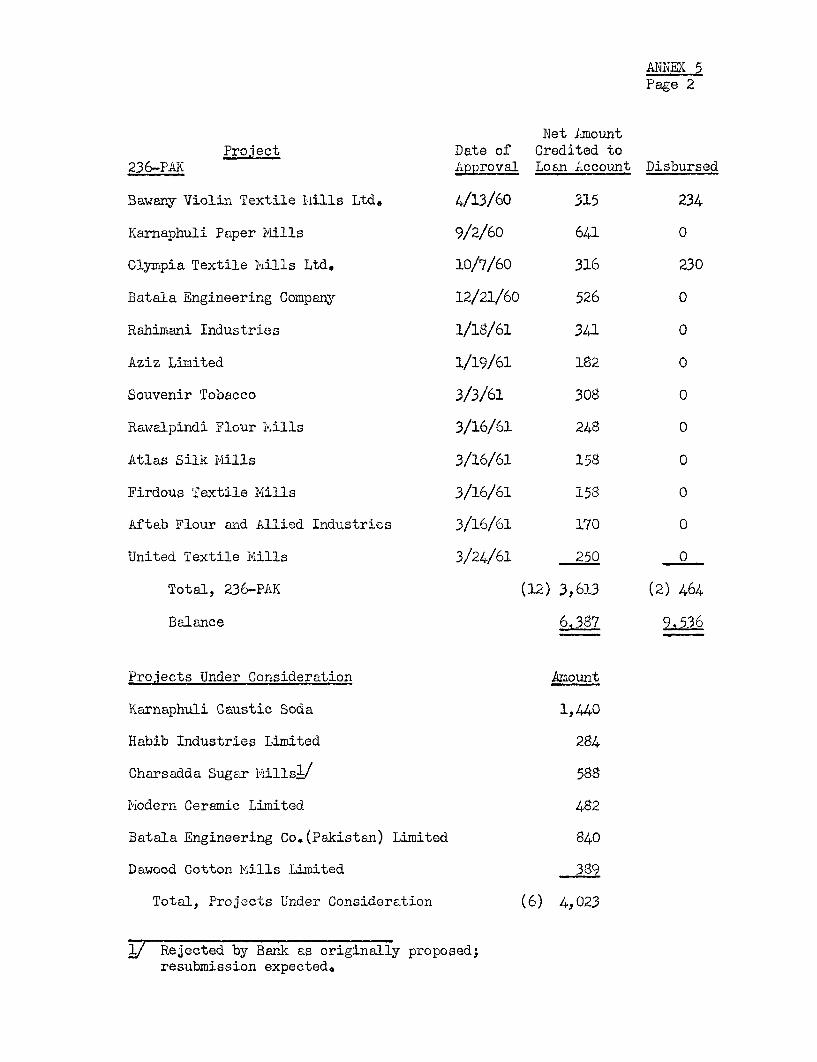

FILE COPYDepartmenlt of Technical Operations

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

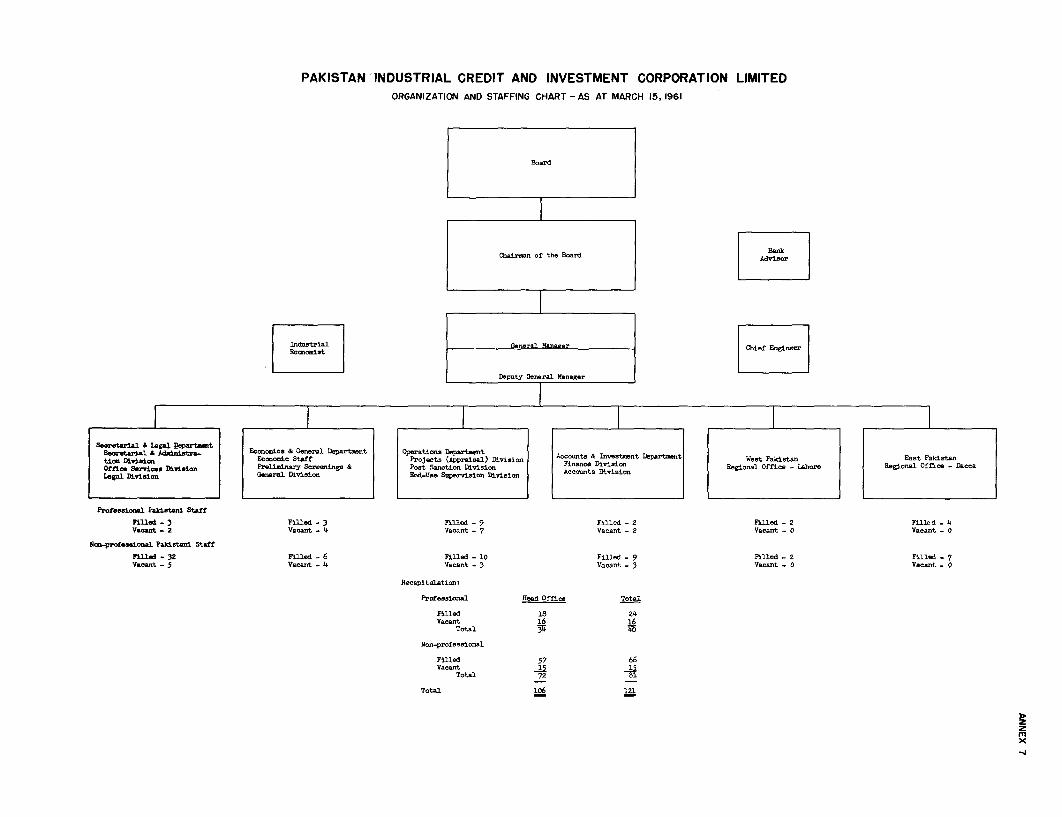

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

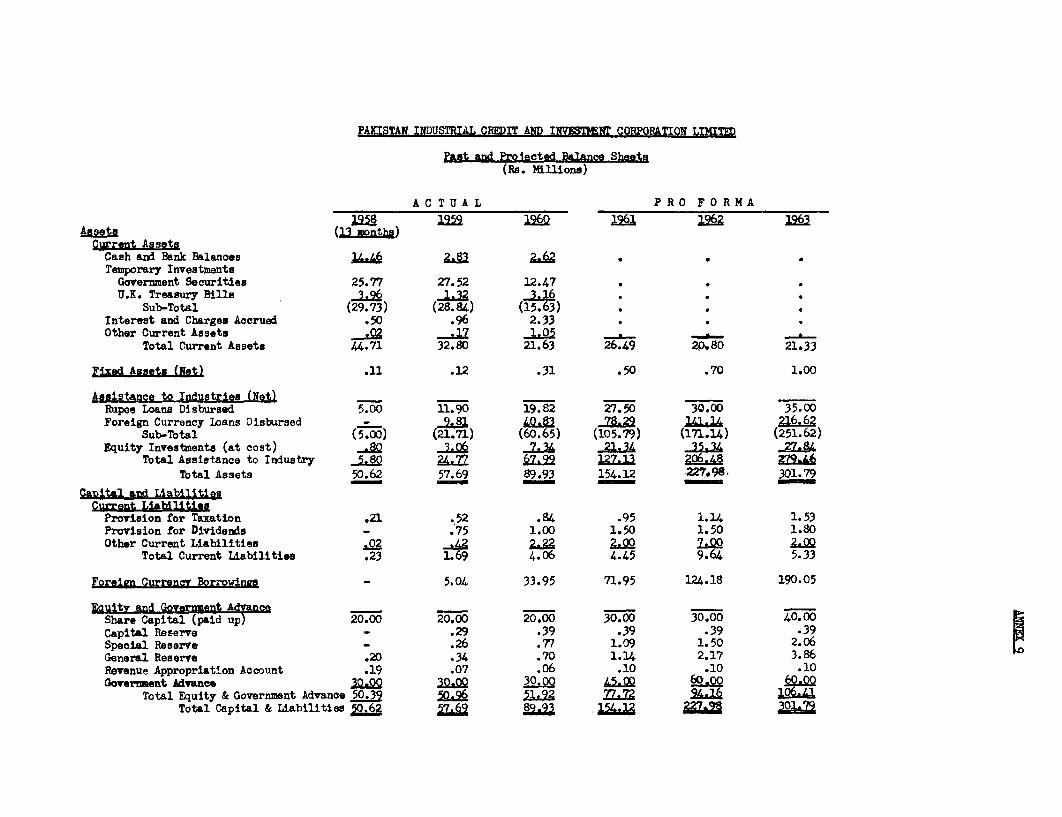

rized

CURRENCY EQUIVALENTS

U.S. $1. 00 = 4.762 Rupees1 Rupee = U.S. $0. 211,000,000 Rupees = U.S. $210,000

APPRAISAL OF PROPOSED THIRD LOAN TO

PAKISTAN INDUSTRIAL CREDIT AND INSTMENT CORPORATION, LIMITED

TABLE OF CONTENTS

Paragraphs

SUMMARY AND CONCLUSIONS . . . . , . . . . i -xiv

I. INTRCDUCTION . . . . . . . . . . . . . . . 2.

II. PURPOSE AND CAPITAL STRUCTURE . . . . . . 2 - 6

III. CREDIT AMD INVESTENT OPERATIONS TO DATE . 7 - 28Rupee Lending . . . . . . 8Foreign Currency Lending. . . . . .,.. 9 - 15Equity Capital Participations . . . . . 16 - 19Underwriting . . . . . . . . . . .. . 20Evaluation of PICIC Operations to Date . 21 - 28

IV. MANAGEMENT AND ORGANIZATION . . . . . . . 29 - 40

V. FINANCIAL POSITION . . .. . . . . . .. 41 - 51

VI. FINANCIAL PROSPECTS . . . . . . .. .. , 52 - 62

VII. ECONOMIC JUSTIFICATION . .l . . . . . . 63 - 65

VIII. CONCLUSIONS AND RBC0MTENDATIONS . . . . . 66 - 71

ANNEXES

1 - Summary of Loan and Investment Operations - 1958-19602 - Actual and Proposed Lending (Graph)3 - Resume of Loans Sanctioned as at December 31, 1960

(Charts)4 - Summary of Foreign Currency Borrowing and Lending

Operations as at December 31, 19605 - Status of IBRD Loans 185-PAK and 236-PAK as at

March 31, 19616 - Board of Directors and Executive Committee as at

December 31, 19607 - Organization and Staffing Chart as at March 15, 19618 - Financial Position (Cumulative)9 - Past and Projected Balance Sheets

10 - Past and Projected Profit and Loss Statements11 - Assumptions Employed in Financial Forecasts

APPRAISAL OF PROPOSED THIRD LQON TO

PAKISTAN INDUSTRIAL CREDIT AND INV\ESTENTT CORPORATION, LIMITED

SUTMARY AMD CONCLUSIONS

i. The Pakistan Industrial Credit and Investment Corporation,Limited (PICIC) has requested a Bank loan of $15 million to augment itsforeign exchange resources. This would be in addition to two previousBank loans totalling $14.2 million, two previous loans from the Develop-ment Loan Fund (DLF) also totalling $14.2 million, and other proposed1961 foreign exchange borrowings of $15 million (para. 1).

ii. PICIC was established in 1957 to assist in the creation, expan-sion, and modernization of private industrial enterprises, to encourageprivate local and foreign capital participation in their financing andto assist generally in the creation of a securities market. Its paid-upcapital is Rs.20 million, of which 60% is held by Pakistani shareholdersand the balance by U.S., Canadian, U.K., and Japanese private interests.PICIC has obtained a 30-year interest-free advance from the PakistanGovernment of Rs.30 million which is subordinated to all other outstandingdebts and to equity capital. As at December 31, 1960, PICIC's resources,including capital, reserves, and its loans from IBPD and DLF amountedto Rs.187.1 million, of which Rs.45.9 million originally was in the formof local currency a-nd Rs.141.2 million in foreign exchange (para. 4).

iii. PICIC is raising an additional Rs.10 million in equity capitalduring the spring of 1961, and proposes to raise a like amount early in1963. For the first time German participation is expected. The Govern-ment of Pakistan has agreed to make an additional Rs.30 million advanceto PICIC prior to June 1962, under terms identical with the first advance,except that interest of about 4% will be charged (paras. 5 - 6).

iv. At the end of 1960, PICIC had a portfolio of 91 loans amountingto Rs.60.7 million outstanding and equity siares in 23 inustrial concerns acquiredat a cost of Rs.7.34 million. In addition its Board had sanctioned, orapproved, 85 loans involving Rs.93.6 million, Rs.67.8 million of which hadbeen committed in loan agreements. Rupee lending has tapered off, due tonew rupee requirements for equity investments. Foreign currency lending,however, has remained a major PICIC activity, since until now there hasbeen virtually no other regular source of foreign currency in Ftkistan fr p2anterection and expansicn in the private sector. Foreign exchange loans for 84

projects amounting to Rs.67,27 million were sanctioned during 1960, morethan were sanctioned during the preceding two-year period. Demand remainshigh, as PICIC during January and February 1961, received 55 new applica-tions for foreign currency loans totalling Rs.103.2 million (paras. 7 - 15)

- ii -

v. During 1960 PICIC also purchased more equity shares than in theperiod 1958-1959. It has acquired most of its shares by exercise of optionsunder loans, but more than a quarter have been purchased on the securitiesmarket. Shares sold and those still held have appreciated in the climbingKarachi securities market. PICIC underwrote its first securities issue in1960 and expects to increase this activity (paras. 16 - 20).

vi. PIGIC's investment and loan portfolio is unseasoned, but alreadythere is evidence that many projects are not moving as quickly or as success-fully as expected. Most loans will probably prove collectible under pre-vailing economic conditions, however, because much of PICIC's lending hasbeen to established businessmen who need foreign currencies, especially forexpansion, but who do not need credit. In this way, and by obtaining equityshares on a relatively riskless basis, PICIC has avoided normal developmentrisks. As a result of lending largely on the basis of assumed credit-worthiness of the borrower, PICIC has not done an adequate job of apprais-ing projects, especially for local currency loans and loans using DLF fundswithout prior approval. Its end-use supervision also has been deficient(paras. 21 - 28).

vii. PICIC's management and staff have yet to reach the level orcapability where existing projects can be supervised and the steady flowof applications can be given adequate analysis. As at March 15, 1961,PICIC had filled only 55% of its planned positions for professional staffin the Karachi office. The key position of Deputy General Manager remainedunfilled. In fact, during the preceding year, several key persons left dueto dissatisfaction with pay and certain personnel practices. PICIC hastaken minor steps to improve the situation, but they may prove to be in-adequate to recruit and hold a competent staff. PICIC recently reorganizedto bring project appraisal and end-use under a single department. A Pro-ject Appraisal Committee, headed by the General Manager, also was establishedand should improve the quality of appraisals. The IBRD Advisor and a foreignChief Enginear have recently been joined by a senior economist to be madeavailable through the U.S. International Cooperation Administration (IC-),Additional foreign technicians in the fields of financial appraisal and secu-rities rnrketirg nayeLso be requt!ed for a year or two, not only to train PICIC'sPakistani staff, but to actually raise the level of performance (paras.29 - 40).

viii. At the start of 1961 PICIC had rupee resources sufficient tolast until mid yoar and its foreign currency resources were coriitted byFebruary. PICIC's financial position is satisfactory and its planned activi-ties can be carried out under the existing debt.equity ratio of 3:1, setforth in the Articles of Association (paras, 41 - 44).

ix. PICIC's after-tax earnings continued to improve in 1960, morethan doubling the 1958-1959 total. They remain modest, however, beingonly 3.8% of capital and surplus, including the interest-free Govermnentadvance. Much of PICIC's retained earnings are attributable to specialtax advantages. Gross income has been largely from interest on loans.

- iii -

Originally PICIC enjoyed a 4% - 5% interest rate spread on the foreign cur-rency it lent, but it recently revised its rates to yield a more modest2% - 3-e%. Thus, future earnings may be increasingly expected from divi-dends and gains on equity shares and from underwriting fees (paras. 45 - 51).

x. PICIC proposes to borrow $30 million in 1961 for the period 1961-1962, including $15 million from the Bank. It has just borrowed $7.5 nil2ionfrom DIF,and is considering German and Japanese offers. PICIC has no firminvestment plan for the period 1961-1963 except for specific cement andsugar projects. Its sustained receipt of applications, however, raiseslittle doubt that the funds can be usefully employed. Even if its proposed1961-1962 borrowings and lendings are accomplished, PICIC will be slightlybehind the ambitious targets set for it by the Second Five-Year Plan. PICICmay face more competition from the Pakistan Industrial Finance Company sincePIFCO also will be lending foreign exchange (paras. 52 - 61).

xi. PICIC should satisfy its rupee requirements by selling portfoliosecurities or by considering raising Rs.10 million share capital in 1962rather than 1963. It should use a prospective credit line with the StateBank of Pakistan only for short-term needs until expected receipts can becollected (paras. 61 - 62).

xii. PICIC's economic contribution cannot be properly measured, becauseit does not yet fully assess the economic merits of its individual projects.In terms of capital formation, foreign exchange earnings or savings, andjob creation, however, the projects will benefit the Pakistan economy.PICIC has loaned to 36 new entrepreneurs and encourages family-owned busi-nesses to permit public participation (paras. 63 - 65).

xiii. After three years, it is still necessary to consider PICIC'srequest for a third loan on the basis of proposals for improved managementrather than on the basis of past performance or demonstrated capability.Nevertheless PICIC's prospects are good, warranting further Bank support.Any loan, however, should be subject to the following conditions:

a) PICIC's account should not be credited with more than$7.5 million until a date to be mutually agreed betweenPICIC and the Bank. This provision would give the Bankan opportunity to evaluate jointly with PICIC's manage-ment at a date roughly mid-point in the crediting periodof the proposed loan, the improvement in PICIC's manage-ment, including project appraisal and end-use activities.

b) PICIC's account should continue to be credited underthe proposed loan only following prior Bank approvalof each project. (However, PICIC might be advisedinformally that a project limit not requiring detailedBank appraisal will be considered on the basis ofimprovement reflected in project appraisal submissionsand the report of any end-use missions.)

- iv -

c) PICIC should agree to utilize its proposed line ofcredit with the State Bank of Pakistan only fortemporary working capital requirements pending thetime when expected receipts can be collected andused for repayment.

d) If Pakistan Government concurrence can be obtained,an amortization schedule should be employed whichcorresponds to PICIC's scheduled collections offunds lent under the loan. The normal repaymentperiod would not exceed 10 years from the date ofcrediting, although extension might be requiredin the case of especially large projects.

(Paras. 66 - 70.)

xiv. Assuming agreement on the foregoing conditions, PICIC is con-sidered to be a suitable organization for a Bank loan of $15 millionequivalent.

I. INTRODUCTION

19 The Pakistan Industrial Credit and Investment Corporation,Limited (PICIC) has requested a Bank loan of $15 million. This amount,together with other planned borrowings, is expected to meet the foreignexchange credit demands of PIGIC's customers within the Pakistan industrialcommunity for the next two years and to achieve partially the lending goalsset for PICIC by the Government of Pakistan under the Second Five-YearPlan. The proposed loan would be the third Bank loan to PICIC. Two earlierloans (Nos. 185-PAK and 236-PAK) were made in 1957 and 1959 for $4.2 millionand $10.0 million, respectively. The following appraisal is based upon in-formation submitted by PICIC and upon investigations of PICICts operationsand prospects carried out by a Bank staff member in the field from MYarch 8to March 22, 1961,

II. PURPOSE AND CAPITAL STRUCTURE

2. PICIC was established to assist in the creation, expansion, andmodernization of private industrial enterprises, to encourage privatelocal and foreign capital participation in their financing, and to assistgenerally in the creation of a securities market.

3. PICIC was incorporated on September 26, 1957 and started operationson December 2, 1957. The corporation has an authorized share capital ofRs.150 million ($31.5 million equivalent). Its paid-up capital is Rs.20million ($4.2 million equivalent), consisting of two million Rs.10/shares.Of these, 60% has been subscribed by Pakistani shareholders, and the balanceby U.S., Canadian, U.K., and Japanese private interests. The 800,000 sharesheld by non-Pakistanis were purchased with foreign currencies except for200,000 shares purchased with rupees by British insurance and other com-panies. Thus, PICICfs first issue of paid-in capital generated Rs.14 mil-lion in rupees and Rs.6 million in U.S. dollars and pounds sterling.PICIC has been permitted to hold these latter funds in NTew York and London,principally for opening letters of credit for borrowers prior to creditingof the loan account by the Bank.

4. On December 17, 1957, PICIC obtained a 30-year interest-freeadvance from the Pakistan Government of Rs.30 million ($6.3 million equiva-lent) with repayments to start in the 16th year (1973). This advance,except for portions becoming due for repayment, is subordinated to allother debts and to equity capital. Consequently, the advance is consideredto be equity under PICICTs Articles of Association and the Bank has per-mitted it to be so considered in all Bank-PICIC dealings. PICIC also hasobtained two loans from the Development Loan Fund (DLF) of $4.2 and $10.0million, respectively. As at December 31, 1960, the corporation had accu-mulated surplus and reserves totalling Rs.l.92 million. On this date,therefore, PICIC's gross resources, including its loans from IBTD and DIF,amounted to Rs. 18'71 million ($39.3 million equivalent), of which Rs.45c9million was originally in the form of local currency and Rs.141.24 million($29.66 million equivalent) in foreign currency (see Annex 8).

- 2 -

5. PICIC is raising an additional Rs.10.0 million in equity capitalduring March, April, and May cf 1961, ani proposes to raise a like amount earlyin 1963. With a single exception, the 1961 issue is being offered bypurchase rights to existing shareholders and preliminary reports indicatethat the issue will be completely subscribed by them. The two issues wouldgenerate a total of Rs.l4 million in rupees and $1.3 million (Rs.6.0 mil-lion equivalent) in foreign currencies, thereby doubling PICIC's paid-incapital. A German bank has offered to participate in PICICts equity capitalto the extent of Rs.2 million in German marks. In order to accommodate theGerman proposal and to keep the current balance between Pakistani andforeign shareholders at the ratio of 3:2, PICIC proposed that the otherforeign interests forego half the increase they otherwise would have beenoffered. If this proposal is accepted by the present foreign shareholders,and present indications suggest a favorable response, the shares issued andsubscribed would be distributed as follows (in millions of rupees):

Present After Proposed 1961 Issue% of % of % of % of

Amount Total Foreign Amount Total Foreign

Held by Pakistanis 12.00 60 18.00 60.0

Held by Foreigners 8.00 40 12.00 40.0American and

Canadian 3.00 15 37.5 3.75 12.5 31.25British 3.00 15 37.5 3.75 12.5 31.25Japanese 2.00 10 25.0 2.50 8.3 20.83German - - - 2.00 6.7 16.67

Total 20.00 30.00

6. The Government of Pakistan is making provision in its currentbudget for a second Rs.30 million advance to PICIC. This advance, whichwill be available during the fiscal year ending June 30, 1962, is under-stood to carry terms identical with the first advance, except that interestwill be charged. The proposed drawings would overthrow temporarily theexisting 3:2 ratio between the Government advance and PICICts share capital.I\egotiations on the rate of interest have ranged between 4% - 4--%, althoughPICICTrs management has reason to conclude that the lower figure will prevail.PICIC proposes to consider the second advance also as equity, and, if thesubordination is the same as for the first, no logical objection can beraised. For the second advance to rank as quasi-equity, however, a changein Article 69 of PICIC's Articles of Association, dealing with borrowingpowers, will be required.

- 3 -

III. CREDIT AND INVESTMENT OPERATIONS TO DATE

7. After its first 37 months of operation, ending December 31, 1960,PICIC had a portfolio consisting of loans for 91 projects amounting toRs.60.65 million and equity shares in 23 industrial concerns purchased ata cost of Rs.7.34 million. A resume of PICIC's loan and investment opera-tions is contained in Annex 1. At the end of 1960 PICIC had a large numberof projects, mostly loans, which had been sanctioned, i.e. approved, by theBoard. PICIC considers loans to be comnitted when a loan agreement witha borrower becomes effective. While almost 85% of the sanctioned loanshad been committed, disbursements continued to lag. On December 31, 1960,27 projects involving Rs.25.85 million had been sanctioned but not committed,and 58 projects involving Rs.67.76 million had been committed but not yctdisbursed. One consequence of PICIC 's brief existence is that its loansin process amounted to almost one and a half times the disbursements out-standing. The relationship of loan sanctions, commitments and disburse-ments may be seen in the two charts in Annex 2. The principal featuresof PICIC's lending are set forth in Annex 3, which shows the relativeuse on foreign and local currencies, the scale of all sanctioned loans,their geographic distribution and industrial classification, and whetherfor improvement of existing projects or for new projects.

Ruoee Lending

8. During PICIC's first two years the easy availability of rupeecredit and keen competition from other domestic financial institutionskept PICICts rupee lending at a level below its local currency resources.Rupee loans represented only one-third of all loans sanctioned in 1958 andonly about one-fourth in 1959, although the device was being employed ofrequiring foreign currency borrowers also to borrow local currency fromPICIC. By 1960 the situation was reversed when it became apparent thatcontemplated equity investments would bring PICIC's rupee resources belowrequirements, despite the planned augmentation of share capital andGovernment advances. Also, PICI0's tax situation became somewhat moreclear, making equity investments relatively more attractive than loans(see para. 45). Finally,PICIC was advised that future Government advanceswould carry an interest charge thereby reducing significantly the spreadbetween rupee funds borrowed and lent. For these reasons, most uncommittedcombined foreign currency and rupee loans were converted during 1960 intosolely foreign currency loans, and only five local currency loans and nocombined loans were sanctioned during that year. Due to reductions inloan amounts sanctioned prior to 1960, the net amount of rupee loanssanctioned in 1960 was only Rs.0.94 million, a small proportion of allloans sanctioned during 1960, and a negligible sum when compared to theamounts of rupee loans sanctioned during the two preceding years (seeAnnex 1). Disbursements of local currency loans have not lagged unduly,as shown in Annex 2.

-4-

Foreign Currency Lending

9. Foreign currency lending has remained PICICts primary businessactivity, due principally to Pakistan ts shortage of foreign exchange. Untilnow PICIC has been virtually the only banking source of foreign currencyfor plant erection and expansion in the private sector. Export bonusvouchers, giving exporters or subsequent voucher holders the right to drawforeign exchange from the Government, carry a premium of 120% - 140%. Thispresumably makes their outright purchase for purposes of plant expansionprohibitive. The Pakistan Government recently made Rs.35.0 million offoreign exchange available at par through the Provincial Governments. Thesefunds were distributed so widely, however, that the average sum made avail-able was Rs.200,000 - Rs.300,00O, thereby preventing the larger entre-preneurs from benefitting from the allocation.

10. As may be seen in Annex 1, foreign exchange loans for 84 projectsamounting to Rs.67.27 million were sanctioned during 1960. This is bothmore projects and a higher loan amount than were sanctioned during the pre-ceding two-year period. The status of PICIC's foreign currency borrowingand lending at the end of 1960 is set forth in Annex 4. At that time,sanctions were outstanding for 26 projects, about 10 of which were understudy bv the Bank prior to approval. Commitments not yet disbursed totalledRs.62.14 million for 56 projects. At the end of 1960 only one-third ofthe amount of sanctioned foreign currency loans had been disbursed. Thisrepresents an improvement over the year-end 1959 situation when only aboutone-quarter of the amount sanctioned had been disbursed (see Annex 2).PICIC's management is alert to this problem, although only part of the causecan be corrected by PICIC. Other causes lie in material shortages, delayscaused by the borrowers, and other conditions outside PICIC's control.

11. The sustained demand for PICIC's foreign currency loans isperhaps best reflected in the number of applications received. During theperiod July-December 1960, PICIC received 126 written applications forRs.229.4 million in foreign currency loans. (The number of informal in-quiries is not available.) During the same period it rejected 43 applica-tions, mostly after failure of the project to survive initial screening,and sanctioned 60. On December 31, 1960 it had under study 68 projectsinvolving Rs.154.8 million, applications for many of which had been inPICIC more than six months. Even more recently, during the months ofJanuary and February 1961, PICIC received 55 more applications for foreigncurrency loans totalling Rs.103.2 million. It is unclear whether thisdemand will slacken as the result of recent developments likely to providebusiness investors with more sources of foreign exchange.

12. It is significant to an understanding of PICIC's role as a dis-penser of foreign exchange that the Government announcement of directallocations last summer resulted in a noticeable drop in applicationsreceived by PICTC, which started in June and July 1960 and which did notend until the fall, after the allocations had been distributed. Itis fair to conclude that, if bonus vouchers carried only a nominal premium,PICIC would have made far fewer foreign currency loans for new plants andvirtually no loans for modernization and balancing, although the latter

- 5 -

category represents about 60% of the foreign currency loans PICIC hassanctioned. It may have been preferable, however, for PICIC to dispenseforeign exchange to industrialists within the framework of Governmentpolicies rather than for this function to be performed by the Governmentdirectly.

13. The status of projects financed from Bank loans Nos. 185-PAK and236-PAK, and those submitted by PICIC for approval, is summarized inAnnex 5. The size, industry, and location of the projects credited as atMarch 31, 1961, is as follows:

Loans Credited Under185-PAK and 236-PAK

Size No. Amount %($ 000's)

Under $200,000 11 1,590 20.8From $200,000 to $500,000 14 3,752 49.2From $500,000 to $1,000,000 2 1,167 15.3Over $1,000,000 1 12125 1L.7

Total 28 7.63L 100.0

Industrial Categorv

Textiles 13 3,090 40.5Sugar 1 1,125 14.7Other Food Processing 5 936 12.3Paper 1 641 8.4Misc. Manufacturing 8 l.8-L 24.

Total 28 ___ _00.0

Geographic Spread

Karachi 9 l,860 24.4Other W. Pakistan 14 4,044 53.0East Pakistan 5 1.730 22.6

Total 28 7,634 100.0

A comparison of these data with the resume of all PICIC loans sanctioned(see Annex 3) reveals that PICIC has been generally relying on Bank fundsfor its larger projects, often in the textile field. These and otherprojects in West Pakistan tend to be larger than those in East Pakistan.

14. Although in a special 1957 agreement the Government freed PICICfrom any foreign exchange risk under the first Bank loan for a four-yearperiod, as a matter of continuing policy PICIC has from the first passedsuch risks on to the borrowers. When the German mark and Dutch guilderwere recently revalued, borrowers of these currencies were immediatelyadvised of their revised liability.

- 6 -

15. By agreement with the Bank, PICIC was given authority to lendfunds under the first loan in amounts up to $10,000 without prior Bankapproval. This option was never used. Under Loan No. 236-PAK, PICICagreed not to submit projects to the Bank for amounts of foreign exchangeless than $150,000. Most of PICIC's smaller projects have been referredto DLF, where prior approval is required only on projects involving loansof $250,000 or more.

Eauity Capital Participation

16. During 1960 PICIC purchased equity shares in industrial concernscosting more than all of its previous holdings. It acquired shares of 11firms at a cost of Ps.4.38 million, at the same time selling shares carried on itsbooks at only Rs.0.97 million cost, including its entire holding of onefirm. On December 31, 1960 it held shares of 23 firms (see Annex 1).These included ordinary shares in 22 firms and preference shares of 3,including one company in which only preference shares are owned. Thetotal acquisition cost of this investment portfolio was Rs.7.34 million.At the end of 1960, market quotations were available for all but threefirms. If shares of these latter are assumed to be valued at cost, themarket value of the portfolio was Rs.9.07 million, representing an un-realized appreciation of 23.5%. This growth in value reflects the currentgeneral upward trend in Pakistan security prices.

17. PICIC has invested in equity shares through four techniques:

a) By direct purchase of securities in the market when ashare is at an attractive price. Such purchases employidle cash and improve PICIC's earning position. Thesecannot be considered current assets like PICIC's hold-ings of Government securities, but neither can they beconsidered normal "assistance to industry". Like allequity shares in PICIC's portfolio their sale will bedetermined by the need for rupee funds and the profitto be realized.

b) As the result of underwriting operations. This is arelatively new PICIC activity described in para. 20.

c) By an option, set forth in a loan agreement forPICIC to purchase shares of a given value at Dar,either at any time Drior to a snecified date duringthe life of the loan or, by debentures convertibleto ordinary shares at par as loan repavments aremade. These options have been attractive businessfor PICIC since unrealized gains often are enjoyed

- 7 -

at the time the option is exercised. Conversely,they have been highly unpopular with borrowers.Only the more excessive premium on export bonusvouchers has made this condition tolerated. Largelybecause of complaints PICIC now obtains convertibledebentures only by mutual agreement and when itsforeign currency lending rate is set 1% below normal(see para. 46). So far even this modified conditionhas not proven attractive to borrowers.

d) By an option, set forth in a loan agreement, for PICICto purchase shares representing a set percentage ofloan at the offering price, at such time as the firmma make a future public offering. This arrangement,of course, is attractive to borrowers and only mildlyattractive to PICIC.

18. Of the shares held on December 31, 1960, PICIC had acquired thosefor one company from underwriting, those from eight companies from exerciseof options. The balance, representing about 27% of the cost of all ofPIICICs equity shares, were acquired by direct purchase on the securitiesmarket. Ihore important, on the same date, PICIC held options to buyshares at par at future dates in 16 companies at a total value of Rs.19.41million. Some of these are exercisable until 1971.

19. PICICGs profit on sale of investments was substantially lowerin 1960 than 1959, falling from Rs.O.29 million to Rs.O.10 million. Thisdecline resulted more from the unwillingness of PICIC's management tosell in a still-rising market and under uncertain tax liabilities, thanfrom non-marketability of the shares at a fair price. Those shares thatwere sold brought an average of 95% above cost. All capital gains havebeen placed in a Capital Reserve and are not normally included in PICICisprofit statement. (They have, however, been included in Annex 10.) Thisreserve, which amounted to Rs.0.39 milli&n on December 31, 1960, wasestablished to cover any tax liabilities which might eventually be assessedon profits from sale of investments, and to cover any losses among equityinvestments due to drastic price fluctuations. At the end of 1960 theCapital Reserve represented only 5.3% of the equity portfolio valued atcost. At the same time the equity investments represented only a modestportion of PICICts business activities, being 11% of outstanding assistanceto industry and only 33$ of PICIC's paid-in capital plus reserves andsurplus.

Underwriting

20. Toward the endof 1960 PICIC underwrote its first share issue inthe amount of Rs.0.3 million. These were ordinary and 8%. cumulativepreferred shares for a local subsidiary of a British firm. PICIC keptapproximately half of the issue as a matter of choice after the shareshad been approved for insurance company investment. It also had an

- 8 -

underwriting commitment outstanding to another foreign subsidiary in the amount ofRs.0.9 million. At the sar:e tire it was negotiating to underwrite an issuefor a proposed joint Pakistan-foreign company which plans to erect a large,modern hotel in Karachi. It ainticipates a broadening demand for theseservices during the next few years, and are attracted by the 2± ounderwritingfee. Despite the experience S the farst issue, the management plans to absorb onlysmall percentages (10% - 20G) of the arount of issues underwritten on a"stani-ty basis", astheugh a contingent liability will exist for the full amount.

Evaluation of PICIC Operations to Date

21, By most objective standards PICIC's portfolio of loans and invest-ments must still be considered to be unseasoned, making a firm conclusionabout the quality of its projects premature. To date, repayments, theacid test of loans made, and sales, the companion standard of equity invest-ments, have only been in token amounts. Even when loans for modernizingand balancing of equipment at existing plants are considered along withloans for new projects, the vast majority of projects has not yet enteredinto production, and none of the new projects has yet reached its plannedfull level of production.

22. Some problems already are emerging, as judged from projectsselected at random for study. Although rnany of the projects are in theirearly construction stages, cost overruns in rupee expenses are appearingin over half of the cases. One project, which had a 44o overrun of rupeeexpenses had a contingency item incorporated into the estimate of only3%. Yany projects have been delayed, some as much as a year, usuiLy from past dif-ficulties of getting Government allocations of cement and reinforcingrods for construction. As a result of these conditions, some projects,especially the smaller ones, are facing tile problem of getting into opera-tion with little or no working capital. In more than one instance PICIChas had to make a second rupee loan to enable construction of the projectto be completed.

23. So far, actual repayment delinquencies are not alarming, totallingRs.0.55 million for nine projects. Seven of these have obtained PICICapproval for postponement of payment due to delays in getting into pro-duction. M.oreover, only Rs.0.04 million is more than six months inarrears. 7erertheless, because of the indications of trouble alreadyapparent in some of the smaller projects, especially local currency loans,it must be expected that PICIC in another four or five years will be con-fronted with some foreclosures and probably some actual losses. Despitesecurity held in the form of mortgages, Pakistan civil law, according tothe General YManager, is inclined to favor a small businessman against alarger corporation and suits at best are likely to be prolonged, expensive,and only partially successful. The total effect of such losses shouldnot jeopardize PICIC's health, especially if reserves can be put aside asprojected.

- 9 -

24. In the larger projects, overruns are being covered by advancesfrom the managing agents, which in some instances are slated for sub-sequent capitalization. The risk involved in projects which essentiallyinvolve selling foreign exchange on credit terms is slight since most ofthese enterprises are capable of repaying the loan within 6 or 12 months.Thus, the great bulk of loans already in PICIC's portfolio, as well asthose approved and committed, is likely to be collected without difficultyunder normal business conditions. Similarly, in a rising securities market,PICIC's holdings of equity shares are likely to be disposable profitablyat will, since many of them were acquired through exercise of options,thereby rendering them relatively risk-free. PICIC's avoidance to date ofmany of the risks normally associated with development banking might beexpected to result in a portfolio of considerable strength.

25. To the extent that the strength of a portfolio may be evaluatedby its balance and diversity, PICIC also appears to measure well. Fromthe figures noted above it is evident that PICIC to date has relied moreon secured loans than on the more speculative equity investments. Sixty-seven per cent of PICIC's loans outstanding are concentrated in four broadindustrial categories (see Annex 3) which are not likely to depart markedlyfrom the general trends of the Pakistan economy. The concentration of 20%of the loan portfolio in the six largest projects is perhaps a feature ofgreater concern, especially since the largest loan is twice as large asthe loan limit prescribed in the Board's own policy. PICIC's loans andinvestments do reveal a studied effort to implement Board policy toproduce as wide a geographic spread as possible, not only among the sectionof East and West Pakistan and the Karachi District, but within these areasas well.

26. It is necessary to distinguish sharply between the quality ofthe projects in PICIC's portfolio and the quality of its project appraisalprocess. Development banks must expect losses as a consequence of riskstaken, but their protection normally lies in the quality of their projectappraisals and end-use supervision. There is evidence that the qualityof PICIC's appraisal pro-ess, especially as measured by the completenessof the appraisal reports, has varied with the source of funds to be lent.Projects to be sent to IBRD for prior approval have usually been repletewith pro forma balance sheets and income and cash flow statements andworking capital estimates. Loans to be submitted to DLF for approvalcontained substantially fewer financial projections, and local currencyloans and DIF loans not requiring prior approval reflected no estimateddata upon which the project could be appraised, except for a brief "profit-ability" study. In the large projects, and princiFally because of theforeign exchange aspect of the transaction, heavy reliance has been placedupon credit ratings. Especially, in PICIC's early days, the terms "largemeans", "fair means", etc., referring to the borrower, continually appearin the recommendations to the Executive Committee as the principal justi-fication for the loan. (While these adjectives are coded by the Pakistanbanking community to rupee amounts, no agreement exists as to whether theamounts cited represent assets or net worth.)

-10 -

27. PICIC continues to operate under the premise that the wealthyindustrial families have unlimited liquid resources. It is not clearwhether the premise would prove valid in the event of a general economicslump which strained Pakistan commercial bank resources. PICIC's projectappraisals sent to the Bank consistently have generated requests for addi-tional data or justification. The Bank has found two projects unacceptableas submitted and has requested that others be modified to remove unsoundfeatures. Thus, it must be concluded that the apparent soundness of muchof PICIC's portfolio is attributable more to the circumstances of PCTICIsoperations and current economic conditions than to the thoroughness andvalidity of its project assessment.

28. PICIC's end-use supervision has apparently been confined princi-pally to the construction of the physical project, but not extended to thefinancial health of the company involved. PICIC has been diligent intrying to receive reports on time, but it has not had the capability ofdetecting omissions in the submission or evaluating financial data, ifsubmitted. The one engineer assigned to this work has not been able tokeep abreast of all projects. Steps being taken to strengthen PICIC'sappraisal and end-use processes are summarized in the following section.

IV. MANAGEMENT AND ORGANIZATION

29. PICIC has a Board of 15 Directors of which 11 represent Pakistanishareholders, three the foreign shareholders, and one the Pakistani Govern-ment. (A list of incumbents on December 31, 1960 is shown in Annex 6.)The Board meets about four times a year and confines itself mainly topolicy matters. The Directors representing Pakistani shareholders are allindustrialists, except the Chairman. This brings to PICIC intensive know-ledge about the industrial environment but perhaps not the broader per-spective which might also be desirable. It also means that many of thecompanies with which the Directors are associated are PICICfs major borrowers.The Executive Committee, composed of the Chairman, one Pakistani Directorfrom Karachi and one from East Pakistan, the Government Director and oneforeign Director, normally meets monthly, principally to consider loanapplications. The Executive Cormittee is empowered to act for the Boardon administrative matters. It is noted that the Executive Committee hasconsidered and sanctioned 10 or more loans in a meeting that lasted slightlylonger than an hour.

30. It is intended that the German participants in PICIC's sharecapital be given a seat on the Board. For this to be accomplished theArticles of Association would have to be amended to increase the number ofBoard Directors. Moreover, under the present provisions of the Articlesof Association, any participant must own 7% of PICIC's share capital or200,000 shares, whichever is greater, to be entitled to a Board seat. Asseen in the table in paragraph 5, the proposed German investment of Rs.2million would represent only 6 2/3% of PICIC's total shares. PICIC pro-poses to amend the Articles to remove the 7% provision.

- 11 -

31. The Chairman of the Board, the second in PICIC's history, is aformer Prime Minister and has extensive influence and contacts. The GeneralManager is a former official of the Central Bank who served as Joint GeneralManager under the first General Manager, a non-Pakistani, and succeeded tooffice when the latter departed early in 1960. His contacts, especiallywith Government, also are widespread6 This combination of backgrounds hasproduced a somewhat more intimate relationship with the Government thanwould normally exist between a private development bank and its government.Tax concessions, mentioned elsewhere, are perhaps one manifestation of thisrelationship. Another is the fact that PICIC sanction of a project isaccepted in lieu of a Governmsent industries license. On the other hand,PICIC has been under constant Government pressure to accelerate its rate oflending activity. The key position of Deputy General M4anager remains un-filled, although a search for qualified candidates continues.

32. The corporation has its head office in Karachi and maintains twobranch offices, one in Dacca, East Pakistan and one in Lahore, West Pakistan.The branch offices could be significant units for the preliminary screeningto applications, since about 80% of PICIC's projects are away from Karachi.Efforts are being made to intensify their participation, although at presentthey are used mostly as contact or liaison posts. The Dacca office has astaff of 11 including 4 professionals. The Lahore office has a staff of4 including 2 professionals. There is some evidence that the six profes-sional staff members are at the moment being underutilized.

33. The Head Office has a table of organization with a total staffof 105 of whom 34 are professionals (see Annex 7). Among these profes-sional staff positions, however, PICIC, on March 15, 1961, had 16 vacanciesor 45% of its potential strength. During the preceding 12 months, 4 pro-fessional people left PICIC. One failed to survive the six months pro-bationary period but the others, including two highly capable senior people,found more lucrative employment elsewhere. Confronted with departures andavowed staff discontent, and counselled by the Bank Advisor and visitingBank staff to heed the problem, PICIC recently reviewed its salary scalesand implemented some minor changes, most affecting junior professionalpersonnel and engineers being recruited. It also provided a 10% housingallowance for some emnployees. It is clear that with these measures, andprobably even before, PICIC can compete with Government and commercialinstitutions including banks. Effective competition, however, is mostlikely to come from European-managed industrial firms. PICIC's managementbelieves that the recent measures taken will enable it to withstand allcompetition, except occasional "pirating" from foreign-managed industrialfirms. No body of professional salary statistics is available to evaluatethis conclusion, but available evidence suggests that the management maystill be taking too large a calculated risk of losing key officers on whomtraining has been and will be focussed. Other professional employees aredissatisfied not only with the pay levels but because they are convincedthat a principle of "equal pay for equal work" is not applied. Even ifactual turnover is not rapid, low morale among employees who tend to viewPICIC as a temporary educational experience can cripple professional per-formance. The need for mobilizing a loyal and effective staff with theconsequent avoidance of turnover should be brought forcefully to the at-tention of PICIC's representative during the loan negotiations.

34. In recent months PICIC has been diligent in trying to bring itscomplement of financial officers and engineers up to full strength. Thisis one of the necessary steps in improving the less than adequate appraisaland end-use activities of earlier years. The nine financial officers andsix engineers provided for in the staffing pattern may not be enough tohandle both the heavy load ahead and supervise the many projects alreadysanctioned, but it will be a far larger staff than PICIC has marshalledbefore and it should be tested. PICICts management appears less inclinedto accelerate recruitment of its other professional personnel--marketeconomists, a securities rarketing expert, arnadainist'ative support officers.During the loan negotiations, the PICIC representative should be madeaware that the Bank expects a full professional complement to be on boardand at work within a few months.

35. The most recent of PICICts many reorganizations was effectiveMarch 1, 1961 (see Annex 7). Its main purpose was to strengthen the pro-ject appraisal capability of the organization, and to bring the appraisaland end-use responsibilities under single supervision. An OperationsDepartment will carry these functions, while the preliminary screeningand economic analysis of projects, including marketing, will be assignedto a separate Economics and General Department. The remaining units willbe the Secretarial and Legal Department. and the Accounts and InvestmentDepartment. In view of the fact that preliminary screening and thoroughappraisal are similar operations, the wisdom of separating responsibilityfor these functions remains to be proved.

36. A main feature of the new organization is the creation of aProject Appraisal Committee (PAC). Chaired by the General Manager, itis comprised of the Chief Engineer, the Industrial Economist, the chiefsof the Economics and Operations Departments, and the Bank's Advisor. ThisCommittee initially screens all project applications for obvious defects,such as non-marketability of the product, obvious non-creditworthiness ofthe applicant, or non-conformity of the project to Government-approvedinvestment categories. Tt also reviews the appraisal report and recom-mendations for those projects which pass initial screening, before suchreports and recommendations are submitted to the monthly Executive Com-mittee meetings. The PAC may be expected to strengthen the Generalivianagerts recommendations to the Executive Committee and tend to assurethat all forms of loan and investment projects will receive equallythorough treatment by the staff.

37. The Bank's Advisor was assigned to PICIC in April 1960 and hasmade a significant contribution to PICICts operations despite staff limi-tations. He has trained personnel, been consulted on project appraisals,and guided the recent reorganization, especially the use of the ProjectAppraisal Committee, into being. An American experienced in market research.to be paid by U.S. International Cooperation Administration (ICA), arrivedin Yay 1961 to take the position of Industrial Economist. The Industrial

- 13 -

Economist and Chief Engineer, also a non-Pakistani, will be able to bringextensive experience to their tasks of guiding and training the economistsand engineers, respectively. It will be noted that these positions areshown outside the chain of command in the organization chart. It mayprove necessary to give them temporary direct responsibility for projectappraisal, letting their prospective Pakistani successors obtain trainingby sitting alongside or serving as deputies.

38. Despite the presence of the Bank Advisor, the services of anintermediary level foreign financial analyst to bring about an early im-provement in the quality of financial appraisals, and to train the invest-ment officers and the Operations Department Chief, may also be required fora one or two-year period. In this way the Bank Advisor could be freedfrom his daily project load to assist in the development of a workingorganization and to advise on procedares, The need for a foreignsecurities analyst to assist underwriting activities and train personnelalso has been raised. If current efforts to obtain a ruling that PICIC'snon-Pakistani employees will have a tax-free salary for a two-year periodare successful, the saving in tax would cover the cost of the two posts.If PICIC can enjoy the services of a full and contented Pakistani staff,of three highly qualified foreigners, situated so as actually to supervisethe appraisal process for a while, plus the Bank's Advisor, improvementshould be recorded.

39. As a further measure for orientation and training, it is plannedto send the Chief, Operations Department, who is a commercial banker bybackground, for training in the Bank for a period of two months during thesummer of 1961. It would be desirable if another staff officer, perhapsan engineer, could receive overseas training later in the year.

40. PICIC's administrative expenses showed a 72% increase in 1960over 1959, rising from Rs.0.68 million to Rs.1.17 million. Although per-sonnel costs increased by 45% between the two years, in 1960 salaries andbonuses were a smaller percentage of total administrative costs than ithad been in 1959. In 1960 vehicle expenses were higher, three houses werefurnished and PICIC s new rented quarters were rermodelled. PICIC hasjust leased offices on the second floor of Jubilee House, below its presentquarters, to contain its growing staff. PICIC expects its administrativeexpenses to grow to Rs.2.1 million by 1963 and Rs.2.8 million by 1965.PICIC is also considering future construction of a Rs.5.5 million officebuilding. If rental income were involved, this might be a good investment,butit should be undertaken only in the light of PICIC's rupee resource situa-tion. The trend in PICIC's administrative expenses should be watched andPICIC should be encouraged to keep its non-personnel expenses low.

- 14 -

V. FINANTC AL POSITION

41. PICIC's financial position at the end of 1960 is set forth inAnnex 8. PICIC had total rupee resources of Rs.45n9 million which, afterdeducting loans outstanding, equity capital participation, fixed assets,and outstanding commitments, left what might be called a free rupee balancefor further industrial assistance operations of only Rs.8.89 million. Thisbalance would be adequate to cover PICIC's requirements only to mid-1961,but the increase in equity shares in 1961 and receipt of the second Govern-ment advance in 1961 and 1962 will temporarily satisfy rupee requirements.

42. Uncommitted foreign currency resources at year-end 1960 amountedto $7.6 million (Rs.36.09 million equivalent). Against this, PICIC hassanctioned loans for $5.3 million. PICIC's foreign exchange resources werecompletely comrzitted for sanctioned projects by the end of February 1961,and additional projects have been tentatively sanctioned.

43. As at December 31, 1960, PICIC was in a satisfactory financialcondition (see Annex 9 for Comparative Summary Balance Sheets), The item"Other Current Assets" includes advances recoverable in cash of Rs.0.99million representing expenditures incurred in appraising the Pakistan cementindustry in general, and the two projects to be assisted by PICIC in parti-cular. PICIC expects to pass these expenses on to the promoters, but therecovery of the full amount remains somewhat uncertain.

44. According to paragraph 69 of its Articles of Association, PICICis authorized to borrow and extend guarantees to a total equal to threetimes the amount of its equity, reserves, and the first Government advanceoutstanding. At December 31, 1960, equity, reserves, and the advanceamounted to Rs.52.92 million; borrowing power would thus be approximatelyRs.159 million. Debt actually drawn down and outstanding on December 31,1960 was only $7.1 million (Rs.34 million equivalent). In viewing adevelopment bank's borrowing position it is also useful to relate to equityits commitments to borrow (as reflected in commitments to lend foreign cur-rencies to its customers), less repayments. On this basis at year end1960 PICIC was committed to lend an additional Rs.62.14 million ($13.05million equivalent), thereby employing only about two-thirds of the debtlimit. Under all of PICIC's agreements to borrow it had available 328.4million (Rs.135 million equivalent), still comefortably below the prescribedlimit.

45. PICIC's 1960 after-tax earnings of Rs.1.92 million more thandoubled the total of 1958 and 1959 earnings (see Annex 10). Although thecorporation is in compliance with local law, it has been overstating itsafter-tax income, and understating its tax liability, by failing to pro-vide for taxes on accrued interest on securities, even though such accrualsare included as income. The amount of such accrued income was less in 1960than in 1959, being Rs.O.18 million, thereby reducing the extent of pre-vious distortion. A small contingent tax liability also exists on capital

- 15 -

gains from sale of securities (see item (c) below). PICIC's reported earn-ings are still modest, representing 9.2% of paid-in capital and surplus asat the end of 1959, but only 3.8% of capital and surplus, including theGovernment advance, and 2.2% of capital employed, including foreign borrow-ings withdrawn. PICIC could have increased its earnings by selling equitiesfrom its portfolio at a reasonable profit. PICIC's provision for 1960 taxesis Rs.0.82 million or less than 3C0% of net income before taxes. This re-sults from PICIC's three tax advantages:

a) Under provisions of the Finance Ordinance of 1960-1961,10% of the gross income of development institutions istax free, provided this amount goes into reserves, andonly until such tax-free reserves equal paid-up capital.PICIC's Special Reserve has been established for thispurpose and Rs.0,26 million of 1959 profits originallyallocated to the General Reserve have been transferredto this account. Thereafter the corporate rate of 50%on taxable income is applicable.

b) Under an unpublished Government notification of 1958,dividends paid PICIC as the owner of equity shares arefree of tax-at-source and excluded from PICIC's taxableincome.

c) Capital gains on securities sold so far have not beentaxed, as Pakistan has no capital gains tax.

46. The 1960 gross income came mostly from interest on loans. Re-turn on foreign exchange loans has in the past been attractive since PICIChad been charging as much as 921-% - 10%, including fringe benefits labelledas "turnover charges". PICIC, however, to avoid criticism revised itsforeign exchange lending rates downward in November 1960, as follows:

Rs.l million or less 7-2-% per annumRs.l to Rs.2.5 million 8% "Rs.2.5 million or over 8 "

plus condition that if a public limitedcompany issues new shares during the lifeof the loan P0CIC can buy up to 20% of theloan amount at the issue price;

or,

with mutual consent, 7AOg per annum plus con-dition that 40% of loan will be in the formof debentures convertible into common stock atpar at the time each loan repayment is made.

- 16 -

47. In addition, a uniform examination and technical assistance feeof 1 of 1% of the loan amount is collectible at the time the Loan Agreementis signed. A commitment charge is levied at the rate of + of 1% per threemonths on the undisbursed portion of the loan. It is estimated that theaverage rate of new foreign exchange loans will be slightly above 8%0, onthe assumption that not many loans will be made at 7±% with the convertibledebenture provision. Thus, the average rate earned on the foreign exchangecomponent of the portfolio may be expected to gradually fall from itspresent level of 42-% - 9% to the new average of about 8%1. On the basis ofcurrent and prospective borrowing and lending rates PICIC should enjoy amargin of about 2% - 3/ on Bank and DLF funds, thereby reducing the earlierprofitability of foreign currency lending.

48. PICIC has enjoyed the full 62/% it charges on its rupee loans, byusing share capital and the interest-free Government advance. As the secondadvance is employed, costing an assumed 4%, the average spread between therupee borrowing and lending rates will fall toward an average of 5%. The62% rate is competitive with other sources of long-term local currencyloans, which sources are limited because loans beyond three to five yearsnormally are not available from commercial banks. The second largest itemwas interest on temporary investments and bank deposits, averaging about3%. Commissions and fees were about equalled by securities earnings, bothdividends and capital gains on sales. Dividends received by PICIC during1960 represented 7.5% of the cost of the 1959 year-end portfolio. Someissues paid as high as 15% on par and the average was about lG', but thetotal holdings of securities are still small.

49. On December 31, 1960 PICIC's total reserves and unappropriatedprofit of Rs.1.92 million represented almost 10%i of paid-in capital. Basedupon market prices of its industrial securities, PICIC also enjoyed anunrealized capital gain of Rs.1.73 million. If the Board follows manage-ment recommendations, the "in hand" amount will be distributed as follows:Rs.0.39 million in the Capital Reserve for capital gains on sales, Rs.0.77million in the Special Reserve, Rs.0.70 million in the General Reserve,and Rs.O.06 million unappropriated profits. No bad debt reserve as suchhas been established, on the basis that no experience exists to determinethe appropriate size. Actually, since the management does not expecttaxes to be due on capital gains and expects market stability to make aninvestment fluctuation reserve unnecessary, it looks upon the CapitalReserve as available for this purpose. Looked at in a hard light, however,all of PICIC's anticipated reserves at year-end 1961 would absorb adelinquency rate representing only 12% of anticipated loan collection in1962, which is not a comfortable margin. The Articles of Associationmake no provision for setting aside a special reserve for repayment ofthe Government advance, which commences in 1973. The management believesthese obligations can be met by proper management of resources and shouldnot be considered until perhaps 1968.

- 17 -

50. All of PICIC's 1958 earnings went into reserve. In 1959 slightlyover 50% of after-tax earnings were paid in the form of a 3 3/4% dividend.In 196u the same income distributTon ratio of half to reserves and half todividends was adopted by the Board and FICIC was able to pay a 5% dividendof Rs.l.0 million. Although an 8% rate for preferred shares is not con-sidered especially attractive, a normal rate for ordinary shares of in-dustrial concerns in the booming Karachi securities market is 4%. PICIC,whose shares are less likely to appreciate than those of an industrialenterprise, is not yet offering an attractive dividend.

51. On March 15, 1961, before its dividend on 1960 earnings and beforeits offering of rights to purchase additional shares, PICIC's shares wereselling for about Rs.12/ for a Rs.10/ per ordinary share. By the end ofApril the shares were selling for Rs.10.8/ per share and the rights carrieda Vo premium. This public assessment probably reflects PICIC's demon-strable earning potential, especially the options to purchase securitiesat par over the next 10 years, its current and planned dividend rate, andthe tax advantages granted by the Government and the close Government-PICICrelationship. PICIC was probably one of the few development banks capablein 1961 of expanding its equity capital at par by a rights offer.

VI. FINANCIAL PROSPECTS

52. Annexes 8, 9, and 10 in their pro forma sections set forthPICIC's financial plan for the period 1961-1963. The assumptions of thisplan have been summarized in Annex 11, together with comments indicatingthe conservative approach embodied in many of them. In view of the im-minent sanction of foreign exchange loans up to the full $29.7 millionavailable to it, PICIC last November requested IBRD and DLF for loanstotalling $30 million in 1961. This was estimated to last two years andwould represent a first step toward the Rs.510 million ($107 million equiva-lent) foreign exchange lending target assigned to PICIC by the SecondFive-Year Plan (1961-1965). DLF at first indicated its ability to loan$15 million in 1961, subsequently reserved its position, and has justmade an initial loan of $7.5 million. The DLF loan is unattractive toPICIC's borrowers in view of the requirement for U.S. procurement on allprojects over $100,000, but often more useful because of its normallyshorter repayment period. One of PICIC's unresolved dilemmas is attempt-ing to devise terms for small balancing loans to its customers whichcorrespond to PICIC's anticipated repayment schedules. Except for theDLF loan, PICIC may have no funds repayable in less than 10 years, althoughthe balancing equipment might otherwise be amortized over five years. Forthis reason another attempt should be made to negotiate for a flexibleamortization schedule whereby repayments to the Bank would correspond toPICIC'z scheduled collections. Due to the foreign exchange facets of suchan arrangement, it will be necessary to consult with the Pakistan Govern-ment on this matter.

- 18 -

53. About the time DLF's lending capabilities became indefinite, PICICbecame aware of an opportunity to obtain part of a German credit line ofDII 150 million being extended to the Government. PICIC applied for DM 20million and currently expects to be allocated half that amount ($2.5 millionequivalent). The Pakistan Industrial Finance Company (PIFCO) is tentativelyslated to get the major share of the credit. The terms are 15 years at6, interest. While procurement is not tied to Germany, it is clear thatfurther lending will be more likely if a significant portion is used topurchase German goods. The Japanese have indicated their willingness tomake a small loan to PICIC, repayable in yen and tied to Japanese procure-ment. If "tied loans" are inevitable, then it may be to PICIC's andPakistan's advantage to enjoy the flexibility accompanying small loans fromseveral sources. From the foregoing it is clear that PICIC's requests forforeign currencies, in addition to the loan requested from the Bank, totalmore than $15 million. While the total credits to be offered are not yetknown, in the forecasts the assumption of $15 million is shown as "OtherForeign Exchange borrowings" for 1961. PICIC is also planning to request$40 million in 1963. These are shown under the same indefinite heading.It will also obtain about $1.3 million in foreign currencies from the pro-posed share increases in 1961 and 1963. PICIC could not fulfill its plannedloan commitments of $16, $20 and $20 million in 1961, 1962, and 1963, re-spectively, without further foreign currency resources in 1963.

54. PICIC has no definite investment plan for the use of its foreigncurrency resources during the period 1961-1963, nor even for 1961. Someof the largest new projects have been sanctioned in principle far in advanceof sanction for specific loan or underwriting amounts and of accumulationof enough supporting data to forward them to IBRD for approval under theproposed loan; for example, $3.5 million to $4 million for two 1,000-tonper day cement plants which PICIC will both underwrite and supply withcredit. Another $4 million to $5 million is earmarked for three sugarplants of which one is already sanctioned and another expected to besanctioned during 1961. Commitment will depend upon Bank satisfaction thatthese are sound projects as submitted and under existing local conditions.Beyond these five large projects lie indefinite plans for a number ofplants in 1962 and 1963 to utilize sugar processing by-products, such asa paper mill to use surplus bagasse, plants to make alcohol, molasses,rubber and furfural. Also mentioned were plants to make light constructionblocks of cement and fibrous stalks, and a cement plant in East Pakistanwhere limestone has been discovered. For the balance of the requirement,PICIC refers to the entire Industrial Investment Schedule developed bythe Government within the framework of the Second Five-Year Plan.

55. Perhaps the certainty of continuing demand for PICIC's foreigncurrency credits, at least in the immediate future, is best supported bythe steady flow of applications cited in paragraph 11. On February 28,1961, PICIC had on hand and under study applications for 92 projectsinvolving Rs.238.7 million ($50.1 million equivalent). The majority ofthese were in the chemicals (including cement), food processing (includingsugar) and engineering fields.

- 19 -

56. A Government-appointed Credit Enquiry Conmission recently madetwo recommendations of importance to PICIC's foreign currency lendingactivities. They proposed that PIFCO for the first time be given foreigncurrencies to lend, and that PIFCO make all foreign currency loans of Rs.0.5million or less and PICIC all loans above that level. PICIC has not fullyimplemented this proposal since PIFCO does not yet have foreign currencyto lend, but PIGIC already is referring some smaller projects to PIFCO.This arrangement might be expected to benefit PICIC for these reasons:

a) Rs.0.5 million is only slightly above the break-evenpoint where the administrative expenses connectedwith a loan are covered by its interest.

b) Loans of these sizes normally require a shorter repaymentperiod, which would only aggravate PICIC's problem of havinglimited funds of shorter term available.

c) Smaller loans are normally harder to collect throughthe courts, while PIFCO, as a Government instrumentality,can rely on summary action to collect loans as fundsdue the Government.

On the other hand, there is some doubt that PICIC will reject all smallloans, or especially, that PIFCO will not enter into agreements for largeloans, thereby providing PICIC with its first effective competition.

57. W4hile foreign exchange lending will remain PICICts major activityduring the coming years, underwriting and equity participation, bothdirectly and through options, are likely to show marked increases in1961-1963 over 1958-1960. This emphasis should enable PICIC to make itsinitial contribution to the formation of a broader capital market. M1ore-over these activities may be expected to increase more than their pro-portionate share of PICIC's earning power. The projections provided byPICIC indicate that, in effect, by 1963 rupee loans will be limited tothe amount of collections fron outstanding rupee loans, with the resultthat the level of loans held will not increase. This approach presumablyis designed to avoid the criticism that would accompany the completecessation of this lending and yet maximize the funds available for moreprofitable equity investments. It must be noted that rupee loans primafacie must be assumed to fill a credit need, while foreign exchangelending involves unmeasurable elements of credit and foreign exchangepurchase. Thus, if unsatisfied effective demand for rupee long-termloans exists, or becomes apparent, for sound projects PICIC should attemptto obtain or free resources sufficient to meet it.

58. Pro forma balance sheets as at December 31, 1961-1963 and in-come statements for the same years are given in Annexes 9 and 10. By theend of 1963, PICIC is expected to have equity, reserves and outstandingGovernment advance totalling approximately Rs.105.81 million. Its reservesand surplus of Rs.5.8l million will equal 14.5% of issued shareholders'capital, but only about 2.1% of estimated loans and investments in PICIC sportfolio. Equity investments at that time will remain somewhat below thetotal of PICICts own share capital and reserves.

- 20 -

59. Profits after tax of Rs.2.30 million and return on stockholders'equity at the end of the previous year of 10.4% estimated for 1961 areexpected to increase by 1963 to Rs14.05 million and 1l.9%. As noted inAnnex 11, these are conservative estimates. Moreover, so long as thepresent trends in the local securities market prevail, earnings can beincreased by "cashing in" unrealized gains in the equity portfolio. Divi-dends are projected at the rates of 5% for 1961 and 1962, and 6% for 1963.

60. PICIC's ability to service its total debt is assured under normlalbusiness conditions. As projected, its pre-tax earnings, plus interestand scheduled loans collections in 1963 will cover its scheduled paymentsof interest and principal only 1.03 times. This unusually low coverageresults mainly from a Rs.4 million gap in 1963 between loan collectionsand loan repayments which, in turn, results from a temporary rate of re-payment to DLF faster than collections of loans made with DLF funds. Inthe case of PICIC, debt coverage of 1.03 times does not represent theextent of its capability to meet fixed obligations without drawing onequity. In 1963 PICIC is proposing to sell Rs.10 million of equities andto purchase Rs.5 million. Assuming a sustained securities market, it couldmeet loan repayments by purchasing less and selling more.

61. In its early projections PICIC estimated a shortfall of rupeeresources in 1962. It proposed to cover the deficit with a line of creditfrom the State Bank of Pakistan, at least to the extent required by under-writing operations. Such borrowing would be appropriate if designed tocover temporary situations, but not as a substitute for medium or long-term borrowing to correct a chronic condition. The Bank's safeguards liepartly in the fact that any borrowings are subject to PICIC's debt-equitylimitation, and, to some extent, in the normal consultation clause in theLoan Agreement. Moreover, PICIC's management will have considerableflexibility in managing its rupee resources due to its assumed ability tosell from its equity portfolio, which at the end of 1963 will, on a costbasis, be almost twice the State Bank of Pakistan credit line proposed.The management has indicated its intent to use these means to convertrupee investments into cash where appropriate and to borrow only fortemporary working capital.

62. Any discussion of PICIC's rupee resources brings to notice thefact that both the Government advance and foreign currency borrowings arebeing doubled in 1961, while share capital is being increased only 5G%.In order to provide sufficient resources to satisfy all legitimate rupeelending and investment requirements without recourse to unsound borrowingPICIC might reasonably consider raising an additional Rs.10 million ofequity capital in 1962 rather than 1963. Since PICIC's 1961 share increasewas accomplished without public sale, an additional increase in 1962 withpublic participation would appear feasible. This is a decision, however,better left to PICIC's management.

- 21 -

VII. ECONOMIC JUSTIFICATION

63. PICIC stands alone arnong Pakistan financial institutions onseveral bases. It is virtually the only investment institution underprivate control. As a user of Bank and DLF funds, it has been the principalsource of untied foreign exchange loans to private entrepreneurs in Pakistan.Acting as a licenser of industrial projects and as an allocator and dispenserof foreign currency PICIC has made a large percentage of the decisionsabout projects to go forward. PICIC's proposed increased role under theSecond Five-Year Plan, whereby it will be responsible for half the invest-ment planned for the private sector, is indicative of its growing importance.

64. It is difficult to document the full extent of PICICTs economiccontribution, since the economic benefits of PICICTs individual projectsare only lightly touched in the appraisal narratives. There is also evi-dence that the benefits result more from the vast need of the Pakistaneconomy rather than from a policy of refined selection. Nevertheless, areview of PICIC's portfolio confirms that most projects will be economicallyadvantageous to the country. Based upon the financial plans submitted byapplicants, it may be estimated that for every Rs.100 PICIC loans at leastRs.105 will be raised and invested in the same projects. The ratio forPICIC's equity investments will be much higher. Based upon the assumptionthat the products otherwise would have to be imported to provide the samelevel of consumer living, it is estimated that most projects requiringforeign exchange will either earn or save in foreign exchange annually upto 50% of the original investment. The projects envisage returns on invest-ment before tax from 10% to 20% profit with current selling prices which,in the case of imports, includes some duty. Ever competition in a freemarket would not render most projects unsatisfactory. Employment oppor-tunities created by the PICIC-assisted projects cannot be quantified, butare known to be significant.

65. In furthering its objective of broadening the capital marketythere are a number of measures already consciously taken by PICIC quiteapart from its plans for underwritings and initial participation in equity.PICIC notes that at least 36 of its borrowers are first-time entrepreneurs,whose savings have been mobilized for a productive venture. Family-ownedconcerns seeking to borrow from PICIC for balancing equipment or new plantsare encouraged to make 49% of their shares available to the public. Thishas been done in the case of cement projects and several others. Privatecompanies applying for loans on several occasions have been prodded intoconverting to public limited companies. PICIC will perhaps make itslargest contribution in the near future in providing development loansfor large projects and in its underwriting and joint equity participationactivities.

- 22 -

VIII. CONCLUSIONS AND RECOM/IEDDATIONS

66. In evaluating PICIC it is necessary to be aware of its close tieto the Pakistan Government ard the privileges and obligations that areconsequent to that relationship. It enjoys the support of its Government,and tangible expression thereof, and yet it must satisfy the Government'ssomewhat breathless development pace if its present important role is tobe maintained. As a result of these pressures, PICIC has acquired alarge portfolio and an even larger group of sanctioned but undisbursedprojects. Mlany of these projects have been for balancing and modernizingequipment or for new plants for entrepreneurs who have required foreigncurrencies rather than investment credit. PICIC0s equity portfolio hasresulted from options exercised and open purchases. Except for some smelldevelopment loans, especially in local currency, the portfolio probably issound. But these business decisions have been made in haste, largely onthe basis of past creditworthiness, and with only nominal technical supportby a few overworked senior staff members. An organization capable of soundtechnical and financial appraisal and vigorous end-use supervision has notyet been created.

67. Thus, after three years, it is still necessary to consider PICIC'srequest for a third loan on the basis of proposals for improved managementrather than on the basis of past performance or demonstrated capability.As foreign exchange becomes less scarce, as competition from PIFCO and otherorganizations increases, PICIC will find itself making more development-type loans and underwriting and participating in the shares of more pro-jects. These activities will involve investment risks and PICIC's prin-cipal protection will be the strength of its project appraisal and super-vision processes.

68. PICIC's financial position is good, its earnings potential fairlyhigh, and its projected reserves beginning to provide a margin againstlosses. It enjoys governmental and public confidence, and can demonstratea demand for its services and funds. It has recently reorganized toemlphasize project appraisal and end-use. Its recruitment effort isbeginning to bear fruit and appears sincere.

69. In view of the considerations in the foregoing paragraph, it isconcluded that PICIC's prospects make it a suitable organization for furtherBank assistance, subject to the following conditions:

a) PICICts account should not be credited with more than$7.5 million until a date to be mutually agreed betweenPICIC and the Bank. This provision would give the Bankan opportunity to evaluate jointly with PICIC's manage-ment at a date roughly mid-point in the crediting periodof the proposed loan, the improvement in PICIC's projectappraisal and end-use supervision.

- 23 -

b) PICIC's account should continue to be credited underthe proposed loan only following prior Bank approvalof each project. (However, PICIC might be advisedinformally that a project limit not requiring detailedBank appraisal will be considered on the basis of improve-ment reflected in project appraisal submissions and thereport of any end-use missions.)

c) PICIC should agree to utilize its proposed line ofcredit with the State Bank of Pakistan only fortemporary working capital requirements pending thetime when expected receipts can be collected andused for repayment. Moreover, an undertaking shouldbe obtained not to utilize more than Rs.5 millionfrom this source without prior Bank approval.

d) If Pakistan Government concurrence can be obtained,an amortization schedule should be employed whichcorresponds to PICIC's scheduled collections offunds lent under the loan. The normal repaymentperiod would not exceed 10 years from the date ofcrediting, although extensicn might be required inexceptional cases.

70. It is further recommended that during the negotiations the PICICrepresentative be advised of:

a) the necessity of strengthening and bringing PICIC'sprofessional staff up to full strength as early aspossible, including filling the key position ofDeputy General Yanager, and maintaining high moraleand thereby avoiding turnover;

b) the desirability, within PICIC's means, of hiringfor a year or two (i) a foreign intermediary-levelfinancial analyst to supervise project appraisalsand train staff and (ii) perhaps a securitiesmarketing expert; and

c) the desirability of utilizing PICIC's foreign tech-nical advisors in the chain-of-command to bringabout an early increase in performance.

71. Provided that agreement on conditions (a) through (c) in para-graph 69 can be obtained, it is recommended that a loan of $15 millionequivalent be made to PICIC.

PAKISTAN INDUSTRIAI CFEDIT AiM INVESTMENT COFPOPATTON. LIMIrED

Summary of Loan and Investment Onerations - 1958 to 1960(Rs. Millions)